Sure, your child needs to be 15 before becoming an authorized user on a credit card account, 18 before signing a binding loan agreement, and 21 before applying for a credit card without a cosigner or some income to pay the bills. But long before that, they are “eligible” to have their identity stolen. In fact, according to a Child Identity Fraud Survey conducted by Javelin Strategy & Research, 1 in 40 households with children under age 18 had at least one child with personal information compromised by identity fraud in 2012.

Fortunately, there are ways to protect your kid from becoming a victim of child identity theft. For starters, parents can request credit reports for children under 14; children 14 and over can request a copy of their own credit reports. There are also credit monitoring services they can employ if they’re worried their kin’s personal information fell into the wrong hands. Here’s how to use credit monitoring to protect your child’s identity.

Why Is Your Child at Risk of Identity Theft?

Identity thieves are targeting children 18 and younger, swiping their Social Security numbers and applying for credit accounts in their names and piling up charges. Why? Because children aren’t in the habit of checking their credit. In fact, they often won’t even have a legitimate credit report unless something’s amiss. Remember, credit reports are a detailed account of your credit history, so until your child becomes an authorized user on your credit card account or gets a student loan, for example, they won’t leave a paper trail. In the meantime, thieves can wreak havoc by opening up bank accounts, credit lines, service contracts like a cellphone plan or more if they get their hands on a kid’s Social Security number.

A stranger who accesses a child’s Social Security Number, a dishonest family member or a friend of the family with access to a child’s personal records may commit this crime. Foster care children are particularly vulnerable to child identity theft because of the number of people who have access to their Social Security numbers.

How Can I Monitor My Kid’s Credit?

To protect your child, get in the habit of monitoring his or her credit reports. Reach out to each of the three major credit reporting agencies — Equifax, Experian and TransUnion — and request copies of your child’s credit records.

You will need to provide each credit reporting agency with your child’s name, address, date of birth, plus copies of your child’s birth certificate and Social Security card. You will also need to provide a copy of your driver’s license or other government-issued identification card and a utility bill showing you live at your current address.

Remember, children generally won’t have credit file unless you’ve added them to a credit card account in your name, so the mere fact that a bureau can generate a credit report for your child could be a sign that something’s amiss. Other signs that your child’s identity may have been stolen include:

Pre-approved credit card mail solicitations in your child’s name

Calls from a debt collector asking to speak to your child

An unexpected denial when you go to open up a bank account for your child

The arrival of cell phone or utility bills in your child’s name

If you discover your child is a victim of identity theft, be sure to report the fraud to the local authorities and the Federal Trade Commission.

What Is Credit Monitoring?

A credit monitoring service keeps tabs on your (or your child’s) credit report and notifies you of any changes that may occur. The major credit bureaus offer their own credit monitoring services, along with many of the major financial institutions and credit card issuers. Some services are even specifically designed to monitor a child’s identity.

Of course, prices for credit monitoring can vary, so it’s a good idea to shop around and compare and contrast them carefully. It’s also a good idea to thoroughly vet any company you’re considering. You can check out their record with online review sites, the Better Business Bureau, the Consumer Financial Protection Bureau or even your state Attorney General’s office.

How Can I Monitor My Own Credit for Identity Theft?

If you’re worried about your own identity being compromised, you should monitor your financial accounts regularly — daily if possible. The earlier you can spot unauthorized charges, the faster you can alert your financial institution and fix the problem.

Monitoring your credit regularly is also important. You should pull the free copies of your credit reports you can get once a year from each of the major credit reporting agencies at AnnualCreditReport.com. Signs of identity theft include mysterious addresses, unfamiliar credit inquiries and a major drop in your credit scores. To keep a closer eye on your credit, you can monitor two of your credit scores for free on Credit.com.

Jeanine Skowronski contributed to the reporting of this article.

This article has been updated. It was originally published August 21, 2014.

You can get an apartment with bad credit, but it may take some strategizing. Apartment applicants with low credit scores can boost their odds by applying with a cosigner, paying more upfront, offering references, or changing the type of units they apply to.

In today’s housing market, you want every possible advantage on a rental application. While letters of recommendation and a solid rental history will get you far, more and more landlords want a high credit score. As a result, it isn’t uncommon to ask if you can get an apartment with bad credit.

While it takes some strategizing, you can get an apartment with low credit. To help you along, we’ll explain how credit impacts your application, explain steps you can take to compensate for low credit, and share tips on boosting your score.

How Credit Impacts Getting Approved for an Apartment

Many landlords and renters run a credit check as part of their rental application process. Like lenders, landlords check your credit to see if you can pay your bills on time. Because renting is an investment, property owners want to minimize risk. So, they assume tenants with high credit are more likely to pay their bills on time.

Remember that your credit score isn’t the only factor on a rental application. While a high score helps, the details on your credit report matter, too. How you got a high or low score can sway property managers one way or the other.

What Credit Score Do You Need to Rent an Apartment?

The score you need depends on the unit. Some rental companies provide an ideal range for their listings. A score of 620 or higher will generally keep landlords from denying your rental application. However, some landlords will expect more, while others don’t look at your score at all.

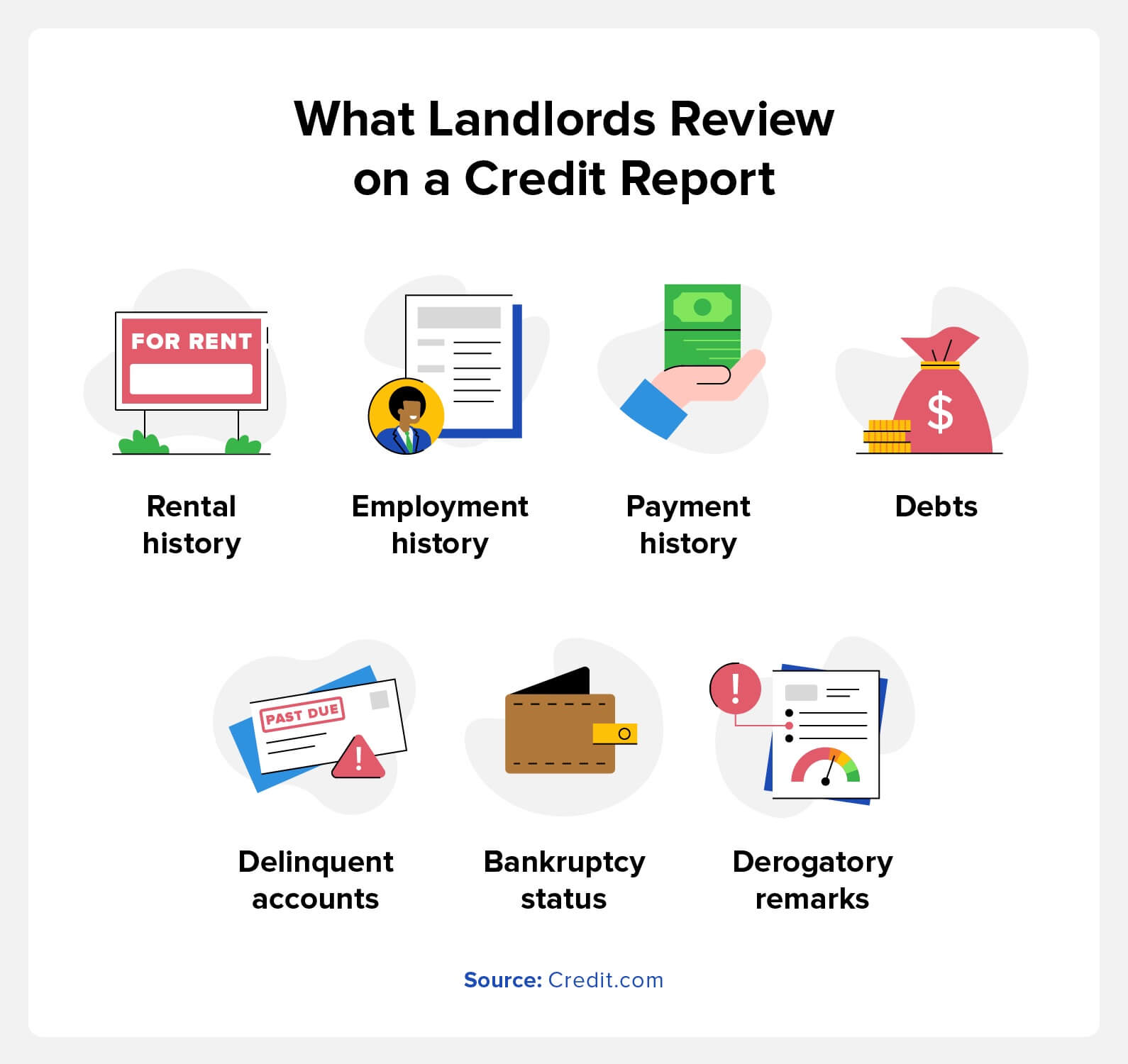

What Do Landlords Look for on a Credit Report?

Renters may treat your credit score like a headline, but there’s more to a credit report than a number. Credit reports tell a story about your spending habits and income. To help landlords pick reliable tenants, a rental credit check includes:

Rental history: Some landlords report rent payments to credit bureaus. As a result, evictions, broken leases, and late or missing payments may appear.

Employment history: Current or past employers may show up on a credit report. Typically, they only appear if you listed them on a credit card application or loan.

Payment history: Credit reports show your history of payments to lenders. Late or missing payments will lower your score and work against your rental application.

Debts: Current and past debts show up on your credit report. By providing payslips, landlords can calculate your debt-to-income ratio. If you make enough to repay your debts responsibly, that improves your application.

Delinquent or collections accounts: An account is delinquent if you miss a payment due date. If you miss enough payments for lenders to transfer your account to a collection agency or sell it to a debt buyer, it becomes a collections account. Both of these hurt your credit score.

Bankruptcy status: Bankruptcy filings will affect your credit score. Landlords may take recent bankruptcies as a sign that you’re a high-risk tenant.

Derogatory remarks: These remarks refer to negative items on your credit report. They include auto repossessions or foreclosures. They hurt your score and hamper a rental application.

Landlords gauge the risk they pose by looking at how applicants spend their money. Someone with a high income but a history of late payments may not make the cut. On the other hand, someone who filed for bankruptcy years ago may be more responsible now.

How to Get an Apartment with Bad Credit

While a low score sets you back, you can learn how to get approved for an apartment with low credit. By following these methods, you can get a leg up in rental applications:

Make an Upfront Payment

Putting down more money upfront can give you an edge on rental applications. Landlords will usually request a security deposit or the first and last month’s rent upfront. To sway a landlord’s opinion, offer the first three months’ rent or put down a higher security deposit.

At the end of the day, renting is an investment. If you can show your landlord that you’ll give them a reliable ROI, it’s all the more likely they’ll accept you. As a bonus, paying more in advance saves you a financial burden for the next few months.

Find a Guarantor or Cosigner for Your Apartment

If a landlord can’t trust you to make payments, you can get someone to sign your lease with you. Someone with a great credit score who signs on with you can assuage a property manager’s worries. However, remember that the person who helps you takes on financial risk. You have two options for this approach:

Cosignerssign a rental agreement with you and share the financial responsibility for it. They must do so on your behalf if you can’t or won’t pay rent.

Guarantors share cosigners’ responsibilities, but they have fewer rights. More specifically, they vouch for you and can make payments on your behalf. However, they aren’t entitled to reside in your unit.

Offer References and Supporting Documents

While credit reports outline your financial history, you aren’t the sum of your spending decisions. You can offer other documents to show your responsibility in an apartment application. Additionally, these documents can prove you can pay rent each month. Some examples of supporting documents include:

Payslips: Offer pay stubs that show you make enough money to pay rent each month.

Letters of recommendation: Reference letters from a friend or employer can attest to your character and responsibility.

Proof of reliable rental history: Account statements and landlord testimonials can prove you always pay rent on time.

A snapshot of your savings account: If all else fails, you can show landlords you have the money to make rent. Be sure to censor sensitive information on your snapshot.

Utility payments: A history of on-time utility payments shows your trustworthiness.

Find Apartments to Rent with No Credit Check

While credit checks are common, not all landlords require one. While these properties aren’t the most competitive, that isn’t always a problem. Apartments with no credit check tend to cost less than ones with one.

If you’re looking for another option, some landlords advertise units with low credit requirements. Again, these properties set a low credit requirement for a reason. That said, if you inspect the unit and it looks good, this route can save you a headache. As you live in low-credit apartments, you can build your score for future applications.

Adjust Your Expectations

If you can’t get around a credit check, reassess the kinds of apartments you can apply for. This isn’t to say you should only apply to units in poor condition. Instead, consider what you’re willing to compromise on. You may have an easier time qualifying for an apartment:

Farther away from your work or downtown area

Without amenities like a gym or pool

That doesn’t include parking

With less square footage than you’d prefer

If you apply with a roommate

Bear in mind that compromising on these points means the apartment may cost less. While living in a less-than-ideal unit, you can save and rebuild your credit while renting. When it comes time to look for a new apartment, you’ll have better odds of getting the one you want.

Tips to Raise Your Credit Before Renting an Apartment

If you plan to send rental applications down the line, you should work to improve your credit. Bear in mind that increasing your credit score takes time. To see a major change, expect months or even a year of work. In that time, follow these tips to improve your credit:

Pay Your Bills on Time

A person’s payment history can make or break their credit score. Central to that payment history: whether you paid your bills on time. Making timely and consistent payments plays a big role in improving your credit score. On top of that, timely payments prove your reliability to a landlord, boosting your chance of getting approved.

Pay Down Any Debt

Paying down debts is one of the best ways to improve your credit score. For this reason, someone who takes on and pays off debt won’t get punished for the debt they take on. Paying off debts shows your fiscal responsibility and proves your finances are on an upward trajectory.

Paying off any kind of debt can improve your score. The main ones to look out for include:

Credit card debt

Student loans

Medical debt

Auto loans

Become an Authorized User for Credit Piggybacking

If you don’t have the resources to boost your credit alone, you can try credit piggybacking. Credit piggybacking lets you benefit from a friend or family member who pays down their debts. By becoming an authorized user on their account, your credit report reflects their payoffs.

You can break the process into a few steps:

Find a friend or family member you trust to spend responsibly.

Become an authorized user on one of their credit cards or lines of credit.

As they pay down their debts, this will show up on your credit report.

By piggybacking on their credit payoffs, your score will improve.

Dispute Credit Report Errors

Sometimes, a low credit score isn’t your fault. Credit reporting errors can come from major credit reporting agencies or the companies giving them information. Credit reporting errors aren’t uncommon, so you should review your report for issues.

Credit reports may contain errors related to:

Accounts held by another person with a similar name to you

Accounts opened by fraudsters who committed identity theft

Closed accounts that still read as open

Accounts incorrectly labeled as delinquent or in collections

Payments that don’t get reflected in your report

Multiple listings of the same debt

Accounts with inaccurate balances or credit limits

To dispute credit report errors, contact the credit bureaus and the company that reported inaccurate information to them. You want to provide supporting documentation that proves the report contains errors. While you can send a dispute by phone, this doesn’t leave a paper trail. Instead, mail a dispute letter or use an online form.

FAQs on Renting an Apartment with Bad Credit

You may still have questions about getting approved for an apartment. To help you out, we’ve answered FAQs on renting apartments with bad credit.

Is 500 a High Enough Credit Score for an Apartment?

You can rent an apartment with a credit score of 500. While it might take you out of the running for expensive units, you should still have a good chance of renting:

Apartments with low credit requirements

Apartments with no credit requirements

Apartments you apply to with a cosigner or roommate.

Can I Reapply for an Apartment After I Get Denied for Bad Credit?

You can apply for the same apartment after getting denied on your first attempt. That said, some renters may throw out your application or ignore it. If you reapply, try to improve your credit and finances between applications.

Do Landlords Need Permission to Run a Credit Check?

Landlords need your permission to run a credit check. The Fair Credit Reporting Act calls rental applications a “permissible purpose.” This gives them the right to view your credit. However, that doesn’t mean landlords can check your score without your consent.

Improve Your Credit for an Apartment with Credit.com

Managing apartment applications is hard enough, even without a low credit score. However, you can get an apartment with bad credit by following the right steps. You’ll see more housing opportunities by learning how credit works, reviewing strategies for getting an apartment with low credit, and following tips to boost your score.

If you’d like a way to streamline raising your credit for rental applications, Credit.com can help. Our rent and utility reporting services ensure that your on-time payment gets reflected on your report. Even if your landlord doesn’t report payments, our tool helps build your credit with every rent payment reported.

Identity thieves are almost always opportunistic—but the crimes they commit feel very personal. Unauthorized credit card charges, bogus loan applications, missing money, and other financial violations make fraud a major nightmare. To keep fraud in check, you need to know how to check your credit report for identity theft, and how to deal with problems when they arise.

In this post, we’ll talk about the warning signs of identity theft—and then we’ll show you how to stamp out fraud before it starts.

Warning Signs of Identity Theft

How Do I Check My Credit for Identity Theft?

To avoid falling victim to identity theft, examine your credit report regularly. You can access a free copy of your credit report from all three bureaus—Equifax, Experian, and TransUnion—once a year. (Through April 2022, you can get free weekly copies of your reports.) You can also use a tool like Credit.com’s Credit Report Card or ExtraCredit to monitor your credit.

When you download your credit report with ExtraCredit, you’ll see a list of positive accounts, late accounts, collections, public records, inquiries and account balances. Your credit report contains a lot of information about you and about your financial habits, and if that information changes unexpectedly, it can indicate identity theft. Here are five of the biggest fraud warning signs to watch out for.

Warning Sign 1: Incorrect Personal Information

Sometimes, incorrect personal information is the result of an innocent mistake. Other times, it means something sinister is going on. If you see your name misspelled, a wrong phone number or address, or an incorrect Social Security number on your credit report, investigate immediately.

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

Warning Sign 2: Lender Inquiries You Don’t Recognize

Credit bureaus keep the details of companies who ask for information about you on record for at least two years. Promotional inquiries and account review inquiries are nothing to worry about, because they’re preapproved credit offer inquiries or inquiries by companies you already do business with.

Hard enquiries from companies you don’t recognize are a different matter. Sometimes, fraudsters make a lot of credit card and personal loan applications in a short period of time, so if you see a recent list of unknown inquiries, someone might be trying to steal your identity.

Tip:Sometimes, the name of a financial institution doesn’t precisely match the name of the company checking your credit. Car dealerships, for example, sometimes run a series of credit checks via different finance companies—so it’s worth double checking before filing a fraud complaint.

Warning Sign 3: Accounts You Never Opened

Only your own accounts—including accounts that you’ve cosigned and for which you’re an authorized user—should appear on your credit report. If you find an unknown account on your credit report, one of two things has happened:

Your credit information has been commingled with someone else’s information by mistake

Your credit has been compromised by a fraudster

If you find an unknown account on your credit report, contact the relevant lender right away and tell them what’s going on.

Warning Sign 4: You Credit Utilization Goes Up

If you suddenly owe more than before and you haven’t changed your spending habits, someone else might be splurging on your behalf. Check your credit card statement very carefully and flag any suspicious transactions straight away. Most credit card companies have a maximum 120-day limit for chargebacks, so it’s important to review purchases regularly.

Warning Sign 5: Your Score Goes Up or Down Unexpectedly

Credit scores change over time. When negative information falls off your credit report after a certain period of time, your score increases. On the other hand, if you apply for too many loans or credit cards in a short space of time, your credit score could take a hit. If your credit score changes dramatically—especially if it’s for the worse—dig deeper.

Warning Sign 6: Public Records You Don’t Recognize

Negative public records can substantially impact your creditworthiness. Bankruptcies, for instance, often remain on record for up to a decade. If you see public records you don’t recognize, alert the issuing agency without delay.

Tip:Liens and civil court judgments used to appear on credit reports, but credit bureaus no longer collect information about those types of public records. Bankruptcies are now the only public records included on credit reports.

Can Someone Steal Your Identity with Your Credit Report?

Your credit report contains a lot of personal information, so it’s a goldmine for identity thieves. With a copy of your report in hand, a potential fraudster might be able to see:

Full name

Birth date

Social Security number

Current and past home addresses

Phone number

Accounts held in your name

Payment records

Public records, including bankruptcies

Many other valuable personal and financial details

Credit report content sometimes varies according to the credit bureau.

If thieves need more information after accessing your credit report, they often choose to misrepresent themselves to get it. Phishing and smishing scams are when criminals pretend to be legitimate financial institutions—or government agencies like the IRS—to get personal information from victims via email or text.

What Is the Safest Way to Check My Credit Report?

You can check your credit report quickly and easily with Credit.com’s ExtraCredit monitoring service. ExtraCredit includes five helpful tools, which help you monitor, build, earn, protect, and restore your credit profile. Two tools in particular can help you avoid or combat identity fraud: Track It and Guard It.

Track It

With ExtraCredit’s Track It tool, you get access to all three credit bureau reports. You can also monitor 28 FICO® scores—the real scores lenders see when they consider auto loan, credit card, and mortgage applications. Track It also includes a helpful credit monitoring tool, which gets updated every month. If something suspicious happens, you’ll notice right away.

Guard It

Many hackers sell consumer information on the dark web. Nefarious individuals use software, specific net configurations, or special authorizations to access the dark web. Thankfully, ExtraCredit’s Guard It tool actively monitors the dark web for consumer information and sends out security alerts when data breaches happen. You also get a $1 million ID insurance policy when you sign up with ExtraCredit.

Get Identity Theft Protection

Identity theft is a big problem in the United States. There were 650,572 cases of identity theft in America in 2019—and over 270,000 of those cases involved credit card fraud. If you see an unknown address or notice an unknown credit card on your credit report, flag it up right away. Tools like ExtraCredit from Credit.com make it easier to monitor your report on a monthly basis, so you can rest more easily.

Getting a credit card is like taking a step toward financial adulthood. It brings you into the world of building credit and paying bills, which almost everyone has to deal with at some point, so it can help to get started as soon as possible.

But the “firsts” of adulthood aren’t always easy, and that includes getting your first credit card. A Credit.com reader recently asked where to start:

Hi, I am 18 years of age, I have no credit history, and I have low income. I’m wanting to get my own place, and would love some help finding a good credit card to build my credit that will accept my low income.

There are three main things that will affect whether or not someone like our commenter could get a credit card: the person’s age, the fact that they have no credit and the amount of money they make.

Privacy Policy

1. Can You Get a Credit Card at 18?

Let’s start with age. Per the Credit CARD Act of 2009, consumers younger than 21 must have proof of independent income or a co-signer in order to get a credit card. It makes sense: If you’re going to get a credit card, you need to be able to show that you can pay your balance.

Why Would I Want to Have a Credit Card at 18?

Having a credit card at 18 can help you to start building your credit early. It also allows you to make purchases that may require a credit card, such as a car rental.

2. Do You Make Enough Money?

That brings us to income. Since this commenter referenced wanting to live independently, it seems unlikely that they’d opt for a co-signer. That means this person would need to provide proof of their income. We don’t know exactly what our commenter means by “my low income” — even if it’s not a lot, it isn’t necessarily a credit card deal-breaker. You could always try to ask a credit card issuer what sort of income they’re looking for among card applicants, but you may not get an adequate answer, given that there’s more that goes into getting approved for a credit card than income.

3. Consider Becoming an Authorized User

If you’re wondering how to get a credit card at 18, becoming an authorized user may be your best solution. An authorized user has permission from the cardholder to use their account to make credit card purchases. Typically, you receive a credit card with your name on it, but there might be limitations as to how much you can spend.

If the credit card company reports authorized users to the credit bureaus and the cardholder makes on-time payments, this option could help boost your credit. As an authorized user, you’re not directly responsible for making monthly credit card payments. Instead, you should make a payment agreement with the cardholder to ensure your bills are paid on time.

4. Get a Secured Credit Card

At 18, it’s likely you have little to no credit history. This factor could prevent you from obtaining a traditional credit card. Despite your lack of credit history, you could qualify for a secured credit card. This type of card requires you to pay a cash security deposit to open the account.

For example, you might need to pay a cash security deposit of $500 to open a credit card with a $500 credit limit. With secured credit cards, monthly payments are typically reported to credit reporting agencies. In many cases, you can increase your credit limit without an additional cash security deposit after several months of making on-time payments.

Get a Student Credit Card

If you’re a college student, you may qualify for a student credit card. These cards are specifically for full- and part-time students at higher education colleges or universities. Credit requirements are typically lower for student credit cards, especially when it comes to the length of credit history.

If you have little to no credit, you may have a better chance of securing a student credit card than a traditional credit card. Keep in mind that credit card companies must still adhere to the regulations of the Credit CARD Act of 2009. So, you still need to have a cosigner, have proof of income or meet other requirements for a student credit card.

5. Ask Someone to Cosign for You

Another option for obtaining a credit card at 18 is asking someone you trust to be a cosigner on the account. This method can help if your cosigner has a good credit score. Both you and the cosigner are responsible for making payments.

How to apply for a credit card at 18 with a cosigner? Unfortunately, none of the major credit card companies allow for cosigners. If you can’t find a credit card you like that allows for a cosigner, you could opt for a joint credit card account. With this type of account, both parties remain responsible for making payments, but it’s likely your cosigner will be listed as the primary cardholder on the account.

Tips to Help You Manage Your Card

Obtaining your first credit card can be exciting, but it also comes with great responsibility. How you handle your credit card purchases and payments can impact your credit score for years to come. It’s important to set up good practices now to protect your future finances.

Set Up Automatic Payments

Setting up automatic payments is a great way to ensure your bills are paid on time. You can use your credit card to pay your bills and then pay your credit card bill by the due date. This process can help you build a strong payment history, which accounts for 35% of your credit score.

Build a Budget

The best way to avoid overspending is to build a budget. Start by tracking your spending for a month and use that information to develop an accurate budget. Be sure to set some money aside each month in a savings account in case of an emergency.

Pay More Than the Minimum Payment Every Month

One of the most important things when it comes to having a credit card is to be sure you’re making at least the minimum payment every month. If possible, you can pay more than the minimum balance to avoid paying interest.

Only Buy Things You Know You Can Pay Off

When you have a credit card, it can be tempting to make large purchases that you might not be able to afford without the credit card. Avoid this temptation. If you buy things you can’t afford, you run the risk of not being able to make your monthly payments.

Late payments can have a negative impact on your credit score. Using up all of your available credit can also reduce your credit score.

Be on Top of Your Statements

It’s crucial that you take having a credit card seriously. Just as you do with your bank account, be sure to check your credit card statements carefully. Take note of how much available credit you have left to avoid going over your credit limit. You also want to make sure you make all your monthly payments on time.

Other Ways to Build Credit

There are several things you can do right now to start the path to building your credit.

Student loans: Student loans can do more than just help you pay college tuition. They can also help you build credit. The important thing is to make sure you start paying on these loans as soon as you’re required to do so.

Emergency fund: You’re never too young to start an emergency fund. Be sure to put a portion of your earnings into a savings account. This strategy can help you in the event of a financial emergency.

Track your credit score: Whether you’re 18 or 80, it’s important to frequently track your credit score. Credit.com offers free credit scores from Experian that are updated every 2 weeks.

Get a job: The easiest way to secure a credit card when you’re only 18 is to maintain a job. If you’re able to prove you can financially handle having a credit card, it’s easier to obtain approval.

Good credit requires responsible financial management over a period of time. However, there are some tactics you can try that help build your credit as fast as possible, if not exactly overnight. Find out more about these tips below.

In This Piece

Add Rent and Utility Payments

Your credit report and score are meant to help demonstrate whether you can manage money responsibly. But not every bill you manage gets reported to the credit bureaus.

Most landlords don’t send payment information to the credit bureaus, for example. And utility providers usually only report when you’ve defaulted on a bill. If you’re looking for how to increase your credit score quickly, getting these timely payments added to your report can be a good idea.

ExtraCredit lets you link rent and utility payments as trade lines to be reported to the credit bureaus. You can access this perk via the service’s Build It function to establish your credit by increasing your history of timely payments.

Pay Down Debt

Paying down debt is potentially one of the best things you can do for your credit. That’s because when you pay down revolving credit, you reduce your credit utilization, which has a big impact on your credit score.

It’s also helpful to pay down debt if you’ve fallen behind or have collection accounts on your credit report. Catching up past-due accounts and keeping up with them reflects positively on your score and can help you boost your credit.

Keep Utilization Low

Revolving credit includes credit cards, lines of credit and home equity lines of credit. Your credit utilization is a ratio of your total revolving credit balance compared to your total revolving credit limit.

For example, imagine you have two revolving credit accounts:

A credit card with a credit limit of $5,000 and a balance of $2,000

A line of credit with a limit of $5,000 and a balance of $1,000

You would have a total credit limit of $10,000 and a total balance of $3,000. That’s a credit utilization of 30%.

Credit utilization accounts for around 30% of your credit score. Keeping your credit utilization as low as possible—ideally below 30%—helps positively impact your scores.

Pay Bills on Time

Always pay all your bills on time. This is less a tip for boosting your credit overnight and more a tip on how not to wreck your credit overnight. One or two slips that lead to you paying bills 30 days or more past due can drastically and negatively impact your credit score.

Get a Secured Credit Card

A secured credit card is a card designed to help those with fair, poor, or bad credit build credit for the future. Getting one can help you boost your score.

Getting a credit card—and using it responsibly—can be a great way to boost your credit without actually going into debt. It might seem like a contradiction, but remember that a credit card doesn’t automatically mean debt. If you pay your balance off each month, you’re never in debt.

But you do still get some of the potential credit-boosting benefits of holding a credit card. The first is that your credit mix may be improved. Creditors like to see that you can manage multiple types of credit, and your credit score benefits when you have both installment and revolving credit.

Having a credit card also lets you address your credit utilization. If you have a credit card and you pay off the balance every month, you’ll have a lower credit utilization with a responsible payment history, which is good for your credit.

Get a Credit Builder Loan

If you already have a credit card, your credit mix might be suffering from the lack of an installment loan. Any type of installment loan—from a car loan to a personal loan—might benefit your credit score if you make your payments regularly and on time.

But for those who don’t have the credit history or score for a traditional installment loan, a savings-secured or credit-builder loan might be a good option. These loans often require deposits or savings accounts that you get back when you’re done paying for the loan, so they’re not loans designed specifically to provide for a financial need. They’re for the purpose of getting an installment loan and positive payment history on your report.

Become an Authorized User

If you don’t feel ready for your own credit card or can’t qualify for one, see if a family member will add you as an authorized user to their credit card account. Many banks and issuers report account activity to both the cardholder’s and authorized user’s credit report.

You do need to make sure you consider this option carefully. First, make sure the person you ask is responsible with their bills. If they pay their credit card bill late, you could end up with negative marks on your report.

Second, make sure the credit card company reports on authorized users. If the information doesn’t get added to your credit report, it can’t have an impact on your credit score.

Dispute Errors on Your Credit Report

Inaccurate items, such as a late payment reported when you never missed a payment, could unfairly bring your score down. Reviewing your reports and challenging errors may help improve your score. You can get a free credit report from each of the three bureaus every year at AnnualCreditReport.com. These are also available weekly for a limited time due to COVID-19.

In addition to rent and utility reporting, ExtraCredit shows you 28 of your FICO® scores and your credit reports from all three credit bureaus. You can check what’s showing up on your reports and what’s affecting your credit scores so you can follow up as necessary.

If you do find an error on your credit report during your investigation, be sure to challenge the accuracy of the error. Under law, you have a right to a credit report that’s fair and free of errors, so if information can’t be proved by the reporter, the credit bureaus may have to remove it.

Set Up Credit Monitoring Account

Invest in credit monitoring to take a proactive approach to protecting your score. By understanding exactly what’s going on with your report, you can address errors quickly and learn how your own actions impact your score. That helps you make potentially score-boosting decisions in the future.

Credit.com’s free Credit Report Card provides a snapshot of your credit report, with information about how you’re doing in the five critical areas for your score. Knowing how you’re doing can help you pinpoint areas that might need some help.

Don’t Close Accounts

This is another tip to keep from dragging down your credit score almost overnight. Keep credit cards and other revolving accounts open if you can, even if you aren’t using them. They can help reduce your credit utilization and increase your credit age, both of which are good for your score.

How Is Credit Score Calculated?

Understanding how your credit score is calculated helps you make good decisions that can boost your score. Credit scores are based on five factors:

Payment history, which is whether you pay your bills on time regularly

Credit utilization, which is how much of your open credit you’ve used

Credit age, which is the average age of your open accounts as well as how long you’ve had credit

Credit mix, which indicates you have a healthy mix of revolving and installment accounts

New credit, i.e., hard inquiries, which refers to whether a lot of lenders are checking your credit to evaluate you for loans

How Often Does Your Credit Score Update?

Credit scores typically update at least monthly, but big changes to your financial situation can boost your score or drive it down more quickly. It really depends on how often your various creditors report this information to the credit bureaus.

Work on Your Credit Now

It’s never a bad time to start working on your credit. Start by signing up for ExtraCredit so you’re in the know about your credit scores and reports and can make educated decisions to build your credit.

You’ve planned your dream vacation and invested thousands of dollars in prepaid reservations. Then, a family member becomes seriously ill or the cruise line that you’ve booked with declares bankruptcy. If you need to cancel a trip for an unexpected reason, you might lose a lot of money.

However, if you used your eligible Capital One card — such as the Capital One Venture X Rewards Credit Card — to book your ticket, you can use the card’s trip cancellation insurance to request reimbursement for some of your prepaid expenses.

Before you book your trip, here’s what you need to know about Capital One trip cancellation insurance, including what the policy covers and how to file a claim.

When does Capital One trip cancellation insurance provide coverage?

Capital One trip cancellation insurance covers trips booked with an eligible Capital One card that are canceled for a covered reason. The list of covered reasons includes:

Death, accidental injury or illness of you or someone in your immediate family.

Financial insolvency of your airline, cruise ship, bus line or other common carrier.

Capital One will require you to have a physician verify any death, bodily injury or illness that is preventing you from completing your trip. Certain types of injuries, such as those caused by participating in sports or while under the influence of drugs or alcohol, are excluded.

To be eligible for trip cancellation insurance, you must book the entire cost of your trip with your Capital One credit card. You can also use Capital One Miles or coupons, as long as the cash component of your trip is booked using your card.

Who does Capital One trip cancellation insurance cover?

When you book a trip with your eligible Capital One card, coverage applies only to you, your spouse or domestic partner and any dependent children under 19 years old who live with you. Children under 25 are also covered if they’re considered full-time students.

If you’re an authorized user on someone else’s Capital One account, you and your family members will be covered as long as you use your card to pay for the trip.

What does Capital One trip cancellation insurance cover?

Capital One trip cancellation insurance covers up to $2,000 per person toward non-refundable common carrier tickets. Common carrier tickets include tickets from airlines, ferry lines, bus lines and other forms of scheduled transportation.

Note that Capital One’s benefit covers a much smaller set of prepaid expenses than trip cancellation policies provided by other cards.

The Capital One trip cancellation insurance covers none of these types of prepaid expenses.

How do I file a claim?

If you need to file a claim with Capital One’s insurance, you’ll initiate it by calling the card benefit administrator at 1-800-825-4062. They’ll ask for preliminary details of your claim over the phone and then send you a series of forms to complete.

🤓Nerdy Tip

Be sure to initiate your claim as soon as possible. Capital One recommends that you submit your claim within 20 days of when your trip is canceled.

Once you’ve received your claims forms, you’ll need to provide all requested information, including proof of loss, and return it to the benefits administrator at:

cbsi Card Benefit Services

550 Mamaroneck Avenue, Suite 309

Harrison, NY 10528

Alternatively, you can initiate your claim by sending a written description of your loss to the benefit administrator or submitting your claim online at Eclaimsline.com.

What if the benefits are insufficient?

Capital One’s trip cancellation benefit only covers the cost of your non-refundable common carrier tickets under a limited set of circumstances. For more comprehensive trip cancellation insurance, you might want to consider a standalone travel insurance policy.

A travel insurance policy usually offers an expanded list of covered reasons that may cause you to cancel a trip and reimburses other prepaid expenses like hotels, rental cars, booked tours and other travel arrangements.

You can use an insurance comparison site like SquareMonth to find a travel policy that best fits your needs.

Capital One trip cancellation insurance recapped

Capital One’s trip cancellation insurance is nice to have, but many will want more than just an airfare reimbursement if they need to cancel their trip — not to mention that the covered reasons for cancellation are quite limited.

If you want more coverage, consider using a credit card that offers more robust travel insurance benefits or buy an additional travel insurance policy.

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are our picks for the best travel credit cards of 2023, including those best for:

Learning how to build credit can help if you have a bad credit score or want to improve your current score. You can start by getting a secured credit card, becoming an authorized user, or getting a cosigner on a loan.

If you have bad credit due to derogatory marks, those marks can stay on your credit report for up to seven to ten years, depending on the type of mark. A low credit score leads to higher interest rates, larger deposits, and a low approval rate for loans and lines of credit. Those just beginning to build their credit will have similar challenges, but there are ways to build or work to repair your credit score.

By learning ways to build credit, you will not only improve your financial health, but it can reduce your stress around finances as well. In this article, we go over 12 tips that can help regardless of your specific credit situation.

Table of contents:

Get Added as an Authorized User

Try a Secured Credit Card

Find a Cosigner

Report Utilities and Bills

Get a Credit-Builder Loan

Pay Your Bills on Time

Regularly Check Your Credit Scores and Reports

Dispute Errors on Your Credit Report

Pay Off Collections

Open New Lines of Credit

Request a Credit Limit Increase

Have a Good Credit Mix

1. Get Added as an Authorized User

Becoming an authorized user is one of the most popular ways to build your credit score because you benefit from someone else’s good, established credit history. Also known as “piggybacking,” becoming an authorized user is when someone adds you to their credit card account.

The odds of approval on a credit application are lower if you have a low or bad credit score, so this is a way to start building credit and improve your ability to get your own card later. When you’re an authorized user, the card company will also report the payment history for your credit report when the primary account holder uses and makes payments on their credit card.

You can have a friend or family member add you as an authorized user. While this can be a great way to build credit, it’s useful to know that this can also negatively affect your or the other person’s credit should either of you miss payments or over utilize the credit line.

2. Try a Secured Credit Card

A secured credit card is a type of credit card that most people can acquire through their bank regardless of their credit score. The primary challenge of getting a credit card with a low credit score is that your credit score is one of the wayslenders evaluate risk. If you don’t have a credit history to show that you know how to manage credit or have derogatory marks on your report, credit card companies may be reluctant to loan you money via a credit card.

Secured credit cards are different because rather than borrowing from a financial institution, you borrow from yourself. You do this by depositing money into the credit card account, which becomes your credit limit. For example, if you opened a secured credit card with a $500 deposit, you will have a $500 credit limit. As you use the card and make regular payments, these will be reported to the credit bureaus to help build your credit history and potentially help improve your score.

3. Find a Cosigner

Similar to becoming an authorized user, you can benefit from a cosigner with a good credit score. On your own, you may not receive approval on a personal loan or car loan. When you have a cosigner with a good credit score, the lender sees loaning to you as less of a risk because the cosigner is also attached to the loan.

Although a cosigner can help with the loan approval process, like becoming an authorized user, your credit can also affect that of your cosigner, so it’s important to make full and on-time payments.

4. Report Utilities and Bills

When learning how to build credit, many people don’t realize that most utilities and bills are not reported to the three major credit bureaus. Fortunately, you can purchase services that will report your utilities and bills. Services like Credit.com’s ExtraCredit® subscription help build credit history for people with no credit history or low credit scores.

5. Get a Credit-Builder Loan

Credit-builder loans do just what you think they do—they are loans that help you build credit. Unlike typical loans, where you fill out an application and receive the funds, credit-builder loans are a sort of savings program. When a bank or financial institution provides you with a credit-builder loan, the funds go into an account, and you make payments on the amount. As you make your payments, the lender reports them to the credit bureaus to help build credit history and potentially improve your score with your on-time payments.

Many credit-building programs have higher interest rates than traditional loans due to the higher risk, but they can help your score in the long term. Once you pay the credit-builder loan off with interest, you receive the full loan amount.

6. Pay Your Bills on Time

If you already have lines of credit or loans, paying your bills on time is one of the best ways to continue building your credit score. Your payment history is 35% of your FICO® credit score, which is why paying your bills on time is helpful.

One of the best ways to ensure you never miss a payment is to set up automatic payments for the minimum amount on your credit cards and bills. You can always make additional payments, but when the money comes out of your bank account automatically, you no longer have to worry about forgetting a payment.

7. Regularly Check Your Credit Scores and Reports

A great habit for building credit or trying to maintain a good credit score is to check your credit score and report regularly. Unlike a car experiencing mechanical issues, there are no warning lights or alarms that go off when your credit score drops or a negative mark appears on your report.

Checking your scores and reports lets you know if there are any issues sooner rather than later. It can also help you stay motivated as you work to build your score as you see the number start to rise.

Although your credit report doesn’t notify you about changes automatically, Credit.com’s ExtraCredit® offers credit monitoring as part of the subscription service. Credit.com also offers a free service whereyou also get your free credit report card to analyze your current score for issues that need your attention.

8. Dispute Errors on Your Credit Report

If you regularly check your credit score and credit report, you may find errors. Sometimes, bill and credit card companies don’t properly report your payments, which can hurt your credit. Credit card fraud and identity theft are also more common than you may think, and this can also cause your credit score to drop. Should you find errors on your credit report, it’s your right to challenge them. To file a formal dispute, you need to write a dispute letter showing documentation of payments and other information to the creditor reporting the error. If you have other potential errors, you can request a verification of the reporting from the credit bureaus. They will investigate then respond with the results, typically within 30 to 45 days.

9. Pay Off Collections

As you now know, derogatory marks on your credit report can have a negative impact on your credit score. When someone doesn’t pay their bills, the account becomes delinquent and a collection agency could buy it. You can find the information about the collection agency on your credit report and then contact them to pay off the debt.

In some cases, a collection agency will let you settle the debt for a fraction of what you owe. When you agree to pay off or settle the debt, you can ask for a pay-for-delete letter. After you pay off a collection agency, the derogatory mark can stay on your credit report for years. A pay-for-delete letter is an agreement that the collection agency will have the collection item removed from your report once you pay it. Get this agreement in writing!

Before negotiating with a collection agency, it’s helpful to also know your debt collection rights.

10. Open New Lines of Credit

For those with an established credit score, a good way to continue improving your credit score is to open new lines of credit. In addition to your payment history, credit utilization is the second-most important factor for your credit score. Your credit utilization is worth 30% of your FICO credit score, and new lines of credit can help keep your utilization low as long as you don’t use them.

Credit utilization is the amount you owe compared to your overall credit limit, and ideally, your utilization should be under 30%. For example, if you have five credit cards with a combined $5,000 credit limit and owe $2,500, your utilization is at 50%. If you open up a new line of credit for an additional $5,000, raising your total limit to $10,000, your utilization is now only 25% if you owe $2,500.

11. Request a Credit Limit Increase

If you don’t want to open new lines of credit but still want to build your credit, you can request a credit increase from your credit card company. This accomplishes the same thing with regard to credit utilization as opening new lines of credit. If you have a good payment history with your credit card company, they are more likely to increase your credit limit, lowering your utilization rate.

12. Have a Good Credit Mix

Your credit mix shows that you can handle multiple types of credit. The two primary credit types are installment and revolving credit. Revolving credit is a line of credit that allows you to spend up to the credit limit, make payments, and then use the credit again. Some common forms of revolving credit include:

Credit cards

Personal lines of credit

Home equity lines of credit (HELOC)

Installment loans are lines of credit that give you an amount you pay down to $0 over time, and then the account closes. Examples of installment loans include:

Auto loans

Home loans

Student loans

Personal loans

Check Your Credit and Start Building It Today

Checking and monitoring your credit scores and credit reports is the key to building your credit and maintaining a positive score. As you continue to build your credit, you may begin to save money on interest rates and have additional financial freedom as you can access more opportunities.

If you want to begin your credit-building journey, Credit.com’s ExtraCredit subscription offers credit monitoring, bill reporting, personalized credit and loan recommendations, and more. You can also access your free credit score and free credit report card through Credit.com today.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

Many people with good credit scores own at least one credit card, with 82% of all credit card holders boasting credit scores of 680 and higher.

When used responsibly, credit cards can be a great tool for building credit. Here’s a complete guide on how to build credit with a credit card.

Table of contents:

5 Best Ways to Build Credit with a Credit Card

To improve your credit score with a credit card, you need to know how to best use your credit card. Responsible credit card usage is key to boosting your credit—it won’t increase simply because you got a credit card. Here are the five best ways to increase your credit score using a credit card.

1. Pay bills on time

One of the most important parts of having a credit card is paying your credit card bill on time. Payment history is the largest factor in your FICO® score at 35%, which means it can make or break your score.

Get into the habit of paying your bills on time every month and watch your score grow. Setting up automatic payments for a few days before your bill is due can help make sure you never miss a payment and give a cushion of time for the payment to go through.

2. Keep your utilization rate low

Your credit utilization rate, or credit utilization ratio, is the amount of credit you’re using divided by the amount of credit available to you (your credit limit).

Let’s say your credit limit is $500. This is the maximum amount you can spend on your credit card before payments are denied, but that doesn’t mean you should spend that much.

It’s best for your credit score to keep your utilization rate under 30%—under 10% is even better! This is because the amount of money you owe impacts 30% of your FICO score and the lower this number is, the better. But how much can you actually spend with your credit card?

If your credit limit is $500, 30% of that is $150. So, you should aim to never have a balance over $150 on your credit card. Even better, shoot for a balance under $50 (10% of your limit).

3. Don’t overspend

You don’t need to carry a balance on your credit card to improve your credit score. Paying off your balance in full every time, not just making the minimum payment, is the best practice.

Carrying a balance can cost you more in credit card interest and late fees. Plus, it may increase your utilization rate and damage your credit score. Do your best to avoid credit card debt and treat your credit card like a debit card—only spending money you have.

4. Use your card regularly

Using your first credit card requires a delicate balance. You don’t want to spend too much and go over your utilization rate, but if you don’t use it regularly enough, the lender may close your account. Using some of your available credit is one of the best ways to boost your credit.

The solution is to use your card to make regular, small purchases. This could include purchases like:

Gas

Groceries

Small, recurring bills

Inexpensive meals

After a while of making these regular purchases and paying them off on time, your credit card provider will probably increase your credit limit, allowing you to spend more with your card. Until then, using your card for these types of purchases can help you establish responsible credit card habits and keep your credit utilization low.

5. Avoid opening more cards

Every time you apply for a new credit card, the creditor makes a hard inquiry on your credit, which drops your credit score a few points. You’ll be able to earn back those points in the long run, but in most cases, if you apply to a bunch of credit cards at once, those hard inquiries will add up and take a toll on your credit.

For this reason, you should only apply for one credit card at a time and make sure it’s a good match for you. When you’re first building your credit, it’s best to start small with one card and take your time to practice building credit with it before opening more accounts.

How to Use Credit Cards to Start Building Credit

To recap, here’s a step-by-step guide to increasing your credit score with your first credit card.

Apply for a credit card you can qualify for.

Connect your bank account for automatic monthly payments.

Make small purchases to use under 30% of your credit limit (under 10% is better).

Pay your balance in full and on time each month.

Avoid opening new credit cards.

Regularly monitor your credit report.

If you’re not sure what kind of credit card to apply for, here are the types of credit cards you can use to start building credit and the advantages of each.

Unsecured credit card: An unsecured credit card, or standard credit card, is great if you qualify for one. They don’t require a deposit to use and often offer rewards.

Secured credit card: This type of card is great if you can’t get approved for a standard credit card. Secured cards require a deposit but then they work like any other credit card.

Student credit card: If you’re a student, it’s typically easier to qualify for a student card than a standard credit card. These cards can have decent rewards too!

Store credit card: Store credit cards can sometimes be easier to qualify for than standard cards. Be sure to choose one for a store you shop at often or can be used at other places besides the specific store.

Authorized user for a credit card: A family member or friend can add you as an authorized user on their credit card. You’ll be able to make purchases and receive credit score benefits but won’t be responsible for charges.

How to Build Credit without a Credit Card

If you’re not ready for a credit card or can’t get approved for one, here are some ways to build credit without a credit card.

Credit-builder loans

Credit-builder loans are a lot like what they sound like. They’re low-interest rate loans that help borrowers with poor or no credit build credit, and they function differently than your typical loan.

With a standard loan, you receive the money you’re borrowing upfront, but with a credit builder loan, the money is held in a savings or CD account until you pay it off. This makes it very low-risk for the lender, as your payments are also adding your collateral to the savings account.

You make monthly payments, including interest on the loan, and making these payments on time will help build your credit. Once you pay off the loan, you get all the money back and in some cases, interest if it was incurred while your savings collateral was being held.

Rent reporting

The three major credit bureaus, Equifax®, Experian® and TransUnion®, only include rent payment information on your credit report if they receive it. Most landlords don’t report this information, but it could benefit your score if you consistently pay your rent on time.

You can ask your landlord to report your rent payments or find a rent reporting service that will let you submit the information yourself. Ideally, your rent payments should be reported to all three bureaus for maximum impact.

Passbook loans

This type of loan is very similar to credit-builder loans, except it uses the money you already have in your savings or CD account as collateral. Interest rates for passbook or CD loans are typically lower than credit cards or personal loans.

Like credit-builder loans, you build credit as you make payments on the loan each month and can access the money once you’ve paid it off. Check that your bank will report your payments to all three credit bureaus before taking out this type of loan.

Building Credit with a Credit Card FAQ

Have more questions about how to use a credit card to build credit? Check out the answers to these common credit card questions.

When should you pay your credit card bill to build credit?

You should pay your credit card bill by its due date, at the very least. Paying your bill early (before the end of your billing period) or making extra payments if you’re planning to carry a balance may help boost your credit score even more since it will reduce your utilization rate.

How fast does a credit card build credit?

While it may take a while to build credit, you can help establish a baseline credit score if you have an account open and active for 6 to 12 months, to allow your FICO® score to be calculated. You may be able to establish a baseline credit score after 6-12 months of making credit card payments on time. With consistent and responsible credit card usage, you should see a positive impact on your credit over time.

Do you need a credit card to build credit?

No, you don’t need a credit card to build credit. Responsible credit card usage is one of the easiest ways to build credit, but it may not be the right answer for everyone. There are other ways to improve your credit score, like taking out loans, reporting rent and utilities or being added as an authorized user to someone else’s credit card.

A credit card is a great way to start building credit. If you’re looking for more ways to boost your credit score, check out our resources on Credit.com and the features included with ExtraCredit. ExtraCredit is a full- credit score monitoring service that can help you understand what areas of your credit you need to work on to build and maintain your good credit.

Disclaimer: The views and opinions expressed in this article are those of the author only and are not endorsed by Credit.com.

When a consumer wants to start building credit, a logical step to take is to get a credit card. However, credit card issuers want to check your credit and payment history before they approve you for a card. Now, if you’re just starting out with credit, you have no credit history to show for, and are often not eligible for credit cards with higher credit limits and rewards.

How do you then get out of this helpless circle? One option is getting a store card. Store cards are often easy to get approved for, even without having previous credit history. And they can help you get into the credit world, at least for starters.

What Is a Store Card?

Store cards are credit cards made by specific stores or brands, for instance; Costco, Walmart, Amazon, etc. These cards are made to be used for purchases at the store. Store cards often offer perks at the store such as bonus points, in-store discounts, and more.

There are store cards that act as credit cards and can be used in any other store on all purchases, besides the specific store. However, the card benefits will usually be specifically at the store. Compare different credit card offers to see which one works best for you.

How a Store Card Can Help You Build Credit-Easy Approval

Store cards are often thought of as beginner cards. They’re often easy to get approved for, even for someone completely new to credit.

That’s how a store card can help you jump-start your credit journey. If you have zero credit, regular credit cards may not approve you for credit cards because they want to see your payment history first. But store cards may have higher approval odds. Carefully consider one in your credit-building journey.

Downside of a Store Card

Though a store card is easy to get approved for, you most likely won’t get approved for a high credit limit. You can get approved for a limit of as low as a couple hundred dollars with a store card. In addition, the APR will usually be very high on store cards.

Store Cards and Your Credit Score

If you’re a beginner to credit and want to build your credit using a store card, here’s how.

Research store cards that report to at least one credit bureau.

Apply for a store card and if approved, use it to. Simply build your credit history by using and paying the card payments. By doing so, you work toward establishing a positive payment history to help get other credit card types later.

After some time of being with a store card, a good idea is to see how your credit score has been affected. Then you can see if applying for a credit card that is a step up to the next level of building more credit history. See some cards that are geared toward building credit history here.

To sum it up, store cards are great for breaking into credit. After some time, you may become eligible for cards that can help you keep building and establishing your credit. From there, to the premium cards you go!

Store Card Pros and Cons

Store cards have their pros and cons.

Pros

Cons

Easier to get approved for

It’s not considered a real credit card according to FICO

Helps you start building credit

Higher interest rates

Store perks and benefits

Can sometimes only be used at the store/brand

Low credit limits

Alternatives for Building Credit

Building your credit is not limited to getting a store card. There are alternative ways to go about building your credit.

Secured Cards

Secured cards work a little differently than regular credit cards. With a secured card, the card issuer requests a deposit from you, a set amount of money which they hold as collateral in case you fail to make payments. The deposit amount is usually the same as your credit limit (a $500 deposit lends to a $500 credit limit).

Secured cards are generally easier to get approved for and with some cards, you don’t need any previous credit history. So, they’re good as a first card. As long as you make on-time payments, you’ll be helping build your credit history.

Secured Card Pros and Cons

Pros

Cons

They’re easier to get approved for

You must leave a deposit

They help start up your credit

They often don’t earn rewards

Authorized User

Another alternative to store cards is building credit through becoming an authorized user on an existing credit card.

When you’re not in a credit position to get approved for your own credit loan, you can get added as an authorized user on the account of a friend, spouse, family member, acquaintance, or anyone else. Usually, depending on the card issue, only family members are allowed. Verify this with the card issuer/

The primary account holder adds you as an authorized user on the account. Only do this on an account that is in good standing. Once the account is reported to the credit bureaus and to your credit report, the account history of the card becomes yours too.

So, if the primary has had the card open for two years and has made on-time payments all that time, that’s now reflected on your credit report. This can help build your credit history.

Pros and Cons of Becoming an Authorized User

Pros

Cons

It can help your credit

You could have conflicts with the primary cardholder

It’s simple to do and there’s no need to lock up funds

A good credit score will make your life a lot easier; it will help you qualify for loans, apartments and even jobs. But you’re not born with a credit history. Much like you have to spend money to make money, you need to borrow money to prove you’re good at borrowing (and paying back your debts). In fact, according to Nationwide, credit scores help insurance companies predict future losses. So, how can you start your credit-building journey? Here are ways new cardholders can build credit.

Understanding Credit Score Perks

Your credit score is woven into almost every area of your life. “Crummy credit can cost you a fortune throughout your life,” explains Matt Schulz, chief credit analyst at LendingTree. “It’s as simple as that. It’ll lead to higher interest rates and fees on mortgages, credit cards and loans. It can keep you from getting the apartment you want. It can lead to higher insurance premiums. It’s a big, big deal.”

There are two main types of credit scores: your FICO Score and your VantageScore. Most lenders review your FICO Score when making a financing decision. It ranges from 300 to 850, with a “good” score starting in the high 600s. It’s calculated based on a variety of factors, including payment history, credit usage, the length of your credit history, and more. The VantageScore follows similar metrics but focuses less on payment history, allowing scores to be generated faster than FICO. Regardless of the type of score, a proven record of responsible borrowing shows lenders that you’re more likely to pay back your debt, and then they can offer you lower interest rates and charge fewer fees.

Related Read: 7 Unexpected Benefits of a Good Credit Score

New to Credit? Here’s How to Build Your Score Quickly

Get a secured credit card. A secured credit card is a great way to build credit from scratch. It works just like an unsecured card, except that you make a security deposit that is equal to the amount of the credit limit. For example, if you deposit $500, your credit limit is also $500. “Consumers love these cards because they’re easy to get and their low credit limits mean there’s no danger of going too wild on a spending spree,” says Schulz. “Banks love them because there’s no risk. If someone doesn’t pay their bill, the bank simply takes the security deposit. It’s a win for everyone involved.” Before applying for a secured card, make sure the lender reports your usage to the three credit bureaus–Equifax, Experian and TransUnion. If it doesn’t, you won’t build credit. Also, check to see if the lender offers an upgrade to an unsecured card.

Make timely payments. Once you have your first credit card–be it secured or unsecured– focus on paying your bill in full on time, every time. Payment history is a big component of your credit score. Each month you pay your full balance on time, you’re proving your creditworthiness. “Think about it like borrowing the car keys from your parents,” explains Schulz. “The first time you do it, they’re not going to let you do much. Once you’ve shown you can handle a little responsibility, they’ll give you more, though. Eventually, they’ll hand over the keys without thinking much of it.”

Use your card often. The more you use your card, the better. The key, though, is to use it smartly. Pick up the check when you’re out to dinner with friends, knowing they’ll reimburse you for their meals. Use it for everyday expenses like groceries and gas. You can even use your card to pay rent, though there will usually be processing fees added on by your landlord. Just remember: Pay the bill in full, every month. You should also never max out your card. Your credit utilization ratio–how much credit you’re using compared to the total credit available to you–is another aspect of your credit score.

Become an authorized user. If you can’t open a credit card yourself yet, become an authorized user on someone else’s account. Ultimately, they will be responsible for the charges on the account, so you need to have a good relationship with this person. Becoming an authorized user allows you to link to this person’s good credit and thus build yours with steady payments.

Apply for a credit-builder loan. A unique way to build credit is to apply for a credit-builder loan. With these loans, you make monthly payments to the lender for a set period of time. The deposits are kept in a savings account or a certificate of deposit. Once the payment period ends, you get the money back, sans fees or interest charged.

Be determined. Building credit can be daunting, but don’t give up. With each passing month, your timely payments will boost your score. Use texts or autopay features to make sure you’re paying your bills on time. Do whatever you need to do to keep at it. Different apps and some credit cards offer estimates of your credit score, but know that you’re entitled to one free credit report every year from AnnualCreditReport.com. Get in the habit of checking your report every year to make sure there are no lingering issues that are hampering your credit-building endeavors.

About the Author

Chris O’Shea is a freelance writer whose work has appeared in GQ, NerdWallet, Esquire, New York Magazine, and more.