You may have thought that mortgage lenders were raking it in, what with the record low mortgage rates currently on offer.

But 2011 was actually the slowest 365 days in mortgage lending since the year 2000, according to figures released by Inside Mortgage Finance.

The company noted that residential home loan origination volume totaled an estimated $1.35 trillion last year, which was down a hefty 17.2 percent from 2010.

The company attributed the weakness to a soft second quarter, when just $280 billion in new mortgages were extended to homeowners.

That was actually the weakest quarter since the end of 2008, when you know what hit the fan.

Around that time, interest rates on the popular 30-year fixed were close to 5%, which is more than a point above where they stand now.

Couldn’t Keep Up With Demand

Interestingly enough, many mortgage lenders have complained about having too much business in recent years, so it’s unclear if they actually wanted more volume.

It wasn’t long ago that Chase supposedly inflated its refinance rates to temper demand, partially because of reduced staff and more manpower directed toward things like loan modifications.

And back in 2009, Wells Fargo complained about the quality of the loan applications it was underwriting, hinting that it may have been hurting them more than it was helping.

Wells Fargo Top Mortgage Lender in Fourth Quarter 2011

Still, the San Francisco-based bank has retained its position as the top mortgage lender in the nation. The company originated $120 billion in mortgages during the final quarter of 2011.

Their market share increased from 27 percent in the third quarter to 30 percent in the fourth quarter. Wow.

They were followed (distantly) by JP Morgan Chase, which brought in a paltry $42 billion.

Coming in third was Citibank with $23 billion in mortgage loan volume. The New York City-based bank pushed ahead of Bank of America, which fell to fourth on $22.4 billion in loan volume.

Bank of America Mortgage Market Share Lower With Countrywide

Yes, you read that right.

Somewhat amazingly, Bank of America’s share of the mortgage market has actually fallen since it scooped up former mortgage lending giant Countrywide Financial.

BofA’s share of the mortgage market has dwindled to roughly six percent, which is less than the 7.8 percent share held back in 2007, before the Countrywide acquisition.

They gave Wells Fargo a run for their money in 2010, but soon after eliminated both their wholesale and correspondent businesses, with the latter providing about half of production.

Now the bank is left with a more focused retail arm, which makes mortgages in-house for its banking customers.

In the long run it’ll probably serve them better given how badly they’ve fared thus far. And they’ve got enough to worry about, what with all those foreclosures…

As we near the end of year, it’s a good time to take stock of our credit cards and review which ones have benefits, requirements, or limits that reset at year-end. We’ll also examine which cards give you a quick double-dip credit when applying at year-end, and take a look at which cards to apply for now.

I’ve been doing this write-up with updates each year for the past number of years (2022, 2021, 2020, 2019, 2018, 2017, 2016, 2015). This year again there were many changes. I updated what came to mind, and there are probably some we missed. Please drop a comment below if you notice any changes or inaccuracies changes and we’ll update accordingly.

Calendar Year Spend Limits

Blue Business Plus and Blue Business Cash cards earn 2x/2% everywhere on up to $50,000 in purchases per calendar year. (A report indicates this resets on January 1st, not the December statement close.)

Amex Gold card earns 4x points at US grocery stores up to $25,000 per calendar year. (Resets with December statement or December 31?)

Amex SimplyCash Plus earns 5% at office/wireless and 3% on your chosen category, up to $50,000 per calendar year for each of those. This resets on January 1st each year.

Amex Everyday Preferred $6,000 limit on the 3x grocery store category per calendar year. (Resets with December statement or December 31?)

Amex Everyday $6,000 limit on the 2x grocery store category per calendar year. (Resets with December statement or December 31?)

Blue Cash Preferred $6,000 limit on the 6% grocery store category per calendar year. This resets January 1 each year, not on the December close date.

Blue Cash Everyday $6,000 limit on the 3% grocery store category per calendar year. This resets January 1 each year, not on the December close date.

The Old Blue Cash card does not reset with the calendar year, it goes with your card anniversary.

The INK Plus/Cash and the INK Preferred years do not reset with the calendar year, it goes with the card anniversary.

Also, remember that the annual limits on points earned for credit card referrals by Chase (50,000-100,000 points, depending on the card) and AmEx (55,000 points/$550) will reset on January 1st. If you’re someone who does a lot of referrals, be sure to max out what you can before December 31 and then start referring again on January 1st.

Q4 Categories: Chase Freedom, Discover, Citi Dividend, and U.S. Bank Cash+ and a few other cards have quarterly categories. The current categories for Q4 will end on December 31. More details here. Likewise, the quarterly $2,500 limit on the Bank of America Cash Rewards card will renew on January 1. There are also some spend offers from Chase, notably the 10x Gas offer, which ends on December 31st.

You have until December 31st to max out your I Bonds purchases which are limited to $10,000 each calendar year.

List of all deals ending on December 31st can be found on our Deals Calendar.

Calendar Year Spend Requirements

Amex Hilton Surpass gets a free weekend night with $15,000 in spend within the calendar year, and gets Diamond status with $40,000 in spend within the calendar year.

Amex Hilton Honors business card gets a free weekend night with $15,000 in spend within the calendar year, it gets a second weekend night with a total of $60,000 in spend within the calendar year. It also gets Diamond status with $40,000 in spend within the calendar year.

Amex Hilton Honors gets Gold status with $20,000 in spend within the calendar year.

Amex Hilton Aspire gets a second free weekend night with $60,000 in spend within the calendar year. (First weekend night comes as a card benefit, and is based on card anniversary, not calendar year.

Amex Delta Reserve – both personal and business versions – earn 15,000 MQMs (18,750 MGMs for 2021 due to temporary bonus) and 15,000 bonus miles $30,000 in spend within the calendar year, and an additional 15,000 MQMs and 15,000 bonus miles if you spend a total of $60,000 within the calendar year.

Amex Delta Platinum – both personal and business versions- earn 10,000 MQMs and 10,000 bonus miles when you spent $25,000 in a calendar year, and an additional 10,000 MQMs and 10,000 bonus miles if you spend a total of $50,000 within the calendar year.

Amex Platinum consumer and business cards – spend $75,000 or more during a calendar year and receive complimentary Centurion lounge access for up to two guests per visit.

Barclay Jetblue Plus card earns Mosaic status with $50,000 in spend per calendar year.

Chase British Airways card gets the Travel Together Ticket benefit when spending $30,000 in a calendar year.

Chase Hyatt card gets an additional night if you spend $15,000 in the past year. This one has now changed to go based on the calendar year. Finish up your spending now if you’re trying to get the additional night and begin your spending for next year on January 1st.

Chase Hyatt cards offer elite nights with spend: the Hyatt consumer card gets 2 nights for every $5,000 spent; this does not reset at all. The Hyatt business card gets 5 nights for every $10,000 spent; this resets with the calendar year.

Citi American Airlines AAdvantage Platinum Select card gets $125 flight discount certificate after spending $20,000 or more – this goes with the cardmember year (based on 12 billing statements), not based on calendar year.

American Express Cards

Airline Credit

Amex Platinum personal, Platinum business, and Hilton Aspire cards have an airline incidental credit each year: $250 for the Hilton Aspire and $200 for the Platinum cards (see what counts here). Unfortunately, gift cards no longer trigger the airline incidental credits.

With these cards, the airline credit is based on the calendar year, not on the statement closing. You can put the airline incidental charges anytime until December 31 and have it count toward the current year. It might have to actually post before year’s end, though; give a few days for that to happen.

The Amex airline credit is different than the others in this list in that you only get reimbursed for incidental spend on your designated airline. Be sure to designate that before putting the charge on the card.

If you’re looking to apply, there is still time to do so and get the airline credit for the current year. The annual fee usually hits around a month after card approval – useful to keep in mind for maximizing the travel credits without annual fees and for triple-dipping. (For those applying in the final few days of the year, see this tip.)

Related: Opening a Schwab Brokerage, Checking, and Amex Platinum Credit Card before Year’s End

Platinum Hotel Credit

The Platinum personal card comes with a $200 annual hotel credit on select prepaid bookings with American Express Travel. Be sure to book before December 31st. You don’t need to complete your travel by that date.

Platinum Uber Credit

The Platinum personal card also comes with a monthly $15 credit, remember that it gets increased to $35 during the month of December.

Platinum Saks Credit

The Platinum personal card also comes with a $50 Saks Fifth Avenue credit twice per year: one from January to June and one from July to December. Be sure to use that up before the end of December. They only charge you after the item ships, so give some leeway here.

Platinum Business Dell Credit

The business Platinum card comes with a $200 Dell credit twice per year: one from January to June and one from July to December. Be sure to use that up before the end of December (along with the Amex Offer at Dell which expires then). Give some leeway for the charge to post by December 31.

Hilton Aspire

The Hilton Aspire card also comes with a $250 Hilton Resort Credit and a free weekend night. Those are based on the cardmember year, not calendar year.

2024 Changes:

The Hilton Aspire $250 resort credit is changing on 1/1/24 to become a $200 resort credit twice per year. This goes based on the calendar year – once for January through June and once for July through December.

The $200 airline incidental credit is also changing to become a $50 airline flight credit each quarter – this goes by the calendar quarter.

The Hilton Surpass card also now has a quarterly $50 credit purchases made directly with a property in the Hilton this goes based on the calendar quarter.

Amex Green

The Green personal card comes with an annual $189 CLEAR credit and annual $100 LoungeBuddy credit. These reset each calendar year, so you should be able to use the credit for this year anytime until December 31.

Other Credits

Bank of America

Premium Rewards

TheBank of America Premium Rewards card comes with $100 airline incidental credit (see what counts here). This resets based on the calendar year. Finish up your statement credit with this one by December 31 (buying AA gift card or United Travel Bank credit is easiest), and start using your new credit on January 1. I’ll buy a gift card right away in case they close that loophole. (Note, the airline incidental meter seems to take a few days/weeks until it shows the reset. While it should be internally reset on January 1st, you might want to wait until you see it reset to zero for the avoidance of doubt.)

Premium Rewards Elite

The Bank of America Premium Rewards Elite Visa card comes with an annual $300 airline incidental credit and $150 lifestyle convenience credit (including streaming services, food delivery, fitness subscriptions and rideshare services). These reset with the calendar year.

Be sure to use up your credits from this year now, and begin using next year’s credits after the new year begins. It can also make sense to apply now and try for a triple dip on the card benefits.

Barclay JetBlue

The Barclay JetBlue Plus card gets $100 calendar year credit for JetBlue Vacations bookings.

Capital One Venture X

The Capital One Venture X personal card offers a $300 credit for bookings made on Capital One Travel. This renews each cardmember year, it’s not based on the calendar year. Same on the Venture X Business card.

Chase Cards

Southwest

Earning 135,000 Southwest points earns you the Southwest Companion Pass. Credit cardholders only need to earn 125,000 miles. The best way to time yourself is to earn the miles at the beginning of the calendar year since Companion Pass continues for the next entire calendar year. For example, if you earn 125,000 Southwest miles during January 2024, you’ll have the Companion Pass for the rest of 2024 and the entire 2025.

The easiest strategy to earn the Companion Pass has always been by getting a credit card signup bonus on the Southwest credit card. In our case, you’ll want to apply sometime in the next couple of months, taking care to ensure NOT to meet the spend requirement until after January 1st. (Technically, you can meet the spend requirement during December, so long as the statement won’t close until after the 1st.) The signup bonus points on the two cards will post after you complete the spend in early 2024, and you’ll have a Companion Pass for nearly two years.

Southwest is currently offering a signup bonus of 75,000 points with $3,000 spend. You can also signup for a Chase Southwest business card and get 80,000 points after $5,000 spend. Or you can earn points by referring friends to the Southwest card, doing category spend, shopping portal spend, or an actual flight. Again, be careful with the timing on ALL points earned.

Many of us are not eligible for any of the Southwest cards at all due to the 5/24 rule, or because you’re a current Southwest cardholder of any version or because you got a bonus within the past 24 months.

$75 Southwest Priority Credit

The new Southwest Priority card comes with a $75 annual Southwest travel credit which runs on the cardmember year, not the calendar year. No need to use it up now, specifically.

Sapphire Reserve

TheChase Sapphire Reserve card comes with a $300 travel credit (see what counts here). This used to be based on the calendar year, but now it’s based on the cardmember year – no specific need to use this now.

And if you’re applying for a new CSR card, there’s no special reason to apply before year’s end. Whenever you apply, you’ll get just one travel credit during the first year (maybe you can squeeze a second credit in right after the year renews).

Those who got the CSR before May 21, 2017, are grandfathered into the old system where the travel credit renewal goes with the calendar year. (It’s based on the December statement closing, not December 31.) Be sure you’ve already used up your credit for this year, and remember that you’ll soon be able to begin using 2020’s credit.

The Chase PYB 1.25 redemption categories ends on December 31, though they are likely to get extended.

Also, remember each quarter to use up your $15 in DoorDash credits.

Sapphire Preferred

The Chase Sapphire Preferred card comes with a $50 annual hotel credit via the Chase travel portal. This resets based on the cardmember year, not the calendar year.

Ritz-Carlton

The Chase Ritz-Carlton card offers up to $300 reimbursements for airline incidental charges (see what counts here). Chase counts the benefit based on the calendar year, not cardmember year. (It goes based on the actual calendar year, not based on your statements.) Use the credits before December 31 and begin using next year’s credit on January 1.

IHG Cards

The Chase IHG card gets a free night each year. This does not reset with the calendar year, it goes with your card anniversary.

IHG cards also have spending thresholds of $10,000, $20,000, or $40,000 to earn Gold/Diamond status for the following year and to earn 10,000 bonus points (and on the Premier $100 credit). These spend requirements go by the calendar year.

The IHG Premier personal and business cards get $25 in United TravelBank credit twice per year: one $25 United TravelBank gets deposited around January 5, and another $25 around July 5. Requires registration first.

Hyatt

The Chase Hyatt cards get a free night each year. These do not reset with the calendar year, it goes with your card anniversary.

The Hyatt Business card gets $100 in Hyatt credits each year. This is based on card anniversary.

United Quest

The United Quest card gets up to $125 in statement credits as reimbursement for United purchases. This goes based on the card anniversary year, not calendar year. The card also offers up to 10,000 miles back for award flight bookings. Again, this goes with the cardmember year, not calendar year.

Citi

Prestige

The Citi Prestige card comes with a $250 travel credit (see what counts here). The year resets on January 1st. Be sure to give a few days leeway for the charges to go from pending to settled.

If you have a Prestige card, use up the credit now, there’s only a few weeks remaining. The Prestige card is not available for new cardmember signups at this time.

Rewards+

The Citi Rewards+ card comes with a 10% rebate on redemptions, up to 10,000 points bonus per year. This is based on your December statement close. Be sure to max out your 100,000 points redemption before your December statement closes so as to get the full 10k bonus. Redemptions that post on your January statement will count toward next year’s allotment.

Expedia+ Voyager

Those who have the Citi Expedia+ Voyager card get $100 annual credit toward airline incidentals on qualified airlines, Wi-Fi carriers, or for the Global Entry application fee. This credit resets each calendar year; be sure to use it up before your December statement closes as any purchases on your January statement will count toward next year’s benefit.

AAdvantage Platinum Select

The Citi American Airlines AAdvantage Platinum Select card gets $125 American Airlines Flight Discount certificate after spending $20,000 or more during your credit cardmembership year (every 12 months from the billing cycle after your anniversary month through the billing cycle of your next anniversary month).

Citigold

Those with Citigold relationship status with Citibank get an annual credit of either $200 or $400 toward subscriptions for Amazon prime, Spotify, Hulu, TSApre/GE, and Costco membership. This credit renews at the end of the calendar year. Be sure to use up your allotment before December 30th.

US Bank Altitude Reserve

The US Bank Altitude Reserve card comes with a $325 annual travel and dining credit. In this case, the travel credit goes based on the cardmember year, not the calendar year. No specific reason to use this now.

Wells Fargo Propel World

The Wells Fargo Propel World card has a $100 airline incidental credit (see what counts here).This credit goes based on the cardmember year, not the calendar year. Check when you applied and be sure to use it up by your anniversary date.

Smaller Banks

CNB Crystal

The CNB Crystal card offers a $350 annual incidental charges (see what counts here). CNB counts this based on the calendar year. Any spend until December 31 will count as part of the current year, and January 1 begins the next year. Be sure to complete your spend before December 31. Give a few days for the charge to settle before year’s end (though it reportedly works on the last day too).

HSBC Premier

The HSBC Premier World Elite comes with $120 annual Lyft credit which is based on the calendar year. Be sure to use these up before December 31.

PenFed Pathfinder

The PenFed Pathfinder comes with $100 annual air travel ancillary credit (see what counts here). The credit is based on the calendar year, be sure to use yours before the year is up.

Buying a home can be a daunting task. However, there are programs in place for first-time homebuyers to make it a little easier.

One of the ways you can get a mortgage, even if you don’t have a big down payment or a perfect credit score, is the Federal Housing Administration (FHA) loan program.

Best FHA Lenders and Online Marketplaces

Here are some of the best FHA loan lenders, as well as marketplaces where you can easily compare your options.

loanDepot

You can live in any state and get access to an FHA mortgage through loanDepot.

This company is known for the fact that loan officers don’t get any sort of incentive to encourage you to take one action over another. This can provide you with peace of mind, knowing that the information you get will be best suited for your needs.

When you use loanDepot, though, you need to watch out for origination fees. You might have to pay between 1% and 5% of the home’s purchase price. Carefully consider terms from other lenders before moving forward.

Read our full review of loanDepot

LendingTree

One of the first places to look for an FHA mortgage is LendingTree, an online marketplace.

Rather than directly offering FHA mortgages to borrowers, LendingTree provides a platform where you can submit your information once, and then have various lenders compete for your business by offering you quotes.

When you fill out the form, make sure you indicate that you’re looking for an FHA loan. When you do that, you can get as many as five loan offers minutes after submitting your loan application.

With the information you get from LendingTree, you can have a pretty good idea of what you qualify for and what you can expect.

Read our full review of LendingTree

Quicken Loans

Over the years, Quicken Loans has become one of the most trusted lenders in the business.

In addition to offering conventional loans, you can also get an FHA loan through Quicken Loans. In fact, Quicken is the largest FHA lender in the country.

They state that you’ll need a credit score of at least 580, a debt-to-income ratio (DTI) of no more than 50%, and a steady employment history.

Quicken Loans has a completely online application process and uses technology to verify employment and income for the majority of applicants.

Even if you don’t end up with an FHA loan, Quicken Loans is very flexible and can help you find a loan that fits your needs.

New American Funding

Access to FHA loans is a hallmark of New American Funding, which offers several programs. With this company, you can even explore the possibility of an FHA renovation loan.

In addition to offering access to numerous programs, they also use manual underwriting, meaning that alternative credit data can be relied on. This can be useful if you have a lower credit score.

While you still have to meet FHA requirements, other underwriting requirements might be a little more flexible.

Read our full review of New American Funding

Flagstar Bank

In addition to allowing applicants to provide nontraditional trade lines for underwriting consideration, Flagstar Bank is also known for offering loan packages meant for professionals.

In many cases, there are specific needs associated with being a CPA, architect, doctor, or lawyer. This is a bank that offers professional loan packages that can meet those needs.

Flagstar’s flexibility can be a great asset. However, it’s also important to note that you might end up with a steep origination fee. Weigh that against the benefits and compare your Flagstar quote with other options.

Read our full review of Flagstar Bank

CitiMortgage

The mortgage arm of Citibank allows you access to the resources of one of the most recognized nationwide banks.

Not only can you access FHA loans through CitiMortgage, but you can also take advantage of other programs, particularly those that benefit military families.

However, you can’t complete the mortgage application online. It might not be a bad idea to get a few online FHA loan quotes and bring them with you when you meet with a CitiMortgage loan officer.

Read our full review of CitiMortgage

U.S. Bank

Another high-profile national bank, U.S. Bank offers several mortgage products. In addition to getting started online, you can also call a number and speak with a mortgage specialist — including someone near you.

U.S. Bank does not publish a public minimum credit score for FHA loans.

U.S. Bank prides itself on the ability to offer personal service so you can apply for your loan using what’s most comfortable for you.

Read our full review of U.S. Bank

Carrington Mortgage Services

It can be very difficult for borrowers with poor credit to take out a conventional mortgage. If your credit score is low due to financial mistakes in your past, then Carrington Mortgage Services may be a suitable option for you.

This mortgage lender is willing to lend to borrowers with credit scores as low as 500, which makes it a viable option for anyone who is struggling to rebuild their credit.

You will end up paying more money in interest, so if you have good credit, you may be able to find better mortgage rates elsewhere.

Interested FHA borrowers can speak with a Carrington loan officer to get started. The loan officer can walk you through the FHA loan application process and make sure you have everything you need to qualify for an FHA loan.

Read our full review of Carrington Mortgage Services

PennyMac

PennyMac is based in California and does have some brick-and-mortar locations, but the company is known for its superior online services. The company is considered one of the top five mortgage lenders in the U.S.

PennyMac offers various loan options, including FHA loans. You’ll get started by applying online, and then a loan officer will contact you over the phone.

Borrowers need to have a minimum credit score of 580 to qualify, so it’s a suitable option for anyone with less-than-ideal credit.

Read our full review of PennyMac

How do FHA loans work?

Understanding FHA loans can help you buy a home that you can afford. Here’s what you need to know about getting an FHA loan and the best FHA lenders.

FHA loans are backed and guaranteed by the federal government. The government doesn’t actually make the loans, though. Instead, FHA loans are actually originated by individual FHA loan lenders who are approved by the government. The Federal Housing Administration backs the loans, so lenders feel more comfortable with borrowers that might seem to present something of a higher risk.

FHA Loan Requirements

With an FHA loan, you can put down as little as 3.5% for a down payment if you have a minimum credit score of 580. Additionally, there are FHA loans available for those with even lower credit scores, as long as they put down 10% of the purchase price.

You apply for an FHA loan much as you would for any other mortgage loan. The FHA lender will still review your credit history, income information, and other factors. Ultimately, this determines whether you’re approved, how much you can borrow, and your interest rate. You’ll have to pay for private mortgage insurance during your FHA loan, though, so be aware of that added cost.

Before you choose a mortgage lender, though, it’s important to compare your options. Just as you can with any other loan quote, you can shop around and compare offers from different FHA mortgage lenders. Start by looking at the best lenders for FHA home loans. That way you have a better chance of receiving terms that work best for you.

Step-By-Step Guide to Applying for an FHA Loan

Applying for an FHA loan is not as intimidating as it may seem, especially if you break it down into manageable steps. Here’s a clear, concise, and practical guide to walk you through the process:

Identify your budget: It’s crucial to understand what you can afford before you start the loan process. Use online mortgage calculators to determine a comfortable monthly mortgage payment based on your income and current debt.

Check your credit score: Ensure your credit score is in the best shape possible, as it directly affects the interest rate you’ll be offered.

Choose an FHA-approved lender: Not all mortgage lenders are approved to offer FHA loans, so make sure the ones you’re considering are on the FHA’s approved lender list.

Get pre-approved: Pre-approval gives you a clear idea of the loan amount you might qualify for. It involves providing your lender with financial information, like your income, assets, and debts.

Find your home: Once pre-approved, you can start house hunting. Remember to stick to homes within your pre-approved budget.

Apply for the loan: After you’ve found your home and made an offer, you can officially apply for the loan.

Essential Documents for FHA Loan Application

Documentation is key to getting an FHA loan. While the specific documents required may vary slightly by lender, you will typically need the following:

Proof of employment and income: This could be W-2 statements, pay stubs, or tax returns.

Credit information: The lender will pull your credit report, but be prepared to provide any additional documentation they request.

Proof of assets: This includes bank statements, retirement accounts, and any investment accounts.

Residential history: You may need to provide your housing history for the past two years.

Appraisal report: An FHA-approved appraiser must evaluate the property you intend to buy.

Improving Your Credit Score and Debt-to-Income Ratio

While FHA loans are known for their lenient credit requirements, improving your credit score can help you secure better loan terms. Here are some ways to boost your score:

Pay all bills on time.

Reduce your credit card balances.

Avoid applying for new credit just before applying for a loan.

Your debt-to-income (DTI) ratio is another important factor. It’s the percentage of your gross monthly income that goes toward paying debts. A lower DTI is preferable as it indicates you have a good balance between debt and income. Ways to improve your DTI include:

Paying down existing debt.

Avoid taking on new debt.

Increasing your income, if possible.

How to Find the Best FHA Lender

To find the best FHA-approved lender, you will want to compare quotes from multiple lenders. Once you have at least three or four FHA loan quotes, it’s time to compare them. You want to make sure you’re comparing apples to apples, though. Some of the items that you need to watch for in a loan offer include:

Loan origination fees

Interest rate (including whether it’s fixed or adjustable)

FHA mortgage insurance

Required down payment

Length of loan term

Closing costs

Estimates for property tax and home insurance

Make sure the terms are roughly the same so you can make a good comparison. You might also want to see if your potential mortgage lenders are willing to run different scenarios if you’re willing to pay points.

Run the Numbers

You might need to run a few numbers on your own to determine which trade-offs are worth it. For example, one FHA mortgage lender might have no origination fees but charge a higher interest rate.

If interest rates are low enough, you might be better off working with an FHA mortgage lender that charges an origination fee.

Carefully consider these items, and look at the total cost of the loan. In the end, you want a loan that is likely to cost you the least amount of money, while still allowing you to afford your monthly payments.

Common FHA Loan Mistakes and How to Avoid Them

Navigating the world of FHA loans can be tricky, and it’s not uncommon to make a few missteps along the way. Here are some common mistakes borrowers make and tips on how to avoid them:

Mistake 1: Not Understanding the Costs Involved

While FHA loans are a great option for many homebuyers, they come with certain costs like upfront mortgage insurance and annual premiums.

Avoidance Tip: Ensure you fully understand all the costs associated with an FHA loan. Factor these costs into your budget to avoid unpleasant surprises down the line.

Mistake 2: Skipping the Pre-Approval Process

Some borrowers jump straight into the house hunting process without getting pre-approved for a loan, which can lead to disappointment if they can’t secure the necessary financing.

Avoidance Tip: Always get pre-approved before you start your home search. This will give you a clear understanding of what you can afford and make you a more attractive buyer to sellers.

Mistake 3: Not Shopping Around for Lenders

Many borrowers stick with their existing bank or the first lender they come across without comparing options.

Avoidance Tip: Take time to shop around. Different mortgage lenders may offer different interest rates, closing costs, and service levels. Comparing lenders can potentially save you thousands of dollars over the life of your loan.

Mistake 4: Overlooking FHA Loan Limits

FHA loan limits can vary by location and property type, and overlooking these limits can complicate the home buying process.

Avoidance Tip: Be sure to check the FHA loan limit for your specific location and the type of property you’re considering. Stay within these limits to ensure a smoother loan application process.

Mistake 5: Neglecting Your Credit Score

Even though FHA loans are known for lenient credit requirements, neglecting your credit score can lead to unfavorable loan terms.

Avoidance Tip: Regularly monitor your credit score. If possible, take steps to improve it before applying for a loan. A higher score can lead to better interest rates and more favorable terms.

Conclusion: Choosing the Right FHA Lender and Final Thoughts

Throughout the journey of homeownership, choosing the right FHA lender can make a significant difference. Your lender plays a pivotal role, not only in terms of offering competitive rates and costs but also providing guidance and support throughout the home buying process. It’s crucial to find a lender that is not only FHA-approved but also aligns with your financial needs and goals.

Keep in mind, FHA loans are an excellent tool for many aspiring homeowners, particularly first-time buyers and those with lower credit scores or a smaller down payment. However, it’s important to understand all aspects of these loans, from the costs involved to the loan limits and the application process.

Before you embark on your home buying journey, equip yourself with the right knowledge. Do your research, consider your options, and don’t hesitate to seek professional advice if you need it. Remember, it’s about finding the right fit for your situation – what works best for you may not work as well for someone else.

While the road to homeownership may seem daunting, it is one filled with opportunities. By avoiding common mistakes, improving your credit score, and choosing the right lender, you can navigate the process with confidence. Homeownership could be closer than you think. Here’s to your successful journey on the road to owning your dream home!

Mortgage credit quality remained “relatively steady” over the past six months, with 94 percent of loans held by nine key national banks current and performing, according to the OCC Mortgage Metrics Report released today.

The comprehensive data set includes more than 23 million first mortgage loans valued at $3.8 trillion, or approximately 40 percent of all home loans outstanding.

Per the report, the 30-59 day delinquency rate fell to 2.37 percent as of the end of March from 2.61 percent in October, while 90+ day mortgage lates increased to 0.98 percent from 0.82 percent.

Along with late mortgage payments, there were a total of 283,988 foreclosures in process as of the end of March, representing 1.23 percent of the total portfolio, up from 0.90 percent, or 205,248 total in October.

Nearly 10 percent (9.64%) of subprime mortgages were deemed seriously delinquent (60+ day lates or bankrupt borrowers 30+ days late), compared to 4.38 percent of Alt-A mortgages and just 0.74 percent of prime loans.

The delinquency rate for subprime loans actually fell three basis points from last October, while it increased 30 bps for Alt-A loans and 14 bps for prime loans.

Unsurprisingly, while subprime mortgages only accounted for less than nine percent of the total loan portfolio, they were involved in 43 of all loss mitigation efforts as of the end of March.

They also accounted for nearly 33 percent of total foreclosures in process, while prime loans representing 62 percent of the portfolio accounted for just 30 percent of foreclosures in process.

With regard to loss mitigation, prepayment plans outnumbered loan modifications by four to one, but increased at a faster rate in the past six months.

Alt-A mortgages made up about nine percent of the total loan portfolio and accounted for 19 percent of all loss mit action.

The report includes data from mortgage lenders like Bank of America, Citibank, First Horizon, HSBC, JPMorgan Chase, National City, USBank, Wachovia, and Wells Fargo.

Check out the whole report here, it’s full of more data.

The so-called “Independent Foreclosure Review” was tweaked Monday to allow borrowers to receive compensation for loan servicing wrongdoings in a more expeditious manner.

As a result of the latest agreement between the Treasury, OCC, and 10 mortgage servicing companies, the Independent Foreclosure Review will be replaced with a “broader framework.”

The new system will ensure that affected borrowers receive compensation regardless of whether they filed a “request for review form,” which was a key component of the original process.

In fact, borrowers don’t need to take any additional action to be eligible for compensation, and should expect to be contacted by a payment agent by the end of March to discuss payment details.

Additionally, receiving compensation doesn’t waive any legal claims borrowers may have against their loan servicers. And each servicer’s internal complaint process will still remain available to affected borrowers.

The following servicers are part of the Independent Foreclosure Review 2.0:

– Aurora – Bank of America – Citibank – JPMorgan Chase – MetLife Bank – PNC – Sovereign – SunTrust – U.S. Bank – Wells Fargo

They have agreed to provide $3.3 billion in direct payments to eligible borrowers, and another $5.2 billion via loan modifications and forgiveness of deficiency judgments.

Of course, the amount of compensation is expected to vary widely, from as little as a few hundred dollars to as much as $125,000, depending on the magnitude of the “error.”

Eligible borrowers include those with loans serviced by the aforementioned companies whose primary homes were in foreclosure in 2009 and 2010.

The original agreement included several more companies, including Countrywide, EMC, HSBC, IndyMac, National City, Wachovia, and Washington Mutual.

As you can see, many of these names are now obsolete, pushed to the brink thanks to high-risk lending that led up to the now infamous mortgage crisis.

Other Loan Servicers May Soon Join

The OCC and Treasury said it is continuing to work with other major servicers involved in shoddy foreclosure practices, such as robosigning, to reach similar agreements.

Under the previous Independent Foreclosure Review, which was announced all the way back in 2011, borrowers had to submit a complaint to their lender or loan servicer on a case-by-case basis.

A review would then be conducted by an independent consultant to determine any financial injury related to foreclosure proceedings.

Examples of financial injury include dual tracking, where servicers continued to pursue foreclosure even while borrowers attempted to modify their loans, or where fees and/or mortgage balances were higher than what was actually owed.

In hindsight, it wasn’t the most effective way of serving the millions who experienced foreclosure during those years, and clearly wasn’t the most cost efficient method.

Bank of America Cleans Up Countrywide Mess

Could 2013 be the year of the great mortgage cleanup? So far it looks that way.

Bank of America also announced yesterday an agreement with Fannie Mae to resolve any issues with bad loans it sold to the government-sponsored entity.

The Charlotte-based bank said it would make a cash payment of $3.6 billion to Fannie while also repurchasing $6.75 billion in residential mortgage loans sold to the company.

The agreement covers pretty much all loans originated and sold to Fannie from 2000 to 2008, including those from now-defunct Countrywide.

Bank of America will also make a cash payment to Fannie to settle future claims for compensation arising out of past foreclosure delays.

And the bank announced the sale of servicing rights of roughly two million mortgages with an aggregate unpaid balance of $306 billion to Nationstar and Walter Investment Management Corp.

The sale includes 232,000 first mortgages classified as 60+ days delinquent.

Bank of America said it held 775,000 such loans as of December 31, 2012, down from 936,000 loans at September 30, 2012.

Once these sales are complete, those numbers will fall dramatically and the Bank may finally be able to look forward.

Visa and Mastercard are both card networks. Both organizations manage the payment networks through which their cards work. Visa and Mastercard are different companies, but they operate in a very similar way.

Four credit card networks tend to compete for space in consumer wallets. They are Mastercard, Visa, Discover and American Express.

According to Statista, Mastercard and Visa have had the largest market share for a while. As of 2021, they accounted for more than 87% of the market. Compare that to Amex’s 10.5% and Discover’s 2.2% and you can see that most credit cards are Mastercard or Visa.

But is one better than the other? Are there really any differences between these two major credit card networks? Find out in our guide to the difference between Mastercard and Visa below.

In This Piece

What’s the Difference Between Mastercard and Visa?

While they’re both credit card processing networks, these are unique and separate companies. They were founded at different times.

Originally known as the BankAmericard credit card program, Visa launched in 1958. Mastercard began as Master Charge: The Interbank Card when it emerged as a BankAmericard competitor in 1966.

Visa cards don’t work on the Mastercard network, and vice versa. You can’t, for example, use a Visa to pay for something in a store that only accepts Mastercard.

How Are Visa and Mastercard Similar?

There are more similarities between Visa and Mastercard than differences. As mentioned earlier, these are both card networks. They both play the middleman between payment processors and issuing banks.

Both companies operate globally, so if you alert your issuer in advance, you should be able to use your Visa or Mastercard in another country when you go on vacation. Whether you pay fees for this service depends on your card issuer and account details—not on Visa or Mastercard.

Both Visa and Mastercard have tens of millions of merchants in their networks, and both companies’ merchant fees are comparable. Both organizations are publicly traded.

What’s the Difference Between a Network and an Issuer?

The credit card network is the middleman between the payment processor and the issuer of the card. When you pay with a credit card, the information is processed through the network to the bank that issued your credit card. On the other side of the transaction, the data that supports the funds transaction is also processed through the network.

Visa and Mastercard are credit card networks. They’re responsible for the infrastructure for these transactions and for protecting the information as it passes between the payment processor and the issuer. For this service, the credit card networks charge a fee—usually paid in part via a small percentage of every transaction.

An issuer is the bank that issues the card. Examples include Chase, Citibank and Capital One. The issuer is the entity that decides whether you’re approved for a credit card and sets interest rates and fees. It’s also the lender that pays for the goods you purchase with your credit card and the entity you pay back with your payments.

How Does Payment Processing Work?

Visa and Mastercard credit card and debit card payments all go through the same payment process—albeit on different networks. The process looks like this:

Consumers swipe cards—or tap contactless cards—in physical stores or enter card details online.

Merchants send payment authorization requests to their payment processors.

Payment processors send payment requests to the appropriate card network.

Card networks “ask” issuing banks for payment authorization.

Issuing banks approve or deny the transaction.

At this point, transactions are—hopefully—authorized, but they’re not settled yet. The process must continue:

Merchants send approved payment requests to payment processors in batches.

Once again, payment processors send transaction details to Visa, Mastercard or other applicable card networks.

Card networks “ask” issuing banks for previously authorized funds.

Issuing banks release the funds, which travel to merchant banks.

Credit card processing network fees get taken out along the way.

Merchant banks transfer funds into individual merchant accounts.

At this point, the store or other merchant has been paid for the goods or services you bought with your credit card. Your next statement should also reflect the purchase.

Other Mastercard vs Visa Similarities

Visa and Mastercard issuers have a range of products to choose from. Debit cards let you spend money already in your bank account—plus your overdraft if you have one set up. Meanwhile, you must fund prepaid cards in advance.

Visa or Mastercard credit cards have the following things in common.

1. Credit Scores Matter

Card issuers make decisions based on consumers’ credit scores. If you want a card with an extra-low APR and a really high credit limit, you’ll need a top-notch credit score. Lower credit scores generally mean lower credit limits and higher interest rates.

If you’re new to credit or you need to repair your credit, look for a credit builder or credit repair card. You won’t have a very high limit to begin with, and your APR might not be very competitive, but if you make regular payments, you’ll soon qualify for a better product.

Surge Mastercard® Credit Card

All credit types welcome to apply!

Monthly reporting to the three major credit bureaus

Up to $1,000 credit limit doubles up to $2,000! (Simply make your first 6 monthly minimum payments on time)

Fast and easy application process; results in seconds

Use your card at locations everywhere that Mastercard® is accepted

Free online account access 24/7

Checking Account Required

See if you’re Pre-Qualified without impacting your credit score

2. Rewards Cards Provide Value

Mastercard and Visa both partner with issuers that offer rewards cards. Rewards include air miles, points, store-specific rewards, food and beverage rewards and cash back. If you use your rewards card in a savvy way, you can save a lot of money.

3. Fees Vary

Visa and Mastercard don’t set fees—issuing banks do. As a result, fees for Visa and Mastercard products vary widely. Make sure you’re familiar with the over-limit, balance transfer, late payment, and foreign transaction fees on each of your credit card accounts—and stay away from credit cards with unreasonable fee structures.

4. Smart Wallets Protect Information

Both Visa and Mastercard cards are compatible with smart wallets like Apple Pay and Google Pay. Smart wallets hide your card information, so they’re more secure than swiping a card or entering card details online. Every year, more and more brick-and-mortar and online retailers accept smart wallet payments.

5. Discount Programs Save You Money

Some credit cards—especially business credit cards—incorporate high-value discount programs. The Visa SavingsEdge program, for example, can save you more than 15% when you shop with qualifying merchants. Mastercard has a similar program, called Easy Savings. In both cases, you need to enroll your card to get money back.

Which Is Better: Visa or Mastercard?

What’s the difference between Mastercard and Visa? Not that much, actually. The major difference is the company that runs the network. Merchants that accept one usually tend to accept the other, and more merchants accept Visa and Mastercard than any other type of card.

Instead of considering whether you should get a Visa or a Mastercard, think about what type of card you want and which bank you want to work with. Apply for a card that offers the rewards you want and has fees that match your budget. Whichever one you choose, you’ll be able to use it around the globe and get a very similar experience from the card network.

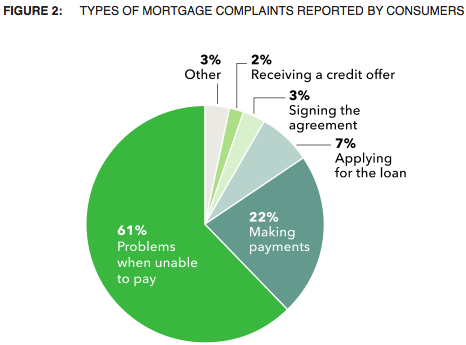

Home loans are the most complained about consumer financial product/service, according to a news release from the Consumer Financial Protection Bureau (CFPB).

The agency said it received approximately 131,300 consumer complaints since July 21, 2011, with 63,700, or 49% of the total, being mortgage-related issues.

Issues related to credit cards accounted for nearly a quarter (23%) of all complaints, followed by bank account issues at 15%, credit reporting concerns at 5%, and student loan problems at 4%.

Ability to Pay the Biggest Mortgage Complaint

The many mortgage complaints were further broken down by type, with “problems when you are unable to pay” the most common.

This category includes issues related to loan modifications, collections, and foreclosure, all prevalent since the mortgage crisis got underway about five years ago.

As you can see from the pie graph above, these types of complaints accounted for nearly two-thirds of all mortgage-related issues, followed by “making payments.”

The “making payments” category covers loan servicing, mortgage payments, and escrow accounts.

This category also relates to modifications, as consumers expressed confusion regarding trial period payments and whether that would guarantee placement into a permanent loan modification.

So if we consider a normal real estate market, about 80% of the complaints could potentially disappear.

Some of the normal market stuff includes “applying for the loan” and “signing the agreement.”

These two categories deal with the loan originator or mortgage broker involved in the transaction, along with any settlement cost disputes.

Just two percent of complaints involved the credit/underwriting decision, and three percent were for “other” issues.

Of all mortgage complaints received, about 56,800 (89%) were sent to companies for review and response – the remainder were referred to other regulatory agencies, still pending, or deemed incomplete.

And the companies involved have already responded to roughly 53,900 (95%) of them.

However, only 1,800 mortgage complaints resulted in “relief,” with the average amount of compensation a paltry $425.

So it’s unclear if making a complaint will result in a meaningful result, not that you should be discouraged from pursuing one.

Additionally, consumers have disputed about 10,500 (23%) of the company responses to their complaints.

Bank of America the Top Offender

Unsurprisingly, Bank of America received the most complaints, according to an analysis of the data from the LA Times.

The company services about 15% of all residential home loans in the U.S., but wound up with 30% of the complaints.

Most of the complaints were related to loan modifications, collections, and foreclosure, likely thanks to its acquisition of Countrywide Mortgage.

Wells Fargo, which handles roughly 30% of the U.S. mortgage market, only received 15.9% of complaints.

And Chase, which has 12.7% market share, received 10% of all mortgage complaints.

Citibank and US Bank rounded out the top five, though at much lower levels than the top three.

How to Make a Mortgage Complaint

If you wish to make a mortgage complaint, heading over to the website is probably the easiest and quickest way. Per the CFPB, the most common route for making a complaint was the website.

Roughly half (48%) of all complaints were submitted through the CFPB website, while 32% were referrals from other regulators and agencies, and nine percent were submitted via telephone.

There are five simple steps:

1. Tell them what happened 2. Tell them your desired resolution 3. Fill out your information 4. Fill out information about the loan/lender 5. Review and submit

You are also able to upload documents related to your complaint, and indicate the type of loan, such as conventional mortgage, FHA loan, reverse mortgage, HELOC, etc.

And if you believe the issue involves discrimination, you can also include that in the complaint.

From there you’ll be able to track the status of your complaint and receive e-mail updates from the CFPB.

They’ll let you know when the offending company responds, and you’ll have a chance to respond to that as well.

The complaints you submit will be shared with state and federal law enforcement agencies in order to improve consumer finance laws, write better rules and regulations, and combat business practices that pose risks to consumers.

So even if you don’t get anything out of it directly, you can help your fellow consumers by speaking up.

The Federal Trade Commission recently revealed the most reported text message scam: bank impersonations.

Reports of bank impersonations by text in 2022 jumped to 20 times the number reported in 2019. According to the FTC, consumers reported a loss of more than $330 million to text message scams in 2022. And cash that’s lost because of bank fraud or scams isn’t covered by the Federal Deposit Insurance Corp. or National Credit Union Administration.

Banks are a safe place to keep your money, but there are still a few basic but important precautions you can take to ensure you don’t fall for a bank-impersonation text scam. Here’s how to protect your money from text message scams impersonating your financial institution.

Don’t make money moves under pressure

Text message scammers will try to make you feel like action is required immediately — at the risk of losing your money. It may come as an urgent message warning you to call or click on a link because of alleged suspicious activity.

“Any type of pressure tactic is not legitimate — that is not your bank,” says Paul Benda, senior vice president of operational risk and cybersecurity at the American Bankers Association. As with any decision about your finances, avoid taking actions when you feel scared, stressed out or pressured.

Don’t click on any links from an unsolicited message

If you receive a text message you’re not expecting, be wary — especially if it looks like it might be from your bank.

In a recent poll by security experts at Security.org, 66% of respondents said that they had received a suspicious text from someone they didn’t know, and about 20% clicked on links texted from strangers, which is never advisable. “Look at any type of unsolicited communication very cautiously,” says Benda.

Major banks were popular choices for scammers to impersonate in 2022. According to the FTC, the most common scam text messages often claimed to be from large banks, including Bank of America, Wells Fargo, Chase and Citibank.

Don’t call a phone number that’s texted to you

Just as you shouldn’t click on a link texted to you from someone you don’t know, don’t click on or dial a phone number you receive in a text. Instead, find the official phone number for your bank by going to its website or mobile app. Initiate contact with your financial institution at its official phone number to ensure you’re talking to a legitimate representative, and verify whether there actually is an issue.

“Making that phone call can be the difference between getting scammed versus not getting scammed,” says Tremaine Wills, a financial advisor and founder of Mind Over Money, a financial literacy company in Newport News, Virginia.

One particular kind of text scam resulted in a median loss of $3,000 in 2022, according to the FTC: a text from someone impersonating your bank, instructing you to reply with a “Yes” or “No” to confirm or deny a suspicious transaction. Once you replied, the scammer would call you under the guise of helping you. Their ultimate goal was to either fraudulently transfer money out of your account or obtain personal information such as a Social Security number.

What to do if you were unable to avoid a scam

If you should happen to fall for a text scammer impersonating your bank, there are a few critical steps to take.

First, alert your bank to the incident and get its help in making sure no more money leaves your account fraudulently. Next, report the scam to local law enforcement. Those first two actions are key for trying to recover any cash that was wrongfully taken from your account.

Finally, file a complaint with the FTC at ReportFraud.ftc.gov and/or report the instance to the Federal Bureau of Investigation’s Internet Crime Complaint Center. The FTC also recommends that you forward suspicious text messages to 7726, which helps wireless providers identify and intercept similar text messages. You can also report and block suspicious text messages within your messaging app.

Having a good idea of your account activity is a key part of protecting your money from scams.

“Have a regular practice of knowing what’s going on with your account,” says Wills. If you’re not completely sure of what’s happening in your account, then you might be more likely to be alarmed by a text message claiming to be from your bank, she says.

This article was written by NerdWallet and was originally published by The Associated Press.

How did the United States become a nation of debtors? When did credit cards become popular? Did you know that many modern credit card policies are the creation of one man?

The Secret History of the Credit Card was a 2004 “Frontline” presentation from the Public Broadcasting System. The program examines the nation’s use of credit and, more specifically, the methods used by credit card companies to obtain enormous profits. The Secret History of the Credit Card won the 2004-2005 Emmy Award for Outstanding Investigative Journalism.

PBS has made the entire program freely available online in RealMedia and Windows Media formats. The broadcast is divided into five segments of roughly twelve-minutes each for easier download.

When this program was produced, 145 million Americans carried credit cards. Of these:

55 million paid in full every month

90 million carried balances

35 million paid the minimum required

Of those who carried credit card debt, the average amount owed was $8,000. “It’s nice to be able to spend what you don’t have,” says man. But the show’s panel of citizens didn’t really understand how credit cards work. They were ignorant of their credit scores, for example.

The Secret History of the Credit Card provides a brief overview of credit reporting agencies and of the credit scores developed by FairIsaac. The median FICO score is 720 out of 850. Risky customers have scores below 600. Three-quarters of American adults have a credit score. A FICO score often determines how much interest a person will pay — terms usually spelled out in the small-print of the contract. (For more on this subject, see my previous explanation of how credit scores work.)

Credit cards are a relatively recent invention. Until the 1980s, they didn’t play a prominent role in American life.

In the early eighties, inflation began to outstrip interest rates, making credit cards a losing proposition for the banks that issued them. (Interest rates were limited by anti-usury laws.) Facing a bleak future, Citibank of New York began searching for options. They found South Dakota, which had recently discarded its anti-usury law, opening the way to unlimited interest rates. Citibank moved its offices to Sioux Falls and, under an obscure Supreme Court decision, was able to export its new higher interest rates to New York and to the entire country. Other credit card companies soon set up shop in South Dakota. And other states — including Delaware — repealed their anti-usury laws in an attempt to lure white collar banking jobs and the associated taxes.

Many current credit card practices can be traced to one man: Andrew Kahr, a sort of credit card whiz kid. Before him, credit cards required customers to pay 5% of their balance every month. Kahr convinced banks to lower minimum payments while raising credit lines, which caused profits to soar. (People charged more and strung it out over longer periods of time.) “High balances are more profitable than small balances,” says Kahr.

From what I’ve seen and read, I believe Kahr is truly an evil man, single-handedly responsible for a lot of the credit trouble Americans face.

The Secret History of the Credit Card describes how Providian, which grew from Kahr’s First Deposit Corp, would receive a check, deposit it, but not credit it to the consumer’s account for several days (or weeks). The consumer would then suffer escalating penalties and fees.

No wonder the credit card industry generates more consumer complaints than any other.

Credit card companies can change their terms at will. There is nothing to prevent issuers from changing their terms. Interest rates are not regulated. Fees are not regulated. Due dates on Sundays and holidays are intentional, and designed to generate late fees.

It is unsurprising that the credit card industry is the most profitable sector of banking.

The Secret History of the Credit Card is a fascinating program, though it’s not really a history — it’s a profile of the credit card industry and its current state. I wish that it were available for download, though. Like a lot of streaming videos, these are flaky. When I paused to answer the phone near the end of one segment, Firefox lost my place and I had to watch most of it over again.

A complete transcript of the program is available. Check out the Secret History of the Credit Card web site for even more information.

If you’re on the lookout for a full service online bank, you might come across CIT Bank. Founded in 2009, CIT Bank is now a division of First-Citizens Bank & Trust Company, which is a leading financial institution with more than $218 billion in assets.

The bank offers a variety of products, including savings and checking accounts, CDs, custodial accounts, and home loans. It stands out for its competitive interest rates that you may not find at traditional banks as well as no monthly maintenance fees or monthly service fees.

While there are no physical branches, live chat support on CIT’s website and mobile app as well as automated phone assistance is available 24/7. If you prefer to speak to a CIT representative directly, you can reach them during regular business hours: Monday through Friday, 9 a.m. to 9 p.m. ET, or Saturday from 10 a.m. to 6 p.m. ET.

CIT Bank doesn’t have an ATM network but it will reimburse you up to $30 per month if you incur out-of-network ATM fees. Rest assured that it’s insured by the Federal Deposit Insurance Corporation (FDIC) for up to $250,000 for an individual account or $500,000 for joint accounts, meaning your money will be safe, no matter what happens to the bank. Let’s take a closer look at CIT Bank so you can decide whether it makes sense for your unique situation.

CIT Bank Pros and Cons

Before you move forward and open an account with CIT Bank, it’s a good idea to consider the benefits and drawbacks.

Pros

Competitive rates: Since CIT Bank has less overhead costs than brick and mortar financial institutions, its yields on deposit accounts and several CIT Bank CDs are competitive. It can allow you to make the most out of your hard earned money.

No fees: Unlike other bank accounts, CIT deposit accounts do not have any monthly maintenance fees, or other common fees. You can use the money you save on fees to meet your financial goals faster.

ATM fee reimbursement: CIT Bank reimburses you up to $30 per month for out-of-network ATM fees. This means you can withdraw cash from any ATM without worrying about high costs.

Small minimum deposit requirements: You don’t need a lot of cash to open up CIT Bank accounts. Many. of the accounts only require $100 to start.

24/7 customer service: CIT’s live chat and automated phone support is available round-the-clock. If you have a question or concern, you’ll be able to receive assistance right away.

Cons

No physical branch locations: CIT is an online only bank, meaning there are no branches for an in-person banking experience. If you decide to bank with CIT, you should feel comfortable with online banking and mobile banking.

Limited product selection: Compared to other financial institutions, CIT’s product line is slim as there are no credit cards, car loans, or IRAs. Fortunately, its lineup of checking accounts, savings accounts, custodial accounts, CDs, and mortgages is still impressive.

Low rates on select CD accounts: Some CDs have lower rates than you may be able to find elsewhere. The good news is you can calculate your returns in advance and won’t have to worry about fluctuations in the market.

No checkbooks: CIT’s eChecking accounts do not include checkbooks. However, you can use CIT to pay other individuals and businesses electronically via Zelle, Apple Pay, and Samsung Pay.

CIT Bank Products

CIT Bank offers a variety of products to help you meet different financial goals. Here’s an overview of each of its current offerings.

Checking Accounts

You can open the CIT Bank eChecking account with as little as $100. It’s unique in that it offers interest on your balance. To earn as much interest as possible, you’ll need to keep at least $25,000 in your account.

As an online checking account holder, you’ll get a debit card with chip technology and 24/7 account access. Plus, you’ll be able to deposit checks and make unlimited withdrawals with the CIT Bank mobile app. In addition, you’ll have access to Zelle, Apple Pay, and Samsung Pay. Unfortunately, the eChecking account doesn’t come with paper checks.

Savings Accounts

CIT Bank offers a few CIT Bank savings accounts you might want to explore., including the CIT Bank Savings Connect, the Savings Builder account, and Platinum Savings account. The CIT Bank Platinum Savings account provides an interest rate of up to 12 times the national average.

There are no fees and interest compounds daily so that you can earn as much as possible. All you need is $100 to open this account. This account is ideal if you’d like to meet your savings goals quickly without a lot of effort.

With the CIT Savings Connect account, you can reap the benefits of a great interest rate and enjoy easy access to your funds. Several noteworthy perks of the Savings Connect include an interest rate of up to 11 times the national average, online banking and mobile banking, remote check deposit, and no monthly service fees.

The CIT Savings Builder is a two-tiered CIT savings account with an interest rate that’s twice the national average. As long as you make at least one $100 deposit per month or maintain a balance of $25,000 or more, you can earn a competitive rate on it. Since the Saving Builder account earns daily compounding interest, you’ll be able to maximize your earning potential. Just like the other CIT saving accounts, the Savings Builder doesn’t have any account opening or maintenance fees.

CIT Money Market Account

The CIT Bank money market account is the way to go if your ultimate goal is to grow your savings and stash your emergency fund. With a minimum opening deposit of $100, you can earn more than two times the national average.

In addition, there is no monthly service fee and you can deposit checks and transfer money using the CIT Bank mobile app. In addition, you’ll be able to earn twice the national average. Just like with the other accounts, you may only make six transactions per statement cycle and can deposit checks and make transfers with the CIT mobile banking app.

CDs

Certificates of Deposit (CDs) might be worth exploring if you like the idea of guaranteed returns. CIT offers several types of CDs, including:

Term CDs: Term CDs are traditional CDs that are widely seen at other banks and range from six months to 60 months. With a term CD, you can lock in an interest rate for a certain time period, regardless of what happens to the market. The longer term you choose, the more interest you’ll earn. You’ll need at least $1,000 to open a term CD.

No-Penalty CDs: Most CDs require you to lock up your money for a set period of time. If you’d like to access it before, you’ll have to pay a penalty. A no-penalty CD is exactly what it sounds like: a CD that doesn’t charge a penalty if you withdraw funds before your term is up. It requires a $1,000 minimum opening deposit and you may be able to access your money after seven days.

Jumbo CDs: If you have a lot of cash saved up, a jumbo CD might make sense. It requires $100,000 to open and doesn’t come with any account opening or monthly maintenance fees. Its terms range from two to five years and the longer you keep your money in one, the higher rate you can lock in.

RampUp CDs: RampUp CDs are for current CIT Bank customers with CDs. With a RampUp CD, you can increase your rate one time during your term if CIT Bank raises rates after you have already opened your account. You’ll need to reach out to CIT Bank directly to learn more about what type of rate you might qualify for.

Custodial Accounts

Custodial accounts are opened under the Uniform Transfers to Minors Act (UTMA). If you have a child under 18, a CIT custodial account can help you save money for their future. You’ll serve as the custodian and have complete control of the account until your child turns 18 or a later age that you designate.

You can contribute as much money as you’d like and may not have to pay federal taxes on part of the earnings. With a custodial account, your child may enjoy money for college, a vehicle, home down payment, and other expenses that can steer them toward a bright future.

Home Loans

CIT Loans does offer mortgages but you have to submit your contact information on its website to start the process and learn more about your options. You’ll need to state the value of the home you’re interested in, your desired loan amount, your zip code, and your credit score range. If you already bank with CIT, you may be eligible for two relationship discounts that lead to a lower rate.

Ten percent of your balance in a CIT bank account may give you 0.1% off your rate. If you keep 25% of your balance in a qualifying cit bank savings account, you might lock in a 0.2% discount. Since the CIT website has limited information about its mortgages online, it’s a good idea to fill out the form and request further details.

CIT Bank Fees

As we mentioned above, CIT Bank doesn’t charge any opening fees or monthly maintenance fees. Also, you can open most accounts with only $100. The bank won’t charge any domestic ATM fees and will reimburse you up to $30 per month for any fees you incur for using other ATMs. If you use an international ATM, however, CIT Bank will charge a monthly fee of 1% plus the fee imposed by the ATM provider. Other fees you should be aware of include:

Debit card replacement fee: 100

Overdraft fee: $30

Returned deposit fee: $10

Bill stop payment fee: $30

Outgoing wire transfer fee: $10

CIT Mobile App

With the CIT mobile banking app, you can bank on the go from just about anywhere. The mobile app is versatile so you can use it to log into our accounts via a password or fingerprint. You can also transfer funds between CIT accounts and an external bank account and take a photo to deposit checks.

Plus, the app allows you to check your balances and transaction history, send and receive money via Zelle, and make secure payments with Samsung Pay and Apple Pay. If you’d like, you can sign up for text banking, which will give you the chance to check your account balances and transactions through text. Many reviewers state that the CIT mobile app is very intuitive so you shouldn’t have any trouble using it, even if you don’t consider yourself tech savvy.

CIT Bank Reputation

Before you go ahead and open a CIT Bank account, you might want to know about its reputation. It has an A- rating on the Better Business Bureau (BBB). On TrustPilot, CIT earned 2.3 out of 5 stars due to negative customer reviews.

Most of the negative reviews have to do with poor customer service and difficulty opening deposit accounts. The majority of the five-star reviews praise CIT for a convenient banking experience and fast response times from the customer service team. You can always try out CIT Bank and move on to another financial institution if you’re unsatisfied for any reason.

How to Access Your Money

Even though there are no physical branches, CIT Bank makes it easy to fund your account and withdraw money.

Deposits

You can fund your account through these methods.

Mobile app: With the mobile app, you can deposit checks and make transfers quickly and conveniently.

ACH transfer: The simplest way to fund your account is to transfer funds electronically from your external bank accounts. Note that it may take up to two business days for the money to show up.

Check: You can mail a physical check to CIT Bank.

Wire transfer: CIT Bank accepts funds via wire transfer.

Withdrawals

Here’s how you can make withdrawals:

CIT Savings Connect: The CIT Savings Connect allows you to make up to six withdrawals or transfers per statement cycle. Keep in mind that any withdrawal and transfer requests you submit via mail don’t count toward this limit. The same goes for telephone requested withdrawals and transfers.

ACH transfer: Free ACH transfers between your account and an external bank account are available.

Check: You can call CIT and ask them to mail you a check without paying a fee.

How to Get Started

To open an account with CIT Bank, visit their website and click the green “Open Account” button on the home page. You can complete the application in 5 minutes or less. Be prepared to provide the following information:

Your home address

Your phone number

Your email address

Your Social Security number

You’ll also need to fund your new account. You can transfer funds from an external checking or savings account, wire funds to your new account, or mail a check to the following address: CIT Bank, N.A. Attn: Deposit Services, P.O. Box 7056, Pasadena, CA 91109.

Lastly, CIT will make two test micro-deposit to your account. You’ll receive an email within three business days that asks you to verify them. The bank will process your transaction as soon as you do.

CIT Bank Alternatives

While CIT Bank offers a lot of benefits, it’s not right for everyone. If you decide CIT isn’t the best choice for your unique needs and preferences, consider these alternative options. Some are online banks while others are traditional financial institutions with brick and mortar locations.

Ally Bank

Like CIT Bank, Ally Bank is an online only bank that offers low fees and high rates. Its product lineup includes checking accounts, savings accounts, CDs, credit cards, mortgages, car loans, personal loans, and retirement accounts. Perhaps the greatest benefit of Ally Bank is that it doesn’t charge any fees.

Capital One

Capital One has approximately 300 branches in select states and more than 50 Capital One Cafes that allow customers to open accounts, deposit cash and checks, and hang out. It also offers no-fee access to more than 70,000 ATMs and attractive rates on savings accounts and CDs. This bank might make sense if you want competitive rates but prefer the option of an in-person banking experience that is not available with CIT.

Chime

Chime isn’t a traditional bank or online bank like CIT. It’s a mobile banking app that provides banking services through Bancorp Bank, N.A. and Stride Bank. The Chime checking account comes with exciting perks like automated savings tools, early direct deposits and free access to over 60,000 fee free ATMs across the country. The Chime high yield savings account is also a solid choice thanks to its competitive interest rate and lack of monthly fees as well as minimum balance requirements.

Citibank

Citibank sounds like CIT Bank but is one of the largest banks in the world. It has hundreds of locations in the U.S. and thousands overseas. If you frequently travel abroad for business or pleasure and want access to branches and ATMs, it should be on your radar. It offers a plethora of accounts but they do come with fees. The good news is many of the fees can be waived if you meet certain balance or direct deposit requirements.

Discover Bank