Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

The average household credit card debt in America is $9,654, and the states with the largest amount of credit card debt are Alaska, Hawaii, and New Jersey.

Between the first quarters of 2022 and 2023, The Federal Reserve Bank of New York reported that the credit card debt in America rose by $145 billion. As of June 2023, we saw a 12-month inflation increase of 3%, the smallest year-over-year increase since March 2021.

By understanding American credit card debt statistics, you’ll better understand where you stand and what you can do to potentially lower your debt. Credit card debt increases your credit utilization ratio, which can hurt your credit and ultimately cost you more money in interest.

We surveyed over 1,100 Americans to learn more about credit card debt statistics in the United States. This data covers the average debt by state, average interest rates, and more. While many of the statistics from our other sources look at the situation as a whole, our data helps us see what’s happening on an individual level.

Despite the national average of Americans having over $9,000 in credit card debt per household, only 14% say they’re “very worried” about their debt.

67% of respondents said they have less than $2,000 in debt, which may indicate that only a concentrated number of people have high amounts of credit card debt.

20% of respondents don’t know how long they’ve been in debt.

The majority of respondents (56%) say their credit card debt is due to unexpected expenses.

74% of respondents said at least one collection agency has contacted them about a past due debt.

In this article, we’ll also provide tips on how to get out of debt and work toward better credit.

Table of contents:

Key Credit Card Debt Statistics

Many factors play into credit card debt, such as the average interest rates, which cards have the best offers, and the balance people carry on their card. These statistics will help you compare your own credit card balance to the national average and see if you’re getting a good deal with your current cards.

Here are the standout findings of various debt statistics:

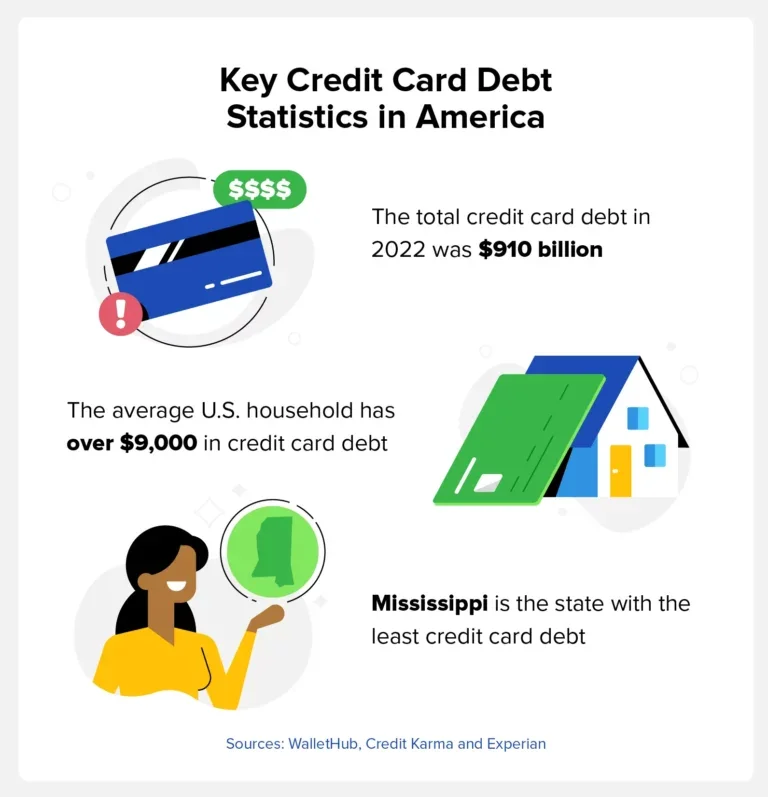

The average American household has over $9,000 in credit card debt. (WalletHub)

Mississippi has the least credit card debt at $5,259 per person. (Credit Karma)

Alaska has the most credit card debt on average at $8,139. (Credit Karma)

Credit cards 90 days or more past due rose to 4.57% in 2023. (FRBNY)

Individuals making $184,000 or more per year have the most credit card debt at an average of $12,600. (Federal Reserve)

The total credit card debt in America as of Q3 2022 was $910 billion. (Experian®)

How Many Credit Cards Carry a Balance

The American Bankers Association releases a quarterly report for consumer credit conditions, and the most recent data comes from the third quarter of 2022.

In America, approximately 43% of credit cards carried a balance, 23% were dormant, and 34% were used but paid off each month. Those who pay off their credit card balance are able to keep a low credit utilization ratio and prevent the accumulation of debt.

Tip: Use our credit card payoff calculator to estimate when you’ll be debt free.

Average Interest Rates for New Credit Card Offers

LendingTree analyzed the terms and conditions of 200 credit cards from upwards of 50 different credit card companies, banks, and credit unions. With this data, they were able to gather an assortment of information involving annual percentage rates (APR).

The APR is the amount of interest consumers pay for their purchases, and the following table is broken down by credit card type.

The following table is based on data from July 2023.

Average Credit Card Debt by State

In February 2023, Credit Karma gathered data from 74 million of their members to see which states had the most and least amount of credit card debt. Below, we’ve compiled a complete list based on Credit Karma’s data that contains the average credit card debt for each of the 50 states alphabetically.

Top 10 States With the Most Credit Card Debt

The following states had the most credit card debt, with Alaska having the highest average credit card debt in America at $8,139 per person.

State

Average credit card debt

1.

Alaska

$8,139

2.

Hawaii

$7,444

3.

New Jersey

$7,306

4.

Maryland

$7,248

5.

Virginia

$7,174

6.

Connecticut

$7,032

7.

New York

$7,029

8.

California

$6,952

9.

Washington

$6,869

10.

Florida

$6,783

Top 10 States With the Least Credit Card Debt

The major credit bureau, Experian, tracks credit card debt data as well and found that between 2021 and 2022, overall credit card debt in the U.S. increased from $785 billion to $910 billion—a 16% increase. The average debt also increased in many states, according to Credit Karma’s report.

State

Average credit card debt

1.

Mississippi

$5,259

2.

Kentucky

$5,455

3.

Wisconsin

$5,593

4.

Arkansas

$5,600

5.

Indiana

$5,601

6.

Alabama

$5,647

7.

West Virginia

$5,674

8.

Iowa

$5,732

9.

Idaho

$5,737

10.

Maine

$5,788

Average Credit Card Debt by Age

Credit Karma’s report with the state-by-state data also broke down credit card debt by age group. Currently, Generation X carries the most credit card debt, while Generation Z carries the least.

Age group

Average credit card debt

11-26 (Generation Z)

$2,781

27-42 (Millennials)

$5,898

41-58 (Generation X)

$8,266

59-77 (Baby Boomers)

$7,464

78-95 (Silent Generation)

$5,649

Average Credit Card Debt by Income

The following data comes from the Federal Reserve’s Survey of Consumer Finances (SCF) and was most recently updated in 2019. The Federal Reserve completed a new survey at the end of 2022 and will have updated data later in 2023.

As you’ll see, higher-income individuals have much more credit card debt than those who make less. This makes sense because high-income individuals are able to get much larger credit lines. But when you look at the debt-to-income ratio, lower-income households have much more consumer debt compared to the amount of money they make.

Percentile of Income

Average credit card debt

Less than 20%

$3,800

20%-39%

$4,700

40%-59%

$4,900

60%-79%

$7,000

80%-89%

$9,800

90%-100%

$12,600

Average Household Credit Card Debt

A recent study from WalletHub found that while total credit card debt in the United States rose 14.1% between 2022 and 2023, household credit card debt only rose by 8.39%.

Their data shows that the average household credit card debt at the end of the first quarter in 2023 was $9,654 adjusted for inflation, which is $738 higher than the same time the previous year. WalletHub’s chart goes back to 1986, and the highest household credit card debt was in 2007 when it was $12,221 on average per household.

Average Credit Card Debt by Race or Ethnicity

Research from Annuity.org shows that Black and Hispanic Americans are less likely to feel financially stable and less likely to have a bank account. This information can help us better understand what’s happening in the financial lives of different communities.

This data comes from the Federal Reserve’s 2019 SCF.

Race

Average credit card debt

White (non-Hispanic)

$6,940

Black or African American (non-Hispanic)

$3,940

Hispanic or Latino

$5,510

Other or multiple races

$6,320

Credit Card Delinquency Rates in America

When someone is at least 30 days past due on their credit card payment, their status becomes delinquent. The number of delinquencies in the United States can be a measure of people’s ability to pay down their credit card debt.

To track this data, Experian conducted a study between 2021 and 2022:

Accounts 30 to 59 days past due increased from 1.04% of total accounts to 1.67%.

The delinquency rate of accounts 60 to 89 days past due increased to 1.01%.

Accounts 90 to 180 days past due rose to 0.63%.

How to Get Out of Credit Card Debt and Improve Your Credit

Credit card debt in America is something many individuals struggle with, and when your debt isn’t under control, it can affect your credit. A lower credit score leads to higher interest rates, which means you’re paying more for your purchases. It can also lead to being denied new credit lines.

Here are some simple steps you can take to start getting out of debt sooner rather than later:

Reduce additional credit card spending: You don’t want to add to your current debt if you don’t have to.

Create a budget: Cutting your spending can help you save additional funds to pay down your debt.

Use the snowball method: Each month, pay off your smallest debt in full. This can help you build momentum as you chip away at your overall debt.

Try debt consolidation: Consolidating your debt may help reduce the interest rate and keep your debt in one place rather than with different creditors.

Get a balance transfer card: Balance transfer cards allow you to transfer credit card debt to a different account, which may have a lower interest rate and will also help you consolidate your debt.

If you need help getting your debt under control and improving your credit, Credit.com has resources to help you learn to better manage your finances. To begin managing your credit, sign up for a free credit report card and check out ExtraCredit®. Our services can help you learn how to work on your credit and educate you about managing your finances so you know how to work toward the life you want.

Methodology for Credit.com data: This survey was conducted for Credit.com using Suzy. The sample consisted of a total of 1,154 responses per question and is statistically representative of the general population. This survey was conducted in December 2022.

As president of the University of Pennsylvania, Amy Gutmann was one of the highest-paid administrators in the nation, receiving in her final year a nearly $23 million payout, largely made up of deferred compensation accrued over her 18-year tenure.

But that’s not all.

» READ MORE: Former Penn president Amy Gutmann earned nearly $23 million in 2021, but most of it was accrued over her 18 years as president

The university’s trustee compensation committee in late 2020 quietly authorized a $3.7 million, 0.38% interest home loan to Gutmann, according to tax records and financial disclosure forms. The loan was to help with her “presidential transition,” said Scott Bok, chairman of Penn’s board of trustees.

Advertisement

Specifically, Gutmann, 73, had lived in the president’s house on campus during her tenure, and she wanted to purchase a home to stay in Philadelphia. She left the presidency in February 2022 to serve as U.S. ambassador to Germany.

“While I won’t be living there while I’m ambassador, we have a place to come back to,” Gutmann said in a 2022 Inquirer interview, noting that she is on unpaid leave from the faculty. “Philly is our home.”

» READ MORE: Confirmed as the next U.S. ambassador to Germany, Amy Gutmann reflects on nearly 18 years as Penn’s president

Penn would not confirm what she purchased with her home loan, but deed records show that in December 2020 — 14 months before Gutmann left the university and two months after the loan was approved — her husband, Michael W. Doyle, a Columbia University professor, closed on a $3.6 million, four-story townhouse in a luxury housing development in the Fitler Square neighborhood. The purchaser’s mailing address on the deed lists “1 College Hall,” which houses administrative offices for the university.

While loans like this are neither illegal nor uncommon, some academics question whether they are financially sound and politically palatable for higher education institutions given the nation’s $1.77 trillion in student loan debt. Faculty and graduate students are striking across the country for better wages and benefits.

At Penn, tuition and room and board will top $84,000 in 2023-24, as the university raised costs 4% this year.

“This is the kind of thing that really undermines the public trust in higher education, particularly the public trust of these elite institutions that have a lot of money,” said Joni E. Finney, retired director of the Institute for Research on Higher Education at Penn. “Amy Gutmann made enough income to purchase that home without Penn’s help.”

Bok did not disclose the terms of the loan, but said it was “consistent with university policy and applicable laws and regulations.”

Gutmann did not respond to requests for comment.

Gutmann’s loans were among Penn’s largest

This home loan arrangement was not unique to Gutmann, nor to Penn.

The university, like some other elite colleges, for decades has provided generous loans to senior leaders, including deans, provosts and presidents. The loans were often for employee recruitment or retention purposes, helping the university attract the best leaders and enabling them to purchase property in Philadelphia’s expensive real estate market, Bok said.

The loans are legal. The U.S. Office of Government Ethics cleared Gutmann to serve as ambassador after she disclosed the loan.

Among Penn’s loan recipients, its largest has been to Gutmann, who also received two other loans from Penn earlier in her tenure, one marked “employee loan” for $700,000 in 2011 and another marked “retention/recruitment” for $1.25 million in 2014. Both were forgiven by the university over a number of years, Bok said.

However, the latest loan is not a form of compensation and is fully expected to be repaid, according to its terms, he said.

It appears she has not begun to pay back the loan. And the amount Gutmann owes to the university had slightly increased in the year since the loan was first extended, the most recent financial tax return shows.

In federal disclosure documents for the ambassador job, she said she will “refinance the loan with a different lender, pay market rate to the university for the remaining period of my government service, or pay off the loan” if the university extends her leave past the initial two years.

A necessary practice, or money misspent?

James Finkelstein, professor emeritus of public policy at George Mason University, who has been studying university president contracts and compensation since the 1990s, said Penn could have invested that money at a higher rate and made more income for the school. He noted that the interest rate she received was the second-lowest of its kind nationwide in more than a decade, and by comparison, the jumbo 30-year fixed rate for mortgages was 3.033% in October 2020 when she got the loan. Today’s rate is even higher, about 7.3%.

Giving the minimum interest rate set by the Internal Revenue Service at 0.38%, the loan would not be subject to taxation, he explained. It assumes that the money will be paid back in three to nine years, he said.

“Why does a university whose mission is educational need to loan this money?” Finkelstein asked. “These presidents are among the most highly paid university presidents in the country. Beyond their base pay, they receive bonuses and deferred compensation. Why is it at the end of their term, the trustees feel the need to reward them further by giving them these loans as they step down?”

Finney said faculty should be outraged.

“Especially as she was walking out the door, what kind of retention are they trying to achieve there?” she asked.

(A university tax record initially coded the $3.7 million as a “retention” loan, but in a later filing, after she was nominated to serve as ambassador, it was reclassified as a “special employee loan.”)

Others defended the arrangement, saying the job of presidents is extremely challenging, with their every move scrutinized and a responsibility for everything that happens at the institution virtually 24 hours a day.

“We’re asking these people to make a very unique kind of commitment,” said Brandon Cotton, president of the Washington- and Florida-based Cotton Law, which represents presidents, provosts and chancellors. “It should be rewarded. In [Gutmann’s] case, they found this method. In my opinion, it was a good method.”

Cotton said he has negotiated for presidents a number of loan agreements, which are often forgivable, and that happens when the leaders deliver outstanding performance.

Gutmann, by all measures, was credited with doing her job exceedingly well, giving Penn nearly two decades of sound and largely smooth leadership. She ran Philadelphia’s largest private employer, a $13.5 billion operation, with its 12 schools, six hospitals, and more than 23,000 full-time undergraduate and graduate students. As Penn’s longest-serving president, she raised more than $10 billion, oversaw construction of many new buildings, and led the school through a recession and pandemic.

» READ MORE: Amy Gutmann: Penn’s long-serving president seeks to bridge the divide | Industry Icons

Penn’s endowment more than quintupled from $4.1 billion, when she left her post as provost of Princeton and joined Penn in 2004, to $20.5 billion in 2022. Under her leadership, Penn prioritized student aid, adopting an all-grants, no-loan financial policy early on in her presidency. And by the time she left, 80% of Penn undergraduates were leaving Penn debt free, she had said.

Still, some say her compensation was simply too much. After news broke of Gutmann’s nearly $23 million payout in her final year, Jonathan Zimmerman, a Penn education professor, wrote a blistering column, asking where the outrage was over this arrangement. Gutmann’s total figure for 2021, reported on the 990 tax form, included her annual compensation of a base salary of $1.56 million and a bonus of $1 million and the $20.2 million deferred compensation and supplemental retirement funds, which also includes investment gains the money made over 17 years.

It did not include the loan.

“I have enormous respect for Amy Gutmann,” Zimmerman said. “I think she was a very successful president. I think presidents have incredibly hard jobs, for which they should be well compensated. But there’s well compensated and then there’s obscene. And we as a culture in higher education and beyond have lost sight of that distinction.”

Finkelstein said: “It’s about the fiduciary responsibility of the university trustees and their judgment.”

A common practice among elite universities

A review of financial tax documents for nearby universities found about two dozen similar home loans extended to staff at Swarthmore, Haverford and Princeton. Others across the United States, from Stanford to Columbia University, have also made similar loans, in some cases to presidents who were leaving.

Columbia gave its recently departed president, Lee Bollinger, a $6 million home loan, tax records show. The former president of the University of Southern California, C.L. Max Nikias, also got one for $3 million.

At some schools, these deals have drawn controversy. New York University notably extended low-interest loans to a former president and top professors to purchase pricey summer homes, drawing scrutiny in a 2013 New York Times investigation.

The loans aren’t always for homes. Drexel University gave its president, John A. Fry, who has been in the role since 2010, a $720,000 loan for an insurance policy, according to the university’s most recent tax filing. Drexel said the policy was purchased on behalf of Fry as part of his overall compensation package.

Over the years, Penn has given its loans varying labels, including “retention,” “recruitment,” “employee loan,” “mortgage assistance” and “special employee” loan. The loans are routinely for primary residences, not vacation homes, the university said. They are to help the employees secure residences near the school.

Penn’s most recent 990 form showed that it also currently has loans extended to Pam Grossman, who recently stepped down as dean of the Graduate School of Education, and Antonia M. Villarruel, dean of the nursing school. Each was for $150,000.

Gutmann’s 5,100-square-foot house, according to a real estate listing from before this sale, was described as a “new world of luxury,” featuring an entrance off a private courtyard, custom doors and millwork, a built-in two-car garage, an elevator, and a fitness center.

Several years were left on the property’s city tax abatement, which reduces the couple’s annual tax bill on the residence to about $6,800. The home has since increased in value by about a half-million dollars, according to online real estate estimates.

This article originally appeared on The Avocado Toast Budget.

This post is sponsored by Credit.com.

Here at the ATB, we are all about budgeting in a way that works for you and finding realistic ways to feel more confident with your money.

Now that 2020 is (finally) over, here are ways that you can start to take hold of your finances and build confidence with your money in 2021.

Write down your short, medium and long term financial goals

I’m a big believer that you don’t need to stress over how to maximize the value of every dollar you come across.

Much of personal finance is behavioral and relies on us finding value in how we navigate our money!

Because of this, I found it incredibly helpful to sit down and brainstorm short, medium and long-term financial goals to decide what I wanted my money to do for me.

Write down your short, medium and long term financial goals

Here’s how I break it up:

Short-term goals – less than two years

Medium-term goals – 2 – 10 years

Long-term goals – 10+ years

Feel free to dream big!

We want to make realistic and attainable goals, but we also want to allow ourselves to dream about what we really want our lives to look like, and how our money plays a role in that.

Get to know your credit score

Wanna know a secret? I avoided my credit score for the longest time.

Turns out, once I finally faced my credit score, I became more empowered to understand how my credit score affects my finances and what I could do to change it.

While free resources can give you a ballpark estimate of your credit score, that score isn’t very useful and certainly isn’t what creditors see!

Knowing your true score, and seeing your credit reports from all three major credit bureaus, gives you security and control over how to navigate your credit score going forward.

While it can be daunting, credit plays an important role in our lives from renting, to car insurance, to mortgages, to career opportunities and more.

That’s why it’s important that you stay informed of what your credit actually looks like that’s why I signed up for ExtraCredit’s free trial!

Set up automatic savings

Automating your savings is LIFE CHANGING.

Setting up automatic savings is often referred to as “paying yourself first” because you are prioritizing saving money for Future You.

There are tons of different savings goals that you can put this money toward, but the important part right now is to set up automatic savings so you can set it and forget it.

Trust me—you miss that money a lot less if you never see it in your account in the first place.

If you have automatic deposits at work, it’s super easy to add a savings account and have a certain % or dollar amount go into that account every month without it EVER hitting your checking.

In my opinion, this is the best way to go. Out of sight, out of mind.

You’re way less likely to touch this money, and you’ll be shocked at how much it grows over time!

If this isn’t an option for you, you’re not out of luck. You can set up automatic savings transfers into your savings account from your checking account through your bank.

Find a budget that works for you

Here at the ATB, we are all about budgeting in a way that makes sense for you and your life.

Budgeting doesn’t have to be stressful and restrictive. It should actually be freeing and allow you to feel more confident and in control of your money!

There’s no one right way to budget, and there are TONS of different types of budgets depending on your income and financial goals.

Personally, I use a zero-based budget which allows me to track and decide where every single dollar I have is going.

If you have big savings goals, low income or high debt, I definitely recommend checking out a zero-based budget.

Learn how to increase your credit score

Your credit score has a bigger impact on your life than just determining your eligibility for loans.

Credit can impact your ability to rent, job opportunities, car insurance rates and more.

Once you know what your credit score is, it’s important to understand what makes up your credit score, and what steps you can take to increase it.

There are five factors that influence your credit score:

Payment History

Amounts Owed

Length of Credit History

New Credit

Credit Mix

Payment History makes up 35% of your credit score, so it is the most important factor.

ExtraCredit gives you the ability to report rent and utility payments, adding new tradelines to your credit profile. Adding payment history to your credit file.

And if you need help working to repair your credit, you can also use the Restore It feature to get an exclusive discount from a leading credit repair company. Remember: your best credit score is an accurate one.

Understanding how to increase your credit can take a lot of stress out of your finances and help you feel more in control of your credit future.

Make a debt payoff plan

I paid off $20k in CC debt in less than a year, and in order to do that, I needed a concrete plan of how I was going to tackle my debt.

Prior to that point, I had just been throwing a little bit here and there, hoping that my balance would eventually decrease.

Shockingly, that never happened.

Once I decided to use the debt avalanche to tackle my credit card debt, I was able to calculate how much extra money I could throw at my debt every month in order to make progress toward my debt free goal.

With this method, I paid the minimum payments on all of my debt except for the one with the highest interest.

With the highest interest debt, I put any extra money I had toward paying that down.

This gave my money more of a purpose than just throwing extra money here and there at my different debts.

It was also reassuring and motivating to see the loan amount decrease drastically as I threw the extra money I had towards it.

Here’s how this social worker has paid off $28,000 of student loan debt in 15 months.

Today, I have a great debt payoff progress story to share from Taylor. Taylor is a social worker who is working on paying off $277,000 of debt and retiring early. She shares tips on how she is cutting her expenses, the ways they’ve increased their income through various side hustles, house hacking advice, and how she qualified for an $88,000 student loan award.Enjoy!

Now, don’t let the title deceive you into thinking we are debt free; we most certainly are not.

As of this writing, we still have $251,195.39 of debt (all student loans).

This is our story about the debt payoff strategies we used in paying off $28,026.02 of debt and our goals for the future!

Who are we?

My name is Taylor, and I am a 29-year-old medical social worker who finished grad school in 2018. I am also a part-time social media coordinator and with both jobs combined, I make $96,000 (gross).

I live with my husband, Bret, who I have been with for 11 years and married for 3. He is a full-time student and has been in grad school since September 2020 (he has about 2 more years left). We love to travel, try new restaurants, hang out with our friends and family, and just have a good time.

I also have a blog at Social Work to Wealth.

Related articles:

How did we get here?

First, I need to give you some background before we get into the nitty gritty of our debt numbers and payoff strategies.

2012: We met when both of us were in college. I was 18 and Bret was 22. Soon after we met, Bret took a few years off from school while I finished my bachelor’s. I relied entirely on student loans, and don’t remember applying to any scholarships. When Bret returned to school to finish his bachelor’s, he did receive some scholarships and worked a summer job to pay forhousing but still needed to rely on student loans to pay the bulk of his tuition.

I will speak for myself when I say I didn’t take the time to calculate how much loan money I actually needed and blindly accepted the total amount. Looking back, maybe I would have needed it all or maybe not, but I wish I would have at least done the exercise.

We have always been open with talking about our debt and money in general, but I remember us both expressing the thought that we would probably always have our student loans. We would just live our life, pay our minimum payments, and that would be that. There was never any talk about debt payoff strategies, or any money management strategies, really.

We went through many life transitions. Living apart for two years while I went to grad school, him returning to school to finish his bachelor’s, various jobs, and a post-bach program.

2019: Bret was finishing up his post-bach program and got accepted into grad school. We were newly engaged and began planning and saving for our wedding scheduled for July 11th, 2020. Such exciting stuff!

March 2020: We got the news our wedding venue was closing for the foreseeable future due to the COVID-19 pandemic, and we decide to cancel our wedding. We switched gears and used the money we saved for a down payment on a new home. Then, we had a small intimate wedding featuring a hot-air balloon with 18 of our closest family members! We personally saved a ton and also had tremendous help from our family.

September 2020: I start a new job and Bret starts grad school. We are newlyweds and settling into our new home in a new city.

I wish I could talk more about 2020 because it was a HUGE year for us with buying a home, moving, getting married, Bret starting grad school and me starting a new job, but that’s a conversation for another day!

Our wedding

From frugal to spenders

When we were saving for our wedding, we were very frugal. Any extra money we had, we put toward our wedding savings (which again, ended up being used for the down payment on our house and a smaller wedding ceremony).

We went from frugal to swiping our cards left and right to prepare for our wedding and furnish our house. It was sooo nice to finally be able to spend the money we had been saving for so long! But this continued into 2020… and 2021…

We were mostly spending on eating out and experiences. We do like to buy “things” but we definitely value food and experiences a lot more. We even decided to put a trip to Hawaii on our credit card costing us around $5,000, along with other expenses, because why not? We deserved it!

We didn’t have much of a budget, our bills were getting paid, but the credit card bill kept increasing. Since I was the only one bringing in income, we took out some student loans to help with a portion of our living expenses. And the credit card bill continued to increase.

The “wake-up call”

The “wake-up call” is such a theme throughout many debt payoff stories. So, here’s mine.

I went to breakfast with two friends in December 2021, and one of them brought up high-yield savings accounts (HYSA). I had never heard of this type of account before and was shocked to learn that these savings accounts had a way better interest rate than a regular savings account.

How was I just hearing about this at 28 years old? My mind was blown!

I thought, what else don’t I know? So of course, that led me to deep dive into the world of personal finance. I consumed any book, video, blog, or podcast I could get my hands on. I read stories after stories of people paying off thousands of dollars’ worth of debt, leveraging credit card points for free travel, investing, and so much more!

It was so motivating. I was hooked! (And still am.)

Bret was open and willing for me to share with him what I was learning. We started realizing that for the last year and a half, we hadn’t been telling ourselves “No”. We had just been buying whatever we wanted, and we had the credit card bill and no savings to show for it.

We learned that we could pay off all our debt and it didn’t have to stay with us forever. We learned there was a way to use a credit card responsibly (we thought we were). We learned that we could even retire early. That one sounded real nice! We dreamed of having more time doing our hobbies, traveling and being with our friends and family. And if we ever had kids, we dreamed of being able to work part-time so we could be home more with them and available for school activities.

Knowing this, we started reining in our spending, trying to just be more “mindful”, but no major change was made.

We take on more debt

April 2022: People in our neighborhood were getting new fences. We started thinking, “Hey, we need a new fence, too…” In some areas it was broken, it hadn’t been stained so was rotting, and was 15 years old. We were also going to get an updated appraisal to see if we could get our primary mortgage insurance (PMI) removed after just two years of owning our home and thought a new fence might help.

A coworker told me she was using a home equity loan to buy a fence and to do some other home renovations. We investigated options and ended up opening a $20,000 home equity line of credit (HELOC) instead with about a 4% interest rate. We buy our fence which ends up being about ~10,000 and we were set on it…

The second “wake-up call”

When it was all said and done, we loved our fence. We still love our fence, it’s beautiful! (And it better be at that price!) We stained it and we believe it will last us for many years.

But we start talking again about our debt and how we probably didn’t need this fence right now. We know we didn’t need this fence right now. Our PMI was removed, and it could have maybe happened even without the fence. Who knows.

We began thinking we need to make some serious changes in the way we manage our money. We need to do more than just be “mindful” about our spending. We make a real plan. We plan to make an actual budget, stop taking on unnecessary debt, and take a break from using our credit cards for the foreseeable future.

May 2022: Beginning of our debt payoff journey

Since we were serious about our new money management changes, I documented how much debt we had so we could track our progress.

$277,721.41

Here was the breakdown:

$260,390.25 in student loans, Bret & I’s combined – various interest rates

$10,676.24 HELOC – 4% interest rate

$5,430.76 is from credit card spending – 4% interest rate*

$449 for furniture – 0% interest rate

$775.16 for Peloton bike – 0% interest rate

*We moved our credit card debt to our HELOC since our credit card was around a 25% interest rate.

July 2023: Current debt numbers

Our current debt balance is $251,195.39, * which are all student loans.

We have paid off a total of $28,026.02 of debt!

*Our current balance will increase to ~$255,000 once Bret gets his final student loan disbursement (more on that later).

I want to also mention that we do have our mortgage, but we aren’t trying to pay that down as quickly as possible for a few reasons: we have a 3% interest rate, we don’t plan on this being our forever home, and one day we might rent it out or sell it.

Actions that helped us pay off $28,026.02 of debt in 15 months

We found a budgeting method that worked for us

We realized we could live off my income alone and not take on anymore debt, but we would have to have a somewhat rigid budget.

Finding a budgeting method that worked for us took some time. I don’t know how many times over the years I have tried to track my expenses in a budget app or an excel sheet, only to find out it was too overwhelming and that I was still overspending!

I am a visual person and learned about the envelope budgeting method, so we decided to give that a try, but use a digital variation.

So, for our entire money management system we have 4 checking accounts and 2 savings accounts (short-term and emergency fund). Our checking accounts include bills, food and miscellaneous, and two personal spending accounts.

This may seem like a lot of accounts to some, but it has worked tremendously for us. I love having a separate account for each major category in our budget so I can easily see how much money we have left in a certain category without having to add every expense into an app or Excel spreadsheet. We are joint owners on all of these accounts.

We then use the zero-based budget method to determine how much goes into each account.

We do have multiple cards to manage, but the pros VERY MUCH outweigh the cons here.

And with our own spending accounts, we have a certain amount of money allotted to us each month, so we individually have some spending freedom. We don’t have to feel guilty and know this money is set aside specifically for our personal spending.

Cut expenses and increased our income

I know some people are tired of hearing about this recommendation, but it’s something that really did help us! We reined in our spending a bit but mostly we had to increase our income. At a certain point, there wasn’t much more to cut.

We didn’t have many streaming services, started to limit our eating out, we didn’t have car payments, and we meal planned and prepped. We did (and still do) aaalll the things. We had to increase our income somehow.

Ways we increased our income

My income increase

I continued with my second job as a social media manager and then started dog sitting.

I have been dog sitting for about 5 years and have primarily used the Rover platform to list myself as a dog sitter. I like this app because it’s easy to use and I can specify various services to offer (e.g., house sitting, boarding, drop in visits, day care, or dog walking).

It also allows me to mark which days I am available and then people reach out to me if I seem like a good fit and my availability matches with their needs! Setting up my profile took some time, but now that it’s done, everything else is fairly low maintenance.

I now just have to respond to inquiries in a timely manner and set up a meet and greet if it seems like a good fit.

I currently only offer house sitting and on Rover and I charge $65/night. Rover takes a cut, so I end up pocketing $52. I also have private clients who pay me directly, and I have gotten those by referrals from past Rover clients. I charge my private clients $40/night.

I recently increased my rates on Rover and have been slow to increase my price with my private clients because they’re loyal.

I don’t make a ton of money dog sitting, but I am able to make a couple hundred dollars a month. My schedule is very limited, but there are people with better availability who make significantly more than I do!

I love animals and we don’t have any due to our sporadic work schedules, so it’s a great way for me to spend time with pets and get paid, too!

Bret’s income increase

Last year, Bret decided to take a break from grad school and soon after, he was offered a summer job in Alaska.

When we first started dating, he used to spend almost every summer there working for a family who owned a set-netting fishery. His uncle had spent many summers in Alaska working for this family and one summer brought Bret to work with him. They would catch salmon and sell it to a buying station in their area.

He went up there for about 6 summers in a row, until he got too busy with school and couldn’t go anymore.

He hadn’t been to Alaska in over 5 years, but someone who worked for the buying station remembered Bret, called him, and asked if he’d be interested in working at the buying station! Since he was already on a break from school, he said yes and worked up there for 8 weeks.

We were able to put every paycheck he earned towards our debt because we could manage all our expenses on my income alone. It was also a great way for Bret to spend part of his summer and I was finally able to visit as I never gotten the chance in previous years.

House hacking

We also started house hacking! We had a spare bedroom and bathroom I would use for my office and occasionally, for guests. A friend of mine and her husband are really into the real estate space and gave us the idea to rent it out.

We weren’t comfortable with the idea of having a long-term roommate, and with both of us working in healthcare, we knew there was a need for short-term and furnished housing for travelling healthcare professionals.

For us, short-term meant renting for 1-6 months, but we were open to individuals staying longer if it worked well for everyone involved!

Some questions we had to address before renting:

Did we need a permit?

How much should we charge for the deposit, rent and pets?

What furniture and amenities are important for travelers?

Where should we list the room?

How to create a lease agreement?

In our county, we did not need a permit to rent out the room if we were renting for at least 30+ days at a time.

After researching rental prices in our area, I found rooms that were of similar caliber listed for $1,100 per month or more. We wanted to be competitive and so we initially settled on $900 per month and have steadily increased it. We have now landed on $995 per month which includes all utilities and internet.

We set the deposit at $995, with an additional $300 for a pet deposit, and no ongoing pet rent.

We wanted to upgrade the furniture in the room and IKEA was a great place for us to find affordable, durable, and aesthetically pleasing furniture. We made sure the room had a bed, large dresser, bedside table, and we kept my desk in there too.

I read it’s important for travelers to have their own TV available so they can unwind in their room. We were able to find a decently priced smart TV off Facebook Marketplace.

Furnished Finder is where we decided to list our room, which started out as a platform for traveling nurses to find furnished housing. It is now used heavily by many healthcare professionals, students, and professionals in other fields.

Travelers reach out to us through the Furnished Finder website and if the dates work out, we move forward with scheduling a video interview. It’s important for us to be able to talk to the person, even if it’s just over video, and we want them to see our faces and home in real time as well.

For the lease agreement, we used ez Landlord Forms, because they have leases for each state with specific information on what’s required to include.

We don’t ask for anything major from tenants. The most important things to us are that they are respectful of our space, don’t smoke in the house, and pay their rent on time. We also added a page at the end for tenants to add two emergency contacts in case we need to call someone on their behalf.

We have had 4 renters so far with the room being occupied for 13 out of the last 14 months. It has really helped us with our debt payoff goals and we have also met some awesome people through the process! We plan to continue renting it out for the foreseeable future.

Applied for in-state student loan help

My state offered a program called the Oregon Behavioral Health Loan Repayment Program where they help minorities in the behavioral health field, or those who serve them, pay back their student loans.

This program is funded by The Behavioral Health Workforce Initiative which has the goal of recruiting and retaining behavioral health providers who, “Are people of color, tribal members, or residents of rural areas of Oregon, and can provide culturally responsive care for diverse communities.”

To apply, I had to show I was employed and actively providing behavioral health services and give them detailed documentation about my student loans. I also had to answer two essay questions related to being a part of and/or working with communities who are underserved and how my training has equipped me with supporting these communities.

I applied last year and was a recipient of an award!

As a recipient, there is a two-year service commitment which means I have to continue providing some sort of behavioral health service during that time frame (which I planned to). Over the next two years, I will be getting ~$88,000 in quarterly disbursements to put towards my student loans. So far this year, I have received ~$11,000, and it’s been life changing to say the least!

Alongside this support, I am also pursuing Public Service Loan Forgiveness (PSLF) for additional student loan relief.

Managing our mental health while paying off debt

Since I am a social worker, I often think about how money and debt affect individuals’ mental health. It’s one of the reasons why I started my blog in the first place.

I realized managing money is a universal task and many of us don’t know what we are doing because talking about money is taboo. And when you have financial stress, it can really take a toll on your mental health. So, I wanted to share our journey in hopes of helping others.

Bret and I aren’t those individuals who want to avoid eating out and fun experiences until we are debt free. And, we are also privileged to not have to take those extreme measures either. It has been important for us to make this journey sustainable and not deprive ourselves of experiences while we are going through it.

Here’s how we are making our journey sustainable:

Still going out to eat

Budgeting for personal spending money, aka fun

Setting realistic debt payoff goals

Putting aside money for travel

Not comparing and thinking other people are better than us because they’re able to pay off their debt quicker

Tracking our debt payoff progress (we use Excel). With so much debt left to pay off, being able to see our progress is really motivating

Openly talking about our debt. Avoidance is a coping mechanism for many, for us, acknowledging and addressing it has been so freeing (but it wasn’t always this way).

Talking about our dreams and reminding ourselves why we want to do this in the first place

We know that if we eliminated going out to eat, budgeting for fun, or both, we could be paying off our debt much quicker. However, that sounds miserable to us. It’s worth it to still go out to dinner, travel, or buy plants (in my case) than to deprive ourselves of the joy these things bring.

We are making great progress and we know in time, we will be debt free.

Our debt payoff journey is not linear

A few months ago, we decided to take out $6,000 of student loans. Bret currently has a full tuition scholarship, so we are tremendously lucky in that regard, but he just learned about some conferences that would be really helpful to his professional growth. We have gotten $1,500 of this loan money already which is included in our current debt balance, but we haven’t received all of it yet.

We could have pinched and saved to avoid taking on any of this debt, but that would have caused me to work more than I currently am. Again, not in line with our current goal of making this journey sustainable!

We were very intentional about how much to take out. We estimated how much he would need for a few conferences and declined the rest. We even opened a separate savings account for the money to make sure it didn’t get accidentally spent on anything.

I’m SO proud of us for that!

The goal here is progress not perfection. So cliche, I know. But we are learning how to think critically about our money, spend thoughtfully, use our money as a tool to reach our goals, and enjoy our life along the way. And right now, that meant taking on a little more debt.

We are moving in the right direction, and we know when he starts working, that will really accelerate our debt payoff journey since we have proven to ourselves we can live on my income alone.

Our plan going forward

Bret is still in school which means his loans are on deferment, so we currently have his on the back burner.

With the loan payment assistance I am receiving, it’s allowing us to put any extra money we have each month towards our savings. Our priority right now is building up a good emergency fund of about $16,000 (~4 months’ worth of expenses).

This has been difficult because of inflation and just little emergencies that keep popping up, but we are slowly making progress.

I am also prioritizing investing in my employer retirement plan, but only up to the amount that gets me my employer match which is 6% of my income.

Bret will be graduating in 2025, so at that time, we will pivot to incorporating his loans into our budget. Our goal is to be debt free by 2028.

It will take a lot of discipline and persistence, but I think we can do it. I am manifesting it!

We want to continue to learn, implement, and grow. We want to keep having transparent discussions about money and building our money foundations. And I personally want to continue sharing our journey with hopes of inspiring, encouraging and educating others. Here’s to sharing the wealth.

Do you have debt? What are you doing to pay it off?

Taylor is a social worker and personal finance blogger at Social Work to Wealth where she shares tips, resources, and lessons learned on her family’s journey to paying off $277,000 of debt and retiring early. She hopes to inspire and empower social workers with financial education so they can have a better relationship with their money. When she’s not working or blogging, you can find her traveling, gardening, trying a new restaurant, or buying too many plants.

Inside: Looking for information on what a typical Christmas bonus in the US is? This guide will help you calculate how much you can expect and what to do with it.

Are you waiting eagerly for that year-end surprise called the Christmas bonus? Like Clark in National Lampoon’s Christmas Vacation?

Or maybe you’re an employer wondering about giving out festive bonuses?

This guide is a jingle bell away with everything you need to know about Christmas bonuses in the United States.

You’ll discover how these additional pays work, what the typical bonus amounts are, tax implications, the benefits of giving a bonus, and wisely spending your bonus. In other words, it decodes everything from the employer’s perspective, right to how it impacts an employee’s pocket and spending decisions.

So, buckle up – you’re about to become a little richer in knowledge. Stay tuned!

What is a typical Christmas bonus?

A Christmas bonus, often referred to as a “13-month-salary,” is a special gift you might receive from your employer at the end of the year.

It depends largely on your company’s resources and financial standing, meaning not everyone will get one.

However, if you’re lucky, you might expect a bonus ranging from 2% to 5% of that, discretionary to your employer.

Thus, the average Christmas bonus would be you could be looking at an additional payout of around $1144-2860, assuming an average income of $57,200.

Does everybody get a Christmas bonus?

Not all employees in the US typically receive a Christmas bonus.

The giving of bonuses varies between companies and roles within those companies.

Personally, I have only had one company that gave out Christmas bonuses. Most companies tend to give their annual year-end bonuses, which may be based on factors like performance or tenure, during the first quarter of the new year.

While a Christmas bonus would be nice as it often serves as an appreciation gesture for hard work throughout the year.

Understanding the concept of Christmas Bonus

A Christmas Bonus is essentially a little financial gift from your employer during the holiday season. Think of it as an extra dollop of icing on your annual salary cake.

It’s typically a percentage of your salary and serves to show appreciation for your hard work throughout the year.

For instance:

Let’s say you earn $80000 a year and your boss awards a Christmas bonus of 5% would then receive an extra $4000 just in time for the festivities.

Your company elects to give all employees a flat $1000 Christmas bonus regardless of seniority.

Note that a Christmas bonus isn’t legally required and varies greatly between businesses.

History of Christmas Bonuses

Woolworth’s birthed this tradition back in 1899, offering a cash bonus of $5 for each year of service with a limit of $25.

In Woolworth’s early years, they established a pattern of rewarding their employees with a generous Christmas bonus.

This practice was seen as an annual tradition and was appreciated by their staff, instilling a sense of loyalty within the workforce.

Over time, Christmas bonuses have evolved not just in amount but in form as well. Besides cash, you could also receive gifts or even lavish holiday parties.

Despite the more modern trend of diminishing Christmas bonuses, this part of Woolworth’s history highlights the positive potential of such incentives.

Factors influencing the amount of Christmas Bonus

Considering factors on the Christmas bonus is crucial because it ensures fair distribution, tailored to individual employees’ performance, length of service, or their specific needs.

We all know that bonuses adequately demonstrate appreciation and recognize the hard work of their employees, increasing their job satisfaction and driving productivity.

So, let’s look into whether or not a Christmas bonus is viable for you or your company.

1. Company policy on Christmas Bonus

A company’s policy about Christmas bonuses is typically laid out in the employee handbook and company policies.

Policies may stipulate that Christmas bonuses are issued under certain circumstances, like when the employee has met specified targets or when the company has performed exceptionally well during the year.

Also, the board of directors may elect to give out one-time Christmas bonuses.

However, if these bonuses are not incorporated into the employee’s employment contract, they are typically subject to the employer’s discretion. Employers must take extra caution to ensure that these bonuses are presented as discretionary and not part of a contractual agreement.

Remember, these factors may vary from one company to another. Always refer to your employer’s specific policies and handbooks for accurate information.

2. Amount of Salary

Your annual gross income might influence the amount of your Christmas bonus, as some employers factor in their employees’ base pay when determining bonus amounts.

However, not all organizations adopt this practice, with some opting for a fixed, equal distribution amongst all staff members regardless of their earnings.

Therefore, depending on your contractual agreement and your employer’s policies, your salary could influence your bonus, but this isn’t a universal rule.

3. Type of Bonus

The types of bonuses vary greatly as companies have the discretion to decide the nature of the bonus, with the decision often driven by the organization’s performance, the individual’s job role, and the overall economic conditions.

They can be incentive-based, linked to performance targets, holiday-exclusive like Christmas bonuses, or tagged to specific business milestones, leading to significant variability.

Here are different types of bonuses you should know about:

Discretionary bonuses: These are given at your employer’s will. They might consider factors like company performance or your personal performance reviews. However, there’s no guarantee you’ll receive one.

Non-discretionary bonuses: These are part of your employment contract. As long as you meet certain criteria, you’ll receive this bonus on top of your salary during the Christmas season.

Non-holiday bonuses: Given outside of the holiday season, these can be extra pay or an item like a company car.

Remember, your bonus type dictates how much you could get for Christmas. Be sure to check your contract!

4. Company Culture

Company culture significantly affects bonuses as it underpins how employees perceive their value and recognition within the organization.

If the culture fosters transparency, fairness, and goal-oriented behaviors, bonuses can effectively serve as an incentive and boost morale. Statistics show that employee loyalty increases when they feel appreciated, which can often be demonstrated through financial bonuses.

Moreover, a culture encouraging open communication assures employees of fair dealing when it comes to awarding bonuses.

Hence, bonuses, when tied to clear goals, become more than just monetary rewards, ensuring employees understand their role in the company’s success.

5. Recipients of the Bonus

In the US, Christmas bonuses are usually gifted to all employees, irrespective of their role or position.

Some of the roles that may receive a Christmas bonus include:

Full-time employees: Usually part of the main workforce, these individuals are often at the receiving end of holiday bonuses.

Part-time employees: Even though they may work fewer hours, many companies consider them for bonuses.

Temporary workers: Though their roles are for a limited time, they are generally excluded as part of the company’s bonus scheme.

Contracted employees: If their contract includes a clause for a holiday bonus, they are quite likely to receive a Christmas bonus. If it does not, they will not receive one.

Remember, the goal is inclusivity, a policy aimed at making every employee feel rewarded and appreciated during the festive season.

6. Holiday Season

Christmas bonuses are commonly offered by employers during the holiday season in the United States. This bonus is seen as a way to show appreciation and respect to employees, which can help to mitigate feelings of burnout.

Companies may elect to give bonuses at other times of the year to motivate their employees and boost their job performance. These bonuses can incentivize individuals to achieve specific company goals, with the promise of additional monetary compensation driving their hard work.

Aside from motivation, off-season bonuses also serve as a token of appreciation, illustrating a company’s recognition and value of their employees’ efforts.

It’s worth noting that a bonus doesn’t necessarily have to be monetary. Examples can also include extra vacation days or other perks.

7. Amount Given to Employees

A Christmas bonus is an extra payment given to employees during the holiday season as a gesture of gratitude for their commitment and hard work.

Factors influencing the Christmas bonus amount include:

Length of service: Employees who’ve been with the company longer might receive a higher bonus. For instance, an employee with a decade of service might receive $1,000 at a rate of $100 per annum.

Based on Salary: Many companies may opt to give a flat percentage related to the salary of their employees.

Flat Amount: Others may give the same amount to all employees across the company.

8. Company’s Financial Resources & Performance

A stronger performing company is more likely to give more bonuses as it typically correlates with higher profits, enabling them to be more generous with employee rewards.

On a company level, if overall performance benchmarks are hit, Christmas bonuses may increase across the board.

In fact, the incentive of bonuses can create a highly driven workforce that pushes towards achieving and even exceeding business goals. Furthermore, companies that distribute bonuses, particularly holiday bonuses, can significantly boost employee morale, fostering both loyalty and a positive company culture.

How to Calculate Your Potential Christmas Bonus

Calculating your Christmas bonus can often seem nebulous, leaving many uncertain about the amount they should expect.

The elusive nature of the Christmas bonus can largely be attributed to the fact that unlike salary, it isn’t typically fixed and may vary based on several factors such as an employee’s performance, the length of their service, or the financial health of the organization.

Despite this, there are a few pointers that can shed light on how to calculate this anticipated festive season reward.

Step 1: Check if you are Eligible for a Christmas bonus

Figuring out your potential Christmas bonus firstly entails a careful examination of the terms of your employment contract, alongside other supporting documentation such as your employee handbook or job offer letters.

These documents accurately establish the contractual relationship between you and your employer and often contain crucial clues about bonus calculations.

For instance, if your contract states that you are entitled to an equivalent of one week’s salary as a Christmas bonus, then you can confidently expect that amount.

Keep in mind the discretion of the employer in case of confusion. Some bonuses might not be contractual but discretionary. Consult your HR department for clarification if needed.

Step 2: Calculate your percentage of the total bonus amount

To calculate your bonus based on your salary, you need to know the exact percentage your employer uses, which usually ranges from 2-5% of your annual earnings.

Multiply your annual salary by the bonus percentage to determine your possible holiday bonus.

For instance, if you earn a yearly salary of $100,000 and your employer gives a 2% bonus, you’ll receive a $2,000 bonus.

Step 3: Is my Christmas Bonus Taxable?

So, if you’re anticipating a hefty holiday bonus, remember, it might be subject to taxes.

Bonuses are often considered supplemental income.

As such, the Internal Revenue Service (IRS) requires a 22% federal income tax on this income, which can reduce your bonus significantly.

State laws also have a part to play. Your holiday bonus is taxed according to your state tax rate, which is another cut from your bonus.

For example, your bonus amount is $5000 after federal taxes of $1100 and state 4% taxes of $200 are deducted, your take-home bonus is $3700.

How to Spend Your Holiday Bonus

The anticipation of receiving that extra lump sum has many employees daydreaming about that eye-catching new car, an extravagantly relaxing vacation, or perhaps the latest tech gadget.

Although it’s tempting to indulge in the pleasure of immediate gratification, there are more finance-savvy alternatives to consider for the effective utilization of your annual bonus.

1. Invest your Christmas Bonus

Getting that skip in your heartbeat when you receive your Christmas bonus is a feeling like no other.

However, the real magic happens when you decide to invest this bonus, making it grow over time instead of spending it all at once.

Here are the top four ways to invest your Christmas bonus:

Wealth Creation: When you invest your bonus, you’re setting yourself up for future wealth. Learn how to invest 10k.

Earn Additional Income: Use your bonus as a kick-start to a side hustle. Many Americans already secure supplemental income this way. In fact, many people are interested in how to make money online for beginners.

Professional Growth: Investing your bonus into professional development is another smart move. Enrolling in online courses that build your technical skills or lead to certifications can enhance your earning potential. Learn to invest 100 to make 1000 a day.

Financial Security: Finally, investing your bonus helps to secure your financial future. Whether it’s putting money into retirement funds or investing in a high-yield savings account, every bit helps set you up for stability and freedom. This sets you up to become financially independent.

Your Christmas bonus could be the first step towards a future of financial growth and security.

2. Consider your financial needs for the coming year

Before you rush to spend your holiday bonus, consider your financial needs for the coming year.

Start by:

Assessing your monthly expenses. How much do you need for essentials like housing, utilities, and food? Compare with the ideal household budget percentages.

Evaluating your emergency fund. Remember, experts recommend at least $1000 in an emergency fund. Plus having three to six months’ worth of expenses stored away in a rainy day fund.

Big expenses coming your way: Do you have any costly expenses like home repairs or car replacement in your future?

You may want to set aside money for those future needs, so you will be financially stable when they happen.

3. Pay Off Bills

Don’t run to the stores before analyzing your debt.

If you have high-interest loans or credit card debt, prioritize paying these down. Our expert tip at Money Bliss is to tackle the highest interest debt first.

Use your bonus to pay off debts: Since a bonus is usually an unexpected sum of money not factored into your annual budget or salary, you can make significant headway in paying off your debts, particularly those with high-interest rates.

Save on interest charges by reducing debt: The bonus can help reduce your debt balance, leading to less interest accruing over time. This move could save you hundreds, even thousands, over the long term.

Consider debt management apps: Apps like UndebtIt help you find a debt free date. Platforms like Tally† can simplify your debt payoff journey with automated payments using a lower-interest line of credit.

Reconsider splurging your holiday bonus: Rather than spending it all on that coveted item or trip, you might want to consider other financially beneficial options.

4. Buy Christmas Gifts

Utilizing your holiday bonus wisely to purchase Christmas gifts can be a smart and rewarding way to use your end-of-year windfall.

Instead of splurging on high-cost items, consider thinking through your holiday gift list and budgeting accordingly.

Bear in mind that enjoying the holiday season doesn’t have to break the bank; as Christmas on a budget is possible.

Don’t forget to spoil yourself with a gift every now and then. You’ve worked hard for this bonus and deserve a treat too.

5. Splurge on Fun Things

It’s absolutely okay to treat yourself with a holiday bonus – after all, you’ve earned it! Using it wisely can add a dash of fun and pure enjoyment to your life.

Now, what do I want for Christmas?

Here are a few fun ways to splurge your holiday bonus:

Dream vacation: The bonus could be your ticket to the vacation you’ve been fantasizing about. Plan carefully to make the most out of it.

Invest in hobby: Whether it’s photography, painting, or gardening, investing in a hobby can prove to be quite rewarding.

Spoil yourself: Get that TV you’ve been eyeing or make a down payment for that new car you fancy.

Remember, pleasure is a great aspect of well-being. So, it’s great to treat yourself once in a while. Just balance it with other financial responsibilities.

6. Invest in Long-Term Goals

Ditch the instant gratification of spending your holiday bonus all at once. Instead, consider investing it towards long-term goals for an even greater payoff.

Here are some easy steps to set you on the right path:

Identify your long-term financial goals. Be it a dream home, kids’ education, or retirement, a clear goal will help you stay motivated.

Assess your current financial situation to gauge how much of the bonus you can invest.

Choose the right investment vehicle. Stocks, bonds, or real estate can be profitable, depending on your risk appetite and time horizon.

Remember, spending wisely today makes for a secure tomorrow.

7. Give Back to the Community

Giving back to your community during the holiday season is a fantastic way to share your fortunes. Not only does it bring joy to those in need, it fosters appreciation, empathy, and understanding.

Here are some thoughtful ways to use your holiday bonus:

Donate to a Local Charity: Identify a local charity that resonates with your values. Every donation counts and your contribution could make a substantial impact.

Sponsor a Family’s Holiday: Many organizations connect sponsors with families in need. Your bonus could help provide them with essential groceries, clothes, toys, and a memorable holiday experience.

Contribute to a Fundraiser: Participate in your community or workplace fundraisers. Your financial support could contribute towards a noble cause, be it medical aid, education, or relief work.

Volunteer Your Time and Skills: Although not a direct use of your bonus, volunteering can be another way to give back. Maybe your bonus might allow you some additional free time to offer.

Remember, volunteering often reflects individual happiness and improves overall well-being.

Do You Expect the Average Christmas Bonus?

Remember, Christmas bonuses can be diversified: from additional checks or sums of money to extra vacation days or tangible gifts.

Everyone always wants a Christmas bonus! So now, you can determine if yours is above or below the average Christmas Bonus!

Based on research, less than a quarter of employers offer a performance-based holiday bonus, so if you’re fortunate enough to receive one, consider investing it to reap greater returns in the future.

The best decision depends on your unique financial situation, so use the above tips to make a smart choice with your bonus money.

Know someone else that needs this, too? Then, please share!!

Inside: Are you struggling to manage your money? Feeling overwhelmed with debt? If so, it’s time to take action and build better habits. This guide will teach you how to create a budget and start your savings. You need these financial tips for young adults.

The importance of sound financial advice for young adults cannot be overstated.

Often, a lacuna exists in our educational system where personal finance is concerned, leaving many young adults ill-equipped for the financial decisions that await them in their adult life.

Yet, you will encounter situations that require a sound understanding of budgeting, credit usage, investment, and an array of other financial tools without any formal education in these areas.

Financial advice can act as a compass, guiding you on a path to financial health and stability.

This early orientation can help you avoid the pitfalls of needless debt accumulation, poor money management, and inefficient financial choices like I made.

That is why it is of utmost importance to start imparting knowledge and financial habits to young adults as early as possible.

Why Financial Advice is Crucial for Young Adults

Money matters! Especially when you’re young and there’s a world of financial responsibilities unveiled before you.

Understanding financial basics early on is key to smart monetary decisions in the future. Here’s why you should consider this vital:

Knowledge Burst: Understanding finance terms, the implications, and their impacts arm you with knowledge for future decisions.

Saving for Later: Early investment in savings accounts or retirement funds can maximize your funds later in life.

Debts Control: Ensuring debts are paid off faster helps avoid excessive interest in the long run.

Investment: Stock or mutual fund investment can multiply your savings in the right condition.

Remember, your financial health requires deliberate action, start early!

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What is the best saving advice for young adults?

The best saving advice for young adults is to start early and save regularly.

This will help you build up a nest egg that you can use in the future.

Personally, this is my own regret as such it took me way too long to become financially sound.

Also, you want to be mindful of your spending and live within your means.

Best Financial Advice for Young Adults

When you’re in your 20s, the world feels like your oyster, ripe with opportunities and potential.

But among this plethora of choices, the most important decisions you make may very well relate to your finances.

While the excitement of earning and spending your hard-earned money can be exhilarating, it is crucial to remember that wise financial decisions made early on can set the stage for long-term financial success.

We have curated some of the best financial advice to help you make informed decisions and set the foundation for a secure financial future.

1. Create a Budget

Creating a budget can seem like a daunting task. However, once correctly accomplished, it can undeniably make your life a lot easier.

Below are some reasons to start budgeting from the start:

Money management: Knowing the ins and outs of your financial transactions helps manage your money efficiently. A budget gives you a clear snapshot of your income and expenses, allowing you to make strategic decisions about spending and saving. This level of control can be incredibly liberating and reassuring.

Financial discipline: Creating a budget encourages discipline when it comes to financial decisions. It can show you areas where you’re spending more than necessary, such as an underutilized gym membership, frequent dining out, or an unused streaming subscription. By addressing these expenses, you could easily save an additional $100 per month.

Alignment with goals: A budget can provide clarity and align your financial actions with your long-term goals. If you are side-tracked and lose sight of these ambitions, the budget serves as a potent reminder to guide you back to the right path.

Effective savings: A budget constitutes a robust tool that allows you to maximize your income and inculcate a savings habit. Essentially, it’s a roadmap that shows you, in real time, where you can minimize and direct those funds into savings. Those savings can then be invested toward achieving significant life goals more efficiently.

Stress reduction: Tracking income and expenditure can culminate in a stress-free financial life. For example, it helps manage unexpected emergencies or allows you to enjoy after-office drinks without any worries about overspending.

To simplify the job, various user-friendly budgeting apps are available.

These digital budgeting tools or apps offer handy features that can streamline tracking expenses and income. These tools can automatically categorize transactions, display visual charts of spending, and send alerts when you’re nearing the limit of a budget category.

Enjoy guilt-free spending and effortless saving with a friendly, flexible method for managing your finances.

Start Your Free Trial.

So, no more wondering where your money went.

With a budget in place, you get to tell your money exactly where to go, and this is an empowering shift from feeling out of control to feeling in control of your finances.

By making budgeting a consistent part of your financial routine, you adopt a proactive approach to your money, making your life easier, and your future brighter.

2. Manage Your Debt

As a young adult, managing your debt is incredibly crucial. Not only does it set the foundation for your financial future, but it also helps to keep your credit score healthy.

Here are some top-notch expert tips on how to effectively manage your debts:

Avoid credit cards whenever possible. Although credit card rewards may seem appealing, they can often lead to unwanted debts. Instead, try using cash, debit cards, or cash app cards.

Don’t finance purchases that depreciate in value over time. Rather than taking a loan for things like cars or other depreciable assets, save up and pay in full.

Minimize education-related costs. This can be achieved by going to in-state schools, considering trade school or community college, living off-campus, and exploring scholarships or work/study programs. Learn how to pay for college without loans.

Pay off your debts methodically. Consider strategies like the debt snowball or avalanche methods to strategically pay off your debts. Use a debt payoff app to find your debt free date.

Remember, being in debt can delay your financial goals.

So, learning to manage your debts early on in your life can have a significant impact on your future finances.

3. Invest Wisely

Investing wisely is a cornerstone of solid financial advice for young adults. It sets the foundation for a financially secure future.

Most people are terrified of the concept of investing and stay away from it, which is the worst decision possible.

Investing is about putting your money to work for you, expecting growth or income over time.

Consistently adding money to your investment portfolio can be more beneficial than staying away or trying to time the market.