Advertiser Disclosure: Credit.com has partnered with CardRatings for our coverage of credit card products. Credit.com and CardRatings may receive a commission from card issuers.

Editorial Disclosure: Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

Snapshot: This is an entry-level student credit card with great perks, especially for those who travel via Uber or order with Uber Eats regularly.

Basic Features

An ongoing APR between reg_apr,reg_apr_type

A annual_fees annual fee

Perfect for people with credit_score_needed credit

Additional Details

You can earn an unlimited 1.5% cash back on every purchase

If you spend $100 in qualifying purchases within the first 3 months of opening the account, you qualify for a free $50 cash bonus!

Only through 11/14/2024, you can get a free UberOne membership and up to 10% cash back on Uber and Uber Eats purchases

Pros

Cons

Unlimited 1.5% cash back with numerous ways to redeem

No introductory APR offer

10% cash back on Uber spending through November 2024

Potentially high APR

Coverage of your Uber One membership fees through November 2024

No annual fee

Ready to learn how to apply?

Full Review of Capital One Quicksilver Student Cash Rewards Credit Card

This card is a great choice for students who may not have any credit built up yet but are looking to get in on cash back rewards. Just a heads up: this card is exclusive to students. So if you’re enrolled in a university, a community college or another post-secondary education institution and want to work on building credit while earning some sweet cash back rewards, this card may be right for you. (This is especially true if you’re planning on Ubering around campus or getting delivery through Uber Eats.)

There are quite a few credit card options available in the student credit card market that offer rewards, good interest rates, and low fees for students with low to non-existent credit who are just starting out. There are a few reasons why we like the card_name (in general, Capital One has great card offers), and a few things to consider before applying. Let’s get into it.

What You’ll Like About This Card

Unlimited 1.5% Cash Back

You can earn 1.5% cash back on your everyday purchases with no limits. Other cash back rewards may offer higher, variable cash back rates on unique purchases, but the Capital One Quicksilver Student Cash Rewards Credit Card is simple, direct, uncomplicated. It also allows you the flexibility to redeem your rewards as cash back, gift cards, or statement credits.

10% Cash Back on Uber Eats

Now through November 2024, you can earn even more by using your card to pay for Uber orders. Spend $50 on Uber or Uber Eats every week for a year, for example, and you can end up with an $260 extra as long as you’re paying off your card every month.

Free Uber One Membership

Another way this card helps you save money is that it covers your Uber One membership through November 2024.

Sound good? Learn more about applying for a Capital One Quicksilver Student Cash Rewards Credit Card

The Drawbacks

No Introductory APR Offer

Cards that come with an introductory 0% APR make it possible to make larger purchases initially and pay them off over time without incurring interest. (If you’re a student, that 0% APR may come in handy when buying books or materials for school). However, this card doesn’t have an introductory 0% APR offer.

Potentially High APR

Depending on your approval status, the APR on your card might be relatively high. It’s not a big deal if you regularly pay off your balance, but you might want to shop around to see if you can get a better rate, especially if you have decent credit already.

How Does It Compare to Other Student Credit Cards?

Revvi Visa® Credit Card

Intro APR: None

Intro APR: None

Intro APR: None

Ongoing APR: reg_apr,reg_apr_type based on creditworthiness

Ongoing APR: reg_apr,reg_apr_type based on creditworthiness

Ongoing APR: 35.99% Fixed

Balance Transfer: None

Balance Transfer: None

Balance Transfer: None

Annual Fee: annual_fees

Annual Fee: annual_fees

Annual Fee: $75 first year, then $48 after

Credit Needed: Scores in the credit_score_needed range

Credit Needed: Scores in the credit_score_needed range

Credit Needed: Scores in the poor – bad range

Is It Worth It?

For students looking to build credit, the Capital One Quicksilver Student Cash Rewards Card can be a good option. If you already spend a decent amount with Uber, you can rack up cash back quickly now through November 2024. Then, you can use that cash to cover books or other necessary expenses or splurge on something fun like a concert or weekend trip.

Are you ready to maximize your credit rewards?

Frequently Asked Questions

What are the credit limits for the Capital One Quicksilver Student Cash Rewards Credit Card (minimum and maximum)?

The credit limit you’re approved for depends on your credit history and ability to pay back any balances. That being said, users of the Capital One Quicksilver Student Cash Rewards Credit Card can likely expect credit limits from a few hundred to a thousand dollars or so.

How soon can I increase my credit limit after being approved for a Capital One Quicksilver Student Cash Rewards Credit Card?

Credit card providers are often willing to increase your credit limit after a period of time in which you have demonstrated on-time payments and responsible credit management.

How good is a Capital One Quicksilver Student Cash Rewards Credit Card for building credit?

This is a decent credit-building card for someone (like a student) just starting to build their credit. Capital One also regularly reports to credit bureaus, so your timely payments will be noted and can help you build credit.

Advertiser Disclosure: Credit.com has partnered with CardRatings for our coverage of credit card products. Credit.com and CardRatings may receive a commission from card issuers.

In July 2016, the Consumer Federation of America (CFA) and VantageScore Solutions reported that most consumers—more than 80%—knew basic facts about their credit scores, including that credit scores are used by lenders to approve or deny mortgages and by credit card issuers to approve or deny credit cards.

While it’s good that most people know the importance of credit scores, the same survey found that many consumers don’t understand credit score details. In other words, about how personal credit works and how credit scores work still confuses people.

How Are Credit Scores Created?

When you borrow money, whether through a revolving account, like credit cards, or an installment account, like an auto loan or student loan, the information is gathered by the credit bureaus. The data the bureaus keep in your credit files is the date used to calculate your credit scores.

When you apply for a loan or card, the bank or issuer may look at just your credit score or at your entire credit file. There are five major areas of information in your credit file that are used to calculate your score:

Payment history

Debt usage, also known as your credit utilization ratio

Age of credit accounts

Types of accounts or account mix

The number of hard inquiries on your credit, not soft inquiries

A good credit score includes a healthy mix of all these factors. Each factor though weighs differently toward a score. Payment history makes up 35% of your score. Debt usage 30%, credit age 15%, and account mix and credit inquiries each make up about 10% of your score.

How Are Credit Scores Used?

You have multiple scores and types of scores and there are different scoring models. The resulting scores and your credit file are used to determine your risk factor for future loans. The three-digit score is a numerical representation that indicates how risky a borrower you are from a lender’s perspective.

Score ranges break down as follows:

Excellent credit: 750+

Good credit: 700-749

Fair credit: 650-699

Poor credit: 600-649

Bad credit: below 600

A higher credit score—roughly 700 or above—can result in your getting approved for better terms and conditions. For example, your credit reports and/or scores impact the deals and interest rate you get when you buy a home, finance a car, rent an apartment, apply for a job, buy insurance, purchase a cell phone or open a new credit card.

The best way to improve your credit score or maintain it is to be responsible with the credit cards and loans you have. Remember those five factors mentioned a minute ago? This is where they come into play—things like making loan and credit card payments on time each month and maintaining a good debt usage or a credit utilization rate—the amount of debt, including credit card debt, you have in relation to your overall credit limit—can help you reach the credit score you’re after.

Using credit irresponsibly by making late payments and maxing out credit limits can have an affect your credit negatively and lower your credit score.

How Does Credit Reporting Work?

The credit reporting system includes three main players:

Consumers

Credit bureaus

Financial companies, such as banks, lenders and credit card issuers

Information about your credit cards, loan accounts and credit inquiries is reported electronically to the three main national credit bureaus—TransUnion, Equifax and Experian—by lenders and creditors roughly every 30 days. The bureaus collect and store your credit information in your credit file for future reference. Meaning, your behaviors can be reviewed in the future by others to determine your risk level.

Businesses, such as auto loan lenders, banks, credit unions, credit card companies and insurance agencies—even employers—use your credit data from the credit bureaus to determine your risk level. Once they have an idea of how risky it is to lend you money, they determine the rates you have to pay or other terms and conditions. Or, they may determine not to loan you money or give you a credit card at all. They may also use this information to send you pre-approved offers in the mail.

The three national credit reporting agencies don’t share information with each other and not all lenders or creditors report to each. As such, your credit reports from TransUnion, Equifax and Experian can contain different information about you. So, it’s important to monitor all three reports because you can never be sure which one will be used when you apply for a new account. You also want to make sure you review them for any errors that are damaging your scores. Learn more about how to dispute an error on your credit reports.

Are Creditors Required to Report to Credit Bureaus?

Not all creditors report your account information to the credit bureaus. And they’re not required to. While businesses are legally required to report accurate information, there’s no law that says they have to report at all. While nearly every major creditor reports to all three bureaus, smaller lenders and banks may not send your monthly account information to all three or any of the credit bureaus.

What’s On Credit Reports?

Along with your credit card and loan account records, basic information about you, like your name, address and recent applications, is recorded in your credit files. Public records such as bankruptcies, tax liens and judgments can also appear on your reports.

Information about your income, race, gender, age, religion or health details isn’t included on credit reports.

Most information expires from your credit reports after 7 to 10 years, but when information expires can vary depending on the circumstance. It’s important to keep the information on your credit reports positive and accurate. And if there’s something inaccurate on your credit reports, you can file a dispute with one or more of the credit reporting bureaus to try and have it removed from your file.

Find Out Where You Stand

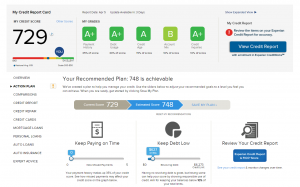

Finding out how credit works is important. And now that you’ve done that, you likely want to know where you stand. You can get your free Experian credit score and a free credit report card on Credit.com.

Your report card includes including a grade for each area that makes up your scores. You see how your payment history, debt and other factors affect your scores, and get recommendations for ways to improve each area if needed.

Your report card is updated every two weeks, so you can check your credit regularly and ensure nothing unexpected pops up. An unexpected change in your score can indicate an issue, such as potential identity theft.

Buying a house and getting a mortgage is a big investment– and not only for you.

When you choose a mortgage lender and are approved for your home loan, your lender is agreeing to lend you all funds necessary to cover your home purchase. Because a house is a high-cost purchase, lenders want to guarantee that you’re not a “risky borrower.” Lenders want to know that you’ll be able to make your monthly payments on time and in full.

How do lenders decide whether you’re a risk?

In most cases, mortgage lenders, or their underwriters, to be exact, will take a look at how well you’ve managed debt in the past, and how well you’re managing debt currently.

So, having debt can be a good thing.

This may seem counterintuitive because if you’re buying a house, you’d want to save as much money as you can. And you probably wouldn’t want your money tied up in other debts, right?

Get matched with a personal

loan that’s right for you today.

Learn

more

Yes, saving money is always a good idea. But having some debt before buying your house can actually be an important factor in getting approved for a mortgage.

Why Debt Matters

To see how well you manage your debts, mortgage underwriters will take a detailed look at your credit score/credit history and your debt-to-income ratio (DTI).

Generally, you’ll want to have a high credit score and a low DTI. A high credit score indicates that you manage your debts responsibly. A low DTI indicates that you don’t have too much of your income tied up in paying off those debts.

Let’s take a closer look at both factors:

Your Credit Score

Each factor in your credit score is defined by debt. And to create and increase your credit score, you need to take on debt and manage it responsibly.

Your credit score is usually impacted by the following five factors:

Payment history — Your payment track record is the most important factor considered in your credit score. Lenders want to know if you’re a trustworthy borrower. And so, they want to see if you make on-time payments on other debts.

Credit utilization (or amounts owed) — Owing money on your credit cards, in particular, is not a bad thing. But, if you’re using too much at one time, underwriters might take that to mean that you’re overextending yourself financially.

Length of credit history — A longer credit history is favorable. But if your credit history is limited, you won’t necessarily be disqualified from borrowing money.

Credit mix — Underwriters want to see how you manage different types of debt.

New credit — If you’ve opened multiple credit accounts at one time, this is a red flag for underwriters because it can suggest that you’re in financial distress.

For a mortgage, you’ll typically need a credit score of at least 620 for a conventional loan. But, it could be best to shoot for a credit score of 700 or above. A higher credit score increases your chances of approval, and also increases the loan amount that you’ll be approved for. But a high credit score could also help you secure a lower mortgage rate, which could save you a significant amount of money over the life of your home loan.

Your Debt-to-Income Ratio (DTI)

Your DTI is a percentage representing how much of your income is put towards paying down debts. Since a mortgage is such a large investment, and your monthly payments could be fairly substantial, underwriters want to make sure that you’ll be able to make those payments. So, the lower your DTI, the better.

In general, a DTI of 36% or lower is ideal. In fact, a DTI above 50% most likely won’t be approved (although there are exceptions).

To calculate your DTI, simply divide your monthly debts by your monthly gross income. If your resulting percentage is higher than 50%, you’ll want to work on paying off some of your debts.

Debt Management Tips

Whether you’d like to reduce your debt before buying a house or just want to maintain a solid credit score by making consistent credit payments, knowing how to manage your debt could help you qualify for a mortgage. And it can also reduce your own stress levels.

The following tips can help you manage debt before buying a house, and could also be helpful once you’ve purchased your dream home and are in the thick of making mortgage payments:

Look at Your Credit Report

Your credit health is an important qualifying factor for a mortgage. So, it can be a good idea to take a look at your credit report to ensure that everything has been reported correctly and that there aren’t any errors. You wouldn’t want your credit score to be negatively impacted because of mistakes in your credit report.

You can order your credit report from any of the three major credit bureaus: Equifax, Experian, and TransUnion using annualcreditreport.com. Or you can even get your free credit report card here on Credit.com.

Once you have your credit report it is important to look at the following:

Your personal information

Your credit accounts

Credit inquiries

If you see any errors or inconsistencies anywhere in your credit report, these can be challenged with the credit bureau that created the report.

Consolidate Your Debt

If you find that you’re making payments on various loans and/or credit accounts, it could save you money (and save you from stress) to consolidate your debts into one. This way, you’re only paying interest on one debt instead of multiple. Therefore, you won’t have multiple payments to keep track of.

Related Read: What Is a Debt Consolidation Loan and How Can You Get One?

Don’t Make Drastic Changes to Your Credit

It can be tempting to pay off debts right before applying for a mortgage. However, doing so could actually hurt your credit score. When you pay off a debt, your credit score will actually drop temporarily.

On the flip side, if you’re trying to build credit and try to open multiple credit cards, or take on other debt before applying for a loan, this will also take a hit on your credit score. Not to mention that seeing a lot of change and new debt before applying for a mortgage is a red flag to underwriters. It can indicate you might not be financially prepared to take on a mortgage.

Make a Budget

Whenever a financial discussion is taking place, budgets are bound to come up. While the concept of making a budget might seem obvious and over-shared, it’s a great way to track your expenses and ensure that you’re meeting all your financial expectations and needs. There are a lot of costs involved with buying a house. So, you’ll want to make sure that you can afford them.

In this case, creating a budget can help you map out your current debts and other expenses in relation to your income. This allows you to see what’s happening and adjust as needed. A budget can give you the peace of mind that you’re not overspending, and are still able to meet all your other financial responsibilities.

Build Your Emergency Fund

Building your emergency fund before getting a mortgage may be one of the most important things you can do. You never know what expenses might arise once you purchase your house, and you don’t want all your money tied up in your mortgage payment and other monthly payments if, for example, your roof needs to be repaired or you encounter water damage.

It’s often encouraged to set aside three to six months worth of expenses in an emergency fund.

The Bottom Line

Buying a house is a big purchase, and it can be daunting to think of getting a mortgage if you are trying to pay down student loans, an auto loan, credit cards, etc. To help you save money and save you from stress, work on paying down other debts so you can be confident in your ability to make mortgage payments and enjoy your new home.

However, you don’t need to be debt-free to buy a house. In fact, some well-managed debt can boost your credit score, showing mortgage underwriters that you are a responsible borrower.

That doesn’t mean that you need to dig yourself into a hole of debt that you’ll never crawl out of. By taking the time to create a budget or analyze your credit report, you can see how you’re doing financially and where some changes can be made. Perhaps you could consolidate some of your existing debt, or you could completely pay off some of your debts.

In the end, you just want to make sure that you’re comfortable taking on a mortgage and can afford to do so.

Owning a car comes with costs that go beyond getting an auto loan or needing to insure your vehicle. Maintenance and repair costs can add up, and it’s essential to be prepared for those financially. In 2021, for example, individuals in the United States spent more than $194 billion on vehicle maintenance and repair. Find out about some of the most common car repairs below, including what they cost.

10 Common Car Repairs and What They Cost

This list of car repairs isn’t comprehensive. However, it includes some of the most repaired or replaced items on vehicles.

Replacing an Oxygen Sensor

Oxygen sensors check the exhaust from a vehicle’s engine to see how much oxygen is in it. Most modern cars have O2 sensors before and after the catalytic converter. Your check engine light can come on when the sensors aren’t working right.

While a rogue O2 sensor may not be an immediate emergency, if it isn’t functioning correctly, it can lead to fuel intake and other issues with the engine. The cost of replacing O2 sensors varies depending on which sensors need replacing and the make and model of your car. On average, you can expect this repair to cost $150 to $500.

Replacing a Catalytic Converter

Catalytic converters control the emissions expelled by vehicle exhaust. They’re required on most new cars. A damaged or broken catalytic converter causes your check engine light to illuminate. If your catalytic converter isn’t working, your vehicle might not pass state inspection requirements where applicable.

In most cases, a catalytic converter replacement doesn’t require much labor. However, the parts can be expensive. The job can cost $900 to $3,500 on average, depending on the make and model of your car and where you get the work done.

Get matched with a personal

loan that’s right for you today.

Brake jobs are common because your brakes and rotors wear down over time. Expect to pay $200 to $500 for a brake service or repair job. If you need a complete brake job, which includes replacement of brakes, calipers, pads and rotors, the cost can average $200 to $800, depending on the quality of the parts, the make and model of your vehicle and where you get the work done.

Tightening or Replacing a Fuel Cap

The cap you take on and off when filling your car with fuel is a critical component. It’s supposed to provide a true seal that keeps the fumes and evaporation of fuel inside the tank. You might need a new one when your fuel cap goes missing or doesn’t create a tight seal. On average, the parts and labor for such a replacement range from around $97 to $102.

Thermostat Replacement

A thermostat in a car measures the temperature in the cooling system and helps ensure the right amount of coolant is being cycled through the engine. That regulation can’t occur if the thermostat is broken, which can lead to issues with an overheating engine. The cost of repairing or replacing a car thermostat is $140 to $300—typically much less than you’d pay for engine damage.

Replacing Ignition Coils

The ignition coils take power from your car’s battery and magnify it enough to cause the spark necessary to ignite the fuel and get your engine running. Bad ignition coils can mean your car doesn’t start. If you need to replace an ignition coil, expect to pay $200 to $300 on average.

Mass Air Flow Sensor Replacement

The mass air flow sensor keeps track of how much air enters certain parts of your engine. Your car needs to know this to allow the right amount of fuel to flow into the engine. If the mass air flow sensor doesn’t work, your check engine light may illuminate, and you may also notice symptoms such as misfires, a rough-running engine, black smoke in the exhaust and engine issues on idle. The cost to replace this part is usually less than $300.

Replacing Spark Plug Wires and Spark Plugs

Spark plugs and wires are necessary to start your vehicle. Sometimes, you can easily replace these parts to save a bit of money. The cost for parts is $125 to $150. If you pay for professional service, expect the cost to be between $190 and $235 in total.

Replacing Evaporative Emissions Purge Control Valve

The purge valve keeps fuel vapors from being released into the air. It’s a required part of vehicle emissions systems. The cost of replacing this part ranges from around $160 to $180.

Replacing Evaporative Emissions Purge Solenoid

Purging solenoids are parts involved in the same process as the purge control valve. You can expect to pay $150 to $300 to get these parts replaced.

Prepare for Car Ownership and Repairs Financially

Owning a car is a significant investment, and it’s important to be prepared for paying your car payment and covering unexpected expenses.

Start by understanding what you need to finance a car, including what’s a good credit score to buy a car. Then you can shop around for an auto loan that meets your needs.

Once you have a car, create a budget and set money aside for emergency needs. You can also work on your credit to ensure you have access to credit cards and loans if you need temporary help with a major unexpected expense.

More on Auto Loans:

Article updated. Originally published April 19th, 2016.

When you buy a pet insurance plan, coverage doesn’t begin immediately. Instead, a waiting period applies before you can make any claims. Pet insurance companies set their own waiting periods, so they’re not the same across the board.

In rare cases, you may be able to get pet insurance with no waiting period, but it still won’t be instant. You’ll have to wait a few days while the company reviews your pet’s medical records and makes a decision.

What are pet insurance waiting periods?

A pet insurance waiting period is the time between when you buy a policy and when coverage begins. If your pet needs to visit the vet during the waiting period, you’ll have to pay for those expenses out of pocket.

🤓Nerdy Tip

Waiting periods generally apply to new policies or those reinstated after a lapse in coverage. If you renew your policy continuously, you usually won’t have to go through another waiting period.

Do any pet insurance companies have no waiting periods?

Most pet insurance companies have waiting periods, but the best ones don’t make you wait long. For example, MetLife’s accident coverage begins immediately, and illness coverage starts after 14 days.

One of the only pet insurance companies without a waiting period is Companion Protect. But you’re eligible only if you adopt a pet from one of its partner shelters, and coverage isn’t instant. There’s usually a delay between sign-up and policy activation while the company reviews your pet’s medical records. Also, a vet visit may be required if your pet hasn’t had one in the past 12 months. This delay acts as an unofficial waiting period.

How long do waiting periods last?

Pet insurance waiting periods may vary depending on where you live and the plan you choose. Below are typical waiting periods for some of the best pet insurance companies.

Can you get pet insurance retroactively?

You can’t buy pet insurance retroactively. If your pet shows signs of an illness or injury before you buy the policy or during the waiting period, it’s considered a pre-existing condition and typically won’t be covered.

🤓Nerdy Tip

If your pet insurance policy lapses, anything your pet has been diagnosed with up until that point can be considered a pre-existing condition and be excluded from coverage. Keep your policy active by paying your premiums on time and renewing before the expiration date.

Types of waiting periods

Pet insurance policies often have different waiting periods for different types of coverage. Here are some common waiting periods.

Accident waiting periods

Accident waiting periods typically last one to 14 days. They apply to accidental injuries like broken bones, fractured teeth, swallowed objects or bites from other animals.

Illness waiting periods

Illness waiting periods tend to be longer than accident waiting periods and can last from 14 to 30 days. They apply to illnesses like cancer, stomach issues, ear infections, heart conditions or allergies.

Waiting periods for orthopedic conditions

Some pet insurance plans have separate waiting periods for orthopedic conditions like hip dysplasia, patella luxation or ligament injuries. These waiting periods sometimes apply to dogs only and can be from 14 days to six months or longer.

For example, Embrace pet insurance coverage for orthopedic conditions in dogs begins after six months, but you can reduce it to 14 days by having your vet do an orthopedic exam. Healthy Paws’ hip dysplasia coverage begins after a 12-month waiting period and is available only to pets enrolled before age six.

Waiting periods for pre-existing conditions

There are two common types of pre-existing conditions: curable and incurable. Most pet insurance companies will cover curable pre-existing conditions that have been symptom-free for at least 180 days to 12 months.

Curable pre-existing conditions are temporary health issues that were treated and resolved before you bought insurance. They can include things like respiratory infections, urinary tract infections, vomiting and diarrhea.

Most pet insurance companies won’t cover incurable pre-existing conditions, but AKC is one exception. Once you’ve had your policy for 365 days, AKC may cover pre-existing conditions other companies may consider incurable, like allergies and chronic ear infections. (This coverage isn’t available in all states.)

Wellness plan waiting periods

Some pet insurance companies offer optional wellness plans to help cover routine services like check-ups, vaccinations and flea and tick prevention. Wellness plans often have no waiting periods.

Why do pet insurance companies have waiting periods?

Waiting periods protect insurance companies from people who sign up for coverage only after their pet gets sick or injured. Without waiting periods, pet owners could sign up for insurance as soon as an emergency happens, file a claim, then cancel their policy once they get a payout. This would increase risk for the pet insurance company and drive up premiums for everyone else. Waiting periods help lower this risk.

How to handle waiting periods

Waiting periods can be frustrating, especially if your pet needs medical attention during that time. Here are some tips for handling waiting periods.

Get insurance early

One way to minimize waiting periods and avoid pre-existing condition exclusions is to get pet insurance early in your pet’s life. The younger and healthier your pet is when you sign up for insurance, the less likely they are to have pre-existing conditions that could limit coverage.

🤓Nerdy Tip

If your pet already has pre-existing conditions, pet insurance may not be worth it. Think about your vet bills over the past few years. If most of them are related to incurable or chronic conditions that a new policy won’t cover, you may be better off creating an emergency fund for your pet.

Look for ways to limit out-of-pocket costs

If you need emergency pet care during a waiting period, there are things you can do to manage costs. Some veterinary clinics offer payment plans through third-party lenders. You can also look into CareCredit, a credit card for medical expenses.

If your pet needs expensive medications, ask your vet about generic alternatives or look into pet prescription discount programs from GoodRx or AARP.

This article originally appeared on The Avocado Toast Budget.

This post is sponsored by Credit.com.

Here at the ATB, we are all about budgeting in a way that works for you and finding realistic ways to feel more confident with your money.

Now that 2020 is (finally) over, here are ways that you can start to take hold of your finances and build confidence with your money in 2021.

Write down your short, medium and long term financial goals

I’m a big believer that you don’t need to stress over how to maximize the value of every dollar you come across.

Much of personal finance is behavioral and relies on us finding value in how we navigate our money!

Because of this, I found it incredibly helpful to sit down and brainstorm short, medium and long-term financial goals to decide what I wanted my money to do for me.

Write down your short, medium and long term financial goals

Here’s how I break it up:

Short-term goals – less than two years

Medium-term goals – 2 – 10 years

Long-term goals – 10+ years

Feel free to dream big!

We want to make realistic and attainable goals, but we also want to allow ourselves to dream about what we really want our lives to look like, and how our money plays a role in that.

Get to know your credit score

Wanna know a secret? I avoided my credit score for the longest time.

Turns out, once I finally faced my credit score, I became more empowered to understand how my credit score affects my finances and what I could do to change it.

While free resources can give you a ballpark estimate of your credit score, that score isn’t very useful and certainly isn’t what creditors see!

Knowing your true score, and seeing your credit reports from all three major credit bureaus, gives you security and control over how to navigate your credit score going forward.

While it can be daunting, credit plays an important role in our lives from renting, to car insurance, to mortgages, to career opportunities and more.

That’s why it’s important that you stay informed of what your credit actually looks like that’s why I signed up for ExtraCredit’s free trial!

Set up automatic savings

Automating your savings is LIFE CHANGING.

Setting up automatic savings is often referred to as “paying yourself first” because you are prioritizing saving money for Future You.

There are tons of different savings goals that you can put this money toward, but the important part right now is to set up automatic savings so you can set it and forget it.

Trust me—you miss that money a lot less if you never see it in your account in the first place.

If you have automatic deposits at work, it’s super easy to add a savings account and have a certain % or dollar amount go into that account every month without it EVER hitting your checking.

In my opinion, this is the best way to go. Out of sight, out of mind.

You’re way less likely to touch this money, and you’ll be shocked at how much it grows over time!

If this isn’t an option for you, you’re not out of luck. You can set up automatic savings transfers into your savings account from your checking account through your bank.

Find a budget that works for you

Here at the ATB, we are all about budgeting in a way that makes sense for you and your life.

Budgeting doesn’t have to be stressful and restrictive. It should actually be freeing and allow you to feel more confident and in control of your money!

There’s no one right way to budget, and there are TONS of different types of budgets depending on your income and financial goals.

Personally, I use a zero-based budget which allows me to track and decide where every single dollar I have is going.

If you have big savings goals, low income or high debt, I definitely recommend checking out a zero-based budget.

Learn how to increase your credit score

Your credit score has a bigger impact on your life than just determining your eligibility for loans.

Credit can impact your ability to rent, job opportunities, car insurance rates and more.

Once you know what your credit score is, it’s important to understand what makes up your credit score, and what steps you can take to increase it.

There are five factors that influence your credit score:

Payment History

Amounts Owed

Length of Credit History

New Credit

Credit Mix

Payment History makes up 35% of your credit score, so it is the most important factor.

ExtraCredit gives you the ability to report rent and utility payments, adding new tradelines to your credit profile. Adding payment history to your credit file.

And if you need help working to repair your credit, you can also use the Restore It feature to get an exclusive discount from a leading credit repair company. Remember: your best credit score is an accurate one.

Understanding how to increase your credit can take a lot of stress out of your finances and help you feel more in control of your credit future.

Make a debt payoff plan

I paid off $20k in CC debt in less than a year, and in order to do that, I needed a concrete plan of how I was going to tackle my debt.

Prior to that point, I had just been throwing a little bit here and there, hoping that my balance would eventually decrease.

Shockingly, that never happened.

Once I decided to use the debt avalanche to tackle my credit card debt, I was able to calculate how much extra money I could throw at my debt every month in order to make progress toward my debt free goal.

With this method, I paid the minimum payments on all of my debt except for the one with the highest interest.

With the highest interest debt, I put any extra money I had toward paying that down.

This gave my money more of a purpose than just throwing extra money here and there at my different debts.

It was also reassuring and motivating to see the loan amount decrease drastically as I threw the extra money I had towards it.

Quick answer: Yes, it’s possible for undocumented immigrants to get a mortgage loan. They face legal and financial obstacles that don’t stand in the way of other purchasers, but millions have done so successfully.

You don’t need to be a resident to own real estate in the United States. Many documented immigrants own homes. While it’s difficult to get accurate statistics about undocumented homeowners for a number of reasons, in 2014, the Migration Policy Institute estimated that around 3.4 million undocumented immigrants owned homes in the United States.

Keep reading to discover how your residency status impacts the home loan process. We’ll also highlight some important information you should know about your rights when applying for a mortgage.

In This Piece

How Residency Status Affects a Home Loan

Understand Your Rights

How to Get a Mortgage

How Residency Status Affects a Home Loan

Overall, residency status plays a significant role in determining the availability and terms of home loans for individuals in the United States.

Green Card Holders

Green card holders are permanent residents eligible for most types of mortgages available to U.S. citizens. This means they must provide proof of income, credit history and other financial documents to qualify for a home loan. In some cases, green card holders might face additional challenges during the home loan and purchase process. Those can include difficulty in obtaining mortgage insurance or a higher down payment requirement, which can vary based on the lender and the type of loan.

Refugees and Asylum Grantees

Refugees and asylum grantees are individuals granted legal status in the United States due to persecution or fear of persecution in their home countries. They may be eligible for certain types of mortgages. However, their ability to obtain a home loan might depend on their specific immigration status and financial circumstances. For example, refugees or asylum grantees who have been in the United States for less than 2 years might have a harder time getting a mortgage because many lenders require at least 2 years of residency to establish credit history.

Get matched with a personal

loan that’s right for you today.

Learn

more

DACA

DACA recipients, or individuals who’ve been granted Deferred Action for Childhood Arrivals, are not eligible for most types of home loans. This is because they don’t have legal permanent residency status. However, some lenders may offer alternative financing options or assistance programs specifically designed for DACA recipients and other undocumented immigrants.

Additionally, DACA recipients who have obtained an Employment Authorization Document and can demonstrate a stable income and credit history may be able to get a mortgage under certain circumstances.

Understand Your Rights

The Fair Housing Act prohibits discrimination in housing based on race, color, national origin, religion, sex, familial status or disability. Immigrants, including those who aren’t U.S. citizens or permanent residents, are protected under the FHA and have the same rights as other individuals.

That includes:

The right to rent or purchase housing without discrimination based on national origin

The right to be treated the same as U.S. citizens or permanent residents in all aspects of the housing process, including advertising, application, screening and approval

The right to request reasonable accommodations in housing, such as modifications to the physical structure of a home or changes to policies or procedures, if disabled

If you believe you’re being discriminated against during the home loan, home buying or other housing process, you should report it.

How to Get a Mortgage as an Undocumented Immigrant

Undocumented immigrants aren’t usually able to qualify for mortgages through traditional services, such as those backed by Fannie Mae and Freddie Mac. However, individuals with an ITIN may be able to get approved for special loans from private lenders. An ITIN (Individual Taxpayer Identification Number) is a unique identifier the IRS uses to process tax returns and payments for those that do not have or do not qualify for a social security number.

Apply for an ITIN

The first step is to apply for an ITIN, or Individual Taxpayer Identification Number. You do this by completing Form W-7 via mail, in person at an IRS-authorized agent or in person at an IRS Taxpayer Assistance Center.

Save for a Down Payment

Because undocumented immigrants can’t usually qualify for federally backed loans, such as those through the FHA, they probably won’t qualify for mortgages with low down payment requirements. Private lenders may require down payments as much as 20% or even 30%. If an undocumented immigrant wants to buy a home, they should start saving as soon as possible. That might mean paying down other debt first.

Get Documentation Ready

In addition to the ITIN, undocumented immigrants will have to provide information to help qualify them for a private home loan. That information can include:

Proof of income, such as recent pay stubs, tax returns or other financial documents

Information about credit history, including any outstanding debts, loans or credit accounts

Recent bank statements that show account balances and transaction history

Identification documents, such as passports or government-issued IDs

Proof of residency status, such as a lease agreement or utility bill in the person’s name

Proof of employment or self-employment, such as a letter from an employer or recent tax returns

Apply for an ITIN Mortgage

Once you have an ITIN, a down payment and all the necessary documentation, you can apply for an ITIN mortgage. Start by browsing the mortgage options in the Credit.com marketplace.

This article originally appeared on The Financially Independent Millennial and was republished with permission.

When consumers purchase a car, there are several things to think about. While the primary process has been handled entirely with test drives and dealerships or private sellers, it’s up to you to continue further down the checklist to get the most out of a used car.

People might think that there’s nothing left to do after buying a car, but don’t forget to take the steps needed to keep a used car on track.

1. Get the Car Insured

When you buy a car, the first thing to always do is to get insurance before leaving the car lot. Getting into an accident just after leaving is a terrifying possibility after spending hard-earned money on a car, even if it’s a used car. Either way, it’s an investment, and buyers need to protect themselves.

It’s a good idea to call around before purchasing the car model you have in mind to get a quote. If that didn’t happen before, getting the best car insurance must be the top priority to get taken care of once a vehicle is purchased. Some dealerships require buyers to have insurance before leaving, so being ready with insurance is imperative for a good experience.

Get matched with a personal

loan that’s right for you today.

Learn

more

2. Check for Existing Recalls

Recalls happen in brand-new and used vehicles as technology changes over time. Sometimes, manufacturers will send out information for a recall because of a necessary update, too. Certain recalls can also affect driver or passenger safety, so recalls cannot be ignored.

After the purchase is complete, buyers can find information about recalls from the National Highway Traffic Safety Administration. Get the vehicle identification number or VIN from the car to complete a search. It’s also a good idea to check for recalls multiple times a year because new recalls are released periodically.

3. Transfer the Title

If a car is purchased from a dealership, the dealership typically handles the title transfer. The title is the official document that proves ownership, so if you buy privately, it’s critical to get this taken care of as soon as possible after purchase.

When purchasing from a private seller, buyers need to verify liens do not exist from the previous owner. If there are, those need to be handled immediately. Buyers need proof that the seller has documents that prove any loans have been paid as required. If a buyer has any questions about transferring a title, the DMV needs to be contacted for state-specific answers.

4. Get the Car Registered

Once a car has been purchased, it must be registered with the DMV soon after. Car dealers will typically handle getting the vehicle registered in the buyer’s name, but it’s different when working with a private seller. Private sellers should provide documentation to the buyer to show to the DMV to get the registration done.

Some of the documents needed include the bill of sale showing the purchase price, the title that has been signed over by the previous owner, the VIN, proof of insurance, odometer reading, sales tax if applicable, and evidence of passed inspections. Buyers also need to contact the local DMV to find out if any further documents are required.

5. Find a Trusted Mechanic

Finding a mechanic can be challenging, which is one reason that buyers may prefer to purchase from a well-respected dealership. Dealerships have mechanics on staff that are responsible for conducting an inspection and doing any preventative maintenance before the purchase.

Private sellers are different, and buyers need to be aware of getting a used car with issues. Ideally, the vehicle should be checked before purchase, but it needs to have a thorough inspection done when that’s not possible. When in need of a trusted mechanic, buyers should research reviews and request recommendations from local groups to get an idea of who to trust.

6. Schedule Any Necessary Repairs

Once the mechanic has had a chance to complete an inspection, it may be recommended to replace spark plugs, belts, or any frayed wires, along with any other issues. There may also be cosmetic issues that may need to be dealt with if the buyer deems these repairs are essential.

Some repairs may be more critical than others, so depending on what the mechanic says, there may be a list that needs to be followed. It’s possible that the new owner might need to prioritize repairs to get things done over time. If that turns out to be the case, working out a schedule with a trusted mechanic will be a great way to get things done.

7. Read the Owner’s Manual

It’s a good idea to read the owner’s manual to get to know your newly purchased vehicle inside and out. It may not be full of entertaining reading, but knowing what the lights on the dashboard mean can be helpful should they come on. Buyers can also read about any potential existing warranties that might still apply to the car.

Getting to know more about the car is helpful because new owners can learn about what to expect regarding the engine and other internal components of the vehicle. It also gives the owner a chance to become familiar with some of the more specific details about different parts of the car.

8. Create a Maintenance Schedule

Using the manual, buyers can also get to know what the regular maintenance schedule is for the car. Each manual contains a suggested maintenance schedule, so a buyer knows what to expect and plan for in the future. Sticking with the recommended schedule can help in saving money over time, too.

Maintenance is a crucial part of being a responsible car owner. That includes keeping an eye on the wear and tear of tires, keeping up with oil changes, and getting regular tune-ups. Finding a trusted mechanic is essential in keeping car maintenance from becoming overwhelming.

9. Consider an Extended Warranty

When purchasing a used car, buyers may also want to consider a used car warranty. There are many different options available for warranties that range from expensive repairs to bumper-to-bumper coverage. Buyers should still do research to figure out the best options available.

Keep in mind that some warranties appear to be scams, so researching is vital in making the best selection. Buyers should also check for any specific fine print regarding repairs and coverage. Some warranties are only effective at particular mechanics, so those might be ones to steer clear from.

10. Get Familiar with Features

Once the car is ready to go, buyers need to familiarize themselves with the car’s features. Learning what all of the buttons do is vital because the last thing anyone wants to deal with is trying to figure out how to open the gas tank at an inopportune time. Knowing how to program the dashboard is helpful, too, to enjoy driving to the perfect soundtrack.

Features go beyond the buttons, though, and include levers for seats and the position of latches if installing a car seat is an essential aspect of the car. Finding out where all of the power outlets are is also important so owners can charge their gadgets as needed.

A Few Last Words on What to Do after Purchasing a Used Car

There’s a lot to think about after purchasing a used car. Getting car insurance and title transfers are essential to getting started. Finding out about recalls is critical to keeping the car safe for drivers and passengers. Once registration is complete, it’s time to get the car inspected by a trusted mechanic.

After that, it’s all about creating a schedule for repairs or maintenance to get the most out of a newly purchased car. Getting familiar with the features is also essential to feel comfortable with a new car, even if it’s a used car, because it will be new to you.

Once all of the necessary tasks are done, it’s time to get down to the fun stuff, like finding the accessories that reflect your personality. Adding some exciting goodies to a vehicle should be a part of what it means to have a new car. Taking care of it with regular car washes and giving the car some character is the icing on the cake. When everything is squared away, it’s time to take a drive and enjoy your new car experience.

Are you thinking about selling your engagement ring? People sell their engagement rings for all sorts of reasons, such as no longer being in a relationship or inheriting a ring. Whatever your reason may be, you can most likely sell your engagement ring and make extra money. You can use this extra money towards paying…

Are you thinking about selling your engagement ring?

People sell their engagement rings for all sorts of reasons, such as no longer being in a relationship or inheriting a ring.

Whatever your reason may be, you can most likely sell your engagement ring and make extra money.

You can use this extra money towards paying off debt (like credit card debt or student loans), starting an emergency fund for unexpected expenses (like medical bills, vet visits, or house repairs), putting the money into your retirement savings, or even saving for financial goals (like a home deposit, buying a car, or going back to school).

Today, you’ll learn how to:

Get your engagement ring appraised

Negotiate for the highest price

Find the best place to sell your engagement ring

And, of course, the step-by-step process of how to sell an engagement ring!

How To Sell An Engagement Ring

How much is an engagement ring worth?

Before you sell your engagement ring, you should try and figure out how much it is worth.

One of the things to think about when valuing a diamond engagement ring is the “4 Cs of a Diamond.” If you want to know where to sell diamond rings, first you must figure this out.

The 4 Cs stand for:

Carat – This is the size of the diamond. Larger diamonds are usually worth more money.

Cut – This is not the diamond shape. Instead, this is the quality of the diamond’s cut which will impact how beautiful and brilliant the diamond is.

Color – A diamond’s value increases with less color, as a completely colorless diamond is worth more.

Clarity – Clarity is all about the imperfections and blemishes that a diamond may have. The fewer there are, the more valuable the diamond.

Other things that may increase or decrease the value of your used engagement ring include:

Condition – The overall condition of the ring is important. A ring that has been taken care of and shows minimal signs of use will typically hold onto more of its value in comparison to a ring that displays noticeable wear and tear.

Resale market – Rings with a popular style or from a well-known designer may see a higher price when resold.

Certification and documentation – Having a document such as a diamond grading certificate can help determine the quality of the ring.

Designer and brand name – Rings from certain designers or brands (such as Cartier or Tiffany & Co.) tend to have a higher resale value due to their reputation and craftsmanship.

Even though a pre-owned engagement ring may have a lower value compared to a new one, it can be a great value for buyers looking for a high-quality ring at a more budget-friendly price. And, that is why people buy them – they can save some money over a new ring.

Recommended reading: 8 Items To Sell Around Your Home For Extra Money

Gather documentation for your engagement ring

If you’ve decided to sell your engagement ring, it’s time to collect all of your paperwork related to the ring such as the diamond’s certification, receipts, and appraisals.

These documents will help figure out the ring’s value, establish its authenticity, and make the process of selling a little more smooth.

Here’s a list of the paperwork you might need:

Appraisal certificate – The appraisal certificate is a professional evaluation of the engagement ring. This document includes details about the diamond’s cut, color, clarity, carat weight, and quality.

Original receipt – Having the original receipt from the purchase of the engagement ring will help show that the ring is authentic.

Diamond certification – If the diamond was graded and certified by a recognized gemological laboratory, this can be helpful.

Gemstone certificates – If your engagement ring has other gemstones besides diamonds, include these certificates for the stones as well.

You don’t need any paperwork to sell an engagement ring, but, it can make things a little easier and may get you a little more money.

How to get an engagement ring appraised

Getting an engagement ring appraised by a certified gemologist or jewelry appraiser will give you an accurate estimate and valuation of how much your engagement or wedding ring is worth.

This can help you when negotiating (such as with a pawnshop) and simply knowing the amount that you should be looking for when selling your ring.

You can get your engagement ring appraised by:

Looking for appraisers – You can search online for certified gemologists or jewelry appraisers in your area. You can also ask local jewelry stores for their recommended appraisers. It’s important to find an appraiser with credentials from places such as the Gemological Institute of America (GIA), the American Gem Society (AGS), or the International Society of Appraisers (ISA).

Contacting the appraiser – Call the appraiser and ask for their fees and to schedule an appointment. You may need to bring documents such as receipts, certificates, or previous appraisals for the ring.

Getting the ring appraised – Take the engagement ring to the appraiser. They will examine the engagement ring’s characteristics including the diamond’s cut, color, clarity, and other important factors.

Receiving the appraisal report – Once the appraisal is done, the appraiser will provide you with the report. This report includes information about the ring’s characteristics as well as an estimated value based on the current market. Ask the appraiser any questions you might have or if you need a question answered.

Where to sell an engagement ring

Now is the time to look at your different options for selling the ring. You can sell engagement rings at jewelry stores, pawn shops, online marketplaces, auction houses, consignment shops, and more.

Some things that you will want to about when deciding where to sell your engagement ring include the amount that they are giving you (of course, you want the most money, right?), the fees that they may be charging to sell your ring, how much work it will take you to sell it (for example, do you have to create the listing or do they?), whether you feel safe meeting someone to exchange the ring for cash in-person, and more.

As you can see, there are going to be pros and cons for each of the places where you can sell your jewelry.

Below, I go further into each of the best places to sell an engagement ring:

1. Sell your engagement ring online in a marketplace

If you want to sell your engagement ring, one of the best ways to get the most money for it is to sell it online.

Selling your engagement ring online can be convenient and also help you reach a wider audience of possible buyers.

Some of the different places you can sell an engagement ring online include eBay, Facebook Marketplace, and Craigslist.

Here’s a step-by-step guide to help you sell your engagement ring online:

Make your ring presentable – You should clean your ring and take quality photos of it from different angles.

Choose the marketplace – There are many different sites to sell your engagement ring like eBay, Craigslist, Facebook Marketplace, specialized jewelry-selling websites, or online auction sites.

Create a detailed listing – In the listing, write a detailed description of the ring along with its condition and any unique features. Be honest about any imperfections. When listing your ring for sale, you should also describe the ring, such as the diamond’s cut, color, clarity, and carat weight.

Set a price – You should research similar engagement rings or get your ring appraised to find the most accurate price based on current market value.

Shipping – If you’re shipping the ring, make sure to package it securely to prevent any damage in transit and also pay for shipping insurance.

2. Sell your engagement ring on Worthy

Similar to the above, some websites are dedicated to selling jewelry and valuables, such as Worthy.

Worthy does not buy your engagement ring directly as that is not their business model, but they will clean it up and sell it for you.

Worthy makes it really easy to make money with your engagement ring and this is the best place to sell engagement rings online. You simply ship your jewelry to their office with a prepaid shipping label (a FedEx label) that they give you (it’s insured as well). Then, once they get the ring, they prep it for auction. They will clean the ring, take professional photos of it, and grade it.

After that, your ring will go up for auction, and professional jewelry buyers can bid on it. You can set a reserve price that you are comfortable with. Once the auction is done, you will receive the final sale amount after Worthy’s fee. Payment is then sent to you within 1-5 days.

The whole process typically takes around 2 weeks from shipping to getting paid.

So, what are Worthy’s fees? They do almost all of the work for you, so it makes sense that they would charge a fee. They take 18% for up to $5,000. After that, it is a 14% fee for $5,001 to $15,000, a 12% fee for $15,001 to $30,000, and a 10% fee for over $30,000.

So, for example, I found a 1-carat diamond ring on Worthy that eventually sold for $2,792. That means the seller received around $2,289 after the 18% fee that Worthy charges.

3. Work with a jeweler

Jewelers may offer to buy your engagement ring. You can simply call around local jewelry stores near you and ask if they buy used engagement rings.

Sometimes this can be the most straightforward and convenient option for selling your engagement ring as you can possibly sell your ring the same day.

To sell your engagement ring to a jeweler, you will want to look for jewelry stores near you and give them a phone call to see if they buy used engagement rings. I recommend looking for ones with positive reviews.

If you have any documentation for your ring then make sure to bring it with you so that you can show the jeweler.

If they are interested in your engagement ring, then they will give you an offer. If you’re happy with the offer, then you can ask any other questions and possibly sign paperwork to get your cash.

Jewelers may offer instant payment either via cash, check, or electronic transfer and you will want to confirm the payment method before completing the sale.

4. Sell your engagement ring to a consignment shop

You may decide you want to sell your used engagement ring to a consignment shop. Consignment shops have benefits such as offering exposure to multiple buyers. However, they likely charge a commission fee.

To sell your engagement ring through a consignment shop, you will want to Google search for consignment shops in your area and specifically look for shops that sell jewelry or high-end items (make sure the shop has good reviews and even testimonials of previous successful sales of engagement rings).

Once you have an idea of which consignment shops you’re interested in selling your ring at, you should ask them questions about their consignment process, what commission rate they charge, and the terms of the sale.

Then, you’ll give the shop the ring to display in their store.

The consignment shop handles the transaction if someone is ready to buy the ring. You’ll receive payment after the commission fees are taken out.

5. Sell your wedding ring to a pawnshop

When people think about where to sell an engagement ring, one of the first places they think about is probably a pawn shop.

And, it makes sense – pawn shops make it very easy and you can sell your engagement ring for cash here. You can most likely even get paid on the same day!

But, you should keep in mind that they usually give you the lowest amount of money.

If you want to sell your old wedding ring to a pawn shop you will first want to make sure the ring looks nice and clean because that can help you get a better price. Get any papers you have about the ring, like appraisals or certificates, to show how much it’s worth, and make sure you know this number before you go in because you will most likely have to negotiate.

Now, when selling at a pawn shop, you can typically negotiate. To do so, you will want to find out the ring’s value, current market trends, and comparable sales. You can even make a better case for your price by showing documents on the ring and appraisals from certified gemologists. If the pawn shop cannot meet that price, you may just want to move on and try to find another buyer.

When the pawn shop makes an offer, remember they need to make a profit too, so it might be lower than you expect. If you’re not happy with the offer, you can try selling it to someone else. If you agree to sell it, you’ll need to show some ID, sign some papers, and then you’ll get paid.

Frequently Asked Questions

Below are answers to common questions about how to sell an engagement ring.

Is it possible to sell an engagement ring?

Yes! Many places buy engagement rings and wedding rings so that you can make money.

How much can you get for selling your engagement ring?

The amount of money that you can get for selling your engagement ring will vary and usually, you can earn anywhere from around 20% to 60% of what was originally paid for it. Yes, this is a wide range (and can mean a difference of hundreds or even thousands of dollars) and this is because there are so many factors that come into the price, such as the condition of the ring, the market demand, and where you decide to sell it.

How much can I sell my 1 carat engagement ring for?

A 1-carat diamond engagement ring will vary due to the 4C’s (cut, clarity, color, and carat). Usually, you can earn around $1,000 to $5,000 for selling a used engagement ring that is 1 carat.

Is it better to sell or pawn an engagement ring?

This depends – do you want to get the ring back? If you decide to sell it, you can get cash right away. This is a good option if you need money quickly.

On the other hand, if you decide to pawn it, the ring can be used as collateral for a loan. This can be a temporary solution if you just need cash right now but you want to get the ring back later. However, it’s very, very important to carefully read and understand the terms and interest rates from the pawnshop so that you can eventually get your ring back.

Why is the resale value of diamonds so low?

So, you may be thinking “But, I paid $10,000 for this ring! Why am I only getting a few thousand dollars?”

You most likely won’t get the same price that the engagement ring was bought for. This is because places that buy your engagement ring still need to make a profit. Plus, they aren’t going to sell the engagement ring for the same price as a brand-new ring.

How can I be safe when selling a ring?

If you aren’t shipping the ring but are meeting in person instead, then you must be careful. You should avoid sharing personal information until you’re 100% sure they are the person they say they are.

I also highly recommend meeting in a public place, such as a police station parking lot. Bringing a family member or friend with you to the appointment or meeting is good so that you aren’t alone. Make sure to use secure payment methods like cash and do not share bank account information, your social security number, or any other sensitive information (buyers do not need this information!!). Also, ignore requests to send the ring before receiving payment and make sure the payment has cleared before proceeding.

Where to sell my wedding ring after a divorce? Is it OK to sell a wedding ring after divorce?

Many people sell their wedding rings after a divorce. If you decide to do so, you can sell your wedding ring on sites like Worthy, Facebook, eBay, and more. Before you sell your engagement ring, though, you should make sure that the ring is legally yours (check your divorce agreement).

How long does it take to sell an engagement ring?

The amount of time that it takes you to sell an engagement ring depends on where you are selling it. For example, selling a ring on Worthy will take around 2 weeks (it takes a little longer to sell on Worthy, but you may get the best price for your diamond jewelry this way because they have many diamond buyers). Whereas, selling it to a pawn shop may mean that you get paid the same day (however, it’s typically for a lot less money).

What is the best way to sell an engagement ring?

The best way to sell your engagement ring depends on what you’re looking for and there is no one best answer for everyone. Do you want to sell your ring for the most money? Or, do you want to sell your engagement ring as fast as you can? Some people may want to just sell the ring to a pawn shop and get it over with. Others may want to take their time and sell it online so that they can get the most money.

How To Sell An Engagement Ring For The Most Money

I hope you enjoyed this article on how to sell your engagement ring for the most money.

Deciding to sell an engagement ring is a big decision to make as you may have an emotional connection to it. Due to this, you should take your time deciding what to do and choose the option that feels best for your situation.

Some of the best places to sell diamond rings include online (such as through Worthy or eBay), or in-person at a consignment shop or to a local jeweler. Many of the places above can be used for selling other pieces of jewelry as well, such as fine jewelry, bracelets, necklaces, earrings, and more.

Each place has its pros and cons. Some will pay you a lot more than others, but some may be much easier and quicker.

I hope you can find the best place to sell your engagement ring and that you get the most money!

Have you tried selling an engagement ring? What do you think is the best place to sell an engagement ring?

Good credit requires responsible financial management over a period of time. However, there are some tactics you can try that help build your credit as fast as possible, if not exactly overnight. Find out more about these tips below.

In This Piece

Add Rent and Utility Payments

Your credit report and score are meant to help demonstrate whether you can manage money responsibly. But not every bill you manage gets reported to the credit bureaus.

Most landlords don’t send payment information to the credit bureaus, for example. And utility providers usually only report when you’ve defaulted on a bill. If you’re looking for how to increase your credit score quickly, getting these timely payments added to your report can be a good idea.

ExtraCredit lets you link rent and utility payments as trade lines to be reported to the credit bureaus. You can access this perk via the service’s Build It function to establish your credit by increasing your history of timely payments.

Pay Down Debt

Paying down debt is potentially one of the best things you can do for your credit. That’s because when you pay down revolving credit, you reduce your credit utilization, which has a big impact on your credit score.

It’s also helpful to pay down debt if you’ve fallen behind or have collection accounts on your credit report. Catching up past-due accounts and keeping up with them reflects positively on your score and can help you boost your credit.

Keep Utilization Low

Revolving credit includes credit cards, lines of credit and home equity lines of credit. Your credit utilization is a ratio of your total revolving credit balance compared to your total revolving credit limit.

For example, imagine you have two revolving credit accounts:

A credit card with a credit limit of $5,000 and a balance of $2,000

A line of credit with a limit of $5,000 and a balance of $1,000

You would have a total credit limit of $10,000 and a total balance of $3,000. That’s a credit utilization of 30%.

Credit utilization accounts for around 30% of your credit score. Keeping your credit utilization as low as possible—ideally below 30%—helps positively impact your scores.

Pay Bills on Time

Always pay all your bills on time. This is less a tip for boosting your credit overnight and more a tip on how not to wreck your credit overnight. One or two slips that lead to you paying bills 30 days or more past due can drastically and negatively impact your credit score.

Get a Secured Credit Card

A secured credit card is a card designed to help those with fair, poor, or bad credit build credit for the future. Getting one can help you boost your score.

Getting a credit card—and using it responsibly—can be a great way to boost your credit without actually going into debt. It might seem like a contradiction, but remember that a credit card doesn’t automatically mean debt. If you pay your balance off each month, you’re never in debt.

But you do still get some of the potential credit-boosting benefits of holding a credit card. The first is that your credit mix may be improved. Creditors like to see that you can manage multiple types of credit, and your credit score benefits when you have both installment and revolving credit.

Having a credit card also lets you address your credit utilization. If you have a credit card and you pay off the balance every month, you’ll have a lower credit utilization with a responsible payment history, which is good for your credit.

Get a Credit Builder Loan

If you already have a credit card, your credit mix might be suffering from the lack of an installment loan. Any type of installment loan—from a car loan to a personal loan—might benefit your credit score if you make your payments regularly and on time.

But for those who don’t have the credit history or score for a traditional installment loan, a savings-secured or credit-builder loan might be a good option. These loans often require deposits or savings accounts that you get back when you’re done paying for the loan, so they’re not loans designed specifically to provide for a financial need. They’re for the purpose of getting an installment loan and positive payment history on your report.

Become an Authorized User

If you don’t feel ready for your own credit card or can’t qualify for one, see if a family member will add you as an authorized user to their credit card account. Many banks and issuers report account activity to both the cardholder’s and authorized user’s credit report.

You do need to make sure you consider this option carefully. First, make sure the person you ask is responsible with their bills. If they pay their credit card bill late, you could end up with negative marks on your report.

Second, make sure the credit card company reports on authorized users. If the information doesn’t get added to your credit report, it can’t have an impact on your credit score.

Dispute Errors on Your Credit Report

Inaccurate items, such as a late payment reported when you never missed a payment, could unfairly bring your score down. Reviewing your reports and challenging errors may help improve your score. You can get a free credit report from each of the three bureaus every year at AnnualCreditReport.com. These are also available weekly for a limited time due to COVID-19.

In addition to rent and utility reporting, ExtraCredit shows you 28 of your FICO® scores and your credit reports from all three credit bureaus. You can check what’s showing up on your reports and what’s affecting your credit scores so you can follow up as necessary.

If you do find an error on your credit report during your investigation, be sure to challenge the accuracy of the error. Under law, you have a right to a credit report that’s fair and free of errors, so if information can’t be proved by the reporter, the credit bureaus may have to remove it.

Set Up Credit Monitoring Account

Invest in credit monitoring to take a proactive approach to protecting your score. By understanding exactly what’s going on with your report, you can address errors quickly and learn how your own actions impact your score. That helps you make potentially score-boosting decisions in the future.

Credit.com’s free Credit Report Card provides a snapshot of your credit report, with information about how you’re doing in the five critical areas for your score. Knowing how you’re doing can help you pinpoint areas that might need some help.

Don’t Close Accounts

This is another tip to keep from dragging down your credit score almost overnight. Keep credit cards and other revolving accounts open if you can, even if you aren’t using them. They can help reduce your credit utilization and increase your credit age, both of which are good for your score.

How Is Credit Score Calculated?

Understanding how your credit score is calculated helps you make good decisions that can boost your score. Credit scores are based on five factors:

Payment history, which is whether you pay your bills on time regularly

Credit utilization, which is how much of your open credit you’ve used

Credit age, which is the average age of your open accounts as well as how long you’ve had credit