The VA home loan: Unbeatable benefits for veterans

For many who qualify, VA home loans are some of the best mortgages available.

Verify your VA loan eligibility. Start here

Backed by the U.S. Department of Veterans Affairs, VA loans are designed to help active-duty military personnel, veterans and certain other groups become homeowners at an affordable cost.

The VA loan asks for no down payment, requires no mortgage insurance, and has lenient rules about qualifying, among many other advantages.

Here’s everything you need to know about qualifying for and using a VA loan.

In this article (Skip to…)

Top 10 VA loan benefits

1. No down payment on a VA loan

Most home loan programs require you to make at least a small down payment to buy a home. The VA home loan is an exception.

Verify your VA loan eligibility. Start here

Rather than paying 5%, 10%, 20% or more of the home’s purchase price upfront in cash, with a VA loan you can finance up to 100% of the purchase price.

The VA loan is a true no-money-down home mortgage opportunity.

2. No mortgage insurance for VA loans

Typically, lenders require you to pay for mortgage insurance if you make a down payment that’s less than 20%.

This insurance — which is known as private mortgage insurance (PMI) for a conventional loan and a mortgage insurance premium (MIP) for an FHA loan — would protect the lender if you defaulted on your loan.

VA loans require neither a down payment nor mortgage insurance. That makes a VA-backed mortgage very affordable upfront and over time.

3. VA loans have a government guarantee

There’s a reason why the VA loan comes with such favorable terms.

The federal government guarantees these loans — meaning a portion of the loan amount will be repaid to the lender even if you’re unable to make monthly payments for whatever reason.

This guarantee encourages and enables private lenders to offer VA loans with exceptionally attractive terms.

4. You can shop for the best VA loan rates

VA loans are neither originated nor funded by the VA. They are not direct loans from the government. Furthermore, mortgage rates for VA loans are not set by the VA itself.

Instead, VA loans are offered by U.S. banks, savings-and-loans institutions, credit unions, and mortgage lenders — each of which sets its own VA loan rates and fees.

This means you can shop around and compare loan offers and still choose the VA loan that works best for your budget.

5. VA loans don’t allow a prepayment penalty

A VA loan won’t restrict your right to sell the property partway through your loan term.

There’s no prepayment penalty or early-exit fee no matter within what time frame you decide to sell your home.

Furthermore, there are no restrictions regarding a refinance of your VA loan.

You can refinance your existing VA loan into another VA loan via the agency’s Interest Rate Reduction Refinance Loan (IRRRL) program, or switch into a non-VA loan at any time.

6. VA mortgages come in many varieties

A VA loan can have a fixed rate or an adjustable rate. In addition, you can use a VA loan to buy a house, condo, new-built home, manufactured home, duplex, or other types of properties.

Or, it can be used for refinancing your existing mortgage, making repairs or improvements to your home, or making your home more energy-efficient.

The choice is yours. A VA-approved lender can help you decide.

Verify your VA loan eligibility. Start here

7. It’s easier to qualify for VA loans

Like all mortgage types, VA loans require specific documentation, an acceptable credit history, and sufficient income to make your monthly payments.

But, compared to other loan programs, VA loan guidelines tend to be more flexible. This is made possible because of the VA loan guarantee.

The Department of Veterans Affairs genuinely wants to make the loan process easier for military members, veterans, and qualifying military spouses to buy or refinance a home.

8. VA loan closing costs are lower

The VA limits the closing costs lenders can charge to VA loan applicants. This is another way that a VA loan can be more affordable than other types of loans.

Money saved on closing costs can be used for furniture, moving costs, home improvements, or anything else.

9. The VA offers funding fee flexibility

VA loans require a “funding fee,” an upfront cost based on your loan amount, your type of eligible service, your down payment size, and other factors.

Funding fees don’t need to be paid in cash, though. The VA allows the fee to be financed with the loan, so nothing is due at closing.

And, not all VA borrowers will pay it. VA funding fees are normally waived for veterans who receive VA disability compensation and for unmarried surviving spouses of veterans who died in service or as a result of a service-connected disability.

10. VA loans are assumable

Most VA loans are “assumable,” which means you can transfer your VA loan to a future home buyer if that person is also VA-eligible.

Assumable loans can be a huge benefit when you sell your home — especially in a rising mortgage rate environment.

If your home loan has today’s low rate and market rates rise in the future, the assumption features of your VA become even more valuable.

VA loan rates

The VA loan is viewed as one of the lowest-risk mortgage types available on the market.

Verify your VA loan eligibility. Start here

This safety allows banks to lend to veteran borrowers at lower interest rates.

Today’s VA loan rates*

Loan Type

Current Mortgage Rate

VA 30-year FRM

% (% APR)

Conventional 30-year FRM

% (% APR)

VA 15-year FRM

% (% APR)

Conventional 15-year FRM

% (% APR)

*Current rates provided daily by partners of the Mortgage Reports. See our loan assumptions here.

VA rates are more than 25 basis points (0.25%) lower than conventional rates on average, according to data collected by mortgage software company Ellie Mae.

Most loan programs require higher down payment and credit scores than the VA home loan. In the open market, a VA loan should carry a higher rate due to more lenient lending guidelines and higher perceived risk.

Yet the result of the Veterans Affairs efforts to keep veterans in their homes means lower risk for banks and lower borrowing costs for eligible veterans.

VA mortgage calculator

Eligibility

Am I eligible for a VA home loan?

Contrary to popular belief, VA loans are available not only to veterans, but also to other classes of military members.

Find and lock a low VA loan rate today. Start here

The list of eligible VA borrowers includes:

Active-duty service members

Members of the National Guard

Reservists

Surviving spouses of veterans

Cadets at the U.S. Military, Air Force or Coast Guard Academy

Midshipmen at the U.S. Naval Academy

Officers at the National Oceanic & Atmospheric Administration.

A minimum term of service is typically required.

Minimum service required for a VA mortgage

VA home loans are available to active-duty service members, veterans (unless dishonorably discharged), and in some cases, surviving family members.

To be eligible, you need to meet one of these service requirements:

You’ve served 181 days of active duty during peacetime

You’ve served 90 days of active duty during wartime

You’ve served six years in the Reserves or National Guard

Your spouse was killed in the line of duty and you have not remarried

Your eligibility for the VA home loan program never expires.

Veterans who earned their VA entitlement long ago are still using their benefit to buy homes.

The VA loan Certificate of Eligibility (COE)

What is a COE?

In order to show a mortgage company you are VA-eligible, you’ll need a Certificate of Eligibility (COE). Your lender can acquire one for you online, usually in a matter of seconds.

Verify your VA home loan eligibility. Start here

How to get your COE (Certificate of Eligibility)

Getting a Certificate of Eligibility (COE) is very easy in most cases. Simply have your lender order the COE through the VA’s automated system. Any VA-approved lender can do this.

Alternatively, you can order your certificate yourself through the VA benefits portal.

If the online system is unable to issue your COE, you’ll need to provide your DD-214 form to your lender or the VA.

Does a COE mean you are guaranteed a VA loan?

No, having a Certificate of Eligibility (COE) doesn’t guarantee a VA loan approval.

Your COE shows the lender you’re eligible for a VA loan, but no one is guaranteed VA loan approval.

You must still qualify for the loan based on VA mortgage guidelines. The guarantee part of the VA loan refers to the VA’s promise to the lender of repayment if the borrower defaults.

Qualifying for a VA mortgage

VA loan eligibility vs. qualification

Being eligible for VA home loan benefits based on your military status or affiliation doesn’t necessarily mean you’ll qualify for a VA loan.

You still have to qualify for a VA mortgage based on your credit, debt, and income.

Verify your VA loan eligibility. Start here

Minimum credit score for a VA loan

The VA has established no minimum credit score for a VA mortgage.

However, many VA mortgage lenders require minimum FICO scores of 620 or higher — so apply with many lenders if your credit score might be an issue.

Even VA lenders that allow lower credit scores don’t accept subprime credit.

VA underwriting guidelines state that applicants must have paid their obligations on time for at least the most recent 12 months to be considered satisfactory credit risks.

In addition, the VA usually requires a two-year waiting period following a Chapter 7 bankruptcy or foreclosure before it will insure a loan.

Borrowers in Chapter 13 must have made at least 12 on-time payments and secure the approval of the bankruptcy court.

Verify your VA loan home buying eligibility. Start here

VA loan debt-to-income ratios

The relationship of your debts and your income is called your debt-to-income ratio, or DTI.

VA underwriters divide your monthly debts (car payments, credit cards, and other accounts, plus your proposed housing expense) by your gross (before-tax) income to come up with your debt-to-income ratio.

For instance:

If your gross income is $4,000 per month

And your total monthly debt is $1,500 (including the new mortgage, property taxes and homeowners insurance, plus other debt payments)

Then your DTI is 37.5% (1500/4000=0.375)

A DTI over 41% means the lender has to apply additional formulas to see if you qualify under residual income guidelines.

VA residual income rules

VA underwriters perform additional calculations that can affect your mortgage approval.

Factoring in your estimated monthly utilities, your estimated taxes on income, and the area of the country in which you live, the VA arrives at a figure which represents your “true” costs of living.

It then subtracts that figure from your income to find your residual income (e.g. your money “left over” each month).

Think of the residual income calculation as a real-world simulation of your living expenses.

It is the VA’s best effort to ensure that military families have a stress-free homeownership experience.

Here is an example of how residual income works, assuming a family of four which is purchasing a 2,000 square-foot home on a $5,000 monthly income.

Future house payment, plus other debt payments: $2,500

Monthly estimated income taxes: $1,000

Monthly estimated utilities at $0.14 per square foot: $280

This leaves a residual income calculation of $1,220.

Now, compare that residual income to for a family of four:

Northeast Region: $1,025

Midwest Region: $1,003

South Region: $1,003

West Region: $1,117

The borrower in our example exceeds VA’s residual income standards in all parts of the country.

Therefore, despite the borrower’s debt-to-income ratio of 50%, the borrower could get approved for a VA loan.

Verify your VA loan eligibility. Start here

Qualifying for a VA loan with part-time income

You can qualify for this type of financing even if you have a part-time job or multiple jobs.

You must show a 2-year history of making consistent part-time income, and stability in the number of hours worked. The lender will make sure any income received appears stable. See our complete guide to getting a mortgage when you’re self-employed or work part-time.

VA funding fees and loan limits

About the VA funding fee

The VA charges an upfront fee to defray the costs of the program and make it sustainable for the future.

Veterans pay a lump sum that varies depending on the loan purpose and down payment amount.

The fee is normally wrapped into the loan. It does not add to the cash needed to close the loan.

Find out if you qualify for a VA loan. Start here

VA home purchase funding fees

Type of Military Service

Down Payment

Fee for First-Time Use

Fee for Subsequent Use

Active Duty, Reserves, and National Guard

None

2.3%

3.6%

5% or more

1.65%

1.65%

10% or more

1.4%

1.4%

VA cash-out refinance funding fees

Type of Military Service

Fee for First-Time Use

Fee for Subsequent Uses

Active Duty, Reserves, and National Guard

2.3%

3.6%

VA streamline refinances (IRRRL) & assumptions

Type of Military Service

Fee for First-Time Use

Fee for Subsequent Uses

Active Duty, Reserves, and National Guard

0.5%

0.5%

Manufactured home loans not permanently affixed

Type of Military Service

Fee for First-Time Use

Fee for Subsequent Uses

Active Duty, Reserves, and National Guard

1.0%

1.0%

VA loan limits in 2024

VA loan limits have been repealed, thanks to the Blue Water Navy Vietnam Veterans Act of 2019.

There is no maximum amount for which a home buyer can receive a VA loan, at least as far as the VA is concerned.

However, private lenders may set their own limits. So check with your lender if you are looking for a VA loan above local conforming loan limits.

Verify your VA loan eligibility. Start here

Eligible property types

Houses you can buy with a VA loan

VA mortgages are flexible about what types of property you can and can’t purchase. A VA loan can be used to buy a:

Detached house

Condo

New-built home

Manufactured home

Duplex, triplex or four-unit property

Find out if you qualify for a VA loan. Start here

You can also use a VA mortgage to refinance an existing loan for any of those types of properties.

VA loans and second homes

Federal regulations limit loans guaranteed by the Department of Veterans Affairs to “primary residences” only.

However, “primary residence” is defined as the home in which you live “most of the year.”

Therefore, if you own an out-of-state residence in which you live for more than six months of the year, this other home, whether it’s your vacation home or retirement property, becomes your official “primary residence.”

For this reason, VA loans are popular among aging military borrowers.

Buying a multi-unit home with a VA loan

VA loans allow you to buy a duplex, triplex, or four-plex with 100% financing. You must live in one of the units.

Buying a home with more than one unit can be challenging.

Mortgage lenders consider these properties riskier to finance than traditional, single-family residences, so you’ll need to be a stronger borrower.

VA underwriters must make sure you will have enough emergency savings, or cash reserves, after closing on your house. That’s to ensure you’ll have money to pay your mortgage even if a tenant fails to pay rent or moves out.

The minimum cash reserves needed after closing is six months of mortgage payments (covering principal, interest, taxes, and insurance – PITI).

Your lender will also want to know about previous landlord experience you’ve had, or any experience with property maintenance or renting.

If you don’t have any, you may be able to sidestep that issue by hiring a property management company. But that’s up to the individual lender.

Your lender will look at the income (or potential income) of the rental units, using either existing rental agreements or an appraiser’s opinion of what the units should fetch.

They’ll usually take 75% of that amount to offset your mortgage payment when calculating your monthly expenses.

VA loans and rental properties

You cannot use a VA loan to buy a rental property. You can, however, use a VA loan to refinance an existing rental home you once occupied as a primary home.

For home purchases, in order to obtain a VA loan, you must certify that you intend to occupy the home as your principal residence.

If the property is a duplex, triplex, or four-unit apartment building, you must occupy one of the units yourself. Then you can rent out the other units.

The exception to this rule is the VA’s Interest Rate Reduction Refinance Loan (IRRRL).

This loan, also known as the VA Streamline Refinance, can be used for refinancing an existing VA loan on a home where you currently live or where you used to live, but no longer do.

Check your VA IRRRL eligibility. Start here

Buying a condo with a VA loan

The VA maintains a list of approved condo projects within which you may purchase a unit with a VA loan.

At VA’s website, you can search for the thousands of approved condominium complexes across the U.S.

If you are VA-eligible and in the market for a condo, make sure the unit you’re interested in is approved.

As a buyer, you are probably not able to get the complex VA-approved. That’s up to the management company or homeowner’s association.

If a condo you like is not approved, you must use other financing like an FHA or conventional loan or find another property.

Note that the condo must meet FHA or conventional guidelines if you want to use those types of financing.

Veteran mortgage relief with the VA loan

The U.S. Department of Veterans Affairs, or VA, provides home retention assistance. The VA intervenes when a veteran is having trouble making home loan payments.

The VA works with loan servicers to offer loan options to the veteran, other than foreclosure.

Find out if you qualify for a VA loan. Start here

In fiscal year 2019, the VA made over 400,000 contact actions to reach borrowers and loan servicers. The intent was to work out a mutually agreeable repayment option for both parties.

More than 100,000 veteran homeowners avoided foreclosure in 2019 alone thanks to this effort.

The initiative has saved the taxpayer an estimated $2.6 billion. More importantly, vast numbers of veterans and military families got another chance at homeownership.

When NOT to use a VA loan

If you have good credit and 20% down

A primary advantage to VA home loans is the lack of mortgage insurance.

However, the VA guarantee does not come free of charge. Borrowers pay an upfront funding fee, which they usually choose to add to their loan amount.

The fee ranges from 1.4% to 3.6%, depending on the down payment percentage and whether the home buyer has previously used his or her VA mortgage eligibility. The most common fee is 2.3%.

Find out if you qualify for a VA loan. Start here

On a $200,000 purchase, a 2.3% fee equals $4,600.

However, buyers who choose a conventional mortgage and put 20% down get to avoid mortgage insurance and the upfront fee. For these military home buyers, the VA funding fee might be an unnecessary expense.

The exception: Mortgage applicants whose credit rating or income meets VA guidelines but not those of conventional mortgages may still opt for VA.

If you’re on the “CAIVRS” list

To qualify for a VA loan, you must prove you have made good on previous government-backed debts and that you have paid taxes.

The Credit Alert Verification Reporting System, or “CAIVRS,” is a database of consumers who have defaulted on government obligations. These individuals are not eligible for the VA home loan program.

If you have a non-veteran co-borrower

Veterans often apply to buy a home with a non-veteran who is not their spouse.

This is okay. However, it might not be their best choice.

As the veteran, your income must cover your half of the loan payment. The non-veteran’s income cannot be used to compensate for the veteran’s insufficient income.

Plus, when a non-veteran owns half the loan, the VA guarantees only half that amount. The lender will require a 12.5% down payment for the non-guaranteed portion.

The Conventional 97 mortgage, on the other hand, allows down payments as low as 3%.

Another low-down-payment mortgage option is the FHA home loan, for which 3.5% down is acceptable.

The USDA home loan also requires zero down payment and offers similar rates to VA loans. However, the property must be within USDA-eligible areas.

If you plan to borrow with a non-veteran, one of these loan types might be your better choice.

Explore your mortgage options. Start here

If you apply with a credit-challenged spouse

In states with community property laws, VA lenders must consider the credit rating and financial obligations of your spouse. This rule applies even if he or she will not be on the home’s title or even on the mortgage.

Such states are as follows.

Arizona

California

Idaho

Louisiana

Nevada

New Mexico

Texas

Washington

Wisconsin

A spouse with less-than-perfect credit or who owes alimony, child support, or other maintenance can make your VA approval more challenging.

Apply for a conventional loan if you qualify for the mortgage by yourself. The spouse’s financial history and status need not be considered if he or she is not on the loan application.

Verify your VA loan home buying eligibility. Start here

If you want to buy a vacation home or investment property

The purpose of VA financing is to help veterans and active-duty service members buy and live in their own home. This loan is not meant to build real estate portfolios.

These loans are for primary residences only, so if you want a ski cabin or rental, you’ll have to get a conventional loan.

If you want to purchase a high-end home

Starting January 2020, there are no limits to the size of mortgage a lender can approve.

However, lenders may establish their own limits for VA loans, so check with your lender before applying for a large VA loan.

Spouses and the VA mortgage program

What spouses are eligible for a VA loan?

What if the service member passes away before he or she uses the benefit? Eligibility passes to an unremarried spouse, in many cases.

Find and lock a low VA loan rate today. Start here

For the surviving spouse to be eligible, the deceased service member must have:

Died in the line of duty

Passed away as a result of a service-connected disability

Been missing in action, or a prisoner of war, for at least 90 days

Been a totally disabled veteran for at least 10 years prior to death, and died from any cause

Also eligible are remarried spouses who married after the age of 57, on or after December 16, 2003.

In these cases, the surviving spouse can use VA loan eligibility to buy a home with zero down payment, just as the veteran would have.

VA loan benefits for surviving spouses

Surviving spouses have an additional VA loan benefit, however. They are exempt from the VA funding fee. As a result, their loan balance and monthly payment will be lower.

Surviving spouses are also eligible for a VA streamline refinance when they meet the following guidelines.

The surviving spouse was married to the veteran at the time of death

The surviving spouse was on the original VA loan

VA streamline refinancing is typically not available when the deceased veteran was the only applicant on the original VA loan, even if he or she got married after buying the home.

In this case, the surviving spouse would need to qualify for a non-VA refinance, or a VA cash-out loan.

A cash-out mortgage through VA requires the military spouse to meet home purchase eligibility requirements.

If this is the case, the surviving spouse can tap into the home’s equity to raise cash for any purpose, or even pay off an FHA or conventional loan to eliminate mortgage insurance.

Qualifying if you receive (or pay) child support or alimony

Buying a home after a divorce is no easy task.

If, prior to your divorce, you lived in a two-income household, you now have less spending power and a reduced monthly income for purposes of your VA home loan application.

With less income, it can be harder to meet both the VA Home Loan Guaranty’s debt-to-income (DTI) guidelines and the VA residual income requirement for your area.

Receiving alimony or child support can counteract a loss of income.

Mortgage lenders will not require you to provide information about your divorce agreement’s alimony or child support terms, but if you’re willing to disclose, it can count toward qualifying for a home loan.

Different VA-approved lenders will treat alimony and child support income differently.

Typically, you will be asked to provide a copy of your divorce settlement or other court paperwork to support the alimony and child support payments.

Lenders will then want to see that the payments are stable, reliable, and likely to continue for another 36 months, at least.

You may also be asked to show proof that alimony and child support payments have been made in the past reliably, so that the lender may use the income as part of your VA loan application.

If you are the payor of alimony and child support payments, your debt-to-income ratio can be harmed.

Not only might you be losing the second income of your dual-income households, but you’re making additional payments that count against your outflows.

VA mortgage lenders make careful calculations with respect to such payments.

You can still get approved for a VA loan while making such payments — it’s just more difficult to show sufficient monthly income.

VA loan assumption

What is VA loan assumption?

One benefit for home buyers is that VA loans are assumable. When you assume a mortgage loan, you take over the current homeowner’s monthly payment.

Verify your VA loan home buying eligibility. Start here

That could be a big advantage if mortgage rates have risen since the original owner purchased the home. The buyer would be able to acquire a low-rate, affordable loan — and it could make it easier for the seller to find a willing buyer in a tough market.

VA loan assumption savings

Buying a home via an assumable mortgage loan is even more appealing when interest rates are on the rise.

For example:

Say a seller-financed $200,000 for their home in 2013 at an interest rate of 3.25% on a 30-year fixed loan

Using this scenario, their principal and interest payment would be $898 per month

Let’s assume current 30-year fixed rates averaged 4.10%

If you financed $200,000 at 4.10% for a 30-year loan term, your monthly principal and interest payment would be $966 per month

Additionally, because the seller has already paid four years into the loan term, they’ve already paid nearly $25,000 in interest on the loan.

By assuming the loan, you would save $34,560 over the 30-year loan due to the difference in interest rates. You would also save roughly $25,000 thanks to the interest already paid by the sellers.

That comes out to a total savings of almost $60,000!

How to assume (take on) a VA loan

There are currently two ways to assume a VA loan.

The new buyer is a qualified veteran who “substitutes” his or her VA eligibility for the eligibility of the seller

The new home buyer qualifies through VA standards for the mortgage payment. This is the safest method for the seller as it allows the loan to be assumed knowing that the new buyer is responsible for the loan, and the seller is no longer responsible for the loan

The lender and/or the VA needs to approve a loan assumption.

Loans serviced by a lender with automatic authority may process assumptions without sending them to a VA Regional Loan Center.

For lenders without automatic authority, the loan must be sent to the appropriate VA Regional Loan Center for approval. This loan process will typically take several weeks.

When VA loans are assumed, it’s the servicer’s responsibility to make sure the homeowner who assumes the property meets both VA and lender requirements.

VA loan assumption requirements

For a VA mortgage assumption to take place, the following conditions must be met:

The existing loan must be current. If not, any past due amounts must be paid at or before closing

The buyer must qualify based on VA credit and income standards

The buyer must assume all mortgage obligations, including repayment to the VA if the loan goes into default

The original owner or new owner must pay a funding fee of 0.5% of the existing principal loan balance

A processing fee must be paid in advance, including a reasonable estimate for the cost of the credit report

Find out if you qualify for a VA loan. Start here

Finding assumable VA loans

There are several ways for home buyers to find an assumable VA loan.

Believe it or not, print media is still alive and well. Some home sellers advertise their assumable home for sale in the newspaper, or in a local real estate publication.

There are a number of online resources for finding assumable mortgage loans.

Websites like TakeList.com and Zumption.com give homeowners a way to showcase their properties to home buyers looking to assume a loan.

With the help of the Multiple Listing Service (MLS), real estate agents remain a great resource for home buyers.

This applies to home buyers specifically searching for assumable VA loans as well.

How do I apply for a VA loan?

You can easily and quickly have a lender pull your certificate of eligibility (COE) to make sure you’re able to get a VA loan.

Most mortgage lenders offer VA home loans. So you’re free to shop and compare rates with just about any company that catches your eye.

Getting a VA loan for your new home is similar in many ways to securing any other purchase loan. Once you find an ideal home in your price range, you make a purchase offer, and then undergo VA appraisal and underwriting.

VA appraisal ensures that the home meets its minimum property requirements (MPRs) and is structurally sound and safe for occupancy.

What’s more, VA-specific mortgage lenders are actually some of the highest-rated (and lowest-priced) on the market. Here are a few we’d recommend checking out.

Time to make a move? Let us find the right mortgage for you

Portions of this article were drafted using an in-house natural language generation platform. The article was reviewed, fact-checked and edited by our editorial staff.

Key takeaways

Fannie Mae and Freddie Mac are government-sponsored enterprises that aim to provide the mortgage market with stability and affordability.

They are major players in the secondary mortgage market, buying loans from lenders and either keeping them or repackaging them as mortgage-backed securities.

Fannie Mae and Freddie Mac were both created by Congress but have different intended purposes and loan-sourcing methods.

As you explore your mortgage options, you’re likely to come across two names: Fannie Mae and Freddie Mac. Although you won’t directly get a home loan through these government-sponsored enterprises (GSEs) — private entities operating under a Congressional charter — they nonetheless have an impact on your getting a mortgage and its terms. Let’s take a closer look at these key players in the mortgage industry, and what distinguishes them.

What are Fannie Mae and Freddie Mac?

Fannie Mae and Freddie Mac are government-sponsored enterprises. Congress created both with the goal of adding stability and affordability to the country’s mortgage market. They also provide banks and mortgage companies with ready access to funds on reasonable terms, adding liquidity to the mortgage market.

Both agencies are major players in the secondary mortgage market. That is, their focus is buying loans from mortgage lenders, giving those institutions more capital to continue offering financing to other borrowers. Fannie Mae and Freddie Mac then either keep them or, more often, repackage them as mortgage-backed securities that can be sold to investors.

By acting as a market-maker — that is, constant buyer — they ensure liquidity in the lending world. As of 2023, Fannie Mae and Freddie Mac support around 70 percent of the mortgage market, according to the National Association of Realtors. That means the majority of conventional loans, those offered by private lenders, end up being backed or purchased by one of the two entities.

Though they set criteria for loans, neither Fannie Mae nor Freddie Mac originate or directly provide mortgages to homebuyers. Instead, you’ll get your loan from a mortgage lender, such as a bank, credit union or online lender, which can then choose to sell the loan to one of these GSEs, assuming the loan’s eligible.

Differences between Fannie Mae and Freddie Mac

While they may seem incredibly similar, Fannie Mae and Freddie Mac have some key differences. Here’s a closer look at what differentiates Freddie Mac from Fannie Mae.

Intended purpose

Fannie Mae was established with the intended purpose of creating a more reliable source of accessible funding for banks and mortgage companies. This, in turn, opened the door to more widely accessible and affordable mortgages for Americans seeking to become homeowners. Congress created Freddie Mac, on the other hand, with the goal of expanding the secondary mortgage market, buying loans that meet its standards from lenders. This function allows lenders to make more loans available to prospective buyers.

Loan sourcing

Although both do buy mortgages, each GSE purchases loans from different sources. In general, Fannie Mae tends to buy loans from larger commercial banks and mortgage lenders, whereas Freddie Mac often buys loans from smaller banks.

Lending requirements

Fannie Mae and Freddie Mac also have slightly different requirements for the mortgages they purchase. In both cases, Fannie and Freddie loans must be conforming loans, or adhere to these standards, for them to be eligible for purchase. The requirements cover the amount of the home purchase price that can be financed, the borrower’s credit score and debt-to-income (DTI) ratio, loan-to-value (LTV) ratio and other factors.

Loan programs

Fannie and Freddie each sponsor different loan programs — mortgage products that expand homeownership opportunities to buyers who may not be able to afford a conventional down payment. These include HFA loans offered through state housing finance agencies, as well as the HomeReady and HomePossible mortgage programs, offered through approved private lenders. Both empower buyers by requiring only a 3 percent down payment.

Similarities between Fannie Mae and Freddie Mac

Now that we’ve covered their differences, let’s touch on how Fannie Mae and Freddie Mac are similar.

Their creation and structure

Both Fannie Mae and Freddie Mac were created by Congress to address issues in the housing market. They exist as publicly-traded corporations that are under the conservatorship of the government.

Buy and sell mortgages

Fannie Mae and Freddie Mac buy loans from lenders and repackage them into mortgage-backed securities. This benefits the mortgage market in a couple of ways. First, it lowers the risk of default for lenders since they don’t have to keep these loans on their books. Plus, selling mortgage-backed securities to investors creates stability in the secondary mortgage market, further lowering risk and leading to lower interest for borrowers.

Increase loan availability

Because Fannie and Freddie buy loans from lenders, this increases the amount of money lenders can loan out. Once they close a loan and sell it to Fannie or Freddie, lenders can re-lend that cash.

Standardize loans

Fannie Mae and Freddie Mac only buy loans that conform to the FHFA’s standards. That means they must be under a certain loan limit and borrowers must meet specific financial requirements. Lenders have adopted these standards for most conventional conforming loans so they can sell their mortgages to Fannie and Freddie.

Fannie Mae and Freddie Mac history

In 1938, the government created Fannie Mae, or the Federal National Mortgage Association, amid the struggles of the Great Depression. The goal of Fannie Mae was to create a more reliable source of funding for banks, opening doors for more Americans to become homeowners, figuratively and literally.

Freddie Mac, short for the Federal Home Loan Mortgage Corporation, came on the scene through an act of Congress in 1970, with a similar purpose of ensuring that there are reliable, affordable mortgage funds available nationwide.

Since 2008, both Fannie Mae and Freddie Mac have operated under the conservatorship of the Federal Housing Finance Agency (FHFA). Though both are currently under a conservatorship of the same agency, the two entities are separate from one another, each with its own shareholders and leadership.

Fannie and Freddie in the 21st century

Both Fannie and Freddie played a role in the Great Recession. In the years leading up to the housing market collapse, they backed or owned numerous subprime mortgages. When the housing bubble burst, economic pressures and large losses led to the need for the government to step in and help them with bailouts. The two agencies took on more debt but, as a result of their losses, they risked becoming insolvent, and were put under FHFA conservatorship. They’ve since paid back most of the bailout money.

During the COVID-19 pandemic, Fannie Mae and Freddie Mac offered mortgage relief and protections to homeowners, including forbearance, loan modification programs and a moratorium on foreclosures and evictions.

Who regulates Fannie Mae and Freddie Mac?

Fannie Mae and Freddie Mac are regulated by two government agencies: the FHFA and the U.S. Department of Housing and Urban Development (HUD). Along with HUD and FHFA oversight, the President of the United States appoints five of the 18 board members at each entity. Further details of the regulation for Fannie Mae and Freddie Mac are laid out in two government acts: The Federal Nation Mortgage Association Charter Act and the Federal Home Loan Mortgage Corporation Corporation Act.

What this means for you

Since you can’t take out a mortgage directly from Fannie Mae or Freddie Mac, why should you care about these big names in the mortgage market? In addition to keeping the mortgage market humming and making homeownership more accessible overall, here’s how they can affect you:

They create more affordable financing options, including lower-down payment loan programs.

They foster competition among lenders, leading to lower rates.

They help set borrowing standards, influencing the qualifications you need to meet to obtain a mortgage.

To find out if you have a Fannie Mae- or Freddie Mac-backed loan:

Both a loan modification and a loan refinance can lower your monthly payments and help you save money. However, they are not the same thing. Depending on your circumstances, one strategy will make more sense than the other.

If you’re behind on your mortgage payments due to a financial hardship, for example, you might seek out a loan modification. A modification alters the terms of your current loan and can help you avoid default or foreclosure.

If, on the other hand, you’re up to date on your loan payments and looking to save money, you might opt to refinance. This involves taking out a new loan (ideally with better rates and terms) and using it to pay off your existing loan.

Here’s a closer look at loan modification vs. refinance, how each lending option works, and when to choose one or the other.

What Is a Loan Modification?

A loan modification changes the terms of a loan to make the monthly payments more affordable. It’s a strategy that most commonly comes into play with mortgages. A home loan modification is a change in the way the home mortgage loan is structured, primarily to provide some financial relief for struggling homeowners.

Unlike refinancing a mortgage, which pays off the current home loan and replaces it with a new one, a loan modification changes the terms and conditions of the current home loan. These changes might include:

• A new repayment timetable. A loan modification may extend the term of the loan, allowing the borrower to have more time to pay off the loan.

• A lower interest rate. Loan modifications may allow borrowers to lower the interest rates on an existing loan. A lower interest rate can reduce a borrower’s monthly payment.

• Switching from an adjustable rate to a fixed rate. If you currently have an adjustable-rate loan, a loan modification might allow you to change it to a fixed-rate loan. A fixed-rate loan may be easier to manage, since it offers consistent monthly payments over the life of the loan.

A loan modification can be hard to qualify for, as lenders are under no obligation to change the terms and conditions of a loan, even if the borrower is behind on payments. A lender will typically request documents to show financial hardship, such as hardship letters, bank statements, tax returns, and proof of income.

While loan modifications are most common for secured loans, like home mortgages, it’s also possible to get student loan modifications and even personal loan modifications. 💡 Quick Tip: A low-interest personal loan can consolidate your debts, lower your monthly payments, and help you get out of debt sooner.

What Is Refinancing a Loan?

A loan refinance doesn’t just restructure the terms of an existing loan — it replaces the current loan with a new loan that typically has a different interest rate, a longer or shorter term, or both. You’ll need to apply for a new loan, typically with a new lender. Once approved, you use the new loan to pay off the old loan. Moving forward, you only make payments on the new loan.

Refinancing a loan can make sense if you can:

• Qualify for a lower interest rate. The classic reason to refi any type of loan is to lower your interest rate. With home loans, however, you’ll want to consider fees and closing costs involved in a mortgage refinance, since they can eat into any savings you might get with the lower rate.

• Extend the repayment terms. Having a longer period of time to pay off a loan generally lowers the monthly payment and can relieve a borrower’s financial stress. Just keep in mind that extending the term of a loan generally increases the amount of interest you pay, increasing the total cost of the loan.

• Shorten the loan repayment time. While refinancing a loan to a shorter repayment term may increase the monthly loan payments, it can reduce the overall cost of the loan by allowing you to pay off the debt faster. This can result in a significant cost savings.

Recommended: What Are Personal Loans Used For?

Refinance vs Loan Modification: Pros and Cons

Loan refinance is typically something a borrower chooses to do, whereas loan modification is generally something a borrower needs to do, often as a last resort.

Here’s a look at the pros and cons of each option.

Loan Modification

Refinancing

Pros

Cons

Pros

Cons

Avoid loan default and foreclosure

Could negatively impact credit

May be able to lower interest rate

You’ll need solid credit and income

Lower your monthly payment

Cash out is not an option

May be able to shorten or lengthen your loan term

Closing costs may lower overall savings

Avoid closing costs

Lenders not required to grant modification

May be able to turn home equity into cash

You could reset the clock on your loan

Benefits of Loan Modification

While a loan modification is rarely a borrower’s first choice, it comes with some advantages. Here are a few to consider.

• Avoid default and foreclosure. Getting a loan modification can help you avoid defaulting on your mortgage and potentially losing your home as a result of missing mortgage payments.

• Change the loan’s terms. It may be possible to increase the length of your loan, which would lower your monthly payment. Or, if the original interest rate was variable, you might be able to switch to a fixed rate, which could result in savings over the life of the loan.

• Avoid closing costs. Unlike a loan refinance, a loan modification allows you to keep the same loan. This helps you avoid having to pay closing costs (or other fees) that come with getting a new loan.

Drawbacks of Loan Modification

Since loan modification is generally an effort to prevent foreclosure on the borrower’s home, there are some drawbacks to be aware of.

• It could have a negative effect on your credit. A loan modification on a credit report is typically a negative entry and could lower your credit score. However, having a foreclosure — or even missed payments — can be more detrimental to a person’s overall creditworthiness.

• Tapping home equity for cash is not an option. Unlike refinancing, a loan modification cannot be used to tap home equity for an extra lump sum of cash (called a cash-out refi). If your monthly payments are lower after modification, though, you may have more funds to pay other expenses each month.

• There is a hardship requirement. It’s typically necessary to prove financial hardship to qualify for loan modification. Lenders may want to see that your extenuating financial circumstances are involuntary and that you’ve made an effort to address them, or have a plan to do so, before considering loan modification.

Recommended: Guide to Mortgage Relief Programs

Benefits of Refinancing a Loan

For borrowers with a strong financial foundation, refinancing a mortgage or other type of loan comes with a number of benefits. Here are some to consider.

• You may be able to get a lower interest rate. If your credit and income is strong, you may be able to qualify for an interest rate that is lower than your current loan, which could mean a savings over the life of the loan.

• You may be able to shorten or extend the term of the loan. A shorter loan term can mean higher monthly payments but is likely to result in an overall savings. A longer loan term generally means lower monthly payments, but may increase your costs.

• You may be able to pull cash out of your home. If you opt for a cash-out refinance, you can turn some of your equity in your home into cash that you can use however you want. With this type of refinance, the new loan is for a greater amount than what is owed, the old loan is paid off, and the excess cash can be used for things like home renovations or credit card consolidation. 💡 Quick Tip: If you’ve got high-interest credit card debt, a personal loan is one way to get control of it. But you’ll want to make sure the loan’s interest rate is much lower than the credit cards’ rates — and that you can make the monthly payments.

Drawbacks of Refinancing a Loan

Refinancing a loan also comes with some disadvantages. Here are some to keep in mind.

• You’ll need strong credit and income. Lenders who offer refinancing typically want to see that you are in a solid financial position before they issue you a new loan. If your situation has improved since you originally financed, you could qualify for better rates and terms.

• Closing costs can be steep. When refinancing a mortgage, you typically need to pay closing costs. Before choosing a mortgage refi, you’ll want to look closely at any closing costs a lender charges, and whether those costs are paid in cash or rolled into the new mortgage loan. Consider how quickly you’ll be able to recoup those costs to determine if the refinance is worth it.

• You could set yourself back on loan payoff. When you refinance a loan, you can choose a new loan term. If you’re already five years into a 30-year mortgage and you refinance for a new 30-year loan, for example, you’ll be in debt five years longer than you originally planned. And if you don’t get a lower interest rate, extending your term can increase your costs.

Is It Better to Refinance or Get a Loan Modification?

It all depends on your situation. If you have solid credit and are current on your loan payments, you’ll likely want to choose refinancing over loan modification. To qualify for a refinance, you’ll need to have a loan in good standing and prove that you make enough money to absorb the new payments.

If you’re behind on your loan payments and trying to avoid negative consequences (like loan default or foreclosure on your home), your best option is likely going to be loan modification. Provided the lender is willing, you may be able to change the rate or terms of your loan to make repayment more manageable. This may be more agreeable to a lender than having to take expensive legal action against you.

Recommended: 11 Types of Personal Loans & Their Differences

Alternatives to Refinancing and Loan Modification

If you’re having trouble making your mortgage payments or just looking for a way to save money on a debt, here are some other options to consider besides refinancing and loan modification.

Mortgage Forbearance

For borrowers facing short-term financial challenges, a mortgage forbearance may be an option to consider.

Lenders may grant a term of forbearance — typically three to six months, with the possibility of extending the term — during which the borrower doesn’t make loan payments or makes reduced payments. During that time, the lender also agrees not to pursue foreclosure.

As with a loan modification, proof of hardship is typically required. A lender’s definition of hardship may include divorce, job loss, natural disasters, costs associated with medical emergencies, and more.

During a period of forbearance, interest will continue to accrue, and the borrower will still be responsible for expenses such as homeowners insurance and property taxes.

At the end of the forbearance period, the borrower may have to repay any missed payments in addition to accrued interest. Some lenders may work with the borrower to set up a repayment plan rather than requiring one lump repayment.

Mortgage Recasting

With a mortgage recast, you make a lump sum payment toward the principal balance of the loan. The lender will then recast, or re-amortize, your remaining loan repayment schedule. Since the principal amount is smaller after the lump-sum payment is made, each monthly payment for the remaining life of the loan will be smaller, even though your interest rate and term remain the same.

Making Extra Principal Payments

With any type of loan, you may be able to lower your borrowing costs by occasionally (or regularly) making extra payments towards principal. This can help you pay back what you borrowed ahead of schedule and reduce your costs.

Before you prepay any type of loan, however, you’ll want to make sure the lender does not charge a prepayment penalty, since that might wipe out any savings. You’ll also want to make sure that the lender applies any extra payments you make directly towards principal (and not towards future monthly payments).

The Takeaway

Loan modification vs loan refinancing…which one wins?

It depends on your financial situation. If you’re dealing with financial challenges and at risk of home foreclosure, you may want to look into a loan modification, which could be easier to qualify for than loan refinancing.

If you’re interested in getting a lower interest rate or lowering your monthly debt payment, refinancing likely makes more sense. A refinance may also make sense if you’re looking to tap your home equity to access extra cash. With a cash-out refi, you replace your current mortgage with a new, larger loan and receive the excess amount in cash.

Think twice before turning to high-interest credit cards. Consider a SoFi personal loan instead. SoFi offers competitive fixed rates and same-day funding. Checking your rate takes just a minute.

SoFi’s Personal Loan was named NerdWallet’s 2023 winner for Best Online Personal Loan overall.

FAQ

What are the disadvantages of loan modification?

A loan modification typically comes with a hardship requirement. A lender may ask to see proof that your financial circumstances are involuntary and that you’ve made an effort to address them before considering loan modification.

A loan modification can also have a temporary negative effect on your credit.

Is a loan modification bad for your credit?

A lender may report a loan modification to the credit bureaus as a type of settlement or adjustment to the loan’s terms, which could negatively impact on your credit. However, the effect will likely be less (and shorter in duration) than the impact a series of late or missed payments or a foreclosure on your home would have.

Photo credit: iStock/AlexSecret

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Checking Your Rates: To check the rates and terms you may qualify for, SoFi conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, we will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

The Department of Veterans Affairs announced that it is pausing foreclosures on VA-backed loans and extending pandemic protections for veterans facing difficulties paying their mortgages.

Officials said Friday that the department will contact mortgage services to pause VA foreclosures and extend the COVID-19 Refund Modification program through May 31, 2024, to ensure that veterans are able to stay in their homes.

The move follows a report Nov. 11 by National Public Radio that found veterans who used the mortgage forbearance program authorized by Congress early in the pandemic were at risk of losing their homes after the VA ended a Partial Claim Payment program that would have allowed them to defer their missed payments to the back of their loan period.

Read Next: US Military Says National Security Depends on ‘Forever Chemicals’

Instead, when the program ended, they received bills from their mortgage companies for the total payments missed, meaning they faced paying large sums to keep their existing low-interest mortgages or refinancing under today’s rates, which are double what they were in January 2022.

According to the NPR report, roughly 6,000 VA homeowners are in the foreclosure process. Another 34,000 are delinquent.

The VA has called for mortgage services to pause foreclosures and will “work with servicers on workable home retention solutions for veterans,” according to a department statement.

The extension of the COVID-19 Refund Modification program will allow veterans to obtain zero-interest, deferred-payment loans from the VA to cover missed payments and modify their existing VA-guaranteed loans to create an affordable monthly payment structure.

VA officials said they are establishing a VA Servicing Purchase program that will allow the department to purchase defaulted VA loans from mortgage companies, modify them, and then put them in the VA’s direct loan portfolio.

“This will empower us to work with veterans experiencing severe financial hardship to adjust their loans — and their monthly payments — so they can keep their homes,” VA officials said in the statement.

The majority of loans described as “VA home loans” are actually VA-backed loans, in which the department guarantees a portion of the loan, ensuring that if a veteran homeowner goes into foreclosure, the lender will recoup some or all of its losses.

The benefits for veterans include better loan terms, such as a more favorable interest rate or smaller to no down payment. According to the department, nearly 90% of all VA-backed home loans are made without a down payment.

Following the NPR report, Senate Democrats Sherrod Brown of Ohio, Tim Kaine of Virginia, Jack Reed of Rhode Island, and Jon Tester of Montana wrote to VA Secretary Denis McDonough calling for a pause and urging him to extend the COVID-era refund program.

“With each additional day that passes, risks mount for borrowers who are facing foreclosure while they wait for a solution from VA. Without this pause, thousands of veterans and service members could needlessly lose their homes,” the senators wrote. “This was never the intent of Congress.”

Tester, who serves as chairman of the Senate Veterans Affairs Committee, released a statement Monday praising the VA for its fast response.

“I’m encouraged to see VA answering my call to quickly address this crisis facing our men and women who risked their lives serving this country and were facing foreclosure through no fault of their own,” Tester wrote in a statement. “This pause will help ensure our veterans, service members, and their families can remain in their homes and get their payments back on track while VA works on a long-term solution.”

VA officials said any veteran struggling with making their mortgage payments should check out the department’s housing assistance website or call 877-827-3702.

Are you struggling to meet your monthly mortgage payments? If so, you’re not alone. Between the impact of COVID-19 and fluctuating inflation concerns, many homeowners are struggling to meet their financial obligations. In fact, records show a 115% increase in the number of home foreclosures in the United States from 2021 to 2022. Unfortunately, many homeowners don’t realize there are various programs available to help them avoid losing their homes. This article covers the home affordability programs offered that may be able to help you avoid foreclosure or lower your monthly mortgage payments.

In This Piece

Finding Mortgage Relief Options

During the pandemic, the government created numerous home loan programs. These programs can help individuals and families overcome financial hardships. Each program has different eligibility requirements, but the home must be your primary residence. Many of these programs are also for homeowners with federally backed mortgages, such as VA, USDA, or FHA loans.

Most of these programs are for people who already have a home and have concerns about paying their mortgage. Those looking to buy their first home may wonder, “How do I know if I can afford a home?” The first step is to conduct a free credit check to find out what your credit score is.

How Can I Save My Home From Foreclosure?

The government has several foreclosure assistance programs to help you avoid losing your home. These government programs may be able to pay a portion of your overdue mortgage payments or pause these payments until you’re back on your feet.

It’s important to explore all your options to determine how these programs can help. You can start by contacting your lender to see what options they have available.

Homeowner Assistance Fund (HAF) Program

As part of the American Rescue Plan Act of 2021, the Homeowner Assistance Fund (HAF) Program helps eligible homeowners impacted by COVID-19 avoid foreclosure. This program can give homeowners money to make past-due mortgage payments and other related costs, such as property taxes, homeowners insurance, home repairs and utility bills. The goal is to ensure homeowners financially impacted by the global pandemic don’t lose their homes.

Get matched with a personal

loan that’s right for you today.

Learn

more

While the distribution of these funds began in 2021, many states still have funds available. To be eligible for the HAF Program, homeowners must earn less than 100% of the median income of the United States or less than 150% of the median income for their specific area (whichever is higher).

You can check your income eligibility with the U.S. Department of Housing and Urban Development. In most cases, homeowners aren’t expected to repay these funds. However, you are expected to continue making on-time payments.

This program is only for those who already own a home. If you’re considering purchasing a home, you want to make sure you have enough money in savings. How much money you need to buy a house depends on various factors, such as your down payment and closing costs.

CARES Act

The Coronavirus Aid, Relief and Economic Security (CARES) Act was enacted to provide economic assistance to individuals and families affected by the pandemic. For eligible homeowners, this act gives them the ability to request forbearance from their mortgage servicer or lender. A forbearance enables homeowners impacted by COVID-19 to pause or reduce their regular mortgage payments for a set period of time.

With the CARES Act, you can request an initial forbearance of up to 180 days. If necessary, you can also request an extension of up to 180 days. The maximum forbearance amount is 360 days.

You’ll need to make up these missed payments—but not in one lump sum. Most lenders allow borrowers to pay this back in installments or to defer these payments to the end of the loan. However, it’s important to understand your obligations prior to entering into a forbearance agreement.

Under the CARES Act, only homeowners with federally backed loans, such as Fannie Mae, Freddie Mac, USDA, VA and USDA loans, are eligible for guaranteed forbearance. Homeowners with private loans should check with their mortgage servicer or lender to see if forbearance is available.

The CARES Act program is ideal for homeowners who are struggling to make their monthly mortgage payments. To be eligible for this program, the global pandemic must have financially impacted you. However, no documentation is required to prove this impact.

To see if you qualify, reach out to your specific mortgage servicer or lender. You should find this contact information on your latest mortgage statement.

Refinance with Your Lender

Refinancing is another option homeowners should consider. Depending on the specifics of your current home mortgage, you may be able to obtain lower monthly payments. Fortunately, the recent housing boom has significantly increased home values for many people. This means homeowners may qualify for refinancing after just a few years of homeownership.

Homeowners with an FHA, a VA, a USDA or another federally backed loan may qualify for a Streamline Refinance process. With this process, eligible homeowners can refinance their home mortgage without a credit check or proof of employment. In fact, with a Streamline Refinance, you may not even need to go through the appraisal process. This means you may be able to refinance your home even if you have little or no equity.

Even if you have a private loan, you may be able to refinance your home loan to lower your monthly payments. If you’re not able to refinance your current home loan, you may be able to request a loan modification. For example, you may be able to change the terms, interest rates or structure of your current mortgage.

When seeking a new home mortgage, it’s important to understand how credit works when buying a house. Before you start the process, you should request a free credit score.

What Other Options Do I Have?

If you’re struggling to make your monthly mortgage payments or looking for a way to lower your monthly payments, compare your home affordability options. Be sure to talk to your mortgage servicer or lender to see what options are available.If you’re considering refinancing your current mortgage, be sure to compare various lenders. Compare current mortgage rates now.

The Fannie Mae Flex Modification Program (FMP) is a mortgage assistance solution designed to relieve borrowers facing financial hardship.

Are you looking to improve your mortgage management but don’t know where to start? Handling mortgage payments is challenging, especially if you’re facing economic difficulties and don’t know where or how to get financial assistance. The Fannie Mae and Freddie Mac Flex Modification Program may be the solution you’re looking for.

Learn what you need to know about the Flex Modification Program: how it works, who qualifies for it, and how you can apply. This comprehensive guide will help you understand the many benefits of FMP for a more stable financial future.

In This Piece:

What Is the Flex Modification Program?

The Fannie Mae Flex Modification program is a mortgage assistance solution designed to relieve borrowers facing financial hardship. This program offers a flexible framework for loans that helps eligible borrowers to modify their monthly mortgage payments and avoid foreclosure.

Modifying the loan terms can make mortgage payments more affordable and sustainable for struggling homeowners.

Get matched with a personal

loan that’s right for you today.

Learn

more

How Do Fannie Mae and Freddie Mac Work?

The mortgage market has a few essential entities, including the government-sponsored enterprises called Fannie Mae and Freddie Mac. Their approach allows lenders to free up funds to provide more mortgage loans to borrowers.

But how does it work? Fannie Mae and Freddie Mac helped make mortgages more accessible by buying them from lenders. This allows lenders to have more money available to provide new mortgages to borrowers or invest in other financial opportunities. For example, if a lender originates a mortgage, they can sell it to Fannie Mae or Freddie Mac, who then include it in their portfolio or package it into mortgage-backed securities.

How Flex Modification Works

The Flex Modification Program offers loan modifications to eligible borrowers experiencing financial hardship. Here’s a breakdown of how the program operates:

Eligibility Requirements:

You must have a mortgage loan owned or guaranteed by Fannie Mae or Freddie Mac.

The mortgage loan must be at least 60 days delinquent or at risk of imminent default.

You must demonstrate a hardship that affects your ability to make timely mortgage payments.

Modification Terms:

The program aims to reduce your monthly mortgage payment to 20% or more below your pre-modification.

The modification may involve adjusting the interest rate, extending the loan term, or forbearing a principal portion.

The goal is to make the mortgage payment more affordable while ensuring it’s sustainable for you.

Application Process:

Apply to the Flex Modification Program through a loan servicer.

The loan servicer will assess your eligibility and collect the necessary documentation.

Once approved, the loan servicer will work with you to finalize the modification terms.

Why Should You Consider the Flex Modification Program?

Before considering the Flex Modification Program, it’s essential to understand its potential pros and cons.

Pros:

Lower monthly payments: The program aims to reduce your mortgage payment to a more affordable level, making it easier to manage your finances on time.

Protection from foreclosure: By modifying your loan, the program can help you avoid the devastating consequences of foreclosure.

Improved financial stability: By participating in the Flex Modification Program, you can regain control of your financial situation. Providing you with a sense of stability and peace of mind, allowing you to focus on rebuilding your financial health.

Simplified application process: Applying for the program is relatively straightforward, and you can work directly with your loan servicer to navigate the process.

Potential principal reduction: The FMP may offer this, which means that a portion of the outstanding loan balance could be forgiven or deferred, reducing the overall amount owed. This can be particularly beneficial if you owe more on the mortgage than your current property value.

Preservation of homeownership: One of the primary goals of the FMP is to help borrowers preserve their homeownership. The program offers a viable alternative to foreclosure by providing a framework for loan modifications.

Cons:

Extended loan term: Modifying your loan may result in a more extended repayment period, meaning you’ll make mortgage payments for longer.

Impact on credit score: While participating in the program doesn’t directly affect your credit score, the delinquency prior to modification might be reported on your credit report.

Limited availability: The program is specifically for Fannie Mae or Freddie Mac borrowers with owned or guaranteed loans. You won’t qualify for this program if either entity doesn’t back your loan. However, other programs may exist. Contact your lender if you’re struggling to make your mortgage payments.

Remember, these pros and cons will vary based on your circumstances. It’s essential to consult with your loan servicer and thoroughly review the modification terms to understand the potential benefits you may receive from participating in the program.

Who Qualifies for the Flex Modification Program?

The Flex Modification Program is designed for borrowers struggling with mortgage payments due to financial hardship.

To qualify for the program, you must meet the following criteria:

Loan ownership: The mortgage loan must be owned or guaranteed by Fannie Mae or Freddie Mac.

Delinquency or imminent default: Borrowers must be at least 60 days delinquent on their mortgage payments or at risk of imminent default.

Demonstrated hardship: Borrowers need to demonstrate a hardship that affects their ability to make timely mortgage payments. Hardships may include job loss, income reduction, medical expenses, divorce, or other significant life events.

Additionally, you must comprehend what a “hardship” entails to be considered for a loan modification. Each situation is evaluated individually, but common examples of hardships include loss of income, disability, serious illness, divorce, or the death of a co-borrower.

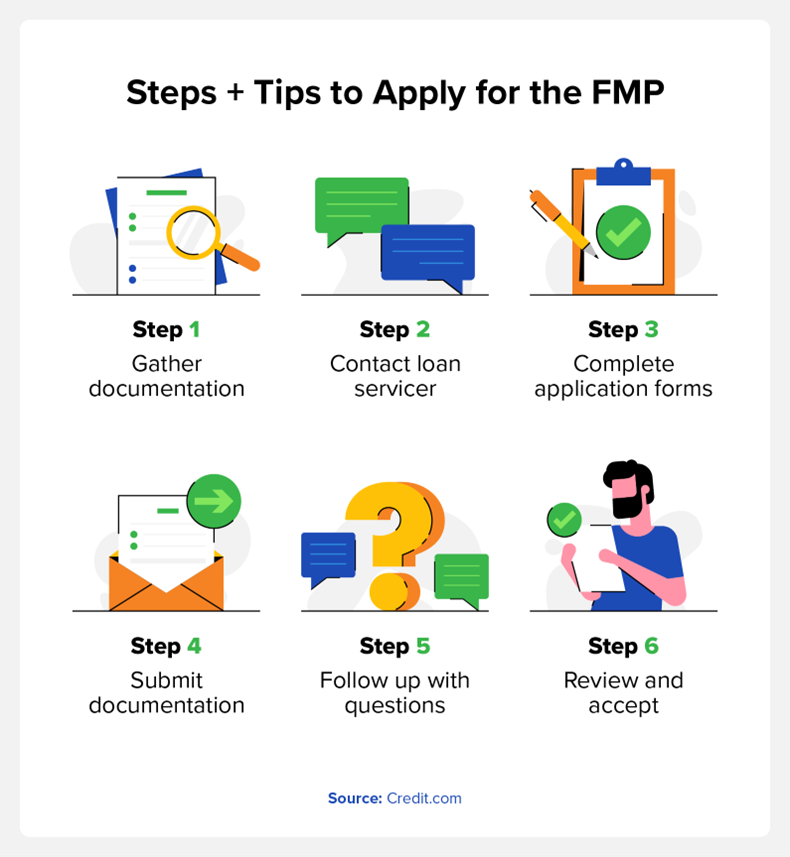

How to Apply for the FMP

If you believe you meet the eligibility requirements for the Flex Modification Program, you can follow these steps and tips to apply:

Gather documentation: Prepare the necessary documents, such as proof of income, bank statements, tax returns, and any other documentation required by your loan servicer.

Contact your loan servicer: Inform your loan servicer about your interest in the Flex Modification Program.

Complete application forms: Your loan servicer will provide the necessary forms and guidance to complete the application process.

Submit documentation: Submit all the required documentation and the completed application forms to your loan servicer.

Follow up and provide additional information: Be proactive in promptly following up with your loan servicer and providing any additional information they request.

Review and accept the modification terms: Once your loan servicer evaluates your application, they will provide you with the proposed modification terms. Review them carefully and, if acceptable, sign and return the necessary paperwork to proceed with the modification.

Remember, each loan servicer may have a specific application process, so it’s crucial to communicate directly with them to ensure you have all the necessary information and are following the correct steps. Having to redo the application process due to easily-avoided mistakes is the last thing you need.

Other Mortgage Payment Help Options

What if I don’t qualify? What can I do? Other mortgage payment assistance options are available if the FMP is not the right fit.

Fannie Mae and Freddie Mac offer additional programs catering to different circumstances. Some of these options include:

Home Affordable Modification Program (HAMP): This aims to help homebuyers struggling with financial hardship and mortgage payments.

Repayment plan: Allows you to catch up on missed mortgage payments by adding a portion of the past-due amount to your regular expenditures over an agreed-upon period.

Forbearance: Temporarily suspends or reduces your mortgage payments with this program. It can be for a specific period, providing short-term relief during financial difficulties, so you can reassess the situation.

But before you move forward with one of these, it’s essential to analyze your alternatives and consult with your loan servicer to determine the best course of action based on your specific circumstances.

FAQs

Let’s address some frequently asked questions about the Flex Modification Program:

Does the Flex Modification Program Affect Your Credit Score?

Participating in the Flex Modification Program doesn’t directly impact your credit score. However, the delinquency prior to modification might be reported on your credit report

What if Fannie Mae or Freddie Mac Doesn’t Own My Loan?

If your loan isn’t owned or guaranteed by Fannie Mae or Freddie Mac, you won’t be eligible for the Flex Modification Program. However, you should contact your loan servicer to inquire about other available mortgage assistance options or loan modification programs specific to your loan type.

How Long Does the Flex Modification Program Last?

The duration of the Flex Modification Program varies depending on the specific terms of the modification. Typically, the program aims to provide long-term mortgage relief by modifying the loan terms to make payments more affordable and sustainable for the borrower.

The revised terms may involve extending the loan term or adjusting the interest rate. It’s important to discuss the duration of the modification with your loan servicer, as it will depend on your circumstances and the terms agreed upon.

Can I Qualify for the Flex Modification Program if I’ve Previously Received a Loan Modification?

If you have previously received a loan modification, you may still be eligible for the Flex Modification Program. However, the specific requirements and eligibility criteria may change depending on your previous modification and the current guidelines set by Fannie Mae and Freddie Mac.

It’s crucial to communicate with your loan servicer and provide them with all the necessary information regarding your previous modification. They will assess your eligibility based on your unique circumstances and guide you through the application process.

Remember, these answers are general guidelines, and you must consult with your loan servicer to get accurate and personalized information based on your situation.

What Are the Next Steps?

The Fannie Mae Flex Modification Program provides borrowers with a potential lifeline during financial hardship. It aims to make mortgage payments more manageable and sustainable by offering loan modifications. If you’re facing challenges with your mortgage payments, exploring the Flex Modification Program and other mortgage payment help options can help you find the assistance you need.

To take control of your mortgage management and improve your financial well-being. Consult with your loan servicer for accurate and personalized information based on your situation, and research different mortgage rates to make informed financial decisions.

Hedging Webinar; Home Insurance Nightmare; GSE Changes; Interview with Henry Broeksmit on Youth in the Industry

<meta name="smartbanner:author" content="We now have a native iPhone and Android app. Download the NEW APP”>

This website requires Javascrip to run properly.

Hedging Webinar; Home Insurance Nightmare; GSE Changes; Interview with Henry Broeksmit on Youth in the Industry

By: Rob Chrisman

Wed, Sep 6 2023, 9:59 AM