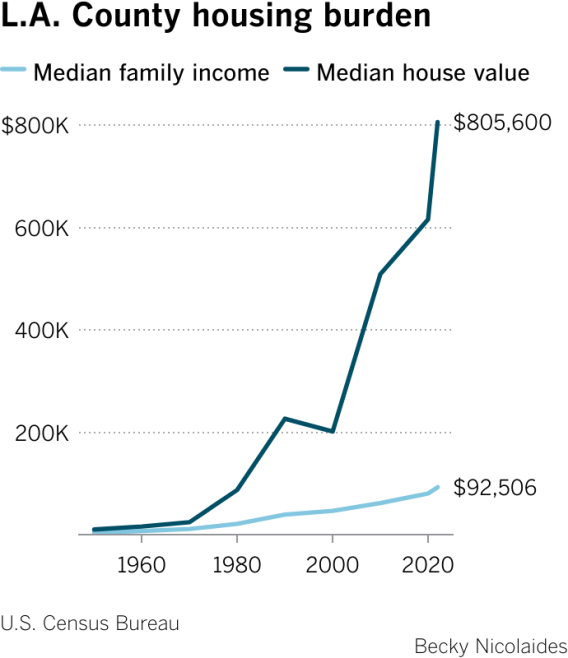

The high cost of housing is driving Southern California’s biggest challenges. Income is not keeping pace with housing costs. It hasn’t for at least two generations, and the problem of unaffordable shelter shows few signs of letting up.

There’s a metric called “housing burden” that lays the situation bare. Over the last 50 years, it tracks the growing, gaping mismatch between income and shelter costs in Los Angeles County.

In 1979, UCLA land experts Leo Grebler and Frank Mittelbach wrote: “As a general, time-honored rule of thumb” house prices in a community “should not exceed 2 to 2½ times the annual income” of its residents.

Within a decade, home prices began to drastically violate this rule. If it were applied today, it would mean a four-person household with the median Los Angeles County income of $98,200 could afford to buy a house that cost $245,500. However, the median home price in the county last month, according to Redfin, was $980,000.

Advertisement

How did things get so unbalanced?

In the 1950s and 1960s, buying a single-family home in Los Angeles was an attainable prospect. The GI Bill and the Federal Housing Authority helped with loans and mortgage dollars (albeit primarily for white families). And home building was on a tear, thanks to the region’s pro-development political climate.

By the 1970s, however, a cascade of factors — local to global — changed the equation.

Housing prices first shot ahead of income in the mid-1970s. Analysts attributed the spike to the first cohort of baby boomers reaching home-buying age, which expanded the pool of buyers and created a seller’s market. The 1973 oil crisis and ensuing inflation pushed buyers to pay up for fear prices would rise even higher. Unrelenting demand thus not only kept pace with prices, it increased them.

Social-demographic factors also factored in. Per capita income doubled from 1966 to 1977, due in part to more women in the workplace. When federal policies struck down gender discrimination in loan and credit decisions, two-income families could qualify for larger mortgage loans, elevating the demand for higher-priced homes.

Advertisement

Then land and building costs climbed, pushing prices even higher. And in 1978, Proposition 13 became law.

The ballot measure slashed property taxes and with them, funding for municipal services. Cities and towns scrambled to recoup the lost revenue. New real estate developments were “money-losers,” as urban planner and former Ventura Mayor William Fulton observed, because property taxes fell so low. Instead, municipalities turned to retail development to generate lucrative sales tax revenue. Prop. 13 thus became a powerful disincentive to build housing.

The rising slow-growth movement put another damper on housing supply. It was pushed by homeowners who resisted adding multifamily housing in single-family neighborhoods or new development in nearby open space.

One study by the California Legislative Analyst’s Office found that by the early 2000s, more than two-thirds of cities and counties in coastal California metro areas had slow-growth policies in place, and that when a community added such a policy, it resulted in a 3% to 5% increase in home prices. Moreover, the historical momentum of R-1 (single family) zoning stymied the construction of multifamily units.

The upshot of all these pressures? From 1980 to 2010 in Los Angeles, the population grew by 31.3% while housing units grew by only 20.6%.

L.A.’s spiraling housing costs paralleled trends in large, global metro regions by the turn of the 21st century, suggesting that forces beyond L.A. were also at work. In the 1990s and early 2000s, the housing bubble was driven by finance structures linked to global markets, inflows of global capital and unregulated banking practices that set off unrestrained and predatory lending and buying frenzies. Even after the 2007-09 banking crisis and Great Recession, home prices in L.A. soon regained traction.

Taking a longer view, economist Robert Shiller traced rising housing costs in the late 1980s and early 2000s across metro areas globally, including L.A. He pinned a good deal of the blame on “irrational exuberance” that motivated uncontrolled buying. The psychological draw of metro areas such as Paris, London, Sydney and L.A. reinforced the belief that land prices would continue to go up and up. Media fed these perceptions. And housing bubbles blew up.

Looking at the housing burden graph, the price surge since 2020 is truly eye-popping. Urban analyst Richard Florida attributes it to pandemic-driven demands for more housing space especially among millennials, a massive shortage of housing overall and, perhaps most disturbingly, the growing competition from large institutional investors who’ve been snapping up homes and apartments in recent years. In 2021, they bought 29% of all single-family homes in California and, with their ability to outbid other buyers, they drive up prices.

Over the last 50 years, L.A.’s housing burden has evolved from challenging to simply unsustainable. The consequences are all around us, in skyrocketing rents, a ubiquitous homelessness crisis, housing overcrowding, rising commuting times to drive-till-you-qualify exurbs, population flows out of California and intensified wealth inequality.

Solutions must come from both the housing and the income side.

Increasing the housing supply is crucial. It must be accompanied by policies that protect individual buyers from corporate competitors, ensure the ongoing production of affordable housing, and guard against gentrification.

Even more importantly, wages and salaries must climb considerably to make housing affordable again. The major employers in our region — from the movie studios to hotels to hospitals and logistics firms — must take a long, hard look at the housing burden graph and see in it their own role in widening the gap. The Writers Guild and actors’ strikes, the Unite Here Local 11 hospitality industry strike and the strike vote last week by Kaiser Permanente healthcare workers speak directly to L.A.’s housing burden.

The struggle to match income to cost of shelter is an inescapable fact of L.A. life that demands swift, conscientious redress.

Becky Nicolaides is a research affiliate at the Huntington-USC Institute on California and the West, and author of “The New Suburbia: How Diversity Remade Suburban Life in Los Angeles After 1945,” forthcoming from Oxford University Press. The data set collected for the book, a granular look at demographics from 1950 to 2010, will be published online by the USC libraries next year.

A huge panel of economists from banks, universities, and investment and research firms weighed in on the direction of U.S. home prices over the next five years.

The consensus was average home price appreciation of 21.99% through 2017, growth that exceeds what Zillow refers to as “pre-bubble rates,” which took place from 1987 to 1999.

During that time period, home prices appreciated annually at a rate of 3.6%, on average.

2013 Strongest of Next Five Years

The 118 panelists indicated that 2013 would be the strongest year in terms of home price appreciation, with values expected to climb an average of 4.6%.

That compares to the 5.5% gain seen in 2012, meaning there should be some moderation despite the positive sentiment.

In 2014, prices are expected to rise another 4.2%, and then dip to between 3.6% and 3.8% for 2015-2017.

All in all, it’s another sign that housing has indeed bottomed, and should slowly work its way back to previous highs seen before the crisis hit.

Who’s the Most Optimistic?

I decided to scour the list of panelists to see first who was included, and second what they thought.

There is an interesting mix of participants on the list, and an even more intriguing divergence of opinion.

Let’s start by looking at who is most confident about home prices going forward, with the cumulative total displayed below:

1. Ethan Penner, Managing Partner at Monday Real Estate Partners – 77.86% 2. David Wyss, Economist at Brown University – 41.53% 3. Christine Chmura / Xiaobing Shuai, Chief Economist / Senior Economist at Chmura Economics & Analytics – 40.22% 4. Rajeev Dhawan, Director, Economic Forecasting Center at Georgia State University – 38.46% 5. Jim Kleckley Director, Bureau of Business Research at East Carolina University – 37.75% 6. Joel Naroff, President at Naroff Economic Advisors Inc. – 37.10% 7. Aneta Markowska, Senior U.S. Economist at Societe Generale – 36.17% 8. Matthew Sippel, Senior Partner at Indus Capital Partners – 35.05% 9. Richard Dorfman, Managing Director at SIFMA – 33.81% 10. Constance Hunter Senior Advisor at International Solutions Network – 32.59%

[Tips for first-time home buyers.]

Who Are the Housing Bears?

Not all panelists were as optimistic as those listed above. In fact, some even feel housing prices will fall over the next five years.

Let’s take a closer look at who thinks housing isn’t the best investment at the moment:

1. John Brynjolfsson, Chief Investment Officer at Armored Wolf, LLC – (11.04%) 2. Mark Hanson, Founder at Hanson Advisors – (8.39%) 3. Gary Shilling, President at A. Gary Shilling & Co. – (5.05%) 4. Barry Ritholtz, CEO at FusionIQ – 7.15% 5. Alex Barron, Founder & Senior Research Analyst at Housing Research Center – 10.36% 6. Komal Sri-Kumar, President at Sri-Kumar Global Strategies, Inc. – 10.38% 7. Parul Jain, Chief Investment Strategist at MacroFin Analytics LLC – 10.41% 8. Paul Ballew, Chief Data and Analytic Officer at Dun & Bradstreet, Inc. – 10.84% 9. Ellen Zentner / Aichi Amemiya, Senior Economist / VP at Nomura Securities International, Inc. – 12.03% 10. Ihab Seblani, Economist at AIG Global Economics – 12.42%

As you can see, the panelists exhibit quite a range in outlook, with some so negative they actually expect home prices to be down five years from now.

However, the lion’s share of panelists sound pretty darn positive, if the numbers are any indication.

Overall, the most optimistic quartile of panelists predict a 6.1% increase in home prices this year, while the most pessimistic quartile sees an average increase of three percent.

When looking at the five-year cumulative total, projections ranged from 11.7% among the most pessimistic quartile to 34.2% among the most optimistic.

For the record, Zillow chief economist Stan Humphries sees home prices rising 18.42% over the five-year period.

You can see the complete list here. There are some other interesting names on the list not mentioned in this post.

As always, you should take anyone’s opinion with a grain of salt. Plenty of so-called experts were wrong leading up to the past crisis, and many will be wrong again. That’s just life.

Also note that this covers national home prices, and that values will vary widely by city, region, etc.

Are you looking for the best side jobs for teachers? Teaching is a great career choice and teachers are very much needed in the world. Unfortunately, though, it is not the highest-paying job that exists. Due to that, you may be looking to find ways to make extra money as a teacher. Side hustles for…

Are you looking for the best side jobs for teachers?

Teaching is a great career choice and teachers are very much needed in the world. Unfortunately, though, it is not the highest-paying job that exists. Due to that, you may be looking to find ways to make extra money as a teacher.

Side hustles for teachers are great because they can help you make extra income, pay off debt, save for a vacation, and more.

Teachers have many useful skills, which make them a great fit for many different side hustles alongside their main teaching job.

Quick Summary on Side Jobs For Teachers:

Online tutoring and selling lesson plans are popular side jobs for teachers that use their existing skills

Selling crafts, selling printables, or teaching online courses can be a nice creative outlet

Short-term and seasonal side gigs like coaching sports or teaching summer school may be better for your schedule than year-round gigs

Best Side Jobs For Teachers

There are 36 side jobs for teachers listed below. If you want to skip the list, here are some jobs that you may want to start learning more about first:

Below are 36 side hustles for teachers.

1. Sell educational printables

Selling educational printables can be a great way for teachers to make extra income and it is great for anyone who wants to learn how to make passive income as a teacher.

An educational printable is a teaching resource, either digital or physical, that educators create to help with learning.

Other teachers buy these for their classes and so do parents.

Educational printables are things like math problems, vocabulary cards, and science experiments. They work for different grades and learning goals, making it an easy way to add to regular teaching or homeschooling. You can share these resources online or print them for in-person classes, making them a helpful tool for improving education.You can learn more at How I Make $400,000 Per Year Selling Educational Printables.

Do you want to make money selling printables online? This free training will give you great ideas on what you can sell, how to get started, the costs, and how to make sales.

2. Tutor online or in person

Tutoring services or helping kids get ready for standardized tests either online or in person can be a great side hustle for teachers.

This option can be a natural fit, as you can use your teaching skills to tutor students.

To start, check out different online tutoring websites like Tutor.com or you can also do in-person tutoring sessions. For in-person tutoring sessions, you can contact local tutoring companies or promote your services on social media or in local Facebook parent groups for your area.

3. Sell your lesson plans

As a teacher, you already make lesson plans for your classes. You can actually sell your lesson plans, earn extra money, and help other teachers.

The most popular platform for this kind of side job is Teachers Pay Teachers (TPT). Here, you can upload your lesson plans, activities, assessments, and other educational resources. Each time someone purchases one of your items, you’ll earn some income.

Lesson plans need to be well-organized, easy to understand, and tailored to specific grade levels and subjects (such as fifth grade math). You should include clear objectives and step-by-step instructions to make your lesson plans more appealing to potential buyers.

4. Coach a school sport or other after-school program

Coaching a school sport is something that you can do within your own school district as many schools are in need of help with their sports teams.

Some sports and after-school programs that can be a teacher’s side hustle include soccer, basketball, volleyball, and track-and-field, as well as clubs such as yearbook, chess, choir, and more.

5. Start a dog bakery

Starting a dog bakery can be a fun side job for teachers who love both dogs and baking.

You can make an extra $500 to $1,000, or even more, each month by making treats for dogs. You can make dog treats like cupcakes, cookies, cakes, and more.

You can learn more at How I Make $4,000 Per Month Baking Dog Treats (With Zero Baking Experience!).

6. Sell crafts on Etsy

Selling crafts on Etsy can be a great way to make extra money by being creative.

Etsy is a website where people from all over can buy and sell handmade and digital products.

Some ideas for products you can create and sell on Etsy that are teaching-related include:

Classroom decor items

Educational games and activities

Customized planner pages and stickers

Flashcards and study materials

Of course, you can create things that aren’t related to teaching at all, such as knitwear, jewelry, and more.

7. Sell on Teachers Pay Teachers

Teachers Pay Teachers (TPT) is a site specifically for educators to buy and sell educational materials, and this is a popular teacher side hustle. If you’ve developed lesson plans, worksheets, or other teaching tools for your classroom, you can share and earn from them on TPT.

I know I talked about selling education printables and lesson plans above, but I want to talk more about Teachers Pay Teachers in its own section because it is such a popular teacher side hustle.

You can sell:

Lesson plans and unit studies

Worksheets and printable activities

PowerPoint presentations and interactive notebooks

Posters, charts, and visual aids

For example, I looked on Teachers Pay Teachers and searched for third grade lesson plans. There, I found over 49,000 results such as math lesson plans about rounding, substitute teacher plans for third graders, reading comprehension lesson plans, and more. Here’s an example of one that you can look at.

The average teacher on Teachers Pay Teachers can make around $300 to $500 extra, but there are some teachers that make hundreds of thousands of dollars extra each year.

8. Babysit

As a teacher, you may find that babysitting is an easy side job to pick up, and, depending on where you live, you may be able to earn around $15 to $25 an hour. Parents love hiring teachers as babysitters because they have so much experience with children.

While babysitting, you’ll find that your existing skills from teaching make a difference in providing the best care possible.

9. Teach English as a second language online

Teaching English as a second language (ESL) online is a popular side job for teachers. As an online ESL teacher, you can help students learn English and work from home.

Most jobs require you to be a fluent English speaker with a bachelor’s degree.

10. Teach summer school

One of the obvious ways for teachers to make extra money in the summer is to teach summer school.

It’s a great way to make use of your teaching skills while earning extra income. Plus, summer school takes place during summer break, so it should fit well with your schedule of already being off from school.

11. Summer camp counselor

Another great option during the summer months is to become a summer camp counselor.

As a counselor, you’ll supervise children in activities such as sports, arts, and crafts. Camps are always looking for instructors with teaching experience, making this a good side job for educators.

12. Grade papers

Grading papers as a side job may appeal to you if you’re looking for a more flexible, at-home option.

Companies such as Measurement Inc. hire teachers to grade student work, such as essays and test answers.

They are hiring evaluators to score in the subjects of English, mathematics, science, and more and pay starts at $15 per hour.

13. Work at a restaurant

If you’re looking for something completely different from teaching, you could take a part-time job at a restaurant.

Working in restaurants can be a good fit for teachers because they often offer flexible hours that can align with your teaching schedule. You can choose jobs like being a server, host, and more.

14. Proofread

As a teacher, you are probably already a great proofreader and are able to spot mistakes easily. With these skills, proofreading can be a great side job. By proofreading, you can help authors, website owners, students, and more improve their writing while earning some extra income.

Even the most skilled writers can make mistakes in grammar, punctuation, and spelling. That’s why hiring a proofreader can be very helpful for pretty much anyone and everyone.

If you want to find online proofreading jobs, I recommend watching this free 76-minute workshop all about how to get started proofreading.

Recommended reading: 20 Best Online Proofreading Jobs For Beginners (Earn $40,000+ A Year).

15. Blog

Blogging can be a fun way for you, as a teacher, to make extra money from home. Many blogs are run by teachers, and I completely get why – you can blog in your spare time and you don’t have to stick to any formal schedule.

To start your own blog, first, choose a topic that you’re interested in writing about, maybe something related to your teaching field or a hobby you enjoy.

You can make money from your blog in ways such as:

Affiliate marketing – Share links to products or services related to the topic you are writing about, and earn a commission for sales generated from your referral links.

Advertising – Include display ads or sponsored posts on your blog.

Courses and ebooks – You can create courses or ebooks related to your area of expertise, and sell them through your blog.

Since I began Making Sense of Cents, I’ve made more than $5,000,000 from my blog, and it all started as a side job.

Learn more at How To Start A Blog FREE Course.

Similar to blogging, a teacher could also start a YouTube channel, a TikTok, and more.

16. Freelance write

If you are looking for side jobs for teachers from home, then becoming a freelance writer can be a great choice.

Freelance writers write content for blogs, websites, magazines, newspapers, advertising companies, and so much more.

You can find different writing jobs on platforms like Upwork and Fiverr, or even find clients on your own, such as by reaching out to websites that you are interested in writing for.

Recommended reading: 14 Places To Find Freelance Writing Jobs – (Start With No Experience!)

17. Transcribe

An online transcriptionist’s job is to listen to video or audio files and then type out everything that they are hearing. There are many different types of transcriptionists, such as legal, general, and medical transcriptionists.

This job requires strong typing and listening skills, and you can work from home on your own schedule.

Transcriptionists earn around $15 to $30 per hour on average.

I recommend watching FREE Workshop: Is a Career in Transcription Right for You? You’ll learn how to get started as a transcriptionist, how you can find transcription work, and more.

Recommended reading: 18 Best Online Transcription Jobs For Beginners To Make $2,000 Monthly

18. Flip used items for resale

Flea market flippers find underpriced items at flea markets, yard sales, and thrift stores, then resell them for a profit. This job requires a good eye for finding valuable items that you believe can be sold for a higher price.

As a teacher, you could find and sell items in the evening, on the weekends, over holiday breaks, and in the summer. You get to make your own schedule, and it can be however many or few hours as you want.

Some items that you can resell include:

Vintage furniture

Collectibles, such as toys, coins, stamps, books, and more

Sporting equipment

Clothing

Electronics

I recommend signing up for a helpful webinar on this topic, How To Turn Your Passion For Visiting Thrift Stores, Yard Sales & Flea Markets Into A Profitable Reselling Business.

19. Bookkeep

Bookkeepers are people who keep track of all the money-related things for businesses. Bookkeepers do tasks like:

Tracking income

Organizing expenses

Making financial reports

This is typically a flexible job that you can do from home on your own time.

You can join the free workshop that focuses on finding virtual bookkeeping jobs and how to begin your own freelance bookkeeping business by signing up for free here.

Recommended reading: How To Find Online Bookkeeping Jobs

20. Sell Canva templates

Creating and selling Canva templates online allows you to work from home in your free time.

A Canva template is like a pre-designed layout that you can use for creating things like social media graphics, Pinterest pins, ebooks, or presentations. It is a helpful starting point if you’re not very skilled at designing from scratch. Business owners, marketing professionals, nonprofit organizations, educators, event planners, restaurants, and more buy templates all the time.

Canva templates come with blank spaces where buyers can add their own words or pictures, adjust colors and fonts, and more. They’re useful for people who want their graphics to look high quality without spending a lot of time in the process (or perhaps they don’t know how to do it so templates help them a lot!).

Making and selling Canva templates can be a great way to earn extra money as you only need to create them once, and then you can sell them as many times as you’d like.

Recommended reading: How I Make $2,000+ Monthly Selling Canva Templates

21. Rover (walk and watch pets)

Rover is a website that links pet owners with pet sitters and dog walkers. You can do this job on the weekends throughout the year, or simply only open up your schedule during the summer months. It is up to you.

Getting started is easy on Rover – you set up a profile that talks about your experience with pets and the services you can provide, like dog walking, pet sitting, and house sitting.

Then, you will receive requests from customers and talk about pricing. Rover takes care of processing payments, and you’ll receive payments directly into your account.

You can sign up for Rover here.

22. Care.com

Another platform for finding pet and house sitting side jobs is Care.com. Care.com is not limited to pet care and includes other caregiving services, such as childcare and senior care.

You can browse available jobs in your area and apply to those that match your skills and interests. Care.com also allows clients to contact you directly for your services after you’ve created a profile. Once a job is completed, you’ll receive payment through the site.

23. Be a virtual assistant

A virtual assistant provides administrative, technical, or creative support to clients from home.

Some of the tasks you might do as a virtual assistant include managing schedules, responding to emails, making travel arrangements, handling social media accounts, and even writing articles or creating presentations.

If you want to become a virtual assistant, I recommend taking the free workshop called 5 Steps To Become a Virtual Assistant.

Recommended reading: Best Ways To Find Virtual Assistant Jobs

24. Be a food photographer

Food photography can be a fun and creative way to earn extra income during your free time. Food photographers do just that – take pictures of food.

Whether you’re working directly for restaurants, magazines, or on a freelance basis, this job allows you to use your skills and interests to create beautiful images.

You can learn more at How To Become a Food Blog Photographer And Earn Over $50,000 Each Year.

25. House sit

As a teacher, you might be looking for ways to make some extra money during breaks or weekends. One option to consider is house sitting, and this is when you watch someone’s home (such as watering their plants and collecting mail) and sometimes take care of pets while their owners are away. People also hire house sitters so that their homes aren’t sitting empty because a visible presence can deter potential thefts.

To get started in house sitting, you can join house-sitting websites to find opportunities in your area, or ask friends and family for referrals (you might want to start by house sitting for people you know and then ask for references that you can use to broaden your job search).

26. Rent out an unused room in your home

If you have a room in your home that you are not using, then you may be able to rent it to someone on either a short-term (such as by becoming an Airbnb host) or long-term basis (getting a full-time roommate).

I have rented out rooms many times in the past, and it was a great way to make some extra income for space that I wasn’t using.

You can learn more at What You Need To Know About Renting A Room In Your House.

27. Rent your garage space

If you have empty storage space, such as a garage, driveway, closet, basement, or attic, you may be able to rent it out and make extra money. This can be a lucrative side hustle where you don’t have to use up much of your spare time.

You can use Neighbor to list your extra space for rent and make up to $15,000 per year by doing so. With Neighbor, you can rent out your garage, driveway, basement, or even a closet.

You can sign up at Neighbor for free here and list your space.

You can also learn more about Neighbor at Neighbor Review: Make Money Renting Your Storage Space.

28. Rent out a photo booth

Renting a photo booth can be a fun side job for teachers.

To get started, you will need to buy a photo booth as well as things like backdrops and props for people to hold in the picture (such as hats, signs, fun things to hold, etc.).

On average, photo booth rentals can range from $500 to $1,000 per event, and in some cases, even more for specialized events or packages with additional features.

I have personally rented a photo booth for an event in the past, and it was a lot of fun!

29. Online surveys and focus groups

Taking online surveys and answering questions for focus groups is very part-time and can be a way to side hustle for teachers.

You share your thoughts plus answer questions and can earn cash or free gift cards.

The survey companies I recommend signing up for are:

American Consumer Opinion

Survey Junkie

Swagbucks

InboxDollars

Branded Surveys

Pinecone Research

PrizeRebel

User Interviews – These are the highest paying surveys with the average being around $60.

Recommended reading: 18 Best Paid Survey Sites To Make $100+ Per Month

30. Voice over act

A voice-over actor is the person whose voice you hear but don’t see in YouTube videos, radio ads, educational videos, and more.

Different companies need a wide variety of voices, and that’s where you come in.

Recommended reading: How To Become A Voice Over Actor And Work From Anywhere

31. Mystery shop

I was a secret shopper in the past, and there were often mystery shops that gave me $100 to put toward a free dinner. I always looked forward to these, as I was living paycheck to paycheck, and I used these restaurant mystery shops to reward myself every now and then.

There were other mystery shops that paid me actual money, and some paid me in free items, such as makeup, movie theater tickets, and car oil changes.

Companies hire mystery shoppers to get an understanding of their customer’s experience. Companies want to know a real product opinion, how the customer felt they were treated at their business, how phone calls were handled, and more.

Basically, mystery shopping is a way to anonymously test the entire shopping experience.

You can learn more at How To Become A Mystery Shopper.

32. Fitness trainer

Fitness trainers help people reach their health goals through customized exercise plans and nutrition advice. This is typically a job where you can choose your schedule, so you can choose to work hours outside of your teaching job, such as in the evenings and on the weekends.

I actually know a few teachers who are fitness trainers on the side, so it must be a good fit!

Another positive is that you can even choose between in-person and online coaching. Online coaching can mean that you can work remotely, making it a more flexible side job for teachers looking to earn extra income.

33. Find random gigs on Craigslist

As a teacher looking for side jobs, you can look for random gigs on Craigslist to earn some extra income. To begin your search, simply go to the Craigslist website and select your city from the home page.

Here are some jobs I found through a quick search:

Cleaning a house

Help assembling furniture

Taking down a shed in a backyard

Garage cleanup

Mover

Handyman

Movie extra

Sign holder

You can even post your own services on Craigslist if you have a skill you’d like to share with others, such as giving music lessons or tutoring.

34. Deliver groceries with Instacart

Grocery delivery services are popular because there are more and more people who want someone to do their grocery shopping for them.

Services like Instacart need personal grocery shoppers, and the average shopper makes $15 to $20 an hour to deliver groceries. Drivers are paid per order, and you get to keep 100% of your tips. You also get to choose your schedule, so a teacher could choose to work in the evenings or on weekends. Or, you could choose to only deliver groceries during the summer.

You can click here to sign up to be an Instacart Shopper.

You can also learn more at Instacart Shopper Review: How much do Instacart Shoppers earn?

There are many other gig ideas that you can try out too, such as Uber Eats and DoorDash.

35. Real estate agent

Some teachers are real estate agents on the side of their full-time job as a teacher. This is because you can list and sell homes on your weekends, during breaks, at night, and over the summer.

Selling homes can be more difficult, though, as your clients may want your full attention during the day occasionally and you would be busy teaching, so this is something to think about.

36. Driver’s ed teacher

A common side hustle for teachers is teaching driving lessons to teenagers and adults. As a teacher, you may be able to check if the high school near you is in need of a teacher for this subject. Or, you can reach out to a local driving school to see if they are hiring.

Driving instructors make around $20 an hour more or less, depending on where you live.

Frequently Asked Questions

Below are answers to common questions about side hustles for teachers.

How can I make money on the side while teaching?

Some good side jobs for teachers include tutoring, freelancing, transcribing, blogging, selling lesson plans, and more.

What can teachers do to make extra money?

Teachers can do a lot of things to make extra money, such as jobs like tutoring, freelance writing, blogging, or creating educational printables.

What is a second career for teachers?

Second careers for teachers can include jobs such as educational consultants, curriculum developers, or even working in corporate training and development.

Do most teachers have 2 jobs?

Many teachers have two jobs. This is for many reasons, such as the typically low pay of a teacher as well as teachers wanting to make money while they are off in the summer.

How to make extra money on Teachers Pay Teachers?

Teachers can make extra money on Teachers Pay Teachers by selling lesson plans and printables.

How can teachers make money in the summer?

Teachers can make money when they’re off in the summer by teaching summer school, helping students with test prep, babysitting, selling lesson plans, working at a restaurant, working as a real estate agent, and more.

What to do after quitting teaching? How do you pivot out of teaching?

Quitting teaching and moving on to something else will take a few steps, and you can begin by thinking about your skills and interests. Then, start exploring different job options and connect with people in the field you’re interested in, attend industry events, and consider getting any certifications that you may need.

How can teachers earn extra income through online tutoring?

Sites like Tutor.com look for teachers to tutor students remotely, and you can even offer your services through social media.

How can a teacher make six figures by utilizing their skills?

While it’s not always easy for teachers to earn a six-figure salary, it is possible if you find ways to make extra income or by starting a business of your own.

What opportunities do music educators have for side income?

Side income ideas for music educators can include jobs like giving private music lessons or working as a weekend or evening instructor at a music school. Music educators can also sell lesson plans (I found some examples on Teachers Pay Teachers here).

What are some good side jobs for teachers?

I hope you enjoyed this article on the best side jobs for teachers.

Whether you are looking for side jobs for teachers from home, side jobs for teachers in the summer, or if you want to learn how to make passive income as a teacher, there are many ways to make extra money as a teacher.

Some of the best side hustles for teachers include:

Sell educational printables

Tutor online or in person

Sell your lesson plans

Coach a school sport

Start a dog treat bakery

Sell crafts on Etsy

Sell on Teachers Pay Teachers

Babysit

Teach English as a second language online

Teach summer school

Summer camp counselor

Grade papers

Work at a restaurant

Proofread

Blog

Freelance write

Transcribe

Flip used items for resale

Bookkeep

Sell Canva templates

Rover (walk and watch pets)

Virtual assistant

Food photographer

House sit

Rent out an unused room in your home

Rent your garage space

Rent a photo booth

Online surveys and focus groups

Voice over act

Mystery shop

Fitness trainer

Find random gigs on Craigslist

Deliver groceries

Real estate agent

Driver’s ed instructor

What do you think are the best ways for teachers to make extra money?

You can get an apartment with bad credit, but it may take some strategizing. Apartment applicants with low credit scores can boost their odds by applying with a cosigner, paying more upfront, offering references, or changing the type of units they apply to.

In today’s housing market, you want every possible advantage on a rental application. While letters of recommendation and a solid rental history will get you far, more and more landlords want a high credit score. As a result, it isn’t uncommon to ask if you can get an apartment with bad credit.

While it takes some strategizing, you can get an apartment with low credit. To help you along, we’ll explain how credit impacts your application, explain steps you can take to compensate for low credit, and share tips on boosting your score.

How Credit Impacts Getting Approved for an Apartment

Many landlords and renters run a credit check as part of their rental application process. Like lenders, landlords check your credit to see if you can pay your bills on time. Because renting is an investment, property owners want to minimize risk. So, they assume tenants with high credit are more likely to pay their bills on time.

Remember that your credit score isn’t the only factor on a rental application. While a high score helps, the details on your credit report matter, too. How you got a high or low score can sway property managers one way or the other.

What Credit Score Do You Need to Rent an Apartment?

The score you need depends on the unit. Some rental companies provide an ideal range for their listings. A score of 620 or higher will generally keep landlords from denying your rental application. However, some landlords will expect more, while others don’t look at your score at all.

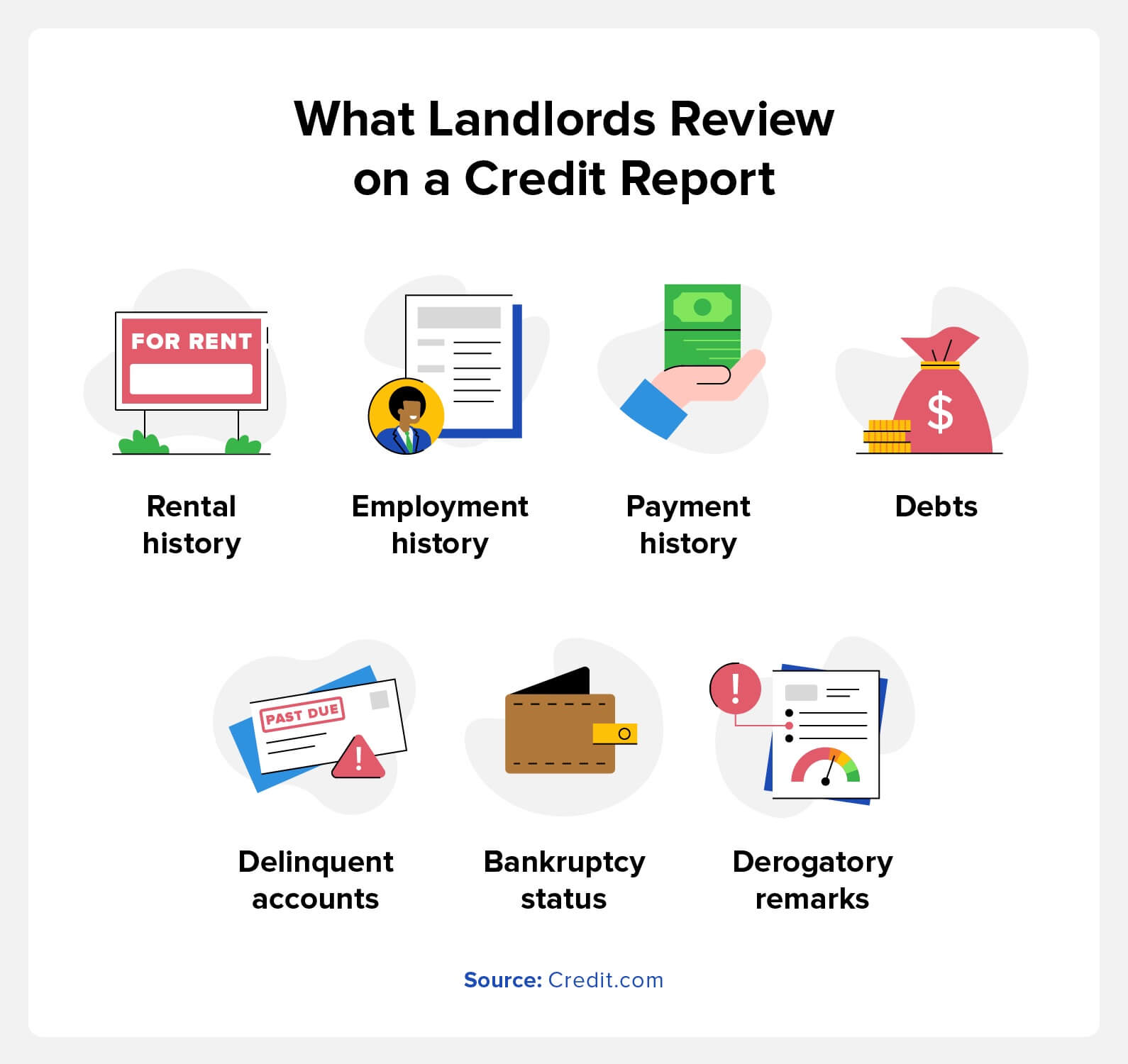

What Do Landlords Look for on a Credit Report?

Renters may treat your credit score like a headline, but there’s more to a credit report than a number. Credit reports tell a story about your spending habits and income. To help landlords pick reliable tenants, a rental credit check includes:

Rental history: Some landlords report rent payments to credit bureaus. As a result, evictions, broken leases, and late or missing payments may appear.

Employment history: Current or past employers may show up on a credit report. Typically, they only appear if you listed them on a credit card application or loan.

Payment history: Credit reports show your history of payments to lenders. Late or missing payments will lower your score and work against your rental application.

Debts: Current and past debts show up on your credit report. By providing payslips, landlords can calculate your debt-to-income ratio. If you make enough to repay your debts responsibly, that improves your application.

Delinquent or collections accounts: An account is delinquent if you miss a payment due date. If you miss enough payments for lenders to transfer your account to a collection agency or sell it to a debt buyer, it becomes a collections account. Both of these hurt your credit score.

Bankruptcy status: Bankruptcy filings will affect your credit score. Landlords may take recent bankruptcies as a sign that you’re a high-risk tenant.

Derogatory remarks: These remarks refer to negative items on your credit report. They include auto repossessions or foreclosures. They hurt your score and hamper a rental application.

Landlords gauge the risk they pose by looking at how applicants spend their money. Someone with a high income but a history of late payments may not make the cut. On the other hand, someone who filed for bankruptcy years ago may be more responsible now.

How to Get an Apartment with Bad Credit

While a low score sets you back, you can learn how to get approved for an apartment with low credit. By following these methods, you can get a leg up in rental applications:

Make an Upfront Payment

Putting down more money upfront can give you an edge on rental applications. Landlords will usually request a security deposit or the first and last month’s rent upfront. To sway a landlord’s opinion, offer the first three months’ rent or put down a higher security deposit.

At the end of the day, renting is an investment. If you can show your landlord that you’ll give them a reliable ROI, it’s all the more likely they’ll accept you. As a bonus, paying more in advance saves you a financial burden for the next few months.

Find a Guarantor or Cosigner for Your Apartment

If a landlord can’t trust you to make payments, you can get someone to sign your lease with you. Someone with a great credit score who signs on with you can assuage a property manager’s worries. However, remember that the person who helps you takes on financial risk. You have two options for this approach:

Cosignerssign a rental agreement with you and share the financial responsibility for it. They must do so on your behalf if you can’t or won’t pay rent.

Guarantors share cosigners’ responsibilities, but they have fewer rights. More specifically, they vouch for you and can make payments on your behalf. However, they aren’t entitled to reside in your unit.

Offer References and Supporting Documents

While credit reports outline your financial history, you aren’t the sum of your spending decisions. You can offer other documents to show your responsibility in an apartment application. Additionally, these documents can prove you can pay rent each month. Some examples of supporting documents include:

Payslips: Offer pay stubs that show you make enough money to pay rent each month.

Letters of recommendation: Reference letters from a friend or employer can attest to your character and responsibility.

Proof of reliable rental history: Account statements and landlord testimonials can prove you always pay rent on time.

A snapshot of your savings account: If all else fails, you can show landlords you have the money to make rent. Be sure to censor sensitive information on your snapshot.

Utility payments: A history of on-time utility payments shows your trustworthiness.

Find Apartments to Rent with No Credit Check

While credit checks are common, not all landlords require one. While these properties aren’t the most competitive, that isn’t always a problem. Apartments with no credit check tend to cost less than ones with one.

If you’re looking for another option, some landlords advertise units with low credit requirements. Again, these properties set a low credit requirement for a reason. That said, if you inspect the unit and it looks good, this route can save you a headache. As you live in low-credit apartments, you can build your score for future applications.

Adjust Your Expectations

If you can’t get around a credit check, reassess the kinds of apartments you can apply for. This isn’t to say you should only apply to units in poor condition. Instead, consider what you’re willing to compromise on. You may have an easier time qualifying for an apartment:

Farther away from your work or downtown area

Without amenities like a gym or pool

That doesn’t include parking

With less square footage than you’d prefer

If you apply with a roommate

Bear in mind that compromising on these points means the apartment may cost less. While living in a less-than-ideal unit, you can save and rebuild your credit while renting. When it comes time to look for a new apartment, you’ll have better odds of getting the one you want.

Tips to Raise Your Credit Before Renting an Apartment

If you plan to send rental applications down the line, you should work to improve your credit. Bear in mind that increasing your credit score takes time. To see a major change, expect months or even a year of work. In that time, follow these tips to improve your credit:

Pay Your Bills on Time

A person’s payment history can make or break their credit score. Central to that payment history: whether you paid your bills on time. Making timely and consistent payments plays a big role in improving your credit score. On top of that, timely payments prove your reliability to a landlord, boosting your chance of getting approved.

Pay Down Any Debt

Paying down debts is one of the best ways to improve your credit score. For this reason, someone who takes on and pays off debt won’t get punished for the debt they take on. Paying off debts shows your fiscal responsibility and proves your finances are on an upward trajectory.

Paying off any kind of debt can improve your score. The main ones to look out for include:

Credit card debt

Student loans

Medical debt

Auto loans

Become an Authorized User for Credit Piggybacking

If you don’t have the resources to boost your credit alone, you can try credit piggybacking. Credit piggybacking lets you benefit from a friend or family member who pays down their debts. By becoming an authorized user on their account, your credit report reflects their payoffs.

You can break the process into a few steps:

Find a friend or family member you trust to spend responsibly.

Become an authorized user on one of their credit cards or lines of credit.

As they pay down their debts, this will show up on your credit report.

By piggybacking on their credit payoffs, your score will improve.

Dispute Credit Report Errors

Sometimes, a low credit score isn’t your fault. Credit reporting errors can come from major credit reporting agencies or the companies giving them information. Credit reporting errors aren’t uncommon, so you should review your report for issues.

Credit reports may contain errors related to:

Accounts held by another person with a similar name to you

Accounts opened by fraudsters who committed identity theft

Closed accounts that still read as open

Accounts incorrectly labeled as delinquent or in collections

Payments that don’t get reflected in your report

Multiple listings of the same debt

Accounts with inaccurate balances or credit limits

To dispute credit report errors, contact the credit bureaus and the company that reported inaccurate information to them. You want to provide supporting documentation that proves the report contains errors. While you can send a dispute by phone, this doesn’t leave a paper trail. Instead, mail a dispute letter or use an online form.

FAQs on Renting an Apartment with Bad Credit

You may still have questions about getting approved for an apartment. To help you out, we’ve answered FAQs on renting apartments with bad credit.

Is 500 a High Enough Credit Score for an Apartment?

You can rent an apartment with a credit score of 500. While it might take you out of the running for expensive units, you should still have a good chance of renting:

Apartments with low credit requirements

Apartments with no credit requirements

Apartments you apply to with a cosigner or roommate.

Can I Reapply for an Apartment After I Get Denied for Bad Credit?

You can apply for the same apartment after getting denied on your first attempt. That said, some renters may throw out your application or ignore it. If you reapply, try to improve your credit and finances between applications.

Do Landlords Need Permission to Run a Credit Check?

Landlords need your permission to run a credit check. The Fair Credit Reporting Act calls rental applications a “permissible purpose.” This gives them the right to view your credit. However, that doesn’t mean landlords can check your score without your consent.

Improve Your Credit for an Apartment with Credit.com

Managing apartment applications is hard enough, even without a low credit score. However, you can get an apartment with bad credit by following the right steps. You’ll see more housing opportunities by learning how credit works, reviewing strategies for getting an apartment with low credit, and following tips to boost your score.

If you’d like a way to streamline raising your credit for rental applications, Credit.com can help. Our rent and utility reporting services ensure that your on-time payment gets reflected on your report. Even if your landlord doesn’t report payments, our tool helps build your credit with every rent payment reported.

This article originally appeared on The Avocado Toast Budget.

This post is sponsored by Credit.com.

Here at the ATB, we are all about budgeting in a way that works for you and finding realistic ways to feel more confident with your money.

Now that 2020 is (finally) over, here are ways that you can start to take hold of your finances and build confidence with your money in 2021.

Write down your short, medium and long term financial goals

I’m a big believer that you don’t need to stress over how to maximize the value of every dollar you come across.

Much of personal finance is behavioral and relies on us finding value in how we navigate our money!

Because of this, I found it incredibly helpful to sit down and brainstorm short, medium and long-term financial goals to decide what I wanted my money to do for me.

Write down your short, medium and long term financial goals

Here’s how I break it up:

Short-term goals – less than two years

Medium-term goals – 2 – 10 years

Long-term goals – 10+ years

Feel free to dream big!

We want to make realistic and attainable goals, but we also want to allow ourselves to dream about what we really want our lives to look like, and how our money plays a role in that.

Get to know your credit score

Wanna know a secret? I avoided my credit score for the longest time.

Turns out, once I finally faced my credit score, I became more empowered to understand how my credit score affects my finances and what I could do to change it.

While free resources can give you a ballpark estimate of your credit score, that score isn’t very useful and certainly isn’t what creditors see!

Knowing your true score, and seeing your credit reports from all three major credit bureaus, gives you security and control over how to navigate your credit score going forward.

While it can be daunting, credit plays an important role in our lives from renting, to car insurance, to mortgages, to career opportunities and more.

That’s why it’s important that you stay informed of what your credit actually looks like that’s why I signed up for ExtraCredit’s free trial!

Set up automatic savings

Automating your savings is LIFE CHANGING.

Setting up automatic savings is often referred to as “paying yourself first” because you are prioritizing saving money for Future You.

There are tons of different savings goals that you can put this money toward, but the important part right now is to set up automatic savings so you can set it and forget it.

Trust me—you miss that money a lot less if you never see it in your account in the first place.

If you have automatic deposits at work, it’s super easy to add a savings account and have a certain % or dollar amount go into that account every month without it EVER hitting your checking.

In my opinion, this is the best way to go. Out of sight, out of mind.

You’re way less likely to touch this money, and you’ll be shocked at how much it grows over time!

If this isn’t an option for you, you’re not out of luck. You can set up automatic savings transfers into your savings account from your checking account through your bank.

Find a budget that works for you

Here at the ATB, we are all about budgeting in a way that makes sense for you and your life.

Budgeting doesn’t have to be stressful and restrictive. It should actually be freeing and allow you to feel more confident and in control of your money!

There’s no one right way to budget, and there are TONS of different types of budgets depending on your income and financial goals.

Personally, I use a zero-based budget which allows me to track and decide where every single dollar I have is going.

If you have big savings goals, low income or high debt, I definitely recommend checking out a zero-based budget.

Learn how to increase your credit score

Your credit score has a bigger impact on your life than just determining your eligibility for loans.

Credit can impact your ability to rent, job opportunities, car insurance rates and more.

Once you know what your credit score is, it’s important to understand what makes up your credit score, and what steps you can take to increase it.

There are five factors that influence your credit score:

Payment History

Amounts Owed

Length of Credit History

New Credit

Credit Mix

Payment History makes up 35% of your credit score, so it is the most important factor.

ExtraCredit gives you the ability to report rent and utility payments, adding new tradelines to your credit profile. Adding payment history to your credit file.

And if you need help working to repair your credit, you can also use the Restore It feature to get an exclusive discount from a leading credit repair company. Remember: your best credit score is an accurate one.

Understanding how to increase your credit can take a lot of stress out of your finances and help you feel more in control of your credit future.

Make a debt payoff plan

I paid off $20k in CC debt in less than a year, and in order to do that, I needed a concrete plan of how I was going to tackle my debt.

Prior to that point, I had just been throwing a little bit here and there, hoping that my balance would eventually decrease.

Shockingly, that never happened.

Once I decided to use the debt avalanche to tackle my credit card debt, I was able to calculate how much extra money I could throw at my debt every month in order to make progress toward my debt free goal.

With this method, I paid the minimum payments on all of my debt except for the one with the highest interest.

With the highest interest debt, I put any extra money I had toward paying that down.

This gave my money more of a purpose than just throwing extra money here and there at my different debts.

It was also reassuring and motivating to see the loan amount decrease drastically as I threw the extra money I had towards it.

One interesting aspect of the home loan process is the sheer number of individuals you’ll work with along the way.

You don’t just speak to a salesperson and call it a day. Lots of people are involved in what is a very complex transaction.

Aside from salespeople, there are loan underwriters, processors, appraisers, escrow officers, real estate attorneys, and more.

Let’s discuss the roles these people hold to help you better understand what it takes to get a mortgage.

Remember, you’re asking to borrow a large sum of money, so it’s going to take time and energy (and lots of people) to get to the finish line.

The Sales Rep/Loan Officer/Mortgage Broker

The first step in the home loan process typically involves a sales person, which can be a banker at your local branch or credit union, a loan officer, or a mortgage broker.

If we’re talking about a purchase, this may come before/during your home search or after you’ve found your property with the assistance of a real estate agent.

If it’s a mortgage refinance, you’d simply jump right to this step to rework the details of your existing home loan if you wanted a rate and term refinance or a cash out refi.

You might be referred to an individual/company, or you might do your own discovery to find a suitable partner. Either way, always look beyond the referral you were given.

Your real estate agent might know a great lender, but you your own research as well.

It’s important to gather multiple quotes from different companies to ensure you get the best deal.

Now, this individual will be your main point of contact during the loan process, and perhaps most importantly, will provide you with pricing.

Bankers and loan officers work at the retail level, while mortgage brokers offer wholesale rates from their lender partners.

You can read more about the differences (banks vs. brokers) but either way they’ll likely be the person you speak with most.

Aside from providing pricing, these individuals can help get you pre-qualified or pre-approved for a mortgage, discuss different loan scenarios, and guide you on loan choice.

If you have mortgage questions, they should be able to provide answers and give you guidance.

They may make certain recommendations, such as down payment amount, loan type, or provide an opinion about paying discount points or when to lock your rate.

This individual will be with you from start to finish, but doesn’t work alone. They’ve got an entire team to help you close your loan in a timely fashion.

FYI, you may also come across a “mortgage planner,” which is an individual who may assist a busy senior loan officer.

They can communicate loan status, provide follow-up, collect conditions, and perform other tasks if the LO is unavailable or simply needs a hand.

The Loan Processor

Once you’ve spoken to a sales representative (or LO/broker) and have decided to move forward, you’ll be in put in touch with a loan processor.

The main goal of the processor is to put together a clean loan file that can be submitted to the underwriting department.

This means collecting key documents, ensuring there are no red flags, double-checking everything, and making any necessary corrections.

The processor may also reach out after the loan is approved to collect additional documents to satisfy any outstanding conditions.

They will also provide updates to the loan officer or broker, who will then keep you in the loop about where you’re at in the process.

The processor essentially acts as a liaison between the underwriter and sales rep/LO/broker.

This ensures things move along smoothly and any hiccups can be resolved quickly without delay.

The Loan Underwriter

The loan underwriter probably holds the most important role in the home loan process.

They decide if the mortgage is approved, declined, or potentially suspended pending further explanation.

It’s for this reason that the loan processor only sends the loan package to the underwriter once everything has been thoroughly checked.

You only get one chance to make a first impression, so it’s imperative to get it right. Otherwise you could face delays or simply get flat out denied.

Aside from approving the loan, the underwriter will also provide a list of conditions needed to close the loan.

Most mortgage approvals are conditional, meaning you might need to furnish additional information or documentation to obtain your final approval.

Once these documents are provided, whether it’s another bank statement or letter of explanation, the underwriter will clear the outstanding conditions and move the loan to the funding department.

The Home Appraiser

While your loan is being reviewed by the underwriter, an appraisal will be ordered to determine the value of the underlying property.

Remember, aside from determining your ability to repay the loan, the bank also needs to ensure the collateral for the loan is valued properly.

This individual will visit the property to assess its condition, take photographs, and determine recent sales comparisons.

They will formulate a valuation based on the property details, such as number of bedrooms and bathrooms, square footage, amenities, location, lot size, condition, and so on.

The value they come up with, known as the appraised value, is used as the basis for the loan-to-value ratio.

Generally, the goal is for the appraiser to support the purchase price of the property or the value declared for a refinance.

If the value is lower, the details of the loan may need to be reworked, such as a higher down payment.

For certain types of loans, such as FHA loans and VA loans, the home appraiser will also ensure that certain Minimum Property Requirements (MPRs) are met.

This ensures the property is safe for the occupants, that there are adequate living conditions, and no major hazards, such as lead paint or termites.

The Home Inspector

If we’re discussing a home purchase, you’ll want to get an inspection done. And you’ll want to do it ASAP while any contingencies are still in place.

While a home inspection typically isn’t required, they’re generally a good idea.

Aside from finding out what’s potentially wrong with the property, you can ask for credits from the seller if the inspector finds any significant issues.

As the name suggests, a home inspector will come out to the property and assess the condition of the structure itself, the foundation, the interior, the roof, the electrical, HVAC, and more.

Some may also inspect the pool and spa, if one exists, though you could be charged extra.

They’ll make notes as they survey the property and issue a formal report afterwards. This can be used to negotiate with the seller if anything material comes up.

The Notary Public

Once it’s time to sign your loan documents, you’ll need to make an appointment with a notary public.

This individual serves “as an impartial witness” when signing important documents, such as those related to a home purchase or mortgage loan.

Your settlement agent should organize a time to meet with this individual to conduct your signing.

The notary may come to your home or meet you somewhere else to review and sign documents.

The main job of the notary is to verify the identity of the signer and ensure they are willing to sign the documents “without duress or intimidation.”

This requires you to furnish identification, such as a driver’s license, during the signing appointment.

The Escrow Officer

Another very important individual in the transaction is the escrow officer, a third-party who facilitates the loan closing and collects/disburses funds to the appropriate parties.

Some of their key roles include preparing final statements for the buyer, such as cash required to close, and determining costs such as property taxes, insurance, prepaid interest, and loan payoffs.

The escrow officer will send you a settlement statement that lists all the fees and closing costs associated with your loan, along with any lender credits and loan payoffs and funds required.

They will also liaise with a title company and forward necessary documents for loan recording.

Importantly, they’ll provide wiring instructions to all parties, including the buyer, so you know where to send funds (cash to close).

If you have questions about things like prepaid items, mortgage impounds, and loan payoffs, they can be particularly helpful.

The Title Agent

To ensure the property is free of any liens, encumbrances, or defects, a title insurance policy is usually required in order to take out a mortgage.

A title agent is the individual who conducts a title search, orders a preliminary title report, and eventually issues title insurance on the subject property. This makes them a licensed insurance agent

They are also in charge of recording the deed and loan documents with the county once the loan has funded.

You might hear the words title and escrow used interchangeably, but title has to do with property ownership/lien history, while escrow is about the calculation, collection, and disbursement of funds.

However, they may perform other settlement tasks beyond just title depending on the state where they’re located.

The Loan Closer/Funder

If you’ve made it this far, it means the loan is almost funded. But there’s still work to be done.

The loan closer/funder has to review the file to ensure everything is accurate and complete, and if not, address and fix any errors or outstanding issues.

They must ensure all prior to funding (PTF) conditions are satisfied and work with the settlement agent to prepare funding figures and timing of disbursement.

This includes the review of signed closing documents and items like hazard insurance and the preliminary title report.

And if everything looks good, request the wire instructions from escrow after a thorough review.

The Real Estate Attorney

Note that in certain states, a real estate attorney could be required to prepare certain documents and/or to conduct the loan closing.

This individual may order and certify a title report, review loan documents, and advise you if necessary.

Beyond that, they can ensure the interests of all parties are protected, and handle any legal issues or disputes that may come up.

One last thing. You may find that there is some overlap with a title company and escrow company, as the former can also provide escrow and notary services as well.

So depending on where you live, you could have one company or individual handle several tasks.

As you can see, there are quite a few people involved in the funding of a home loan, which explains why they take a month or longer to close.

Once you know more about each person’s role, it should be easier to navigate the home loan process and make better sense of it all.

And perhaps adjust your expectations that there isn’t a same-day mortgage and likely won’t be for the foreseeable future.

The mortgage market faces a turning point, experts say, asnew fixed mortgage rates have stayed below variable rates for several months and predictions grow that the cash rate has peaked.

National Australia Bank and Westpac last week became the latest banks to reduce some of their fixed rates, with both lenders dropping certain two-year rates, following cuts from the Commonwealth Bank in August.

For the first time since January last year, the average fixed rate dipped below the average variable rate in May.Credit: AFR

Chief executive of mortgage broker Finspo, Angus Gilfillan, said new fixed interest rates had crossed a pivotal threshold, dipping below new variable rates for the first time since January 2022.

“The current situation suggests an inflection point, where the market no longer expects interest rate rises to occur in the medium term,” he said.

While the average new variable rate has increased 2.5 percentage points to 5.95 per cent over the past year – exceeding the 1.75 percentage point increase in the Reserve Bank cash rate over the same period – Gilfillan said average new fixed rates increased by a more modest 1.7 percentage points to 5.8 per cent.

Fixed rates, which have traditionally played a small part in Australia’s home loan market, tend to reflect the money market’s view on the future path of the cash rate.

“Fixed rates are historically higher than variable rates when rate hikes are expected on the horizon,” Gilfillan said.

Some economists have called a peak in the Reserve Bank’s cash rate, forecasting a fall as early as March. While some fixed rates have fallen lately, RateCity figures still show the majority of recent fixed-rate changes have been increases.

Advertisement

RateCity research director Sally Tindall said the major banks’ reductions recently could be an early sign some fixed rates are on their way down. At the same time, banks have been trying to rein in some of the more aggressive discounts they are offering on variable-rate loans, and Tindall said none of the big four banks had an advertised variable rate under 6 per cent.

Westpac last week raised one of its advertised variable rates for new customers, and Tindall said this was the 22nd rise to new customer rates from a big four bank since March. She said this trend showed “a strategic move to walk away from the cut-throat competition in the home loan market”.

She said it was unlikely that variable rates among the big four would return below 6 per cent until the Reserve Bank began cutting the cash rate.

As banks raised their variable rates, the number of customers choosing to fix their home loans has risen, albeit from low levels. Gilfillan said the proportion of customers choosing fixed rates had doubled over the past three months to 9.4 per cent in July, although it remains below the peak of 46 per cent in July 2021 when banks were offering ultra-low fixed rates.

Morningstar analyst Nathan Zaia said banks may have lowered their fixed rates recently to attract customers who were coming to the end of their previous fixed-rate contracts.

“The banks are probably looking for a way to lock their customers in, at least for a few years,” he said, as the mortgage rate cliff plays out.

Banks have signalled their intentions to walk away from cut-throat competition in the past few months in an effort to protect their margins, and have been less generous in some of the discounts they are offering customers on variable-rate loans.

“The banks are still offering very competitive pricing, but they’re not competing as hard,” Zaia said.

Once banks have made their repayments to a pandemic-era RBA funding program called the term funding facility (TFF), Zaia said the intensity of competition would probably fade.

“If the cash rate starts falling, they may not pass all the decreases on to borrowers,” he said. “Once they’re past the TFF repayments, banks will have more flexibility and there’s really little incentive for them to compete hard.”

The Business Briefing newsletter delivers major stories, exclusive coverage and expert opinion. Sign up to get it every weekday morning.

Millie Muroi is a business reporter at The Sydney Morning Herald covering banks, financial services and markets.Connect via Twitter or email.

Looking for jobs where you work alone? If you’re an introvert or simply want minimal human interaction, here are 40 ideas.

Looking for the best jobs where you work alone? If you’re an introvert or simply want minimal human interaction, here are 40 ideas.

With there being so many different types of jobs out there nowadays, more and more people are looking for jobs where they can be by themselves, away from the busy office or customers. They find comfort in jobs where they can do tasks on their own, letting them really concentrate and do well in what they do best.

For me, I have worked mostly alone for over a decade now, and I wouldn’t change it for the world. I enjoy the flexibility of working on my own and having less stress.

Jobs that let you work this way are usually appealing to introverted individuals, those who like a calmer setting, or people who just work better with more independence.

Knowing which jobs let you work alone is really important for those who want to find the right mix of being on their own and getting things done well.

Top Jobs Where You Work Alone

There are 40 jobs where you can work alone listed below. If you want to skip the list, here are some jobs that you may want to start learning more about first:

Benefits of Jobs Where You Work Alone

More and more people are looking for jobs where they can work alone, and I get it! I have been working mostly alone for over a decade and I really love it.

After all, a person spends so much of their time working, so you might as well like what you’re doing. If you’re an introvert, or if you like working by yourself, there are jobs where you can do just that.

Some of the positives of working alone include:

Less stress if you’re an introvert – If you’re an introvert, then you may feel stress when working with other people, such as coworkers and customers.

Getting more stuff done in less time – Working alone may mean that you can complete your tasks faster because there are fewer distractions.

Having a more flexible schedule – Some jobs where you work on your own sometimes let you choose when you want to work, as long as you get the work done.

If you’re looking for jobs where you work alone, think about what you’re good at and what you enjoy (and also think about what you don’t like!).

40 Jobs Where You Work Alone

Below are 40 jobs where you can work on your own. The jobs below range from earning a part-time to a full-time income too.

1. Proofreader

Proofreaders check and edit written content for errors and inconsistencies, and this job requires strong attention to detail and excellent grammar skills.

If you’re good at paying close attention to details, then proofreading could be an ideal work-alone job for you.

Authors, website owners, and students often hire proofreaders to improve their work. There’s a high demand for proofreaders, and you can find jobs through many different platforms.

Even the most skilled writers can make mistakes in grammar, punctuation, and spelling. That’s why hiring a proofreader can be very helpful for pretty much anyone and everyone.

If you want to find online proofreading jobs, I recommend joining this free 76-minute workshop focused on proofreading. In this workshop, you’ll learn how to begin your own freelance proofreading business.

Recommended reading: 20 Best Online Proofreading Jobs For Beginners (Earn $40,000+ A Year).

2. Virtual Assistant

One of my first side jobs was as a virtual assistant and it was a fun and flexible way to earn income. While you do have a boss when you are a VA, a lot of the tasks that you do will require you to take charge and complete them by yourself in your own home.

A virtual assistant is someone who helps people with office tasks from a distance. This could be from your home or while you’re traveling. It might include things like replying to emails, setting up appointments, and managing social media accounts.

This job can pay you more than $50,000 each year.

If you want to find part-time or full-time virtual assistant jobs, I recommend joining the free workshop called “5 Steps To Become a Virtual Assistant“.

Recommended reading: Best Ways To Find Virtual Assistant Jobs

3. Bookkeeper

Bookkeepers are people who keep track of all the money-related things for businesses such as writing down sales, keeping a record of expenses, and making financial reports.

This is a job where you can work alone and a typical salary is $40,000+ each year. Plus, you’ll mainly be dealing with numbers and not people.

You can join the free workshop that focuses on finding virtual bookkeeping jobs and how to begin your own freelance bookkeeping business by signing up for free here.

Recommended reading: How To Find Online Bookkeeping Jobs

4. Blogger

Blogging is a great way to make money while working on your own. It’s one of the reasons I really enjoy it, haha! I get to work by myself, for myself, and I can pick the projects I want to work on.

As a blogger, you write content for others to read online. You get to choose what you want to write about as well as how you want to make money blogging because there are so many different options (like affiliate marketing or displaying ads).

You can begin a successful blog about a specific topic like finance, travel, lifestyle, family, and many others.

Blogging is my main source of income, and it has completely transformed my life. I have the freedom to travel whenever I want, set my schedule, and be my boss.

Since I began Making Sense of Cents, I’ve made more than $5,000,000 from my blog. I earned this money by working with companies through sponsored partnerships, affiliate marketing, display ads, and selling online courses.

Learn more at How To Start A Blog FREE Course.

5. Delivery Driver

Delivery drivers pick up and drop off packages. And, they get to work by themself most of the time as they are in the vehicle alone.

A delivery driver may drive a car, truck, or even a bike, depending on the company they work for. They don’t usually have a boss watching them all day nor have to deal with very many customers for long periods.

6. Book Reviewer

Book reviewers read books and share their thoughts in book reviews.

There are websites where you can get paid for sharing your thoughts about books and you may earn money through PayPal or a bank transfer, and sometimes you get to keep the book you reviewed.

They don’t just want positive reviews either, they want to know what you really think! You see, authors and publishers like to send out free copies of their books so that they can get honest opinions. Just like us, they know it’s helpful to read reviews before deciding if a book is worth the time.

Some sites that pay for book reviews include Online Book Club, Kirkus Media, and BookBrowse.

Recommended reading: 7 Best Ways To Get Paid To Read Books

7. Deliver RVs or Cars