If you’re interested in the world of real estate, the first thing you must do is become licensed. Once you meet the requirements and take and pass the licensing test, you can begin to sell houses to happy families, and with hard work, you can make a good living. Many people give up before they start because they fear taking the licensing exam, but with proper research and an understanding of the job, you can pass the test and start building your brand.

What To Know Going In

Before hitting the books and taking the time to get your real estate license, you must know what you can do with that certification and the other skills you’ll need that aren’t always taught in school. First, know that there are many different jobs that you can perform once you get your license. In addition to selling houses, you can work as a property manager, real estate attorney, home inspector, real estate photographer, and more. So, if any of those titles interest you, read on and consider your license.

Stay On Top Of Trends

While you’ll be learning a lot during your license classes, remember that your education doesn’t stop just because you passed the test. As time goes on, it’s necessary to stay on top of current news and trends so you can be the best agent you can be. For instance, you’ll want to learn how climate change impacts the real estate industry. Weather and rainfall can impact desirable locations around the country, and you may get questions about how climate change can affect property values.

Along those lines, you should keep up-to-date on industry data and trends such as the growing interest in eco-friendly homes. You should know which sustainable home upgrades have the greatest return on investment such as solar panels and energy-efficient doors and windows. If you are working with a seller, you can advise what financing options your client has to finance upgrades such as home equity and Federal Housing Administration loans. Home buyers will likely have questions in this regard, and you’ll want to have the answers.

A Positive Self Image Is Essential

While certification and a license are essential, so is having a positive self-image because it’s a way to enhance your professional opportunities in the real estate world. When you’re confident in yourself, and it shows, your clients will have more confidence in you. By practicing self-care and dressing for success, you give off the impression that you care about yourself and what you do, and clients will respond positively to what they see.

You can build your self-confidence by setting goals for yourself, like selling a house in a certain price range and then celebrating that accomplishment.

Application Steps And State Requirements

When you’re confident that you want to continue a career path as a real estate agent, you need to get your license. Note that every state may have different requirements, so do your research to ensure you follow the right steps. In many cases, you may first be required to pass a background check so the state can ensure that you’re honest and have the integrity necessary to handle a client’s personal information and discuss sensitive financial topics.

Next, you will likely need to complete various classes to learn about real estate and get the information necessary to pass your licensing exam. Some states require over 100 hours of pre-licensing courses, including those about real estate principles, finance, and how to complete essential forms. Keep in mind that these classes and the eventual application will cost money. According to The CE Shop, you can expect to pay between $300-$1,000, depending on the state.

After completing those classes, most states will require you to pass a pre-license course final exam to ensure that you’ve retained the information you’ve been taught. Get past that, and it’s time to apply for a license. The application will ask about your personal information, and you’ll also need to submit copies of your exam score and work authorization.

Finally, you’ll take your state licensing exam. You’ll have a certain time frame to take the test, and you’ll need to get a score according to your state guidelines. After you pass, you can join a real estate broker and gain experience out in the field.

What To Do Moving Forward

While obtaining your real estate license is a significant task, this is only the first step you’ll need to take during your long career as a real estate agent. Your education is far from over. Your particular state may require that you follow continuing education requirements. For example, in Delaware, you’ll need to take post-licensing courses 90 days after you’ve received your initial license, and in Indiana, you’ll be required to take 30 hours of post-licensing education within the first two years of being licensed.

There are also additional titles that you can gain over time to supplement your education and potentially earn more money. Some of these designations and certifications include a GREEN Designation, which provides the tools to help you understand and market properties with green features that customers are so excited about. You could also become a Certified Residential Specialist. Doing so will help you to learn more about the industry and potentially earn three times as much as agents who don’t have the designation.

Finally, while securing your license and certifications and learning the ropes, take the time to build your brand and make a name for yourself. Invest in professional photos and create a website to build your online presence. Start networking with other agents by attending industry events and seminars. Remember that you won’t be a success overnight, but by working hard and keeping your eye on the prize, you will find success.

Conclusion

These are the basic principles to remember when applying for and obtaining your real estate license. Remember to research the rules in your state to ensure you’re fully compliant. Once licensed, take on the world one property at a time.

Find topics in marketing, technology, and social media for realtors, and housing market resources for homeowners. Be sure to subscribe to Digital Age of Real Estate.

Mortgage rates have risen to their highest levels in more than 20 years, making it harder to afford a home. And yet, out of necessity or desire, hundreds of thousands of people buy homes every month.

With the 30-year fixed rate topping 7%, NerdWallet asked real estate agents and mortgage loan officers for advice on how home buyers can stretch their homebuying dollars in this time of high interest rates. Here are nine tactics that they suggested.

1. Ask the seller to reduce the mortgage rate

Temporary mortgage rate buydowns have become commonplace since rates surged in early 2022. With a temporary rate buydown, the seller pays a portion of the buyer’s interest payments upfront. This reduces the house payments for the first one, two or three years of ownership.

“This is a common strategy for new-home builders, but it can also be used in the purchase of resale homes,” said John Bianchi, executive vice president for loanDepot. (All sources in this story commented via email.) “Negotiating a temporary buydown with the seller can help soften the blow of high interest rates, reducing your monthly payment for one to three years.”

In one typical setup, the seller’s payment effectively cuts the buyer’s interest rate by 2 percentage points in the first year, and by 1 percentage point in the second year. After that, the buyer pays the full interest rate. This is known as a 2-1 buydown.

Another option is to reduce the mortgage rate permanently, using discount points. One discount point equals 1% of the loan amount; each point typically reduces the interest rate by around 0.25 percentage point.

“Home buyers have an opportunity to get a seller to pay for these methods to lower their interest rate,” said Chuck Vander Stelt, a real estate agent in Valparaiso, Indiana. “Some home buyers should seriously consider offering a more generous price to the seller in exchange for a large closing cost concession and then use those funds to buy down the interest rate as much as possible.”

2. Use part of your down payment to pay down debt

When you apply for a mortgage, the lender considers your total debt payments for the house, car, student loans and credit cards. Sometimes it makes sense to divert some of your intended down payment money to cut the higher-rate debt first, said David Kuiper, vice president and senior mortgage banker for Dart Bank in western Michigan.

“While the mortgage payment will be slightly higher, the total debt/payments is lower, making the proposed purchase more affordable,” Kuiper said.

3. Use home buyer assistance programs

State and local governments sponsor an abundance of programs to make homes affordable for home buyers, especially first-timers. Some programs offer down payment assistance and help with closing costs. Others offer favorable interest rates or tax credits.

Details differ from state to state. Some programs are targeted to certain counties, cities or neighborhoods. Others are intended for specific groups of people, such as teachers, first responders or renters who live in public housing. Some programs have income limits.

4. Ask the seller to finance the purchase

You can give the seller an IOU for part of the home’s value and make monthly payments directly to the seller at an interest rate that’s lower than you could get from a bank. This arrangement is called “seller financing” and has its roots in the early 1980s, when mortgage rates zoomed as high as 18%.

You might wonder why a seller would agree to such a deal. “They will often do this in order to get the price they want,” said Janie Coffey, who leads the Coffey Team with eXp Realty in St. Augustine, Florida. The seller gets full price while you get a break on the interest rate.

Seller financing usually has an end date: Within three, five or 10 years, the buyer must get a mortgage from a lender to pay off the amount owed to the seller. Coffey explained that the type of seller open to this arrangement often has paid off the mortgage “and is OK to wait for their big payoff.”

Seller financing is complex. Use an experienced real estate attorney to draw up the contract.

5. Don’t wait for a rate you like better

“If the right house comes along and the payment is affordable (even if you don’t like the interest rate), you should buy the house,” Kuiper said.

You often hear that you should buy now and refinance someday, after interest rates fall. That’s not Kuiper’s point. His point was this: If mortgage rates fall, more buyers will rush into the market. They’ll make competitive offers and drive home prices higher, “essentially wiping out any advantage of the lower interest rate.”

6. Don’t get distracted by things you don’t need

Some sellers want flexibility about the closing date, would prefer the buyer to make repairs, and are scared of accepting an offer from a buyer who ends up failing to qualify for the mortgage.

Vander Stelt advises staying focused on price with these hassle-avoidant sellers, while being flexible on the rest of the offer on the house. “Do this by offering the best terms you can, including buying the home as-is, a closing date and possession that works best for the seller, and illustrating how strong of a candidate you are to get your mortgage approved,” he said.

You can demonstrate that you’re a strong mortgage candidate by showing a preapproval letter and by sharing financial information, such as account balances that prove you have the cash for the down payment.

7. Buy a house that needs work

Buying a fixer-upper is an old-fashioned, time-tested way to save money. “If you can be patient, it’s worth buying a home that needs work and slowly fixing it up over time or taking a renovation loan to acquire the home and do the work upfront,” said Brian Koss, regional sales director for Movement Mortgage, in Danvers, Massachusetts.

8. Build a house or buy a brand-new one

“Building a new home can provide more certainty around how long you will have to wait to move in, it can provide more cost certainty, and it can save you money in the short and long term by avoiding costly remodels, appliance repairs and unexpected repairs of older parts of the home,” said Jeffrey Ruben, president of WSFS Mortgage in the Greater Philadelphia area.

Buying a new home in a development has some of the same advantages. And today’s buyers have good reason to shop for new construction because there’s a shortage of existing homes for resale.

9. Rent out part of the house

Coffey suggested using an old strategy with a trendy name — house hacking — “buying a property like a duplex, where you live in one unit and rent out the other,” she said.

If you buy a duplex, triplex or quadplex, and you live in one unit, you can include the expected rental income for the others when qualifying for a loan. In some cases, you can qualify for a mortgage using expected rental income from an accessory dwelling unit, such as a basement apartment or a tiny house in the backyard.

If you buy a home today, you’re stuck with high mortgage rates for the time being. But by employing some creativity, you might find a way to afford homeownership.

Real estate attorney Lauren Griffin said UCC liens ‘are a new kind of fraud that we haven’t seen before.’

NEW ORLEANS — David Bryan and his wife Annemarie Ellgaard both grew up in New Orleans, met at Tulane University and sent their daughter to their alma mater. A quarter century after moving away to Minneapolis, they bought their forever home Uptown and decided to retire back in the Crescent City.

But their dream was nearly derailed this spring, by something that looked like typical junk mail. Bryan almost threw away a letter from a California lender called GoodLeap, thinking it was solicitation for a home equity loan. It turned out to be a statement for a $45,000 loan taken out in his name, without his knowledge, to cover new doors and windows that he never ordered and were never installed.

“GoodLeap paid the construction company directly,” Bryan said. “They didn’t have any proof that the work was done or anything. They just took their word for it that the work was done, paid them directly the $45,000… If it didn’t happen to me, I’d sit back and think, boy, this is ingenious.”

WWL Louisiana has learned that GoodLeap accepted more than three dozen loan applications with New Orleans property owners’ real names and addresses, but automated signatures and fake Social Security and telephone numbers. Law enforcement sources confirm that GoodLeap paid loans for about 20 of those applications directly to Metairie contractor Deep South Renovations, based on automatic signatures from Deep South’s owner, Samantha McGee.

GoodLeap says it’s a victim of fraud and is working with the FBI field office in Sacramento, Calif. But property owners say GoodLeap failed to perform basic due diligence to confirm their personal information before releasing the money to Deep South and slapping a UCC lien on their properties – liens that prevented some of them from taking out legitimate loans or selling their houses.

“To protect consumers and GoodLeap itself, GoodLeap has an extensive due diligence and fraud prevention process,” said Jesse Comart, GoodLeap’s executive vice president for communications. “GoodLeap is also a victim of this fraud. And we certainly regret that these innocent consumers were also swept up in this fraud.”

Stealing Social Security numbers

Comart said GoodLeap was victimized by “a highly sophisticated group that appears to have the ability to create or obtain fraudulent (Social Security Numbers), and then associate the SSNs with innocent property owners.”

GoodLeap has canceled 20 UCC liens in New Orleans alone since August. Comart said the lender has canceled all loans it identified as fraudulent but declined to say how many were specifically associated with Deep South and how much McGee’s company received, citing the pending FBI investigation.

But it appears Deep South used more than one lender to collect bogus home-improvement loan proceeds. Quentella Livers found out Deep South collected $45,000 on a loan from GoodLeap to put solar panels on her house, using a fake application using her maiden name, Richard. Not only did she not get any solar panels, but she also discovered a second UCC lien for new floors and other home improvement work she didn’t get. She said she then found out another California lender, Dividend Solar Finance, had paid Deep South $54,000 for that bogus loan.

She managed to get GoodLeap to cancel its lien in August. Dividend just canceled its lien last week.

“It’s taken a lot out of me. It’s been a whirlwind,” she said.

Real estate fraud has been on the rise this year, with scammers using automated signatures to falsify deeds in attempts to sell properties out from under the rightful owners. But real estate attorney Lauren Griffin said UCC liens “are a new kind of fraud that we haven’t seen before.”

Griffin, a lawyer at New Orleans based Crescent Title, said she got a call this summer from a client about a GoodLeap lien that he didn’t even know about until another victim called to warn him.

“Fraudsters are trying anything they can right now,” she said.

Loans taken out in the victims’ names

The first warning came from a Gentilly property owner, who researched the Orleans Parish property records, then spoke to eight others who all said GoodLeap had placed UCC liens on their properties and paid Deep South Renovations $45,000 for work at their houses that was never done.

Livers said if it hadn’t been for the Gentilly man writing her a letter to warn her, she might not have known about the $45,000 GoodLeap loan or the $54,000 Dividend loan in her name.

“I figured that I couldn’t possibly be the only victim,” said the Gentilly man, who didn’t want to give his name because he filed a police report against McGee and said he’s concerned for his safety. “It’s really galling that somebody can get away with this so easily.”

Bryan, Livers and the Gentilly man say they have been interviewed by FBI agents about McGee. The FBI’s Sacramento field office said it could not confirm or deny an investigation. But the New Orleans Police Department confirmed its White Collar Crimes Unit is investigating.

Deep South appears to have walked away with close to a million dollars in bogus loans, even though its state contractor’s license has been revoked and its office in Metairie is a vacant storefront. McGee is also facing financial default in multiple court cases.

In one of them, a Jefferson Parish judge ordered McGee to pay Louisiana Pain Specialists more than $400,000 on a debt that’s been in default for more than two years. Court records show she failed to show up for a garnishment hearing last month and the judge issued an attachment for her arrest.

Also this summer, she was renting a townhouse in Metairie and entered a bond for deed agreement to purchase the home over time. The seller, Ronald Lopiparo, said she only paid half of the $100,000 down payment and hasn’t made any of the monthly purchase payments since. He issued a default notice last week and says he plans to evict her.

The U.S. Marshals Service confirmed agents went to the townhouse in tactical gear in April 2022. Brian Fair, a U.S. Marshals spokesman, said McGee was arrested for failing to show up in federal court on a separate matter.

Neighbors saw McGee pull up in her late-model Mercedes earlier this week and WWL Louisiana went to knock on her door shortly after she entered the house, but she wouldn’t answer the door. She hasn’t answered any phone calls or text messages over the last few weeks, either.

How to protect yourself

Griffin says property owners can do a few things to protect themselves against fraudulent UCC liens. They can freeze their credit. They can also sign up for notifications whenever a new document is filed in the land records. That service is available through the Jefferson and St. Tammany parish clerks offices, but not yet in Orleans or St. Bernard parishes.

Orleans Parish Chief Deputy Clerk Alexandria Irvin said Orleans is in the “testing stages of our Land Records courtesy real estate notification service with an anticipated launch date January 2024.” She said property owners will have to register an email address to receive the alerts.

Selling a house amid a divorce can make an already-complicated situation even more complex. The need to manage a real estate transaction while also managing your interpersonal conflict is stressful, but sometimes financially necessary. Every couple’s situation will be a little bit different, of course, but if you need to sell the marital house due to a divorce, here are answers to some common questions and other things to consider during this difficult process.

Should I sell the house before getting divorced?

You can sell a property before, after or during a divorce, and the best option may be different for each couple. A number of factors can impact the best timing, including housing market conditions, how amicable your split is and the financial needs of each spouse.

One thing that can be useful is to work with a real estate agent who has experience in divorce transactions. “The common denominator for a divorce sale is that the divorcing parties must mutually agree to sell the marital property,” says Lou Rodriguez, an agent with United Realty Consultants in South Florida and author of “Selling Your Home During Divorce: How Everyone Can Win.”

An additional consideration for the timeline of your home sale is the potential profit you stand to make. If the value of the property has gone up significantly since you purchased it, you may have to pay capital gains tax, and the amount is very different depending on whether your taxes are filed jointly or as single individuals. For single tax filing status, you must pay taxes on anything over $250,000 in capital gains. That number doubles to anything over $500,000 if you file jointly as a married couple.

If you sell before the divorce is finalized, be sure you have a plan for what will happen with the earnings. “You’ll want to be careful how you handle the proceeds of the sale so that those proceeds are divided fairly during the divorce process,” says Randi Dukes, an agent with Repeat Realty in Dallas–Fort Worth and a divorce real estate specialist who has earned the RCS-D (Real Estate Collaboration Specialist–Divorce) designation. “It’s often recommended that those proceeds go into a separate account that can be divided upon divorce, rather than mixing the proceeds into other joint accounts.”

What are the options?

When you are going through a divorce, there are several different ways you could decide to sell the family home. Here are some common options.

Sell the house outright

“Often, selling the house makes the most sense because it provides both parties with a lump sum of money to establish a new home and a fresh start,” says Dukes. Selling the property outright means the proceeds can be more easily divided between two people. It also gives both partners the opportunity to establish the next phase of their lives.

Sell it to your spouse

Sometimes it makes more sense for one partner to continue owning the house. This can happen when one partner will have primary custody of the children, for example, as it eliminates the need for the children to move out of their home and be uprooted.

However, this option only works if the partner buying the home can make it work financially. “The spouse keeping the house needs to do their due diligence to make sure keeping it is a sound decision,” Dukes says. “A real estate agent can look at the title to see if there are any liens or second mortgages that one spouse may not know about, and the spouse can talk to a lender or financial advisor to see if they can actually afford to keep the house.”

If this is your plan, make sure you get all your legal ducks in a row. The partner selling the house will likely need to sign a quitclaim deed giving up their rights to the property and transferring them to the other partner — have a real estate attorney manage this process.

Co-own it

You could decide to hang on to the property and continue to own it together. Co-owning might allow you to rent out the property and both gain rental income, for example. Or, you could make the property work for both of you to live there with a renovation that divides it into two units. This can be a viable option for parents who both want to stay near the children.

Give it to your kids or family members

If you’d rather keep the home in the family than sell it, you could consider gifting the property to your adult children or another relative. This option eliminates the need to prepare the property for a sale and could be a way for both partners to put the property in the hands of someone they love. Again, be sure to have a real estate attorney handle the deal for you to ensure that ownership is properly transferred — and it’s a good idea to talk to a tax professional as well, to understand any tax or estate planning implications.

Community property states vs. equitable distribution states

There are two main legal approaches to how property is divided after a divorce. It all depends on whether you’re in a community property state or an equitable distribution state.

The majority of states fall into the category of equitable distribution, which means if one party earns or purchases certain assets, those assets are considered theirs individually. The assets don’t become shared property unless both parties agree to share them. “I live and work in Florida, an equitable distribution state, which simply means Florida courts will divide marital property in a manner which it considers fair, but not necessarily equal,” says Rodriguez.

Community property states, on the other hand, consider all assets acquired during a marriage to be jointly owned by both parties, and they are divided equally in the event of a divorce. Only nine of the 50 states are community property states, according to the IRS: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin.

How to sell a house during a divorce

Selling a house can be stressful and time-intensive no matter what. Follow these steps if you decide to sell your house during your divorce proceedings.

1. Hire an experienced real estate agent and lawyer

Not every real estate agent or attorney knows how to navigate the conflict and tension that can come with selling a house during a divorce. It’s important to work with someone who has experience in sales like this, or even specializes in them.

“I would recommend that you work with someone who knows how to work in high-conflict situations and has experience in getting people moving in one direction to accomplish shared goals,” says Rodriguez. “Because whatever happens during the sale — accepting an offer, countering an offer, all the way to signing closing documents — requires that both parties agree each step of the way. It makes a difference having a transactionally experienced listing agent who has worked with other divorcing clients.”

2. Get a home estimate and agree on a sale price

It’s important that both parties come together on pricing. There are various ways to determine how much your home is worth, from online estimators to a thorough analysis of your local market prepared by a real estate agent. But a professional home appraisal, which will cost several hundred dollars, is probably the most accurate assessment of a home’s market value.

3. Sell the home and split up the net proceeds

Once you agree on the terms and price for selling the home, your agent will guide you through the home-selling process. This will involve preparing the home for the market, taking professional photos for the listing, listing and marketing the property, coordinating showings, reviewing offers and preparing all the closing paperwork. Once the sale is closed and complete, the proceeds will be shared as required by your state and established by your attorney.

Next steps

Ready to sell? It’s important to find a local real estate agent both of you feel you can trust. “Look for someone with additional training in divorce real estate, and ask them about their experience,” says Dukes. This type of agent will be skilled in handling not only the home sale but also any interpersonal conflict that may arise.

FAQs

The best time to sell a house will be different for different couples. “If both spouses agree, then selling your house before filing for divorce is an option — if you’re trying to take advantage of a strong seller’s market, this might be a good idea,” says Randi Dukes, a Dallas–Fort Worth Realtor who specializes in divorce real estate. However, selling the house after the divorce may be the right choice for other couples. Whichever timeline you choose, it’s important that both partners agree on the process.

In some cases, if both parties can’t come to an agreement on how to sell the property, yes, a court may intervene to force the sale. The laws will differ depending on your state and your specific circumstances, so be sure to consult both your divorce lawyer and a real estate attorney in your area.

Rent prices are on the rise, with the average cost increasing 18% between 2017 and 2022. But buying a home requires a hefty down payment and good credit. Renting to own your home can give you the best of both worlds, but there are some downsides.

If you’re thinking about signing a rent-to-own agreement, it’s important to weigh the pros/cons of rent-to-own home deals. Here’s what you need to know before you sign on the dotted line.

What are rent-to-own homes?

When you own a home, part of your monthly payments goes toward paying off the principal. If you stay in the home long enough, you’ll own it.

The same doesn’t apply to rentals. Your monthly rent solely covers your costs of living in that home, whether it’s a condo, apartment, townhouse, or single-family house.

A rent-to-own home lets you pay rent to live on the property, with the option to buy it when the lease runs out. In some cases, a portion of your rent goes toward the purchase price, but that isn’t always the case.

How does rent-to-own work?

A rent-to-own agreement is essentially a lease agreement with an option to buy. Rent-to-own contracts should be read thoroughly. Those options can vary from one contract to another.

When you sign a rent-to-own contract, you pay an upfront fee called an option fee. This is typically 1 to 5% of the home’s purchase price, and it’s non-refundable.

It’s important to note that a lease does not relieve you of the requirements to buy a house. You’ll still have to qualify for a mortgage and make a down payment. It’s merely a way to buy yourself some time and possibly put some of your rent toward the purchase price of a home.

Lease Option vs. Lease Purchase

Before you sign, pay close attention to the lease agreement you’re signing. There are two types, and one contractually obligates you to buy the property.

Lease Option Agreement

A lease option agreement is the best deal of the two for you, the buyer. You’re signing a lease option contract that merely gives you first rights to the house when the lease is up. If you change your mind, find a better deal, or can’t qualify for a mortgage, you can find somewhere else to live and move your belongings out.

Since the option fee is nonrefundable, it’s important to note that you will lose money if you choose not to buy. Calculate this loss when you’re deciding whether to buy.

Lease Purchase Agreement

Unlike a lease option agreement, lease purchase agreements obligate you to buy at the end of the lease. Since it’s a contract, that means you’re legally obligated to purchase the house.

This can be risky for a couple of reasons. Once you’re in the house, you may see issues you didn’t notice when you were first touring the house. Things could change with the neighborhood or your circumstances that you couldn’t know at the outset.

But the biggest issue with a lease purchase contract could simply be that you aren’t eligible for a mortgage to buy the house. Make sure you know, up front, what penalties or liabilities you’ll face if you can’t buy the house when your lease is up.

Even though both agreements operate differently on your end, they do obligate the seller to give you the option to buy when your lease expires. This puts you in a position to own a home at a predetermined future date, giving you the opportunity to start planning.

Length of a Rent-to-Own Agreement

Rent-to-own contracts start with a lease period that can be up to five years but is usually less than three. The thought is that the rental period will give a renter time to qualify for a mortgage. During this time, you’ll work on building your credit, if necessary, and saving for a down payment.

In some cases, a rent-to-own arrangement could have renewal terms. That means if you reach the end of the lease and want more time, you can extend the lease. With this option, though, the property owner could increase your monthly rent or the purchase price.

Preparing for Homebuying

During your lease term, you’ll make each monthly rent payment in exchange for remaining in the house. But it’s important during that time that you work toward purchasing the house when your time is up. Here are some things to do to boost your chances of landing a mortgage once your lease expires.

Boost Your Credit Score

Your rent-to-own deal requires that you qualify for a mortgage once the term is up. To do this, you will need to meet the minimum credit score requirements. You can get a free copy of your credit report each year at AnnualCreditReport.com, but there are also credit monitoring services that can help you stay on top of things.

Although requirements can vary from one lender to the next, Experian cites the following credit scores as necessary to land a mortgage:

FHA: If you qualify, a Federal Housing Association loan will accept credit scores as low as 500.

USDA loans: Those who meet the requirements can qualify with a score as low as 580.

Conventional loan: Generally 620 or higher, but some lenders require 660 at minimum.

VA loans: Eligible military community members and their families can obtain loans with scores as low as 620.

Jumbo loan: These loans cover houses at a higher price, so you’ll need a score of at least 700.

Save for a Down Payment

In addition to a good credit score, you’ll need to put some money down on your new home. Down payment requirements vary by loan type, but it’s recommended that you put at least 20% down. That means if you’re buying a $200,000 home, you’ll need at least $40,000 by closing.

There are lower down payment options, but if you choose those, your mortgage payments will include something called private mortgage insurance. This will increase your monthly payment by $30 to $70 per $100,000 borrowed.

If you can’t save up 20%, you may qualify for an FHA loan, which requires as little as 3.5% down. Both VA and USDA loans have zero down payment options, and there are programs offering down payment assistance to those who qualify.

The best part about rent-to-own properties, though, is that some come with rent credits. With a rent credit, a percentage of your rent will go toward your required down payment. Calculate in advance how much you’ll have in that escrow account at the end of your lease to make sure you save enough to supplement it.

What are the pros of rent-to-own?

Rent-to-own homes can be a great option, especially during a tight housing market. If there’s a house you want to buy, but you can’t make a down payment or your credit isn’t where it should be, it could be a great workaround. Here are some of the biggest benefits of rent-to-own agreements.

Rent May Go Toward Purchase Price

Depending on the terms of the rental agreement, renting to own could help you work toward paying for the home. Instead of the full amount of your rent being pocketed by a landlord, a percentage of your rent could go toward the eventual purchase price. Before signing, pay attention to rent credits and try to negotiate the best deal possible.

The Purchase Price Is Locked In

When a landlord agrees to a lease option, the home’s purchase price is written into the contract. That price will typically be higher than what the market says it’s currently worth. This means if the U.S. housing market sees an unexpected increase, you’ll be buying the home for less than its value. Even if the market dips, once you purchase the house and remain there for a few years, you may be able to sell it at a profit.

You’ll Buy Extra Time

For many renters, the rent-to-own period provides time to qualify for a mortgage. If you’ve researched all the options and found you’re close but not quite there yet, a rental period could be just what you need.

Before you choose this option, though, take a look at your circumstances. If substantial existing debt and poor credit mean you won’t qualify, you may need more than the few years you’ll get with a rent-to-own agreement.

No Moving Necessary

Let’s face it. Moving can be a pain. You have to pack everything up, line up a moving truck and get help moving, and unpack your items once you’re in the new location.

With a rent-to-own agreement in place, you skip the hassle of moving. You’ve already been in that home, making monthly rent payments, for at least a couple of years. You’ll simply go through the closing process and switch from rent payments to mortgage payments.

What are the cons of rent-to-own?

If you can get a mortgage, that’s always going to be a better option than renting or leasing to own. But there are some instances where renting without the buy option could be better for you. Here are some things to consider.

Rent-to-Own Home Maintenance

Before you sign any lease agreement, it’s important to read the fine print. One thing to note, specific to own agreements, is who will be responsible for maintenance during the rent-to-own period. If you rent without the promise of eventual ownership, your landlord will take care of those costs. In some cases, rent-to-own agreements require the renter to handle all repairs.

But there’s an upside to handling repairs on your own. To your landlord, the property is technically yours. That means you likely will give it more TLC. Still, it’s well worth it to pay for a home inspection before you agree to a rent-to-own agreement. This will identify any serious issues that will need to be addressed before you buy.

Option Fee

One distinguishing feature of a rent-to-own property is the option fee. This is usually between 1 and 5% of the purchase price and is non-refundable. That means if you don’t ultimately qualify for a mortgage, you’ll lose that money.

Home Values Could Drop

Property values aren’t guaranteed. Your landlord estimates the value of the property, but if you’re in a rising market, you might get that home at a steal. While that’s good news for you, the reverse can happen. If housing prices drop substantially during that time frame, you could find yourself buying a property for more than it’s worth.

Contract Breaches Can Be Costly

Rental agreements are a legal obligation. If you don’t pay your rent, your landlord can evict you and keep your security deposit. But rent-to-own contracts bring an additional level of risk. Missed payments mean you could be evicted and lose all the money you’ve put in. That includes the upfront fee and any rent credit you’ve earned.

All that money will also be lost if you can’t qualify for a mortgage when your rental time is up. These agreements can give you some breathing room. However, if your low credit scores, income, lack of a down payment, or employment situation make you ineligible for a mortgage, you could be searching for another rental while losing everything you’ve paid on the lease-to-own home.

Steps to Buy a Rent-to-Own Home

Once you’ve decided renting to own is the route you want to take, you may wonder what to do next. The following steps can help you ensure you get the best deal in a rent-to-own agreement.

1. Find a Home

This is more challenging than it might sound, especially if you’re looking in a competitive real estate market. Rent-to-own homes are extremely rare, so you may have to find a home for sale and try to negotiate this type of setup.

Typically, homeowners become renters when they can’t sell their homes. This means your rent-to-own contract might be on a home that’s in a less desirable or convenient area of town. For someone whose home has been on the market for a while, being able to collect rent money with the promise of a sale in a few years can be a huge relief.

For best results, find a real estate agent who can help you track down a home and negotiate with the seller. The National Association of REALTORS® maintains a directory of real estate agents, but you can also ask for a referral or find real estate agents nearby who have brokered these types of deals recently.

2. Research the Home

Even if it’s tough to find a lease-to-own home in your area, don’t snatch up the first one you find. Crunch the numbers to make sure the rent and purchase price make financial sense for you. Look at the sale history of the home to verify that the owner’s estimated purchase price is somewhat within what the median home price will likely be when your lease expires.

3. Research the Seller

The seller needs to be looked into as well. This is even more important with rent-to-own agreements since this person will be your landlord for the entire lease period. If you see any red flags during your interactions with the seller, move on.

4. Choose the Right Terms

Before you make a real estate purchase, you would have a closing attorney review the documents. The same goes for a rent-to-own agreement. Run all the paperwork past a real estate attorney to make sure there’s nothing in the contract that will hurt you in the long run.

Your real estate agent should be able to negotiate the best terms for you, including how each rent credit will help you build equity and what happens at the end of the lease.

5. Get a Property Inspection

Any time you make a home purchase, it’s essential to know what you’re buying. The same is true for rent-to-own properties. A home inspector can check things out and make sure you aren’t purchasing a home with serious issues.

6. Start Preparing to Buy

Once you start making rent payments, it’s time to start preparing for your eventual home purchase. Chances are, you’ll have to make a sizable down payment on a home loan, so plan to have that ready. Also, keep an eye on your score with all three credit bureaus and make sure you’ll qualify.

A rent-to-own contract can be a good deal for both the buyer and the seller. It can give you time to save money and improve your credit score. A real estate lawyer should take a look at your contracts and make sure your best interests are protected.

Bottom Line

Rent-to-own homes present a unique option for potential homeowners. This approach offers the opportunity to enter the homeownership arena at a slower pace, allowing individuals to build credit, save for a down payment, and experience living in the home before making a final purchase decision.

However, the rent-to-own path isn’t free from drawbacks. Potential buyers should be wary of unfavorable terms, higher monthly payments, and the risk of losing money if they decide not to buy. Ultimately, like all significant decisions in life, choosing a rent-to-own option requires careful consideration and thorough research.

Frequently Asked Questions

Where can I find rent-to-own houses?

Rent-to-own houses can be found through specialized websites dedicated to these types of listings, local real estate agents familiar with the concept, or sometimes through classified advertisements in local newspapers or online platforms.

Can I find rent-to-own homes on Zillow?

Yes, Zillow does list rent-to-own homes. When searching for properties, you can filter the search results to show only rent-to-own options. However, availability may vary based on the region and market conditions.

How long is the typical rent-to-own contract?

The typical lease term ranges from one to five years, but terms can vary based on the agreement between the homeowner and tenant.

Do I have to buy the house at the end of the lease?

No, the decision to buy is optional. However, if you decide not to purchase, you may lose any upfront fees or additional monthly amounts set aside for the potential purchase.

Can the seller change the purchase price once set?

Generally, the purchase price is fixed in the initial agreement. However, some contracts may have clauses allowing price adjustments based on market conditions.

What happens if the property value decreases during the lease period?

If the home’s value decreases and you’ve agreed on a set purchase price, you could end up paying more than the current market value. It’s crucial to negotiate terms that protect your interests.

Who is responsible for repairs and maintenance?

The agreement should clearly outline these responsibilities. In most cases, the tenant bears the responsibility for maintenance and repairs during the lease term.

What’s the benefit of a rent-to-own agreement for sellers?

Sellers can generate rental income while waiting to sell, often at a premium. It also widens the pool of potential buyers, especially those who need time to improve their credit or save for a down payment.

How do property taxes work in a rent-to-own agreement?

In a rent-to-own scenario, the property taxes are typically the responsibility of the homeowner, as they still retain ownership of the property during the rental period. However, the specific arrangement can vary based on the terms of the agreement.

Some contracts may stipulate that the tenant pays the property taxes directly or reimburses the homeowner. It’s crucial for both parties to clearly understand and agree upon who will cover the property tax obligation before entering into a rent-to-own contract.

If I don’t buy, do I get a refund for the extra money paid?

Typically, the extra money paid above regular rent, often referred to as “rent premium,” is forfeited if you decide not to buy.

Is the rent in a rent-to-own agreement higher than usual?

Often, yes. A portion of the monthly rent may be used for the potential down payment or purchase price, making it higher than the average rent for similar properties.

What’s the difference between rent-to-own and mortgage?

Rent-to-own is an agreement where a tenant rents a property with the option to buy it at the end of the lease. No bank is involved initially, and the tenant isn’t obligated to buy. A mortgage, on the other hand, is a loan specifically for purchasing a property. The buyer borrows money from a bank or lender and agrees to pay it back with interest over a predetermined period.

Does rent-to-own hurt your credit?

A rent-to-own agreement, in itself, doesn’t usually affect your credit. However, if the homeowner reports late payments to credit bureaus, it could hurt your credit score. On the positive side, consistently paying on time and eventually securing a mortgage can benefit your credit.

What is another name for rent-to-own?

Rent-to-own agreements can go by various names, including:

Lease to purchase

Lease option

Rent-to-buy

Rent-to-purchase option

Lease purchase

Each of these terms represents the concept of renting a property with the potential option to buy it after a set period.

When you take out a mortgage, whether it’s a refinance or a home purchase, you may come across the phrase “cash to close.”

Virtually all mortgages require some financial contribution from the borrower to fund the loan.

It might be down payment funds, it might be lender fees, or it might be prepaid charges like property taxes and homeowners insurance.

There’s a good chance it’ll be a combination of these things, which will need to be paid at closing via a verified account.

Let’s talk more about the meaning of cash to close, how it’s calculated, and how it’s paid.

Cash to Close on a Home Loan Is More Than Just Closing Costs

If you look at your paperwork, you should see a list of closing costs associated with your home loan.

You can see estimates of these costs on both your initial Loan Estimate (LE) and also on your Closing Disclosure (CD).

And when it’s about time to close your loan, on the settlement statement prepared by your escrow officer or real estate attorney.

On these documents, you should see things like the loan origination fee, underwriting and processing fees, and other lender fees.

Additionally, there will likely be a charge for an appraisal, along with a charge for title insurance, homeowners insurance, and escrow services.

Under that escrow/title umbrella, more fees will be listed, such as courier fees, wire fees, notary fees, loan tie in fees, settlement fees, and on, and on.

There will also be recording fees and transfer taxes, along with prepaid items such as X number of months of taxes or insurance.

That’s the closing cost piece, which includes both lender fees (if applicable), and third-party fees, such as the insurance, appraisal, title/escrow.

Pretty straightforward, but we also have to consider the down payment, any deposit such as earnest money, and any seller or lender credits.

Then some math needs to be done to figure out the final amount due, which is, drumroll, the cash to close.

Fortunately, there’s a section on the LE and CD called “Calculating Cash to Close,” which breaks it all down for you.

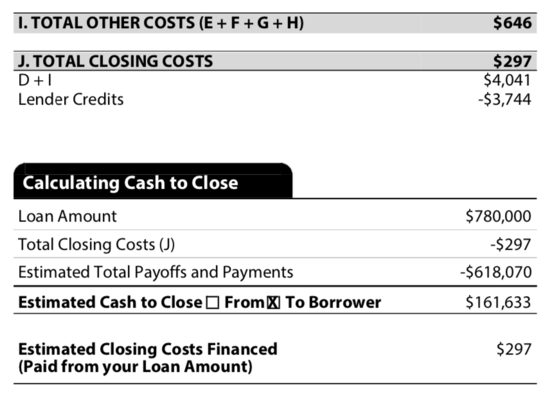

How to Calculate Cash to Close: An Example

It’s probably easier to look at an example rather than keep talking about it. So check out the screenshot above, taken from a Closing Disclosure.

As you can see, it lists total closing costs, down payment funds, deposits, and credits.

In this example, the purchase price is $852,500 and the home buyer is putting down 20% to avoid mortgage insurance and get a better mortgage rate.

They’ve got $12,432.26 in closing costs, of which $435 was paid out-of-pocket before closing for an appraisal.

The borrower made a $25,875 earnest money deposit for 3% of the purchase price as well, which was originally $862,500 before a slight price reduction.

They didn’t finance any closing costs, nor did they receive any funds via the transaction.

But they did get a seller credit of $7,500 and a $4,372.88 rebate from their real estate agent.

So to tally it up, we have $182,932.26 in total costs, and $38,182.88 in credits.

That means the borrower still owes $144,749.38, which is the remaining balance after their deposit and various credits.

It covers the remaining down payment and remaining closing costs, and is typically wired to escrow at closing.

What About Cash to the Borrower?

Now let’s look at a cash out refinance. In this case, there is cash going to the borrower at closing because they’re tapping their home equity.

So instead of sending money to the lender, the bank is sending money to the borrower.

In this example, the borrower also took advantage of a lender credit, which offset nearly all of their closing costs.

Their loan payoff on their existing mortgage was $618,070 and the new loan amount was $780,000.

That would send $161,930 to the borrower, but once we subtract the $297 in remaining closing costs, it’s $161,633.

Sending the Cash to Close: Some Things to Remember

When it comes time to send your cash to close funds, you’ll likely do so via wire, or possibly a cashier’s check.

Either way, the funds must come from a sourced account that was verified during the underwriting process.

For example, a bank account you verified earlier on by connecting it in the digital application or uploading monthly statements.

This way they know the money is actually coming your own funds, and not some other unverified source.

If it does come from a non-sourced account, it could delay your loan closing and cause a lot of headaches.

Remember, such funds should also be seasoned for at least two months prior as well, meaning in the account and untouched for 60+ days.

Again, this ensures the funds are your own and not someone else’s, or worse, a loan, which you deposited into your own account.

If you have questions about what is owed, it’s always helpful to speak directly with the settlement officer, who can go over everything with you line by line.

That way you know exactly what you owe, why you owe it, and most importantly, where exactly to send it.

To summarize, there are a lot of costs associated with a home loan, many of which you won’t be aware of until you go through the process yourself.

This is why it’s imperative to get a robust mortgage pre-approval and set aside funds well before beginning your home search.

One interesting aspect of the home loan process is the sheer number of individuals you’ll work with along the way.

You don’t just speak to a salesperson and call it a day. Lots of people are involved in what is a very complex transaction.

Aside from salespeople, there are loan underwriters, processors, appraisers, escrow officers, real estate attorneys, and more.

Let’s discuss the roles these people hold to help you better understand what it takes to get a mortgage.

Remember, you’re asking to borrow a large sum of money, so it’s going to take time and energy (and lots of people) to get to the finish line.

The Sales Rep/Loan Officer/Mortgage Broker

The first step in the home loan process typically involves a sales person, which can be a banker at your local branch or credit union, a loan officer, or a mortgage broker.

If we’re talking about a purchase, this may come before/during your home search or after you’ve found your property with the assistance of a real estate agent.

If it’s a mortgage refinance, you’d simply jump right to this step to rework the details of your existing home loan if you wanted a rate and term refinance or a cash out refi.

You might be referred to an individual/company, or you might do your own discovery to find a suitable partner. Either way, always look beyond the referral you were given.

Your real estate agent might know a great lender, but you your own research as well.

It’s important to gather multiple quotes from different companies to ensure you get the best deal.

Now, this individual will be your main point of contact during the loan process, and perhaps most importantly, will provide you with pricing.

Bankers and loan officers work at the retail level, while mortgage brokers offer wholesale rates from their lender partners.

You can read more about the differences (banks vs. brokers) but either way they’ll likely be the person you speak with most.

Aside from providing pricing, these individuals can help get you pre-qualified or pre-approved for a mortgage, discuss different loan scenarios, and guide you on loan choice.

If you have mortgage questions, they should be able to provide answers and give you guidance.

They may make certain recommendations, such as down payment amount, loan type, or provide an opinion about paying discount points or when to lock your rate.

This individual will be with you from start to finish, but doesn’t work alone. They’ve got an entire team to help you close your loan in a timely fashion.

FYI, you may also come across a “mortgage planner,” which is an individual who may assist a busy senior loan officer.

They can communicate loan status, provide follow-up, collect conditions, and perform other tasks if the LO is unavailable or simply needs a hand.

The Loan Processor

Once you’ve spoken to a sales representative (or LO/broker) and have decided to move forward, you’ll be in put in touch with a loan processor.

The main goal of the processor is to put together a clean loan file that can be submitted to the underwriting department.

This means collecting key documents, ensuring there are no red flags, double-checking everything, and making any necessary corrections.

The processor may also reach out after the loan is approved to collect additional documents to satisfy any outstanding conditions.

They will also provide updates to the loan officer or broker, who will then keep you in the loop about where you’re at in the process.

The processor essentially acts as a liaison between the underwriter and sales rep/LO/broker.

This ensures things move along smoothly and any hiccups can be resolved quickly without delay.

The Loan Underwriter

The loan underwriter probably holds the most important role in the home loan process.

They decide if the mortgage is approved, declined, or potentially suspended pending further explanation.

It’s for this reason that the loan processor only sends the loan package to the underwriter once everything has been thoroughly checked.

You only get one chance to make a first impression, so it’s imperative to get it right. Otherwise you could face delays or simply get flat out denied.

Aside from approving the loan, the underwriter will also provide a list of conditions needed to close the loan.

Most mortgage approvals are conditional, meaning you might need to furnish additional information or documentation to obtain your final approval.

Once these documents are provided, whether it’s another bank statement or letter of explanation, the underwriter will clear the outstanding conditions and move the loan to the funding department.

The Home Appraiser

While your loan is being reviewed by the underwriter, an appraisal will be ordered to determine the value of the underlying property.

Remember, aside from determining your ability to repay the loan, the bank also needs to ensure the collateral for the loan is valued properly.

This individual will visit the property to assess its condition, take photographs, and determine recent sales comparisons.

They will formulate a valuation based on the property details, such as number of bedrooms and bathrooms, square footage, amenities, location, lot size, condition, and so on.

The value they come up with, known as the appraised value, is used as the basis for the loan-to-value ratio.

Generally, the goal is for the appraiser to support the purchase price of the property or the value declared for a refinance.

If the value is lower, the details of the loan may need to be reworked, such as a higher down payment.

For certain types of loans, such as FHA loans and VA loans, the home appraiser will also ensure that certain Minimum Property Requirements (MPRs) are met.

This ensures the property is safe for the occupants, that there are adequate living conditions, and no major hazards, such as lead paint or termites.

The Home Inspector

If we’re discussing a home purchase, you’ll want to get an inspection done. And you’ll want to do it ASAP while any contingencies are still in place.

While a home inspection typically isn’t required, they’re generally a good idea.

Aside from finding out what’s potentially wrong with the property, you can ask for credits from the seller if the inspector finds any significant issues.

As the name suggests, a home inspector will come out to the property and assess the condition of the structure itself, the foundation, the interior, the roof, the electrical, HVAC, and more.

Some may also inspect the pool and spa, if one exists, though you could be charged extra.

They’ll make notes as they survey the property and issue a formal report afterwards. This can be used to negotiate with the seller if anything material comes up.

The Notary Public

Once it’s time to sign your loan documents, you’ll need to make an appointment with a notary public.

This individual serves “as an impartial witness” when signing important documents, such as those related to a home purchase or mortgage loan.

Your settlement agent should organize a time to meet with this individual to conduct your signing.

The notary may come to your home or meet you somewhere else to review and sign documents.

The main job of the notary is to verify the identity of the signer and ensure they are willing to sign the documents “without duress or intimidation.”

This requires you to furnish identification, such as a driver’s license, during the signing appointment.

The Escrow Officer

Another very important individual in the transaction is the escrow officer, a third-party who facilitates the loan closing and collects/disburses funds to the appropriate parties.

Some of their key roles include preparing final statements for the buyer, such as cash required to close, and determining costs such as property taxes, insurance, prepaid interest, and loan payoffs.

The escrow officer will send you a settlement statement that lists all the fees and closing costs associated with your loan, along with any lender credits and loan payoffs and funds required.

They will also liaise with a title company and forward necessary documents for loan recording.

Importantly, they’ll provide wiring instructions to all parties, including the buyer, so you know where to send funds (cash to close).

If you have questions about things like prepaid items, mortgage impounds, and loan payoffs, they can be particularly helpful.

The Title Agent

To ensure the property is free of any liens, encumbrances, or defects, a title insurance policy is usually required in order to take out a mortgage.

A title agent is the individual who conducts a title search, orders a preliminary title report, and eventually issues title insurance on the subject property. This makes them a licensed insurance agent

They are also in charge of recording the deed and loan documents with the county once the loan has funded.

You might hear the words title and escrow used interchangeably, but title has to do with property ownership/lien history, while escrow is about the calculation, collection, and disbursement of funds.

However, they may perform other settlement tasks beyond just title depending on the state where they’re located.

The Loan Closer/Funder

If you’ve made it this far, it means the loan is almost funded. But there’s still work to be done.

The loan closer/funder has to review the file to ensure everything is accurate and complete, and if not, address and fix any errors or outstanding issues.

They must ensure all prior to funding (PTF) conditions are satisfied and work with the settlement agent to prepare funding figures and timing of disbursement.

This includes the review of signed closing documents and items like hazard insurance and the preliminary title report.

And if everything looks good, request the wire instructions from escrow after a thorough review.

The Real Estate Attorney

Note that in certain states, a real estate attorney could be required to prepare certain documents and/or to conduct the loan closing.

This individual may order and certify a title report, review loan documents, and advise you if necessary.

Beyond that, they can ensure the interests of all parties are protected, and handle any legal issues or disputes that may come up.

One last thing. You may find that there is some overlap with a title company and escrow company, as the former can also provide escrow and notary services as well.

So depending on where you live, you could have one company or individual handle several tasks.

As you can see, there are quite a few people involved in the funding of a home loan, which explains why they take a month or longer to close.

Once you know more about each person’s role, it should be easier to navigate the home loan process and make better sense of it all.

And perhaps adjust your expectations that there isn’t a same-day mortgage and likely won’t be for the foreseeable future.

This article is reprinted by permission from NerdWallet.

Mortgage rates have risen to their highest levels in more than 20 years, making it harder to afford a home. And yet, out of necessity or desire, hundreds of thousands of people buy homes every month.

With the 30-year fixed rate topping 7%, NerdWallet asked real estate agents and mortgage loan officers for advice on how home buyers can stretch their homebuying dollars in this time of high interest rates. Here are nine tactics that they suggested.

1. Ask the seller to reduce the mortgage rate

Temporary mortgage rate buydowns have become commonplace since rates surged in early 2022. With a temporary rate buydown, the seller pays a portion of the buyer’s interest payments upfront. This reduces the house payments for the first one, two or three years of ownership.

“This is a common strategy for new-home builders, but it can also be used in the purchase of resale homes,” said John Bianchi, executive vice president for loanDepot. (All sources in this story commented via email.) “Negotiating a temporary buydown with the seller can help soften the blow of high interest rates, reducing your monthly payment for one to three years.”

In one typical setup, the seller’s payment effectively cuts the buyer’s interest rate by 2 percentage points in the first year, and by 1 percentage point in the second year. After that, the buyer pays the full interest rate. This is known as a 2-1 buydown.

Another option is to reduce the mortgage rate permanently, using discount points. One discount point equals 1% of the loan amount; each point typically reduces the interest rate by around 0.25 percentage point.

“Home buyers have an opportunity to get a seller to pay for these methods to lower their interest rate,” said Chuck Vander Stelt, a real estate agent in Valparaiso, Indiana. “Some home buyers should seriously consider offering a more generous price to the seller in exchange for a large closing cost concession and then use those funds to buy down the interest rate as much as possible.”

Also see: Avoiding the 30-year mortgage loan trap can save you hundreds of thousands of dollars

2. Use part of your down payment to pay down debt

When you apply for a mortgage, the lender considers your total debt payments for the house, car, student loans and credit cards. Sometimes it makes sense to divert some of your intended down payment money to cut the higher-rate debt first, said David Kuiper, vice president and senior mortgage banker for Dart Bank in western Michigan.

“While the mortgage payment will be slightly higher, the total debt/payments is lower, making the proposed purchase more affordable,” Kuiper said.

3. Use home buyer assistance programs

State and local governments sponsor an abundance of programs to make homes affordable for home buyers, especially first-timers. Some programs offer down payment assistance and help with closing costs. Others offer favorable interest rates or tax credits.

Details differ from state to state. Some programs are targeted to certain counties, cities or neighborhoods. Others are intended for specific groups of people, such as teachers, first responders or renters who live in public housing. Some programs have income limits.

Don’t miss: We bought a falling-down 100-year-old home. We tried to renovate, but things took a turn for the worse.

4. Ask the seller to finance the purchase

You can give the seller an IOU for part of the home’s value and make monthly payments directly to the seller at an interest rate that’s lower than you could get from a bank. This arrangement is called “seller financing” and has its roots in the early 1980s, when mortgage rates zoomed as high as 18%.

You might wonder why a seller would agree to such a deal. “They will often do this in order to get the price they want,” said Janie Coffey, who leads the Coffey Team with eXp Realty in St. Augustine, Florida. The seller gets full price while you get a break on the interest rate.

Seller financing usually has an end date: Within three, five or 10 years, the buyer must get a mortgage from a lender to pay off the amount owed to the seller. Coffey explained that the type of seller open to this arrangement often has paid off the mortgage “and is OK to wait for their big payoff.”

Seller financing is complex. Use an experienced real estate attorney to draw up the contract.

Related: How the U.S. housing market got stuck in the ’80s

5. Don’t wait for a rate you like better

“If the right house comes along and the payment is affordable (even if you don’t like the interest rate), you should buy the house,” Kuiper said.

You often hear that you should buy now and refinance someday, after interest rates fall. That’s not Kuiper’s point. His point was this: If mortgage rates fall, more buyers will rush into the market. They’ll make competitive offers and drive home prices higher, “essentially wiping out any advantage of the lower interest rate.”

6. Don’t get distracted by things you don’t need

Some sellers want flexibility about the closing date, would prefer the buyer to make repairs, and are scared of accepting an offer from a buyer who ends up failing to qualify for the mortgage.

Vander Stelt advises staying focused on price with these hassle-avoidant sellers, while being flexible on the rest of the offer on the house. “Do this by offering the best terms you can, including buying the home as-is, a closing date and possession that works best for the seller, and illustrating how strong of a candidate you are to get your mortgage approved,” he said.

You can demonstrate that you’re a strong mortgage candidate by showing a preapproval letter and by sharing financial information, such as account balances that prove you have the cash for the down payment.

7. Buy a house that needs work

Buying a fixer-upper is an old-fashioned, time-tested way to save money. “If you can be patient, it’s worth buying a home that needs work and slowly fixing it up over time or taking a renovation loan to acquire the home and do the work upfront,” said Brian Koss, regional sales director for Movement Mortgage, in Danvers, Massachusetts.

Read: Should you buy a fixer? These are the 5 cheapest states to make home renovations.

8. Build a house or buy a brand-new one

“Building a new home can provide more certainty around how long you will have to wait to move in, it can provide more cost certainty, and it can save you money in the short and long term by avoiding costly remodels, appliance repairs and unexpected repairs of older parts of the home,” said Jeffrey Ruben, president of WSFS Mortgage in the Greater Philadelphia area.

Buying a new home in a development has some of the same advantages. And today’s buyers have good reason to shop for new construction because there’s a shortage of existing homes for resale.

Read: U.S. construction spending rose in June, marking seventh straight monthly increase

9. Rent out part of the house

Coffey suggested using an old strategy with a trendy name — house hacking — “buying a property like a duplex, where you live in one unit and rent out the other,” she said.

If you buy a duplex, triplex or quadplex, and you live in one unit, you can include the expected rental income for the others when qualifying for a loan. In some cases, you can qualify for a mortgage using expected rental income from an accessory dwelling unit, such as a basement apartment or a tiny house in the backyard.

Also see: Homeowners locked into ultralow mortgage rates consider short-term rentals, but cities are cracking down

If you buy a home today, you’re stuck with high mortgage rates for the time being. But by employing some creativity, you might find a way to afford homeownership.

More From NerdWallet

Holden Lewis writes for NerdWallet. Email: [email protected]. Twitter: @HoldenL.

When you’re about to make an offer on a home, your real estate agent will ask how much “earnest money” you’d like to put down. Earnest money is a type of security deposit, also known as a “good faith” deposit, made to the seller of a home. It represents your intent to buy the property by showing the seller you’re serious about purchasing the property. In most cases, earnest money can also act as a deposit on the property you’re looking to buy.

This Redfin article gives an overview of what earnest money is, why you need it, and how much you may need, and how to protect the money once you deposit it.

What is earnest money in real estate transactions?

Earnest money is the money you pay after a home seller has accepted your offer on a house and before closing on the home. Earnest money assures the seller that you as the buyer are acting in good faith, and it provides them with some compensation in case you back out of the deal without a valid, contractual reason.

Once the seller’s agent is able to confirm that your earnest money has been deposited into an escrow account, the buyer and seller will enter into a purchase agreement and the seller’s agent will mark the listing as a pending sale — in effect taking the property off the market. At this stage, various inspections, appraisals, and possibly other contingencies you had in the offer contract move forward to finalize the sale.

Who keeps earnest money if the deal falls through?

If the buyer backs out, the earnest money is paid to the seller. If the deal falls through due to something coming up on the home inspection that would be prohibitively expensive (like a cracked foundation) or any other contingency listed in the contract, the buyer gets their earnest money back.

How much earnest money do you need to offer?

The buyer and seller can negotiate the earnest money deposit amount, but it typically ranges from 1% to 3% of the sale price, depending on the market. However, if you’re buying a home in a seller’s market (when there are more buyers than homes for sale), or bidding on a highly competitive home, the earnest money deposit might range between 5% and 10% of a property’s sale price.

Be sure to talk to your real estate agent about how much earnest money you should offer in the housing market you’re competing in.

Do you need to pay earnest money?

In the strictest technical terms, the answer is no – earnest money is not a requirement when you make an offer on a house. However, your offer likely won’t receive the seller’s serious consideration without putting a good faith deposit down of some kind. Earnest money can act as added insurance for both parties in the transaction.

How is earnest money paid and where does it go?

In most cases, your earnest money deposit is paid to the escrow or title company, which holds it in an escrow account until the transaction closes. If you work with a real estate attorney, the deposit may be put into escrow there. You can pay this deposit with a personal check, a cashier’s check from the bank, a money order, or wired funds, depending on the terms of your contract.

What does the good faith deposit count toward?

Once the sale of the home has been completed, the earnest money you paid can be applied toward your closing costs or down payment. Alternatively, you can receive your earnest money back after closing. Because the sale went through the home sellers do not get to keep the earnest money deposit.

When does a seller keep the earnest money deposit?

If you fail to meet your offer’s contractual obligations, your earnest money could now belong to the seller. Examples include:

After the due diligence period is over (usually a couple of weeks), you learn that the home sits in a flight path or near a refinery and you decide to walk.

You back out for any reason not listed as a contingency in the contract.

You cannot close on time, without a relevant contingency, and the contract has a “time is of the essence” term.

If you face any of these issues but still want to purchase the house, don’t give up. Have your agent get with the seller’s real estate agent. If you are upfront about the situation, the seller may extend the timeframe.

Is earnest money refundable?

As a buyer, you can reclaim your earnest money for a couple of reasons:

If the seller doesn’t fulfill their side of the purchase contract. For example, if the home inspection found faulty windows and the seller agreed to replace them – but did not follow through by the contract deadline. That breach of contract allows a buyer to back out of the purchase and receive a refund of their earnest money.

If you have a contingency in place, and you have a reason related to that contingency to cancel the contract. There are a number of contingencies you can put into the contract and, if not met, you can walk away from the deal with your good faith deposit in hand.

Other examples of when your earnest money would commonly be refunded:

The title company finds a lien against the property.

Your lender denies you the loan, but you have a financing contingency in your offer.

If your offer is contingent on selling your current home, but you are unable to do so after a given period of time.

If you have an appraisal contingency, and the home appraises at a lower rate but the seller won’t reduce the price of the home.

Having a contingency may also allow you to negotiate the terms of your contract. For example, you may be able to ask the seller to perform repairs or give a credit at escrow to cover the agreed-upon repair costs. Typically, a buyer and seller can negotiate a resolution so the sale can be completed.

What if a buyer can’t afford a good faith deposit?