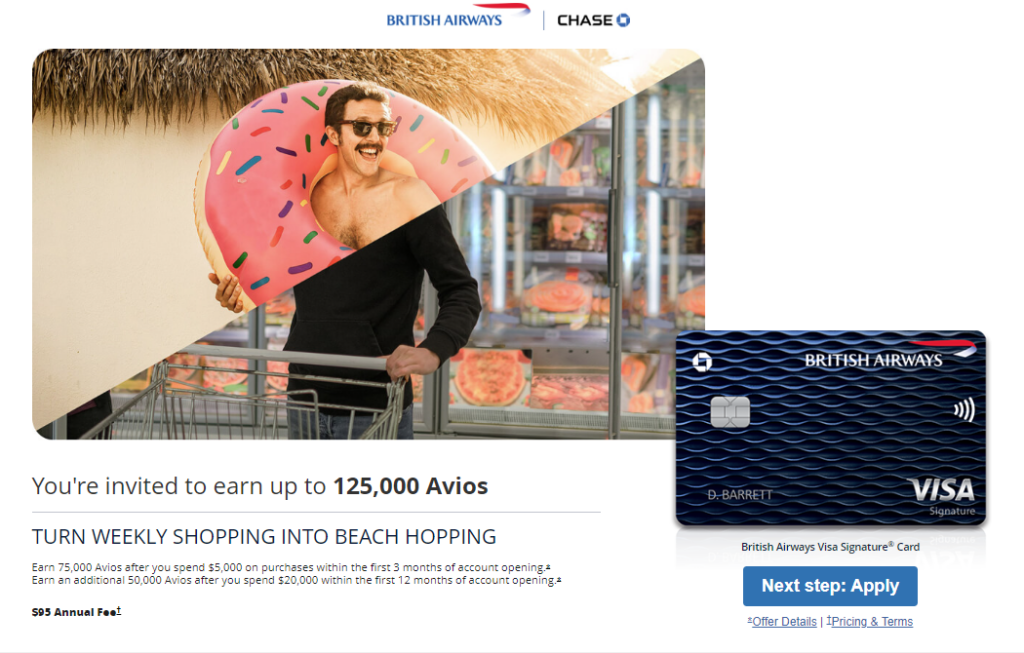

Direct link to offer : British Airways | Aer Lingus | Iberia

Chase is offering up to 125,000 points on the Chase British Airways card

75,000 points after $5,000 in spend within the first 3 months

An additional 50,000 points after $20,000 in spend within the first 12 months

Card Details

$95 annual fee not waived first year

Chase’s 5/24 rule does apply to this card.

Card earns at the following rates:

Earns 3 Avios per $ on British Airways purchases

Earns 1 Avios per $ on all other purchases

As a general rule, Chase does match offers.

Our Verdict

We’ve previously seen a 100,000 bonus with $5,000 in spend, but recently bonuses were 75,000 points after $5,000 in spend or 100,000 points after $20,000 in spend. Not really worth it for most people due to the high spend requirement. We won’t add this to our list of the best credit card bonuses for now.

Visa and Mastercard are both card networks. Both organizations manage the payment networks through which their cards work. Visa and Mastercard are different companies, but they operate in a very similar way.

Four credit card networks tend to compete for space in consumer wallets. They are Mastercard, Visa, Discover and American Express.

According to Statista, Mastercard and Visa have had the largest market share for a while. As of 2021, they accounted for more than 87% of the market. Compare that to Amex’s 10.5% and Discover’s 2.2% and you can see that most credit cards are Mastercard or Visa.

But is one better than the other? Are there really any differences between these two major credit card networks? Find out in our guide to the difference between Mastercard and Visa below.

In This Piece

What’s the Difference Between Mastercard and Visa?

While they’re both credit card processing networks, these are unique and separate companies. They were founded at different times.

Originally known as the BankAmericard credit card program, Visa launched in 1958. Mastercard began as Master Charge: The Interbank Card when it emerged as a BankAmericard competitor in 1966.

Visa cards don’t work on the Mastercard network, and vice versa. You can’t, for example, use a Visa to pay for something in a store that only accepts Mastercard.

How Are Visa and Mastercard Similar?

There are more similarities between Visa and Mastercard than differences. As mentioned earlier, these are both card networks. They both play the middleman between payment processors and issuing banks.

Both companies operate globally, so if you alert your issuer in advance, you should be able to use your Visa or Mastercard in another country when you go on vacation. Whether you pay fees for this service depends on your card issuer and account details—not on Visa or Mastercard.

Both Visa and Mastercard have tens of millions of merchants in their networks, and both companies’ merchant fees are comparable. Both organizations are publicly traded.

What’s the Difference Between a Network and an Issuer?

The credit card network is the middleman between the payment processor and the issuer of the card. When you pay with a credit card, the information is processed through the network to the bank that issued your credit card. On the other side of the transaction, the data that supports the funds transaction is also processed through the network.

Visa and Mastercard are credit card networks. They’re responsible for the infrastructure for these transactions and for protecting the information as it passes between the payment processor and the issuer. For this service, the credit card networks charge a fee—usually paid in part via a small percentage of every transaction.

An issuer is the bank that issues the card. Examples include Chase, Citibank and Capital One. The issuer is the entity that decides whether you’re approved for a credit card and sets interest rates and fees. It’s also the lender that pays for the goods you purchase with your credit card and the entity you pay back with your payments.

How Does Payment Processing Work?

Visa and Mastercard credit card and debit card payments all go through the same payment process—albeit on different networks. The process looks like this:

Consumers swipe cards—or tap contactless cards—in physical stores or enter card details online.

Merchants send payment authorization requests to their payment processors.

Payment processors send payment requests to the appropriate card network.

Card networks “ask” issuing banks for payment authorization.

Issuing banks approve or deny the transaction.

At this point, transactions are—hopefully—authorized, but they’re not settled yet. The process must continue:

Merchants send approved payment requests to payment processors in batches.

Once again, payment processors send transaction details to Visa, Mastercard or other applicable card networks.

Card networks “ask” issuing banks for previously authorized funds.

Issuing banks release the funds, which travel to merchant banks.

Credit card processing network fees get taken out along the way.

Merchant banks transfer funds into individual merchant accounts.

At this point, the store or other merchant has been paid for the goods or services you bought with your credit card. Your next statement should also reflect the purchase.

Other Mastercard vs Visa Similarities

Visa and Mastercard issuers have a range of products to choose from. Debit cards let you spend money already in your bank account—plus your overdraft if you have one set up. Meanwhile, you must fund prepaid cards in advance.

Visa or Mastercard credit cards have the following things in common.

1. Credit Scores Matter

Card issuers make decisions based on consumers’ credit scores. If you want a card with an extra-low APR and a really high credit limit, you’ll need a top-notch credit score. Lower credit scores generally mean lower credit limits and higher interest rates.

If you’re new to credit or you need to repair your credit, look for a credit builder or credit repair card. You won’t have a very high limit to begin with, and your APR might not be very competitive, but if you make regular payments, you’ll soon qualify for a better product.

Surge Mastercard® Credit Card

All credit types welcome to apply!

Monthly reporting to the three major credit bureaus

Up to $1,000 credit limit doubles up to $2,000! (Simply make your first 6 monthly minimum payments on time)

Fast and easy application process; results in seconds

Use your card at locations everywhere that Mastercard® is accepted

Free online account access 24/7

Checking Account Required

See if you’re Pre-Qualified without impacting your credit score

2. Rewards Cards Provide Value

Mastercard and Visa both partner with issuers that offer rewards cards. Rewards include air miles, points, store-specific rewards, food and beverage rewards and cash back. If you use your rewards card in a savvy way, you can save a lot of money.

3. Fees Vary

Visa and Mastercard don’t set fees—issuing banks do. As a result, fees for Visa and Mastercard products vary widely. Make sure you’re familiar with the over-limit, balance transfer, late payment, and foreign transaction fees on each of your credit card accounts—and stay away from credit cards with unreasonable fee structures.

4. Smart Wallets Protect Information

Both Visa and Mastercard cards are compatible with smart wallets like Apple Pay and Google Pay. Smart wallets hide your card information, so they’re more secure than swiping a card or entering card details online. Every year, more and more brick-and-mortar and online retailers accept smart wallet payments.

5. Discount Programs Save You Money

Some credit cards—especially business credit cards—incorporate high-value discount programs. The Visa SavingsEdge program, for example, can save you more than 15% when you shop with qualifying merchants. Mastercard has a similar program, called Easy Savings. In both cases, you need to enroll your card to get money back.

Which Is Better: Visa or Mastercard?

What’s the difference between Mastercard and Visa? Not that much, actually. The major difference is the company that runs the network. Merchants that accept one usually tend to accept the other, and more merchants accept Visa and Mastercard than any other type of card.

Instead of considering whether you should get a Visa or a Mastercard, think about what type of card you want and which bank you want to work with. Apply for a card that offers the rewards you want and has fees that match your budget. Whichever one you choose, you’ll be able to use it around the globe and get a very similar experience from the card network.

Update 9/21/23: Bonus is at 30,000 if you apply via the Credit Karma link (ht RJ)

As rumored Wells Fargo has launched the new Autograph card. Card details are as follows:

Welcome bonus 30,000 points on $1,500 in first 3 months (worth $300)

Card earns at the following rates:

3x on dining, transit, travel, and streaming services, gas, phone plans

1x everywhere else.

Redemption details:

Rewards can be redeemed in $25 increments for 2,500 points. Or get in $20 increments for 2,000 points at the Wells Fargo ATM.

Minimum of 100 Rewards Points or $1 in Cash Rewards in your Rewards Account is required.

Redeem for Purchases is another option.

Automatica redemptions can be set up in $25 increments.

Points do not expire while this Credit Card account is open.

No annual fee.

No foreign transaction fees.

Visa Signature benefits.

Update History:

Update 5/13/23: Bonus now 20,000 instead of 30,000.

Update 3/25/23: Bonus is 30,000 points when you do a google search for Wells Fargo Autograph. Hat tip to TheBigDonDom. You can also use this link.

Update 1/12/23: Bonus reduced to 20,000 points.

Update 7/20/22: It’s now possible to product change to this card. Most Visa® credit card types are available to switch with the exception of College, Secured, The Private Bank, Wells Fargo Advisors, Hotels.com® and any Propel American Express® cards.

American Express has changed the terms on Delta personal cards to exclude getting the sign up bonus across the Delta family of cards. The previous terms stated:

Welcome offer not available to applicants who have or have had this or previous versions of this Card. We may also consider the number of American Express Cards you have opened and closed as well as other factors in making a decision on your welcome offer eligibility.

The new terms differ based on the card you’re apply for:

Delta gold:

You may not be eligible to receive a welcome offer if you have or have had this Card the Delta SkyMiles® Platinum American Express Card, the Delta SkyMiles® Reserve American Express Card or previous versions of these Cards.

Delta Platinum:

You may not be eligible to receive a welcome offer if you have or have had this Card, the Delta SkyMiles® Reserve American Express Card or previous versions of these Cards.

Delta Reserve:

You may not be eligible to receive a welcome offer if you have or have had this Card or previous versions of this Card.

Basically gold has the most restrictive terms and Reserve has the same terms as before. It’ll be interesting to see if similar language gets added to the business cards or if they will remain the same. Seems like the play is to get the gold card first, then platinum, then reserve and that way you can still hit all three bonuses without issue.

In the list of things you want to be doing around the holidays, fending off scam artists has to be at the bottom. And yet, the holidays can be a prime time for scammers hoping to take advantage of the busy season. One fraudulent transaction is easily overlooked in a bank statement full of gift purchases, and there may not be time to dispute suspicious charges when you’re hosting out-of-town guests.

Research-based advisory firm Javelin Strategy & Research defines an identity fraud scam as a tactic that a criminal uses to steal someone’s personal information for the purpose of illegal financial gain. Consumers lost $43 billion in 2022 to these scams, according to Javelin’s 2023 Identity Fraud Study.

If there’s good news, it’s that there were fewer reported victims of identity fraud in 2022 as compared with 2021, with a 17% decrease in the amount of money lost to scams. The bad news is that scammers have become more sophisticated in their methods and have a new tool in their arsenal: artificial intelligence. AI programs can be used to generate scam emails, text messages or audio recordings that mimic the speech of loved ones.

An awareness of scammers’ latest tools and tactics is a potent defense against identity fraud. Here are five credit card scams to watch out for this holiday season.

1. The Amazon scam

Amazon will be the go-to holiday shopping destination for many people. But as our inboxes fill with order confirmation emails and delivery updates, be cautious about messages that claim to be from Amazon. Scammers may contact you by email, text or phone in an attempt to steal your credit card information. They may say that you need to update your payment method to prevent your Prime membership from expiring, or that your Amazon account will be deleted unless you verify your account by providing payment details.

How to fight it: If you’re unsure if an email or text message is legitimate, don’t click on any links in it. Instead, log in to your Amazon account and go to the Message Center, which contains a record of all communications from Amazon. If you’re contacted by phone, don’t provide your credit card information. Amazon won’t ask for payment information by phone. And never input your Amazon payment info on any website except Amazon.com.

2. The romance scam

The holiday season may heighten feelings of loneliness, which can make romance scams particularly effective. After creating a fake profile on a dating website or social media platform, scammers will strike up a relationship with their victims before making a plea for money. Common reasons for needing money include medical or legal bills or funding for an investment opportunity. The 2023 Consumer Impact Report from the Identity Theft Resource Center, a nonprofit that helps victims of identity crimes, noted that romance scams consistently report six-figure losses, highlighting the seriousness of this scam.

How to fight it: If someone you’ve met on a dating website or social media platform asks you for money, research their name and do a Google reverse image search of their profile picture to try to figure out if they’re masquerading behind another’s identity. Investigate any detail that sounds suspicious; you don’t have to automatically accept what someone says as truth.

Don’t give payment details or personal information that could be used to open credit cards to someone you haven’t physically met.

3. The gift card scam

Gift cards make great stocking stuffers or last-minute gifts, but they’re also a favorite target of scammers. The scammer will contact victims by phone, email or text and ask them to purchase gift cards, usually as a form of payment for an outstanding bill or as prepayment for a service they’re offering to render.

For example, a person posing as a computer technician says he can remove a virus from your laptop in exchange for a $100 Amazon gift card. Once the gift card has been bought, the scammer asks for the gift card’s number and PIN. That way, the scammer doesn’t need to expend any effort getting their hands on the actual card.

How to fight it:No legitimate business or government agency accepts gift cards as payment. Whenever you buy gift cards, keep the receipts and take pictures of the card numbers and PINs in case you need to file a report with the gift card company or the Federal Trade Commission.

4. The charity scam

Donations tend to spike between Thanksgiving and Christmas, and some scammers capitalize on the increased spirit of generosity during this time. Pretending to solicit donations on behalf of a charity, scammers will ask for donations by phone, email, text or a crowdsourcing platform. They may prompt you to enter payment information on a bogus website or give it over the phone.

How to fight it:When you’re asked to make a donation, get the charity’s name and the cause it supports. If you aren’t sure whether you’re corresponding with a legitimate charity, take a beat to do more research. Look up the charity’s name on a website that vets nonprofits, like Charity Watch or Charity Navigator.

When making donations, pay with a credit card if possible: The major card issuers have zero-liability policies that offer you financial protection from fraud. Payments made in cash, cryptocurrency or by wire transfer are harder to recoup; if you’re asked to donate in those ways, it could be a sign that you’re dealing with a scammer.

5. The lottery scam

Coming into a windfall of cash during the holidays sounds too good to be true, and it probably is. In this scam, the criminal claims you’ve won a physical or monetary prize, which is yours as long as you remit payment or hand over your payment information to cover a processing fee.

How to fight it: Ask for the name of the company claiming you’ve won the sweepstakes, and contact them to confirm whether you’re a winner or not. Take care, though, to look up the company’s information yourself rather than using a phone number provided to you by the person saying you’ve won.

A real sweepstakes doesn’t require payment; a real prize is, by definition, free and won by chance. You don’t need to send payment or disclose personal information to win a true lottery.

How to minimize damage and recover from a scam

Even the most vigilant among us can fall victim to a scam. However, there are steps you can take to minimize the damage and work toward recovery.

Prevention: Freeze your credit file with the three major credit bureaus: TransUnion, Experian and Equifax. Scammers can’t open a new credit line in your name when a freeze is in place. You might also elect to receive alerts of suspicious account activity on your credit card, or even when any transaction is made.

Mitigation: If you think your credit card has been compromised, place a lock on the card so it can’t be used until you unlock it. Then, call your card issuer — ask for the fraud department, if one exists — and communicate your concerns.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

Many people with good credit scores own at least one credit card, with 82% of all credit card holders boasting credit scores of 680 and higher.

When used responsibly, credit cards can be a great tool for building credit. Here’s a complete guide on how to build credit with a credit card.

Table of contents:

5 Best Ways to Build Credit with a Credit Card

To improve your credit score with a credit card, you need to know how to best use your credit card. Responsible credit card usage is key to boosting your credit—it won’t increase simply because you got a credit card. Here are the five best ways to increase your credit score using a credit card.

1. Pay bills on time

One of the most important parts of having a credit card is paying your credit card bill on time. Payment history is the largest factor in your FICO® score at 35%, which means it can make or break your score.

Get into the habit of paying your bills on time every month and watch your score grow. Setting up automatic payments for a few days before your bill is due can help make sure you never miss a payment and give a cushion of time for the payment to go through.

2. Keep your utilization rate low

Your credit utilization rate, or credit utilization ratio, is the amount of credit you’re using divided by the amount of credit available to you (your credit limit).

Let’s say your credit limit is $500. This is the maximum amount you can spend on your credit card before payments are denied, but that doesn’t mean you should spend that much.

It’s best for your credit score to keep your utilization rate under 30%—under 10% is even better! This is because the amount of money you owe impacts 30% of your FICO score and the lower this number is, the better. But how much can you actually spend with your credit card?

If your credit limit is $500, 30% of that is $150. So, you should aim to never have a balance over $150 on your credit card. Even better, shoot for a balance under $50 (10% of your limit).

3. Don’t overspend

You don’t need to carry a balance on your credit card to improve your credit score. Paying off your balance in full every time, not just making the minimum payment, is the best practice.

Carrying a balance can cost you more in credit card interest and late fees. Plus, it may increase your utilization rate and damage your credit score. Do your best to avoid credit card debt and treat your credit card like a debit card—only spending money you have.

4. Use your card regularly

Using your first credit card requires a delicate balance. You don’t want to spend too much and go over your utilization rate, but if you don’t use it regularly enough, the lender may close your account. Using some of your available credit is one of the best ways to boost your credit.

The solution is to use your card to make regular, small purchases. This could include purchases like:

Gas

Groceries

Small, recurring bills

Inexpensive meals

After a while of making these regular purchases and paying them off on time, your credit card provider will probably increase your credit limit, allowing you to spend more with your card. Until then, using your card for these types of purchases can help you establish responsible credit card habits and keep your credit utilization low.

5. Avoid opening more cards

Every time you apply for a new credit card, the creditor makes a hard inquiry on your credit, which drops your credit score a few points. You’ll be able to earn back those points in the long run, but in most cases, if you apply to a bunch of credit cards at once, those hard inquiries will add up and take a toll on your credit.

For this reason, you should only apply for one credit card at a time and make sure it’s a good match for you. When you’re first building your credit, it’s best to start small with one card and take your time to practice building credit with it before opening more accounts.

How to Use Credit Cards to Start Building Credit

To recap, here’s a step-by-step guide to increasing your credit score with your first credit card.

Apply for a credit card you can qualify for.

Connect your bank account for automatic monthly payments.

Make small purchases to use under 30% of your credit limit (under 10% is better).

Pay your balance in full and on time each month.

Avoid opening new credit cards.

Regularly monitor your credit report.

If you’re not sure what kind of credit card to apply for, here are the types of credit cards you can use to start building credit and the advantages of each.

Unsecured credit card: An unsecured credit card, or standard credit card, is great if you qualify for one. They don’t require a deposit to use and often offer rewards.

Secured credit card: This type of card is great if you can’t get approved for a standard credit card. Secured cards require a deposit but then they work like any other credit card.

Student credit card: If you’re a student, it’s typically easier to qualify for a student card than a standard credit card. These cards can have decent rewards too!

Store credit card: Store credit cards can sometimes be easier to qualify for than standard cards. Be sure to choose one for a store you shop at often or can be used at other places besides the specific store.

Authorized user for a credit card: A family member or friend can add you as an authorized user on their credit card. You’ll be able to make purchases and receive credit score benefits but won’t be responsible for charges.

How to Build Credit without a Credit Card

If you’re not ready for a credit card or can’t get approved for one, here are some ways to build credit without a credit card.

Credit-builder loans

Credit-builder loans are a lot like what they sound like. They’re low-interest rate loans that help borrowers with poor or no credit build credit, and they function differently than your typical loan.

With a standard loan, you receive the money you’re borrowing upfront, but with a credit builder loan, the money is held in a savings or CD account until you pay it off. This makes it very low-risk for the lender, as your payments are also adding your collateral to the savings account.

You make monthly payments, including interest on the loan, and making these payments on time will help build your credit. Once you pay off the loan, you get all the money back and in some cases, interest if it was incurred while your savings collateral was being held.

Rent reporting

The three major credit bureaus, Equifax®, Experian® and TransUnion®, only include rent payment information on your credit report if they receive it. Most landlords don’t report this information, but it could benefit your score if you consistently pay your rent on time.

You can ask your landlord to report your rent payments or find a rent reporting service that will let you submit the information yourself. Ideally, your rent payments should be reported to all three bureaus for maximum impact.

Passbook loans

This type of loan is very similar to credit-builder loans, except it uses the money you already have in your savings or CD account as collateral. Interest rates for passbook or CD loans are typically lower than credit cards or personal loans.

Like credit-builder loans, you build credit as you make payments on the loan each month and can access the money once you’ve paid it off. Check that your bank will report your payments to all three credit bureaus before taking out this type of loan.

Building Credit with a Credit Card FAQ

Have more questions about how to use a credit card to build credit? Check out the answers to these common credit card questions.

When should you pay your credit card bill to build credit?

You should pay your credit card bill by its due date, at the very least. Paying your bill early (before the end of your billing period) or making extra payments if you’re planning to carry a balance may help boost your credit score even more since it will reduce your utilization rate.

How fast does a credit card build credit?

While it may take a while to build credit, you can help establish a baseline credit score if you have an account open and active for 6 to 12 months, to allow your FICO® score to be calculated. You may be able to establish a baseline credit score after 6-12 months of making credit card payments on time. With consistent and responsible credit card usage, you should see a positive impact on your credit over time.

Do you need a credit card to build credit?

No, you don’t need a credit card to build credit. Responsible credit card usage is one of the easiest ways to build credit, but it may not be the right answer for everyone. There are other ways to improve your credit score, like taking out loans, reporting rent and utilities or being added as an authorized user to someone else’s credit card.

A credit card is a great way to start building credit. If you’re looking for more ways to boost your credit score, check out our resources on Credit.com and the features included with ExtraCredit. ExtraCredit is a full- credit score monitoring service that can help you understand what areas of your credit you need to work on to build and maintain your good credit.

Finding out how much you’ve spent with a credit card probably isn’t anyone’s favorite task; nevertheless, it’s an important one for optimal financial health.

Checking your credit card balance is the only way to know how much you must pay the card issuer in order to avoid interest charges. As credit card APRs are notoriously high, paying off your credit card bill in full and on time saves you money — and preserves your credit scores.

Regular check-ins on your credit card account can also help you stay on budget and be more mindful of your spending habits.

Credit card issuers want to get paid, so they offer a variety of ways for cardholders to check their credit card balance, some of which are surprisingly low-tech.

Here’s how to do it.

What is a credit card balance?

At the most basic level, a balance on a credit card refers to the amount a cardholder owes to the card issuer, say, Barclays or Chase. There are a few different types:

Statement balance. The amount owed at the close of a billing cycle, which is usually 28-31 days long. The statement balance will appear on the credit card statement. Issuers may send electronic statements or hard copies via mail.

Current balance. Also known as an outstanding balance, the current balance is the amount you owe at the moment you check your account. It may or may not be the same as your statement balance, depending on your card usage and your payments in between billing cycles

Negative balance. If your account has a negative balance, you don’t owe the issuer anything. On the contrary, a negative balance indicates that the issuer owes you.

Ready for a new credit card?

Create a NerdWallet account for insight on your credit score and personalized recommendations for the right card for you.

How do you check your credit card balance?

There are many ways to check your credit card balance; pick the one that’s most convenient for you.

Log into your account online.

Log into your account via the issuer’s app.

🤓Nerdy Tip

If you want to know your current balance and statement balance, check your account online or in the app. Some credit card statements may not show both.

Review your credit card statement. An electronic statement may be accessed online or in the app, or you can request a paper statement. Note that some issuers charge a fee to send copies of credit card statements.

Call the issuer at the number on the back of your credit card.

Ask a representative in person. For example, if you have a Bank of America®-issued card, you could ask for your statement balance at a local branch. Want to know the balance on a store credit card such as a Macy’s card? Head to the closest store and ask one of the employees to look up your credit card balance.

Balance alerts. Some issuers allow cardholders to receive alerts that notify them when their credit card balance hits a certain amount. Alerts can usually be sent via text or email.

It’s now possible to activate all 5% category credit cards for the fourth quarter of 2023, including the Chase Freedom, Chase Freedom Flex, Discover IT, Citi Dividend, US Bank Cash+ and some smaller cards. In this post we’ll provide the activation link for each card and links to track your spend, along with strategies to help increase spend in these categories.

Dates: October 1st – December 31, 2023. Store purchases can usually be done until the last minute while online purchases should be given a buffer zone of a day or two.

Activation Link / FAQ / Sample Stores & Exclusions / Our original post

With the Freedom and Freedom Flex cards, activate to earn 5% back this quarter on up to $1,500 in spend at PayPal, Wholesale Clubs, and at Select Charities.

Paypal – Should work for any purchase with Paypal payment. This is always a easy and useful category given that many/most online retailers accept Paypal, e.g. Walmart, Target, Best Buy, etc.

I sometimes pay my taxes with a credit card via Paypal to trigger this category, read more about paying taxes with a credit card in this post.

Some people might find it worthwhile to swallow the 2.9% Paypal fee and max out this category by paying family or friends with their Freedom card. Just note the fine print technically excludes this: “Person-to-Person (P2P) transactions made with your Chase Freedom card on PayPal may be prohibited or not eligible for 5%.”

You can also do your year-end charitable giving with Paypal payments on many charities, or to almost any charity with Paypal Giving Fund.

Readers note that if you use the Freedom Flex via Paypal at Dining or Drugstores you’ll end up getting 7x due to the extra 2x bonus the card has on those categories.

Wholesale Clubs – Should work for Costco, Sam’s Club, BJs, and similar.

Bear in mind, Costco in-club only accepts Visa cards; online you can use Mastercard as well, and you can even order Costco Cash cards for use in-club. Also note, gas at Costco will not work to earn the 5x; the workaround is to buy Costco Cash cards in-club and use those to purchase gas.

You can buy Sam’s Club gift cards at the club or online which can then be used at Walmart or Walmart.com or Walmart gas. (Or you can buy Walmart e-gift cards from Paypal Digital Gifts which also earns 5x as part of the Paypal category.)

Some wholesale clubs sell third-party gift cards or even Visa gift cards.

Exclusions: “Gas, fuel, wholesale specialty service purchases such as travel, insurance, cell phone and home improvement will not qualify in this category. Mastercard not accepted at Costco warehouses or at gas stations.”

Select Charities – includes: American Red Cross, Equal Justice Initiatives, Feeding America, Habitat for Humanity, International Medical Corps, International Rescue Committee, Leadership Conference Education Fund, NAACP Legal Defense and Educational Fund, National Urban League, Thurgood Marshall College Fund, United Negro College Fund, UNICEF USA, United Way, World Central Kitchen GLSEN, Out and Equal, Sage.

Tip: Click this link (login required) to check how far you are along the $1,500.

Discover – Amazon, Target

Activation Link / Our original post

With your Discover card, activate to earn 5% back this quarter on up to $1,500 in purchases on Amazon.com and at Target.

Amazon.com

Target – Not very useful for someone who already has the 5% Target REDcard. It can still be useful for buying Target gift cards at Target which do not earn 5% on the Target REDcard.

Activate to earn 5% Cashback Bonus at Amazon.com and Target from 10/1/23 (or the date on which you activate 5%, whichever is later) through 12/31/23, on up to $1,500 in purchases. Amazon.com purchases include those made through the Amazon.com checkout, like digital downloads, Amazon Fresh orders, Amazon Local Deals, Amazon Prime subscriptions, and items sold by third party merchants through Amazon.com’s marketplace. This also includes purchases in-store at Amazon Go. Amazon, the Amazon.com logo, the smile logo and all related marks are trademarks of Amazon.com, Inc. or its affiliates. Target purchases include those made in store at Target, Target.com, or through the Target app. Purchases from individual merchants and stand-alone stores within physical Target locations may not be eligible for this promotion. Purchases made online or through the Target app from Target affiliates, individual merchants or stand-alone stores may not be eligible for this promotion, including, but not limited to, targetoptical.com and targetphoto.com.

Tip: Login, then click this link to see you how far along the $1,500 you are.

Citi Dividend – Add Me

Landing Page | Our Original Post

With your Dividend card, activate to earn 5% back this quarter at ADD ME. Citi is different than the other cards in that you have a $6,000 annual cap rather than a $1,500 quarterly cap. You can get 5% back on up to $6,000 in this quarter or you can save the entire amount for a different quarter, or you can use part up each quarter.

US Bank Cash+/Elan – Select your Categories

Activation link | Merchant List | Our Original Post

U.S. Bank Cash+ and Elan Max offer 5% cash back in two categories, up to $2,000 combined total per quarter. Keep in mind that Car Rentals was recently replaced with TV, Internet, and Streaming Services.

Here are the current options:

TV, Internet, and Streaming Services

Home utilities

Select clothing stores

Cell phone providers

Electronic Stores

Gyms/Fitness

Fast food

Ground Transportation

Sporting goods

Department Stores

Furniture Stores

Movie theaters

Tip: Login here, then scroll down and click on the red “View Your Cash+ History” button.

Bank of America Customized Cash Rewards

Our Original Post

The Cash Rewards card from Bank of America offers 3% back on one selected category, up to $2,500 per quarter. If you don’t select anything it defaults to gas. Once you selected a category for one quarter, that remains your category in the future unless you change it. Each calendar month you can change it if you’d like, but you’re always limited to $2,500 for the entire quarter.

Gas and EV charging stations (default category)

Online Shopping; this category also includes cable, streaming, internet, and phone plan

Dining

Travel

Drug Stores

Home Improvement/Furnishings

This category is especially lucrative for those who have Preferred Rewards status with Bank of America which can get you 5.25% back on one of these categories at the higher relationship level.

Lots of useful categories here. Important note: the Cash Rewards card also offers 2% back at grocery stores and wholesale clubs up to $2,500 per quarter, and that $2,500 limit combines with the Category Selection limit. After spending $2,500, you’ll earn 1% back on everything.

Other Cards with 5% Category

Nusenda FCU – Retail, Online, Restaurants

Landing Page | Our Original Post

Earn 5% this quarter on up to $1,500 in purchases on Retail Stores, Online Retail Purchases, Restaurants.

This is on top of the regular 1% for a total earn of 6% back.

Abound CU – Amazon

Landing page | Our Original Post

Abound Credit Union Visa Platinum card offers 5% on up to $2,000 on Amazon purchases.

Langley FCU – Grocery, Streaming, Cable, Department Stores

Landing Page | Our Original Post

Langley Federal Credit Union offers 5% back each month in one selected category, on up to $100 cash back total ($2,000 spend).

The category options at time of this writing: Streaming, Cable & Internet services, Grocery, Department Stores.

Vantage West [AZ] – Select your Category

Landing Page | Our Original Post

Get 5x points on the category of your choice, up to $1,500 per quarter. Eligible categories:

Safe Credit Union Cash Rewards Visa card offers 5% this quarter on your choice of one category each quarter (with no apparent limit). This quarter the categories are:

American Express has sent out e-mails offering increased bonuses on the Business Delta cards. Offers are as follows:

Gold Delta SkyMiles® Business Credit Card 80,000 miles after $6,000 in spend within the first three months. Plus, earn an additional 5,000 Bonus Miles after you make an eligible Delta purchase with your new Card within your first 6 months

Platinum Delta SkyMiles® Business Credit Card 90,000 miles after $8,000 in spend within the first three months. Plus, earn an additional 10,000 Bonus Miles after you make an eligible Delta purchase with your new Card within your first 6 months

Delta Reserve® Credit Card for Business 100,000 miles after $12,000 in spend within the first three months. Plus, earn an additional 20,000 Bonus Miles after you make an eligible Delta purchase with your new Card within your first 6 months

Our Verdict

None of these bonuses are at all time highs. Given the recently announced Delta changes I’d recommend waiting for better offers to come along unless you have an urgent need for the miles.