Generally, it helps to save up to 20-25% of a house’s sales price. However, factors like geographical location, economic climate, real estate interest rates, and global events will influence how much money you’ll need to buy a house.

Key Takeaways:

An ideal down payment is 20% to 25% of a home’s value.

USDA and VA home loans traditionally don’t require down payments.

If you make a down payment below 20%, you may be required to get private mortgage insurance.

How much money do you need to buy a house? That cost depends on numerous factors like inflation and real estate trends. According to the Census, homes sold for a median price of $420,700 in January 2024.

Thankfully, you don’t need to pay off that amount all at once. A down payment that’s 20% to 25% of a home’s value can help you secure a property. Even if you don’t have the funds to make a sizeable down payment, low and no-down-payment mortgage options are available.

Below, we’ll share our expertise to help you learn all about loans and mortgage options. We’ll also answer several common questions and share helpful tools, like Credit.com’s mortgage calculator.

All Costs Associated with Buying a House

Spend enough time shopping around for houses, and you’ll learn very quickly that a property’s sales price isn’t the only expense you’ll have to pay. Below, we’ll cover down payments, earnest money deposits, and other factors that determine the real cost of a home.

Get matched with a personal

loan that’s right for you today.

Learn

more

Down Payments for Different Mortgage Options

According to the United States Census Bureau, 661,000 new homes were sold in January 2023. Most homebuyers don’t pay off their properties in full from the get-go. Instead, they cover a portion of the home’s cost with a down payment, then gradually pay off the remaining value via monthly mortgage payments.

“How do home mortgage rates work?” and “What types of mortgages am I eligible for?” are common questions for first-time homebuyers.

Below, we’ll discuss four mortgage options and break down how each of them works.

1. Conventional Mortgage

A conventional loan is a mortgage option that’s offered by a private lender instead of the government. Mortgage companies, credit unions, and banks offer conventional loans, though they might require a down payment between 20% and 25% of a property’s sales price.

Lenders might request that you purchase private mortgage insurance (PMI) if your down payment is less than 20%. PMI reimburses lenders if you don’t make your mortgage payments, and borrowers will have to pay for coverage annually.

2. USDA Mortgage

The United States Department of Agriculture (USDA) offers this unique mortgage to borrowers who live in rural areas. A USDA mortgage has no down payment requirement, and its interest rate is very competitive.

To qualify for a USDA loan, you need to:

Buy an eligible property. Your potential home has to be in an eligible rural area.

Meet income guidelines. To qualify for a USDA loan, your income can’t exceed a state-specific amount.

Use the home as your primary dwelling. You have to live on the property permanently.

Be a U.S. citizen, a U.S. national, or a qualifying resident alien. Foreign nationals not authorized to remain in the United States can’t get USDA loans.

You’ll also need to meet the lender’s credit requirements. On average, a credit score of 620 or more will qualify you for a government-backed USDA loan.

3. FHA Mortgage

The Federal Housing Administration (FHA) offers this distinct government-backed mortgage. Borrowers can secure an FHA mortgage with a down payment as low as 3.5%.

Borrowers with very low credit scores might be eligible for an FHA loan, at the expense of having more strict loan limits and higher up-front costs.

To get an FHA loan, you need to meet the following requirements:

Primary residence. The house associated with your loan must be your primary residence. You can’t rent it out to others for profit.

FHA maximum limit. FHA loans can only apply to properties within a set price range. In 2024, the maximum FHA loan amount is $498,257 for single-family homes.

Debt-to-income ratio. To qualify for an FHA loan, you must spend a maximum of 43% of your income on housing costs and housing-related debt.

4. VA Home Loans

Veterans Affairs (VA) loans offer low credit requirements and come with no down payment restrictions.

Certain people qualify for VA loans, including:

Service members who’ve served for at least 90 days consecutively.

Veterans who’ve served at least 181 continuous days, depending on their deployment date.

National Guard members with six years of Active Reserve status or 90 consecutive days of active duty service.

Surviving spouses of veterans, including veterans who are missing in action or being held as a prisoner of war (POW).

Earnest Money Deposit

An earnest money deposit is a payment that buyers can place to demonstrate how serious they are about obtaining a property. Earnest money deposits are normally between 1% and 3% of a property’s sales price. This deposit is not the same as a down payment.

When you make an earnest money deposit, those funds are put into an escrow account. If the seller of a property closes on a deal with you, your earnest money deposit is then added to your down payment. If the seller doesn’t close on the deal with you, it’s possible to regain your earnest money deposit if contingencies are set in place.

Several common contingencies include:

Home inspection contingency: Buyers request to have an inspection conducted on a property. If problems are discovered, buyers can back out of a deal.

Home sale contingency: Buyers who might need to sell their current home can ask for extra time.

Insurance contingency: This is for buyers who may need time to obtain home insurance for a property.

Closing Costs

Closing costs include taxes, appraisals, home inspection costs, title costs, and attorney fees. They’re generally between 3% and 6% of your mortgage principal. Your mortgage principal is the amount you borrow—so the bigger your down payment, the less you’ll pay in closing costs.

Let’s use the $200,000 home above as an example. Consider these three 4% closing cost scenarios:

Your down payment is 10%, or $20,000, leaving a mortgage principal of $180,000. Your closing costs will roughly amount to $7,200.

You offer20%, or $40,000, as your down payment. Your mortgage principal is $160,000, and you’ll pay $6,400 in closing costs.

You apply for a mortgage with no down payment, so your mortgage principal is $200,000. Ultimately, you’ll pay $8,000 in closing costs.

Home-Buying Examples

Next, we’ll show you how to determine your down payment on a home with the previous loans as examples. Let’s imagine your dream home is on the market for $200,000.

Down payments for conventional mortgages are usually $10,000 – $40,000.

USDA mortgages normally don’t require down payments.

An FHA mortgage can cost as little as $7,000.

A VA home loan also doesn’t require a down payment.

USDA and VA home loan mortgage options have the lowest up-front costs for eligible borrowers. An FHA mortgage is less costly than a conventional loan, but interest rates will affect your total payments in the long term.

Financial Resource Ideas

Making a down payment can be challenging because you need a paper trail of your purchases. In most cases, you can’t use borrowed money for a down payment.

Conversely, we know several creative ways to come up with a down payment:

Profits earned from stock or bond sales

Filing for an IRA or 401(k) withdrawal

Paying with money from your checking or savings account

Cash earned from a money market account

Using funds from your retirement account

Monetary gifts

You can roll other funds, like your tax return or a security deposit refund, into your down payment, too.

How Much Money Should I Save Before Buying a House?

It’s important to look at the big picture when buying a house. You’ll need to pull together a down payment and closing costs, but you’ll also need to budget for removal costs, inspections, and repair fees.

A tool like a monthly budget template can put your common expenses into perspective and help you better understand how much house you can afford with your current income.

When Should I Seek Mortgage Relief?

“What happens if I miss a mortgage payment?” is another concern for new and long-time homeowners. First, know that your home won’t immediately be foreclosed on if you miss a payment. Foreclosure usually isn’t imminent unless you’ve missed two or three payments.

If your mortgage payments aren’t within reach, you can contact your lender and explain your specific situation. Seeking forbearance, which is a temporary pause on your payments, can also help you regain your bearings.

Prepare to Buy a Home with Credit.com

Knowing your credit score and understanding the elements that affect it can help you know what you need to do to prepare for loan opportunities.

Sign up for Credit.com’s ExtraCredit® subscription to check out 28 of your FICO® scores. Afterward, visit our mortgage rates page to get additional information.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

Making a financial plan can be intimidating, especially if you don’t know all of the essential budget categories you should include. Budgeting isn’t a one-size-fits-all process either, as the importance of each category will largely depend on your specific financial situation.

This article will review the top 12 budget categories that can bolster your financial plan. Credit.com also has multiple personal finance resources that can enhance your financial literacy.

Several important budget categories account for housing, transportation, health care, entertainment expenses, and more.

Key Takeaways:

The prioritization of budget categories will be unique to your needs.

Some expenses have fixed prices, while others have variable costs. You’ll need to account for both from one month to the next.

Tools like money apps and budget spreadsheets can help you visualize your spending habits.

Table of Contents:

Why Do I Need a Budget?

A budget can ensure that you aren’t caught off-guard by bills throughout the month—especially near the month’s end or right before you get paid. Keeping a budget can also provide long-term data based on your spending habits and serve as a snapshot of your priorities.

Effective budgets can help you plan for longer-term goals, like retirement, and inform you of what expenditures truly make you happy—and which ones aren’t necessary.

Fixed Expenses vs. Variable Expenses

Fixed expenses refer to items that essentially cost the same each month, with very little fluctuation in terms of pricing. Mortgage and rent payments, auto loan payments, and internet service bills will likely fall into this category.

Variable, or flexible, expenses can drastically differ from one month to the next. The amount you spend on groceries, clothes, entertainment, and even medical appointments can all vary over time.

Top 12 Budget Categories to Add to Your Plan

The following budget categories can help you map out your monthly expenses. Depending on your unique circumstances, these categories may need to be adjusted in terms of their priority.

1. Housing Expenses

Housing often takes top priority as your living space is directly tied to your long-term health and safety. You also need a stable housing situation to perform well at work and ensure that you have the funds to make your mortgage or rent each month.

While there’s no strict maximum for the housing category, you can expect to spend anywhere from 25% to 35% of your income on your mortgage or rent payments. If your housing budget exceeds more than 35% of your monthly income, refinancing your mortgage or looking for another living space might be more expense-friendly in the long run.

Items that fall in housing expenses:

Rent

Mortgage Payment

Appliances

Household Repairs

2. Utilities

The ability to live comfortably in your home is just as crucial for your health as actually having one, which is why utilities are usually another high-priority item. Many residential buildings in some urban areas have ordinances that require certain utilities, like water and electricity, to be considered safe living.

Utilities rarely come close to the top of the list of expenses in terms of cost, and you can reduce their cost with proper management. Depending on their usage, you can expect to spend around 5% to 10% on monthly utilities.

Items that fall in the utilities category:

Electricity

Water

Telephone

Natural gas

Sewer

Trash

Heating

Air conditioning

3. Transportation Costs

Owning or leasing a vehicle, along with repairing it, can be another high-priority expense. Some areas may complement alternative means of transportation, such as public transit or biking—which would result in much less money going toward this category.

The cost of owning a car includes the tags, licenses, and maintenance on top of the monthly car payments. Depending on your method, transportation or travel expenses will likely cost you anywhere from 10% to 15% per month.

Items that fall in transportation costs:

Gasoline

Car payment

Registration fees

Vehicle repairs and maintenance costs

New tires

4. Groceries

Groceries (not food from restaurants) and water encompass our basic needs. Store-bought groceries and water may require a large chunk of your income, though this category offers a lot of flexibility in terms of total spending.

Cooking dinner at home with groceries can help you save money, as many home-cooked meals can last multiple days. You should probably expect to spend between 10% and 15% of your monthly income on food expenses.

Items that fall in the food category:

Grocery budget

School lunch

5. Insurance

This broader category covers numerous subcategories that apply to different people. For example, if you live in a large, urban area with well-run public transportation, you may not have to worry about auto insurance.

Insurance may be classified under different categories depending on who you ask. Some pundits include health care in this category, for example. Depending on what type of insurance you need and your insurance premiums, you can look to spend anywhere between 10% to 25% of your income on this category.

Items that fall in the insurance category:

Life insurance

Auto insurance

Renters insurance

Homeowners insurance

Health insurance

Vision insurance

Disability insurance

Dental insurance

Vision insurance

Pet insurance

6. Health care

This category may have higher or lower priority depending on your specific health needs. Health and dental insurance in America is also quite costly—making them one of the primary reasons Americans go bankrupt.

Health care costs include annual checkups, clinic visits, prescription medications, and general medicines, like pain relievers. Health care is a variable expense because some months can be costly while others don’t have any expenses. Even when you don’t have any expenses, it’s a good idea to put away a little cash for a rainy day.

Items that fall in the health care category:

Anticipated copays

Prescription medications

Orthodontic work (braces)

Prescription eyeglasses

Primary care visits

Dental care visits

7. Savings

Everyone needs some kind of emergency fund to cover those unforeseen expenses. Regularly dedicating a small portion of your monthly income can help you save for major life events down the road.

There’s no hard line about what amount you should save, but a safe bet is between 5% and 10% of your monthly income. Saving this amount can help you handle emergency expenses and create a nest egg for a future big purchase.

Items that fall in the savings category:

Emergency fund

Health savings accounts

Fun money

Three to six months’ worth of expenses

Saving for a specific purchase (vehicle, college savings, vacation, etc.)

8. Retirement

While you could argue that retirement or a 401(k) is a type of savings, we refer to savings as money that can be used for any expense without penalty. Retirement accounts like IRAs help you save money that’s intended for use in the future. If you take money out of your retirement account before the preset time (unless you have a 457(b) account), you will incur a 10% tax penalty.

Much like savings, this is another category without a hard-line amount that you should contribute but should see at least 5% to 15% of your income. Ideally, you can primarily rely on this money once you’ve retired.

Items that fall in retirement:

Employer-sponsored retirement plan

401(k)

403(b)

Roth IRA

457(b)

9. Debt

This category applies to a significant portion of the U.S. population—especially those who have a student loan, credit card debt, or personal loans. Debt is a consideration that often has a lower priority level because we can pay it off over time. That said, it’s important to make sure you don’t fall behind on your payments as the penalties and fees can compound if left unchecked.

Because everyone’s situation is different, there’s no given amount of your monthly income you should dedicate to debt payments. We do, however, recommend that you pay more than the monthly minimum.

Items that fall in the debt category:

High-interest credit cards

Vehicle loan

Student loans

Personal loans

Medical bills

10. Personal Care and Hygiene Items

This category encompasses both wants and needs. Toilet paper and toothpaste should be considered “needs,” while designer clothes or expensive watches are examples of “wants.”

Because most personal expenses are lower priority, there’s no expected amount you should budget for this category, but it should remain relatively low on your list of priorities. Ensure that everything else above on this list is covered first, then look to see what you can spare on these purchases.

Items that fall in the personal care and hygiene category:

Shampoo

Deodorant

Toothbrush/toothpaste

Gym memberships

Shoes

Dry cleaning

Toiletries

Laundry detergent

Cleaning supplies

Diapers

Hair care

11. Entertainment

This category sits at the bottom of our list for a good reason, but it’s still essential to include. If you find yourself in a budget crunch, this is easily one of the first categories you should reduce until finances stabilize.

Sporting events, vacations, or streaming services like Netflix fall into this category. Given its otherwise low priority, there is no set amount you should spend on entertainment, and extra money can shift from month to month.

Items that fall in the entertainment category:

Books

Electronics

Restaurant dining

Concert tickets

Events

Vacations

Movies

Coffee

12. Other

This low-priority category covers pretty much anything else not already discussed. That can include property taxes that are a high priority in most circumstances, but you can often work with the IRS to get a debt repayment plan.

Various “other expenses” might also include donations, parking fees, child support, gifts, and school supplies, depending on your circumstances.

Some of these other expenses are significantly more important than others, but things like home improvement can be considered a kind of investment.

Items that fall in the other budget category:

Miscellaneous expenses

Child care

Holiday decor

Special occasions

Alimony

Anniversary presents

Tutoring

Private school

How Do I Make a Budget?

Considering the budget categories we presented in this article, one budgeting method that could work for you is a monthly budget spreadsheet. Or, you can use a budgeting app like Mint or another high-end competitor.

There are plenty of resources to use, so you should do lots of research on any budgeting apps that you consider downloading. Since not all of the apps work the same, search through different apps to find what best serves your budgetary needs.

What Is a 50/30/20 Budget?

Numerous financial pundits advocate for a 50/30/20 budget scheme, in which 50% of your income goes to necessary expenses, 30% goes to savings accounts, and 20% goes to wants and miscellaneous expenses. It’s also not uncommon to see people devote 30% of their funds to wants and 20% to savings.

This strategy often faces scrutiny during periods of economic strife, such as high inflation rates. Nevertheless, many budgeting apps may recommend this plan if your current income can support it.

Refine Your Budgeting Plans With Credit.com

The categories we’ve discussed today, along with their corresponding priority levels, can all vary from person to person. Building the best budget for your specific needs calls for a bit of craftiness and professional assistance.

Credit.com offers a wealth of tools and resources to help build credit, such as a free monthly budget template and services that allow you to report your utility and rent to the credit bureaus.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

A financial hardship letter explains an unforeseen circumstance that has made you unable to make regular payments on a loan and requests a modification to help you get back on track.

No matter how well you prepare, many Americans will encounter times of financial hardship due to circumstances outside of their control. Events such as company layoffs, natural disasters, and divorce can throw a wrench in our finances, making us unable to pay our financial obligations.

Instead of falling behind on payments during difficult times, take a proactive approach to your finances. Sending a financial hardship letter to your creditor can help you salvage your credit score while you get back on your feet.

Read on to discover what these letters are, situations that warrant them, and how to write your own.

Table of Contents:

What Is a Hardship Letter?

A financial hardship letter is a correspondence you send to a creditor that explains why your current financial situation prevents you from making debt payments. After providing details about your hardship, such as the cause and timeline, request that the creditor provide a mutually beneficial solution.

Depending on your specific circumstances, you could suggest to your lender that they assist you by:

Suspending your monthly payments for the time being

Decreasing your payment amount

Lowering your interest rate

Pardoning overdue payments

Waiving penalties for late payments

Adjusting the terms of your loan

Resolving your debt for an amount less than you owe

For example, if you were recently injured due to an accident, you could ask the creditor to temporarily pause your payments until you recover.

What Is Considered Financial Hardship?

Since everyone’s situation is different, you may be wondering what qualifies as financial hardship. A financial hardship is any scenario beyond your control that makes you unable to pay for your living expenses.

Examples of financial hardships include, but are not limited to, the following:

Employment layoff

Pay cut

Home foreclosure

Decreased number of working hours

Job relocation

Natural disaster

Emergency event

Divorce or separation

Military deployment or transfer

Death of a spouse or family member

Incarceration

Serious injury or illness

As you can see, the examples above are out of your control. On the other hand, circumstances that creditors are not likely to deem as a financial hardship include:

Poor money management or overspending

Routine expenses

Voluntary employment shift

Purchase of a home

Decrease in property value

Payment of college tuition

Investment losses

How to Write a Hardship Letter

When writing your financial hardship letter, address it to the loss mitigation department of your lender. Include your contact information and loan number so they can identify your account. Write your letter clearly and concisely, following the instructions provided below.

1. Explain Your Hardship

Be honest with your creditor about the circumstances surrounding your hardship, but keep your explanation concise. Aim to keep your explanation under one page.

While you should include relevant details such as what caused the hardship and when it started, don’t include unnecessary information. For example, you might inform the creditor that you’re going through a divorce and the legal fees are causing financial strain, but you don’t need to go into the cause of the divorce.

Remember to be truthful—don’t exaggerate your circumstances or include inaccurate information.

2. Provide Documentation to Back Up Your Claim

Provide up-to-date and relevant documentation as evidence for the statements you make in the letter to bolster your claim. Documents the lender may want to review include:

Bank statements

Pay stubs

Tax returns

Medical bills

Employee termination letter

Divorce certificate

Military orders

Proof of incarceration

3. List Steps You’ve Taken to Alleviate Your Financial Burden

Let the creditor know the actions you’ve already taken to help improve your financial situation and pay your debt. Steps you might take include limiting expenses, selling personal items, or working a side gig to make extra income. This provides the lender with additional context and shows that you’re taking personal responsibility for your financial situation.

4. Clearly State Your Request

The purpose of writing a hardship letter is to request help from the creditor during your difficult time. Make sure to clearly state exactly the action they can take to assist you and how it will help you. Provide your proposed solution or a couple of suggestions the lender might consider.

5. State Your Commitment to Paying Your Debt

Conclude your letter with a statement expressing to the lender that you’re committed to paying your debt and finding a solution that works for both of you. Sign your name to the end to formally close the letter.

Financial Hardship Letter Template + Sample

Below is a hardship letter sample and template to help you get started. When using the template, make sure to enter your own information where there is bolded text.

Harry Jones, Loss Mitigation Department of Georgia Bank

444 Peach Lane

Atlanta, GA 30033

Re: Account #10122467894231

DearHarry Jones:

I am writing this letter to request assistance with my personal loan during a time of financial hardship.

Approximately two weeks ago, I was let go from my job due to company-wide layoffs. As a result, I have been unable to continue making regular payments on my loan. I have included my termination letterthat proves the validity of my hardship.

While I have taken steps to increase my income during this time, such as babysitting and selling old clothes, I am still not able to make full payments.

I fully intend to pay off my loan and am requesting your help to get me back on track. I would like to discuss possible solutions such as temporarily pausing payments, lowering my interest rate, or any other option that might be available to me. I expect my hardship to be resolved in approximately three to six months, after which I can resume my regular payments.

I want to reiterate my intention to fulfill my financial obligation. If you have any questions or would like to discuss a solution, please contact me at (912) 333-3333oremail me at [email protected].

Thank you for taking the time to review my request, and I hope we can come to a mutually beneficial agreement. Your support during this time of financial hardship is greatly appreciated.

Sincerely,

Mary Smith

How to Get Through Financial Hardship

In addition to writing a hardship letter, here are some other tips to help you get through times difficult times and continue to reach your financial goals:

Create a budget: Use a monthly budget template to write down your monthly income, expenses, and debt to paint a full picture of your current financial situation.

Consider debt consolidation: If you have many different debts, debt consolidation can simplify your finances and help you pay your balance quicker and at a lower interest rate.

Limit unnecessary expenses: During difficult times, it’s important to only spend money on the essentials. Consider canceling subscriptions, reducing electricity use, and eating at home to save money.

Start a side hustle: Having multiple income streams can help mitigate financial burdens. Examples of side hustles include pet sitting, driving for a ride-share company, online tutoring, and joining a focus group.

Build an emergency fund: Aim to save three to six months’ worth of expenses as a cushion in case of a personal emergency or unexpected expense.

Writing a financial hardship letter can help you maintain a good credit score during a crisis. While navigating your situation, it’s important to continue monitoring your credit. To make this easier during times of stress, check your free credit report card to see what’s happening with your credit at a glance.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

One of the best ways to grow your wealth is to take advantage of a high-yield savings account and make money from the interest. Depending on your age, the average savings in America can vary, but those who start younger can build more wealth because they have more time.

Use our free simple savings account calculator to see how your money can make money over time from interest payments.

Simple Savings Calculator

Total Savings

$

Breakdown of Savings

Starting Deposit

Total Contributions

Earned Interest

Simple Savings Account Calculator Help

The simple savings account calculator helps you easily calculate the annual percentage yield (APY) and accurately show how your investment can grow. Below, we go over each aspect of the calculator and how it works.

Starting deposit: When you open a savings account, this is your initial deposit. This first deposit plays a big role in how much your wealth will grow over time.

Monthly contribution amount: It’s beneficial to continue depositing into your savings account monthly. Adjust this amount in the savings account calculator to see how much your money can grow and benefit from compound interest.

Number of years: Giving your money time to grow is the ideal strategy due to compound interest.

Annual interest rate: Interest rates can vary depending on the bank and type of account. You can use certificates of deposit (CDs), a high-yield savings account, or money market accounts. Be sure to shop around to find the best interest rates before you decide.

How Much Should You Save Each Month?

How much you save each month is unique to your financial situation. However much you choose to deposit into your savings account, the important thing is to be consistent. One way to do this is by setting up automatic transfers from your checking to your savings each month after a payday.

You’ll also want to ensure you’re budgeting properly so you don’t fall behind on other expenses like bills or debt payments. A monthly budget template can help you create a strategy and see what amount works for you.

How Do You Calculate APY?

To calculate the simple interest amount in a savings account, multiply the account balance by the annual percentage rate. For example, if you save $10,000 in a year and have a high-yield savings account with a 4% interest rate, the calculation is:

$10,000 x 0.04 = $400

How Savings Can Improve Your Financial Well-Being

Having a savings account is not only helpful for building your wealth, but it also provides you with some security in an emergency. By finding a savings account with a high interest rate, you will make money by simply storing your savings in the account.

Improving your credit score can also help your financial well-being. A good credit score lets you benefit from lower interest fees and access to additional loans and lines of credit. If you want to know where you stand with your credit, sign up for your free credit report card. You can also utilize Credit.com’s ExtraCredit® service to get credit monitoring alerts, additional credit reporting, and more.

Helpful Links to Start Saving

Check out some of our other articles for more tips and strategies for saving and growing your wealth.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

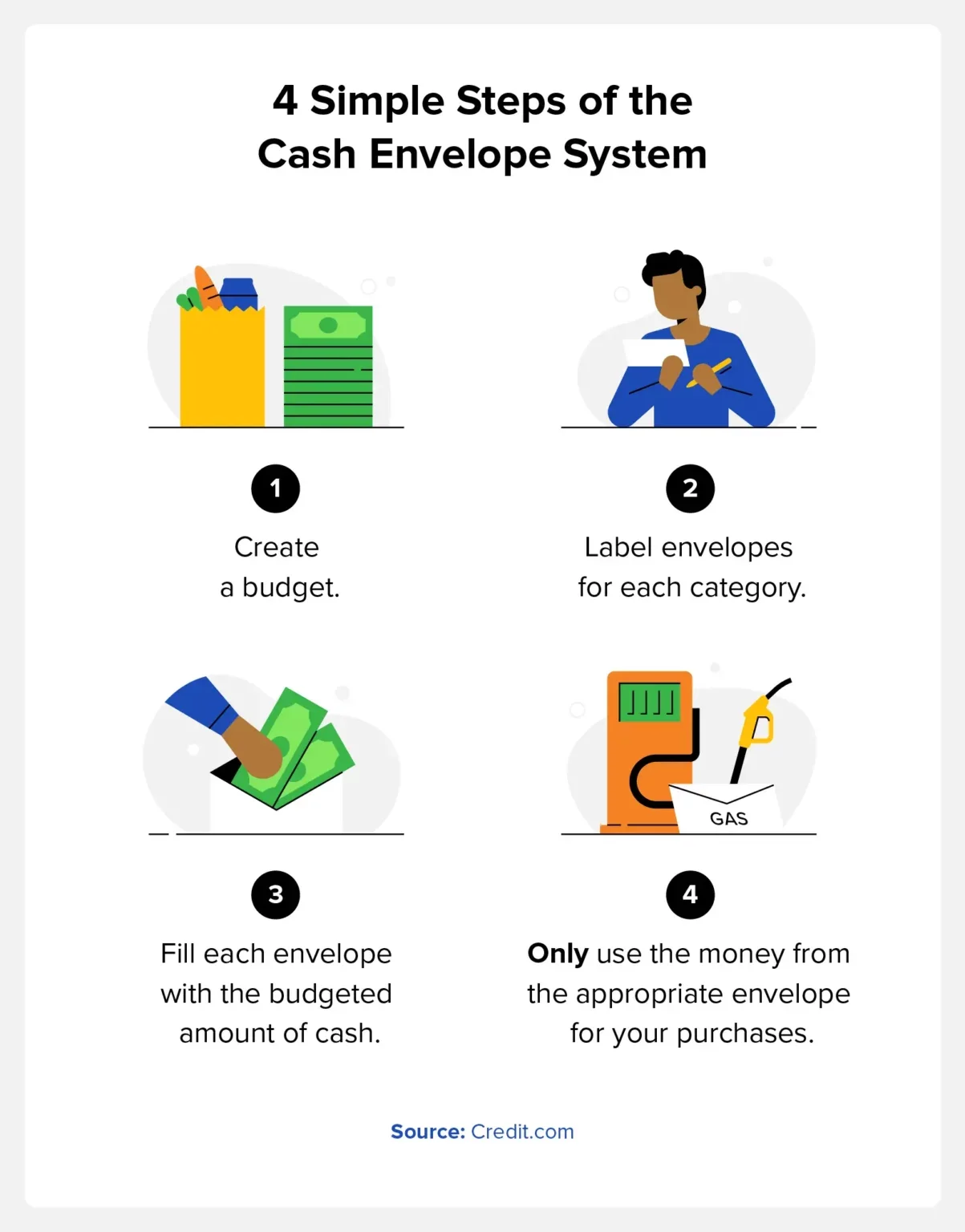

The cash envelope system is a budgeting tool that helps you develop self-discipline by only spending the allotted amount of cash from labeled envelopes each month. It can help reduce overspending and impulsive purchases.

Budgeting is one of the best ways to keep track of your spending, pay down debt, and build wealth. Unfortunately, many Americans don’t take advantage of preparing a monthly budget. Our team at Credit.com surveyed over 1,000 Americans, and 27 percent said they don’t think a budget is necessary.

We also found that 15 percent of people don’t want to feel restricted by a budget, and 24 percent simply don’t think they will stick to it. Fortunately, with the cash envelope system, it’s easy to do both.

Today, you will learn about this simple budgeting method that can help you save money, lower your debt, and potentially help raise your credit score.

Key takeaways:

You can use cash envelopes as a monthly budget by putting cash in different envelopes for spending categories.

The system is ideal for people who have a habit of impulsive spending or overspending.

It allows you to monitor your money rather than guessing how much you’re spending.

The cash envelope system is often called “cash stuffing” on social media apps like TikTok.

What Is the Cash Envelope System?

The cash envelope system, also known as “cash stuffing,” is an easy-to-use budgeting tool that helps track how much money you have to spend. You’ll put the cash in labeled envelopes and check each envelope throughout the budgeting period to see how much money you have left to spend.

Different budgeting systems work for different people. For some, having a monthly budget template on their computer is the best option. Others may benefit more from being able to physically see how much money they have left for purchases like groceries, gas, and entertainment.

How the Cash Envelope System Works

Before cash stuffing, you will need to organize your money envelopes into different categories. If it helps, you can start with a spreadsheet budget template, or you can write down the categories in a notebook. Some of the top budget categories to consider include:

Utilities

Fuel or transportation costs

Groceries

Healthcare and medications

Savings

Debt

It’s also beneficial to ensure you have cash envelopes for areas where you typically overspend. This may be eating out, buying clothes, or online shopping. You can allocate money toward these areas, but the goal is to ensure you don’t overspend.

During the month, whenever you spend money in one of these categories, you only use the money from the appropriate envelope. For example, if you enjoy buying a $5 cup of coffee on your way to work and allocate $100 to that envelope, take $5 out of it each morning.

The cash envelope system is a way to hold yourself accountable for your spending. This means that once the money is gone from an envelope, it’s gone. If you miscalculated how much you need in a certain category, revisit your budget the following month and tweak the amounts.

You can refill your envelopes at the start of each budgeting period or after each paycheck.

The Benefits of the Cash Envelope System

There are pros and cons that come along with every budgeting strategy, so it’s helpful to know the benefits and drawbacks and find the one that’s right for you. The cash-stuffing envelope system is great for people who don’t check their bank account daily or are better with their money when using cash.

Additional benefits include:

Avoiding overdraft fees

Minimizing overspending

Increasing accountability

Helping with disciplined spending

By sticking to cash, the system also helps reduce the frequency with which you use your credit card, minimizing interest fees.

The Downsides of the Cash Envelope System

The cash envelope system isn’t for everyone, and it may create some additional challenges. The primary downside of this budgeting system is that you need to go to your bank or an ATM whenever you need to refill your envelopes. It’s also beneficial to consider that carrying large amounts of cash has the risk of losing it for the money being stolen.

Some of the other downsides include:

It’s time-consuming.

You get no credit card rewards.

You can only spend the amount contained within each envelope.

The other challenge with the cash envelope system is making online payments or automatic payments. Automatic payments are a great way to avoid forgetting about a payment and accruing late fees. You can still use the cash envelope system, but you will need to keep track by writing on the back of the envelope, similar to balancing a checkbook.

Should You Use the Cash Envelope System?

This budgeting system is ideal for people who are quick to pull out their debit or credit card and have trouble with overspending. It can be difficult to track your money electronically, but using physical cash can help many people stick with a budget.

The system is also a great way to budget for beginners. It’s a simple system, and you can start with just a few categories. If you know you have a problem with overspending on ordering food or going out, use this system to allocate a specific amount of cash for these activities.

FAQ

Although the cash stuffing system is a simple method, there are some common questions people have when getting started.

Can the Cash Envelope System Work If You Make Online Payments?

The most common method is to create a physical envelope while keeping the money in your bank account for online payments. You can keep track by writing on the back of the envelope each month.

What If an Envelope Runs Out of Cash?

If you run out of cash from the envelope, stay disciplined and avoid borrowing money from other envelopes. Revisit your budget and find ways to save in different categories, earn extra money, or reduce your spending.

How Do You Use the System When Emergency Expenses Happen?

Emergencies happen, and in these cases, you can shift money around from your envelopes and budget accordingly the following month. It’s also helpful to build an emergency fund for these situations, and you can also keep a credit card for emergency funds.

What Do You Do If There’s Money Left Over in Your Cash Envelope?

Money left over in cash envelopes means you’re doing a great job with your budget. You can use this to treat yourself or add to your personal spending money envelope the next month. You may also want to use this extra money to make extra debt payments or put it in your savings account.

How the Cash Envelope Budget System Can Help Improve Your Credit

Creating a budget is a great way to get your finances under control and create quality spending habits. The cash envelope system is also helpful for reducing your debt and improving your credit. One of the key factors of your credit score is credit utilization, so allocating an envelope toward paying down your debt and using leftover money for additional payments can help increase your score.

For additional credit resources, you can sign up for Credit.com’s free credit report card or our ExtraCredit service.

Inside: Are you looking for an affordable budgeting app that offers a range of features? YNAB may be the perfect choice for you! This guide will compare YNAB vs Mint, highlight their key features, and help you decide which is best for your needs.

Are you trying to make a choice between Mint and YNAB for managing your financials?

Here’s a comprehensive overview that would definitely point you in the right direction.

Both Mint and YNAB have proven to be efficient and reliable online budgeting tools, but their offering varies in some aspects.

While Mint shines with its free budgeting tools and comprehensive credit score and report management capabilities, YNAB stands distinguished with its robust features and specialist credit management options, making it worth its fee for some users.

Herein, we dive into the similarities, differences, and unique functionalities of both platforms to help you decide which one best aligns with your financial management needs and lifestyle.

As a finance expert, I’ve seen both YNAB and Mint apps work wonders for different people.

In my opinion, both have unique value. Novices may find Mint’s overview helpful, while more determined budgeters might prefer YNAB.

Remember, it’s perfectly fine to use both if it aids your long-term money management.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What is YNAB?

YNAB is a budgeting software I’ve utilized that provides detailed financial tracking and education for effective money management. Also, known as you need a budget app.

Adhering to its unique Four Simple Rules for Successful Budgeting, every dollar is assigned a specific task. YNAB operates via an online account or a mobile app, involving color codes and features like ‘The Inspector’ for efficient budget overview. However, it’s important to note that YNAB caters only to the zero budgeting style and charges a monthly subscription fee.

This is a great budgeting method as it gives you a cash flow budget plan for your money.

Overall, YNAB helped me gain control over my finances by setting realistic goals, getting one month ahead on bills, and focusing on each dollar’s purpose.

What is Mint?

Mint is a free, all-in-one finance platform owned by Intuit that can be used to easily manage my money.

It links all accounts in one place for easy tracking and includes features such as budgeting, credit score monitoring, and bill tracking.

For instance, Mint categorizes transactions, monitors changes in my credit score, and sets up budgetary limits.

With over 30 million users, Mint is a leading free tool in personal finance management.

A step up from Mint would be Intuit’s Quicken platform or Simplifi budget app.

Comparison of YNAB and Mint Apps

Mint is a comprehensive, free budgeting app, that provides an overall view of your finances. It links to your accounts, tracking and categorizing spending, while also offering savings tips. Conversely, YNAB, a paid app, focuses on giving users control over budgeting. It will link to your accounts and encourage a proactive role in handling finances.

These are two of the budget apps available on the market.

In my opinion, if you’re seeking an easy-to-use app offering a holistic view of your spending and savings, Mint is a perfect choice. However, if you’re looking for a stringent budget management system with more control, YNAB is worth the investment.

Kristy @ Money BLiss

1. YNAB vs Mint: Features

YNAB and Mint are both renowned budgeting apps, but they possess some notable differences.

While both support account linking, goal setting, and spending tracking, Mint pulls ahead with its investment and credit score tracking features.

YNAB distinguishes itself with a forward-thinking, zero-based budgeting strategy and benefits like manually adding transactions. Think budget by paycheck style.

From the ease of use standpoint, both are equally user-friendly.

2. YNAB vs Mint: Budgeting Snapshot

YNAB offers a rigorous, manually updated budgeting snapshot that employs a zero-based budgeting philosophy. This feature provides a detailed outlook, encouraging users to assign every dollar a job.

On the other hand, Mint has an automated tracking system that offers an all-in-one snapshot of all financial accounts and spending categories.

Mint integrates your accounts, offering useful tips and an overview of your finances. Conversely, YNAB requires a manual categorization of income and expenses but affords more budgeting control. Similar to using the ideal household budget percentages.

The budgeting snapshot in Mint is best suitable for individuals seeking a hands-off approach, while YNAB is ideal for those who prefer an in-depth, hands-on budget strategy.

A great way to move digital from your budget binder with envelopes.

3. YNAB vs Mint: Goal Setting

The Goal Tracking feature in YNAB allows users to set various budgeting goals such as saving targeted amounts of money or conversely working towards getting out of credit card debt. This in-built functionality provides a structured pathway for users to stick to and pursue their financial objectives effectively.

Your interaction with your YNAB account through the goal-tracking tool ties back to YNAB’s four Simple Rules for Successful Budgeting, aiding in fiscal responsibility.

This innovative feature assists individuals in staying focused on their planned budgets, ensuring they are empowered to make strides toward their unique financial goals.

Mint however doesn’t offer this feature.

4. YNAB vs Mint: Interface

While YNAB is ideal for meticulous budgeters prioritizing forward planning, Mint is perfect for those seeking an easy-to-use, comprehensive glimpse of their financial standing.

YNAB’s interface is focused on budgeting, featuring tools for expense tracking, goal setting, and manual transaction input.

In contrast, Mint offers a comprehensive overview of your financial health, automatically categorizing expenses, tracking investments, and offering set-up alerts.

5. YNAB vs Mint: Categorization

Mint offers automated categorization of transactions, which eases the process of budgeting for the user. However, it doesn’t allow the removal of default categories, and the addition of new ones might take time due to server communication.

On the other hand, YNAB allows a deeper level of categorization, with an option to visually nest categories, and more effortless editing of these categories.

In my opinion, Mint’s categorization feature suits a casual budgeter looking for automation, while YNAB would be ideal for those desiring granular control over their personal budget categories.

6. YNAB vs Mint: Mobile App & Cross Platforms

Both YNAB and Mint offer comprehensive personal finance management via mobile apps, compatible with iOS, Android, and desktops.

YNAB stands out with its Apple Watch integrations and a slightly better syncing experience based on user reviews on Trustpilot1.

YNAB also syncs across a desktop app as well.

7. YNAB vs Mint: Alerts

Mint provides a wide selection of alerts, including low balances, upcoming bill payments, over-budget warnings, ATM fees, and unusual expenditure notifications.

These comprehensive alerts from Mint give a more thorough financial pulse check but can be overwhelming for some.

On the other hand, YNAB recently added live push notifications based on your preferences.

8. YNAB vs Mint: Syncing

YNAB leads the game when it comes to synchronization, outshining Mint. While Mint supports numerous banks, issues with synchronization often lead to grievances among its users. YNAB, on the other hand, offers smoother syncing and fewer complaints, proving its superiority.

Many users find YNAB’s syncing consistent and reliable.

Personally, I believe that if you prioritize seamless syncing and don’t mind spending $14.99 a month, YNAB becomes a clear choice.

However, if you’re okay with potential sync issues and prefer free usage, Mint could be more suitable.

It’s crucial to pick according to your priorities and needs.

9. YNAB vs Mint: Savings Accounts

Mint offers automatic expenditure tracking and classifies my spending into categories, providing a comprehensive view of where my money is going.

YNAB, on the other hand, empowers me to manually budget my net income each month, ensuring I don’t overspend and promoting a proactive approach to saving.

10. YNAB vs Mint: Investment Tracker

Mint offers investment tracking features, allowing users to view their investment portfolio and monitor performance.

In contrast, YNAB lacks this feature, not providing any investment tracking at all.

As a user, if you highly prioritize tracking investments in one place, you may lean towards using Mint. Conversely, if investment tracking is less important to you than budgeting, YNAB’s strong budgeting emphasis, despite its lack of investment tracking, makes it a considerable option.

11. YNAB vs Mint: Learning Curve with your Finances

YNAB has a steeper learning curve, necessitating a proactive approach to money management by assigning every dollar a purpose. Thus, YNAB gives you a free 34-day free trial to understand how to use the app.

Mint, however, requires minimal user input post-account linkage and auto-categorizes your spending. For sheer ease of use, Mint might appeal to novices looking for automated budget tracking.

On the other hand, users wishing to take charge of their finances might appreciate YNAB’s proactive, behavior-altering approach. Despite having a steeper learning curve, YNAB offers an abundance of online tutorials and customer support, making the learning process manageable and rewarding.

The same is true when you are learning to use the biweekly budget template.

12. YNAB vs. Mint: Data Security

Data security is a paramount concern when utilizing online budgeting apps as they deal with sensitive financial information.

Apps like YNAB and Mint incorporate stringent security measures to protect user data.

For instance, YNAB uses a one-way salted and hashed password system and data encryption.

Mint, on the other hand, employs two-factor authentication and a Touch ID sensor for iOS for enhanced security.

Nonetheless, it’s important to note that while these apps provide bank-level security, Mint does anonymize and sell user data to advertisers.

13. YNAB vs Mint: Advertising

YNAB derives income primarily from subscription fees offering an ad-free experience, holding a straightforward revenue model. In contrast, Mint generates income through affiliate commissions by advertising financial products to users and selling anonymized user data!

Mint, contrastingly, is a free app reliant on ads and sells anonymized user data for third-party advertisements.

From my perspective, if avoiding ads and preserving data privacy matters to you, YNAB’s approach might be more appealing. However, if you prefer a free service and don’t mind the ads, Mint would be suitable.

14. YNAB vs Mint: Customer Support

When evaluating the customer support of Mint and YNAB, it’s evident that YNAB takes a more well-rounded approach.

With a commitment to respond to email queries within 24 hours, YNAB also provides educational resources such as the “get started” class, their blog, and user forums. This is in contrast to Mint, which, despite offering live chat support, has had reports of slow response times.

Both platforms offer online training materials, but YNAB seems more comprehensive and responsive in its support-providing role. Overall, YNAB appears to be the preferred choice when customer support is a primary consideration.

15. YNAB vs Mint: Cost

Mint is a free, ad-supported budgeting app while YNAB is a subscription-based model of $14.99 monthly or $99 annually.

However, for individuals seeking in-depth surgical budgeting capabilities without concerns for associated costs, YNAB’s price might represent a great investment.

Given the claimed average user saves $600 in two months and $6,000 in the first year.2

For those budgeting with minimal funds, the free price tag of Mint might be more attractive, but you are giving away your privacy.

Pros and Cons of YNAB vs Mint

Our Favorite

Key Features:

YNAB offers a comprehensive approach to budgeting, helping you plan monthly budgets based on your income. It also offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

YNAB’s superior synchronization skills make it the winner in this area. YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners

YNAB provides an option to manually add and upload transactions from accounts each month, a feature that Mint does not offer.

YNAB prioritizes user privacy, requires an opt-in to access budgeting data, and doesn’t sell user data.

Key Features:

Mint offers a centralized platform for monitoring all your financial accounts, including credit cards and bank accounts.

It provides a complete financial overview at a glance through the auto-population of data from linked accounts.

Mint’s features include detailed reporting in multiple categories, free credit score access, and exceptional compatibility with financial institutions.

The service is free, funded by ads and offers, and it best serves those who wish to categorize spending, budget their monthly expenses, and access all financial details from one place.

Lack of investment tracking feature

Customer service is only accessible via email, which might not be ideal for urgent queries

Steep learning curve which requires time and effort to navigate through.

Mint, which belongs to Intuit, automatically accesses all data and sells the data. Thus, an intrusion of privacy.

Budgeting feature doesn’t enable effective planning of future expenses.

Mint suffers from more technical glitches and synchronization issues.

Ads included in the free version of Mint can be obtrusive and may deter users.

$14.99 monthly or $99 annually

Free to Use, But Served Ads and They Sell your Data.

Offers a 100% money-back guarantee at any point of use.

Does not require credit card information to signup, a departure from the usual free trial model)

Our Favorite

Key Features:

YNAB offers a comprehensive approach to budgeting, helping you plan monthly budgets based on your income. It also offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

YNAB’s superior synchronization skills make it the winner in this area. YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners

YNAB provides an option to manually add and upload transactions from accounts each month, a feature that Mint does not offer.

YNAB prioritizes user privacy, requires an opt-in to access budgeting data, and doesn’t sell user data.

Lack of investment tracking feature

Customer service is only accessible via email, which might not be ideal for urgent queries

Steep learning curve which requires time and effort to navigate through.

$14.99 monthly or $99 annually

Offers a 100% money-back guarantee at any point of use.

Does not require credit card information to signup, a departure from the usual free trial model)

Key Features:

Mint offers a centralized platform for monitoring all your financial accounts, including credit cards and bank accounts.

It provides a complete financial overview at a glance through the auto-population of data from linked accounts.

Mint’s features include detailed reporting in multiple categories, free credit score access, and exceptional compatibility with financial institutions.

The service is free, funded by ads and offers, and it best serves those who wish to categorize spending, budget their monthly expenses, and access all financial details from one place.

Mint, which belongs to Intuit, automatically accesses all data and sells the data. Thus, an intrusion of privacy.

Budgeting feature doesn’t enable effective planning of future expenses.

Mint suffers from more technical glitches and synchronization issues.

Ads included in the free version of Mint can be obtrusive and may deter users.

Free to Use, But Served Ads and They Sell your Data.

Who should use YNAB?

From my experience, YNAB works best for those who are ready to seriously manage their money and spend some time learning a new budgeting approach. Its use of the zero-based budgeting system not only makes you more intentional with your money but also demands active participation in decision-making.

YNAB’s ability to link to your accounts and its multitude of educational resources available are admirable features I’ve used.

YNAB offers detailed financial tracking and built-in education, but its monthly subscription fee and suitability for a specific budgeting style may be limiting for some.

However, it comes with a monthly or annual cost – a worthy investment for those searching for a robust, hands-on, and future-focused budgeting tool. Most YNAB budgets agree they save multiples of the subscription cost.

However, it can be less suitable for those not ready for a hands-on approach or those sensitive to subscription pricing.

Who should use Mint?

On the other hand, Mint is an all-in-one app that automatically tracks and categorizes your spending.

Based on my experience, Mint is an excellent tool for novice-level budgeters seeking to track their expenses, set budgets, and manage their finances with ease. This budgeting app allows a comprehensive view of all your financial accounts, which differentiates it from YNAB.

If you’re comfortable seeing ads and not needing investing features, Mint could be a perfect fit. However, if you require the ability to assign multiple savings goals to one account or a bill pay feature, YNAB may be more suitable for you.

Therefore, Mint is most applicable for beginners seeking a free and user-friendly budgeting platform.

YNAB vs. Mint: Which is better for you?

As a content writer and budgeting app user, I find Mint and YNAB are unique in their offerings.

Mint automatically tracks and categorizes your spending, providing an intuitive picture of where your money goes, ideal for beginners in budgeting.

In contrast, YNAB promotes a proactive approach, helping to set and monitor budgets, hence perfect for those with specific financial goals. To sum up, Mint offers a simplified, passive overview, while YNAB is excellent for a detailed, forward-thinking approach to managing finances.

Personal preferences and needs really influence the choice here. Do you need intricate control and don’t mind paying a fee? YNAB might be your fit. Prefer automation and want a free option? Mint could work for you.

YNAB vs Mint: Verdict

As an expert in personal finance tools, I’ve explored both YNAB and Mint.

In my experience, there are distinct differences between YNAB and Mint. For my readers, I recommend YNAB.

YNAB, with its laser-focused approach towards budgeting, is a boon for individuals needing extensive assistance in the budgeting arena. You learn to assign every dollar with intention, thereby gaining a higher degree of control over your finances.

This proactive approach will help you to be financially independent faster.

To sum up, if detailed budgeting is your priority, choose YNAB.

YNAB

Enjoy guilt-free spending and effortless saving with a friendly, flexible method for managing your finances.

Pros:

Comprehensive approach to budgeting, helping you plan monthly budgets based on your income.

Offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

Superior synchronization skills make it the winner in this area.

YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners.

Option to manually add and upload transactions from accounts each month.

YNAB prioritizes user privacy.

Start 34 Day Free Trial

However, for a more holistic financial insight with less emphasis on budgeting, Mint might be the better choice.

Now, make sure to check out our Quicken Review.

Source

TrustPilot. “YNAB Review.” https://www.trustpilot.com/review/ynab.com. Accessed on September 27, 2023.

YNAB. “YNAB Pricing.” https://www.ynab.com/pricing/. Accessed on September 27, 2023.

Know someone else that needs this, too? Then, please share!!

Inside: Looking to celebrate Christmas on a budget? This guide has you covered with creative and affordable ways to do just that.

Are you stressed out about how to afford a fabulous Christmas on your budget? Worry not.

This festive season isn’t about how much cash you fork out, it’s about creating lasting memories and spreading joy.

Why let financial woes dampen the joyous yuletide spirit when you can celebrate a charming Christmas on a budget?

Remember, it’s your money, your decisions, and your rules – no guilt trips or social pressures should force you into spending Christmas in debt.

Today you will learn:

Determine your Christmas budget: Figure out what’s a comfortable amount for you to spend and stick to it religiously.

Be creative with gift giving: Homemade presents or heartfelt letters can be more valuable than pricey items.

Find simple ways to save money: Use these money saving tips to enjoy a festive holiday season.

This holiday season, celebrate responsibly, within your means, for a Christmas that’s merry, bright, and totally guilt-free!

Why Celebrate Christmas on a Budget?

Embracing a budget-friendly Christmas can prove to be not only a smart choice but one filled with warmth, delight, and genuine joy.

Enjoy valuable family bonding time with exciting games and shared activities. Volunteer work, a day of holiday baking, or a simple drive-through Christmas lights sightseeing trip can leave a lasting impression. Look through this Christmas bucket list.

Opt for economical, yet thoughtful gifts or stick to fun gift exchange rules, such as the “four gift rule” for your kids. Remember, it’s the sentiment behind the gift that matters the most.

In essence, an economical holiday season needn’t be a dull affair, rather it’s an opportunity to make it more heartfelt and unforgettable.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What to buy for Christmas on a tight budget?

Yes, friend, you can buy meaningful Christmas gifts while sticking to a budget.

In fact, the thought behind a gift is often what makes it special, not the price tag.

A few ideas include homemade gifts, gift cards, subscriptions, and second-hand items. With a little creativity, you can find the perfect present for everyone on your list without spending a fortune.

Below you will find plenty of great gift guides for Christmas that won’t break the bank.

Benefits of a Budget Christmas

1. Allows you to plan ahead and stay on track 2. Prevents overspending 3. Buy gifts that are within your budget 4. Focus on quality over quantity 5. Ensures that everyone gets a gift 6. Helps you avoid debt during the holidays 7. Prevents you from feeling stressed out about money during the holidays 8. Be creative and come up with unique gifts 9. Save for next year’s holiday budget 10. Stay connected to the spirit of the holidays

Savings with Christmas on a Budget

From homemade Christmas decorations to unique gift ideas, it’s possible to create magical moments that’ll last a lifetime without a hefty price tag.

Embrace the true spirit of Christmas – love, family, and togetherness, rather than commercialism, and read on to discover how.

Learn the simple ways to celebrate the festive season without breaking the bank with our creative and budget-friendly Christmas ideas.

1. Think about a No Gift Christmas

Having a No Gift Christmas is a creative and budget-saving alternative to traditional holiday festivities, especially suitable if funds are tight. Why not consider it?

Here are some benefits:

You can alleviate the holiday stress often associated with spending on gifts.

It fosters the idea of Christmas as a season of togetherness, not just gift-giving.

It offers the potential for unique and memorable experiences, like volunteering or creating fun traditions with your loved ones.

Remember, having a memorable Christmas doesn’t have to cost much, or anything at all Learn more about a no gift Christmas.

2. Make Your Own Gifts

DIY Christmas gifts are your perfect solution. They not only save pennies but are laced with your love and creativity.

Start by exploring plenty of creative gift ideas available for free online. Need help? Look for “homemade gifts for Christmas” and you’ll be surprised.

Compile a list of possible gifts from homemade candles to personalized coupon books, keeping the recipient’s likes in mind.

Remember, your efforts will reflect in your gift. So, unleash your creativity and let the magic begin.

3. Borrow Instead of Buy

Borrowing instead of buying is a clever way to have a festive holiday while keeping things budget-friendly. This concept is simple: swap decorations, games, or even gifts with friends, neighbors, or family

Discuss your idea with your circle and organize swapping parties to exchange items.

The key is to creatively engage and make it a fun, budget-conscious activity. After all, Christmas is about sharing and caring!

Remember, return borrowed items in their original condition to maintain trust.

4. Attend Free Events

The Christmas season doesn’t have to be a strain on your wallet. Attending free community events can provide fun and festive celebrations:

To find these events, check your local newspaper or community websites. Be sure to:

Take advantage of free refreshments, but also bring your own to share.

Consider hosting a potluck dinner before or after community events.

Attending free events supports your local community.

Remember, Christmas is about togetherness, not extravagant spending.

5. Make Your Own Decorations

To create a festive atmosphere this season, you could repurpose items around your house or make your own decorations.

Choose a color theme and gather items in those shades, then place them together on a mantel or coffee table to create a coordinated layout.

For a natural touch, clip pine needles, branches, or herbs from your garden, and enhance them with glitter.

Additional budget-friendly options include taking advantage of sales and discounts at thrift stores or crafting handmade decorations such as ribbons from fabric strips or Christmas cookie ornaments.

6. Keep Track of Your Christmas Expenses

Just like throughout the year, budgeting is critical to your financial success.

Nothing changes with Christmas, it is crucial to track and budget your holiday expenses. Jot down every potential cost – from the Christmas tree, and food, to holiday décor.

Be thoughtful about what you really need and opt for items you can use for years.

This is one of the cash envelope categories I recommend saving for. To effectively manage your expenses, assign specific dollar amounts to each item on the list, ensuring you stay within your budget.

Enjoy guilt-free spending and effortless saving with a friendly, flexible method for managing your finances.

Start Your Free Trial.

7. Share the Spirit

Embracing frugality during the holiday season can not only help you save money, but can also create memorable experiences and meaningful connections.

Small gestures, such as sending heartwarming physical letters to loved ones instead of emails, can still convey thoughtfulness and spur the holiday spirit.

By centering your holidays around family activities and endeavors, like homemade ornaments or a scavenger hunt with small gifts, the focus shifts from materialism to fellowship and unity.

Find more frugal Christmas ideas.

8. Check Out Bargain Stores

Bargain stores provide the perfect solution for savvy holiday shoppers looking to save money without compromising on quality or variety. Not only can you find unique, quirky gifts, but you can also keep a lid on your spending while doing so.

Stores like consignment shops or websites such as Craigslist often have high-quality used toys that are nearly new if you’re willing to look carefully.

Another option is to look at discount retailers like TJMaxx as they often host sales during the holiday season, making it even easier for you to save money while hunting for the perfect gifts.

9. Save Money Throughout the Year

Automating your savings for the Christmas season can be a practical and efficient strategy. The 100 envelope challenge is perfect for this!

By setting aside just $50 each month, you could accumulate up to $600 by December, providing a decent budget for your holiday expenses. This method can ease the financial stress during the holiday season, letting you enjoy the festivities without worrying about overspending.

Consider setting up automatic transfers to a high-interest savings account. This ensures your Christmas funds grow without your intervention.

Lastly, try a no-spend month where you only cover essential bills, giving your savings a significant boost.

10. Start a Side Hustle for More Money to Spend

Engaging in side hustles throughout the year can help you significantly cover your holiday expenses.

By delivering food, completing microtasks, selling gently used items, or shoveling snow, you create extra earnings that can go directly into your Christmas fund.

For instance, extra income from a seasonal retail job could help finance gift-purchasing without straining your usual budget.

This strategy not only prevents potential post-holiday debt but also allows you to enjoy the season without financial stress.

In fact, more people are interested in how to make money online for beginners.

This is the perfect side hustle if you don’t have much time, experience, or money.

Many earn over $10,000 in a year selling printables on Etsy. Learn how to get started by watching this free workshop.

If you’ve ever wanted to make a full-time income while working from home, you’re in the right place!

This intensive training combines thousands of hours of research, years of experience in growing a virtual assistant business, and the power of a coach who has helped thousands of students launch and grow their own business from scratch.

11. Shop Online Instead of Going to the Mall

Shopping online for your Christmas gifts can seriously ease your holiday stress, and potentially save you money.

Let’s explore why skipping the mall and clicking your way to a merry Christmas might be your best bet this year:

No dealing with holiday crowds or cranky shoppers.

Enjoy sales and deals without leaving your home.

Track prices over time to grab the best deals.

Use Rakuten to save even more money on purchases.

For smart online shopping, prepare a list of gifts before diving in. Take advantage of the “wish list” option on platforms to curate items of choice and make sure you first glance over deal sites before making purchases.

12. Have a Christmas Potluck

Host a festive potluck! Invite friends and family, asking each to bring their favorite dish.

Here are some tips for a successful event:

Get organized and ask guests to bring specific types of food. This prevents duplicate dishes and ensures a balanced meal.

Introduce a fun element. Try a cookie swap or a silly game like “Guess the Cookie.”

Keep decor simple. A large vase filled with greenery and baubles can effectively replace a pricey Christmas tree.

Remember simplicity is key in food and decor. Costly ingredients and complicated recipes aren’t prerequisites for a memorable Christmas.

Remember, the holiday is about togetherness, not extravagance!

13. Make Your Own Cookies

There’s a unique pleasure derived from making your own cookies during the holiday season instead of buying them. More so, the cookies you’ve invested your time and creativity into can double as thoughtful, homemade gifts, adding another level of sentiment.

Apart from being a cost-effective option, it brings an opportunity to bond with friends and family during cookie exchange or decorating gatherings.

Making your personally crafted cookies also gives you control over ingredients catering to specific dietary needs or preference

Indeed, making your own cookies adds value that surpasses the mere cost savings, it infuses the holiday season with warmth, joy, and a sense of shared experience.

14. Cross Off Activities from your Christmas Bucket List

Having a joyful Christmas doesn’t necessarily mean overspending. In fact, integrating cost-effective activities into your holiday routine can make the season more meaningful and fun.

This Christmas Bucket list post offers an extensive and diverse list of creative ideas for budget-friendly Christmas shopping, gifting, and celebrating.

Additionally, downloading the free printables and a Christmas Budget Template will make the process even more manageable and fun.

15. Have a No-Gift Party

A no-gift Christmas party is an affordable and fun holiday celebration where attendees do not exchange gifts. It’s a great option for those looking to save money and still enjoy the festive season.

Here are steps to make it happen:

Step 1: Decide on the party type, either a simple gathering or a potluck dinner.

Step 2: Inform guests about the no-gift policy in advance.

Step 3: Organize exciting, cost-effective activities such as a game night.

Step 4: Engage guests with games for a joyful event.

Expert Tip: Conversation and laughter are your best tools.

16. Make a Christmas Memory Book

Creating a Christmas memory book is an affordable and engaging way to celebrate the holiday season, especially when you’re on a tight budget.

To start, you can utilize items already at your disposal in your house such as old photos, greeting cards, and crafts.

Spend some time penning down heartfelt messages and your favorite holiday memories associated with each picture or craft. Embellish the pages with affordable decorating materials like glitter, stickers, or color pens.

Not only does this create a personalized touch, but it also serves as a nostalgic keepsake that can be cherished for years to come.

Tip: Digitize your memory book by creating an electronic version. This can also help preserve the original items.

17. Spend Time With Loved Ones

Celebrating Christmas on a budget doesn’t mean skipping on the fun.

It’s about cherishing time spent with loved ones, harnessing creativity, and making priceless memories that last a lifetime.

Here are some cost-effective activities you can embrace this festive season:

Share stories of memorable Christmas experiences.

Organize virtual celebrations with extended family and friends.

Create your own family-themed board game.

Bake Christmas cookies or make a popcorn Christmas tree.

Stream a Christmas church service.

If snow is around, engage in snow play.

Dance to classic Christmas music.

Put together an annual family calendar.

Participate in one of these Christmas Challenges!

Remember, it’s not about what’s under the tree that matters, but rather, who’s around it.

18. Stash Christmas presents all year

Do what I do! Begin addressing the issue of holiday budgeting by stashing Christmas presents all year round.

This is a smart and stress-reducing move!

Find deals throughout the year rather than spending lavishly in December. Hang on to items like discounted gifts in your secret gift closet!

As you build an inventory of diverse items, you will be ready for birthdays or sudden party invites – you’re always prepared!

Just be careful to stop shopping when your list is fulfilled to avoid overspending.

19. Write a Christmas Gift List

Creating a Christmas gift list can be an effective way to manage your holiday spending. This helps you understand the overall picture of your holiday expenditure.

Start by writing down the names of every person for whom you consider buying a gift.