HOUSTON, April 4, 2024 /PRNewswire/ — Cornerstone Home Lending, a division of Cornerstone Capital Bank (“Cornerstone”) and a leading provider of home financing solutions, proudly announces the appointment of Michael A. Iorio as Senior Vice President of Strategic Partnerships. In his new role, Mike will spearhead the expansion of Cornerstone’s Homebuilder Partnership business across targeted builder accounts nationwide, with a focus on cultivating new relationships and enhancing service offerings.

Mike brings to Cornerstone over 25 years of industry expertise, particularly in the areas of ABA partnerships. Prior to joining Cornerstone, Mike served in various leadership capacities, where he oversaw sales initiatives and optimized business relationships for numerous ABA/JV entities, while also contributing to the board of directors for many of those organizations.

Mike’s academic background includes a Bachelor of Business Administration from the University of Notre Dame and an MBA from Northwestern’s Kellogg Graduate School of Management.

“We are thrilled to welcome Mike to the Cornerstone family,” said Adam Laird, CEO of Cornerstone Home Lending. “His proven track record of success and deep industry knowledge will be invaluable as we continue to expand our homebuilder platforms and create new opportunities for both Cornerstone and our dedicated team members.”

About Cornerstone:

Created by Cornerstone Home Lending’s acquisition of and merger with The Roscoe State Bank, Houston-based Cornerstone Capital Bank (“Cornerstone”) has a combined operating history dating back to 1906, with mortgage banking, mortgage loan servicing, commercial banking, and institutional banking divisions. Its nationally recognized residential mortgage lending team, which continues to operate as Cornerstone Home Lending, has assisted families with more than 500,000 home financing loans since its inception in 1988. In addition to residential mortgage lending, Cornerstone Home Lending provides full-service, in-house mortgage loan servicing operations under the name Cornerstone Servicing, which combines a superior record of customer care with top-tier technologies. Cornerstone’s 1,500 team members across the country are guided by a core Mission, Vision, and Convictions statement. Visit www.houseloan.com, www.cornerstonecapital.com, www.rsb.bank and www.cornerstoneservicing.com to learn more.

The IRS says it heard the objections raised by small-business lenders to its plan to block access to loan applicants’ income and other tax-related data. “We … are assessing our ability to provide return information when necessary while keeping taxpayer information confidential and protected from disclosure,” the agency says.

Al Drago/Bloomberg

For banks, credit unions and other small-business lenders, this is an IRS-related story with a happy ending — kind of.

Responding to a determined lobbying campaign by a broad consortium of financial services trade groups, the U.S. tax-collection agency has agreed to suspend a policy change that would have blocked small-business lenders from accessing borrowers’ income data through its Income Verification Express Service.

“We acknowledge the concerns raised and are assessing our ability to provide return information when necessary while keeping taxpayer information confidential and protected from disclosure,” the IRS wrote in a March 6 policy update statement. “Although IRS announced the policy change on January 2, 2024, we are suspending that change as we seek input from you and other stakeholders on possible changes and impacts to the program.”

Scott Stewart, CEO of the Innovative Lending Platform Association, acknowledged that the IRS could revert to its original policy stance after its review. At the same time, even a temporary respite represents a major achievement, Stewart said.

“Federal agencies don’t do this,” Stewart said in an interview. “To get a federal agency of any kind, let alone the IRS, [to acknowledge a misstep] is really exceptionally rare. I don’t know if I’ve ever seen a reversal like this. The IRS deserves credit for realizing this policy requires further review.”

The Innovative Lending Platform Association was one of 11 financial services industry trade groups, including the Independent Community Bankers of America, American Bankers Association, America’s Credit Unions and the Mortgage Bankers Association, that endorsed a Jan. 24 comment letter opposing the IVES policy change. IVES is the platform that lets taxpayers give third parties — like lenders — permission to see tax return or wage information.

Under the IRS’ original concept, it would have delivered tax data only to lenders making mortgages. In all other instances, the agency would have delivered the data directly to individual taxpayers to protect their privacy.

Lenders value the ability to obtain tax returns from the IRS as a critical tool in underwriting and preventing fraud. They were concerned the policy change would add complexity, time and cost to applications while at the same time making it easier for bad actors to game the system.

“You could see how fraudsters might just digitally alter their tax returns and they could send it off to the lender,” Stewart said. “I hope they’re going to move toward [opening] the system in an [application programming interface] fashion so that everyone can get access and overall lower the cost of credit and capital for small businesses, consumers, people looking for insurance — everybody.”

An application programming interface, or API, is software code that allows a website, application or program to more easily share information with other websites, applications or programs.

In their announcement last week, IRS officials “said they were suspending the decision indefinitely,” Ryan Metcalf, head of public affairs for Funding Circle US, said in an interview. “I’m not concerned it’s coming back. It seems like the IRS has backed off. … This is a huge win for American consumers and small businesses.”

It’s far from game over, though.

“It’s good news [the IRS] has returned to the status quo,” Metcalf said. “We still have issues to resolve. We still have to work out how we resolve the authentication issue, can we have private APIaccess to log in, can we expand the data in the transcript — all of those things we’re still seeking are outstanding.”

Beyond access to tax data, lenders and borrowers want the IRS to make it easier to use IVES. Currently, borrowers have to create IRS accounts and verify their identities with the agency before they can request that a transcript be delivered to a lender. That route is time-consuming and redundant, since the lenders themselves are required to verify identity under know-your-customer requirements, Metcalf said.

“The [optimal] outcome is we want a borrower to be able to submit a [transcript request] to the lender, the lender hands that to the IRS and we get the tax return in real time,” Metcalf said. “Or, if the lender has an account with the IRS already, they should just be able to log in to that account in our application. That’s the API access. … That’s what we want. We want that optionality of either/or.”

Bipartisan legislation introduced in the House of Representatives in May 2023 would address the authentication issue by enabling taxpayers to designate a financial institution or other service provider to receive tax data. The bill, introduced by North Carolina Republican Patrick McHenry, chairman of the House Financial Services Committee; California Democratic Rep. Jimmy Panetta; and Colorado Democratic Rep. Brittany Petterson, is currently under consideration by the Ways and Means Committee.

Funding Circle backs the legislation as it is currently written and is hoping to strengthen its language in the wake of the IRS’ action. “We’re getting ready to update that bill to address additional issues. … We would probably add on to it to make sure the IRS doesn’t revisit this policy decision,” Metcalf said.

The IRS didn’t respond to a request for comment at deadline.

Stewart attributed the IRS’ initial policy restricting IVES access to a desire to protect taxpayer information. “Their duty is paramount,” Stewart said, but he was quick to add that allowing API interface with IVES could be accomplished without compromising data integrity. “We don’t think creating this API is going to do anything to endanger the taxpayer, as long as you have them making the request directly through the lender or the insurance company or the bank.”

This story has been updated to add New York Community’s closing share price on Wednesday, as well as to note that the bank amended its investor presentation after the market closed to include guidance on net interest income in 2024.

January 31, 2024 5:44 PM EST

This story has been updated to add New York Community’s closing share price on Wednesday, as well as to note that the bank amended its investor presentation after the market closed to include guidance on net interest income in 2024.

Indymac Bancorp said today that it posted a $184.2 million first-quarter loss, or $2.27 per share, compared to profit of $52.4 million, or 70 cents per share, in the same period a year earlier.

The mortgage banking segment of the company’s business, which includes loan production, servicing, and commercial banking, posted a net loss of $8 million, compared to net earnings of $58 million a year ago.

The company said the loss reflected the severe dislocation in the secondary market for non-agency loans and Indymac’s shift to a more retail-centric, GSE-based business model.

Indymac produced $9.6 billion in mortgage loans during the quarter, down from over $12 billion in the fourth quarter, with 88 percent of loan origination volume saleable to the GSEs and all funded via deposits, with no capital markets funding sources.

With regard to the quality of new production, the S&P lifetime loss estimate fell to 0.23 percent from 1.86 percent a year ago, and first mortgage payment defaults declined to 0.6 percent in April from 2.2 percent in December.

Indymac was also able to reduce losses in the production segment by 66 percent compared to the fourth quarter as a result of “rightsizing” sales and staff and turning efforts toward agency production.

The second largest independent mortgage lender built up $2.7 billion in credit reserves, up from $2.4 billion in the prior quarter, and maintained its $4 billion in operating liquidity, stressing that less was actually needed with lower production volume.

CEO Mike Perry said the company was able to reduce credit losses to $249 million during the quarter, a 71 percent drop from the fourth quarter, and noted that roughly 50 percent of the first quarter loss could be attributed to recent staff reductions, office closures, and ceased business activities.

He said he expects the mortgage segment to be profitable in the second quarter and onward, and projects just a $20 million fourth quarter loss.

Additionally, the Pasadena, CA-based mortgage lender projects declining quarterly losses throughout the year, but does not expect to turn a profit in 2008 as long as home prices continue to sink.

Shares of Indymac fell 28 cents, or 8.16%, to $3.15 in afternoon trading on Wall Street.

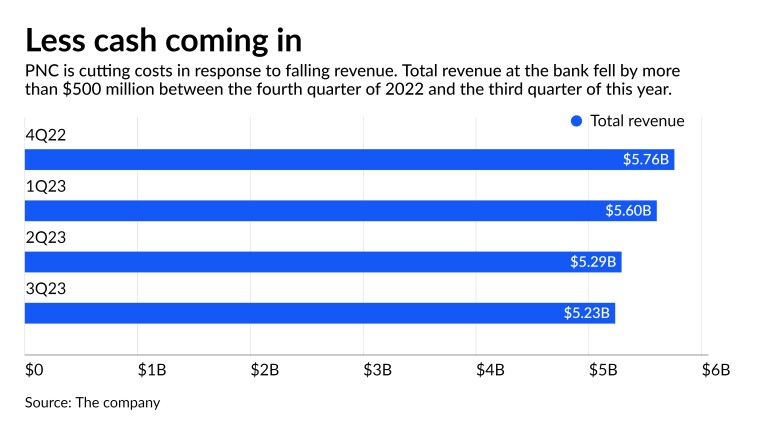

Amid falling revenue, PNC Financial Services Group said it will trim 4% of its workforce to curtail costs by $325 million and prop up its profitability in 2024.

The $557 billion-asset bank’s executives said during a third-quarter earnings call Friday that PNC initiated the staff cuts earlier this month in response to lower lending activity and declining interest income. Total revenue of $5.3 billion was down $60 million from the prior quarter and down $316 million from a year earlier.

The Pittsburgh-based bank had acknowledged earlier this week that it was cutting jobs. But it left many of the details of the plan, which will span PNC’s geographic footprint and business lines, for its earnings presentation and call on Friday.

“What’s new is basically dropping the run rate related to personnel and just tightening the ship in what is a tougher revenue environment,” CEO Bill Demchak told analysts on the call.

The projected savings, which amount to about 2% of PNC’s expected 2023 expenses, are projected to drop to the bottom line next year. They will come on top of $400 million-$450 million of savings from an annual “continuous improvement program” that was already underway, PNC said.

In July, the bank initiated a round of layoffs in its mortgage and home equity divisions. Home lending is under heavy pressure across the industry after mortgage rates more than doubled over the past two years.

In total, PNC is targeting $725 million of 2024 expense cuts, though the layoffs will necessitate a $150 million one-time charge in the fourth quarter.

The cuts will likely boost PNC’s bottom line next year, but its fourth-quarter earnings will be adversely impacted by the staff reduction charge, Autonomous Research analyst John McDonald wrote in a note to clients.

Meanwhile, Raymond James analyst Michael Rose lowered his 2024 earnings per share projection for PNC. He cited a belief that the bank’s net interest income and fee income will be lower than previously expected, and that its credit costs will be higher than previously projected, as factors offsetting the bank’s cost savings.

Rose estimated operating earnings per share of $13.45 for this year and $12.65 for 2024. Still, he maintained his “market perform” rating on PNC’s shares.

PNC Chief Financial Officer Robert Reilly explained the expense reductions by saying that 11 Federal Reserve interest rate hikes since early 2022 have taken a toll on bread-and-butter interest income and pushed up funding costs.

The trends crimped PNC’s net interest margin, which declined by eight basis points from the second quarter to 2.71%. The bank’s net interest income declined by $92 million, or 3%, from the prior quarter.

Third-quarter loans were down 2% from the prior quarter and averaged $320 billion, as more commercial borrowers moved to the sidelines amid the lofty rates.

Deposits were down 1% to $423 billion, even as PNC paid up for funding. The rate the bank paid on interest-bearing deposits increased to 2.26%, up from 1.96% for the prior quarter. That trend more than offset gains on loan yields of 18 basis points in the quarter to 5.75%.

PNC started 2023 with about 61,500 employees. It said the layoffs would be nearly completed by the end of this year.

“While decisions involving personnel are never easy, we believe they will help us more effectively and efficiently deliver for our customers and stakeholders, and we’ll continue to be diligent in our expense management going forward,” Demchak said.

Reilly emphasized that, following the July cuts, every expense category in the third quarter remained stable or declined from the second quarter. Overall noninterest expense of $3.2 billion was down 4%. Still, with no end in sight to high rates, more actions were needed to keep costs in check next year, he said.

“The current environment poses meaningful pressures,” Reilly said. “As a result, we took a hard look at our organizational structure and identified opportunities to operate more efficiently through staff reductions.”

PNC reported third quarter net income of $1.57 billion, or $3.60 per share. That was up from $1.5 billion, or $3.36, for the prior quarter but down from $1.64 billion, or $3.78, a year earlier. Analysts polled by FactSet Research Systems were expecting third quarter earnings of $3.10 per share.

MILWAUKEE, Sept. 14, 2023 /PRNewswire/ — Northwestern Mutual, a leading financial security company, announced today that Anne F. Ackerley and Andrew J. Harmening have been appointed to serve on its Board of Trustees. As a mutual company with a responsibility to policyowners, Northwestern Mutual has a Board of Trustees elected by its policyowners with responsibility … [Read more…]

Strong household spending and a resilient labor market could help the U.S. economy avoid a recession in 2024, the American Bankers Association’s Economic Advisory Committee says.

Jamie Kelter Davis/Bloomberg

Resilient household spending and a strong labor market will likely help the U.S. economy avoid a severe recession, according to a new forecast from economists at some of the country’s biggest banks.

The economy is poised to grow at a rate of less than 1% through the second quarter of 2024, the American Bankers Association’s Economic Advisory Committee said Monday. That is low compared with the second quarter rate of 4.1% but well above the dire predictions some economists once harbored for 2024.

“The odds of a soft landing have improved quite dramatically in the near term,” said Simona Mocuta, chief economist at State Street Global Advisors and the chair of the ABA’s committee of economic advisors.

The specter of recession has weighed on banks for close to 18 months, since the Federal Reserve began its campaign of rate hikes in March 2022. The health of the U.S. economy plays a key role in the profitability of banks, so the prospect of a contraction in economic growth raised red flags for banks large and small. The likely avoidance of one of the harsher economic scenarios — a severe recession — is good news for banks, which are also contending with generally tighter profit margins and increasing competition for customers.

Robust consumer spending has helped boost the U.S. economy so far in 2023, the ABA economists noted. Low unemployment and strong wage gains mean households have been able to keep up with many of their spending habits, even as inflation has persisted.

Inflation is also expected to improve in the coming quarters. Big-bank economists anticipate inflation levels to continue to cool to an annualized rate of 2.2% by the second quarter of 2024, close to the central bank’s target rate of 2%.

Although the overall economic picture is brighter, economists warn that there are several lingering threats that could make it more difficult for the U.S. economy and banks alike to grow.

The economists expect businesses to invest less capital in the short term, which could weigh on loan growth at banks. Loan growth at U.S. commercial banks increased 4.5% in the second quarter from a year earlier, according to Federal Deposit Insurance Corp. data.

About 4.4% of the labor forcewill be unemployed by the end of 2024, according to the economists’ forecast. A higher unemployment rate could make it more difficult for laid-off workers to make loan payments, potentially boosting the level of charge-offs at banks.

Credit quality reached historic lows during the pandemic, when many creditors offered grace periods and other breaks to struggling borrowers until the economy got back on track. Analysts expect asset quality to continue to deteriorate, with loan-loss increases spreading beyond the credit card and commercial real estate arenas.

“Investors are eager to learn how much higher net charge-offs are expected to go, especially with the student loan moratorium coming to an end,” Jason Goldberg, managing director and senior equity analyst at Barclays, wrote in a recent research note.

Certain elements of the ABA’s advisory committee’s forecast provide a strong contrast to the details issued when the last forecast was issued earlier this year, when economists believed the U.S. was on the edge of a mild recession.

“The tone of the conversation certainly feels much more positive today,” Mocuta said.

The ABA committee includes economists from some of the country’s largest banks. The group meets twice a year to discuss the economic environment and issue forecasts on economic growth, inflation and the trajectory of interest rate moves.

This year’s committee features representatives from U.S. Bank, Wells Fargo, JPMorgan Chase, State Street, Comerica Bank, BMO, TD Bank, PNC Financial Services, Deutsche Bank, First Horizon, Regions Financial, Northern Trust, Wilmington Trust and Morgan Stanley.

A Moody’s survey of 55 banks pointed to office loans as one the riskiest property types. Office loans have been hit by the shift toward remote work at some companies.

Jeenah Moon/Bloomberg

Banks are facing substantial risk of losses from commercial real estate loans, according to a new Moody’s survey of lenders, which found that some borrowers are already struggling and others may hit trouble when more of their loans mature.

The survey’s findings also suggest that some banks may not be tracking CRE borrowers’ health as closely as others — since they weren’t able to provide fully up-to-date metrics when asked.

The lack of timeliness in some banks’ disclosures was “eye-opening,” said Stephen Lynch, senior credit officer at Moody’s Investors Service. Up-to-date data about commercial property values and borrowers’ ability to cover their interest payments is critical for spotting potential problems, Lynch said.

“Good underwriting can maybe compensate for subpar portfolio analytics,” Lynch said, but strong analytics give banks the ability to mitigate problems early, rather than the often-costlier option of letting them bubble up.

The survey drew responses from 55 banks — including large, regional and community banks — in June and July. Since banks’ public disclosures are somewhat limited, Moody’s asked the respondents to provide more detail about certain key metrics.

Those measures include the percentage of CRE loans maturing soon; debt service coverage ratios, which show borrowers’ debt obligations relative to their cash flow; and loan-to-value ratios, which quantify the amount of debt outstanding as a percentage of the property’s value.

Some banks provided up-to-date data, while others submitted information from the end of 2022.

The Moody’s survey found that U.S. banks have significant amounts of CRE loans that will mature in the next 18 months. For the median bank that responded, those loans amounted to 46% of their tangible common equity — a percentage that Moody’s said was material. Some banks were substantially above that figure.

Upcoming maturities may pose problems for borrowers because they’ll need to refinance those loans, and they’ll need to do so at much higher interest rates and with banks being more demanding in their underwriting criteria.

Properties whose values have fallen sharply may get some help from providers of private capital, which can kick in additional equity to help property owners meet banks’ more stringent criteria. But the amount of money available likely isn’t going to “move the needle,” given the large amount of loans outstanding, Moody’s Lynch said.

While private equity firms, hedge funds and other sources of private capital may see opportunities to jump in, they are “not going to solve every problem,” said Brendan Browne, an analyst at the ratings firm S&P Global. Private money will help where companies see a chance to make significant returns, but there will also be cases “where the economics probably just don’t work well enough,” Browne said.

Overall, banks will feel “some pain” on CRE loans — particularly banks with larger exposures to the sector, Browne said. Most of the banks that S&P rates don’t have such outsized exposures, he added.

The Moody’s survey pointed to office and construction loans as the riskiest property types, given the shift at some companies toward remote work and the fact that properties that serve as collateral for construction loans don’t earn income while those loans are outstanding.

A loan may be at greater risk now if the borrower is having a tougher time paying its obligations. So Moody’s asked banks about how many of their loans have debt service coverage ratios below 1, an indication that the borrower does not have adequate cash flow.

The median respondent has 13.5% of its tangible common equity in CRE loans where the debt service coverage ratios are below 1, Moody’s survey found.

That figure was higher than Moody’s expected, Lynch said.

NexTier, the holding company of NexTier Bank, will acquire Mars Bancorp, the holding company of Mars Bank. Terms of the deal were not disclosed.

The combined company and branch locations will operate under the NexTier Bank brand, both banks said in a release Thursday. With the acquisition, NexTier Bank will have total assets in excess of $2.6 billion.

Clem Rosenberger, NexTier’s president and CEO, will lead the combined institution. Meanwhile, Jim Dinoise, president and CEO of Mars, will join the NexTier Bank Board of Directors upon the consummation of the transaction.

“This merger ensures our customers will continue to receive access to the products, services, and technology they need while maintaining the relationship-driven, hands-on service they’ve come to expect,” Dionise said in a statement.

Mars Bank — an independent community bank in Pennsylvania — offers mortgage lending, retail and commercial banking in six locations throughout the state.

Mars Bank held $520.8 million in assets as of June 30, 2023.

In the mortgage lending business, Mars Bank offers 30-year fixed conventional, FHA loans, a medical professionals mortgage program, construction loans, home equity loans and Home Equity Line of Credits (HELOCs), according to its website.

Mars Bank posted an origination volume of $50.9 million across 234 loans in the past 12 months, according to the mortgage data platform Modex.

NexTier Bank has 27 branches in western and central Pennsylvania and had $2.1 billion in assets as of June 30, 2023.

In its mortgage division, the bank offers construction, purchase loans, home equity loans as well as HELOCs in addition to providing consumer loans, wealth management and merchant services.

NexTier Bank produced $50.6 million in origination across 205 loans over the past 12 months, Modex showed.

Data from the July jobs report released Friday fell roughly in line with expectations. Job gains came in lower than both the 278,000 monthly average for the first half of 2023 and the 399,000 average of 2022. Total nonfarm payroll employment increased by 187,000 jobs, compared to 209,000 in June, according to data released by the Bureau of Labor Statistics.

The unemployment rate changed little at 3.5%, compared to 3.6% in May, with the total number of unemployed persons falling to 5.8 million. The unemployment rate has remained between 3.4% and 3.7% since March 2022.

In June, job openings eased back to 9.6 million, bringing the openings rate to 5.8%. Meanwhile job quits slipped to 3.8 million or 2.4%.

“The incoming economic data continue to convey conflicting signals about the strength of the economy. Indicators of manufacturing and service sector health remain lackluster, measures of inflation have moved lower, while GDP growth in the second quarter was stronger than expected and consumer spending remains resilient,” said Mortgage Bankers Association VP and Deputy Chief Economist Joel Kan.

While job growth is weakening, and wage growth is holding steady, both metrics are still above the pace that would be consistent with the Federal Reserve’s inflation target, noted Kan.

“However, we expect that the FOMC will hold the federal funds target at its current level given the declining trend in inflation,” he added.

The lion’s share of the job growth in June came from gains in health care (+63,000), social assistance (+24,000), financial activities (+19,000), and wholesale trade (+18,000), according to the report.

Employment in the construction industry continued to trend up in July, adding 19,000 jobs, especially in the residential construction space. The ongoing shortage of housing inventory helped spur an increase in home building and home improvement activity, Kan said.

On average, the industry added 16,000 jobs per month in the second quarter of the year, after employment was essentially flat in the first quarter. Over the month, a job gain in real estate and rental and leasing (+12,000) partially compensated for a loss in commercial banking (-3,000).

Furthermore, residential building construction employment was flat year-over-year in July, while non-residential was up by 5.9%, according to First American Economist Ksenia Potapov. Compared with pre-pandemic levels, residential building employment is up 10%, while non-residential building is up 3%.

“Like June, the fastest monthly growth came from residential specialty trade contractors. This sub-sector comprises establishments whose primary activity is performing specific activities, such as pouring concrete, site preparation, plumbing, painting and electrical work,” said Potapov.

Employment in the professional and business services sector and in the leisure and hospitality sector changed little in July.

What’s next ?

At the July Fed meeting, the FOMC hiked the benchmark rate by a quarter percentage point, as widely expected. During the press conference that followed the meeting, Fed Chair Jerome Powell said that another rate hike in September is “certainly possible,” but so is a pause.

According to Realtor.com‘s chief economist Danielle Hale, today’s report is unlikely to sway the Fed.

“Today’s jobs report is unlikely to change those odds significantly as it is one of several pieces of additional data that the Fed will have to consider before the next decision. The Fed will see not only an additional jobs report, but also two more readings each on consumer prices and producer prices along with several other indicators before its September 19-20 meeting and decision,” said Hale.

On the housing market, she said that conditions are still favorable for households, supporting housing demand. However, climbing mortgage rates remain a substantial obstacle for homebuyers. Hale expects more “coping strategies” on the buyer’s end, such as moving further away to find affordability. Another outcome will be that affordable markets, such as those in the Midwest, will continue to see an outsized level of housing activity for both homeowners and renters, she said.

As existing homeowners remain rate-locked into their homes with no financial incentive to move, homeowners are likely to increasingly turn to renovating their homes to suit their evolving needs, added Potapov.