Recent swings in mortgage rates are helping to drag down contract signings, which fell 5% in January, the National Association of REALTORS® reported this week. Pending home sales, a forward-looking indicator of housing activity based on contract signings, were down 8.8% compared to a year earlier.

“The job market is solid, and the country’s total wealth reached a record high due to stock market and home price gains,” says NAR Chief Economist Lawrence Yun. “This combination of economic conditions is favorable for home buying. However, consumers are showing extra sensitivity to changes in mortgage rates in the current cycle, and that’s impacting home sales.”

In recent weeks, mortgage rates have started creeping back toward 7%. Freddie Mac reports the 30-year fixed-rate mortgage averaged 6.94% this week, marking a two-month high. “While this is still below the rates seen in the fall of 2023, it impacts home buyers’ excitement about entering a spring market,” says NAR Deputy Chief Economist Jessica Lautz. The monthly mortgage payment for a $400,000 home, assuming a 20% down payment, now translates to about $2,116, Lautz adds. “For first-time buyers who are the most price-sensitive, the rise in mortgage rates poses a cause for concern, as they may be priced out of the market.”

Indeed, “the recent boomerang in rates has dampened already tentative homebuyer momentum as we approach the spring, a historically busy season for home buying,” adds Sam Khater, Freddie Mac’s chief economist. “While sales of newly built homes are trending in a positive direction, higher rates and elevated prices continue to pose affordability challenges that may leave potential home buyers on the sidelines.”

Freddie Mac reports the following national averages with mortgage rates for the week ending Feb. 29:

30-year fixed-rate mortgages: averaged 6.94%, rising from last week’s 6.9% average. A year ago, 30-year rates averaged 6.65%.

15-year fixed-rate mortgages: averaged 6.26%, dropping slightly from last week’s 6.29% average. Last year at this time, 15-year rates averaged 5.89%.

NAR’s chief economist Lawrence Yun said in remarks accompanying the release that high mortgage costs were the main barrier to homebuying intentions in the present market. “This combination of economic conditions is favorable for homebuying,” Yan said. “However, consumers are showing extra sensitivity to changes in mortgage rates in the currently cycle, and that’s impacting … [Read more…]

LOS ANGELES — The average long-term U.S. mortgage rate rose for the fourth consecutive week, another setback for prospective homebuyers just as the spring homebuying season gets going.

The average rate on a 30-year mortgage rose to 6.94% from 6.90% last week, mortgage buyer Freddie Mac said Thursday. A year ago, the rate averaged 6.65%. The average rate is now just below its highest level since mid-December, when it was 6.95%.

When mortgage rates rise, they can add hundreds of dollars a month in costs for borrowers, limiting how much they can afford in a market already out of reach for many Americans. They also discourage homeowners who locked in rock-bottom rates two or three years ago from selling.

Rates have been creeping higher in recent weeks as reports showing stronger-than-expected inflation at the consumer and wholesale levels and the economy stoked worries among bond investors that the Federal Reserve will wait until later this year before it begins cutting interest rates. A closely followed inflation report on Thursday showed showed prices across the country rose pretty much as expected last month.

Investors’ expectations for future inflation, global demand for U.S. Treasurys and what the Fed does with interest rates can influence rates on home loans.

Despite the recent increase, the average rate on a 30-year mortgage is still down from the 23-year high of 7.79% it reached in late October.

The pullback in rates in November and December helped lift sales of previously occupied U.S. homes by 3.1% in January versus the previous month to the strongest sales pace since August.

Still, the recent uptick in rates is an unwelcome shift for would-be homebuyers just as the spring homebuying season ramps up.

“The recent boomerang in rates has dampened already tentative homebuyer momentum as we approach the spring, a historically busy season for homebuying,” said Sam Khater, Freddie Mac’s chief economist. “While sales of newly built homes are trending in a positive direction, higher rates and elevated prices continue to pose affordability challenges that may leave potential homebuyers on the sidelines.”

Competition for relatively few homes on the market and elevated mortgage rates are limiting house hunters’ buying power on top of years of soaring prices.

Already there are signs that the rise in rates in recent weeks has had an impact on home sales.

Contract signings on U.S. homes fell 4.9% in January from the previous month and were down 8.8% from a year earlier, the National Association of Realtors said Thursday. The report is a barometer of future home purchases as there’s typically a lag of a month or two between a signed contract and a completed sale.

Meanwhile, home loan applications have declined for three consecutive weeks, according to the Mortgage Bankers Association.

Homeowners seeking to refinance got some good news this week. Borrowing costs on 15-year fixed-rate mortgages, popular with homeowners refinancing their home loans, declined this week, pulling down the average rate to 6.26% from 6.29% last week. A year ago it averaged 5.89%, Freddie Mac said.

The numbers: Pending home sales fell in January as rising mortgage rates pushed buyers out of the housing market.

Pending home sales fell 4.9% in January from the previous month, according to the monthly index released Thursday by the National Association of Realtors (NAR).

Pending home sales reflect transactions where the contract has been signed for an existing-home sale, but the sale has not yet closed. Economists view it as an indicator of the direction of existing-home sales in subsequent months.

The drop in pending home sales was the largest since August 2023, when they fell 5%.

The sales pace fell short of expectations on Wall Street. Economists were expecting pending home sales to increase by 1.5% in January.

Transactions were down 8.8% from last year.

Big picture: Mortgage rates began their ascent to 7% towards the end of January, when the market saw that the Federal Reserve would not be cutting interest rates in March.

Even slight increases in rates can affect how much some buyers can afford to buy a home. At 7%, the monthly payment on a $400,000 home would be roughly $2,700, and buyers would potentially need to earn $108,440 a year to afford that comfortably.

Looking ahead, applications for purchase mortgages are trending down, as mortgage rates remain over 7% at the end of February. That indicates that sales activity may be muted in the coming months.

What the Realtors said: “The job market is solid, and the country’s total wealth reached a record high due to stock market and home price gains,” Lawrence Yun, chief economist at the NAR, said in a statement.

While “this combination of economic conditions is favorable for home buying,” he added, “consumers are showing extra sensitivity to changes in mortgage rates in the current cycle, and that’s impacting home sales.”

What they’re saying: “Pending home sales, or contract signings, measure the first formal step in the home sale transaction, namely, the point when a buyer and seller have agreed on the price and terms,” Hannah Jones, senior economic research analyst at Realtor.com, said in a statement.

“Pending home sales tend to lead existing home sales by roughly one-to-two months and are a good indicator of market conditions,” she added. And “the recent uptick in rates could mean slower seasonally adjusted sales as the spring homebuying season kicks off.”

Rates for 30-year mortgages dropped again, but homes remain unaffordable in most areas. (iStock)

Mortgage rates dropped to 6.63% this week, according to Freddie Mac’s Primary Mortgage Market Survey. Rates for 30-years fixed-rate mortgages were 6.69% last week, dropping by 0.06 percentage points.

Rates for 15-year mortgages also dropped slightly from 5.96% last week to 5.94% this week. Both 15-year mortgages and 30-year mortgage rates are still higher than they were last year.

A year ago, 30-year mortgages sat at 6.09%, on average, while 15-year mortgages averaged 5.14%, Freddie Mac reported.

“Mortgage rates have been stable for nearly two months, but with continued deceleration in inflation we expect rates to decline further,” Freddie Mac Chief Economist Sam Khater explained.

“The economy continues to outperform due to solid job and income growth, while household formation is increasing at rates above pre-pandemic levels. These favorable factors should provide strong fundamental support to the market in the months ahead.”

As mortgage rates drop, you may decide it’s the right time to finally buy a home. To find the right mortgage for your needs, Credible can show you multiple mortgage lenders all in one place and provide you with personalized rates within minutes.

HOMEOWNERS INSURANCE RATES ON THE RISE, MAINLY DUE TO INCREASE IN NATURAL DISASTERS

Home prices are lowering in some major cities

After remaining for high most of the year, home prices are dropping slightly in some metro areas.

Data from a recent S&P report showed prices in 12 out of 20 metro areas decreasing. This decrease in prices has led some households to move across state lines in search of more affordable areas.

Charlotte, Providence and Indianapolis saw the largest increase in buyers as they fled high-cost cities, stated a Zillow report.

Households that made these moves found homes were $7,500 less, on average, than where they left.

Cities that saw the highest outflow in households included Chicago, San Diego and Cincinnati. These metro areas often have higher housing costs and less robust economies, Zillow found.

If you think you’re ready to shop around for a home loan, consider using Credible to help you easily compare interest rates from multiple lenders, all without affecting your credit score.

HOMEOWNERS MOVING ACROSS STATE LINES, SEEKING AFFORDABILITY, FIND IT IN CERTAIN CITIES

It’ll be years before homes are affordable for the average buyer

The housing market is trudging toward recovery, largely thanks to mortgage interest rates dropping in recent months.

“The surge in pending home sales and new home sales, both determined by contract signings in the early stages of the buying process, indicates increased participation from buyers in the market,” explained Realtor.com Economist Jiayi Xu in response to Freddie Mac’s recent mortgage rates update. “Simultaneously, the recent rise in listing activity suggests that sellers are closely monitoring mortgage rates and adjusting their selling strategies accordingly.”

Potential homebuyers won’t see a full recovery anytime soon, however. JP Morgan experts predict that the real estate market will become affordable again about three and a half years from now. This is largely dependent on continued interest rate decreases.

“Despite the promising increase in listing activity, inventory is likely to remain low as sellers may not respond as swiftly as anticipated. In other words, a more substantial improvement in mortgage rates is necessary to attract more sellers to the market,” Xu said.

Until rates drop more substantially, mortgage payments are likely to stay high. In November 2023, the average monthly mortgage payment was $2,198, up from $1,993 a year earlier, a National Association of Realtors report found.

If buying a home is your near future, make sure you’re getting the best mortgage lender and rates with the help of Credible. Credible helps you compare rates and lenders and get a mortgage pre-approval letter in minutes.

JUST OVER 15% OF HOME LISTINGS WERE CONSIDERED AFFORDABLE IN 2023: REDFIN

Have a finance-related question, but don’t know who to ask? Email The Credible Money Expert at [email protected] and your question might be answered by Credible in our Money Expert column.

(Bloomberg) — A gauge of pending US existing-home sales rebounded sharply in December to a five-month high, suggesting the recent drop in mortgage rates is helping to stabilize the resale market.

Most Read from Bloomberg

The National Association of Realtors’ index of contract signings increased 8.3% to 77.3 after holding at a record low a month earlier, according to data out Friday. Last month’s advance — the largest since mid-2020 — exceeded all estimates in a Bloomberg survey of economists.

“The housing market is off to a good start this year, as consumers benefit from falling mortgage rates and stable home prices,” Lawrence Yun, NAR’s chief economist, said in a statement. “Job additions and income growth will further help with housing affordability, but increased supply will be essential to satisfying all potential demand.”

While 30-year fixed mortgage rates remain below 7%, a sustained decline is needed to encourage more homeowners to list homes that are financed at much lower levels. Until that develops, a limited inventory of previously owned homes will make it difficult for the resale market to rapidly gain traction.

A lack of listings have also worked to keep existing-home prices elevated. At the same time, builders have been filling the void with new construction. The number of new houses for sale at the end of 2023 rose to a more than one-year high, helping push those prices down.

The pending-home sales report is a leading indicator of existing-home sales given houses typically go under contract a month or two before they’re sold. Those sales are expected to increase 13% this year, according to NAR’s economic outlook. They slumped 18.7% in 2023.

The NAR’s report showed the index of contract signings for existing homes jumped nearly 12% in the South, the biggest US housing market. That was the largest advance since June 2020. Pending sales also surged 14% in the West and climbed 5.6% in the Midwest.

The National Association of Realtors (NAR) releases two widely followed home sales reports. Existing Home Sales measure transactions of homes other than new construction (i.e. previously owned and occupied homes). The Pending Sales index is an advance indicator for Existing Homes. It measures contract signings but not closed sales.

Through a combination of historically low affordability and inventory, both metrics have been operating at the lowest levels in more than a decade (not including the temporary drop in pending sales seen at the onset of pandemic lockdowns). Today’s pending sales update kept the index perfectly unchanged at those long term lows.

There were small regional variations as follows:

Northeast… +0.8% versus last month (down 6.4% from last year)

Midwest …. +0.5% versus last month (down 2.2% from last year)

South……… -2.3% versus last month (down 6.5% from last year)

West………. +4.2% versus last month (down 4.9% from last year)

As seen in the chart above, the sharpest deceleration in the pace of sales is likely behind us. Recent changes have been much smaller by comparison. NAR is hopeful for 2024, citing the recent decline in mortgage rates.

Additionally, NAR’s Chief Economist Lawrence Yun noted “although declining mortgage rates did not induce more homebuyers to submit formal contracts in November, it has sparked a surge in interest, as evidenced by a higher number of lockbox openings.”

Sales of previously owned U.S. homes fell by the most in nearly a year in October, highlighting the toll elevated mortgage rates and still-high prices continue to take on the resale market.

Contract closings decreased 4.1% from a month earlier to a 3.79 million annualized pace, still the lowest since 2010, National Association of Realtors data showed Tuesday. The figure was weaker than all but one estimate in a Bloomberg survey of economists.

The combination of soaring mortgage rates and stubborn prices has been discouraging buyers and sellers alike. However, with mortgage rates retreating as the Federal Reserve nears the end of its tightening cycle, that’s offering some hope that the housing market may be bottoming out.

“Fortunately, mortgage rates have fallen for the third straight week, stirring up buying interest,” said Lawrence Yun, NAR’s chief economist. “Though limited now, expect housing inventory to improve after this winter and heading into the spring.”

The median selling price climbed 3.4% from a year earlier to $391,800, the highest for any October in data back to 1999. Yun added that nearly a third of homes sold above their list price, indicating that multiple offers are still occurring — particularly on starter and mid-priced homes.

Even though the number of homes for sale ticked up from a month earlier to 1.15 million, it’s still the lowest for any October in the series. At the current sales pace, it would take 3.6 months to sell all the properties on the market. Realtors see anything below five months of supply as indicative of a tight market.

The NAR’s report showed 66% of homes sold were on the market for less than a month. Properties remained on the market for 23 days on average in October, up slightly from September.

Existing-home sales account for the majority of US housing and are calculated when a contract closes. Data on new-home sales, which make up the remainder and are based on contract signings, are due next week.

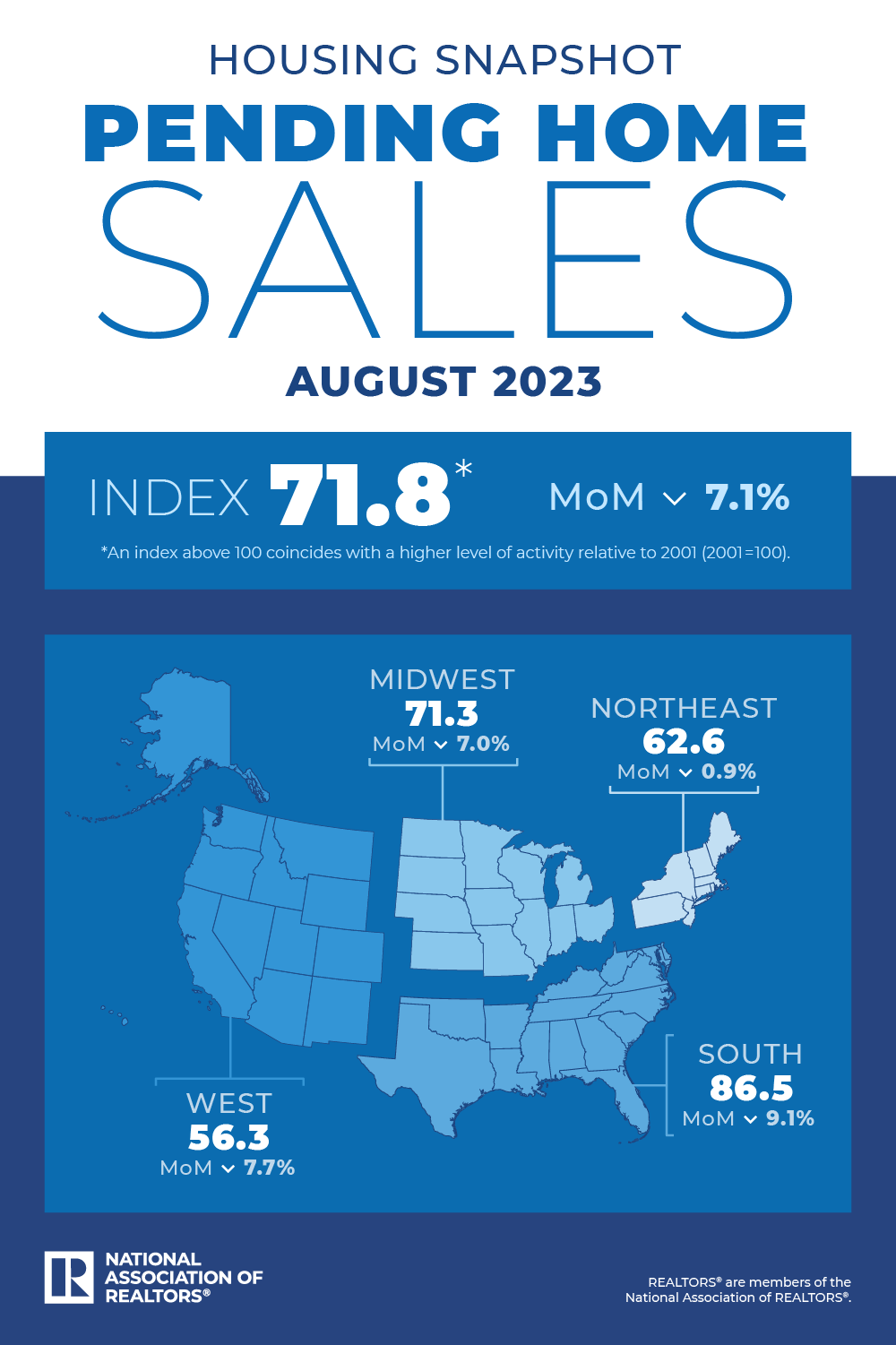

The National Association of REALTORS® reported Thursday that contract signings tumbled 7.1% month over month in August as mortgage rates float above 7%, pushing many aspiring home buyers to the sidelines. All four major U.S. regions saw monthly decreases, according to NAR. Pending home sales are down 19% from a year earlier. “It’s clear that increased housing inventory and lower interest rates are essential to revive the housing market,” says NAR Chief Economist Lawrence Yun.

Mortgage rates have been rising above 7% since August, which has diminished the pool of home buyers, Yun says. “Some would-be home buyers are taking a pause and readjusting their expectations about the location and type of home to better fit their budgets.”

Home shoppers also are grappling with higher home prices. The median price nationwide for an existing home rose nearly 4% year over year in August and has held above $400,000 for three consecutive months, according to NAR data.

New-home sales, which were a bright spot for the housing market recently, also dropped nearly 9% last month to their weakest level since March. Builders blamed elevated mortgage rates and challenging affordability conditions for the decline.

“Builders continue to grapple with supply-side concerns in a market with poor levels of housing affordability,” says Alicia Huey, chairperson of the National Association of Home Builders. “Higher interest rates price out demand, as seen in August, but also increase the cost of financing for builder and developer loans, adding another hurdle for building.”

Little Relief in Sight

Housing affordability fell in July as monthly mortgage payments climbed 18.4%, according to NAR’s latest Affordability Index. (At the time of the index’s last reading, mortgage rates were 6.92%.) At the same time, the median family income increased only 4.4%. The index showed that the typical family nationwide couldn’t afford a median-priced home.

In recent weeks, mortgage interest rates have reached the highest level since 2000, prompting loan demand to sink to a 27-year low, the Mortgage Bankers Association reported this week.

At its meeting last week, the Federal Reserve voted to pause increases to its benchmark interest rate but hinted at another hike before the end of the year.

“Overall, [mortgage] applications declined as both prospective home buyers and homeowners continue to feel the impact of these elevated rates,” says MBA Economist Joel Kan. Mortgage applications to purchase a home last week fell 27% lower than the same week a year ago, MBA reports.

“The Federal Reserve must consider the sharply decelerating rent growth in its consideration of future monetary policy,” Yun says. “There is no need to raise interest rates. Moreover, the government shutdown will disrupt some home sales in the short run due to the lack of flood insurance or delays in government-backed mortgage insurance.”

Mirroring the trend for new home sales(+4.4%), pending home sales rose 0.9% in July, according to data released Wednesday by the National Association of Realtors (NAR).

Year over year, pending home sales were down 14%, a smaller decrease than the 15.6% annual drop recorded in June. However, unlike the market for new homes, which has recovered convincingly above last year’s lows (+31.5%), pending home sales continue to lag behind year-ago levels (-14.0%). The NAR’s Pending Home Sales Index climbed to a reading of 77.6 in July. An index of 100 is equal to the level of contract activity in 2001.

“The small gain in contract signings shows the potential for further increases in light of the fact that many people have lost out on multiple home buying offers,” said NAR Chief Economist Lawrence Yun. “Jobs are being added and, thereby, enlarging the pool of prospective home buyers. However, rising mortgage rates and limited inventory have temporarily hindered the possibility of buying for many.”

Month over month, contract signings increased in the South and West but decreased in the Northeast and Midwest

Regionally, on a month-over-month basis, the South (95.3) and the West (61.3) pending home sales climbed and showed the smallest declines from one year ago, according to Realtor.com Chief Economist Danielle Hale. Meanwhile the Northeast (63.2) and the Midwest (77.5) interestingly fell, even though these two regions recently boasted more robust real estate activity and stronger pricing. Compared to a year ago, pending sales activity was down by more than 20% in the Northeast region, the biggest decline in that region over the past year, noted Lisa Sturtevant, Bright MLS chief economist.

“Greater availability of homes for sale in the South and price breaks in the West were likely contributors,” said Hale.

Overall, pending home sales fell in all four U.S. regions compared to one year ago.

Two consecutive months of increases doesn’t necessarily mean that the housing market is moving

The median existing home price crawled north of $400,000 in July while interest rates inched above 7%.

“These significant affordability challenges, as well as a continued dearth of inventory, lower the likelihood that pending sales will continue to grow,” said Kate Wood, home and mortgage expert at NerdWallet.

While it is common for pending sales to decline between June and July, this year’s situation is tougher, said Sturtevant.

“Buyers are being forced to lengthen their home search since there are so few properties available for sale,” she said.

In fact, two out of three Mid-Atlantic buyers who purchased in July had to make an offer on more than one home before they were successful, found a Bright MLS’s recent survey.

Sales activity is expected to remain slow for the rest of the year, as inventory remains low and mortgage rates remain high, noted Sturtevant.