Inside: Explore financial independence: Unveil why a debt-free life could be your path to riches, with practical strategies for lasting wealth without owing. Perfect for millennials or those new to managing money.

In an era where financial burdens weigh heavily on so many, adopting a lifestyle of debt-free living emerges as the modern epitome of wealth.

I’ve come to understand that true affluence isn’t just measured by the amount of dollars in your bank account, but by the freedom from the chains of debt. It’s not just about strict budgeting or cutting corners; it’s about the elevated sense of security and control that comes from owing nothing to anyone.

Encountering the peace of mind that accompanies a debt-free life has indeed propelled our financial well-being and moved us closer to our FI number.

But, the question for today, is being debt free the new rich, and the secret to true wealth. Let’s dig into that answer.

Debt-Free as the Gateway to Modern Affluence

In the past, wealth was often measured by the accumulation of material possessions and the perceived status they conferred.

Today, however, there’s a growing recognition that true affluence lies in financial freedom. Redefining wealth to include the absence of debt reflects a holistic understanding of prosperity in today’s economy.

Is being debt-free the new rich?

The question “Is being debt-free the new rich?” is more relevant than ever in a society enmeshed with credit and consumption.

Being debt-free signals a shift from traditional wealth, defined by material possessions, to a contemporary form of richness—one where financial stability and peace of mind take precedence.

Yes, being debt free will lead to increased wealth over time.

Debunking the Myth: Rich vs. Debt-Free

Many hinge their perceptions of wealth on income and assets without considering the crippling effects of debt. Being rich traditionally meant having substantial financial resources, but without considering debt, this view is incomplete.

Many individuals labor under misconceptions about living a debt-free life, believing it to be a goal that’s out of reach or mired in unrealistic sacrifices.

Let’s dispel these myths and highlight how a debt-free life is not only achievable but also a liberating choice that defies conventional financial norms.

Myth #1: You need a credit card to survive in today’s economy.

Many people believe a credit card is essential for building credit and making daily purchases. However, if you are unable to repay that credit card bill at the end of the month, then you shouldn’t use one.

Credit cards are helpful especially if you benefit from the credit card rewards. Many millionaires used the cash envelope system to get where they are at.

Myth #2: Student loans are the only path to higher education.

The notion that college is unaffordable without borrowing is widespread, yet there are numerous alternatives to student loans for funding education.

Learn how to get paid to go to school with scholarships, grants, work-study programs, and attending community college first. These are all viable strategies to pursue higher education without incurring massive debt.

Myth #3: Car payments are an unavoidable monthly expense.

Car payments are often accepted as a normal part of finance management, but it’s a myth that you’ll always have one. This one still makes me cringe – car payments are not considered normal.

By saving up and purchasing a reliable used vehicle, many can avoid the cycle of car loans, and even if a loan is necessary, paying it off quickly can relieve you from years of ongoing payments.

Myth #4: Debt is a necessary tool to achieve financial success.

Contrary to the belief that leveraging debt is how wealthy individuals build their empires, many successful people use debt strategically, if at all.

It’s possible to accumulate wealth through saving, investing wisely, and living within one’s means, all without relying on debt. Building wealth debt-free is slower but more stable and reduces the risks associated with borrowing.

Plus it increases the debt-to-income ratio.

Myth #5: Paying Off Debt is Too Hard and Takes Forever

Paying off debt utilizing strategies such as the debt snowball or avalanche method instead of waiting is crucial for several reasons.

Both approaches provide structured plans that create discipline, making it less overwhelming to tackle debt systematically. Paying off debts faster with these methods typically reduces the total interest paid over time, leading to significant savings.

Moreover, the quicker you become debt-free, the sooner you can redirect your income toward building wealth, saving for the future, or investing in opportunities. Finally, the psychological boost from witnessing debts disappear can be incredibly motivating, improving your financial confidence and relieving stress associated with high levels of debt.

Myth #6: Pointless to Pay Off Debt if Making More on the Money

Paying off debt can sometimes seem counterintuitive, especially if you’re making more on your money through investments or savings compared to the interest on your debt. While from a purely mathematical standpoint, it may make financial sense to keep the debt and grow your investments, the freedom from being debt-free transcends numbers.

However, the psychological benefits of not owing money—such as reduced stress, increased mental well-being, and the peace of mind that comes with financial security—often outweigh the potential financial gains from investing.

Debt can feel like a burden, and removing this can lead to a clearer mindset, freeing up mental energy and resources to focus on other aspects of life.

Myth #7: I’ll Be Broke Forever

Overcoming “I am broke” mindset to achieve debt freedom often requires a substantial shift in both behavior and perspective.

It involves breaking the cycle of living paycheck to paycheck and resisting instant gratification by prioritizing financial goals over immediate desires. Replacing impulsive spending habits with disciplined budgeting and intentional saving can be a challenging, yet empowering transition.

This transformation not only demands goal-setting but also a deep understanding that possessions do not measure true wealth but by financial security and the freedom it brings.

Myth #8 – Debt Won’t Limit Your Financial Freedom

Debt often acts as a chain that restricts monetary mobility.

Carrying debt means committing future earnings to past expenses, limiting the ability to invest in opportunities or save for unforeseen events.

True financial freedom can only be found when these chains are broken, unlocking the full potential to use your income to shape the life you desire. This is what you will learn here at Money Bliss.

Strategies for Achieving a Debt-Free Life

Achieving a debt-free life involves setting clear, attainable goals, exercising self-restraint to avoid unnecessary expenditures, and creating a focused plan of action to eliminate existing debts.

By embracing contentment and understanding that happiness isn’t tied to material possessions, one can redirect funds towards paying off debts, paving the way for a life with greater financial independence and security.

Tip #1 – From Calculating Debts to Making a Payoff Plan

Embarking on the journey to debt freedom begins with a clear assessment of your financial landscape. It’s essential to compile a comprehensive list of your debts, noting balances, interest rates, and minimum payments.

Armed with this information, constructing a tailored payoff plan becomes your blueprint to financial liberation. Taking this active step forward is where the climb back to solvency begins.

Tip #2 – Overcoming Social Pressures and Lifestyle Inflation

Social pressures and lifestyle inflation are formidable obstacles in the pursuit of debt freedom.

The urge to spend is often magnified by the fear of missing out (FOMO) and the desire to match others’ spending habits (aka Joneses). Overcoming these cultural norms is critical for individuals determined to maintain financial health and resist the lure of indebtedness.

Tip #3 – Budgeting, Saving, and Earning More

Budgeting is the roadmap to tracking and controlling your spending while saving ensuring you’re prepared for the future. Consider it carving a path to financial freedom.

Earning more, whether through advancement in your current role or side hustles, accelerates debt repayment. Balancing these pillars is key – spend wisely, save diligently, and earn aggressively to break the chains of debt.

Tip #4 – The Shift Towards Minimalism and Non-Materialism

A growing number of individuals are embracing minimalism, finding richness in life’s experiences over the accumulation of goods.

This paradigm shift from materialism to non-materialism spotlights the value of simplicity and intentional living. It’s a conscious choice to prioritize quality over quantity, creating space for financial freedom and personal growth.

Tip #5 – Investing and Saving: The Vehicles for Sustainable Wealth

Once debt is cleared, saving and investing become the twin engines driving the journey toward sustainable wealth. This is the #1 overlooked thing I see too often.

The idea of investing in stocks is overwhelming to too many; thus, you are doing nothing with your money.

A savings account offers a cushion against life’s uncertainties, while investments can grow your wealth exponentially over time. By harnessing the power of compound interest and diversification, you’re not just avoiding financial pitfalls but actively building your monetary legacy.

Tip #6 – The Necessary Sacrifices for Long-Term Gain

Achieving debt freedom often requires sacrifices that can test your resolve in the short term. I can attest to this over and over. But, then I see progress on my journey and I’m grateful.

Whether it’s forgoing a luxury purchase, downsizing your living space, or choosing a staycation over a lavish holiday, these decisions contribute to a greater financial objective. Embracing necessary sacrifices paves the road to long-term gain and a richer future, free from financial constraints.

Tip #7 – Leveraging a Debt-Free Status for Financial Growth

Living debt-free opens doors to financial opportunities previously blocked by loan repayments and high interest rates. You are focused on improving your liquid net worth.

This status can be leveraged for growth by increasing investments, acquiring assets, or starting a business without the drag of debt. It’s about transforming newfound liquidity into channels that foster wealth expansion and provide long-term financial security.

Real Stories: Transformations from Debt to Wealth

The tales of debt freedom resonate with hope and inspiration.

Imagine the relief of one less bill in the mailbox or the pride in finally owning your car outright. These personal anecdotes serve as powerful testaments to the life-altering impact of paying off debt.

Scott Alan Turner felt trapped by student loans for years, only to transform their financial narrative by dedicating extra payments to their debt and eventually questioning every single impulse purchase.

Each story underscores a unique journey of dedication, strategy, and eventual liberation that changes lives fundamentally.

The Ripple Effect on Families and Future Generations

Debt freedom not only transforms individual lives but also sends ripples through families and across generations.

Free from financial burdens, parents can invest in better education for their children, save for their own retirement, and instill the value of living within one’s means. Creating a new family legacy.

FAQ: Embracing a Debt-Free and Wealthy Outlook

Being truly debt-free means you have no outstanding financial obligations—no loans, no credit card balances, and no debts lingering over your head.

It reflects a clean slate of financial commitments, allowing for unrestricted use of your income and providing a robust platform for financial growth and security.

While happiness is subjective, studies consistently link less debt to higher levels of contentment. 1

People without debt often report a greater sense of peace and well-being, liberated from the anxieties and constraints associated with debt. Freeing oneself from financial liabilities allows for a lifestyle focused on experiences and personal fulfillment, factors known to enhance happiness.

It is generally advantageous to be completely debt-free, as it alleviates financial stress, increases disposable income, and contributes to a solid foundation for building wealth. Without the burden of debt repayments, individuals can allocate funds to savings, investments, or personal passions, enhancing their overall quality of life and financial stability.

Avoiding debt is often seen as countercultural because society promotes a credit-fueled economy, where debt is normalized for consumption and lifestyle enhancement.

Challenging this norm by rejecting debt goes against these ingrained beliefs, embracing financial independence and self-reliance over societal expectations and instant gratifications.

Freedom from Debts

Clearing up this confusion underscores the significance of being debt-free as a true indication of financial health and prosperity.

Embracing a debt-free life is not merely about financial stability—it’s about the profound sense of freedom and the joy that comes with it.

Being free from debt is your ticket to robust retirement savings, potentially leading to an earlier and more comfortable retirement.

The ultimate luxury lies in this liberty; the contentment from knowing you live within your means, free from the shackles of debt. Achieving this might require discipline, setting clear goals, and a commitment to self-restraint, but the payoff is unparalleled.

If this vision inspires you, why not start that journey to financial independence today? Each step, no matter how small, moves you closer to realizing your dreams without the weight of debt steering your course.

Now, the time is for you to become the next millionaire with no money.

Source

Motley Fool. “Study: The Psychological Cost of Debt.” https://www.fool.com/the-ascent/research/study-psychological-cost-debt/. Accessed March 14, 2024.

Know someone else that needs this, too? Then, please share!!

Did the post resonate with you?

More importantly, did I answer the questions you have about this topic? Let me know in the comments if I can help in some other way!

Your comments are not just welcomed; they’re an integral part of our community. Let’s continue the conversation and explore how these ideas align with your journey towards Money Bliss.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

A lot has been written about whether now is the best time to buy stocks.

Many think that it is a good idea, and others are still skeptical. So which one should you believe?

This article will help answer the question once and for all with facts rather than opinions.

But first, let’s look at some statistics:

S&P 500 Total Returns for 2021 was 28.71% (source)

In the past 20 years (2003-2021), the S&P 500 was down three times. (source)

Over the 10 year period of 2011-2020, the S&P 500 averaged 13.9% (source)

With that said, will it be best to invest now?

Honestly, that is an answer no one can give you. And the movies about Wall Street won’t help you either.

However, you can learn to read charts become a technical analysis trader, and have a better idea of where the market is going.

The stock market is a volatile thing. It can go up or down at any time. As the statistics show, it goes up more often than down.

Is it Smart to Invest in Stocks?

The stock market is a great way to make money whether for income or for long-term investments. Plus it is a lot more accessible than you think.

With stocks on an upswing lately, it might be tempting to dive in. But do not get too excited just yet!

You must learn how to invest in stocks.

Are you ready to make money in the stock market? If so, learn the steps to start investing today.

In order to make educated decisions, it is crucial that you understand what makes stocks go up or down.

Since you might be asking yourself whether it is a good time to buy stocks after the market has been on such an upswing for several months. The answer is yes, but there are some important factors you should consider before handing over your money.

This article will discuss how the stock market works and provide you with reasons why now may not be a great time to invest in stocks as well as alternatives that could make sense for you if this is indeed a bad time to purchase them.

Read more!

What is the Stock Market?

The stock market is a system of securities, such as stocks and bonds, in which investors buy and sell ownership stakes to each other on various exchanges using money or their own businesses.

Simply put, the stock market is a place where people invest money.

There are many different ways to invest in the stock market, but one of the most popular ways is through buying stocks.

Investing in stocks is a commonly used way to make money.

In the stock market, people can buy and sell shares of companies they believe will rise in value. You can participate by investing in the stock market by buying individual shares of a company like AMZN (Amazon), investing in an ETF like VTI, or investing with a mutual fund, such as VTSAX.

One former assistant principal, Teri Ijeoma, changed her life when she left her job as an educator and become an active trader.

What does it mean when the stock market is up or down

When the stock market is up, it means that stocks have been doing well.

Conversely, when the stock market is down, it means that stocks are losing value.

You have heard the saying… buy low, sell high.

Stocks are an investment that you can purchase in order to make a profit, but the best time to buy stocks is when they are at their lowest price.

If you bought a stock for $100 and its value increased by 10%, then your stock would be worth $110. However, if you bought 20 stocks at $100 and the value increased by 10%, then your new value is $2,200. If you are trading options, then your return (and risk) is much greater.

When the market is up or down there are always going to be opportunities to make money from the stock market!

The hardest part for the novice investor is to determine when to buy and sell.

Thankfully, there is a great investing course to help you figure out how to invest in stocks and options.

Timing the Stock Market

Can you even time the stock market?

Many people are concerned with timing the stock market because of its volatility. Honestly, no one knows what the stock market will do.

As a technical stock trader, you will learn based on previous actions how the market and individual stocks may react.

When day traders or swing traders “time” the market, they are using time frames to make their predictions. Those traders who manage their risk and potential losses well will do better in the market.

For the average investor or someone going off a friend or Reddit recommendation, timing the market can be detrimental to your portfolio.

The real answer to the question, “Is now a good time to buy stocks?” is that there’s no such thing as an ideal moment. It could be a great time or it could also be terrible timing. There are too many variables and market risks which makes this decision very difficult for investors.

Too many times, investors fall into the trap of panic selling while stock prices are low and buying when stocks are high on the fear of missing out (FOMO).

That is why the common knowledge states don’t time the market.

However, I can tell you that you can time the market. If (and it is a big if) you are willing to put the time and effort into an investing education as you would going to college.

Many people have found success in timing the market.

Why investing is always a good idea

Remember earlier in this post, we stated the stock market has averaged 13.9% over the past 10 years and only had 3 negative years in the past twenty.

Simply put, that means you can make money, and investing is a good idea.

That is better than the flip side of your money sitting in the back earning slightly above 0% and when you account for inflation, your money is worthless.

The stock market is (almost) always following an upwards trajectory.

This means investors are more likely to experience gains in their investments than they would if the prices were going down. Moreover, it’s almost never a good idea to just let your money sit doing nothing for years on end because inflation will eventually force you into losing value at some point.

Instead of waiting until then and hoping for the best, focus on what you want instead of what the market is doing at any specific moment.

Must Read: How To Invest In Stocks For Beginners: Investing Made Easy

Is now a good time to invest?

This is the wrong question. The better question to ask would be “What is a good time to invest?”

It is not always a good time to invest. Before buying stocks, it is important that you do your research and have a clear purpose for investing in the first place. Once you know why you are investing, then it will be easier to answer when now might actually be a good time.

What are your goals for investing in stocks?

Are you looking to make extra money?

Do you enjoy learning about the fundamentals of your favorite companies?

Do you have the time to invest to learn about investing in stocks and executing trades?

The desire to increase your investment accounts and net worth appealing?

If you answered yes, then you are ready to start investing in stocks.

If you said no, then stick to consistently investing in EFTs or mutual funds. That is still a solid investing strategy!

The bottom line is whether you are ready to invest. The stock market will continue to do its thing whether you choose to participate or not.

Why does the stock market just keep going up?

The stock market has been steadily climbing for the long trend.

As a result, it’s important to be aware of the factors that influence how much you can profit from stocks. This includes understanding what drives stock prices and when these markets are likely to go up or down.

The reality is that there is no such thing as an “always” in investing — there will always be downturns at some point for any market, but those dips won’t last forever either.

As history proves, the stock market over time will keep going up.

Why has the stock market dropped?

This is the #1 reason why most people are terrified of investing in the stock market.

The fear of the stock market dropping and losing money. Or maybe they were burned in the previous market corrections in 2001 or 2008.

Typically, the stock market has dropped because of the following:

The global economy is going through a rough patch.

There is fear that the US may be headed for another recession.

The US is experiencing inflation that has caused the Federal Reserve to raise interest rates.

In other words, investors are uncertain about the future of the global economy and are afraid of a recession in the US, which will have a significant impact on the stock market.

Just remember, the S&P 500 has come back each time after posting a year or two of negative returns.

However, you can still make money as an investor when the market goes down! Learn how to ride that elevator up and down.

What are the best times to trade stocks?

Ask a few different investment gurus and you are likely to get a variety of answers such as:

It is best to trade stocks when the market is down and on a day with low volume. This way, you are less likely to be hit with volatility that could cause your profits to drop.

The best times to trade stocks are when the market is stable, meaning that there are few fluctuations in price. The most optimal time to enter and exit the market is during a period of low volatility.

The best time to trade stocks is when the market is at an all-time high. (very wrong idea, so don’t try this one)

Traders should try and stay away from markets when volatility or uncertainty is high.

It is important to understand the best times for trading stocks in order to maximize profits.

Overall, your trading plan will tell you the best time for you to trade stocks. Over time with practice in a simulated account, you will be aware of the best times for trading.

Your best times will be different than mine; they will vary for all of us and that is okay. We all view the stock market and read charts in our own way.

Best Stocks to Buy Right Now

What are the stocks to invest in right now? Should you buy stocks now?

Well, first of all, I am not an advisor telling you what to invest in. You are responsible for doing your due diligence.

The best stocks to buy are the stocks that you understand the best– YOUR Watchlist!

Typically, that means following 10 stock tickers and learning everything you can about how those stocks move.

Other investing gurus may tell you the best stock to buy is one that has a low price-to-earnings ratio. This is because the company has room for growth, and they are more than likely not overvalued in the market. They look for industries that are experiencing either a slowdown or an increase in competition.

Personally, I like to stick with strong, healthy companies to buy.

Many times the best stocks to buy right now are growth stocks, which have been very successful in 2021. These types of companies grow rapidly and offer significant returns on investment in a short period time frame.

What are the best stocks to buy now or put on a watchlist? These are the most popular stocks investors tend to follow:

Apple (Nasdaq: AAPL)

Advanced Microdevices (Nasdaq: AMD)

Amazon (Nasdaq: AMZN)

Meta / Facebook (Nasdaq: FB)

Nvidia (Nasdaq: NVDA)

Tesla (Nasdaq: TSLA)

More Best Stocks to Buy

When you invest in these stocks as an investor, it is important that you look for them during their good moments so that your investments will increase significantly over time and always have risk management strategies in place (BEFORE YOU ENTER THE TRADE).

Can You Afford to Buy Stocks?

There are a lot of factors that go into determining the best time for someone to begin investing or trading stocks.

The most important aspect is whether or not you have enough money at your disposal, which can be determined by your personal financial situation.

Other factors that may play a role in determining the best time to trade are whether or not the person trading has a specific investment objective, and if they have a time-sensitive need.

You need to know your long-term goals for buying stocks.

Are you buying stocks as a long-term investor or if you are buying stocks for income?

Either way, you need a solid idea of how to plan to manage your risk and maximize your profit. That is why investing in stocks is so enticing for so many traders.

Read Now: How Fast Can You Make Money in Stocks?

So, should you buy stocks now?

The current market conditions are a great time to buy or short-sell stocks.

However, there are many trading mistakes when investors place a trade.

Whether we are experiencing a bull run or heading into a bear market, there is always money to be made in the stock market. You should not question yourself is it time to buy stocks.

Regardless, you must invest the money in a solid investing education. That is non-negotiable.

If you want to go out and start buying stocks without investing knowledge, that is fine. Just do not complain if you lose more money than the only investing course I recommend. Check out my Trade and Travel review.

You must do your own due diligence when investing in stocks and finding a good time to buy stocks.

This is your investing journey!

Your journey will be different than my investing journey. That is okay because we each will find our niche and how we like to trade stocks.

Back to the original question, is now a good time to buy stocks?

Overall, you must look for the best companies to invest in. That will make you successful at investing.

Know someone else that needs this, too? Then, please share!!

Did the post resonate with you?

More importantly, did I answer the questions you have about this topic? Let me know in the comments if I can help in some other way!

Your comments are not just welcomed; they’re an integral part of our community. Let’s continue the conversation and explore how these ideas align with your journey towards Money Bliss.

This week’s Afford Anything blog post is a well-balanced diet:

Robert Kiyosaki predicts a massive crash — [philosophical]

Sobering stats about the housing market — [analytical]

Secret strategies to save on seasonal shopping — [practical]

The Robert Who Cried Wolf

Famed investor Robert Kiyosaki, author of Rich Dad, Poor Dad, recently caused an internet stir by predicting “the start of the biggest crash in history.”

Of course he did.

Kiyosaki is constantly crying wolf. It’s good for (his) business.

Bad news travels faster than good news.

People who prioritize attention over truth will use that to their advantage. Kiyosaki is a shrewd businessman. He understands the profit potential in strategic pessimism.

But that’s bad news for his followers. Per the law of large numbers, it’s reasonable that some people have kept their cash on the sidelines, rather than investing in the markets, after heeding his warnings. And that has massive lifelong ramifications on their wealth and retirement.

Lesson: Beware of anyone who peddles *negativity bias* in order to stay relevant.

These economic fear-mongerers don’t hold accountability for their track record of wrong predictions.

Their followers are the ones who suffer.

This is why it’s critical to choose your mentors carefully — and it’s precisely why you should never blindly enroll in an online class that’s taught by some random person whose ideas you haven’t vetted.

If you’re curious how often Kiyosaki has made the wrong call, note that Stanford-trained data scientist Nick Maggiulli, our guest on Episode 375 of the Afford Anything podcast, shared this illustration on X:

Imagine if you stayed on the sidelines …

Pessimism has a visceral appeal. It’s evolutionarily advantageous to be hyper-aware of threats.

Our ancestors didn’t survive the jungle or savanna by appreciating the beautiful flowers. They survived by staying hyper-vigiliant of danger. This explains why negativity bias is so innate, so intrinsic. It’s a survival mechanism.

But in the modern developed world, pessimism keeps us overly conservative. We choose the “safe” major. We take the “steady” job. We tilt too heavily into conservative investments when we’re young, and we panic when our 401k’s start to decline. We avoid real estate investing and starting side businesses because these seem too risky.

Pessimism stifles innovation, entrepreneurship, and creativity. It locks us into mundane careers and middling investments as we muddle through risk-averse lives. In the end, we haven’t endured huge losses, but neither have we *embraced a shot* of winning.

As Episode 284 podcast guest Morgan Housel eloquently said:

“Pessimists get to be right. Optimists get to be rich.”

No, The Fed Lowering Interest Rates by 25 Basis Points Is Not Going to Flood the Market with New Housing Inventory 🙄

A little history lesson:

Once upon a time, in 2008, there was a Great Recession. It scared many investors and homebuilders, and they stopped making new homes.

In the decade that followed the Great Recession, new construction reached its lowest point since the 1960’s.

By 2019, the housing shortage amounted to 3.8 million units. This means there were 3.8 million more families and individuals who wanted a place to live — either to rent or buy — than there were homes available.

Then the pandemic struck. The prices of copper, lumber and other construction items shot through the roof (no pun intended). Builders had to raise home sale prices due to higher materials costs. Prices soared.

In 2020 and 2021, people across the internet cried, “Why are they charging so much more than the home is worth?!” — not realizing that “worth” is a function of the cost of labor + the cost of materials + the premium of scarcity.

And when supply is curtailed — as it was by 3.8 million units as of 2019 — there’s an ample scarcity premium.

Then inflation climbed. The Federal Reserve raised interest rates 11 times during their 2022-2023 cycle, resulting in a rapid escalation of mortgage rates.

This created a “lock-in effect” among existing homeowners. Nobody wants to trade a mortgage with a 3 percent fixed interest rate for an alternate mortgage with a 7 percent rate.

Existing homeowners with a mortgage have a huge incentive to hold.

Sellers who *need* to get rid of their property — for example, because they’re moving to another country — list their homes on the market. But homeowners who simply *want* to upsize or downsize are, for the most part, staying put.

This has created even more housing supply pressure.

Meanwhile, homebuilders — who must borrow money to finance their operations — are seeing the cost of capital skyrocket. Many have curtailed new construction, putting further pressure on the supply pipeline.

So we have a long-running confluence of factors that, piece by piece, keep exacerbating the housing supply crunch.

And this leads to today’s takeaway:

No, this problem will not magically solve itself the moment that the Fed reduces interest rates.

The Fed is meeting today and tomorrow. They’re widely expected to hold rates steady. (They’ll make an official announcement at 2 pm on Wednesday.)

There’s rampant speculation that the Fed will lower interest rates in Q1 or Q2 of next year.

— And —

There seems to be a pervasive myth that once interest rates decline, those “locked-in” homeowners will rush to list their homes for sale, flooding the market with new inventory.

The supply-demand imbalance will tilt in the buyer’s favor, home prices will plummet, and housing will become affordable once again.

Yet that is pure fantasy, disconnected from the data.

Imagine 10 people. Nine of them have mortgage rates that are less than 6 percent. The stat is 91.8 percent of mortgaged homeowners, to be precise.

Wait.

Imagine those same 9 people, the 9 out of 10 who have a sub-6 percent interest rate. Here’s how they break down:

One has an interest rate between 5 to 6 percent.

Two have an interest rate between 4 to 5 percent.

Six have an interest rate below 4 percent. The exact stat is 62 percent.

Let me say that again:

Six out of 10 mortgaged homeowners have an interest rate that’s below 4 percent.

Meanwhile:

One-half of mortgaged homeowners (49 percent) say they’d consider listing their home only if interest rates fell below 4 percent, according to a Redfin survey conducted by Qualtrics.

So this myth that if the Fed lowers interest rates, the market will get flooded with new inventory? — That scenario isn’t likely to happen for a long, long, looooong time.

As of Dec 12, 2023, the current average 30-year fixed rate for a buyer with a 740-760 credit score is 7.4 percent. Multiple reductions in interest rates won’t begin to approach the sub-4 percent rates of yesteryear.

The “lock-in effect” will last for longer than you might expect.

Lesson:Don’t wait to buy a home based on speculation about the market. If you have both the money and desire to buy a home, DO IT NOW. Homes are likely going to get more expensive in the future, not less.

How to Not Flush AS MUCH Money Down the Toilet This Holiday Season

Yeah, I know.

The holiday season is custom-built for parting with your money. Every store is promoting sales, discounts, offers. Limited time only.

It’s scarcity on steroids.

Holiday deals tap into the part of our brain that says — “this deal is only available now; I should snag it while I still can.”

Our FOMO creates jobs and drives the economy.

Since holiday spending is human nature, let’s forgo the guilting, shaming and finger-wagging that’s so endemic to the personal finance and FIRE community.

It’s counterproductive. Guilt and shame over holiday spending doesn’t change human behavior, it merely robs the joy from it.

It’s like chowing down a piece of chocolate cake while simultaneously fretting about the sugar.

You’re eating the cake regardless. You may as well enjoy it.

Instead, let’s accept that some degree of holiday spending is normal, and let’s focus on how to find the best deal possible.

Here are four pointers. (If you have more to add, please share these with the Afford Anything community) —

#1: If you’re buying an item at a mid-size company’s website (i.e., a merchant that’s bigger than a mom-and-pop shop, but not a big box retailer like Target or Amazon) — move your cursor near the “back” arrow on the browser.

This is called “exit intent,” and it often triggers pop-ups with discount codes.

#2: For online purchases: Create an account, put an item in your cart, and then leave the website.

This is called “abandoned cart,” and often triggers an automation in which the company emails you a limited-time-offer discount code.

#3: If you’re buying something expensive (over $500 – $1,000 or more), track the price for a few weeks, especially around the holidays. On sites like Wayfair, I’ve seen prices fluctuate daily.

#4: The least useful savings tip: Googling discount / promo codes or pulling these codes from mass aggregator websites.

You may get lucky, but typically 9/10 are expired or don’t work; they just yield a bunch of extra open tabs on your browser.

There’s an enormous selection of third-party websites and browser extensions that claim to help with this, with varying degrees of efficacy.

I’m not going to recommend any specific tools; recommendations are both dynamic and better crowdsourced. Please share your experience with the community.

“Fear of missing out is just that — fear,” says licensed professional counselor Justin Kahn of Point Pleasant, New Jersey. However, in today’s society, this fear runs rampant with about 69 percent of millennials experiencing FOMO (fear of missing out) daily. To proactively combat feelings of FOMO as we head into the coldest nights and darkest days of the year, we asked eight experts to share their tips for fighting FOMO and seasonal blues with us.

1. Disconnect from social media

“One of my favorite tips for fighting FOMO — or at least reduce it — is to get off social media. If you are scrolling on social media and you feel competitive or experience jealousy, take a breath and put your phone down. Scrolling endlessly on your phone can lead to FOMO and anxiety. Do a social media cleanse and delete apps off your phone if they are causing anxiety,” says owner and holistic therapist Katie Ziskind, LMFT, RYT500 from Wisdom Within Counseling.

“It’s important to know there are events that you won’t be able to attend and that’s okay. As well, it’s OK to not get invited to all social events. Know that you won’t always be invited to everything and that’s OK, too.”

“Give yourself permission to let go and not over-commit. Know that if you do too much, you will feel out of balance. If you have FOMO, you might over-commit and try to do too much, you will be leaving yourself mentally and emotionally exhausted.”

2. Reframe your perspective

“Because we often focus on what everyone else is doing, we can forget that everyone also has a no list — the things they gave up because it didn’t matter as much as what they said yes to,” says Tiffany Rochester, a clinical psychologist from We’re On The Same Mountain. “You might miss out on an experience because you choose to prioritize staying within budget or being close to friends. Focus on what it is you decide to have rather than what you pass up.”

3. Practice mindfulness and gratitude

“FOMO may often be the result of a racing mind that is always craving for more and forgetting to notice what is truly important. I recommend these two tips for fighting FOMO,” says Archana Bahuguna, the founder of Pahoti Wellness.

“Try to slow down and remain mindful of who you are. If you like, you can practice a simple meditation practice like observing a lit candle’s natural light for a few minutes while breathing deeply and slowly.”

“Work on developing a gratitude practice. Pick your favorite writing utensil and jot down a list of all you are grateful for. This will help you remember all your blessings.”

4. Decorate your apartment

“In your apartment, always surround yourself with things that make you smile. Make sure to fill your apartment space and your personal life with safe, positive people who love you,” says certified life and business coach, Megan Smidt.

5. Get crafty

“Combat FOMO by staying creative and working with a craft that keeps your hands and mind busy,” says Maddie from CraftJam. “Activities like crochet, embroidery and watercolor help with anxiety and stress relief while helping you stay present (and off your phone)!”

6. Become your best friend

“Be your own bestie, plain and simple. You can never miss out if you’re having a good time — even if you’re alone. Whether you’re making spontaneous Target runs for apartment decorations, pampering yourself with a spa night or planning a scenic drive, there’s no limit to solo entertainment,” says the Just Girl Project.

7. Tune into the seasons

“The changes of seasons can impact mood and motivation. Make sure to maintain your exercise routines along with efforts to get outside,” says Main Street Counseling, “There are plenty of fall and winter activities that can help you cope with symptoms of seasonal depression, including hiking, biking, fishing, skiing, snowboarding and ice skating.”

8. Look to the light

“Seasonal affective disorder (SAD) is real. If the shorter days and longer nights affect your mood and wellbeing, remember — orient to the light,” says the Foundation for Positive Psychology.

“Try bringing color into your space, add new curtains with a fun print or cheerful color. Additionally, full-spectrum lights help bring more warmth and light into any space. Consider hanging up fairy lights — the way they brightly twinkle will reflect happiness into your space.”

“Remember, every winter solstice holiday is about preserving the light through the winter season as we and the earth sleep to emerge anew for spring. Always tend to your inner fire.”

Beat the winter blues

According to the Mayo Clinic, SAD is a type of depression that relates to the changing seasons. In fact, most people with SAD start experiencing symptoms around this time each fall — typically coinciding with Daylight Saving Time ending and continuing through the winter months. While about six percent of people experience winter depression, another 20 percent may experience mild SAD.

These are the most common signs and symptoms of SAD:

Feeling sad and depressed most of the time in a seasonal pattern

Low energy

Constant tiredness

Loss of interest in activities

Changes in appetite or weight

Sleeping too much

Sleeping too little

Difficulty concentrating

Feeling irritated, agitated or sluggish

Having frequent thoughts about death or suicide

If you’re experiencing these signs and symptoms, you don’t have to go through them alone. There are resources aplenty that offer confidential, free help:

Practice, practice, practice

Let’s get real, removing Instagram from your phone or taking up a new craft is often easier said than done. That being said, make sure to give yourself plenty of grace as you practice and apply these tips for fighting FOMO in your everyday life.

Charlsie Niemiec has spent the last 10 years working as a content marketing and social media editor and strategist. With in-house experience ranging from The Elf on the Shelf to CNN to Piedmont Healthcare, Charlsie has freelanced for the last four years with clients ranging from ESPN to the Atlanta Beltline. When she’s not copyediting or scrolling on Twitter, she is walking her very scruffy wirehaired terriers mixes Leonard and Biscuit or probably watering one of her 54 houseplants.

If you’re like most Americans, you love your plastic and swiping or tapping through your day. In fact, about 84% of Americans have at least one credit card, with the average wallet holding three.

The national love affair with credit cards is built on their convenience, how they provide a line of credit to enable buying things we can’t quite afford to pay for with cash, and those enticing rewards that are often offered.

But the picture is not altogether rosy: As a nation, US citizens have more than $1 trillion in credit card debt. And with interest rates averaging over 20%, that debt can be hard to chip away at.

To help you better understand how credit cards work, how much credit card debt people typically have, and what are smart strategies for paying down credit card debt, keep reading. You’ll learn interesting facts as well as helpful hints.

10 Facts About Credit Card Debt

Ready to learn more about credit card debt, a form of revolving debt? These 10 credit card facts will help you better understand who has how much debt and where difficulties paying the balance typically crop up.

1. More Than Half of Americans Have Outstanding Credit Card Debt

A majority of active credit card accounts carry a balance, according to the American Bankers Association. The specific figure is 56%. This indicates that carrying a balance is a common situation for many Americans, even with the eye-wateringly high interest that’s charged.

Recommended: Tips for Using a Credit Card Responsibly

2. Households with Credit Card Debt Owe an Average of Almost $8,000

American families had an average credit card balance of $7,951, according to calculations using Federal Reserve Bank of New York and US Census Bureau data. In 2013, that figure was $5,508.

Just because this is the norm, it doesn’t mean that it’s ideal: The best-case scenario is to only charge as much as you can afford to pay off in full every month. 💡 Quick Tip: A SoFi Credit Card provides access to a line of credit. It’s essentially a short-term loan that you repay each month.

3. It Can Take More Than a Decade to Pay Off $7,951 in Debt

Racking up credit card debt takes much less time than getting rid of it. Let’s assume that like the average American, you have $7,951 in credit card debt, as noted above.

At the current average interest rate of 21.19% on existing accounts, with a $150 monthly payment, it would take you 158 months — or 13 years and two months — to pay that off. And you would pay $15,606.40 in interest, or almost twice the original amount you charged!

But the more you can pay each month, the faster you’ll extinguish the debt. In this example, if you increase your monthly payment to $500, you’d pay off the debt in just a year and seven months and only spend $1,465.06 in interest. These scenarios are, however, assuming that you are not accruing new debt and therefore paying off larger credit card bills.

4. Gen Xers Have the Most Credit Card Debt

Ready for more credit card facts? Here is how age and debt intersect. Gen Xers, the generation that includes people born between 1965 and 1980, have the highest average credit card balance: $9,589. Next in line are Baby Boomers, born between 1946 and 1964, who have somewhat less debt — $8,192 on average — than Gen Xers.

5. Alaskans Have the Highest Credit Card Debt

In a state by state analysis of credit card debt, Alaska residents led the pack with $7,324 per person. Those who live in Wisconsin were found to have the lowest at $4,987.

6. 42% of College Students Have Credit Card Debt

The habit of carrying credit card debt unfortunately starts early, with more than four out of 10 college students carrying a balance on their credit cards. Of these, 28% say their debt exceeds $2,000. They say they accumulated that amount due to nonessential purchases, such as impulse buys, Uber rides, or fancy coffees. 💡 Quick Tip: To avoid paying interest, pay off your credit card bill in full and on time each month. Only making the minimum payment each month can lead to paying a lot in interest over time.

7. One in Three Americans Owes More On Credit Cards Than They Have Saved

This may be a scary fact about debt, but one in three US adults owes more on their credit card than they have saved. In fact, 36% say this is the case, versus just 22% a year earlier. That shows a two-sided problem: too much spending and too little saving.

Recommended: Paying Off $10,000 in Credit Card Debt

8. Richer People Have Credit Card Debt Longer

More interesting credit card debt facts: People who earn more than $100K a year are more than two times as likely as lower earners to have credit card debt for five years or longer. Among six-figure earners, 72% say they have had debt for at least a year vs. 53% of those who earn less than $50,000 per year. When considering those who’ve held credit card debt for five years or more, you’ll find that 27% of the high earners vs. 13% of the lower earners are in that situation.

Perhaps this statistic suggests that high-earners feel they have the means to handle debt and therefore don’t rush to repay it.

9. Men Have More Debt Than Women

Men have an average of $6,357 in credit card debt, while women have an average of $6,232. Perhaps not a huge difference, but so much for the myth of women shopaholics using credit cards to fill an overflowing closet with shoes.

There are many potential reasons for this difference, but some studies have found that women are less comfortable with debt.

10. There’s a Good Chance You’ll Die With Credit Card Debt

Here’s the last of these debt facts, and it can be a grim one: Nearly three-fourths of Americans are in debt when they die, according to one benchmark study.

And 68% die with credit credit card balances — more than the share who have mortgage debt (37%) or car loans (25%) when they pass away. That’s not exactly a desirable legacy. Although family members don’t generally become responsible for the debt, it may be taken out of the deceased person’s estate.

Why Is Credit Card Debt So Common?

There are many reasons that Americans have so much credit card debt, from rising healthcare and educational costs to lack of emergency savings to a cultural consumerism that encourages people to live beyond their means.

Regarding that last point, you may hear about the phenomenon referred to as Fear of Missing Out or FOMO spending, which is a modern version of “keeping up with the Joneses.” In other words, because your friends, coworkers, or influencers you follow on social media are buying something, you feel you should as well.

Or perhaps part of the problem can be explained by what is known as lifestyle creep. This situation occurs when you earn more money but your spending rises too, so your wealth doesn’t grow. For example, if you took a new, higher-paying job and decided to lease a luxury car or take a couple of lavish vacations, your wealth wouldn’t increase, though your credit card balance might.

Tips on Avoiding Credit Card Debt

Perhaps these facts about debt will motivate you to work on avoiding a credit card balance. If so, the following strategies could help.

• Review different budgeting methods, and find one that works for you. Many people use the popular 50/30/20 budget rule, for example. Also, see if your bank offers tracking and budgeting tools to help you rein in spending.

• Gamify savings. You might try sleeping on it rather than making impulse buys to see if the urge to spend passes; it often does. Or go on a spending freeze for a specific period of time or for a certain kind of purchase (say, no dining out in March; no clothing purchases in April).

• Try buying with cash or your debit card vs. plastic. That will help prevent your debt from snowballing.

• Consider trying a balance transfer card, which typically gives you a period of zero interest during which time you can pay down what you owe.

• In terms of a debt payoff strategy, you might investigate getting a personal loan with a lower rate than what your card charges. That could allow you to pay off the plastic debt and then have more manageable monthly payments.

• Seek help if you are really struggling to get your debt under control. Nonprofit organizations can help you accomplish this.

Opening a Credit Card With SoFi

Now that you know some facts about credit card debt and ways to pay it off, you may be looking for a new card that better suits your financial and personal goals. Shopping around to compare features, such as interest rates and rewards, can be a wise move.

Looking for a new credit card? Consider a rewards card that can make your money work for you. With the SoFi Credit Card, you earn cash-back rewards on all eligible purchases. You can then use those rewards for travel or to invest, save, or pay down eligible SoFi debt.

The SoFi Credit Card offers unlimited 2% cash back on all eligible purchases. There are no spending categories or reward caps to worry about.1

Take advantage of this offer by applying for a SoFi credit card today.

FAQ

What are the main causes of credit card debt?

Credit card debt can crop up in a variety of ways. Sometimes it’s because expenses get pricier, whether due to lifestyle creep or inflation. Other times, it’s not being mindful about daily spending and making impulse buys. Given how many Americans have more credit card debt than money saved, it’s a common but challenging issue.

How much does the average person have in credit card debt?

Credit card debt facts reveal different angles on this number. The average American household has $7,951 in credit card debt. Some studies put the individual figure at $,5,573.

How serious is credit card debt?

Credit card debt can be very serious. It’s high-interest debt, and it can be difficult to pay off. It can make it hard for individuals to save for their future and can negatively impact their debt to income ratio, which can be an issue when applying for loans.

The SoFi Credit Card is issued by SoFi Bank, N.A. pursuant to license by Mastercard® International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

1Members earn 2 rewards points for every dollar spent on purchases. No points will be earned with respect to reversed transactions, returned purchases, or other similar transactions. When you elect to redeem rewards points as cash deposited into your SoFi Checking and Savings account, as a statement credit to a SoFi Credit Card account, as fractional shares into your SoFi Invest account, or as a payment toward your SoFi Personal Loan or Student Loan Refinance, your rewards points will redeem at a rate of 1 cent per point. For more details please visit the Rewards page. Brokerage and Active investing products offered through SoFi Securities LLC, member FINRA/SIPC. SoFi Securities LLC is an affiliate of SoFi Bank, N.A.

1See Rewards Details at SoFi.com/card/rewards.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

A flexible expense is a non-essential item in your budget. Because it’s not a must-have, you can change the expense in question to help save money. For example, while the newest smartphone (with all kinds of amazing camera functions) might be enticing, purchasing it could add strain to your budget. Instead, you could continue using the phone you bought last year and not increase that expense. In this way, managing flexible expenses can be key to making a budget that helps you reach your financial goals.

Flexible expenses span many categories, from dining out to travel to self-care. These expenses are negotiable, meaning you can save money by reducing or changing how often you spend on these items and services.

Here’s how to distinguish flexible expenses from inflexible expenses and how to reduce your monthly costs on them.

What Is a Flexible Expense?

The definition of a flexible expense is an item in your budget that you can modify or adjust as needed. These are different from necessities with fixed costs, such as rent and health insurance.

In addition, it’s worth noting that a fluctuating bill is not necessarily a flexible expense. For instance, while you might turn the thermostat down a degree or two to be thrifty or the price of fuel might shift, heating your home during cold months isn’t a negotiable expense.

Flexible expenses are those you change to make room in your budget. These may at times be commonly forgotten monthly expenses, such as buying birthday gifts or loading up on toys for your pet, but they aren’t essential for life.

Therefore, you can change them if you want. Perhaps you realize something (boredom? FOMO?) has been a cause of overspending in a specific area, or maybe you want to start saving money for a financial goal, like the down payment on a house.

Flexible Expense Examples

Flexible expenses are daily or monthly expenses you can change or eliminate. Here are examples of items in your budget that have wiggle room:

• Vacations. You might decide against saving for a vacation in Mexico and instead have a staycation to free up some funds.

• Beauty treatments. Having your hair or nails done is an expense you could eliminate or pay for less frequently.

• Electronics. A new phone or tablet can be a nice upgrade, but, if the one you bought three years ago is in working order, replacing it is a flexible expense.

• Food. This is a good example of an expense that can be either a flexible or inflexible expense. Everyone has to eat, that’s a fact. But planning meals and saving money on groceries when you shop are examples of how you might manage the inflexible cost of feeding yourself. There is a range of how much you might pay, but you will have to pay something.

However, when it comes to how often you eat out, get fancy lattes on the go, and meet friends for drinks, those are flexible expenses you can cut (even entirely) to save money. Those expenses are likely to vary too; for instance, you might dine out more around holidays.

• Entertainment. How much you spend on streaming services and cable television isn’t a necessary expense. It’s a flexible one. Yes, this kind of entertainment can be fun and relaxing, but you could cut cable or limit yourself to one or two streaming services.

Ready for a Better Banking Experience?

Open a SoFi Checking and Savings Account and start earning up to 4.50% APY on your cash!

Recommended: 30 Fun and Affordable Hobbies

Flexible Expenses vs Inflexible Expenses

When you make a budget, inflexible expenses are the ones that are permanent and vital to daily life. For example, your mortgage, credit card minimum payments, and car loan costs are inflexible expenses. But, of course, they are flexible at a certain point. For instance, you could refinance your home to lower your mortgage payment or pay off a debt to get rid of it.

However, these require significant financial shifts and are more challenging to adjust to than your flexible expenses. As mentioned above, flexible expenses can reflect the wants vs. needs in life, or your discretionary spending. Flexible expenses can include dining out, deciding to upgrade your car or electronics, taking a vacation, purchasing gifts for others, paying to redecorate your home, joining a gym or yoga studio, and the like.

These are things many of us spend money on, but how much you spend and how often is under your control.

Flexible Expense Budgeting

Taking control of your flexible expenses can mean making a budget to manage your money and prevent overspending. One approach to take is the 50/30/20 budget rule. This popular system involves designating 50% of your income for essentials, such as housing and transportation, 30% for nonessential expenses, and saving the remaining 20%. Your flexible expenses will go into the 30% portion of the budget.

For example, say your monthly take-home pay is $5,000. Half your income ($2,500) goes towards your needs, and 30% ($1,500) is for flexible expenses. The remaining $1,000 gets put towards savings. So, your job is to make your non-essential expenses fit into the $1,500 portion of your budget.

That said, the 50/30/20 rule might not work for you, especially if more than half your income goes toward essentials. Not to worry: You can approach flexible expenses from another angle. Instead, you can take your bank and credit card statements from the past three months, identify the flexible expenses, and decide which ones you can cut from your budget or reduce. For instance, you might realize you’re spending $75 at coffee shops every month and decide to make your own coffee every morning.

Where Flexible Expenses Should Be Funded From

You can pay for flexible expenses by opening a checking account and using funds in it for those charges. For instance, you might have your cable bill linked to your bank account to make an automatic payment every month. You might tap a linked debit card when you shop for, say, some new shoes.

A credit card with rewards could also be a good way to pay for flexible expenses. Getting cash back on every purchase can be a good perk when paying for flexible expenses. For example, using specific credit cards for such major expenses as flights and hotels during a vacation can provide considerable rewards. However, you’ll want to be wary of carrying too much of a balance on your credit card since that’s typically high-interest debt that can be hard to pay off.

Also worth noting: If you have enough money in an emergency fund, that could be useful for specific flexible expenses, such as unexpected bills. Not things like taking a long weekend away, but perhaps paying for a car repair bill that you didn’t see coming.

Recommended: Reasons Why It’s So Hard to Save Money

The Takeaway

A flexible expense is one you can usually change at will to fit your budget or an expense that can pop up without warning. These irregular expenses usually reflect your spending habits, such as how often you’ve dined out or treated yourself to some new clothes or electronics. Recognizing and wrangling these flexible expenses can help you take control of your finances. Also, keeping some cash in an interest-bearing bank account can be one way to afford fluctuations in these expenses.

Interested in opening an online bank account? When you sign up for a SoFi Checking and Savings account with direct deposit, you’ll get a competitive annual percentage yield (APY), pay zero account fees, and enjoy an array of rewards, such as access to the Allpoint Network of 55,000+ fee-free ATMs globally. Qualifying accounts can even access their paycheck up to two days early.

Better banking is here with up to 4.50% APY on SoFi Checking and Savings.

FAQ

Is rent a flexible expense?

Because rent is a consistent monthly cost, it isn’t a flexible expense. This bill doesn’t fluctuate, and you’re usually only able to change it by moving somewhere else.

How do you budget for flexible expenses?

You can budget for flexible expenses with the 50/30/20 rule, where 50% of your income is for inflexible expenses and 30% of your income is for flexible expenses. The remaining 20% is for saving. This 30% provides a boundary in which you must fit paying for the nonessentials, like entertainment and travel.

What is an example of a flexible expense?

Flexible expense examples include a vacation and a meal out. Both are flexible expenses because they are nonessential expenses. You dictate the cost because you choose where you’ll go and what luxuries, treats, and events you’ll pay to partake in.

Do flexible expenses stay the same?

Flexible expenses regularly change based on your spending habits. For example, your choices regarding food and entertainment drive how much you’ll spend in these areas. You can change these habits weekly or monthly to adjust how much you’re spending, unlike rent or a car note.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with direct deposit activity can earn 4.50% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Direct Deposit means a deposit to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Direct Deposit”) via the Automated Clearing House (“ACH”) Network during a 30-day Evaluation Period (as defined below). Deposits that are not from an employer or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, do not constitute Direct Deposit activity. There is no minimum Direct Deposit amount required to qualify for the stated interest rate.

SoFi members with Qualifying Deposits can earn 4.50% APY on savings balances (including Vaults) and 0.50% APY on checking balances. Qualifying Deposits means one or more deposits that, in the aggregate, are equal to or greater than $5,000 to an account holder’s SoFi Checking and Savings account (“Qualifying Deposits”) during a 30-day Evaluation Period (as defined below). Qualifying Deposits only include those deposits from the following eligible sources: (i) ACH transfers, (ii) inbound wire transfers, (iii) peer-to-peer transfers (i.e., external transfers from PayPal, Venmo, etc. and internal peer-to-peer transfers from a SoFi account belonging to another account holder), (iv) check deposits, (v) instant funding to your SoFi Bank Debit Card, (vi) push payments to your SoFi Bank Debit Card, and (vii) cash deposits. Qualifying Deposits do not include: (i) transfers between an account holder’s Checking account, Savings account, and/or Vaults; (ii) interest payments; (iii) bonuses issued by SoFi Bank or its affiliates; or (iv) credits, reversals, and refunds from SoFi Bank, N.A. (“SoFi Bank”) or from a merchant.

SoFi Bank shall, in its sole discretion, assess each account holder’s Direct Deposit activity and Qualifying Deposits throughout each 30-Day Evaluation Period to determine the applicability of rates and may request additional documentation for verification of eligibility. The 30-Day Evaluation Period refers to the “Start Date” and “End Date” set forth on the APY Details page of your account, which comprises a period of 30 calendar days (the “30-Day Evaluation Period”). You can access the APY Details page at any time by logging into your SoFi account on the SoFi mobile app or SoFi website and selecting either (i) Banking > Savings > Current APY or (ii) Banking > Checking > Current APY. Upon receiving a Direct Deposit or $5,000 in Qualifying Deposits to your account, you will begin earning 4.50% APY on savings balances (including Vaults) and 0.50% on checking balances on or before the following calendar day. You will continue to earn these APYs for (i) the remainder of the current 30-Day Evaluation Period and through the end of the subsequent 30-Day Evaluation Period and (ii) any following 30-day Evaluation Periods during which SoFi Bank determines you to have Direct Deposit activity or $5,000 in Qualifying Deposits without interruption.

SoFi Bank reserves the right to grant a grace period to account holders following a change in Direct Deposit activity or Qualifying Deposits activity before adjusting rates. If SoFi Bank grants you a grace period, the dates for such grace period will be reflected on the APY Details page of your account. If SoFi Bank determines that you did not have Direct Deposit activity or $5,000 in Qualifying Deposits during the current 30-day Evaluation Period and, if applicable, the grace period, then you will begin earning the rates earned by account holders without either Direct Deposit or Qualifying Deposits until you have Direct Deposit activity or $5,000 in Qualifying Deposits in a subsequent 30-Day Evaluation Period. For the avoidance of doubt, an account holder with both Direct Deposit activity and Qualifying Deposits will earn the rates earned by account holders with Direct Deposit.

Members without either Direct Deposit activity or Qualifying Deposits, as determined by SoFi Bank, during a 30-Day Evaluation Period and, if applicable, the grace period, will earn 1.20% APY on savings balances (including Vaults) and 0.50% APY on checking balances.

Interest rates are variable and subject to change at any time. These rates are current as of 8/9/2023. There is no minimum balance requirement. Additional information can be found at http://www.sofi.com/legal/banking-rate-sheet..

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

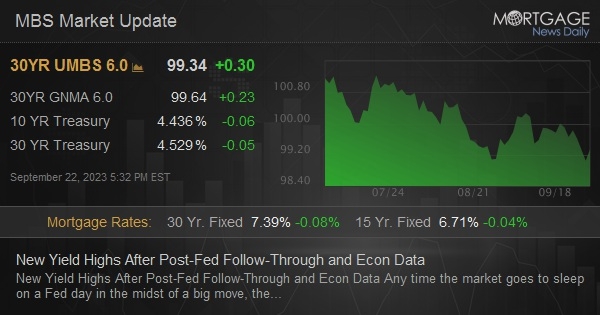

New Yield Highs After Post-Fed Follow-Through and Econ Data

By:

Matthew Graham

Thu, Sep 21 2023, 4:07 PM

New Yield Highs After Post-Fed Follow-Through and Econ Data

Any time the market goes to sleep on a Fed day in the midst of a big move, there’s a stronger than average possibility that overseas markets will add some momentum in the prevailing direction. That direction is “UP!” as far as rates and yields are concerned. The overseas FOMO selling brought yields to new long term highs overnight and a big beat in Jobless Claims made for another few bps of selling. After that, bonds managed to level off fairly well, but they may have benefited from the acceleration in stock selling.

Jobless Claims

201k vs 225k f’cast, 221k prev

Philly Fed

-13.5 vs -0.7 f’cast, 12 prev

Philly Fed Prices

25.7 vs 20.8 prev

08:34 AM

Much weaker overnight with additional selling after data. 10s up 8bps at 4.478. MBS down almost half a point.

12:52 PM

Calm trading since 9am with MBS down 7 ticks (.22) and 10yr up 7bps at 4.47%.

03:29 PM

Some illiquidity weighing on MBS but still generally flat. 6.0 coupons down roughly a quarter point. 10s up 7.9bps at 4.478

Download our mobile app to get alerts for MBS Commentary and streaming MBS and Treasury prices.

FOMO spending stands for “fear of missing out,” meaning you are dropping dollars to keep up with what others are doing. That might mean anything from trying the skincare product a favorite celeb swears by to dining at the super-pricey new omakase place all your friends are raving about or even signing your toddler up for an enrichment class because your neighbor says it’s a fab headstart.

The fear of missing out can change how many people relate to their cash. It can trigger impulsive and compulsive spending and lead to “splashing out” on things they never had any intention of purchasing. In other words, it can motivate them to live (too) large and wind up with pricey credit card debt and little progress towards their savings goals.

If you’re wondering how to stop FOMO spending, know this: It doesn’t mean subsisting on ramen and never traveling. It does mean being mindful and meaningful so you don’t get caught up in trying to match what your free-spending friends may do. Here, you’ll learn more about FOMO spending and how not to overdo it.

Wait, Back Up—What Is FOMO?

FOMO, or Fear Of Missing Out, is a feeling of anxiety someone might experience about not being part of an event that is happening, usually triggered these days by seeing social media posts from friends enjoying an activity (from a Taylor Swift concert to a holiday in Croatia) and wishing you were part of the fun. While it’s certainly true that businesses employ FOMO tactics to get you to buy things, it’s not just a sales strategy.

Nick Hobson Ph.D., says “While the fear of missing out has always been there, the explosion of social media has launched our young people headfirst into the FOMO experience.”

For many people, social media can be their main community lifeline, and having the impression that you are not part of the “in” group is enough to trigger a stress response like FOMO.

FOMO Spending Definition

So how is FOMO spending defined? It’s when a fear of missing out propels you to spend money (perhaps too much money) to feel as if you are part of the crowd and keeping up with your peers.

Examples could be feeling as if two far-flung vacations a year are must-haves because that’s what your coworkers do. Or perhaps it means plunking down four figures on a designer bag because all your friends have one. At a smaller scale, it could mean joining the other moms every morning after drop-off for a fancy latte. It’s all part of feeling as if you’re on the same level as your peers…and it all can add up.

💡 Quick Tip: Want to save more, spend smarter? Let your bank manage the basics. It’s surprisingly easy, and secure, when you open an online bank account.

FOMO Spending to Keep Up with Peers

How widespread is FOMO spending? One recent study found that almost 40% of more than 1,000 Americans ages 18 to 34 said they have gone into debt just to keep up with their friends’ lifestyles. This is FOMO taken the financial extreme.

People may try to overcome FOMO by spending more than they have on things like travel, clothes, food, and going out. Whether it’s bigger “once-in-a-lifetime” experiences you can’t miss out on like trips, music festivals, or weddings, or even smaller events like dinner and drinks, FOMO spending can impact your finances and ability to build wealth over time.

• FOMO spending often stems from peer pressure to buy something you can’t afford so that you can still participate in a group.

• It could stem from feelings of insecurity; you want to show others that you fit in and do so by spending more than you might otherwise.

Unfortunately, this can add up to extra spending, money stress, and debt.

Ready for a Better Banking Experience?

Open a SoFi Checking and Savings Account and start earning 1% APY on your cash!

How Many People FOMO Spend?

As noted above, one recent study found that 40% of people admit to FOMO spending. And those are the ones willing to admit to it. The figure could be considerably higher.

One study found almost twice that percentage of people admitted to going into debt to keep up with their friends’ spending. That’s a startling figure and shows just how common FOMO spending can be.

💡 Quick Tip: Your money deserves a higher rate. You earned it! Consider opening a high-yield checking account online and earn 0.50% APY.

4 Tips to Avoid FOMO Spending

Reining in FOMO spending can be hard, especially if your friends are truly living at a different income level than you. But odds are, some of your friend group might be in the same situation and are overspending in an effort to impress. You can avoid FOMO shopping or at least cut back on spending by trying these tips:

1. Suggest Free Alternatives

The first way to conquer FOMO spending is to simply stop spending! While it’s of course easier said than done, why not come up with a free alternative when a friend suggests plans?

Meeting for up for a $10 bubble tea at a cafe could just as easily turn into sitting on your couch with a homemade cup of joe. Friends want to go out to the movies or the mall? Suggest visiting a museum on a day they offer free admission instead.

2. Limit Your Card Usage and Carry Cash

Limiting your spending on credit or even debit cards and making the majority of your purchases with cash will drastically impact how often you impulse-spend on something when the feeling of FOMO creeps in.

If you only withdraw a certain amount before heading out to dinner or the bar, you’ll already have a pre-set budget that you know you feel comfortable spending. So maybe you only have one pricey cocktail or skip coffee and dessert: You can still have a great experience going out.

3. Create a Budget and Stick to It