Home prices are on the rise again, especially in large metro areas, after a lull leading into 2023. Seven cities, including Atlanta, Charlotte, Detroit, and Miami are at all-time highs as measured by the Case-Shiller U.S. National Home Price NSA Index. So saving for a down payment for your first house can be tough. This is especially true if you’re trying to buy that first home while you also have student loans to pay off. And if you’d like to purchase that home super fast before prices soar higher, it can feel impossible.

But here’s the good news: It’s definitely doable, even within just 12 months, if you accelerate your savings and prepare wisely. Follow our strategy below to take that big step into home ownership fast. 💡 Quick Tip: When house hunting, don’t forget to lock in your home mortgage loan rate so there are no surprises if your offer is accepted.

Months 1–3: Save Like You’ve Never Saved Before

Do the Math

The median home price in the U.S. in late 2023 was $431,000. Saving 10% for a down payment on a home at that price is far more manageable than following the old 20%-down school of thought, especially when you have student loans to pay off. To succeed at saving $43,100 in a year’s time, you’ll need to save $3,592 a month, which seems slightly more plausible if you take a breath and break it down into 52 weeks, at $829 a week. Of course, you’ll want to crunch the numbers for the type of home you’re looking to purchase. If you can find a well-priced property and put even less than 10% down, you may need significantly less cash on hand.

But don’t put your calculator away yet.

In addition to saving for the down payment, you’ll need to factor in closing costs, which typically amount to about 3% of the home price. So for a home that costs $431,000, you would need to add $249 to your weekly savings goal.

Yeah, that’s a big chunk of change. But don’t panic; the first step is always the hardest. Just imagine yourself landing your first job or hosting your first big party. You managed that and you’ll manage this too. And remember to consider student loan refinancing, which can help lower your interest rate, monthly payments, and ultimately save you money.

Revise Your Budget

Hunker down and take a hard look at your budget. If you’ve decided to refinance your student loans, don’t forget to adjust your monthly fixed expenses to account for your lower payments. Compare your income and expenses to get a clear view of your spending habits, and then make the necessary changes to meet your weekly savings goals.

Look closely at your expenses to see what you can give up to increase your savings, and what costs you can cut back on. Can you join a rideshare group to save on gas? Part with a streaming subscription or two? Also, consider setting limits on eating out and buying clothing or gadgets you don’t really need.

Recommended: Home Affordability Calculator

Flex your Negotiation Muscles

Put your savvy bargaining skills to use to get lower interest rates on existing credit cards and auto loans, or discounted rates on subscription services.

Start a Home Fund

Open a savings account just for your down payment, and avoid dipping into it. This will help you keep careful tabs on your progress.

Reach out to Your Family and Friends

Within your 12 months of saving, you’ll have a birthday and celebrate gift-giving holidays. Let your friends and family in on your major goal of buying a house, and ask that they contribute money toward a down payment in lieu of material presents.

Just remember that if you receive unusually large sums or a large number of deposits in the months leading to your home purchase, you may need gift letters from the generous people in your life, indicating that there is no expectation of repayment. Depending on the mortgage loan, rules vary when it comes to how much of your down payment can come from gifts.

Months 3–6: Keep Saving. And Focus on Earning More

Ramp up Your Income

Think of creative ways to use your expertise and skills to boost your income. You did invest a substantial amount of time and money in your education, after all, so maximize the ROI to rake in some extra cash to put toward your home fund.

Perhaps you can roll out an e-course or teach a professional seminar at your local community college. Or look for a way to make extra money from home. And, if the time is right, ask for a raise.

Months 7–9: Build Your Credit (and Keep Saving)

Review Your Credit Report

Check your credit report to make sure it is error-free and that your credit score is as high as it can be. And mind the cardinal rule of credit scores: Pay your credit cards, student loans, and bills on time.

Check your credit utilization ratio (the amount of your credit card balances against their limits), too; you want that number to be low.

Now is also the time to be wary of applying for new lines of credit, as that will result in lenders doing a “hard pull” on your credit. Too many of these within a 6-month time frame could ding your credit score.

Recommended: First-Time Homebuyer Guide

Keep an Eye on Your DTI

Make sure your debt-to-income ratio (DTI) is as low as possible. Your DTI is a key part of securing a home mortgage loan, and while the lower the better, it should fall below 36% — although for certain types of mortgage the DTI can be as high as 43%. 💡 Quick Tip: Don’t have a lot of cash on hand for a down payment? The minimum down payment for an FHA mortgage loan is as low as 3.5%.

Months 10–12: Learn About the Mortgage Process (While You Keep Saving)

Do Your Mortgage Application Prep

Your mortgage company will require quite a bit of paperwork to get your loan approved. Familiarize yourself with the mortgage loan application process. Also check your credit score once more to make sure it’s still solid.

Explore Homebuyer Assistance Programs

There are many different programs designed to help first-time homebuyers gain access to home ownership. A loan from the Federal Housing Administration, for example, may help you purchase a home even if you haven’t saved a heap of cash for a down payment or if your credit score isn’t at the highest level.

If a fixer-upper is your goal, a HUD loan may be worth exploring. And depending on where you’re looking to buy, you might find city- or state-specific homebuyers assistance programs.

The Takeaway

Saving for a down payment and the associated costs of buying a home is a big endeavor, but with persistence and discipline, both in terms of your spending and your home-search process, you can find a home and have the down payment necessary to purchase it. The same careful planning that got you to college and helped you secure a student loan will help you achieve your dream of becoming a homeowner.

Looking for an affordable option for a home mortgage loan? SoFi can help: We offer low down payments (as little as 3% – 5%*) with our competitive and flexible home mortgage loans. Plus, applying is extra convenient: It’s online, with access to one-on-one help.

SoFi Mortgages: simple, smart, and so affordable.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

SoFi Mortgages Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility for more information.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

¹FHA loans are subject to unique terms and conditions established by FHA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. FHA loans require an Upfront Mortgage Insurance Premium (UFMIP), which may be financed or paid at closing, in addition to monthly Mortgage Insurance Premiums (MIP). Maximum loan amounts vary by county. The minimum FHA mortgage down payment is 3.5% for those who qualify financially for a primary purchase. SoFi is not affiliated with any government agency.

It’s not uncommon to hit a moment in your financial life when you could use some cash…like, right away. Maybe you have a slew of unexpected expenses, get laid off, or need to help a loved one in need. Whatever the case, you may be craving a quick cash infusion.

To help out, here’s a list of 23 ways to get some money flowing your way ASAP. Some are online methods, others are in-person, but all can help you out when you are in a pinch.

Read on to see which of these ideas may suit you, plus tips on staying safe as you go after those additional funds.

When You Need Quick Cash

Many people hit a time when they could really use some additional cash. Perhaps you moved to a new town and need to put down a security deposit on a rental as well as pay your movers. Or you are a freelancer, and one of your clients is slow to pay. Or you need pricey dental work which isn’t fully covered by your health insurance. Or perhaps you just went overboard on holiday gift buying, and now your credit card bill is due.

Whatever the reason, if you need to get money fast and don’t want to break out your high-interest plastic to see you through, don’t panic. There can be an array of ways to bring in cash quickly. Some are online (taking marketing surveys), some are in person (dog walking), but there is likely to be at least a couple that suit your preferences and your situation.

💡 Quick Tip: An online bank account with SoFi can help your money earn more — up to 4.60% APY, with no minimum balance required.

Online vs Offline Money-Making Opportunities

As you look into ideas for how to get money fast, one key consideration is whether you want to do so online or offline. Perhaps both ways suit you, but many people have a preference.

If you have a job, are caring for dependents, or otherwise are under time constraints, you may prefer to squeeze in your money-making activities here and there. Online opportunities may suit you well, since some are available 24/7. For example, you could upload items you want to sell on eBay at any hour.

For others, offline work is more suitable. If, say, you are a brilliant guitar player and have a knack for sharing your skills, music lessons could be a good path, and you might find doing these in person more rewarding than via Zoom. Or holding a yard sale and selling off unwanted stuff could bring in a good amount of cash quickly.

Making Money Online

To help you scope out opportunities, consider this list of online ways to make quick cash.

1. Take Online Surveys and Market Research

From the privacy of your home, at your convenience, you could be earning small amounts of money (which can add up) by taking online surveys, watching videos, or even sharing your search history. These typically help marketers gain insight into consumer behavior and opinions Some places to sign up: Branded Surveys, Inbox Dollars, and Survey Junkie sites.

2. Sign Up for Freelancing Platforms

Do you have a skill to share…and sell? You might be able to offer your writing, social media, web design, translation, or other talents on a platform like Upwork, and get paid for freelance gigs. This can be an especially good way to make money even with no job.

3. Sell Products on E-Commerce Websites

If you are artsy or craftsy, you might try posting your work for sale online. Whether you make necklaces, take great nature photos, or knit beautiful baby sweaters, Etsy is a popular option. Just keep in mind that e-commerce websites typically have posting fees and then take a cut of your sales.

4. Offer Online Tutoring and Courses

You might be able to make quick cash by teaching online. Did you score in the top percentile on a standardized test or ace high-school physics? Are you pretty much fluent in French, or can you make bake-off-worthy cakes? You might be able to do remote tutoring or offer a class online. The key to bringing in quick cash here will be marketing your services well, so do a little online research upfront about how to bring an audience your way.

5. Try Affiliate Marketing

Do you love social media and have a strong presence, whether as a gamer, sharer of clothing hauls, or a guide to neighborhood businesses? If so, you could make quick cash via affiliate marketing. This means that you earn a commission on every visit, sale, or sign-up that you generate for a brand or merchant. You can learn more at affiliate marketing sites such as SemRush.

6. Find Unclaimed Money

Did you know that unclaimed funds, whether from forgotten-about bank accounts or insurance benefit checks that were never cashed, can wind up with the state government and sit, waiting to be claimed? It may be a bit of a longshot, but it can’t hurt to check out this unclaimed funds website and see if there is any cash in your name that you might collect.

7. Claim App Referrals

You may be used to those “Refer a friend and get $25!” offers online. If the shoe fits, as they say, wear it! For instance, if a buddy signs up for a PayPal or a Swagbucks account at your recommendation, you could benefit with a small chunk of change heading your way as a thank you.

8. Open a Bank Account

The personal finance business can be competitive these days, and some banks will offer you a tidy sum to open an account with them. This is among the more common bank bonuses, and while amounts will vary, you could earn a quick $250 this way. These offers are often at online vs. traditional banks. Just be sure to read the fine print before you sign up to make sure that there aren’t fees or minimum balances that would be challenging for you.

9. Sell Unused Gift Cards

Here’s a slightly weird way to make money. Do you have a gift card or two, maybe sent by a well-intentioned relative, sitting unused? Perhaps you never go to the coffee chain the card is for, or you don’t have a branch of the store nearby. You might recoup some of the card’s value by selling it on a site like CardCash, ClipKard, or GiftCash.

10. Get Paid Sooner

Need more ideas for how to make quick cash? This one doesn’t exactly bring in more money but can give you access to your earnings sooner. Some financial institutions will make your paycheck available up to 48 hours early when you sign up with direct deposit. Again, this isn’t a sum beyond what you earn, but it can let you, for instance, pay bills on time when you otherwise couldn’t.

11. Work as a Virtual Assistant

In this age of automation, many jobs can be done remotely as long as you have computer and wifi access. That includes being someone’s assistant and helping with tasks like scheduling, correspondence, and travel arrangements. Look for listings on sites like FlexJobs and LinkedIn.

💡 Quick Tip: If your checking account doesn’t offer decent rates, why not apply for an online checking account with SoFi to earn 0.50% APY. That’s 7x the national checking account average.

Making Money Offline

Need more inspiration on how to make quick cash? There are plenty of ways to do so in the real world instead of online. Here is an assortment of ideas for getting some money into your bank account, where it’s needed most.

12. Do Local Odd Jobs and Gigs

Are there any services, whether one-off or ongoing, that you could offer? You might be able to help a senior with shopping, do yard work, assist someone with cleaning out their basement before they move, or set up for a party. Take a look at sites like Fiverr, Craigslist, or Nextdoor, as well as locations like community bulletin boards at cafes and other locations.

13. Sell Unused or Unwanted Items

Your junk could be someone else’s treasure that they might be willing to pay for. You could have a yard sale or visit one of the many places to sell your stuff. Items that could be sale-worthy include good condition electronics, cookware, clothing, sports equipment, housewares, home decor, your vinyl collection, and more.

14. Pet Sit or Walk Dogs

Here’s another idea for how to make quick cash, and it’s perfect for animal lovers: Do some pet sitting or dog walking. Using a well-known social networking site or a pet sitting site could help get attention and build the business; you might also try posting flyers in your neighborhood offering dog-walking services. Cash payments can make this a good gig for those who don’t want to wait for their money.

15. Tutor or Skill Share

As mentioned above, if you have a skill or talent (from speaking great Spanish to coding), you could tutor or offer instruction. Local schools and community centers could be a good place to market your skills; think about what credentials you can tout to show prospective students that you have the know-how.

16. Recycle for Cash

In this era of eco-consciousness, there are plenty of opportunities to recycle for cash. This can be as simple as gathering your own and your neighbors’ unwanted cans and bottles and redeeming them, or you might get scrap metal via Craigslist or Freecycle and then sell it to a scrap yard. And who knew? You might even earn quick cash via recycling cardboard at BoxCycle.

17. Take Care of Children or Elders

Could you do some babysitting, childcare, or eldercare to bring in cash? You’re likely to have some warm and fuzzy feelings too after doing gigs like these and helping others. Caregivers may have to go through an in-depth vetting process to sign up with an agency like Care.com, so be prepared to answer lots of questions (Do you have experience? What would you do in an emergency? Will you cook and clean?) and provide background information and ID.

18. Pawn Items of Value

Let’s say you have an urgent car repair bill and unfortunately haven’t got enough saved in an emergency fund. You could get cash quick by pawning an item (think jewelry, wristwatches, electronics, and musical instruments). This means you take it to a pawn shop, get cash, and if you come back and repay the loan in a certain time frame, you retake possession of the item. If you don’t, the pawn shop can sell it. This practice could benefit you when you need money fast.

19. Rent Out Extra Space

You’ve probably heard about the sharing economy, which can allow people to monetize their unused space. For instance, if you live in a popular area and have an extra bedroom, you might rent it out on Airbnb to people visiting your town for a few nights. You may even be able to rent out your unused parking space on Spacer.

20. Deliver Food

It’s a sign of the times: Food delivery, from groceries to restaurant meals to bubble teas, is on the rise. You might be able to make some fast money by doing this kind of delivery via a service like DoorDash, UberEats, InstaCart, and GrubHub, among others. This can be a good way to use your free time to bring in some cash when you need it quickly.

21. Drive Rideshare

Similarly, if you have access to a car, you could drive a rideshare for a company like Uber or Lyft. Whether ferrying people to the airport, work, or out to dinner, it can be a good way to monetize your free time.

22. Flip Free Items

Are you handy? Here’s a way to get some money flowing your way: You could snag items from Freecycle, Craigslist, Nextdoor, or even the curb, and refurbish and sell them as a low-cost side hustle. Maybe someone is getting rid of an old coffee table or nightstand that’s in rough shape. You could refinish or paint it and sell it at a profit. Yes, it takes a bit of time to do this work, but the opportunity to bring in perhaps a couple of hundred dollars for your effort is real.

23. Cash in Your Coins

Here’s an easy idea for making quick cash: Look around your house for that coin jar that many people have shoved in a closet or on a windowsill. If you have a stash of quarters somewhere, you might be surprised by how much it can add up to. Getting it to the bank or a retailer that offers coin counting and redemption services could bring you a good infusion of cash.

Combining Online and Offline Opportunities

Now that you’ve read this list, you can begin to think about which ideas spark the most interest or best suit your situation. When you want to make quick cash, you don’t have to try just one method.

Feel free to mix up online and offline techniques to make money fast. You might drive a rideshare on Sundays and tutor via Zoom twice a week. It’s all about what works best for you.

Balancing Your Time

One thing to remember as you work to bring in extra cash is that it is possible to overdo it. Whether you have a job and/or a family or are unemployed and single (or anything in between), remember that you do need downtime and rest. Don’t overschedule yourself with odd jobs and other money-making tasks. You need to balance your time. And if you are sleep-deprived and exhausted, you can’t do a good job making money anyway!

Tips for Staying Safe While Making Quick Cash

A word or two of warning as you look for ways to make quick cash: There are occasionally scams and dangerous situations out there. Be savvy as you move ahead.

Avoiding Scams

If an opportunity to make money sounds too good to be true, it probably is. There are quite a number of employment scams out there, so be vigilant. Work-from-home scams and overpayment scams are common; check out Fraud.org’s site to learn more and protect yourself.

When selling items, also proceed with caution. There are also fraudsters using overpayment and money order trickery to get something for nothing.

Managing Personal Information

If you are applying for gig work, be cautious about to whom you send your personal information (such as your Social Security number and banking details). Do your research and vet the recipient of this info; otherwise, you might be dealing with a scammer who is trying to commit identity theft.

The Takeaway

Many people encounter a moment when they could really use some cash quickly. Happily, there are many ways to get money flowing your way, both online and offline. From dog walking to selling your unwanted stuff, from tutoring to taking surveys on your laptop, there are likely several options that can suit your needs.

And once you make that extra moolah, make sure it’s working hard for you and earning you some interest, thanks to a good banking partner.

Interested in opening an online bank account? When you sign up for a SoFi Checking and Savings account with direct deposit, you’ll get a competitive annual percentage yield (APY), pay zero account fees, and enjoy an array of rewards, such as access to the Allpoint Network of 55,000+ fee-free ATMs globally. Qualifying accounts can even access their paycheck up to two days early.

Better banking is here with up to 4.60% APY on SoFi Checking and Savings.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with direct deposit activity can earn 4.60% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Direct Deposit means a deposit to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Direct Deposit”) via the Automated Clearing House (“ACH”) Network during a 30-day Evaluation Period (as defined below). Deposits that are not from an employer or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, do not constitute Direct Deposit activity. There is no minimum Direct Deposit amount required to qualify for the stated interest rate.

SoFi members with Qualifying Deposits can earn 4.60% APY on savings balances (including Vaults) and 0.50% APY on checking balances. Qualifying Deposits means one or more deposits that, in the aggregate, are equal to or greater than $5,000 to an account holder’s SoFi Checking and Savings account (“Qualifying Deposits”) during a 30-day Evaluation Period (as defined below). Qualifying Deposits only include those deposits from the following eligible sources: (i) ACH transfers, (ii) inbound wire transfers, (iii) peer-to-peer transfers (i.e., external transfers from PayPal, Venmo, etc. and internal peer-to-peer transfers from a SoFi account belonging to another account holder), (iv) check deposits, (v) instant funding to your SoFi Bank Debit Card, (vi) push payments to your SoFi Bank Debit Card, and (vii) cash deposits. Qualifying Deposits do not include: (i) transfers between an account holder’s Checking account, Savings account, and/or Vaults; (ii) interest payments; (iii) bonuses issued by SoFi Bank or its affiliates; or (iv) credits, reversals, and refunds from SoFi Bank, N.A. (“SoFi Bank”) or from a merchant.

SoFi Bank shall, in its sole discretion, assess each account holder’s Direct Deposit activity and Qualifying Deposits throughout each 30-Day Evaluation Period to determine the applicability of rates and may request additional documentation for verification of eligibility. The 30-Day Evaluation Period refers to the “Start Date” and “End Date” set forth on the APY Details page of your account, which comprises a period of 30 calendar days (the “30-Day Evaluation Period”). You can access the APY Details page at any time by logging into your SoFi account on the SoFi mobile app or SoFi website and selecting either (i) Banking > Savings > Current APY or (ii) Banking > Checking > Current APY. Upon receiving a Direct Deposit or $5,000 in Qualifying Deposits to your account, you will begin earning 4.60% APY on savings balances (including Vaults) and 0.50% on checking balances on or before the following calendar day. You will continue to earn these APYs for (i) the remainder of the current 30-Day Evaluation Period and through the end of the subsequent 30-Day Evaluation Period and (ii) any following 30-day Evaluation Periods during which SoFi Bank determines you to have Direct Deposit activity or $5,000 in Qualifying Deposits without interruption.

SoFi Bank reserves the right to grant a grace period to account holders following a change in Direct Deposit activity or Qualifying Deposits activity before adjusting rates. If SoFi Bank grants you a grace period, the dates for such grace period will be reflected on the APY Details page of your account. If SoFi Bank determines that you did not have Direct Deposit activity or $5,000 in Qualifying Deposits during the current 30-day Evaluation Period and, if applicable, the grace period, then you will begin earning the rates earned by account holders without either Direct Deposit or Qualifying Deposits until you have Direct Deposit activity or $5,000 in Qualifying Deposits in a subsequent 30-Day Evaluation Period. For the avoidance of doubt, an account holder with both Direct Deposit activity and Qualifying Deposits will earn the rates earned by account holders with Direct Deposit.

Members without either Direct Deposit activity or Qualifying Deposits, as determined by SoFi Bank, during a 30-Day Evaluation Period and, if applicable, the grace period, will earn 1.20% APY on savings balances (including Vaults) and 0.50% APY on checking balances.

Interest rates are variable and subject to change at any time. These rates are current as of 10/24/2023. There is no minimum balance requirement. Additional information can be found at http://www.sofi.com/legal/banking-rate-sheet..

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

When you buy through links in this article, we may earn an affiliate commission.

In the digital age, the concept of home is being reimagined by the advent of smart technology, transforming everyday living spaces into hubs of convenience, comfort and entertainment. Never has this been so clear as when you take even a cursory tour of the HGTV Smart Home 2023. If you need further evidence of just how expansive this industry is becoming, a study by Grand View Research, Inc. determined that the home automation industry will reach a staggering $444.98 billion by 2030.

Smart home technology, once fodder for dystopian storylines on TV, has evolved into a widely accepted seamless integration of devices and systems that streamline tasks, enhance security and personalize our environment. From the moment you wake to the soft glow of a sunrise simulation to the reassuring click of a smart lock securing your home at night, these intelligent systems work collaboratively to simplify routines, conserve resources and provide peace of mind. Smart home devices not only respond to our immediate commands but also anticipate our needs, learn our preferences and adapt to our lifestyles, offering a bespoke living experience that was once the stuff of science fiction.

Image Source: HGTV

Noteworthy tech in the HGTV Smart Home 2023

Each year, HGTV builds a new, technologically advanced home in a different location within the United States. The contest is typically run as a sweepstakes, where viewers can enter for a chance to win the annual smart home. Entries are usually accepted online through the HGTV website or via mail. The main prize is, of course, the HGTV Smart Home itself, which includes the home, all of its furnishings and the latest home technology. In addition to the home, there are often other prizes, like cash awards or vehicles.

Coolest devices in the 2023 HGTV Smart Home

Laid out below are just a few of the most highly sought-after pieces of smart home tech in this year’s HGTV Smart Home 2023 and their less expensive counterparts.

GE Profile Kitchen hub

The GE Profile Kitchen Hub is a unique and high-tech kitchen appliance from General Electric. It’s designed to serve multiple functions and is geared towards making the kitchen experience more interactive and connected.

Interactive screen: The GE Profile Kitchen Hub features a large touchscreen display that can be used to access recipes, watch videos, control smart home devices and more.

Vent hood: The screen is built into a vent hood, allowing it to sit above your range or cooktop. This design not only provides essential ventilation but also offers a central view for following recipes or watching videos as you cook.

Cameras: The device includes front-facing and downward-facing cameras. The front-facing camera can be used for video calls, while the downward-facing camera is intended to capture your cooking, which can be useful for sharing your culinary adventures on social media or with family.

Integrated apps: The Kitchen Hub comes with a suite of applications designed for the kitchen. These can include recipe apps, music and video streaming services and other smart home integrations.

Connectivity: Being a smart device, the Kitchen Hub connects to your home’s Wi-Fi network. This allows it to pull up recipes, stream content and interact with other smart devices in your home.

U+ Connect: This is GE Appliances’ smart platform that allows various devices to connect and communicate. For example, if you have a GE oven, the Kitchen Hub can interact with it, setting temperatures, timers and more.

Not looking to shell out nearly $1,200 for this type of tech? Consider an Alexa. While not as advanced as the Kitchen Hub, it is still a solid virtual assistant option for the kitchen.

DAKboard Wall Display v2 Plus

DAKboard is a digital wall calendar that integrates with various online calendar services to display your events, tasks, weather and other custom information. The DAKboard Wall Display v2 Plus is one of their products, designed to be a versatile, visually appealing display for personal and professional environments.

Screen: The Wall Display v2 Plus includes a high-resolution screen designed to make texts and images clear and easy to read from a distance.

Customization: DAKboard is known for its highly customizable displays. Users can choose different layouts, fonts and color themes to match their preferences or interior design.

Connectivity: The device connects to Wi-Fi to sync with various online services like Google Calendar, Apple Calendar, Microsoft Outlook and others.

Photo display: Besides showing calendar and weather information, DAKboard devices can cycle through personal photos or artwork, making them a dynamic alternative to traditional picture frames.

Integration: DAKboard devices support integration with various third-party services for weather, to-do lists, news and more.

While the Dakboard Wall Display v2 Plus will run you close to $500, the Skylight Calendar is a solid replacement for around to $200 less.

Image Source: Samsung

Samsung AirDresser Grand

The Samsung AirDresser is an in-home garment refreshing system, which uses air and steam to clean and deodorize clothing. It is part of a new category of home appliances intended to reduce the frequency of traditional washing and dry cleaning.

Jet air and air hangers: The system blasts air to loosen and remove dust from inside and outside your clothes.

Steam cleaning: It uses steam to sanitize clothing, removing bacteria, viruses and allergens.

Deodorization filter: The filter captures and reduces odors, leaving clothes smelling fresh.

Gentle drying: Clothes are dried at a low temperature to reduce the risk of shrinkage and heat damage.

Smart control: Integration with Samsung’s SmartThings ecosystem to monitor and control the device remotely through a smartphone app.

Self-cleaning: An internal system helps to maintain the device by removing scale and residue.

Wrinkle care: The AirDresser can smooth out wrinkles without the need for ironing.

Capacity and design: The AirDresser Grand offers a larger capacity to accommodate more items of clothing and potentially an updated design or premium finish.

Not nearly as fancy as the $1,100 AirDresser Grand, a handheld steamer, like the Conair Turbo EstremeSteam is a great option for quick sanitization and keeping clothes wrinkle-free with ease.

SimpliSafe Wireless Home Security System

SimpliSafe is a company that offers a variety of home security products and services, with an emphasis on ease of installation and use. Their systems are known for being wireless and user-friendly. These systems are typically marketed toward homeowners and renters looking for a quick, easy and effective DIY security solution.

DIY installation: SimpliSafe systems are designed for easy setup without the need for professional installation. The devices can be placed on shelves or adhered to walls without drilling.

Variety of packages: SimpliSafe provides different equipment packages to suit various home sizes and security needs. You can start with a basic set and expand with additional sensors and accessories as needed.

Components: A typical SimpliSafe kit includes a base station, which is the central hub of the system, wireless door and window sensors, motion detectors and a keypad. Additional components might include glass break sensors, smoke detectors, carbon monoxide detectors and panic buttons.

No contract monitoring: SimpliSafe offers optional professional monitoring services on a month-to-month basis, without the need for long-term contracts. This professional monitoring can dispatch emergency services in case of a break-in, fire or other incidents.

Smartphone control: SimpliSafe has an app that allows you to arm and disarm your system, receive alerts and monitor your home from anywhere.

Integration: SimpliSafe systems can integrate with smart home devices and platforms, like Amazon Alexa and Google Assistant, allowing for voice control and other smart home automation.

SimpliCam: They offer an indoor camera called SimpliCam, which can be used to keep an eye on your home while you’re away. It comes with features like motion alerts and the ability to stream live video.

Design: SimpliSafe sensors and devices have a discreet and modern design to blend in with home decor.

Battery and cellular backup: The system is equipped with battery backup to keep your home secure during a power outage, and the professional monitoring service includes cellular backup to maintain communication with the monitoring center if the Wi-Fi goes down.

Environmental protection: SimpliSafe also offers sensors that detect water leaks and freezing temperatures to help prevent environmental damage in your home.

Privacy protection: Features like camera shutters allow customers to control their privacy.

While the Simplisafe wireless home security system is great, it does come at a price, of about $320. If you’re looking to spend a little less, don’t fret, Amazon is full of more affordable DIY wireless security systems.

Moxie Showerhead and Wireless Speaker

The Moxie Showerhead and Wireless Speaker is a product by Kohler, known for combining the functionality of a showerhead with the entertainment feature of a wireless speaker.

Showerhead: It’s designed to provide a full-coverage spray, offering a quality shower experience with good water pressure.

Removable wireless speaker: The center of the showerhead houses a wireless speaker that can be easily detached and used independently. The speaker connects to devices via Bluetooth to play music, podcasts or other audio streams.

Water-resistant: The speaker is designed to be water-resistant, which is essential for any electronic device used in a shower.

Rechargeable battery: The speaker has a built-in rechargeable battery. When fully charged, it supports several hours of playtime.

Magnetic docking: The speaker is held in place with magnets, which makes it simple to detach and reattach to the showerhead.

Harman Kardon sound: Some versions of the Moxie speaker are engineered with sound by Harman Kardon, delivering a high-quality audio experience.

Voice assistant compatibility: Depending on the model, the speaker can sometimes be compatible with voice assistants, which would allow you to control music and other functions with voice commands.

Multiple colors and finishes: The Moxie showerhead may come in a variety of colors and finishes to match different bathroom decors.

Installation: It’s designed to be easy to install, fitting onto a standard shower arm.

For those who enjoy listening to music or podcasts in the shower, the Moxie Showerhead and Wireless Speaker system brings convenience and a bit of luxury to the everyday routine. If you’re looking for the same luxury at a more affordable price, you’re in luck. There are plenty of showerhead speaker combos at all price points on Amazon.

Image Source: Kohler

Anthem Digital Shower Control

The Anthem Digital Shower Control is another Kohler product that provides a high level of personalization and precision for the showering experience. It is designed to provide a user-friendly interface to control various aspects of the shower.

Digital interface: The Anthem Control includes a minimalist display with easy-to-read buttons.

Customizable settings: Users can save their preferred shower settings, making it easy to start the shower with their personalized preferences at the touch of a button.

Multiple outlet controls: The system can control multiple water outlets, allowing users to switch between them or use them simultaneously for a luxurious shower experience.

Smart home integration: Advanced models feature integration with smart home systems, enabling control via voice commands or through smartphone apps.

Easy installation: Even though it is a sophisticated system, companies like Kohler design these controls to be as easy to install as possible, sometimes compatible with existing plumbing.

Safety features: Many digital showers include safety features like automatic shut-off after a certain period or if the water gets too hot, which can prevent scalding.

Energy saving: Some models offer features that help conserve water and energy, aligning with eco-friendly practices.

If you’re after the type of precision temperature control that only a digital display like the Anthem Digital Shower Control can provide, consider the much more streamlined and affordable BLTFAUCER Digital Display. While it doesn’t provide as much customization as the Anthem model, it will allow you to achieve and monitor the exact shower temperature you want.

Elements Hexagon Starter Kit

The Elements Hexagon Starter Kit is a product by Nanoleaf, which is a company known for producing smart lighting solutions that are popular for their modular, geometric design and customizable lighting scenes. The Elements Hexagon Starter Kit is part of Nanoleaf’s Elements line, which focuses on combining smart lighting technology with decor.

Hexagonal panels: These are the core of the product, designed to be attached to form patterns on your wall. They’re hexagon-shaped to allow for a variety of configurations.

Wood look: Unlike the original Nanoleaf light panels, which have a very futuristic look, the Elements line has a more natural wood-like appearance, allowing them to blend into home decor more seamlessly when turned off.

Customizable lighting: Users can customize the illumination of each panel to create scenes or set the ambiance. This can include warm to cool white light settings, designed to mimic natural elements like a fireplace or thunderstorm.

Interactive control: The lights can be controlled via an app, where users can select or design scenes, schedule on/off times and adjust the brightness. They can also respond to touch or sound.

Smart home integration: The kit is compatible with most smart home systems, allowing for voice control.

Rhythm feature: With the rhythm feature, the panels can synchronize with music in real time, creating dynamic light shows in response to the audio they detect.

Simple installation: The panels attach to the wall with adhesive strips, which are included in the starter kit, making for a relatively easy setup without needing to drill holes.

Expandability: The starter kit includes a certain number of panels but can be expanded by purchasing additional expansion packs at any time.

The Elements Hexagon Starter Kit is a great system for incorporating upscale and entirely unique lighting into a space. That said, there are also a ton of customizable hexagon lighting solutions on Amazon for a range of prices.

Smart home. Seamless tech. Smiling faces.

The rise of smart home technology stands as a testament to human ingenuity and the quest for an enhanced quality of life. As we look to the future, the integration of these intelligent systems into our homes continues to evolve, bringing new levels of ease and enjoyment. These devices do more than just perform tasks — they create experiences, foster safe environments, and cultivate moments of joy and relaxation.

In a world where time is precious and personal happiness is paramount, the smart home is less about the gadgets and more about the freedom they afford us — the freedom to spend less time managing our homes and more time savoring the pleasures of life. As we embrace this era of connected living, we find that the true genius of smart home technology lies in its ability to fade into the background, creating a symphony of convenience.

Looking for your own place to add tech to? Whether you want to replicate the HGTV Smart Home 2023 or just add some DIY home automation, the future revolves around tech-forward homes. Check out our available apartments and houses for rent.

Inside: Intuit bought its popular Mint app and now it shutting down leaving users scrambling to find an alternative. This guide will help you understand Intuit’s decision to move Mint to Credit Karma and provide a list of alternatives for personal finance management.

In an era where personal finance apps are thriving more than ever, the shutdown news of Intuit’s Mint app comes as a shock for many.

When I heard the news, I couldn’t believe my ears… moving Mint’s feature to Credit Karma – a credit repair app?!?!

Once I got over the shock, I knew you wanted the best information out there to decide on what to do next.

Our guide here is dedicated to helping Mint users navigate the ongoing changes and prepare for what’s next in their personal finance journey.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

The Downfall: Intuit’s Decision to Shut Down Mint

Mint has always been a beacon in the realm of top budgeting apps; mostly due to the fact it was free.

However, Intuit’s decision to close Mint marks the end of an era. Yet, there is a teaser… Mint is propelling people to Credit Karma.

Here is a statement in the Mint App News:

“Credit Karma is thrilled to invite all Minters to continue their financial journey on Credit Karma, where they will have access to Credit Karma’s suite of features, products, tools and services, including some of Mint’s most popular features.”

Mint App News1

Mint’s commendable service, free albeit with ads, which has been helping many people manage their finances effectively, will be missed by Minters—time to understand why this happened.

Why is Mint Shutting Down?

Credit: Intuit MintLife 1

A surprising fact is that a free personal finance app like Mint isn’t a sustainable business. Most free apps have marginal direct costs associated with their services, unlike personal finance apps. They heavily rely on expensive data aggregators to gather the necessary financial data, causing a steady revenue loss for Mint per free user.

Intuit’s model has never been able to cover these costs leading to a revenue crisis. That was a key reason why I believe Intuit decided to shut down Mint. While Intuit denied Mint’s expenses being material in their quarterly earnings calls in 2023, they did note however they are looking to grow their consumer base across all of their products. 2

The Controversy Surrounding Mint’s Shutdown

While the financial reason behind Mint’s closure is understandable, this decision has provoked a wave of consternation among the users. Massive user outcry on Reddit underscores the integral role Mint played in their lives, and some even accuse Intuit of abandoning its commitment to free financial management resources.3

Given the fairly recent acquisition of Mint into Intuit, this may be surprising for many including these Twitter users.10

Not totally surprised to see this move to kill @Mint by @Intuit. @CreditKarma had plans to compete directly with Mint while independent & it makes sense to have a single consumer portal.

Very worried about the execution. 😬 https://t.co/pki8J3R2lg

— Adam Nash (@adamnash) November 1, 2023

Intuit is shutting down budgeting app Mint and is trying to get people to instead use Credit Karma, an app without any budgeting functionality https://t.co/j2AXvLtd6F

— bart (@bart_smith) November 2, 2023

Pt 1/2 Opened my @mint app today to find that they had moved the platform over to Credit Karma! What the hell!? And worst of all, they got rid of all of the features that I liked about Mint! I loved Mint, it helped me take my personal finances seriously!!

— Trevbotplaya (@trevbotplaya) October 25, 2023

When is Mint shutting down?

Yes, Mint is being shut down. Mint’s curtains will be drawn on January 1, 2024.

From this date, users will no longer be able to access their accounts or use any Mint services as we know them today.

So, don’t be caught off-guard; stay prepared and choose the right alternative before Mint bids adieu. We have other options below to help you guide this transition.

Mint User’s Guide: Next Steps to Credit Karma

Okay, one piece of advice I always give at Money Bliss is to plan and carve your own money journey. So, let’s move from panic to planning:

What should Mint users do now?

It’s natural to feel perturbed by Mint’s shutdown. Yet, the smart step is to immediately switch to planning mode.

Some crucial actions include exporting your transactions from Mint for future use and deleting your account once you have secured all necessary information.

In this interim period, also make sure to explore personal finance app alternatives, considering their features and support services, to find one that fits your needs perfectly.

Starting Afresh: Alternatives to Mint App

In light of recent events, here are the best apps available for Minters.

Switching to a new personal finance app might feel daunting initially, but there’s no need to worry. This era offers a wide array of options, many of which employ advanced technology and provide a user-friendly experience.

Look for apps that offer seamless data importation from Mint with a CSV file, comprehensive financial overview, dependable security features, and preferably, competitive pricing as well.

Diving into Details: A Comparison of Mint Alternatives

When comparing Mint alternatives, consider factors such as user interface, functions, cost, and customer feedback. Each app has its unique strengths.

For instance, YNAB stands out for budgeting, and Quicken shines in terms of portfolio management, while Simplifi offers a user-friendly interface. You may pick a budget app based on your budgeting preference, such as budget by paycheck or zero based budgeting.

Research thoroughly to find the app that delivers your personal financial needs the best.

YNAB

YNAB, or You Need a Budget, stands out for its award-winning budgeting system. It’s not a clone of Mint, but rather, it takes a unique approach to helping people proactively track spending and work towards financial goals.

YNAB stands out in personal finance management since it allows for utmost user control with its four simple pillars:

Give Every Dollar a Job

Embrace Your True Expenses

Roll with the Punches

Age Your Money

Additionally, YNAB presents flexible customization options for category names, a feature that enhances user experience, along with an open-source toolkit for extensive reporting while maintaining supreme user data privacy.

Learning Curve: YNAB requires diligence and customization in its early stages, but offers a robust set of personalized budgeting tools once users cross the learning curve.

Import Existing Mint Transactions: Yes 4

Price: Free 34 day trial and then a subscription-based model of $14.99 monthly or $99 annually.

Most people struggle with YNAB because of the steeper learning curve as well as getting one month ahead on their money. This is YNAB’s rule #4 to age your money, which is a smart money move and one we do personally.

No need to compare YNAB vs Mint anymore.

YNAB

Enjoy guilt-free spending and effortless saving with a friendly, flexible method for managing your finances.

Pros:

Comprehensive approach to budgeting, helping you plan monthly budgets based on your income.

Offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

Superior synchronization skills make it the winner in this area.

YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners.

Option to manually add and upload transactions from accounts each month.

YNAB prioritizes user privacy.

Start 34 Day Free Trial

YNAB vs Mint

Simplifi

Simplifi by Quicken is a budgeting app that strikes a fine balance between complexity and simplicity.

Cheaper than a gallon of gas per month, Simplifi by Quicken a great bargain that offers a clean, intuitive, and clutter-free interface. It allows users to effortlessly track their spending, monitor savings goals, capture bills, and more.

Learning Curve: Simplifi is smooth due to its user-friendly interface and detailed instructions

Import Existing Mint Transactions: Yes 6

Price: Starting at $2.39/ month for new users

Simplifi has been rated as a preferred choice for people who want a fuss-free app to manage finances.

simplifi

Manage your money less in 5 minutes each week.

Reach your money goals with confidence!

“The easiest, most comprehensive way to both see where your money is going and plan for future expenses.”

Start FREE Trial

Quicken

This is the personal finance software I have been using for over 25 years.

Quicken offers robust personal finance management tools that make it easier to track expenses, income, and investments. Many people complain their budgeting feature isn’t up to par, but their cash flow reporting overcomes this as you can see your spending and plan accordingly.

Quicken Classic Deluxe: Robust & feature-rich | Best for power users

Quicken Classic Premier: Robust & feature-rich including investment| Best for serious users

Quicken Classic Business & Personal: Best-in-class business features integrated with our flagship personal finance product

Quicken might be the most suitable option for current Mint users due to its compatibility and ease of use. Unlike Mint, Quicken is not free, but its expansive features such as detailed expense tracking, report generation, and robust investment tracking arguably justify the cost. Plus you can add attachments of receipts into the transactions.

Learning Curve: Quicken may present a significant learning curve for beginners.

Import Existing Mint Transactions: Yes 5

Price: Starts at $4.19/ month for Quicken classic for new users. All plans have a 30 day money back guarantee.

It’s a perfect match for anyone requiring a comprehensive personal finance tool. You can sync between multiple devices as I covered in my Quicken review.

Quicken

Personal finance and money management software allows you to manage spending, create monthly budgets, track investments, retirement and more.

I have used this platform for over 20 years now.

Pros:

Birds-eye view of your complete financial picture.

Conveniently download your spending activities, and automatically categorize them (Quicken connects to over 14,000 financial institutions).

Track investments with it’s features like portfolio analytics, retirement goals, and market comparison.

Cons:

Little complex to use at first, the learning curve is moderate.

Yearly subscription-based model to use the platform.

Save 40% on New Memberships

Our Review

Monarch Money

Monarch Money’s unique selling point is its robust data connectivity. Armed with state-of-art financial transaction infrastructure that integrates with various data aggregators, Monarch promises effective budgeting and financial planning. It’s not free but offers a 7-day free trial to test its features.

Its subscription charges are $14.99 per month or $99.99 per year, a fair trade for its impressive service.

This is the latest top budget app to surface as true competition.

Learning Curve: Monarch Money boasts an intuitive and user-friendly interface, making the learning curve minimal and easy for new users.

Import Existing Mint Transactions: Yes 7

Price: Try Monarch Premium for free for 7 days. Then choose between the $14.99/month or annual $99/year plan.

Monarch Money facilitates financial planning with goal setting and forecasts, allows Mint transactions importation for history preservation, has customer-driven rapid development, provides a multi-user platform for collaborative financial management, is available across multiple platforms, and provides efficient customer service.

Tiller Money

Tiller Money might be the perfect solution for spreadsheet enthusiasts. This unique budgeting tool uses spreadsheets to manage finances and daily transaction updates. It is highly customizable with categories and reports to help you stay on top of your spending.

Tiller Money is a definite contender in the personal finance app scene.

Learning Curve: While Tiller Money requires a basic understanding of spreadsheets, users can easily customize it to suit their personal budget needs.

Import Existing Mint Transactions: Yes 8

Price: Starts with a free trial for 30 days and then charges a reasonable annual fee of $79.

A notable feature is its ability to pull and categorize credit card transactions, providing an in-depth view of spending habits.

Tiller Money

Your financial life in a spreadsheet, automatically updated each day.

Tiller is the fastest, easiest way to manage your money with the unlimited flexibility of a spreadsheet.

Update your finances in one place, so you can take control of spending, optimize cash flow, and confidently plan your financial future.

Pros:

Tiller automatically updates Google Sheets and Microsoft Excel with your latest spending, balances, and transactions each day.

No more tedious data entry, CSV files, or logging into multiple accounts.

You can customize everything and finally track your money, your way.

Try Tiller Free

Empower

Empower, formerly known as Personal Capital, is a comprehensive personal finance app that provides tools for managing income, expenses, assets, and liabilities.

With its intuitive interface, Empower users can seamlessly track their spending, create custom budgets, and even get insights into their net worth which can be updated on a monthly basis, thereby aiding in effective financial management. Additionally, their retirement planner is one of the best available – plus for free.

Learning Curve: Empower has a relatively intuitive interface, making the learning curve fairly manageable for new users.

Import Existing Mint Transactions: No 9

Price: Free to use

The downfall is Empower provides wealth management services, so there is a heavy sales pitch to bring assets under management.

Empower

Empower offers powerful tools to help you plan your investment strategy along with basic budgeting features and a great net worth tool.

As a free app, Empower can help you to save money, save time, and even make more money.

Get Started

Empower Personal Wealth, LLC (“EPW”) compensates Money Bliss for new leads. Money Bliss is not an investment client of Personal Capital Advisors Corporation or Empower Advisory Group, LLC.

How to Move From Mint to Credit Karma?

Yep, I gave you the alternatives to Mint first.

Yet, the goal for Intuit is to move to Credit Karma. The core issue right now is while we do know which features will be transferred from Mint to Credit Karma. We are not sure as Minters if we will like the new layout and features offered with Credit Karma.

Right now, the budgeting feature will not be offered at Credit Karma, which I know for many Money Bliss readers is a big feature lost.

Learn more on how to move from Mint to Credit Karma.

Intuit’s Current Portfolio of Products

Intuit buying out Mint in 2020, you may be wondering about the current products offered by Intuit. 10

Intuit offers a range of financial and tax preparation products, including

Most notable is the success of TurboTax and Credit Karma.

Frequently Asked Questions

Once Mint shuts down, it’s crucial to know that Intuit will no longer have access to your financial data. All account and transaction information associated with your Mint profile will be deleted permanently from Mint’s databases.

To prevent any loss of important financial information, make sure to export all your transactions from Mint before the shutdown date arrives.

This highlights the importance of regularly backing up financial data as you may not know the next steps a company has for their product.

Yes, you can migrate your Mint data to a different personal finance app before Mint shuts down.

After you export your transactions from Mint, you can then import them to your new finance management app, ensuring you seamlessly carry over all essential financial information and continue managing your finances smoothly. However, bear in mind that the steps to do this may vary depending on the app you choose as your next financial companion.

Coping with the Closure: Dealing with the Loss of Mint

For long-time Minters, Mint’s shutdown can feel like losing a trusted companion. It’s natural to feel a sense of loss and uncertainty. I completely understand. That is why I haven’t switched from Quicken because of the long-term history.

However, remember that technology promises continual growth and evolution. There are numerous other personal finance apps out there, likely even better ones suited to your needs.

So, take a deep breath, do your research, and move on to the next chapter of your financial journey with confidence.

Source

Intuit MintLife. “Intuit Credit Karma welcomes all Minters!” https://mint.intuit.com/blog/mint-app-news/intuit-credit-karma-welcomes-minters/. Accessed November 1, 2023.

Intuit. “Event Details – Intuit Investor Day 2023.” https://investors.intuit.com/events-and-presentations/event-details/2023/Intuit-Investor-Day-2023/default.aspx. Accessed November 1, 2023.

Reddit. “Thoughts on the Mint shutdown from Monarch CEO (and first Mint product manager.” https://www.reddit.com/r/mintuit/comments/17llnbu/thoughts_on_the_mint_shutdown_from_monarch_ceo/. Accessed November 1, 2023.

YNAB. “File-Based Import: A Guide.” https://support.ynab.com/en_us/file-based-import-a-guide-Bkj4Sszyo. Accessed November 1, 2023.

Quicken. “Quicken for Windows: Importing Address Book Records From Another Program.” https://www.quicken.com/support/quicken-windows-importing-address-book-records-another-program. Accessed November 1, 2023.

Quicken Simplifi. “How to Manually Import Transactions.” https://help.simplifimoney.com/en/articles/4413430-how-to-manually-import-transactions. Accessed November 1, 2023.

Monarch. “Move data over from Mint to Monarch.” https://help.monarchmoney.com/hc/en-us/articles/4411877901972-Move-data-over-from-Mint-to-Monarch. Accessed November 1, 2023.

Tiller. “How to Easily Export Mint Transactions to a Spreadsheet.” https://www.tillerhq.com/exporting-mint-transaction-data-into-a-google-sheet-spreadsheet/. Accessed November 1, 2023.

Empower. “Am I able to see more than 3 months of data in Empower Personal Dashboard after I first link my account?” https://support-personalwealth.empower.com/hc/en-us/articles/201170160-Am-I-able-to-see-more-than-3-months-of-data-in-Empower-Personal-Dashboard-after-I-first-link-my-account-. Accessed November 1, 2023.

Intuit MintLife. “Intuit to Acquire Mint.com.” https://mint.intuit.com/blog/press/intuit-to-acquire-mint-com/. Accessed November 1, 2023.

Know someone else that needs this, too? Then, please share!!

Did the post resonate with you?

More importantly, did I answer the questions you have about this topic? Let me know in the comments if I can help in some other way!

Your comments are not just welcomed; they’re an integral part of our community. Let’s continue the conversation and explore how these ideas align with your journey towards Money Bliss.

All of us have done some foolish things when we were just little kids. Most of those are only for fun and are seemingly safe. However, it’s not always the case; some of the things we do as children can have a greater impact on our childhood—or worse, they’re affecting us in still as adults. Here are 12 things people did innocently as children that affected their childhood. Let us know in the comments if you resonate with some of the things listed here!

1. Messenger Bags and Side-Bangs

Photo Credit: Shutterstock.

Do you like wearing messenger bags? Having bangs when you’re a kid?

Well, one Reddit user shared, “I used to wear messenger bags in the 6th grade to be trendy, and wore my bangs to cover my left eye. Now I have borderline severe scoliosis from the weight of the bag being on one side, and my left eye is lazy.”

2. Playing Music Too Loud

Photo Credit: Shutterstock.

One commenter said, “Wear headphones and play the music as loud as my walkman/discman would go. Now I have tinnitus.”

Another one replied, “Oof it’s rough! I have a particular day and time that I know I screwed my hearing up, and I’ve had tinnitus ever since.”

One Redditor added, “It’s literally what happened to me. I always used to get it would last like 30 seconds and go away. It would suck, but I always knew it would stop. And then… one night, I was sleeping, and it woke me up out of my sleep. It never went away. I’ve had it for 8 years now. Some days are bad, and some days I barely notice it. It’s always noticeable when I’m going to sleep. Just gotta learn to live with it, sadly.”

3. Not Brushing Your Teeth

Photo Credit: Shutterstock.

Were you also lazy about brushing your teeth? Well it doesn’t take long for you to start having dental problems.

“Was too lazy to brush my teeth. My parents didn’t seem to notice if I did it or not. I’d probably only do it for like 30 seconds every other day. And only ever once a day. I’m now facing lots of expensive treatment and having to go to private because getting an NHS is nigh on impossible,” one user shared.

“Same. Spent over £3k sorting my teeth in my 20’s, from years of neglect. 12 fillings, two root canals and 3 years of braces. Decent enough teeth now thankfully, but could have [saved] much pain if I’d [brushed] and [gone to the dentist],” someone replied.

4. Lying on One Side Too Much

Photo Credit: Shutterstock.

One Reddit user shared, “I used to use my laptop lying down on one side with my arm propping up my head, for hours and hours. I have permanent back alignment issues.”

Another user replied, “I still do this when I’m tired, and it always ends up with a first rib subluxation. I’m used to doing it, though, it’s a tough habit to break.”

Another one added, “I have always leaned on my right side, and now I have tendinitis in my rotator cuff, and I’m only reminded not to lean if it starts hurting shortly after I start leaning that way.”

5. Finding Safe Places

Photo Credit: Shutterstock.

Some of us have had a terrible childhood, and sadly, most of those memories and defense mechanisms we’ve come to use as children will still greatly affect us in adulthood.

One person stated, “Hide in small spaces to get away from my abusive parents. Now whenever I’m panicking, I try to look for small spaces to hide in and will panic more if I can’t find one.”

The second person replied, “The feeling of despair I get when I realize there’s nowhere for me to hide is terrible. It’s like being stuck in the middle of the ocean. I’m sorry you experienced the same thing.”

6. Being Antisocial

Photo Credit: Shutterstock.

While you may have enjoyed your own company as a child by playing video games all day, it may ultimately significantly impact your adulthood.

One Redditor stated, “Being an introvert and staying home playing video games all the time, now that I’m 28 don’t have any friends, the loneliness is getting worse.”

Another one replied, “Oof I feel this. I never really learned how to be social and make lasting friends. At least I found a husband who also avoided everyone and played video games lol.”

One commenter said, “I kinda feel this, but I don’t regret the gaming. It was fun. And I still made lots of friends when I went to college, who I still hang out and play games with. Maybe I’m just lucky, but you might find some luck too if you manage to find people who share your interests.”

7. Wearing Bad Shoes

Photo Credit: Shutterstock.

“Wore nothing but chucks and flats from age 12 to my late twenties and now my feet are messed up,” someone shared.

“Really? How is that harmful?” another user asked.

“No arch support,” someone replied.

A fourth commenter added, “No. Humans were never made to need arch support. Muscles in the foot should be strengthened by use (barefoot walking). Now we need arch supports because we smash our feet so dang narrow and reshape the foot with modern footwear our feet are literally deformed. Hence the need for supports, cushioning, toe spring, shoes with heel drop, etc.”

8. Not Showing Emotions

Photo Credit: Shutterstock.

One person shared, “Hid my emotions because I was trying to be ‘manly.’ Now I have psychological issues from trying to be someone other than myself, not to mention high blood pressure, back and neck pain, hair loss, and a number of other ailments.”

Then the second person replied, “I’m sad that the older generations were taught that men shouldn’t ‘have emotions’, I’m glad it’s being realized that everyone has emotions, we’re not robots after all! I hope you find peace.”

9. Eating Your Feelings

Photo Credit: Shutterstock.

Do you binge eat when things get too complicated and too much to handle? While it can help you a bit when dealing with stress, it actually does more harm than good.

“I have a weird relationship with food from binge eating so much and my dad basically getting us McDonald’s on the daily. I’m not overweight, but I’m definitely unhealthy and steadily gaining more weight than I’m comfortable with. Cooking somewhat healthy meals at home is easy for a week, then I fall back into my old ways.”

“Put a stop to it now seriously i was raised on McDonald’s and Burger King. I’m 32 and literally… I’m the fattest I’ve ever been. Just got a trainer, and his reaction to my soda intake was an eye opener,” someone replied.

10. Staring at the Sun

Photo Credit: Shutterstock.

Do you remember staring at the sun when you were a kid? Well, you’re not the only one.

“I don’t know why, but I stared at the sun wearing 3d glasses for a minute or two. Now, when I close my left eye, the white walls are very slightly reddish. When I close my right eye, the white walls are very slightly bluish. Definitely damaged some cones in my eyes,” shared one person.

11. Bullying Others

Photo Credit: Shutterstock.

One person stated, “I was a bully. A horrible bully. And I live with shame every day of my life because of it.”

The second person replied, “You can’t undo your past, but you can work on doing some ‘good’—help the underprivileged, something for the environment, kids, animals… Lots of ways to give back to society and feel better. Make it happen!”

A third commenter added, “Think of it this way: the fact that you feel bad about it now means that you have grown as a person. You know how bad you were before and have the knowledge of how to be good now. A lot of people don’t come to this realization in their whole lives, so you did something special.”

Do you have similar experiences you’d like to share? Let us know in the comments.

Source: Reddit.

These are 10 Things That Completely Destroyed The Love in a Relationship

Photo Credit: Shutterstock.

There’s no question that relationships can be confusing, but here are some of the top things to avoid if you want to keep your relationship healthy!

10 Actors and Actresses People Refuse to Watch Ever Again

Photo Credit: Shutterstock.

We all have a favorite actor or actress, but most of us have a least-favorite as well. Check out this list of actors and actresses people never want to see performing again!

Top 10 Worst Human Inventions of All Time

Photo Credit: Shutterstock.

Some inventions are world-changing, and some of them, well, they change the world in the wrong ways. Here are some of the worst inventions Redditors could think of.

10 Famous Celebrities Who Look Like They Smell Terrible

Photo Credit: Shutterstock.

We’ve all had moments of hygiene faux pas—but these celebrities just look like they don’t take care of themselves at all.

10 Terrible Fads People Are Glad Died Out

Photo Credit: Shutterstock.

Every fad has its time in the limelight, but some of them come and go faster than others; and some just need to die out right away. Check out this list of fads of which people were happy to see the last.

No one can predict the future of real estate, but you can prepare. Find out what to prepare for and pick up the tools you’ll need at Virtual Inman Connect on Nov. 1-2, 2023. And don’t miss Inman Connect New York on Jan. 23-25, 2024, where AI, capital and more will be center stage. Bet big on the future and join us at Connect.

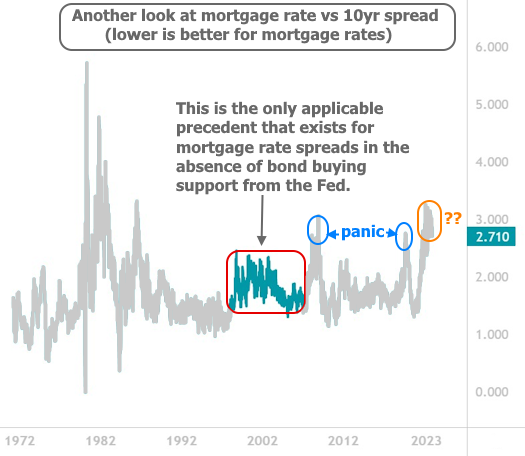

Economists are scratching their heads and housing industry leaders are venting their frustrations as mortgage rates continue a relentless climb to new heights not seen in more than two decades, chasing yields on government debt that are being pushed higher by factors beyond Federal Reserve tightening.

The Optimal Blue Mortgage Market Indices, which track daily rate lock data, show rates on 30-year fixed-rate conforming loans hitting a new 2023 high of 7.59 percent Tuesday — an all-time high in Optimal Blue records dating to 2017.

At 7.95 percent, rates on jumbo mortgages that exceed Fannie Mae and Freddie Mac’s loan limits looked poised to push through the 8 percent benchmark, as paper losses mount at banks that fund most jumbo lending and Treasury yields rise.

National Association of Realtors Chief Economist Lawrence Yun vented his frustration with Fed policymakers, who have telegraphed their intention to implement at least one more rate hike this year.

“The Fed is overdoing the rate hike,” Yun said in a LinkedIn post Wednesday. “The economy is measurably slowing. Even the lagging indicator job gains are coming in light.”

Yun said he’s worried that rising interest rates could actually fuel inflation as would-be homebuyers throw in the towel, fueling more demand for rentals, and making housing more scarce as builders balk at paying higher rates on construction loans.

A weekly survey of lenders by the Mortgage Bankers Association (MBA) showed that applications for purchase loans were down a seasonally adjusted 6 percent last week when compared to the week before, and 22 percent from a year ago.

Joel Kan

“The purchase market slowed to the lowest level of activity since 1995, as the rapid rise in rates pushed an increasing number of potential homebuyers out of the market,” MBA Deputy Chief Economist Joel Kan said in a statement.

With rates on 30-year fixed-rate conventional loans rising for the fourth consecutive week to the highest rate since 2000, Kan said some borrowers searching for ways to lower their monthly payments are turning to adjustable-rate mortgage (ARM) loans.

Although ARM loans accounted for 8 percent of mortgage applications last week, they had an even bigger share when mortgage rates made a similar surge last fall. During the second week of October 2022, ARM loans accounted for 13 percent of applications, the highest share since March 2008.

Appearing on CNBC’s “Squawk Box,” Yun noted that rates on ARM loans aren’t much lower than those for more traditional 30-year fixed-rate conventional loans (according to the MBA survey, rates on ARM loans averaged 6.49 percent last week). “My advice right now is go into the 30-year fixed, because even with that, one can always refinance once the interest rate goes down,” Yun said. “The mortgage rates are topping out now — hopefully there is some downward drift in the upcoming months.”

MBA CEO Bob Broeksmit expressed similar sentiments on CNBC Wednesday, urging the Fed to “be clear that they’re done with rate increases” and to also “make clear that they’re not going to sell mortgage-backed securities off their balance sheets.”

Jumbo mortgage rates spike

Homebuyers seeking jumbo mortgages exceeding Fannie and Freddie’s conforming loan limits — $726,200 for one-unit properties in most areas of the country — have been hit particularly hard by recent rate increases.

At this time last year, rates on jumbo mortgages were about half a percentage point less than for conforming loans. Now the situation has reversed, with the “spread” between jumbo mortgages and conforming loans widening to nearly 40 basis points on Wednesday, according to Optimal Blue rate lock data.

Conforming loans are largely financed by investors who buy mortgage-backed securities guaranteed by Fannie and Freddie. But jumbo mortgages are mostly provided by banks that hold the loans on their books. Stresses on regional banks sparked by the failures of Silicon Valley Bank, Signature Bank and First Republic Bank have made jumbo loans more expensive and harder to come by this year.

This week, Rocket Mortgage began offering some relief by pricing mortgages of up to $750,000 as conforming, in anticipation that Fannie and Freddie’s 2024 loan limits will go up by at least 3 percent on Jan. 1 to reflect home price appreciation over the last year.

Mike Fawaz