It’s entirely possible to sell a house with a mortgage. In fact, it’s common to sell a property that still has a mortgage, because most people don’t stay in a home long enough to pay off the home loan.

With the help of your lender and real estate agent, you can move ahead and sell a house with a mortgage. Yes, there’s a bit of paperwork involved, but settling your mortgage at the closing table shouldn’t prove too challenging.

Here’s everything you need to know about selling a home with a mortgage.

What Happens to Your Mortgage When You Sell Your Home?

When you sell your home, the amount you contracted with the buyer is put toward your mortgage and settlement costs before any excess funds are wired to you. Here’s how it works for different transaction types.

A Typical Sale

In a typical sale, homeowners will put their current home on the market before buying another one. Assuming the homeowners have more value in their home than what is owed on their mortgage, they can take the proceeds from the sale of the home and apply that money to the purchase of a new home.

A Short Sale

A short sale is one when you cannot sell the home for what you owe on the mortgage and need to ask the lender to cover the difference (or short).

In a short sale transaction, the mortgage lender and servicer must accept the buyer’s offer before an escrow account can be opened for the sale of the property. This type of mortgage relief transaction can be lengthy (up to 120 days) and involves a lot of paperwork. It’s not common in areas where values are falling or at times when the real estate market is dropping.

When You Buy Another House

There are several roads you can take when you buy another house before selling your own. You may have the option of:

• Holding two mortgages. If your lender approves you for a new mortgage without selling your current home, you may be able to use this option when shopping for a mortgage. However, you won’t be able to use funds from the sale of your current home for the purchase of your next home.

• Including a home sale contingency in your real estate contract. The home sale contingency states that the purchase of the new home depends upon the sale of the old home. In other words, the contract is not binding unless you find a buyer to purchase the old home. The two transactions are often tied together. When the sale of the old home closes, it can immediately fund the down payment and closing costs of the new home (depending on how much there is, of course). Keep in mind that a home sale contingency can make your offer less competitive in a hot real estate market where sellers are not willing to wait around for a buyer’s home to sell.

• Getting a bridge loan. A bridge loan is a short-term loan used to fund the costs of obtaining a new home before selling the old home. The interest rates are usually pretty high, but most homebuyers don’t plan to hold the loan for long.

💡 Quick Tip: You deserve a more zen mortgage. Look for a mortgage lender who’s dedicated to closing your loan on time.

Selling a House With a Mortgage: Step by Step

Here are the steps to take to sell a home that still has a mortgage.

Get a Payoff Quote

To determine exactly how much of the mortgage you still owe, you’ll need a payoff quote from your mortgage servicer. This is not the same thing as the balance shown on your last mortgage statement. The payoff amount will include any interest still owed until the day your loan is paid off, as well as any fees you may owe.

The payoff quote will have an expiration date. If the outstanding mortgage balance is paid off before that date, the amount on the payoff quote is valid. If it is paid after, sellers will need to obtain a new payoff quote.

Determine Your Home Equity

Equity is the difference between what your property is worth and what you owe on your mortgage (your payoff quote is most accurate). If your home is worth $400,000 and your payoff amount on the existing mortgage is $250,000, your equity is $150,000.

When you sell your home, you gain access to this equity. Your mortgage, any second mortgage like a home equity loan, and closing costs are settled, and then you are wired the excess amount to use how you like. Many homeowners opt to use part or all of the money as a down payment on their next home.

Secure a Real Estate Agent

A real estate agent can walk you through the process of selling a home with a mortgage and clear up questions on other mortgage basics. Your agent will be particularly valuable if you need to buy a new home before selling your current home.

Set a Price

With your agent, you will look at factors that affect property value, such as comparable sales in your area, to help you set a price. There are different price strategies you can review with your agent to bring in more buyers to bid on your home.

Accept a Bid and Open Escrow

After an open house and showings, you may have an offer (or a handful). Consider what you value in accepting an offer. Do you want a fast close? The highest price? A buyer who is flexible with your moving date? A buyer with mortgage preapproval?

You may also choose to continue negotiating with prospective buyers. Once you’ve selected a buyer and have signed the contract, it’s time to go into escrow.

Review Your Settlement Statement

You’ll be in escrow until the day your transaction closes. An escrow or title agent is the intermediary between you and the buyer until the deal is done. While the loan is being processed, title reports are prepared, inspections are held, and other details to close the deal are being worked out.

Three days before, you’ll see a closing disclosure (if you’re buying a house at the same time) and a settlement statement. The settlement statement outlines fees and charges of the real estate transaction and pinpoints how much money you’ll net by selling your home. 💡 Quick Tip: Generally, the lower your debt-to-income ratio, the better loan terms you’ll be offered. One way to improve your ratio is to increase your income (hello, side hustle!). Another way is to consolidate your debt and lower your monthly debt payments.

Selling a House With a Negative Equity

Negative equity means that the value of an asset (such as a home) is less than the balance due on the loan against it. Say you purchased a property for $400,000 with a $380,000 loan, but then the real estate market took a nosedive. Your property is now worth $350,000, less than the amount of the mortgage.

If you have negative equity in the home and need to sell it, it is possible to sell if you come up with the difference yourself.

In this scenario (an alternative to a short sale), you pay the difference between the amount left on your mortgage note and the purchase offer at closing. So in the example above, if you sold the house for $350,000, at the closing, you would need to pay the loan holder an additional $30,000 to clear the debt.

The Takeaway

Selling a house with a mortgage is common. The buyer pays the sales price, and that money is used to pay off your remaining mortgage, your closing costs, and any second mortgage. The rest is your profit.

Looking for an affordable option for a home mortgage loan? SoFi can help: We offer low down payments (as little as 3% – 5%*) with our competitive and flexible home mortgage loans. Plus, applying is extra convenient: It’s online, with access to one-on-one help.

SoFi Mortgages: simple, smart, and so affordable.

FAQ

Who is responsible for the mortgage on the house during the sale?

The homeowner is responsible for continuing to pay the mortgage until paperwork is signed on closing day.

What happens if you sell a house with a HELOC?

When you sell a home that has a home equity line of credit with a balance, a home equity loan, or any other kind of lien against the house, that will need to be paid off before the remaining equity is paid out to you.

What happens to escrow money when you sell your house?

Your mortgage escrow account will be closed, and any money left will be refunded to you.

Can I make a profit on a house I still owe on?

Yes. You can make a profit if the amount you sell your house for is greater than the amount you owe on it, less closing and settlement costs.

Can I have two mortgages at once?

Yes, you can have two mortgages at once if the lender approves it.

Photo credit: iStock/Beton studio

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

SoFi Mortgages Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility for more information.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Selling your house is often one of the largest financial transactions you’ll make in your life. It can be complex and emotionally challenging, especially if it’s your first time dealing with a home sale or if the house is full of family memories.

Despite these challenges, millions of people successfully sell their homes each year. The process is well-trodden, but each sale has its unique circumstances and can come with many curveballs.

Whether you’re downsizing, upgrading, relocating, or just ready for a change, selling your house is a big step. The task might seem daunting, but remember, you’re not alone. Many resources can guide you through this process, providing advice and support along the way.

This guide aims to simplify the process and provide you with step-by-step instructions to help sell your house.

From setting your objectives to finally handing over the keys, we’ll walk you through each stage. We will address common challenges and offer expert insights to ensure you’re well-prepared for the journey ahead. Our goal is to help you sell your house at the best possible price within your desired timeline, while minimizing stress and maximizing satisfaction.

Understand Your Selling Objectives

The first step in any successful real estate transaction is understanding your motivations and objectives for selling. Be clear about your goals and timeline to create a selling strategy that will get you the price you want for your home within the timeframe desired.

Why are you selling?

Your motivations for selling might be tied to lifestyle changes, financial circumstances, or relocation for work. Perhaps you’ve outgrown your current house, or maybe it’s become too big after the kids have moved out. You might need to relocate for a new job or prefer a change in scenery as you approach retirement. By identifying your reasons for selling, you’ll have a clearer idea of what you want to achieve with the sale.

What’s your timeline?

Your timeline can significantly influence your selling strategy. If you’re in a rush due to reasons like a job relocation or closing on another home, you may have to price your property more competitively to attract a faster sale. However, if you have the luxury of time, you can afford to be patient and wait for an offer that matches your ideal price.

Evaluate Your Financial Position

Understanding your financial situation is essential in the home-selling process. A realistic view of your finances will help you make informed decisions, particularly in setting a reasonable asking price.

Understand Your Home Equity

Equity refers to the portion of your property that you truly “own” – it’s the difference between the current market value of your home and the remaining balance on your mortgage. Knowing your equity can give you an idea of your potential profits from the sale.

Consider Your Outstanding Mortgage

The amount left on your mortgage is another critical factor. If your outstanding balance is more than your home’s sale price, you may need to consider a short sale, which requires your lender’s approval and can affect your credit score.

Estimate Closing Costs

Closing costs are the fees and expenses you pay to finalize your home’s sale, excluding the commission for the real estate agent. They may include title insurance, appraisal fees, and attorney fees, among other costs. These are usually about 2-5% of the purchase price. Understanding these costs is crucial as they directly impact your net proceeds from the sale.

Taking the time to clarify your selling objectives and understanding your financial position will pave the way for a more streamlined and successful home-selling experience. These factors are not just critical for setting a realistic asking price but also for aligning your home sale with your larger financial or life goals.

Prepare Your House for Sale

Once you’ve identified your selling objectives, the next step is to prepare your house for the market. A well-prepared home can catch the attention of more prospective buyers and even command a higher sale price.

Home Improvements and Necessary Repairs

Before you list your home, assess its overall condition. Some minor upgrades and necessary repairs can significantly enhance your home’s appeal, often leading to a faster sale or higher selling price.

Deep Cleaning and Carpet Cleaning

Begin with a deep clean to ensure your home looks its best. Pay attention to often-overlooked areas, such as baseboards, window sills, and ceiling fans. If you have carpets, consider hiring a professional carpet cleaning service to remove any stains or odors. Cleanliness can significantly influence a buyer’s first impression.

Minor Upgrades and Fixes

Next, tackle minor upgrades and repairs that could deter potential buyers. This could include painting walls with a fresh, neutral color, fixing any plumbing or electrical issues, and ensuring all appliances are in working order. Although these tasks may seem small, they can make a big difference to potential buyers.

Stage Your House

Staging your house involves preparing it for viewing by potential buyers. It can significantly impact how quickly your home sells and the price.

Hire a Professional Stager

A professional stager, although an extra cost, can be a worthwhile investment. For a few hundred dollars, they can transform your space and make it appealing to as many potential buyers as possible. They use strategies like optimal furniture placement, accentuating natural light, and choosing neutral decor to make your home attractive and inviting.

Depersonalize Your Home

Part of effective staging involves depersonalizing your home. This means removing personal items like family photos, collections, and mementos. The aim is to create a neutral space where potential buyers can easily envision themselves and their own belongings. It’s all about helping buyers picture your house as their future home.

In the competitive real estate market, first impressions count. By investing time, money and effort in staging your house for sale, you can stand out from the competition and make a great impression on prospective buyers. These preparations could translate into a quicker sale and potentially a higher price.

Set the Right Price

One of the most critical decisions in the home-selling process is determining the right asking price. Setting a competitive price can help attract more prospective buyers, shorten the time your home spends on the market, and potentially yield a higher sale price.

Understand the Importance of Pricing

Choosing the right price is not just about the amount you’d like to receive. It’s also about understanding buyer psychology and local market trends. Pricing your home correctly can result in more interest, more showings, and ultimately, more offers.

Get a Comparative Market Analysis

A key tool for setting the right price is a Comparative Market Analysis (CMA). A CMA provides information about recent home sales in your area, adjusted for differences in features and conditions, giving you a good idea of what buyers might be willing to pay for your home.

Hire a Great Real Estate Agent

A great real estate agent can provide an accurate and comprehensive CMA. They have the experience and local market knowledge to understand which homes are truly comparable to yours and how various features and upgrades impact pricing.

Consider Comparable Sales

Comparable sales, or “comps,” are recent home sales in your area that are similar to your property in size, condition, and features. Your real estate agent will look at these comps, adjust for differences, and use the information to guide you towards a fair and attractive list price.

Adjust for Features and Conditions

Every home is unique, and its features and condition will impact its value. Your real estate agent will consider these factors when setting your home’s list price. For example, if your home has a new roof or a remodeled kitchen, it might command a higher price compared to a similar home without these upgrades.

Setting the right price is both an art and a science. It requires an understanding of the local real estate market, an evaluation of comparable sales, and an assessment of your home’s unique features. By enlisting the help of a great real estate agent and leveraging their expertise, you can set a competitive price that will attract serious buyers and maximize your profits.

Market Your House

Once your house is ready for sale and priced right, the next step is to get the word out to prospective buyers. Effective marketing can attract more interest and lead to quicker, more competitive offers.

Use High-Quality Professional Photos

Professional photography plays a crucial role in marketing your house. High-quality photos can showcase your home’s best features and give potential buyers a good first impression. Homes listed with professional photos tend to receive more views online, which can lead to faster sales and often at higher prices.

Craft a Compelling Listing Description

A well-written listing description can spark interest and invite potential buyers to learn more. Highlight your home’s unique features, recent upgrades, and what makes it special. Remember, you’re not just selling a property, you’re selling a lifestyle. Allow your real estate agent to offer feedback and help you create an enticing, optimized listing that will also show up in search results when people are looking for a home like yours.

Host Open Houses and Private Showings

Open houses and private showings are opportunities for potential buyers to experience your home in person. Be flexible with your schedule and make your house available for viewing as often as you can. The more people who walk through your door, the better your chances of receiving an offer.

The Role of a Good Real Estate Agent in Marketing

Marketing a house involves a significant time commitment and a specific set of skills. This is where a good real estate agent comes into play.

Leverage the Multiple Listing Service (MLS)

A good real estate agent can list your property on the Multiple Listing Service (MLS), a database of homes for sale that’s used by real estate professionals. An MLS listing can increase your home’s visibility, attracting other real estate agents and their clients.

Find a Realtor with A Proven Track Record

Choose a real estate agent with a proven track record of sales in your area. Their experience and local market knowledge can be invaluable in promoting your home effectively and attracting serious buyers.

In a crowded real estate market, standing out is key. By leveraging professional photography, crafting a compelling listing description, and utilizing the expertise of a good real estate agent, you can market your home effectively, attracting more potential buyers and increasing your chances of a successful sale.

Evaluate Offers and Negotiate

Once your marketing efforts start paying off and offers begin to come in, it’s time to shift focus to negotiation. The goal here is to achieve the best possible terms that align with your selling objectives.

How to Evaluate Offers

When you receive an offer, it’s essential to look beyond the offered price. While the highest offer might seem the most appealing, it’s not always the best choice.

Consider the Buyer’s Lender

Understanding where the buyer’s financing comes from is important. Offers from buyers who are pre-approved by a well-known lender may carry less risk than those from buyers who are not pre-approved or who are using a less established lender.

Assess the Down Payment

The size of the buyer’s down payment can indicate their financial stability. A larger down payment may suggest that the buyer has solid finances and is serious about purchasing your home.

Understand the Buyer’s Timeline

A buyer’s timeline can be just as important as their offered price. A qualified buyer who can close quickly might be more attractive than a higher offer that’s contingent on selling a current house.

How to Manage Multiple Offers

Receiving multiple offers can be exciting, but it can also be overwhelming. Your real estate agent can help you with this process.

Consult with Your Real Estate Agent

Your real estate agent’s experience can be invaluable in this situation. They can guide you through your options, help you compare offers side by side, and give advice based on their understanding of the current real estate market and the specifics of each offer.

Make the Best Decision Based on Your Needs

When reviewing multiple offers, it’s important to consider your own needs and priorities. For example, if you need to sell quickly, you might prioritize a buyer who can close sooner, even if their offer is not the highest.

Negotiating and accepting offers can be a complex part of the selling process. It’s not just about accepting the highest offer, but understanding the nuances of each proposal and making the best decision for your circumstances. With the right real estate agent by your side, you can handle this process confidently and successfully.

Close the Sale

After you’ve accepted an offer, the next step is to finalize the transaction. The closing process involves several stages, including a home inspection, title search, potential repair negotiations, and final paperwork signing. Here’s what to expect:

The Due Diligence Period

The due diligence period allows the buyer to further investigate the property after their offer has been accepted. During this time, the buyer’s agent will arrange for a home inspection.

Home Inspection and Report

A professional home inspector will thoroughly examine your property and generate an inspection report. This document details the condition of the house and outlines any potential issues, from minor maintenance concerns to significant structural problems.

Negotiating Repairs

If the inspection report reveals necessary repairs, there may be further negotiations. Buyers might ask you to handle the repairs, reduce the sale price, or offer a credit at closing to cover the repair costs.

The Title Search and Insurance

As part of the home buying process, the buyer’s lender will work with a title company to conduct a title search. This ensures the house is free from liens or claims and that you have a clear title to transfer to the new owners.

Understanding Title Insurance

Buyers might also negotiate for you to pay for title insurance as part of the closing costs. Title insurance protects the buyer and their lender from future property ownership claims, unexpected liens, or undisclosed property heirs.

Sign the Final Paperwork

The last step in the home sale process is the closing meeting. Here, you’ll sign the final paperwork, which includes key documents such as:

The Bill of Sale

This document transfers the ownership of personal property (like appliances or furniture) included in the home sale.

The Deed

This legal document transfers ownership of the property from you, the seller, to the buyer.

Documents Prepared by a Real Estate Attorney or Real Estate Brokerage

The closing process involves many legal documents. These might be prepared by a real estate attorney or real estate brokerage to ensure everything is in order.

Closing the sale of your house can be a complex process. However, understanding each step can help you proceed with confidence and reach a successful conclusion to your home sale journey.

Post Sale Considerations

Even after the final paperwork has been signed, and the new owners have the keys, there are a few additional factors to consider. The sale of your house doesn’t just end at the closing table. Let’s delve into these post-sale considerations.

Understand the Tax Implications

Selling your house can have significant tax implications. The application of taxes largely depends on the profit you make from the sale and how long you’ve lived in the house.

Capital Gains Tax Exemption

If the house was your primary residence for at least two of the last five years before selling, you might qualify for a capital gains tax exemption. This can significantly reduce your tax liability.

Consult with a Tax Professional

However, tax laws can be complex, and every situation is unique. Consult with a tax professional or a certified public accountant to fully understand the potential tax impacts. They can provide guidance tailored to your specific circumstances.

The Move to Your New Home

Moving to your new home involves logistical and financial considerations. Plan ahead for moving costs, including professional movers, moving supplies, and potential temporary housing.

Keep Records of Your Home Sale Expenses

It’s wise to keep a comprehensive record of all home sale-related expenses. This includes real estate agent commissions, home improvements made before the sale, and any fees or costs associated with closing. These records can be crucial for your future tax returns or financial planning.

Some of your moving costs may be tax-deductible if you or a member of your household is in the military, and you are moving due to a military order. Previously, moving costs were tax-deductible for many people who were relocating due to a job. After 2025, these deductions may return.

Conclusion

Selling your house is a significant event, and educating consumers about the process can reduce stress and result in a better outcome. By preparing your home, pricing it right, and working with a competent real estate agent, you can complete the transaction smoothly and efficiently.

The selling process might seem overwhelming, but with thorough preparation and the right team on your side, it can be an exciting time. Remember, every house can sell, it just requires the right strategy, a competitive price, and a bit of patience.

Frequently Asked Questions

What should I do if my house isn’t selling?

If your house isn’t attracting buyers, various factors could be at play. The asking price may be too high, marketing efforts might be insufficient, or the house’s condition could be deterring potential buyers. Consult with your real estate agent to pinpoint potential problems and devise solutions. You may need to reduce the price, enhance your marketing strategy, or invest in necessary home improvements.

Can I sell my house myself instead of using a real estate agent?

Yes, selling your house yourself is an option. This is known as “For Sale By Owner” (FSBO). However, selling a house involves complex tasks like pricing, marketing, negotiating, and handling legal paperwork. Real estate agents possess the expertise and experience to deal with these challenges. If you opt for FSBO, be prepared for a significant time commitment and be ready to handle these tasks yourself.

How long does it usually take to sell a house?

The timeline for selling a house can vary greatly and depends on numerous factors, such as local market conditions, the home’s condition and price, and even the time of year. On average, it can take anywhere from a few days to a few months. Your real estate agent can give you a better estimate based on local trends and your specific situation.

What is a seller’s market, and how can it impact my home sale?

A seller’s market occurs when the demand for homes exceeds the current supply. This often results in homes selling more quickly and at higher prices. If you’re selling your house in a seller’s market, it can be an advantage as you may get multiple offers and a higher sale price.

Should I make repairs before selling my house?

Whether to make repairs before selling your house often depends on the type and extent of the repairs and the overall condition of your house. Small repairs and improvements, like painting or fixing leaky faucets, can make a good impression on buyers. If your home has more more substantial issues, discuss the repairs with your real estate agent to weigh the cost against the potential return on investment.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

MA non-judicial mortgage foreclosure can take about 120 days, or four months, to complete. Judicial foreclosures vary depending on your state. In California, this process can take two to three years.

A nonjudicial mortgage foreclosure can take about 120 days, or four months, to complete. Judicial foreclosures vary depending on your state. In California, this process can take two to three years.

If you’ve fallen behind on your mortgage payments, the threat of foreclosure can become overwhelming. If you wonder “How long does foreclosure take?” know that you still have options.

Understanding what you can do if your house is in foreclosure can help you mitigate the damage done to your credit and overall financial health. Depending on your situation, you might even discover how to save your home from foreclosure.

What Is Foreclosure?

Foreclosure means that your mortgage lender can legally repossess your house due to nonpayment. They can then sell your house to help repay the debt you owe on it. And this is true whether you are behind on your first or second mortgage. Home mortgage rates will define when lenders can begin the foreclosure process—this is typically determined by how behind on your payments you are.

Get matched with a personal

loan that’s right for you today.

Learn

more

Remember that every state has different rules and regulations for foreclosure procedures, and many states offer exceptions that may work in your favor. If you think you may be in danger of foreclosure, work with a legal professional to determine your state’s guidelines.

For example, in some states, you have to miss a certain number of payments before foreclosure processes can begin. Some states may also allow you to reinstate the loan up until a specific deadline.

What Happens When a House Goes Into Foreclosure?

State and federal laws, your mortgage agreement, and the mortgage holder’s personal decisions are major factors. Generally, the foreclosure process starts three to six months after you miss your first mortgage payment, assuming you don’t catch up on payments.

State laws vary, so work with a legal adviser or your lender to determine what will happen in your specific situation. In general, mortgage foreclosure involves the following steps:

The mortgage holder gives the defaulting homeowner a written notice of default. This is a formal notice that you have fallen behind on your payments and are in default.

The homeowner receives a limited amount of time to correct the default and pay all amounts due. That can include interest, penalties, attorney charges, and any other fees allowed by your state’s laws and your mortgage contract.

Once the time allowed for the homeowner to correct the default has passed, the mortgage holder will give notice of a foreclosure sale. This is the actual day of foreclosure.

Many states have a redemption period after the foreclosure sale, allowing you to reclaim your home.

Foreclosure actions can wipe out some of the property owner’s debt, such as the original mortgage, home equity loans, and second mortgages. However, you still have to pay any remaining costs associated with your second mortgage.

You might also be responsible for some of the mortgage payments even after losing your home. If the property sells for less than the balance owed on the original loan, a lender could file a deficiency judgment against you in court.

A deficiency judgment requires that you repay the difference and it lets the mortgage holder collect your assets to compensate for the debt. Not all states allow deficiency judgments in all circumstances. Work with a lawyer or legal adviser to determine your rights and plan of action.

Lenders’ Obligations in a Mortgage Foreclosure

Lenders have different obligations in different states. However, when it comes to mortgage foreclosures, they all typically have at least three common requirements:

Notice of default. In most states, lenders are required to provide a homeowner with sufficient notice of default. The lender must also provide notice of the property owner’s right to cure the default before the lender can initiate a foreclosure proceeding.

Written proof of money owed under the mortgage. Lenders are usually required to file statements that itemize the amount the property owner owes under the mortgage.

The amount owed includes the principal, interest, late charges, attorney fees, and any other charges the lender is permitted to charge under the terms of the mortgage or the laws of the state.

Service member relief. Lenders are also required to certify in writing that the property owner is not a member of the armed services before initiating a foreclosure action.

The Servicemembers Civil Relief Act is intended in part to protect deployed active-duty service people. If you are a member of the armed services, consult an attorney about your rights as they concern foreclosure proceedings.

Ways to Stop or Prevent a Foreclosure

The best way to stop a foreclosure is to take action to prevent the lender from beginning the process. When possible, try these proactive ways to save your home from foreclosure:

Catch up on your default. In many cases, the first notice of default provides you with options for catching up on what you owe. If you can make up your payments and stay current, the lender is much less likely to foreclose.

Ask for a loan modification. Many lenders will work with you if you need help making your loan payments. Home affordability programs can help you catch up on late payments or potentially reduce the amount you pay if you’re experiencing financial hardship.

Request a short sale. If you can’t afford your home anymore, you can request a short sale. The lender has to agree to a short sale, but if they do, you can sell the house to a third party for less than you currently owe.

In some states, the difference is forgiven, while in others, you may be required to pay the difference between the sale price and the remaining loan amount. A short sale will affect your credit, but the effect will be less than that of a foreclosure or bankruptcy.

File for bankruptcy. Filing a bankruptcy petition that includes your mortgage puts an automatic stay in place. This means that lenders can’t continue any type of collection procedure until the bankruptcy has been resolved or dismissed.

Whether or not you keep your home depends on what type of bankruptcy you file and whether you can work out mortgage payments in the future. Filing for bankruptcy can have severe consequences for your credit and finances. Consult with an attorney before moving forward with this option.

Defenses Against Foreclosure

If the lender has already filed for foreclosure and none of the options above will work for you, you might be able to legally fight the filing with a technical or substantive defense. Only you and your attorney can determine how to proceed through the process.

One example of a technical defense is when a property owner is not given adequate notice of the default and proceedings. However, technical defenses are often not very helpful in preventing foreclosures because a mortgage holder can easily correct the defense by correcting the procedural defect.

Substantive defenses use the terms of the mortgage itself to halt a foreclosure. Here are some examples of substantive defenses to the foreclosure process:

You aren’t in default, and the debt and interest have been paid on time according to the terms of the mortgage.

The mortgage holder committed fraud in obtaining the mortgage.

If you believe you may have a legal reason to stop the foreclosure, you need to file an objection to the sale with the court. In most states, you can file objections before the foreclosure sale takes place, after the sale takes place, or before the court ratifies the sale if the sale was improperly conducted.

When a debt is forgiven in a foreclosure action, taxpayers are considered to have made money. That means that the taxpayer or property owner may owe taxes on the difference between the value of the home and what is owed on the mortgage and forgiven in the foreclosure action. You will want to work with your tax professional to help determine your tax responsibility in this situation.

Consider this example to understand how it might work:

You owe $120,000 on the home. The bank sells your home for $100,000.

The bank accepts the $100,000 it got in the sale and forgives the rest of the debt via foreclosure, which means it doesn’t seek to collect that money from you.

The IRS considers that $20,000 as a form of income because it’s money you should have had to pay but didn’t. You might owe taxes on that $20,000.

Help Your Credit With Credit.com

Short sales and other foreclosure proceedings can hurt your credit by a substantial amount. Foreclosure can appear on your credit report for seven years. In many cases, you will be required to wait two to eight years before you can purchase another home.No matter what happens with a foreclosure, it’s a good idea to find out where your credit stands and how you can work to improve it. Credit.com provides a Free Credit Report Card that offers a look at your credit history and a better understanding of how you’re doing with the five factors that impact your score.

If you’re having a tough time getting home loan financing using a mortgage broker or a local mortgage lender, consider contacting a portfolio lender directly to close your mortgage.

They can offer solutions that others cannot, and may have just what you’re looking for. For example, a portfolio lender may be willing to offer you a no-down payment mortgage while others are only able to give you a loan up to 97% loan-to-value (LTV).

The same might be true if you have bad credit, a high DTI ratio, or any other number of issues that could block you from obtaining traditional mortgage financing.

What Is a Portfolio Loan?

A home loan unique to the lender offering it

That comes with special terms or features

Other mortgage lenders do not offer

It is kept on the bank’s books as opposed to being sold to investors

In short, a “portfolio loan” is one that is kept in the bank or mortgage lender’s loan portfolio, meaning it isn’t sold off on the secondary market.

By servicing the loans themselves and keeping them in portfolio, these lenders are able to take on greater amounts of risk, or finance loans that are outside the credit box because they don’t need to be resold to investors with specific underwriting guidelines.

These companies have the ability to bend the rules when they see a deal worth doing, whereas mortgage lenders that must adhere to Fannie Mae, Freddie Mac, and the FHA have very little wiggle room.

You see, most loans that are sold off are backed by Fannie and Freddie, or the FHA in the case of FHA loans, so very rigid underwriting standards must be met without exception.

Portfolio lenders, on the other hand, can create their own underwriting guidelines because they aren’t at the mercy of an outside agency if they’re actually willing (and able) to keep the loans they make.

A lot of small and mid-size lenders don’t have the same authority because they must sell their loans off on the secondary mortgage market due to liquidity constraints. And investors are becoming increasingly selective as to which loans are actually purchased.

Who Owns My Home Loan?

Most home loans are sold shortly after origination

So the bank that funded your loan likely won’t service it

Look out for paperwork from a new loan servicer after your loan funds

Unless it’s a portfolio loan

Many mortgages today are originated by one entity, such as a mortgage broker or mortgage lender, and then quickly resold to investors who earn money from the repayment of the loan over time.

Gone are the days of the neighborhood bank offering you a mortgage and expecting you to repay it over 30 years, culminating in you walking down to the branch with your final payment in hand. Well, there might be some, but it’s now the exception rather than the rule.

In fact, this is part of the reason why the mortgage crisis took place in the early 2000s. Because originators no longer kept the home loans they made, they were happy to take on more risk.

After all, if they weren’t the ones holding the loans, it didn’t matter how they performed, so long as they were underwritten based on acceptable standards. They received their commission for closing the loan, not based on loan performance.

Today, you’d be lucky to have your originating bank hold your mortgage for more than a month. And this can be frustrating, especially when determining where to send your first mortgage payment. Or when attempting to do your taxes and receiving multiple form 1098s.

This is why you have to be especially careful when you purchase a home with a mortgage or refinance your existing mortgage. The last thing you’ll want to do is miss a monthly payment right off the bat.

So keep an eye out for a loan ownership change form in the mail shortly after your mortgage closes. If your loan is sold, it will spell out the new loan servicer’s contact information, as well as when your first payment to them is due.

Portfolio Loans May Solve Your Financing Problem

Large loan amount?

High DTI

Low credit score

Recent credit event such as short sale or foreclosure

Late mortgage payment

Own multiple investment properties

Need an asset-based income loan

Now back to portfolio loans. If you’re having a tough time getting approved for a mortgage, or finding a particular type of loan, consider a portfolio lender.

As noted, these types of mortgage lenders can offer things the competition can’t because they’re willing to keep the loans on their books, instead of relying on an investor to buy the loans shortly after origination.

They also offer mortgages that fall outside the guidelines of Fannie Mae, Freddie Mac, the FHA, the VA, and the USDA.

That’s why you might hear that a friend or family member was able to get their mortgage refinanced with U.S. Bank or a similar portfolio lender despite having a low credit score or a high LTV.

So if you’re in need of a $5 million jumbo loan, or an interest-only mortgage, or something else that might be considered unique, look to portfolio lending to solve your financing woes.

They may also be able to work with you if you’ve experienced a recent credit event, such as a late mortgage payment, a short sale, or a foreclosure. Really, anything that falls outside the box might be considered by one of these lenders.

Some of the largest portfolio lenders include Chase, U.S. Bank, and Wells Fargo, but there are many smaller players like Bank of Internet, BancorpSouth, Caliber Home Loans, and Wintrust Mortgage.

Portfolio Loan Rates

Portfolio mortgage rates may be higher

Than typical home loan rates

Because the loan programs aren’t necessarily available everywhere

Meaning you may pay for the added flexibility

Now let’s talk about portfolio loan mortgage rates, which as you might suspect, may not be as low as the competition.

Ultimately, many mortgages originated today are commodities because they tend to fit the same underwriting guidelines of an outside agency like Fannie, Freddie, and the FHA.

As such, the differentiating factor is often rate and closing costs, since they’re all basically selling the same thing. You may also see customer service, or in the case of Rocket Mortgage by Quicken Loans, a quirky ad campaign and some unique technology.

For portfolio lenders who offer a truly unique product, loan pricing could be entirely up to them, within what is reasonable. If the loan program is really special, and only offered by them, expect rates significantly higher than what a typical market rate might be.

If their portfolio home loan program is just slightly more flexible than what the agencies mentioned above allow, mortgage rates may be comparable or just a bit higher.

It really depends on your particular loan scenario, how risky it is, if others lenders offer similar financing, and so on.

At the end of the day, a portfolio loan is a solution that isn’t offered by every bank, so you should go into it expecting a higher rate. But if you can get the deal done, it might be a win regardless.

MoMo Productions/ Getty Images; Illustration by Austin Courregé/Bankrate

Portions of this article were drafted using an in-house natural language generation platform. The article was reviewed, fact-checked and edited by our editorial staff.

Key takeaways

VA loans are mortgages guaranteed by the U.S. Department of Veterans Affairs, available to eligible veterans, active-duty service members and surviving spouses.

VA loans can be used to purchase a primary residence, refinance a current mortgage or cover renovation costs.

VA loans offer several benefits, including no required down payment, no private mortgage insurance (PMI) and competitive interest rates.

A VA loan is a great option for you if you’re a qualifying active-duty military personnel or veteran. They often have more relaxed financial requirements than conventional loans, requiring no down payment or private mortgage insurance. They also typically have lower interest rates than FHA and conventional loans.

Here’s a breakdown of what VA loans are, how they work and how you can get one.

What is a VA loan?

A VA loan is a loan guaranteed by the U.S. Department of Veterans Affairs (VA). That’s not to say the VA provides these loans. Instead, mortgage lenders offer VA loans, knowing that the government guarantees them. This makes lenders more confident in lending, often offering a VA loan with a lower interest rate than a conventional mortgage.

The VA doesn’t officially set a credit score requirement for these loans. Instead, it leaves this up to the lender, with lenders requiring anywhere from a 580 to 640 minimum score. VA loans don’t require a down payment, which can make homeownership more attainable for those who qualify because you’ll need less money upfront.

How does a VA loan work?

Getting a VA loan is similar to securing a conventional loan.

Basically, you fill out paperwork from the VA that verifies your eligibility for the program. You also receive what’s known as your entitlement, which is the dollar amount guaranteed on each VA loan. While VA loans technically have no loan limit, lenders might be willing to loan up to four times the amount of your entitlement.

You can get a VA loan with no money down and, unlike other loans, you won’t have to pay for mortgage insurance. That’s because the government guarantees your loan. However, you’ll need to pay a funding fee, which costs a certain percentage of the loan total. This fee keeps the program functioning so future veterans and service members can use it.

Types of VA loans

VA loan type

Description

VA mortgage

Allows qualified service members to purchase a home with no minimum down payment.

VA construction loan

Eligible service members can use this loan to build the home of their dreams.

VA rate-term refinance

Allows service members without an existing VA loan to change their loan term or secure a lower interest rate.

VA cash-out refinance

Allows service members to swap their conventional mortgage with a VA loan, with an option to turn home equity into cash if needed.

IRRRL loan

Allows service members to replace a VA mortgage with a VA Interest Rate Reduction Refinance Loan (IRRRL), which can offer lower interest rates. It can also be used to change from an adjustable-rate loan to a fixed-rate loan.

VA rehab and refinance

Can be used by service members to finance the cost of improvements made to the home.

VA jumbo loan

Allows service members to finance a home with a sales price exceeding the conforming loan limits.

Native American loan

Available to Native American veterans to help them purchase, build, improve or refinance a home located on federal trust land.

Who qualifies for a VA loan?

The VA sets service requirements for active-duty military personnel and veterans to qualify for a VA loan. You can check the full eligibility requirements on the VA’s website, but the basics are:

You’re currently on active military duty, or you’re a veteran who was honorably discharged and met the minimum service requirements.

You served at least 90 consecutive active days during wartime or at least 181 consecutive days of active service during peacetime.

Or, you served for more than six years in the National Guard or Selective Reserve.

If your spouse died in the line of duty, you may qualify for a VA loan.

The first step in applying for a VA loan is getting a VA Certificate of Eligibility (COE). This certificate shows the lender that you meet the VA loan requirements for eligibility.

How to apply for a VA loan Certificate of Eligibility (COE)

You can get a VA loan Certificate of Eligibility by applying through your eBenefits portal online or applying through your lender.

To apply, you need to provide some data based on your current status. Veterans need to provide a DD Form 214, and active-duty service members need a signed statement of service. A statement of service should include:

Full name

Date of birth

Social Security number

The date you started duty

Any lost time

Name of the command providing the information

Different requirements may apply for National Guard or Reserve members, as well as surviving spouses. You can find more information through the VA’s benefits website, or by speaking to a qualified lender.

Other VA loan requirements

You should also keep these VA loan requirements and rules in mind:

VA loan limit: As of 2020, if you have full entitlement, there is no limit on the size of your loan. However, your lender may impose its own terms, and your entitlement will still be pegged to conforming mortgage limits.

You do have a home loan limit if you have remaining entitlement: You have an active VA loan you’re still paying back; or you paid a previous VA loan in full and still own the home; or you refinanced your VA loan into a non-VA loan and still own the home; or you had a compromise claim (or short sale) on a previous VA loan and didn’t repay it in full; or you had a deed in lieu of foreclosure on a previous VA loan; or you had a foreclosure on a previous VA loan and didn’t repay it in full.

If you have remaining entitlement, your VA home loan limit is based on the county loan limit where you live. This means that if you default on your loan, the VA will pay your lender up to 25 percent of the county loan limit minus the amount of your entitlement you’ve already used. Check your county loan limit here.

Property type: Investment properties and vacation homes cannot be purchased using VA loan proceeds. Furthermore, you must occupy the home and use it as your primary residence.

Credit score: The VA does not specify a minimum credit score requirement. However, borrowers might have a hard time getting approved by a lender if they don’t have at least a 620 FICO Score.

Income: Borrowers need to show they have the income to make the mortgage payments. It’s equally important to not have a huge debt load since the lender will assess your debt-to-income ratio (DTI), or the percentage of your monthly income that’s spent on debt payments.

Assets and down payment: There is no down payment requirement for VA loans, but the lender may have overlays (or specific criteria) that mandate a down payment in place for borrowers with lower credit scores.

Reserve funds: Many lenders require borrowers to have an adequate amount of reserves — generally two to three months of mortgage payments — before clearing you to close on your loan.

It’s also possible to use home loan benefits after bankruptcy, as long as sufficient time has passed, typically two years after filing for Chapter 7 bankruptcy or 12 months after Chapter 13 bankruptcy.

VA home loan pros and cons

For those who are eligible, VA loans have many benefits, but they also have drawbacks to consider.

Pros of a VA loan

Some of the key advantages of VA loans include:

Lower borrowing costs: VA loans can be cheaper than their conventional mortgage counterparts.

No down payment: VA loans allow you to purchase a home with zero down payment, making homeownership more accessible for those who may struggle to save a large lump sum. You need at least 3 percent down for a conventional mortgage.

No mortgage insurance: Unlike many other types of mortgages, VA loans do not require you to pay private mortgage insurance (PMI), potentially saving you hundreds of dollars per month.

Competitive interest rates: Because the government guarantees these loans, lenders are able to offer lower interest rates than you’d typically find with conventional loans.

Capped lender fees: The VA limits lender fees (like loan origination fees) to 1 percent of the loan amount. This can result in lower closing costs than other loan types.

Cons of a VA loan

Despite the many benefits, VA loans also have a few downsides to consider:

VA funding fee: VA loans come with a funding fee that can vary depending on your military category, down payment amount and whether you’ve previously used a VA loan. You can finance this fee into the loan amount, adding to the total cost of the loan, or you can pay it upfront at closing.

Limited to primary residences: You can only use VA loans to purchase a primary residence, not vacation homes or investment properties. However, you can buy up to a four-unit property with a VA loan as long as one unit is your primary residence.

Not all properties qualify: Not every property will meet the VA’s minimum property requirements (MPRs), which can limit your potential housing options.

Longer closing process: The VA loan process can take slightly longer than other loan types due to extra steps such as the VA appraisal.

How to apply for a VA loan

After you’ve obtained your COE and are ready to apply, there are a few steps you need to take:

Gather your financial paperwork.

Look for lenders that offer VA loans.

Get approved for a VA loan through at least three lenders.

Compare each lender’s offer and choose the best option.

Shop for a home and submit an offer.

Have a seller accept your offer and get a signed purchase agreement with the seller.

Get a VA home appraisal and inspection.

Work with the lender through the underwriting process, promptly responding to questions and requests for documentation.

If you’re struggling with your VA loan, there’s extra help available. The VA can help you negotiate with your lender if you can’t make payments. With the help of the VA, it’s possible to avoid foreclosure through loan modification or other repayment plans. Call 877-827-3702 if you need help.

VA loan FAQ

VA loans can have term lengths of 10 to 30 years. In addition, they can be fixed-rate or adjustable-rate mortgages (ARMs). The interest rates for VA loans are typically lower than those for conventional loans, mainly because the VA guarantees a portion of the loan, which reduces the risk for the lender. These rates change frequently, so check Bankrate’s VA home loan rates to compare offers from different lenders.

A key feature of VA loans is the entitlement. This is the amount of the loan that the VA will guarantee to the lender if you default. There are two types of entitlement:

Basic entitlement: Up to $36,000 for loans worth less than $144,000, or 25 percent for loans of that amount or more.

Bonus entitlement: Up to 25 percent of the Federal Housing Finance Agency (FHFA) loan limit, minus the basic entitlement.

If you’re purchasing a loan that costs more than $144,000, the bonus entitlement can be used.

No, VA loans don’t require PMI or any other mortgage insurance. That’s because the VA loan entitlement usually amounts to more than 20 percent of the home’s value. However, while you won’t need to pay for mortgage insurance, you will have to pay a funding fee.

As with any mortgage, different lenders have various closing costs. You might need to pay for discount points, a credit check, VA appraisal fees, title insurance and other costs, including local and state taxes. While you don’t have to worry about PMI, you do have to pay a VA funding fee. Your VA funding fee depends on the size of your VA loan down payment, and whether it’s your first-time use of the benefit.

Down payment

First-time use

Subsequent use

0%-5%

2.15%

3.30%

5%-9.99%

1.50%

1.50%

10% or more

1.25%

1.25%

So, while a VA loan down payment isn’t required, it can save you money to make a down payment.

Quick note: Disabled veterans who receive disability benefits are exempt from the VA funding fee.

Also, it’s possible to wrap your VA closing costs into the loan amount. However, that increases how much you need to borrow and can cost you more.

I’ve already written about it not being the best time to buy a home right now, at least from a pure investment standpoint.

In short, home prices are expensive relative to incomes, mortgage rates have more than doubled, and there’s little quality inventory.

And now we can quantify just how long it takes to break even on a house, per a new analysis from Zillow.

Hint: it’s a long, long time, even if you’re able to muster a big 20% down payment.

So if you’re thinking about buying a home today, prepare to stick around for the long-haul.

How Long to Break Even on a House These Days?

– 3% down payment: 13 years and six months to make a profit. – 5% down payment: 13 years and three months to make a profit. – 10% down payment: 12 years and seven months to make a profit. – 20% down payment: 11 years and three months to make a profit.

A new Zillow analysis tried to determine how long you’d need to own your home before you could sell it for a profit.

This factors in the closing costs associated with the home purchase, the mortgage interest paid, home maintenance costs, and the sales costs once it came time to list the property.

Specifically, they assume 3% closing costs at purchase, 1% home maintenance fees, and 6% in closing costs at the time of sale, along with all that mortgage interest.

In reality, it could be even higher. It’s not unusual for real estate agents to charge 5-6% of the sales price.

So if you’re putting down just 3%, you’re already in the hole, especially once you consider those closing costs as well.

To offset all those expenses, you need to make regular payments to principal each month and hope the property appreciates in value over the years as well.

The rule of thumb says it normally takes about 3-7 years to break even on a home purchase, with perhaps five years the average.

But that number has risen sharply lately thanks to a combination of sky-high asking prices and equally expensive mortgage rates.

How long you ask? Per Zillow, home buyers today can expect to spend approximately 13.5 years in their house before being able to sell at a profit!

In other words, you better really like your house unless you want to sell for a loss, or worse, be forced to do a short sale.

It Takes More Time to Turn a Profit in Affordable Housing Markets

And here’s the irony. It actually takes longer to turn a profit in more affordable housing markets.

Those purchasing a home in places like Cleveland, Baton Rouge, El Paso, Akron, or Indianapolis might need to wait at least 20 years to reach this crucial profit point.

As for why, it’s because of the slower historical growth rate in these more affordable areas.

Without home price appreciation doing most of the heavy lifting, it takes a lot more time to build home equity.

Simply put, principal payments are a lot less impactful than increases in property values, especially on a high-rate mortgage where most of the payment goes toward interest.

It’s the worst in Cleveland, where Zillow says it can take a whopping 22 years and 10 months to turn a profit.

Similar timelines can be seen in the other metros mentioned, meaning it’s not always advisable to buy a home just because it’s cheap.

There’s a Faster Road to Profit in Expensive Housing Markets

Again, while seemingly counterintuitive, it’s actually easier to turn a profit if you buy a home in an expensive metro.

Of course, the barrier to entry will likely be higher, but it’s one of those rich get richer stories.

For example, in notoriously expensive Bay Area metros such as San Jose or San Francisco, California, the break-even timeline to profit is a much shorter 7 to 7.5 years.

This is still a long time historically speaking, but it is considerably less than in those “cheap” housing markets.

Similar short purchase-to-sale profit timelines can be found in San Diego, Los Angeles, and Miami.

As you can see, these are highly-sought after cities where demand always tends to be strong, and supply always low. And because of that, home prices are often rising.

But there’s a big barrier to entry, whether it’s the high asking price or the large down payment required.

Either way, this data tells us it might not be the best time to purchase a home at the moment, even if you can muster a 20% down payment.

It could be advantageous to wait for a better combination of lower asking prices, cheaper mortgage rates, and better inventory.

Of course, there are reasons to buy a home other than for the investment. But you still need to be prepared to stick around for a while.

Read more: Pros and cons of renting vs. buying a home

About a week ago, Bank of America released details of its so-called “Mortgage to Lease” program, which as the name implies, allows homeowners to lease the homes they previously mortgaged.

So let’s take a closer look to see just what Bank of America is doing here.

First things first, this is a very limited pilot program, so don’t assume you can head down to Bank of America, fill out some paperwork, and then ditch your pesky mortgage but not your beloved house.

In fact, fewer than 1,000 customers will be “invited” to participate in the Mortgage to Lease program, meaning your chances of being selected are only slightly better than winning the Mega Millions jackpot.

Additionally, only homeowners in Arizona, Nevada, and New York are part of the pilot, so if that’s not you, you’re out of luck, at least for the moment.

Requirements for the Mortgage to Lease Program:

[checklist]

Mortgage is owned by Bank of America

Mortgage is 60 days + delinquent

All other loan modification solutions have been exhausted or ignored

Face high risk of foreclosure

Have no second mortgages

Still occupy the home

Have enough income to make affordable rent payments

[/checklist]

So while this looks like a lengthy list, it’s probably not all that uncommon. Well, the lack of second mortgages probably is, as most homeowners who are currently in trouble went with 100% financing. And most used second mortgages to get there.

But for those with one loan who still managed to find themselves underwater, or at least behind on mortgage payments, and couldn’t manage a short sale or deed-in-lieu of foreclosure, this program may be a winner.

That is, if you actually want to stay in the home that gave you so much heartache.

How the Mortgage to Lease Program Will Operate

Assuming you do, participants in the program will agree to transfer title of their home to Bank of America, and their outstanding principal will be forgiven. In other words, you won’t owe the bank anything for owing more than the mortgage is worth.

In exchange, you’ll have the opportunity to rent the house you currently reside in for up to three years, with rental payments set at or below the current market rental rate.

The rental payment will be less than the old mortgage payment, and the homeowner will be relieved of normal homeowner costs, such as homeowners insurance and property taxes.

Bank of America will have a property management company oversee the rental properties, and eventually the inventory of homes will be transitioned to investor ownership.

However, if all goes well, the investors can keep the tenants in the homes for as long as they see fit. And possibly even sell them back to the homeowners.

Will it Work?

Bank of America’s Mortgage to Lease program isn’t at all groundbreaking. In fact, Fannie Mae’s very similar Deed for Lease program has been around for more than two years.

Regardless, it seems like Bank of America’s new initiative is very limited in scope, and only targets customers who have made no effort to change their unfortunate situation.

If anything, it seems like a last gasp opportunity to avoid a foreclosure for BofA (and the losses that come with it), while the homeowner in question is probably just seeing how long they can hang on without making a payment (free rent).

My guess is a homeowner that hasn’t shown any interest in a loan mod or any other foreclosure alternative probably won’t be all that interested in this program, given the only upside is staying in a house they can’t afford, or aren’t willing to fight for.

Above is a collection of words that essentially illustrate (and sum up) what I’ve written about over the past six years on this blog.

I recently came across a website called Wordle that lets you create “beautiful word clouds,” which are indeed powerful.

I simply began writing down any words that came to mind, all of which you’ll find on this website in one post or another.

Some virtually unknown concepts have become household names, like short sale and underwater mortgage. Back in 2006, most homeowners could hardly imagine anything so terrible would happen to them.

But this is the new reality we face.

The last several years have been a roller coaster ride for homeowners in America, and while it looks like things appear to be getting better, we aren’t out of the woods yet.

And what has taken place over the past several years won’t soon be forgotten.

When all is said and done, millions of homeowners will have been displaced thanks to the ongoing mortgage crisis. And we have all been affected, whether we rent or own.

So take a moment to reflect and look back. This has definitely been a defining moment in history.

Hopefully we’ll learn from our past mistakes and make better decisions going forward to avoid another collapse, but history tends to have a habit of repeating itself…

Click on the photo above to see the larger, original version.

The Federal Housing Finance Agency, which oversees Fannie Mae and Freddie Mac, has released details of a new program to expedite short sales.

The program consolidates Fannie and Freddie’s current short sale programs, including the original Home Affordable Foreclosure Alternative (HAFA) programs and other proprietary ones.

The new streamlined approach will be known as the “Standard Short Sale/HAFA II,” and is designed to make short sales easier for those most in need.

Short Sales for Those Still Making Payments

First and foremost, the new guidelines will allow homeowners with Fannie or Freddie mortgages to pursue a short sale, even if they are current on their mortgage payments, assuming they have an eligible hardship.

At the moment, it’s difficult (but not impossible) to get a short sale going unless you fall behind on your payments, which kind of defeats the purpose of attempting to avoid full-blown foreclosure.

With HAFA II, loan servicers will be able to quickly qualify such borrowers without any additional approval from Fannie or Freddie.

Common hardships listed by the FHFA include unemployment, divorce, long-term disability, increased housing expenses, disaster (natural or man-made), business failure, and death of a borrower or household wage earner.

The streamlined process will also work for those who are transferred to a job or accept a new career opportunity more than 50 miles away.

This should help more borrowers conduct short sales without the massive credit score hits associated with multiple missed mortgage payments.

[Short sale vs. foreclosure with regard to credit]

Fannie and Freddie have also agreed not to pursue a deficiency judgment in exchange for a small financial contribution (assuming the borrower has sufficient income/assets).

It’s unclear how small it may be, but I would venture to say that most homeowners won’t want to pay it.

Service members who are relocated will also be automatically approved for short sales, even if current on their mortgages (and they won’t be subject to paying the contribution).

Quicker Short Sales for Those Already Behind

HAFA II also addresses those who are already behind on their mortgage payments and sailing full steam toward foreclosure.

These borrowers will enjoy an expedited approach to better deal with the time sensitive nature of the foreclosure process.

This means the documentation needed to demonstrate hardship may be reduced or even eliminated in some cases.

To further speed things up, or at least not unnecessarily slow things down, Fannie and Freddie will offer up to $6,000 to second mortgage holders to accelerate the short sales.

At the moment, a secondary lien holder can slow down a short sale by negotiating for a larger chunk of the outstanding balance, effectively stalling the entire process.

So hopefully the $6,000 will be enticing enough to speed along the process in most cases.

The new guidelines will also provide clarity on processing a short sale if a foreclosure sale is pending so borrowers can get last minute offers in and avoid losing their home.

Currently, loan servicers are required to review and respond to short sale offers within 30 days of receiving them.

They must also provide weekly status updates if the short sale is still under review after 30 days, and must finalize decisions within 60 days of the receipt of the offer.

Note: Borrowers who take part in the program will not be eligible for another mortgage backed by Fannie or Freddie for at least two years after the short sale occurs.

The HAFA II program will be effective come November 1, 2012.

There’s been a lot of confusion about short sales, especially with regard to how they affect one’s credit score.

Plenty of people have recommended them as an alternative to foreclosure, even going as far as to say they can spare you the nasty credit score ding.

And while they can be a worthwhile foreclosure alternative, the credit score impact really isn’t much different.

This has been an issue for a while because common sense and logic would tell you that a short sale is better than foreclosure.

Being a Good, Bad Borrower

After all, if you choose to short sell your home, you’re making a conscious effort to work with your lender.

As opposed to hastily packing your things and heading for the hills, or stripping your home of its precious copper and selling it on the black market.

That should be rewarded, right? And the mortgage crisis was a one-off event, which made good consumers “break bad.”

If anything, agreeing to a short sale should tell other creditors that you mean well, even if you can’t or don’t want to continue making your monthly mortgage payments on your underwater home.

Unfortunately, this sentiment hasn’t translated to higher credit scores. Fico still sees foreclosures and short sales as very similar negative events.

But why? Aren’t they totally different?

Data Backs It Up Folks

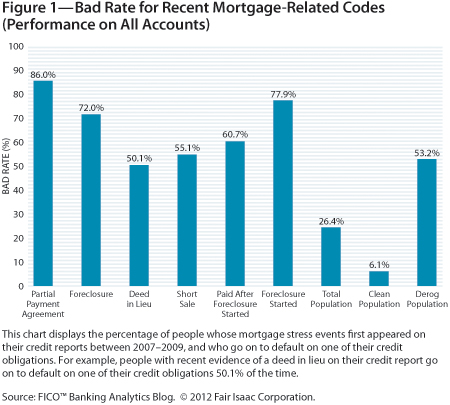

Whether foreclosures and shorts sale are similar or not, data collected by Fico proves that those who short sell are higher risk than other borrowers.

Fico looked at data from October 2009 to October 2011, discovering that more than one out of every two borrowers who experienced a short sale defaulted on another credit account within two years.

The number was actually 55.1%. Yikes. Does this mean the floodgates were opened post-short sale? That the veritable seal was broken for many of these borrowers?

Was their moral compass thrown and no longer incentive enough to keep up with their obligations? Or was it that the short sale itself really coincided with financial distress?

Whatever the reason, it’s clear (from the data) that short sales and risk go hand in hand.

As you can see from the chart, credit default risk post-foreclosure was even higher, at a rate of 72%.

But Fico didn’t feel the difference (about 17%) was material enough to merit a “more positive treatment” for short sales.

Additionally, most short sellers have mortgage delinquencies on their credit reports.

To compare, roughly only one in 50 borrowers with a Fico score in the high 700 range defaults on one of their credit obligations.

So clearly having that number jump from one to 25 is an issue, which explains why Fico smacks the credit scores of those who experience a short sale.

What About Loan Mods and Fico Scores?

There have also been a lot of questions about how loan modifications affect credit scores, or more specifically, Fico scores.

Will that HAMP loan modification hurt your credit score, or is it just treated as a standard refinance?

Currently, Fico says there is no impact (beyond perhaps a credit inquiry) as long as the loan mod is reported using the proper Consumer Data Industry Association (CDIA) comment codes.

There was even a bill introduced to ensure loan mods didn’t hurt consumer credit scores.

But Fico is currently evaluating whether the incidence of such events leads to greater credit risk.

In other words, if the findings are similar to short sales, consumers who agree to a loan mod could see their Fico scores take a hit as well.

But only time will tell on that one, since the data is so fresh. There’s plenty of re-default data out there though, so you have to wonder.