Airbnb is back in the headlines in Los Angeles: Thousands of short-term rental hosts are breaking the law, and the city isn’t taking the problem seriously enough.

If this sounds like a familiar story, it is. In 2019, shortly after the city had announced it was beginning to enforce its short-term rental rules, I found that illegal rentals were still flourishing. My follow-up studies in 2021 and 2022 showed the same thing.

Advertisement

Why should we care about illegal short-term rentals? The simple answer is that they are making housing scarcer and less affordable for Angelenos. A landmark study led by Kyle Barron of the National Bureau of Economic Research found that Airbnb was responsible for nearly one-fifth of all the residential rent increases in the United States between 2012 and 2016. A Los-Angeles specific study led by Hans Koster from Vrije Universiteit Amsterdam found that between 2014 and 2018, Airbnb was responsible for a more than 30% increase in housing prices in Venice, as well as large price increases in other major tourist destinations in Los Angeles.

Higher housing costs directly increase homelessness. Looking at the impact of short-term rentals in Los Angeles from 2014 through 2022, I estimated that short-term rentals are responsible for 5,000 extra Angelenos experiencing homelessness each night. This is a human tragedy but also a financial one — it would cost the city $1.3 billion to build enough supportive housing to accommodate them.

Short-term rental hosts in Los Angeles are required to get a license from the city, and they’re allowed to operate a rental only out of their own principal residence. But these rules don’t seem to be working. When I crunched the numbers last year, I found that nearly half of the short-rentals operating in Los Angeles are illegal. A big portion had no license number at all, a quarter of the listings with a license number were using a fake or expired one, and many more were clearly commercial operations rather than home-sharing arrangements involving a principal residence.

What should the city be doing about this? First, it should get serious about collecting fines from short-term rental hosts who are breaking the rules. A year ago, records from the city indicated that it was collecting less than $4,000 a month in home-sharing ordinance fines. Yet by my analysis, if every host who broke the rules were paying the proper fines, that number should be more than a thousand times larger — at least $50 million per year.

In practice, if the city started rigorously enforcing its own rules, hosts would stop breaking the law with such impunity and the fines collected would go down. But that’s a good thing: Similar to the approach of imposing so-called “sin taxes” on alcohol and cigarettes, part of the rationale for aggressively enforcing fines would be to discourage a socially harmful activity, not simply to raise revenue from that same activity.

Advertisement

Second, in addition to going after hosts, the city should hold short-term rental companies — Airbnb, but also the many smaller players in the market — financially responsible for illegal activities occurring on their platforms. Currently the home-sharing ordinance mandates fines of $1,000 per day for platforms accepting reservations for illegal listings, but such fines are rarely collected. The city should start collecting them widely and increase their size to the point that the platforms have no choice but to start taking them seriously.

The government of Quebec, where I live and work, has introduced fines of up to $100,000 per listing that does not have a valid license number. These numbers are tantamount to saying to Airbnb and the other platforms “follow the rules or leave town,” and it is long past time for Los Angeles to take the same approach.

Finally, the city should rescind its extended home-sharing licenses. These licenses allow hosts to offer short-term rentals year-round, and they enrich a small number of commercial operators at the cost of residents paying more for their own housing. In a city with as many high-quality tourist accommodation options as Los Angeles, there is no conceivable public interest rationale for letting scarce housing serve as de facto hotels. Whatever revenue the city brings in via transient occupancy taxes is swamped by the extra housing costs imposed on Los Angeles residents.

Home sharing can be a win-win for Los Angeles’ economy and housing market. A modest amount of part-time rentals would offer visitors a wider range of accommodation options while helping some residents meet their housing costs. But this works only if the city starts insisting that short-term rental hosts and platforms play by the rules — and starts punishing them if they don’t.

David Wachsmuth is an associate professor of urban planning at McGill University and the Canada Research Chair in Urban Governance.

At last glance, 30-year fixed mortgage rates were sitting above 7%. Despite this, there are virtually no homes for sale.

One would assume that after such a massive interest rate spike, demand would flounder and supply would flood the market.

Yet here we are, looking at a housing market that has barely any for-sale inventory available.

And when you remove the new home inventory (from home builders) from the equation, it’s even worse.

Let’s explore what’s going on and what it might take to see listings return to the market.

Why There Are No Homes for Sale Right Now?

The housing market is highly unusual at the moment, and has been for quite some time.

In fact, since the pandemic it’s never really been normal. The housing market came to a halt in early 2020 as the world stopped, but then took off like a rocket.

If you recall, the 30-year fixed spent the entire second half of 2020 in the sub-3% range, fueling voracious demand from buyers.

And as Zillow pointed out, the age demographics had already lined up nicely for a surge of demand anyway.

Around that time, some 45 million Americans were expected to hit the typical first-time home buyer age of 34.

When you combined the demographics, the record low mortgage rates, a pandemic (which allowed for increased mobility), and already limited inventory, it didn’t take much to create a frenzy.

At the same time, you had existing homeowners buying up second homes on the cheap, due to those low rates and generous underwriting guidelines.

And let’s not forget investors, who were taking advantage of the very accommodative interest rate environment and the insatiable demand from buyers.

The rise of Airbnb and short-term rentals (STRs) coincided with this low-rate environment, potentially taking additional inventory off the market.

This quickly depleted supply, which was already trending down thanks to a lack of new home building after the prior mortgage crisis.

Home builders got burned in the early 2000s as foreclosures and short sales spiked and prices plummeted. And their excess supply sat on the market.

As a result, they developed cold feet and didn’t build enough in subsequent years to keep up with the growing housing needs of Americans.

Collectively, all of these events led to the massive housing supply shortage.

Low Mortgage Rates Got Buyers in the Door, But Will They Ever Leave?

Low supply aside, another unique issue affecting housing supply is a concept known as mortgage rate lock-in.

In short, there’s an argument that today’s homeowners have such low mortgage rates that they won’t sell. Or can’t sell.

Either they don’t want to give up their low mortgage rate simply because it’s so cheap. Or they are unable to afford a home purchase at today’s rates and prices.

Simply put, most can’t trade in a 3% rate for a 7% rate and purchase a home that’s probably more expensive than theirs was a few years earlier.

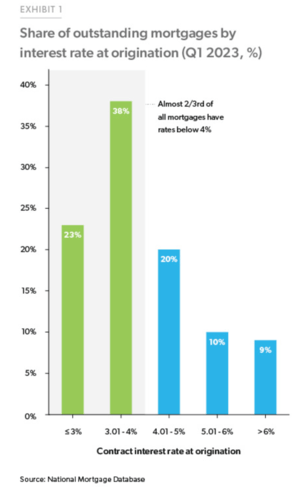

And this isn’t some tiny subset of the population. Per Freddie Mac, nearly two-thirds of all mortgages have an interest rate below 4%.

And nearly a quarter have a mortgage rate below 3%. How on earth will these folks sell and buy a replacement home if prices haven’t come down, but have in fact risen?

The answer is most will not budge, and will continue to enjoy their low, fixed-rate mortgage for many years to come.

This further explains why inventory is so tight and not really improving, despite the Fed’s attack on housing demand via 11 rate hikes.

[Why are home prices not dropping?]

Housing Supply Is at an All-Time Low

Redfin reported that the total number of homes for sale hit a record low in August.

Active listings were down 1.1% month-over-month on a seasonally adjusted basis, and a whopping 20.8% year-over-year.

That’s the biggest annual decrease since June 2021. However, new listings have ticked higher the past two months on a seasonally adjusted basis.

In August, new listings increased 0.8% from a month earlier after increasing the month before that.

But due to nearly a year’s worth of monthly declines prior to that, new listings were still off a big 14.4% year-over-year.

This meant months of supply stood at just two months, well below the 4-5 months usually considered healthy.

Redfin Economics Research Lead Chen Zhao noted that “new listings have likely bottomed out,” arguing that those who are locked in by low rates have already decided not to sell.

That leaves those who must sell their property, due to stuff like divorce or a change in work-from-home policy.

Interestingly, even some WFH homeowners are moving back closer to work, but keeping their homes because they can rent them out.

Because homeowners got in so cheap, it’s not out of the question to keep the old house and go rent or buy another property.

All of this has created a huge dearth of existing home supply, but there is one winner out there.

Home Builders Are Gaining a Ton of Market Share

While existing homes, also known as previously-owned or used homes, are hard to come by, newly-built homes are somewhat plentiful.

In fact, newly built single-family homes for sale were up 4.5% year-over-year in June, per Redfin, while existing homes for sale were down 18%.

And roughly one-third of homes for sale were new builds, up markedly from prior years and well above the norm that might be closer to 10%.

Astonishingly, new homes accounted for more than half (52%) of single-family homes for sale in El Paso, Texas.

Similar market share could be seen in Omaha (46%), Raleigh (42.1%), Oklahoma City (39%), and Boise (38%).

Meanwhile, the National Association of Realtors (NAR) predicts that new home sales will increase 12.3% this year, and 13.9% in 2024.

As for why home builders are seeing a big increase in market share, it’s mostly due to a lack of competition from existing home sellers.

In short, they’re the only game in town, and they don’t need to worry about finding a replacement property if they sell (like existing homeowners)

Additionally, they’re able to tack on huge incentives such as rate buydowns, including temporary and permanent ones, along with lender credits.

This allows them to sell at higher prices but make the monthly payment more palatable for the buyer.

Perhaps more importantly, it allows buyers to still qualify for a mortgage at today’s sky-high prices.

When Will More Homes Hit the Market?

For now, this new reality is expected to be the status quo. After all, those with so-called golden handcuffs have 30-year fixed-rate mortgages.

That means they can continue to take advantage of their dirt-cheap mortgage for the next few decades.

This includes second home owners and investors, who got in cheap when prices were much lower and mortgage rates were also on sale.

Meanwhile, the home builders don’t seem to be going nuts with supply, and even if they ramped up production, it wouldn’t satisfy the market.

Remember, existing home sales typically account for around 85-90% of sales, so builders won’t come close to satisfying demand.

The only real way we get a big influx of supply is via distress, sadly. That could be the result of a bad recession with mass unemployment.

And it could be triggered by the 11 Fed rate hikes already in the books, coupled with a lack of new stimulus and the resumption of things like student loan payments.

Compounding that is sticky inflation, which has made everything more expensive and is quickly depleting the savings accounts of Americans.

But even then, you could argue that a mass loan modification program would be unveiled to at least keep owner-occupied households in their properties.

Considering how cheap their housing payments are, assuming they’ve got a low fixed-rate mortgage, it’d be hard to find them a cheaper alternative, even if renting.

In the early 2000s this wasn’t the case because the typical homeowner held a toxic mortgage, such as an option ARM or an interest-only loan. And many weren’t even properly qualified to begin with.

Read more: Today’s Housing Market Risk Factors: Is Real Estate in Trouble?

This article is reprinted by permission from NerdWallet.

Mortgage rates have risen to their highest levels in more than 20 years, making it harder to afford a home. And yet, out of necessity or desire, hundreds of thousands of people buy homes every month.

With the 30-year fixed rate topping 7%, NerdWallet asked real estate agents and mortgage loan officers for advice on how home buyers can stretch their homebuying dollars in this time of high interest rates. Here are nine tactics that they suggested.

1. Ask the seller to reduce the mortgage rate

Temporary mortgage rate buydowns have become commonplace since rates surged in early 2022. With a temporary rate buydown, the seller pays a portion of the buyer’s interest payments upfront. This reduces the house payments for the first one, two or three years of ownership.

“This is a common strategy for new-home builders, but it can also be used in the purchase of resale homes,” said John Bianchi, executive vice president for loanDepot. (All sources in this story commented via email.) “Negotiating a temporary buydown with the seller can help soften the blow of high interest rates, reducing your monthly payment for one to three years.”

In one typical setup, the seller’s payment effectively cuts the buyer’s interest rate by 2 percentage points in the first year, and by 1 percentage point in the second year. After that, the buyer pays the full interest rate. This is known as a 2-1 buydown.

Another option is to reduce the mortgage rate permanently, using discount points. One discount point equals 1% of the loan amount; each point typically reduces the interest rate by around 0.25 percentage point.

“Home buyers have an opportunity to get a seller to pay for these methods to lower their interest rate,” said Chuck Vander Stelt, a real estate agent in Valparaiso, Indiana. “Some home buyers should seriously consider offering a more generous price to the seller in exchange for a large closing cost concession and then use those funds to buy down the interest rate as much as possible.”

Also see: Avoiding the 30-year mortgage loan trap can save you hundreds of thousands of dollars

2. Use part of your down payment to pay down debt

When you apply for a mortgage, the lender considers your total debt payments for the house, car, student loans and credit cards. Sometimes it makes sense to divert some of your intended down payment money to cut the higher-rate debt first, said David Kuiper, vice president and senior mortgage banker for Dart Bank in western Michigan.

“While the mortgage payment will be slightly higher, the total debt/payments is lower, making the proposed purchase more affordable,” Kuiper said.

3. Use home buyer assistance programs

State and local governments sponsor an abundance of programs to make homes affordable for home buyers, especially first-timers. Some programs offer down payment assistance and help with closing costs. Others offer favorable interest rates or tax credits.

Details differ from state to state. Some programs are targeted to certain counties, cities or neighborhoods. Others are intended for specific groups of people, such as teachers, first responders or renters who live in public housing. Some programs have income limits.

Don’t miss: We bought a falling-down 100-year-old home. We tried to renovate, but things took a turn for the worse.

4. Ask the seller to finance the purchase

You can give the seller an IOU for part of the home’s value and make monthly payments directly to the seller at an interest rate that’s lower than you could get from a bank. This arrangement is called “seller financing” and has its roots in the early 1980s, when mortgage rates zoomed as high as 18%.

You might wonder why a seller would agree to such a deal. “They will often do this in order to get the price they want,” said Janie Coffey, who leads the Coffey Team with eXp Realty in St. Augustine, Florida. The seller gets full price while you get a break on the interest rate.

Seller financing usually has an end date: Within three, five or 10 years, the buyer must get a mortgage from a lender to pay off the amount owed to the seller. Coffey explained that the type of seller open to this arrangement often has paid off the mortgage “and is OK to wait for their big payoff.”

Seller financing is complex. Use an experienced real estate attorney to draw up the contract.

Related: How the U.S. housing market got stuck in the ’80s

5. Don’t wait for a rate you like better

“If the right house comes along and the payment is affordable (even if you don’t like the interest rate), you should buy the house,” Kuiper said.

You often hear that you should buy now and refinance someday, after interest rates fall. That’s not Kuiper’s point. His point was this: If mortgage rates fall, more buyers will rush into the market. They’ll make competitive offers and drive home prices higher, “essentially wiping out any advantage of the lower interest rate.”

6. Don’t get distracted by things you don’t need

Some sellers want flexibility about the closing date, would prefer the buyer to make repairs, and are scared of accepting an offer from a buyer who ends up failing to qualify for the mortgage.

Vander Stelt advises staying focused on price with these hassle-avoidant sellers, while being flexible on the rest of the offer on the house. “Do this by offering the best terms you can, including buying the home as-is, a closing date and possession that works best for the seller, and illustrating how strong of a candidate you are to get your mortgage approved,” he said.

You can demonstrate that you’re a strong mortgage candidate by showing a preapproval letter and by sharing financial information, such as account balances that prove you have the cash for the down payment.

7. Buy a house that needs work

Buying a fixer-upper is an old-fashioned, time-tested way to save money. “If you can be patient, it’s worth buying a home that needs work and slowly fixing it up over time or taking a renovation loan to acquire the home and do the work upfront,” said Brian Koss, regional sales director for Movement Mortgage, in Danvers, Massachusetts.

Read: Should you buy a fixer? These are the 5 cheapest states to make home renovations.

8. Build a house or buy a brand-new one

“Building a new home can provide more certainty around how long you will have to wait to move in, it can provide more cost certainty, and it can save you money in the short and long term by avoiding costly remodels, appliance repairs and unexpected repairs of older parts of the home,” said Jeffrey Ruben, president of WSFS Mortgage in the Greater Philadelphia area.

Buying a new home in a development has some of the same advantages. And today’s buyers have good reason to shop for new construction because there’s a shortage of existing homes for resale.

Read: U.S. construction spending rose in June, marking seventh straight monthly increase

9. Rent out part of the house

Coffey suggested using an old strategy with a trendy name — house hacking — “buying a property like a duplex, where you live in one unit and rent out the other,” she said.

If you buy a duplex, triplex or quadplex, and you live in one unit, you can include the expected rental income for the others when qualifying for a loan. In some cases, you can qualify for a mortgage using expected rental income from an accessory dwelling unit, such as a basement apartment or a tiny house in the backyard.

Also see: Homeowners locked into ultralow mortgage rates consider short-term rentals, but cities are cracking down

If you buy a home today, you’re stuck with high mortgage rates for the time being. But by employing some creativity, you might find a way to afford homeownership.

More From NerdWallet

Holden Lewis writes for NerdWallet. Email: [email protected]. Twitter: @HoldenL.

Looking to build wealth with the best income-generating assets? As you set out on the path to financial freedom, understanding the different types of income-generating assets can truly change your life. This is because you can invest in assets that will generate you income, earning you more passive income. Today’s article will introduce you to…

Looking to build wealth with the best income-generating assets?

As you set out on the path to financial freedom, understanding the different types of income-generating assets can truly change your life.

This is because you can invest in assets that will generate you income, earning you more passive income.

Today’s article will introduce you to a range of assets that reliably bring in cash, giving you peace of mind and the freedom to live life on your own terms.

From traditional investments like stocks and bonds to more creative options like peer-to-peer lending or real estate, income-generating assets give you the power to diversify your portfolio and build wealth over time.

Related content:

What are income generating assets?

Before we begin, I want to talk about the basics on income-generating assets, in case you are new to the subject or if you want a background first.

Income-generating assets are investments that, as the name suggests, generate income for you. These are assets that provide you with a steady cash flow, allowing you to earn passive income and build your wealth over time.

Examples include rental real estate and dividend-paying stocks (we will go over 17 different types of income-generating assets below in more detail).

There are several benefits of the best income-generating assets such as:

Passive income: You earn money without actively working, and this can provide financial freedom and the ability to focus on other things in life. You can earn money in your sleep, while on vacation, making dinner, and more.

Diversification: You can diversify your investments so that all of your income is not coming from just one source.

Wealth building: Earning income and generating a steady cash flow can help you build your wealth over time.

Note: Please keep in mind that there is no one-size-fits-all approach when investing in any of these income-producing assets. Everyone is different and while one asset may work great for someone, it may not be the right asset for you. I recommend doing as much research as you can if you are interested in one of the asset investments I talk about below.

Types Of Income Generating Assets

There are many types of income-generating assets. Some may be more traditional such as dividend-paying stocks, and others may be more alternative income-generating assets, such as selling stock photos, and even renting out your driveway.

Today, I will talk about 17 different types of income-generating assets, but this is not a full list of the best income-producing assets. There are many, many more!

The different types of income-generating assets that I will talk about today include:

1. Dividend-paying stocks

One of the best assets to invest in are dividend-paying stocks.

Dividends are simply a payment in cash or stock that public companies distribute to their shareholders.

The amount of a dividend is determined by a company’s board of directors, and they are given as a way to reward those who have stock in their company. Both private and public companies pay dividends, but not all companies pay dividends.

How do dividends work? If you own shares of a dividend-paying stock, then a dividend is paid per share of that stock. So, if you have 10 shares in Company ABC, and they pay $5 in cash dividends each year, then you will get $50 in dividends that year. While dividends can be paid on a monthly, quarterly, or yearly basis, they are most commonly paid out quarterly — so, four times a year. In this example, the $5 in cash dividends the company pays each year will most likely be distributed as $1.25 per quarter for each share of stock.

The most common type of dividends are cash dividends. Shareholders may choose to get this deposited right into their brokerage account. Stock dividends are another common type of dividend. In this case, shareholders get extra shares of stock instead of cash.

Both cash dividends and stock dividends are great income-generating assets that will earn more money for you.

As a shareholder, you can earn income when companies distribute profits to their shareholders. Look for stocks with a history of consistent dividend payouts and a high dividend yield. Keep in mind that dividend stocks are still subject to market fluctuations, and just because a company has paid a dividend in the past does not mean that they always will in the future.

Related content:

2. High-yield savings accounts and CDs

High-yield savings accounts and CDs are a great way to grow your savings, but most people have their money in accounts with low rates. Unfortunately, that means many of you are losing out on some easy money.

Savings accounts at brick-and-mortar banks are known for having really low interest rates. That’s because they have a much higher overhead — paying for the building, paying the tellers to help you in person at the bank, etc.

High-yield savings accounts offer an easy option for earning interest on your cash. Online banks often offer higher interest rates than traditional banks. As of the writing of this blog post, you can easily find high-yield savings accounts that can earn you above 4.00%.

Certificates of Deposit (CDs), another form of income-generating assets, are FDIC insured and provide a guaranteed interest rate over a specific term. Remember that access to your money is limited during the term of the CD. You will agree upon the term before putting your money in the CD. The terms typically vary in length from around 3 months to 5 years.

Money market accounts are also offered by banks and often with a higher yield than other types of savings accounts.

3. Real estate

Real estate is one of the most common income-generating assets that people think of.

Investing in rental properties is a popular way to generate steady cash flow. You can earn rental income from tenants, and properties typically appreciate in value over time.

Location and property management are important factors that can impact your return on investment.

By investing in real estate, you may be investing in residential properties, commercial real estate, short-term rentals, REITs, and more.

Recommended reading: How This Woman In Her 30s Owns 7 Rental Homes

4. Real estate investment trusts (REITs)

An REIT is a company that owns and manages income-producing real estate. They then sell shares to investors like stock.

By investing in REITs, you can make money in the real estate market without actually owning real estate.

So, if you don’t want to be a landlord, then this may be something for you to look into. This makes it much more passive than actually owning real estate and having to manage it.

You can even diversify your income stream with REITs by investing in different property types, such as residential homes, commercial office space, industrial, and retail store properties.

5. Bonds

Bonds are fixed-income investments that are issued by governments and companies. If you own a bond, you receive interest payments from borrowers on a regular basis.

An easy way to explain this is: When you buy a bond, you are giving someone a loan and they are agreeing to pay you back with interest.

Bonds with higher credit ratings are generally a safer investment but may offer lower interest rates.

6. Mutual funds

Mutual funds gather funds from investors to invest in stocks, bonds, or other securities. Basically, the funds are pooled together and there’s a fund manager who chooses the best investments.

Income-generating assets like this have multiple types of mutual funds available for multiple types of investors. Some of these fund types include bond funds, stock funds, balanced funds, and index funds.

Mutual funds typically have higher fees because they have fund managers who are actively trying to beat the market.

With a mutual fund, you get diversification because the fund manager mixes the assets in it.

7. Index funds and exchange-traded funds (ETFs)

ETFs and index funds are popular options for those who are looking to diversify their portfolio of income-generating assets.

This is because index funds and ETFs track a specific market index and invest in a wide range of stocks or other assets, instead of picking and choosing stocks in an attempt to beat the market. This is what makes them different from mutual funds.

They often have lower fees and higher diversification compared to actively managed funds.

8. Annuities

Annuities are long-term investments offered by insurance companies that give you a guaranteed income stream to build wealth. In exchange for a lump-sum payment or periodic contributions (such as monthly or annually), you’ll receive steady payments in the future.

The way it works is you pay premiums into the annuity for a set amount of time. Later, you stop paying premiums, and the annuity starts sending regular payments to you. Some are even set up to pay you back with a lump sum.

Annuities can be fixed or variable. A fixed annuity offers a guaranteed payment amount — which means a predictable income for you. As for a variable annuity, the payment amount does vary, depending on how the market is doing.

9. Websites and blogs

Starting a website can generate income through the money-making assets of advertising, affiliate marketing, or the sale of products and services.

Since I started Making Sense of Cents, I have earned over $5,000,000 from my blog through affiliate marketing, sponsored partnerships, display advertising, and online courses. These income-generating assets make sense for building wealth.

Blogging allows me to travel as much as I want, have a flexible schedule — and I earn a great income doing it.

Now, it’s not entirely passive, but I do earn semi-passive income from my blog.

You can learn how to start a blog in my How To Start a Blog FREE Course.

Here’s a quick outline of what you will learn:

Day 1: Why you should start a blog

Day 2: How to decide what to write about (your blog niche!)

Day 3: How to create your blog (in this lesson, you will learn how to start a blog on WordPress)

Day 4: The different ways to make money with your blog

Day 5: My advice for making passive income with your blog

Day 6: How to get pageviews

Day 7: Other blogging tips to help you see success

Recommended reading: The 25 Most-Asked Blogging Questions To Get You Started Today

10. Royalties and intellectual property

Intellectual property, such as patents, copyrights, and trademarks, can generate income through licensing fees or royalties. This particular option is good for creative professionals, such as authors, musicians, and inventors, who are looking for income-generating assets.

Royalties are a way to earn income from your creative work or intellectual property. By granting others permission to use or distribute your intellectual property, you can receive ongoing payments known as royalties.

Whether you’re a musician, author, inventor, or artist, royalties offer a passive income stream as your creations continue to generate revenue over time.

Royalties can be paid out periodically or as a lump sum on these passive income assets, depending on your agreement with the licensee.

11. Stock photos

If you have a talent for photography, you can monetize your skills by selling stock photos on platforms such as Shutterstock or Adobe Stock. The more high-quality images you upload, the more potential passive income you can generate.

With stock photography, you simply upload photos that you have taken to a platform such as DepositPhotos, turning your pictures into income-generating assets. Then, you will receive a commission whenever someone buys one of your stock photos.

Stock photos are used for all sorts of reasons by websites, companies, blogs, and more. Businesses need stock photos because they are not usually in the business of taking photos of everything that they need. Instead, they can use stock photos to make their content, website, or business more visually appealing.

Some examples of stock photography include pictures of:

Travel, vacations, landmarks, outdoor adventures

Family members, such as parents, children, family gatherings

Food and drink

Cars, boats, RVs

Businesses, pictures of people in meetings, in an office.

Sports, professional events

Animals, such as household pets or wildlife

The photo possibilities are almost endless for this type of income-generating asset.

Recommended reading: 18 Ways You Can Get Paid To Take Pictures

12. Crowdfunding and peer-to-peer lending

Crowdfunding platforms enable you to invest in real estate deals with a smaller amount of money than buying real estate up front, giving you a passive income through rental income or even a property increasing in value.

Peer-to-peer lending platforms allow you to lend money directly to borrowers. Typically you can earn higher returns than traditional savings accounts, though there’s always the risk of a borrower not paying you back.

Both of these types of assets — crowdfunding and peer-to-peer lending — use technology to connect investors with those looking for funding.

13. Renting out storage space

If you own unused land or unused space in your home, renting it out for storage can be a simple way to generate passive income.

You can offer storage solutions for vehicles or boats. If you have a smaller space, then offer it to store personal belongings. You can rent out your driveway, closet, basement, attic, and more. You can even rent out a shelf.

A website where you can list your storage space is Neighbor. You can earn $100 to $400+ each month on this platform. This depends on the demand in your area and the type of income-generating assets you are renting out. And, you can choose who, what, and when — who to rent to, what things are stored, and when it will happen.

You can learn more at Neighbor Review: Make Money Renting Your Storage Space.

14. Short-term rentals

Short-term rentals can be a lucrative income-generating asset if you own properties in popular tourist destinations or business hubs.

Websites like Airbnb provide a platform to rent out your property to travelers for short periods, potentially generating higher returns than traditional long-term leases.

Furnished Finder is another website for short-term rentals. This is a way to connect with travel nurses in need of short-term housing.

Keep in mind that rental income can be affected by local regulations, potential vacancies, or seasonal fluctuations.

15. Car rentals

Car rental platforms like Turo allow you to rent out your car when you’re not using it. Assets that generate cash flow include your own wheels, and that means no significant initial investment besides the cost of the car you already own.

Be mindful of risks such as wear and tear, insurance, and potential damage caused by renters.

It’s an affordable alternative to traditional rental car companies for customers, and it’s a good way to make money if you’re already working from home and don’t need your car, or are a two-car household.

Turo is one of a few different places to rent out your car, turning your vehicle into one of your income-generating assets. Your car is covered by Turo with up to a $1 million insurance policy. You can also pick the dates for when your car is available and set your rates.

Turo says you can earn an average of $706 per month by listing your car on their site.

16. RV rentals

Similarly to car rentals, RV rentals can provide additional income by renting out your recreational vehicle when you’re not using it. Your RV could easily become one of your income-generating assets.

You may be able to earn $100 to $300 a day, or even more, by renting out your RV on RVShare.

If you have an RV that is just sitting there and not being used, then you may be able to earn an income with it by renting it out to others who are interested in RVing. Cash flow-generating assets like RVs are a win-win for both you and the renter who wants to experience life in a recreational vehicle.

You can learn more at How To Make Extra Money By Renting Out Your RV.

17. Vending machines

With a vending machine business, you can generate income by selling a variety of products, from food to fishing supplies, beauty products to baby items, and more.

You may be able to earn $1,000+ a month by running a vending machine business. That’s enough reason to take a closer look at income-producing assets like this.

You can learn more at How To Start A Vending Machine Business – How I Make $7,000 Monthly.

Questions about income generating assets

Here are common questions that you may have about income-generating assets:

How do I start passive income from nothing?

Starting passive income from nothing requires creativity and resourcefulness. You can begin by identifying skills you possess or interests that can be turned into income-generating opportunities.

What are the assets that generate income?

The assets I talked about above include:

Dividend-paying stocks and stock market investing

High-yield savings accounts and CDs

Real estate

Bonds

Mutual funds

Index funds and exchange-traded funds

Annuities

Websites and online businesses

Royalties and intellectual property

Stock photos

Crowdfunding and peer-to-peer lending

Renting out your storage space

Car rentals

RV rentals

Vending machines

How do I start buying income generating assets?

There are traditional investments or more creative options. Do as much research as you can before deciding which option fits you best.

What are good assets to buy?

After deciding if you want to purchase traditional investments or more creative options, choose an asset that you can afford and best fits your lifestyle.

What are the best assets to buy for beginners?

For beginners seeking income-generating assets, you may want to look into:

Dividend-paying stocks for your investment portfolio

Crowdfunded real estate investing: Platforms like Fundrise allow smaller investments with lower risk exposure.

ETFs and index funds: They provide diversification and passive income through dividends.

What is income generating real estate?

Income-generating real estate refers to properties that produce regular rental income, such as apartments, commercial properties, or short-term vacation rentals.

How do I start passive income in real estate?

There are a few ways that you can earn passive income from real estate, including:

Buying a property, such as an apartment building or duplex, and renting it out to tenants

Using real estate crowdfunding platforms

Investing in REITs

How to make passive income with real estate without owning property?

You don’t need to actually own property in order to make money with real estate. Instead, you can earn passive income from real estate by investing in REITs and using real estate crowdfunding platforms.

This is an option for those who want to be diversified with their income-generating assets but don’t want to spend all of their money or time on a single piece of real estate.

How to make $1,000 a day in passive income?

Making $1,000 a day in passive income with assets that produce income will not be easy. If it were easy, then everyone would be doing it, after all.

Making $1,000 a day in passive income may require a large amount of money up front, diversifying into different assets mentioned above, and lots of patience from you because it will take time to make that kind of money.

You may want to start off by focusing on building multiple income streams and reinvesting your profits as you earn them.

What to think about before investing in income producing assets?

There are many different things to think about when it comes to income-generating assets. You want to find the best assets to invest your money in that will also be the best fit for you.

Remember, as I said at the beginning of this article, not everything will be applicable to everyone. Everyone is different! You may prefer to create a stock photo portfolio and hate real estate, whereas someone else may really enjoy being a real estate investor — or it may even be the other way around.

Here are some of my tips if you are interested in income-generating assets:

Do your research and talk to experts —I recommend researching as much as you can on the asset you are interested in. And, if you still have questions, don’t be afraid to talk to an expert.

Diversify — One of the important parts of building a successful income-generating portfolio is finding ways to be diversified.

Think about the risks —When making money, there’s usually some sort of risk. I recommend evaluating the risks and seeing what you are comfortable with.

What are the best books on income generating assets?

Some highly recommended books on income-generating assets include:

The Simple Path to Wealth by JL Collins

The Millionaire Real Estate Investor by Gary Keller

The Little Book of Common Sense Investing by John C. Bogle

Income Generating Assets — Summary

I hope you enjoyed this article on the best income-generating assets. As you learned, there are many different types of assets that you can invest in so that you can earn an income.

The best income-producing assets, if they’re right for you, can truly change your life.

With these assets, you can build wealth through a reliable passive income, giving you peace of mind and freedom to live life on your own terms.

Are you looking to build income-generating assets? What are your favorite ways?

The “Brady Bunch” house, renovated by HGTV, has sold for more than $2 million below its original asking price.

After spending the summer on the market, the Studio City property just closed escrow. Historic home enthusiast Tina Trahan, whose husband, Chris Albrecht, was once chief executive of HBO, scooped up the sitcom gem for $3.2 million.

In May, after purchasing the home for $3.5 million in 2018 and overhauling it in the series “A Very Brady Renovation,” HGTV listed the groovy digs for $5.5 million.

As to why HGTV accepted an offer more than $2 million below asking (and $300,000 shy of what it paid in 2018), Compass’ Danny Brown, the listing agent on the property, told The Times in an email, “This is a one of kind property which was impossible to comp. This is not a home anyone would ever live in.” Savvy investors, he said, understand that laws governing short-term rentals are “nuanced and restrictive,” limiting the value of the property for that use.

“We felt the property was worth about $3M – $3.5M and that’s exactly where it landed because there are no intellectual property rights that are included in the sale,” Brown said.

Built in 1959 with Late Modernist architecture, the house was used only for exterior shots during the sitcom’s five-season run from 1969 to 1974, followed by decades of syndication that cemented the mixed family of eight in the annals of American pop culture.

When HGTV bought the home, its interior bore no resemblance to the place where audiences watched the Brady children grow up. Scenes shot inside the Brady residence were filmed on sets built on Soundstage 5 at Paramount Studios in Hollywood.

In 2018, HGTV looked to meld the two realities and bought the house at 11222 Dilling St. for nearly double the original asking price. The channel outbid Hollywood celebrities, including former ‘N Sync member Lance Bass.

The network spent an additional $1.9 million to re-create the TV home where America came to know Mike, Carol, Greg, Marcia, Peter, Jan, Bobby and Cindy Brady. HGTV even added a second story to accommodate all the rooms that were seen in the show.

Advertisement

HGTV documented the process on “A Very Brady Renovation,” which featured the six actors who played the Brady children. The cast, alongside HGTV hosts Drew and Jonathan Scott, worked to gut the house while the crew painstakingly reproduced the set’s rooms and 1970s decor — down to the cabinet hardware. The online listing for the house invited buyers to “own a piece of pop culture history” and showed images of its detailed and polished 5,140-square-foot interior, which has five bedrooms and five bathrooms.

HGTV said the home came equipped with “many of its contents, including customized pieces such as the green floral living room couch and the credenza with a 3-D printed horse sculpture.”

“HGTV spent about $5.5M+ purchasing and gutting the house which is why we listed it at $5.5M even though we knew it was an aspirational list price,” Brown said via email. “By the way, HGTV did fine making revenue on ‘The Very Brady Renovation’ show and several other ancillary revenue streams. As for my brother from another, Lance Bass, perhaps third time’s the charm?”

Times staff writer Jonah Valdez contributed to this report.

Homeowners can now see potential short-term rental income estimates on Realtor.com thanks to an integration with Airbnb.

Short-term rental earnings estimates for hosting one room or the entire house will be available to homeowners via Realtor.com’s My Home dashboard, according to an announcement on Thursday.

The estimated earnings for a seven-day rental are based on Airbnb data from similar listings in the ZIP code.

A recent survey from Realtor.com and CensusWide found that 39% of homeowners have or would consider renting out part of their primary home, with 23% having rented out their home previously or are planning on doing so in the future and 16% reporting that they are considering renting out part or some of their home in the future.

Financial reasons are the primary motivator for homeowners to rent out their home, as 34% who have rented or plan to rent out their home are doing so in order to save money for a home purchase with a higher mortgage rate, while 29% are doing it prepare for potential upswings in a variable mortgage and 21% are doing it to help pay their current mortgage.

According to Realtor.com, the integration will also enable homeowners to see if it is a good idea to rent out their current home as an alternative to selling it. Of the homeowners surveyed, 60% reported they would consider renting out their current home rather than selling, if they look to buy or rent elsewhere, with 21% citing extra income from a renter and 19% citing the ability to maintain the home equity they have built as primary motivators.

“Short-term rentals are a great way to help with some of the costs of homeownership – renting out their house for a couple days or weeks out of the year when it’s not in use could generate extra income that can be put toward the mortgage, maintenance, or even help cover the cost of a vacation,” Mausam Bhatt, the chief product officer of Realtor.com, said in a statement. “By arming homeowners with information about how much they could potentially make by renting a room or their whole home on Airbnb, Realtor.com is helping them better understand their options and in turn make more informed decisions about their home.”

Realtor.com’s integration with Airbnb comes as many metro areas are looking to crackdown on short term rentals. Earlier this month, thousands of New York City Airbnb listings vanished from the market as the city introduces some of the strictest regulations in the U.S. for short-term rentals. City councils in Dallas, Philadelphia and New Orleans have passed their own restrictions on short-term rentals.

If you peruse real estate listings on Realtor.com, you might come across a new Airbnb integration.

This week, the two companies announced a collaboration that lets homeowners see how much they could fetch to rent out a room, or the entire house.

It comes at a time when short-term rentals, or STRs for short, are somewhat under-fire given their immense growth.

The Airbnb story also happens to coincide with a residential housing shortage, with some critics blaming STRs on the lack of supply.

In any event, if you’re interested in seeing your Airbnb earnings estimates, you’ll need to add your property to Realtor’s My Home dashboard first.

How to Find Your Airbnb Host Estimate on Realtor.com

To get started, you’ll need to head over to the My Home dashboard on Realtor.com and add your property if you haven’t already.

This will also entail creating an account on Realtor.com if you don’t have one. It’s fairly simple and seems to only require an email and password.

From there, you’ll see a variety of information pertaining to the property added, including its RealEstimate, which is the site’s take on a Zestimate.

You’ll also see a tab titled “Host or rent,” which will contain your Airbnb host estimate. It provides both an entire home estimate and a room estimate.

A sample of the entire home estimate can be seen in the screenshot above. The single room estimate can be seen below.

It defaults to a 7 nights out of a month to give you a rough estimate of what you could earn via the Airbnb platform for renting it out for part of the month.

The estimates, which are provided by Airbnb, consider factors such as the zip code and bedroom count.

Airbnb reviews booking data over the past 12 months from the top 50% of similar listings (based on earnings) in the area where your home is located.

Then it computes nightly earnings, which are defined as the price set by each Airbnb Host minus the Airbnb Host service fee.

Note that Airbnb doesn’t subtract cleaning fees, taxes or other hosting expenses you might charge/incur when calculating the nightly estimate.

At the moment, these estimates are only available for U.S. addresses and do not factor in the number of guests a listing might accommodate.

And while they may strive to provide an accurate estimate, it’s just an estimate and no guarantee of what you’d actually earn.

Actual earnings can depend on a variety of factors, such as availability, listing price, and demand in the area.

Lastly, and here’s the biggie, the ability to host your property may also depend on local laws.

In other words, it may not actually be permitted to list your property as an STR in your city.

Is the Airbnbust Finally Upon Us?

There have been rumblings for a while now about a so-called “Airbnbust,” the premise being that too many first-time landlords purchased homes with the express purpose of making them STRs.

And now that there are so many of them, the hosts may encounter buyer’s remorse.

This could be due to unforeseen problems, a lack of experience being a host, complaints from neighbors, or simply that the earnings just aren’t there.

Throw in the fact that some hosts acquired multiple properties and these problems could be exponential.

Of course, some hosts might be raking in the dough, depending on how cheap they got in and how much demand their property has.

After all, many of these properties were purchased when 30-year fixed mortgage rates were 2-3%. And when home prices were half what they are now.

So even if competition rises, or they run into issues like unexpected refunds or cancellations on the platform, they may still do just fine.

But the real doomers out there think these STRs will be the first shoe to drop, setting off a panic and an eventual wider housing crash.

Critics on the other side say there aren’t enough of these properties to make a major impact, but in certain vacation areas there are larger concentrations.

Another issue is lack cities are beginning to ban STRs, with New York City being the latest to impose major restrictions.

This week, they launched new rules that only allow sub-30 day rentals if hosts register with the city.

And they “must commit to being physically present in the home for the duration of the rental, sharing living quarters with their guest.”

In other words, you can only rent out a room, like a traditional Bed and Breakfast, assuming it’s for less than a month.

And no more than two guests are allowed at a time, meaning larger families are effectively out of luck.

Obviously, sweeping changes like this could lead to a flood of sales if a long-term rental isn’t feasible (or simply as lucrative).

But it all remains to be seen. Many of those critical of Airbnb and other STR platforms such as VRBO, feel many of these properties could be going to families, instead of being rented out for a profit.

Especially first-time home buyers looking to lay down roots and start a family.

The STR gold rush may have also inadvertently sent home prices even further out of reach for the average person just looking to realize the American Dream.

Financial considerations and interest rates are a key reason some homeowners are choosing to rent their homes rather than sell

A majority of homeowners would consider renting out their current home on a short-term basis rather than selling it in the current market.

That’s according to a survey released Thursday by Realtor.com and CensusWide, which included responses from 2,000 homeowners. They found that 60% of respondents would consider renting their current home versus selling if or when they decide to buy or rent a home somewhere else. The survey was conducted online in July 2023.

Some 23% of respondents had rented out their home before or planned to rent out part of their home out in the future. An additional 16% of respondents said they would consider doing that.

With the 30-year mortgage rate at over 7%, many homeowners are reluctant to sell. Short-term rentals are a way of earning extra cash and, for those who can afford it, of holding onto their home should they decide to move to a new place.

The company released the survey in conjunction with the launch of a new tool on Realtor.com that allows users to see estimates of short-term-rental income from Airbnb (ABNB).

Homeowners can look at potential earnings estimates for hosting their whole house or even one room. The estimated earnings for a seven-day rental are based on Airbnb data from similar listings in the same zip code, Realtor.com said.

Realtor.com is operated by News Corp (NWSA) subsidiary Move Inc., and MarketWatch is a unit of Dow Jones, also a subsidiary of News Corp.

Cities like New York are tightening short-term rental laws

Recent legislation may complicate homeowners’ plans to try their hand at short-term renting, however. In New York, a new ordinance that went into effect Sept. 5 requires all short-term-rental hosts to be registered with the city, live in the place they are renting, be present when renters are staying and have a maximum of two guests.

The new rules will likely eliminate many Airbnb listings in New York. Airbnb filed a lawsuit against the city in June, calling the rules a “de facto ban against short-term rentals in New York City,” per court documents. A judge dismissed the case in August.

Airbnb called the new rules “extreme and oppressive.” In a statement released to Associated Press, the company said the city’s new rules “appear intended to drive the short-term rental trade out of New York City once and for all.”

The total number of Airbnb listings in the city could fall by 70%, according to an estimate from Skift.

Other cities, including San Francisco and Seattle, have limits on how many properties one person may rent out on a short-term basis. In Los Angeles, hosts may only rent their primary residence on a short-term basis, and only for up to 120 days per calendar year.

Financial considerations for renting rather than selling

Financial considerations were a key reason homeowners told Realtor.com they would choose to rent out their homes instead of selling them, with 21% saying they would like to earn extra income from renting and 19% saying they would rather rent their home out in order to maintain the equity they had built.

And since many homeowners either purchased their home at an ultralow interest rate or refinanced to a very low rate, they might consider renting as an way to make money while holding on to that home.

Homeowners also had specific plans for that extra income: A third said they wanted to pursue the short-term rental route to earn extra income that they would save toward buying another home with a higher mortgage rate; 29% said they wanted to be prepared in the event that their adjustable-rate mortgage payments increased in the future; and 21% said they wanted the income to help pay for their current mortgage.

-Aarthi Swaminathan

This content was created by MarketWatch, which is operated by Dow Jones & Co. MarketWatch is published independently from Dow Jones Newswires and The Wall Street Journal.

Running an Airbnb in L.A. has never been more profitable.

As the city tries to crack down on illegal listings, and advocacy groups complain about the company’s effect on L.A.’s housing crisis, hosts are charging higher rates than ever while raking in bigger and bigger payouts.

But don’t expect them to talk about it.

Data show that a vast number of homes are operating without an active registration, which is required by the city to operate a short-term rental. Several such hosts spoke to The Times anonymously for fear of being fined by the city or, worse, getting their listing shut down by Airbnb.

“This is my primary source of income,” said one host who operates three different listings. “I’m finally making a decent living off of this. One listing alone wouldn’t cut it.”

Advertisement

Since 2020, revenues for hosts have steadily risen far beyond pre-pandemic levels. The average revenue climbed to $17,654 in 2022, up more than $4,000 year-over-year, and the numbers are at a similar pace for 2023, according to data from short-term rental analytics company AllTheRooms.

In total, L.A. hosts earned a combined $375 million last year, a spokesperson for Airbnb said.

A few factors contribute to the rise. For one, daily rates for Airbnb rentals have spiked over the last four years, swelling from $152 in 2019 to $244 in 2023. It’s a trend that’s happening across the short-term rental industry, as hotel and VRBO rates have steadily risen since the COVID-19 pandemic as well.

Basic supply and demand is another factor. Save for a drop during the first few months of the pandemic, Airbnb occupancy rates have largely stayed consistent, with the average rental occupied more than 40% of the time. But the amount of listings has dropped dramatically.

In August 2019, there were 16,973 Airbnb listings in L.A. Currently, there are 7,360.

Supply is down for now, but advocates worry that if revenues continue to rise, more homeowners will convert properties into Airbnbs.

Advertisement

Much of the drop was due to the pandemic, but the supply hasn’t risen since 2020 partly due to the city’s enforcement of its Home-Sharing Ordinance, a law that went into effect in 2019 that limits Angelenos to hosting only short-term rentals in their primary residence — homes where they can prove they live at least six months per year.

L.A. and Airbnb have worked in tandem over the years to enforce the law, launching a system in 2020 that streamlines the process of identifying and taking down illegal short-term rental listings.

It has been effective; the number of listings for short-term rental units across all home-sharing sites has dropped more than 70% over the last four years, going from roughly 36,600 in November 2019 to just under 10,000 in June 2023, according to the city planning department.

But plenty remain.

The Times previously reported that thousands of listings violate the law, and last year, a report claimed that 22% of L.A. listings host guests for more than 180 days a year.

“I can’t afford to rent out my place for only six months a year. I’d lose half my revenue,” said one host who rents a two-bedroom apartment in Hollywood on Airbnb.

Two other Airbnb hosts hung up the phone mid-interview when asked about whether their listing was their primary residence, or whether their registration number was valid.

“It’s a don’t ask, don’t tell system. I can’t afford to have my business threatened over a registration number,” one said.

The average daily rate for an Airbnb in L.A. has risen to $244 in 2023.

(K.C. Alfred San Diego Union-Tribune)

As of August, there are 4,293 active home-sharing registrations, according to the city’s planning department. But on Airbnb alone, there are currently 7,360 listings up for rent.

“L.A. has a big enough rent problem on its own, and then you have a rogue industry that swoops into the city and starts taking rental properties off the market,” said Peter Dreier, a professor at Occidental College.

Dreier worked with the team that drafted Measure ULA, a new tax that funnels money toward affordable housing initiatives, and said that the short-term rental industry is contributing to both the housing crisis and homelessness crisis.

“When you take units off the market and rent them to tourists, one consequence is that it leads to more people fighting over fewer units. And that leads to higher rents,” he said.

The planning department is preparing a report with other departments analyzing enforcement of the Home-Sharing Ordinance. It will provide recommendations to the City Council on how to improve the program.

In the meantime, more listings bring more tax dollars. L.A. charges a 14% transient occupancy tax, often called a “bed tax,” paid by guests in a hotel or a short-term rental such as an Airbnb.

In the 2021-22 fiscal year, the city collected $33.88 million in transient occupancy taxes, according to the planning department.

It’s a hefty amount, but a report from McGill University urban planning professor David Wachsmuth suggests that the city could be raking in even more by fining illegal short-term rental listings.

The study claimed that 45% of all short-term rental listings are illegal in one way or another, and that the city could have levied between $56.8 million and $302.2 million in fines in 2022.

“I’ve never paid a fine, but my guests pay the tax. As long as the city’s getting money from somewhere, they’ll be fine,” said the Hollywood Airbnb host.

Randy Renick, an attorney with Hadsell Stormer Renick & Dai LLP, serves as executive director of Better Neighbors LA, a coalition that includes hotel employees, renters’ rights groups and housing advocates. He co-founded the group in 2019 as a public education campaign to emphasize the impact that short-term rentals have on communities.

He said rental hosts bend the rules in a few ways. One strategy is the bait-and-switch, where a host will advertise that a property is somewhere near the border of Los Angeles, such as West Hollywood, and thus not subject to L.A.’s stringent rules. But when renters show up, the property is actually in L.A.

Others give false registration numbers — some more cleverly than others.

“1234567 was popular for a while,” Renick said.

Some simply use expired registration numbers, and others used an active registration number but for several properties.

The organization’s website keeps a hotline for Angelenos to call and report illegal listings in their neighborhood, and Renick said they receive multiple calls per week.

From there, they urge the city to take action for matters both small and large. Sometimes it’s a call asking to enforce a fine on a certain property, and sometimes it’s a campaign on how short-term rentals can drive up long-term rent in an area by taking homes off the market and renting them to tourists.

“We try to show the impact of short-term renting and how it’s contributing to the housing and homelessness crisis,” Renick said. “Robust enforcement will result in returning thousands of units back to long-term rental.”

He pointed to Santa Monica and New York City as two cities that L.A. could model itself after. Santa Monica has a robust enforcement system, including multiple full-time staff focused on interviewing owners and issuing fines to illegal listings.

The coastal city allows only short-term rentals (less than 30 days) if the host lives on the property throughout the visitor’s stay. New York City adopted a similar rule last year, and the enforcement begins on Tuesday.

Though it has a long way to go, Renick said L.A. has raised the bar on proof required to show that a listing is the host’s primary residence.

Frank Tai, the owner of a luxury beachfront rental in Playa del Rey, has seen that process firsthand. He has only one listing and makes sure to renew his license every year, but the process has gotten more laborious over the years as both the city and Airbnb look to catch illegal listings.

“I’m in compliance, but it’s a lot of work. I fill out a 40-page application every year and send in property tax statements, utility bills and other documents,” he said. “Every year, something gets kicked back. They’re trying to stay on top of things.”

Tai said the process is well worth it. His rental is very profitable; it’s booked throughout the entire summer, and nightly rates double during vacation season. He didn’t even experience a slowdown during the pandemic, simply a switch from out-of-town customers to L.A. locals looking for a staycation.

“I don’t sneak around the system, but I’m guessing people do because it’s so profitable,” he said.

With record-low inventory nationwide, real estate agents seem to be hearing the same thing day in and day out: “I’d list my home, but where would I move?”For most agents, that’s the end of the conversation, ending the possibility of taking a new listing as well as facilitating the buyer side. Nationwide, inventory is at all-time lows. According to Altos Research, this week there are only 465,000 active listings. We are still at least a million listings shy of being a balanced market, so this excuse is not going to subside anytime soon.

Stop answering clients’ concerns by saying, “Yeah, there’s really nothing on the market, I mean everything in the MLS is already pending.I’ll put you into my search widget and we’ll watch for something to pop up together.”

While that’s onemethod of finding a home for your would-be sellers to buy, you can’t end the conversation there and expect to do any business this year. The key is to set up the ‘drip system,’ then move the conversation forward by being a problem solver. How does someone list and buy at the same time successfully in a market like this?

Here are 10 solutions for sellers who what to buy that go beyond waiting and watching for magic inventory to appear.

Build a home instead of chasing after the scarce resale inventory

30% of available homes are new construction, so there are several advantages to this option. First, many builders are buying down interest rates using their in-house financing. Builders are closing loans in the 4.5 to 5.5% range currently! Next, the house is new. No rehab for them and no inspection woes for you. Your client can get their home on the market a few months before construction is complete and not have to move twice. Finally, when your client builds, they don’t have to compete in a bidding war.

Buy first, close and then list the previous home

Don’t assume your clients won’t or can’t utilize this option. They may have a downpayment saved that isn’t their home equity. They might use a bridge loan to borrow their equity, close on the next home and then sell the old one. You don’t know if you don’t ask. The advantage here is that your client can make a non-contingent offer, secure their next home and deal with their old house later. Make sure you know lenders who offer bridge loans and understand how to explain this option.

Sell first, rent for a while and take the time to look for the right home

The advantage here is the seller has cashed out their equity and is ready to pounce on the right home, but without the pressure of scheduling closing and possession dates. Who are your go-to leasing agents? Maybe youare a leasing agent. Consider both traditional rentals, short-term vacation rentals, as well as apartment complexes. Many have some great amenities which could work for a short to longer-term lease while you help your client find the right home to buy.

Offer acceptance contingent on seller finding suitable housing

The buyer will probably want a specific time frame, but you can usually get 90 to 120 days to secure the next home. Many buyers in today’s market are simply anxious to find the right home, so they will be flexible with the seller’s situation. It’s still a seller’s market. The advantage to your client is they won’t have to move twice and you’ve built in enough time to look for the next place.

Convert the previous home into a rental

You can handle the lease yourself or refer it to your favorite leasing agent. The home stays an asset for your client and they can keep their low-interest rate mortgage. Don’t assume that this isn’t an option. You have to ask! Remember that Americans currently have record-high credit scores. They may be more comfortable taking this option than you think. In some markets, keeping the home and turning it into a short-term rental can be very profitable. It might be the best option for your client. You can always run the numbers and see if it makes sense, at least in the short term.

Leasing back the home

In this scenario, the buyer is happy because they secured the house, and your seller is happy because they have both time and money coming in to facilitate their move to the next place. Once the home has been purchased by the new owners, your clients would essentially pay rent to stay while they house hunt.

Buying an RV, a houseboat or a sailboat

There are endless examples of sellers who cashed out their homes, bought a recreational home and traveled for a while. You might be surprised that it’s not just baby boomers or retirees who are doing this! Another version of this option involves sellers cashing out and renting a series of short-term rentals in different areas of the country or the world, trying out new possibilities before they decide where to land.

Find your would-be seller an off-market home to purchase where that seller has flexibility

In this scenario, you are in complete control of both sides of the transaction, and you may pick up yet another client when the off-market seller also needs to buy. Refer to our podcast series and HousingWire articles about how to find inventory that’s not in the MLS.

Moving into an assisted living care facility

Many of the homes that are coming onto the market right now are in 55 and over communities. There is also inventory from families downsizing, new empty-nesters moving and the like. Are you prospecting in those neighborhoods?

Moving in with relatives

Whether that’s moving in with parents, kids or cousins somewhere else, it can be a short-term solution for sellers who don’t have another property in mind yet.

Bottom line? You can’t just wait around for listings to appear for your sellers! Stop relying on your ‘drip system.’ Be proactive with different solutions that could work for them. You’ll have more transactions and they’ll value your expertise, netting you both current business as well as future repeat and referrals.

Tim and Julie Harris host the nation’s #1 podcast for real estate professionals. https://timandjulieharris.com/category/podcast has new podcasts every day. Tim and Julie have been real estate coaches for more than two decades, coaching the top agents in the country through different types of markets. https://PremierCoaching.com to get started for FREE today.