The Independent Budget Office of New York City released its preliminary budget analysis for 2009 today, revealing that last year was one of the worst on Wall Street as the mortgages crisis ate into firms’ profits.

“Problems in the U.S. housing market have spilled over into financial services—the industry that drives New York City’s economy,” the report said.

“With financial institutions expected to ultimately write-off several hundred billions of dollars of assets, they have sharply reined in lending and other activities. After near-record profits of $20.9 billion in 2006, IBO projects that the final tally of Wall Street profits in 2007 will be $3.2 billion, their lowest level since 1994.”

The report noted that this year isn’t expected to be much better, with projected profits of just $6.6 billion, followed by $12.2 billion in 2009.

The IBO forecasts a loss of $0.9 billion for the first quarter of 2008, but then expects positive quarterly profits for the remainder of the year.

“Mirroring this weakness, employment in the city’s financial services industry will fall by 12,600 jobs (2.7 percent) in 2008 and another 7,600 jobs (1.7 percent) in 2009.”

“As the financial sector’s woes spread through the rest of the local economy, IBO projects that employment growth will stall this year and next.”

According to the report, a “brief recession” is underway and expected to continue during the first half of 2008, followed by moderate growth in the second half, with New York City likely to be hit harder because of its reliance on the financial sector.

“The effects on employment growth and personal income will be deeper and longer lasting here in the city than in the nation as a whole.”

The IBO said tax revenues in NYC are expected to fall this year and next, the first time since the Sept. 11 attacks, but should rise in 2010 when the U.S. economy begins to rebound.

See the complete list of banks, mortgage lenders, and other financial institutions affected by the ongoing mortgage crisis.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law Firm’s editorial disclosure for more information.

The debt avalanche method is an accelerated debt repayment strategy that involves paying off the debt with the highest interest first, then rolling those payments to your next highest-interest debt until all your debt is paid off.

Getting out of debt can seem overwhelming when you’re sitting at your kitchen table trying to pay bills each month or if debt collectors are harassing you. It’s even worse when all you can think about is everything else you could spend money on: a family vacation, a new car. But with a bit of dedication and a plan, it’s possible to regain your financial freedom with an accelerated debt repayment strategy like the debt avalanche method.

Read on to learn how to use the debt avalanche method to pay off your debt faster than you may have thought possible.

What is the debt avalanche method?

The debt avalanche method is an accelerated debt repayment method. When using this strategy, you make minimum monthly payments on all your debts and put any additional funds toward paying down the debt with the highest interest rate.

Once you’ve repaid that debt, roll that minimum payment and additional funds over into the debt with the next highest interest rate. Repeat the process until you’ve paid off all your debts.

The debt avalanche method is a good strategy for most types of debt:

Student debt

Credit card debt

Auto loans

Medical debt

Debt avalanche vs. debt snowball: What’s the difference?

The debt avalanche is often compared to the debt snowball—another accelerated debt repayment method. In a debt snowball, instead of paying off the debt with the highest interest rate, you direct all your extra money toward paying off the debt with the lowest balance.

While both methods will pay off debt faster than if you had no strategy, you’ll see more quick wins if you opt for the snowball method, making it a good option for people who are easily discouraged.

You can also combine the two methods by prioritizing paying off the smallest debt with the highest interest rate to save on interest and see quick wins.

How to use the debt avalanche method to pay down debt

To use the debt avalanche method, follow these steps:

Build up an emergency fund. This will ensure an unexpected bill doesn’t throw off your payment plan. Experts recommend having enough in your emergency fund to cover six months of living expenses.

Make a list of all your debts. Include their balances, interest rates and minimum payment amounts. Organize your list from the highest interest rate to the lowest.

Total your monthly expenses and income. Add up all the money you spend on monthly living expenses and monthly minimum payments on debt. Also note your monthly income.

Determine how much money you have to put toward additional debt payments. Tally what you have left over each month after paying monthly expenses and minimum payments. You’ll put this “extra money” toward debt each month.

Each month, put the extra money toward the debt with the highest interest rate. This should be in addition to the regular monthly minimum payments.

Put any unexpected income toward the debt with the highest interest rate. If you get any unexpected income, such as a tax refund or bonus at work, put that toward your accelerated payment as well.

When you’ve paid that debt off, roll over that debt’s minimum payment and your extra monthly income toward the debt with the next highest interest rate. Continue paying the minimum payment on all other debts.

Repeat until you’ve cleared all your debts. As you pay off debts, your payments to the other debts will increase.

Debt avalanche example

Let’s look at an example use of the debt avalanche method.

You have three outstanding debts:

A student loan for $10,000 with 5 percent interest and a minimum monthly payment of $400

A credit card debt of $5,000 with 25 percent interest and a minimum monthly payment of $100

A home repair loan for $3,000 with 15 percent interest and a minimum monthly payment of $275

And after monthly living expenses and the three minimum payments, you have $250 leftover in your budget to put toward accelerated payments.

Since your credit card debt has the highest interest rate, start by paying the extra $250 in addition to the $100 monthly payment. That means you’ll pay $350 each month.

Once you’ve paid off your credit card debt, your debt with the next highest interest rate is the home repair loan, so that’s where you’ll start sending your extra payments each month. Roll over the $350 you paid monthly for the credit debt to the home repair loan. Added to the minimum payment of $275, you’ll pay $625 toward the loan each month.

When the home repair loan debt is clear, focus on your student loan, which has the lowest interest rate of your three debts. Roll over the $625 you were paying to the home repair loan to the minimum payment for the student loan, for a total monthly payment of $1,025.

If you use the debt snowball method discussed earlier, you’d start by paying off your smallest debt, which in this case is the home repair loan.

Pros and cons of the debt avalanche method

The debt avalanche method is one of the most logical and cost-effective debt repayment plans, but it isn’t perfect.

The advantages of the debt avalanche method are:

You’ll save on interest. This method helps you pay off your debt early, saving you what you would have paid in interest.

You’ll pay back your debt faster. By steadily making payments larger than the minimum, you can shave months off your repayment plan.

The disadvantages of the debt avalanche method are:

Larger debts can take longer to pay back. If you know you need small wins to stay motivated, this can negatively impact your ability to stick with your accelerated payment plan.

Unexpected bills or unstable income can hinder your progress. This method only works if you can make regular payments larger than your minimum payment.

Other ways to pay off credit card debt

While many people find the debt avalanche method to be a helpful strategy for getting out of debt, there are other ways to pay off debt that may better fit your situation.

You can also use any of the following methods:

Balance transfer credit card: Some credit cards have promotional offers for 0 percent APR on balance transfers to new customers. If you qualify, you can transfer your debt on a high-interest credit card to one of these cards. Pay attention to when the promotional 0 percent APR ends, or you’ll have to pay interest again. In this situation, it makes the most sense to devote any extra income after monthly expenses to this debt to clear it faster.

Debt consolidation loan: Take out a loan for the amount of all your debt and use the money to pay off those individual debts. Then pay off your consolidation loan each month. This makes repayment easier because you’re only making one monthly payment, but be careful that the interest rate on your consolidation loan is less than the interest rates on your other debt. Otherwise, you’ll end up paying more in interest over time.

Home equity line of credit: Borrow against your home’s equity. Often these lines of credit have lower interest rates than credit cards.

Debt management plans: If you cannot pay off your debt within five years even with a strict budget, or if your total monthly minimum payments are more than your monthly income, consider getting professional help. A debt counselor can help you create a debt management plan to pay off your debt. However, secured debt (a debt with collateral, such as your car or your home) won’t qualify for a debt management plan.

Is the debt avalanche method right for you?

The debt avalanche method is an excellent option for repaying debt faster, but it doesn’t fit every situation. If you are intent on saving money while you repay debt and are motivated enough to keep going without small wins along the way, the debt avalanche method may be your path to financial freedom. While using the debt avalanche—or any accelerated debt repayment plan—it’s essential to continue with behaviors that maintain or improve your credit. Stay current on all your bills, create and stick to a budget and track your spending. Lexington Law Firm may be able to help you on your journey to repair your credit. Take our free credit assessment today to learn more.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.

Reviewed By

Alexis Peacock

Supervising Attorney

Alexis Peacock was born in Santa Cruz, California and raised in Scottsdale, Arizona.

In 2013, she earned her Bachelor of Science in Criminal Justice and Criminology, graduating cum laude from Arizona State University. Ms. Peacock received her Juris Doctor from Arizona Summit Law School and graduated in 2016. Prior to joining Lexington Law Firm, Ms. Peacock worked in Criminal Defense as both a paralegal and practicing attorney. Ms. Peacock represented clients in criminal matters varying from minor traffic infractions to serious felony cases. Alexis is licensed to practice law in Arizona. She is located in the Phoenix office.

Inside: Do you want to claim your partner as a dependent on your taxes? This guide will explain the rules of claiming dependents whether girlfriend or boyfriend and help you take the necessary steps to do so.

Navigating the waters of tax credits can be tricky, especially when it involves claiming an unmarried partner as a dependent.

The Internal Revenue Service (IRS) does permit the declaration of a non-relative adult as a dependent, provided certain conditions are met.

And that is where it gets tricky for the tax novice.

That is where we are going to reference the IRS guidance, so you can determine whether or not you qualify for this deduction.

By pointing you in the right direction, you can understand the specific tests and requirements to avoid any tax-related complications.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

Understanding dependency in the context of taxes

The word “dependent” might remind you of a newborn baby or an elderly family member. But in tax terms, the meaning broadens.

In the IRS terms, a “dependent is a person, other than the taxpayer or spouse, who entitles the taxpayer to claim a dependency exemption.” 1

This might be a child, an adult family member, a significant other, or even a close friend. This term “qualifying relative” is crucial in IRS parlance for its implications on your tax dues.

Typically, any person can qualify as a dependent if more than half of their financial support, including living and medical expenses, is taken care of. Also, it’s an opportunity to boost one’s tax return by up to $500 with the Other Dependent Tax Credit.

What qualifies a person as a dependent?

The IRS bases dependents on two categories: “Qualifying children” and “Qualifying relatives.”2 You might think of a qualifying child as your son or daughter. Expanding the scope, a qualifying relative can be a sibling, a parent, or even a significant other.

The essence lies in their financial reliance on you and the nature of your relationship. They ought to:

Be related to you via blood, marriage, or adoption;

You provide over 50% of their financial support including housing, food, medical care, and other expenses

They are U.S. citizen.

The income of the possible dependent.

These nuanced rules might sound overwhelming, but IRS guidance and tax experts like TurboTax can help lighten the load.

Now, let’s address this sticking point: Can you actually claim your partner as a dependent? The following section unravels the mystique.

TurboTax

TurboTax® is the #1 best-selling tax preparation software to file taxes online. Easily file federal and state income tax returns with 100% accuracy.

This is how I have filed my personal taxes for many years.

Get Started

Can I Claim My Partner as a Dependent?

You can claim your partner as a dependent on your tax return, provided they meet certain criteria explained by the IRS, including passing the non-qualifying child test, the citizen or resident test, the joint return test, the income test, and the dependent taxpayer test.

I know this is where it gets difficult to follow for the average person.

So, we are here, to break this terminology down into layman’s terms, as such you can then make the best decision for your tax situation.

If you are still confused, then consult with an online tax software like TurboTax or a tax professional for guidance on your personal taxes.

Basic requirements for claiming your partner as a dependent

This essentially means that your partner should be financially dependent on you, where you bear more than half of their living expenses.

In essence, claiming your partner as a dependent revolves around these fundamentals: 2

Residency: Your partner must have been living with you for the full tax year.

Income limit: Your partner’s gross income should not exceed $4,700 for the year 2023.

Support Requirement: You are the main pillar for your partner’s financial needs by covering over half of their total expenses.

Anyone Else Claiming Them: None else should claim your partner as their dependent.

Unmarried. Your partner must be unmarried legally.

All fulfillment of these criteria moves you a step closer to enjoying some tax relief.

Confirm with an accountant or tax expert as exceptions can exist, such as temporary absences due to illness, education, business, and others.

Common scenarios where you can claim your partner as a dependent

Claiming a partner as a dependent isn’t as fancy as it sounds, but it’s plausible. Here are common scenarios enabling you to do so:

Co-habiting Before Marriage: You and your partner share a home, and you pay more than half of your partner’s living costs. However, your living situation cannot violate local laws, as in some states, “cohabitation” by unmarried people is against the law.

Unemployed Partner: Your partner’s tie with working life is severed (e.g., due to health issues or being laid off), and you bear most of the living expenses.

Supporting Student Partner: Your partner pursues their education, and you shoulder the majority of their expenses.

Take this interactive IRS quiz to determine whom I may claim as a dependent.

How much will I get if I claim my girlfriend as a dependent?

Now the pivotal question: what’s the advantage in dollars and cents?

In essence, claiming your partner as a dependent will slash your taxable income by $500 with the Other Dependent Tax Credit. 3

If you already qualify for Head of Household status with another dependent, then it is possible your deduction may be more. 4

Remember, there’s no one-size-fits-all answer. When tax complexities strike, consult an expert!

Is it better to claim my girlfriend as a dependent?

Honestly, like most tax questions, the answer is: it depends.

If you’re covering your partner’s majority expenses and they’re fulfilling all IRS criteria, then claiming them can bring solid tax savings.

Yet, bear in mind:

If your partner earns substantial income (greater than $4,700), they might lose personal benefits by becoming your dependent.

By claiming your partner, their Social Security or medical benefits may take a hit.

So, assess your partner’s income, benefit entitlements, and your tax situation. Then, tread wisely.

e-file

E-file makes tax season a breeze with its user-friendly interface, ensuring a seamless and stress-free experience for filers.

Simplify your tax journey by choosing E-file.

Start Now

Important Rules to Keep in Mind When Claiming Your Partner

When filing taxes, it’s crucial to understand that both parties are responsible for the accuracy of each other’s tax reporting and liability.

It’s worth noting that tax advantages and disadvantages exist in the scenario of being married and filing jointly, such as potential reductions in your tax bracket and sharing of business losses. So, it may be something to consider.

Can I claim my girlfriend as a dependent if she has no income?

In a nutshell, yes! If your girlfriend had no income in the tax year, you might claim her as a dependent. Given you provide over half of her total support and she lived with you all year, you’re golden.

For 2023, your partner’s gross income should not exceed $4,700.

However, keep in mind that in cases where public assistance or Social Security benefits are her primary financial sources, claiming her could negatively impact those benefits.

Learn the answer to do you have to file taxes if you have no income.

Remember: tax waters are often murky. When in doubt, lean on a tax professional’s shoulder!

Support factors

Answering the support question plays a hefty role in determining who qualifies as a dependent.

You shouldn’t just share the living cost; you should pay more than half of it. Remember, it includes an array of expenses, like food, clothing, education, or medical expenses.

The implication of your partner being claimed by someone else

Here’s a key rule: if someone else is claiming your partner as a dependent, you’re out of the game. The IRS rules say a person can be claimed as a dependent by only one taxpayer in a single tax year.

This could happen if your partner perhaps lives part of the year with someone else like a parent.

Another possibility is if your partner is legally married still, then they would have to file a married, filing separately return.

So, if your partner qualifies as someone else’s dependent, even if they don’t claim them, you can’t claim your partner.

Frequent Situations Where You Can’t Claim Your Partner as a Dependent

Considerations for Non-resident or Non-citizen partners

If your partner isn’t a U.S. citizen, resident, or national, the dependent claiming game changes. Notably, nonresident aliens cannot be claimed as dependents.

However, if your partner is a resident of Canada or Mexico or a U.S. national, you may claim them. But they should be living with you full-time. 2

This rule extends to partners awaiting changes in their residency or citizenship status. In such cases, you must wait until their status changes before claiming them.

When your partner earns more than the stipulated income threshold

When your partner’s income level sails past the IRS limit ($4,700 in 2023), claiming them as a dependent slips off the table. 2

Any part-time job, seasonal work, or income source counts, even those seemingly negligible. As soon as they cross this threshold, regardless of how heavily they rely on you or where they reside, they can’t qualify as your dependent.

Make sure to stay updated on IRS rules. They adjust the income limit for inflation annually, which changes this income ceiling. Keep an eye peeled for those IRS updates!

TurboTax

TurboTax® is the #1 best-selling tax preparation software to file taxes online. Easily file federal and state income tax returns with 100% accuracy.

This is how I have filed my personal taxes for many years.

Get Started

How to Officially Claim Your Partner on Your Taxes

To officially claim your partner as a dependent on your tax return, you will do this when you file your taxes.

Thankfully, this is made easier with online software companies like TurboTax or H&R Block.

The same is true when you are trying to figure out how to file taxes without a W2.

Necessary steps to claim your partner on your taxes

You will first identify them as “other qualifying dependent” or “other qualifying relative”.

Gather the facts first: Confirm your partner’s income, residency, and who has been supporting them for more than half the year.

Document expenses: Keep track of all relevant bills and receipts to demonstrate your majority support.

Use tax software or a professional: Follow prompts about dependents in tax software like TurboTax. They could guide you through the process and specifics.

Complete relevant Tax Forms: Prepare the necessary forms such as Form 1040 and Schedule H and have proof of residency, financial support, gross income information, and certification of your domestic partnership to support your claim.

File your return: Don’t forget to include your partner’s details and tick the correct boxes.

Remember, the devil is in the details. So carefully evaluate your situation to avoid missteps, and consult with a tax professional when in doubt.

Pitfalls to avoid while filing tax returns

While preparing to file your tax returns, beware of these common pitfalls:

Incorrect income calculation: Ensure you tally your partner’s gross income accurately. Reminder: it should not eclipse $4,700 in 2023.

Overlooked Living Qualification: Your partner must have resided with you the entire year. Temporary absences (illness, education) can be exceptions.

Ignoring Other Claimants: If someone else is poised to claim your partner as a dependent – even if they don’t – you can’t claim them.

Emergency Funds Consideration: If your partner taps into their savings for a large expense, this could speak against you providing most of their support.

Forgotten Documents: Maintain a record of bills, receipts, and other expense documents.

The IRS overlooks no mistakes, so take care and stay informed. When in doubt, professional tax help is a button away.

Frequently Asked Questions (FAQ)

Intriguing question! Here’s the short answer: Your partner’s marital status may indeed affect your ability to claim them as a dependent.

For instance, if your partner is married and files a joint tax return with their spouse, you can’t claim them as a dependent.

Remember, tax rules are lock-key specific, and bending them can lead to penalties. Always seek advice from a tax professional.

While you might be able to claim your partner as a dependent, laying claim on their children as dependents is unlikely. IRS rules are clear: you can claim a dependent only if they’re your child or relative.

Since your partner’s children don’t fulfill this requirement, you can’t claim them unless they can be considered your qualifying relative AND you provide more than half of their support.

As always, it’s best to run this by a tax professional for clarity on your unique situation. All we tax-seers can do is guide; the decision falls on your shoulders.

Here’s the hard truth: if your partner didn’t live with you all year, you couldn’t claim them as a dependent. IRS rules are stringent about this: your partner must have the same home as you for the entire year. That is 365 days, no less.

However, IRS grants a green light to temporary separations due to special circumstances like illness, education, military service, or even a holiday. The key lies in their intent to return and, of course, their follow-through.

Stay wise and stay informed, and consult with a tax analyst to seal your decision with assurance.

Get Online Help

Navigating tax rules and regulations doesn’t need to be overwhelming. With the advent of online help, understanding whether you can claim your partner as a dependent becomes considerably more manageable. Here are a few benefits of seeking online help:

Convenience: With online help, you can access the information you need anywhere, anytime. No need to schedule appointments or deal with traffic to get to a tax office. You can get the updates and instructions right from the comfort of your own home.

Accessibility: Some great examples of accessible platforms are TurboTax, e-File, and H&R Block which provide 24/7 support and resources. They offer a wealth of information and experts at your fingertips.

Expertise: Apart from the convenience, these websites employ tax experts who deliver professional analysis and guidance tailored to your specific needs. Specifically, you can use TurboTax Live Full Service for someone to do your taxes from start to finish. Or you can ask questions with TurboTax Live Assisted.

File your own taxes with confidence using TurboTax. This can greatly simplify the process and minimize potential missteps.

Now, Can I Claim my Unmarried Partner as a Dependent is Up to You

As they say, “Ignorance of the law is no excuse”. The same holds true for tax rules.

Falsely claiming a dependent can lead to severe penalties, not just a dinging of your wallet. You’d be sailing the choppy waters of tax evasion, which can bring on hefty fines or even dark days behind bars.

In blatant cases, the IRS could impose a Civil Fraud Penalty. That means a penalty amounting to 75% of the unpaid tax amount resulting from fraud. 5

In short, play by the rules! Accurate and clear tax filing may seem tedious, yet it will steer clear of any legal trouble. Remember, it’s always safer to ask if you are unsure!

Now, are you wondering why do I owe taxes this year?

Source

Internal Revenue Service. “Tax Tutorial.” https://apps.irs.gov/app/understandingTaxes/hows/tax_tutorials/mod04/tt_mod04_glossary.jsp?backPage=tt_mod04_01.jsp#dependent. Accessed October 23, 2023.

Internal Revenue Service. “About Publication 501, Dependents, Standard Deduction, and Filing Information.” https://www.irs.gov/forms-pubs/about-publication-501. Accessed October 23, 2023.

Internal Revenue Service. “About Publication 501, Dependents, Standard DeductionUnderstanding the Credit for Other Dependents.” https://www.irs.gov/newsroom/understanding-the-credit-for-other-dependents. Accessed October 23, 2023.

Intuit TurboTax. “Guide to Filing Taxes as Head of Household.” https://turbotax.intuit.com/tax-tips/family/guide-to-filing-taxes-as-head-of-household/L4Nx6DYu9. Accessed October 23, 2023.

Know someone else that needs this, too? Then, please share!!

Did the post resonate with you?

More importantly, did I answer the questions you have about this topic? Let me know in the comments if I can help in some other way!

Your comments are not just welcomed; they’re an integral part of our community. Let’s continue the conversation and explore how these ideas align with your journey towards Money Bliss.

You may have read a certain ABC news report that a man made his final mortgage payment with pennies he had collected over the years.

If not, the story goes like this. During the past 35 years, Milford, Massachusetts resident Thomas Daigle began saving pennies to pay off the mortgage on his first home.

The first one was supposedly found on the ground of the parking lot as he left the bank where he obtained his mortgage.

He told his wife at the time that he’d use pennies to make his final mortgage payment, and because “his word” meant everything, he stuck to it.

As time went on, any penny he encountered would be collected and put with the rest, eventually rolled and packed into boxes in his basement.

He kept a tally of the total number of pennies so he’d know when he met his goal.

And in April, on his 35th wedding anniversary, he took the pennies down to Milford Federal Savings and Loan Association and made his final payment, just as he said he would.

It is estimated that the 62,000 pennies weighed roughly 427 pounds, depending on the material they were made with.

Cool Yes, Practical No

While this story is heartwarming and certainly admirable in a very unconventional type of way, it’s clearly nowhere close to practical.

Sure, he was able to save $620 worth of pennies and make a “free” mortgage payment, but let’s analyze the amount of work he put into it.

The man picked up pennies and sifted through his coins for pennies and rolled them for decades – that is certainly a lot of work for $620, especially when inflation adjusted.

He probably also obsessed over pennies for years and drove his wife nuts.

The poor employees at the savings and loan also had to count the 400 pounds of pennies once he brought them in, probably only agreeing to it because of the nature of the story and the fact that it’s their 125th anniversary this year.

A Better Alternative

What Daigle could have done instead was make biweekly payments, or simply make an extra payment each year.

Or pay a little extra each time he made a monthly mortgage payment.

Even if he only added $10 or $20 to his mortgage payment each month, he would have saved a whole lot more than one single payment.

He probably could have refinanced his mortgage as well as mortgage rates dropped over the years and shortened his term.

And he would have paid his mortgage off early while saving thousands of dollars, not just $620.

Oh, and he wouldn’t have had to touch a single penny or waste hours rolling them.

Of course, he may have enjoyed the whole process, and clearly was happy to have met his goal.

The takeaway here is that simple things like paying a little bit extra or refinancing when rates drop substantially can lead to huge savings on your mortgage over the long term.

So take a proactive approach to your mortgage – it’s a huge financial decision and one that needs lots of care and attention over the years, not just at the outset.

For the record, Daigle said he’s no longer saving pennies, and seems to want nothing to do with them at this point.

He’s now focused on collecting grandchildren, who will likely pass down this story for generations. Hopefully none will repeat it.

According to reports from the second quarter of 2022, the total of all household debt in the United States is a whopping $16.15 trillion. Mortgages make up the bulk of that debt, with student loan, auto loan and credit card debt trailing behind.

On average, adults in the United States carry debt loads ranging between $20,800 and $146,200. If you’re in debt and looking for a way to pay it off, making a plan is a critical step. Find out more about how to get out of debt below.

1. Collect All Your Paperwork in One Place

Before you can get out of debt, you need to know how much debt you actually have. You should also know who you owe and what the terms are, as this can help you prioritize debt payments to pay them off faster.

Start by collecting all your debt paperwork in one place and creating a master list of everything you owe. You can do this in a spreadsheet or with a pen and paper. Information to gather includes:

Statements for all your debts. One way to do this is to spend a month saving all your financial mail and email so you have a comprehensive picture of your debt.

Regular bills that aren’t debts. Your cell phone and utility bills, as well as your rent, should all be included when you gather this financial information. Information about income. Look at paycheck stubs or your bank accounts so you know what, on average, you can expect in income each month.

Your credit reports. Get your free credit reports at AnnualCreditReport.com to ensure you know about all the debt you owe.

Tip: Sign up for ExtraCredit to see your credit reports and 28 FICO® scores in one place.

2. Create a Budget and Determine What You Can Pay Every Month

Using the information you gathered in the above step, create a monthly budget. Make sure you cover all your bills and minimum debt payments. When possible, include an amount that can go toward building your savings. Allocate funds for essentials, such as groceries and gas.

Once you cover all the needs for the month, figure out how much money you have left. How much of that can you put toward extra debt payments so you can start getting ahead on debt?

3. Manage Your Debts in Collections

If you see that you have any debts in collections when you pull your credit reports, make sure you have a plan for taking care of them. Collection accounts have a serious negative impact on your credit score. Creditors may also sue you and try to collect on these accounts via wage garnishments or bank levies if you don’t take action to manage collections. That can throw a huge wrench into your plan for getting out of debt.

Tip: If you don’t enjoy manual calculations, check out Tally. You can use Tally to total up your expenses, pay down credit card bills, and generally figure out where you stand.

4. Consider Your Options

There are two main approaches to paying off debt as quickly as possible: the snowball method and the avalanche method.

The snowball method involves paying off accounts with the lowest balances first. You take any extra money you have—even if it’s just $50—and add it to your regular minimum monthly payment on that small balance. When that balance is paid off, you take the extra $50 plus the minimum payment and add it to the next biggest balance. You keep doing this as you work your way up to larger balances, paying your debt off faster and faster.

With the avalanche method, you tackle accounts according to interest rates. You start by paying off accounts with the highest interest rates first. The thought behind this method is that you save money in the long run by tackling high-interest debt first.

5. Try to Reduce Your Interest Rates

Interest refers to how much your debt costs. If you have a lower interest rate, your debt costs less and you can pay it off faster. Here are some ways you can try to reduce interest rates on your debts:

Ask for a lower interest rate. If you’re a credit card account holder in good standing and your credit history and score has improved since you got the card, you may be able to get a better rate. Call customer service for your card and let them know you are looking for a better deal. They may agree to lower the rate to keep you as a cardholder.

Look into debt consolidation or refinancing. A debt consolidation loan provides funds you can use to pay off higher-interest debts. Refinancing occurs when you get a new loan for a home or car. If you had lackluster credit when you got your auto loan, for example, you may be able to refinance it for a lower rate if your credit has improved.

Get a balance transfer credit card. You may be able to transfer balances from a credit card with a high interest rate to one that has an introductory low APR offer. This may allow you to pay off the debt over the course of 12 to 22 months without incurring any more interest expense.

Upgrade Triple Cash Rewards Visa®

$200 bonus after opening a Rewards Checking Plus account and making 3 debit card transactions*

Unlimited cash back on payments: 3% on Home, Auto, and Health categories and 1% on everything else after you make payments on your purchases

No annual fee

Combine the flexibility of a credit card with the predictability of a personal loan

No touch payments with contactless technology built in

See if you qualify in minutes without hurting your credit score

Great for large purchases with predictable payments you can budget for

Mobile app to access your account anytime, anywhere

Enjoy peace of mind with $0 Fraud liability

*To qualify for the welcome bonus, you must open and fund a new Rewards Checking Plus account through Upgrade and make 3 qualifying debit card transactions from your Rewards Checking Plus account within 60 days of the date the Rewards Checking Plus account is opened. If you have previously opened a checking account through Upgrade or do not open a Rewards Checking Plus account as part of this application process, you are not eligible for this welcome bonus offer. Your Upgrade Card and Rewards Checking Plus account must be open and in good standing to receive a bonus. To qualify, debit card transactions must have settled and exclude ATM transactions. Please refer to the applicable Upgrade VISA® Debit Card Agreement and Disclosures for more information. Welcome bonus offers cannot be combined, substituted, or applied retroactively. The bonus will be applied to your Rewards Checking Plus account as a one-time payout credit within 60 days after meeting the conditions.

Do Your Best to Pay More Than the Minimum

Only paying the minimum on high-interest debt, such as credit card debt, doesn’t get you out of debt fast. It can take years—dozens of them—to pay off credit card balances if you’re only making minimum payments.

Instead, put more than the minimum on your debt whenever possible. You may also want to put any additional funds you receive—such as a tax refund—on your debt to help with this process.

Consider More Options for Getting Out of Debt

Creating a budget, managing your money wisely, and making extra payments toward your debt all help you get out of debt. Here are some other ways you can deal with debt:

Increase your income while cutting unnecessary spending. Join the gig economy with a side job to earn extra money, or sell things you don’t need via online marketplaces.

Undergo credit education and counseling. These services can help you make the most of your monthly budget.

Engage in debt settlement. You may be able to negotiate with creditors, especially for accounts in collections, to settle debts for less than you owe. Just make sure you understand any effects on your credit.

Enter a debt management plan. During such a plan, you make a single payment to a trustee. They use those funds to pay your debts, hopefully in a way that gets you out of debt faster. Declare bankruptcy. If you find you’re unable to pay your debts, much less make extra payments, you may need another option. Chapter 7 and Chapter 13 bankruptcy are potential considerations.

How to Avoid Getting into Debt

Paying off debt doesn’t have to be impossible, but it can be challenging. For many people, it requires altering years’ worth of financial habits. If you’re not already in debt, it may be easier to stay out of it. Create a budget and stick to it, spend wisely and avoid using credit cards for things you don’t need or can’t afford to buy with cash.

When you take out a mortgage, whether it’s a refinance or a home purchase, you may come across the phrase “cash to close.”

Virtually all mortgages require some financial contribution from the borrower to fund the loan.

It might be down payment funds, it might be lender fees, or it might be prepaid charges like property taxes and homeowners insurance.

There’s a good chance it’ll be a combination of these things, which will need to be paid at closing via a verified account.

Let’s talk more about the meaning of cash to close, how it’s calculated, and how it’s paid.

Cash to Close on a Home Loan Is More Than Just Closing Costs

If you look at your paperwork, you should see a list of closing costs associated with your home loan.

You can see estimates of these costs on both your initial Loan Estimate (LE) and also on your Closing Disclosure (CD).

And when it’s about time to close your loan, on the settlement statement prepared by your escrow officer or real estate attorney.

On these documents, you should see things like the loan origination fee, underwriting and processing fees, and other lender fees.

Additionally, there will likely be a charge for an appraisal, along with a charge for title insurance, homeowners insurance, and escrow services.

Under that escrow/title umbrella, more fees will be listed, such as courier fees, wire fees, notary fees, loan tie in fees, settlement fees, and on, and on.

There will also be recording fees and transfer taxes, along with prepaid items such as X number of months of taxes or insurance.

That’s the closing cost piece, which includes both lender fees (if applicable), and third-party fees, such as the insurance, appraisal, title/escrow.

Pretty straightforward, but we also have to consider the down payment, any deposit such as earnest money, and any seller or lender credits.

Then some math needs to be done to figure out the final amount due, which is, drumroll, the cash to close.

Fortunately, there’s a section on the LE and CD called “Calculating Cash to Close,” which breaks it all down for you.

How to Calculate Cash to Close: An Example

It’s probably easier to look at an example rather than keep talking about it. So check out the screenshot above, taken from a Closing Disclosure.

As you can see, it lists total closing costs, down payment funds, deposits, and credits.

In this example, the purchase price is $852,500 and the home buyer is putting down 20% to avoid mortgage insurance and get a better mortgage rate.

They’ve got $12,432.26 in closing costs, of which $435 was paid out-of-pocket before closing for an appraisal.

The borrower made a $25,875 earnest money deposit for 3% of the purchase price as well, which was originally $862,500 before a slight price reduction.

They didn’t finance any closing costs, nor did they receive any funds via the transaction.

But they did get a seller credit of $7,500 and a $4,372.88 rebate from their real estate agent.

So to tally it up, we have $182,932.26 in total costs, and $38,182.88 in credits.

That means the borrower still owes $144,749.38, which is the remaining balance after their deposit and various credits.

It covers the remaining down payment and remaining closing costs, and is typically wired to escrow at closing.

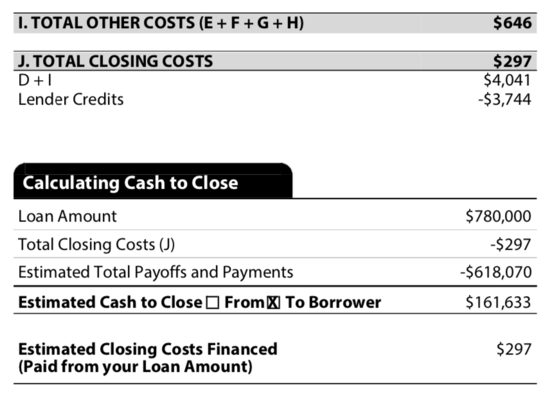

What About Cash to the Borrower?

Now let’s look at a cash out refinance. In this case, there is cash going to the borrower at closing because they’re tapping their home equity.

So instead of sending money to the lender, the bank is sending money to the borrower.

In this example, the borrower also took advantage of a lender credit, which offset nearly all of their closing costs.

Their loan payoff on their existing mortgage was $618,070 and the new loan amount was $780,000.

That would send $161,930 to the borrower, but once we subtract the $297 in remaining closing costs, it’s $161,633.

Sending the Cash to Close: Some Things to Remember

When it comes time to send your cash to close funds, you’ll likely do so via wire, or possibly a cashier’s check.

Either way, the funds must come from a sourced account that was verified during the underwriting process.

For example, a bank account you verified earlier on by connecting it in the digital application or uploading monthly statements.

This way they know the money is actually coming your own funds, and not some other unverified source.

If it does come from a non-sourced account, it could delay your loan closing and cause a lot of headaches.

Remember, such funds should also be seasoned for at least two months prior as well, meaning in the account and untouched for 60+ days.

Again, this ensures the funds are your own and not someone else’s, or worse, a loan, which you deposited into your own account.

If you have questions about what is owed, it’s always helpful to speak directly with the settlement officer, who can go over everything with you line by line.

That way you know exactly what you owe, why you owe it, and most importantly, where exactly to send it.

To summarize, there are a lot of costs associated with a home loan, many of which you won’t be aware of until you go through the process yourself.

This is why it’s imperative to get a robust mortgage pre-approval and set aside funds well before beginning your home search.

“The IDR account adjustment puts everybody closer to the statutory [student loan] cancellation that they could be eligible for under the income-driven repayment plans, regardless of whether or not they enrolled in an IDR plan in the past,” explains Kyra Taylor, a staff attorney focused on student loans at the National Consumer Law Center.

Even if your loans aren’t automatically forgiven, the account adjustment will move you closer to the end of your repayment period and closer to forgiveness if you sign up for an IDR plan, which typically takes 20 or 25 years of full monthly payments.

For borrowers who’ve been in repayment for less than 20 or 25 years, here are answers to questions about the IDR account adjustment, and steps they can take to get the most out of it.

When will the IDR adjustment happen if I don’t get automatic forgiveness?

Borrowers who receive IDR credit under the account adjustment — but not enough to automatically qualify for forgiveness — will see their payment count updated sometime in 2024. The Education Department has not given an exact date yet.

How much IDR credit will I get?

To find out how much credit toward IDR forgiveness you’ll receive under the one-time IDR account adjustment, you can tally past payments yourself. Generally, borrowers get IDR forgiveness after 20 or 25 years on an IDR plan, or 240 or 300 monthly payments, which are capped at a certain percentage of their income.

Log in to your Federal Student Aid account at StudentAid.gov to see how long you’ve been in repayment. For detailed information, including descriptions of specific forbearance or deferment periods, request your account history from your servicer.

The adjustment will include the following past periods, through August 2023, toward the number of monthly payments needed to reach forgiveness:

Any month a borrower was in repayment, even if the payments were late or partial. The type of repayment plan doesn’t matter.

Time spent in forbearance, either periods lasting 12 or more consecutive months or a cumulative 36 or more months.

Any month spent in deferment, other than in-school deferment, before 2013.

Any month spent in economic hardship or military deferments on or after Jan. 1, 2013.

Any months in repayment, forbearance or a qualifying deferment before a loan consolidation.

Any months spent in COVID-19-related forbearance.

Past months spent in default will generally not be included in the recount, though borrowers who enroll in the temporary Fresh Start program to get out of default will get IDR credit from March 2020 through the date they leave default.

How to benefit from the account adjustment

The account adjustment will be automatic for most borrowers, but some borrowers need to take an extra step before the end of 2023. If you want to benefit from the account adjustment to reach loan forgiveness more quickly, you must sign up for an IDR plan.

Consolidate your loans if necessary

Borrowers with certain types of loans will need to consolidate them into direct loans by the end of 2023 to receive the account adjustment.

These types of loans must be consolidated to receive IDR credit if they don’t reach the forgiveness threshold:

Commercially managed FFEL Program loans, i.e., those held by companies like Navient.

Perkins loans.

Health Education Assistance Loan (HEAL) Program loans.

Parent PLUS loans.

If you consolidate loans that were in repayment for different periods of time, the new consolidation loan gets the maximum amount of IDR credit that accrued among the loans, Taylor explains.

Enroll in an IDR plan

Federal student loan borrowers will need to start making payments again this fall. Interest resumed on Sept. 1, and bills will come due in October.

For borrowers who anticipate having a leftover balance after the account adjustment, enrolling in an IDR plan now is very important, says Mike Pierce, executive director of the Student Borrower Protection Center, a nonprofit that advocates for student debt relief. This will allow borrowers to continue making progress toward IDR loan forgiveness once payments restart, he says.

SAVE is a good option for most borrowers. Benefits include halved monthly bills for most borrowers with undergraduate loans, no compounding interest if you make regular payments and faster forgiveness for borrowers with smaller balances.

Some middle- or low-income borrowers could even see $0 monthly payments under SAVE, while working toward loan forgiveness. For these borrowers, SAVE “is basically an extension of the payment pause that you just have to fill out some paperwork for,” Pierce says.

Parent PLUS borrowers are only eligible for the Income-Contingent Repayment plan, which is the “least generous” of the four IDR plans, says Taylor. Monthly ICR payments can be high: they’re capped at 20% of the borrower’s discretionary income, rather than 5% to 10% under the other three IDR plans.

Borrowers with parent PLUS loans should see how close they are to cancellation and whether it’s worth it to consolidate and enroll in ICR as a step toward loan forgiveness, Taylor explains.

What if I’m enrolled in Public Service Loan Forgiveness?

If you have at least one approved PSLF form, you may see your payment count adjusted as early as the fall of 2023. Servicers will continue to adjust PSLF counts monthly until the final adjustment in 2024.

Under the account adjustment, you’ll get PSLF credit for any month, dating back to October 2007, in which you had qualifying employment and were in a repayment status, regardless of the payments made, loan type or repayment plan. Borrowers who qualify for PSLF get loan forgiveness after just 10 years, or 120 monthly payments.

The account adjustment is automatic for all PSLF-eligible Direct Loans, including consolidated and unconsolidated parent PLUS loans — but borrowers with commercially or federally held FFELP loans must consolidate them before the end of 2023 to receive the adjustment.

Use the Federal Student Aid office’s PSLF Help Tool to certify periods of employment and track progress toward loan forgiveness under PSLF.

Paper trading is simulated trading, done for practice without real money. It’s a way to test different trading strategies without the risk of losing money, before an investor starts trading with real capital.

The practice gets its name from how investors would once mark down their hypothetical stock purchases and sales — and track their returns and losses — on paper. But today, investors typically use digital platforms to virtually test out hypothetical investment portfolios, day-trading tactics, and broader investing strategies.

How do Paper Trades Work?

What is paper trading? In its most basic form, paper trading involves selecting a stock, group of stocks, or a sector, then writing down the ticker or tickers and choosing a time to buy the stock. The paper trader then writes down the purchase price or prices.

When they sell the stock or stocks, they write down that price as well, and tally up their return. 💡 Quick Tip: Before opening any investment account, consider what level of risk you are comfortable with. If you’re not sure, start with more conservative investments, and then adjust your portfolio as you learn more.

Pros and Cons of Paper Trading

Paper trading has both benefits and drawbacks. Here are a few factors to consider before you try paper trading.

The Pros of Paper Trading

Build skills: Paper trading is a way to learn and build trading skills in either a bear or a bull market. For new traders, a virtual trading platform offers a way to make rookie mistakes without risking real money. It’s a method to get comfortable with the process of buying and selling stocks, and making sure you don’t enter a limit order when you mean to place a market order.

Test out strategies: Paper stock trading allows for experimentation. For example, an investor might hear about shorting a stock. But they may not know how the process works, and what it actually pays out. Paper trading permits investors to learn how these trades work in practical terms. Or, they might want to try out other strategies, such as swing trading.

Learn about strengths and weaknesses: Paper trading is also a way for investors to learn about their own strengths and weaknesses. Traders lose money in the markets for a number of personal reasons. Some stick to their guns too long, while others give up too soon when the market is down. Some lose money because they panic, while others lose money because they ignore clear warning signs. Paper trading is a way for investors to learn their own tendencies and weaknesses without paying for the lesson.

Keep emotions out of it: Finally, paper trading can help teach investors to keep their emotions in check while the markets are going up and down. Investing with hypothetical dollars can be good practice in the valuable art of making rational decisions in stressful situations and allow investors to find risk management techniques that work best for them.

The Cons of Paper Trading

It’s not real: The biggest drawback of paper trading is that it’s not real. An investor can’t keep the returns they earn paper trading. And those paper returns can lead the investor to have an unrealistic sense of confidence, and a false sense of security. Paper trading also doesn’t account for real-life situations that might require an investor to withdraw money from the market for personal reasons or the impact of an unexpected recession.

The emotional impact is hard to gauge: Paper trading does limit the impact of emotions, but once an investor’s real, actual money is in play, it may be more difficult to reign in emotions. That money represents a month’s salary, or a semester’s tuition, or a house payment, and so forth, so it can be hard to remain calm and keep perspective when the market plunges over the course of a trading day.

Could be misleading: While paper trading offers important lessons, it can also mislead investors in other ways. If a paper trading strategy focuses on just a few stocks, or using one trading strategy, they can easily lose sight of how broader market conditions actually drive the performance of those stocks, including stock volatility, or their strategy, or have an inflated confidence in their ability to time the markets. They need to realize their holdings or strategy may offer very different results in a real-world scenario.

Doesn’t involve the true costs of trading: Another danger with paper-trading is that traders may overlook the cost of slippage and commissions. These two factors are a reality of actual trading, and they erode an investor’s returns. Slippage is the difference between the price of a trade at the time the trader decides to execute it and the price they actually pay or receive for a given stock.

Especially during periods of high volatility, slippage can make a significant impact on the profitability of a trade. Any difference, up or down, counts as slippage, so slippage can be good news at times. Since brokerage commissions and other fees always come out of a trader’s bottom line, paper traders should include them in their model. 💡 Quick Tip: Are self-directed brokerage accounts cost efficient? They can be, because they offer the convenience of being able to buy stocks online without using a traditional full-service broker (and the typical broker fees).

Live Trading vs Paper Money

When an investor uses live trading, they are using real money to buy and/or sell stocks or other securities. They will confront market fluctuations and need to make decisions, sometimes quickly, about what to do. Live trading can be very stressful, but it does offer the opportunity for an investor to earn money. However, it also comes with the very real risk of losing money.

With paper trading, there is no money involved to lose. But once again, it’s not “real,” so while it may teach you some basics, paper trading does have limits and drawbacks, as detailed above.

Paper Trading in the Digital Age

Wondering how to paper trade? There are different ways to do it. Some investors swear by a tangible notebook-and-paper approach to paper trading, others keep a spreadsheet, which allows them to track other factors involved in the investment, including the exact time of the purchase and sale, volume, holding period, index direction, overall market volatility, and other factors they may be studying.

But while paper or spreadsheets are valuable tools, most investors testing out their trading chops or portfolio-construction skills now prefer virtual trading platforms, which pit a hypothetical portfolio or strategy against real markets. These platforms mimic the look and feel of an actual trading platform, but deal only in hypothetical assets. Understanding a platform can make it easier to transition to real-life trading in the future.

On these platforms, an investor will start with fake money and begin trading. As they do, they can track the fluctuations in an account’s value, along with profit and loss, and other key metrics. Many trading simulators offered by online brokerages allow investors to virtually trade in real-time during live markets without risking their money. For some investors, this can be a valuable experience before they dive in with real money–and the potential for real losses.

Recommended: Managing the Common Risks of Day Trading

How to start paper trading

If you’d like to try paper trading, be sure to research your investments, just like you would if you were investing for real, and use the same amount of paper money you would use in real life. This will help mimic the actual experience.

If you choose to paper trade with a pencil and paper, you can simply choose a stock or group of stocks, write down the ticker, and pick a time to buy the stock. You then write down the purchase price, or prices. When you sell the stock you record that price and then figure out your up their return.

If you decide to use a virtual trading platform, you’ll need to choose a platform. There are many free platforms available. You may want to look for one that has live market feeds so that you can practice trading without delays.

Setting up a Paper Trading Account

Once you’ve selected a virtual trading platform, you’ll set up an account. Simply log onto the platform and follow the prompts to set up an account. Once you’ve done that, there should be a “paper trading” option you can click on.You’ll need to select a balance and then you should be able to start simulating trading.

The Takeaway

Paper trading can be a way to learn about investing. By keeping track of all trades, and the losses or gains they generate, it creates a low-stress practice for examining why certain stocks, and certain trades, perform the way they do. That can be invaluable later, when there’s real money on the line.

However, remember that paper trading isn’t real. In real-life trading with an investment account, you’ll have the potential for gains, but also for losses. Make sure you are comfortable taking that risk.

Ready to invest in your goals? It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here).

Invest with as little as $5 with a SoFi Active Investing account.

FAQ

Do you make money from paper trading?

No. With paper trading, there is no real money involved, so there is no opportunity to make (or lose) money. Paper trading is a way to learn about trading without risking money.

How realistic is paper trading?

Paper trading involves using real trading strategies and simulates a real market experience. However there are no real losses or gains since no real money is involved. Because of that, it doesn’t convey a fully realistic experience.

Is paper trading good for beginners?

Paper trading can be a way to learn the basics of investing. A beginner could build their skills and test different strategies without risking loss. However, paper trading can be misleading because there is no real risk involved. An investor might be tempted to take more risks than they would in a real life investing scenario, for instance.

Why is paper trading important?

Paper trading could be important because it allows beginning investors to practice trades, build their skills, and test different market strategies, without the risk of losing money. However, it can’t replicate the experience of real trading with actual money and the potential to possibly lose money, which someone who tries paper trading should keep in mind.

Photo credit: iStock/fizkes

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Colorado Springs-area home sales fell again last month and prices remained flat as the local housing market continued to feel the effects of spiking mortgage rates.

According to a new Pikes Peak Association of Realtors market trends report that examined home sales last month that took place mostly in the Springs and surrounding El Paso County:

• Single-family home sales totaled 1,067 in August, a nearly 22% decline from the same month last year and the 15th consecutive month that local sales have fallen on a year-over-year basis.

• Homes spent an average of 29 days on the market in August before they sold, an increase from 17 days during the same month last year.

• The median price, or midpoint, of homes that sold in August was $480,000, a 0.1% drop from $480,592 in August 2022. Home prices had increased each month from December 2014 to November 2022, but began to slide late last year and now have declined on a year-over-year basis in eight out of the last nine months.

• The supply of homes listed for sale totaled 2,420 in August, down 8.3% from the same month last year. On the one hand, August’s listings were the most for any month since November, yet they remained far below pre-Great Recession years, when August inventories often topped 3,000 and 4,000.

The Springs-area housing market, like that of many other cities, has done an about-face since the second half of last year because of higher long-term mortgage rates.

For years, historically low rates in the neighborhood of 3% for a 30-year, fixed-rate loan helped spur a furious demand for single-family homes. That demand, coupled with a shortage of properties for sale, sent Springs-area median home prices soaring over several years; in June 2022, they hit a record high of $495,000.

Sign up for free: News Alerts

Stay in the know on the stories that affect you the most.

Success! Thank you for subscribing to our newsletter.

After the Federal Reserve began to hike interest rates last year to tamp down surging inflation, mortgage rates rose, too, and roughly doubled to more than 6% for 30-year loans by the end of last year.

That trend of high rates continued through the first several months of this year. In mid-August, long-term mortgages topped 7%; last week, the national average for a 30-year, fixed rate mortgage was 7.18%, according to mortgage buyer Freddie Mac.

Higher rates have priced many homebuyers out of the market and sent sales plunging.

Local real estate agents, however, have said that the demand for homes remains relatively strong. As a result, and combined with tight inventories, prices haven’t plunged, though they are down from their record highs.

The new home side of the Springs-area housing market also has felt the effects of higher mortgage rates.

In August, 127 permits were issued for the construction of single-family, detached homes, according to a new Pikes Peak Regional Building Department report. August’s tally was up 15.5% compared with the same month last year.

But the pace of home construction through the first eight months of this year remains well behind the same period in 2022, Regional Building Department figures show. Through August of this year, single-family detached permits totaled 1,655, down 36.4% from 2,604 on a year-over-year basis.

Pssst. Some People Think NFP Could be Even Weaker Than Forecast

By:

Matthew Graham

Thu, Aug 31 2023, 4:35 PM

Pssst. Some People Think NFP Could be Even Weaker Than Forecast

This morning’s economic data came out slightly stronger than expected, on balance, and bonds rallied anyway. Granted, Core PCE inflation was 0.2 vs 0.2, but excluding housing, core PCE was higher for the 2nd straight month and the annual tally remains way too high and very flat. Add the lower jobless claims number (and the beat in Chicago PMI if you want) and the most logical reaction would have been to sell. In the market’s defense, shorter term rates DID sell, but not too much. One is forced to conclude that month-end trading distorted the day OR that there’s a fair amount of belief in the whisper number on NFP being lower than forecast due to labor strikes. We’d emphasize that such whisper numbers do not matter in a world where NFP routinely surprises by 100k+ and where the whispers are only thinking of a 30-40k delta.

Jobless Claims

228k vs 235k f’cast, 232k prev

Core PCE Inflation m/m

0.2 vs 0.2 f’cast, 0.2 prev

Challenger Job Cuts

75.15k vs 23.69k prev

08:50 AM

Flat overnight and flat after data. 10yr down 0.6 bps at 4.106. MBS up 1 tick.

11:32 AM

Modest strength continues for long end. 10yr down 1.8bps at 4.094. MBS up an eighth.

03:02 PM

Off the best levels in the PM hours. Not much volatility surrounding month-end 3pm closing bell. 10yr down 2bps at 4.09, but up from lows of 4.077. MBS still up 2 ticks (.06), but down 3 ticks (0.09) from highs.

04:20 PM

Some illiquidity-driven weakness making for a 1 tick (0.03) loss in MBS. Some organic weakness bringing 10yr up to 4.104 (but still down .8bps on the day).

Download our mobile app to get alerts for MBS Commentary and streaming MBS and Treasury prices.