For years broker channel evangelists told me that a down market would give them an edge on their retail brethren. Well, it’s certainly been a down market. How has the broker channel fared in the wake of the Fed rate hikes?

We asked the good folks at mortgage data technology firm InGenius to run the numbers, comparing the first six months of 2022 to the first six months of this year. Take a look.

“From the first six months of 2022 to first six months of 2023, brokers have increased their percentage from 23% to 28% while retail has decreased by that same percentage,” Jeff Walton, CEO and co-founder of InGenius, said. “There’s definitely a shift and while we know there is a lot of movement going on with people losing jobs because of mergers or closures, a certain percentage are moving to brokerage instead of another retail company.”

It shouldn’t come as a great surprise that wholesale has gained market share as refi activity has slowed. A significant number of retail lenders were purpose-built to pump out huge refi volumes with a call center model. Broadly speaking, the broker space tends to be more relationship focused, which lends itself better to a purchase environment.

Though virtually every mortgage lender is down because of the high-rate environment (excepting homebuilder-affiliated mortgage firms, of course), purchase volumes are still above 2019 levels. It’s refinancings that have fallen off a cliff, and they are unlikely to return in force in 2024. Should current market conditions remain, I expect the broker channel to gain a couple more points of market share over the next year (even after several notable lenders exited the channel and United Wholesale Mortgage exerts its dominance).

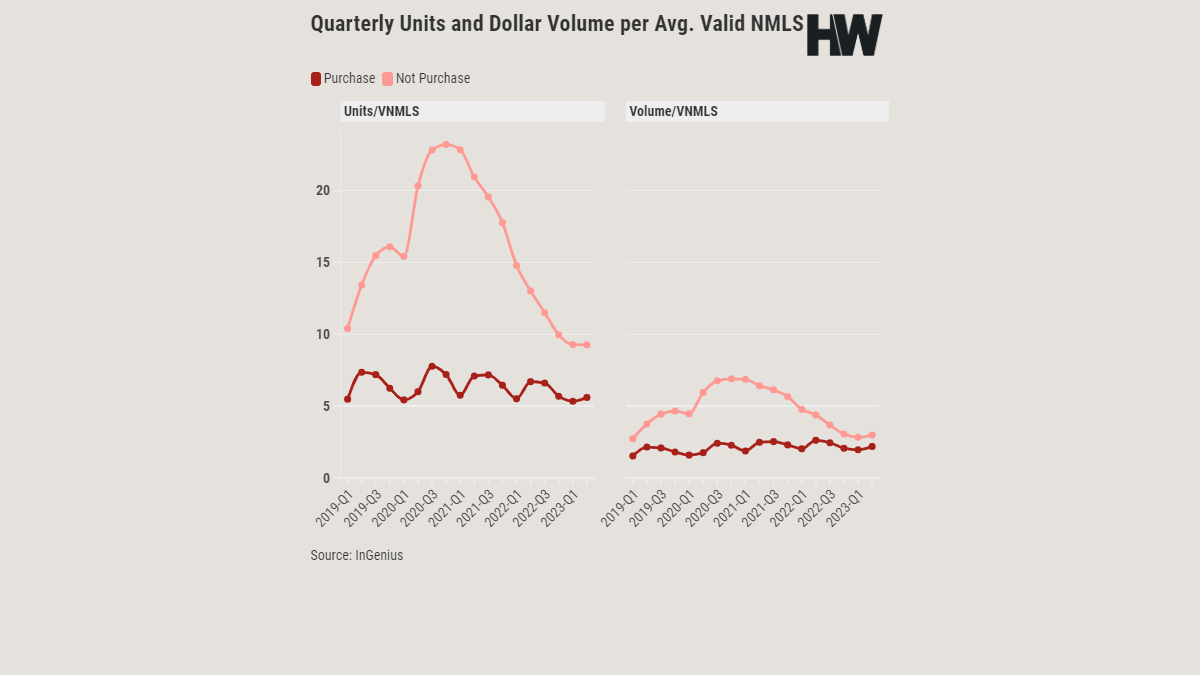

Setting channel side, where are we in terms of the overall LO landscape? Let’s look at InGenius’ data on the number of loan officers and corresponding production levels.

The InGenius data dating back to Q1 2019 points to some sobering trends. In Q2 2023, the number of valid LOs fell to 89,094. That’s well below the high of 181,656 achieved in Q3 2021 and even the average of about 146,000 since early 2019.

Since Q1 2019, the average LO has pumped out just under 16 loans per quarter at $4.8 million in origination volume. At the height of the boom, in Q1 2021, the average LO originated nearly $6.9 million. But in Q2 2023, the average LO generated just 9 loans worth $2.9 million. It’s a big drop.

If you’re looking for a silver lining, it’s undoubtedly that purchase volume per LO has remained consistent. The average LO achieved $2.2 million in purchase volume in Q2 2023, besting the average since Q1 2019.

It’s not crazy to think that the LOs who haven’t been able to generate enough purchase business have already washed out. About 20,000 LOs have dropped out per quarter since Q2 2022, per InGenius data. How many more are just hanging on?

While the next year will likely continue to be a relative struggle for even high producers (many of the industry’s best are down 50% year-over-year), the opportunities for purchase-tested LOs when the market rebounds could be fantastic. All they have to do is survive.

In our weeklyDataDigest newsletter, HW Media Managing Editor James Kleimann and Data Journalist Will Robinson break down the biggest stories in housing through a data lens. Sign up here! Have a subject in mind? Email James at [email protected].

Demand for home decor products is surging as people are inclined to show their creativity through DIY activities. Consumers prefer sustainable options to decorate their home interiors because of growing concerns about environmental impacts.

NEWARK, Del, Oct. 05, 2023 (GLOBE NEWSWIRE) — The home decor market is projected to register a valuation of US$ 216,291.4 million in 2023 and reach up to US$ 394,715.7 million by 2033. The global market is securing a CAGR of 6.2% during the forecast period.

Get your Sample Report: https://www.futuremarketinsights.com/reports/sample/rep-gb-4831

Manufacturers are Designing Customized Home Decor Solutions

Manufacturers are designing customized home decor solutions as per consumers’ expectations. They are offering personalized, durable, and unique options with eco-friendly practices. Some of the customized solutions for home decor are as follows:

Personalization: Manufacturers offer personalized home decor products, including high-quality material, custom color, and concise designs. They are also offering interior design as per consumers’ tastes and preferences.

Modular and Configurable Furniture: Manufacturers provide customized, fit, and layout modular furniture systems of different sizes. They are also adapt to change as per customers needs.

Custom Upholstery: These custom upholstery furniture, including chairs, sofas, tables, and beds, are offered by manufacturers as per customers’ selection. Consumers widely prefer these for their creative home decor.

Artful Decor: Consumers are fond of creativity and artwork. They desire high-end manufacturers to build bespoke furniture designs. The customers are also collaborating with special designers to create a specific piece of home decor.

Custom Lighting: Creating unique lighting solutions for home decor interior are rapidly growing to look lavish and breath-taking. They fix them according to size, design, and area.

Digital Tools: Manufacturers offer digital tools to their customers. Through these tools, customers can finalize their products by visualizing them.

Tailored Textiles: Customized textiles are widely used for home decor, including cushions, curtains, and bedding. They seek aesthetic fabrics to match their home decor for specific areas.

“Social media platforms’ influence on home decor is rapidly fueling the industry. The adoption of DIY culture and smart home integration solutions is at its peak for renovating houses with environmental awareness,” Opines Sneha Verghese, Senior Consumer Goods and Products Consultant at Future Market Insights (FMI).

Key Takeaways:

The home decor market is registering a CAGR of 6.2% between 2023 to 2033.

The United States is expected to register a maximum CAGR of 26.4% by dominating the global market by 2033.

Japan is anticipated to capture a CAGR of 6.4% in the global market by 2033.

The United Kingdom significantly drives the global market with its vintage home decor, with a CAGR of 2.5%.

With a CAGR of 4.6%, Germany is rapidly advancing the global market.

Home furniture is estimated to lead the global market by 2033 based on product type.

Access the Complete Report Methodology Now! https://www.futuremarketinsights.com/request-report-methodology/rep-gb-4831

Key Players Are Capturing Huge Revenue in the Global Market

Key players are offering affordable home decor solutions as per consumers’ requirements. They are capturing significant revenue through their innovations and product improvements. Key players are adopting various marketing methods to bring new ideas to the table to highlight the market share. These marketing tactics are mergers, acquisitions, collaborations, product launches, and agreements.

These players offer online home decor products, hand-made products, and sustainable products of growing concerns about the environmental crisis. They are targeting genuine consumers to boost sales. Key players are taking relevant feedback from their customers to improve their silly gaps and offer high-quality products to them.

Key Companies in the Home Decor Market:

IKEA

The Home Depot

Williams-Sonoma, Inc.

Wayfair

Ethan Allen

Crate & Barrel

Bed Bath & Beyond

Ashley Furniture Industries

RH (Restoration Hardware)

Herman Miller

Pier 1 Imports

La-Z-Boy

Crate and Barrel

Anthropologie

Houzz

Overstock.com

Tempur Sealy International

Surya

Z Gallerie

Recent Developments in the Home Decor Market

In 2022, Home24 announced its new expansion of its business portfolio in seasonal products and home textiles.

2021 Herman Miller Inc. acquired Knoll Inc. to design advanced home decor.

About the Consumer Product Division at Future Market Insights (FMI)

Future Market Insights (FMI) consumer product team offers comprehensive business intelligence services, with a vast array of reports and data points analyzed across 50+ countries over a decade. The team provides consulting services and end-to-end research, offering expert analysis, actionable insights, and strategic recommendations to clients worldwide. Contact them to explore how they can assist with your unique business intelligence needs.

Unlock Strategic Knowledge: Get Instant Access to Our Detailed Report: https://www.futuremarketinsights.com/checkout/4831

Key Segments in the Home Decor Market

Product Type:

Distribution Channel:

Retail Stores

Direct to Consumer

Manufacturer Stores

E-commerce Stores

Discount stores

Rental Stores

Club Stores

DIY Stores

Application:

Indoor

Outdoor

Other Applications

Region:

North America

Latin America

Europe

Japan

APEJ

MEA

Author

Sneha Varghese (Senior Consultant, Consumer Products & Goods) has 6+ years of experience in the market research and consulting industry. She has worked on 200+ research assignments pertaining to Consumer Retail Goods. Her work is primarily focused on facilitating strategic decisions, planning and managing cross-functional business operations, technology projects, and driving successful implementations. She has helped create insightful, relevant analysis of Food & Beverage market reports and studies that include consumer market, retail, and manufacturer research perspective. She has also been involved in several bulletins in food magazines and journals.

Explore FMI’s Extensive Ongoing Coverage in the Consumer Product Domain

Wall Décor Market Size: The wall décor market is estimated to be valued at US$ 60.15 billion in 2023 and is expected to reach US$ 85 billion by 2033. The adoption of wall décor is likely to advance at a CAGR of 3.5% during the forecast period.

Teen Room Décor Market Share: The global teen room décor market is expected to register a staggering double-digit CAGR of 4% by garnering a market value of US$ 147 Billion.

Aquarium Decor Market Demand: The aquarium decor market is estimated at US$ 2,648.2 million in 2023 and is projected to reach US$ 4,313.6 million by 2033, at a CAGR of 5.0% from 2023 to 2033. The aquarium decor market share in its parent market is 2% to 6%.

Wall Art Market Trends: The global wall art market size is expected to top a valuation of US$ 94.8 billion by 2033. It is set to witness a CAGR of 5.4% in the review period 2023 to 2033.

Wall Covering Products Market Analysis: The wall covering products market is projected to register a CAGR of 4.5% during the forecast period. It is likely to rise up from US$ 31.3 Billion in 2021 to reach a valuation of US$ 50.8 Billion by 2032.

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 5000 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Nandini Singh Sawlani

Future Market Insights Inc. Christiana Corporate, 200 Continental Drive, Suite 401, Newark, Delaware – 19713, USA T: +1-845-579-5705 For Sales Enquiries: [email protected] Website: https://www.futuremarketinsights.com LinkedIn| Twitter| Blogs | YouTube

Michael Hsu, acting director of the Office of the Comptroller of the Currency, said Friday that the forthcoming Community Reinvestment Act final rule to be released Tuesday is designed to increase bank lending and investments in underserved communities.

Bloomberg News

WASHINGTON — Acting Comptroller for the Currency Michael Hsu said Friday that the largest banks will bear the most significant burden of a forthcoming Community Reinvestment Act implementation rule from the Federal Deposit Insurance Corp., Federal Reserve and Comptroller of the Currency designed to expand bank lending and investments to underserved communities.

“It’s a long rule — don’t print it all out at one time, you’re going to run out of ink” Hsu said at the annual conference of the National Bankers Association, which represents minority depository institutions. “But at a high level, there’s got to be more, it has to be better and it’s got to be faster. In very simple terms, that’s it: The amount of CRA investments and lending has to go up.”

Hsu said the long-awaited rule, which the FDIC board and Federal Reserve Board will vote on during an open meeting Tuesday, is designed to be more cognizant of the various challenges facing communities, and by extension permissive of having CRA activities be directed at local communities’ most pressing needs. The rule will also strive to streamline the process of determining whether certain lending activities and investments qualify for CRA credit.

“It has to be better — more targeted,” Hsu said. “Not every locale is equal — one size doesn’t fit all. So it has to be better calibrated to those situations. And it’s got to be faster. We can’t be sitting around and trying to do a lot of different determinations on a bunch of different things. So we try to do that across the board.”

Hsu added that the final rule takes into account the compliance burdens associated with the proposed changes and the limited capacity of smaller banks — including minority depository institutions and community development financial institutions — to meet higher compliance costs.

“We got a lot of comments about this. The biggest burden for the data and changes are really on the largest banks,” Hsu said. “So, for smaller banks we’ve really tailored our expectations. And for MDIs, CDFIs and others, we’ve tried to put the wind at their backs. I can’t go into any details on that, stay tuned, go read it on Tuesday, but we’re very excited for it.”

The Community Reinvestment Act was passed in 1977, and requires banks to extend credit, investments and services to all communities within its service area — not just the most affluent and therefore profitable communities. But the CRA’s definition of service area has traditionally been linked to a bank’s branch network, even as more banking services are performed digitally. Banks and community groups have long agreed that various aspects of the CRA implementation rules are out of date.

Former Comptroller of the Currency Joseph Otting made CRA reform the centerpiece of his tenure during the Trump administration but faced opposition from community advocacy organizations and fellow regulators. The Fed, FDIC and OCC issued a revised CRA implementation rule in May 2022 that initially met with positive feedback from banks and community organizations, though banks have since cooled on the measure.

Speaking separately at the National Bankers Association event Friday, FDIC Chair Martin Gruenberg emphasized that a core aspect of the reform is to decouple CRA activities from communities solely in which banks have physical branches. As outlined in last year’s notice of proposed rulemaking, banks with lending activity above a certain threshold will be required to meet CRA obligations whether they have a physical branch in those communities or not.

“If that lending done in communities where a bank does not have a physical presence is not subject to a CRA evaluation, over time the relevance of CRA to the banking market in the United States — and to ensuring that banks serve all the communities in which they do business — will diminish,” Gruenberg said. “The core thing this rulemaking, as the NPR proposed, will do will be to extend CRA evaluations of banks whether or not [they] have a physical presence in the community.”

The nation’s largest home builder, D.R. Horton, also has its own affiliated mortgage lender known as “DHI Mortgage.”

Recently, new home sales have surged in popularity due to the mortgage rate lock-in effect.

Essentially, existing homeowners aren’t selling their properties because they’ve got ultra-low fixed interest rates on their home loans.

At the same time, mortgage rates have surged higher, resulting in big financing incentives from home builders to move their newly-built home inventory.

Let’s take a hard look at what DHI Mortgage has to offer and whether an in-house lender is the way to go.

DHI Mortgage Fast Facts

Full service mortgage lender offering home purchase loans and refis

Founded in 1997, headquartered in Austin, Texas

Parent company D.R. Horton is the nation’s largest home builder

Publicly traded company (NYSE: DHI)

Also operate DHI Title and D.R. Horton Home Insurance Agency

Aim to be a one-stop shop for newly-built home buyers

Funded roughly $20 billion in home loans during 2022

Most active in the states of Texas, Florida, and California

Licensed to do business in 34 states

DHI Mortgage is a full-service mortgage lender owned by parent company D.R. Horton.

They were founded in 1997 and are headquartered in Austin, Texas.

D.R. Horton is the largest home builder in the United States, slightly bigger than competitor Lennar, which also has a captive mortgage company called Lennar Mortgage.

The home builder got its start back in 1978 when Don R. Horton built his first home in Fort Worth, Texas.

Since then, the company has grown into a near-$35 billion dollar company that is publicly-traded on the New York Stock Exchange (NYSE: DHI).

The company’s shares are owned by legendary investor Warren Buffett, who sees strength in home building given the lack of existing home supply.

Aside from operating their in-house mortgage lender DHI Mortgage, they also run an affiliated title company and insurance agency.

This means home shoppers can use DHI Title for their title insurance needs and D.R. Horton Home Insurance Agency for their homeowners insurance, assuming it’s competitively priced.

The goal is to create a one-stop shopping experience for home buyers and streamline what is often a daunting process.

Last year, they funded about $20 billion in homes, with nearly 30% of overall volume coming their home state of Texas, per HMDA data.

They are also quite active in Florida, California, Arizona, Georgia, Nevada, and The Carolinas.

How to Apply with DHI Mortgage

While you can get pre-qualified for a mortgage online via the DHI Mortgage website, they say to get in touch with your mortgage loan originator to submit a full loan application.

It’s unclear if this means you can still apply electronically after speaking with a loan officer, or if you have to apply in-person.

They do have branch locations and sales offices at their home builder developments, which could facilitate this process.

Unfortunately, their website is a bit limited when it comes to information, so you’ll probably need to speak with a human before proceeding to an application.

Their online system, powered by fintech company Blend, does seem to allow for online refinance applications along with the pre-qualifications.

If you visit their website, it’s also possible to search for a local loan originator by state, branch, or by name.

They say they have digital options for buyers, but don’t make clear what those are. My assumption is they do offer some sort of online loan submission process.

And likely the ability to complete tasks electronically, whether it’s satisfying loan conditions or checking loan status.

However, I would like to see more information in this department.

Loan Programs Offered by DHI Mortgage

Home purchase loans

Refinance loans

Conventional loans including Fannie/Freddie 3% down

FHA loans

VA loans

USDA loans

Fixed-rate and adjustable-rate options

Temporary buydowns

Affordable housing loans

DHI Mortgage offers the most popular loan options out there, whether it’s 3% down conforming loan backed by Fannie Mae or Freddie Mac or an FHA loan.

You can get both a home purchase loan or a mortgage refinance, though I doubt many existing homeowners would use them for a refinance unless mortgage rates were ultra-competitive.

The full menu of government-backed mortgages is offered, including FHA loans, VA loans, and USDA loans.

And both fixed-rate and adjustable-rate options are available, including the 30-year fixed, 15-year fixed, 7/1 ARM, and 5/1 ARM.

They also appear to offer jumbo loans that exceed the conforming loan limit in pricier regions of the country.

However, they don’t appear to offer any second mortgages, such as HELOCs or home equity loans.

But temporary buydowns, such as 2-1 buydown, are offered, as well as other affordable housing loans if buying in specific locations or with low-to-moderate income.

DHI Mortgage Rates

Speaking of mortgage rates, DHI Mortgage doesn’t have a page on their website dedicated to rates or lender fees for that matter.

So you’ll be a little bit in the dark there. Be sure to ask your loan originator what fees they charge, such as loan origination fees, application fees, processing and underwriting, etc.

The good news is I did see special interest rate offers on the D.R. Horton website, which is typical of home builders.

They often offer special incentives to their home buyers who also use their affiliated lender.

In this case, I saw a 5.50% fixed rate FHA loan offer, which was also available on VA and USDA loans.

And a 5.75% fixed rate conventional loan offer that only required a five percent down payment.

So chances are they can offer some pretty competitive rates if you buy a D.R. Horton property and use DHI Mortgage.

DHI Mortgage Home Buyers Club

Those with imperfect credit can take advantage of the “DHI Mortgage Home Buyers Club.”

It pairs in-house credit consultants with prospective home buyers to prepare them for homeownership.

While it doesn’t guarantee loan approval or improved credit scores, they will work with you to boost your overall credit profile.

They’ll also ask you to complete a HUD-approved homebuyer education course while your credit consultant comes up with a credit profile improvement strategy.

This might entail removing inaccurate items on your credit report, paying down high balances, and getting current on any past due accounts.

The goal is to clean up your credit history and improve chances of mortgage approval, and potentially snag a lower mortgage rate depending on credit score improvement.

DHI Mortgage Reviews

As always, I try to track down customer reviews online to see what past customers think of the lender in question.

And they don’t appear to be great, based on what I could find. Their headquarters in Austin has a 2.6/5 rating from about 40 Google reviews.

Over at WalletHub, it’s a similar 2.6/5 rating from just over 30 reviews, with some customers citing poor communication and delays.

You can also find reviews for individual loan officers if you go on Zillow and search by name or location.

DHI Mortgage currently has a ‘B+’ rating with the Better Business Bureau (BBB), which isn’t fantastic and likely due to customer complaints.

They also have a 1.14/5 rating on the BBB website based on customer reviews.

To sum things up, their website could do with improving and their mixed reviews raise some questions about customer service.

On the bright side, they offer a good amount of loan programs and might have financing specials that beat out the competition.

Ultimately, it would probably come down to price if deciding between them and a different lender.

Though I assume most DHI Mortgage customers are also likely D.R. Horton home buyers, so there will likely be a big push to stay in-house.

Just be sure to speak with other mortgage companies, independent mortgage brokers, and so on to weigh your options.

Convenience is great, but not at the price of higher closing costs and/or interest rates. So definitely shop around.

Lastly, note that DHI Mortgage sells most of the loans it originates, meaning it’s likely your loan will be sold and transferred to a new loan servicer shortly after closing.

DHI Mortgage Pros and Cons

The Good

Special financing incentives to D.R. Horton home buyers

Might be a quicker/easier home buying process using affiliated companies

Branch locations allow borrowers to work with in-person if preferred

DHI Mortgage Home Buyers Club helps credit challenged buyers

Free mortgage calculator and homebuyer education resources online

Lots of loan programs to choose from including fixed-rate loans and ARMs

The Perhaps Not

Only licensed in 34 states

No mention of mortgage rates or lender fees online

Clunky website with limited information

Don’t seem to able to apply for a home loan electronically

Do not offer second mortgages or home equity products

Inside: Do you want to know the legit ways on how to make 200 dollars fast? This guide will show you how to start working on fast money ideas. With tips on side hustles, online trading, and more, you’ll be able to build up a healthy bank account in no time.

Do you want to know the different ways to make 200 dollars in your leisure time? I bet you do! We all would like extra money in our pockets.

In an era of digitization, earning an extra $200 in your spare time has become more accessible.

Various online platforms offer numerous possibilities to gain this amount swiftly without any major investments or specialized skills. Utilizing these platforms can not only help you reach your financial goal but also provide you with an enjoyable experience.

Let’s delve into the uncomplicated and quick ways to make 200 dollars fast.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

Best Ways to Make Money 200 Dollars Fast

Discover the best ways to earn 200 dollars quickly by enlisting and acquiring the necessary skills.

You don’t even need to start a business or learn new skills virtually if you need the following legit ways to make $200 fast.

Just to note, you will find many of these ideas to be similar to how to make 300 dollars fast.

1. Sell Things You No Longer Need

Want to declutter and make some quick cash, to the tune of 200 dollars?

Start selling your no-longer-needed items and hit your goal. This method perfectly fits for minimalists looking to clear out space, or parents whose kids frequently outgrow their clothes and toys.

For instance, selling gently used toys or clothes could net you $200 in no time. Who knew making money could be as easy as cleaning up?

Even better turn this into a money-making business by flipping items for a living.

2. Sell gift cards

Struggling to add cash to your wallet? Turn those neglected gift cards lounging in your drawers into quick money.

Convert idle (Gift Cards) money to tangible cash by listing and selling on sites like CardCash at a discounted rate.

Another option is to trade your gift cards (you won’t use them) into something you want (like Apple or Amazon). So, weigh your options wisely.

In fact, you can read my CardCash review on my personal experience trading in gift cards.

3. Take on freelance jobs

Let’s start harnessing our skills and take on freelancing jobs online. Freelancing offers a flexible and income-generating platform, perfect for anyone looking to make a quick buck.

It is an effective income hustle, proven by data-driven facts. Best yet, it’s not exclusive to professionals alone. As a beginner, freelance gigs can offer an excellent starting point.

To get started, build a solid profile on a freelance platform that best suits your skills. Offer your virtual skills by getting jobs done in freelancing and experience good compensation for your comfort zone through this job.

4. Get Paid to Travel by Housesitting

Immerse yourself in a world of four-legged friends, greenery, and cozy, well-furnished homes while your wallet gets a welcomed cash addition.

Housesitting is not just about watching homes; it includes pet sitting and dog walking. All you need to do is join such platforms at no cost, set your rates and hours, and voila, you’re earning money while sleeping.

Essentially make money in your leisure time while enjoying the companionship of adorable pets. Who knew earning extra money could indeed entail wagging tails and furry hugs by signing up with Trusted Housesitters?

5. Rent Out Your Spare Space

Do you have spare space gathering dust? Turn it into a $200 goldmine!

Rent your unused closet, driveway, or extra room and have a quick injection of cash. Websites like Neighbor and VRBO are ideal platforms where you can list and rent out these spaces.

Start by exploring the listings in your area, identify the market range, and list your space accordingly. The extra income is just a few clicks away.

Best suited for property owners with underutilized spaces, this idea can serve as a consistent source of income and isn’t just a one-time fix.

6. Participate in Focus Groups

Get ready to voice your opinion and earn 200 dollars instantly!

Focus groups can be your golden ticket to making a quick $200. From my personal experience, they are organized discussions run by companies eager to pay for consumer insights.

Follow these steps and you could be cashing in:

Start by signing up and participating in a focus group that typically involves finding a suitable event in your area.

Involve yourself with popular websites like Bestmark.

Once you start searching for focus groups, you are likely to be targeted with sponsored ads on Facebook that match up to your opportunities.

By participating in discussions, I have earned a range from $50 to over $200.

7. Babysitting is Great Money

Looking for a quick way to pad your wallet? Babysitting is the golden ticket.

This gig is ideal for teenagers, college students, or anyone with some free evenings or weekends who enjoys hanging out with kids and can tolerate the occasional tantrum.

Start marketing your talent by creating a profile on care portals like Sittercity. Having a certificate in CPR can increase your profile and give assurance to the parent looking for a babysitter.

Remember to start with your personal network. Friends, family, and neighbors are a great way to kickstart your babysitting journey. With a bit of effort, you could be earning in less than 24 hours.

8. Make Videos

Are you passionate about making your own video or editing someone’s video to earn an incredible 200-dollar quickly? Jumpstart your day by hitting each click on your computer and adding sound effects on various kinds of videos on any social media.

You can also monetize your own videos by becoming a YouTube vlogger content creator and signing up for the YouTube Partner Program.

With an incredible shift to a remote life, you can now instantly earn from making your own videos through ad sponsorship, brand affiliation, and paid subscription on any application.

9. Get a Side Hustle

Engage yourself in a side gig, a savvy way to rake in cash promptly. Side hustles harmonize best with go-getters seeking financial flexibility or pursuing dreams outside the 9-to-5 grind.

Kickstart your hustle journey with free webinars or training. These platforms provide insights into key strategies and the nitty-gritty of the field.

Get cracking now to transform your monetizing dreams into reality!

Very popular are these side hustles for men. Or especially these side hustles for college students!

10. Online trading with Stocks and Options

Trading stocks and options emerge as a financial adrenaline rush, providing a swift track to earning money. You can convert spare moments into potential cash gains with just a few clicks.

Expert tips include starting with research, practicing with a simulation trading account, and diversifying your portfolio to mitigate risks.

The journey to online trading success begins with educating yourself. You must participate in a free investing webinar to undergo training to grasp trading basics, understand market trends, and form your strategy.

Check out how I learned to trade stocks and options with this Trade and Travel review.

Trade & Travel

Learn to trade stocks with confidence.

Whether you want to:

Retire in peace without financial anxiety

Pay your bills without taking on a side hustle

Quit your 9-5 and do what you love

Or just make more than your current income….

Making $1,000 every.single.day is NOT a pie-in-the-sky goal.

It’s been done over and over again, and the 30,000 students that Teri has helped to be financially independent and fulfill their financial dreams are my witnesses…

11. Take Up a Part-Time Job

Eager to fill your pockets a bit more, huh? Part-time jobs are your key to fast cash without compromising your ‘me-time’.

A part-time job supplements your primary income, leaving your piggy bank a bit heavier. Where you get to choose the timing that fits around your primary commitments.

Honestly, some of the best part-time jobs are actually low-stress jobs after retirement. You don’t need to wait for extra money. So, go get that financial freedom and earn more than just the minimum.

12. Yard Sale

Hosting a yard sale is a nonchalant trick to amass cash swiftly. It’s your winning lottery ticket staring at you from your cluttered garage floor.

Kick-off by hosting it on Friday or Saturday, when shopping spirits fly high! If your neighborhood or city has a date set for a community garage sale or jackpot, you’ll be swimming in extra traffic.

Don’t hesitate to unleash your inner salesperson, but remember, no rule binds you to wait for an event to rake in cash.

Remember, yard sales are your fast lane to quick money, and with these tips, you’re ready to speed!

13. Make Money with Your Collectibles

Turn your old favorite collection of Pokemon cards or Beanie Babies into a treasure chest waiting to be unlocked.

This money-making method is perfect for those who have carefully amassed certain collectibles over time. Sign up for eBay now and enlist your collectibles, antiques, and merch items to earn from it.

Want to kickstart your financial journey with collectibles? Find the most popular items to flip as well as insights on what to look for.

14. Collect and sell items from the trash

It’s time to transform your everyday trash into a hefty stash of cash! Collecting recyclable trash can be turned into a worthwhile moneymaker.

Start by saving cans, bottles, or scrap metal that you’d usually throw away. Then, locate a local recycling center that’s willing to pay for these items – the prices may surprise you!

This method is great for anyone willing to invest a little time and energy, particularly those who are environmentally conscious and eager to declutter. Perfect job for those who are frugal green.

Think about it, that old toaster might just be your next treasure trove! You may even find some highly valuable items in the trash to flip!

15. Sell Used Clothing

Selling used clothing is a clever and straightforward way to turn spare time into real cash.

Remember, a vibrant description for your clothes will attract buyers, so play up any unique or high-quality aspects of your garments.

Fashion enthusiasts want to earn a quick buck on the side. Begin by taking a charming picture of your clothes and posting it to Facebook Marketplace and ThredUp.

16. Do Social Media Marketing

Welcome to the era of making money by simply being social media savvy. Transform your digital skills into quick cash through Social Media Marketing.

Explore the digital world that awaits with all of the social media platforms. You can create engaging content while responding to the readers.

Take your skills to the next level, consider enriching your knowledge via a free webinar or online training.

This is an easy job that pays more than $25 an hour.

17. Sell Printables on Etsy

Do you love making creative paintings and printable designs? Imagine, your beautifully designed chore chart or a fascinating word puzzle bringing joy to scores of customers.

You can dive into this free training to jumpstart your side hustle. This method is a sure-shot hit for you.

Find out which digital products to sell on Etsy.

18. Invest in Cryptocurrencies

Do you have extra money in savings in your account and don’t know where to invest it?

Since 2008, cryptocurrency has taken the world by storm. Known for its decentralizing nature and secured by cryptography, it’s no regular dough.

Turn the tides in your favor and download an investment app to make your $200 grow faster. Consider taking a free webinar or training for a crash course.

You see, investing in cryptocurrencies is not a heavy-duty task. With the right smarts and patience, you can ride the next crypto wave!

19. Get Paid to Click

Among the numerous ways to earn an extra $200, getting paid to click is a simple and fun method.

Websites provide users with the opportunity to earn money through ‘pay to click’ surveys or rewarding viewers for ad consumption. Additionally, apps such as Survey Junkie and Swagbucks allow you to earn money by taking surveys, participating in focus groups, or simply navigating the web.

Each user generally earns from a few cents to a dollar per click. With patience and consistent effort, you can gradually accumulate your earnings to reach your $200 target.

Here are the top legit survey platforms:

20. Check Out Cashback Apps

Earn a cashback every time you shop at your favorite retail store or online.

Start off by signing up for apps like Dosh, Fetch, Rakuten, and Ibotta which offer bonuses just for signing up.

Lastly, apps like Acorns or CoinOut provide cash back on everyday shopping, even rounding up your purchases to add a bit more to your savings.

21. Do Odd Jobs as a TaskRabbit

Wanna earn cash quickly? Sign up and do freelance labor with TaskRabbit.

This user-friendly job marketplace connects people in need of task assistance with capable individuals willing to complete the tasks for a fee. It offers a diverse array of tasks, from assembling furniture and helping with moves to painting, yard work, and minor home repairs.

Just by performing various tasks, such as events staffing, running errands, or crafting. With the average TaskRabbit making double the minimum wage, this might be the gig for you.

TaskRabbit

Find local jobs that fit your skills and schedule.

With TaskRabbit, you have the freedom and support to be your own boss.

Plus set your own rates!

Get Started

22. Earn Money with Your Knowledge

Using your personal set of skills is a major advantage in freelancing platforms such as Fiverr, Upwork, and Freelancer.com.

Be it graphic design, content creation, SEO mastery, or even web development, you can monetize these proficiencies directly from your home. Data shows a significant growth in the gig economy over the past decade, suggesting a flourishing potential for remote work and online income generation.

Remember, your vast knowledge pool is your strength here. So, focus on what you’re best at, and let the money flow in.

Indeed, by effectively marketing your skills, pulling in a sum over $200 within a few hours is achievable. Remember to value your work appropriately and not devalue your aptitude just to land a job.

23. Tutoring

Online tutoring provides plenty of diverse opportunities in various subjects beyond just English. You can choose to specialize in specific topics and decide to tutor students of different age groups – from young children to college students.

Platforms like VIPKID and Magic Ears allow qualified tutors to offer virtual classes, specifically in the English curriculum for kids aged 4-12 years.

Tutors are usually compensated with payments ranging from $7 – $9 per class or up to $25 or more per hour. Also, you can increase your rate once you gain experience and build a reputation as a tutor. With in-person tutoring, you can expect to earn $20 an hour or more.

24. Petsitting

Looking for a quick way to make $200 fast? If you’re an animal lover, offering pet-sitting services isn’t just enjoyable, but also quite profitable.

Simply sign up with platforms like Rover, you can possibly get paid two days after service completion and you can always set your own rates. Just by walking the dog from house sitting.

Fun fact: Dog sitters often earn up to $50 a day. This is flexible and enjoyable work that could definitely help you reach your $200 target quicker than you’d imagine!

Rover

Get paid to play with pets!

Rover makes it easy and promotes you to the nation’s largest network of pet owners.

Earn money doing something you love.

Become a Sitter

25. Collect Scrap Metals and Junk

One man’s trash is indeed another man’s treasure.

Thinking of ways to earn quick cash? Consider collecting scrap metals and junk. This simple but profitable task can be done by anyone, with no particular set of skills necessary. All you need are keen eyes, a truck, and, admittedly, a little bit of strength to do the following:

Identify Metals: Start by identifying the most valuable metals – brass, copper, and aluminum.

Collect: Gather your metals, either from your home or by browsing local dumps. Remember, one man’s trash can be another man’s treasure.

Sell: Locate a local scrapyard and sell your haul at a fair price.

Keep in mind that patience is key; you might start with just $100 a day, but with experience, this can increase to a lucrative $500 a day!

26. Cash Out Your Coins

Are you sitting on a pile of coins? Maybe it’s time to cash them out. Here’s how:

Gather all your change together. Check under the sofa cushions, in car cup holders, and even in the bottom of your bag.

Take your coins to a coin-counting machine. These can be found at many grocery and department stores as well as your local bank.

Deposit these coins in a savings bank.

Expert Tip: Many banks provide free coin-counting services to their customers. Save on the counting machine charges by using these instead.

27. Run A Dropshipping Business

Dropshipping is a retail fulfillment method where you sell products without ever handling the inventory. This side hustle could potentially make you a quick $200 if executed strategically. Ready to dive in?

To level up, consider enrolling in free webinars on sites like Skillshare or free dropshipping training programs like Oberlo 101. This method is most suitable for those game to learn the ins and outs of online retail business and are ready to deal with customer interactions.

Remember, selling high-demand items will turn a quicker profit!

28. Do Micro Tasks

Looking to make cash fast? Turn your spare time into cash by capitalizing on microtask websites and get paid for completing simple jobs!

This method is particularly effective for those with meticulous attention to detail and those who can afford to spend some time on basic tasks such as data entry, data verification, information sorting, and transcription.

Microtasking might not be a golden goose, but it sure can help you accrue $200 surprisingly fast. The beauty of this hustle is in its simplicity, making easy money with minimal to no investment.

29. Find Sign-Up Bonuses

Did you know that many banks and credit companies offer sign-up bonuses as a strategy for attracting new clients?

For instance, some banking promotions in the United States can offer bonuses of up to $300 in total value when you sign up for a new account or credit card. Also, there are several credit cards that provide bonuses ranging from $500 to $800 or more, simply for registering and spending a defined amount within a specific timeframe.

Some cards, such as Chase Sapphire Preferred, offer lucrative rewards like a $1,000 bonus after a spend of $4,000 in the first 3 months.

It’s definitely rewarding to explore these possibilities to supplement your income, but it’s crucial to maintain a good credit score and commit to paying off your balance monthly to avoid any interest charges.

30. Cash Advances

Cash advances offer a rapid solution, but it’s essential to use them wisely.

Basically, a Cash advance is an advance on your next paycheck, and yes, it’s a viable way to get your hands on some quick cash. Also, some budget apps like Chime offer this service automatically.

Keep in mind, though, it’s an advance and not additional income. So, plan your expenses wisely and make it count!

FAQ

If you’re on a quest to make $200 as fast as possible, we’ve got your back. From selling items you own to completing quick gigs online, there is a plethora of opportunities out there for everyone.

For example, suppose you’re handy at a skill – be it haircuts, car repairs, pet sitting, or painting. You can start by offering your services to people in your neighborhood.

Or, if you’re the digital savvy type, consider selling items you no longer need on online platforms such as Facebook Marketplace or Craigslist. You’d be surprised at how quickly you can make money from items collecting dust in your home.

Ultimately, make sure you choose a fast money-making plan that aligns with your skills, interests, and resources. Go forth and rake in that cash.

If you need to make $200 today, you have a range of options at your disposal.

You can try different online strategies, including participating in online surveys, offering your skills on freelance platforms, or even reselling items online. While many people will sell the idea of a blog to make money, that is not a way to make money today.

Remember, the key is to zone in on tasks that require minimal effort but offer swift returns; these could include grandma sitting, dog walking, or even participating in online offers and promotions.

To kick-start your financial venture, locate valuable items in your home that you no longer need. Your dusty old guitar or that once-loved designer handbag could do the trick. Sell these items on widely used platforms such as Craigslist or Facebook Marketplace for instant cash.

Also, in the digital age, skills are an asset. Offering your skills on platforms like Fiverrcan turn your talents into quick cash. Don’t underestimate the power of quick gigs!

Tapping into the world of free sign-up bonuses can also fill your wallet quickly. Or even participating in a paid focus group!

If you need to make $200 quickly, there are several tried and tested methods. You could start by driving for Uber or Lyft for the evening during a concert.

My preferred method is trading options in the stock market. While this one is a skill, I developed over time. It has proved to be a tried and true method for me to make $200 in a few hours.

Time to Get 200 Dollars Instantly

By reading this article, you have learned and discovered the most effective ways to earn $200 quickly.

In order to have quick success, here are tips to help you out:

Sign up for a complimentary training or webinar that focuses on effective and proven methods of earning money swiftly.

Learning from other’s experiences can certainly save you some trial and error.

Ensure these training modules offer you practical skills and insights rather than just theory. Real-world applications of these strategies are what will help you rake in some quick cash.

Remember, your motivation and dedication are as important as the information and tools you acquire.

If you are looking to make a little bit more, check out how to make 500 dollars fast. Or even how to make 2000 fast!

Know someone else that needs this, too? Then, please share!!

This program can reduce the time needed to save for a down payment and provide another option for those who are otherwise ready to take on a mortgage payment

SEATTLE, Aug. 24, 2023 /PRNewswire/ — Zillow Home Loans announced its 1% Down Payment program to allow eligible home buyers to pay as little as 1% down on their next home purchase. This program is initially being offered on properties located in Arizona, with plans to expand to additional markets. With the 1% Down Payment program, borrowers who qualify can now save just 1% to cover their portion of the down payment and Zillow Home Loans will contribute an additional 2% at closing. The 1% Down Payment program can reduce the time eligible home buyers need to save and open homeownership to those who are otherwise ready to take on a mortgage.

Most markets are in the midst of an affordability crisis, and saving for a down payment remains one of the biggest barriers for many potential home buyers. This is especially true for first-time buyers, who are often paying high rents. Typical asking rent nationwide is $2,062, or 3.6% higher than one year ago and up 31% since the start of the pandemic. (The typical rent in the U.S. in February 2020 was $1,597.) The combination of record-breaking home price appreciation and rising interest rates means a majority of first-time buyers (64%) are putting down less than 20%, and one-quarter of first-time buyers are putting down 5% or less.

Zillow Home Loans’ 1% Down Payment program lowers the down payment barrier and increases access to the housing market for eligible borrowers. An analysis by Zillow Home Loans’ shows that by reducing the down payment burden to 1% of the purchase price, a home buyer looking to purchase a $275,000 home in Phoenix, Arizona, who makes 80% of their area’s median income and saves 5% of their income would need only 11 months to save for the down payment. By comparison, the same buyer who needed to save 3% of the purchase price would require two and half years (31 months) to save that amount.

“For those who can afford higher rent payments but have been held back by the upfront costs associated with homeownership, down payment assistance can help to lower the barrier to entry and make the dream of owning a home a reality,” said Zillow Home Loans’ senior macroeconomist Orphe Divounguy. “The rapid rise in rents and home values means many renters who are already paying high monthly housing costs may not have enough saved up for a large down payment, and these types of programs are welcome innovations in lowering the potential barriers to homeownership for those who qualify.”

Home buyers looking to purchase in the next year should take steps to research and prepare for getting a mortgage as they start on their home-financing journey. Among those steps:

Understand your credit profile: Credit scores are key to getting approved for a mortgage, but for many home buyers, understanding credit is complex.

Improve your credit score: Once buyers familiarize themselves with what’s in their credit report, they can take steps to pay down existing debts, pay bills on time, and review their credit report and dispute possible errors.

Avoid closing accounts: Don’t close an account to remove it from your report. Those accounts aren’t automatically removed and will continue to show up on your report.

Hold off on financing large new purchases: Wait to make purchases that need to be financed, such as a car, until after you close on a home. This type of purchase will impact your debt-to-income ratio, which will negatively affect the amount of home loan you qualify for.

Determine what affordability looks like: Once buyers have a good understanding of their credit report and their credit score is at least 620 (generally the lowest score accepted by mortgage lenders) it’s time to understand how much home they can afford. Use Zillow’s mortgage affordability calculator to customize payment details.

Zillow Home Loans’ 1% Down Payment program is currently available to eligible borrowers in Arizona, with plans to expand. Through the 1% Down Payment program, Zillow Home Loans will pay 2% of the down payment for eligible borrowers. The 2% is paid through closing and not as a payment to the borrower. Interested applicants should call 1-833-372-1449 to speak with a Zillow Home Loans representative to learn more about the program and determine if it’s the right fit for their circumstances.

About Zillow Group Zillow Group, Inc. (NASDAQ: Z and ZG) is reimagining real estate to make it easier to unlock life’s next chapter. As the most visited real estate website in the United States, Zillow® and its affiliates offer customers an on-demand experience for selling, buying, renting, or financing with transparency and ease.

Zillow Group’s affiliates and subsidiaries include Zillow®; Zillow Premier Agent®; Zillow Home Loans™; Trulia®; Out East®; StreetEasy®; HotPads®; and ShowingTime+™, which houses ShowingTime®, Bridge Interactive®, and dotloop®. Zillow Home Loans, LLC is an Equal Housing Lender, NMLS #10287 (www.nmlsconsumeraccess.org).

SOURCE Zillow Home Loans

For further information: Media contact: Jessica Drum, Zillow Home Loans, [email protected]

Famed Cuban-American alto saxophonist, clarinetist, and composer Paquito D’Rivera is looking for a buyer for his longtime home in New Jersey.

Located on the Hudson River waterfront, the majestic North Bergen Colonial he’s been calling home since 2001 is currently on the market for $1.65 million, with Angela Cuciniello of Coldwell Banker Realty in Hoboken holding the listing.

“It is an honor to have been selected by Paquito to represent his amazing home,” said Cuciniello about working with the jazz icon.

Photo credit: Jump Visual courtesy of Coldwell Banker Realty

D’Rivera, celebrated both for his artistry in Latin jazz and his achievements as a classical composer, has 5 Grammy Awards (and 9 Latin Grammys) under his belt, and an impressive total of 16 nominations.

He has also received a Lifetime Achievement Award from Carnegie Hall for his contributions to Latin music, among many other industry accolades that recognized his achievements — which spanned decades and tens of solo albums and collaborations. Paquito D’Rivera was also one of the founding members of the United Nation Orchestra, a 15-piece ensemble organized by Dizzy Gillespie to showcase the fusion of Latin and Caribbean influences with jazz.

At 75, he is still busy composing classical pieces for clarinet and performing, including collaborations with classical cellist Yo-Yo Ma.

The jazz legend bought the New Jersey house back in 2001 for $750,000, and the 4-bedroom home has served as his primary residence ever since. And as it turns out, there aren’t many like it.

“This is a rarity, one of only three Colonials of this size nestled on Boulevard East with sweeping views of the sparkling Manhattan skyline from across the Hudson,” listing agent Angela Cuciniello tells us. “It is rich in history and touched by fame.”

Photo credit: Jump Visual courtesy of Coldwell Banker Realty

Originally built in 2011, the 4-bedroom, 4.5-bathroom brick home has been well maintained and updated throughout the decades, retaining its historic charm.

D’Rivera expanded the house’s original footprint, adding a two-story addition, a supersized chef’s eat-in kitchen, a junior bedroom suite on the second level, and five-zone climate control throughout more than 4,100 square-feet of space.

Photo credit: Jump Visual courtesy of Coldwell Banker Realty

The home’s charming features include a formal entrance foyer, a three-story staircase, large rooms with 10-foot ceilings, detailed moldings, and an abundance of windows, including stained glass.

See also: Tony Soprano’s house is a real-life home in New Jersey — and the pool and driveway look awfully familiar

Highlights of the first floor are a living room with marbled fireplace, a den that opens to a large blue-stone terrace, and a sizeable formal dining room. On the upper two floors are four generously sized bedrooms, three full baths and a Juliette balcony that overlooks picturesque postcard views of the New York City skyline and Hudson River.

The lower level offers a spa, sauna, steam room and a billiards room.

Photo credit: Jump Visual courtesy of Coldwell Banker RealtyPhoto credit: Jump Visual courtesy of Coldwell Banker RealtyPhoto credit: Jump Visual courtesy of Coldwell Banker RealtyPhoto credit: Jump Visual courtesy of Coldwell Banker RealtyPhoto credit: Jump Visual courtesy of Coldwell Banker Realty

Designed to entertain, the home features a heated Gunite swimming pool, while the backyard outdoor space is enclosed by motorized steel gates.

Photo credit: Jump Visual courtesy of Coldwell Banker Realty

The location doesn’t leave much to be desired, as Paquito D’Rivera’s house is just a short stroll away from shopping and dining on the waterfront, and an approximately 20-minute commute to New York City.

Photo credit: Jump Visual courtesy of Coldwell Banker Realty

Featured image credit: Jump Visual courtesy of Coldwell Banker Realty, insert Jacek Proszyk, CC BY-SA 4.0, via Wikimedia Commons

More stories

This Trophy Apartment Was Once Owned by Composer Leonard Bernstein

Stephen Colbert’s house in New Jersey, the former ‘set’ of ‘The Late Show’

‘The Watcher’ house: Facts vs. fiction, the true story of 657 Boulevard in Westfield, NJ

These streets will make you feel brand new. Big lights will inspire you.

The Big Apple is one of the most iconic places on Earth. New York City residents even go as far as to associate the concrete jungle with who they are as a person. With world-class museums, accessible public transportation, delicious restaurants, influential theatres and many famous landmarks, the city is truly a tourist’s paradise.

But while visiting is fun, moving to New York City may feel overwhelming. Between apartment hunting, navigating steep annual rent and the various boroughs of the city, the city feels like no other city.

In this guide, we’ll break down what you need to know before you pack your bags and set off to become a New Yorker.

Moving to New York: the complete Big Apple overview

New York City is the most populous city in the United States. Thinking of the city might conjure up images of the Empire State Building, the Statue of Liberty and the bright lights of Broadway.

However, there’s much more to the city than the tourist hotspots. New York City is divided into five boroughs: Manhattan, Brooklyn, Queens, the Bronx and Staten Island. Each has a distinctive personality, with different cultural influences and attractions.

While each area is different, here are some key figures to give you a glimpse of the city overall.

Population: 8,500,000

Population density (people per square mile): 29,302.6

Median income: $70,663

Average studio rent: $4,264

Average one-bedroom rent: $5,367

Average two-bedroom rent: $7,914

Cost of living index: 100

Popular neighborhoods in New York

Between all five boroughs, New York City has hundreds of neighborhoods to explore. But don’t let this intimidate you. They’re all connected by New York’s world-famous transit system, so you can peruse them at your leisure. Here are a few of our favorite neighborhoods to get you started.

Astoria: Astoria is located in Queens, just across the river from Manhattan’s Upper East Side. This charming neighborhood is made up of low-rise buildings and small businesses, giving it a more suburban feel than you might expect in the big city.

Riverdale: Who said you couldn’t get beautiful green spaces in New York City? Riverdale, located above Manhattan in the Bronx, is known for its natural landscapes. With Van Cortlandt Park, Wave Hill and stunning Hudson River views, this quiet residential neighborhood is ideal for New Yorkers who still want to enjoy the great outdoors.

West Village: The West Village, located in downtown Manhattan, perfectly encapsulates the New York you know from your favorite movies and TV shows. This charming spot is tucked inside the larger Greenwich Village. It features tree-lined streets, historic brownstones and plenty of well-preserved historical landmarks from the neighborhood’s bohemian past.

Upper East Side: The Upper East Side offers excellent residential options and world-famous cultural sites. Located between Central Park and the East River, the neighborhood offers plenty of places to get outside and explore. The Upper East Side is also home to Museum Mile, where more than a dozen art and history museums await.

Williamsburg: Williamsburg is a great example of New York’s diversity. The Brooklyn neighborhood has long been a place where cultures blend, with plenty of eclectic dining, art and entertainment options. It’s also known for its family-friendly atmosphere with parks and tree-lined streets.

The pros of moving to New York

New York, the city that never sleeps, holds a unique place in the hearts of its residents. There’s no place in the world quite like New York City and few cities that even come close to comparable. Here are just a few of the reasons that people love living in this city.

A true cultural melting pot

More languages are spoken in NYC than in any other American metro. With its long, rich immigration history, the city hosts a colorful blend of traditions, cuisines and lifestyles. Especially through the distinct boroughs of New York City, which each have its own unique personality and cultural identity.

From the vibrant energy of Manhattan to the artistic ambiance of Brooklyn, the historical charm of Queens, the green serenity of the Bronx and the island spirit of Staten Island, no matter where you go in New York, you’ll always have the opportunity to learn about a different culture.

No car required

New Yorkers love to complain about their subway system. However, even they secretly know they have it better than most people in the other cities. New York City’s subway serves more than 400 stations, making it a breeze to get where you need to be.

The subway map shows the subway also connects to numerous bus lines, ferry stops and commuter trains, giving riders even more options. From the Upper West Side to Staten Island, the subway is the easiest way to get around your new city.

There’s always something to do

Getting bored in NYC just might be impossible. The city boasts hundreds of restaurants, bars, museums, theaters and places to shop. New York City also has excellent parks, scenic riverfront trails and even beaches. Whether your ideal Saturday is spent at the Metropolitan Museum or taking a subway ride to walk the Brooklyn Bridge, you will never run out of places to explore.

The cons of moving to New York City

Of course, no city is perfect. Here are a few downsides that you should consider before you move to New York.

The high cost of living

New York City is one of the most expensive cities in America. Here, you can expect everything from your monthly rent to your groceries to cost a bit more. Space is also at a premium, so even expensive rentals tend to be smaller than what newcomers might be used to. Even your security deposit will be a tad pricier than you are probably used to.

It’s hard to avoid the crowds

NYC is the most densely populated city in America. As such, it can be hard to avoid the crowds when you’re out and about. Neighborhoods in midtown and downtown Manhattan can get particularly packed, so plan accordingly. Consider neighborhoods like Staten Island and Brooklyn when opting for a less densely populated area in New York, with all the same perks and amenities.

The realities of big-city living

Living in any big city can take some getting used to and New York is no exception. The city can be noisy, dirty and downright overwhelming. If you’re coming from a smaller city or town, New York may feel like a different planet. It’s best to visit the Big Apple during your apartment hunt to really get a feel for the space and pace of the city.

How to get started on your move to New York

New York is a city that’s in constant motion. But for the people who live here, no place feels more like home. If you’re ready to make New York your home, we’re here to guide you every step of the way. Find your perfect New York City apartment here, and get ready for your journey to the city that never sleeps.

Methodology

Rent prices are based on a rolling weighted average from Apartment Guide and Rent.’s multifamily rental property inventory of one-bedroom apartments. Data was pulled in October 2023 and goes back for one year. We use a weighted average formula that more accurately represents price availability for each individual unit type and reduces the influence of seasonality on rent prices in specific markets.

Population and income numbers are from the U.S. Census Bureau. Cost of living data comes from the Council for Community and Economic Research.

The rent information included in this article is used for illustrative purposes only. The data contained herein do not constitute financial advice or a pricing guarantee for any apartment.

Wesley is a Charlotte-based writer with a degree in Mass Communication from the University of South Carolina. Her background includes 6 years in non-profit communication and 4 years in editorial writing. She’s passionate about traveling, volunteering, cooking and drinking her morning iced coffee. When she’s not writing, you can find her relaxing with family or exploring Charlotte with her friends.

From 2022 to 2023, the size of the average personal loan taken out in the previous 12 months by those who got one from a financial institution rose 25%, from $5,046 to $6,299, according to a new NerdWallet survey. The increase was driven by a jump in average loan size among millennials, ages 27-42, (up 78%, from $3,305 to $5,891) and Gen Xers, ages 43-58, (up 45%, from $5,276 to $7,668).

Younger generations were more likely to have borrowed using a personal loan, with millennials topping the list at almost 1 in 2 (48%) taking out a loan in the previous 12 months, followed by Gen Zers, ages 18-26, (39%), Gen Xers (38%) and baby boomers, ages 59-77, (13%).

The 2023 survey, conducted online by The Harris Poll over the period Sept. 7-11, 2023, among over 2,000 U.S. adults ages 18 and older, also found divisions in how generational cohorts view borrowing for nonessentials as well as how they perceive the role of personal loans in their financial plans.

Key takeaways

Many borrowers take out a personal loan just to make ends meet. A third (33%) of recent borrowers (i.e., those who took out a personal loan in the past 12 months) say they took out a loan to cover basic expenses, like food and utilities.

Younger Americans have a more favorable view of “buy now, pay later” (BNPL) loans. More than half of both Gen Zers (56%) and millennials (59%) agree that BNPL loans are, in general, a smart way to make purchases. Agreement drops to 40% of Gen Xers and 24% of boomers.

Americans are divided on borrowing for nonessential purchases. Two-thirds (67%) of Americans say borrowing for nonessentials (things other than food, shelter, etc.) is irresponsible. Revealing an age gap, just 55% of Gen Zers agree, though 74% of boomers do.

Personal loans used for survival — and splurging

Borrowers took out personal loans for a variety of reasons, but covering basic expenses topped the list. Around 1 in 3 Americans (33%) who took a loan out in the last 12 months say they did so in part to cover things like utilities, food and clothing.

Vehicle repairs (27%), home repairs or improvements (25%) and debt consolidation (20%) rounded out the top four reasons for taking out a loan. Debt consolidation was the second most popular option for older cohorts, with Gen Xers (27%) and boomers (21%) both ranking it just behind everyday expenses.

On the other end of the spectrum, younger borrowers were more likely to say they’ve borrowed for nonessential purchases like vacations and items they wanted but couldn’t afford. They are also more likely to borrow to pay for nonmedical emergencies and for purchases related to their work.

Rounding things out, about 1 in 5 borrowers (18%) say they took out their loan to pay for medical costs not covered by their insurance. Around 1 in 6 (16%) took out the loan to pay for health and wellness services (like gym memberships or therapy) and 15% took out the loan to finance the purchase of a vehicle.

Making smart borrowing decisions

Choosing the right way to borrow can make a huge impact on how much you ultimately pay and whether you’re able to keep up with your debt. Companies that offer buy now, pay later for smaller purchases often don’t charge interest, which can help keep payments lower than if using a credit card. Consolidating high-interest credit cards into a lower-rate personal loan can save hundreds of dollars over the life of the loan.

“The key with a debt consolidation loan is to get a lower rate than you’re currently paying,” says NerdWallet personal loans writer Annie Millerbernd. “By doing that, you’re reducing the total interest cost on your debt.”

You can also make sure your budget accounts for repaying any borrowing you’ve already done. That can help you balance your monthly spending and make more informed choices when you’re shopping for those nonessentials.

Americans’ borrowing beliefs vary by age group

We found generational divides to be fairly common in attitudes toward borrowing. Generally, younger generations are more open to the use of loans for nonessential purchases and see loans as an important part of their financial plans.

Asked if they agree with the statement, “Personal loans are an important part of my financial planning,” 45% of Gen Zers and 51% of millennials agree. Around 3 in 10 Gen Xers (29%) and just about 1 in 7 boomers (14%) agree.

There was a similar divide surrounding buy now, pay later loans. Just over half of Gen Zers (56%) and a similar portion (59%) of millennials say BNPL loans are, in general, a smart way to make purchases. Agreement falls to 2 in 5 Gen Xers (40%) and just 24% of boomers.

When we asked Americans how they feel about borrowing for nonessentials, two-thirds (67%) say borrowing for nonessentials is irresponsible. That’s a sentiment most common among boomers, with around three-quarters (74%) agreeing. Boomers were also the least likely (1%) to say they took out a loan to make a purchase they wanted but couldn’t afford (Gen Z, 23%; millennials, 25%; and Gen X, 8%).

That division in attitude was mirrored when we asked specifically about using loans to pay for vacations or health and wellness services. Around 2 in 5 Gen Zers (38%) and millennials (44%) agree that loans are a good way to pay for vacations. A quarter (27%) of Gen Xers felt the same way, along with just 16% of boomers.

Paying for health and wellness services (like gyms and spirituality classes) with a loan seems worth it to around 3 in 5 Gen Zers (60%) and millennials (58%). That falls to around 2 in 5 Gen Xers (38%) and just 29% of boomers.

How to be a responsible borrower

Responsibility and familiarity with financial products can affect what options are the right fit for a borrower. A loan presented to a 24-year-old with a part-time job and little borrowing experience may be a poor fit, but that same offer may be just right for a 22-year-old working full time.

When considering a loan, a good first step is to assess your existing budget and whether there’s room for monthly loan payments. It can also pay to check your credit and do what you can to elevate your score. Borrowers with strong credit receive the lowest rates on personal loans.

Compare multiple options for borrowing, whether it’s a personal loan from an online lender or a shorter-term buy now, pay later loan.

Finally, it’s important to understand how much you’ll ultimately be repaying and over what period that payment will need to be made. By comparing types of loans and their costs, borrowers can be sure they’re selecting the best possible loan for their financial situations.

“Research is your best friend when you’re about to borrow money,” Millerbernd says. “Ask yourself whether you’ll have enough money when the payment comes due to make it on time and whether you can get a more affordable loan elsewhere.”

Loans spur a mix of emotions, from high to low

Borrowing comes with a range of emotions, from the elation of getting a mortgage to buy a first home to the fear of paying off a large hospital bill on credit.

About 2 in 5 borrowers (41%) say they’re planning to repay their loan earlier than they’re required to. Conversely, 14% of borrowers say they’re not sure how they’ll be able to repay their loans. That’s a worry more common with Gen Z borrowers. Close to a quarter (23%) say they’re not sure how they’ll be able to pay back their loan.

Around 1 in 4 borrowers (28%) say taking out their loan was a last resort. That’s a sentiment common across generations (27% of Gen Zers, 26% of millennials and 29% of Gen Xers).

Shame showed up more for younger borrowers. Around 1 in 4 Gen Z borrowers (26%) say they felt ashamed to have to take out their loan, compared to 19% of millennials and 12% of Gen X borrowers.

Younger consumers were also more likely to say they felt their lender charged them a higher interest rate for their loan because they were desperate borrowers. About 1 in 5 Gen Z borrowers (21%) and millennial borrowers (22%) expressed that feeling, while just 1 in 10 Gen X borrowers (9%) say the same thing.

Around 1 in 4 borrowers (23%) say their loan allowed them to buy something that made them happy, which they wouldn’t have been able to purchase without a loan. Younger generations were more likely to agree with that sentiment (Gen Z, 28%; and millennials, 27%).

Where to find help

Financial advisors (55%) topped the list of sources when we asked who Americans would trust to give them advice on personal loans. Friends and family came next (46%), and Gen Z Americans put it at the top of their list with 3 in 5 (60%) saying they trusted those in that group.

About 2 in 5 Americans (39%) say bank representatives were a trustworthy source, though just about a quarter (26%) trusted bank websites and personal finance websites/apps (25%). Business partners (12%), media personalities who hand out financial advice (8%) and coworkers (8%) filled in most of the back half.

The very bottom of the trust barrel belongs to social media influencers (7%), though there’s a generational divide. Gen Zers (17%) and millennials (14%) were more likely than either Gen Xers (3%) or boomers (1%) to trust such influencers.

Finding trusted help

Personal loans are just that — personal. Depending on your comfort with borrowing and the amount you need, there are many different options available to you. Just because you may have taken out your last loan from your primary bank doesn’t mean it’ll be the best spot for your next loan.

Consumers with low credit scores may need to do additional digging to find reputable lending sources and avoid predatory lending that takes advantage of those in tight spots.

“Many lenders let you pre-qualify to check your rate with no hard credit check, which is a huge advantage for borrowers, because if you don’t like one lender’s offer, there are plenty more to try out before you apply,” Millerbernd says.

Methodology

This survey was conducted online within the United States by The Harris Poll on behalf of NerdWallet from Sept. 7-11, 2023, among 2,049 U.S. adults ages 18 and older, among whom 588 have taken out a personal loan in the past 12 months. The sampling precision of Harris online polls is measured using a Bayesian credible interval. For this study, the sample data is accurate to within +/- 2.7 percentage points using a 95% confidence level. For complete survey methodology, including weighting variables and subgroup sample sizes, please contact [email protected].

DUBLIN–(BUSINESS WIRE)–The “United States Home Loan Market Competition Forecast & Opportunities, 2028” report has been added to ResearchAndMarkets.com’s offering.

The United States home loan market is expected to experience significant growth to 2028

The United States home loan market is undergoing a transformation, driven by several key factors that are reshaping the lending landscape. These factors include a growing pool of potential homebuyers, the automation of loan processes, and the pervasive trend of digitalization.

Home loans, typically extended by financial institutions, serve as the financial backbone for individuals aspiring to acquire residential properties. These properties can range from completed, move-in-ready homes to those still in construction phases. Banks and non-banking financial companies (NBFCs) both offer home loans, often determining interest rates based on the borrower’s creditworthiness. These loans commonly come with lengthy repayment periods of up to 30 years, structured through equated monthly installments (EMIs).

In recent years, the demand for mortgages in the United States has experienced a notable upswing, primarily catalyzed by heightened home purchasing activities during the COVID-19 pandemic. Consequently, this surge has generated substantial demand within the purchase market, attracting banks, nonbank lenders, and investors operating in the mortgage sector.