Apache is functioning normally

Mortgage delinquencies kept rising slightly in the fourth quarter of 2023 as Americans continued to indulge in personal spending. But delinquency rates remain well below historic averages, according to new data from the Mortgage Bankers Association (MBA).

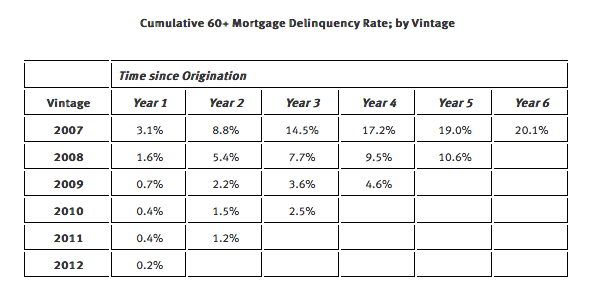

Delinquent home loans on one- to four-unit properties rose to a seasonally adjusted rate of 3.88% of all loans outstanding at the end of Q4 2023, up from 3.62% in the previous quarter but slightly below the rate of 3.96% a year earlier, according to MBA’s National Delinquency Survey.

The historic average for the seasonally adjusted mortgage delinquency rate from 1979 through 2023 is 5.25%.

“Mortgage delinquencies increased across all product types for the second consecutive quarter,” Marina Walsh, MBA’s vice president of industry analysis, said in a statement.

“While the overall delinquency rate is still very low compared to the historical average, the pace of new loans entering delinquency picked up and some loans moved into later stages of delinquency. The resumption of student loan payments, robust personal spending, and rising balances on credit cards and other forms of consumer debt, paired with declining savings rates, are likely behind some borrowers falling behind at the end of 2023.”

Delinquency rates increase across the board

The 30-day delinquency rate increased by 7 basis points (bps) between the third and fourth quarters to 2.10%. The 60-day delinquency rate increased to 0.73%, up from 0.62% in Q3, while the 90-day rate increased to 1.05%, up from 0.98%.

By loan type, the delinquency rate for conventional loans reached 2.61%, up from 2.5% in the previous quarter. The Federal Housing Administration (FHA) delinquency rate recorded a larger jump to 10.81%, up from 9.5%, the highest level since the third quarter of 2021. And the past-due rate for U.S. Department of Veterans Affairs (VA) loans rose to 4.07%, up from 3.76%.

Additionally, the percentage of loans in the foreclosure process decreased to 0.47%, down 2 bps from the prior quarter and down 10 bps year over year. This is the lowest foreclosure inventory rate since the fourth quarter of 2021.

Last Friday, the January jobs report showed that the national economy added 353,000 new jobs, exceeding the monthly average of 255,000 new jobs per month in 2023. But any weakening in employment conditions would likely lead to further increases in mortgage delinquencies in the coming quarters, Walsh added.

Louisiana, West Virginia, Illinois, Texas and New Mexico posted the largest quarterly increases in their overall mortgage delinquency rates.

Related

Source: housingwire.com