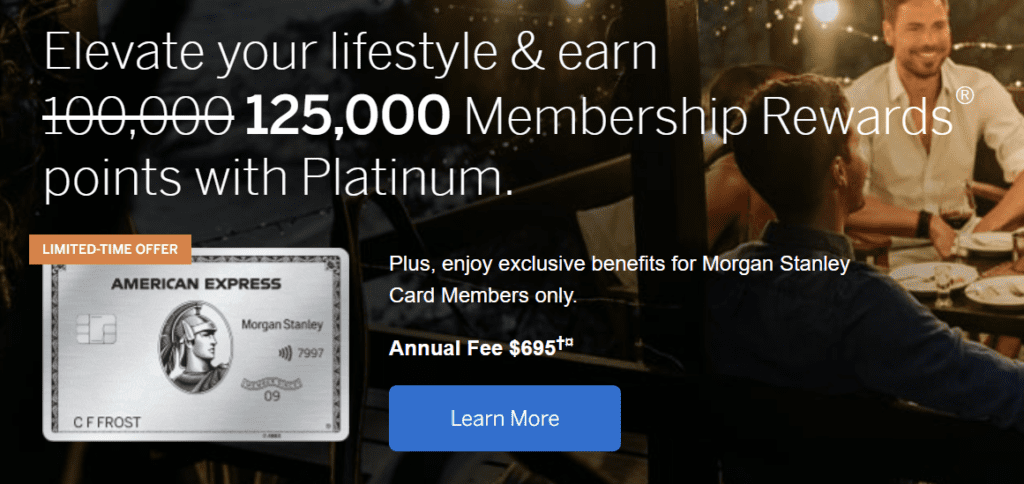

Update 9/28/23: The 125k offer has come back again now after many months of being lower. (ht USCCG)

The Offer

Direct link to offer

American Express is offering 125,000 points after $6,000 in purchases within the first six months of being a cardmember

Card Details

Annual fee of $695 is not waived the first year

Morgan Stanley version of the Platinum card offers one free Platinum authorized user, then $195 for each one thereafter

Authorized Gold cards are free

Full details here

Card earns at the following rates:

5x points per $1 spent on purchases made with airlines or with American Express Travel

5x points per $1 spent on hotel & airline bookings made directly from the American Express travel website

1x points on all other purchases

$200 airline incidental credit per calendar year

$200 Uber credit ($15 per month and additional $20 in December)

Lounge access:

Centurion lounge access

International American Express lounge access

Delta SkyClub lounge access

Priority pass select membership

Airspace lounge access

$240 digital entertainment credit. This is a credit of $20 per month and can be used on Peacock, Audible, SiriusXM and The New York Times.

$200 hotel credit. This can be used on select prepaid bookings (Fine Hotels + Resorts® and The Hotel Collection) when using American Express Travel

$179 Clear credit

$300 Equinox credit. This is a $25 credit each month

Global Dining Access by Resy

The Global Lounge Collection

Our Verdict

You need to be a Morgan Stanley customer to be eligible for this card and you can no longer use the access investing work around unfortunately. It’s rare we see increased offers on these co-branded versions of the Platinum card, so it’s worth signing up if you are eligible and can make use of all the various credits. We will add this to our list of the best credit card bonuses.

Your credit score communicates with lenders your level of credit trustworthiness. As a result, those with higher credit scores qualify for higher credit limits and better interest rates. Your credit score will play a major role if you plan to purchase a house or apply for a loan in the future.

Understanding credit scores and what they mean can improve your financial literacy. We gathered the following credit score statistics to help you get a better sense of where your credit score stands compared to other Americans.

Key findings:

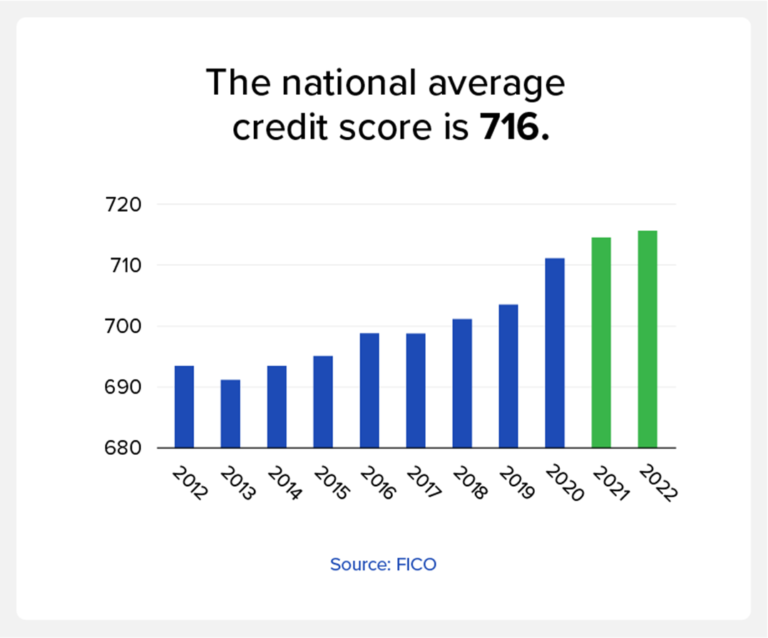

The national average FICO® Score is 716 as of April 2022 (FICO)

About 10% of the U.S. population doesn’t have a credit record and are “credit invisible.” (Consumer Financial Protection Bureau)

Ages 76 and up have the highest average credit score at 760. (American Express)

Women’s and men’s average FICO Scores are virtually the same. (Experian)

Average U.S. credit score

The national average FICO Score is 716 as of April 2022. This is the same as when FICO last reported on it a year ago.

Average credit score by state

While your location doesn’t affect your credit score, some states have a higher average credit score than others as seen in the statistics listed below.

While 31 states (and the District of Columbia) have average FICO scores that are higher than the national average of 716, the upper Midwest and New England continue to have the best average FICO Scores. (FICO)

Minnesota, Vermont, New Hampshire and Wisconsin all have scores that are 23 points higher than the national average, with scores of 742, 739 and 737, respectively. (FICO)

Mississippi, Louisiana, Alabama and Arkansas have the lowest credit scores at 662, 668, 672 and 673, respectively. (WalletHub)

Average credit score by age

Since credit history length is a factor that influences your credit score, it makes sense that the average credit score increases with age as seen below.

Approximately 58% of consumers with the highest credit score are between the ages of 56 and 74. (Money Geek)

The average score for adults aged 18 to 29 increased by 24 points between April 2017 and April 2022; 19 points for those aged 30 to 39; 19 points for those aged 40 to 49; 13 points for individuals in their 50s; and 10 points for those aged 60 and older. (Nerd Wallet)

As of 2021, ages 18-24 have the lowest average credit score at 679. (American Express)

Ages 76 and up have the highest average credit score at 760. (American Express)

Average credit score by race

Average credit scores can differ across demographics like race. However, keep in mind that race doesn’t directly influence your credit score.

Average credit score by gender

Although women couldn’t legally apply for credit until 1974, women’s and men’s average FICO Scores are still very close in range at 705 for men and 704 for women as of 2019, according to Experian.

Average credit score by income

A common credit score myth is that your income contributes to your credit score. Although this is untrue, the statistics below show a correlation between income and credit score.

Approximately 25% of low-income consumers don’t have enough knowledge to raise their credit scores. (Consumer Federation of America)

The median credit score of 658 for lower income individuals suggests that many borrowers are unlikely to have access to affordable credit as those with scores above 720. (Federal Reserve Bank of New York)

Those considered high income have the highest average credit score at 774. (American Express)

Average FICO Score in the U.S.

FICO is an analytics firm that developed the credit scoring models used today. The national average FICO Score is 716 as of April 2022, the same as when FICO last reported on it a year ago. Here are some FICO statistics.

Average FICO Score by generation

The Silent Generation (ages 77 and up) has the highest average credit score at 760. (Experian)

The average credit score of baby boomers (ages 58-76) is 742 in 2022, up two points from 2021. (Experian)

Generation X (ages 42-57) has an average credit score of 706. (Experian)

The average credit score of Millennials (ages 26-41) is 687. (Experian)

Generation Z (ages 18-25) has an average credit score of 679 in 2022, the same as 2021. (Experian)

Generation

Average credit score (2022)

Silent Generation

760

Baby Boomers

742

Generation X

706

Millenials

687

Generation Z

679

Average VantageScore in the U.S.

VantageScore is the second most popular credit scoring model in the U.S. As of September 2022, the average VantageScore was 697.

Credit card utilization statistics

Credit utilization refers to the amount of your available credit you’re currently using. Your credit utilization ratio is calculated by adding up your balances and then dividing by the total of your credit limits. Keeping your credit utilization ratio low can help raise your score.

Individuals with credit scores 800 to 850 have an average credit utilization ratio of 5.7%. (Experian)

Consumers with credit scores considered “very good” (740-799) have an average utilization ratio of 12.4%. (Experian)

Those with credit scores in the “good” range (670-739) have an average credit utilization ratio of 32.6 %. (Experian)

47.6% of the population opened at least one new credit account in the last year. (FICO)

Approximately 26 million U.S. adults, or 10%, don’t have a credit record and are “credit invisible.” (Consumer Financial Protection Bureau)

19 million Americans have a credit history but lack a credit score because their report is insufficient or out of date. (Consumer Financial Protection Bureau)

The 15% growth in credit card balances from 2021 to 2022 is the highest in more than 20 years. (Federal Reserve Bank of New York)

Currently, 83% of American people own at least one credit card. (Zippia)

There are currently 26.5% more credit card holders in 2022 than there were in 2017—just five years ago. (Zippia)

FAQ

Whether you’re new to credit or just need a refresher, we’ve answered some common questions about credit scores below.

What is a good credit score?

According to FICO, a good credit score is 670-739 or above, while a very good credit score is 740-799. A credit score that is 800 or above is considered exceptional.

How to check your credit score

To check your credit score, order a free copy of your credit report from each of the three credit bureaus. You can also check your credit score for free by visiting Credit.com.

What contributes to your credit score?

The factors that contribute to your credit score are payment history, amounts owed, credit history length, credit mix, and new credit.

What is the highest credit score?

The highest credit score is 850 for most FICO and VantageScore models.

How to work on your credit score

You can see from the above credit score statistics that everyone’s credit varies. If you checked your credit score and it’s currently low, we have resources available to help educate you about your credit so that you can qualify for the best rates available.

American Express is discontinuing the upgrade with points program starting December 3, 2023. On statements the following is stated:

Effective December 3, 2023, American Express Card Members with a Membership Rewards account will no longer have access to the Upgrade with Points program and, accordingly, will not have the option to use Membership Rewards points to place an offer on a seat upgrade for any upcoming flights. This will not impact offers placed for a seat upgrade prior to December 3, 2023. All pending offers will still be processed and accepted or declined by the airline. This will not impact any offers that, as of December 3, 2023, have already been accepted or declined by the airline. Upgraded tickets for accepted offers will continue to be valid.

Not a huge loss given how bad value this program was but something to be aware of.

The number on your credit card is more than a passcode to payments when you swipe your card. Many of the digits have a specific meaning. Find out what a credit card number is, what it means, and why it matters.

In This Piece

What Is a Card Number?

A credit card number is a unique number that helps identify your account and card. This number makes it possible for you to pay with the card and for money to be taken out of the right account.

Think about it similarly to your checking account number. Your personal checks are printed with a specific series of numbers. First is the routing number, which indicates which bank the check draws on. Next is the account number, which tells which account the money should come from.

Credit card numbers work the same way. Each part of that long number has a specific function. These are standardized by the International Organization for Standardization (ISO).

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

How to Tell the Credit Card Type by the First Four Digits

The first digit in any credit card number tells you what type of card it is—Visa, Mastercard, Discover, or Amex. Card numbers of each type always start with the same number:

3: American Express or cards under the Amex umbrella

4: Visa

5 or 2: Mastercard

6: Discover

American Express goes even further by starting card numbers with either 34 or 37, depending on the secondary branding on the card.

That first digit plus the next five in the credit card number is called the Issuer Identification Number (IIN) or Bank Identification Number. This identifies the credit card company and its network, similar to the bank routing number on a personal check.

In some cases, the IIN may be eight digits. To allow for more IINs to support growing needs, the ISO is requiring the financial industry to move to eight-digit IINs.

The rest of the digits in your credit card number, with the exception of the final number, are related to your specific account. They aren’t necessarily the same numbers that appear in the account number on your statement. But this string of numbers is tied to your account so that payment processes use the right account when you make a credit or debit card payment.

The last digit of a credit card number is known as the check digit. This number is applied in an unusual formula that helps determine if your credit card number is valid when you enter it. Using this formula, it takes only a fraction of a second for a computer to confirm that a credit card number is valid.

What Do the Last Four Digits on a Credit Card Mean?

The last four digits of your credit card number don’t actually mean much on their own, but there’s a reason you might be asked for them. If you save a credit card in an online account or other database, the information has to be encrypted. Employees of that company can’t just look up accounts and see full credit card information. They’re usually only able to see the last four digits.

You might be asked to confirm those numbers to ensure the right card is being charged. You might also be asked to confirm them when buying something online with a saved card number to ensure you’re really you and not someone who’s hacked into an account.

You can’t tell a credit card number by the last four digits. However, you could find a credit card you’ve saved in an account, such as on Amazon, by the last four numbers. Those are the only digits you’ll be able to see when you look at the saved payment methods in your account.

How Many Numbers Are in a Credit Card?

Typically, credit card numbers are 16 or 15 digits. Only American Express uses the 15-digit format. Around 2020, Visa started issuing some cards with 19-digit card numbers, but these aren’t typically used in the United States.

Finding the Right Credit Card

Before applying for a new credit card, determine what kind of credit card you need. For example, if you want to maximize rewards, you may want a cash-back card with perks that match your budget. If you’re looking to build credit, you may need to apply for a secure credit card that’s easy to get with lackluster credit.

To understand what options might be right for you, check your credit. This helps you know what type of credit card you might be approved for.

Then educate yourself about applying for a credit card online. Review options that seem appropriate for you and pick the best one. You can get started in our credit card marketplace. Gather all the information you need and apply.

You’ve done your research, checked your credit reports to make sure they’re accurate, and you’re ready to get serious about buying a car. You feel more than ready to sign on the dotted line and drive home in your new ride.

It could happen. Or, you could drive home in your old vehicle, kicking yourself for having forgotten one of the documents you need to finalize the purchase. Here’s how to lay the groundwork for getting the deal done on the day you’re ready to buy.

Four Steps to Prepare to Buy a Car

Step 1:

You’ll want to talk to your insurance agent about what it will cost to insure the make and model you are considering buying. You don’t want that figure to be a surprise, and you also want to find out how soon you will need to notify your insurer you have the new vehicle.

Step 2:

Talk to your bank or credit union and get pre-approved for the loan you’ll need—and do this close to your planned purchase date. You may get something resembling a blank check (up to a certain maximum) that must be signed by you and the dealer. By getting pre-approved, you will know the total loan amount and interest rate you qualify for. Even if you plan to finance at the dealer, it can’t hurt to come in with a pre-approval; you are far less likely to agree to a longer term or higher interest rate because you really want to drive that new car home today. It can also help you stay within your budget by serving as a solid reminder of how much you planned to spend and how long you were willing to make payments — before the showroom floor made it so hard to remember.

Get matched with a personal

loan that’s right for you today.

Make sure you have your driver’s license and proof of auto insurance with you. You shouldn’t be driving without these documents anyway.

Step 4:

Obvious as this seems, be sure you have a way of funding your down payment. If it’s not cash, make sure the dealer accepts the form of payment you’re planning to use. (If you forget to do this, you would not be the first, but that would be little consolation.)

Expert Tip: Be cautious about having your credit pulled unnecessarily. Each inquiry made for the purpose of extending credit can cause a small, temporary decrease in your credit score. And while inquiries for the purpose of getting a car loan made in a two-week period should count as only one entry, we’ve heard from consumers who have told us their credit scores dropped as the result of multiple auto loan inquiries. Some dealerships now ask customers to fill out a credit application even before a test drive, and there are reports that some have checked credit without customer consent. It can help to keep an eye on your credit through this process for this reason. Hard inquiries into your credit require permission, and it can be illegal for your credit to be pulled without your approval in this manner. You can get a credit report summary and two credit scores, updated monthly for free on Credit.com, to track your standing.

Can You Purchase a Car with a Credit Card?

Speaking of your down payment, you may have wondered if this can be charged to a credit card — or if the entire car can be paid that way. The answer is yes and no. It is possible that the dealership will not accept a credit card payment for the car, as this can come with large merchant fees that lower their profits. However, if your credit is in good standing, then it is still possible.

A better option would be to use your credit card for just the down payment. Not only is this better for your credit, since using all of your available $10,000–$15,000 credit limit can damage your credit score, but it’s more likely to be accepted by the dealer.

Finally, you’ll want to use a credit card that has excellent benefits. An appropriate credit card can earn you big rewards on your car purchase or other auto-related purchases. We have given you a couple examples of worthy rewards cards below.

Planning to Trade In Your Car? Don’t Forget These Items for the Dealership

If you plan to trade in a car, you have a bit more to do.

You will need to bring the following items to the dealership:

Your car’s certificate of title (If it has gone missing, your state department of motor vehicles can tell you how to get it replaced.)

The car’s current registration

Your car keys and the owner’s manual

Your account number or a payment stub if you still have a car loan (We’re going to hope that if this is the case, your car is worth more than you owe.)

A clean car, paying special attention to areas out of sight but convenient for stashing things: under seats, over the visors, in the glovebox and in every corner of the trunk

Besides a new car, expect to come home with a good bit of paperwork. Pay special attention to the purchase and sale agreement. You will need the information there to get or update your insurance — and you might even need it at tax time next year if you bought a car that qualifies for a tax credit.

What Do I Need to Apply for an Auto Loan?

While you won’t need to drive all the way to a dealership to get an auto loan (you can simply apply online), you will still need some important documents in front of you to easily fill out the application.

What do you need?

Proof of identity through an ID or passport

Your credit report, which the lender can pull using your name, address, date of birth and social security number

A valid state-issued driver’s license

Proof of monthly income through pay stubs or social security income receipts

Proof of residence through mortgage statements or utility bills

Contact information for personal references (note: this may not be required)

Vehicle make and model

Proof of car insurance

Payment type (cash, credit, debit, etc.)

Your car’s registration if you are trading in the vehicle

The list is rather long, but having each document will speed up the process and prevent you from going back and forth between your files.

Get Your Auto Loan and Car with the Help of Credit.com

Make sure that you can qualify for an auto loan by checking your free credit score, provided through Experian. From there, you can apply for your auto loan with confidence and compare credit cards that can help you finance your new car.

Frequently Asked Questions

Will my credit rating affect my auto insurance rates?

You should choose auto insurance coverage based on your credit rating and overall coverage needs. Check out Credit.com for car insurance quotes and to compare rates.

How can I find a credit card with a low interest rate to charge my car purchase?

We don’t recommend that you put your entire purchase onto your credit card, but there are cards with low APR or no APR for up to 15 months available to compare. If you can pay off the remaining balance during this period, then these credit cards may be for you.

How good should my credit be to get a credit card that is appropriate for a car purchase?

You mentioned that hard inquiries can affect my credit score. What is a hard inquiry?

A hard inquiry is a credit check that indicates you have applied for credit, usually through a loan. Each time a hard inquiry is pulled from a different lender, your credit score can drop by up to 10 points, because it indicates that a lender has reviewed your credit and that you are trying to open up a new line of credit.

Note: At publishing time, the Chase Sapphire Preferred® Card and American Express Green card are offered through Credit.com product pages, and Credit.com is compensated if our users apply and ultimately sign up for this card. This content is not provided by the card issuer(s). Any opinions expressed are those of Credit.com alone, and have not been reviewed, approved or otherwise endorsed by the issuer(s).

Note: It’s important to remember that interest rates, fees and terms for credit cards, loans and other financial products frequently change. As a result, rates, fees and terms for credit cards, loans and other products cited in these articles may have changed since the date of publication. Please be sure to verify current rates, fees and terms with credit card issuers, banks or other financial institutions directly.

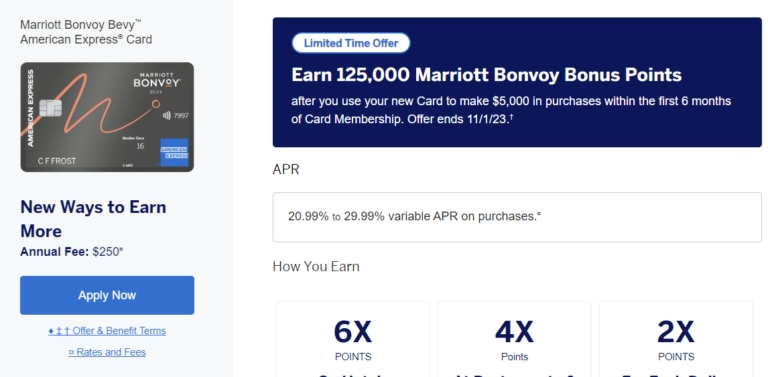

Updates to the Marriott Bonvoy Bevy™ American Express® Card welcome offer

The $250-annual-fee Marriott Bonvoy Bevy™ American Express® Card’s latest welcome offer is sure to excite Bonvoy enthusiasts with a big jump in value for the same spending requirement.

Here’s how the two offers compare:

New offer: Earn 125,000 Marriott Bonvoy bonus points after you use your new Card to make $5,000 in purchases within the first 6 months of Card Membership. Terms Apply.

Previous offer: Earn 85,000 Marriott Bonvoy bonus points after you use your new Card to make $5,000 in purchases within the first 6 months of Card Membership. Terms Apply.

Ongoing rewards: The Marriott Bonvoy Bevy™ American Express® Card will continue to offer its ongoing rewards rate of 6 points per dollar spent on participating Marriott Bonvoy hotels; 4 points per dollar spent at restaurants worldwide and at U.S. supermarkets (up to $15,000 in combined purchases per year); and 2 points per dollar spent on all other eligible purchases. Terms apply.

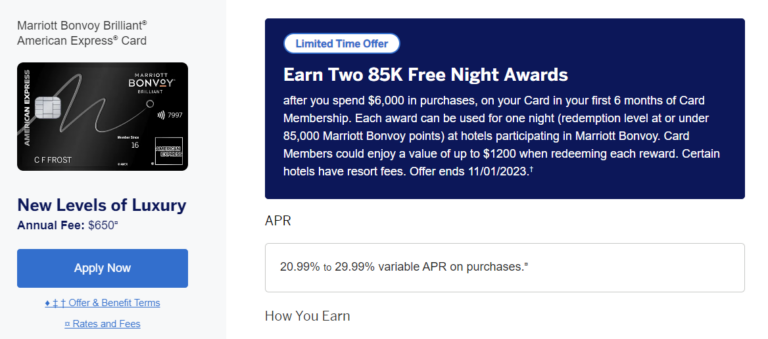

Updates to the Marriott Bonvoy Brilliant® American Express® Card welcome offer

The latest offer on the $650-annual-fee Marriott Bonvoy Brilliant® American Express® Card offers the potential for significantly more value with the same spending requirement. But since the offer comes in the form of free night certificates rather than points, you’ll sacrifice flexibility when you redeem.

Here’s what’s changing and what’s staying the same:

New offer: Earn two 85K Free Night Awards after you spend $6,000 in purchases on the Card in your first 6 months. Each award can be used for one night (redemption level at or under 85,000 Marriott Bonvoy points) at hotels participating in Marriott Bonvoy. Card Members could enjoy a value of up to $1,200 when redeeming each reward. Certain hotels have resort fees. Offer ends 11/1/2023. Terms Apply.

Previous offer: Earn 95,000 Marriott Bonvoy bonus points after you use your new Card to make $6,000 in purchases within the first 6 months of Card Membership. Terms Apply.

Ongoing rewards: The Marriott Bonvoy Brilliant® American Express® Cardwill continue to offer its ongoing rewards rate of 6 points per dollar spent at participating Marriott Bonvoy hotels; 3 points per dollar spent at U.S. restaurants; 3 points per dollar spent on flights booked directly with airlines; and 2 points per dollar spent on all other eligible purchases. Terms apply.

Are the new offers better?

Although they’re not the best offerings, the latest welcome offers on AmEx’s Marriott Bonvoy cards are quite a boost in value. For the Bevy card, you’ll earn nearly 50% more points than the previous offer. And if you’re able to use the free night certificates for full value for the Brilliant card, the new offer represents a 78% boost.

But while the latest Marriott Bonvoy Brilliant® American Express® Card offer carries significantly higher value, it comes with far less flexibility. The two Free Night Awards are worth up to 85,000 points per night, but they expire one year from when they’re issued.

Plus, it may be difficult to redeem them for full value. If you redeem the 85,000-point certificate at a hotel that’s charging 60,000 points for the night you want to stay, you won’t get the difference back in points. On the other hand, an 85,000-point certificate may not cover a luxury St. Regis or Ritz Carlton hotel stay, which could cost 100,00 points or more per night. (Marriott does allow you to apply certificates toward a higher-priced room and cover the difference with up to 15,000 points.)

Marriott Bonvoy points can be redeemed at more than 8,600 hotels worldwide. Bonvoy points can also be transferred to certain airline partners, or redeemed for car rentals, gift cards, and other options. The value of points may vary depending on how you redeem them.

How the cards compare

When comparing these new welcome offers, there are a few more factors about the two cards worth keeping in mind, most notably the difference in annual fees. The Marriott Bonvoy Bevy™ American Express® Card, which comes with complimentary Gold status, carries an annual fee of $250. Notably, it does not come with an automatic free annual stay. The Marriott Bonvoy Brilliant® American Express® Card comes with automatic Platinum status and a higher (though less flexible) welcome offer. But with an annual fee of $650, those extra perks come at a steep cost.

Here’s a breakdown of how the two cards compare:

At a glance

Marriott Bonvoy Bevy™ American Express® Card

Marriott Bonvoy Brilliant® American Express® Card

Annual fee

Welcome offer

Earn 125,000 Marriott Bonvoy bonus points after you use your new Card to make $5,000 in purchases within the first 6 months of Card Membership. Terms Apply.

Earn two 85K Free Night Awards after you spend $6,000 in purchases on the Card in your first 6 months. Each award can be used for one night (redemption level at or under 85,000 Marriott Bonvoy points) at hotels participating in Marriott Bonvoy. Card Members could enjoy a value of up to $1,200 when redeeming each reward. Certain hotels have resort fees. Offer ends 11/1/2023. Terms Apply.

Ongoing rewards

6 points per $1 spent on participating Marriott Bonvoy hotels.

4 points per $1 spent on up to $15,000 in combined purchases per year at restaurants worldwide and at U.S. supermarkets.

2 points per $1 spent on all other eligible purchases.

Terms apply.

6 points per $1 spent at participating Marriott Bonvoy hotels.

3 points per $1 spent at U.S. restaurants and on flights booked directly with airlines.

2 points per $1 spent on all other eligible purchases.

Terms apply.

Other benefits

1,000 Marriott Bonvoy bonus points with each qualifying stay.

Complimentary Gold Elite status.

A Free Night Award after making $15,000 in purchases per year for any hotel worth 50,000 points or less.

15 Elite Night Credits each calendar year.

Terms apply.

One Free Night Award each year after card renewal for any stay at a redemption level of 85,000 points or less.

Automatic Platinum Elite status.

$300 statement credit for restaurant purchases (up to $25 per month).

American Express is offering a bonus of 125,000 points after $5,000 in spend on the first 6 months on the Marriott Bonvoy Bevy.

Card Details

$250 annual fee

Card earns at the following rates:

Earn 6X points for every $1 spent at Marriott properties

Earn 4X points for every $1 spent on the first $15,000 in combined purchases each year on grocery stores and dining

Earn 2X points for every $1 spent on all other purchases

Free Night Award every calendar year, after $15,000 in spend within that calendar year (good for up to 50,000 points)

Complimentary Gold Elite status

15 elite night credits toward elite status

Welcome offer not available to applicants who (i) have or have had The Ritz-Carlton® Credit Card from JPMorgan, the J.P. Morgan Ritz-Carlton Rewards® Credit Card, the Marriott Bonvoy Bountiful™ Credit Card from Chase, the Marriott Bonvoy Boundless® Credit Card from Chase, the Marriott Rewards® Premier Plus Credit Card from Chase, the Marriott Bonvoy® Premier Credit Card from Chase, the Marriott Bonvoy Bold® Credit Card from Chase, or the Marriott Bonvoy® Premier Plus Business Credit Card from Chase or the Marriott Rewards® Premier Plus Business Credit Card from Chase in the last 30 days, (ii) have acquired the Marriott Bonvoy Bountiful™ Credit Card from Chase the Marriott Bonvoy Boundless® Credit Card from Chase, the Marriott Bonvoy Bold® Credit Card from Chase in the last 90 days, or (iii) received a new Card Member bonus or upgrade offer for the Marriott Bonvoy Bountiful™ Credit Card from Chase, the Marriott Bonvoy Boundless® Credit Card from Chase, or the Marriott Bonvoy Bold® Credit Card from Chase in the last 24 months.

Our Verdict

This is the standard increased bonus on this card. Overall not a good bonus, especially with the high annual fee. We won’t be adding this to our best credit card bonuses.

Sign up for the Marriott Bonvoy Brilliant card and earn two free night certificates good on a property up to 85,000 points when you spend $6,000 within the first six months

Card Details

$650 annual fee

$300 dining statement credit

Card earns at the following rates:

6x points per $1 spent at participating SPG & Marriott Rewards hotels

3x points per $1 spent at U.S. restaurants and on flights booked directly with airlines

2x points per $1 spent on all other purchases

Free night award every year after your card account anniversary (can be used at any property that costs under 50,000 points per night)

Complimentary gold elite status

Platinum elite status after you spend $75,000 or more on the card in a calendar year

15 nights towards elite status (you’re restricted to getting this benefit once per Marriott Loyalty program number)

Unlimited complimentary priority pass lounge access for you and up to two accompanying guests

Statement credit for Global Entry ($100) or TSA PreCheck ($85) every four years

No foreign transaction fees

Free in-room premium internet access at SPG & Marriott participating hotels

Welcome offer not available to applicants who (i) have or have had The Ritz-Carlton™ Credit Card from JPMorgan or the J.P. Morgan Ritz-Carlton Rewards® Credit Card in the last 30 days, (ii) have acquired the Marriott Bonvoy Boundless™ Credit Card from Chase, the Marriott Rewards® Premier Plus Credit Card from Chase, the Marriott Bonvoy™ Premier Credit Card from Chase, the Marriott Rewards® Premier Credit Card from Chase, the Marriott Bonvoy Bold™ Credit Card from Chase, the Marriott Bonvoy™ Premier Plus Business Credit Card from Chase or the Marriott Rewards® Premier Plus Business Credit Card from Chase in the last 90 days, or (iii) received a new Card Member bonus or upgrade offer for the Marriott Bonvoy Boundless™ Credit Card from Chase, Marriott Rewards® Premier Plus Credit Card from Chase, the Marriott Bonvoy™ Premier Credit Card from Chase, the Marriott Rewards® Premier Credit Card from Chase, the Marriott Bonvoy Bold™ Credit Card from Chase, the Marriott Bonvoy™ Premier Plus Business Credit Card from Chase or the Marriott Rewards® Premier Plus Business Credit Card from Chase in the last 24 months.

Our Verdict

Bonus was 100k + free night certificate recently, that was a much better deal with more flexibility. Annual fee has also increased by $200 since then as well. We won’t be adding this to our list of the best credit card bonuses.

For most people, the Chase Sapphire Preferred® Card is a better starting point in the travel rewards market. (There’s a reason NerdWallet describes it as “nearly a must-have for travelers.”) It offers higher rewards earnings on everyday purchases, and those rewards carry a 25% higher redemption value when used to book travel through the Chase travel portal. That’s a lot of value for a modest annual fee of $95.

The Platinum Card® from American Express is marketed as a premium travel card. Its rewards earning rates focus on select travel spending, and it carries more luxury benefits, including lounge access, high-end fitness, shopping and hotel credits. However, those premium benefits come with a premium annual fee of $695 — a hard cost to justify for many people.

Here’s a side-by-side comparison so you can decide which card is right for you.

How the cards compare

Chase Sapphire Preferred® Card

on Chase’s website

The Platinum Card® from American Express

Annual Fee

Welcome offer

Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That’s $750 toward travel when you redeem through Chase Ultimate Rewards®.

Earn 80,000 Membership Rewards® Points after you spend $8,000 on purchases on your new Card in your first 6 months of Card Membership.

Terms apply.

Rewards

5 points per $1 spent on all travel purchased through Chase Ultimate Rewards®.

3 points per $1 spent on dining (including eligible delivery services and takeout).

3 points per $1 spent on select streaming services.

3 points per $1 spent on online grocery purchases (not including Target, Walmart and wholesale clubs).

2 points per $1 spent on travel not purchased through Chase Ultimate Rewards®.

1 point per $1 spent on other purchases.

Through March 2025: 5 points per $1 spent on Lyft.

Points are worth 1.25 cents apiece when redeemed for travel through Chase Ultimate Rewards®.

5 Membership Rewards points per $1 spent on flights booked directly with airlines or with American Express Travel.

5 points per $1 spent on prepaid hotels booked through American Express Travel.

2 points per $1 spent on other eligible travel booked through AmEx.

1 point per $1 spent on all other purchases.

Other benefits

A $50 annual credit on hotel stays purchased through Ultimate Rewards®.

Each account anniversary, cardmembers will earn bonus points equal to 10% of total purchases made the previous year.

1:1 transfer partners, including United, Southwest, JetBlue, Marriott and Hyatt.

$200 annually for airline incidentals, like bag fees, on one designated airline when you enroll.

$200 annually for prepaid hotel bookings through American Express Travel at more than 2,000 hotels. (Fine Hotels and Resorts or The Hotel Collection properties.)

$189 annually for Clear membership.

$100 statement credit every 4 years for a Global Entry application fee or a statement credit up to $85 every 4.5 years for a TSA PreCheck when charged to your card.

1:1 transfer partners, including Air Canada, Air France, British Airways, Delta and Virgin Atlantic.

Terms apply.

Lounge access

Access for you and 2 guests to over 1,400 lounges worldwide from partners including Priority Pass and Plaza Premium Group. Terms apply.

Access to over 40 American Express Centurion and Escape lounges. Terms apply. Fees may apply for guest access.

Foreign transaction fee

Still not sure?

Why the Chase Sapphire Preferred® Card is better for most people

Lower annual fee

The Chase Sapphire Preferred® Card packs a lot of punch in terms of travel rewards value, all with a manageable $95 annual fee. Compare that with The Platinum Card® from American Express’s eye-popping $695 annual fee — an intimidating figure for many travelers. While the Amex Platinum does advertise a wide range of travel and shopping credits to offset that fee, taking full advantage of those benefits can be burdensome.

More value, more dometic transfer partners

When using your points to book travel through the issuer’s portal, Chase Ultimate Rewards® are more valuable. Points earned from the Chase Sapphire Preferred® Card are worth an impressive 1.25 cents per point. That’s an outsized value compared with the American Express travel portal, where Membership Rewards points are redeemed at one cent per point on flights and certain hotel bookings. Other hotel bookings made through AmEx carry a value of 0.7 cent per point.

Plus, Chase’s transfer partners include several well-known domestic airlines and hotel brands, offering easy accessibility for points redemption. American Express offers more transfer options than Chase, and savvy travelers can find outsized value for their points. But AmEx’s transfer partners are primarily foreign airlines, making Membership Rewards points more challenging to transfer for U.S.-based domestic travelers.

Full list of Chase transfer partners

Aer Lingus (1:1 ratio).

Air Canada (1:1 ratio).

Air France-KLM (1:1 ratio).

British Airways (1:1 ratio).

Emirates (1:1 ratio).

Iberia (1:1 ratio).

JetBlue (1:1 ratio).

Singapore (1:1 ratio).

Southwest (1:1 ratio).

United (1:1 ratio).

Virgin Atlantic (1:1 ratio).

Hyatt (1:1 ratio).

InterContinental Hotels Group (1:1 ratio).

Marriott (1:1 ratio).

Full list of AmEx transfer partners

Aer Lingus (1:1 ratio).

AeroMexico (1:1.6 ratio).

Air Canada. (1:1 ratio).

Air France/KLM (1:1 ratio).

ANA (1:1 ratio).

Avianca (1:1 ratio).

British Airways (1:1 ratio).

Cathay Pacific (1:1 ratio)

Delta Air Lines (1:1 ratio).

Emirates (1:1 ratio).

Etihad Airways (1:1 ratio).

Hawaiian Airlines (1:1 ratio).

Iberia Plus (1:1 ratio).

JetBlue Airways (2.5:2 ratio).

Qantas (1:1 ratio).

Qatar Airways (1:1 ratio).

Singapore Airlines (1:1 ratio).

Virgin Atlantic Airways (1:1 ratio).

Choice Hotels (1:1 ratio).

Hilton Hotels & Resorts (1:2 ratio).

Marriott Hotels & Resorts (1:1 ratio).

Better earnings rates on everyday spending

Both cards earn 5x per $1 spent on travel booked through their travel portals, but the Chase Sapphire Preferred® Card is the clear winner for everyday spending. It earns 3x on dining, streaming services, and online grocery purchases (excluding Walmart, Target and wholesale clubs), while the Amex Platinum earns 1x in each of those categories. Terms apply.

Get a card that takes you farther

Sign up with NerdWallet to get a full picture of your spending and personalized recommendations for cards that will help you see the world.

Why you might want The Platinum Card® from American Express

Lounge access

In this category, there’s no competition. If airport lounge access is a high priority, you’ll be best served by The Platinum Card® from American Express.

Where the Chase Sapphire Preferred® Card offers no lounge access, the AmEx Platinum is known for its top-notch airport lounge benefits, including access to over 1,400 lounges in more than 500 airports worldwide. Those include more than 40 American Express Centurion and Escape lounges, and additional access through partners like Priority Pass and Plaza Premium Group. Terms apply.

Booking with the airline

When it comes to booking flights, experienced travelers know that the way you book can make a big difference in the ease of changing or canceling your plans. So while both the Chase Sapphire Preferred® Card and Amex Platinum offer 5 points per dollar spent on flights booked through their respective travel portals, The Platinum Card® from American Express has a leg up in offering that same earnings rate for flights booked directly through the airline. Terms apply.

The Sapphire Preferred, on the other hand, offers the 5x points rate only if you book your flights through the Chase travel portal. That can pose a problem in the event of a weather delay, cancellation, or any other trip interruption.

The prestige factor

Both cards are metal, but The Platinum Card® from American Express carries a certain luxury gravitas that the Chase Sapphire Preferred® Card can’t compete with — and doesn’t try. That prestige has some cash value, too. When used correctly, the card’s luxury perks add up quickly to help offset its eye-popping annual fee. When you enroll, those include statement credits of up to $300 per year toward an Equinox gym membership, $50 twice per year at Saks Fifth Avenue, $200 per year in Uber cash ($15 per month plus an extra $20 in December), and $200 a year for prepaid hotel bookings through The Hotel Collection or Fine Hotels + Resorts properties, just to name a few. Terms apply.

However, if these benefits don’t match your lifestyle, you’ll be paying mostly for the cachet of pulling the famous platinum card out of your wallet. Only you can decide how much that prestige is worth.

Which card should you get?

The Chase Sapphire Preferred® Card and The Platinum Card® from American Express are two of the best travel rewards cards on the market, but they have different strengths and weaknesses. Chase Sapphire Preferred® Card is a great choice for travelers who want a card with a low annual fee and great rewards for everyday spending. The Amex Platinum may be the better choice for frequent travelers who value lounge access and luxury benefits — but given the card’s steep $695 annual fee, it’s important to make sure you can take full advantage of all those benefits before you sign up.

To view rates and fees of The Platinum Card® from American Express, see this page.

Visa and Mastercard are both card networks. Both organizations manage the payment networks through which their cards work. Visa and Mastercard are different companies, but they operate in a very similar way.

Four credit card networks tend to compete for space in consumer wallets. They are Mastercard, Visa, Discover and American Express.

According to Statista, Mastercard and Visa have had the largest market share for a while. As of 2021, they accounted for more than 87% of the market. Compare that to Amex’s 10.5% and Discover’s 2.2% and you can see that most credit cards are Mastercard or Visa.

But is one better than the other? Are there really any differences between these two major credit card networks? Find out in our guide to the difference between Mastercard and Visa below.

In This Piece

What’s the Difference Between Mastercard and Visa?

While they’re both credit card processing networks, these are unique and separate companies. They were founded at different times.

Originally known as the BankAmericard credit card program, Visa launched in 1958. Mastercard began as Master Charge: The Interbank Card when it emerged as a BankAmericard competitor in 1966.

Visa cards don’t work on the Mastercard network, and vice versa. You can’t, for example, use a Visa to pay for something in a store that only accepts Mastercard.

How Are Visa and Mastercard Similar?

There are more similarities between Visa and Mastercard than differences. As mentioned earlier, these are both card networks. They both play the middleman between payment processors and issuing banks.

Both companies operate globally, so if you alert your issuer in advance, you should be able to use your Visa or Mastercard in another country when you go on vacation. Whether you pay fees for this service depends on your card issuer and account details—not on Visa or Mastercard.

Both Visa and Mastercard have tens of millions of merchants in their networks, and both companies’ merchant fees are comparable. Both organizations are publicly traded.

What’s the Difference Between a Network and an Issuer?

The credit card network is the middleman between the payment processor and the issuer of the card. When you pay with a credit card, the information is processed through the network to the bank that issued your credit card. On the other side of the transaction, the data that supports the funds transaction is also processed through the network.

Visa and Mastercard are credit card networks. They’re responsible for the infrastructure for these transactions and for protecting the information as it passes between the payment processor and the issuer. For this service, the credit card networks charge a fee—usually paid in part via a small percentage of every transaction.

An issuer is the bank that issues the card. Examples include Chase, Citibank and Capital One. The issuer is the entity that decides whether you’re approved for a credit card and sets interest rates and fees. It’s also the lender that pays for the goods you purchase with your credit card and the entity you pay back with your payments.

How Does Payment Processing Work?

Visa and Mastercard credit card and debit card payments all go through the same payment process—albeit on different networks. The process looks like this:

Consumers swipe cards—or tap contactless cards—in physical stores or enter card details online.

Merchants send payment authorization requests to their payment processors.

Payment processors send payment requests to the appropriate card network.

Card networks “ask” issuing banks for payment authorization.

Issuing banks approve or deny the transaction.

At this point, transactions are—hopefully—authorized, but they’re not settled yet. The process must continue:

Merchants send approved payment requests to payment processors in batches.

Once again, payment processors send transaction details to Visa, Mastercard or other applicable card networks.

Card networks “ask” issuing banks for previously authorized funds.

Issuing banks release the funds, which travel to merchant banks.

Credit card processing network fees get taken out along the way.

Merchant banks transfer funds into individual merchant accounts.

At this point, the store or other merchant has been paid for the goods or services you bought with your credit card. Your next statement should also reflect the purchase.

Other Mastercard vs Visa Similarities

Visa and Mastercard issuers have a range of products to choose from. Debit cards let you spend money already in your bank account—plus your overdraft if you have one set up. Meanwhile, you must fund prepaid cards in advance.

Visa or Mastercard credit cards have the following things in common.

1. Credit Scores Matter

Card issuers make decisions based on consumers’ credit scores. If you want a card with an extra-low APR and a really high credit limit, you’ll need a top-notch credit score. Lower credit scores generally mean lower credit limits and higher interest rates.

If you’re new to credit or you need to repair your credit, look for a credit builder or credit repair card. You won’t have a very high limit to begin with, and your APR might not be very competitive, but if you make regular payments, you’ll soon qualify for a better product.

Surge Mastercard® Credit Card

All credit types welcome to apply!

Monthly reporting to the three major credit bureaus

Up to $1,000 credit limit doubles up to $2,000! (Simply make your first 6 monthly minimum payments on time)

Fast and easy application process; results in seconds

Use your card at locations everywhere that Mastercard® is accepted

Free online account access 24/7

Checking Account Required

See if you’re Pre-Qualified without impacting your credit score

2. Rewards Cards Provide Value

Mastercard and Visa both partner with issuers that offer rewards cards. Rewards include air miles, points, store-specific rewards, food and beverage rewards and cash back. If you use your rewards card in a savvy way, you can save a lot of money.

3. Fees Vary

Visa and Mastercard don’t set fees—issuing banks do. As a result, fees for Visa and Mastercard products vary widely. Make sure you’re familiar with the over-limit, balance transfer, late payment, and foreign transaction fees on each of your credit card accounts—and stay away from credit cards with unreasonable fee structures.

4. Smart Wallets Protect Information

Both Visa and Mastercard cards are compatible with smart wallets like Apple Pay and Google Pay. Smart wallets hide your card information, so they’re more secure than swiping a card or entering card details online. Every year, more and more brick-and-mortar and online retailers accept smart wallet payments.

5. Discount Programs Save You Money

Some credit cards—especially business credit cards—incorporate high-value discount programs. The Visa SavingsEdge program, for example, can save you more than 15% when you shop with qualifying merchants. Mastercard has a similar program, called Easy Savings. In both cases, you need to enroll your card to get money back.

Which Is Better: Visa or Mastercard?

What’s the difference between Mastercard and Visa? Not that much, actually. The major difference is the company that runs the network. Merchants that accept one usually tend to accept the other, and more merchants accept Visa and Mastercard than any other type of card.

Instead of considering whether you should get a Visa or a Mastercard, think about what type of card you want and which bank you want to work with. Apply for a card that offers the rewards you want and has fees that match your budget. Whichever one you choose, you’ll be able to use it around the globe and get a very similar experience from the card network.