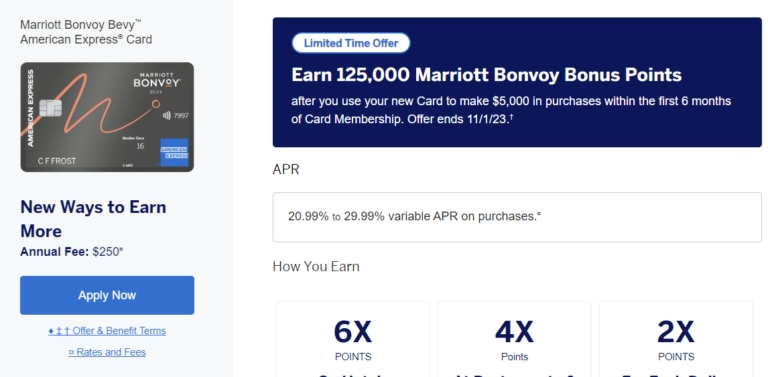

American Express is offering a bonus of 125,000 points after $5,000 in spend on the first 6 months on the Marriott Bonvoy Bevy.

Card Details

$250 annual fee

Card earns at the following rates:

Earn 6X points for every $1 spent at Marriott properties

Earn 4X points for every $1 spent on the first $15,000 in combined purchases each year on grocery stores and dining

Earn 2X points for every $1 spent on all other purchases

Free Night Award every calendar year, after $15,000 in spend within that calendar year (good for up to 50,000 points)

Complimentary Gold Elite status

15 elite night credits toward elite status

Welcome offer not available to applicants who (i) have or have had The Ritz-Carlton® Credit Card from JPMorgan, the J.P. Morgan Ritz-Carlton Rewards® Credit Card, the Marriott Bonvoy Bountiful™ Credit Card from Chase, the Marriott Bonvoy Boundless® Credit Card from Chase, the Marriott Rewards® Premier Plus Credit Card from Chase, the Marriott Bonvoy® Premier Credit Card from Chase, the Marriott Bonvoy Bold® Credit Card from Chase, or the Marriott Bonvoy® Premier Plus Business Credit Card from Chase or the Marriott Rewards® Premier Plus Business Credit Card from Chase in the last 30 days, (ii) have acquired the Marriott Bonvoy Bountiful™ Credit Card from Chase the Marriott Bonvoy Boundless® Credit Card from Chase, the Marriott Bonvoy Bold® Credit Card from Chase in the last 90 days, or (iii) received a new Card Member bonus or upgrade offer for the Marriott Bonvoy Bountiful™ Credit Card from Chase, the Marriott Bonvoy Boundless® Credit Card from Chase, or the Marriott Bonvoy Bold® Credit Card from Chase in the last 24 months.

Our Verdict

This is the standard increased bonus on this card. Overall not a good bonus, especially with the high annual fee. We won’t be adding this to our best credit card bonuses.

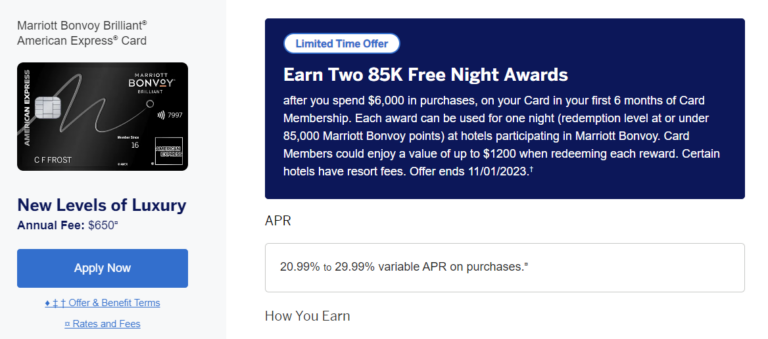

Sign up for the Marriott Bonvoy Brilliant card and earn two free night certificates good on a property up to 85,000 points when you spend $6,000 within the first six months

Card Details

$650 annual fee

$300 dining statement credit

Card earns at the following rates:

6x points per $1 spent at participating SPG & Marriott Rewards hotels

3x points per $1 spent at U.S. restaurants and on flights booked directly with airlines

2x points per $1 spent on all other purchases

Free night award every year after your card account anniversary (can be used at any property that costs under 50,000 points per night)

Complimentary gold elite status

Platinum elite status after you spend $75,000 or more on the card in a calendar year

15 nights towards elite status (you’re restricted to getting this benefit once per Marriott Loyalty program number)

Unlimited complimentary priority pass lounge access for you and up to two accompanying guests

Statement credit for Global Entry ($100) or TSA PreCheck ($85) every four years

No foreign transaction fees

Free in-room premium internet access at SPG & Marriott participating hotels

Welcome offer not available to applicants who (i) have or have had The Ritz-Carlton™ Credit Card from JPMorgan or the J.P. Morgan Ritz-Carlton Rewards® Credit Card in the last 30 days, (ii) have acquired the Marriott Bonvoy Boundless™ Credit Card from Chase, the Marriott Rewards® Premier Plus Credit Card from Chase, the Marriott Bonvoy™ Premier Credit Card from Chase, the Marriott Rewards® Premier Credit Card from Chase, the Marriott Bonvoy Bold™ Credit Card from Chase, the Marriott Bonvoy™ Premier Plus Business Credit Card from Chase or the Marriott Rewards® Premier Plus Business Credit Card from Chase in the last 90 days, or (iii) received a new Card Member bonus or upgrade offer for the Marriott Bonvoy Boundless™ Credit Card from Chase, Marriott Rewards® Premier Plus Credit Card from Chase, the Marriott Bonvoy™ Premier Credit Card from Chase, the Marriott Rewards® Premier Credit Card from Chase, the Marriott Bonvoy Bold™ Credit Card from Chase, the Marriott Bonvoy™ Premier Plus Business Credit Card from Chase or the Marriott Rewards® Premier Plus Business Credit Card from Chase in the last 24 months.

Our Verdict

Bonus was 100k + free night certificate recently, that was a much better deal with more flexibility. Annual fee has also increased by $200 since then as well. We won’t be adding this to our list of the best credit card bonuses.

Visa and Mastercard are both card networks. Both organizations manage the payment networks through which their cards work. Visa and Mastercard are different companies, but they operate in a very similar way.

Four credit card networks tend to compete for space in consumer wallets. They are Mastercard, Visa, Discover and American Express.

According to Statista, Mastercard and Visa have had the largest market share for a while. As of 2021, they accounted for more than 87% of the market. Compare that to Amex’s 10.5% and Discover’s 2.2% and you can see that most credit cards are Mastercard or Visa.

But is one better than the other? Are there really any differences between these two major credit card networks? Find out in our guide to the difference between Mastercard and Visa below.

In This Piece

What’s the Difference Between Mastercard and Visa?

While they’re both credit card processing networks, these are unique and separate companies. They were founded at different times.

Originally known as the BankAmericard credit card program, Visa launched in 1958. Mastercard began as Master Charge: The Interbank Card when it emerged as a BankAmericard competitor in 1966.

Visa cards don’t work on the Mastercard network, and vice versa. You can’t, for example, use a Visa to pay for something in a store that only accepts Mastercard.

How Are Visa and Mastercard Similar?

There are more similarities between Visa and Mastercard than differences. As mentioned earlier, these are both card networks. They both play the middleman between payment processors and issuing banks.

Both companies operate globally, so if you alert your issuer in advance, you should be able to use your Visa or Mastercard in another country when you go on vacation. Whether you pay fees for this service depends on your card issuer and account details—not on Visa or Mastercard.

Both Visa and Mastercard have tens of millions of merchants in their networks, and both companies’ merchant fees are comparable. Both organizations are publicly traded.

What’s the Difference Between a Network and an Issuer?

The credit card network is the middleman between the payment processor and the issuer of the card. When you pay with a credit card, the information is processed through the network to the bank that issued your credit card. On the other side of the transaction, the data that supports the funds transaction is also processed through the network.

Visa and Mastercard are credit card networks. They’re responsible for the infrastructure for these transactions and for protecting the information as it passes between the payment processor and the issuer. For this service, the credit card networks charge a fee—usually paid in part via a small percentage of every transaction.

An issuer is the bank that issues the card. Examples include Chase, Citibank and Capital One. The issuer is the entity that decides whether you’re approved for a credit card and sets interest rates and fees. It’s also the lender that pays for the goods you purchase with your credit card and the entity you pay back with your payments.

How Does Payment Processing Work?

Visa and Mastercard credit card and debit card payments all go through the same payment process—albeit on different networks. The process looks like this:

Consumers swipe cards—or tap contactless cards—in physical stores or enter card details online.

Merchants send payment authorization requests to their payment processors.

Payment processors send payment requests to the appropriate card network.

Card networks “ask” issuing banks for payment authorization.

Issuing banks approve or deny the transaction.

At this point, transactions are—hopefully—authorized, but they’re not settled yet. The process must continue:

Merchants send approved payment requests to payment processors in batches.

Once again, payment processors send transaction details to Visa, Mastercard or other applicable card networks.

Card networks “ask” issuing banks for previously authorized funds.

Issuing banks release the funds, which travel to merchant banks.

Credit card processing network fees get taken out along the way.

Merchant banks transfer funds into individual merchant accounts.

At this point, the store or other merchant has been paid for the goods or services you bought with your credit card. Your next statement should also reflect the purchase.

Other Mastercard vs Visa Similarities

Visa and Mastercard issuers have a range of products to choose from. Debit cards let you spend money already in your bank account—plus your overdraft if you have one set up. Meanwhile, you must fund prepaid cards in advance.

Visa or Mastercard credit cards have the following things in common.

1. Credit Scores Matter

Card issuers make decisions based on consumers’ credit scores. If you want a card with an extra-low APR and a really high credit limit, you’ll need a top-notch credit score. Lower credit scores generally mean lower credit limits and higher interest rates.

If you’re new to credit or you need to repair your credit, look for a credit builder or credit repair card. You won’t have a very high limit to begin with, and your APR might not be very competitive, but if you make regular payments, you’ll soon qualify for a better product.

Surge Mastercard® Credit Card

All credit types welcome to apply!

Monthly reporting to the three major credit bureaus

Up to $1,000 credit limit doubles up to $2,000! (Simply make your first 6 monthly minimum payments on time)

Fast and easy application process; results in seconds

Use your card at locations everywhere that Mastercard® is accepted

Free online account access 24/7

Checking Account Required

See if you’re Pre-Qualified without impacting your credit score

2. Rewards Cards Provide Value

Mastercard and Visa both partner with issuers that offer rewards cards. Rewards include air miles, points, store-specific rewards, food and beverage rewards and cash back. If you use your rewards card in a savvy way, you can save a lot of money.

3. Fees Vary

Visa and Mastercard don’t set fees—issuing banks do. As a result, fees for Visa and Mastercard products vary widely. Make sure you’re familiar with the over-limit, balance transfer, late payment, and foreign transaction fees on each of your credit card accounts—and stay away from credit cards with unreasonable fee structures.

4. Smart Wallets Protect Information

Both Visa and Mastercard cards are compatible with smart wallets like Apple Pay and Google Pay. Smart wallets hide your card information, so they’re more secure than swiping a card or entering card details online. Every year, more and more brick-and-mortar and online retailers accept smart wallet payments.

5. Discount Programs Save You Money

Some credit cards—especially business credit cards—incorporate high-value discount programs. The Visa SavingsEdge program, for example, can save you more than 15% when you shop with qualifying merchants. Mastercard has a similar program, called Easy Savings. In both cases, you need to enroll your card to get money back.

Which Is Better: Visa or Mastercard?

What’s the difference between Mastercard and Visa? Not that much, actually. The major difference is the company that runs the network. Merchants that accept one usually tend to accept the other, and more merchants accept Visa and Mastercard than any other type of card.

Instead of considering whether you should get a Visa or a Mastercard, think about what type of card you want and which bank you want to work with. Apply for a card that offers the rewards you want and has fees that match your budget. Whichever one you choose, you’ll be able to use it around the globe and get a very similar experience from the card network.

The following is a guest post by Daniela MckVicker, a blogger for Top Writers Review.

Considering offering credit to your customers? A credit policy is a document that you need. It outlines the conditions of credit sales, giving your customers one more way to make orders. For your business, it helps encourage new sales and manage associated risks.

If you need help with writing a business credit policy, consider these guidelines.

What Is a Credit Policy?

A credit policy is a document that defines credit and payment terms for customers and policies to mitigate risk from extending credit to those who can’t meet their obligations. These guidelines are critical for businesses selling their products and services in credit.

When broken down into essential parts, a credit policy includes:

Evaluation of a customer’s creditworthiness

Decision process to extend credit to customers (terms, conditions, etc.)

Credit limits for customers

Methods of dealing with delinquent accounts

A sound credit policy minimizes the risk of not receiving funds from sales made on credit. So, writing this policy requires knowledge of a company’s financial capabilities, applicable laws, and risks involved.

Get matched with a personal

loan that’s right for you today.

Learn

more

Before Writing: Credit Policy Do’s and Don’ts

If you’re writing a new draft or updating the current credit policy, keep these tips in mind:

Don’t keep it confidential. Everyone in your company should know how you’re going to manage credit sales.

Don’t make the policy so strict, so you have opportunities to adjust the credit decision-making process later.

Don’t make the policy too broad and/or open to interpretation. This might cause conflicting interpretations by department members or other stakeholders.

Do make credit approval limits clear for those with authority to grant credits.

Do include procedures to reduce credit risks and sales where customers are unable to pay off the debt.

Do include guidelines on keeping company and customer information private.

Do state that any unlawful or unethical behavior within the credit department is strictly prohibited.

How to Write an Effective Business Credit Policy

Let’s go over each important section in business credit policies.

1. Explain the Purpose of the Policy

The first section of a business’s credit policy is dedicated to the conditions, responsibilities, and rights of the credit department. Describe how it works and helps to meet the goals you’re trying to achieve as an organization.

For example:

“The credit department is responsible for establishing payment terms for the company’s customers and monitoring these terms to ensure compliance. The present credit policy describes alternative payment methods to customers.”

Treat this section as an introduction that you’ll later use to teach employees. Save the specifics for the subsequent parts – there’s plenty of space for that.

2. List the Roles and Responsibilities of Credit Department Members

Explain the duties of each member who works in the credit department. By doing so, you’re defining their roles and letting them know what’s expected of them.

Here are some common credit department positions, along with brief descriptions:

Chief Financial Officer (CFO). Responsible for managing the entire department, making policies and finance-related decisions

Credit manager. Organizes and controls the credit department by training personnel, setting up credit rules and procedures, and authorizing credit limits. Reports directly to CFO

Collections manager. Manages the credit collection effort by collaborating with third-party collection agencies. Reports to the credit manager

Credit analyst. Reviews financials, evaluates and assigns credit lines for customers

Billing clerk. Prepares the invoices and sends them to customers in time.

3. Describe Credit Application Process

The credit application process is the process that leads to the initiation or extension of credit to a customer. In this section, the main purpose is to explain this process and the procedure of approval.

To apply for credit, customers must also provide a number of documents. Commonly, companies request credit bureau reports, credit references, financial statements, and public records.

Some of the most important points to provide in this section:

Description of conditions on which a customer can apply for credit

Documents the customer must provide to get their application reviewed (bank references, statement of payment terms, etc.)

Identification of credit department employees responsible for reviewing customer applications

Description of the customer’s creditworthiness evaluation and relevant credit limits.

4. Decide Who Can Get Extended Credit

Obviously, your business can’t give away credits like Christmas cookies. In some cases, customers will have histories of not delivering on their obligations–so your policy should call for credit checks on every applicant.

In addition to asking customers to provide relevant documents, have your credit department also get in touch with nationwide credit reporting agencies. The three main credit bureaus are Equifax, Experian, and TransUnion, which can provide a free credit report once every 12 months.

Advise your customers on how and when to talk to a credit reporting agency about their reports. Keep in mind, however, that you’re legally required to ask customers for permission before making a credit report inquiry.

5. Set Credit Limits

The credit policy defines the credit limit for your business. In other words, it gives your employees instructions on the amount to give and when to stop extending credit. Following these guidelines will help to reduce many risks.

For small businesses, a $5,000 credit limit is reasonable. This amount could reach up to $10,000 for a mid-sized company. However, the right amount for your business depends on two things: a customer’s credit history and your liabilities.

First, take a good look at a customer’s documents (income, debts, etc.) to determine the limit they could realistically handle. Second, ask yourself if you could still pay your own liabilities if that customer failed to pay credit on time. If the answer is “no,” then reducing the credit limit should be a good idea. Make sure to include these credit limits in your policy.

6. Define Terms and Conditions of Credit Sales

These are the terms and conditions for delivering products or services on credit. They’re essential for credit applications, sales contracts, emails, orders, and invoices–all sales-related documents.

They protect your rights by setting credit limits, customer responsibilities, and other important points. For example, describe when you will begin charging interest, extension conditions, interest rate, late payment fees, early payment discounts, and deposit requirements.

7. Plan for Handling Past Due Accounts

Unfortunately, even with your best effort to manage credit risks, some customers won’t pay collections on time. That’s why you need to have a plan for pursuing unpaid debts.

In most cases, credit policies instruct to send urgent payment reminders. Consider using debt collection agencies if a customer doesn’t pay after getting notified multiple times. Should that customer fail to meet their obligations on more than one sale, close their account.

8. Make Changes

A credit policy should be “a living document.” To evaluate if their credit department helps to meet business goals, companies have to measure its performance. This is where specific goals based on the company’s strategy come in.

For example, the credit department might be tasked with reducing the average number of days it takes to collect on credit sales by 20%. Comparing credit sales data for a defined period defines if the credit department met this goal.

The effectiveness of credit department efforts measured by goals defines changes to be made in the policy. If the department struggles to meet the goals, consider making appropriate changes to the document.

A proposed set of higher risk weights for mortgage-related assets at banks could broadly compound current strains on home affordability and conflict with other policies and rulemaking promoting it, critics testified at a congressional hearing Thursday.

The new rules not only increase portfolio lending expenditures for low down payment loans, but aspects like a possible change affecting servicing rights also add costs for lenders and the market at large, said Bob Broeksmit, president and CEO, Mortgage Bankers Association.

The rights and associated work of handling loan payments are a key cost for the mortgage industry at large and if depositories further withdraw from investments in them, costs for nonbank lenders already struggling to profit due to higher rates could rise, he said.

“The mortgage servicing value is an integral part of how every mortgage is priced, not just mortgages made by these banks,” Broeksmit said at a House Financial Services subcommittee hearing. The subcommittee involved is focused on financial institutions and monetary policy.

Mortgage servicing rights already have a relatively high risk weighting under current bank capital rules that discourage holding them in amounts above 25% of Tier One common equity. The proposal would lower the cap to 10% of common stock or other assets in that category.

Broeksmit also reiterated his past criticisms of moving from a risk-weighting of 50% for most home mortgages outside the income-producing sector, to a proposed step-up of percentages in that category by loan-to-value ratio that’s in excess of global Basel III rules.

“If these increased capital requirements go into effect, banks will make fewer mortgage loans or they will raise the price,” said Broeksmit.

He also doubled-down on his previously stated concerns about the fact that the new requirements don’t account for the additional protection private mortgage insurance can provide to loans with lower down payments.

Others testifying said the capital rules could put a strain on mortgages that have balloon payments due in a higher rate market.

“In a time of historic inflation, the fastest increase in interest rates in modern history, and a growing likelihood of the credit crunch, now is not the time to raise capital levels,” said Committee Chair Rep. Andy Barr, R.-Ky. “Such action threatens to further constrain credit availability and put already-sensitive sectors such as commercial real estate in further peril.”

The new capital rules also could be a constraint on lines of credit used both by businesses and consumers, Broeksmit said.

“If I understand this voluminous proposal correctly, banks would be required to hold capital on the maximum amount that could be drawn rather than the amount that is outstanding. That could have a really chilling effect on … small business credit and also home equity lines of credit where consumers take that out and use it as they need it,” he said.

Other speakers and some Democratic members of Congress debated the assertion that the rule would hurt access to financing.

“We strongly disagree that new capital requirements will undermine credit availability,” said Alexa Philo, senior policy analyst, Americans for Financial Reform, after Rep. Ayanna Pressley, D.-Mass, asked whether the new rules could protect the availability of lending in a downturn.

There’s a significant body of research that has found that domestic financial institutions with higher reserves provided more financing than those with lower capital levels, Philo said.

“Well capitalized, large U.S. banks had higher loan originations and liquidity,” she said.

American Express has sent out e-mails offering increased bonuses on the Business Delta cards. Offers are as follows:

Gold Delta SkyMiles® Business Credit Card 80,000 miles after $6,000 in spend within the first three months. Plus, earn an additional 5,000 Bonus Miles after you make an eligible Delta purchase with your new Card within your first 6 months

Platinum Delta SkyMiles® Business Credit Card 90,000 miles after $8,000 in spend within the first three months. Plus, earn an additional 10,000 Bonus Miles after you make an eligible Delta purchase with your new Card within your first 6 months

Delta Reserve® Credit Card for Business 100,000 miles after $12,000 in spend within the first three months. Plus, earn an additional 20,000 Bonus Miles after you make an eligible Delta purchase with your new Card within your first 6 months

Our Verdict

None of these bonuses are at all time highs. Given the recently announced Delta changes I’d recommend waiting for better offers to come along unless you have an urgent need for the miles.

Lenders deny loan applications due to reasons like poor credit, insufficient collateral, industry and more

Getting denied a small business loan doesn’t mean businesses can’t secure one in the future

Before reapplying for a loan, determine why the previous application was denied and make sure you’re applying with the right lender

Starting or growing a business may require financing, but not all business loan applications are successful.

According to the Federal Reserve’s 2023 Report on Employer Firms, 21 percent of surveyed loan applicants were denied for loans in 2022. That number is expected to go up considering lenders are expected to continue tightening their lending standards for the rest of 2023.

We’ll explore the most common reasons for denial and provide solutions to increase your chances of approval when reapplying for a small business loan.

Too much debt

If your business carries a significant amount of debt, it may hinder your ability to repay a new loan. Lenders view excessive debt as a risk because it can lead to default. And if you default on a business loan, a few things may happen, including the lender seizing business or personal property to recover the borrowed funds.

Your best course of action is to focus on reducing your existing debt load. You can do this by renegotiating terms with creditors, consolidating loans or making additional payments. Also, limit the use of your available credit, which adds to your debt and impacts your ability to build business credit.

Bad credit

A business owner with bad credit is a red flag for lenders. It suggests that you may struggle to manage your finances.

If you have a history of late or missed payments and defaults, consider making a few changes to how you manage your personal and business finances. For example, set up autopay so bills are paid on time and review your credit report to dispute errors and inaccuracies.

You won’t see immediate changes to your score. So if you need funds right away, look into lenders who specialize in business loans for bad credit.

Don’t meet the lender’s eligibility requirements

Failing to meet a lender’s eligibility requirements for a business loan can result in denial. All lenders have specific criteria related to credit scores, annual revenue, time in business and other factors.

It’s important to review the eligibility requirements of potential lenders before applying. If you don’t meet the lender’s criteria, consider alternative lenders. But if you are set on working with a specific lender, focus on improving your business’s financial health so you qualify for a loan.

Not enough collateral

With a secured small business loan, businesses must pledge assets that can be seized if they default on the loan. Since the collateral for a business loan is used as a form of repayment and needs to cover the outstanding balance on the loan, if these assets aren’t of significant value, lenders may deny your loan application.

You can work to build up your business’s assets so you qualify for secured financing options in the future, but if you need funding as soon as possible, explore alternative financing options that don’t require collateral.

Bankrate insight

Online lenders typically offer a variety of unsecured business loans, including business lines of credit and merchant cash advances. Loan amounts will likely be significantly lower than secured business loan amounts. If you don’t have a high credit score and strong business financials, you may see loan amounts of $100,000 or less.

Not enough free capital or cash flow

Lenders want to see that your business has sufficient cash flow to repay the loan. If there’s no evidence of enough free capital or cash flow, they can’t approve you.

Before applying for another small business loan, complete a cash flow analysis to figure out ways to better manage your expenses and free up cash so you can afford the monthly payments. You can also increase your revenue. The required annual revenue varies, but if your business brings in at least $100,000, you could get approved with some online lenders.

You can also explore invoice factoring or merchant cash advances, which are short-term business loans designed to help businesses that need quick access to capital.

Don’t have a business checking account

A business checking account is a valuable tool that can help you manage your business finances more effectively. While it isn’t a requirement to start or run a business, many lenders, including OnDeck, Bank of America and Fundbox won’t approve loan applications for businesses without business checking accounts.

To meet this requirement, simply open a business checking account. If your lender offers a full suite of business banking products and services, consider opening an account to establish a relationship and potentially access discounts.

Industry risk

Some lenders don’t want to risk lending to businesses in certain industries due to the odds of failure or unstable revenue. For example, restaurants and real estate businesses may be disqualified from a small business loan.

Research lenders who are familiar with your industry and the associated risks. Many alternative lenders don’t have the same industry restrictions as traditional lenders, so you could be better off going this route. But they often come at a high price due to interest and fees.

Don’t have a business plan

Not all lenders require a business plan, but the ones that do want to see a clear and detailed outline of how you’ll use the loan, how it will benefit your business and if your business has the potential to earn the revenue necessary to repay the loan.

Creating a well-thought-out business plan that demonstrates your vision, strategy, goals and financial potential can get you closer to loan approval. A few things to include are:

Executive summary

Company description

Summary of market research

Financial plan

Why was my SBA loan denied?

Compared to traditional small business loans, SBA loans offer extended terms and reduced interest rates, with average SBA interest rates falling between 10.75 percent and 16.50 percent.

In 2022, SBA approvals for 7(a) loans were under 50,000 and only about 9,000 for 504 loans. That’s according to data from the SBA Weekly Lending Report. When an SBA loan is denied, it could be for similar reasons as traditional loans, but the SBA has additional criteria that businesses may fall short of meeting.

Common reasons for SBA loan application denial include:

Poor personal or business credit scores

Insufficient collateral

Insufficient cash flow

High existing debt

Ineligible business, size or industry

Missing documents or information

Bankrate insight

If your SBA loan is denied, you’ll need to wait 90 days before reapplying. During that time, check with your lender to see why your SBA loan was denied and make changes or consider applying for a different type of SBA loan.

What to do if your business loan is denied

If your small business loan is denied, this doesn’t mean you won’t get the funding you need. You can reapply for a loan, but there are a few things you’ll want to take care of first.

Start by identifying the reason for the denial. Whether it’s due to poor credit history, insufficient cash flow or another issue, this insight is what you need to get your future loan application approved.

Depending on the reason, for example, if you don’t have a business checking account or business plan, you can be ready to reapply in a few days or weeks. But if your business’s poor financial health is to blame, making improvements may take some time but can lead to a more affordable business loan. But if you can’t wait, consider looking into a different lender that is willing to work with you.

Before you reapply for a small business loan, work to boost your creditworthiness by making timely payments and reducing existing debt. And don’t be afraid to explore alternative lenders and government-backed programs with flexible lending criteria.

Bottom line

Poor credit, insufficient cash flow, lack of a business plan and other issues can prevent you from securing a small business loan. It can be disappointing when you get denied funding, but it’s important to understand why because it’s an opportunity to create a plan and implement solutions to significantly improve your business’s financial health. And, by the time you’re ready to reapply, you’ll seem less risky to lenders and have better odds of approval.

Frequently asked questions

Credit score requirements vary by lender, but you can secure a business loan with a score as low as 500.

Yes, it is possible to get a business loan with no money. Certain business loans, such as SBA microloans, equipment loans and business credit cards, are designed for new businesses with no revenue. But waiting to secure financing might be the better option since some business loans may not come with favorable rates and terms for businesses with no revenue.

Getting a small business loan can be challenging, but it depends on the loan type, lender, their requirements and your qualifications, including credit score and annual revenue. Start by getting your personal and business credit scores and reviewing your credit report. Then look at lenders and their eligibility requirements to see which ones will work with you.

Bank of America is offering 70,000 miles when you spend $3,000 or more within the first 90 days of account opening.

Card Details

Annual fee of $95 is not waived

Card earns at the following rates:

3x miles per $1 spent on Alaska Airlines tickets, vacation packages, and cargo purchases

2x miles for every $1 spent on eligible gas, cable, streaming services and local transit (includes ride share) purchases

1x miles on all other purchases

Free checked bag for you and up to six other passengers on your reservation

No foreign transaction fees

Earn a 10% rewards bonus on all miles earned from card purchases if you have an eligible Bank of America account

Priority boarding benefit

20% back on all Alaska Airlines inflight purchases

$100 off an annual Alaska Lounge+ Membership when you pay with your new card

Get Alaska’s Famous Companion Fare from $122 ($99 fare plus taxes and fees from $23) each account anniversary after you spend $6,000 or more on purchases within the prior anniversary year

This card will not be available to you if you currently have or have had the card in the preceding 24 month period. This does not apply to the business credit card product.

A lot of these details are from recent changes.

Our Verdict

Not as good as the 70k + $100 offer, I tried to do a dummy booking but didn’t see 70k + $100 unfortunately. I’d wait a bit to see if that starts to appear, but 70k might be enough for some people to apply.

Chase is offering 65,000 Hyatt points after $5,000 in spend within the first three months when you open a new World of Hyatt Business card and an additional 15,000 bonus points after you spend $12,000 within the first 6 months

Card Details

$199 annual fee (fee is NOT waived the first year)

Card earns at the following rates:

Earn 4x points per dollar at Hyatt properties

Earn 2x points per dollar on your top three categories, from a selection of the following eight categories (they call this “Adaptive accelerator”):

Dining

Shipping

Airline tickets when purchased directly with the airline

Local transit & commuting

Social media & search engine Advertising

Car rental agencies

Gas stations

Internet, cable & phone services

Earn 2 points per dollar on fitness club and gym memberships

Earn 1 point per dollar on all other spend

Spend $50,000 or more on the card in a calendar year and receive 10% of redeemed points back as Bonus Points for the remainder of the calendar year (maximum of 20,000 Bonus Points per calendar year)

Earn $100 in Hyatt credit each anniversary year: Spend $50 or more at any Hyatt property and earn $50 in statement credits up to two times each anniversary year

Automatic Discoverist status in World of Hyatt (typically requires 10 Tier-Qualifying Nights or 25,000 Base Points)

Gift up to 5 Discoverist statuses to their company employees (they do not have to be cardholders)

5 Tier-qualifying night credits with each $10,000 in spend on the card in a calendar year

With World of Hyatt’s 2021 reduced elite status criteria, World of Hyatt Business Credit cardmembers can earn top tier Globalist status with $60,000 in spend on the card now through Dec. 31, 2021.

Access to Hyatt Leverage, Hyatt’s global business travel program that offers special rates to qualifying small and mid-sized enterprises at participating Hyatt hotels worldwide

No foreign transaction fees

No fee for employee business cards

Primary rental car collision damage waiver

Our Verdict

This is the same bonus that the card launched with and an all time high (actually not as good as that only required $5,000 total spend). Hopefully it becomes available as a referral bonus as well. Could definitely be worth it for some people, especially as Chase business cards don’t count towards your 5/24 status (you still need to be under 5/24 to get approved though). We will add this to our list of the best credit card bonuses.

Rewards optimizers use the term “trifecta” to describe a combination of three credit cards from one issuer that have complimentary benefits. When combined, the cards create a rewarding synergy that helps you earn more points and get more value out of your redemptions.

Chase and American Express offer popular trifecta combinations for people seeking travel rewards. While you can mix and match different cards to create an optimal trifecta based on your spending habits, there is a recommended combination for each issuer.

In a head-to-head showdown, the Chase trifecta comes out ahead for most people — you’ll pay significantly less in annual fees, get easier-to-use travel credits, rewards and travel partners, and have broader acceptance around the world. The Chase trifecta is also more accessible for people who don’t qualify for a small-business credit card.

At a glance

Here’s a look at the rewards-earning rates for each trifecta. (For details about specific benefits and statement credits offered by each card, check out the individual review pages linked above.)

Chase trifecta

AmEx trifecta

Rewards earning rates

Chase Sapphire Reserve®:

10 points per dollar spent on hotels and car rentals booked through Chase and Chase Dining purchases.

5 points per dollar spent on flights booked through Chase.

3 points per dollar spent on travel and dining.

1 point per dollar on all other spending.

Chase Freedom Flex℠:

5% cash back on up to $1,500 in combined purchases each quarter on bonus categories that you activate (1% back after).

5% back on travel booked through Chase.

3% back at restaurants and drugstores.

1% back on all other non-bonus-category spending.

Chase Freedom Unlimited®:

5% back on travel booked through Chase.

3% back at restaurants and drugstores.

1.5% on all other spending.

The Platinum Card® from American Express:

5 points per dollar for flights booked directly with airlines or through AmEx Travel (on up to $500,000 per calendar year, then 1x).

5 points per dollar for prepaid hotels booked with AmEx Travel.

1 point per dollar on all other purchases.

American Express® Gold Card:

4 points per dollar at restaurants, including takeout and delivery in the U.S.

4 points per dollar at U.S. supermarkets (on up to $25,000 per calendar year in purchases, then 1x).

3 points per dollar on flights booked directly with airlines or through AmEx Travel.

1 point per dollar on all other purchases.

The Blue Business® Plus Credit Card from American Express:

2 points per dollar on the first $50,000 in purchases per calendar year (then 1x).

Terms apply.

Overall annual fees

$945. Terms apply.

Why the Chase trifecta is better for most people

Lower annual cost

The collective annual cost of the Chase trifecta is $550, with the Chase Sapphire Reserve® having the only annual fee.

That’s 42% cheaper than the $945 annual cost of the AmEx trifecta, which includes annual fees of $695 on The Platinum Card® from American Express, $250 on the American Express® Gold Card and $0 on The Blue Business® Plus Credit Card from American Express.

Sure, the AmEx trifecta offers hundreds of dollars worth of coupon-book style credits for services like Uber and Walmart+ that can help offset the higher annual cost. But the catch is that many of these credits are limited in scope: the $240 annual entertainment credit, for example, is doled out in $20 monthly increments and applies to a handful of entertainment subscriptions only. You may have to go out of your way to optimize the potential value of the credits.

Easier-to-use travel credits

The Chase Sapphire Reserve® comes with a $300 annual travel credit that applies to all eligible travel purchases. It doesn’t get any easier — simply book travel like hotel, airfare or rental car with your card, and receive a statement credit.

By comparison, The Platinum Card® from American Express comes with an annual $200 airline fee credit (enrollment required), but it too has several caveats. You must select only one airline from a short list of options to apply the credit. It only applies to incidental charges like in-flight refreshments and checked baggage, and the charge must be made separately from the ticket purchase. The card also comes with an annual $200 hotel credit, but that only applies to specific luxury hotels that are prepaid through the American Express travel portal. Since prepaid hotels are often nonrefundable, you could incur a significant out-of-pocket expense if your plans change. Terms apply.

More valuable rewards

All three cards in the Chase trifecta earn Chase Ultimate Rewards®. These rewards can be combined into your Chase Sapphire Reserve® account, where they are redeemable through the Chase Ultimate Rewards® travel portal at a rate of 1.5 cents each. That makes 6,666 Ultimate Rewards® worth $100 in travel.

American Express Membership Rewards points are worth 1 cent each when booking airfare and 0.7 cent a piece when booking hotels through the AmEx travel portal. It would cost 10,000 points for $100 in airfare, or 14,286 points for a $100 hotel stay. That’s significantly less value than you can get for the same number of Ultimate Rewards®.

🤓Nerdy Tip

Though classified as cash back cards, the Chase Freedom Flex℠ and Chase Freedom Unlimited® earn Ultimate Rewards® points. But if you hold just those cards, the points are worth 1 cent each toward travel booked through Chase and are unable to be transferred to travel partners. Adding the Chase Sapphire Reserve® unlocks the ability to transfer to partners and increases the value of the points to 1.5 cents each.

More accessible travel partners

Both Chase and AmEx have a broad list of airline and hotel transfer partners — American Express has 21 travel partners compared with Chase’s 14. But more isn’t always better.

In this case, Chase wins for many travelers with quality over quantity. Ultimate Rewards® can be transferred to partners like United Airlines, Southwest Airlines and Hyatt at no cost.

While American Express boasts more partners, the majority of them are international airlines and not as familiar to many. Transferring points to these airlines can yield impressive value, but can also cause more headaches and confusion to navigate. The biggest domestic transfer partner for AmEx is Delta Airlines — however, you’ll pay an excise tax for transferring points to Delta (and a few others).

Full list of Chase transfer partners

Aer Lingus (1:1 ratio).

Air Canada (1:1 ratio).

Air France-KLM (1:1 ratio).

British Airways (1:1 ratio).

Emirates (1:1 ratio).

Iberia (1:1 ratio).

JetBlue (1:1 ratio).

Singapore (1:1 ratio).

Southwest (1:1 ratio).

United (1:1 ratio).

Virgin Atlantic (1:1 ratio).

Hyatt (1:1 ratio).

InterContinental Hotels Group (1:1 ratio).

Marriott (1:1 ratio).

Full list of AmEx transfer partners

Aer Lingus (1:1 ratio).

AeroMexico (1:1.6 ratio).

Air Canada. (1:1 ratio).

Air France/KLM (1:1 ratio).

ANA (1:1 ratio).

Avianca (1:1 ratio).

British Airways (1:1 ratio).

Cathay Pacific (1:1 ratio)

Delta Air Lines (1:1 ratio).

Emirates (1:1 ratio).

Etihad Airways (1:1 ratio).

Hawaiian Airlines (1:1 ratio).

Iberia Plus (1:1 ratio).

JetBlue Airways (2.5:2 ratio).

Qantas (1:1 ratio).

Qatar Airways (1:1 ratio).

Singapore Airlines (1:1 ratio).

Virgin Atlantic Airways (1:1 ratio).

Choice Hotels (1:1 ratio).

Hilton Hotels & Resorts (1:2 ratio).

Marriott Hotels & Resorts (1:1 ratio).

No business cards required

Our recommended Chase trifecta consists of all personal credit cards. That makes it broadly accessible to anyone with a credit profile that qualifies for the three cards. However, you’ll have to be eligible for a small-business credit card to craft the ideal AmEx trifecta.

The Blue Business® Plus Credit Card from American Express and its ability to earn 2 points per dollar for all purchases on up to $50,000 annually is the glue that really holds the AmEx trifecta together, since the other cards only earn 1x on non-bonus spending. If you don’t qualify for a small-business card, the Chase trifecta is the easy choice. Terms apply.

Better international acceptance

All Chase credit cards carry the Visa or Mastercard logo, making them usable nearly anywhere credit cards are accepted throughout the globe. American Express has closed the acceptance gap domestically, but still lags behind Visa and Mastercard abroad. If you’re looking to use your card internationally, your surefire bet is the Chase trifecta.

Why you might want the AmEx trifecta

Big grocery and restaurant spend

The American Express® Gold Card offers a sky-high 4 points per dollar spent at U.S. supermarkets (on up to $25,000 in annual spend) and restaurants. The Chase trifecta earns an everyday 3 points per dollar at restaurants, and the potential to earn 5 points per dollar on up to $1,500 in quarterly spend if grocery stores are selected as a rotating bonus category on the Chase Freedom Flex. If you have an outsized budget for dining out or groceries, the math may have you leaning toward the AmEx trifecta. Terms apply.

Elite status and luxury perks

You might prefer the AmEx trifecta if you value elite status and exclusivity. By holding The Platinum Card® from American Express, you’ll get complimentary gold elite status with Hilton and Marriott (enrollment required), President’s Circle status with Hertz, Emerald Club Executive status with National, 24-hour access to a concierge for those hard-to-access reservations or tickets, and access to members-only VIP experiences at prestigious events like Wimbledon and the Kentucky Derby. Terms apply.

If you value these perks, the AmEx trifecta may be worth the added annual cost.

Airport lounge access

If you’re a frequent flyer and often find yourself in airports, lounge access can be a great way to escape the commotion of the terminal. In addition to a Priority Pass Select membership (which the Chase trifecta also has), the AmEx trifecta also lets you access AmEx Centurion and International Lounges, Delta Sky Clubs (only when flying Delta) and Plaza Premium, Escape and Airspace network lounges.

That’s a huge footprint that includes complimentary access to over 1,400 airport lounges. If you want lounge access, the AmEx trifecta may be better for you.

🤓Nerdy Tip

The Chase Sapphire Reserve® offers a dining credit (normally $28 each) for you and a guest at participating Priority Pass restaurants. The Priority Pass access granted by AmEx cards excludes these restaurants.

Which trifecta should you get?

Most people will do better with the Chase trifecta. The annual cost is significantly lower, the benefits and rewards are more transparent and easy to use, and your points are worth more when booking travel through the Chase travel portal. The AmEx trifecta could be a good choice for those who value a broader airport lounge footprint and luxury benefits, but realize you’ll be paying a lot more for those perks.

To view rates and fees of The Platinum Card® from American Express see this page.To view rates and fees of the American Express® Gold Card, see this page.To view rates and fees of The Blue Business® Plus Credit Card from American Express, see this page.