The Federal Housing Finance Agency, which oversees Fannie Mae and Freddie Mac, has released details of a new program to expedite short sales.

The program consolidates Fannie and Freddie’s current short sale programs, including the original Home Affordable Foreclosure Alternative (HAFA) programs and other proprietary ones.

The new streamlined approach will be known as the “Standard Short Sale/HAFA II,” and is designed to make short sales easier for those most in need.

Short Sales for Those Still Making Payments

First and foremost, the new guidelines will allow homeowners with Fannie or Freddie mortgages to pursue a short sale, even if they are current on their mortgage payments, assuming they have an eligible hardship.

At the moment, it’s difficult (but not impossible) to get a short sale going unless you fall behind on your payments, which kind of defeats the purpose of attempting to avoid full-blown foreclosure.

With HAFA II, loan servicers will be able to quickly qualify such borrowers without any additional approval from Fannie or Freddie.

Common hardships listed by the FHFA include unemployment, divorce, long-term disability, increased housing expenses, disaster (natural or man-made), business failure, and death of a borrower or household wage earner.

The streamlined process will also work for those who are transferred to a job or accept a new career opportunity more than 50 miles away.

This should help more borrowers conduct short sales without the massive credit score hits associated with multiple missed mortgage payments.

[Short sale vs. foreclosure with regard to credit]

Fannie and Freddie have also agreed not to pursue a deficiency judgment in exchange for a small financial contribution (assuming the borrower has sufficient income/assets).

It’s unclear how small it may be, but I would venture to say that most homeowners won’t want to pay it.

Service members who are relocated will also be automatically approved for short sales, even if current on their mortgages (and they won’t be subject to paying the contribution).

Quicker Short Sales for Those Already Behind

HAFA II also addresses those who are already behind on their mortgage payments and sailing full steam toward foreclosure.

These borrowers will enjoy an expedited approach to better deal with the time sensitive nature of the foreclosure process.

This means the documentation needed to demonstrate hardship may be reduced or even eliminated in some cases.

To further speed things up, or at least not unnecessarily slow things down, Fannie and Freddie will offer up to $6,000 to second mortgage holders to accelerate the short sales.

At the moment, a secondary lien holder can slow down a short sale by negotiating for a larger chunk of the outstanding balance, effectively stalling the entire process.

So hopefully the $6,000 will be enticing enough to speed along the process in most cases.

The new guidelines will also provide clarity on processing a short sale if a foreclosure sale is pending so borrowers can get last minute offers in and avoid losing their home.

Currently, loan servicers are required to review and respond to short sale offers within 30 days of receiving them.

They must also provide weekly status updates if the short sale is still under review after 30 days, and must finalize decisions within 60 days of the receipt of the offer.

Note: Borrowers who take part in the program will not be eligible for another mortgage backed by Fannie or Freddie for at least two years after the short sale occurs.

The HAFA II program will be effective come November 1, 2012.

There’s been a lot of confusion about short sales, especially with regard to how they affect one’s credit score.

Plenty of people have recommended them as an alternative to foreclosure, even going as far as to say they can spare you the nasty credit score ding.

And while they can be a worthwhile foreclosure alternative, the credit score impact really isn’t much different.

This has been an issue for a while because common sense and logic would tell you that a short sale is better than foreclosure.

Being a Good, Bad Borrower

After all, if you choose to short sell your home, you’re making a conscious effort to work with your lender.

As opposed to hastily packing your things and heading for the hills, or stripping your home of its precious copper and selling it on the black market.

That should be rewarded, right? And the mortgage crisis was a one-off event, which made good consumers “break bad.”

If anything, agreeing to a short sale should tell other creditors that you mean well, even if you can’t or don’t want to continue making your monthly mortgage payments on your underwater home.

Unfortunately, this sentiment hasn’t translated to higher credit scores. Fico still sees foreclosures and short sales as very similar negative events.

But why? Aren’t they totally different?

Data Backs It Up Folks

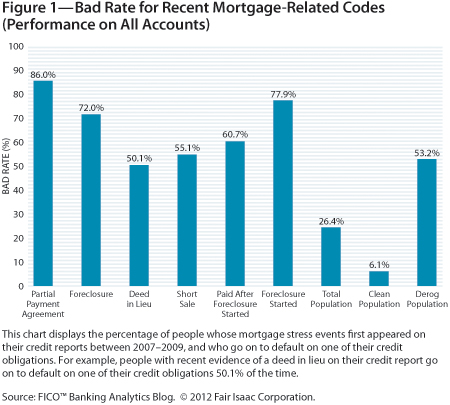

Whether foreclosures and shorts sale are similar or not, data collected by Fico proves that those who short sell are higher risk than other borrowers.

Fico looked at data from October 2009 to October 2011, discovering that more than one out of every two borrowers who experienced a short sale defaulted on another credit account within two years.

The number was actually 55.1%. Yikes. Does this mean the floodgates were opened post-short sale? That the veritable seal was broken for many of these borrowers?

Was their moral compass thrown and no longer incentive enough to keep up with their obligations? Or was it that the short sale itself really coincided with financial distress?

Whatever the reason, it’s clear (from the data) that short sales and risk go hand in hand.

As you can see from the chart, credit default risk post-foreclosure was even higher, at a rate of 72%.

But Fico didn’t feel the difference (about 17%) was material enough to merit a “more positive treatment” for short sales.

Additionally, most short sellers have mortgage delinquencies on their credit reports.

To compare, roughly only one in 50 borrowers with a Fico score in the high 700 range defaults on one of their credit obligations.

So clearly having that number jump from one to 25 is an issue, which explains why Fico smacks the credit scores of those who experience a short sale.

What About Loan Mods and Fico Scores?

There have also been a lot of questions about how loan modifications affect credit scores, or more specifically, Fico scores.

Will that HAMP loan modification hurt your credit score, or is it just treated as a standard refinance?

Currently, Fico says there is no impact (beyond perhaps a credit inquiry) as long as the loan mod is reported using the proper Consumer Data Industry Association (CDIA) comment codes.

There was even a bill introduced to ensure loan mods didn’t hurt consumer credit scores.

But Fico is currently evaluating whether the incidence of such events leads to greater credit risk.

In other words, if the findings are similar to short sales, consumers who agree to a loan mod could see their Fico scores take a hit as well.

But only time will tell on that one, since the data is so fresh. There’s plenty of re-default data out there though, so you have to wonder.

Bank of America announced late Friday that it is in the process of mailing roughly 150,000 letters to distressed homeowners, offering to pay off their second mortgages as part of the national foreclosure settlement.

Before this announcement, they had been lacking in the assistance department and getting bad press because of it.

The Charlotte-based bank said it began mailing the letters back in July, and will continue to inform pre-qualified homeowners throughout the year.

The program is opt-out, meaning the borrower’s second mortgage will be fully paid off, or “extinguished,” unless the customer contacts the bank within 30 days of receiving the letter to decline the offer.

By paying off the second mortgages of struggling borrowers, Bank of America said its goal is to put homeowners in better equity positions in the hopes they’ll get back on their feet.

In other words, if they can remove the burden of a big second mortgage and push the borrower’s loan-to-value ratio below 100%, homeowners might change their tune and ride out the storm, especially with the prospect of rising home prices on the horizon.

Who Qualifies for Relief?

First and foremost, you must have a second mortgage. That’s a big no-brainer.

On top of that, the mortgage must be owned and serviced by Bank of America, though it technically doesn’t matter who owns the first mortgage.

Bank of America only seems to be offering this assistance to those behind on their mortgage payments, namely second mortgages.

However, there may be cases where borrowers are current on their second mortgages and delinquent on the first, probably because payments on the former are more manageable.

At the moment, only those who receive the letters are eligible, so calling the bank probably won’t get you very far.

But you can still contact the bank to see if you’re eligible for other relief, such as a loan modification via their proprietary program.

What Are the Implications?

Well, because the entire second mortgage is being paid and closed, it will no longer get in the way of any foreclosure proceedings.

So there is a dark side to this potentially, assuming the borrower is in the process of foreclosure and the second mortgage was complicating an otherwise streamlined process.

Bank of America explicitly mentions that the elimination of a second mortgage won’t necessarily stop foreclosure proceedings tied to the first mortgage.

At the same time, the lack of a second mortgage means it won’t stand in the way of a possible loan modification or a short sale, so it goes both ways.

Still, most second mortgages are going for pennies on the dollar in short sale transactions, and with that opt-out business, you have to wonder.

When it comes to credit scores, Bank of America will report the account as paid and closed, meaning it shouldn’t hurt (or necessarily help) the consumer in any way.

This also means Bank of America won’t come after the homeowner for a deficiency judgment, though the forgiveness of debt could trigger a tax liability if an exception isn’t granted.

Ally/GMAC, Chase, Citi, and Wells Fargo are the other lenders involved in the 49-state settlement announced back in February, which doesn’t include Oklahoma.

An FHA loan is a mortgage loan that’s provided under a program from the Federal Housing Agency (FHA), which is a part of the U.S. Department of Housing and Urban Development (HUD). These loans offer prospective homebuyers with lower credit scores and down payments the change to purchase a home. These loans are insured by the FHA, but they are not made by the FHA. Find out more about FHA loan limits, credit requirements, and other factors related to these mortgage loans below.

In This Piece

What Is an FHA Loan?

An FHA loan is a loan insured by the Federal Housing Administration. That doesn’t mean the FHA gives you the loan. You have to go through an approved FHA lender for this type of mortgage. The fact that FHA loans are insured by the federal government reduces some of the risk for lenders. That can make it easier, in some ways, for borrowers to get approved.

Difference Between an FHA Loan and Conventional Mortgage

The most popular—and perhaps most widely known—types of mortgages include conventional home loans, called conventional fixed-rate mortgages, and FHA loans.

Conventional home loans are not insured by a government agency, such as the FHA or the US Department of Veterans Affairs (VA loans). Conventional loans require credit scores of at least 620. In exchange for higher interest rates, you can put down as little as 3% for a conventional home loan. With a lower down payment, you’ll have to pay personal mortgage insurance (PMI) either upfront or monthly for a conventional home loan. And, a conventional loan has a higher interest rate and requires a lower debt-to-income ratio than an FHA loan.

An FHA loan, on the other hand, is insured by the FHA. People with credit scores as low as 580 can qualify, but down payments need to be 3.5% or higher. FHA loans require a mortgage insurance premium be paid upfront and as part of the monthly payment. Interest rates for FHA loans are lower than with a conventional loan. And borrowers can have higher debt-to-income ratios compared to borrowers using a conventional loan.

Get matched with a personal

loan that’s right for you today.

Learn

more

FHA Mortgage Loan

Conventional Mortgage Loan

Required Credit Score

500+ credit score

640+ credit score

Credit History Impact on Qualification

Shorter wait times after negative credit events, such as foreclosure, short sale, bankruptcy and divorce

Longer wait times after negative credit events, though some lenders may be flexible depending on circumstances

Typical Down Payment

As low as 3.5%

As low as 3%, with advantages for a larger down payment

Mortgage Insurance

Requires both a 1.75% upfront premium and 0.45%-1.05% annual premium

Unless you make a 20% down payment, you must buy private mortgage insurance. Usually this is included in the cost of the loan and can be canceled when you have 20% equity or more

Typical Interest Rate

Lower interest rates than a conventional loan for many borrowers

Potentially higher interest rates than an FHA loan, unless you have stellar credit and a large down payment

Required Debt-to-Income Ratio

Higher debt-to-income ratio acceptable

Lower debt-to-income ratio than an FHA loan

Types of FHA Loans

The FHA offers a number of loan programs you might be able to take advantage of:

FHA Loan Limits

How much you can finance with an FHA loan is limited. The exact figures depend on the location of the property and what type of property it is. You can use the US Department of Housing and Urban Development’s FHA mortgage limits tool to find out the numbers for your location.

The FHA mortgage limit floor in 2022 is $420,680, and the ceiling is $970,800.

Individual FHA loans are also limited by the value of the home being purchased. At most, you can get an FHA loan for the total value of the property in question. However, people with lower credit scores may not be able to borrow that much.

FHA Loan Credit Requirements

The minimum credit score requirement for an FHA loan is 500. If your score is less than 500, you can’t be approved for an FHA mortgage loan.

If your score is between 500 and 579, you can get an FHA loan, but you can’t be approved for maximum value. At most, lenders can approve you for up to 90% of the value of the home. That means you’ll need at least 10% as a down payment. It could be more depending on other factors, including your credit history, income, and current expenses.

If you’re buying a home for $200,000 with a low qualifying credit score, then, you might need to pay $20,000 or more as a down payment.

For borrowers with a score of 580 and higher, maximum financing is possible. Typically, that means a down payment of 3.5%. In the case of a $200,000 home, that would equal $7,000.

FHA Loan Documentation Requirements

When you apply for an FHA loan, plan on providing the lender with the following documentation:

Driver’s license

Social Security number

Last paycheck

W-2s for the past two years

Valid tax returns for two years

Bank, investment, and credit card account statements for three months

Signed and dated letters detailing any gift funds used to purchase the home, that must explicitly state that you don’t need to pay back the money.

There are no minimum or maximum salary requirements to qualify for an FHA loan. If your lender requires any additional documentation, they can walk you through the requirements to ensure you have everything in order.

FHA Loan Property Requirements

In addition to your required documentation, there are property requirements as well.

FHA loans can only be used for the primary residence of the borrower.

They cannot be used for second homes.

They cannot be used to buy investment property.

One of the homebuyers must occupy the home within 60 days of closing.

You can only use an FHA loan to buy a multifamily home (up to four units) if you plan to live in one of the units.

An FHA appraisal and inspection are required to determine the fair market value of the home.

They cannot be used to flip a home.

Benefits of FHA Loans

There are many potential benefits for FHA loans:

Lower credit score requirements than conventional mortgages

Fairly competitive interest rates

Lower down payment requirements than many other options

Shorter wait times after negative credit events, such as foreclosure, short sale, and bankruptcy

Certain fees may be lower on an FHA loan, too, particularly when it comes time to closing. The FHA loan program allows for coverage of some of those costs by the seller or another applicable third party.

Disadvantages of an FHA Loan

If your down payment is lower than 20%, the disadvantage you’ll face with an FHA loan is the MIP. Costs for MIP are typically higher than the private mortgage insurance (PMI) borrowers have to pay on conventional loans—especially when you account for the upfront MIP you’ll pay on an FHA loan.

The upfront MIP (UFMIP) fee is 1.75% of the base loan amount, which gets applied regardless of your loan term or LTV ratio. The annual MIP fee, paid in 12 monthly installments, depends on the terms of your loan and your loan-to-value ratio. Annual MIPs range from 0.45% to 1.05% of the amount you’re borrowing and your loan term.

MIP is harder to cancel than PMI on a conventional loan. Conventional mortgage lenders let you out of PMI once you pay your mortgage down to 78% of the home’s value at the time of purchase. Plus, you can ask your lender to cancel your PMI on a conventional loan early if you’ve paid your mortgage down to 80% of that original value ahead of schedule.

And, if you put a smaller down payment on an FHA loan, your mortgage payment will be higher than a conventional loan with a higher down payment.

COVID-19 and FHA Loans

The COVID-19 pandemic did have an impact on FHA loans. For example, HUD notes that while processing for FHA loans continued during the pandemic, changing remote worker situations could lead to delays. FHA loans, which are federally backed, also qualified for forbearance options during the pandemic. This provided some relief to homeowners struggling to pay their mortgages due to income loss. These specific relief measures have expired, but federally backed loans may see other benefits like this that conventional mortgages don’t qualify for.

For future buyers in the years after the COVID-19 pandemic, the biggest impact may be buying power. FHA loans require inspections and have rules about appraisals and prices that conventional loans don’t have. When bidding for homes in a competitive market—where cash buyers and those backed by conventional mortgages are bidding well above asking price—FHA buyers may find it harder to compete.

Should I Consider an FHA Loan?

The FHA loan program is great for borrowers who don’t have a lot of cash on hand for a down payment or need some flexibility when it comes to underwriting. That’s true for first-time home buyers and people buying their second or third homes too. It is also an ideal option for people with lower credit score—lower than the 620 minimum for a conventional loan.

If you do have the resources to make a large down payment and your credit score is in good shape, you may be better off going with a conventional home loan—given that you can skip the PMI.

Of course, regardless of type, you should only get a mortgage you can repay. Learn how much house you can afford as a starting point.

Prepare for Your House Hunt

The best way to arm yourself for house shopping—in any market—is to do your homework. Start by getting a look at your credit report and scores to avoid any surprises. Take time to build or repair your credit where possible before you apply for a mortgage. Then, look at your budget to figure out how much house you can afford.

Then browse options for mortgages to find competitive rates and a short list of lenders you want to work with. FHA loans are great tools, and they can be especially helpful for those with lackluster credit. But make sure you consider all your options before you settle on a loan.

What a difference a few months make in the real estate market. Last summer, home prices were selling on the cheap in many cities across the nation.

Fast forward to spring, and the housing market kind of “sucks.” There’s really no other way to put it.

First off, there’s no inventory. This has been an issue for a while now.

Put simply, there’s just very little out there for an individual or family looking to buy a home, at least in the areas they might want to live.

Sure, there are those properties that have been on the market for months, but there’s a reason they’ve been on the market for months.

And yes, you can probably go to a new community built by a mega home builder and find a house, but it’ll likely be on the fringe of a major city next to empty dirt lots and tractors.

Bad Inventory Rising

Because there is a shortage of homes to buy

Prospective sellers are able to list their duds

Knowing that buyers are becoming increasingly desperate

And may overlook flaws or simply settle as a result of the slim pickings available

Now that the housing market is heating up and the media is (rather obnoxiously) getting on board, inventory is finally rising. Let’s call it an inevitable timing thing.

You see, there is real hope in the housing market. And while hope is good for some, it’s not good for buyers, just sellers who finally see the light after so many years in the dark.

Their real estate agents are giving them the green light to dump their properties while avoiding the lengthy short sale process and nasty credit score ding.

Today, these would-be sellers are able to push the values just that little bit more to sell them as standard sales, instead of going the formerly popular short sale route.

After all, a short sale made sense when there was no hope of getting out unscathed, but now that things are looking up, why not hang on a touch longer and avoid the negative ramifications of selling short?

Unfortunately, this means the individual on the other end is picking up the slack at an inflated price, instead of snagging a deal.

Competition Is Extremely Fierce

Not only are the available homes often less desirable

But the competition for these properties is much higher than normal

Making the housing market a really bad place to be as a buyer

Since no one wants to overpay for a home they don’t even love

Factor in the intense competition and you’ve got a double whammy on your hands.

We’re talking inflating the listing price to make it a standard sale, then receiving multiple bids that often push the final sales price above the original ask.

In other words, today’s buyers are acquiring properties with the future home price appreciation already built in.

And that assumes prices actually do increase – it’s not a foregone conclusion, just a rosy expectation at the moment.

I’m also seeing a lot of the notoriously bad properties rear their ugly heads again. Many of these homes sat on the market for months without a single offer, but now they’re going into escrow in a matter of days.

Something is definitely wrong with this picture. I don’t care how low mortgage rates are…

I’ll Wait for Another Dip

The housing recovery won’t feature home prices that go up in a straight line

Just like the downturn ebbed and flowed despite ultimately declining

There might be windows if you’re patient and keep an eye on things

But do expect home prices to keep on rising, and know that it’s okay to just hold off if you don’t find something you truly love

If I wanted to buy a home, I’d hang on and wait for the temporary madness to come to an end. There’s clearly a bubble mentality in the air again, with everyone and their mother bullish on housing.

Whenever that’s the case, it makes for a rather ominous situation. The increase in inventory involves a ton of previously underwater homes that no one wanted, even at lower prices. Or homes that were taken off market and abruptly thrown back on the MLS.

So why would you buy these same homes today at a significant premium? Because a magazine cover said, “Housing Is Back?”

The economy is still in tatters and things don’t exactly appear bright. If anything, a looming stock market crash seems to be on the horizon.

No, the sky isn’t falling, and housing is indeed on the mend after so many off years. But I do see the current cycle as an unsustainable period of growth that will likely unravel as the year goes on.

It’s going to be a bumpy road to recovery, not just a bottom followed by a surge back to new highs. We’ve seen this optimism in past years, only to watch the wheels fall off time and time again.

If you see something you love, go for it. If you’re worried about the missing the boom, you might want to sit down and reassess the situation.

Read more: Buying a home during a seller’s market.

Several years ago, when the mortgage crisis first materialized, an interest rate reset chart from Credit Suisse began circulating on the Internet.

The picture said more than a thousand words – it essentially foretold disaster for the housing market, and it largely delivered.

Fast forward to 2013, and you’d think we’d be out of the woods, seeing that the chart was from all the way back in 2007.

But there is yet another wave of resets on the horizon, and this time it’s home equity lines of credit (HELOCs).

More 10-Year Draw Periods End in 2014

Most HELOCs are designed so a homeowner can draw from the line of credit for the first 10 years, and then pay back the balance during the following 15 years.

To further accommodate homeowners, the initial 10-year draw period allows for interest-only payments. And people tend to like to make smaller payments.

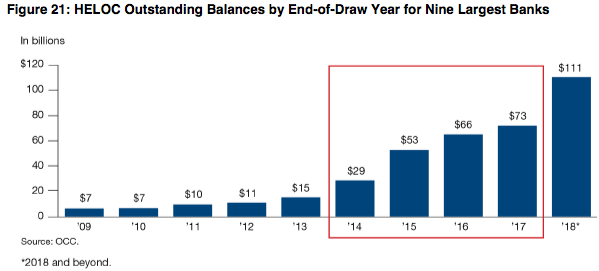

Per a new report from Fitch Ratings titled, “U.S. Banks – Home Equity ReSet Risk Hitting the ReSet Button in 2014,” home equity lending surged in 2004 as credit conditions eased and home prices shot higher.

The screenshot above from the OCC’s Fall 2012 Semiannual Risk Perspective illustrates that (it actually gets worse in later years).

According to Fitch, HELOCs outstanding increased 42% in 2004, and home prices still aren’t back to 2004 levels in many areas of the country.

In other words, most borrowers who still have their HELOCs will have a difficult time refinancing out of them.

And borrowers are essentially hit with two payment increases. For one, they must make principal and interest payments, as opposed to paying interest-only.

Additionally, the amortization period drops to just 15 years. So if you only paid interest for the entire draw period, you’d have a full balance to pay off in just 15 years.

Clearly this could increase monthly mortgage payments significantly, especially for those who took out large HELOCs.

During the boom, there were plenty of homeowners who used HELOCs as second mortgages to finance their hefty purchases. We’re talking $200,000+ loan amounts and higher in California and other pricey states.

For these folks, the payment increase will be nothing to sneeze at.

And Fitch believes individual bank disclosure on the risk of home equity payment resets is “generally inadequate.” So are banks not being upfront about their increased default risk on HELOCs?

It May Not Be That Bad

Fitch noted that only a “handful of rated banks” made disclosures about their home equity loan situation, meaning they could be holding out on the truth.

But there are a number of good things happening that should offset this anticipated payment shock.

For one, a decent amount of these loans were probably already paid off, refinanced, or extinguished when associated properties sold or were lost to foreclosure or short sale.

Secondly, many distressed homeowners have taken advantage of HAMP or HARP and other programs for those with negative equity.

As a result, their total monthly mortgage payments have been greatly reduced, even if a reset is coming on their second mortgage.

In fact, if homeowners are saving several hundred dollars a month on their first mortgages thanks to a massive interest rate reduction, it should be more than enough to offset a payment increase on the HELOC.

If anything, they can take their savings on the first mortgage and apply it to the HELOC, and probably still wind up with money left over.

Additionally, home prices are on the rise, meaning many of these homeowners are getting back above water, or even lowering loan-to-value ratios to levels where a traditional refinance is possible.

Lastly, the prime rate, which dictates what a borrower will pay on a HELOC, is as low as it can go, at just 3.25%.

Before the crisis, the prime rate was as high as 8.25%, so rates on HELOCs are rock bottom as well.

In other words, we probably don’t have too much to worry about collectively, though certain homeowners will definitely be affected.

And that could mean more payment defaults and foreclosures, and more losses for the big banks that hold all these loans.

A new survey from Zillow revealed that prospective home buyers may be “ill-prepared to take out a mortgage,” with basic mortgage questions answered incorrectly nearly one-third of the time.

For example, 34% of prospective buyers indicated that they weren’t aware you could get a mortgage with a down payment of less than five percent.

Zillow countered this myth by noting that loan requests with down payments between 3.5% and 5% have risen 570% over the past two years in the Zillow Mortgage Marketplace.

There are indeed options for those putting down less than five percent, including FHA loans, which only require 3.5% if your credit score is 580 or higher, and also specialty programs, such as Fannie Mae Homepath, which requires just 3% down.

Of course, with the housing market white-hot these days, you’ll be hard pressed to get your offer accepted if you’re only able to put down five percent or less.

A large down payment can separate you from the crowd if there are multiple offers, so it’s not always wise to put down as little as possible.

At the same time, a low down payment can raise your mortgage payment in three different ways, making life more difficult assuming you land the house.

Zillow also found that a quarter (26%) of buyers believe they must close their loan with the bank that pre-approved them. Again, not true, regardless of the scare tactics employed.

Often, a seller will have a preferred lender that they want you to get pre-approved with, but you’re under no obligation to use them. However, getting the pre-approval is a sign of good faith if you’re serious about getting your offer accepted. You can switch lenders after the fact…

24% Believe Best Mortgage Rates Are With Banks

Meanwhile, roughly a quarter of respondents looking to buy indicated to Zillow that the best mortgage rates and fees can be found with banks they currently do business with.

Again, this isn’t necessarily true, though it could be. Your bank may or may not have the best deal, and the only way you’ll know for sure is to shop around.

Most consumers only bother to obtain a single mortgage quote, which can result in thousands of lost dollars over the years.

Learn more about effective mortgage rate shopping to ensure you get your hands on the rate you deserve.

Even those who already have a mortgage lack basic understanding. For example, one in five of these respondents didn’t know you could refinance if underwater.

If you’re one of these people, there is a program called HARP that allows borrowers to refinance, regardless of loan-to-value ratio. Homeowners with FHA loans can also execute a streamline refinance without LTV constraints.

This means there could be millions of untapped HARP refinances, which is good news for loan originators bracing for a slowdown in refinance activity this year.

Finally, about half (47%) of current homeowners surveyed believe you must wait a year between refinancing.

Once again, this is a myth – you can pretty much serially refinance if you want to, though some loans contain prepayment penalties that will cost borrowers.

And it doesn’t always make sense to refinance. Make sure you do the math first to determine if it’ll actually save you some money.

[Refinance rule of thumb.]

After all, you won’t want to spend a ton of money refinancing, only to sell your property a year or two later. If you’re serious about paying off the mortgage, it may make more sense to refinance to a lower rate.

For those who are considering selling in the near future, refinancing could be a losing proposition.

More survey takeaways:

– 34% of prospective home buyers don’t know what the term APR means – 50% of prospective home buyers don’t know mortgage rates change daily – 31% of current homeowners wrongly believe you must wait seven years after short sale or foreclosure to buy again

Don’t Blame Consumers for Mortgage Confusion

While some of these stats may seem alarming, you can’t really blame consumers for their naïve understanding of mortgages.

As I always say, mortgages are very complicated, even for the experts. Additionally, the landscape is always changing, so what’s true today may be wrong tomorrow.

If guidelines were set in stone, it’d be a lot easier to navigate the mortgage market, but they’re not. Rules also vary by bank, thanks to lender overlays and product niche.

[See: Why every lender will disappoint you for more on that.]

The latest mortgage crisis changed a lot of things, and there are even more changes on the horizon, such as the Ability-to-Repay and Qualified Mortgage definitions.

For these reasons, you really need to “put in the time” when going about getting your mortgage. Don’t rush it.

It’s probably one the biggest financial decisions you can make, so do your homework and shop around. Or simply regret not doing so after the fact.

In a bid to perhaps stay relevant, though in the FHA’s own words, to continue “its commitment to fully evaluate borrowers who have experienced periods of financial difficulty due to extenuating circumstances,” borrowers may now be eligible for an FHA loan just one year after experiencing a short sale, foreclosure, or even a bankruptcy.

The news came via a new mortgagee letter (13-26) posted on HUD’s website Friday.

While it sounds completely irresponsible and crazy, especially seeing that we’re just a year or two out of the worst mortgage crisis in recent history, they do have some standards in place to ensure not just anyone can get a mortgage again.

Did You Experience an “Economic Event?”

In order to get approved for an FHA loan just one year after experiencing such a massive credit hit, you must prove it was due to an “Economic Event,” otherwise known as unemployment or a “severe” reduction in income.

Of course, by severe reduction they’re only talking about a minimum 20% reduction in household income for a period of at least six months.

The last time I checked, it’s pretty common for individuals to see their income fluctuate like that. And the FHA is even allowing those with seasonal or part-time employment to qualify under these new rules.

However, there are a few more checks and balances. The lender must analyze the borrower’s credit to determine that they were a sound borrower before the Economic Event took place, and that their credit only went downhill after the incident.

Additionally, borrowers must re-establish “Satisfactory Credit” for a minimum of 12 months prior to receiving their FHA loan.

In other words, your credit report should be clear of any late housing or installment payments during the past 12 months, or any major derogatory events on revolving lines of credit.

Additionally, a year must have passed since the date of the foreclosure, deed-in-lieu, short sale, or bankruptcy.

[Getting a mortgage after a short sale with no waiting period.]

Lastly, participants in this initiative must receive homeownership counseling or a combination of homeownership education and counseling.

The minimum requirement is a single hour of one-on-one counseling from a HUD-approved housing counseling agency, and they must address the cause of the Economic Event and steps taken to overcome and avoid reoccurrence.

It must be completed at least 30 days before submitting a loan application, but no more than six months prior. Counseling can be conducted in person, over the phone, or even online.

To sum it up, in order to qualify you must:

[checklist]

Prove the negative credit event was the result of a loss of employment or significant loss of income

Prove that you have recovered and re-established satisfactory credit

Apply at least 12 months after the negative event took place

Complete housing counseling to avoid similar missteps in the future

[/checklist]

The loan must also meet all other applicable FHA eligibility and policy criteria.

So all in all it appears to be a pretty darn accommodating new rule to help former homeowners qualify for a mortgage.

Interestingly, the FHA has seen its market share take a hit thanks to new rules aimed at shoring up its reserves, such as requiring mortgage insurance for the life of the loan and increasing annual insurance premiums.

But I suppose the FHA’s original mission is to serve the underserved, so it makes sense that they would be the ones to allow this type of loan program.

The rule change applies to FHA loans with case numbers assigned on or after August 15, 2013 through September 30, 2016. It works for purchase money mortgages in all FHA programs aside from Home Equity Conversion Mortgages (reverse mortgages).

If you’re interested to see if you qualify, find a lender that specializes in FHA loans so they can guide you through the process and increase your odds of approval. You’ll want to submit an airtight application to avoid any hiccups.

One major issue that has plagued homeowners over the past few years has been a lack of equity, making it impossible to sell without a short sale.

Worse than that, many lacking equity have decided to simply hand in the keys and walk away, a testament to their desperation.

But thanks to recent home price gains nationwide, more and more borrowers are acquiring healthy amounts of equity, plenty enough to throw up a standard sale on the MLS if they’d like.

A new graphic from RealtyTrac illustrates this equity boom, and Honolulu is tops when it comes to the “equity rich,” despite being surrounded by water.

By equity rich, they mean having 50% or more equity in the home. Put another way, having a LTV ratio below 50%, which is quite favorable in the mortgage world.

As you can see, 36% of homes (62,891 total) in the Hawaiian capital are rich in equity, meaning these households could all sell whenever they want to without any trouble (barring the circus that is the mortgage industry messing things up).

San Jose, CA has the second largest percentage of equity rich homes at 35% (131,622 homes), followed by Poughkeepsie, NY at 30% (25,188 homes).

In terms of totals, California has the largest number of equity rich homes at 597,436, or 26% of homes.

It’s followed by New York, NY with 578,785 homes (27%) and San Francisco with 282,793 (29%).

Unsurprisingly, most of these metropolitan areas are quite affluent, and there are probably plenty of cash buyers in the mix, including scores of investors.

They’re also established cities, meaning many homeowners have probably lived in the homes a lot longer than in newer cities such as Las Vegas or Phoenix.

Many Homes in Foreclosure Now Have Equity Too

RealtyTrac also took a look at homes in the process of foreclosure that now have equity thanks to those recent price gains.

Somewhat amazingly, 72% of foreclosures (1,541 homes) in Pittsburgh have some level of equity.

It is followed by Poughkeepsie, NY at 71% (1,065 homes) and Honolulu, HI at 69% (451 homes).

The largest number of homes in foreclosure that have positive equity can be found in Dallas, Texas, likely because of their strict lending rules that limit cash out to low LTVs.

This sheds some light on the causes of the crisis as well, and backs up a study by Fed researcher Steven Laufer that blamed cash out loans for the large number of defaults and eventual foreclosures.

The Data Means More Inventory Is in the Pipeline

What it all means is that there is going to be a lot more housing inventory now and in the near future, assuming homeowners finally pull the trigger.

Apparently a good chunk of them are waiting for prices to rise further before selling, but you’ve got to believe that more and more will take the plunge as prices continue to rise and higher rates thin the eligible pool of buyers.

Additionally, because more homeowners are gaining equity, there will be fewer and fewer short sales and foreclosures. That too should bolster home prices, as distressed sales drag down prices.

These sellers may also become subsequent buyers sooner if they can avoid a fire sale and keep their credit clean, all of which should help the housing market recover.

The only concern is an eventual tipping point where there is too much overpriced inventory. But hopefully that is some years out.

It’s not quite subprime all over again, but now that higher mortgage rates seem to be an absolute certainty, banks and lenders are looking for new ways to drum up flagging business.

One such method popular during any slowdown in production is to ease underwriting guidelines, such as credit score and down payment requirements, loan-to-value maximums, and so on.

And now that interest rates on home loans are more than a full percentage point higher than they were a couple of months ago, this phenomenon is beginning to take shape.

Eliminating Overlays to Stay Competitive

Let’s face it; there are far fewer loans out there now that refinancing volume is beginning to tank.

While purchase activity is expected to take charge as soon as the fourth quarter of this year, it still won’t be enough to make up for the shortfall, which explains all those layoffs.

As a result, lenders are effectively being forced to ease guidelines to stay competitive and gain (or even retain) market share.

Yesterday, private mortgage insurer Genworth said it expanded “its Simply UnderwriteSM guidelines to eliminate nearly all overlays and ensure ease of use for customers that deliver loans using the automated underwriting systems (AUS) of the government-sponsored enterprises (GSEs).”

So going forward, mortgages with a LTV ratio as high as 97% and a FICO score as low as 620 that are accepted by the GSEs are also likely to be approved for PMI with Genworth.

For the record, 620 is the subprime cutoff, but a 620 FICO score coupled with only three percent down is probably the definition of layered risk, which isn’t a good thing.

On Monday, non-bank originator Amerisave also announced that it was eliminating conventional overlays, meaning they’ll now approve whatever Fannie Mae allows, without any extra fees.

Before lending began to ease, most banks imposed overlays on top of what Fannie and Freddie (and the FHA) deemed deliverable.

In effect, it meant guidelines weren’t as loose as they could have been, largely because banks were concerned with credit quality and buybacks. But now that lending has essentially dried up, it seems the spigot has opened once again.

It’s a Slippery Slope

Earlier this summer, the top mortgage lender in the nation also got more lax. Wells Fargo upped its maximum LTV for jumbo loans to 85% from 80%, which is yet another sign that we’re inching back toward high-risk home loan lending.

While that might sound conservative, Wells has traditionally kept things a little tighter than the competition.

Still, that’s nothing compared to what some of the pure refinance shops are getting into, now that their business virtually disappeared overnight.

CashCall is offering 125% second mortgages, which were popular during the boom. Yes, loans for more than the value of the property.

And the FHA now seems to be just fine with borrowers applying for a loan just one year after short sale, foreclosure, or bankruptcy.

Of course, it remains to be seen whether lenders will actually get on-board with that, or if they’ll throw in their own overlays.

But it’s clear that lending is beginning to loosen up in a hurry, which some might argue is overdue, where others might fear another collapse.