housing demand

Apache is functioning normally

Purchase application data

Last year, when mortgage rates fell from 7.37% to 5.99%, we got three good months of positive purchase application data until the first week of February before mortgage rates started to run higher from 6%-8%. We need to focus on the data weekly to see if lower mortgage rates can once again spur purchase applications because we are working from such historically low levels that it doesn’t take much to move the needle.

So far, we have had back-to-back positive prints, and the year-over-year decline is at the lowest level all year long. However, this is due to extremely easy year-over-year comps. Let’s see how this looks in the critical time from the second week of January to the first week of May 2024. Remember, application data looks out 30-90 days before it hits the sales data.

Purchase application data was up 3% versus last week, making the year-to-date count 20 positive prints, 23 negative prints, and one flat week.

Mortgage rates and the 10-year yield

The 10-year yield ranged from a high of 4.69% to a low of 4.38% last week, and mortgage rates went from a high of 7.58% to a low of 7.36%. More importantly, the CPI data came in light, and it looks like that might have been the final nail in the coffin for the Federal Reserve in terms of raising rates as the growth rate of inflation has cooled down enough that the market is now pricing in a few rate cuts in 2023.

Still, the 10-year yield and mortgage rates are higher today than last year, and the inflation growth rate is lower than the peak inflation growth rate in 2022. I talked about how much lower mortgage rates can go from here in this recent podcast. As I have stressed, if the market believes the Fed is done with rate hikes, history says the next big move is lower bond yields and mortgage rates.

Weekly housing inventory data

As someone who believes that housing inventory will grow with higher rates, I was hopeful that when mortgage rates got above 7.25% we would have a few weeks this year of 11,000-17,000 growth, which isn’t a lot. I failed 100% of the time so far.

We would usually be in a seasonal decline by now, but inventory growth has recently picked up due to higher rates. So, higher rates did their thing, just not big enough for my taste. Mortgage rates have fallen, so this is something to consider next year if they keep falling because that traditionally means flat to lower inventory data, assuming that the economy is still expanding.

Last year, according to Altos Research, the seasonal peak for housing inventory was Oct. 28.

- Weekly inventory change (Nov.10-Nov. 17): Inventory rose from 566,941 to 569,898

- Same week last year (Nov. 11-Nov. 18): Inventory fell from 572,347 to 569,571

- The inventory bottom for 2022 was 240,194

- The inventory peak for 2023 so far is 569,898

- For context, active listings for this week in 2015 were 1,120,115

The one positive inventory story for 2023 is that new listing data — while trending at the lowest levels ever in history — didn’t create a brand new low level, no matter how high mortgage rates rose. Even though we saw a noticeable decline week to week, new listings are positive year over year, still trending at the lowest levels ever. I talked about how new listings data is forming a bottom on CNBC recently.

Traditionally, one-third of all homes take price cuts before they sell. When mortgage rates rise, and demand decreases, the percentage of homes with price cuts usually increases. This is why it’s so crazy that this year, even with higher home prices and rates recently, we haven’t been able to catch up to price cuts in 2022 when home prices were falling month to month.

Even as mortgage rates got to 8%, we have consistently been 4% below last year’s levels of price cuts. If mortgage rates fall more over the next six months, this data line will be exciting as we head into Spring 2024.

- 2023: 39%

- 2022: 43%

- 2021: 28%

The week ahead: Leading Economic Index and existing home sales

This week is a holiday with Thanksgiving, but we have some important economic data coming up: the leading economic index and the existing home sales report. We should see a pick up in the monthly supply of homes with mortgage rates rising as much as it did for this report. People will wait to see how Black Friday sales perform, but Black Friday doesn’t mean the same thing it did 30 years ago. We will see if the bond market and mortgage rates are volatile in a holiday-light trading week.

Source: housingwire.com

Apache is functioning normally

On the construction side, homebuilders as well as land developers found it hard to finance projects because of high short-term interest rates. On the consumer side, a large number of prospective buyers sat on the sidelines as housing affordability worsened.

Shelter remained the largest contributor to inflation in October, according to the CPI report. However, the rate of housing inflation is steadily falling and there are high hopes that interest rates will fall in 2024.

“While builder sentiment was down again in November, recent macroeconomic data point to improving conditions for home construction in the coming months,” NAHB Chief Economist Robert Dietz said in a statement.

“In particular, the 10-year Treasury rate moved back to the 4.5% range for the first time since late September, which will help bring mortgage rates close to or below 7.5%. Given the lack of existing home inventory, somewhat lower mortgage rates will price-in housing demand and likely set the stage for improved builder views of market conditions in December.”

NAHB forecasts approximately a 5% increase for single-family housing starts in 2024 as financial conditions ease.

Homebuilders continued to make adjustments to boost their sales

According to the survey, 36% of builders cut home prices, up from 32% in the previous two months. It was the highest share of builders cutting prices recorded in one year.

According to the NAHB, the average price discount remained at 6%, unchanged from the previous month.

All three major HMI indices posted declines in November. Homebuilders’ gauge of current sales conditions fell to 40. The gauge measuring traffic of prospective buyers declined to 21. And the component charting sales expectations over the next six months fell to 39.

The three-month moving averages for HMI all declined across the four major regions in November. The Northeast fell one point to 49; the Midwest dropped three points to 36; the South fell seven points to 42; and the West posted a six-point decline to 35.

Source: housingwire.com

Apache is functioning normally

Don’t miss out on Dallas.

The Dallas housing market is a nuanced picture of competition and change, mirroring the complex economic forces at play. As the latest figures roll in, analysts are keenly observing the subtle shifts that could signal the future trajectory of property values and market dynamics in one of Texas’ top cities.

Home prices in Dallas

In recent months, the Dallas housing market has been defined by healthy competition. The median home price has risen to an impressive $420,000, a 6.3% year-over-year increase, signaling sustained growth in property values. Each Dallas home, on average, garners two offers, with a median time of 33 days from listing to contract — a slight increase from the previous year.

Competition in the Dallas housing market

The Dallas housing market’s competitiveness is more than a matter of bidding wars; it’s reflected in the numbers across the board. With a 61 on the Redfin Compete Score™, the latest trends point to a market that’s competitive but not cutthroat. Dallas homes are being sold at a slight discount, typically around 2% below the listed price, with the sale-to-list price ratio sitting at 97.9%. However, some homes defy this trend, fetching around 1% above list price and transitioning to pending sales in a brisk 15 days.

Migration patterns to and from Dallas

These transactions take place against the backdrop of a dynamic migration pattern. The Dallas housing market is influenced not only by internal factors but also by the ebb and flow of people. While a fifth of the residents are exploring housing options outside the metro area, the vast majority remain committed to the Dallas market. The city has become a prime destination for buyers from coastal cities like Los Angeles and San Francisco, as well as New York, adding an influx to the local housing demand.

Environmental effects on the Dallas housing market

Environmental considerations are also shaping the Dallas housing market. Buyers are increasingly aware of the risks posed by natural occurrences. The average properties in Dallas face moderate flood risks and wildfire threats. On the other hand, wind and heat present major concerns, with nearly all properties in Dallas at risk over the next three decades.

Getting around in Dallas

The walkability, bikeability, and transit options in Dallas score 46, 49 and 39, respectively, out of 100. These figures highlight the necessity of a car for most residents, despite some available public transportation options and the developing infrastructure for cyclists.

Settle down in Dallas

The Dallas housing market remains a competitive arena where timing, price and environmental factors play crucial roles. The city’s real estate scene is a confluence of migration trends, market competition and infrastructure capabilities, all of which contribute to a market that is as challenging as it is rewarding for those navigating its waters.

Renting in Dallas

Shifting focus to the rental market, there are plenty of attractive options in Dallas for those not looking to buy. As of the latest figures, the rental market in Dallas presents a range of pricing, reflecting the variety and scale of the city’s neighborhoods and housing options.

Average rent in Dallas

The average rent for a studio in Dallas stands at $1,477, marking a 4% increase over the past year — evidence of a steady demand for these compact living spaces. For those seeking more room, one-bedroom apartments have seen a decrease in average rent, now at $1,371, which is a 5% reduction from the previous year.

This suggests a shift in the market dynamics, possibly driven by changing preferences or a supply adjustment. The average rent for two-bedroom apartments has also decreased by 4%, positioning the current rate at $1,862.

Image source: Rent./Sagemont

Dallas rent ranges

The rental ranges in Dallas illustrate a high-end market dominance, with nearly half of the apartments falling into the $2,101 and above category. This indicates a substantial segment of the market catering to more affluent tenants or those seeking premium amenities. Meanwhile, apartments priced between $1,501 and $2,100 account for 27% of the market, providing options for those with moderate to high rental budgets.

At the more affordable end of the spectrum, 18% of the apartments are priced between $1,001 and $1,500, aligning with the national median for similar urban settings. Notably absent are options below $700, which highlights a pressing shortage of low-end rental options in the Dallas market, a challenge for budget-conscious renters.

Your Dallas apartment awaits

These figures underscore a rental market as layered and dynamic as the city itself, with a range of options catering to different lifestyles and budgets. As Dallas continues to attract new residents from around the country and across the globe, the rental market is likely to continue reflecting the broader trends of the housing sector at large, with adjustments in pricing and availability that mirror the always-changing Dallas housing market.

Ready to settle down in your dream Dallas apartment? You’re only a few clicks away.

Source: rent.com

Apache is functioning normally

The trough for the mortgage origination market is nearing an end point and 2024 is shaping up to be a better year for the industry, economists of the the Mortgage Bankers Association (MBA) said at the 2023 Annual Convention & Expo in Philadelphia, Pennsylvania.

The MBA doesn’t expect the Federal Reserve to hike interest rates further this year as real rates – which are inflation-adjusted– are 2%.

“They’re already at a place where if they do nothing, and inflation holds or falls further from here, they’re going to be slowing the rate of growth and the cumulative impact of the rate increases they’ve already made are not fully felt yet,” said Mike Fratantoni, MBA’s chief economist and senior vice president for research and industry technology.

Based on the cautious messages from even the hawkish Fed members, Fratantoni projected that the central bank will “definitely not be going to hike in November, a small chance that they would come back in December if these numbers turn around.”

The MBA’s view is that the Fed will cut interest rates three times in 2024 and inflation may come down a bit faster as a result.

“I’m pretty confident that if this rate path precedes as we’re expecting, this is the bottom. 2023 is going to be the low-volume (mortgage origination volume) year for this cycle. So after falling 50% from 2021 to 2022, our current estimate has it falling almost 30% from 2022 to 2023. But then a rebound in 2024 — up 19%,” Fratantoni said.

Purchase originations are forecast to increase 11% to $1.47 trillion next year.

In terms of units, the MBA expects about 5.2 million units in the total number of loans originated in 2024, up from this year’s expected 4.4 million.

“It’s still a pretty challenging environment relative to if you look back historically, this is close to where we were in 2014. Maybe just below where we were in 2018 — still a challenging year for the industry,” Joel Kan, vice president and deputy chief economist of MBA, said.

Mortgage rates will drop, but challenges linger

MBA’s baseline forecast is for mortgage rates to end 2024 at 6.1% and reach 5.5% at the end of 2025 as Treasury rates decline and as the spread narrows.

The historically high spreads between mortgage rates and the 10-year Treasury yield – which was triggered by the uncertainty about monetary policy and the direction of quantitative tightening – will resolve in a “favorable direction over the course of the next six to 12 months,” Fratantoni added.

The MBA raised expectations of a mild recession in the first half of 2024 due to the combination of the cumulative impact of the rate hikes, the banking system tightening down on all forms of credit and the slow global environment all leading to a slowdown in the US.

The unemployment rate is expected to rise to 5% by the end of 2024 from the current rate of 3.8%. Inflation, in return, will gradually decline towards the Fed’s 2% target by the middle of 2024, Fratantoni said.

As mortgage rates come down to the 6%-range in 2024 and the 5% range in 2025, borrowers will see less of a trade-off in moving, Kan projected.

Kan added: “I think that’s when you’re going to see more inventory free up, that’s when we’re going to see more of these housing transactions able to take place.”

The MBA anticipated first-time homebuyers will account for a large portion of housing demand over the next few years, given the largest age cohort entering its prime homeownership ages.

“There will still be challenges, as median purchase and interest payments remain high, for-sale inventory is scarce, particularly for entry-level homes, and credit availability is low,” Kan said.

A couple more painful quarters ahead

The mortgage origination market for banks and independent mortgage banks was painful given that they all saw five consecutive quarters of net production losses.

While production losses were less severe in Q2 2023 from the previous two quarters, lenders are projected to have a few more painful quarters until the end of the spring of 2024 – mainly due to the traditionally slow winter season, Marina Walsh, CMB and vice president of industry analysis, anticipated.

For lenders, excess capacity continues to be a challenge with low productivity levels and high expenses per loan.

“Lenders have reduced their head counts and gross expenses, but the record-low volume is a primary driver of these escalating per-loan costs,” Walsh said.

The MBA previously estimated that a 30% decrease in the mortgage industry employment from peak to trough will need to occur, given the decrease in production volume.

The MBA estimated that the industry is roughly two-thirds of the way there from the previously mentioned 30% overcapacity in the industry.

Mortgage industry employment dropped 20% in 2023 from the peak in 2021 and the number of active MLOs for state-licensed companies dropped 29% from the same period, according to the MBA.

Source: housingwire.com

Apache is functioning normally

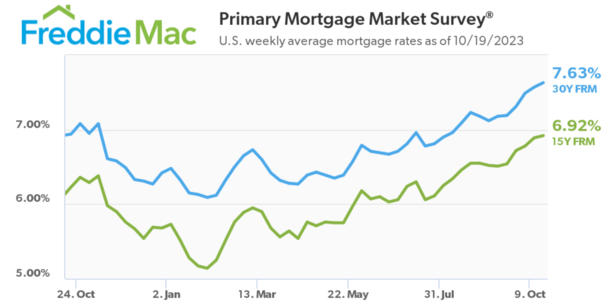

If you thought 8% mortgage rates were bad, what about 9% mortgage rates?

What was once unthinkable is now not so hard to believe, with 30-year fixed mortgage rates climbing ever higher.

At last glance, the 30-year was priced at 7.63%, per Freddie Mac’s lagging weekly survey.

But other estimates have been higher, including MND’s daily index that put the 30-year at a ripe 8.03%.

And today I even saw someone calling for 12% mortgage rates by Q2 2024. Yikes!

Are 9% Mortgage Rates Next?

I’ve already written about 7% mortgage rates and 8% mortgage rates for that matter, at the time wondering if and when they’d arrive.

Now here I am writing about 9% mortgage rates, which is worrisome given those past fears coming to fruition.

However, that doesn’t necessarily mean we keep going higher from here, nor do we climb another 1% higher.

If you look at mortgage rates over the past year, they’ve gone up, but not by an enormous amount.

Take Freddie Mac’s weekly survey data, which pegged the 30-year fixed at 6.48% to begin 2023.

Today, they said the 30-year fixed averaged 7.63%, which represents an increase of 1.15%.

Yes, it’s higher. And yes, it’s further eroding home buyer affordability and hurting housing demand. But an increase of just over 1% over more than 10 months isn’t massive movement.

Consider the year 2022, when the 30-year kicked off January at 3.22% and ended with a bang at 6.42% in December.

Mortgage rates literally almost doubled during 2022 (short two basis points), while they’ve only risen 17% so far in 2023.

So the rate of ascent has slowed tremendously, if there is but one silver lining here (the other actually being that more high-rate loans being originated will present opportunity later).

Anyway, because mortgage rates are now a lot higher, the percentage gains pale in comparison. And there’s the question of rates nearing their peak.

I’m not convinced we go to 9%, at least by Freddie Mac’s measure, or even MND’s.

Sure, some loan scenarios with layered risk (low FICO score, high LTV, investment property, etc.) may already be at 9%. Or close.

But for the average home loan scenario, I don’t know if we go that high. If anything, 8% rates could signal a turning point.

The 21st Century High for Mortgage Rates Is 8.64% Per Freddie Mac

While we’re on the subject, I’d like the point out that the 21st century high for the 30-year fixed is 8.64%, per Freddie Mac data.

And it took place during the week of May 19th, 2000. So we are not far off from hitting a new high for this century, assuming rates continue their upward trajectory.

But until then, I’d be wary of anyone saying rates haven’t been this high since the 1990s, or something to that effect.

Also, recall that rates only increased 1.15% so far in 2023. They’d still need to rise another one percent by Freddie’s measure to get there.

Maybe that happens, maybe it doesn’t. Either way, there’s still a ways to go to reach that point.

Do We Need Higher Rates, or Just More Time to Let Them Sink In?

Everyone seems to be obsessed with higher and higher interest rates. As if pushing them ever higher will fix inflation.

But do they actually need to keep climbing into the stratosphere, or are we simply being impatient?

Perhaps they just need time to do their thing, which is basically what Fed chair Jerome Powell echoed today.

It coincides with the higher for longer mantra, that interest rates will need to stay at elevated levels longer than expected.

That could be enough to slow demand, consumer spending, home price appreciation, new hiring, etc.

They don’t necessarily need to keep going up from here. And that’s perhaps why the Fed is taking a wait and see approach with their own policy rate.

Of course, the Fed doesn’t control mortgage rates, but their own fed funds rate can act as a signal for the direction of the economy, and long-term rates such as 30-year fixed mortgage rates.

The fact that they’ve essentially stopped hiking should be a somewhat bullish sign that rates are sufficiently restrictive.

Powell also noted that the bond market might be turning its attention to the federal deficit and increased government spending, for which a couple wars might be to blame.

So there might be less importance to look at what the Fed is up to as there was earlier in the year.

The 10-Year Bond Yield Is About to Hit 5%

Meanwhile, the 10-year bond yield, which has been a fairly reliable indicator of 30-year mortgage rates, nearly hit 5% today.

At last glance, it was literally 4.99%, with apparent resistance at slightly higher levels. Some believe it could be a tipping point where bond buyers see opportunity.

If that’s true and yields calm down, chances are mortgage rates can too. At the same time, the mortgage rate spread between the 10-year yield is double its normal.

Usually around 170 basis points, it has widened to over 300 bps, meaning 5% yield plus that spread puts the 30-year fixed at roughly 8%.

During normal times, the math puts the 30-year fixed at about 6.75%. That alone would go a long way in fixing mortgage rates.

But until mortgage-backed securities (MBS) investors get more certainty, those spreads will remain wide.

Especially when you consider the prepayment risk if rates go down a lot and everyone refinances their 7-8% mortgages.

The takeaway for me at this juncture is that mortgage rates probably will continue rising from here, but maybe only gradually and by much smaller amounts.

That’s the good news. The bad news is they might have to linger at these high levels for longer than anticipated.

Ultimately, I really don’t want to write an article about 10% mortgage rates anytime soon.

Source: thetruthaboutmortgage.com

Apache is functioning normally

If you don’t believe mortgage rates and home prices can fall together, just look at what home prices have done in the face of 7% mortgage rates.

Despite the 30-year fixed surging from sub-3% levels to near-8% levels in less than two years, home prices hit fresh all-time highs.

So why is it so difficult to imagine the opposite scenario, where both interest rates and property values fall in tandem?

It seems the human mind wants there to be an inverse relationship between rates and prices when there often is not.

The good news is it’s possible that both rates and prices moderate from here, ushering in a better level of housing affordability.

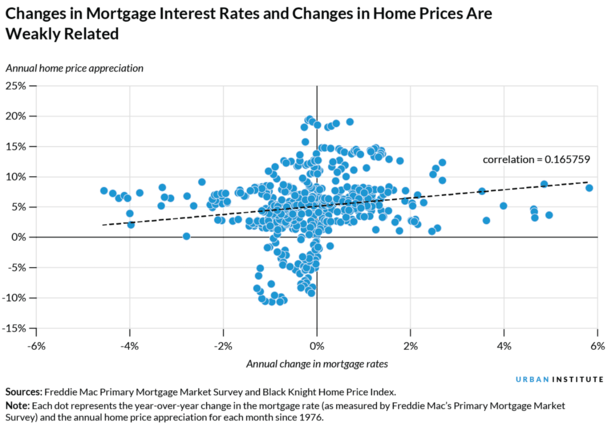

Home Prices and Mortgage Rates Don’t Have Much of a Relationship

The Urban Institute wrote an article last year about the relationship between home prices and interest rates when mortgage rates were rapidly ascending.

They noted that since 1976, there has been “a positive but weak relationship” between the two.

In other words, higher mortgage rates are often accompanied by higher home price appreciation, though this tendency isn’t robust.

Still, it defies the logic many housing bears and everyday humans possess, where they assume higher mortgage rates must equate to lower home prices.

After all, if it becomes more expensive to purchase a home, the price must come down. That’s their argument at least.

But when you look at other necessary items (shelter also being a necessity), people don’t stop buying them because the cost goes up.

And one also needs to consider why mortgage interest rates are high to begin with. Often, interest rates are high because the economy is running hot.

This means there are more consumers out there making more money, which ostensibly means more of them can afford to buy expensive houses.

One other factor to consider is all-cash buyers – a large percentage of home buyers forgo mortgages to get the deal done, especially investors.

So while higher interest rates might affect the average home buyer, they don’t affect everyone.

Home Prices and Inflation Have a Strong Positive Relationship

While higher mortgage rates and home price appreciation have a weak, but still positive relationship, inflation and home price appreciation have a strong one.

That is to say that a higher rate of inflation is associated with higher home price appreciation.

And this association is significantly stronger than the relationship between mortgage rates and home prices.

Inflation has been front and center for the past couple years, and the Fed has been actively fighting it via 11 fed funds rate hikes since early 2022.

At the same time, home prices haven’t fallen, though the rate of appreciation has. Still, when you consider the 30-year fixed more than doubling in such a short time span, you’d expect housing market carnage.

Instead, we’ve seen home prices hit new all-time highs. Last week, the FHFA reported that home prices were up 0.8% in July from a month earlier, and up 4.6% year-over-year.

While that might sound too good to be true, consider that high interest rates are often correlated with periods of strong economic growth, low unemployment, rising wages, and high inflation.

Put another way, when the economy is hot, home prices tend to rise because more people have money and jobs to support mortgage payments, even if they grow larger.

This means housing demand can increase or at least remain steady, even if affordability erodes over time.

Housing Affordability at Its Worst Since 1984

Of course, affordability has worsened significantly of late because both rates and prices have continued to rise, pushing the national payment-to-income ratio to its highest level since 1984.

Per Black Knight, it takes a $2,423 principal and interest payment to purchase the median-priced home with 20% down and a 30-year fixed mortgage.

This is up 91% from $1,155 just two years ago, when the Fed ended Quantitative Easing (QE) and began their campaign known as Quantitative Tightening (QT).

Clearly this has slowed home price appreciation, which had been running at a double-digit clip. But as noted, prices keep on rising.

Nominal Home Prices Are Sticky and Rarely Fall

The Urban Institute noted that mortgage rates have mostly just declined since 1976.

There have only been a few periods when rates increased more than 1.5 percentage points year-over-year.

However, rates did rise rapidly from September 1979 to March 1982 (remember those 1980s mortgage rates) and from September 1994 to February 1995.

This caused the rate of home price appreciation to slow quickly, similar to what we saw lately.

During that 1979 to 1982 mortgage rate rise, home price appreciation decelerated from 12.9% to just 1.1%.

And from September 1994 to February 1995, it slowed from 3.2% to 2.6%.

During each of these time periods, real home price appreciation (adjusted for inflation) went negative, but nominal home prices only went negative once a recession was under way.

In other words, you need the economy to fall apart if you want home prices to come down. And guess what could also come down at the same time?

What About Falling Home Prices Combined with Lower Mortgage Rates?

So we’ve discussed how home prices and mortgage rates can rise together, though the relationship isn’t a strong one.

But that a robust economy tends to lift home prices higher, as has been the case over the past many years.

If that’s true, can’t the opposite also be correct? Can’t mortgage rates and home prices fall at the same time, perhaps because of disinflation and a cooling economy?

The answer is yes they can. If and when the economy takes a turn for the worse, the Fed could pivot and begin cutting its own policy rate.

At the same time, mortgage rates could retreat from recent highs and make their way lower as well.

And home prices could also begin to fall as a recession sets in, resulting in job losses, pay cuts, higher unemployment, and lower housing demand.

This counters the notion that mortgage rates back in the 4-5% would set off another housing market frenzy filled with bidding wars and rapidly appreciating prices.

Simply put, if home prices and mortgage rates can rise together, they can also fall together.

Ideally, we see moderation on both fronts, with home prices maybe pulling back from recent highs, at least on a real, inflation-adjusted basis, while mortgage rates also ease.

This could help to tackle the affordability issues currently plaguing the housing market.

Just remember though that the other big problem is supply. There simply aren’t enough homes for sale, and as we all know, scarcity leads to higher prices.

Source: thetruthaboutmortgage.com

Apache is functioning normally

BIRMINGHAM, Ala. (WBRC) – Housing demand is cooling off as mortgage rates hit the highest levels seen in over two decades. Many may be wondering whether they should wait to buy a home.

Bennie Waller, a real estate professor with the University of Alabama, says you might not want to hold your breath for those rates to come down.

As of Thursday, the 30-year rate averaged 7.31%, the highest rates have been. For context, just one year ago the average was about 5.6%.

Waller says first-time homebuyers or those looking to trade up can’t get the product they need because of interest rates.

I asked Waller whether buyers should wait if possible. He says there might not be much use in that.

“If you think that it’s the home you want, if you’re committed to being there or you think you’re going to be there for an extended period of time, I don’t think you’re going to see too much relief from these high interest rates in the next five, six, seven, maybe even the next decade,” he says.

Waller also says he believes the high mortgage rates are also going to effect rental prices, because more people will not qualify for loans, or not want to apply for one with such a high rate.

Get news alerts in the Apple App Store and Google Play Store or subscribe to our email newsletter here.

Copyright 2023 WBRC. All rights reserved.

Source: wtvy.com

Apache is functioning normally

“U.S. home prices continued to rally in July 2023,” Craig Lazzara, managing director at S&P DJI, said. “Our National Composite rose by 0.6% in July, and now stands 1.0% above its year-ago level. Our 10- and 20-City Composites each also rose in July 2023, and likewise stand slightly above their July 2022 levels.”

“Although the market’s gains could be truncated by increases in mortgage rates or by general economic weakness, the breadth and strength of this month’s report are consistent with an optimistic view of future results,” Lazzara added.

In July, prices rose in all 20 cities after seasonal adjustment, and in 19 of them before adjustment.

Chicago (+4.4%), Cleveland (+4.0%) and New York (+3.8%) posted the largest price gains on a year-over-year basis, repeating the ranking we saw in May and June.

At the other end of the scale, the worst performers were Las Vegas (-7.2%) and Phoenix (-6.6%).

The Midwest (+3.2%) continued as the nation’s strongest region, followed by the Northeast (+2.3%). The West (-3.8%) and Southwest (-3.6%) remained the weakest regions.

“The Case Shiller index indicates that the typical home price in July 2023 is about 45% higher than it was four years ago in July 2019,” said Bright MLS Chief Economist Lisa Sturtevant. “This is about the same rate of price growth that occurred during the 2002 through 2006 period when subprime lending drove exuberant housing demand.

“But that is where the similarities end. Today’s housing market is very different from the one that led up to the 2008 financial crisis and ultimately a 20 to 40% home price correction. Inventory is still very low by historic standards and buyers who are able to handle higher mortgage rates are still finding the market very competitive. Mortgage holders are well-qualified and subprime loans are rare. Housing equity is at an all-time high, providing homeowners a very deep cushion against a downturn. Demand is strong, driven by the large millennial population that is in prime first-time homebuying age.”

The rental market has offered a more extended break in pricing

Indeed, rents dipped for a fourth month compared to a year ago, Hale said. However, the cumulative drop in rents remains relatively modest nationwide, only down 2% from the peak. Furthermore, regional trends vary, with some markets still seeing relatively robust rental growth. Meanwhile, a record-high number of multi-family units are on the way, which will provide some relief over the next several months, even as multi-family starts slow, Hale concluded.

Source: housingwire.com