Continuing their downward trend of recent weeks, rates for the 30-year fixed mortgage fell back under 7% for the first time since April 11, Freddie Mac said.

The 30-year FRM declined 8 basis points, to 6.94% on May 23 from the prior week’s 7.02%, the Freddie Mac Primary Mortgage Market Survey reported. For the same week in 2023, the rate averaged 6.57%.

Meanwhile the 15-year FRM had a smaller drop of 4 basis points to 6.24% from 6.28%, but up from 5.97% one year ago.

This creates an “unexpected windfall” for homebuyers, said Freddie Mac Chief Economist Sam Khater.

“Although this week’s data on previously owned home sales showed a decline, total inventory of both new and existing homes is up,” Khater said in a press release. “Greater supply coupled with the recent downward trend in rates is an encouraging sign for the housing market.”

The drop in rates took place even though the 10-year Treasury went through some gyrations in the past seven days. It closed at 4.38% on May 16, with a low of 4.32% that day.

The next day’s intraday low was 4.39%, while the 10-year yield hit a high of 4.46% on Wednesday and in early trading on Thursday reached 4.5%, and by 11:30 a.m. was at 4.49%.

Other indicators, which use different methodologies (Freddie Mac uses rates on Loan Product Advisor submissions), were higher on the week-to-week comparison.

Lender Price product and pricing engine data on the National Mortgage News website at 11:30 a.m. on Thursday had the 30-year FRM at 7.03%, up from 6.856% seven days prior.

The Zillow website had the 30-year fixed at 6.71% at that time, up 4 basis points from Wednesday’s 6.67% and 7 basis points from the previous week’s average of 6.64%.

The minutes from the last Federal Open Market Committee meeting caused bond investors to reassess their forecasts for inflation and the economic outlook,” said Orphe Divounguy, senior economist at Zillow Home Loans, in a Wednesday night statement.

While the April data showed inflation is once again moving in the right direction, “there are still questions among Fed committee members about whether policy is restrictive enough to bring inflation down to the 2% target,” Divounguy said. “Although a moderation in consumer spending is expected to pull inflation lower, progress on inflation has been modest at best in the first quarter.”

Divounguy pointed to the prevailing view that the FOMC will make one or two rate cuts this year. When it comes to mortgages, the Personal Consumption Expenditures price index report next week should likely cause some repricing activity.

Moderation in mortgage rates led to a pickup in demand for residential real estate, but limited inventories across the country hindered actual home sales, the Federal Reserve reported in its Beige Book survey of regional business contacts that was published Wednesday.

Several Fed districts reported that a dearth of for-sale inventory contributed to faster home price growth since January. The spring homebuying season, which got underway a bit earlier than usual, was off to a good start in districts like New York and Dallas.

“Should mortgage rates fall, demand for residential real estate would increase, encouraging buyers who had been waiting on the sideline to move forward with home purchases,” according to the Beige Book.

The outlook for future economic growth remained generally positive as economists, market experts and business organization leaders interviewed for the report noted expectations for stronger demand and less restrictive financial conditions over the next six to 12 months.

The Beige Book, which was compiled by the Federal Reserve Bank of San Francisco using information gathered on or before Feb. 26, does not reflect the most recent rise in mortgage rates, which have surpassed 7% on HousingWire’s Mortgage Rates Center.

The Beige Book is published two weeks before each meeting of the policy-setting Federal Open Market Committee. The FOMC is expected to leave its benchmark interest rate unchanged when policymakers gather on March 19-20. The benchmark rate was last changed in July 2023, when it was raised to a range of 5.25% to 5.5%.

Federal Reserve Chair Jerome Powell reiterated Wednesday that policymakers still need to gain “greater confidence” that the battle against inflation is conquered before cutting interest rates.

“We believe that our policy rate is likely at its peak for this tightening cycle,” Powell said during testimony before the House Financial Services Committee. “If the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year.”

Following are excerpts of statements on housing conditions from the Federal Reserve districts, drawn from the newly released Beige Book.

***

Boston: Residential Realtors expressed growing optimism as both property listings and pending home sales increased. Contacts cited modest declines in mortgage rates since last fall as a likely reason for buyers’ increased willingness to enter the market.

Although inventory levels remained low, listings increased by modest to significant margins around the First District in recent months, lending increased optimism for sales moving forward. Still, contacts emphasized that the number of units for sale stayed far short of what they considered a balanced market, and that a dearth of inventories had contributed to faster house price growth from 2022 to 2023.

New York: Housing markets strengthened as the spring selling season got underway a bit earlier than normal. While inventory generally remained exceptionally low, inventory in New York City has begun to normalize. Many buyers who were waiting for a reprieve in mortgage rates have started to return with the intention of refinancing later. Though mortgage rate lock-in continues to limit new listings, particularly in the New York City suburbs, listings have increased in upstate New York as people have continued to leave the area for warmer climates.

Still, with such limited inventory, home prices have continued to press higher. Bidding wars were prevalent in the New York City suburbs but have been more limited in upstate New York.

Philadelphia: The inventory of for-sale properties remained extremely low as it has since the pandemic began. But real estate agents noted that higher interest rates have severely limited new listings over the past year and were responsible for the significantly lower level of closings.

New-home builders continued to report steady sales at relatively strong levels, in part because of the lack of existing for-sale homes. Most expect their pipeline of contracts to keep construction busy through the year.

Cleveland: Residential construction contacts reported that demand increased as mortgage rates declined. But real estate agents indicated existing-home sales changed little because inventory remained low.

Looking ahead, homebuilders and real estate contacts anticipated that demand would increase should mortgage rates fall, encouraging some “customers [who had been] waiting on the sideline” to move forward with home purchases.

Richmond: Respondents noted an increase in listings and buyer activity, but the elevated mortgage rate made buyers more tentative on making home purchase decisions. Sales prices have flattened, but there were still multiple offers on many homes.

Days on market increased slightly but remained below historic averages. The home construction market was constrained as it was difficult to find land and to receive permitting for new developments. Residential construction costs started to moderate this period.

Atlanta: As mortgage rates retreated from cyclical highs, homeownership affordability improved throughout the district. But home sales in most major markets ended the year well below seasonal norms and remained significantly behind pre-pandemic levels. Potential buyers locked into historically low mortgage rates remained reluctant to move, and migration into the district moderated through 2023, resulting in diminished housing demand.

Existing-home inventory levels were also suppressed by the “lock-in effect,” resulting in flat to moderate price growth in many markets. Demand for newly constructed homes was boosted by the lack of existing homes and builders.

Chicago: Residential real estate activity was down moderately, although prices were steady overall. High interest rates and a low supply of existing homes for sale continued to hold back activity.

St. Louis: Residential real estate sales have slowed since our previous report. Contacts in Arkansas and Tennessee reported that the low end of the market continues to be strong, while contacts in Missouri and Southern Indiana reported higher-end homes selling better. Rental rates for residential real estate have remained unchanged since our previous report.

Minneapolis: Single-family development remained soft, with modest but spotty increases in some district markets compared with a year earlier. A Minnesota contact said that “consumers quite abruptly stopped spending discretionary income on larger home improvements.”

Dallas: Home sales rose during the reporting period, and contacts noted that the spring selling season was generally off to a good start. Cancellation rates were down, buyer incentives were less prevalent, and builders said they were raising prices slightly in some markets.

Outlooks were positive, although contacts cited economic and political uncertainty, diminished affordability and tight lending.

San Francisco: Real estate activity rose slightly overall. Residential construction strengthened. Demand for single-family homes picked up slightly, as mortgage rates, though still elevated, moderated a bit in recent weeks. To attract reluctant homebuyers, some homebuilders began offering variable-rate mortgages at below-market interest rates, which revert to market pricing after a year, at which point buyers are reportedly expecting rates to be lower.

The positive signals for the housing market in 2024 include improvements in rates, affordability, and available inventory, alongside a moderation of monthly home price growth on a seasonally adjusted basis. The current market remains driven by interest rates. With the recent dip in rates, a noticeable uptick in purchase mortgage demand has reached levels comparable … [Read more…]

While the economy continues to expand and added 2.7 million jobs in 2023, signs point to a normalization in the labor market as job growth is expected to moderate in 2024. MORE

While mortgage rates have moved sideways since mid-December, housing continues to be impacted by higher mortgage rates with total home sales on track to be the lowest since 2012. MORE

Facing higher borrowing costs, borrowers are paying more discount points to buy down their mortgage rate, but they may not be getting the benefit. MORE

Recent developments

U.S. economy: According to the latest estimate of U.S. economic growth for Q3 2023, the economy grew at a seasonally adjusted annualized rate (SAAR) of 4.9%, slightly slower than the second estimate but still the fastest since Q4 2021— and among the fastest growth in the last 20 years. Consumption spending growth was revised down from a SAAR of 3.6% in the second estimate to 3.1% in the final estimate. This was mainly led by a decline in spending on services but remained the largest contributor to growth at 2.1 percentage points. After nine consecutive quarters of negative growth, residential investment growth came in much stronger than the initial estimates at a SAAR of 6.7%.

The labor market remained much stronger than expected in 2023 and defied expectations of a slowdown. The economy added 216,000 jobs in December, bringing the total jobs added in 2023 to 2.7 million.1 While total jobs added in 2023 was lower than the historical highs of 2021 and 2022, job growth was still remarkable given the high interest rate environment the economy faced. The unemployment rate remained unchanged in December at 3.7% compared to November 2023, but moved up 0.3 percentage points over the year.

While job growth remained significant over the year, some indications of a softer labor market are starting to creep in. The labor force participation rate as well as employment to population ratio decreased 0.3 percentage points over the month to 62.5% and 60.1% respectively. Downward revisions to October and November job growth meant the 3-month average job gain in the fourth quarter of 2023 was the lowest since the third quarter of 2019, if we exclude the 2020 recession. However, the torrid pace of job growth was unlikely to be sustained and employment growth is approaching levels consistent with a balanced labor market. Heading into 2024, we might see a moderation in job growth, which would be more consistent with long-run growth in the U.S. labor force. Job openings edged down slightly to 8.8 million in November 2023, according to the Bureau of Labor Statistics (BLS) Job Openings and Labor Turnover Survey. The ratio of job openings to unemployed, a metric that the Federal Reserve has been tracking to gauge the strength of the labor market, declined from a high of around 1.8 in January 2023 to 1.4 in November.

Inflation continues to trend towards the Federal Reserve’s target rate of 2%. The preferred measure of inflation of the Federal Reserve, the Core Personal Consumption Expenditure (PCE) measure increased at a rate of 3.2% year over year, the smallest annual increase since May 2021.2 While inflation has been moderating as the labor market normalizes, a reacceleration of home prices along with still high average hourly earnings growth at 4.1% year over year, could mean that getting to the 2% target might take longer than expected.

U.S. housing market: The housing market felt the impact of higher rates in 2023 with total annual home sales on track to be the lowest since 2012. Total (existing and new) home sales reached 4.4 million units in November 2023, down 1.2% as compared to October 2023 and 6.2% below November 2022. Total home sales averaged around 4.8 million from January through November 2023. Existing home sales were at 3.8 million as of November 2023 and averaged 4.1 million through November 2023.3 The existing housing inventory grew 15.3% year to date in November but the level of inventory (1.1 million homes available for sale in November) remains extremely low by historical standards.4 The rate-lock effect, which was the main driver of the lack of existing inventory, continued to push buyers towards the new home market. The number of new homes available for sale increased 2.7% year-to-date and was up 2.5% from the previous month. Overall, the sales of new homes averaged 666,000 in 2023 as compared to 637,000 in 2022.5

Falling interest rates have spurred the confidence of both potential homebuyers as well as the homebuilders. The Housing Market Index, which had decreased since August increased in December 2023. While existing home sales increased in November, pending home sales for November were still weak and saw a 5.2% decrease from the previous year. The FHFA Purchase-Only Home Price Index indicated that as of October of 2023, home prices rose 6.1% year to date, and as more home buyers enter the market amidst the lack of inventory, the pressure on prices could increase further.

U.S. mortgage market: Mortgage rates were on an upward trajectory for most of 2023, reaching 23-year highs in October. However, since the last week of October, rates have been declining mainly on the expectation of rate cuts by the Federal Reserve along with easing inflationary pressures. The average 30-year fixed-rate mortgage, as measured by Freddie Mac’s Primary Mortgage Market Survey® (PMMS®), fell almost one percentage point from the last week in October through mid-December. Despite the decline in recent weeks, mortgage rates are 13 basis points higher than they were at the beginning of the year. Mortgage activity also declined with purchase applications down almost 12% in 2023 and total applications down 7% even as refinance applications increased 15% over the year.6

Tighter financial conditions and higher overall interest rates are starting to impact mortgage delinquency rates. Total mortgage delinquency rates were up 0.25 percentage points from 3.37% in Q2 2023 to 3.62% in Q3 2023 according to the MBA’s National Delinquency Survey. The delinquency rate on conventional mortgages increased from 2.29% to 2.5% in Q3 2023 while the delinquency rate of VA loans was up from 3.7% to 3.76% over the same period. The largest increase was in the delinquency rate of FHA loans which increased 0.55 percentage points from 8.95% in Q2 to 9.5% in Q3. Interestingly, serious delinquency rates (90+ DQs) went down across the board between Q2 and Q3. Foreclosure starts increased from 0.13% in Q2 to 0.19% in Q3 2023 but remain low compared to its historical average.

Outlook

The U.S. economy exhibited tremendous resilience last year on strong consumer spending. We expect economic growth to slow this year as consumer spending starts to fade. Under our baseline scenario, with a slowing economy, the unemployment rate will see a modest uptick, and inflation will continue to moderate.

With inflation remaining above the Federal Reserve’s target rate of 2%, we do not expect the Federal Reserve to start cutting the federal fund rates immediately. However, it will continue to pause on interest rate hikes. We expect rate cuts in the second half of the year if the job market cools off enough to keep inflation muted. Under this scenario, we expect mortgage rates to ease throughout the year while remaining in the 6% range.

Falling rates will breathe some life into the housing market with some recovery in home sales. However, home sales are expected to grow only modestly due to a lack of inventory in the market. The demand for housing, however, will remain high based on a large share of Millennial first-time homebuyers looking to buy homes, which will push home prices up. We forecast home prices to increase 2.8% in 2024 and 2.0% in 2025 nationally.

Under our baseline scenario, we expect increases in both purchase and refinance volumes this year and into 2025. On purchase originations, higher home sales and growth in home prices will drive the dollar volumes of purchase originations up. However, we do not expect purchase origination volumes to reach the levels seen in 2021 and 2022 as lack of inventory will limit home sales. The drop in mortgage rates will push refinance originations up, as buyers who obtained higher interest rates in 2023 will likely refinance into lower rates. However, rates remaining around the 6% range will not provide enough refinance incentives to millions of homeowners who currently have rates below 6%. And therefore, we expect refinance volume to grow only modestly this year. Overall, we forecast total origination volumes to improve this year and into the next.

January 2024 SPOTLIGHT:

Declining affordability led borrowers to pay more discount points to buy down rates, but our research suggests it may not be worth it

Mortgage rates, as measured by Freddie Mac’s PMMS®, increased significantly in 2023 compared to the record lows of the past few years. On October 26, 2023, the average 30-year fixed-rate mortgage stood at 7.79%, a 23-year high. Since then, mortgage rates have moderated, but remain high by recent historical standards. These higher mortgage rates led many borrowers to make the decision to pay points in order to lower the rate when purchasing a house or refinancing an existing mortgage. During the low interest rate environment, few borrowers opted to pay discount points when obtaining a mortgage, but as rates started creeping up in the early 2022, we saw more borrowers paying discount points to lower their rate.

Using Freddie Mac closing data, we examined how often borrowers pay discount points and how many points they pay. For this analysis, the points we are focusing on are for permanent interest rate reductions throughout the life of the loan.7 To that end, we looked at a borrower profile that roughly matches our PMMS® population: mortgage for a home purchase or refinance of a one-unit, single-family owner-occupied property with a fully amortizing 30-year fixed-rate mortgage. We further restricted our sample to borrowers with conforming loans, and with credit scores 740 or above and a loan-to-value (LTV) ratio between 75 and 80 (inclusive).

We found that the share of borrowers who paid discount points increased in 2023 (Exhibit 1). For example, about 58.8% of purchase mortgage borrowers paid discount points in 2023, compared to 31.3% and 53.6% of purchase borrowers in 2021 and 2022 respectively. The share paying discount points was higher for noncash- out and cash-out refinance borrowers, 59.9% and 82.4%, respectively. Also, conditional on paying points, refinance borrowers tended to pay much higher points: 0.99 points for purchase borrowers compared to 1.16 and 1.76 points for non-cash-out and cash-out refinance borrowers, respectively.

It is interesting to note, however, that the interest rate differential between borrowers who pay discount points and those who do not pay discount points is very small. Through November 2023, the average effective rate on purchase loans for borrowers who did not pay discount points was 6.69% versus 6.86% for those who did pay points. This result seems to suggest that paying discount points may not be worth it from the consumers’ point of view. Indeed, some academic research8 has shown that in many circumstances paying discount points can be a poor financial decision. However, while our tabulation shows that borrowers who do not pay points generally receive lower mortgage rates compared to similar borrowers who do pay points, we do not control completely for borrower observed and unobserved attributes. Therefore, we cannot say with certainty that for any particular borrower, the relationship between discount points paid and interest rate is negative.9

Enlarge Image

Exhibit 2 compares the quarterly average discount points paid by Freddie Mac borrowers (home purchase, owner occupied, one-unit properties). From 2018 through 2021, borrowers that matched the PMMS® profile, (borrowers with origination LTV between 75 and 80 and FICO score 740 or higher) paid about the same average amount of points compared to all purchase borrowers. Starting in 2022 and continuing through 2023, higher credit quality borrowers tended to pay fewer points compared to all borrowers. In 2023, borrowers that matched the PMMS® profile paid on average about 0.06 less points or about 10% less compared to all purchase borrowers.

Enlarge Image

Prime borrowers who pay discount points on average have higher incomes and are obtaining higher loan balances when purchasing a home compared to borrowers who do not pay points. For example, in 2023 the average loan amount for purchase loans with points paid at origination was $360,000, compared with an average loan amount of $370,000 for mortgages where the borrowers did not pay points. In 2023, the average annual income of a “no discount points” borrower was $148,000, higher than the $140,000 average annual income for borrowers who paid points.

Our analysis on the closing files data shows that there is a difference in borrower behavior across the U.S. when it comes to paying discount points and origination fees. For example, in 2023 over 70% of prime purchase borrowers in HI, NM, WV, OR, WA, and DE paid discount points when closing on their mortgage while less than 50% of borrowers paid discount points in VT, IA, MA, IL, NE, ND, and WI. Exhibit 3 below shows the breakdown by state in 2023.

Enlarge Image

Our analysis shows that mortgage borrowers in 2023 were more willing to pay discount points than in previous years, and that the likelihood of paying points was greater for lower credit quality borrowers compared to the high-quality mortgage borrowers captured in our PMMS® profile population. We also saw that borrowers in the Midwest were less likely to pay points compared to borrowers in the Pacific and Mountain West. If interest rates stabilize in 2024, it will be interesting to observe whether borrowers opt to pay fewer points, or if the recent uptick in paying discount points is a more permanent shift in the mortgage market.

Footnotes

1 Non-Farm Employment, Bureau of Labor Statistics

2 BEA

3 National Association of Realtors (NAR)

4 From January 1999 through December 2019 the average number of existing homes available for sale averaged 2.2 million, about double the number of homes available for sale in November 2023.

5 U.S. Census Bureau and U.S. Department of Housing and Urban Development

6 Mortgage Bankers Association (MBA)

7 For an analysis of temporary buydowns see our previous Research Brief: https://www.freddiemac.com/research/insight/20230731-temporary-mortgage-rate-buydown-activity-spiked-in.

8 See for example: Agarwal, S., Ben-David, I. and Yao, V., 2017. Systematic mistakes in the mortgage market and lack of financial sophistication. Journal of Financial Economics, 123(1), pp. 42-58.

9 For a more detailed analysis see: Mota, N., Palim, M. and Woodward, S., 2022. Mortgages are still confusing… and it matters—How borrower attributes and mortgage shopping behavior impact costs. Fannie Mae Working Paper. https://www.fanniemae.com/media/45841/display

Average mortgage rates fell moderately yesterday. That was a bit of a surprise (though a welcome one) because yesterday’s inflation report would normally have pushed them higher. Read on for why markets might have reacted unexpectedly.

Earlier this morning, markets were signaling that mortgage rates today might fall. But these early mini-trends often switch direction or speed as the hours pass — as we saw yesterday.

Current mortgage and refinance rates

Find your lowest rate. Start here

Program

Mortgage Rate

APR*

Change

Conventional 30-year fixed

7.015%

7.03%

-0.07

Conventional 15-year fixed

6.28%

6.31%

-0.1

Conventional 20-year fixed

6.91%

6.93%

-0.065

Conventional 10-year fixed

6.09%

6.125%

-0.14

30-year fixed FHA

5.875%

6.545%

-0.3

30-year fixed VA

5.99%

6.14%

-0.085

5/1 ARM Conventional

6.31%

7.56%

-0.005

Rates are provided by our partner network, and may not reflect the market. Your rate might be different. Click here for a personalized rate quote. See our rate assumptions See our rate assumptions here.

Should you lock your mortgage rate today?

Yesterday’s fall in mortgage rates showed markets continuing to have faith in a “soft landing,” which will occur if we continue to see falling inflation together with a resilient economy. Indeed, it suggests that faith can’t be shaken even by occasional unfriendly data.

I think a soft landing remains the most likely scenario for 2024.

So, my personal rate lock recommendations are:

LOCK if closing in 7 days

FLOAT if closing in 15 days

FLOAT if closing in 30 days

FLOAT if closing in 45 days

FLOATif closing in 60days

However, with so much uncertainty at the moment, your instincts could easily turn out to be as good as mine — or better. So let your gut and your own tolerance for risk help guide you.

>Related: 7 Tips to get the best refinance rate

Market data affecting today’s mortgage rates

Here’s a snapshot of the state of play this morning at about 9:50 a.m. (ET). The data are mostly compared with roughly the same time the business day before, so much of the movement will often have happened in the previous session. The numbers are:

The yield on 10-year Treasury notes tumbled to 3.93% from 4.04%. (Good for mortgage rates.) More than any other market, mortgage rates typically tend to follow these particular Treasury bond yields

Major stock indexes were rising this morning. (Bad for mortgage rates.) When investors buy shares, they’re often selling bonds, which pushes those prices down and increases yields and mortgage rates. The opposite may happen when indexes are lower. But this is an imperfect relationship

Oil prices increased to $74.42 from $72.80 a barrel. (Bad for mortgage rates*.) Energy prices play a prominent role in creating inflation and also point to future economic activity

Goldprices climbed to $2,065 from $2,036 an ounce. (Good for mortgage rates*.) It is generally better for rates when gold prices rise and worse when they fall. Gold tends to rise when investors worry about the economy.

CNN Business Fear & Greed index — inched lower to 73 from 75. (Good for mortgage rates.) “Greedy” investors push bond prices down (and interest rates up) as they leave the bond market and move into stocks, while “fearful” investors do the opposite. So lower readings are often better than higher ones

*A movement of less than $20 on gold prices or 40 cents on oil ones is a change of 1% or less. So we only count meaningful differences as good or bad for mortgage rates.

Caveats about markets and rates

Before the pandemic, post-pandemic upheavals, and war in Ukraine, you could look at the above figures and make a pretty good guess about what would happen to mortgage rates that day. But that’s no longer the case. We still make daily calls. And are usually right. But our record for accuracy won’t achieve its former high levels until things settle down.

So, use markets only as a rough guide. Because they have to be exceptionally strong or weak to rely on them. But, with that caveat, mortgage rates today look likely to decrease. However, be aware that “intraday swings” (when rates change speed or direction during the day) are a common feature right now.

Find your lowest rate. Start here

What’s driving mortgage rates today?

Yesterday

I suspect that Wall Street has bought the narrative of a soft landing (see above) and, for now, is prepared to stick to it through thick and thin. That’s my only real explanation for why mortgage rates fell yesterday despite an unfriendly inflation report.

True, some saw the report as less unfriendly than others. The New York Times (paywall), for example, reported it under the headline, “Price Increases Tick Higher, but Show Moderation.”

But the consumer price index (CPI) was undeniably worse than expected. And that would normally exert some upward pressure on mortgage rates. Still, let’s not give this gift horse too close a dental inspection.

Today

Producer price indexes (PPIs) are typically less important than CPIs. But they still sometimes affect mortgage rates.

Today’s PPI showed factory-gate and wholesale prices rising more slowly than expected. And that would normally be good for mortgage rates. However, as we saw yesterday, markets don’t always follow such “rules.”

Next week

Rather like this week, next week starts slowly but contains an important economic report. Things are especially quiet on Monday because bond markets are closed for Martin Luther King Day. And closed bond markets mean mortgage rates shouldn’t move. (So, we shall not be publishing this daily report on Monday.)

Tuesday’s similarly dull with no economic reports scheduled for release.

However, Wednesday is potentially next week’s big day for mortgage rates, led by the retail sales report for December. But, after that, things tail off again.

Don’t forget you can always learn more about what’s driving mortgage rates in the most recent weekend edition of this daily report. These provide a more detailed analysis of what’s happening. They are published each Saturday morning soon after 10 a.m. (ET) and include a preview of the following week.

Recent trends

According to Freddie Mac’s archives, the weekly all-time lowest rate for 30-year, fixed-rate mortgages was set on Jan. 7, 2021, when it stood at 2.65%. The weekly all-time high was 18.63% on Sep. 10, 1981.

Freddie’s Jan. 11 report put that same weekly average at 6.66%, up from the previous week’s 6.62%. But note that Freddie’s data are almost always out of date by the time it announces its weekly figures.

Expert forecasts for mortgage rates

Looking further ahead, Fannie Mae and the Mortgage Bankers Association (MBA) each has a team of economists dedicated to monitoring and forecasting what will happen to the economy, the housing sector and mortgage rates.

And here are their rate forecasts for the last quarter (Q4/23) and the following three quarters (Q1/24, Q2/24 and Q3/24).

The numbers in the table below are for 30-year, fixed-rate mortgages. Fannie’s were updated on Dec. 19 and the MBA’s on Dec. 13.

Forecaster

Q4/23

Q1/24

Q2/24

Q3/24

Fannie Mae

7.4%

7.0%

6.8%

6.6%

MBA

7.4%

7.0%

6.6%

6.3%

Of course, given so many unknowables, both these forecasts might be even more speculative than usual. And their past record for accuracy hasn’t been wildly impressive.

Important notes on today’s mortgage rates

Here are some things you need to know:

Typically, mortgage rates go up when the economy’s doing well and down when it’s in trouble. But there are exceptions. Read ‘How mortgage rates are determined and why you should care’

Only “top-tier” borrowers (with stellar credit scores, big down payments, and very healthy finances) get the ultralow mortgage rates you’ll see advertised

Lenders vary. Yours may or may not follow the crowd when it comes to daily rate movements — though they all usually follow the broader trend over time

When daily rate changes are small, some lenders will adjust closing costs and leave their rate cards the same

Refinance rates are typically close to those for purchases.

A lot is going on at the moment. And nobody can claim to know with certainty what will happen to mortgage rates in the coming hours, days, weeks or months.

Find your lowest mortgage rate today

You should comparison shop widely, no matter what sort of mortgage you want. Federal regulator the Consumer Financial Protection Bureau found in May 2023:

“Mortgage borrowers are paying around $100 a month more depending on which lender they choose, for the same type of loan and the same consumer characteristics (such as credit score and down payment).”

In other words, over the lifetime of a 30-year loan, homebuyers who don’t bother to get quotes from multiple lenders risk losing an average of $36,000. What could you do with that sort of money?

Verify your new rate

Mortgage rate methodology

The Mortgage Reports receives rates based on selected criteria from multiple lending partners each day. We arrive at an average rate and APR for each loan type to display in our chart. Because we average an array of rates, it gives you a better idea of what you might find in the marketplace. Furthermore, we average rates for the same loan types. For example, FHA fixed with FHA fixed. The end result is a good snapshot of daily rates and how they change over time.

How your mortgage interest rate is determined

Mortgage and refinance rates vary a lot depending on each borrower’s unique situation.

Factors that determine your mortgage interest rate include:

Overall strength of the economy — A strong economy usually means higher rates, while a weaker one can push current mortgage rates down to promote borrowing

Lender capacity — When a lender is very busy, it will increase rates to deter new business and give its loan officers some breathing room

Property type (condo, single-family, town house, etc.) — A primary residence, meaning a home you plan to live in full time, will have a lower interest rate. Investment properties, second homes, and vacation homes have higher mortgage rates

Loan-to-value ratio (determined by your down payment) — Your loan-to-value ratio (LTV) compares your loan amount to the value of the home. A lower LTV, meaning a bigger down payment, gets you a lower mortgage rate

Debt-To-Income ratio — This number compares your total monthly debts to your pretax income. The more debt you currently have, the less room you’ll have in your budget for a mortgage payment

Loan term — Loans with a shorter term (like a 15-year mortgage) typically have lower rates than a 30-year loan term

Borrower’s credit score — Typically the higher your credit score is, the lower your mortgage rate, and vice versa

Mortgage discount points — Borrowers have the option to buy discount points or ‘mortgage points’ at closing. These let you pay money upfront to lower your interest rate

Remember, every mortgage lender weighs these factors a little differently.

To find the best rate for your situation, you’ll want to get personalized estimates from a few different lenders.

Verify your new rate. Start here

Are refinance rates the same as mortgage rates?

Rates for a home purchase and mortgage refinance are often similar.

However, some lenders will charge more for a refinance under certain circumstances.

Typically when rates fall, homeowners rush to refinance. They see an opportunity to lock in a lower rate and payment for the rest of their loan.

This creates a tidal wave of new work for mortgage lenders.

Unfortunately, some lenders don’t have the capacity or crew to process a large number of refinance loan applications.

In this case, a lender might raise its rates to deter new business and give loan officers time to process loans currently in the pipeline.

Also, cashing out equity can result in a higher rate when refinancing.

Cash-out refinances pose a greater risk for mortgage lenders, so they’re often priced higher than new home purchases and rate-term refinances.

Check your refinance rates today. Start here

How to get the lowest mortgage or refinance rate

Since rates can vary, always shop around when buying a house or refinancing a mortgage.

Comparison shopping can potentially save thousands, even tens of thousands of dollars over the life of your loan.

Here are a few tips to keep in mind:

1. Get multiple quotes

Many borrowers make the mistake of accepting the first mortgage or refinance offer they receive.

Some simply go with the bank they use for checking and savings since that can seem easiest.

However, your bank might not offer the best mortgage deal for you. And if you’re refinancing, your financial situation may have changed enough that your current lender is no longer your best bet.

So get multiple quotes from at least three different lenders to find the right one for you.

2. Compare Loan Estimates

When shopping for a mortgage or refinance, lenders will provide a Loan Estimate that breaks down important costs associated with the loan.

You’ll want to read these Loan Estimates carefully and compare costs and fees line-by-line, including:

Interest rate

Annual percentage rate (APR)

Monthly mortgage payment

Loan origination fees

Rate lock fees

Closing costs

Remember, the lowest interest rate isn’t always the best deal.

Annual percentage rate (APR) can help you compare the ‘real’ cost of two loans. It estimates your total yearly cost including interest and fees.

Also, pay close attention to your closing costs.

Some lenders may bring their rates down by charging more upfront via discount points. These can add thousands to your out-of-pocket costs.

3. Negotiate your mortgage rate

You can also negotiate your mortgage rate to get a better deal.

Let’s say you get loan estimates from two lenders. Lender A offers the better rate, but you prefer your loan terms from Lender B. Talk to Lender B and see if they can beat the former’s pricing.

You might be surprised to find that a lender is willing to give you a lower interest rate in order to keep your business.

And if they’re not, keep shopping — there’s a good chance someone will.

Fixed-rate mortgage vs. adjustable-rate mortgage: Which is right for you?

Mortgage borrowers can choose between a fixed-rate mortgage and an adjustable-rate mortgage (ARM).

Fixed-rate mortgages (FRMs) have interest rates that never change unless you decide to refinance. This results in predictable monthly payments and stability over the life of your loan.

Adjustable-rate loans have a low interest rate that’s fixed for a set number of years (typically five or seven). After the initial fixed-rate period, the interest rate adjusts every year based on market conditions.

With each rate adjustment, a borrower’s mortgage rate can either increase, decrease, or stay the same. These loans are unpredictable since monthly payments can change each year.

Adjustable-rate mortgages are fitting for borrowers who expect to move before their first rate adjustment, or who can afford a higher future payment.

In most other cases, a fixed-rate mortgage is typically the safer and better choice.

Remember, if rates drop sharply, you are free to refinance and lock in a lower rate and payment later on.

How your credit score affects your mortgage rate

You don’t need a high credit score to qualify for a home purchase or refinance, but your credit score will affect your rate.

This is because credit history determines risk level.

Historically speaking, borrowers with higher credit scores are less likely to default on their mortgages, so they qualify for lower rates.

For the best rate, aim for a credit score of 720 or higher.

Mortgage programs that don’t require a high score include:

Conventional home loans — minimum 620 credit score

FHA loans — minimum 500 credit score (with a 10% down payment) or 580 (with a 3.5% down payment)

VA loans — no minimum credit score, but 620 is common

USDA loans — minimum 640 credit score

Ideally, you want to check your credit report and score at least 6 months before applying for a mortgage. This gives you time to sort out any errors and make sure your score is as high as possible.

If you’re ready to apply now, it’s still worth checking so you have a good idea of what loan programs you might qualify for and how your score will affect your rate.

You can get your credit report from AnnualCreditReport.com and your score from MyFico.com.

How big of a down payment do I need?

Nowadays, mortgage programs don’t require the conventional 20 percent down.

In fact, first-time home buyers put only 6 percent down on average.

Down payment minimums vary depending on the loan program. For example:

Conventional home loans require a down payment between 3% and 5%

FHA loans require 3.5% down

VA and USDA loans allow zero down payment

Jumbo loans typically require at least 5% to 10% down

Keep in mind, a higher down payment reduces your risk as a borrower and helps you negotiate a better mortgage rate.

If you are able to make a 20 percent down payment, you can avoid paying for mortgage insurance.

This is an added cost paid by the borrower, which protects their lender in case of default or foreclosure.

But a big down payment is not required.

For many people, it makes sense to make a smaller down payment in order to buy a house sooner and start building home equity.

Verify your new rate. Start here

Choosing the right type of home loan

No two mortgage loans are alike, so it’s important to know your options and choose the right type of mortgage.

The five main types of mortgages include:

Fixed-rate mortgage (FRM)

Your interest rate remains the same over the life of the loan. This is a good option for borrowers who expect to live in their homes long-term.

The most popular loan option is the 30-year mortgage, but 15- and 20-year terms are also commonly available.

Adjustable-rate mortgage (ARM)

Adjustable-rate loans have a fixed interest rate for the first few years. Then, your mortgage rate resets every year.

Your rate and payment can rise or fall annually depending on how the broader interest rate trends.

ARMs are ideal for borrowers who expect to move prior to their first rate adjustment (usually in 5 or 7 years).

For those who plan to stay in their home long-term, a fixed-rate mortgage is typically recommended.

Jumbo mortgage

A jumbo loan is a mortgage that exceeds the conforming loan limit set by Fannie Mae and Freddie Mac.

In 2023, the conforming loan limit is $726,200 in most areas.

Jumbo loans are perfect for borrowers who need a larger loan to purchase a high-priced property, especially in big cities with high real estate values.

FHA mortgage

A government loan backed by the Federal Housing Administration for low- to moderate-income borrowers. FHA loans feature low credit score and down payment requirements.

VA mortgage

A government loan backed by the Department of Veterans Affairs. To be eligible, you must be active-duty military, a veteran, a Reservist or National Guard service member, or an eligible spouse.

VA loans allow no down payment and have exceptionally low mortgage rates.

USDA mortgage

USDA loans are a government program backed by the U.S. Department of Agriculture. They offer a no-down-payment solution for borrowers who purchase real estate in an eligible rural area. To qualify, your income must be at or below the local median.

Bank statement loan

Borrowers can qualify for a mortgage without tax returns, using their personal or business bank account. This is an option for self-employed or seasonally-employed borrowers.

Portfolio/Non-QM loan

These are mortgages that lenders don’t sell on the secondary mortgage market. This gives lenders the flexibility to set their own guidelines.

Non-QM loans may have lower credit score requirements, or offer low-down-payment options without mortgage insurance.

Choosing the right mortgage lender

The lender or loan program that’s right for one person might not be right for another.

Explore your options and then pick a loan based on your credit score, down payment, and financial goals, as well as local home prices.

Whether you’re getting a mortgage for a home purchase or a refinance, always shop around and compare rates and terms.

Typically, it only takes a few hours to get quotes from multiple lenders — and it could save you thousands in the long run.

Time to make a move? Let us find the right mortgage for you

Current mortgage rates methodology

We receive current mortgage rates each day from a network of mortgage lenders that offer home purchase and refinance loans. Mortgage rates shown here are based on sample borrower profiles that vary by loan type. See our full loan assumptions here.

Do you want to learn how to find data entry jobs from home? Here’s how you can make money doing data entry at home. If you’re looking for a data entry position, I have all the details for you here. Whether you want to be a full-time or part-time employee, work remotely, or become a freelancer,…

Do you want to learn how to find data entry jobs from home? Here’s how you can make money doing data entry at home.

If you’re looking for a data entry position, I have all the details for you here. Whether you want to be a full-time or part-time employee, work remotely, or become a freelancer, there are many different kinds of data entry jobs that you may be interested in.

In this article, you’ll learn:

What are data entry jobs

How much a data entry clerk makes

Where to find data entry jobs

And more!

Recommended reading: 21 Best Entry Level Work From Home Jobs

What Are Data Entry Jobs?

Data entry jobs are run by data entry clerks, who have many tasks including typing and data transcription. You can find these types of jobs in many different fields, including healthcare, finance, research, and administration.

Data entry is exactly what you’ll be doing – you will be entering data on a computer system.

Data entry jobs include work tasks such as:

Typing data into computer systems

Updating data into databases

Managing data

These jobs require accuracy and being able to handle all kinds of information involving text and numbers.

Other tasks for data entry freelance jobs may include:

Typing

Listening to audio files and transcribing them into written documents

Data transcription

Legal transcription

Data validation (for example, you may be comparing the data to what you have to make sure it was input correctly)

Data organization

Customer service

Your tasks will mainly depend on the job description, as they can vary from company to company.

Recommended reading: 18 Best Online Transcription Jobs For Beginners To Make $2,000 Monthly

Who is a good fit for this job?

Being a data entry clerk requires:

Attention to detail and data management

Fast typing speed

Communication skills

Ability to work efficiently

Accurate with data

Proficiency with certain data entry software (such as spreadsheets, Google Sheets, Google Docs, Microsoft Word, or Microsoft Office)

The ability to handle sensitive information

Basic computer skills are extremely helpful with data entry work, as everything will be done with a computer (or laptop).

Many people who work in online data entry jobs like how this field typically works alone from home and remote data entry jobs are a possibility as well.

Plus, you can typically get started in this career field not needing many years of experience, as there are many entry level data entry jobs that you can start with no experience. Data entry jobs usually require a high school diploma or equivalent.

How Much Money Can You Make From Data Entry?

The amount of money you make depends on many things including your location, experience, the industry you work in, and how hard the data entry tasks you are being paid to do. Your pay can also depend on your shift (are you working Monday through Friday at a company, or in your spare time at home?), your work location (companies in certain places tend to pay more), your typing speed (the faster you can type, the more you can get done!), and more.

The average data entry salary in the United States is between $25,000-$45,000 per year, with the average hourly rate being about $18 per hour. Some data entry positions pay less and some pay more, of course.

There are benefits of working this type of job as well, such as being able to find flexible jobs where you can work from home, or even while traveling.

15 Best Places To Find Data Entry Jobs From Home

Here are the 15 best places to find data entry jobs from home.

1. FlexJobs

FlexJobs is an online job search platform that lists remote and flexible job opportunities. Every job listed on FlexJobs has been found and checked to make sure it’s not junk, an ad, or a scam. This is why FlexJobs requires people to pay for a subscription to use their site too.

Listings on FlexJobs include positions for remote work, flexible schedules, part-time work, and even freelance opportunities.

To use FlexJobs, you need a paid account to apply for jobs. In the FlexJobs search bar, search for “data entry” and many positions will come up in this field showing you what qualifications are needed, if it’s 100% remote, and what the tasks include.

I did a quick search on FlexJobs, and I found remote data entry jobs, part-time data entry jobs, freelance data entry jobs, and entry-level data entry jobs. There were many companies that were looking to hire for this position within just the last few days, and from many different fields.

Note: Even though there is a cost to use FlexJobs, if you don’t successfully find a job on FlexJobs, you can ask for a refund.

2. Upwork

UpWork is one of the largest freelancing platforms that connects freelancers with clients who need various types of services, such as data entry. UpWork has thousands of jobs available at any time and makes it very easy to search for data entry jobs.

As a freelancer on UpWork, a 10% fee is taken out of any earnings made from UpWork jobs. This is an important thing to think about before finding jobs on UpWork as this fee can add up quickly.

When I searched on Upwork, I found 2,197 Data Entry Specialist jobs posted. Some of the companies hiring for data entry positions on Upwork included Microsoft, Airbnb, Nasdaq, and more.

3. Amazon MTurk

Amazon MTurk is a platform operated by Amazon that connects people and businesses who need help with tasks like data entry. It is a crowdsourcing marketplace where companies can outsource their jobs.

MTurk has jobs not only in data entry, but image or video tagging, content moderation, transcription, and more.

This is how MTurk works:

Search for jobs through Amazon Mturk and click on a job that interests you.

Accept the tasks and follow the instructions for the job.

Submit your work once the job is completed.

Once the company or individual approves your work, your earnings are available.

4. Microworkers

Microworkers is an online platform that connects people to businesses to do small and quick tasks, referred to as “micro-jobs”. These tasks can range from data entry, data validation, website testing, and more.

Freelancers using Microworkers to find jobs so that they can work as little or as much as they want. Your potential for earning is whatever you want it to be, because you can accept as many jobs as you’re able to complete.

To find jobs on Microworkers, click on the “jobs” tab and browse through hundreds of listed tasks. Each task will show different instructions and the time you have to complete the job. The job will also show how much you will earn for finishing the tasks.

5. Clickworker

Clickworker connects businesses with freelancers who are in charge of completing small, quick assignments.

Besides data entry, you can also earn money with Clickworker by answering surveys, doing research, translating, and more.

As a Clickworker, you will get a list of available assignments that you can choose from. The tasks available to you will depend on your skills, education, past work assignments, and any qualification tests you pass.

6. SigTrack

SigTrack is a site dedicated to data entry jobs. Jobs on SigTrack primarily focus on collecting and verifying voter signatures for political campaigns, initiatives, and petitions.

There is plenty of work available on SigTrack with the average hourly rate going from $11-$12 per hour.

You cannot reside in California or Massachusetts to work for SigTrack.

7. Fiverr

Fiverr is an online job marketplace that allows freelancers to list their digital services, including data entry, graphic design, writing, web development, and a lot more.

Companies or small businesses looking for freelancers search Fiverr for help on their projects.

It’s important to note that Fiverr does take a 20% cut of your earnings, so keep that in mind if you search for a job here.

I found 69,727 jobs related to data entry on this site, so competition can be pretty tough. You will have to find a way to stand out if you want to post a listing on Fiverr.

8. Axion Data Entry Services

Axion Data Entry Services is a company that does data entry and data processing for businesses, such as for managing and digitizing their data.

As an employee of the Axion Data Entry Services team, you’ll be evaluated for accuracy and your attention to detail, and you are paid at a flat rate per entry or for each document you enter.

The more skills and qualifications you have, the more you will earn at Axion Data Entry Services.

9. DionData Solutions

DionData Solutions connects data entry specialists to businesses and organizations. DionData Solutions works for clients who need help in managing and digitizing large volumes of data accurately and efficiently.

At DionDate Solutions, data entry specialists work on:

Medical claims

Mailing lists

Surveys

Subscription fulfillments

Enrollment forms

Warranty cards

Product registration cards

Inventories

And more.

10. Capital Typing

Capital Typing is a company that sells services such as data entry, transcription, virtual assistance services, and other admin support roles.

Capital Typing specializes in on-demand and long-term outsourcing solutions to help companies streamline their operations.

Due to the type of business they run, they are in need of data entry workers.

11. We Work Remotely

We Work Remotely is a job board that focuses primarily on remote jobs. This platform is home to the largest remote work opportunity in the world with over 4.5 million visitors.

Many companies hire workers from this site, such as Google, Amazon, and more. So, there are many big companies that list jobs here.

This online platform allows companies to hire remote workers for all kinds of jobs including data entry. Jobs posted include information such as what the company is looking for, what the ideal candidate has as far as qualifications go, salary and benefits, and the steps to apply.

12. Virtual Vocations

Virtual Vocations is a job platform that lists remote and telecommute job opportunities.

This platform is designed to help remote workers find legit online jobs, making it as easy as possible to get started working from home.

Jobs listed on Virtual Vocations list key responsibilities for the job, and required qualifications.

When I looked, Virtual Vocations currently has 7 jobs related to data entry listed.

13. Scribie

Scribie is a transcription and audio captioning service that provides services to businesses and individuals. Scribie specializes in converting audio and video files into written text.

To apply as a Scribie transcriptionist you need to:

Sign up as a Transcriber

Connect your PayPal account

Take a transcription test

Scribie pays $5-$20 per audio hour (Scribie claims that a person can make around $800 a month by working 8 hours each day.). The pay is a little on the lower end, but Scribie does give you automated transcripts, which can save you around 60% of the typing effort.

You’ll simply listen to the audio clips that they give you, compare them to the automated transcription (such as applying context, identifying mistakes, and correcting the automated transcript that they give you). Then, you can get paid.

14. GoTranscript

GoTranscript is a platform that connects businesses with professional data entry specialists. Data entry specialists on GoTranscript work on documents related to the medical, legal, and academic fields.

With a 98% customer satisfaction rate, GoTranscript relies on hiring the best data entry specialists.

They pay up to $0.60 per audio or video minute, with an average earnings of around $150 per month.

15. Working Solutions

Working Solutions is a site that works with independent contractors on jobs related to industries like health and insurance, senior living, fitness, hospitality, and education.

Working Solutions independent contractors’ tasks include things like handling customer care calls, emails, and video chats.

You can often find data entry jobs on this site.

Frequently Asked Questions About Data Entry Jobs

Below are answers to common questions about data entry jobs from home.

Is work-at-home data entry legitimate? Can you really make money doing data entry at home?

Work at home data-entry jobs are legit and can be found quite easily online.

Here are some tips to help you find a legit work at home data entry job.

Use FlexJobs – Since FlexJobs job listings are all curated and checked for accuracy, you’ll have more peace of mind. Companies listing jobs on FlexJobs include Apple, Salesforce, United Healthcare, Dell, Capital One, and many more.

Be cautious – If a job posting makes exaggerated claims about high earnings with little to no effort, it’s likely a red flag. Legit data entry jobs give fair compensation (above minimum wage) for the data entry tasks performed. But, a legitimate company won’t ever pay $10,000 a week or something high like that.

Research the company – You should look for an official website for the company, a physical address, any information you can find on the Better Business Bureau, and even a contact phone number. Scammers generally use generic email addresses and websites that lack information.

Don’t pay thousands to become a data entry clerk – Some companies may ask you to have a data entry certificate. If they ask for this, make sure they aren’t charging you an arm and a leg for it.

Unfortunately, with many work from home careers, there are a lot of scams. But, that doesn’t mean that data entry isn’t real.

There are many places to find the best data entry jobs. But, you still have to be smart!

Which site is best for data entry jobs?

The best sites for data entry freelance jobs include:

FlexJobs

UpWork

Fiverr

We Work Remotely

Job listing sites like the platforms above often are great places to start if you are looking for entry level data entry jobs from home.

Is data entry a hard job to do? Can a beginner do data entry?

Data entry is often an entry-level job and is relatively easy to get started with. If you don’t have trouble with typing accurately and inputting data, then you most likely won’t have a problem with finding work at home data entry jobs.

For most new jobs in data entry, you will want to make sure you include a relevant cover letter and resume. Even if you are brand new to work-from-home data entry jobs, you can still tailor these documents to the company and position so that you can get the job.

Can I do data entry with my phone?

Okay, so I hear this question all the time. And, I get it – being able to work from your phone would be great.

Depending on the job, you can possibly do data entry from your smartphone, but it won’t be nearly as efficient and easy as doing this kind of work on a computer.

The small screen size on your phone makes data entry more challenging, and your typing will be much slower compared to working on a laptop. Plus, some software may not be available on your phone.

If you want to make the most money with stay at home data entry jobs, then it’s probably best to get a laptop or a computer.

Data Entry Jobs From Home – Summary

I hope you enjoyed today’s article on how to find online data entry jobs from home.

Data entry jobs are great for people completely new to this field as you don’t need prior experience to become a data entry specialist.

Plus, with the average salary from $25,000-$45,000, finding a data entry position is a good career path to get started with if you want to work from home and possibly have a flexible schedule.

What’s your best place to find work from home data entry jobs?

During highly challenging times for mortgage holders as the Reserve Bank of Australia (RBA) hit borrowers with a succession of interest rate rises, the mortgage broking industry continued to deliver strong results.

The Mortgage and Finance Association of Australia’s latest Industry Intelligence Service report found in the 12 months to March 2023, mortgage brokers settled a record $358.68 billion in home loans.

The MFAA said brokers have maintained a strong market share, writing 69.6 per cent of all residential home loans in the March 2023 quarter. Conversely, market share of the major banks declined in the March 2023 quarter to 45.8 per cent following a 2.7 percentage point increase in the December 2022 quarter to 49.9 per cent.

MFAA CEO Anja Pannek said the 16th edition of the report focused on the six-month period from October 1 2022 to March 31 2023, drawing on data supplied by the industry’s leading aggregator brands to provide mortgage broker, industry performance and demographic data.

“The period covered in the report coincided with a period of intense refinancing as fixed rate mortgages reverted to variable, clients encountered serviceability constraints and a moderation of property prices in some markets,” Pannek said.

“This confluence of factors can be seen in this industry research, however, the outstanding service mortgage brokers deliver to their clients has remained a constant throughout this time.”

While another strong result for brokers, the report noted in comparison to the October 2021 – March 2022 period, the total value of loans settled by mortgage brokers declined 8.63 per cent.

However, Pannek said the broker channel still outperformed the overall home loan lending market.

“Whilst the value of home loans settled by brokers declined 8.63 per cent for the period, the lending market as a whole – broker and proprietary channels – declined 10.89 per cent over the same period. This highlights that the broker market is meeting more needs of more consumers in a challenging economic environment,” she said.

Bell Partners is ready to assist if you want a more competitive interest rate with your current lender or are looking to refinance to a different product elsewhere in the market.

Fannie Mae chief economist Doug Duncan attributed the moderated pace of growth to the impact of higher mortgage rates on affordability. As of last week, the 30-year fixed-rate mortgage averaged 7.57%, according to Freddie Mac. “Slightly slowing house price growth may reflect in part the affordability impact of the higher mortgage rate environment – even … [Read more…]

Somewhere between the timeless allure of traditional and the clean lines of contemporary, we find transitional style.

As spaces evolve with modern times, so too does the desire for a balanced blend of the old and new. We’ll delve into the nuances of the transitional design style, an embodiment of sophistication and simplicity, harmoniously woven together.

Keep in mind, transitional style is all about finding that sweet equilibrium, where curated antiques meet minimalist modern, creating a unique and welcoming space that ultimately feels like home. Here’s how you can spot the look in real life and recreate it in your own spaces.

Transitional style 101

What are some basics of the transitional interior design look? Not every transitional space will check every box, but you’re likely to find a medley of the following features.

Neutral color palette: One of the hallmarks of transitional design is a largely neutral color palette. Think beiges, grays, creams and tans, which serve as a base. This doesn’t mean color is absent; rather, pops of color are introduced sparingly through accessories, art and accent pieces.

Clean lines with curved profiles: Furniture in transitional spaces combines the straight lines seen in more contemporary pieces with the curves and detailing of traditional designs. For instance, a sofa might have clean, minimalist lines but be upholstered in a classic fabric or have tufted details.

Mix of materials: You’ll often see a mix of materials in transitional design. This might mean a glass coffee table with an ornate wooden base, or a modern metal light fixture above a traditional dining set. The juxtaposition of these materials creates visual interest.

Texture and fabric: With a neutral color palette, texture plays a big role in transitional style. Think tufted rugs, linen drapes and textured cushions. A variety of fabrics from leather to velvet can be used — in moderation — to bring depth, warmth and drama to any space.

Less ornamentation: Unlike traditional design, which might include heavy moldings or detailed woodworking, transitional spaces tend to be on the simpler side. However, they’re not as stark or minimalist as traditional Scandinavian or Japanese interior design styles.

Art and accessories: Transitional apartments might showcase modern art in ornate frames, or traditional art in sleek, minimalist frames. Accessories, like vases or lamps, should strike a balance between the contemporary and traditional. It’s all about toeing the line between styles without leaning too far in one direction.

Functional and uncluttered spaces: While the look is balanced, transitional design embraces functionality. This means adequate storage solutions to ensure spaces are free of unnecessary items, which is especially important in apartment settings where space may be at a premium.

Natural light: Embracing natural light is key in transitional design. Light and airy window treatments that allow for plenty of sunlight help make the space feel open and welcoming without requiring additional accessories or loud colors.

Area rugs: To define spaces, especially in an open-concept apartment, use area rugs. This helps to visually break up the space while also adding warmth and texture.

Consistency: Even though transitional style is about blending, it’s important to maintain a sense of consistency. This means not every piece in a room should be a mix of modern and traditional. The goal in transitional design is that the room — as a whole — achieves this balance.

Transitional design style in action

If you want to apply the transitional style to your apartment, start with a neutral foundation, incorporate modern and traditional elements carefully and remember to keep it functional and uncluttered. With a keen eye for design and balance, you can create a space that feels equal parts fresh and timeless.

Soft transitional design: a 2023 trend

In 2023, the soft transitional interior design style gained significant popularity for its harmonious blend of traditional and contemporary elements. This style is characterized by its emphasis on creating a warm and inviting atmosphere while maintaining a clean and streamlined aesthetic.

While both soft transitional and OG-transitional interior design styles share common transitional elements, the former distinguishes itself through its heightened emphasis on comfort, a subdued color palette with subtle pops of color and a strong focus on textures that contribute to a warm and inviting atmosphere. With this in mind, you might see more cozy blankets, stacks of pillows, soft textures and more handmade keepsakes to embrace your best “soft life” and remind you of what you value most.

Transitional design: A how-to guide

Transitional style strikes a delicate balance between the timeless elegance of traditional designs and the sleek minimalism of contemporary style. This design approach merges the best of both worlds to create a harmonious space that feels cozy yet sophisticated. For apartment renters, mastering the transitional style can result in a home that is functional and uniquely personal.

Transitional design tips for renters

Need a few starting tips to implement this design in your home? Start by trying a few of these.

Start with the basics: For apartment renters, it’s best to start with the essentials. Invest in key pieces like a versatile sofa, a neutral rug or a functional dining set. These foundational items set the stage for the rest of the decor. With the larger pieces out of the way, you can add small artifacts and accessories over time to fully round out your design and make your place feel fully like home.

Modular furniture: Given the sometimes limited space in apartments, opting for modular furniture can make a big difference. These pieces can be easily rearranged or adapted to fit different spaces, making them perfect for transitional stylists who love to switch things up every few months.

Layered lighting: Lighting plays a crucial role in transitional spaces. Incorporate different light sources – from ambient and task lighting to accent lights. This layered approach not only provides functionality but also adds depth and warmth to the apartment.

Temporary touches: Renters often face restrictions when it comes to permanent changes. But that doesn’t mean you can’t achieve the transitional style. Removable wallpapers, peel-and-stick tiles and adhesive hooks can transform spaces without compromising the apartment’s original state.

Personal artifacts: Just because it’s transitional doesn’t mean it can’t be personal. Integrate family heirlooms, personal artworks or cherished collectibles. These items add warmth to any room and tell a story, making even the most cookie-cutter apartment unit feel like home.

Remember to rely on balance

Transitional style is about balance. It embraces change while respecting tradition. This approach offers apartment renters the flexibility to evolve their decor over time without straying too far from the foundational elements that make their space feel like home. With careful planning and a keen eye for design, any apartment can radiate the effortless elegance of transitional style.

Traditional and modern meet in transitional design

The beauty of transitional style lies in its innate ability to resonate with a wide range of audiences. It’s a symphony of eras, harmonizing the classic charm of traditional pieces with the sleek essence of contemporary design. As we’ve explored in this article, mastering this style isn’t about strict rules or rigid definitions; it’s about embracing fluidity, adaptability and a keen eye for balance.

As spaces continue to evolve and reflect the multifaceted personalities of their inhabitants, transitional style stands out as a testament to timelessness, bridging the past and the present in an expertly choreographed dance of design perfection.

Still looking for that perfect space to showcase your style? Browse our available apartments for rent here.

A native of the northern suburbs of Chicago, Carson made his way to the South to attend Wofford College where he received his BA in English. After working as a copywriter for a couple of boutique marketing agencies in South Carolina, he made the move to Atlanta and quickly joined the Rent. team as a content marketing coordinator. When he’s off the clock, you can find Carson reading in a park, hunting down a great cup of coffee or hanging out with his dogs.

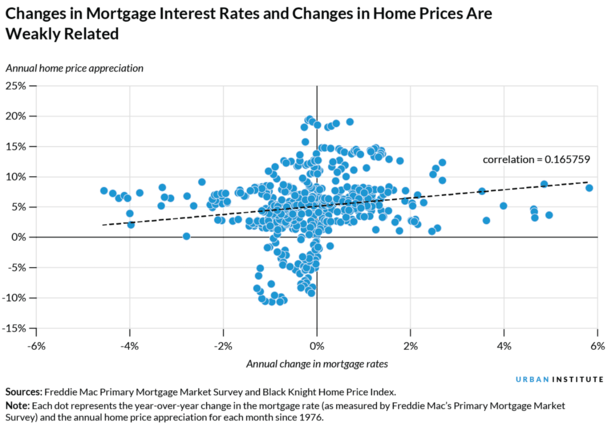

If you don’t believe mortgage rates and home prices can fall together, just look at what home prices have done in the face of 7% mortgage rates.

Despite the 30-year fixed surging from sub-3% levels to near-8% levels in less than two years, home prices hit fresh all-time highs.

So why is it so difficult to imagine the opposite scenario, where both interest rates and property values fall in tandem?

It seems the human mind wants there to be an inverse relationship between rates and prices when there often is not.

The good news is it’s possible that both rates and prices moderate from here, ushering in a better level of housing affordability.

Home Prices and Mortgage Rates Don’t Have Much of a Relationship

The Urban Institute wrote an article last year about the relationship between home prices and interest rates when mortgage rates were rapidly ascending.

They noted that since 1976, there has been “a positive but weak relationship” between the two.

In other words, higher mortgage rates are often accompanied by higher home price appreciation, though this tendency isn’t robust.

Still, it defies the logic many housing bears and everyday humans possess, where they assume higher mortgage rates must equate to lower home prices.

After all, if it becomes more expensive to purchase a home, the price must come down. That’s their argument at least.

But when you look at other necessary items (shelter also being a necessity), people don’t stop buying them because the cost goes up.

And one also needs to consider why mortgage interest rates are high to begin with. Often, interest rates are high because the economy is running hot.

This means there are more consumers out there making more money, which ostensibly means more of them can afford to buy expensive houses.

One other factor to consider is all-cash buyers – a large percentage of home buyers forgo mortgages to get the deal done, especially investors.

So while higher interest rates might affect the average home buyer, they don’t affect everyone.

Home Prices and Inflation Have a Strong Positive Relationship

While higher mortgage rates and home price appreciation have a weak, but still positive relationship, inflation and home price appreciation have a strong one.

That is to say that a higher rate of inflation is associated with higher home price appreciation.

And this association is significantly stronger than the relationship between mortgage rates and home prices.

Inflation has been front and center for the past couple years, and the Fed has been actively fighting it via 11 fed funds rate hikes since early 2022.

At the same time, home prices haven’t fallen, though the rate of appreciation has. Still, when you consider the 30-year fixed more than doubling in such a short time span, you’d expect housing market carnage.

Instead, we’ve seen home prices hit new all-time highs. Last week, the FHFA reported that home prices were up 0.8% in July from a month earlier, and up 4.6% year-over-year.

While that might sound too good to be true, consider that high interest rates are often correlated with periods of strong economic growth, low unemployment, rising wages, and high inflation.

Put another way, when the economy is hot, home prices tend to rise because more people have money and jobs to support mortgage payments, even if they grow larger.

This means housing demand can increase or at least remain steady, even if affordability erodes over time.

Housing Affordability at Its Worst Since 1984

Of course, affordability has worsened significantly of late because both rates and prices have continued to rise, pushing the national payment-to-income ratio to its highest level since 1984.

Per Black Knight, it takes a $2,423 principal and interest payment to purchase the median-priced home with 20% down and a 30-year fixed mortgage.

This is up 91% from $1,155 just two years ago, when the Fed ended Quantitative Easing (QE) and began their campaign known as Quantitative Tightening (QT).