Buying your own debt for pennies on the dollar might seem like a great way to get out of debt fast. However, you can’t actually do this due to how debt buying works. Debts of this nature are sold in large bundles to debt collectors and other agencies. Learn more about how debt buying works, why it’s not an answer to your debt concerns, and what you can do to handle debt instead below.

In This Piece

How Debt Buying Works

Debt buying occurs when creditors gather old debts—also sometimes called bad debts—into portfolios. They sell these portfolios of debts to debt buyers at a fraction of the original value of the debt.

For example, imagine a credit card company that has thousands of delinquent accounts. It may gather 1,000 old accounts that are 180 days or more past due. Say the average owed on each of these accounts is $1,000—that would be a total of $1,000,000 in old debt.

The credit card company might sell the debt at a fraction of that value, such as 15 cents on the dollar. In that case, the debt buyer would purchase the debt for $150,000.

Once the debt buyer purchases this portfolio of debt, they can either try to collect on the original debt or sell the debt. In many cases, the debt buyers go through the portfolio, keeping debts they think they can collect and selling off others in a similar method.

If the debt buyer is able to collect any of the debt, the money is theirs to keep. So, in the hypothetical example above, if the debt buyer collects $250,000 of the original $1,000,000 in debt it purchased, it makes a profit of $100,000.

Why Are Debt Buyers Used?

The reason original creditors use debt buyers is that at some point, they consider debt uncollectible. They don’t want to spend any more of their own resources trying to collect on the debt. They could simply write the debt off and be done with it, but if they sell the debt to a debt buyer, they’re able to recoup at least some of their losses.

Many common types of debt can be sold to debt buyers. These include but aren’t limited to:

Credit card debts

Medical debts

Unpaid utility bills

Debts related to auto loans or mortgages

Can You Buy Your Own Debt?

You can’t buy your own debt because no one sells individual debts. It doesn’t make business sense on either side to do so. Instead, debts are sold in huge portfolios that cover many accounts. It would be difficult to impossible to discover what bundle of debt your debt would be placed in before the lender sells it off, never mind that you would likely pay more than your debt is worth to purchase both your debt and the debt of hundreds of other people.

For the creditor, selling off large sets of old, uncollected debt is a way to write things off the books while getting at least some payment. For the debt buyer, buying a large portfolio of debt at pennies on the dollar is a conservative gamble. Debt buyers hope that by investing in many accounts they’re able to collect money on some of them.

How to Deal With Debt Buyers

Because you can’t buy your own debt, someone else might. Here are some things you can do to deal with debt buyers if they end up holding your old debts:

Make sure it isn’t a zombie debt. These are debts that have already aged out of the statute of limitations for collection. However, they’ve risen to the top of a debt buyer’s or collector’s books, and someone is trying to resurrect them.

Negotiate to settle the debt. Debt buyers didn’t buy your debt for full price, so they don’t have to collect the full amount to make a profit. They’re often motivated to settle at less than the amount owed if you could pay them immediately.

Stand up for your rights. Your rights as a consumer are protected under federal and state laws. Make sure you understand your rights so you can stand up for them as you deal with debt buyers and collectors.

Manage Your Debt Better

Managing your debt in a responsible and proactive way can help you avoid debt buyers altogether because you never let your debts get so delinquent they might be sold. Some things you can do to manage your debt include:

Creating and sticking to a budget. When you’re spending within your means and making debt decisions that work with your budget, you’re less likely to fall behind on payments.

Pay all your debts on time. Use tools such as debt management apps to reduce the chance you might forget a debt or lose track of one.

Being proactive with debts. If you find yourself in a position where it’s impossible to keep up with a debt, such as being temporarily unemployed or dealing with a medical crisis, reach out to the creditor immediately. Many creditors have programs and options to help you deal with this type of issue.

Know what’s on your credit report. Keep up with your credit report so you don’t end up with old debt you thought was paid off coming back to haunt you. You can get a copy of all three of your major credit reports and track 28 of your credit scores when you sign up for ExtraCredit.

Does being an authorized user affect your credit? Well, becoming an authorized user can help you build your credit under the right circumstances. Before you agree to be an authorized user or add an authorized user to your account, it’s important to understand the potential risks and benefits. This article provides more information about how adding an authorized user works and how it could impact your credit.

In This Piece

What Is an Authorized User?

An authorized user is a person who has the authority to use another person’s credit card account. In many cases, the authorized user receives a credit card in their name. Unlike co-signers and joint account holders, authorized users aren’t financially responsible for making payments.

Typically, cardholders only add someone they trust, such as a child or significant other, as an authorized user. There are a few reasons a cardholder might want to add an authorized user to their account, including:

To help the person build their credit history

To make it easier for the authorized user to make payments when the cardholder isn’t available

To allow someone to make purchases on the cardholder’s behalf

The primary reason a person wants to become an authorized user is that they’re unable to secure a credit card on their own. For example, a child may not have the established credit to get a credit card, so a parent adds their child as an authorized user under their account.

Authorized Users Versus Joint Accounts

Authorized users aren’t the same as joint account holders. Authorized users can charge money to your account, but they can’t add other authorized users and they can’t dispute charges. They also can’t request credit limit increases, transfer balances, or close your account.

In contrast, joint account holders can do all of those things and more. Joint account holders are jointly liable for the account, and they’re also jointly liable for repayments.

How Do Authorized Users Work?

The process of adding an authorized user to your account varies between credit card companies. Some credit card providers may have age and other requirements that must be met before you can add an authorized user. You may also be able to set limits on how much the authorized user can charge to your credit card.

You’ll need basic information about the person you’re adding, such as name, date of birth, and Social Security number. You should contact your credit card company directly to see how this process works.

Once the application process is complete, the authorized user receives their card. They can use it just like any other credit card. Depending on the specific credit card company and your preferences, you may be able to give the authorized user access to your account information so they can track packages and report a lost card, errors, or potential fraud. Keep in mind that giving the authorized user access to your account may also allow them to see your purchase history and redeem special rewards.

It’s important to note that authorized users don’t receive credit card bills and aren’t responsible for making payments. This responsibility lies solely with the cardholder.

Can I Build Credit as an Authorized User?

For a long time, authorized users were able to build credit by “piggybacking” on the primary account holder’s own good credit record. Many modern scoring models no longer recognize this loophole—but a few still do. If you’re hoping to build credit by becoming an authorized user, you need to do two things:

Check if the card company reports authorized users to credit bureaus.

See if authorized users are reported as if they’re account holders.

If the account holder’s card company does report authorized user activity, you’ll see an individual account on your credit report. Providing the primary cardholder continues to make payments and handle the account responsibly, you’ll likely benefit from the listing.

Can Adding Authorized Users Hurt Your Credit?

Before adding an authorized user to your credit card account, you need to ask yourself several questions.

Does adding an authorized user affect my credit?

Will adding an authorized user hurt my account?

Will adding an authorized user help their credit?

The answer to these questions depends a lot on your specific credit card company. Not all credit card companies report authorized users to the credit bureaus. If your credit card company doesn’t report authorized users, adding them to your account will have no impact on their credit score. If, on the other hand, your credit card company does report authorized users, it can help them start building up credit.

Either way, adding an authorized user to your credit card account shouldn’t automatically effect your credit history. However, there are several ways taking this step could hurt your credit score over time.

First, if the authorized user charges too much to your credit card, you may have difficulty making your monthly payments. Payment history makes up 35% of your FICO score. So if you can’t make your monthly payment because of charges accrued by an authorized user, your credit profile, and wallet, could take a hit. If possible, set limits for how much your authorized user can charge to your credit card account. This step can help to reduce the risk of overspending.

Secondly, additional charges to your credit card account can also increase your credit utilization ratio. The more you charge to your credit card, the higher your credit utilization ratio is. Your outstanding debt accounts for about 30% of your overall credit score. You should try to keep your debt ratio under 30%.

What if an Authorized User Misuses Their Card?

Let’s imagine you are the primary account holder, and your teenager is the authorized user. What would happen if they decided to buy a new wardrobe without telling you? The answer is simple—you’d be on the hook for the whole amount. Your wallet could take a serious hit.

Does Removing an Authorized User Hurt Their Credit?

If your authorized user doesn’t behave, you can remove them from your account pretty quickly. At that point, they can no longer use their card and can’t charge any more money to your account.

Credit age history makes up 15% of your credit score. If your credit card company previously reported the authorized user as an individual account holder and they suddenly get removed from your account, the removal might look like a closed account, regardless, it will likely be removed for age calculations. In that case, the formerly authorized user’s credit score could dip.

Does Being an Authorized User Affect Your Credit?

Becoming an authorized user could affect your credit if the credit card company reports your status to the credit reporting agencies. If the credit card company doesn’t report your authorized user status, taking this step won’t impact your credit score at all. However, you’ll still have the benefit of charging purchases to a credit card.

How being an authorized user impacts your credit depends largely on the cardholder’s payment history. If the cardholder has a strong history of making on-time credit card payments, it could help you build your credit and increase your credit score. On the other hand, if the cardholder has frequent missed or late payments, it could hurt your credit score.

It’s important to understand the cardholder’s credit history before agreeing to become an authorized user. It’s also important to repay the cardholder for any purchases you make as quickly as possible. This step will help the cardholder make their payments on time.

How Long Does It Take an Authorized User to Show Up on Credit Report?

It takes about 30 days for your authorized user status to reflect on your credit report. However, not all credit card companies report authorized users to the credit bureaus. In these cases, your credit report may never show that you’re an authorized user.

What to Consider About Authorized Users

If you want to build your credit by becoming an authorized user, start by talking to friends and family members you trust. Be sure the cardholder has good credit and makes on-time payments.

If a friend or family member agrees to add you as an authorized user, it’s important to set clear boundaries right from the start. For example, determine your specific credit limit right away and whether the cardholder wants you to ask for permission before using the card.

You also need to make a clear payment agreement. Determine exactly how much you’ll pay each month and the date monthly payments are due. Make sure you create a budget so you know exactly how much you can afford to pay each month. Also, be sure to track your purchases so you know exactly how much you owe.

It’s crucial to have this agreement in place before becoming an authorized cardholder. This agreement allows you to know exactly what’s expected of you. It can also help you determine if this is the right option for you.

Four Tips to Bear in Mind

Set clear spending rules before you make family members authorized users.

Talk to prospective authorized users about credit, including credit utilization.

Set up text message alerts to make sure you know when authorized users make purchases.

Remove authorized users if they don’t stick to the rules you make.

Simply Adding Authorized Users Won’t Hurt Your Credit—but Be Careful

Ultimately, authorized users aren’t a threat to your credit unless they misuse your credit card account. Many authorized users coexist happily with main account holders for many years. Problematic authorized users, unlike joint account holders, can be easily removed.

If you’re thinking of adding an authorized user and you want to keep track of your credit, why not subscribe to ExtraCredit from Credit.com? ExtraCredit is great if you’re an authorized user—tools like Build It can help you strengthen your credit profile by letting you add rent and utilities as trade lines to your credit history.

A hard credit inquiry is when a credit card issuer or another lender reviews a credit report as part of your credit application. Their request to review your credit will be shown as a hard inquiry on your credit report and will affect your credit score.

Let’s say you’re looking to apply for a new credit card. Whether you want to expand your available credit, create a credit mix, or simply apply for a credit card online with your desired rewards, you’ll often encounter a hard inquiry.

A hard credit inquiry—or a hard credit check—is a natural part of the credit card application process. It happens when the lender or bank associated with your credit card company checks your credit report to see if you are eligible for acceptance.

What Are Hard Inquiries?

Hard inquiries—or hard credit checks—occur whenever a lender or bank accesses your credit account. The credit bureaus log the activity, recording the date and the name of the company or entity that accesses it.

Hard inquiries refer to when a lender accesses your credit report to evaluate your merit as a borrower. In other words, hard inquiries happen when lenders look at the information in your report to decide whether to approve or deny your credit card application.

How Do Hard Inquiries Impact Your Credit?

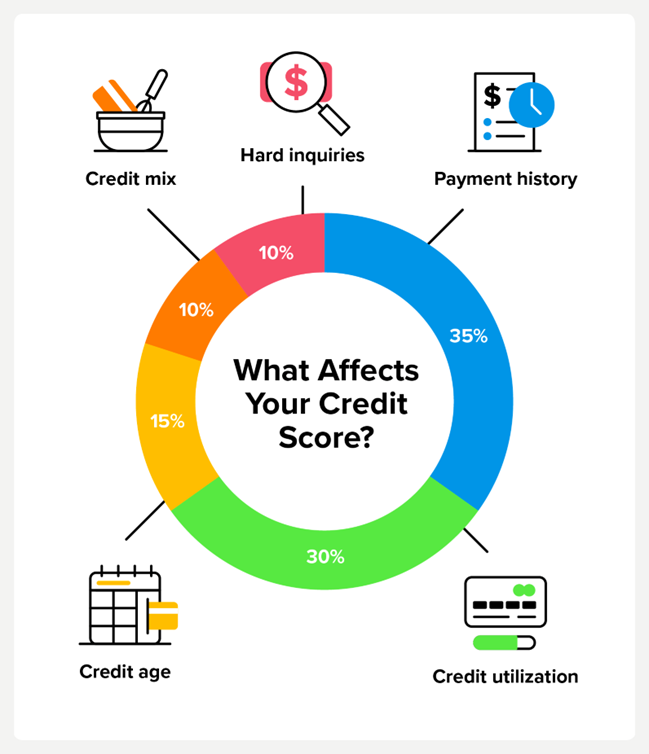

Hard inquiries aren’t the most impactful thing that affects your credit score, but they are one of the five major factors that make up your credit score. That’s because having many hard inquiries on your account looks like you’re chasing credit. Lenders don’t want to see that behavior from potential borrowers as it reduces their credibility.

Here are the five factors that impact your credit score:

Payment history accounts for around 35% of your credit score. This factor is whether you pay your bills on time and as agreed upon.

Credit utilization accounts for around 30%. This reports how much of your available revolving credit limit you’re actively using.

Credit age accounts for around 15% of your score. This is how long you’ve had credit and the age of your oldest accounts.

Credit mix makes up around 10% of your credit score. Creditors want to see that you can manage different types of accounts, such as revolving and installment accounts.

Hard inquiries affect around 10% of your score. This is the number of recent hard inquiries on your report.

Hard Inquiries vs. Soft Inquiries

Not all inquiries that show up on your credit report impact your score. Only those that evaluate your financial creditworthiness do—these are hard credit checks.

Soft inquiries, which are purely informational, have little to do with credit and don’t have the same impact. They’re also not usually visible to lenders or banks—only you.

Hard inquiries

Soft Inquiries

Affect your credit score

Don’t affect your credit score

Count against your credit score for 1 year

Appear only to you on your credit report

Occur during the approval process

Occur during pre-approval processes

Happen when you’re actively searching for credit

Happen during noncredit screenings and background checks

Require your authorization

Do not require authorization

Examples of Hard Inquiries

Hard inquiries happen when you apply for a line of credit that will impact your financial health. Hard credit checks will affect your credit score and stay on your credit report for a year or two, so having too many of them in a short period may hurt you in the long run.

Credit card companies, car dealerships, banks, lenders, and others may perform a hard credit check only after your written approval—you will always know when a hard credit check will happen.

Examples of things that will require hard inquiries include:

Examples of Soft Inquiries

Soft inquiries typically happen for nonfinancial inquiries and don’t affect your credit score. Typically, only you can see the soft credit checks on your report. Soft credit checks also don’t need your permission to happen. Though employers will request permission for background checks, creditors can run a soft credit pull to prequalify you for marketing purposes. Note that you do have the opportunity to opt out of those soft checks, though.

Soft inquiries happen when:

Employers run background checks

Credit card companies do a pre-approval process

Utility companies screen you

You check your credit report

Disputing Hard Credit Inquiries

You should always review the hard inquiries on your credit report to ensure that you authorized them. If you see something on your credit report that you didn’t authorize or approve, you can dispute your hard inquiry by following these steps:

Reach out to your current lenders and confirm that they didn’t create a hard credit inquiry for your credit.

Research the creditor that authorized the hard inquiry. Sometimes, they will remove the inquiry from your report.

Open a formal dispute with the credit bureaus. You will normally do this by filing a dispute on an online platform.

You will generally need to wait around 30 days (give or take) before receiving a reply about your hard inquiry dispute. When the credit bureaus reach a conclusion, they will remove the hard inquiry from your credit report.

Frequently Asked Questions

How Long Do Hard Inquiries Last?

According to Experian®, hard inquiries remain on your credit report for 25 months. However, they only tend to impact your credit score in the first 12 months.

How much a hard inquiry affects your credit depends on various factors, including what your credit score was to begin with. Experian notes that a hard inquiry can bring your score down 5-10 points on average. The drop might be even less if you have excellent credit and no other issues.

How Many Hard Credit Inquiries Is Too Many?

There’s no set number of inquiries that are too many. If you suddenly have a lot of inquiries, it can look bad to potential creditors. And if you’re losing up to 10 points for each one, you could drop from excellent or good credit to fair or poor credit with just five or more inquiries.

Spacing out the inquiries and ensuring that your credit report doesn’t take a hit can help minimize these issues. It also gives your score time to recover before another inquiry.

Are Hard Inquiries Bad?

Not necessarily. They’re simply an aspect of how credit reporting works—it’s actually good that this information gets recorded. Knowing who accessed your personal credit information and why can help keep you informed on your credit application history.

That said, hard inquiries aren’t neutral. They can impact your credit, so you want to keep them to a minimal number when possible.

What Triggers a Hard Inquiry?

Any time you apply for credit-related accounts with a lender, you will trigger a hard inquiry that will appear on your credit report. It’s important to remember that you will always authorize hard credit checks, so be mindful of how you space them out and what loans you need at what times.

Minimize Your Hard Inquiries

So, how do you reduce the impact of hard inquiries on your credit score? Nowadays, it can be challenging to go through life without ever applying for credit. But you can follow the steps below to reduce how hard inquiries impact your score:

Don’t spread out loan shopping: Credit scoring models know that you’ll want to shop around for the best rates. Because of that, multiple applications for credit during short periods can appear as a single inquiry on your credit report.

Don’t apply without confidence: Understand your credit score and what type of credit you are likely to qualify for, and only apply when you need the credit. Otherwise, you’ll rack up hard inquiries for no reason.

Manage other aspects of your score responsibly: Make payments on time, keep your credit utilization low, and manage multiple types of accounts well. These all have more impact on your credit score than hard inquiries.

Keep tabs on your credit report: The last step in minimizing hard inquiries is tracking your report and score. Check your credit regularly to see where you stand and whether potential mistakes could bring down your score.

You can check your Vantage 3.0 score with Credit.com’s free Credit Report Card or get many versions of your FICO® Score with ExtraCredit®. Neither of these options constitutes a hard inquiry, so using them won’t hurt your credit.

The number on your credit card is more than a passcode to payments when you swipe your card. Many of the digits have a specific meaning. Find out what a credit card number is, what it means, and why it matters.

In This Piece

What Is a Card Number?

A credit card number is a unique number that helps identify your account and card. This number makes it possible for you to pay with the card and for money to be taken out of the right account.

Think about it similarly to your checking account number. Your personal checks are printed with a specific series of numbers. First is the routing number, which indicates which bank the check draws on. Next is the account number, which tells which account the money should come from.

Credit card numbers work the same way. Each part of that long number has a specific function. These are standardized by the International Organization for Standardization (ISO).

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

How to Tell the Credit Card Type by the First Four Digits

The first digit in any credit card number tells you what type of card it is—Visa, Mastercard, Discover, or Amex. Card numbers of each type always start with the same number:

3: American Express or cards under the Amex umbrella

4: Visa

5 or 2: Mastercard

6: Discover

American Express goes even further by starting card numbers with either 34 or 37, depending on the secondary branding on the card.

That first digit plus the next five in the credit card number is called the Issuer Identification Number (IIN) or Bank Identification Number. This identifies the credit card company and its network, similar to the bank routing number on a personal check.

In some cases, the IIN may be eight digits. To allow for more IINs to support growing needs, the ISO is requiring the financial industry to move to eight-digit IINs.

The rest of the digits in your credit card number, with the exception of the final number, are related to your specific account. They aren’t necessarily the same numbers that appear in the account number on your statement. But this string of numbers is tied to your account so that payment processes use the right account when you make a credit or debit card payment.

The last digit of a credit card number is known as the check digit. This number is applied in an unusual formula that helps determine if your credit card number is valid when you enter it. Using this formula, it takes only a fraction of a second for a computer to confirm that a credit card number is valid.

What Do the Last Four Digits on a Credit Card Mean?

The last four digits of your credit card number don’t actually mean much on their own, but there’s a reason you might be asked for them. If you save a credit card in an online account or other database, the information has to be encrypted. Employees of that company can’t just look up accounts and see full credit card information. They’re usually only able to see the last four digits.

You might be asked to confirm those numbers to ensure the right card is being charged. You might also be asked to confirm them when buying something online with a saved card number to ensure you’re really you and not someone who’s hacked into an account.

You can’t tell a credit card number by the last four digits. However, you could find a credit card you’ve saved in an account, such as on Amazon, by the last four numbers. Those are the only digits you’ll be able to see when you look at the saved payment methods in your account.

How Many Numbers Are in a Credit Card?

Typically, credit card numbers are 16 or 15 digits. Only American Express uses the 15-digit format. Around 2020, Visa started issuing some cards with 19-digit card numbers, but these aren’t typically used in the United States.

Finding the Right Credit Card

Before applying for a new credit card, determine what kind of credit card you need. For example, if you want to maximize rewards, you may want a cash-back card with perks that match your budget. If you’re looking to build credit, you may need to apply for a secure credit card that’s easy to get with lackluster credit.

To understand what options might be right for you, check your credit. This helps you know what type of credit card you might be approved for.

Then educate yourself about applying for a credit card online. Review options that seem appropriate for you and pick the best one. You can get started in our credit card marketplace. Gather all the information you need and apply.

This correlation between the average cost of living and credit card limit continues when we look at the 10 states with the lowest average credit card limit. In the chart below, the states marked with an asterisk are also on the list of states with the lowest cost of living.

State

Average Credit Card Limit

Average Credit Score

Mississippi*

$21,676

667

Arkansas

$24,570

683

West Virginia*

$24,684

687

Alabama*

$25,621

680

Louisiana

$25,781

677

Kentucky

$25,962

692

Oklahoma*

$26,041

682

Indiana*

$26,676

699

Idaho

$26,871

711

Iowa*

$27,052

720

Source: Experian, Wisevoter

How Are Credit Card Limits Determined?

Credit card companies use several factors to determine your limit, which they review periodically over time. Some factors count more than others, varying by the credit card issuer.

Your Credit Score

A higher credit score indicates you are more likely to pay your debts, which tells credit card issuers you are lower-risk. As a result, people with higher credit scores often have higher credit card limits.

According to FICO®, a variety of factors determine credit scores, including:

Payment history: Your payment history determines 35% of your credit score, which shows how likely you are to pay your debts on time.

Credit utilization rate: Your credit utilization rate is the ratio of the debt you owe to the total amount of credit available to you. You can factor your credit utilization rate by dividing your current balance by your total credit limit and multiplying the result by 100. A healthy credit utilization rate is considered anything below 30% —any higher and potential lenders may consider you overextended.

Length of credit history: The longer your credit history, the better picture a lender has of your risk level. A short history isn’t necessarily bad unless it contains a poor payment history and high utilization rate.

Recent hard inquiries: A hard inquiry is a record of a lender checking your credit. Too many hard inquiries in a short period can lower your credit score temporarily, so experts recommend six months between hard inquiries.

Credit card companies also use your credit score to determine your interest rate, so keeping an eye on your score with free credit reports is important.

Monthly Income

Credit card issuers want to know if you have monthly income to ensure you can pay your debts. The higher your monthly income, the more likely you are to get approved for a higher credit limit.

Monthly Expenses

Credit card companies look at your total monthly expenses, especially compared to your monthly income. Generally, they’ll look at your monthly housing costs (mortgage or rent), although they may also ask for information about other regular expenses such as utilities. Your monthly expenses are then compared to your monthly income to determine your credit card limit.

High monthly expenses won’t hurt your credit card limit as long as your monthly income is high enough to cover them.

Debt-to-Income Ratio

Credit card issuers also examine your debt-to-income ratio when determining your credit card limit. Experts consider anything under 36% to be a good debt-to-income ratio for a credit card.

To calculate your DTI ratio, divide your total recurring monthly debt (mortgage, auto loan, student loans, existing credit card debt, etc.) by your gross monthly income (how much you make before taxes) and multiply the answer by 100.

Your History with the Issuer

If you already have a positive credit history with the company issuing the credit card, they may be more likely to give you a higher credit limit. However, if they feel you have too many cards or a rocky credit history with them, they may issue a lower credit limit.

The Issuer’s Credit Approval Policies

Every credit card company wants to avoid risk and crafts a specific set of policies to determine how much credit to extend to a cardholder. Its policies may consider elements not listed here or weigh factors differently than another company, which is why credit card limits are not standard across companies.

Current Economic Outlook

When the economy is healthy, credit card companies may be more open to taking risks and offer higher credit card limits. However, when the economy is uncertain, such as during the pandemic, issuers are less likely to take risks, offering lower credit card limits for new cardholders.

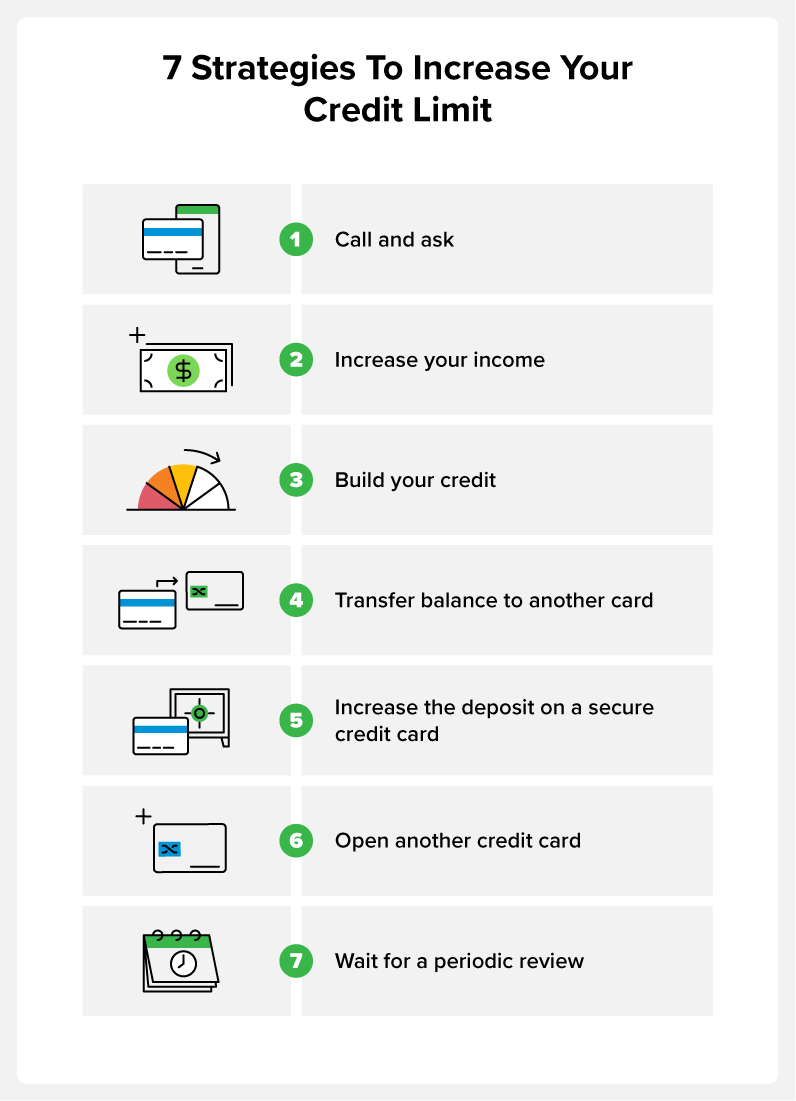

How to Get a Higher Credit Limit

A low credit card limit isn’t necessarily bad, but it can make getting approval for additional loans or credit challenging if your credit utilization rate is too high. It can also put large purchases, such as an appliance or unexpected car repair, out of reach.

To get a higher credit card limit:

Call your credit card issuer and ask for an increase. Call the customer service number on the back of your card and ask the representative for a higher credit card limit. Only consider this if you are trying to lower your credit utilization rate to raise your credit score. They look for six months of on-time payments and will ask for updates on your annual income, employment status, and monthly expenses before deciding.

Increase your income. Since monthly income is a factor in your credit limit, increasing your monthly income can boost your credit card limit. Ask for a raise at work, get a second job, or start a side hustle. When your credit card issuer sees you have more income, they may offer you a higher credit limit. You can update this information with them anytime by contacting them directly, or you can wait until they discover it in a periodic review of your status.

Build your credit. Pay your bills on time and pay down debt to increase your credit score. Over time, your credit score should increase, which can lead your credit card issuer to raise your credit limit.

Transfer the balance from one card to another. Some credit cards allow you to transfer debt from one account to another in a credit transfer. If you have multiple credit cards and one allows credit transfers, transfer the debt from one card to another. This won’t increase your credit card limit overall, but it can increase the amount of credit available on a specific card.

Increase your deposit on a secure credit card. If your card is a secured credit card, your credit card limit directly correlates to your security deposit. Add more to your security deposit, and you’ll have a higher credit card limit.

Open another credit card. This won’t increase the credit card limit on your current card, but it will expand how much credit is available to you. Avoid temporarily dinging your credit score by waiting six months between credit card applications.

Wait. Most credit card companies annually review your account, and as long as you pay your bills on time, they can likely naturally increase your credit card limit.

You can also always pay off purchases immediately rather than waiting until the end of your payment period to gain access to more credit without increasing your credit limit.

Credit scores strongly indicate what your potential credit card limit will be, so learn more about yours today. Before applying for a new credit card, get a sense of where you stand with a credit report card. Then use the tools and features in ExtraCredit to see where you need to work toward your credit goals to qualify for a higher credit card limit.

FAQ

Here are some answers to common questions regarding credit card limits.

What Happens if I Go Over My Credit Limit?

If you try to make a purchase over your credit limit, most credit card companies will deny the transaction. Some may allow the purchase but charge a fee, although most companies have abandoned this practice.

If I Request an Increase to My Credit Limit, Will That Impact My Credit Score?

When you request an increase to your credit card limit, your credit score may drop if your credit card issuer places a hard inquiry on your credit score. This can temporarily lower your credit score, and not all credit card companies do so.

Getting a credit card is like taking a step toward financial adulthood. It brings you into the world of building credit and paying bills, which almost everyone has to deal with at some point, so it can help to get started as soon as possible.

But the “firsts” of adulthood aren’t always easy, and that includes getting your first credit card. A Credit.com reader recently asked where to start:

Hi, I am 18 years of age, I have no credit history, and I have low income. I’m wanting to get my own place, and would love some help finding a good credit card to build my credit that will accept my low income.

There are three main things that will affect whether or not someone like our commenter could get a credit card: the person’s age, the fact that they have no credit and the amount of money they make.

Privacy Policy

1. Can You Get a Credit Card at 18?

Let’s start with age. Per the Credit CARD Act of 2009, consumers younger than 21 must have proof of independent income or a co-signer in order to get a credit card. It makes sense: If you’re going to get a credit card, you need to be able to show that you can pay your balance.

Why Would I Want to Have a Credit Card at 18?

Having a credit card at 18 can help you to start building your credit early. It also allows you to make purchases that may require a credit card, such as a car rental.

2. Do You Make Enough Money?

That brings us to income. Since this commenter referenced wanting to live independently, it seems unlikely that they’d opt for a co-signer. That means this person would need to provide proof of their income. We don’t know exactly what our commenter means by “my low income” — even if it’s not a lot, it isn’t necessarily a credit card deal-breaker. You could always try to ask a credit card issuer what sort of income they’re looking for among card applicants, but you may not get an adequate answer, given that there’s more that goes into getting approved for a credit card than income.

3. Consider Becoming an Authorized User

If you’re wondering how to get a credit card at 18, becoming an authorized user may be your best solution. An authorized user has permission from the cardholder to use their account to make credit card purchases. Typically, you receive a credit card with your name on it, but there might be limitations as to how much you can spend.

If the credit card company reports authorized users to the credit bureaus and the cardholder makes on-time payments, this option could help boost your credit. As an authorized user, you’re not directly responsible for making monthly credit card payments. Instead, you should make a payment agreement with the cardholder to ensure your bills are paid on time.

4. Get a Secured Credit Card

At 18, it’s likely you have little to no credit history. This factor could prevent you from obtaining a traditional credit card. Despite your lack of credit history, you could qualify for a secured credit card. This type of card requires you to pay a cash security deposit to open the account.

For example, you might need to pay a cash security deposit of $500 to open a credit card with a $500 credit limit. With secured credit cards, monthly payments are typically reported to credit reporting agencies. In many cases, you can increase your credit limit without an additional cash security deposit after several months of making on-time payments.

Get a Student Credit Card

If you’re a college student, you may qualify for a student credit card. These cards are specifically for full- and part-time students at higher education colleges or universities. Credit requirements are typically lower for student credit cards, especially when it comes to the length of credit history.

If you have little to no credit, you may have a better chance of securing a student credit card than a traditional credit card. Keep in mind that credit card companies must still adhere to the regulations of the Credit CARD Act of 2009. So, you still need to have a cosigner, have proof of income or meet other requirements for a student credit card.

5. Ask Someone to Cosign for You

Another option for obtaining a credit card at 18 is asking someone you trust to be a cosigner on the account. This method can help if your cosigner has a good credit score. Both you and the cosigner are responsible for making payments.

How to apply for a credit card at 18 with a cosigner? Unfortunately, none of the major credit card companies allow for cosigners. If you can’t find a credit card you like that allows for a cosigner, you could opt for a joint credit card account. With this type of account, both parties remain responsible for making payments, but it’s likely your cosigner will be listed as the primary cardholder on the account.

Tips to Help You Manage Your Card

Obtaining your first credit card can be exciting, but it also comes with great responsibility. How you handle your credit card purchases and payments can impact your credit score for years to come. It’s important to set up good practices now to protect your future finances.

Set Up Automatic Payments

Setting up automatic payments is a great way to ensure your bills are paid on time. You can use your credit card to pay your bills and then pay your credit card bill by the due date. This process can help you build a strong payment history, which accounts for 35% of your credit score.

Build a Budget

The best way to avoid overspending is to build a budget. Start by tracking your spending for a month and use that information to develop an accurate budget. Be sure to set some money aside each month in a savings account in case of an emergency.

Pay More Than the Minimum Payment Every Month

One of the most important things when it comes to having a credit card is to be sure you’re making at least the minimum payment every month. If possible, you can pay more than the minimum balance to avoid paying interest.

Only Buy Things You Know You Can Pay Off

When you have a credit card, it can be tempting to make large purchases that you might not be able to afford without the credit card. Avoid this temptation. If you buy things you can’t afford, you run the risk of not being able to make your monthly payments.

Late payments can have a negative impact on your credit score. Using up all of your available credit can also reduce your credit score.

Be on Top of Your Statements

It’s crucial that you take having a credit card seriously. Just as you do with your bank account, be sure to check your credit card statements carefully. Take note of how much available credit you have left to avoid going over your credit limit. You also want to make sure you make all your monthly payments on time.

Other Ways to Build Credit

There are several things you can do right now to start the path to building your credit.

Student loans: Student loans can do more than just help you pay college tuition. They can also help you build credit. The important thing is to make sure you start paying on these loans as soon as you’re required to do so.

Emergency fund: You’re never too young to start an emergency fund. Be sure to put a portion of your earnings into a savings account. This strategy can help you in the event of a financial emergency.

Track your credit score: Whether you’re 18 or 80, it’s important to frequently track your credit score. Credit.com offers free credit scores from Experian that are updated every 2 weeks.

Get a job: The easiest way to secure a credit card when you’re only 18 is to maintain a job. If you’re able to prove you can financially handle having a credit card, it’s easier to obtain approval.

Good credit requires responsible financial management over a period of time. However, there are some tactics you can try that help build your credit as fast as possible, if not exactly overnight. Find out more about these tips below.

In This Piece

Add Rent and Utility Payments

Your credit report and score are meant to help demonstrate whether you can manage money responsibly. But not every bill you manage gets reported to the credit bureaus.

Most landlords don’t send payment information to the credit bureaus, for example. And utility providers usually only report when you’ve defaulted on a bill. If you’re looking for how to increase your credit score quickly, getting these timely payments added to your report can be a good idea.

ExtraCredit lets you link rent and utility payments as trade lines to be reported to the credit bureaus. You can access this perk via the service’s Build It function to establish your credit by increasing your history of timely payments.

Pay Down Debt

Paying down debt is potentially one of the best things you can do for your credit. That’s because when you pay down revolving credit, you reduce your credit utilization, which has a big impact on your credit score.

It’s also helpful to pay down debt if you’ve fallen behind or have collection accounts on your credit report. Catching up past-due accounts and keeping up with them reflects positively on your score and can help you boost your credit.

Keep Utilization Low

Revolving credit includes credit cards, lines of credit and home equity lines of credit. Your credit utilization is a ratio of your total revolving credit balance compared to your total revolving credit limit.

For example, imagine you have two revolving credit accounts:

A credit card with a credit limit of $5,000 and a balance of $2,000

A line of credit with a limit of $5,000 and a balance of $1,000

You would have a total credit limit of $10,000 and a total balance of $3,000. That’s a credit utilization of 30%.

Credit utilization accounts for around 30% of your credit score. Keeping your credit utilization as low as possible—ideally below 30%—helps positively impact your scores.

Pay Bills on Time

Always pay all your bills on time. This is less a tip for boosting your credit overnight and more a tip on how not to wreck your credit overnight. One or two slips that lead to you paying bills 30 days or more past due can drastically and negatively impact your credit score.

Get a Secured Credit Card

A secured credit card is a card designed to help those with fair, poor, or bad credit build credit for the future. Getting one can help you boost your score.

Getting a credit card—and using it responsibly—can be a great way to boost your credit without actually going into debt. It might seem like a contradiction, but remember that a credit card doesn’t automatically mean debt. If you pay your balance off each month, you’re never in debt.

But you do still get some of the potential credit-boosting benefits of holding a credit card. The first is that your credit mix may be improved. Creditors like to see that you can manage multiple types of credit, and your credit score benefits when you have both installment and revolving credit.

Having a credit card also lets you address your credit utilization. If you have a credit card and you pay off the balance every month, you’ll have a lower credit utilization with a responsible payment history, which is good for your credit.

Get a Credit Builder Loan

If you already have a credit card, your credit mix might be suffering from the lack of an installment loan. Any type of installment loan—from a car loan to a personal loan—might benefit your credit score if you make your payments regularly and on time.

But for those who don’t have the credit history or score for a traditional installment loan, a savings-secured or credit-builder loan might be a good option. These loans often require deposits or savings accounts that you get back when you’re done paying for the loan, so they’re not loans designed specifically to provide for a financial need. They’re for the purpose of getting an installment loan and positive payment history on your report.

Become an Authorized User

If you don’t feel ready for your own credit card or can’t qualify for one, see if a family member will add you as an authorized user to their credit card account. Many banks and issuers report account activity to both the cardholder’s and authorized user’s credit report.

You do need to make sure you consider this option carefully. First, make sure the person you ask is responsible with their bills. If they pay their credit card bill late, you could end up with negative marks on your report.

Second, make sure the credit card company reports on authorized users. If the information doesn’t get added to your credit report, it can’t have an impact on your credit score.

Dispute Errors on Your Credit Report

Inaccurate items, such as a late payment reported when you never missed a payment, could unfairly bring your score down. Reviewing your reports and challenging errors may help improve your score. You can get a free credit report from each of the three bureaus every year at AnnualCreditReport.com. These are also available weekly for a limited time due to COVID-19.

In addition to rent and utility reporting, ExtraCredit shows you 28 of your FICO® scores and your credit reports from all three credit bureaus. You can check what’s showing up on your reports and what’s affecting your credit scores so you can follow up as necessary.

If you do find an error on your credit report during your investigation, be sure to challenge the accuracy of the error. Under law, you have a right to a credit report that’s fair and free of errors, so if information can’t be proved by the reporter, the credit bureaus may have to remove it.

Set Up Credit Monitoring Account

Invest in credit monitoring to take a proactive approach to protecting your score. By understanding exactly what’s going on with your report, you can address errors quickly and learn how your own actions impact your score. That helps you make potentially score-boosting decisions in the future.

Credit.com’s free Credit Report Card provides a snapshot of your credit report, with information about how you’re doing in the five critical areas for your score. Knowing how you’re doing can help you pinpoint areas that might need some help.

Don’t Close Accounts

This is another tip to keep from dragging down your credit score almost overnight. Keep credit cards and other revolving accounts open if you can, even if you aren’t using them. They can help reduce your credit utilization and increase your credit age, both of which are good for your score.

How Is Credit Score Calculated?

Understanding how your credit score is calculated helps you make good decisions that can boost your score. Credit scores are based on five factors:

Payment history, which is whether you pay your bills on time regularly

Credit utilization, which is how much of your open credit you’ve used

Credit age, which is the average age of your open accounts as well as how long you’ve had credit

Credit mix, which indicates you have a healthy mix of revolving and installment accounts

New credit, i.e., hard inquiries, which refers to whether a lot of lenders are checking your credit to evaluate you for loans

How Often Does Your Credit Score Update?

Credit scores typically update at least monthly, but big changes to your financial situation can boost your score or drive it down more quickly. It really depends on how often your various creditors report this information to the credit bureaus.

Work on Your Credit Now

It’s never a bad time to start working on your credit. Start by signing up for ExtraCredit so you’re in the know about your credit scores and reports and can make educated decisions to build your credit.

Do you have bill collectors contacting you about unpaid debt? If so, it’s important to understand your rights. Even if you have debt that’s still unpaid, your creditors only have a certain amount of time to take legal action against you.

So, before you think about talking to a bill collector or agreeing to a new payment arrangement, it’s important to know what the statutes of limitations are in your state. It’s these statutes that can help you determine your next step.

Keep reading to learn more about what statutes of limitations on debt collection are and how they work.

In This Piece

What Is a Statute of Limitations on Collections?

The statute of limitations on collections is the amount of time a creditor or debt collector has to file a lawsuit to collect unpaid debt. These statutes vary by state, type of debt and terms of the contract, if there is one.

Occasionally, creditors and debt collectors may try to file a lawsuit after the statute of limitations has ended. So, it’s your responsibility to provide the courts with proof that it’s past the statute of limitations. So, be sure to save any payments made or communications you had with any creditor or collections agency.

When the clock for the statute of limitations on debt begins varies from state to state. It either starts when you miss your first payment or when you have the last communication with the creditor or debt collector.

Can a Debt Collector Restart the Clock on My Old Debt?

There’s a chance that communication with a debt collector could restart the clock on the statute of limitations. For example, if you agree to any new payment arrangement or make a payment, this act could restart the clock.

Effect of Statute of Limitations on Your Credit Report

If you’re looking for ways to repair your credit, the statute of limitations has no impact. It’s important to understand that the statute of limitations doesn’t affect how long a debt can remain on your credit report. These are two different policies.

In most cases, a debt can remain on your credit report for up to seven years. This is the case even if the statute of limitations has ended. This means that while creditors may no longer be able to take you to court, your debt could still impact your credit score.

What Is the Statute of Limitations on Debt Collections by State?

Statutes of limitations on collections vary by state and by type of credit account. There are four basic types of debt:

Written debt. Written debt occurs when there’s a signed contract that details the terms of the loan. This doesn’t have to be a formal contract. It can simply be written on a piece of paper.

Oral debt. Oral debt is a verbal agreement made between two people that details the terms of the debt.

Promissory notes. Promissory notes are written agreements where you agree to make a set number of payments over a set number of years. While it is also a form of written debt, promissory notes normally include a promise to repay as well as a repayment schedule. This makes them more legally binding than a written debt or IOU. Common types of promissory notes include home mortgages and student loans.

Open-ended credit. Open-ended credit includes any type of revolving credit account, such as credit cards.

Below is a look at the statute of limitations on collection by state, broken down by debt type.

State

Written Contract

Oral Contract

Promissory

Open-Ended

Alabama

6

6

6

3

Alaska

3

3

3

3

Arizona

6

3

6

6

Arkansas

5

3

5

5

California

4

2

4

4

Colorado

6

6

6

6

Connecticut

6

3

6

6

Delaware

3

3

3

4

Florida

5

4

5

5

Georgia

6

4

6

6

Hawaii

6

6

6

6

Idaho

5

4

5

4

Illinois

10

5

10

5

Indiana

10

5

10

6

Iowa

10

5

10

6

Kansas

5

3

5

3

Kentucky

10

5

15

10

Louisiana

10

10

10

3

Maine

6

6

20

6

Maryland

3

3

6

3

Massachusetts

6

6

6

6

Michigan

6

6

6

6

Minnesota

6

6

6

6

Mississippi

3

3

3

3

Missouri

10

5

10

5

Montana

8

5

8

5

Nebraska

5

4

5

4

Nevada

6

4

3

4

New Hampshire

3

3

6

3

New Jersey

6

6

6

6

New Mexico

6

4

6

4

New York

6

6

6

6

North Carolina

3

3

5

3

North Dakota

6

6

6

6

Ohio

6

6

6

6

Oklahoma

5

3

6

3

Oregon

6

6

6

6

Pennsylvania

4

4

4

4

Rhode Island

10

10

10

10

South Carolina

3

3

3

3

South Dakota

6

6

6

6

Tennessee

6

6

6

6

Texas

4

4

4

4

Utah

6

4

6

4

Vermont

6

6

6

6

Virginia

5

3

6

3

Washington

6

3

6

6

West Virginia

10

5

6

5

Wisconsin

6

6

10

6

Wyoming

10

8

10

8

Source: The Balance

How Long Can You Legally Be Chased for a Debt?

Just because the statute of limitations has ended doesn’t mean you don’t still owe the debt. It only means that creditors and debt collectors can no longer sue you in court to collect the money due. Technically, you still owe the debt. So, debt collectors and creditors can still try to collect this money.

This means you still might receive calls from debt collectors. It’s important to understand that if you make a new payment agreement regarding an old debt, it can restart the statute of limitations for collections clock. At that point, the debt collector could sue you in court no matter how old the debt is.

Get Help Repairing Your Credit

If you’re working to repair your credit, you may want to pay your debt off even if the statute of limitations has ended. For example, if you live in a state that has a 3-year statute of limitations on credit card debt, this debt may still show up on your credit report for up to seven years.

Paying this debt may be the only way to repair your credit before the end of the 7-year period by possibly reducing the impact of this debt by paying it off. If this is the case, the credit card company may work out a deal with you for a lower amount. Sometimes, these companies agree to remove some of the interest accrued to receive some money. This can be a good option for low-income families looking to repair their credit.

Sign up for Credit.com today and take the first step toward understanding your credit and what factors are impacting your credit health.

Learning how to build credit can help if you have a bad credit score or want to improve your current score. You can start by getting a secured credit card, becoming an authorized user, or getting a cosigner on a loan.

If you have bad credit due to derogatory marks, those marks can stay on your credit report for up to seven to ten years, depending on the type of mark. A low credit score leads to higher interest rates, larger deposits, and a low approval rate for loans and lines of credit. Those just beginning to build their credit will have similar challenges, but there are ways to build or work to repair your credit score.

By learning ways to build credit, you will not only improve your financial health, but it can reduce your stress around finances as well. In this article, we go over 12 tips that can help regardless of your specific credit situation.

Table of contents:

Get Added as an Authorized User

Try a Secured Credit Card

Find a Cosigner

Report Utilities and Bills

Get a Credit-Builder Loan

Pay Your Bills on Time

Regularly Check Your Credit Scores and Reports

Dispute Errors on Your Credit Report

Pay Off Collections

Open New Lines of Credit

Request a Credit Limit Increase

Have a Good Credit Mix

1. Get Added as an Authorized User

Becoming an authorized user is one of the most popular ways to build your credit score because you benefit from someone else’s good, established credit history. Also known as “piggybacking,” becoming an authorized user is when someone adds you to their credit card account.

The odds of approval on a credit application are lower if you have a low or bad credit score, so this is a way to start building credit and improve your ability to get your own card later. When you’re an authorized user, the card company will also report the payment history for your credit report when the primary account holder uses and makes payments on their credit card.

You can have a friend or family member add you as an authorized user. While this can be a great way to build credit, it’s useful to know that this can also negatively affect your or the other person’s credit should either of you miss payments or over utilize the credit line.

2. Try a Secured Credit Card

A secured credit card is a type of credit card that most people can acquire through their bank regardless of their credit score. The primary challenge of getting a credit card with a low credit score is that your credit score is one of the wayslenders evaluate risk. If you don’t have a credit history to show that you know how to manage credit or have derogatory marks on your report, credit card companies may be reluctant to loan you money via a credit card.

Secured credit cards are different because rather than borrowing from a financial institution, you borrow from yourself. You do this by depositing money into the credit card account, which becomes your credit limit. For example, if you opened a secured credit card with a $500 deposit, you will have a $500 credit limit. As you use the card and make regular payments, these will be reported to the credit bureaus to help build your credit history and potentially help improve your score.

3. Find a Cosigner

Similar to becoming an authorized user, you can benefit from a cosigner with a good credit score. On your own, you may not receive approval on a personal loan or car loan. When you have a cosigner with a good credit score, the lender sees loaning to you as less of a risk because the cosigner is also attached to the loan.

Although a cosigner can help with the loan approval process, like becoming an authorized user, your credit can also affect that of your cosigner, so it’s important to make full and on-time payments.

4. Report Utilities and Bills

When learning how to build credit, many people don’t realize that most utilities and bills are not reported to the three major credit bureaus. Fortunately, you can purchase services that will report your utilities and bills. Services like Credit.com’s ExtraCredit® subscription help build credit history for people with no credit history or low credit scores.

5. Get a Credit-Builder Loan

Credit-builder loans do just what you think they do—they are loans that help you build credit. Unlike typical loans, where you fill out an application and receive the funds, credit-builder loans are a sort of savings program. When a bank or financial institution provides you with a credit-builder loan, the funds go into an account, and you make payments on the amount. As you make your payments, the lender reports them to the credit bureaus to help build credit history and potentially improve your score with your on-time payments.

Many credit-building programs have higher interest rates than traditional loans due to the higher risk, but they can help your score in the long term. Once you pay the credit-builder loan off with interest, you receive the full loan amount.

6. Pay Your Bills on Time

If you already have lines of credit or loans, paying your bills on time is one of the best ways to continue building your credit score. Your payment history is 35% of your FICO® credit score, which is why paying your bills on time is helpful.

One of the best ways to ensure you never miss a payment is to set up automatic payments for the minimum amount on your credit cards and bills. You can always make additional payments, but when the money comes out of your bank account automatically, you no longer have to worry about forgetting a payment.

7. Regularly Check Your Credit Scores and Reports

A great habit for building credit or trying to maintain a good credit score is to check your credit score and report regularly. Unlike a car experiencing mechanical issues, there are no warning lights or alarms that go off when your credit score drops or a negative mark appears on your report.

Checking your scores and reports lets you know if there are any issues sooner rather than later. It can also help you stay motivated as you work to build your score as you see the number start to rise.

Although your credit report doesn’t notify you about changes automatically, Credit.com’s ExtraCredit® offers credit monitoring as part of the subscription service. Credit.com also offers a free service whereyou also get your free credit report card to analyze your current score for issues that need your attention.

8. Dispute Errors on Your Credit Report

If you regularly check your credit score and credit report, you may find errors. Sometimes, bill and credit card companies don’t properly report your payments, which can hurt your credit. Credit card fraud and identity theft are also more common than you may think, and this can also cause your credit score to drop. Should you find errors on your credit report, it’s your right to challenge them. To file a formal dispute, you need to write a dispute letter showing documentation of payments and other information to the creditor reporting the error. If you have other potential errors, you can request a verification of the reporting from the credit bureaus. They will investigate then respond with the results, typically within 30 to 45 days.

9. Pay Off Collections

As you now know, derogatory marks on your credit report can have a negative impact on your credit score. When someone doesn’t pay their bills, the account becomes delinquent and a collection agency could buy it. You can find the information about the collection agency on your credit report and then contact them to pay off the debt.

In some cases, a collection agency will let you settle the debt for a fraction of what you owe. When you agree to pay off or settle the debt, you can ask for a pay-for-delete letter. After you pay off a collection agency, the derogatory mark can stay on your credit report for years. A pay-for-delete letter is an agreement that the collection agency will have the collection item removed from your report once you pay it. Get this agreement in writing!

Before negotiating with a collection agency, it’s helpful to also know your debt collection rights.

10. Open New Lines of Credit

For those with an established credit score, a good way to continue improving your credit score is to open new lines of credit. In addition to your payment history, credit utilization is the second-most important factor for your credit score. Your credit utilization is worth 30% of your FICO credit score, and new lines of credit can help keep your utilization low as long as you don’t use them.

Credit utilization is the amount you owe compared to your overall credit limit, and ideally, your utilization should be under 30%. For example, if you have five credit cards with a combined $5,000 credit limit and owe $2,500, your utilization is at 50%. If you open up a new line of credit for an additional $5,000, raising your total limit to $10,000, your utilization is now only 25% if you owe $2,500.

11. Request a Credit Limit Increase

If you don’t want to open new lines of credit but still want to build your credit, you can request a credit increase from your credit card company. This accomplishes the same thing with regard to credit utilization as opening new lines of credit. If you have a good payment history with your credit card company, they are more likely to increase your credit limit, lowering your utilization rate.

12. Have a Good Credit Mix

Your credit mix shows that you can handle multiple types of credit. The two primary credit types are installment and revolving credit. Revolving credit is a line of credit that allows you to spend up to the credit limit, make payments, and then use the credit again. Some common forms of revolving credit include:

Credit cards

Personal lines of credit

Home equity lines of credit (HELOC)

Installment loans are lines of credit that give you an amount you pay down to $0 over time, and then the account closes. Examples of installment loans include:

Auto loans

Home loans

Student loans

Personal loans

Check Your Credit and Start Building It Today

Checking and monitoring your credit scores and credit reports is the key to building your credit and maintaining a positive score. As you continue to build your credit, you may begin to save money on interest rates and have additional financial freedom as you can access more opportunities.

If you want to begin your credit-building journey, Credit.com’s ExtraCredit subscription offers credit monitoring, bill reporting, personalized credit and loan recommendations, and more. You can also access your free credit score and free credit report card through Credit.com today.

Congratulations! You’re officially an adult. Turning 18 opens a world of possibilities and freedom, but it also comes with additional responsibilities. One important responsibility to start thinking about is building your credit profile.

Credit can be a critical resource. A good credit score helps you get approved for loans and credit cards. It also helps reduce the expense associated with your debts, as you’re more likely to get approved for lower interest rates if your credit is better.

Your credit score and history can also help—or hinder—you when you’re applying for certain types of employment, a new apartment, utilities, or auto insurance. Find out more about credit and how to build credit at 18 in the guide below.

How to Start Building Credit at 18

1. Learn How Credit Works 2. Monitor Your Credit Score and Reports 3. Sign Up for ExtraCredit 4. Become an Authorized User 5. Get a Secured Credit Card 6. Apply for a Credit Builder Loan 7. Understand How Student Loans Can Help Your Credit 8. Don’t Try to Overdo It 9. Make a Budget and Stick to It

1. Learn How Credit Works

You know that knowledge is power, and understanding how to get credit and how it all works can make a big difference. Here are a few basics.

Your Credit Score

There are multiple scoring models, but they all work to provide a numerical score that tells lenders how likely you are to pay back your debts. Higher credit scores are more attractive to lenders and creditors. Five main factors influence your score:

Your Credit Report

Your credit reports are maintained by three major credit bureaus—Experian, TransUnion, and Equifax. They contain data on your current and past debts, payment history, residential history, and other information about your credit history. This data is supplied by lenders, creditors, and businesses where you have accounts. The information on these reports is fed into the credit scoring models to determine your credit score.

Here’s where it starts getting complex. The information on those reports isn’t always the same. Some businesses and lenders only report to one or two of the credit bureaus. Some don’t report to any.

So, your credit report can be a little different with each of the bureaus. That means your credit score can also vary depending on which report and scoring model is being used.

2. Monitor Your Credit Score and Reports

Once you understand some basics about credit, you should take a look at your own credit reports. Monitoring your credit is one of the best ways to learn what will positively or negatively impact your scores. It also helps you catch inaccuracies or signs of identity theft sooner. Is there an account on your report that’s not yours? It could be bringing your score down even before you learn how to start building credit! If you find inaccurate negative information on your credit report, you can challenge it.

There are a few ways to check your credit reports.

AnnualCreditReport: You can request one report per year from each of the three bureaus at AnnualCreditReport.com. The bureaus are allowing you to request your reports weekly due to the effects of coronavirus through April 2022.

Credit Report Card: You can also get information about your credit reports via the free Credit Report Card at Credit.com. This is a breakdown of how you’re doing with each of the five major factors that impact your credit score. Your personal Credit Report Card can help you understand where you might need to work to positively impact your credit.

ExtraCredit: If you’re really serious about understanding your credit reports and scores, sign up for ExtraCredit. The Track It feature lets you see 28 of your FICO® scores and credit reports from all three credit bureaus. These scores are ones that lenders look at when making approval decisions.

ExtraCredit does more than just show you your credit scores. Have you recently started paying rent or utilities? The Build It feature lets you add them as tradelines with the TransUnion and Equifax credit bureaus. That means you’ll get credit for bills you’re already paying—building your credit profile each month that you pay those bills.

This is important, because rent and utility payments don’t usually show up on credit reports. That’s simply because utility companies and landlords don’t tend to bother to report them. ExtraCredit helps you ensure you’re getting credit for those on-time payments anyway.

4. Become an Authorized User

If a friend or family member has a credit card and is an account holder in good standing—meaning they pay their bills on time—ask if they’ll add you as an authorized user. Make sure that their credit card company reports to the credit bureaus for authorized users first or this is a pointless exercise.

You don’t even need a card or to use their account. If the credit card company reports on authorized users, you’ll get their on-time payments posted to your credit reports if your friend or family member makes them.

If you’re looking for how to start building credit at 18, this can be a quick method. However, it does come with some potential risk. If that person doesn’t pay on time or runs up their credit card balance, your credit score could suffer from the negative reports too.

5. Get a Starter Credit Card

For those who want to know how to start credit building without someone else, a secured credit card might be a good place to start. Some credit card companies also offer unsecured credit cards for those with no credit. These tend to have low credit limits and may have high interest rates.

If you can’t find an unsecured credit card, though, a secured card is much easier to get in general. You have to secure it with a deposit—typically in the amount of the credit limit. For example, if you put down a $250 security deposit, your initial credit limit is $250.

You build credit by using the card and paying the bill on time each month. Make sure you opt for a credit card that reports to all three of the bureaus to maximize the benefits to your credit history. Usually after a certain number of timely payments, you get your security deposit back and may even be eligible for an increase in credit limit.

Two options you might consider are the OpenSky Secured Visa and UNITY Visa Secured card.

OpenSky® Secured Visa® Credit Card

No credit check to apply and find out instantly if you are approved

OpenSky gives everyone an opportunity to improve their credit with an 85% average approval rate for the past 5 years

Get considered for a credit line increase after 6 months, with no additional deposit required

You could be eligible for the OpenSky Gold Unsecured Card after as few as 6 months

Reports to all 3 major credit bureaus monthly, unlike a prepaid or debit card. Easy application, apply in less than 5 minutes right from your mobile device

View your FICO® Score through your OpenSky account, an easy way to stay on top of your credit

Nearly half of OpenSky cardholders who make on-time payments improve their FICO score 30+ points in the first 3 months

Your refundable* deposit, as low as $200, becomes your OpenSky Visa credit limit

Offer flexible payment due dates which allow you to choose any available due date that fits your payment schedule

*View the cardholder agreement

UNITY® Visa Secured Credit Card – The Comeback Card™

Unlike your Prepaid Card, UNITY Visa secured card can help you build your credit. Apply online in less than 5 minutes, and you could be approved today!

No Minimum Credit Score required; low fixed interest rate of 17.99%; Fully refundable FDIC security deposit* required at time of application; if you have a min of $250 to deposit immediately, you can start now!