As parents, we want the best for our children: health, happiness — and hardy credit. Having a strong credit profile can determine whether your kid gets approved for a loan or how much they’ll pay for car insurance when they’re grown. But establishing credit for someone with no credit history is challenging.

A common workaround is for parents to add their children as authorized users on their credit card accounts. Credit checks aren’t required, and the user can quickly piggyback on the primary cardholder’s credit history. But this arrangement isn’t always the right move. Here’s what to know about the potential limitations of adding your kid as an authorized user and alternative ways they can build credit.

They might be too young to reap the benefits

If you’re hoping to boost your child’s credit before they even learn to tell time, you could face roadblocks. For one, your kid may not qualify for authorized user status. While some card issuers don’t have age restrictions, others require a minimum age of 13 or older.

Even if you can add your child, the issuer may not report their account details to the credit bureaus. Some issuers allow kids as young as 13 to become authorized users but only report credit information for those age 18 and older. It’s wise to ask your credit card company how authorized user arrangements work.

Get score change notifications

See your free score anytime, get notified when it changes, and build it with personalized insights.

Misuse can lead to damaged credit

Being an authorized user doesn’t guarantee improved credit. “Same as the primary account holder, it can affect your credit positively or negatively, depending on how the card is used,” says Bruce McClary, senior vice president of membership and communications at the National Foundation for Credit Counseling.

If you have a record of on-time payments and don’t use too much available credit, that can generate or help your kid’s credit score. But your credit and your child’s can suffer if either person uses the account unfavorably.

Ultimately, it’s up to the parent to keep the account in good standing.

“When you add someone as an authorized user, that’s what they are. They’re authorized to use the card but they are not legally bound to pay the bill. You are legally bound to pay the bill,” says Julie Beckham, an accredited financial counselor and financial educator in the Boston area.

You don’t need to give your kid the credit card. As long as the primary cardholder keeps their account open and active, the authorized user’s credit will share the effects. If you give your child the card, set some ground rules. Talk about when it’s OK to use the card, how much they’re allowed to spend and who will make the payments. Some credit card companies let you place spending limits for authorized users.

Authorized user status might not be enough for future lenders

Some lenders don’t take authorized user accounts into consideration when reviewing credit applications or give them much weight. “If you’re a lender and you’re looking at someone and you see the designation that they’re an authorized user rather than the primary account holder, it’s just telling you that this person did not have to go through a credit approval process to have access to that account,” McClary says.

Having an account in their own name puts your kid in a stronger position because it shows they’re equipped to manage payments. You can guide them toward opportunities in adulthood.

“There are credit-builder loans that are available. There are starter credit cards for young adult consumers, where the threshold for approval is a little bit lower. You can also look at options for secured credit cards that require no credit check, but they require a good faith deposit in order to open the account,” McClary says.

Track your credit score with the NerdWallet app

Track your budget, finances and credit – all in one place and all for free.

Explore other ways to get your child credit-ready

The best way to set your child up for success is to talk to them about money, Beckham says.

You could look over your credit reports together or explain how many hours you need to work to pay for things like dinners or fun outings.

Encouraging good routines, like doing chores and turning in homework on time, is also important. “They’re transferable habits that can help them in their life financially as they build credit,” Beckham says.

Give your child opportunities to practice managing money before they graduate to credit. Beckham suggests letting kids test the waters with a checking or savings account. “Starting with their own money is always better because there is a sense of ownership and accountability to that,” she says.

This article was written by NerdWallet and was originally published by The Associated Press.

“Hey, kid, get out there and play a clean game and have fun … oh, and remember to send the IRS your quarterly estimated tax check and don’t forget about the social post you owe Vinny’s Pizzeria today,” shouts the hypothetical parent of a student earning NIL money in 2024.

Lots of talented people have become young entrepreneurs in the couple of years since it became permissible for college and, in many states, high school students to cash in on their own personal brand. It’s a concept referred to as name, image and likeness (NIL) — think of a recognizable college athlete getting paid to endorse a brand’s product or a player selling signed merchandise.

While the vast majority of kids aren’t working with an Arch Manning-like windfall, people earning modest amounts may be more vulnerable to money missteps, experts say.

Young stars hoping to profit off their brand need to be savvy about their money. If you’re an athlete, here are five tips to keep in mind.

1. Review contracts carefully

It’s easy to understand why a teenage athlete might be overly eager to sign any business deal that comes their way, but tread carefully, says Helen Drew, a professor of practice in sports law at the University of Buffalo.

“Student athletes are somewhat at the mercy of the people who would be engaging with them,” she says. “It’s hard to know whether or not the deal is worth taking.”

Drew recalls a deal she saw in which a student was being asked to give power of attorney as part of the deal. “He [the student] had no idea what that meant,” she said.

A power of attorney is a legal document that lets another person or business act on your behalf in certain situations, and probably isn’t top of mind for a 19- or 20-year-old.

“[Student athletes] have to understand a contract before they sign it,” says Luke Fedlam, partner and chair of sports law at Porter Wright Morris & Arthur LLP in Columbus, Ohio.

Drew says to pull your parents in, use caution and vet the business before signing anything. “If it looks too good to be true, it probably is.”

And if you spot a term like “power of attorney,” you may want to consult an attorney.

2. Budget earnings to last

When a reputable deal does go through, you can get paid. That’s when you have to start thinking about the future.

Assuming you’re not Bronny James, expect deals to be sporadic with varied pay. Even for those able to earn six or seven figures, classic financial concepts still apply.

Fedlam advises young earners to buckle down with a budget and plan for how to spend and save the money.

It’s a concept that needs to be drilled into adults, too. But once you do it — open a spreadsheet and set some spending guardrails — you’ll be glad you did. Put some money in savings to establish your emergency fund. Strive for $500, then build it up from there.

If your personal brand is bringing a sustainable income, it would be wise to put retirement savings on your radar now.

3. Plan to pay taxes

While you’re finding room for savings, keep the IRS in mind, too.

The good thing about a regular day job, boring as it sounds, is employers typically withhold taxes from your check — so you don’t have to do the math later. That may not be the case with a one-off NIL deal.

“Typically in these agreements, the responsibility for paying taxes is passed to the student athlete,” Drew says.

Depending on your earnings, you may need to pay self-employment tax and make quarterly estimated tax payments to avoid a big bill come April.

Athletes with higher earnings and multiple sources of income may want the help of an accountant.

4. Budget your time, too

There are many ways athletes can make money from their name, image and likeness, but social media influencer marketing tops the list of NIL activities, says Bill Carter, an NIL educator and consultant and founder of Student-Athlete Insights. (For example, Company X gives a student athlete money to post about a product on the athlete’s social media account.)

Posting for pay may sound like music to a teenager’s ears, but it may also be more work than you think.

Carter administers a monthly NIL survey of a panel of 5,000 college student athletes and 1,000 high school prospects.

According to data from the poll, a social media post as part of an influencer campaign takes about three hours, on average.

Athletes used to free-posting personal stuff on social media may be taken aback by the planning, coordination and communication required to post for a business, Carter says.

If you’re an athlete already working with limited free time, be prepared to grind it out off the field, too.

5. Seek education

Experts say financial education is essential for young athletes navigating NIL, but acknowledge it’s a work in progress.

School programs aren’t necessarily built for what comes with NIL, Drew says. She also laments the lack of basic financial education in grade school.

“The types of things these kids need are things every adult needs,” she says. “Maybe you don’t need to balance a checkbook anymore. But you should probably have some understanding of what the ramifications of signing any kind of contract are.”

Carter says his survey results regularly show student athletes involved with NIL are eager to learn more about areas like investing and the basics of how to build credit.

The good news is you can gain financial clarity by reading about budgeting, saving, credit and investing from reputable sources online. If NIL becomes a reality for you, there are more specialized resources like AdvanceNIL.com, which Fedlam co-founded to provide education for athletes and families.

And when your playing (and paid posting) days are over, what you learned could set you up for financial success in what’s next.

Editor in Chief Sarah Wheeler sat down with Matt VanFossen, CEO of Absolute Home Mortgage and Mortgage Automation Technologies, to talk about his unique view of the housing ecosystem and how it influences how he builds technology. Van Fossen not only heads a mortgage lender and a tech company, but is the president of the Mortgage Bankers Association of New Jersey and a board member of the Community Home Lenders of America.

Sarah Wheeler: You wear a lot of hats. How do all those different roles influence the technology you build?

Matt VanFossen: We build technology not only to sell but that we want to use. That culture resonates throughout our company and into our product lines. A differentiating factor of our tech is that lots of point of sale systems are built to faciitate loan officers with the business they already have. While we do that, we’re also focused on driving new business — from new clients but also from the relationships they already have.

We are focused on compliance and data capture at the top of the funnel, so we look at: how do we introduce loan officers not only to new technology, but to new business opportunities?

SW: What does that look like in very practical terms?

MVF: We realized that we needed to focus on the real estate agents our loan officers work with. Over the past 10 years, loan officers have become accustomed to forwarding their application right to the referral and taking the app, but what about their real estate agent counter-parties? Right now LOs have to go and remind agents and constantly be in front of them asking about referrals.

But a real estate agent has a limited amount of resources for elevating their referral. They might be driving down the road when they get a call or text message. Then they have to take whatever information they got and manually enter into their CMS. So we recoded the point of sale system so we can partner with agents on software. Now they have their own online application, but it’s not an application for a mortgage — it’s an application to buy or sell a house.

And now, anytime the agent uses those workflows, the loan officers are privy to that information. LOs can easily go in and see if they need to be preapproved and do that from their phone. So we reverse-engineered a lot of what we’ve built for loan officers and applied it to agents.

We basically created a massive collaboration system. From the first point of contact the customer has with the agent, they are being introduced to a digital ecosphere and they can remain in sthe ame portal all the way through the transaction. It’s the same portal to sign docs, eClose, get servicing information, even post-closing information. And if they ever need to apply for a new mortgage or refinance, they’re still living inside that port. So we’re keeping our customer from the first point of interaction all the way till the end of the real estate transaction and for the remainder of their lives inside of a single ecosphere.

SW: What was the “aha” moment that led to this development?

MVF: I hang out with a lot of LOs and agents, just in a social context, so the aha moment came when I was on a trip with friends. One is an agent and the other is an LO, and they both had to step away from the table like four different times, and I realized that the agent was getting new client referrals and had to pass that back to their team manually. I had completely missed this — that real estate agents don’t have an online application. An LO can text the link to their application portal, but not the agent. I realized we’ve been focusing for a decade on how to streamline this process for LOs but had abandoned our counterparties.

Because of my positions at a tech company, a mortgage company and in regulatory compliance, I have a view into all three points of this triangle — and I have developers that can go build it! Sitting on top of all three at the same time, I can see how they are all intimately intertwined, and I can test it with my own lender. I’m a user of this tech so I’m the mad scientist that’s experimenting on himself! I can jump in and code something, call an agent to have them come in and see it, then use with my own clients first. Then we can think about the enterprise version. It’s almost farm-to-table programming.

SW: So does that mean you only build versus buy?

MVF: No, because there are differet platforms that have some amazing features. We will build over buy in certain things but you can’t take over everything. We have some fabulous vendor tech partners in this industry. We’re focused on point of sale because it gives us control over the loan officer and agent and client experience, so we want to be in the driver’s seat for that.

But even with that mini-POS for agents, it’s not a full-blown CRM and they still need to use their CRM vendors, who will be better at journey campaigns, for example. And we work with awesome loan origination systems like Encompass to maintain compliance and a database. We can’t conquer every avenue so for us it’s about strategy and where we can get the biggest lift with our own tech and then shop the marketplace for strategic partners.

SW: What keeps you up at night? Security?

MVF: I am constantly thinking about this and how I’m not only responsible for cybersecurity for my various companies but also now my point of sale. But we’re very unique and the architecture we built for it was not possible more than a year ago. So rather than having two databases — one POS database where people apply online and then that application goes into another database where you hold that PII inside of it, and you synch those through an API — we don’t do it that way. We have single source of truth.

When an application comes in, or any of the Realtor referrals come in, they all get logged immediately into ICE’s Encompass. We don’t have a database — it all instantaneously, through an encrypted API transaction, as soon as the application hits it goes into Encompass. So there’s only one place and location and all of the loan data resides in that. So we are now more secure than ever because ICE has phenomenal information security. So what we do is put a customization layer on top of it. It’s a highly configurable, easy-to-use user interface that shares a database, rather than maintaining two databases. And that solves a lot of cybersecurity issues.

The other thing that keeps me up is mortgage rates and when we’ll see quantitative easing. What the industry really needs is to get some tailwind into the market.

When you look at the three things I’m involved in — I’m running a lender, I’m running a FinTech and I’m in advocacy. What solves all of that is a little bit lower interest rates. That will strengthen the housing market and make sure that independent mortgage bankers have stability in extremely volatile times. That ensures the tech company will continue to innovate, and all of those things together is going to help consumers, especially low to moderate income consumers.

HousingWire Editor in Chief Sarah Wheeler sat down with Jason Bressler, CTO at United Wholesale Mortgage (UWM) to talk about how the lender is developing a smart, innovative IT team by giving them a safety net to fail. This interview has been edited for length and clarity.

Sarah Wheeler: UWM develops all their software in-house. What are some of the advantages of that?

Jason Bressler: We’ve got control over the entire product from start to finish, so I’m never relying on somebody who isn’t part of my team to be able to build anything. When I build it all in house, I architect it from the start from both the technical aspect and business aspect, specifically for the wholesale channel and the broker model. At that point, I’ve got the ability to deploy and adapt as quickly as I want, which winds up being seven, eight, nine times a day sometimes to make the product perfect, instead of having to wait on somebody else.

So I’ve got speed, I’ve got control and everything I build is meant to be scaled as quickly as possible to as many brokers who come into the wholesale channel as possible.

SW: How is UWM leveraging AI right now?

JB: We are wholly invested in AI right now. Because we’re build versus buy, I am partnering with some very large AI firms to build an entire AI suite and vertical. We’re using AI in every facet of everything that we have: in all of our existing systems, all of our existing products and then also in new technology and new products.

SW: What’s the competitive advantage there?

JB: From a generative standpoint, it obviously puts information at the fingertips of our team members and our brokers. But the real oomph that comes with AI is the large language modeling and how you can get so predictive with the data that you have. And then you can use AI to very accurately detect fraud, for example. You can use AI to very accurately build out a data lake that gives you access to multitudes of different data streams and shows you things that you didn’t even know that you needed to know, to make great business decisions. From a data standpoint it’s those things that have changed the game.

SW: When I had you on the HousingWire Daily podcast in the spring, you and I talked about the way you source tech staff from other parts of UWM through your X program. How is that program faring with volume down?

JB: Even with volume down, we’re so committed to technology that my team continues to grow. When we talked in May we were at 1,300 team members and now we’re over 1,500. I think so many companies are missing out on the next wave of technologists because those people don’t have a degree, or they didn’t have adequate training.

I see it as this is where I should be investing almost everything that I have — getting them in now while the mortgage market isn’t as hot as it has been. I think we’re in for such an extended, long refinance boom, that the sooner that I get them in, trained and get them acclimated to the tech stack, the sooner that I make them solutionists. And that’s really the thing, we’re so big on making them problem-solvers, but that takes time.

SW: Are there any examples you could point out of people who you wouldn’t necessarily think would funnel into technology, who have done a really great job in the program?

JB: I mean, I could name 1,000! When I first started the program seven years ago underwriters made the best technologists because they are so oriented to guidelines and problem solving and analytical thinking. Now it’s a very competitive program and we have people applying from everywhere in the company.

We have one woman who was driving school buses for a while, then joined UWM in operations. She was in operations for a very short time before we brought her into the X program. She went through the developer program and moved into DevOps, and she’s one of our strongest team members. She was really smart, very ambitious, and then constantly just kept asking questions and trying to do different things and it just accelerated her career growth at UWM.

SW: What keeps you up at night?

JB: What we can do that will continue to drive our innovation. I really want to be the Google of fintech. So how do we become the technology team, working inside of this mortgage company, that creates product that is so far above what anyone else is doing that not only do technologists want to work here, but the rest of the fintech world looks at us and says, how the hell are they doing that?

SW: How do you make sure that your team is continuing to stary sharp and be innovative?

JB: Two things. One is something I instituted a while ago called lab time. Every week on Wednesday between nine and 11, everything in IT just shuts down. We do innovative lab time where I don’t want it to be something new, what I want is for every team to find ways to make existing systems, processes and technology more efficient, first and foremost. And that’s all they get to do. And then because they’re efficient with their time during the eight hours that they’re in these four walls, they find the time to work on that off to the side off of their existing backlog. There are so many innovative things that come out of that.

Secondly, I have such a strong culture and desire for people to constantly fail. If you’re not failing, you are not doing your job. They know that they’ve got a giant safety net at UWM to fail. As long as you don’t do it in production, you should fail as much as you possibly can and learn from it and just don’t make the same mistake twice. That failure has created so much innovation,because people are not afraid to just throw anything up against the wall to see, could this actually work? And then we just go all in and try to build off of that.

SW: Practically, how do you encourage that mentality?

JB: As the CTO, it all starts with me, so I will get up in front of all 1,500 people once a month and tell a story about how I failed that last month, or last week, or yesterday. And then I have people constantly sharing their failures to the entire IT team, so that everybody knows, they are not in this alone. It really is okay to fail — you’re not going to get fired, you’re not going to get reprimanded, you’re just going to learn from it and keep getting better.

SW: Your team works all together on one big floor of UWM. How do you think that gets better results than having people distributed?

JB: Part of what makes us so special is the fact that if you have a question, you can literally just turn your chair around and say, ‘Hey, I have a question.’ Instead of sending an email, or setting up a zoom call or teams and hope that somebody can explain it, that person can just literally turn around and look at your computer screen and say, ‘Oh, I see what’s happening right here, change this up.’ It’s small, tiny little things like that that you constantly get from having everybody in one office solution and all the time.

SW: What’s your favorite part of the day of the workday?

JB: Every Wednesday for 90 minutes I do open office hours. Anybody can come talk to me about literally anything for 10 minutes. If they want to talk about pay, they can come directly to me, or if they have a new idea, or want to know what their career looks like. Those are the best and most exciting times of my day — talking to team members about their career.

SW: What makes you excited about the role technology can play in mortgage this year and other years?

JB: Technology will be the everything in mortgage — it’s already trending that way. What excites me the most is I know that UWM technology will create a huge gap between UWM and whoever happens to be number two in the overall market space, not just wholesale. My technology and what my team builds and what we do — we’ll be the catalyst for all of that.

I’m working at the No. 1 mortgage company in the country so I get to take more risks and there are more opportunities for me and my team to do all kinds of crazy stuff and be innovative.

HousingWire Editor in Chief Sarah Wheeler sat down with Rick Arvielo, co-founder and CEO of New American Funding (NAF), to talk about AI, why he chose to start NAF Technology India and how to keep NAF innovative. This interview has been edited for length and clarity.

Sarah Wheeler: New American Funding is known for building rather than buying technology. Are you still in that mode?

Rick Arvielo: Yes, and as a matter of fact, we’ve really doubled down on the effort. I’ve always kind of led the charge in our tech build, and as we’ve gotten bigger, it’s just harder for me to devote the time to immerse myself in that. So within that last couple of years, we brought in some great leaders — we’ve been lucky to attract some top talent to New American Funding,

Another fairly material decision we made was about a year and a half ago, we made the decision to rely on some offshore assistance. But having some experience with that, I didn’t really want to find contract offshore providers. So we decided to open our own company in India: NAF Tech India. We have about 150 New American Funding employees over there now to help supplement our somewhat lofty tech build goal.

SW: What has that experience been like?

RA: It’s great! We’ve been using contractors here and there for some time just because it’s often a lower cost, but what we find is with contractors, oftentimes, they’ll give you their “A” players to get you into contract and then they move those people on to their next target. Then you’re left with people that don’t measure up to the initial bar. So, we just realized that the only way that we were going to control that world is to own it ourselves — and it’s quite an undertaking.

You’ve got to incorporate over there, you’ve got to get space and build it out, you’ve got to find the leadership and then start hiring staff. That took about a year, but we’ve been full force now for about a year.

The challenge with the U.S. really has a lot to do with the escalating pay scales [for tech workers] which is very hard to digest in a market like we’re in right now. It will have you second guessing your decision to build versus buy! But also, when you bring people in, it takes some time just to get them familiar with your tech stack. And if they then get attracted away by somebody wanting to pay them a little bit more, it’s just a big expense to digest.

So having that foothold in India, where they have vast expertise, and really have them part of New American Funding so we can indoctrinate them into our culture — something they care about as much as Americans — it’s been a fun exercise.

SW: Is it similar to just having another location?

I would say the only thing that’s a little different is the time zones. But we live in a virtual world anyway right now — most of our tech people don’t work in our corporate office, they’re working from wherever they are.

I think that the quality of engineer over there is really good. We’re now finding that we need to invest in bringing more product people into India so they’re intimately familiar with what we’re doing. So when they’re busy during our nighttime and they get stuck or need help, there’s somebody there that can answer those questions. We’re starting to build out that infrastructure now as well.

SW: What advantages does building this way gives you in this particular market?

RA: Cost efficiencies are probably the biggest advantage. There is a stark difference between what you have to pay a technician here in the United States and what you have to pay a technician in India. Not to take advantage of anyone. But, we’re privately funded — we’re not public, it’s just Patty and me — so we have to be very careful about the dollars we spend, especially in a real estate market that’s under pressure like ours is. So to go as hard and as fast as we want to go with our tech initiatives, we needed to bring on a lower cost resource to supplement and help us stay within our budget.

SW:Are you guys rolling out a lot of different products for them?

RA: Our goal is always to improve the experience for our loan originators and our consumers. Millennials are digital natives and Gen Z doesn’t know anything but a digital lifestyle experience. Our goal is to take that seriously and try to develop technologies for both our loan officers and our consumers, to give them a real-time experiences.

When I looked at the vendors that are out there that have done a lot of this — that comes with as many challenges as benefits, because technologies are changing quickly. And when you’re a vendor and you’ve invested over years to develop techn, and then this technology morphs and changes, a lot of times they find themselves painted into a corner because they have to support people that are already using their stuff. So our goal is to develop the foundation, and have the technical prowess to be able to pivot for our needs, and not the need of some vendors’ 100 customers.

SW: How is New American Funding leveraging AI?

RA: I think artificial intelligence can bring a lot to the table, to the extent it can be taught. That’s the beauty of AI — it’s a large language model and neural networks are so far beyond human beings, they can arrive at answers much more quickly and accurately. We do a lot of transactions, so we can take those transactions and teach a large language model more quickly than maybe a smaller competitor.

AI is so new, but we’re focused on getting the right people on the boat, to have the subject matter expertise so that they can bring these types of solutions and allow people time to become comfortable with the transition. It’s not that we want to replace their job — it has nothing to do with that, it has to do with making them more efficient. But creating this new ecosysem is a bigger effort than you would think. And it’s not just operations or marketing — it’s just about every part of the business where AI can make a difference. And you still need to be very careful massaging it into the organization so people aren’t defensive and they don’t feel threatened by it.

SW: How do you keep making sure you’re on the edge of innovation where it matters?

RA: For me, personally, I just find people better than me. I mean, don’t get me wrong, I have a lot of confidence, but I’m also 61 years old so I’m not the guy anymore to direct tech. I used to be, but today, it’s very important that I find people much better than I am: much more immersed, much more contemporary in the way they think, and bring them in to help make those decisions. And we’ve probably worked harder on that than just about anything else over the last few years.

New American Funding has always been what I call skinny at the top — it’s been me, Patty, Christy Bunce our president, and a handful of other people that we really rely on. And I needed to fill in puzzle pieces with people who really had that level of expertise and just a new perspective that was better, more relevant and younger than mine, to be honest with you.

And we’re blessed that we’ve been able to find those people and attract them to New American Funding, and they’re really making their mark. And we’re such a better business today than we were even a handful years ago, when I was in charge, because I just don’t know what they know. And I think that it was important for me to recognize that myself, and to be able to figure out a way to attract that top talent to New American Funding.

SW: What keeps you up at night?

RA: I think, to be blunt, not f*ing up. We’re 3,800 employees at New American Funding and those people rely on me to not screw it up and to make sure that I make the right fiscal decisions for our company, that we have the right vision, we invest the right money and execute in the right way, so that everyone can continue to do their work and earn their living and take care of their lives. So when I feel pressure, it really has more to do with that than anything else.

We don’t swing for the fences at New American Funding. We think things out. We’re very deliberate in our growth, because I don’t want to do something that jeopardizes the wherewithal in the business and put 3,800 souls at risk, especially in a market like this. We had an unprecedented run through the COVID years, obviously, but now is the time to really make wise decisions so you don’t have an undue impact on the organization.

Generally, the credit bureaus consider anything over 670 a good credit score.

Considering applying for a new line of credit like a mortgage or credit card, but not sure how your credit score stacks up? If your score is 670 or higher, you’re doing fairly well. The best credit score and the highest credit score possible is 850 for both FICO® and VantageScore® models. FICO considers a score between 800 and 850 to be “exceptional,” while VantageScore considers a score above 780 to be “excellent.” It’s possible to get an 850 credit score, but it’s tough to achieve.

In This Piece

What Is a Good Credit Score?

A good credit score will depend on the scoring model, but either 670 or above would be considered good. Credit scores calculated using the FICO or VantageScore 3.0 scoring models range from 300 to 850. Those scores are broken down into five categories, though the breakdowns differ slightly. Since they have somewhat different range calculations, what’s considered good for VantageScore may be considered fair for FICO, and what’s considered very good for FICO may only be good by the VantageScore model.

FICO and VantageScore aren’t the only credit scoring models. However, they are the most commonly used models and the ones used by the three major credit bureaus: Experian®, Equifax® and TransUnion®. Some lenders even have their own scoring models. But most lenders and credit card companies use FICO scores or VantageScores.

What Is a Good FICO Score?

For FICO, a good credit score is 670 or higher. A score over 739 would be considered very good, while a score above 800 is considered exceptional—the highest designation possible aside from a perfect 850.

What Is a Good VantageScore?

In the VantageScore 3.0 model, a good score is 661 or higher. Since this model doesn’t have a designation between good and excellent, the range of good scores is much wider than it is for FICO. Excellent scores start at 781 rather than 800 in this model, with 850 also being considered a perfect score.

Understanding Credit Score Ranges

The credit score ranges vary depending on whether you’re looking at a FICO score or a VantageScore. They line up fairly similarly, but their score designations have different labels — FICO lacks a “very poor” designation, while VantageScore lacks a “very good” range. Here’s how they break down.

FICO Score Range

Poor: 300-579

Fair: 580-669

Good: 670-739

Very Good: 740-799

Exceptional: 800-850

VantageScore Range

Very Poor: 300-499

Poor: 500-600

Fair: 601-660

Good: 661-780

Exceptional: 781-850

Credit Score Range Chart

To give you a clear idea of how FICO and VantageScore’s credit score ranges compare, here’s a comparison credit score range chart.

What Are Credit Scores?

The three-digit figures called credit scores are what scoring institutions use to rate your credit profile based on your credit report. Since these bureaus have their own records, your score might differ from one scoring institution to the next.

Your score suggests to potential creditors how likely you could be to repay a loan, pay off a credit card, make late payments, and default on payments. Basically, it helps them determine whether you’re an acceptable risk and if they should approve your application for a loan or credit card. A low score doesn’t always mean lenders will decline your application. Instead, it might mean they’ll consider approving you with higher interest rates or less favorable loan terms.

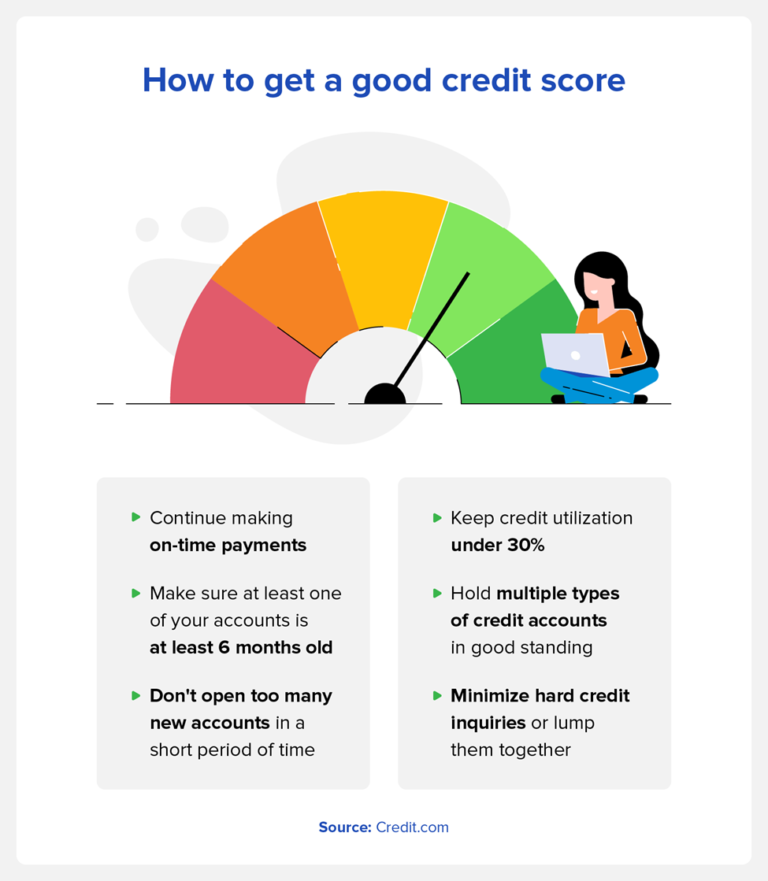

How to Get a Good Credit Score

VantageScore and FICO scores are calculated using similar information. Each model may use slightly different terms for these, but here’s what they’re looking for.

Payment History

FICO weight: 35 percent

VantageScore weight: 40 percent

Late and missed payments can have a major impact on your credit score. Both FICO and VantageScore take your history of payments into account when calculating your score and look at your number of late payments, the number of accounts you’ve missed payments on, and the overall number of missed payments. Maintaining a consistent, on-time payment history goes a long way in establishing good credit.

Amounts Owed/Credit Utilization

FICO weight: 30 percent

VantageScore weight: 20 percent

Credit utilization is calculated as a ratio. It divides the amount of credit you’ve used by your total credit limit. If your credit limit is $5,000, for example, and you use $2,000 in credit, your utilization rate is 40 percent. It’s recommended to keep this rate to 30 percent or less and preferably below 10 percent. To help improve your credit score, try to reduce your utilization ratio if you often find yourself going above 30 percent.

Length of Credit History/Credit Age

FICO weight: 15 percent

VantageScore weight: 21 percent

Your credit history refers to the amount of time your credit accounts have been open, averaged across all of your accounts. That means that if your credit history has factored in your oldest account for the last 15 years but you suddenly close that account, your average credit age will drop accordingly, which could also lead to a drop in your credit score.

For that reason, it’s a good idea to maintain your oldest credit accounts. As a rule of thumb, try to make sure you have one account that’s six months old or older open at all times.

Credit Mix

FICO weight: 10 percent

VantageScore weight: N/A

Your credit mix refers to the number of revolving and installment accounts you have open. Here’s how those accounts differ:

Installment accounts: These are essentially defined long-term loans like home mortgages or vehicle financing on which you make payments in specified amounts over a predetermined period.

Revolving accounts: These types of accounts set a specific amount of credit you can use as needed, such as a credit card. You only pay back the amount of credit you borrow against this limit.

Potential lenders will want to know you can manage both of these account types, so it helps to have a history of successfully managing each. While FICO has a category explicitly for this, VantageScore does not—though it still may factor into other elements of your VantageScore. As such, it can be helpful to have multiple types of accounts in good standing regardless of the scoring model.

New Credit/Recent Credit

FICO weight: 10 percent

VantageScore weight: 5 percent

Opening multiple new credit accounts in a short period of time can have a negative impact on your credit score. Since lenders may see it as a red flag for a borrower to have several recent accounts open, it may be helpful to let your current accounts continue aging while paying them off consistently if you want to maintain or improve your score.

Balances and Available Credit

FICO weight: NA

VantageScore weight: 14 percent

Though only VantageScore has categories specifically for balances (11 percent) and available credit (3 percent), they still play a role in your FICO credit score. The amount of money you owe to lenders and your available credit factor into credit history and utilization rate, so keeping your balances low in comparison to your available credit can be a good idea when trying to achieve a good credit score.

A Note on Credit Inquiries

A hard credit inquiry gets pulled when a lender requests your credit report to assess your creditworthiness. This type of inquiry can drop your score by as much as 5 to 10 points and may stay on your credit report for up to two years, but it will impact your score for only 12 months. To get and maintain good credit, it’s best to avoid these as much as possible.

If you need to apply for multiple credit accounts in a short time or want to shop around for loan rates, it can help to keep those applications within a 14-45-day window so they get grouped into one inquiry. FICO and VantageScore differ on this, with FICO using 45 days and VantageScore using only a 14-day span.

Keep in mind this is only for hard inquiries, as soft inquiries shouldn’t affect your score.

How Lenders Use Credit Scores

Credit scores can offer a gauge of creditworthiness for lenders to determine things like whether or not to approve you for a credit line, how much credit to approve you for, and what your interest rate should be. But while your credit score has a big role to play in this, it’s considered alongside your credit report. Lenders may also consider your income, debt, and your ratio of debt to income.

How Can I Get My Credit Scores?

You can request a full credit report from all three credit bureaus from AnnualCreditReports.com, however, your score is not included with your report.

Most online options for viewing your credit score—free or paid—are limited to one or two scores. ExtraCredit from Credit.com takes it twenty-six steps further by offering you 28 of your FICO scores from all three major credit bureaus. When you sign up for an ExtraCredit account, you can also earn money when you get approved for select offers, monitor your accounts with $1 million identity theft insurance, and get exclusive discounts froma leader in credit repair services. All for one low monthly price.

If you’re not ready for ExtraCredit, Credit.com also offers a free Credit Report Card. This comes especially in handy as it offers you your Experian VantageScore 3.0 credit score for free.

FAQs about Good Credit Scores

Want to know more? Here are a few common questions about what good credit scores are and how they’re used.

Do Lenders Prefer a Good VantageScore Score over a Good FICO Score?

Lenders don’t necessarily prefer one score over the other. It’s likely, though, that a given lender uses only one credit-scoring institution. FICO reports that 90% of the top U.S. lenders use FICO scores when deciding whether to loan money to an applicant. On the other hand, VantageScore states that between March 2021 and February 2023, approximately 14.5 billion VantageScore credit scores were used.

Both models are consistent enough that knowing where you stand in one gives you a reliable indication of your credit in general.

What Is a Good Credit Score to Buy a House?

A FICO score of 580 is the minimum credit score required to qualify for maximum financing. , according to the U.S. Department of Housing and Urban Development. Below 580, borrowers will have to make a minimum downpayment of 10 percent. That doesn’t necessarily mean that you’re guaranteed to qualify for a loan with maximum financing with a score of 580 or above, but it’s what you’ll need if you want the flexibility of a lower down payment.

What Is the Highest Credit Score?

850 is the highest credit score possible for both the FICO and VantageScore models.

What Is Credit?

Credit is access to capital provided by a lender with an expectation that it will be repaid within an agreed time frame. This could be a set installment account—such as a mortgage or car loan that gets paid off gradually—or a revolving account like a credit card with a maximum balance that can be borrowed at a given time.

What if I Don’t Have a Good Credit Score?

Now that you know what’s a good credit score, it’s crucial to act on yours. If your credit is fair or poor, find out why. Then you can address the factors and work to improve your score.

Do you need more credit history? Check out our ExtraCredit Build It feature! Use ExtraCredit to report rent and utility bills you’re already paying and add them to your credit profile as tradelines. This allows the credit bureaus to see additional payment information from you, which can help you build your credit profile.

Does being an authorized user affect your credit? Well, becoming an authorized user can help you build your credit under the right circumstances. Before you agree to be an authorized user or add an authorized user to your account, it’s important to understand the potential risks and benefits. This article provides more information about how adding an authorized user works and how it could impact your credit.

In This Piece

What Is an Authorized User?

An authorized user is a person who has the authority to use another person’s credit card account. In many cases, the authorized user receives a credit card in their name. Unlike co-signers and joint account holders, authorized users aren’t financially responsible for making payments.

Typically, cardholders only add someone they trust, such as a child or significant other, as an authorized user. There are a few reasons a cardholder might want to add an authorized user to their account, including:

To help the person build their credit history

To make it easier for the authorized user to make payments when the cardholder isn’t available

To allow someone to make purchases on the cardholder’s behalf

The primary reason a person wants to become an authorized user is that they’re unable to secure a credit card on their own. For example, a child may not have the established credit to get a credit card, so a parent adds their child as an authorized user under their account.

Authorized Users Versus Joint Accounts

Authorized users aren’t the same as joint account holders. Authorized users can charge money to your account, but they can’t add other authorized users and they can’t dispute charges. They also can’t request credit limit increases, transfer balances, or close your account.

In contrast, joint account holders can do all of those things and more. Joint account holders are jointly liable for the account, and they’re also jointly liable for repayments.

How Do Authorized Users Work?

The process of adding an authorized user to your account varies between credit card companies. Some credit card providers may have age and other requirements that must be met before you can add an authorized user. You may also be able to set limits on how much the authorized user can charge to your credit card.

You’ll need basic information about the person you’re adding, such as name, date of birth, and Social Security number. You should contact your credit card company directly to see how this process works.

Once the application process is complete, the authorized user receives their card. They can use it just like any other credit card. Depending on the specific credit card company and your preferences, you may be able to give the authorized user access to your account information so they can track packages and report a lost card, errors, or potential fraud. Keep in mind that giving the authorized user access to your account may also allow them to see your purchase history and redeem special rewards.

It’s important to note that authorized users don’t receive credit card bills and aren’t responsible for making payments. This responsibility lies solely with the cardholder.

Can I Build Credit as an Authorized User?

For a long time, authorized users were able to build credit by “piggybacking” on the primary account holder’s own good credit record. Many modern scoring models no longer recognize this loophole—but a few still do. If you’re hoping to build credit by becoming an authorized user, you need to do two things:

Check if the card company reports authorized users to credit bureaus.

See if authorized users are reported as if they’re account holders.

If the account holder’s card company does report authorized user activity, you’ll see an individual account on your credit report. Providing the primary cardholder continues to make payments and handle the account responsibly, you’ll likely benefit from the listing.

Can Adding Authorized Users Hurt Your Credit?

Before adding an authorized user to your credit card account, you need to ask yourself several questions.

Does adding an authorized user affect my credit?

Will adding an authorized user hurt my account?

Will adding an authorized user help their credit?

The answer to these questions depends a lot on your specific credit card company. Not all credit card companies report authorized users to the credit bureaus. If your credit card company doesn’t report authorized users, adding them to your account will have no impact on their credit score. If, on the other hand, your credit card company does report authorized users, it can help them start building up credit.

Either way, adding an authorized user to your credit card account shouldn’t automatically effect your credit history. However, there are several ways taking this step could hurt your credit score over time.

First, if the authorized user charges too much to your credit card, you may have difficulty making your monthly payments. Payment history makes up 35% of your FICO score. So if you can’t make your monthly payment because of charges accrued by an authorized user, your credit profile, and wallet, could take a hit. If possible, set limits for how much your authorized user can charge to your credit card account. This step can help to reduce the risk of overspending.

Secondly, additional charges to your credit card account can also increase your credit utilization ratio. The more you charge to your credit card, the higher your credit utilization ratio is. Your outstanding debt accounts for about 30% of your overall credit score. You should try to keep your debt ratio under 30%.

What if an Authorized User Misuses Their Card?

Let’s imagine you are the primary account holder, and your teenager is the authorized user. What would happen if they decided to buy a new wardrobe without telling you? The answer is simple—you’d be on the hook for the whole amount. Your wallet could take a serious hit.

Does Removing an Authorized User Hurt Their Credit?

If your authorized user doesn’t behave, you can remove them from your account pretty quickly. At that point, they can no longer use their card and can’t charge any more money to your account.

Credit age history makes up 15% of your credit score. If your credit card company previously reported the authorized user as an individual account holder and they suddenly get removed from your account, the removal might look like a closed account, regardless, it will likely be removed for age calculations. In that case, the formerly authorized user’s credit score could dip.

Does Being an Authorized User Affect Your Credit?

Becoming an authorized user could affect your credit if the credit card company reports your status to the credit reporting agencies. If the credit card company doesn’t report your authorized user status, taking this step won’t impact your credit score at all. However, you’ll still have the benefit of charging purchases to a credit card.

How being an authorized user impacts your credit depends largely on the cardholder’s payment history. If the cardholder has a strong history of making on-time credit card payments, it could help you build your credit and increase your credit score. On the other hand, if the cardholder has frequent missed or late payments, it could hurt your credit score.

It’s important to understand the cardholder’s credit history before agreeing to become an authorized user. It’s also important to repay the cardholder for any purchases you make as quickly as possible. This step will help the cardholder make their payments on time.

How Long Does It Take an Authorized User to Show Up on Credit Report?

It takes about 30 days for your authorized user status to reflect on your credit report. However, not all credit card companies report authorized users to the credit bureaus. In these cases, your credit report may never show that you’re an authorized user.

What to Consider About Authorized Users

If you want to build your credit by becoming an authorized user, start by talking to friends and family members you trust. Be sure the cardholder has good credit and makes on-time payments.

If a friend or family member agrees to add you as an authorized user, it’s important to set clear boundaries right from the start. For example, determine your specific credit limit right away and whether the cardholder wants you to ask for permission before using the card.

You also need to make a clear payment agreement. Determine exactly how much you’ll pay each month and the date monthly payments are due. Make sure you create a budget so you know exactly how much you can afford to pay each month. Also, be sure to track your purchases so you know exactly how much you owe.

It’s crucial to have this agreement in place before becoming an authorized cardholder. This agreement allows you to know exactly what’s expected of you. It can also help you determine if this is the right option for you.

Four Tips to Bear in Mind

Set clear spending rules before you make family members authorized users.

Talk to prospective authorized users about credit, including credit utilization.

Set up text message alerts to make sure you know when authorized users make purchases.

Remove authorized users if they don’t stick to the rules you make.

Simply Adding Authorized Users Won’t Hurt Your Credit—but Be Careful

Ultimately, authorized users aren’t a threat to your credit unless they misuse your credit card account. Many authorized users coexist happily with main account holders for many years. Problematic authorized users, unlike joint account holders, can be easily removed.

If you’re thinking of adding an authorized user and you want to keep track of your credit, why not subscribe to ExtraCredit from Credit.com? ExtraCredit is great if you’re an authorized user—tools like Build It can help you strengthen your credit profile by letting you add rent and utilities as trade lines to your credit history.

Ready to buy a home? Whether you’ve already found your dream home or you’re just starting the process, one thing’s for sure—you’ll probably need a home loan. But before you start looking into mortgages, you might need to give your credit score a little evaluation. You need a decent score to get a decent mortgage, but what’s the minimum credit score for a home loan?

The short answer? It depends on a lot of things. If you’re ready to start looking for home loans, but aren’t sure if your score is up to par, we’re to help. Keep reading to learn if your credit score is mortgage-ready.

A Quick Look at Minimum Credit Scores for Mortgages

Mortgages are complex forms of financing, so a lot of factors come into play when you’re applying. Find out more about the minimum credit requirements for these types of loans—and why your credit score even matters—below.

Why Does Your Credit Score Matter for a Mortgage Loan?

Your credit history tells a financial story about you. It lets mortgage lenders better understand whether you’re reliable, how likely you are to pay off your debt and whether your debt-to-income ratio is low enough to allow you to cover your current debt obligations in addition to a new mortgage payment.

If you have bad credit, you may look like a risky investment to potential lenders and you’ll be less likely to get the approval. Or, if you do get approved, you may be required to pay higher interest rates than individuals with a better credit score might pay.

Luckily, you can still get approved for a home loan even with a lower-than-average score. That’s because your credit score is critical, but it’s not the only factor lenders consider. Plus, different types of loans come with different requirements, so you don’t always need a good credit score to qualify.

Get matched with a personal

loan that’s right for you today.

Learn

more

What Credit Score Do You Need to Get a Mortgage?

As stated above, the required credit score really depends on what type of loan you’re looking at. Let’s break it down a bit, defining these types of loans, so you can understand more about mortgages and some of your options.

Credit Requirements for Conventional Mortgage Loans

Conventional mortgage loans are not backed by a government entity. They’re offered via private lenders, including banks and mortgage companies. Typically, you need good credit to qualify for a conventional mortgage. For this purpose, that’s considered to be 640 or higher.

However, if you fall slightly short of that mark, you might still be able to find a lender if your payment history, debt-to-income ratio and other factors are positive. Ultimately, lenders need to know that you’re likely to pay your mortgage as agreed and that you also have the resources to do so.

Credit Requirements for Government-Backed Mortgage Loans

Credit requirements for government-backed loans get a bit more complex. Since these loans are all or partially backed by federal government agencies, lenders may approve you even if you don’t have good credit. However, that doesn’t mean everyone gets approved. Here are some basics about eligibility and minimum credit score requirements for various government-backed mortgage types.

Credit Score Requirements for USDA Loans

These loans are partially backed by the federal government and are available to individuals buying qualifying suburban or rural homes. USDA loan lenders must conduct a thorough review of an applicant’s credit profile. Here are just some of the rules they must apply:

If three credit scores are present, they take the middle one. If two credit scores are present, they take the lowest one. If only one or no credit score is present, the lender must do a credit analysis and obtain alternate credit verification.

The credit score must be based on at least two trade lines (open accounts) that were active at least 12 of the past 24 months. In short, if you don’t have much credit or you haven’t dealt in credit for years, you may have a challenge getting approved.

There must be no significant delinquencies or collection accounts.

Credit Score Requirements for VA Loans

VA loans are available to eligible veterans and their families and are backed by the Department of Veterans Affairs. They don’t require a down payment or private mortgage insurance. The VA does not establish minimum credit score requirements and requires lenders to conduct a comprehensive credit analysis.

VA loans don’t have maximum debt ratios, but the lender has to provide compensating factors that prove they can pay the mortgage if their debt-to-income ratio is more than 41%. Veterans who borrow without a down payment may be limited to mortgages of $453,100 or less.

Credit Score Requirements for FHA Loans

FHA loans are backed by the Federal Housing Administration and are seen as a lower risk by lenders because they’re government-backed loans. This option is a common choice for anyone who qualifies as a first-time home buyer because of its relatively low minimum credit score requirements.

Credit score requirements for FHA loans are:

580 or higher for maximum financing—this means you wouldn’t need a down payment or could have a very small down payment, depending on other factors.

500 or higher for partial financing—this means you’d need at least some down payment orwould need to buy a house for less than it was worth.

You can’t get approved for an FHA loan with a credit score less than 500. Other factors do impact approval, such as your payment history, income and debt level.

Do You Need Good Credit to Refinance Your Mortgage?

A refinance is still a mortgage, so yes, you typically need good credit to get approved for one. Many of the minimum credit scores for home loans above apply to refi loans too. One benefit you get when refinancing is that you may owe less than your house is worth. That could reduce the need for down payments and even help you access better interest rates because the lender has less risk in making the loan.

Has COVID-19 Impacted Mortgage Credit Requirements?

Yes, COVID-19 has impacted minimum credit scores for mortgages. These changes are typically made by each bank. In the early months of the pandemic, uncertainty led many banks to drastically reduce home loans or even put them on hold. For example, in April 2020, JPMorgan Chase changed credit requirements to at least a 700 credit score with a 20% down payment.

However, falling interest rates and improved economic factors caused many banks to loosen requirements in the later months of the pandemic and into 2021. Ultimately, you’ll need to do your research when you’re ready to apply for a mortgage loan to find out what options you might qualify for.

What You Can Do Now

First, check your credit score. You might consider signing up for ExtraCredit. You’ll get access to 28 of your FICO scores—and you’ll see the credit scores that mortgage lenders see. ExtraCredit also has features such as Build It to help you positively impact your credit score if you need to boost it before applying for a mortgage.

Once you have a credit score that’s above 640—or, even more optimally, above 700—you can start shopping for mortgage loans and good rates. And remember that if you do get approved, your credit score also impacts your interest rates. Always ensure you know what your mortgage is going to cost you each month and over the life of the loan.

In July 2021 alone, more than 700,000 new home sales were processed. While that sounds like a lot, the number is lower compared to 2020, due in part to a housing shortage. Pair that shortage with plenty of people looking to make a home purchase and you have a competitive market in 2021 and beyond.

You might think that these are just numbers—but understanding the housing market is pivotal to the mortgage approval process. If you’re considering buying a home, we’re here to guide you through the mortgage process. Get ready to be set up for success.

In This Piece

Understand Your Credit History and Score

The home loan approval process includes a pretty thorough credit check. While you might be able to get approved for an FHA mortgage loan with a credit score as low as 500, most traditional mortgage loans require at least a 620 or higher.

While your credit score might make or break you at the beginning of a mortgage application process, once you continue the process, your entire credit history becomes important. Mortgage lenders look at issues such as delinquencies or open collections accounts on your credit history. They may also require that you make good on any open collections accounts before your mortgage approval can go through.

It’s a good idea to understand your credit history and score months before you plan to apply for a home loan. That way, you have time to resolve any issues or dispute inaccurate negative information that could be dragging your score down.

You can get a free credit report from each of the major credit bureaus at AnnualCreditReport.com. You can also sign up for services such as ExtraCredit to get ongoing access to your credit reports and scores. ExtraCredit also includes features such as Build It that help you work on building your credit so you have a better chance at getting the mortgage loan—and rates—you want in the future.

Get matched with a personal

loan that’s right for you today.

Learn

more

Prepare Your Personal Finances for the Home-Buying Process

Your credit isn’t the only financial factor that impacts your mortgage application process. Yes, your history of on-time payments to other creditors is important. But so is your ability to make payments on the mortgage loan in the future. Lenders are likely to be concerned with:

Your debt-to-income ratio, or DTI. This is how much of your income you need each month to pay your existing debts. The lower this figure is, the better. According to the Consumer Financial Protection Bureau, most mortgage lenders won’t approve home loans that bring a consumer above 43% DTI.

Your income. In most cases, you’ll need to demonstrate that you have the income or other financial means to make your monthly mortgage payments. Your income can impact how much you can get approved for or whether you’re approved at all.

Your cash savings or other assets. If you need to make a down payment on your mortgage loan, you may need to demonstrate where that cash came from. You can get creative with sourcing your down payment within some rules, but you can’t always borrow it. And you can’t have cash show up in your account suddenly in the middle of your mortgage approval process without an explanation.

Understanding what mortgage lenders look at when considering you for a home loan could proactively help your case. Start early and work on reducing debt, increasing income and saving money for your down payment.

Decide What Mortgage You Can Afford

When you’re close to ready to start looking for a house and applying for a mortgage, take time to get an idea of how much mortgage you can actually afford. Start by taking a look at your budget—or create one if you don’t already have one.

Try to factor in expenses related to a new home, including savings for emergency repairs or maintenance. Once you know how much of a monthly payment you can afford, use an online mortgage calculator to test various loan and interest amounts. This helps you figure out your limits for home price, so you look for properties you can afford.

Research Potential Mortgage Options

Armed with knowledge about your budget, your credit and your overall financial status, hopefully you’re ready to do some research. Don’t apply yet—you want to apply for mortgages when you’re ready to make an offer on a home.

In the meantime, do some research. Talk to your bank, and maybe even reach out to a mortgage broker. That way, you’ll know your options and what you might qualify for.

Gather Documents to Apply for a Mortgage

During your research, make notes about what documents and items a mortgage lender requires for the application. Gather those documents and information before you apply for preapproval or a mortgage. You’ll save major time and hassle during the home loan approval process.

Some items you might need include:

Identification, such as a driver’s license or other government-issued ID.

Documentation of your income, such as paycheck stubs, W2 forms or tax returns.

Documentation of assets, especially assets like savings or investment accounts that might be involved in sourcing your down payment.

Your Social Security number for the credit check.

Documents showing you paid or settled any collections accounts or other negative issues on your credit report.

You may be asked for other items or documents throughout the mortgage underwriting process. When you apply for a mortgage make sure you’re available via email or phone, in case lenders have extra questions for you.

Consider Getting Pre-approved for a Mortgage

Getting pre-approved for a mortgage can be a good step. Preapproval doesn’t mean you’ve successfully completed the entire mortgage approval process. However, it does mean the lender did a cursory review of your credit history and score—as well as any income information you reported—and is fairly comfortable saying you’ll be approved with a certainrate.

Preapproval letters let you shop more confidently for a home. They also help demonstrate to sellers that you’re serious about your offer and will probably follow through without financial hiccups. In a competitive market with numerous offers on each home, this can make your offer more attractive to some sellers.

Apply for Mortgages Within a Short Period of Time

Finally, once you’re ready to purchase a home, ensure you apply for mortgages within a short period of time. Each time you apply for a loan, your credit is hit with a hard inquiry—which will bring your score down a bit. But the credit scoring models treat multiple mortgage applications within a short period of time as a single hard inquiry, because it’s assumed you may want to shop around for a good deal.

You should also be ready for the prospect of being approved with conditions. This means the mortgage lender will approve your loan as long as you meet certain conditions, which could include:

Providing supplemental documentation of credit history or income.

Satisfying the lender’s requirements for copies of banking statements or other documents.

Explaining an inconsistency or issue on your credit report.

Settling an old collections account or other debt.

Verifying where funds for a down payment came from.

Start Your Mortgage Application Process Today

Ultimately, being successful with the home loan application process comes down to being prepared and in good financial standing—or as in as good financial standing as you can. If you’ve gone through the above steps and are ready to apply for a mortgage, consider shopping for rates today.

Good credit requires responsible financial management over a period of time. However, there are some tactics you can try that help build your credit as fast as possible, if not exactly overnight. Find out more about these tips below.

In This Piece

Add Rent and Utility Payments

Your credit report and score are meant to help demonstrate whether you can manage money responsibly. But not every bill you manage gets reported to the credit bureaus.

Most landlords don’t send payment information to the credit bureaus, for example. And utility providers usually only report when you’ve defaulted on a bill. If you’re looking for how to increase your credit score quickly, getting these timely payments added to your report can be a good idea.

ExtraCredit lets you link rent and utility payments as trade lines to be reported to the credit bureaus. You can access this perk via the service’s Build It function to establish your credit by increasing your history of timely payments.

Pay Down Debt

Paying down debt is potentially one of the best things you can do for your credit. That’s because when you pay down revolving credit, you reduce your credit utilization, which has a big impact on your credit score.

It’s also helpful to pay down debt if you’ve fallen behind or have collection accounts on your credit report. Catching up past-due accounts and keeping up with them reflects positively on your score and can help you boost your credit.

Keep Utilization Low

Revolving credit includes credit cards, lines of credit and home equity lines of credit. Your credit utilization is a ratio of your total revolving credit balance compared to your total revolving credit limit.

For example, imagine you have two revolving credit accounts:

A credit card with a credit limit of $5,000 and a balance of $2,000

A line of credit with a limit of $5,000 and a balance of $1,000

You would have a total credit limit of $10,000 and a total balance of $3,000. That’s a credit utilization of 30%.

Credit utilization accounts for around 30% of your credit score. Keeping your credit utilization as low as possible—ideally below 30%—helps positively impact your scores.

Pay Bills on Time

Always pay all your bills on time. This is less a tip for boosting your credit overnight and more a tip on how not to wreck your credit overnight. One or two slips that lead to you paying bills 30 days or more past due can drastically and negatively impact your credit score.

Get a Secured Credit Card

A secured credit card is a card designed to help those with fair, poor, or bad credit build credit for the future. Getting one can help you boost your score.

Getting a credit card—and using it responsibly—can be a great way to boost your credit without actually going into debt. It might seem like a contradiction, but remember that a credit card doesn’t automatically mean debt. If you pay your balance off each month, you’re never in debt.

But you do still get some of the potential credit-boosting benefits of holding a credit card. The first is that your credit mix may be improved. Creditors like to see that you can manage multiple types of credit, and your credit score benefits when you have both installment and revolving credit.

Having a credit card also lets you address your credit utilization. If you have a credit card and you pay off the balance every month, you’ll have a lower credit utilization with a responsible payment history, which is good for your credit.

Get a Credit Builder Loan

If you already have a credit card, your credit mix might be suffering from the lack of an installment loan. Any type of installment loan—from a car loan to a personal loan—might benefit your credit score if you make your payments regularly and on time.

But for those who don’t have the credit history or score for a traditional installment loan, a savings-secured or credit-builder loan might be a good option. These loans often require deposits or savings accounts that you get back when you’re done paying for the loan, so they’re not loans designed specifically to provide for a financial need. They’re for the purpose of getting an installment loan and positive payment history on your report.

Become an Authorized User

If you don’t feel ready for your own credit card or can’t qualify for one, see if a family member will add you as an authorized user to their credit card account. Many banks and issuers report account activity to both the cardholder’s and authorized user’s credit report.

You do need to make sure you consider this option carefully. First, make sure the person you ask is responsible with their bills. If they pay their credit card bill late, you could end up with negative marks on your report.

Second, make sure the credit card company reports on authorized users. If the information doesn’t get added to your credit report, it can’t have an impact on your credit score.

Dispute Errors on Your Credit Report

Inaccurate items, such as a late payment reported when you never missed a payment, could unfairly bring your score down. Reviewing your reports and challenging errors may help improve your score. You can get a free credit report from each of the three bureaus every year at AnnualCreditReport.com. These are also available weekly for a limited time due to COVID-19.

In addition to rent and utility reporting, ExtraCredit shows you 28 of your FICO® scores and your credit reports from all three credit bureaus. You can check what’s showing up on your reports and what’s affecting your credit scores so you can follow up as necessary.

If you do find an error on your credit report during your investigation, be sure to challenge the accuracy of the error. Under law, you have a right to a credit report that’s fair and free of errors, so if information can’t be proved by the reporter, the credit bureaus may have to remove it.

Set Up Credit Monitoring Account

Invest in credit monitoring to take a proactive approach to protecting your score. By understanding exactly what’s going on with your report, you can address errors quickly and learn how your own actions impact your score. That helps you make potentially score-boosting decisions in the future.

Credit.com’s free Credit Report Card provides a snapshot of your credit report, with information about how you’re doing in the five critical areas for your score. Knowing how you’re doing can help you pinpoint areas that might need some help.

Don’t Close Accounts

This is another tip to keep from dragging down your credit score almost overnight. Keep credit cards and other revolving accounts open if you can, even if you aren’t using them. They can help reduce your credit utilization and increase your credit age, both of which are good for your score.

How Is Credit Score Calculated?

Understanding how your credit score is calculated helps you make good decisions that can boost your score. Credit scores are based on five factors:

Payment history, which is whether you pay your bills on time regularly

Credit utilization, which is how much of your open credit you’ve used

Credit age, which is the average age of your open accounts as well as how long you’ve had credit

Credit mix, which indicates you have a healthy mix of revolving and installment accounts

New credit, i.e., hard inquiries, which refers to whether a lot of lenders are checking your credit to evaluate you for loans

How Often Does Your Credit Score Update?