WASHINGTON, D.C. (September 27, 2023) — Mortgage applications decreased 1.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 22, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 2 percent compared with the previous week. The Refinance Index decreased 1 percent from the previous week and was 21 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 27 percent lower than the same week one year ago.

“Mortgage rates moved to their highest levels in over 20 years as Treasury yields increased late last week. The 30-year fixed mortgage rate increased to 7.41 percent, the highest rate since December 2000, and the 30-year fixed jumbo mortgage rate increased to 7.34 percent, the highest rate in the history of the jumbo rate series dating back to 2011,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Based on the FOMC’s most recent projections, rates are expected to be higher for longer, which drove the increase in Treasury yields. Overall applications declined, as both prospective homebuyers and homeowners continue to feel the impact of these elevated rates. The purchase market, which is still facing limited for-sale inventory and eroded purchasing power, saw applications down over the week and 27 percent behind last year’s pace. Refinance activity was down over 20 percent from last year and accounted for approximately one third of applications. Many homeowners have little incentive to refinance.”

The refinance share of mortgage activity increased to 31.9 percent of total applications from 31.6 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 7.5 percent of total applications.

The FHA share of total applications decreased to 14.1 percent from 14.2 percent the week prior. The VA share of total applications decreased to 10.9 percent from 11.0 percent the week prior. The USDA share of total applications increased to 0.5 percent from 0.4 percent the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) increased to 7.41 percent, the highest level since December 2000, from 7.31 percent, with points decreasing to 0.71 from 0.72 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $726,200) increased to 7.34 percent, the highest level since the series’ inception in January 2011, from 7.32 percent, with points decreasing to 0.78 from 0.80 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA increased to 7.16 percent, the highest level since March 2002, from 7.08 percent, with points increasing to 0.96 from 0.92 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 15-year fixed-rate mortgages increased to 6.73 percent, the highest level since July 2001, from 6.62 percent, with points increasing to 1.17 from 1.08 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 5/1 ARMs increased to 6.47 percent from 6.42 percent, with points increasing to 1.58 from 1.10 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The survey covers over 75 percent of all U.S. retail residential mortgage applications, and has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks, and thrifts. Base period and value for all indexes is March 16, 1990=100.

If you would like to purchase a subscription of MBA’s Weekly Applications Survey, please visit www.mba.org/WeeklyApps, contact [email protected] or click here.

The survey covers over 75 percent of all U.S. retail residential mortgage applications, and has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks, and thrifts. Base period and value for all indexes is March 16, 1990=100.

The Federal Reserve ended its long streak of interest rate hikes last week, but the pause may offer little reprieve to Americans squeezed by higher borrowing costs.

The decision left interest rates unchanged at a range of 5% to 5.25%, the highest level since 2001. However, policymakers also opened the door to additional rate increases this year, meaning there could be more pain for would-be homebuyers in the form of steeper mortgage rates.

“Higher rates are a positive for savers, but it also means mortgage rates may not fall all the way back to where they were in 2020 and 2021,” said Sonu Varghese, global macro strategist at Carson Group.

Mortgage rates spiked over the past year as the Fed waged an aggressive campaign to crush high inflation. In the span of just 16 months, the central bank approved 11 rate increases – the fastest pace of tightening since the 1980s.

A pedestrian passes the Federal Reserve building in Washington, D.C., on June 3, 2023.

MORTGAGE CALCULATOR: SEE HOW MUCH HIGHER RATES COULD COST YOU

While the federal funds rate is not what consumers pay directly, it affects borrowing costs for home equity lines of credit, auto loans and credit cards.

READ ON THE FOX BUSINESS APP

Rates on the popular 30-year fixed mortgage are currently hovering around 7.19%, according to Freddie Mac, well above the 6.29% rate recorded one year ago and the pre-pandemic average of 3.9%. It is near the highest level in two decades.

MORTGAGE DEMAND DROPS AGAIN AS INTEREST RATES EASE SLIGHTLY

Below, you can calculate how volatile increases and decreases in rates could affect the typical cost of a monthly mortgage.

Even just a minor change in rates can affect how much would-be homebuyers pay each month.

A recent study from LendingTree compared the average monthly payments on 30-year fixed-rate mortgages in April 2022 – when the rate hovered around 3.79% – and one year later, when rates jumped to 5.25%.

It found that higher rates cost borrowers hundreds more each month and potentially add as much as $75,000 over the lifetime of the 30-year loan.

The monthly mortgage payment for a median-priced home, calculated using the current 30-year mortgage rates and a 6% down payment, is about $2,590. That is dramatically higher than just three years ago, when that same mortgage payment would cost about $1,779.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

The spike in mortgage rates comes as the Federal Reserve wages an aggressive campaign to crush high inflation, raising interest rates at the fastest pace in decades in a bid to cool the economy and tame runaway prices.

While the federal funds rate is not what consumers pay directly, it affects borrowing costs, including everything such as home equity lines of credit, auto loans and credit cards.

Even just a minor change in mortgage rates can affect how much potential homebuyers pay each month.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

“Higher mortgage rates have radically altered homebuyer purchasing power and have been a key factor in existing home sales dropping from a more than 6.5 million unit pace in early 2022 to the roughly 4 million unit pace in recent months,” said Danielle Hale, chief economist at Realtor.com. “Perhaps more importantly, higher mortgage rates continue to keep existing homeowners sidelined because they don’t want to borrow at today’s much higher rates.”

Original article source: See how much higher mortgage rates are actually costing you

While the good news about housing keeps flooding in, one piece of negative data jumped out at me today.

The latest Zillow Negative Equity Report released today revealed that nearly one out of every five (18.6%) Las Vegas homeowners with a mortgage owed double what their home was worth as of the end of the fourth quarter.

In other words, if their home’s present value is $100,000, their mortgage balance is somewhere around $200,000.

For most people, this would signal being past the point of no return. After all, most of us have enough trouble paying off a mortgage when we’re above water, so the thought of owing double is daunting, even with a kick-butt mortgage rate.

Of course, if you stick around long enough, home price appreciation should do some of the heavy lifting, but it’s still a big ask for struggling homeowners.

While I cherry-picked a bad piece of data, it should be noted that 26.7% of Vegas homeowners were in this position one year earlier, so it’s not nearly as bad as it was.

And only 8.9% of underwater homeowners are delinquent on their mortgage payments, down from 9.9% a year earlier.

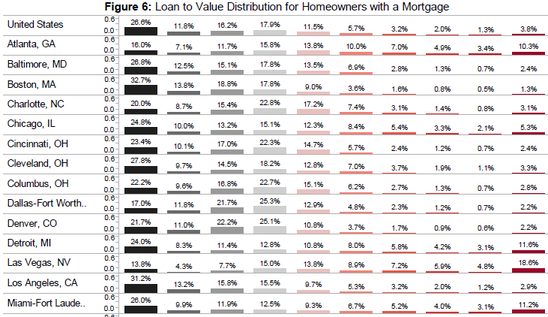

So yes, things are getting better…at the same time, the 200%+ loan-to-value (LTV) ratio bracket was the most prominent in Sin City.

In other words, if you went door to door and asked Vegas homeowners with mortgages what their LTV was, most would say 200%+.

The second largest distribution for Vegas homeowners was the 80-100% LTV tier (15% of borrowers), followed by the 100-120% LTV tier and under 40% tier, both at 13.8%.

3.8% of American Mortgagors Owe More Than Double Home’s Worth

If we expand the data to the whole of the United States, 3.8% of Americans with mortgages owed more than double what their homes were worth at the end of 2012.

That’s pretty scary, though the majority of U.S. homeowners with mortgages (26.6%) have LTV ratios south of 40%.

And 72.5% have a LTV somewhere below 100%, meaning they’re not the proud owners of an underwater mortgage.

If you look at the graphic below, you’ll notice that the LTV distribution is improving in every category, thanks to continued home price appreciation.

The low-LTV brackets are rising, and the high-LTV brackets are declining. All good news…

Overall, Zillow noted that the negative equity rate dropped to 27.5% in the fourth quarter from 28.2% a quarter earlier, and is now well below the 31.1% rate seen at the end of 2011.

As a result, nearly two million homeowners were able to get below the 100% LTV mark in 2012, though 13.8 million remain underwater.

Still, roughly one-third of all homeowners own their homes free and clear because they don’t have a mortgage.

Where’s the Inventory?

Zillow also has a nice little chart detailing how many homeowners will be “freed from negative equity” in 2013.

Using this data, we can guess which metros will see an increase in housing inventory, as that many more borrowers will finally be able to list their homes and move on to greener pastures.

The company expects 72,696 homeowners in Los Angeles to get above water in 2013, making it the leading metro in terms of total numbers.

Nearby Riverside is expected to “free” 62,407 homeowners, which represents a 21.2% decrease in the negative equity rate there, the second largest percentage decrease behind Sacramento (-21.3%).

In hard-hit Vegas, only 8,435 homeowners are expected to get above water this year, which represents just a 4.3% decline in negative equity.

And in Chicago, negative equity is actually forecast to get worse, with 7,019 more homeowners going under in 2013.

But overall, 999,601 homeowners should be “freed” in 2013, thanks in part to Zillow’s 3.3% home appreciation estimate.

This all reminds me of a post I wrote back in 2010, which claimed some real estate markets wouldn’t see a return to peak home prices until 2039.

In other words, while there is plenty of good news, it’s going to take a while to undo this mess.

According to a report prepared by the Congressional Research Service (CRS) earlier this month, there would be several immediate impacts following the program’s expiration.

“The authority to provide new flood insurance contracts will expire,” the CRS report said. “Flood insurance contracts entered into before the expiration would continue until the end of their policy term of one year.”

The borrowing authority of NFIP from the U.S. Treasury would also be reduced from $30.245 billion to $1 billion. Flood mitigation assistance grants would still be available, but “the expiration of the key authorities listed above would have potentially significant impacts on the remaining NFIP activities,” the CRS explained.

There would also be a chilling effect on the mortgage industry, according to experts and lawmakers.

“By law or regulation, federal agencies, federally regulated lending institutions and government-sponsored enterprises must require certain property owners to purchase flood insurance as a condition of any mortgage that these entities make, guarantee, or purchase,” the CRS report said.

Without NFIP, mortgage activity would be seriously diminished, as Sen. John Kennedy (R-Louisiana) stated.

“If for some reason the flood insurance program expires, existing policies are still in effect until their expiration date, and claims will continue to be paid as long as FEMA has money,” Kennedy said on the Senate floor on September 13. “However, the federal requirement that you have to purchase flood insurance under certain circumstances to get a mortgage would be suspended, which means that many mortgage companies would not loan the money to homeowners.”

In previous instances when NFIP lapsed, mortgage activity was temporarily halted. However, according to the CRS report, Congress eventually moved to reauthorize the program retroactively.

“In past NFIP lapses, borrowers were not able to obtain flood insurance to close, renew, or increase loans secured by property in [a Special Flood Hazard Area (SFHA)] until the NFIP was reauthorized,” the report said. “During the lapse in June 2010, estimates suggest over 1,400 home sale closings were canceled or delayed each day, representing over 40,000 sales per month. These figures applied to residential properties, but commercial properties were also affected by the NFIP lapse.”

The National Association of Realtors (NAR) has prepared an FAQ document to advise members of the potential impacts an NFIP lapse would have on the housing industry. They specify that a currently debated continuing resolution (CR) that would fund the federal government after September 30 includes an NFIP extension. Still, political observers and some in Washington are preparing for government funding to lapse.

The White House on Friday instructed federal agencies to prepare for a shutdown, according to reporting from the Associated Press.

“With the October 1 start of a new fiscal year and no funding in place, the Biden administration’s Office of Management and Budget began to advise federal agencies to review and update their shutdown plans, according to an OMB official,” the AP report said. “The start of this process suggests that federal employees could be informed next week if they’re to be furloughed.”

So, you’re considering purchasing a home? There’s a lot to think about—there’s lots of mortgage buzzwords and industry lingo to decipher. It can all be very overwhelming, especially for first-time home buyers.

One of the main decisions you need to make regarding your mortgage is selecting a fixed-rate or an adjustable-rate mortgage. Fixed-rate mortgages charge the same fixed interest rate for the duration of the loan. Adjustable-rate mortgages, on the other hand, have rates that fluctuate over time.

It’s important to understand how each type of mortgage works and how interest rates can impact your mortgage payments. Keep reading to learn more.

Key Takeaways

Interest rates for fixed-rate mortgages remain constant over the life of the loan.

ARM mortgages start with a lower fixed-rate period before switching to variable rates that are assessed regularly.

Deciding if an ARM or fixed-rate mortgage is right for you depends on your specific situation.

In This Piece

How Adjustable-Rate Mortgages (ARM) Work

Interest rates with an adjustable-rate mortgage, also referred to as an ARM, are variable—meaning they can change over time. Typically, ARMs start with a fixed-rate period, such as one, three, five, seven, or 10 years. After this initial period, interest rates adjust annually based on the current index. Your mortgage agreement details these terms.

When shopping for an ARM, you’ll notice that many types are listed as a ratio, such as 1/1, 3/1, 5/1, 7/1, 10/1 and more. The first number represents the number of years the mortgage will remain at the fixed-rate amount. In the example above, this would be one, three, five, seven, or 10 years.

The second number indicates how often the rates are adjusted after the initial fixed-rate phase is over. In most cases, this number is one, to represent one year. This means that rates are adjusted annually for most adjustable-rate loans.

Get matched with a personal

loan that’s right for you today.

Learn

more

Fortunately, many ARM agreements also include a cap for interest rates. For instance, one of the most common types of ARM is 5/1 with a 2/6 cap. This notation means the mortgage has a five-year fixed-rate period, after which the rates will reset every year. Interest rates, however, can’t increase more than 2% in any given year and not more than 6% in total over the life of the mortgage.

During the initial fixed-rate period of your mortgage, your monthly payments remain exactly the same. However, once this period is over, your monthly mortgage payments are likely to change from year to year depending on interest rates.

How Fixed-Rate Mortgages Work

Unlike an adjustable-rate mortgage, interest rates with a fixed-rate mortgage remain constant throughout the life of the mortgage. One of the best benefits of a fixed-rate mortgage is that your monthly payments remain exactly the same until the loan is paid in full. However, the amount of principal paid each month may fluctuate.

A disadvantage of fixed-rate mortgages is the potential for interest rates to decrease dramatically over the course of the loan. However, you can choose to refinance your mortgage, if you qualify, to take advantage of these lower rates.

ARM vs. Fixed-Rate Mortgage: Example Mortgage Payments

The table below can help you better understand the difference between mortgage payments for ARMs and fixed-rate loans.

Type of loan

5/1 ARM

30-year Fixed-Rate Loan

Mortgage amount

$400,000

$400,000

Interest rates

6.86%

7.66%

Monthly payments

$2,623.71 per month during the initial five-year fixed-rate period (payments will adjust annually thereafter)

$2,840.81

As you can see, initial interest rates are typically much lower for ARMs than for fixed-rate loans. However, after this initial phase, these rates can increase, which will also increase monthly payments. Use our convenient mortgage calculator to determine how much you can expect your monthly payments to be per month for an ARM and a fixed-rate mortgage.

Is an ARM or Fixed-Rate Mortgage Better?

There are advantages and disadvantages to both adjustable-rate and fixed-rate mortgages. For example, fixed-rate mortgages are easier to budget because monthly payments remain the same throughout the life of the mortgage. This can be a huge advantage for homeowners who are concerned about increasing rates.

However, if interest rates decline over the course of your loan, you’ll be stuck paying a higher amount. It may be possible to refinance your mortgage to take advantage of these lower rates. However, you must still have the right credit score to buy a home.

On the other hand, a great advantage of ARMs is that they typically offer lower initial interest rates. Oftentimes, homeowners have lower monthly payments during this initial phase vs. those opting for fixed-rate loans. The disadvantage is that interest rates could spike during the fixed-rate phase. If this happens, homeowners could face significantly higher mortgage payments at the end of the initial fixed-rate period.

Why Would You Choose an Adjustable Rate Over a Fixed Rate?

Adjustable-rate mortgages are an attractive offer for many first-time home buyers. First, they offer lower interest rates for the first several years, which results in lower monthly payments. Secondly, many first-time home buyers only plan to stay in their homes for several years before upgrading to larger houses.

In these cases, an ARM loan can be an ideal option because they’re likely to move before the end of the fixed-rate phase or soon after. This option allows them to enjoy lower interest rates until they’re ready to upgrade.

Tips for Choosing

Ultimately, selecting an ARM or a fixed-rate mortgage is a personal decision that depends on your specific situation. However, if you’re trying to choose between these two options, here are some factors to consider.

How Long Will You Be in the Home?

The first thing you want to consider is how long you plan to stay in your new home. If your plans are to remain in the home for only several years, an ARM may be the best option. For instance, if you plan to stay in your home for less than seven years, a 7/1 ARM will allow you to take advantage of lower interest rates until you sell the home.

If, on the other hand, this is your forever home, and you have no plans on moving in the near future, a fixed-rate mortgage that offers consistent monthly payments may be the better option.

How Frequently Does the ARM Adjust?

You also want to check the details of the loan and determine how often ARM rates will adjust. For example, a 7/1 ARM offers 7 years of ARM rates at the fixed rate, then the interest rates readjust every year afterward. Rates on a 7/6 ARM will readjust every six months. If this is too much fluctuation for your budget, you may want to consider a fixed-rate mortgage.

What Are Interest Rates Like?

Another thing you want to consider is the current state of interest rates and predictions for future increases or decreases. When interest rates are low, investing in a fixed-rate mortgage can help you lock in these lower rates. Alternatively, when interest rates are high or rising, it may make more sense to select an ARM, with hopes that these rates will come back down before the initial fixed-rate period ends.

How Much Can You Afford Now?

ARMs typically offer lower monthly payments during the first few years. This can be an attractive option for those just beginning their careers and planning to increase their earnings in the future. An adjustable-rate mortgage allows you to take advantage of lower monthly payments now and risk possible higher payments when you have more wealth.

Can You Afford a Payment Increase?

It’s important to recognize that as interest rates with an ARM adjust, so will your monthly payments. Make sure you can budget these shifts. Even if ARM caps are in place, monthly payments can increase quickly, especially with a six-month adjustment frequency. If you’re uncertain of your ability to maintain higher monthly payments, you may want to choose a fixed-rate mortgage.

Understand Your Options

Fixed-rate and adjustable-rate mortgages are both good options for home buyers. The important thing is to understand the difference between these two choices and to evaluate your specific situation. When you factor in these issues, you can better determine which option is right for you.

PNC has increased the signup bonus on the Cash Rewards Visa card to $200 after $1,000 spend (previously $100) within the first three billing cycles. You can see that offer on PNC here.

Additionally, there is an in-branch offer which will offer double cashback during the first year. PNC will automatically post any earned double cash back to your account one year after opening.

Offer is valid 9/6/23 – 11/6/23

You can try calling into a banker at a PNC branch to see if they can process the branch offer over the phone, just make to get confirmation that it’s for the double cash back offer.

You can see an image of the offer on this website.

Card Details

No annual fee

Sign up bonus of $100 after $1,000 in purchases

Card earns at the following rates ($8,000 annual cap on the 2%/3%/4% categories):

4% cash back on gas purchases

3% cash back on dining purchases

2% cash back on grocery purchases

1% cash back on all other purchases

Introductory 0% APR on balance transfers for the first 12 billing cycles following account opening when the balance is transferred within the first 90 days following account opening

You can redeem for cash back when you have $25 or more in your account

Applications restricted to the following states: AL, DC, DE. FL, GA, IL, IN, KY, MD, MI, MO, NC, NJ, OH, PA, SC, VA, WI, WV

Read our full review here.

Our Verdict

The $200 signup bonus can be done online, and for the hassle of going in branch you’ll hopefully be able to get this offer with the double cashback. If someone can max out the $8,000 on gas, that would get you an extra $320 in cashback (that’s in additional to the generous 4% regular earn rate on gas).

PNC branches are around in many states, listed above. I can see this being a nice deal for someone who can max out the gas category, and possibly even for the other categories. Some people might also consider signing up for the online offer to get the $200 signup bonus. The ongoing rate of of 4% on gas is pretty nice too, irrespective of any signup bonus.

Updates to the Marriott Bonvoy Bevy™ American Express® Card welcome offer

The $250-annual-fee Marriott Bonvoy Bevy™ American Express® Card’s latest welcome offer is sure to excite Bonvoy enthusiasts with a big jump in value for the same spending requirement.

Here’s how the two offers compare:

New offer: Earn 125,000 Marriott Bonvoy bonus points after you use your new Card to make $5,000 in purchases within the first 6 months of Card Membership. Terms Apply.

Previous offer: Earn 85,000 Marriott Bonvoy bonus points after you use your new Card to make $5,000 in purchases within the first 6 months of Card Membership. Terms Apply.

Ongoing rewards: The Marriott Bonvoy Bevy™ American Express® Card will continue to offer its ongoing rewards rate of 6 points per dollar spent on participating Marriott Bonvoy hotels; 4 points per dollar spent at restaurants worldwide and at U.S. supermarkets (up to $15,000 in combined purchases per year); and 2 points per dollar spent on all other eligible purchases. Terms apply.

Updates to the Marriott Bonvoy Brilliant® American Express® Card welcome offer

The latest offer on the $650-annual-fee Marriott Bonvoy Brilliant® American Express® Card offers the potential for significantly more value with the same spending requirement. But since the offer comes in the form of free night certificates rather than points, you’ll sacrifice flexibility when you redeem.

Here’s what’s changing and what’s staying the same:

New offer: Earn two 85K Free Night Awards after you spend $6,000 in purchases on the Card in your first 6 months. Each award can be used for one night (redemption level at or under 85,000 Marriott Bonvoy points) at hotels participating in Marriott Bonvoy. Card Members could enjoy a value of up to $1,200 when redeeming each reward. Certain hotels have resort fees. Offer ends 11/1/2023. Terms Apply.

Previous offer: Earn 95,000 Marriott Bonvoy bonus points after you use your new Card to make $6,000 in purchases within the first 6 months of Card Membership. Terms Apply.

Ongoing rewards: The Marriott Bonvoy Brilliant® American Express® Cardwill continue to offer its ongoing rewards rate of 6 points per dollar spent at participating Marriott Bonvoy hotels; 3 points per dollar spent at U.S. restaurants; 3 points per dollar spent on flights booked directly with airlines; and 2 points per dollar spent on all other eligible purchases. Terms apply.

Are the new offers better?

Although they’re not the best offerings, the latest welcome offers on AmEx’s Marriott Bonvoy cards are quite a boost in value. For the Bevy card, you’ll earn nearly 50% more points than the previous offer. And if you’re able to use the free night certificates for full value for the Brilliant card, the new offer represents a 78% boost.

But while the latest Marriott Bonvoy Brilliant® American Express® Card offer carries significantly higher value, it comes with far less flexibility. The two Free Night Awards are worth up to 85,000 points per night, but they expire one year from when they’re issued.

Plus, it may be difficult to redeem them for full value. If you redeem the 85,000-point certificate at a hotel that’s charging 60,000 points for the night you want to stay, you won’t get the difference back in points. On the other hand, an 85,000-point certificate may not cover a luxury St. Regis or Ritz Carlton hotel stay, which could cost 100,00 points or more per night. (Marriott does allow you to apply certificates toward a higher-priced room and cover the difference with up to 15,000 points.)

Marriott Bonvoy points can be redeemed at more than 8,600 hotels worldwide. Bonvoy points can also be transferred to certain airline partners, or redeemed for car rentals, gift cards, and other options. The value of points may vary depending on how you redeem them.

How the cards compare

When comparing these new welcome offers, there are a few more factors about the two cards worth keeping in mind, most notably the difference in annual fees. The Marriott Bonvoy Bevy™ American Express® Card, which comes with complimentary Gold status, carries an annual fee of $250. Notably, it does not come with an automatic free annual stay. The Marriott Bonvoy Brilliant® American Express® Card comes with automatic Platinum status and a higher (though less flexible) welcome offer. But with an annual fee of $650, those extra perks come at a steep cost.

Here’s a breakdown of how the two cards compare:

At a glance

Marriott Bonvoy Bevy™ American Express® Card

Marriott Bonvoy Brilliant® American Express® Card

Annual fee

Welcome offer

Earn 125,000 Marriott Bonvoy bonus points after you use your new Card to make $5,000 in purchases within the first 6 months of Card Membership. Terms Apply.

Earn two 85K Free Night Awards after you spend $6,000 in purchases on the Card in your first 6 months. Each award can be used for one night (redemption level at or under 85,000 Marriott Bonvoy points) at hotels participating in Marriott Bonvoy. Card Members could enjoy a value of up to $1,200 when redeeming each reward. Certain hotels have resort fees. Offer ends 11/1/2023. Terms Apply.

Ongoing rewards

6 points per $1 spent on participating Marriott Bonvoy hotels.

4 points per $1 spent on up to $15,000 in combined purchases per year at restaurants worldwide and at U.S. supermarkets.

2 points per $1 spent on all other eligible purchases.

Terms apply.

6 points per $1 spent at participating Marriott Bonvoy hotels.

3 points per $1 spent at U.S. restaurants and on flights booked directly with airlines.

2 points per $1 spent on all other eligible purchases.

Terms apply.

Other benefits

1,000 Marriott Bonvoy bonus points with each qualifying stay.

Complimentary Gold Elite status.

A Free Night Award after making $15,000 in purchases per year for any hotel worth 50,000 points or less.

15 Elite Night Credits each calendar year.

Terms apply.

One Free Night Award each year after card renewal for any stay at a redemption level of 85,000 points or less.

Automatic Platinum Elite status.

$300 statement credit for restaurant purchases (up to $25 per month).

Mortgage application activity bounced back from the holiday-shortened prior week but is still running significantly below historic levels. The Mortgage Bankers Association (MBA) said its Market Composite Index, a measure of application volume, increased 5.4 percent on a seasonally adjusted basis during the week ended September 15. On an unadjusted basis, the Index increased 16 percent compared with the week that started with Labor Day.

The Refinance Index rose 13 percent week-over-week and was 29 percent lower than the same week in 2022. The refinance share of mortgage activity increased to 31.6 percent of total applications from 29.1 percent the previous week.

The seasonally adjusted Purchase Index gained 2.0 percent compared to the prior week. The unadjusted Purchase Index increased 12 percent and was 26 percent lower than the same week one year ago.

“Mortgage applications increased last week, despite the 30-year fixed rate edging back up to 7.31 percent – its highest level in four weeks,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Purchase applications increased for conventional and FHA loans over the week but remained 26 percent lower than the same week a year ago, as homebuyers continue to face higher rates and limited for-sale inventory, which have made purchase conditions more challenging. Refinance applications also increased last week but are still almost 30 percent lower than the same week last year.”

Added Kan, “The average loan size on a purchase application was $416,800, the highest level in six weeks. Home prices in many markets have been supported by low inventory and resilient housing demand for available homes.”

Other Highlights from MBA’s Weekly Mortgage Applications Survey

The average size of a purchase loan, $416,800, was almost $4,000 higher than the prior week while the overall size of loans drifted down from $368,100 to $365,600.

The FHA share of total applications was unchanged at 14.2 percent while the VA share dipped to 11.0 percent from 11.3 percent. USDA applications accounted for 0.4 percent of total applications, identical to the previous week.

The 7.31 percent average contract interest rate for conforming 30-year fixed-rate mortgages (FRM) was 4 basis points higher than a week earlier. Points were unchanged at 0.72.

The rate for jumbo 30-year FRM increased to 7.32 percent from 7.25 percent,with points increasing to 0.80 from 0.72.

Thirty-year FHA-backed FRM had a rate averaging 7.08 percent with 0.91 point. The prior week the rate was 7.04 percent,with 0.98 point.

Fifteen-year FRM rates declined by an average of 10 basis points to 6.62 percent while points increased to 1.08 from 1.01.

The average contract interest rate for 5/1 adjustable-rate mortgages (ARMs) decreased to 6.42 percent from 6.59 percent,with points decreasing to 1.10 from 1.16.

The ARM share of activity decreased to 7.2 percent of total applications from 7.5 percent.

Collecting and trading Pokémon cards has been a popular hobby since the 1990s for both children and adults. In fact, as a kid, I was obsessed with Pokémon cards. I enjoyed opening new packs, collecting cards, and trading with my friends. And, I know I’m not alone. So many people have enjoyed Pokémon cards over…

Collecting and trading Pokémon cards has been a popular hobby since the 1990s for both children and adults.

In fact, as a kid, I was obsessed with Pokémon cards. I enjoyed opening new packs, collecting cards, and trading with my friends. And, I know I’m not alone. So many people have enjoyed Pokémon cards over the years as well.

As the value of certain cards continues to rise, finding the best places to sell your collection of Pokémon cards is more important than ever.

Whether you’re looking to make some extra cash, simply downsize your Pokémon card collection, or if you are decluttering everything you own and find a long lost box of childhood mementos, knowing where and how to sell your Pokémon cards can be important to make the most money.

In this article, I’ll discuss some of the best places to sell Pokémon cards online and locally and provide tips on how to price and present your cards in the best way.

Quick Summary

Identify and evaluate the value of your Pokémon cards before selling. Some cards are worth way more than others. For example, one card may be worth $0.10, and another may be worth over $100,000.

Look at your different selling options to see how you can get the most money.

Learn effective selling tips and strategies for presenting your cards to potential buyers.

How To Sell Pokemon Cards

Selling your Pokémon cards can be an exciting and profitable way to make money, especially if you have rare, holographic, or near-mint-condition cards in your collection.

To help you make the most profit, follow these tips to find the best places to sell your Pokémon cards. Before starting your Pokémon cards selling journey, it’s important to know your cards’ condition, rarity, and type.

Related: How I Made $40,000 In One Year Selling Items

Near-mint cards with no creases, scuffs, or whitening edges tend to have a higher value. Also, rare and holographic cards, like the famous Charizard, are highly wanted by fans, collectors, and trading card game enthusiasts, making them valuable in the Pokémon card market.

To figure out how rare your Pokémon card is, look for the symbols in the bottom right corner of your card and if you have a lot of cards, then you should become familiar with the Pokémon card rarity indicators, as well as the different sets and booster packs in which your cards were released.

For more accurate valuations, you may even look for professional grading services, such as Professional Sports Authenticator (PSA). They evaluate and grade cards based on their condition, ensuring buyers of their authenticity and quality.

If you’re selling Pokémon cards online, make sure to take clear, high-quality pictures that showcase your cards’ condition, as this will give potential buyers a better idea of what they’re purchasing.

By following these tips and tricks, you’ll be prepared to sell your Pokémon cards and get the most amount of money.

Best Places To Sell Pokemon Cards Online

There are many ways to sell Pokémon cards online. Here are some Pokémon selling sites to start with:

1. eBay

eBay is one of the most popular marketplaces for selling Pokémon cards due to its large reach of customers around the world.

I did a quick search on eBay and there are currently over 160,000 Pokémon cards for sale – so they definitely have a huge market!

You can choose to sell your cards through auctions or fixed price listings. When selling on eBay, be mindful of the seller fees and PayPal fees that will be deducted from your earnings. Shipping will also be another cost.

eBay is especially good for selling valuable cards, such as holographic cards or rare Charizard cards. To reach a wider audience and increase the chances of a successful sale, make sure you write detailed descriptions and add high-quality photos of your cards so that people are more likely to click on your listing.

2. Troll and Toad

Troll and Toad is an online store that specializes in collectible card games, such as selling Pokémon cards and they have been around for over 25 years.

They offer a buy list where you can sell your cards for cash or store credit. To sell on Troll and Toad, simply use their search bar to find the cards you want to sell, add them to your cart, checkout, and then ship your cards to them.

This is a great feature of Troll and Toad – the fact that you can see the exact cards they will accept and the exact amount that they will pay you for each Pokémon card. As you will learn below, many of the Pokémon card selling websites have this same feature, which is so helpful!

After you complete the list of cards that you plan on selling to them, you will print out an invoice that they give you, and then choose a payment method. Then, you will ship your box of Pokémon cards to them. Once they receive the package, they will verify the cards that you have sent to make sure they are in the correct condition as you stated. After that, they will pay you.

Troll and Toad also accepts Pokémon cards in bulk.

Keep in mind that they may be selective about the cards they accept, so it’s important to research and determine the value of your cards beforehand.

3. Mercari

Mercari is a site where you can quickly set up an account and start selling your used items, such as Pokémon cards. This site is not dedicated to just Pokémon cards, but they do have many listed and it is an easy option for Pokémon collectors.

There are well over 1,000 Pokémon cards listed on Mercari.

It’s important to create persuasive listings with photos and a relevant, detailed description, and include relevant keywords related to Pokémon cards. (Remember, they don’t just sell Pokémon cards, they also sell clothes and other items, so keywords are important!). Also, Mercari takes a minimum 10% fee from each sale you make on their platform.

4. TCGplayer

TCGplayer is a popular site with card game collectors in the U.S. and Europe.

People love selling on this site because they say it’s easy to use and they have great customer service.

To sell Pokémon cards on TCGplayer, simply list your cards on the TCGplayer marketplace, set your prices, and wait for potential buyers to purchase them. The marketplace handles the transactions, making the selling process easy.

Note: You will have to pay a commission fee of around 12–13% for each sale you make on TCGplayer, and you might also have shipping costs.

Here’s a quick guide on how to sell Pokémon cards on TCGplayer:

Create a seller account – You will need an account to get started selling Pokémon cards.

Set up your inventory – Once your seller account is created, you can start listing your Pokémon cards for sale. Enter details like the card’s name, set, condition, and quantity available.

Pricing your cards – Decide on the prices for your Pokémon cards. You can either manually set the prices or use TCGplayer’s automated pricing tool to match the market rates. TCGplayer has a pricing algorithm to help sellers be competitive and adjust prices based on the market demand.

Shipping options – Decide on the shipping options you will have for buyers.

Receiving payments – TCGplayer usually collects payments from buyers, processes the orders, and then deposits the money into your seller account. From there, you can withdraw your funds.

Maintain your inventory – Keep your inventory up to date. Remove sold items and add new ones to reflect the current availability of your Pokémon cards.

5. Card Cavern

Card Cavern is an online store that specializes in buying and selling Pokémon cards.

They have a straightforward buylist system where you can quickly find the cards they’re interested in and the prices they’re willing to pay.

Then, you ship your cards to them (they recommend purchasing tracking and insurance).

If you choose to sell your cards to Card Cavern, you’ll receive payment through PayPal or receive store credit, depending on your preference.

Their buy rates only apply to near-mint, English, tournament legal cards. You can send as many or as little Pokémon cards as you want to Card Cavern.

6. Dave & Adam’s

Dave & Adam’s is an online store for trading cards, including Pokémon cards, and it has been around for over 30 years.

They offer a buy list where you can see which cards they’re currently interested in purchasing. If your cards match their buy list, you can submit a sell request, ship your cards to them, and receive payment via check, PayPal, or store credit.

If you have a big collection, they will even travel to you.

7. Pokémon Facebook Groups

Pokémon Facebook Groups are communities of Pokémon card collectors and enthusiasts who use the platform to buy, sell, and trade cards. Pokémon Facebook Groups are exactly what you think – Facebook groups for Pokémon card collectors.

This can be a great place to sell your Pokémon cards because these groups are filled with people who are very interested in buying Pokémon cards.

These groups allow you to talk directly with fellow collectors and cater to various interests, such as specific regions, sets, or rarity levels.

To sell your Pokémon cards in these groups, make sure you follow group rules, post clear photos, and respond quickly to potential buyers’ inquiries.

8. CCG Castle

CCG Castle is a website that specializes in games since 2007.

They buy Pokémon cards that you no longer need and have a buy list on their site that will tell you exactly what they are accepting and how much they will pay you for it. They pay in either PayPal cash or store credit.

Best Places To Sell Pokemon Cards Near Me

If you’re looking to sell your collection or particular Pokémon cards, there are several options near you to consider. This section will cover the best local places where you can sell your cards, such as Facebook Marketplace, comic book stores, pawn shops, and Craigslist.

9. Facebook Marketplace

A popular and easy way to sell your Pokémon cards is through Facebook Marketplace. Nearly everyone has a Facebook account, so it can be easy for you to get started, and it allows you to connect with local buyers who might be interested in your cards.

Posting on Facebook Marketplace is simple, and you can include photos, descriptions, and set your price. Also, you can communicate with potential buyers through Facebook Messenger, making it easy to negotiate and set up a meeting location.

There are no listing fees when selling on Facebook Marketplace, which means that you get to keep everything you earn. But, you do have to handle everything yourself.

10. Local comic book stores

Comic book stores, particularly those that specialize in trading cards, card games, and board games, can be a great place to sell your collection.

Many local comic shops are interested in buying Pokémon cards to stock their inventory for other gamers and collectors.

You can visit stores in your local area, ask if they purchase Pokémon cards, and provide the store owner with a list or photos of your cards. They may make an offer on the spot or ask you to come back later. Remember, each comic store is different, so it’s a good idea to try a few stores near you to compare offers and don’t stop at just one.

11. Pawn shops

Another option to consider is pawn shops.

Pawn stores are known for buying various items, including sports cards and collectibles like Pokémon cards. Take your cards to a few pawn shops near you and see if they’re interested in buying your collection.

Keep in mind that pawn shops usually offer lower prices than other options (this is because selling Pokémon cards is not their sole business), but they can be a quick and convenient way to sell more popular cards.

12. Craigslist

Craigslist is a site for buying and selling various items locally – I’m sure you’ve heard of it. You can create a detailed listing for your Pokémon cards, including pictures, descriptions, and asking prices.

Interested buyers in your area can contact you, allowing you to arrange a meetup in a safe and convenient location.

Craigslist is usually a little more difficult to sell Pokémon cards on and that is because this site does not specialize solely in Pokémon cards and is very localized.

Where to Sell Pokemon Cards in Bulk

Selling your Pokémon cards in bulk may be something that you are interested in if you simply don’t have the time to look each one up.

When selling your Pokémon cards in bulk, it’s important to find the right platform. In this section, we’ll focus on three popular options: Full Grip Games, Safari Zone, and Sell2BBNovelties. With their unique offerings and easy-to-sell process, these companies can help you get the most value for your collection if you simply don’t have the time or have too many cards to sort through.

13. Full Grip Games

Full Grip Games is a local game shop in Ohio that buys bulk Pokémon cards online and in person.

At Full Grip Games, they make it easy for you to sell your bulk cards in increments of 100 or 1,000. Also, they accept rares and other card types as well. To make things simpler for you, their website has a bulk buy list that breaks down all the packs and cards they accept along with individual prices.

To get started, follow these easy steps:

Click on the “Buylist Instructions” link on their website.

Choose their full singles buylist or their bulk buylist.

Select the cards in your collection according to the buylist.

Review the pricing and total value of the cards submitted.

Once done, send the cards following their shipping instructions.

Once they receive your bulk cards, it will take them around one week to go through them. For the cards they accept, you can get paid via PayPal, store credit (you will get a 30% bonus if you choose the store credit option), or check via USPS mail.

14. Safari Zone

Safari Zone is another great option to consider for selling your Pokémon cards in bulk. They accept a wide range of cards, but they do need to be in near-mint condition.

Here’s what you should do to sell your cards on Safari Zone:

Create an account on the Safari Zone website.

Review the cards they purchase on their buy list.

Enter the card details.

After submitting the card information, you’ll receive a quote for your collection.

Ship your cards to Safari Zone, and they will process your payment after validating the cards.

Safari Zone only pays via store credit.

15. Sell2BBNovelties

Sell2BBNovelties is a website that has been around since 1999 that specializes in toys and collectibles, such as Pokémon cards.

They have an easy platform to sell your Pokémon cards in bulk and accept various card types, including rares, holographic, and common/uncommon cards.

To sell your Pokémon cards on Sell2BBNovelties, simply:

Go to their website and click on the “Buying Prices” tab.

Select the cards you’re selling according to their buying list.

When you’re ready, submit the form. You’ll receive a confirmation email with the total value of the cards and further instructions.

Ship your cards to Sell2BBNovelties, and they will process your payment upon receiving and verifying your cards.

You can receive payment for the cards they accept in either PayPal cash or store credit.

How to Make a Website to Sell Pokemon Cards

If you have the time and a lot of cards, you may even be interested in starting a website to sell your Pokémon cards.

Creating a website to sell your Pokémon cards is a great idea to reach a wider audience and have lower fees. Of course, there will be more work in this because you will be managing everything yourself.

Choose a platform and create your design – Look for an easy-to-use platform to build your website – my favorite is WordPress. You will want to pick a clean looking design that customers can look at on both computer and phone. Most platforms have a variety of premade themes that you can use. You can also personalize your website by adding your logo, choosing colors that represent your brand, and adding images.

Organize your products – Categorize your Pokémon cards by sets, rarity, or other criteria that make sense for your target audience. Clear product descriptions and high-quality images of each card will help potential buyers too.

Set up payment and shipping – Choose a payment gateway to securely process transactions. Options like PayPal, Stripe, or Square are widely used and reliable. Choose shipping options and rates based on your preferred carriers and shipping destinations.

Create valuable content – In addition to listing your Pokémon cards, consider creating helpful content such as blog posts or videos that add value to your website and attract more readers and buyers. Providing informative content will establish you as an expert in the field and help drive traffic to your site.

Promote your website – Use social media, search engine optimization (SEO), or even paid advertising to increase page views to your website.

Related: How To Start A Website Free Course

Pokemon Card Selling Tips and Strategies

Selling your Pokémon cards can be an exciting way to make extra money, but it’s important to have a little strategy so that you can make the most money and find the most buyers.

Here are some tips for selling your Pokémon cards successfully.

Determine the value of your cards. You should research how rare the card is, the origin, and the condition of your cards, as these factors will affect their worth. Keep an eye out for rare and valuable cards (such as first edition cards and illustrations), as these will attract more interest from collectors. Grading your cards can help with this process – professional grading services can rate the condition of your cards and encapsulate them in a case, increasing their value.

Consider where to sell your cards.There are numerous platforms for selling Pokémon cards online, such as eBay, where you can list your cards as single items or in an auction format. There are also more specialized Pokémon selling websites which are dedicated to trading cards. These sites often have dedicated communities of potential buyers who are very interested in Pokémon cards.

Write clear and accurate descriptions of your cards.You should always be clear and honest about your card’s condition. For example, are there any scratches or bends? Is there a tear or water damage?

Ship your cards carefully.Carefully package your Pokémon cards to protect your cards from damage during transit. You will want to keep your cards waterproof and not use rubber bands (rubber bands can damage the cards). Also, consider offering a tracking number and insurance to your buyer as an additional layer of security. Many of the Pokémon selling sites above have a very exact way they want you to ship the cards to them to prevent any damage, so be sure to see what their rules are.

By following these Pokémon card selling tips and tricks, you can increase the chances of finding the best places to sell your Pokémon cards.

Frequently Asked Questions

Here are answers to common questions about selling Pokémon cards.

How do I know if my Pokemon cards are worth money?

So, how do you know if the Pokémon cards that you have are worth anything? Many people have Pokémon cards, probably stuffed in a box somewhere, or maybe you came across some.

Whatever your reason is, yes, your Pokémon cards may be worth something.

Knowing the value of your Pokémon cards is important before selling, and there are a few key things to think about.

First, look at the rarity symbols on your cards: a circle indicates a common card, a square represents an uncommon card, and a star denotes a rare card. These symbols help you determine the rarity of your cards and their potential worth.

The condition of your cards also plays a big role in their value. Cards in mint condition, meaning they have no visible wear or damage, are worth more than cards with minor imperfections. Holographic cards, especially in mint condition, can be more valuable.

To take it a step further, you could even get your Pokémon cards professionally valued and graded by a reputable company like PSA. Grading involves a professional inspection of your card’s condition, assigning a numerical grade based on factors such as centering, corners, edges, and surface. The higher the graded number, the better the condition and, often, the higher the value.

Keep in mind that while Pokémon cards typically have higher values, other trading card games like Yu-Gi-Oh can also be valuable. Make sure to research the prices of similar cards sold recently, and compare the condition of your cards to decide if they’re worth selling.

How do I sell Pokemon cards for cash?

To sell your Pokémon cards for cash, first organize your cards by set and look for rare ones to see what you have. Once you’ve prepared your collection, follow the selling instructions on your chosen platform.

You can sell your Pokémon cards online, locally near you, and even in bulk.

Where can I find buyers for my Pokemon cards?

You can find buyers for your Pokémon cards on online marketplaces, local card shops, and social media groups. Websites like eBay and TCGplayer are popular places for selling Pokémon cards, as well as community forums and local collector’s events.

What are some reputable websites to sell Pokemon cards?

There are many reputable sites to sell Pokémon cards as we discussed above, such as:

eBay

Troll and Toad

Mercari

TCGplayer

Card Cavern

Dave & Adam’s

Pokémon Facebook Groups

Full Grip Games

Safari Zone

Sell2BBNovelties

Where is the best place to sell Pokemon cards?

The best place to sell your Pokémon cards depends on your preferences. eBay gives you a worldwide market and you are probably already familiar with their platform.

TCGplayer and Troll and Toad specialize in trading card sales and have a lot of Pokémon cards for sale.

Pokémon Facebook Groups are a great way to connect with those interested in Pokémon cards, and there are no listing fees – but you would be dealing with people on your own and handling everything yourself.

Are there any local stores that buy Pokemon cards?

Some local stores, like comic book shops, game stores, and pawn shops, may buy Pokémon cards. You can call local stores to see if they buy cards before bringing your collection in person.

Can you sell Pokemon cards on Etsy?

Etsy is generally geared towards handmade and vintage items, so it’s not an ideal platform for selling Pokémon cards. It’s best to stick with platforms like eBay, TCGplayer, or Troll and Toad for selling trading cards.

I did a search for Pokémon cards on Etsy and it said there were 43,326 results, but I think many of these are for custom art, in that they would be turning a picture of you or your pet into a Pokémon card. So, not the same thing.

Can I sell Pokemon cards on eBay?

Yes, you can sell Pokémon cards on eBay. It is one of the most popular sites for selling Pokémon cards and it gives you control over pricing and listing options.

Can you sell Pokemon cards at GameStop?

GameStop typically does not buy or sell individual Pokémon cards.

Do pawn shops buy Pokemon cards?

Some pawn shops may buy Pokémon cards, especially if they are valuable or rare. Call your local pawn shops or visit them in person to inquire about their interest in buying Pokémon cards. Remember, they do not specialize in Pokémon cards and have a smaller market, so you may not get as much for your Pokémon cards at a pawn store.

What does TCG and CCG mean?

As you’re going through the sites above looking for one of the best places to sell your Pokémon cards, you may come across these two terms. CCG means collectible card game and TCG means trading card game.

How can I determine the value of my Pokemon cards?

Figuring out the value of your Pokémon cards involves considering factors like:

rarity

condition

age

Websites like TCGplayer and Troll and Toad provide price guides and historical sales information to help you estimate the value of your cards.

How do I check the value of my Pokemon cards?

Check the value of your Pokémon cards by researching on websites like TCGplayer, eBay, and Pokémon Price. These platforms can give you a good idea of the current market value for individual cards.

Do you need a license to sell Pokemon cards?

You generally do not need a license to sell Pokémon cards, unless you’re planning to sell them by opening an in-person store. Check your local regulations to make sure you’re following any required guidelines.

How much is Charizard Pokemon card worth?

Charizard cards vary widely in value and can be worth anywhere from $25 to over $50,000. The Charizard Pokémon card that is worth the most is typically a mint condition 1st Edition from the base set.

What Pokemon cards are worth more than $100?

Some Pokémon cards worth more than $100 include rare Pokémon cards, such as first edition holographic cards from the original sets, high-grade cards, misprints, and promotional cards like the Pokémon Illustrator card.

What is the most expensive Pokemon card?

The most expensive Pokémon card varies over time; some examples include the Pokémon Illustrator card, the 1st Edition Charizard, or unique, one-of-a-kind promo cards handed out during official Pokémon events. The rarest Pokémon cards obviously cost more money and sell for more.

According to TCGplayer, the most expensive Pokémon cards include:

Pokémon World Championships No. 2 Trainer Promo

No. 2 Trainer Toshiyuki Yamaguchi (2000)

Neo Genesis 1st Edition Lugia (2000)

Super Secret Battle No. 1 Trainer (1999)

Family Event Trophy Kangaskhan (1998)

Test Print Blastoise Gold Border (1998)

Tsunekazu Ishihara Signed Promo (2017)

Trophy Pikachu No. 3 Trainer Bronze (1997)

Commissioned Presentation Blastoise Galaxy Star Holo (1998)

First Edition Shadowless Holographic Charizard #4 (1999)

Illustrator Pikachu (1998)

These were all sold for over $100,000 each.

Best Places To Sell Pokemon Cards – Summary

I hope you enjoyed this article on the best places to sell Pokémon cards and how to sell Pokémon cards for cash.

If you have Pokémon cards that you no longer want, there are many ways you can sell them. And, they may be worth a lot of money!

To figure out the value of the Pokémon cards that you want to sell, you’ll want to look at their rarity symbols, Pokémon card condition, grading (if applicable), and market comparisons. Understanding these factors will help you decide if your cards are worth selling and where to find the best prices.

Once your cards are sorted and evaluated, it’s now time to choose the best places to sell your Pokémon cards. Here are some popular options:

eBay – This site has millions of Pokémon cards sold every year. It’s a great place to find a worldwide audience, but remember to factor in shipping costs and eBay fees.

Facebook Marketplace and Pokémon Facebook Groups – Connect with local collectors or fans without worrying about shipping fees. This option may mean that you will meet the buyer in person.

Local comic shops – These stores can be an easy place to sell your cards, especially if they specialize in Pokémon cards or trading card games.

TCGplayer – Catering specifically to trading card game fans, this site has a dedicated space for buying and selling Pokémon cards.

Other options include Troll and Toad, Card Cavern, Dave & Adam’s, Sell2BBNovelties, pawn shops, and more.

Good luck selling your Pokémon cards!

What do you think is the best place to sell Pokemon cards for cash?