Reporting by Saqib Iqbal Ahmed; Writing by Ira Iosebashvili; Editing by Stephen Coates

Apache is functioning normally

FHFA revises current single-family mortgages backed by Fannie Mae, Freddie Mac (iStock)

FHFA revises current single-family mortgages backed by Fannie Mae, Freddie Mac (iStock)

The Federal Housing Finance Agency (FHFA) will revise the treatment of active single-family mortgages backed by government-sponsored enterprises Fannie Mae and Freddie Mac for which borrowers elected a COVID-19 forbearance under the Enterprises’ representations and warranties framework, according to its newest media release.

“Under the updated rep and warrant policies, loans for which borrowers elected a COVID-19 forbearance will be treated similarly to loans for which borrowers obtained forbearance due to a natural disaster,” the FHFA said. “As a result, loans with a COVID-19 forbearance will remain eligible for certain rep and warrant relief based on the borrower’s payment history over the first 36 months following origination.”

FHFA Director Sandra L. Thompson argued that homeowners, who needed more time to keep up with housing costs during the pandemic, benefited from a mortgage forbearance plan that would reduce or suspend mortgage payments.

“Forbearance was an invaluable tool for borrowers experiencing financial hardship due to the COVID-19 pandemic,” Thompson said. “Servicers went to great lengths to implement forbearance quickly amid a national emergency, and the loans they service should not be subject to greater repurchase risk simply because a borrower was impacted by the pandemic.”

The Enterprises’ existing rep and warrant policies with respect to natural disasters allow the time the borrower is in forbearance to be included when demonstrating a satisfactory payment history in the first 36 months following origination, the FHFA noted. These policies will now expand to loans for which borrowers elected a COVID-19 forbearance.

Thompson stressed the importance of helping current and prospective homeowners manage present housing conditions at the Mortgage Bankers Association Annual Convention last week. “In a housing market like this one, it is all the more important that both our policies and the industry’s efforts align to support existing and aspiring homeowners,” Thompson said. “That is why I believe a model based on partnership and mutual feedback is necessary for us to achieve our shared goal of promoting affordable and sustainable housing opportunities.”

If you’re considering becoming a homeowner, it could help to shop around to find the best mortgage rate. Visit Credible to compare options from different lenders and choose the one with the best rate for you.

MORTGAGE RATES KEEP CLIMBING, BUT BUYERS CAN FIND THE BEST DEALS BY DOING THESE TWO THINGS: FREDDIE MAC

Mortgage rates are continuing their ascent. The average 30-year fixed-rate mortgage rose to 7.63% for the week ending Oct. 19, according to the Freddie Mac’s latest Primary Mortgage Market Survey. This time in 2022, the 30-year fixed-rate was below 7%.

Buyers may do well for themselves by browsing for the best home loans and making a considerable down payment. Freddie Mac’s Chief Economist Sam Khater said “in this environment, it’s important that borrowers shop around with multiple lenders for the best mortgage rate.”

Freddie Mac announced last week the launch of DPA One®, a new tool that strives to help mortgage lenders quickly find and match borrowers to down payment assistance programs nationwide.

“DPA One delivers a one-stop shop at no cost that brings lenders and their borrowers greater detail and visibility into these programs, while seamlessly connecting the right assistance program with the lender, housing counselors and borrowers who need this assistance the most,” Sonu Mittal, Freddie Mac’s senior vice president of and head of single-family acquisitions, explained.

“With research showing down payment is the single largest barrier to first-time homebuyers attaining homeownership, borrowers should also ask their lender about down payment assistance,” Khater said.

If you’re looking to buy a home, you could still find the best mortgage rates by shopping around. Visit Credible to compare your options without affecting your credit score.

MANY AMERICANS PREPARING FOR A RECESSION DESPITE SIGNS THAT SAY OTHERWISE: SURVEY

By end of 2023, there is likely to have been around 4.1 million existing home sales in the U.S., which would mark the weakest year of home sales since the Great Recession of 2008, according to a Redfin report.

Redfin’s Economic Research Lead Chen Zhao said current conditions have led to buyer and seller hesitancy across the board.

“Buyers have been in a bind all year,” Zhao said. “High mortgage rates and still-high prices are making it harder than ever to afford a home, shutting many young people out of homeownership and causing homeowners to reevaluate whether 2023 is the right time to move. Mortgage rates are staying high longer than anticipated, keeping away everyone except those who need to move and pushing our sales projection for the year down to a 15-year low.

“The last time home sales were this low was during the Great Recession,” Zhao continued.

Redfin agents suggest that buyers invest in newly built properties which are performing more strongly than existing-home sales. Newly constructed homes saw sales increase 1.5% year-over-year in September as prices dropped about 4%, according to Redfin’s data.

Based on the findings from a National Association of Realtors (NAR) report, the total amount of home sales decreased by 2% from August to September and have dropped 15.4% since September 2022.

Looking to reduce your home buying costs? It may benefit you to compare your options to find the best mortgage rate. Visit Credible to speak with a home loan expert and get your questions answered.

AFFORDABILITY KEEPING YOU FROM OWNING A HOME? HERE’S HOW YOU CAN GET READY

Have a finance-related question, but don’t know who to ask? Email The Credible Money Expert at [email protected] and your question might be answered by Credible in our Money Expert column.

Source: foxbusiness.com

Average mortgage rates on 30-year fixed home loans continued their march towards 8% this week as the Treasury yield surpassed 5%. Rates have been steadily climbing for seven straight weeks, the longest consecutive increase since Spring 2022, according to Freddie Mac‘s Primary Mortgage Market Survey.

The average 30-year, fixed-rate mortgage rose to 7.79% as of Oct. 26. That’s up 16 basis points from the previous week and up 71 basis points from 7.08% a year ago, the survey showed.

HousingWire’s Mortgage Rates Center showed Optimal Blue’s average 30-year fixed rate for conventional loans at 7.83% on Thursday, compared to 7.78% the previous week.

“Rates have risen two full percentage points in 2023 alone and, as we head into Halloween, the impacts may scare potential homebuyers,” Sam Khater, Freddie Mac’s chief economist, said in a statement.

“Purchase activity has slowed to a virtual standstill, affordability remains a significant hurdle for many and the only way to address it is lower rates and greater inventory.”

As mortgage rates keep climbing, mortgage applications sank to their lowest level since 1995.

According to Bob Broeksmit, president and CEO of the Mortgage Bankers Association (MBA), the lack of inventory and the affordability challenges are the main culprits, steering prospective home shoppers to the sidelines.

“We expect mortgage volume to decline nearly 30% this year to $1.64 trillion, before an expected 19% rebound in 2024 as rates finally start to trend downward,” Broeksmit said in a statement.

However, recent home sales readings stressed the resiliency of the housing market as buyers kept shopping despite the challenging environment.

This week, new-home sales and pending-home sales posted month-over-month gains in September. However, Realtor.com Senior Economic Research Analyst Hannah Jones expects home sales activity to hover at a low level until the end of 2023.

The National Association of Realtors (NAR) also forecasts that existing-home sales will drop by 17.5% in 2023, reaching an annualized rate of 4.15 million units sold.

For mortgage rates to improve, investors will need reassurance that the Fed will pause its contractionary policy at its next meeting next week, Jones said in a statement.

Source: housingwire.com

While existing homebuyers have been battling high mortgage rates for months — which are now at 8% — the builders are wooing buyers with lower rates and incentives. Today, the new home sales data beat expectations and surprised people. However, sales have been rising slowly for some time.

Using a low bar of sales from last year, the builder’s incentives have created more sales growth and their significant advantage is that they’re offering lower rates to move homes. Imagine what the existing home sales market would look like if mortgage rates were below 6%. We certainly wouldn’t be trending below 4 million existing home sale today if that was the case.

From Census: New Home Sales: Sales of new single‐family houses in September 2023 were at a seasonally adjusted annual rate of 759,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 12.3 percent (±16.6 percent)* above the revised August rate of 676,000 and 33.9 percent (±22.9 percent) above the September 2022 estimate of 567,000..

As you can see in the chart below, new home sales are slowly growing, There’s nothing gangbusters here, but new home sales have been slowly moving higher for some time. This is very different from the housing bubble years, where sales were booming like crazy and got close to 1.4 million. Currently, the seasonal adjusted annual rate of sales is just 759,000.

From Census: For Sale Inventory and Months’ Supply The seasonally adjusted estimate of new houses for sale at the end of September was 435,000. This represents a supply of 6.9 months at the current sales rate.

Here’s my model for understanding the builders.

We have been able to build more single-family housing, and single-family permits have been slowly rising, which offsets the multifamily weakness that should be here for some time now, as we can see in the chart below. The monthly supply of new homes is falling from the recent peak but needs more work to return to pre-COVID-19 levels.

One of the things I like to do is break down the monthly supply data into subcategories. We have a lot of homes in the pipeline that still need to get built; this is why the builders are making deals. As we see in the monthly supply data, they had a spike last year and are forced to create incentives to move homes. Here’s how the supply breaks down:

One of the data lines that very few people know about, but is critical to the inventory story in the U.S., is how many new homes are built and ready for sale! It’s not a lot now, nor has it ever been a lot. Even during the housing bubble crash years, we never got above 200,000. Most active listings’ inventory growth comes from the existing home sales market.

Keep things simple with today’s new home sales report: the builders confidence has been falling for months as rates have risen; many builders can’t pay down rates, and the ones that do are taking a hit on their profit margins.

However, the builders’ profit margins are still higher today than in the previous decade. This is the first time this century that we have seen a noticeable gap between purchase application data and new homes because, as we all know, the builders are singing: Baby, it’s cold outside…come inside for lower rates.

Source: housingwire.com

Fall is typically a busy time for the housing market, but it’s off to a slow start in Santa Cruz County, with home sales and prices weakening across parts of the region in September as soaring mortgage rates caused some prospective buyers to cool their heels.

The county saw 107 home sales in September, down about 15% from August, when there were 126 sales. The market was significantly quieter than in September 2022, when the county saw 132 home sales — or 19% more than last month. Sales activity fell the most in pricier markets such as Santa Cruz and Aptos compared to August, but rose in more-affordable Watsonville.

The countywide median sale price dropped 3.5% last month to $1.142 million, compared to $1.185 million in August. That’s in part because buyers purchased smaller homes on average, according to data from the Santa Cruz County Association of Realtors, but also because higher interest rates have deterred buyers from paying over the list price, said Coldwell Banker agent Jessica Wallace.

“Things are selling, but they’re on the market for longer and not many sales are going over the asking price,” she said. “On average, things are selling for about 98% of the asking price, which is actually a normal market.”

Wallace explained that in 2022 properties sold for an average of 102.4% of their asking price, and in 2021, things sold for an average of 104% of the asking price.

“It seemed like most properties had multiple offers, some had like 25 offers, which is crazy,” she said. “And it would be common to hear of properties routinely getting something like 10 offers.”

Mortgage rates hit their highest point in more than 20 years this month, with 30-year mortgage rates reaching an average of 7.63% last week, according to data from Freddie Mac. That compares to a recent low of less than 3% in 2021.

While mortgage rates have been hovering around 6-7% for much of the past year, the recent bump has been enough for some buyers to feel additional pressure.

“We’re seeing a little bit more of a lull than we’re probably used to, and rates going up a bit again didn’t help,” said Santa Cruz County Association of Realtors President Jennifer Watson. “That causes people to fall into a fear mentality and many start to pull back.”

Wallace agreed, saying that mortgage rate increases have proven to be “killing buyers’ affordability” in an already expensive market. “A person trying to put 20% down and looking at possibly an 8% interest rate is not fun,” she said.

The city of Santa Cruz saw 27 home sales in September, five fewer than in August. The average home sale involved a smaller property, causing the median price to dip from $1.532 million to $1.5 million. That’s still a 6% increase over September of last year.

Watsonville, which has been one of the busiest markets in the county, saw 20 home sales in September, three more than in August and four more than in September 2022.

The slight uptick in sales made Watsonville the second-busiest market last month — a spot usually occupied by Aptos. Aptos saw 17 home sales in September, eight fewer than in August.

However, buyers’ preference for smaller homes and fewer sales over asking price brought the Watsonville median sale price down significantly to $727,500 from $810,000 in August — about a 10% drop.

Realtors say the market slowdown isn’t all bad news, however. Watson explained that as some buyers pull back from the market, that can open the door for other buyers who have previously been outbid on properties.

“Especially with our lower-end market, some have been looking for three or more years and have either been beaten out by cash or people spending on a pandemic house,” said Watson. “Now, they have that time to negotiate a little bit more.”

Properties are also still selling despite the consistent upticks in mortgage rates. Some select properties are still drawing very high bids — Wallace cited a Seabright house that sold for $450,000 over list price in recent weeks.

“If you told me 10 or 12 months ago that rates would be where they are today, I would have said no one will be buying or selling real estate,” said Marvin Christie, co-owner and president of Anderson Christie Real Estate, adding that he too has seen some clients pull back because of high mortgage rates. “And here we are, still buying and selling real estate.”

And agents continue to look ahead to next year, when they still believe that rates will drop.

“I expected the short-term [rates] to stay steady and the long-term to start declining by now,” said Christie. “That hasn’t taken effect, but I still believe that it will. It’s just a matter of time.”

Have something to say? Lookout welcomes letters to the editor, within our policies, from readers. Guidelines here.

Source: lookout.co

Home equity lending in the United States is on the rise. While reverse mortgage volume has yet to benefit from that spiked interest, consumer curiosity about Home Equity Lines of Credit (HELOCs) appears to be translating into significant volume gains for that product, according to Bankrate.

“Online searches for ‘HELOC’ rose 305 percent this year, reaching an all-time high in July 2023, according to a Google traffic analysis by real estate platform RubyHome,” the Bankrate article said.

But that curiosity is also translating into volume. Based on data released by both ATTOM Data Solutions and the Mortgage Bankers Association (MBA) this past summer, “lenders originated more than 284,000 HELOCs in the second quarter of the year,” up from just under 252,000 in the first three months of 2023, while debt from home equity loans is projected to increase by more than 11% by the end of this year.

Part of this is likely due to a spike in home prices, which has been observed in the market since the beginning of the COVID-19 pandemic.

“The median home sales price stood at $394,300 in September 2023, according to the National Association of Realtors,” the article said. “While down from the record high of $413,800 in June 2022, it still represents a 2.8% increase year-over-year.”

Home equity-related debt also appears to be a growing segment of personal debt carried by homeowners. A survey for Creditcards.com showed that 7% of Americans hold debt in the form of home equity loans and/or lines of credit, but homeowners are also using equity as a source of extra cash to be able to further invest in their homes.

“Many people are tapping into their home equity to spruce up their homes, and better equip them to meet their family’s needs,” the article explained. “Borrowing money to upgrade their current home makes a lot more sense than trying to buy into a new one nowadays.”

That rise in home price appreciation, in addition to increasing levels of tappable equity for homeowners, also translates into a challenging housing market for prospective buyers, which may give some insight into the motives related to additional equity-based debt.

Source: reversemortgagedaily.com

For those of you still wondering why home prices haven’t plummeted, despite significantly higher mortgage rates, it’s because there isn’t a negative correlation.

A lot of people seem to think that home prices and mortgage rates have an inverse relationship, but it simply isn’t true.

Just look at history and you’ll see that it’s perfectly normal for home prices and interest rates to rise.

Or for both rates and prices to fall in tandem. Ultimately, there isn’t a strong correlation either way.

However, home sales certainly slow down when the cost of financing rises, as we’ve seen this year.

First off, let’s look at the current dynamic in the housing market. Both mortgage rates and home prices have risen considerably over the past year and change.

The 30-year fixed has climbed from around 3% to start 2022 to 7.63% today, per Freddie Mac weekly survey data.

Despite this more than doubling in interest rates, home prices increased 4.6% from July 2022 to July 2023, per the FHFA’s latest seasonally adjusted monthly House Price Index (HPI).

This is higher than the annual growth rate since 1991, which seems like a head-scratcher. How could home prices outperform with mortgage rates surging?

Well, higher mortgage rates generally indicate that the economy is hot, which it most certainly has been over the past year and change.

More jobs and increased wages, coupled with a low interest rate environment, increased the money supply and led to a lot more consumer spending and an increase in prices, home prices included.

Unfortunately, this also resulted in high inflation, which is why the Fed has raised its own policy rate 11 times since early last year.

But this economic strength is what continues to propel home prices higher, coupled with a severe lack of for-sale inventory.

So if you’re wondering why 8% mortgage rates haven’t sunk the home prices, now you know.

On the other hand, when mortgage rates increase significantly, home sales tend to take a big hit.

This happens for obvious reasons, the main one being a lack of affordability. Fewer home buyers can qualify when financing costs are prohibitively high.

Sure, folks have seen their wages increase and they might have a good job, but their DTI ratios aren’t what they used to be.

Per NAR, total existing-home sales fell 2.0% in September from August to a seasonally adjusted annual rate of 3.96 million.

Sales were down 15.4% year-over-year from 4.68 million in September 2022, and are now at their lowest sales pace since October 2010.

For reference, existing home sales exceeded the six million mark back in 2021, the highest level since 2006.

Meanwhile, the inventory of unsold listings was up 2.7% in September from a month earlier, totaling 1,130,000 homes for sale.

But supply was off 8.1% compared with September of 2022, representing just 3.4 months at the current sales pace. That’s well below NAR’s desired 6-month supply.

However, despite less demand and fewer buyers, the lower number of sales isn’t resulting in lower prices.

Instead, we simply have a housing market with low demand and low supply, and not a lot of budging from sellers on price.

That could change as time goes on, but even with mortgage rates around 8% we’ve yet to see big price declines. And we might not.

What’s perhaps even stranger to the untrained eye is that when mortgage rates swing higher, home prices seem to outperform.

That brings me to an interesting piece written by Jonathan Lansner, who looked at home prices and sales volume in Southern California, and the impact of higher/lower mortgage rates.

He found that median prices have appreciated 4.7% since 1988, but this annual gain in Los Angeles averaged 7.6% when mortgages “were in their steepest jumps.”

Meanwhile, when mortgage rates “were in their steepest drops,” LA median home prices only experienced 1.6% gains.

So you’re telling me high mortgage rates fueled even higher home prices. And declining mortgage rate resulted in falling home prices?

Apparently, yes. As for why, it’s the economy! Remember, mortgage rates tend to rise when the economy is doing well.

And they often decline when the economy goes downhill, or falls into a recession, which some believe is overdue at this point.

I wrote a piece a while back regarding this very topic and found that mortgage rates went down during every recession since 1980.

The one exception was the 1973-1975 recession, when 30-year fixed mortgage rates increased slightly from 8.58% to 8.89%.

With regard to jobs, Lansner noted that over the past 35 years, employment grew 2.7% annually in California when mortgage rates “surged,” but shrank at a 0.7% annual pace when rates “tumbled.”

So maybe just maybe, prospective home buyers will discover that lower mortgage rates are accompanied by lower asking prices, possibly in 2024.

Read more: Mortgage rates and home prices can fall together.

Source: thetruthaboutmortgage.com

Traders work on the floor of the New York Stock Exchange (NYSE) in New York City, U.S., August 29, 2023. REUTERS/Brendan McDermid Acquire Licensing Rights

NEW YORK, Oct 19 (Reuters) – Relentless selling of U.S. government bonds has brought Treasury yields to their highest level in more than a decade and a half, roiling everything from stocks to the real estate market.

The yield on the benchmark 10 year Treasury – which moves inversely to prices – briefly hit 5% late Thursday, a level last seen in 2007. Expectations that the Federal Reserve will keep interest rates elevated and mounting U.S. fiscal concerns are among the factors driving the move.

Because the $25-trillion Treasury market is considered the bedrock of the global financial system, soaring yields on U.S. government bonds have had wide-ranging effects. The S&P 500 is down about 7% from its highs of the year, as the promise of guaranteed yields on U.S. government debt draws investors away from equities. Mortgage rates, meanwhile, stand at more than 20-year highs, weighing on real estate prices.

“Investors have to take a very hard look at risky assets,” said Gennadiy Goldberg, head of U.S. rates strategy at TD Securities in New York. “The longer we remain at higher interest rates, the more likely something is to break.”

Fed Chairman Jerome Powell on Thursday said monetary policy does not feel “too tight,” bolstering the case for those who believe interest rates are likely to stay elevated.

Powell also nodded to the “term premium” as a driver for yields. The term premium is the added compensation investors expect for owning longer-term debt and is measured using financial models. Its rise was recently cited by one Fed president as a reason why the Fed may have less need to raise rates.

Here is a look at some of the ways rising yields have reverberated throughout markets.

Higher Treasury yields can curb investors’ appetite for stocks and other risky assets by tightening financial conditions as they raise the cost of credit for companies and individuals.

Elon Musk warned that high interest rates could sap electric-vehicle demand, which knocked shares of the sector on Thursday. Tesla’s shares closed the day down 9.3%, as some analysts questioned whether the company can maintain the runaway growth that has for years set it apart from other automakers.

With investors gravitating to Treasuries, where some maturities currently offer far above 5% to investors holding the bonds to term, high-dividend paying stocks in sectors such as utilities and real estate have been among the worst hit.

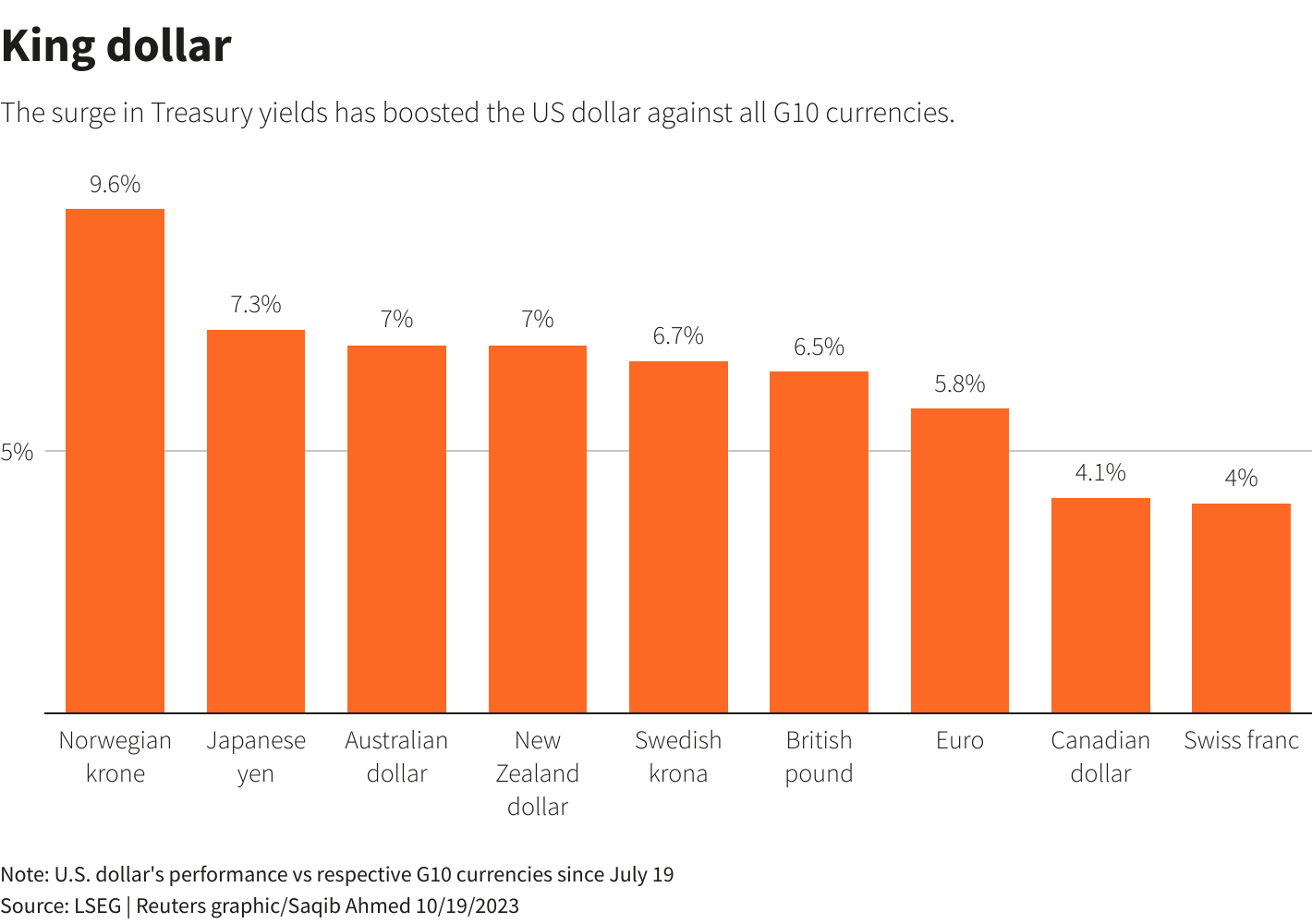

The U.S. dollar has advanced an average of about 6.4% against its G10 peers since the rise in Treasury yields accelerated in mid-July. The dollar index, which measures the buck’s strength against six major currencies, stands near an 11-month high.

A stronger dollar helps tighten financial conditions and can hurt the balance sheets of U.S. exporters and multinationals. Globally, it complicates the efforts of other central banks to tamp down inflation by pushing down their currencies.

For weeks, traders have been watching for a possible intervention by Japanese officials to combat a sustained depreciation in the yen, down 12.5% against the dollar this year.

“The correlation of the USD with rates has been positive and strong during the current policy tightening cycle,” BofA Global Research strategist Athanasios Vamvakidis said in a note on Thursday.

The interest rate on the 30-year fixed-rate mortgage – the most popular U.S. home loan – has shot to the highest since 2000, hurting homebuilder confidence and pressuring mortgage applications.

In an otherwise resilient economy featuring a strong job market and robust consumer spending, the housing market has stood out as the sector most afflicted by the Fed’s aggressive actions to cool demand and undercut inflation.

U.S. existing home sales dropped to a 13-year low in September.

As Treasury yields surge, credit market spreads have widened with investors demanding a higher yield on riskier assets such as corporate bonds. Credit spreads blew out after a banking crisis this year, then they narrowed in subsequent months.

The rise in yields, however, has taken the ICE BofA High Yield Index (.MERH0A0) near a four-month high, adding to funding costs for prospective borrowers.

Volatility in U.S. stocks and bonds has bubbled up in recent weeks as expectations have shifted for Fed policy. Anticipation of a surge in U.S. government deficit spending and debt issuance to cover those expenditures has also unnerved investors.

The MOVE index (.MOVE), measuring expected volatility in U.S. Treasuries, is near its highest in more than four months. Volatility in equities has also picked up, taking the Cboe Volatility Index (.VIX) to a five-month peak.

Reporting by Saqib Iqbal Ahmed; Writing by Ira Iosebashvili; Editing by Stephen Coates

Our Standards: The Thomson Reuters Trust Principles.

Source: reuters.com

Southern California home sales hit an eight-month high in April as Bay Area sales jumped 28.8 percent from March, but it’s not as pretty as it sounds, according to the latest analysis from DataQuick.

The company said 15,615 houses and condos sold in the Southland during April, up 21.9 percent from March, but still off 19 percent from April 2007.

Not to mention the fact that last month was also the worst April since 1995, when 15,303 homes sold, and well below the average April sales figure of 25,311.

And foreclosure sales as a percentage of the total homes sold rose to 37.5 percent in April, up from 35.8 percent in March and just 4.6 percent a year ago.

In Riverside County, foreclosure sales accounted for 52.7 percent of the transactions.

Two-thirds of Southland sales in April consisted of homes priced under $500,000, largely because jumbo loan financing has been frozen for quite some time, accounting for just 15.1 percent of sales during the month, down from roughly 40 percent a year ago.

Bay Area Sales Up as Prices Fall

A total of 6,310 homes and condos sold in nine counties in the Bay Area during April, up from 4,898 in March, but off 15.3 percent from the 7,447 sold a year earlier.

It was the slowest April since 1995, when only 5,636 homes were sold.

The median price paid for a home last month was $518,000, off 3.4 percent from $536,000 one month earlier and more than 20 percent from $659,000 a year ago.

Jumbo loans accounted for just 28.8 percent of the sales financed last month, down from 63.4 percent last year.

Foreclosure sales accounted for just over a quarter of the April sales, with levels as high as 44 percent in Contra Costa County and 54 percent in Solano County.

(photo: docentjoyce)

Source: thetruthaboutmortgage.com

DOJ’s concern over housing affordability and commission rates For the mortgage sector, the spotlight on commission rates comes at a time when the housing market is already grappling with low supply and escalating mortgage costs. The Biden administration’s focus on these rates is intertwined with the broader issue of housing affordability. On a median existing-home … [Read more…]

A home for sale in the Ashby Acres community in Phoenix on Sept. 6, 2023. (Photo by Kevinjonah Paguio/Cronkite News)

PHOENIX – High home sales prices and mortgage interest rates are squeezing out first-time home buyers from entering the market, especially as incomes have not kept up, housing experts say.

In 2020, the housing market was in a frenzy. High numbers of homes were selling, agents’ inventories were low and offers were frequently being made over list prices, said Jason Giarrizzo, a realtor with West USA Realty, who has been in the industry for 31 years.

Coming out of 2020, during the COVID-19 pandemic, the market continued to surge as people began buying real estate, Giarrizzo said. “We weren’t sure where the market was going to go, (if) it (was) going to plummet because of you know, the shutdown and everything, but it was quite the opposite.”

A balanced market in the Phoenix metropolitan area would have inventory levels of about 30,000 properties, Giarrizzo said, but by the end of 2021 inventory began to shrink to about 4,400 properties in the area.

Then, home prices hit a high and interest rates began to climb as the Federal Reserve started raising rates in an attempt to head off inflation. “In all my years of real estate, I don’t think I saw the inventory spike to the level that it did in such a short period of time. We went from 4,400 properties just coming into spring to almost 20,000 properties for sale by summer,” Giarrizzo said.

The downtown Phoenix skyline overlooks homes in the Willo Historic District in Phoenix on Sept. 6, 2023. (Photo by Kevinjonah Paguio/Cronkite News)

Now, the inventory is at about 13,000, which is still half of what a balanced inventory is for the Phoenix metropolitan area, Giarrizzo said.

As mortgage loan interest rates have risen, that frenzy has subsided, especially for the first-time buyers market, Giarrizzo said.

Mortgage loan interest rates vary widely based on factors such as the individual market, credit score of the buyer, price of the home, down payment, rate type, loan term and type.

The current average rate for a conventional 30-year fixed mortgage is at or below 8.063% for a $430,000 home in Arizona for a buyer with a credit score of 700-719 who puts 10% down, according to the Consumer Financial Protection Bureau.

Chris Giarrizzo, a mortgage loan officer at Lennar Mortgage, who has been in the industry for over 23 years and is married to Jason Giarrizzo, said many hourly workers are struggling to afford housing, whether it’s a home purchase, or even rent.

The median home sale price in the Phoenix metropolitan area in September 2023 was $435,700, according to Redfin, a real estate firm that tracks prices and trends.

“I actually wouldn’t say necessarily it’s a bad time to buy a home, it’s just a challenging time to buy a home,” Chris Giarrizzo said.

Although mortgage loan rates have been this high before, high sales prices are providing little relief to buyers, she said, and there’s no relief anticipated until possibly sometime next year.

The last time 30-year fixed mortgage loan rates reached 8% was in 2000.

It was a combination of people who moved to the state and people who had more disposable income following the pandemic shutdown that drove the market takeoff in the Phoenix metropolitan area in 2020, Chris Giarrizzo said.

“We weren’t out shopping and weren’t traveling, and so I’ll be honest, not only in my industry, but in several industries, people had said that they had never been as busy. … We were all working a lot of hours,” Chris Giarrizzo said.

A “perfect storm” of high demand, low interest rates and not enough inventory drove home values up, creating the frenzy of people paying over list price because there was so much competition, she said.

“You’ve got a lot of people that are just sitting on the sidelines right now, eager to jump in and buy their first home,” Chris Giarrizzo said.

Many people locked in low interest rates years ago, so even if it makes sense to move or downsize, they don’t, because they’ll be looking at interest rates of over 7%, Jason Giarrizzo said.

A February Realtor.com survey found that 82% of homeowners with existing low-rate mortgages feel “locked in.”

“Even though the frenzy is over, I don’t see a plummet in home values,” Jason Giarrizzo said. “We’re not going to see big spikes in inventory, I think, due to those people that have locked in on those low rates.”

Interest rates will eventually fall, but when and by how much is hard to predict, Chris Giarrizzo said, noting rates under 3% were largely pandemic-driven and will probably not be seen again.

In August 2021, the 30-year mortgage rate hovered around 2.8%, according to data from the Arizona Regional Multiple Listing Service.

“If we can get rates back into the fours or fives (percent), I think we’ll see a start to return to a more balanced market,” Chris Giarrizzo said.

In northern Arizona, where Jason Giarrizzo also sells real estate, the properties are being sold more quickly and at much higher prices, although there is still low inventory. “I’ve been working more in that $1 million to $2.5 million range, and actually I’m seeing a lot of those deals go in cash,” he said.

But in Payson, and other nonluxury home markets in northern Arizona, the same housing squeeze is being felt, where the housing is largely unaffordable due to the combination of rates and list prices, Chris Giarrizzo said.

J Cruz, a 46-year-old Phoenix park ranger, started his home search two months ago and does not see a light at the end of the tunnel.

“Trying to find a good deal – that’s been very hard and challenging,” Cruz said. “Monthly mortgage payments are way too high for what I want, and it’s not feasible to pay that every month.”

He fixed his credit score, saved for a down payment and recently started the process of getting a home loan.

But mortgage interest rates are one of the things holding Cruz back. “I don’t want to get into a home that I can afford for a few months and not be able to afford two years from now,” he said.

Cruz is in search of a three-bedroom home in Phoenix, Peoria or Glendale, and even though he is a full-time city employee and has good benefits, he and many of his co-workers have part-time jobs to make ends meet.

“Even though we have a full-time job with the city, you know, in today’s economy it is still a little bit hard,” Cruz said.

New-build financing at interest rates lower than market rate is probably the best route for a lot of first-time buyers, especially if they are struggling to qualify, Chris Giarrizzo said.

Federal Housing Administration loans are available for first-time homebuyers, with down-payment options as low as 3.5%.

Zillow Home Loans is offering a 1% down payment incentive to buyers in Arizona to reduce the amount of time that it takes for eligible buyers to save.

The program is intended for buyers who have kept up with high monthly rent payments but have not been able to save for a down payment.

“I would just advise borrowers that the less down you’re putting, the higher your (monthly) payments are going to be,” Chris Giarrizzo said.

Source: cronkitenews.azpbs.org