Mortgage giant Mr. Cooper has tapped Mike Weinbach, a veteran banking executive, as president following current leader Chris Marshall’s expected retirement at the end of this year.

Weinbach, the longtime CEO of Chase Home Lending and former CEO of consumer lending at Wells Fargo, will begin his role Feb. 1, Mr. Cooper announced Tuesday. Marshall, also the company’s vice chairman, will remain onboard to assist with the transition and lead fundraising for Mr. Cooper’s mortgage servicing rights fund.

“I have long admired Mr. Cooper’s impressive record of growth and profitability as well as their commitment to the customer experience, and I am thrilled to hit the ground running with this fantastic team,” said Weinbach in a press release.

Company chairman and CEO Jay Bray in a statement commended Weinbach’s background in consumer lending. Weinbach worked at JPMorgan Chase from 2003 through 2020, heading mortgage operations in his final five years there. He worked in the newly-created consumer lending role at Wells from 2020 to 2022, overseeing the launch of a new portfolio of credit cards.

The incoming president will oversee Mr. Cooper’s originations, servicing and technology efforts. Weinbach steps in at a critical time for the publicly traded giant, following a massive data breach in November exposing the Social Security numbers of over 14 million customers. The incident has spawned over a dozen class action lawsuits from consumers, while Moody’s in November suggested the incident could impact the firm’s creditworthiness.

The company reported strong earnings in the third quarter, posting net income of $275 million, nearly double the amount of its second quarter results. Bray, at the time of the earnings and Marshall’s retirement announcement in October, credited Marshall for implementing “bank-like” efficiencies to the company during the pandemic.

Kurt Johnson, Mr. Cooper’s executive vice president and chief financial officer, then anticipated gains in owned servicing moving forward. As part of the firm’s busy 2023, it closed in August on the acquisition of the servicing business of Home Point Capital. That transaction added $83 billion in MSRs to bring Mr. Cooper’s servicing portfolio closer to $1 trillion.

Do you need health insurance? Did you know that there are many part-time jobs with health insurance that you may be able to apply for? These types of part-time jobs are great because they not only help you to make more income but they also give you benefits like health insurance. Health benefits are usually…

Do you need health insurance?

Did you know that there are many part-time jobs with health insurance that you may be able to apply for?

These types of part-time jobs are great because they not only help you to make more income but they also give you benefits like health insurance.

Health benefits are usually associated with full-time employment, but a growing number of companies give these perks to part-time employees as well. Companies know that in order to keep good employees, giving helpful benefits like health insurance helps them with this.

You may need a part-time job with health insurance for many different reasons, such as perhaps your full-time job doesn’t come with good health insurance, or maybe you are only looking for part-time hours to make extra money.

My husband worked at UPS for many years, mainly for the health insurance. And, so did many other people who worked there. The health insurance at UPS is one of the best I’ve ever seen, and it’s available to part-time workers.

And, you may be able to find a part-time job that comes with medical insurance like this too!

Key Takeaways

UPS is known for having many valuable benefits for their part-time workers, such as health insurance.

Starbucks is another place where you can get health insurance, even working part-time. After putting in an average of 20 hours a week over three months, you can get medical, dental, and vision plans.

There are many other jobs that give you health insurance as well and even other great benefits like tuition reimbursement and parental leave.

Best Part-Time Jobs With Health Insurance

Below are the best part-time jobs with health insurance coverage.

1. UPS

If you’re looking for a part-time job with health insurance, UPS can be a great choice. At UPS, even part-time employees can get health benefits.

This is probably one of the most popular jobs ever when it comes to getting great health insurance. UPS is a very popular choice for those who are looking for health insurance.

Like I said earlier, my husband worked at UPS for years, mainly for the health insurance. And, so did many other people that we know, such as many of our personal friends, his brother, our friend’s parents, and so many more people that we personally know.

Many of the part-time jobs at UPS are for package sorters and UPS truck loaders.

Part-time UPS workers get the same healthcare benefits as full-time workers. They don’t have to pay premiums, and there is low or no co-insurance and co-pays.

Plus, part-time employees at UPS earn an average of $20 per hour after 30 days. As a part-time employee at UPS, you’re promised at least 3.5 hours of work each day you’re scheduled.

There are also other benefits you can qualify for, such as you can get a pension when you retire, help paying for college, and paid time off for vacations and holidays.

Recommended reading: 26 Best Weekly Pay Jobs To Make Money Quick

2. Starbucks

If you’re looking for part-time work and need health insurance, Starbucks might be the place for you.

Starbucks gives health, dental, and vision insurance to all part-time workers who put in at least 20 hours per week on average after working 240 hours.

Starbucks also has a generous benefits package, such as dental care, a 401(k), vacation time, college tuition reimbursement, and more.

Another nice employee benefit is Starbucks’ parental leave – workers at Starbucks who are eligible and welcoming a new child can take time off and receive pay replacement through parental leave. Additionally, Starbucks gives Family Expansion Reimbursement, giving up to $10,000 for adoption, surrogacy, or intrauterine insemination for eligible partners.

3. REI

REI has a new medical plan called the REI Access Plan, which gives medical coverage to every employee who works at REI, even part-time employees.

The REI Access Plan gives medical coverage to employees after working for only three months, no matter how many hours they work (so, if you only work one day a week, you can qualify!). This plan is in addition to the existing health care options for employees who work an average of 20 or more hours per week over a 12-month period.

The health insurance coverage includes checkups for free with in-network doctors, mental health support, hospital care, and physical therapy. It also covers pharmacy costs and provides access to virtual healthcare through Teladoc.

4. National Guard

As a National Guard member, you get to serve your country and community, and you also have access to job benefits like health insurance.

You and your family can get low-cost health insurance through a plan called Tricare Reserve Select (TRS).

In 2023, the individual monthly health insurance plan cost $48.47, and family plans cost $239.69.

You’re also eligible for low-cost life insurance that pays up to $400,000.

National Guard members respond to emergencies (such as natural disasters), serve as law enforcement, and more. Guard members have about two days of drills each month and spend two weeks on annual training every year.

5. Costco

If you’re interested in a part-time job that includes health insurance, you might want to look into working at Costco.

There are many different kinds of jobs that you can find at Costco, such as cashier, baker, forklift driver, gas station attendant, member service assistant, stocker, and so much more.

Costco gives health insurance to part-time employees who work 23 or more hours each week.

Their health insurance comes with low out-of-pocket monthly premiums and co-pays. They provide medical, dental, and vision benefits that can be used for yourself and/or your family.

I know a few people who left their day job to work at Costco due to the good pay, nice benefits, and fun work environment. So, it can be a great one to look into!

Recommended reading: 20+ Best Jobs That Pay $20 An Hour Or More

6. Chipotle

At Chipotle, you can work part-time and still get health insurance. They understand that you might be studying, have another job, or need extra time for yourself. That’s why they offer flexible schedules.

If you join their team, even part-timers can sign up for health insurance. All Chipotle crew members are eligible for the Anthem Preventive Plus, Delta Dental PPO plan, and EyeMed PPO vision plan.

They also have 100% tuition coverage for select programs. You can learn about agriculture, technology, and business. If you’re into something else, they give up to $5,250 for other study areas.

Other helpful benefits from Chipotle include paid time off, 401(k) retirement savings plans, free meals, an annual bonus, a gym membership discount, and more.

7. Walmart

At Walmart, you can find part-time jobs that come with health insurance.

Part-time jobs with health insurance at Walmart include stocking shelves, unloading trucks, customer service, cashier, and more.

If you’re working at least 30 hours per week over a 60-day period, you can become eligible for coverage.

Once you meet the hours requirement, you can choose from different health plans. These plans are not just any plans; they include options for medical, dental, and vision coverage.

8. JPMorgan Chase

JPMorgan Chase gives health insurance to part-time employees, such as for entry-level jobs like being a bank teller or in customer service.

For example, as a part-time associate banker, you’ll be helping customers with their banking needs. You will be talking to them about their accounts and showing them how to use the bank’s products and services.

To get health insurance at JPMorgan Chase, you need to work at least 20 hours a week, and their benefits include medical, vision, and dental coverage.

9. Delta Airlines

If you’re looking for part-time work and need health insurance, you might want to find a job at Delta Airlines.

There are many different jobs at Delta Airlines that could fit your needs, even if you work part-time. These can include becoming a ticket agent, gate agent, customer service, and more.

They have multiple health plans that you may be interested in, plus dental and vision plans.

Delta also gives paid long-term disability coverage, optional short-term disability insurance, and company-paid basic life insurance.

10. Amazon

If you’re looking for a part-time job with health insurance, you may want to look for a job at Amazon.

Amazon is one of the largest companies in the world, so it makes sense that they would give good health insurance.

Amazon’s medical plans cover things like prescription drugs, emergency and hospital care, mental health, X-rays, and lab work.

There are no exclusions for pre-existing conditions in any of Amazon’s medical plans. They have many different plans, so it means that you can pick the one that fits you and your family the best. Plus, all plans cover 100% of preventive care.

The benefits available to you can vary based on how many hours you work each week and where you live. For example, if you are full-time or work 40 hours a week, you get one set of benefits. If you work between 30-39 hours or 20-29 hours, your benefits may be different. And if you’re in certain states, these standard benefits might not apply.

11. Lowes

At Lowe’s, you can find many jobs that could fit your schedule, and they offer both part-time and full-time positions.

Lowe’s gives affordable health insurance plans to both part-time and full-time workers. These plans cover medical, dental, and vision, and you can get low-cost prescription drugs after 30 days.

If you head to the Lowe’s worker’s benefits website here, you can actually see a preview of your different benefit options. I thought this was really handy. I clicked on “Prospective Lowe’s Associate” which then showed me their medical plan pricing. I typed in my zip code, and it showed me that there was one available medical plan in my area for a part-time Lowe’s Associate.

This plan started at $38.60 for Employee Only. For Employee + Children, the plan then costs $106.18. For Employee + Family, the cost is $152.52 each month. This medical plan includes an annual deductible of $0 and an out-of-pocket maximum of $9,100 for an individual plan or $18,200 for a family plan.

This platform also showed me pricing for their dental coverage, which is through Delta Dental. The pricing for this started at $9.60 per month for an Employee Only plan.

Other employee benefits from Lowe’s include off-the-job accident insurance, identity protection insurance, life insurance of $20,000, short-term disability insurance, 401(k), and an Employee Stock Purchase Plan (ESPP).

12. Ikea

If you’re considering a part-time job, Ikea is a place you might think about. Ikea gives health benefits to its part-time workers, and you get benefits if you work at least 20 hours a week.

IKEA’s health insurance is from Anthem, and many find the premiums reasonable. Besides health coverage, IKEA also offers dental, vision, and prescription coverage. Additionally, employees enjoy benefits like paid time off, parental leave, pet insurance, and income protection.

Some examples of part-time jobs with health insurance at Ikea include retail sales associate, customer service representative, forklift operator, and food service team member.

13. Whole Foods Market

If you’re looking for a part-time job that offers health insurance, Whole Foods Market might be a place to consider. To get health insurance at Whole Foods, part-time employees need to work at least 30 hours per week.

Examples of part-time jobs at Whole Foods include sales associate, customer service representative, cashier, and more.

14. Trader Joe’s

Trader Joe’s is a popular place to work, especially if you want a part-time job with health insurance.

Trader Joe’s has medical, dental, and vision plans for eligible crew members, and the company covers a big part of the cost, which starts as low as $25 per month.

They also have competitive pay, a retirement plan, up to a 20% store discount, paid time off, and more.

14. Staples

If you work part-time at Staples, you can get helpful health benefits. Staples provides medical, dental, and vision plans for both full-time and part-time employees.

You become eligible for these benefits if you work at least 15 hours a week.

All part-time associates are also eligible for other employee benefits like dental, vision, life, dependent life, accidental death, and short-term disability insurance coverage.

Some examples of part-time jobs at Staples include retail sales associate, cashier, stocker, and more.

15. Home Depot

Home Depot has a generous benefits package for its employees, which includes medical coverage, dental insurance, vision coverage, short-term disability, and more.

Part-time employees can qualify for benefits if they work an average of 16 hours per week or more during a 90-day period.

Some examples of part-time jobs at Home Depot include cashier, sales associate, customer service representative, stocker, and more.

Frequently Asked Questions About Part Time Jobs With Health Insurance

Below are answers to common questions about part-time jobs with health insurance.

Which jobs have the best health insurance? What companies have the best healthcare benefits?

Jobs at larger companies like UPS and Starbucks usually have better health insurance, even for part-time employees. They have good health insurance because they want to keep and attract good employees who will stay for a long time.

Remember to check if you need to maintain a certain number of working hours to keep your health insurance active as the requirements can change. Each company is different too, so make sure to look at the details for each job.

What companies give medical insurance to part-timers?

Companies such as UPS, Staples, and Chipotle are known for giving health insurance to part-time workers. Each company has its own criteria for eligibility, so you’ll need to check if you meet their requirements.

How can I find nearby jobs that give health benefits quickly?

You can start by seeing if any of the companies mentioned above have job openings near you.

Does Starbucks give health insurance to part time employees?

Yes, Starbucks gives part-time employees the option to enroll in health insurance plans, including medical, dental, and vision coverage, as long as they meet certain eligibility criteria (such as a minimum amount of hours worked each week).

Is health insurance through work worth it?

Yes, getting health insurance through your job can be a way to save money as well as get access to health insurance. My husband did this for years, and he had great health insurance that was extremely cheap.

Part-Time Jobs With Health Insurance – Summary

I hope you enjoyed this article about how to find part-time jobs with health insurance for medical care.

Health insurance isn’t only for full-time employees.

Yes, there are jobs that will give you medical insurance for working just part-time shifts!

Finding the right part-time job with health insurance and a nice benefits package is very possible across many different industries. Companies like UPS, Starbucks, and Costco are known for giving health and medical insurance to part-time workers.

This can be a game changer for you if you are balancing multiple jobs, attending school, or have family obligations that don’t allow for a full-time position.

What other part-time jobs come with health insurance? Leave a comment below and let me know!

JPMorgan Chase said today that fourth-quarter profit fell 34 percent largely due to subprime exposure and higher delinquencies tied to home equity loans.

Fourth-quarter earnings fell to $2.97 billion, or 86 cents a share, compared to $4.53 billion, or $1.26 a share, in the same period a year ago.

Despite falling short of the analyst-anticipated 93 cents a share, revenue climbed to $17.38 billion from $16.19 billion the year prior, beating analyst expectations of $17.05 billion.

For the entire year, net income rose to a record $15.4 billion, or $4.38 a share, on record revenue of $71.4 billion.

JPMorgan upped its provisions for loan losses by $2.54 billion during the quarter, and wrote down $1.3 billion on subprime positions, including subprime CDO’s.

The company saw an increase of $395 million for losses tied to home equity loans and an $124 million increase for subprime mortgage loan losses.

Home equity net charge-offs were $248 million (1.05% net charge-off rate), compared to $51 million (0.24% net charge-off rate) a year ago.

Subprime mortgage net charge-offs were $71 million (2.08% net charge-off rate), compared to $17 million (0.65% net charge-off rate) a year ago.

Total mortgage loan originations were $40 billion in the fourth quarter, up two percent from the third quarter and 34 percent from the prior year, while total third-party mortgage loans serviced increased 17% from the prior year to $614.7 billion.

In regard to a possible acquisition, Dimon seemed to hint that a purchase could be on the horizon.

“I think in terms of either buying assets or buying companies, we’re very open minded and we figure we can do the right kind of due diligence and understand the values and that we’re giving the value that we’re getting, we would be very happy to do it,” Dimon said during the conference call. “This environment doesn’t change that at all. It just may make it more likely.”

Shares of Chase rose $2.88, or 7.35%, to $42.05 in afternoon trading on Wall Street.

Editor’s note: In June 2014, the Consumer Financial Protection Bureau (CFPB) took enforcement action against Truist for unlawful and deceptive practices. Truist was ordered to pay at least $500 million to underwater borrowers, provide $40 million to victims of foreclosure, pay a penalty to the Department of Justice and establish homeowner protections to prevent further violations. Because of this, we can’t currently recommend Truist as a lender.

Truist offers several options for mortgage purchase and refinance loans, including doctor loans for qualified physicians and dentists. If you’re thinking about applying for a mortgage from Truist, here’s what you should know first.

Truist

Blueprint Rating

Truist overview

Truist has roots that date back to 1872, when the Branch Banking and Trust Company (BB&T) was founded. In 2019, BB&T merged with SunTrust Banks to form the Truist Financial Corporation.

Unfortunately, in its short time as Truist, the company has garnered thousands of poor reviews from customers. The company is accredited with the Better Business Bureau (BBB) and has an A+ BBB rating. However, as of Dec. 12, 2023, the company has a BBB star rating of just 1.09 out of 5.0, based on over 2,300 customer reviews. Customers complained about having trouble contacting customer service and others complained about fraudulent activities within their account. Truist seems to send an automated reply to these reviews, telling them to contact the company directly.

As of Dec. 12, 2023, Truist has also earned a star rating of 1.2 out of 5.0 stars on Trustpilot, based on 1,300 reviews.

How to qualify for a Truist mortgage

Truist offers a variety of mortgage loans, each with its own requirements. Here’s how to put yourself in the best standing to qualify for a Truist mortgage.

How to apply for a Truist mortgage

Compare lenders and get pre-qualified. Before you apply, be sure to compare as many mortgage lenders as possible, including Truist, to find the right loan for your needs. Consider interest rates, repayment terms, eligibility requirements and other factors as you weigh your choices. Truist as well as many other lenders allow you to pre-qualify with only a soft credit check that won’t affect your credit score — this will give you an idea of how much you can borrow and help you set a budget.

Pick a lender and apply. If you choose to go forward with Truist, you can start the formal application process online, by phone or in person at a local Truist branch. Speak with a loan officer to complete the application and determine the right type of mortgage for you. Be prepared to provide required documents, such as proof of income, assets, identification and previous tax statements. Work with the bank to answer any questions and document requests in a timely manner to avoid delays.

Close on the loan. The loan approval process with Truist typically takes about 30 to 60 days. If you’re approved, your loan will be scheduled to close. On closing day, you’ll sign paperwork and pay the closing costs, after which you’ll get the key to your new home.

Pros of a Truist mortgage

Offers doctor loans to medical and dental professionals.

Offers construction-to-permanent loans.

Can apply online, over the phone or in person in some areas.

Cons of a Truist mortgage

Doesn’t offer mortgages backed by the U.S. Department of Agriculture (USDA).

Poor customer service reviews.

Only available in 15 states and Washington, D.C.

Truist perks and special features

Savings and discounts

Like many other lenders, Truist offers you the option to buy mortgage points. These will permanently lower the interest rate on your loan for an upfront fee. If you intend to stay in the home for the length of the loan, mortgage points can save you thousands of dollars on interest payments.

Offers doctor loans

If you’re a medical doctor or dentist, a doctor loan could be a good option. These loans aren’t offered by many lenders. But with Truist’s doctor loan, qualified physicians and dentists can get a more favorable interest rate and make a lower or no down payment, even if they have student loans.

Offers construction-to-permanent loans

Another loan type that Truist offers that a lot of other mortgage lenders don’t is a construction-to-permanent loan. If you’re building a home, you can get one loan that funds the construction. Once the construction is complete, this loan will roll over into a traditional mortgage.

With Truist’s construction-to-permanent loan, you’ll make interest-only payments during construction and have only one set of closing costs for the land, construction and mortgage. Plus, there are no penalties for prepayment, so you don’t have to worry about being charged if you pay the mortgage off early.

Multiple ways to apply

Truist offers you the ability to apply over the phone, online or in person. With so many people turning to online mortgage applications, the fact that Truist offers physical locations can be an asset if you prefer to apply for a mortgage in person. Buying a home is a big decision and having someone to talk to face-to-face can be helpful.

How Truist could improve

Offer USDA loans

For much of rural America, a USDA loan increases their ability to own a home. These government-backed loans are for low-income families buying a home in specific rural areas. Truist, however, doesn’t offer these loans, which limits options for those who don’t live in cities. If Truist wants to improve its offerings, one way could be to provide a USDA loan option.

Improve customer service

Just browsing sites like BBB and Trustpilot can leave you with the impression that Truist isn’t well-regarded. There are a lot of negative reviews, complaining about a variety of things. These include the bank’s slowness in responding to deposits, improper handling of accounts and multiple accounts being hacked. Customers complain that they often are required to visit branches in person to resolve these issues, which is a problem when there are limited hours.

Expand availability

Truist is only available in 15 states and Washington, D.C. Its locations are mostly in the South and eastern parts of the country. Truist’s mortgages could reach more people if it expanded its availability to additional areas.

While Truist’s roots lie in operating as a traditional brick-and-mortar bank, it could make its mortgages available to a wider part of the country while maintaining its current in-person branches.

Truist customer service and reviews

There are multiple ways to contact Truist. You can visit a branch in person, connect on social media or call. You can talk to someone Monday through Friday, 8 a.m. to 8 p.m. Eastern Time (ET) and 8 a.m. to 5 p.m. ET on Saturdays. After hours, there’s 24-hour automated assistance.

The company also offers a mobile app, which lets you view your accounts, make payments and more. The app has a rating of 4.7 out of 5.0 stars on both the App Store and the Google Play store as of Dec. 12, 2023. However, many recent reviews note that the app has suffered since the merger to form Truist, with customers citing that recent versions are slow and unstable.

Customer reviews

Truist has received many negative reviews from customers on sites like BBB and Trustpilot. Some trends among these reviews state that the company is difficult to contact, accounts are often locked and promotions the company runs are misleading.

As of Dec. 12, 2023, these reviews have resulted in a BBB customer rating of 1.09 out of 5.0 stars and a Trustpilot rating of 1.2 out of 5.0 stars.

CFPB action

In 2014, SunTrust (a predecessor of Truist), was required by the CFPB to pay customers $540 million due to wrongfully servicing their loans. The company was also required to pay a penalty of $418 million to the Department of Justice. These institutions found that SunTrust was illegally foreclosing on homes by denying loan modifications, deceiving homeowners and charging unauthorized fees.

Truist alternatives: Truist vs. Bank of America vs. Chase

It’s important to consider a wide variety of mortgage lenders before applying for a loan. Two competitors to consider in addition to Truist include Bank of America and Chase.

Bank of America is a multinational financial company with ties back to 1784, when its predecessor, the Massachusetts Bank, was founded. As of 2021, it holds over $3.17 trillion in total assets and operates worldwide.

Chase Bank is a subsidiary of the holding company JPMorgan Chase & Co. Its history dates back to 1799 when its predecessor was founded as The Manhattan Company. As of 2021, JPMorgan Chase & Co. held over $3.7 trillion in total assets, making it the largest financial institution in the country.

While Truist is a big bank with a lot of history, both Bank of America and Chase are much larger than Truist. Mortgages are small parts of their businesses. With either of these banks, you might have more financing options. However, with a place like Truist, you could have a more personalized experience. While Truist is only available in 15 states and Washington D.C., that can be a positive as chances are higher that a Truist loan officer would be more familiar with state laws and assistance programs.

Frequently asked questions (FAQs)

The exact credit score you’ll need to get a Truist mortgage depends on the type of loan you choose. You must have a minimum credit score of 620 to qualify for FHA, VA and conventional mortgages. For jumbo loans, you’ll need a score of at least 680.

Truist mortgages are available in 15 states plus Washington, D.C. These states include:

Alabama

Florida

Georgia

Indiana

Kentucky

Maryland

New Jersey

North Carolina

Ohio

Pennsylvania

South Carolina

Tennessee

Texas

Virginia

West Virginia

Single-family homes, condominiums and some multi-unit properties are all eligible properties for personal mortgages. Truist also offers loans for real estate investors.

Truist is one of the 10 largest banks in the U.S. You don’t get that without repeat customers. Still, the recent merger of BB&T and SunTrust has caused hiccups with client accounts. Also, in 2014, SunTrust the CFPB required SunTrust to pay customers $540 million in relief due to wrongfully servicing their loans.

As interest rates increased rapidly throughout 2022, the number of refinance mortgage originations declined. The composition of these refinances also changed. Cash-out refinances – where a homeowner borrows an amount substantially greater than what they owe on their existing mortgage – became more common than non-cash-out (also known as “rate-and-term”) refinances. An equity “cashed out” from the home – which, in turn, increases the mortgage balance – is often used by the borrower to pay down other debts, fund home repairs, and pay for educational expenses, among other big-ticket purchases. A cash-out refinance takes the place of the original mortgage, but alternative products that tap home equity, such as home equity loans and home equity lines of credit, leave the original first-lien mortgage intact. Such needs for cash may be necessary and unavoidable, hence the persistence of some (albeit reduced) amount of cash-out refinances even in the face of rising interest rates.

Despite the recent decrease in volume, cash-out refinance originations are a segment of the mortgage market worth monitoring, especially since they were considered one of the mechanisms that exacerbated the 2008 financial crisis.1 In the case of both cash-out and non-cash-out refinances, the borrower’s home is used as collateral for the loan. Failing to make payments or meet other loan conditions can result in the borrower losing their home through foreclosure. The added risk for borrowers originating a cash-out refinance, especially in today’s interest-rate environment, is that their mortgage payments and mortgage loan terms are both likely to increase.

Who are the homeowners taking out cash-out refinances, and are their loans comparable to non-cash-out refinance loans? Are cash-out refinance borrowers more likely to become delinquent? In this post, we look at the loan and borrower characteristics of homeowners who originated a cash-out refinance compared to a non-cash-out refinance. We study refinances originated between 2013 and 2023. This allows us to study delinquencies—one manifestation of risk—throughout the post-crisis period, and how they vary among the population. This period includes periods of falling and rising interest rates, as we have observed recently. With this information, we can better gauge the risk to consumers and the housing market of the recent trends in refinances. We find that:

Cash-out refinances were a larger share of all refinances during periods of rising interest rates.

Borrowers of cash-out refinances had lower credit scores, lower incomes, and smaller loan amounts compared to non-cash-out refinance borrowers.

Loan-to-value and debt-to-income ratios were similar for cash-out and non-cash-out refinances.

Cash-out refinances had larger shares of older, female, Black, and Hispanic borrowers, compared to non-cash-out refinances.

Serious delinquencies were rare for borrowers with higher credit scores, regardless of whether the refinance was cash-out or not.

For borrowers with lower credit scores, both cash-out and non-cash-out refinance borrowers have similar two-year delinquency rates, except for a relative increase in delinquencies among cash-out refinance borrowers in 2017—a year marked by rising interest rates.

We conclude with a comparison of the market for cash-out refinances before the financial crisis to the post-crisis time period, as well as potential concerns with cash-out refinances to monitor going forward.

Loan and borrower characteristics of refinances

We used refinance data in the National Mortgage Database to compare the loan characteristics and two-year delinquency status of cash-out refinances and non-cash-out refinances. The National Mortgage Database is a representative 1-in-20 sample of all closed-end first-lien mortgages in the United States. We identify refinances as cash-out refinance mortgages when the total value of sampled refinance loans and their associated junior liens were more than five percent larger than the total value of the preceding loans and associated junior liens.

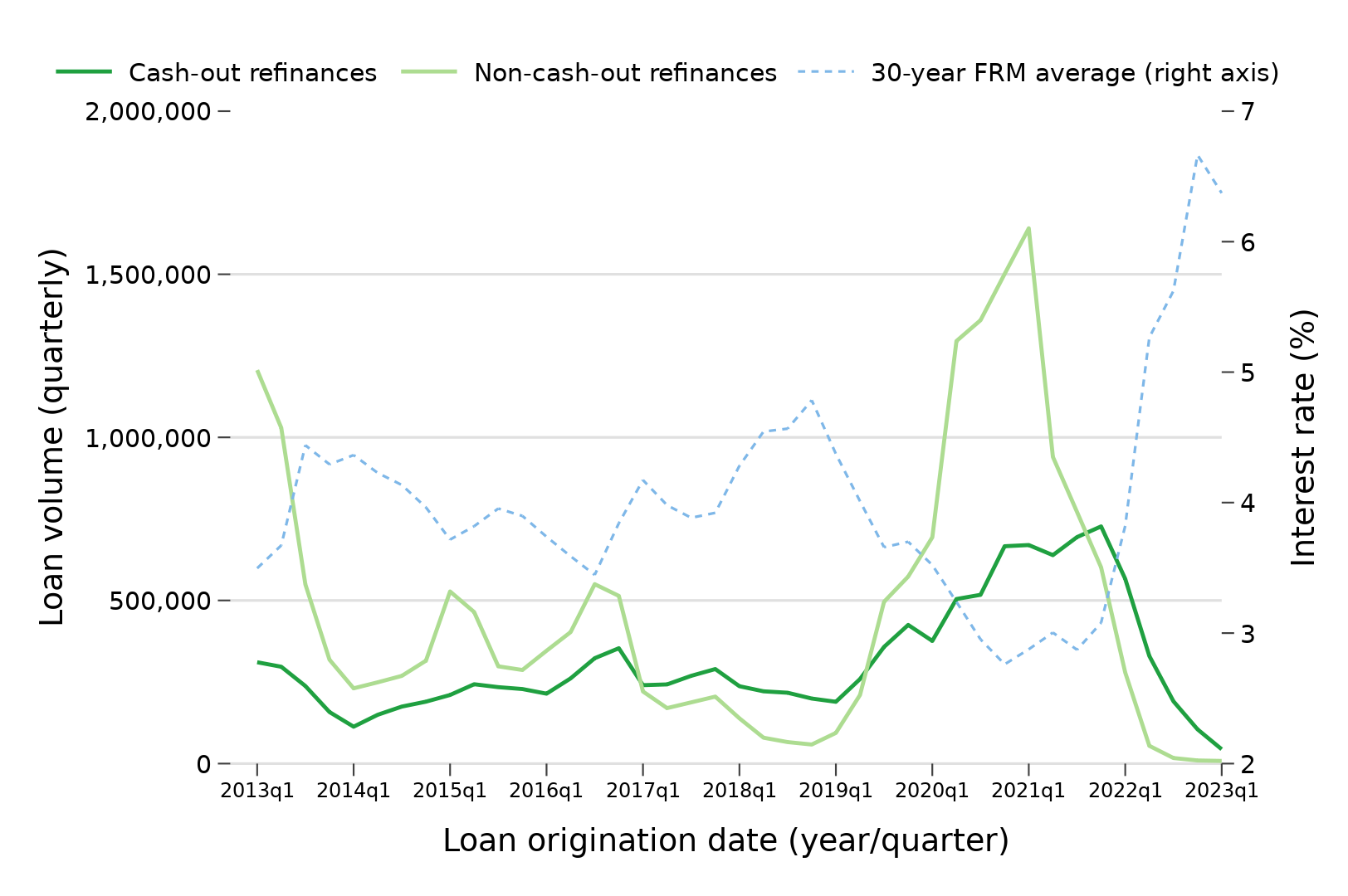

Figure 1 shows the quarterly volume of refinances, cash-out and non-cash-out, from the first quarter of 2013 through the first quarter of 2023 (the latest quarter for which we have data). We added the average interest rate on 30-year fixed-rate mortgages from Freddie Mac’s Primary Mortgage Market Survey on the right axis.

As Figure 1 indicates, non-cash-out refinances are typically more common when interest rates are decreasing and borrowers seek better rates compared to their original mortgages. Cash-out refinances make up a larger proportion of all refinances during periods when interest rates are increasing, such as 2017 to 2019 and 2022 to 2023. For example, from 2013 to 2019, cash-out refinances averaged about 240,000 originations per quarter, followed by an increase to almost 730,000 in the fourth quarter of 2021. Cash-out refinance volumes then fell throughout 2022, down to 44,000 originations in the first quarter of 2023.

Figure 1: Quarterly volume of cash-out versus non-cash-out refinances, 2013-2023

Source: National Mortgage Database

Figure 2 plots median credit scores by refinance type. The median credit scores of cash-out refinance borrowers were lower than non-cash-out refinance borrowers throughout the 2013-2023 period.

Figure 2: Median credit score at origination of cash-out versus non-cash-out refinances, 2013-2023

Source: National Mortgage Database

Figure 3 plots median combined loan-to-value ratios (100 percent less borrower equity in the house) by refinance type. The median combined loan-to-value ratios for cash-out refinances are generally similar to or lower than non-cash-out refinances originated in the same period, except during high interest-rate periods from 2017 to 2019 and 2022 to 2023, when median combined loan-to-value ratios for cash-out refinances are relatively higher than non-cash-out refinances.

Figure 3: Median combined loan-to-value ratio at origination of cash-out versus non-cash-out refinances, 2013-2023

Source: National Mortgage Database

Table 1 describes other loan and borrower characteristics of cash-out and non-cash-out refinances originated between 2013 and 2023. We see that the median loan amount and borrower incomes for cash-out refinances were smaller than for non-cash-out refinances; the primary borrowers for cash-out refinances were older; and cash-out refinances were more likely to only have female borrowers and borrowers aged 62 and older. Cash-out refinance borrowers were also more likely to be Hispanic or Black and less likely to be Asian, compared to non-cash-out refinance borrowers.

Table 1: Loan and borrower characteristics by cash-out versus non-cash-out refinances

Loan/borrower characteristics

Cash-out refinances

Non-cash-out refinances

Loan amount (median)

$198,000

$241,700

Cash-out amount (median)

$37,131

N/A

Interest rate (median)

3.62%

3.38%

Combined loan-to-value ratio (median)

70

72

Debt-to-income ratio (median)

36

34

Borrower income (median)

$84,000

$102,000

Credit score (median)

741

765

Age of primary borrower (median)

51

47

Share of refinances with only female borrowers (%)

22.8

18.8

Share of refinances with only age 62 and older borrowers (%)

21.1

15.0

Share of refinances with any Hispanic borrower (%)

10.5

9.6

Share of refinances with any Black borrower (%)

9.1

7.5

Share of refinances with any Asian borrower (%)

4.7

9.8

Share of refinances with any American Indian borrower (%)

0.7

0.5

Share of refinances with any Native Hawaiian/Pacific Islander borrower (%)

0.7

0.8

Share of refinances with any borrower listing two or more races (%)

1.9

1.7

Observations (N)

641,657

957,748

Note: Sample includes refinance mortgages that were opened between the first quarter of 2013 and the first quarter of 2023. A cash-out refinance is identified when the total value of the sampled refinance loan and their associated junior liens was more than five percent larger than its preceding loan and associated junior liens. “Only female (or only age 62 and older) borrowers” means that for loans with only one borrower, that borrower is female (or age 62 and older), and for loans with multiple co-borrowers, that all co-borrowers are female (or age 62 and older). Source: National Mortgage Database.

Delinquencies of refinanced mortgages: the importance of borrowers’ credit scores

In terms of delinquencies at the two-year mark after their refinance loan origination, Figure 4 shows two-year delinquency rates of refinances, by year originated, from 2013 to 2020. We use a broad measure of delinquency: 60 or more days past due, including other adverse conditions such as bankruptcy and foreclosure. We also split the sample by credit score: refinances with a borrower credit score at or below the median credit score of 756 at origination (left panel) compared to refinances with a borrower credit score above the median (right panel).

Figure 4: Rates of serious delinquency (60+ days or worse) two years after origination for cash-out versus non-cash-out refinance borrowers

Source: National Mortgage Database.

We first see that serious delinquencies two years after origination are rare among both types of refinances involving borrowers with higher credit scores: no higher than 0.1 percent for originations between 2013 and 2020. By contrast, serious delinquencies are more likely among refinances involving borrowers with lower credit scores but are still uncommon in absolute terms: ranging between 0.7 and 0.8 percent for all refinances originated between 2013 and 2016, followed by an increase in 2017 to 1 percent for cash-out refinances and 0.9 percent for non-cash out refinances.2 Two-year delinquency rates then fall among all refinances with lower credit scores originated after 2018, likely due to mortgage forbearance programs in the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

Worth noting is the increase in two-year delinquency rates for cash-out refinances originated in 2017. We know that these borrowers refinanced at a time when interest rates were rising (see Figure 1), and that credit scores were lower overall for cash-out borrowers in 2017 compared to previous years (see Figure 2). These findings from 2017 suggest that we may see increased delinquencies among cash-out refinance mortgages originated in 2022, another period with an increase in interest rates and a decrease in cash-out borrowers’ credit scores.

Discussion and potential concerns with cash-out refinances

In summary, during periods of rising interest rates, refinance volume declines and their composition shifts toward cash-out refinances, since homeowners may need cash from their home even when interest rates increase. From the first quarter of 2013 to the first quarter of 2023, cash-out refinances tended to have smaller loan amounts, lower borrower incomes, and lower borrower credit scores compared to non-cash-out refinances, but other loan characteristics, such as loan-to-value and debt-to-income ratios, were similar. We then showed that two-year delinquency rates were similar between both types of refinances, with only a noticeable increase for lower credit-score borrowers taking out cash-out refinances in 2017.

Prior research has focused on cash-out refinances as one of the mechanisms that exacerbated the 2008 financial crisis. However, mortgage originations from 2013 to 2023 are fundamentally different from mortgage underwriting before the financial crisis. Many risky features are now absent from the market – for example, interest-only mortgages, negative amortization mortgages, and mortgages with loan-to-value ratios over 100 percent – and lenders are now required to document borrowers’ ability to repay their loans. As we have shown above, most cash-out refinances now have loan-to-value ratios below 80 percent, requiring a 20 percent or more drop in house prices to be underwater. Most cash-out amounts are also below $50,000 during this period, and the volume of cash-out refinances has been declining each quarter since the start of 2022. Although cash-out refinances gained popularity from 2019 to 2021 due to record-low interest rates , the amount of equity extracted was lower than during the pre-2008 boom, despite home prices having increased substantially. These characteristics of cash-out refinances over the past decade suggest that cash-out refinances are now a smaller source of systemic risk than before the 2008 financial crisis.

Beyond the potential systemic risk of equity extraction contributing to a new financial crisis, cash-out refinances present at least two other concerns for borrowers. First, research from the JPMorgan Chase Institute showed that a typical cash-out refinance in their data had a longer loan term and larger monthly payment compared to the paid-off mortgage. This suggests that cash-out borrowers are more likely to still be paying off their mortgage and less likely to own their home free and clear in retirement, potentially exposing these borrowers to more future financial shocks while the mortgage is outstanding. Second, a cash-out refinance with a higher interest rate than the prior paid-off mortgage could effectively lead to much higher borrowing costs, relative to the original mortgage or to other sources of credit, like home equity loans or home equity lines of credit, that do not raise the interest rate on the existing first-lien loan balance.3 Prior research has shown that higher interest rates can cause delinquency and default.4 This relationship highlights the importance for borrowers of finding and obtaining lower interest-rate loans, and aligns with efforts to help borrowers refinance when interest rates fall as a way to avoid delinquencies.

As the interest-rate environment continues to evolve, the CFPB’s Office of Research will continue analyzing mortgage refinances and other home equity loan products to understand consumers’ borrowing decisions and loan performance.

A new mortgage help plan coined “Project Lifeline” was unveiled today by the Treasury Department and the Department of Housing and Urban Development.

The plan will assist borrowers who are 90 days or more past due on their mortgage, and will not be limited to high-cost subprime mortgage holders like previous plans targeted.

Borrowers with prime loans, Alt-A mortgages, fixed-rate loans, and second mortgages will also be eligible for assistance under the new plan.

Project Lifeline will allow seriously delinquent homeowners to delay foreclosure proceedings for 30 days while lenders attempt to work out new terms to avoid one.

“For many families, Project Lifeline will temporarily pause the foreclosure process long enough to find a way out. Loan modifications may follow. And, this program is not only available to subprime borrowers but to people with any kind of home mortgage,” said HUD Secretary Alphonso Jackson.

“There’ll be homeowners who still take no action and some will still walk away,” Treasury Secretary Henry Paulson said. “But some borrowers facing immediate foreclosures may find solutions.”

Letters will be sent out to homeowners more than 90 days behind on their mortgage, at which point the homeowner has 10 days to respond and provide additional financial information so the lender is able to determine new mortgage payment options.

It will initially involve major mortgage lenders like Bank of America, Citigroup, Countrywide, JPMorgan Chase, Washington Mutual and Wells Fargo, on a pilot basis.

The move comes as banks and lenders continue to take on huge losses related to the recent rise in foreclosure proceedings.

The plan is intended to supplement efforts already in place via programs like FHASecure and Hope Now, which offer some solutions to homeowners but leave many others with few places to turn.

“The sum total of these actions is a powerful correction to the downward spiral of the housing market. It will lead to a reversal of misfortune, saving homes and equity, providing necessary sanity and salvation for many families on the brink of foreclosure,” said Jackson.

It’s good to see that government officials are finally realizing that it’s not just a subprime crisis, but rather a complete overhaul that is needed.

Representative Maxine Waters, a Democrat from California, held a town hall meeting on Saturday at Inglewood High School where she pointedly asked executives from City National Bank, PNC Financial Services and Wells Fargo & Co., if they would each open a branch in her district. Photographer: David Paul Morris/Bloomberg

David Paul Morris/Bloomberg

LOS ANGELES – Rep. Maxine Waters held a town hall meeting on Saturday where she pointedly asked executives from City National Bank, PNC Financial Services and Wells Fargo & Co., if they would each open a branch in her district. She said she wanted to hold the banks accountable for promises made in recent merger agreements or consent orders.

The town hall meeting at Inglewood High School got fiery at times as Waters pressed the three bank executives to answer questions from constituents in her 43rd congressional district in South Los Angeles. Waters, the ranking member of the House Financial Services Committee, said she invited all the top banks to attend but was turned down by Bank of America, Citigroup, JPMorgan Chase and U.S. Bancorp.

Next week, the Senate Banking Committee plans to hold an annual oversight hearing with executives from the nation’s top banks. Waters said she was disappointed that Republicans in the House would not hold a similar hearing. Her town hall, she said, would try to fill in the gap.

When Jeffrey Martinez, executive vice president and head of branch banking at PNC Bank, described how the Pittsburgh bank was upholding its pledge to invest an eye-popping $88 billion in local communities over four years as part of its 2020 acquisition of BBVA, Waters asked specifically if PNC was coming to her neighborhood.

“When are you going to open up a branch in my district?” Waters said. “We have a problem with branch banking not being available to us in all of our communities in the way they should be. We call them banking deserts.”

Martinez responded: “That’s a great question, it’s an important one and one of the things we’ve slated even though we’re new to California.”

“We would like to help you find a location,” Waters said, to thunderous applause and laughter from the crowd of about 300. “I’m so looking forward to establishing” a branch here, she added.

Waters then described how City National Bank in Los Angeles had agreed in January to pay $31 million to settle redlining allegations brought by the Justice Department. As part of the agreement, City National has promised to open one branch in a majority-Black and Hispanic neighborhood in L.A. County.

“Can you discuss where you might be opening the branch?” Waters asked. “Where are you with all of this?”

David Cameron, City National’s executive vice president of personal and business banking responded, “That is a great question,” drawing laughter from the audience.

“I don’t have any announcement on where we’re going to put that branch.”

To which Waters replied: “Oh, we’ll help you,” to further applause from the audience.

City National plans “to go above and beyond,” the agreement to invest at least $29.5 million in a loan subsidy fund for residents of majority-Black and Hispanic neighborhoods in Los Angeles County, Cameron said. The bank has hired more than 20 loan officers to support the initiative to provide grants of up to $15,000 each to first-time homebuyers.

Waters also questioned why City National did not have a mortgage loan officer at a local branch on Crenshaw Boulevard in Los Angeles.

“You’ve done well at that branch, are you going to expand that branch and put a loan officer there?” Waters said. “Can you do these things?”

Waters skillfully thanked each of the bankers for showing up to the town hall meeting, while also hitting them hard on consent orders.

“I really thank you for coming today. I know that you know we have a lot of questions for you, based on the fines that you received and all of that,” she told Cameron, and then asked the audience to give him a round of applause.

She also asked Colleen Canny, Wells Fargo’s executive vice president and national head of branch banking, why the San Francisco bank has been closing so many branches, which Waters estimated at 2,000 branch closings over many years. She cited the Wells Fargo 2016 fake accounts scandal that led the Federal Reserve to impose an asset cap on the bank.

“First tell us, why did you close those branches?” Waters asked.

Canny said that customer transactions through branches have fallen 50% over the past three years as more banking is done online, through mobile apps or ATMs.

“We still think branches are important and we continue to look at our branch footprint to ensure we have the proper coverage,” Canny said.

Waters lamented that banks are closing branches in inner cities where seniors who may not necessarily use a cell phone to bank still prefer to go to a branch in person.

“I want to tell you something that is a cultural discovery for everybody,” Waters told the bankers and the audience. “We like to go to a teller as we put our money across the counter. We like this kind of interaction with the people that we do service with and this is the kind of cultural consideration that the bank should take into account.”

At the town hall, which lasted for four hours, constituents asked a wide range of questions including why there were long lines at their local branches and why they were not able to get small business loans or even speak directly to the same banker on each visit. CFPB Director Rohit Chopra, who spoke after the bankers, answered a range of questions on reverse mortgages, digital redlining and junk fees.

Waters also lambasted the banking industry generally for Republican-led efforts in the House, which voted on Friday to nullify the Consumer Financial Protection Bureau’s small-business data-collection rule. Despite the bill’s passage in a 221-202 vote, President Joe Biden has vowed to veto the bill and uphold the rule.

The head organizer for Rise Economy, the consumer group formerly known as the California Community Reinvestment Coalition, asked the bankers generally why they did not support the Consumer Financial Protection Bureau.

“Your industry trade groups are attacking the CFPB, they’re attacking fundamental consumer protections … and very basic data on small business lending that we fought hard for for nearly 10 years,” said Jyotswaroop Kaur Bawa, chief of organizing and campaigns at Rise Economy. “We want you to tell us specifically how many Black and Hispanic-owned businesses you make loans to and at what rate—that’s what the fight is about.”

The small-business lending rule is expected to be used by the CFPB to identify discrimination, though the bureau exempted more than 2,000 community banks and small businesses from the rule. The coalition sued the CFPB in 2019 for taking so long to issue the rule, which Dodd-Frank’s Section 1071 mandated.

The 1071 rule was about wealth-building and closing the wealth gap, Waters said.

“The Senate Republicans put up a great fight against getting the rule, the data that we needed to determine why we can’t get small business loans — they fought us very hard, and they said they represented the banks,” Waters said. “Republicans won on trying to kill that rule that would give us information that would show that Blacks, Latinos, women and LGBTQ would not be getting small business [loans.]”

Water did commend one bank: First Citizens BancShares, which acquired the failed Silicon Valley Bank and last month announced an agreement to invest more than $6.5 billion in California and Massachusetts communities through an updated community benefits plan. The agreement, Waters said, paved the way for a branch to be opened in Watts.

Waters characteristically played to the audience by rattling off the various programs created after the pandemic including loans that banks delivered via the Paycheck Protection Program.

“You’re wondering, if there’s all this money around, why haven’t we been able to get some of it,” Waters said.

In a stunning bit of news, JPMorgan Chase said today that it will acquire flagging investment bank Bear Stearns for just $2 per share, a sharp contrast to its $30 closing price on Friday and its 52-week high of $159.36.

The stock-for-stock transaction will exchange 0.05473 shares of Chase common stock per one share of Bear Stearns stock, valuing the multi-billion dollar world banking giant at just $236 million.

The move has already been approved unanimously by both companies’ Board of Directors and effective immediately, Chase will guarantee the trading obligations of Bear Stearns and provide management oversight.

“JPMorgan Chase stands behind Bear Stearns,” said Jamie Dimon, Chairman and Chief Executive Officer of JPMorgan Chase, in a statement. “Bear Stearns’ clients and counterparties should feel secure that JPMorgan is guaranteeing Bear Stearns’ counterparty risk. We welcome their clients, counterparties and employees to our firm, and we are glad to be their partner.”

“This transaction will provide good long-term value for JPMorgan Chase shareholders. This acquisition meets our key criteria: we are taking reasonable risk, we have built in an appropriate margin for error, it strengthens our business, and we have a clear ability to execute.”

The move is nothing short of a rescue, as Bear Stearns flirted with bankruptcy after biting off much more than it could chew in the mortgage securities market over the last year and change.

And the collapse of such an influential power on Wall Street would have sent shock waves through already spooked financial markets, wreaking havoc on world economies.

On Friday, Chase and the Federal Reverse Bank of New York agreed to provide emergency funding to Bear for an initial period of 28 days to address liquidity concerns, though that clearly wasn’t enough to save the 85-year old company.

Chase also noted in its statement that the Fed will provide special financing of up to $30 billion related to the transaction.

The deal, which was quickly approved by the Federal Reserve, the Office of the Comptroller of the Currency (OCC) and other federal agencies, is expected to close expeditiously in the second quarter.

At this time, it’s unclear what will happen to Bear Stearns’ existing mortgage platform, Bear Stearns Residential Mortgage Corporation.

In related news, the Fed lowered the federal funds rate to 3.25 percent from 3.50 percent and created another emergency lending facility for investment banks to secure short-term loans.

JPMorgan Chase announced this morning that it had revised the terms for a takeover of beleaguered investment bank and mortgage lender Bear Stearns, upping the bid to $10 a share from just $2 previously.

Bear Stearns common stock would now be exchanged for 0.21753 shares of JPMorgan Chase common stock (up from 0.05473 shares), based on Chase’s Thursday closing price.

Additionally, Chase and Bear have entered into a share purchase agreement in which Chase will buy 95 million newly issued shares of Bear Stearns, or 39.5 percent of the outstanding stock after the issuance, for the same price.

“We believe the amended terms are fair to all sides and reflect the value and risks of the Bear Stearns franchise,” said Jamie Dimon, Chairman and Chief Executive Officer of JPMorgan Chase, “and bring more certainty for our respective shareholders, clients, and the marketplace. We look forward to a prompt closing and being able to operate as one company.”

The purchase of the 95 million shares, which has been approved by both companies’ Board of Directors, is expected to be completed on or near April 8.

“Our Board of Directors believes that the amended terms provide both significantly greater value to our shareholders, many of whom are Bear Stearns employees, and enhanced coverage and certainty for our customers, counterparties, and lenders,” said Alan Schwartz, President and Chief Executive Officer of Bear Stearns.

“The substantial share issuance to JPMorgan Chase was a necessary condition to obtain the full set of amended terms, which in turn, were essential to maintaining Bear Stearns’ financial stability.”

The $30 billion in special financing coming from the Federal Reserve Bank of New York’s has also been amended so that Chase will realize the first $1 billion in losses associated with Bear Stearns assets being financed and the Fed will fund the remaining $29 billion.

Shares of Bear Stearns were up a whopping $6.83, or 114.59%, to $12.79 in midday trading on Wall Street, revealing that investors still value the company above the new offer.

The stock had been trading just under six dollars in a prior trading session, but still stands far below its value of roughly $80 per share less than a month ago.

Top-20 U.S. mortgage lender Bank of America (BofA) reported declining mortgage and home equity production in the third quarter of 2023, compared to the previous quarter. And more declines are yet to come if regulators’ proposed capital rules are applied to banks, according to BofA’s executives.

On July 27, the Federal Reserve, Federal Depository Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC) released the proposed changes for the Basel III rule (called the Basel endgame). It significantly increases capital requirements for banks.

“If we add to our capital, it will reduce our lending capacity to American businesses and consumers, and those trade-offs are being debated,” Brian Moynihan, chair and CEO of BofA, said in a call with analysts on Tuesday morning.

“But as far as the rules are concerned, there are many parts of the rules that our industry doesn’t agree with because of double counts or increased trading and market risk. And we’re talking to those proposals and working, and we’re hopeful they’ll change,” Moynihan added.

According to Moynihan, BofA holds the required capital today. “And, of course, we’d have to build a buffer to that throughout the implementation period.”

“Once we understand the final rules, we’ll, of course, have a chance to optimize our balance sheet and appropriately price assets to improve the return on tangible common equity.”

Regarding the mortgage space, Alastair Borthwick, BofA’s chief financial officer, said, “It is a little puzzling that you see some of the RWA [risk-weighted assets] increases for mortgage loans.”

“Now what would happen is we’d have to adjust the pricing, and it would become more expensive,” Borthwick said.

Mortgage, home equity volumes

BofA’s mortgage originations totaled $5.6 billion during the third quarter of 2023, a 5.8% decline from $5.9 billion posted in the second quarter and a 35.8% drop from the $8.7 billion originated in the third quarter of 2022.

BofA’s sequential production decline follows that of Wells Fargo, which also posted lower mortgage volumes during the third quarter. Meanwhile, JPMorgan Chase slowly improved its production in the period, showing a different path.

BofA also originated $2.42 billion in home equity loans in the third quarter, which was flat compared to last year but lower than the $2.54 billion volume in the previous quarter.

Bank of America had $229 billion in outstanding residential mortgages on its books through Sept. 30, up from $228.7 billion in Q2 2023 and $228.4 billion in the third quarter of 2022.

The home equity portfolio was $25.6 billion at the end of the third quarter, down from $25.9 billion from the previous quarter — and a decline from $27.3 billion a year prior.

Bank of America’s total mortgage-backed securities reached a $32.1 billion fair value as of Sept. 30, compared to $33 billion as of June 30, 2023.

Overall, the bank posted a net income of $7.8 billion from July to September, increasing 5.3% quarter over quarter and 10% year over year.

Deposits at Bank of America were $1.88 trillion in the third quarter of 2023, flat compared to the previous quarter. The consumer banking division posted a net income of $2.86 billion, up $11 billion compared to the prior quarter, according to its filing with the Securities and Exchange Commission (SEC).