A mortgage broker acts as an intermediary between you and potential lenders. The broker’s job is to compare mortgage lenders on your behalf and find interest rates that fit your needs. Mortgage brokers have lists of lenders they work with, which can make your life easier.

Mortgage brokers are licensed and regulated financial professionals. They gather documents from you, pull your credit history, and verify your income and employment, using the information to help you apply for loans and negotiate terms in a short time.

Once you settle on a loan and a lender that works best for you, your mortgage broker will collaborate with the lender’s underwriting department, the closing agent (usually the title company) and your real estate agent to keep the transaction running smoothly through closing day.

A mortgage broker can save you time and may offer you a wider array of options than if you shop on your own. But brokers don’t work for free, so you should expect to pay for their services at some point in the process.

1. What makes mortgage brokers different from loan officers?

Loan officers, as opposed to mortgage brokers, are employees of one lender who are paid set salaries, plus bonuses. Loan officers can write only the types of loans their employer chooses to offer.

Mortgage brokers, meanwhile, deal with many lenders to find loans for their clients. Mortgage brokers, who can work within a mortgage brokerage firm or independently, may be able to give borrowers access to a broad selection of loan types.

2. How does a mortgage broker get paid?

Mortgage brokers are most often paid by lenders, sometimes by borrowers, but, by law, never both. That law — the Dodd-Frank Act — also prohibits mortgage brokers from charging hidden fees or basing their compensation on a borrower’s interest rate.

You can also choose to pay the mortgage broker yourself. That’s called “borrower-paid compensation.” Though even when the fee is paid by the lender, often it is rolled into the loan itself, meaning the borrower eventually still pays the bill.

Shop around for mortgage brokers and ask how much to expect to pay in fees, which are typically 1% to 2% of the loan amount. The competitiveness — and home prices — in your market will have a hand in dictating what mortgage brokers charge. Federal law limits how high compensation can go.

3. Is a mortgage broker right for me?

You can save time by using a mortgage broker; it can take hours to apply for preapproval with different lenders, and then there’s the back-and-forth communication involved in underwriting the loan and ensuring the transaction stays on track.

However, that convenience comes at a cost, which is something to consider if you’re especially tight on funds. You also might sacrifice a sense of control and direct interaction with a lender when you turn the process over to a broker, a feeling that could be unnerving when making such a big purchase.

If you seek expert guidance and streamlined lender comparisons, and you are willing to pay a premium for these services, a mortgage broker may be right for you.

🤓Nerdy Tip

When choosing a lender, pay attention to lender fees. Specifically, ask what fees will appear on Page 2 of your Loan Estimate form in the Loan Costs section under “A: Origination Charges.” Then, take the Loan Estimate you receive from each lender, place them side by side and compare your interest rate and all of the fees and closing costs.

That head-to-head comparison among different options is the best way to make the right choice.

4. How do I choose a mortgage broker?

The best way to find a mortgage broker is to ask friends and relatives for referrals, but make sure they have actually used the broker.

Learn all you can about the broker’s services, communication style, level of knowledge and approach to clients.

Another referral source: Ask your real estate agent for the names of brokers that they have worked with and trust. Some real estate companies offer an in-house mortgage broker as part of their suite of services, but you’re not obligated to go with that company or individual.

Finding the right mortgage broker is just like choosing the best mortgage lender: It’s wise to interview at least three people to find out which services they offer, how much experience they have and how they can help simplify the process.

Check your state’s professional licensing authority to ensure they have mortgage broker’s licenses in good standing.

Also, read online reviews and check with the Better Business Bureau to assess whether the broker you’re considering has a sound reputation.

Frequently asked questions

What exactly does a mortgage broker do?

A mortgage broker finds lenders with loans, rates, and terms to fit your needs. They do a lot of the legwork during the mortgage application process, potentially saving you time.

How do mortgage brokers get paid?

Mortgage broker fees most often are paid by lenders, which may add to the total cost of a loan, though they sometimes can be paid directly by borrowers. Competition and home prices will influence how much mortgage brokers get paid.

What’s the difference between a mortgage broker and a loan officer?

Mortgage brokers will work with many lenders to find the best loan for your situation. Loan officers work for one lender.

How do I find a mortgage broker?

The best way to find a mortgage broker is through referrals from family, friends and your real estate agent. But don’t just take their word for it. Do your homework when selecting a mortgage broker by investigating their licenses, reading online reviews and checking with the Better Business Bureau.

Explore mortgages today and get started on your homeownership goals

Get personalized rates. Your lender matches are just a few questions away.

A day after targeting the title insurance industry, the Biden Administration has put the rest of the real estate finance process in its crosshairs.

On March 8, the Consumer Financial Protection Bureau posted a blog inviting consumers to tell it how “junk fees” in the closing process affect them.

While not able to speak to the specifics of the posting, nor about any possible actions the regulator might take, the Community Home Lenders of America “is thrilled that they’re jumping into this,” Scott Olson, its executive director, said in an interview.

“We’ve actually used this phrase [junk fees] ourselves a couple of years or so ago” he said in regards to click fees lenders are charged by third party vendors, which are passed on to consumers.

Others in the industry had a hard time understanding where the CFPB was coming from.

“The CFPB’s blog post is baffling and reveals little understanding of how the mortgage market works or awareness of its own regulations that provide for full fee transparency and limits on what can be charged,” Bob Broeksmit, president and CEO of the Mortgage Bankers Association, said in a lengthy statement.

“The fees mentioned are clearly disclosed to borrowers well before a home purchase on forms developed and prescribed by the Dodd-Frank Act and the CFPB itself,” he added, referring to the TILA-RESPA Integrated Disclosures, also known as TRID. One of those disclosures, the loan estimate, is given when the borrower contacts the originator and is supposed to be used to shop.

The other form – the closing disclosure presented at the end of the process – must be within certain tolerances of the data provided on the loan estimate.

“In 2020, the CFPB issued a report praising its own rule for improving consumers’ ability to locate key information, compare terms and costs between initial disclosures and final disclosures, and compare terms and costs across mortgage offers,” Broeksmit said.

But in Olson’s view, “transparency is not the same as competition.”

The CHLA has been supportive of the use of title insurance alternatives like attorney opinion letters, that could reduce costs to borrowers.

“We think that opening up the line of sight on some of these things is reasonable where there really is not competition,” Olson said.

CHLA plans to “comment vigorously” to the CFPB, he continued, adding that it has done so regarding competition and fees charges in the not-so-distant past, particularly in regards to the Intercontinental Exchange purchase of Black Knight.

As far back as 2003, if not even earlier, the government has had so-called mortgage junk fees in its crosshairs. Mel Martinez, Department of Housing and Urban Development secretary under President George W. Bush, said in a speech before the National Community Reinvestment Coalition almost exactly 11 years ago that members of Congress did not understand that reform proposal would help consumers understand the mortgage process and the costs involved so they don’t become “victims” of junk fees and broker abuse.

The CFPB, in its recent post, took its own shot at the lender policy portion of title insurance, saying the borrower has no control or options.

“Instead of paying this fee themselves, lenders make borrowers pay the cost,” said the blog posting authored by Julie Margetta Morgan, associate director. “The amount that borrowers pay for lender’s title insurance is often much greater than the risk.”

The CHLA has been supportive of the use of title insurance alternatives like attorney opinion letters, that could reduce costs to borrowers.

“We think that opening up the line of sight on some of these things is reasonable where there really is not competition,” Olson said.

The American Land Title Association issued commentary on the CFPB blog.

“Reform of mortgage closing costs is unnecessary,” the ALTA response said. “The contradictory use of the term ‘junk fee’ conflicts with the White House’s own definition, which cites the lack of disclosure of the fee being charged.”

Credit reports also were specifically mentioned as a problem area in the CFPB posting, claiming the business lacks competition and choice.

“The CFPB has heard reports of recent costs spiking 25% to as much as 400%,” the agency said. “At the same time, we estimate that nationwide credit reporting companies made over $1.3 billion annually.”

CFPB is also looking for consumer comment on the payment of discount points, although the posting does not distinguish between temporary and permanent rate buydowns.

“We are paying particular attention to the recent rise in discount points,” the posting said. “A higher percentage of borrowers reported paying discount points in 2022 than any other years since this data point was first reported in 2018.”

The agency said 50.2% of home purchase borrowers paid some discount points in 2022, with the median dollar amount being $2,370, up from 32.1% and $1,225 one year earlier.

While the proposed tax credit appears unlikely to get through a Republican-controlled Congress, Biden has the ability to use the CFPB to push his housing policy agenda.

An ‘unwelcome surprise’

A CFPB blog post on Friday states that families closing a mortgage “often get an unwelcome surprise: closing costs that all too often are full of junk fees.”

According to the CFPB, one measure of closing costs is total loan costs, which includes title insurance, credit report, appraisal, and origination. These costs increased by 21.8% from 2021 to 2022, reaching nearly $6,000, per the CFPB post. And, as they are fixed, they have an “outsized impact on borrowers with smaller mortgages,” it added.

The post provoked a strong reaction from the Mortgage Bankers Association (MBA). Its president and CEO, Bob Broeksmit, stated that the use of the term junk fees is “illogical” and contradicts the White House’s definition, which is “lack of disclosure of the fee being charged.”

“The fees mentioned are clearly disclosed to borrowers well before a home purchase on forms developed and prescribed by the Dodd-Frank Act and the CFPB itself,” Broeksmit said in a prepared statement.

Broeksmit added that the Bureau’s “TRID” rule in 2015 and other rules imposed in 2020 reformed mortgage disclosures and customers’ ability to read these documents.

What’s the CFPB monitoring?

The CFPB said it will closely examine three topics: discount points, lenders’ title insurance, and credit reports.

Discount points have surged in recent years as mortgage rates have risen and competition has gotten more fierce. They were used by 50.2% of home purchase borrowers in 2022, compared to 32.1% in 2021. And, despite lenders selling points to reduce rates, it “may not always save borrowers money, however, and may indeed add to borrowers’ costs,” the CFPB said.

In another criticism of housing finance practices, the CFPB said lenders force borrowers pay for their title insurance, and the amount “is often much greater than the risk.”

Regarding credit reports, HousingWire reported in December that lenders’ prices would jump in 2024. The CFPB said that the “credit reporting industry is highly concentrated” and that “these steep increases in a market that lacks competition and choice warrant further scrutiny.”

“In the coming months, the CFPB will continue working to analyze mortgage closing costs, seek public input, and, as necessary, issue rules and guidance to improve competition, choice, and affordability,” the blog post reads. “We will also continue using our supervision and enforcement tools to make it safer for people to purchase homes and to hold companies accountable.”

Broeksmit has argued for years that it’s the CFPB that has made mortgage lending more expensive for consumers. The agency announces “new legal obligations without formal process or deliberation, enforcing novel and untested legal theories, and making it very difficult for firms to understand their legal obligations,” he said in 2022. A year later he described housing policy coming from Washington, D.C. as “extreme overregulation.”

In response to the CFPB’s latest “baffling” blog post, he noted that the agency has already imposed limits on lenders’ fees. The services covered, such as appraisals and flood hazard certifications, bring efficiency to the mortgage market and benefit consumers. The Federal Housing Administration (FHA), Department of Veterans Affairs (VA), Fannie Mae, and Freddie Mac also require these services.

The MBA, according to him, is also concerned “regarding rising costs of the tri-merge credit reports” and shares the “desire to help more Americans become homeowners.”

“MBA is eager to continue working with the Biden administration in these efforts but will vigorously oppose politically motivated proposals that only increase regulatory costs, reduce competition, or otherwise make it more difficult for Americans to get the credit necessary to achieve homeownership,” Broeksmit said.

It was late 2022 and Mike was feeling the pressure. Mortgage rates had climbed close to the 7% range and he was determined to remain competitive on pricing with rival loan officers in North Carolina.

But there was a problem: pricing exceptions, in which the lender takes the hit, were becoming scarce at his company. So he did what a lot of retail loan officers in the industry were doing — Mike would reclassify a self-generated lead as a corporate-generated lead, thus slashing his compensation from 125 basis points down to as low as 50 bps, giving him a low enough rate to win the client and eventually close the deal. His manager and company bosses knew that he and other LOs were lying about where the lead source came from, he said.

The lower comp rate stung. After Mike paid his loan officer assistant, he was clearing just 40 bps. Still, it was better than nothing. After all, tens of thousands of loan officers had already exited the industry because they couldn’t generate enough business.

“At this time, I didn’t really think of it as an ethical issue,” Mike, whose last name is being withheld for fear of retaliation, told HousingWire in an interview in late November. “But it started to wear on me to where it was like, okay, I’m getting price-shopped left and right. I’m feeling the pressure to cut my pay, because when I do it, and my agent partners, they see that I do that, and then they’ll tell people they refer to me. ‘Hey, he can dig deeper if he really has to.’”

Mike continued: “Well, doesn’t that smack of bad faith if I’m not offering them my best price from jump? I would get people saying to me, ‘I’m not going to go in with you. I don’t feel comfortable with you, because you tried to get me to go for a higher pricing first, and then only offered a better deal once I told you I had another offer.”

Mike said he left that lender in early 2023 as a result of the ‘bucket game’ and refuses to manipulate where lead sources are coming from at his current shop.

“It’s a race to the bottom,” he said of the practice.

Over the past two months, HousingWire has interviewed more than a dozen loan officers, mortgage executives, attorneys and also reviewed several companies’ loan officer contracts and text messages between recruiters and prospects to shed light on the growing issue of pricing bucket manipulation, which critics say distorts market pricing and could represent a violation of fair lending laws.

It’s unknown how many retail lenders are engaged in the practice of falsifying lead sources to lower loan officer pay, but industry practitioners say it’s widespread, and in most cases, reclassifying leads into different pricing buckets before they lock is not permitted by the Consumer Financial Protection Bureau’s rules under Regulation Z.

It’s also unclear whether the CFPB is policing the practice; HousingWire could find no record of enforcement actions taken, and the agency’s audits are not public record.

Evolution of the LO Comp rule

In the wake of the housing crash in 2008, the CFPB created new rules that reshaped how loan officers were compensated. The architects of the new rules wanted to prevent loan officers from taking advantage of borrowers, which was a common occurrence in the days leading up to the Great Recession.

Under an updated Regulation Z, lenders could no longer pay loan officers differently based on terms of loans other than the amount of credit extended. In theory, this means loan officers provide the same service and pricing on loans, reducing the risk of steering.

“LOs also can’t get paid on proxies, and they define proxies to be pretty straightforward: some factor that correlates to terms over a significant number of transactions, and the LOs have the ability to change that factor,” said Troy Garris, co-managing partner at Garris Horn LLP.

But the CFPB did allow loan officers to be compensated differently based on lead sources, which do not fall under the category of terms or proxies and are neither a right or an obligation.

For example, when an existing customer calls the lender’s call center for a new mortgage or refinance, and the lender redirects the loan to the LO, “the LO gets paid less because it was sourced from the company, and it is less work for the LO,” said Colgate Selden, a founding member of the CFPB and an attorney at SeldenLindeke LLP. When it’s an outside lead, “the LOs generated the lead themselves; they are spending time marketing to new borrowers, so they get paid more.”

Attorneys told HousingWire that in the current marketplace, violations of LO Comp rules can arise when lenders and LOs alter compensation by changing the lead source after the initial contact with the borrower to lower their rate and secure the deals. Regulation Z generally does not allow LOs to change which lead source was used.

But, in today’s competitive market, “I do think there’s an incentive, especially on the LO side, to find ways to do something different – and probably also for companies to decide to take more risk,” said Garris. “We believe this is happening because people are frequently asking if there’s a rule change.”

How the ‘bucket game’ works

LOs who spoke to HousingWire said managers often told them they wouldn’t get pricing exceptions on deals, so if they wanted to gain an edge it would have to come out of their pay. Three loan officers at three different retail lenders described it as a feature of their lender’s business model.

“You feel out a prospective client during the initial conversation, get a sense of whether they know how everything works, if they’ve spoken to another lender, if they’re going to shop you, right? And you quote them the best possible rate you could give them that day, knowing that you’ll put them in a bucket just before lock,” said one Wisconsin-based LO. “It doesn’t really matter what you quote them in the initial conversation as long as you can get it below competitors around lock time…either through a pricing exception or the bucket [manipulation].”

One top-producing California-based loan officer said she was excited when a top 35 mortgage lender tried to recruit her with the promise of multiple pricing buckets. Having the buckets would provide her flexibility that her current lender didn’t offer, she thought at the time.

“What the [recruiting] company told me explicitly was the loan originator, when they go to lock the loan, they check a box – is it self, branch or corp gen? And you only get to check one box, but it’s the loan officer’s choosing, not the branch,” she said. “So the loan originator is choosing, not the branch that says I’m going to give you a lead and this is the comp for it. Not the corporate advertisement or online group that says you’re getting this lead from us and here’s documentation that it occurred and now you’re going to get less comp. It’s the ultimate in legalized fraud. Because it’s not true.”

These days, many lenders have pricing buckets for corporate-generated leads, branch leads, builder leads, marketing service agreement (MSAs) leads, internet leads from aggregators and more. In and of itself, it’s legal, provided the lead really did come from the source and it’s diligently tracked by the lender.

Loan officers and mortgage executives interviewed by HousingWire said some lenders justify the practice of manipulating the buckets by telling LOs it’s legal and they’ve been audited by the CFPB, which has not found any wrongdoing. Several executives accused of the practice declined to comment on the record about pricing bucket manipulation, though they all said they track leads as required and are in full compliance with the law.

Selden, the former CFPB attorney, said that LOs are telling borrowers who complain about high mortgage rates that companies are “running a special offer.” Borrowers are directed to the company’s website, where, by indicating the LO name, they supposedly qualify for a special deal with a lower rate. In reality, at lenders without adequate controls to prevent lead source manipulation, this shifts the source from self-generated to an in-house lead.

LOs interviewed by HousingWire said that in some cases they would be able to change the lead referral source themselves, and in other cases they’d need a manager to alter the lead source in the loan origination system.

While many instances of price bucket manipulation were directed by managers, LOs would also self-select, said Mike.

“Most of the time you don’t have a loan estimate from a competitor, you’re just afraid that you’re going to lose it because you’re so embarrassed about the rate. And that’s why a lot of my comrades… were going to the corporate-generated lead bucket before they even confirmed that they had to. Partly because you wanted to lead with your best price.”

Steve vonBerg, an attorney at law firm Orrick in Washington, D.C., worked as a loan officer and underwriter for seven years. He emphasized the potential trouble for lenders and LOs inaccurately classifying the lead source.

“Often, a [CFPB] examiner would see if the lead channel changed later in the process. That could be legitimate: the borrower starts working with an LO, and it’s a self-sourced lead for that LO, but then decides to buy a home in a different state in the middle of the process; the second LO that it has to be transferred to has now an internal-company referral, and so the lead source would legitimately change,” vonBerg said. “But, if there isn’t a legitimate reason for the lead source changing midstream, that would be fairly easy for an examiner to identify.”

“It’s wrong”

Victor Ciardelli is frustrated by the bucket game. Deeply frustrated. The Guaranteed Rate founder and CEO says he is losing money and loan officers to rivals because of a business practice that he says is flagrantly illegal, pervasive, and does not appear to be slowing down anytime soon.

Some rival retail lenders, he says, are creating up to a dozen pricing buckets for their loan officers. The tiered nature of the bucket comp structure in many cases — self generated being the highest at up to 150 bps, 100 bps for another ‘bucket,’ 80 bps for another, down to 60 bps, 40 bps and sometimes all the way to zero — proves that it is a deliberate business strategy, he said.

“It wasn’t intended that the loan officer at the time that they’re talking to the consumer and quoting them a rate, that the loan officer can put the consumer in any bucket they want,” he said in an interview with HousingWire. “But that is exactly what’s happening. What’s exactly happening is the fact that there’s all these different pricing buckets for a lot of these different companies out there. And that the loan officer is allowed to go in and offer the consumer whatever rate based on what the loan officer wants.”

He argued that LOs are maximizing their personal income per borrower.

“It’s no different than what happened prior to Dodd-Frank, where it was the wild, wild West and people were playing games with customers on rates and fees,” said Ciardelli. “It’s the same thing today. There’s no difference except the fact that there’s a law in place that tells the mortgage company and the individual loan officer. And the loan officers know that they’re violating the law. It’s greed.”

Ciardelli says the rival CEOs — he declined to name individuals and said it’s an industry-wide problem — are establishing these buckets and know “full well that the bucket is put in place in order to lie about where the lead source is coming from.”

They have an obligation to know where the leads are coming from, that the loan officers are putting them in the appropriate bucket and that they are being tracked, he said.

“The loan officer may take a hit on that loan, and may make less on that loan, but the company themselves doesn’t take the hit, their margin stays the same. So the company CEO is happy, because they’re like, ‘I’m giving my loan officers all this flexibility to go out and be competitive and win deals. And they’re going to win more deals than anybody else out there, because they’re going to be able to slot the individual borrower into these different lead channels. So the individual CEO is making all the money. They’re the ones killing it.”

Ciardelli says he asked about the bucket pricing game and attorneys all told him no, it’s not legal, he said.

“I’ll play by whatever the law is…But when the rules are set up to be a certain way and people are not following the rules, then that’s a problem.”

Two other executives at large retail lenders also said they’ve lost loan officers to competitors who are sanctioning, if not directing, the manipulation of pricing buckets.

“The LOs get told this is legal, it’s just pricing flexibility so they can compete, and they have a compliance team that monitors it,” said one executive at a regional lender in the South. “Obviously that’s not true… What’s happening is they [the lenders] are pricing high and basically forcing the LOs to cut from say 150 [basis points down to 50 [basis points] on some loans because otherwise they just won’t do enough business. It’s a feature, not a bug, as they say. We asked our attorneys if we could do this and they told us absolutely not.”

The Mortgage Bankers Association (MBA) is aware of the issue. The organization asked an outside attorney from Orrick Herrington & Sutcliffe LLP to study the permissibility of the practice. In a letter sent to members in February 2023, Orrick advised MBA members that changing the lead source of a loan after beginning work on the application in order to make a competitive pricing concession “is not permissible.”

The letter has had little meaningful impact, sources told HousingWire. If anything, the practice has increased over the last year.

Fair lending concerns

Another repercussion in the market is that savvy borrowers gain access to lower rates when lead sources are manipulated. Less educated applicants could be quoted higher rates for the same loan, raising concerns about fair lending practices.

But this argument prompts a broader discussion on the efficacy of the LO comp rule, with divergent opinions on the matter.

“I used to be an MLO for seven years. I was in the industry in the 2000s until it melted down, and then I ended up going to law school because I had lost my job. I originated hundreds of loans myself, and personally, I think overall the rule is a good rule,” vonBerg said.

vonBerg elaborated: “Under the old regime, LOs were not incentivized to offer their consumers the best loan and best pricing for them. They were incentivized to give them the loans and pricing where they would make more money. Although it has some issues that should be corrected, I think the LO comp rule makes a lot of sense, in that it removes a gigantic conflict of interest.”

Not everyone shares this viewpoint.

“The LO comp rulewas designed to prevent steering to high-cost loans. And really, those things don’t exist anymore. We can’t put borrowers in homes that they can’t afford,” said Brian Levy, Of Counsel at Katten and Temple, LLP.

According to Levy, the rule creates “a tremendous amount of anxiety for the mortgage lending industry that doesn’t benefit consumers in any meaningful way.”

“The industry is frustrated. They’re unable to easily reduce prices. For example, in the past, before the rule was around, LOs were able to take less as a commission, just like any other salesperson – a car salesperson – to make the deal work. That’s illegal now for loan officers. The mortgage company can make that decision [of lowering their margins and reducing rate], but the loan officer cannot.”

Levy noted that some consider the LO comp rule to be a de facto fair lending rule.

“But we already have fair lending rules. The idea that if the loan officer is discounting their fees, they would end up discounting on a discriminatory basis would already be problematic under existing law, so you don’t need the LO comp rule to make that illegal. It’s already illegal to discriminate in pricing. That said, it’s not illegal for people to negotiate just like you can negotiate a car price.”

The CFPB has also taken issue with other forms of pricing concessions over the last year. In the summer of 2022, the agency reported that pricing exceptions, in which the lender offers a discount, had harmed protected classes, who were less likely to be offered discounts.

Where’s the CFPB?

Multiple sources said the CFPB audits about 20% of mortgage lenders per year, and because of the prevalence of this practice, would undoubtedly have come across lead bucket pricing manipulation by now.

Why there hasn’t been any enforcement to date or whether there’s a future enforcement action is just on the horizon is hard to know.

The CFPB, which is undertaking a broad review of the LO Comp rule, declined to make anyone available to speak on the issue.

“We cannot comment on any ongoing enforcement or supervision matters,” said Raul Cisneros, a Bureau spokesperson. “Those who witness potential industry misconduct should consider reporting it by going here. Additionally, we always welcome stakeholder feedback on any of our rules, including the loan officer compensation rules.”

In early 2023, the CFPB initiated a review of Regulation Z‘s mortgage loan originator rules, which include certain provisions regarding compensation. However, industry experts do not foresee substantial changes or anticipate the CFPB addressing the issue of lead source manipulation.

“In fact, there haven’t been a lot of public enforcement actions by the CFPB in several years [on the LO comp rule]. But having said that, we used to complain that the CFPB was participating in regulation by enforcement, and now they seem to be regulating by supervisory highlights,” Kris Kully, a law firm Mayer Brown partner, said.

The CFPB’s latest move regarding the LO Comp Rule was to issue a supervisory highlight in the summer stating that compensating an LO differently based on whether a loan product was originated in-house or brokered to an outside lender is prohibited.

Industry practitioners said the lack of enforcement from regulators has allowed the pricing bucket manipulation practice to flourish, creating an uneven playing field.

“You have all these companies that all of a sudden are starting to get a free pass,” Ciardelli said. “They’re like, ‘I’m not having any audits. I’m not having anybody come and say anything to me. I mean, nothing’s really happening. I’m pretty much unscathed here.’ And year after year goes by, there’s no auditors, there’s no issues. And then they start to move the needle on how they’re running their business and decisions they’re making. And they have less fear of the government, less fear of the existing rules that are in place, because the rules that were set up are not being enforced.”

Another mortgage executive speculated that the pricing bucket games will come to an end not because of CFPB enforcement, but because loan officers and executives will battle it out in court.

“I’ve got calls from loan officers who feel like they’ve been pushed into a lower commission scale than they thought they were going to get to start with,” he said. “I hired somebody from a well-known lender. When they hired her, they told her, ‘Hey, these are what the rates are and this is what the commission is.’ When she got over there, the rates they were quoting were the lead-based rates, not the hundred-based points they were promising her… I don’t think the enforcement will come from the CFPB. I think it’ll come from some type of lawsuit like that.”

The lasting impact of LOs cutting their comp to win clients and close deals won’t be clear until mortgage rates meaningfully fall for a sustained period.

But many fear that the genie can’t be put back in the bottle.

“We’ve done this so much that they’ve built it into their pricing,” said Mike, the loan officer in North Carolina. “They are pricing things higher, assuming that we’re going to cut our pay, and protect their margins. So to me that’s the bigger issue for us selfishly, is we start doing that, and it’s going to become the norm. The pricing system and everything is going to assume that we’ll do that.”

He mused that RESPA guidelines prohibit an LO from buying a Realtor partner a Big Mac after a closing but lying about a lead source is not policed.

“Personally being an LO, the biggest issue to me is, they’re screwing with us and just… That’s how all these shops are finding a lifeline to keep their doors open. ‘We don’t have to pay them 100 bps, we can just pay them 50, and they’ll take it on the chin.’ And it’s like, yeah, we’ll take it on the chin. Many of us are using the heck out of our credit cards right now to survive. It’s not cool.”

Representative Maxine Waters, a Democrat from California, held a town hall meeting on Saturday at Inglewood High School where she pointedly asked executives from City National Bank, PNC Financial Services and Wells Fargo & Co., if they would each open a branch in her district. Photographer: David Paul Morris/Bloomberg

David Paul Morris/Bloomberg

LOS ANGELES – Rep. Maxine Waters held a town hall meeting on Saturday where she pointedly asked executives from City National Bank, PNC Financial Services and Wells Fargo & Co., if they would each open a branch in her district. She said she wanted to hold the banks accountable for promises made in recent merger agreements or consent orders.

The town hall meeting at Inglewood High School got fiery at times as Waters pressed the three bank executives to answer questions from constituents in her 43rd congressional district in South Los Angeles. Waters, the ranking member of the House Financial Services Committee, said she invited all the top banks to attend but was turned down by Bank of America, Citigroup, JPMorgan Chase and U.S. Bancorp.

Next week, the Senate Banking Committee plans to hold an annual oversight hearing with executives from the nation’s top banks. Waters said she was disappointed that Republicans in the House would not hold a similar hearing. Her town hall, she said, would try to fill in the gap.

When Jeffrey Martinez, executive vice president and head of branch banking at PNC Bank, described how the Pittsburgh bank was upholding its pledge to invest an eye-popping $88 billion in local communities over four years as part of its 2020 acquisition of BBVA, Waters asked specifically if PNC was coming to her neighborhood.

“When are you going to open up a branch in my district?” Waters said. “We have a problem with branch banking not being available to us in all of our communities in the way they should be. We call them banking deserts.”

Martinez responded: “That’s a great question, it’s an important one and one of the things we’ve slated even though we’re new to California.”

“We would like to help you find a location,” Waters said, to thunderous applause and laughter from the crowd of about 300. “I’m so looking forward to establishing” a branch here, she added.

Waters then described how City National Bank in Los Angeles had agreed in January to pay $31 million to settle redlining allegations brought by the Justice Department. As part of the agreement, City National has promised to open one branch in a majority-Black and Hispanic neighborhood in L.A. County.

“Can you discuss where you might be opening the branch?” Waters asked. “Where are you with all of this?”

David Cameron, City National’s executive vice president of personal and business banking responded, “That is a great question,” drawing laughter from the audience.

“I don’t have any announcement on where we’re going to put that branch.”

To which Waters replied: “Oh, we’ll help you,” to further applause from the audience.

City National plans “to go above and beyond,” the agreement to invest at least $29.5 million in a loan subsidy fund for residents of majority-Black and Hispanic neighborhoods in Los Angeles County, Cameron said. The bank has hired more than 20 loan officers to support the initiative to provide grants of up to $15,000 each to first-time homebuyers.

Waters also questioned why City National did not have a mortgage loan officer at a local branch on Crenshaw Boulevard in Los Angeles.

“You’ve done well at that branch, are you going to expand that branch and put a loan officer there?” Waters said. “Can you do these things?”

Waters skillfully thanked each of the bankers for showing up to the town hall meeting, while also hitting them hard on consent orders.

“I really thank you for coming today. I know that you know we have a lot of questions for you, based on the fines that you received and all of that,” she told Cameron, and then asked the audience to give him a round of applause.

She also asked Colleen Canny, Wells Fargo’s executive vice president and national head of branch banking, why the San Francisco bank has been closing so many branches, which Waters estimated at 2,000 branch closings over many years. She cited the Wells Fargo 2016 fake accounts scandal that led the Federal Reserve to impose an asset cap on the bank.

“First tell us, why did you close those branches?” Waters asked.

Canny said that customer transactions through branches have fallen 50% over the past three years as more banking is done online, through mobile apps or ATMs.

“We still think branches are important and we continue to look at our branch footprint to ensure we have the proper coverage,” Canny said.

Waters lamented that banks are closing branches in inner cities where seniors who may not necessarily use a cell phone to bank still prefer to go to a branch in person.

“I want to tell you something that is a cultural discovery for everybody,” Waters told the bankers and the audience. “We like to go to a teller as we put our money across the counter. We like this kind of interaction with the people that we do service with and this is the kind of cultural consideration that the bank should take into account.”

At the town hall, which lasted for four hours, constituents asked a wide range of questions including why there were long lines at their local branches and why they were not able to get small business loans or even speak directly to the same banker on each visit. CFPB Director Rohit Chopra, who spoke after the bankers, answered a range of questions on reverse mortgages, digital redlining and junk fees.

Waters also lambasted the banking industry generally for Republican-led efforts in the House, which voted on Friday to nullify the Consumer Financial Protection Bureau’s small-business data-collection rule. Despite the bill’s passage in a 221-202 vote, President Joe Biden has vowed to veto the bill and uphold the rule.

The head organizer for Rise Economy, the consumer group formerly known as the California Community Reinvestment Coalition, asked the bankers generally why they did not support the Consumer Financial Protection Bureau.

“Your industry trade groups are attacking the CFPB, they’re attacking fundamental consumer protections … and very basic data on small business lending that we fought hard for for nearly 10 years,” said Jyotswaroop Kaur Bawa, chief of organizing and campaigns at Rise Economy. “We want you to tell us specifically how many Black and Hispanic-owned businesses you make loans to and at what rate—that’s what the fight is about.”

The small-business lending rule is expected to be used by the CFPB to identify discrimination, though the bureau exempted more than 2,000 community banks and small businesses from the rule. The coalition sued the CFPB in 2019 for taking so long to issue the rule, which Dodd-Frank’s Section 1071 mandated.

The 1071 rule was about wealth-building and closing the wealth gap, Waters said.

“The Senate Republicans put up a great fight against getting the rule, the data that we needed to determine why we can’t get small business loans — they fought us very hard, and they said they represented the banks,” Waters said. “Republicans won on trying to kill that rule that would give us information that would show that Blacks, Latinos, women and LGBTQ would not be getting small business [loans.]”

Water did commend one bank: First Citizens BancShares, which acquired the failed Silicon Valley Bank and last month announced an agreement to invest more than $6.5 billion in California and Massachusetts communities through an updated community benefits plan. The agreement, Waters said, paved the way for a branch to be opened in Watts.

Waters characteristically played to the audience by rattling off the various programs created after the pandemic including loans that banks delivered via the Paycheck Protection Program.

“You’re wondering, if there’s all this money around, why haven’t we been able to get some of it,” Waters said.

WASHINGTON, D.C. – The Consumer Financial Protection Bureau, the Federal Reserve Board, and the Office of the Comptroller of the Currency today announced that the 2024 threshold for whether higher-priced mortgage loans are subject to special appraisal requirements will increase from $31,000 to $32,400.

The threshold amount will be effective January 1, 2024, and is based on the annual percentage increase in the Consumer Price Index for Urban Wage Earners and Clerical Workers, known as CPI-W, as of June 1, 2023.

The Dodd-Frank Act added special appraisal requirements for higher-priced mortgage loans, including that creditors obtain a written appraisal based on a physical visit to the interior of the home before making a higher-priced mortgage loan. The rules implementing these requirements contain an exemption for loans of $25,000 or less, adjusted annually to reflect CPI-W increases.

Read the Appraisals for Higher-Priced Mortgage Loans Exemption Threshold.

Media Contacts:

CFPB: Michael Robinson (202) 597-4022

Federal Reserve Board: Emma Jones (202) 452-2955

OCC: Stephanie Collins (202) 649-6870

###

The Consumer Financial Protection Bureau (CFPB) is a 21st century agency that helps consumer finance markets work by making rules more effective, by consistently and fairly enforcing those rules, and by empowering consumers to take more control over their economic lives. For more information, visit www.consumerfinance.gov.

Over the past few years, regulators have been working to right the wrongs that occurred during the mortgage boom and subsequent bust to ensure history doesn’t repeat itself.

One focus has been on improving mortgage disclosures so homeowners can actually make sense of what they’re reading.

The latest development is a model form for mortgage statements, which came about thanks to the Dodd-Frank Act, spearheaded by the Consumer Financial Protection Bureau.

It amends the Truth in Lending Act by adding a section on “Periodic Statements for Residential Mortgage Loans.”

This is similar to the credit card overhaul, which has led to more transparent monthly statements that spell out your current balance, how much interest you will pay, when your payment is due, and more.

What’s On the New Mortgage Statement Form?

The new mortgage form, which is pending public comment (including yours if you want to get involved), specifies that the following items must be included:

– the principal loan amount – the current interest rate – the date when the interest rate may reset (if adjustable) – description of any late fees – description of any prepayment penalty – phone number and e-mail address to obtain more info about mortgage – information about housing counselors

Check out the form here

The first item on the list specifies what your current loan balance is, which is pretty straightforward. It is also accompanied by a maturity date, which is when the mortgage will be paid off in full.

On the top right side of the form is your account number, payment due date, and amount due. It also includes an alternative amount if you pay late.

Below that, your monthly mortgage payment is broken down into principal, interest, and escrow, which includes taxes and insurance. It displays what you paid last month in each of these departments, and also what you’ve paid year to date.

I think the form should also include the total amount of interest and principal paid since loan inception as well, so hopefully they’ll include that.

This can help illustrate how much homeowners spend on interest versus principal over the years, and could lead to shorter-term mortgages.

[30-year vs. 15-year fixed mortgage]

The proposed form will also include transaction activity for the past month detailing what amount you paid, including any late fees if applicable. This can be handy as proof of payment if there are any disputes.

The current mortgage rate will also be listed prominently. If it’s a fixed-rate mortgage, there won’t be any mention of a possible interest rate reset.

If it’s an adjustable-rate mortgage, there will be text that says, “until X date” next to the interest rate. This is helpful to ensure borrowers know how long their interest rate is fixed, as this date often gets lost in the shuffle.

Below that is information regarding a prepayment penalty, assuming one applies, including how much you will owe for prepayment.

Ensure Extra Payments Go Where You Want Them

My favorite part of the new form is the box pertaining to any overpayment. At the bottom of the new form, it allows you to designate where you want additional funds to be applied.

So if you want to make extra payments each month, you can specify that they be directed toward principal or escrow, to avoid the lender or loan servicer doing what they please.

There is also a large box toward the bottom of the form that provides information for those experiencing financial difficulty, including where to find a state or federally approved housing counselor.

All in all, it looks like a good improvement to the mix of mortgage statement forms currently used by loan servicers.

It will likely increase transparency and lead to a better understanding among homeowners, who are often in the dark when it comes to making sense of their mortgage.

This form should reduce homeowner abuses and perhaps even defaults.

What do you think of the new form? Is it missing anything important?

WASHINGTON, D.C. – Today, U.S. Senator Sherrod Brown (D-OH), Chairman of the Senate Committee on Banking, Housing, and Urban Affairs, took to the Senate floor ahead of a Congressional Review Act (CRA) vote to overturn the Consumer Financial Protection Bureau’s rule on small business lending pursuant to Section 1071 of the Dodd-Frank Act. The rule is designed to promote access to credit and combat discrimination in small business lending by making small business lending data more transparent.

Sen. Brown’s remarks, as prepared for delivery, follow:

Our middle class relies on strong small businesses.

Small business ownership is the second-largest source of personal wealth in this country – only behind owning a home. Small businesses make up more than 40 percent of our economy.

To build strong small businesses, entrepreneurs need credit. A loan lets you turn an idea into a business, or invest in your company to hire more workers.

That’s why small business credit is so essential to our economy and to our middle class.

But today, small business lending takes place in the dark. We don’t have good data about how lenders are serving the small businesses in their communities.

And we don’t have good data about who lenders might be leaving behind.

Without transparency, it’s all too easy for entrepreneurs in Ohio to lose out.

The data we do have suggest too many small business owners aren’t getting a fair shot at a loan for their business.

Take rural small businesses. We know that rural communities have seen bank branch closures for years, drying up access to credit for small businesses. We need the data to understand how to reach these business owners, and grow small town economies.

Or take small business owned by women or people of color. The data we do have suggest they’re more likely to be denied loans and charged higher interest rates.

You don’t need reports and studies to know that most Ohioans don’t get a fair shake from big banks and the financial system. But you do need accurate information to fight back.

That’s why, in 2010, Congress required the CFPB to get that information, and this spring, the CFPB issued a rule to finally implement the law and bring transparency to the small business lending market.

We’re talking about basic data on the borrowers’ demographics, loan pricing, application approvals, and other critical information – just like we do with mortgages.

With this data, we’ll be able to see gaps in the small business lending market—allowing programs to expand access to credit for small businesses, like small businesses in rural areas.

And more data means more accountability—ensuring that lenders reach minority communities and helping to root out discrimination.

We’ve seen this model work before.

After we began publishing data about home mortgages, more Americans of all races and backgrounds were able to achieve the dream of home ownership.

This still protects people’s privacy – borrowers aren’t required to submit information if they don’t want to.

Of course, the big banks and their lobbyists are putting up a fight. They always do.

But I’m not going to help Wall Street avoid accountability.

I want to see more Ohio small businesses get loans and grow and be successful, and we are not going to let the banking lobby stand in the way.

I hope my colleagues will stand up for small businesses, stand up for entrepreneurs, and vote against this resolution.

A financial instrument is simply a contract between entities that represents the exchange of money for a certain asset. Financial instruments include most types of investments: cash, stocks, bonds, mutual funds, exchange-traded funds (ETFs), certificates of deposit (CDs), loans, derivatives, and more.

Financial instruments facilitate the movement of capital through the markets and the broader economic system. While this may take different forms, the flow of capital remains a central feature.

What Is a Financial Instrument?

Generally Accepted Accounting Principles (GAAP) defines a financial instrument as cash; evidence of an ownership interest in a company or other entity; or a contract. A financial instrument confers either a right or an obligation to the holder of the instrument, and is an asset that can be created, modified, traded, or settled.

Investors can trade financial instruments on a public exchange. The New York Stock Exchange (NYSE) is an example of a spot market in which investors can trade equity instruments for immediate delivery. 💡 Quick Tip: The best stock trading app? That’s a personal preference, of course. Generally speaking, though, a great app is one with an intuitive interface and powerful features to help make trades quickly and easily.

Financial Instrument vs Security

A security is a type of financial instrument with a fluctuating monetary value that carries a certain amount of risk for the individual or entity that holds it. Investors can trade securities through a public exchange or over-the-counter market.

The federal government regulates securities and the securities industry under a series of laws, including the Securities Act of 1933, the Securities Exchange Act of 1934, and the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010.

All securities are financial instruments but not all financial instruments are securities.

Like financial instruments, securities fall into different groups or categories. The four types of securities include:

• Equities. Equities represent an ownership interest in a company. Stocks and mutual funds are examples of equity securities.

• Debt. Debt refers to money lent by investors to corporate or government entities. Corporate and municipal bonds are two examples of debt securities.

• Derivatives. Derivatives are financial contracts whose value is tied to an underlying asset. Futures and stock options are derivative instruments.

• Hybrid. Hybrid securities combine aspects of debt and equity. Convertible bonds are a type of hybrid instrument.

Recommended: Bonds vs. Stocks: Understanding the Difference

Types of Financial Instruments

Financial instruments are not all alike. There are different types of financial instruments in different asset classes. Certain financial instruments are more complex in nature than others, meaning they may require more knowledge or expertise to handle or trade.

1. Cash Instruments

Cash instruments are financial instruments whose value fluctuates based on changing market conditions. Cash instruments can be securities traded on an exchange, such as stocks, or other types of financial contracts.

For example, a certificate of deposit account (CD) is a type of cash instrument. Loans also fall under the cash instrument heading as they represent an agreement or contract between two parties where money is exchanged.

2. Derivative Instruments

Derivative instruments or derivatives draw their value from an underlying asset, and fluctuate based on the changing value of the underlying security or benchmark.

As mentioned, options are a type of derivative instrument, as are futures contracts, forwards, and swaps.

3. Foreign Exchange Instruments

Foreign exchange instruments are financial instruments associated with international markets. For example, in forex trading investors trade currencies from different currencies through global exchanges.

Asset Classes of Financial Instruments

Financial instruments can also be broken down by asset class.

4. Debt-Based Financial Instruments

Companies use debt-based financial instruments as a means of raising capital. For example, say a municipal government wants to launch a road improvement project but lacks the funding to do so. They may issue one or more municipal bonds to raise the money they need.

Investors buy these bonds, contributing the capital needed for the road project. The municipal government then pays the investors back their principal at a later date, along with interest.

5. Equity-Based Financial Instruments

Equity-based financial instruments convey some form of ownership of an entity. If you buy 100 shares of stock in XYZ company, for example, you’re purchasing an equity-based instrument.

Equity-based instruments can help companies raise capital, but the company does not have to pay anything back to investors. Instead, investors may receive dividends from the stock shares they own, or realize profits if they’re able to sell those shares for a capital gain.

Are Commodities Financial Instruments?

Commodities such as oil or gas, precious metals, agricultural products and other raw materials are not considered financial instruments. A commodity itself, such as pork or copper, doesn’t direct the flow of capital.

That said, there are certain instruments whereby commodities are traded, including stocks, exchange-traded funds, and futures contracts.

A futures contract represents an agreement to buy or sell a certain commodity at a specific price at a future date. So, for example, an orange grower might sell a futures contract agreeing to sell a certain amount of their crop for a set price. An orange juice company could then buy a contract to purchase oranges at X price.

For the everyday investor, futures trading in commodities typically doesn’t mean you plan to take delivery of two tons of coffee beans or 4,000 bushels of corn. Instead, you buy a futures contract with the intention of selling it before it expires. 💡 Quick Tip: It’s smart to invest in a range of assets so that you’re not overly reliant on any one company or market to do well. For example, by investing in different sectors you can add diversification to your portfolio, which may help mitigate some risk factors over time.

Uses of Financial Instruments

Investors and businesses may use financial instrument for the following purposes:

1. As a Means of Payment

You already use financial instruments in your everyday life. When you write a check to pay a bill or use cash to buy groceries, you’re exchanging a financial instrument for goods and services.

Likewise, business entities may charge purchases to a business credit card. They’re borrowing money from the credit card company and paying it back at a later date, often with interest.

2. Risk Transfer

Investors use financial instruments to transfer risk when trading options and other derivative instruments, such as interest rate swaps. With options, for example, an investor has the option to buy or sell an underlying asset at a specified price on or before a predetermined date. A contract exists between the individual who writes the option and the individual who buys it. This type of financial instrument allows an investor to speculate about which way prices for a particular security may move in the future.

3. To Store Value

Businesses often use financial instruments in this way. For example, say you default on a credit card balance. Your credit card company can write off the amount as a bad debt and sell it to a debt collector. Meanwhile, businesses with outstanding invoices they’re awaiting payment on can use factoring or accounts receivables financing to borrow against their value.

4. To Raise Capital

Companies may issue stocks or bonds in order to get access to capital that they can invest in their business. In this case, the financial instruments could be a means of raising capital for one party and a store of value for the other.

Importance of Financial Instruments

Financial instruments are central to not only the stock market, but also the financial and economic system as a whole. They provide structures and legal obligations that facilitate the regulated exchange of capital via investing, lending and borrowing, speculation and growth.

In short, financial instruments keep the financial markets moving, and they also help businesses to keep their doors open and allow consumers to manage their finances, plan for the future, and invest with the hope of future gains.

For example, you may also have a savings account that you use to hold your emergency fund, an Individual Retirement Account (IRA) that you use to save for retirement and a taxable brokerage account for trading stocks. Your checking account is one of the basic tools you might use to pay bills or make purchases.

You might be paying down a mortgage or student loans while occasionally using credit cards to spend. All of these financial instruments allow you to direct the flow of money from one place to another.

The Takeaway

Financial instruments are integral to every aspect of the financial world, and they also play a significant part in business transactions and day-to-day financial management. If you trade stocks, invest in an IRA, or write checks to your landlord, then you’re contributing to the movement of capital with various financial instruments. Understanding the different types of financial instruments is the first step in becoming a steward of your own money.

Ready to invest in your goals? It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here).

Invest with as little as $5 with a SoFi Active Investing account.

Photo credit: iStock/Love portrait and love the world

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Exchange Traded Funds (ETFs): Investors should carefully consider the information contained in the prospectus, which contains the Fund’s investment objectives, risks, charges, expenses, and other relevant information. You may obtain a prospectus from the Fund company’s website or by email customer service at [email protected]. Please read the prospectus carefully prior to investing. Shares of ETFs must be bought and sold at market price, which can vary significantly from the Fund’s net asset value (NAV). Investment returns are subject to market volatility and shares may be worth more or less their original value when redeemed. The diversification of an ETF will not protect against loss. An ETF may not achieve its stated investment objective. Rebalancing and other activities within the fund may be subject to tax consequences.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Well, the Consumer Finance Protection Bureau finally released its “Ability to Repay” and “Qualified Mortgage” rules today.

At first glance, they look to be pretty lackluster, and the CFPB seems to be asking more questions than it is giving answers.

As part of Dodd-Frank reform arising out of the latest mortgage crisis, lenders must now ensure that borrowers have the ability to repay their mortgages.

While this sounds like a no-brainer, prior to the crisis just about anyone with a pulse could take out a home loan.

The CFPB included the story of a victimized borrower in its press release, though you have to wonder how many of these homeowners actually knew they couldn’t afford the loans before agreeing to apply for one.

Sure, it went both ways, but it was both lenders and borrowers who were at fault for the crisis.

Ability-to-Repay Rule

The new “Ability-to-Repay rule” requires lenders to underwrite pretty much ALL new residential home loans a lot more stringently than in past years, namely the 2000s.

However, the new mortgage rules are pretty much on par with today’s underwriting standards, which have become much more rigorous in light of past abuses.

I say pretty much all because HELOCs, time-share plans, reverse mortgages, bridge loans, and certain construction-to-perm loans are exempt from the ATR rule.

As part of the ATR rule, lenders must consider and verify eight (8) underwriting criteria:

– Current income or assets – Current job status – Credit history – Monthly payment on mortgage – Monthly payment on any other loan tied to subject property – All other debt obligations – The borrower’s debt-to-income ratio

So basically underwriters need to do their due diligence, which has always been the case.

There is nothing groundbreaking here, just basic underwriting at its purest and best, including verifying that borrowers have sufficient income and assets to take out a sizable home loan.

This means no stated income loans or no doc loans, which were prevalent during the housing boom.

Additionally, lenders can’t use teaser rates to qualify borrowers; only the full principal and interest payment will suffice.

However, if a borrower is being refinanced out of a high-risk loan, such as an ARM, interest-only loan, or option arm, into a more stable loan, the full underwriting process is not necessary.

Certain federal refinancing programs such as HARP 2 will also be exempt from these rules.

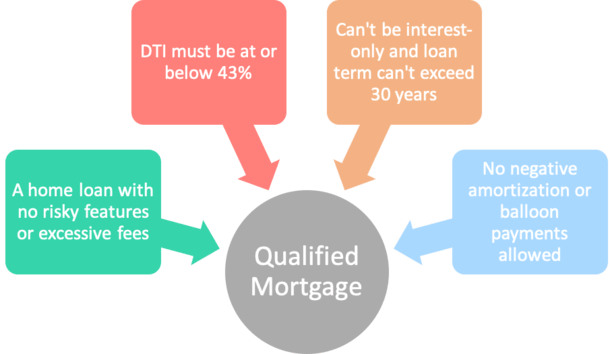

What Is a Qualified Mortgage?

The CFPB also released its definition of a “qualified mortgage,” which is presumed to meet the ATR rule requirements as well, and provide the most protection to borrowers (and more importantly, lenders).

Qualified mortgages have even more mandatory features, including the following:

– No excessive upfront points/fees – No interest-only loans – No negative amortization loans – No loan terms beyond 30 years – Max debt-to-income ratio of 43% – No balloon mortgages (unless small creditor in rural/underserved area)

For a transitional period (seven years), the DTI limit will not be enforced if the loans are eligible for purchase by Fannie Mae, Freddie Mac, or the FHA.

So in essence, the DTI limit won’t really be an issue for most loans, seeing that the majority are sold to Fannie or Freddie.

*The FHA Qualified Mortgage definition is pretty much the same as Fannie and Freddie’s, except for the APR thresholds, which are detailed below.

Here is a look at the max points and fees for Qualified Mortgages, currently capped at 3% of the loan amount if $100,000 or higher, and a proposal made by the Mortgage Bankers Association to increase them for smaller loan amounts:

Note that many third-party fees for things like title insurance, escrow, appraisal and credit reports aren’t part of the fee calculation (unless they come from a creditor affiliate, the creditor receives compensation, or the fees are deemed unreasonable).

Additionally, discount points may be limited based on the loan’s APR relative to the average prime rate offer (APOR).

It’s all very confusing at the moment, so hopefully over time some of these issues will be clarified.

Types of Qualified Mortgages

Qualified Mortgages with Rebuttal Presumption

This category of QMs covers “higher-priced loans” reserved for borrowers with insufficient or poor credit history. These loans are distinguished as those with APR more than 150 basis points (1.5%) above the “Average Prime Offer Rate” (APOR) benchmark.

Assuming the loan finds its way into default, the borrower can “rebut the presumption” that the lender actually considered their ability to repay the loan.

The CFPB notes that the borrower would have to prove that the lender didn’t consider their other living expenses after the mortgage and other debts were accounted for.

Note: For FHA loans, mortgages with an APR greater than APOR + 115bps + on-going Mortgage Insurance Premium (MIP) are considered Rebuttable Presumption Qualified Mortgages.

Qualified Mortgages with Safe Harbor

The second category of QMs is reserved for lower-priced loans made to borrowers who present little risk. These loans are defined as those with APR less than or equal to 150 basis points (1.5%) above the APOR benchmark.

Lenders will be assumed to have “legally satisfied” ATR requirements, meaning they won’t be on the hook for the loan if it goes bad.

However, borrowers can still challenge the lender if they believe the loan fails to meet the rules of a QM.

In both categories, borrowers also have the right to challenge lenders for violating any other federal protection laws.

Note: For FHA loans, mortgages with APRs less than or equal to APOR + 115bps + on-going MIP are considered Safe Harbor Qualified Mortgages.

More Ability-to-Repay Proposals

The CFPB is also seeking public comment for a number of other proposals, including whether there should be exemptions for non-profit creditors and housing finance agencies promoting affordable housing and community development (grey area).

Exemptions are also being floated for homeownership stabilization programs intended to prevent foreclosures, such as the Making Home Affordable initiative.

Additionally, community banks and smaller credit unions that originate and hold loans in their own portfolios could be given QM status.

Finally, the CFPB wants advice on how best to calculate the loan origination compensation rules, including specific limits on mortgage points and fees.

All said, there are plenty of unanswered questions here, and much of it sounds like the same nonsense all over again. The type of rule making that is circumvented before it’s even written.

Still, it will be interesting to see if “QM loan” becomes a household name, and makes non-QM loans much more expensive.

The Ability-to-Repay rule and proposed amendments are expected to go into effect in January 2014.