The Mortgage Bankers Association (MBA) and the National Mortgage Servicing Association (NMSA) are expressing their views on a recently revised Federal Housing Administration (FHA) loss mitigation proposal, stating that it needs additional adjustments to effectively address the challenges it is designed to tackle.

The proposed policy

FHA in May submitted — and in November, updated — a draft Mortgagee Letter (ML) to the Single Family Drafting Table, an online portal for stakeholders to review proposed policies. The proposed ML would establish a new loss mitigation option for mortgage borrowers called the “payment supplement.”

It would establish “a new home retention option to help struggling homeowners meet their mortgage obligations,” according to the May 2023 announcement from FHA. “The new option, called the Payment Supplement Partial Claim, would allow mortgage servicers to use the FHA Partial Claim both to bring a borrower’s mortgage current and to provide temporary reductions to their monthly mortgage payments for up to five years.”

Industry response

Members of the MBA and NMSA submitted a letter to FHA Commissioner Julia Gordon on the matter this week, largely supporting it but making a series of key recommendations designed to address industry concerns.

“The resources required to implement and maintain the Payment Supplement, including a servicer’s ongoing obligation to borrowers and [the U.S. Department of Housing and Urban Development (HUD)] throughout the Payment Supplement Period, require additional amendments to the Draft ML,” the letter explained.

“We are very encouraged by FHA’s thoughtful process to date and request certain changes to allow for the successful implementation of Payment Supplement by reducing [its proposal’s] operational, compliance, liquidity, and reputational risks,” the letter added.

The payment supplement policy “[combines] a standalone Partial Claim to bring the mortgage current with a new monthly principal reduction (MoPR), which will temporarily provide a monthly payment towards the principal portion of a borrower’s monthly mortgage payment, without requiring the mortgage to be modified,” the letter said.

The payment supplement would also “provide a temporary payment reduction for three years, after which the Borrower will be responsible for resuming payment of the full monthly [principal and interest] amount.”

Recommendations

The MBA and NMSA letter makes four key recommendations: to increase the proposed incentive payment from $1,000 to $3,500; to provide the model note and payment supplement agreement while “remov[ing] enforceability;” to end the payment supplement if a borrower re-defaults during the supplement period; and to provide 9-12 months for successful implementation of the policy.

“Sustainable loss mitigation policy is necessary to preserve affordable homeownership,” the letter said. “FHA guidance must continue to reduce the program’s complexity as the draft ML touches on all aspects of a servicer’s operations and loan lifecycle.”

Servicer engagement with borrowers is “heavily impacted through multiple required communication touchpoints,” and the supplement as currently proposed “remains administratively burdensome and costly to temporarily implement and maintain as a solution under the COVID-19 Recovery Loss Mitigation waterfall,” the letter explained.

Addressing the identified gaps will improve the borrower experience, the letter said, as well as “reduce the risk of inadvertent noncompliance for servicers and establish a permanent program.”

The Mortgage Bankers Association issued a statement this afternoon in response to a report released by the Center for Responsible Lending this morning, calling it misleading and self-serving.

In the report, the CRL claimed mortgage lenders weren’t doing enough to assist homeowners and suggested court-supervised modifications of distressed mortgages, a solution currently barred by existing bankruptcy laws.

“By choosing to misread and misinterpret the existing data on subprime loans, officials at the Center for Responsible Lending have again demonstrated they are more interested in advancing their own legislative agenda than in having an honest debate about the real scope of the problem and how to help those most in need,” said David G. Kittle, Chairman-Elect of the Mortgage Bankers Association.

“According to Moody’s, more than 50 percent of borrowers with subprime ARMs scheduled to reset in the first eight months of 2007 refinanced or otherwise paid off their loans prior to the rate reset.”

“So more than half of those loans that CRL cites as at-risk will never see their rates reset. In fact, the bankruptcy changes CRL advocates for would actually make it harder for consumers to refinance out of their subprime loans because it would increase the cost of all new loans.”

“And CRL’s stubborn insistence on clinging to ‘loan modification‘ as the only means by which a lender can help a borrower in trouble only serves to further mislead policymakers into overreaction.”

“Repayment plans, forbearance and even short sales are all widely accepted ways of helping a consumer avoid foreclosure. And yet CRL ignores them, because including them would better demonstrate the vast efforts lenders make,” Kittle continued.

It’s clear that the MBA is vehemently opposed to bankruptcy reform, releasing several statements claiming such legislation would cause mortgage rates to soar, and even going so far as to launch the “Stop the Bankruptcy Cram Down Resource Center”, which provides state and county-level data indicating the potential costs to the average homeowner.

“Policymakers should ignore this report as it is more rhetoric than fact. Bankruptcy reform is not the answer for consumers having trouble making their mortgage payments. It will drive up the cost of credit in the form of higher rates, larger down payments and greater closing costs.”

“Further, bankruptcy is a logistical and financial nightmare for consumers. Filing for bankruptcy is expensive and approximately two-thirds of all bankruptcy plans fail. Nobody should be holding it out as a better alternative to working with your lender to try to find a mutually agreeable resolution.”

On December 12th, the House Judiciary Committee passed HR 3609, the so-called “Emergency Home Ownership and Mortgage Equity Protection Act of 2007.”

The proposed legislation ends a 110-year old federal protection that prevents bankruptcy judges from altering the terms of mortgage loans tied to primary residences, a move the MBA believes will result in interest rates one-and-a-half to two points higher.

While delinquencies remain low overall, the number of delinquent loans ticked up in November, according to the latest ICE Mortgage Monitor report. Furthermore, the delinquency rate among FHA loans is at a nine-year high, and will be worth watching closely in 2024, the report said.

The national delinquency rate climbed to 3.39% in November, which is up 13 basis points from October and down 10 basis points from November 2022.

In November, serious delinquencies (90+ days past due) rose month over month, adding 12,000 additional borrowers in that category for 459,000 people in total. However, the rate of serious delinquencies remained 21% below the November 2022 level.

Meanwhile, early-stage delinquencies (30 and 60 days past due) continued to increase. In November, 70,000 additional borrowers were 30 days or more late on their mortgage payments, amounting to 1,804,000 loans. Moreover, early-stage delinquencies among VA loans hit their highest non-pandemic levels since 2009.

Foreclosure starts decreased by 12.2% in November to 29,000 with active foreclosure inventory falling to 216,000, some 23% and 24% below 2019 levels respectively

The five states with the worst mortgage performance were Mississippi, Louisiana, Alabama, Indiana and Arkansas. At the other end of the spectrum, California, Idaho, Washington, Montana and Colorado were the states that showed the best mortgage performance.

A handful of consumer advocacy groups sent letters today to Senate Banking Committee Chairman Christopher Dodd and House Financial Services Committee Chairman Barney Frank, urging them to conduct congressional hearings on Bank of America’s proposed acquisition of Countrywide Financial in an effort to protect at-risk homeowners.

“Congress has a one-time opportunity to take millions of current homeowners out of financial jeopardy, and stabilize the financial well-being of countless neighborhoods,” wrote Alan Fisher, executive director of the California Reinvestment Coalition.

“Congress can ensure that this vast amalgamation of these two financial giants has a positive impact, and create the model for resolution of our nation’s growing economic disaster.”

Fisher also noted that the proposed merger could lead to job cuts, which in turn could slow down the loan modification efforts currently underway intended to make mortgage payments more manageable for struggling homeowners.

The groups, which include The California Reinvestment Coalition, Community Reinvestment Association of North Carolina, Neighborhood Economic Development Advocacy Project (New York), and New Jersey Citizen Action, are concerned because Bank of America hasn’t released a specific plan detailing efforts to keep borrowers in their homes.

“Working families and communities will suffer if Bank of America is allowed to take control of Countrywide’s portfolio without stringent oversight, and without a concrete commitment to work with distressed borrowers to prevent foreclosure,” said Josh Zinner, co-director of the Neighborhood Economic Development Advocacy Project of New York City.

The merger of the two mortgage lenders will result in a combined servicing portfolio of $1.9 trillion, or roughly 21 percent of the national mortgage market, meaning the choices they make will have a significant impact on the mortgage industry as a whole.

“With this proposed merger, Bank of America undertakes responsibility for hundreds of thousands of potential foreclosures,” says Peter Skillern, executive director of the Community Reinvestment Association of North Carolina.

“They must make a commitment to mitigate the damage done by Countrywide Mortgage. A bigger, badder bank is not a solution, a bigger better bank can be.”

Some 122,000 Countrywide borrowers got an unpleasant surprise this week when they were told that they could no longer draw on their home equity lines of credit.

According to a letter obtained by Mortgage Implode, those who received the notices had either experienced a significant decline in their property value, been delinquent in paying their monthly mortgage payments, failed to pay property taxes or insurance, or violated certain terms associated with the loan.

One example given in the letter is a situation in which a borrower claims a property is their primary residence during loan origination, only for Countrywide to later discover that the property is in fact non-owner occupied.

Countrywide said other reasons not listed in the memo could spark similar action, and that the move wasn’t temporary, but rather an ongoing policy.

According to the LA times, Countrywide is using “computer modeling” to determine which customers are upside down on their mortgages to determine who will lose the right to withdraw money from their credit lines.

Chase to Tighten Guidelines on Second Mortgages

According to a memo sent to mortgage brokers this week, Chase is reducing the maximum combined-loan-to-value on second mortgages because of falling property values.

Beginning Monday, the New York-based bank and mortgage lender will no longer originate loans exceeding 85 percent CLTV on primary residences.

“Chase is committed to remaining in the wholesale business and in doing such, finds that we cannot afford to be in a position of lending at or above 100% loan-to-value, especially after accounting for falling home prices,” the memo said.

The bank is also reducing the max debt-to-income ratio to 40% for purchases and refinances for borrowers with credit scores below 700 and requiring that properties be off the market for 180 days to be eligible for a refinance.

IndyMac Limits Super Jumbo Lending

In related news, IndyMac released a memo yesterday saying it would limit super jumbo loan amounts to $2 million, and will no longer accept stated income documentation.

Borrowers who are able to provide full documentation will be limited to a maximum DTI of 40 percent, down from a previous 50 percent.

The Pasadena-based lender said the move would result in improved pricing on related products.

As interest rates increased rapidly throughout 2022, the number of refinance mortgage originations declined. The composition of these refinances also changed. Cash-out refinances – where a homeowner borrows an amount substantially greater than what they owe on their existing mortgage – became more common than non-cash-out (also known as “rate-and-term”) refinances. An equity “cashed out” from the home – which, in turn, increases the mortgage balance – is often used by the borrower to pay down other debts, fund home repairs, and pay for educational expenses, among other big-ticket purchases. A cash-out refinance takes the place of the original mortgage, but alternative products that tap home equity, such as home equity loans and home equity lines of credit, leave the original first-lien mortgage intact. Such needs for cash may be necessary and unavoidable, hence the persistence of some (albeit reduced) amount of cash-out refinances even in the face of rising interest rates.

Despite the recent decrease in volume, cash-out refinance originations are a segment of the mortgage market worth monitoring, especially since they were considered one of the mechanisms that exacerbated the 2008 financial crisis.1 In the case of both cash-out and non-cash-out refinances, the borrower’s home is used as collateral for the loan. Failing to make payments or meet other loan conditions can result in the borrower losing their home through foreclosure. The added risk for borrowers originating a cash-out refinance, especially in today’s interest-rate environment, is that their mortgage payments and mortgage loan terms are both likely to increase.

Who are the homeowners taking out cash-out refinances, and are their loans comparable to non-cash-out refinance loans? Are cash-out refinance borrowers more likely to become delinquent? In this post, we look at the loan and borrower characteristics of homeowners who originated a cash-out refinance compared to a non-cash-out refinance. We study refinances originated between 2013 and 2023. This allows us to study delinquencies—one manifestation of risk—throughout the post-crisis period, and how they vary among the population. This period includes periods of falling and rising interest rates, as we have observed recently. With this information, we can better gauge the risk to consumers and the housing market of the recent trends in refinances. We find that:

Cash-out refinances were a larger share of all refinances during periods of rising interest rates.

Borrowers of cash-out refinances had lower credit scores, lower incomes, and smaller loan amounts compared to non-cash-out refinance borrowers.

Loan-to-value and debt-to-income ratios were similar for cash-out and non-cash-out refinances.

Cash-out refinances had larger shares of older, female, Black, and Hispanic borrowers, compared to non-cash-out refinances.

Serious delinquencies were rare for borrowers with higher credit scores, regardless of whether the refinance was cash-out or not.

For borrowers with lower credit scores, both cash-out and non-cash-out refinance borrowers have similar two-year delinquency rates, except for a relative increase in delinquencies among cash-out refinance borrowers in 2017—a year marked by rising interest rates.

We conclude with a comparison of the market for cash-out refinances before the financial crisis to the post-crisis time period, as well as potential concerns with cash-out refinances to monitor going forward.

Loan and borrower characteristics of refinances

We used refinance data in the National Mortgage Database to compare the loan characteristics and two-year delinquency status of cash-out refinances and non-cash-out refinances. The National Mortgage Database is a representative 1-in-20 sample of all closed-end first-lien mortgages in the United States. We identify refinances as cash-out refinance mortgages when the total value of sampled refinance loans and their associated junior liens were more than five percent larger than the total value of the preceding loans and associated junior liens.

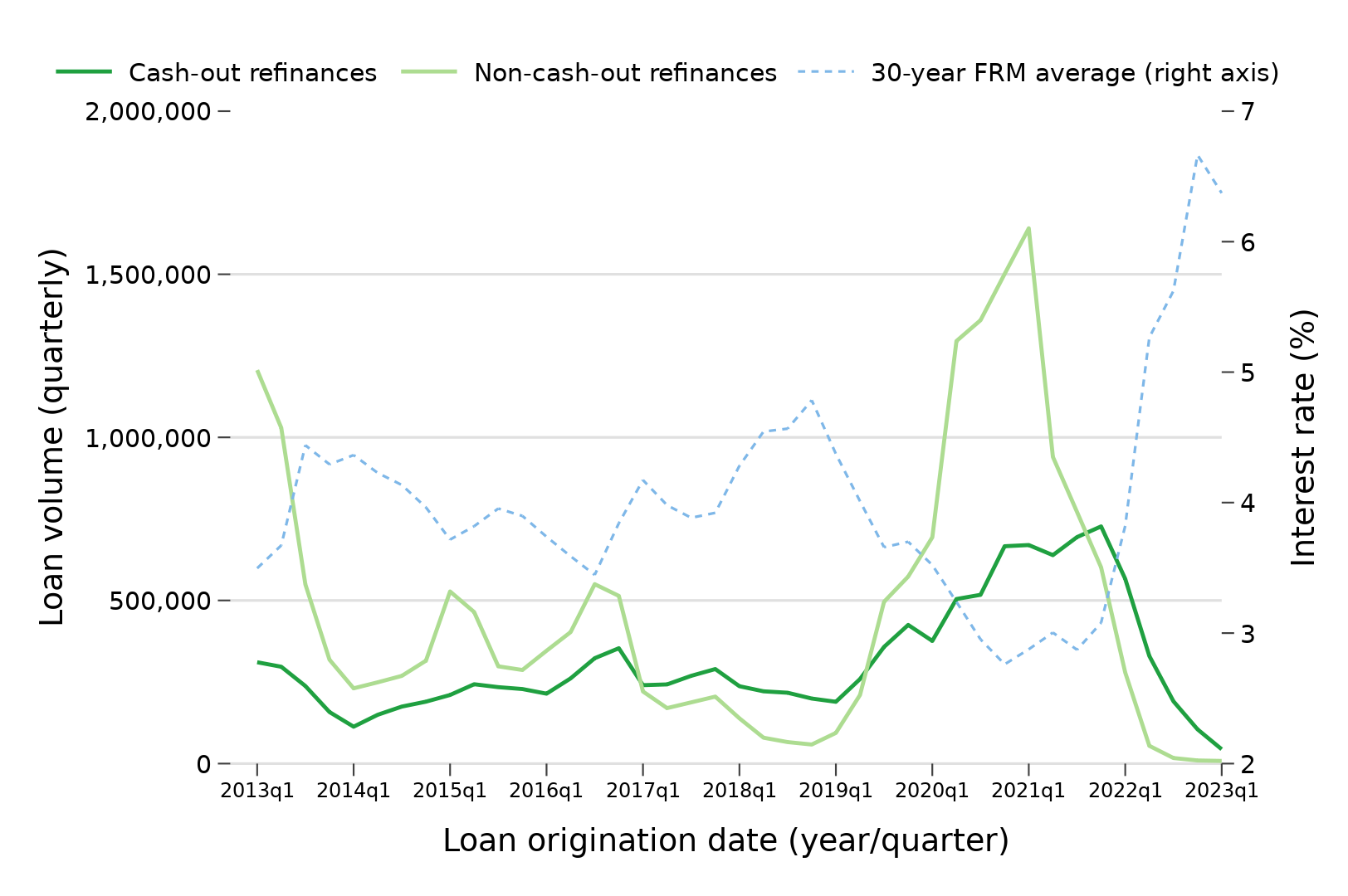

Figure 1 shows the quarterly volume of refinances, cash-out and non-cash-out, from the first quarter of 2013 through the first quarter of 2023 (the latest quarter for which we have data). We added the average interest rate on 30-year fixed-rate mortgages from Freddie Mac’s Primary Mortgage Market Survey on the right axis.

As Figure 1 indicates, non-cash-out refinances are typically more common when interest rates are decreasing and borrowers seek better rates compared to their original mortgages. Cash-out refinances make up a larger proportion of all refinances during periods when interest rates are increasing, such as 2017 to 2019 and 2022 to 2023. For example, from 2013 to 2019, cash-out refinances averaged about 240,000 originations per quarter, followed by an increase to almost 730,000 in the fourth quarter of 2021. Cash-out refinance volumes then fell throughout 2022, down to 44,000 originations in the first quarter of 2023.

Figure 1: Quarterly volume of cash-out versus non-cash-out refinances, 2013-2023

Source: National Mortgage Database

Figure 2 plots median credit scores by refinance type. The median credit scores of cash-out refinance borrowers were lower than non-cash-out refinance borrowers throughout the 2013-2023 period.

Figure 2: Median credit score at origination of cash-out versus non-cash-out refinances, 2013-2023

Source: National Mortgage Database

Figure 3 plots median combined loan-to-value ratios (100 percent less borrower equity in the house) by refinance type. The median combined loan-to-value ratios for cash-out refinances are generally similar to or lower than non-cash-out refinances originated in the same period, except during high interest-rate periods from 2017 to 2019 and 2022 to 2023, when median combined loan-to-value ratios for cash-out refinances are relatively higher than non-cash-out refinances.

Figure 3: Median combined loan-to-value ratio at origination of cash-out versus non-cash-out refinances, 2013-2023

Source: National Mortgage Database

Table 1 describes other loan and borrower characteristics of cash-out and non-cash-out refinances originated between 2013 and 2023. We see that the median loan amount and borrower incomes for cash-out refinances were smaller than for non-cash-out refinances; the primary borrowers for cash-out refinances were older; and cash-out refinances were more likely to only have female borrowers and borrowers aged 62 and older. Cash-out refinance borrowers were also more likely to be Hispanic or Black and less likely to be Asian, compared to non-cash-out refinance borrowers.

Table 1: Loan and borrower characteristics by cash-out versus non-cash-out refinances

Loan/borrower characteristics

Cash-out refinances

Non-cash-out refinances

Loan amount (median)

$198,000

$241,700

Cash-out amount (median)

$37,131

N/A

Interest rate (median)

3.62%

3.38%

Combined loan-to-value ratio (median)

70

72

Debt-to-income ratio (median)

36

34

Borrower income (median)

$84,000

$102,000

Credit score (median)

741

765

Age of primary borrower (median)

51

47

Share of refinances with only female borrowers (%)

22.8

18.8

Share of refinances with only age 62 and older borrowers (%)

21.1

15.0

Share of refinances with any Hispanic borrower (%)

10.5

9.6

Share of refinances with any Black borrower (%)

9.1

7.5

Share of refinances with any Asian borrower (%)

4.7

9.8

Share of refinances with any American Indian borrower (%)

0.7

0.5

Share of refinances with any Native Hawaiian/Pacific Islander borrower (%)

0.7

0.8

Share of refinances with any borrower listing two or more races (%)

1.9

1.7

Observations (N)

641,657

957,748

Note: Sample includes refinance mortgages that were opened between the first quarter of 2013 and the first quarter of 2023. A cash-out refinance is identified when the total value of the sampled refinance loan and their associated junior liens was more than five percent larger than its preceding loan and associated junior liens. “Only female (or only age 62 and older) borrowers” means that for loans with only one borrower, that borrower is female (or age 62 and older), and for loans with multiple co-borrowers, that all co-borrowers are female (or age 62 and older). Source: National Mortgage Database.

Delinquencies of refinanced mortgages: the importance of borrowers’ credit scores

In terms of delinquencies at the two-year mark after their refinance loan origination, Figure 4 shows two-year delinquency rates of refinances, by year originated, from 2013 to 2020. We use a broad measure of delinquency: 60 or more days past due, including other adverse conditions such as bankruptcy and foreclosure. We also split the sample by credit score: refinances with a borrower credit score at or below the median credit score of 756 at origination (left panel) compared to refinances with a borrower credit score above the median (right panel).

Figure 4: Rates of serious delinquency (60+ days or worse) two years after origination for cash-out versus non-cash-out refinance borrowers

Source: National Mortgage Database.

We first see that serious delinquencies two years after origination are rare among both types of refinances involving borrowers with higher credit scores: no higher than 0.1 percent for originations between 2013 and 2020. By contrast, serious delinquencies are more likely among refinances involving borrowers with lower credit scores but are still uncommon in absolute terms: ranging between 0.7 and 0.8 percent for all refinances originated between 2013 and 2016, followed by an increase in 2017 to 1 percent for cash-out refinances and 0.9 percent for non-cash out refinances.2 Two-year delinquency rates then fall among all refinances with lower credit scores originated after 2018, likely due to mortgage forbearance programs in the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

Worth noting is the increase in two-year delinquency rates for cash-out refinances originated in 2017. We know that these borrowers refinanced at a time when interest rates were rising (see Figure 1), and that credit scores were lower overall for cash-out borrowers in 2017 compared to previous years (see Figure 2). These findings from 2017 suggest that we may see increased delinquencies among cash-out refinance mortgages originated in 2022, another period with an increase in interest rates and a decrease in cash-out borrowers’ credit scores.

Discussion and potential concerns with cash-out refinances

In summary, during periods of rising interest rates, refinance volume declines and their composition shifts toward cash-out refinances, since homeowners may need cash from their home even when interest rates increase. From the first quarter of 2013 to the first quarter of 2023, cash-out refinances tended to have smaller loan amounts, lower borrower incomes, and lower borrower credit scores compared to non-cash-out refinances, but other loan characteristics, such as loan-to-value and debt-to-income ratios, were similar. We then showed that two-year delinquency rates were similar between both types of refinances, with only a noticeable increase for lower credit-score borrowers taking out cash-out refinances in 2017.

Prior research has focused on cash-out refinances as one of the mechanisms that exacerbated the 2008 financial crisis. However, mortgage originations from 2013 to 2023 are fundamentally different from mortgage underwriting before the financial crisis. Many risky features are now absent from the market – for example, interest-only mortgages, negative amortization mortgages, and mortgages with loan-to-value ratios over 100 percent – and lenders are now required to document borrowers’ ability to repay their loans. As we have shown above, most cash-out refinances now have loan-to-value ratios below 80 percent, requiring a 20 percent or more drop in house prices to be underwater. Most cash-out amounts are also below $50,000 during this period, and the volume of cash-out refinances has been declining each quarter since the start of 2022. Although cash-out refinances gained popularity from 2019 to 2021 due to record-low interest rates , the amount of equity extracted was lower than during the pre-2008 boom, despite home prices having increased substantially. These characteristics of cash-out refinances over the past decade suggest that cash-out refinances are now a smaller source of systemic risk than before the 2008 financial crisis.

Beyond the potential systemic risk of equity extraction contributing to a new financial crisis, cash-out refinances present at least two other concerns for borrowers. First, research from the JPMorgan Chase Institute showed that a typical cash-out refinance in their data had a longer loan term and larger monthly payment compared to the paid-off mortgage. This suggests that cash-out borrowers are more likely to still be paying off their mortgage and less likely to own their home free and clear in retirement, potentially exposing these borrowers to more future financial shocks while the mortgage is outstanding. Second, a cash-out refinance with a higher interest rate than the prior paid-off mortgage could effectively lead to much higher borrowing costs, relative to the original mortgage or to other sources of credit, like home equity loans or home equity lines of credit, that do not raise the interest rate on the existing first-lien loan balance.3 Prior research has shown that higher interest rates can cause delinquency and default.4 This relationship highlights the importance for borrowers of finding and obtaining lower interest-rate loans, and aligns with efforts to help borrowers refinance when interest rates fall as a way to avoid delinquencies.

As the interest-rate environment continues to evolve, the CFPB’s Office of Research will continue analyzing mortgage refinances and other home equity loan products to understand consumers’ borrowing decisions and loan performance.

Some Americans who are high earners, but not rich yet are opting for non-traditional mortgages.

Interest-only mortgages offer lower monthly payments, at least initially, but can be risky.

They’re best suited for buyers of higher-end property who invest their money elsewhere.

Thanks for signing up!

Access your favorite topics in a personalized feed while you’re on the go.

Advertisement

With home prices and mortgage rates sky high, potential homeowners — even those with deep pockets — are looking for ways to ease the cost burden.

Some Americans who are high earners, but not rich yet, known as HENRYs, are opting for unusual interest-only mortgages that boost affordability, at least in the short-term. These loans allow the borrower to pay just interest and none of the principal for a certain number of years. The loans are generally reserved for more affluent buyers of higher-end property who can afford a sizeable down payment and have sufficient money saved.

There are some attractive benefits of this kind of loan. They offer lower monthly payments at first, which allow borrowers to invest the money they would otherwise spend to pay off their house on other, higher-return investments. They also allow borrowers whose incomes are expected to rise in the future to buy more expensive homes than they otherwise would be able to afford.

There are also higher risks than a conventional mortgage. Borrowers won’t gain equity in their home, beyond the down payment they made. They’re on the hook for potentially higher mortgage payments in the future, and if their home value declines, they could lose the equity they have or the ability to refinance. Some interest-only loans require borrowers to pay off the entirety of the principal once the interest-only period ends.

Advertisement

When Sam, whose last name is known to Business Insider, and his wife were looking to buy a home in Brooklyn in the spring of 2022, the homes they liked largely exceeded their budget, which was between $2–$2.5 million.

But one day they got an unexpected opportunity. Their neighbors directly across the street from their rental apartment in Carroll Gardens were about to put their three-bedroom brownstone on the market. The house was exactly what they were looking for, except it was priced at $3.1 million. But their neighbors offered to sell it to them before putting it on the market. Without broker’s fees, the home would cost about $2.8 million.

Sam, a self-employed marketing consultant, was initially concerned the house was just too risky and expensive of a purchase. The future of New York City real estate was still somewhat unclear as many who fled the city when the pandemic hit were slow to return.

But when First Republic bank offered him and his wife a 40-year interest-only loan, they sprung for it. They paid a 20% down payment and locked in a low mortgage rate of between 2.6 and 2.7% for the first 10 years of the loan, and a guarantee that their rate would double at that point.

Advertisement

Their monthly, interest-only mortgage payment is just under $5,000 per month, which is just a few hundred dollars more than they were previously spending on rent.

Eighteen months later, Sam and his wife are still happy with their decision. They can easily afford their payments now, are saving up for the future rate-hike, and Brooklyn real estate is booming. The couple thinks they’ll be in the house for fifteen or twenty years, at which point their kids will be through high school and they might downsize or leave the city.

“These days, it seems like a pretty safe bet that in 10 to 20 years from now, the value will be higher,” he said. “I don’t know if it’s going to skyrocket or be a little bit higher, but we don’t think it’ll go down.”

A deal for ‘sophisticated investors’

Sam and his wife are the target demographic suitable for an interest-only loan. But these mortgages can be very risky if a borrower doesn’t have sufficient funds to handle higher payments down the line, or the property loses value, in which caseborrowers have to be prepared for potentially higher interest rates after the initial stage of their loan is over.

Advertisement

These loans are a “niche product” that should be reserved for high-end real estate purchases by borrowers who are “sophisticated investors,” said Chen Zhao, the head of economic research at Redfin. Since you’re not building equity in your home under an interest-only mortgage, those who take out these loans should be investing their money in other ways that are likely to give them a better return, Zhao said.

The proliferation of interest-only mortgages could also evenhurt buyers who can’t afford to take advantage of them. Because they allow affluentborrowers to buy more expensive homes, they can help inflate prices in already high-cost markets. Claes Bäckman, a researcher at the Leibniz Institute for Financial Research SAFE in Germany who has studied the introduction of interest-only mortgages in Denmark, says the loan type doesn’t significantly boost affordability or allow more young people to become homeowners.

“I think it will certainly help the buyers who can afford to get one of these, but if they are competing against other buyers who can also get an interest-only mortgage, they might not get much of a benefit in terms of affordability,” Bäckman said.

Renzo Salazar maintains the yard around a foreclosed home after the bank hired him to keep the home from falling into complete dilapidation on November 10, 2011 in Miami, Florida.

Joe Raedle/Getty Images

A history of predatory lending

Interest-only mortgages were much more common, especially for less-affluent borrowers, in the years leading up to the 2008 financial crisis. At the time, many homebuyers were offered risky loans they couldn’t afford, which ultimately led to the subprime mortgage crisis.

Advertisement

After the financial crisis, the federal government passed regulations on risky mortgages, making interest-only loans much less common. But with home prices soaring and interest rates stubbornly high, buyers are again opting for riskier loans, including interest-only.

Hillary, whose last name is known to Business Insider but requested partial anonymity to protect her husband’s business, and her husband were victims of these predatory lending practices. In 2007, the couple took out an interest-only mortgage to buy a $585,000 home in San Diego. The house was down the street from Hillary’s motherand the couple wanted it to be their forever home, so they splurged. While their real estate agent warned them against taking out such a large, high-interest loan, the bank encouraged them to take on two loans without any down payment — one at 8% and the other at 9% interest.

When the financial crisis hit, Hillary’s husband, a commission-based financial advisor, saw his income plummet. Hillary, a self-employed photographer, also took a hit. Then the couple had a new baby. They were soon forced to take out loans to make their $4,000 monthly mortgage payments. When they asked their bank to modify the terms of the loan, it refused. The couple declared bankruptcy and ultimately sold the house in 2012 for just $365,000.

Looking back now, Hillary thinks she and her now ex-husband were too optimistic about their future income when they bought the house, but that her bank was reckless.

Advertisement

“They clearly should never have given us a loan,” Hillary said. “But when you’re young and it’s the, quote, perfect home for you, you know, what are you supposed to do?”

She’s concerned that some buyers are now falling into a similar trap of believing they’ll be able to refinance their loans later for a better deal.

In the broader world of real estate, interest-only mortgages could be contributing to another crisis. These days, interest-only mortgages are increasingly popular among commercial real estate buyers. They made up 88% of new commercial mortgage-backed issuances in 2021 — an increase from 51% in 2013, The Wall Street Journal reported based on data from the company Trepp.

And it’s not going well for borrowers. Commercial mortgage defaults are on the rise. With interest rates so high, many office building owners aren’t able to secure new loans they can afford. In May 2023, Fitch Ratings estimated that 35% of pooled securitized commercial mortgages due between April and December of this year would be ineligible for refinancing.

Advertisement

Consumer protection advocates are are concerned that homebuyers are increasingly opting for non-traditional mortgages that carry higher risks. Some borrowers are attracted to interest-only loans by the lower monthly costs, but aren’t prepared for worst-case scenarios, and to ultimately pay more to own their home.

“It’s a question of, do people understand that this is a product that’s going to be more expensive for them long term, or are they just enticed by the lower monthly payments?” Bäckman said.

Freddie Mac Chief Richard Syron addressed homebuilders in prepared remarks at the NAMB Annual Convention in Orlando yesterday, calling the current housing correction the worst seen in our lifetime, “unless you’re over 80.”

He noted that the housing boom was initially driven by cheap home sales and steady price appreciation that eventually got out of hand, leading to unaffordable housing and the emergence of exotic loan programs designed to bring monthly mortgage payments down.

“Eventually, the market began to get ahead of itself. Prices continued to rise faster than household incomes, stretching affordability not just in high-cost markets, but in other areas of the country as well.”

“In response, there was a proliferation of new “affordability” mortgage products aimed at lowering the initial costs of financing a home. While most of these products worked reasonably well when house prices were rising, many could be dangerous if prices stagnated and began to fall.”

Think option-arms, when appreciation tamed negative amortization.

“Part of the danger was the high debt levels people took on. For example, under today’s market conditions, a 95 percent loan-to-value (LTV) mortgage originated two years ago may be effectively 110 percent LTV today. By contrast, during the boom, this same 95 percent LTV mortgage would have been down to an 80 percent LTV after two years.”

Of course that led to an eventual credit tightening, with a lack of available credit outside of prime conforming mortgages further dampening slumping homes sales and making life difficult for homeowners in higher cost markets.

“Many observers have noted that the only part of the market behaving more or less normally is the conforming market, the one in which Freddie Mac and Fannie Mae – the government-sponsored enterprises, or GSEs – primarily operate.”

“By contrast, borrowers in the jumbo market are paying up to a full percentage point more for a mortgage. That’s a record high, and about four times the normal spread.”

Syron went on to explain that the conforming loan limit increase signed into law by President Bush yesterday was a positive initiative, but one that presents a series of challenges to the GSEs.

Should be interesting to see how this plays out, and how much cheaper jumbo loans will be once the system is ironed out.

MGIC Investment Corp, the leading U.S. mortgage insurer, posted a larger-than-expected $1.47 billion fourth quarter loss as more homeowners fell behind on their mortgage payments.

The company lost $18.17 per share, much higher than the $8.13 per share analysts polled by Reuters had expected, and a far cry from profit of $121.5 million, or $1.47 per share, a year earlier.

For the entire year, MGIC lost $1.67 billion, or $20.54 per share, as claims almost quadrupled to $2.37 billion from $613.6 million.

Revenue for the fourth quarter was $399.1 million, up 8.7 percent from $367.2 million a year ago.

Net premiums written increased nearly 25 percent to $380.5 million during the quarter, up from $367.1 million in the same quarter in 2006.

New insurance written was $76.8 billion, compared to $58.2 billion in 2006, with $211.7 billion primary insurance in force at the end of 2007, compared with $176.5 billion the previous year.

MGIC said claims totaled $1.35 billion during the fourth quarter, up from $187.3 million a year earlier and $50 million more than it had estimated last month, with larger losses realized in places like Florida and California.

It also set aside $1.2 billion for losses related to securitizations and took a $33 million charge for collapsed subprime mortgage venture C-BASS.

The company also revealed that it had hired an advisor to explore ways to shore up capital, but noted that it has “adequate” capital to meet its claim obligations.

Starting March 3, MGIC will require at least 5 percent down on homes in so-called restricted markets, including entire states like Arizona, California, Florida and Nevada.

It’s been a terrible year for mortgage insurers, as both Radian and Milwaukee-based MGIC recorded their first ever quarterly losses.Shares of MGIC fell $2.07, or 14.60%, to $12.11 in early afternoon trading on Wall Street.

Mortgage insurance is typically required by mortgage lenders when the loan-to-value exceeds 80 percent.

While mortgage rates have seen some dips in recent weeks, rates are still higher than they were a year ago. And though there’s plenty of interest in homeownership, it’s still difficult for most people to afford to purchase a house.

A number of closely followed mortgage rates slumped over the last seven days. 15-year fixed and 30-year fixed mortgage rates both decreased. The average rate of the most common type of variable-rate mortgage, the 5/1 adjustable-rate mortgage, also saw rates trending downward.

High interest rates and house prices, together with limited for-sale inventory, have effectively kept a lid on homebuying demand throughout 2023. That was especially clear when mortgage rates surged past 8% in October, causing new-home sales to fall by 5.6% and existing-home sales to fall by 4.1% from the prior month.

About these rates: Like CNET, Bankrate is owned by Red Ventures. This tool features partner rates from lenders that you can use when comparing multiple mortgage rates.

Once the average rate for a 30-year fixed mortgage fell below 8% in early November, home loan applications started slowly inching up, according to the Mortgage Bankers Association. Mortgage interest rates, which are influenced by macroeconomic factors, such as inflation, job growth and the bond market, as well as investor confidence and global events, are always somewhat volatile. But experts note that changing economic conditions, particularly slowing inflation, could help mortgage rates stabilize in 2024.

Today’s average mortgage interest rates

If you’re in the market for a home, check out how today’s mortgage rates compare to last week’s. We use data collected by Bankrate to track rate changes over time. This table summarizes the average rates offered by lenders across the country:

Average mortgage interest rates

Product

Rate

Last week

Change

30-year fixed

7.32%

7.53%

-0.21

15-year fixed

6.74%

6.80%

-0.06

30-year jumbo mortgage rate

7.39%

7.59%

-0.20

30-year mortgage refinance rate

7.46%

7.63%

-0.17

Rates as of December 12, 2023.

Where mortgage rates are headed

At the start of the pandemic, mortgage rates were near record lows, around 3%. That all changed as inflation began to surge and the Federal Reserve kicked off a series of aggressive interest rate hikes, which indirectly drove up mortgage rates. Now, 20 months after the Fed’s first increase in March 2022, mortgage rates are well above 7%.

The central bank has kept interest rates steady since late July, but mortgage rates continued to climb until fairly recently. Following the Fed’s November meeting, mortgage rates dropped lower for the first time in months due to a mix of economic factors, including a shift in the 10-year Treasury yield, weaker jobs data and a better-than-expected inflation report.

Any mortgage forecast is simply an estimate, but experts say that improved inflation data and an end to the Fed’s rate-hike cycle could be signaling the start of a slow recovery in home loan rates. Most major housing authorities predict average mortgage rates to return to the 6% range around mid-2024.

“Rates will hold steady in the near term, except in the event of unexpected news or developments,” said Matt Dunbar, senior vice president of Southeast Region at Churchill Mortgage. The Fed, which is in a holding pattern to collect more data, will likely stay the course with a rate pause unless there are unwelcome surprises in the December inflation and jobs reports.

Calculate your monthly mortgage payment

Getting a mortgage should always depend on your financial situation and long-term goals. The most important thing is to make a budget and try to stay within your means. CNET’s mortgage calculator below can help homebuyers prepare for monthly mortgage payments.

What is a good loan term?

When picking a mortgage, remember to consider the loan term, or payment schedule. The most common mortgage terms are 15 years and 30 years, although 10-, 20- and 40-year mortgages also exist. Mortgages can either be fixed-rate and adjustable-rate mortgages. The interest rates in a fixed-rate mortgage are set for the duration of the loan. The interest rates for an adjustable-rate mortgage are only fixed for a certain amount of time (commonly five, seven or 10 years), after which the rate adjusts annually based on the current interest rate in the market.

When choosing between a fixed-rate and adjustable-rate mortgage, consider the length of time you plan to live in your home. If you plan on living long-term in a new house, a fixed-rate mortgage may be the better option. Fixed-rate mortgages offer more stability over time compared to adjustable-rate mortgages, but adjustable-rate mortgages may offer lower interest rates upfront. As a result, a growing share of homebuyers are leaning toward ARMs.

30-year fixed-rate mortgages

The 30-year fixed-mortgage rate average is 7.32%, which is a decrease of 21 basis points from seven days ago. (A basis point is equivalent to 0.01%.) A 30-year fixed mortgage, the most common loan term, is a good option if you’re looking to minimize your monthly payment. A 30-year fixed rate mortgage will usually have a lower monthly payment than a 15-year one, but often a higher interest rate.

15-year fixed-rate mortgages

The average rate for a 15-year, fixed mortgage is 6.74%, which is a decrease of 6 basis points from the same time last week. Though you’ll have a bigger monthly payment compared to a 30-year fixed mortgage, a 15-year loan will usually be the better deal if you can afford the monthly payments. You’ll usually be able to get a lower interest rate, pay less interest in the long run and pay off your mortgage sooner.

5/1 adjustable-rate mortgages

A 5/1 adjustable-rate mortgage has an average rate of 6.67%, a downtick of 11 basis points from the same time last week. You’ll typically get a lower interest rate (compared to a 30-year fixed mortgage) with a 5/1 ARM in the first five years of the mortgage. But you could end up paying more after that time, depending on how the rate adjusts with the market rate. For borrowers who plan to sell or refinance their house before the rate changes, an ARM could be a good option. If not, changes in the market may significantly increase your interest rate.

How to find personalized mortgage rates

You can get a personalized mortgage rate by contacting your local mortgage broker or using an online calculator. To find the best home mortgage, take into account your goals and current finances. Be sure to look at the annual percentage rate, or APR, which reflects the mortgage interest rate plus other borrowing charges. By comparing the total cost of borrowing from multiple lenders, you can make a more accurate apples-to-apples comparison.

Your specific mortgage rate will vary based on factors including your down payment, credit score, debt-to-income ratio and loan-to-value ratio. Having a higher down payment, a good credit score, a low DTI and LTV or any combination of those factors can help you get a lower interest rate.

The interest rate isn’t the only factor that affects the cost of your home. Be sure to also consider fees, closing costs, taxes and discount points. You should shop around and talk to several different lenders from local and national banks, credit unions and online lenders to find the best mortgage for you.

Though mortgage rates and home prices are high, the housing market won’t be unaffordable forever. It’s always a good time to save for a down payment and improve your credit score to help you secure a competitive mortgage rate when the time is right for you.