In the United States, it’s illegal to drive a car without car insurance. Depending on the state you’re driving in, the consequences of doing so can range from a fine to a misdemeanor on your record. So, if you’re planning on hitting the road anytime soon, be sure to purchase car insurance to avoid penalties.

In this article, we’ve researched the average cost of car insurance by state to give you a better idea of how much to budget.

Key findings:

According to AAA, the national average cost of car insurance for a full-coverage policy was $1,588 in 2022.

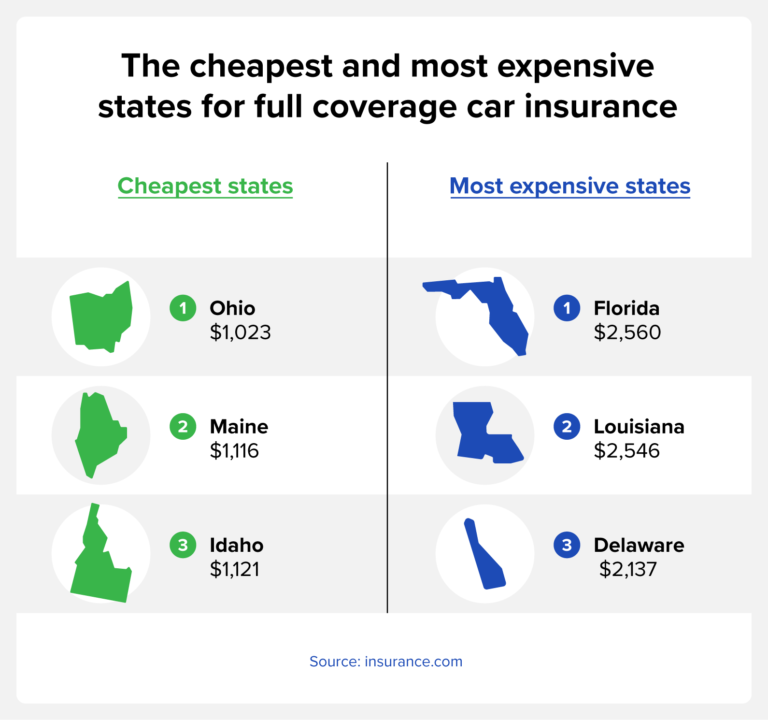

On average, the cheapest states for full coverage car insurance are Ohio, Maine and Idaho, while the most expensive states are Florida, Louisiana and Michigan.

USAA, Geico and State Farm offer the cheapest minimum coverage plans, while USAA, Geico and Nationwide offer the cheapest full-coverage insurance.

The average cost of car insurance tends to decrease with age, but starts to rise again around age 70.

Individuals with high credit scores pay lower car insurance premiums on average compared to those with poor credit.

How much is car insurance?

According to AAA, the national average cost of car insurance for a full-coverage policy was $1,588 in 2022. This figure is based on an under 65 years old driver who lives in the city or suburbs, has over six years of driving experience, and has not been involved in any accidents.

Average cost of car insurance by state

When calculating the cost of car insurance, the state you live in plays a role in how much you can expect to pay. This is because factors like population density, climate, road conditions and crime rate in your area can play a part in the likelihood that you’ll file a claim.

According to insurance.com, the cheapest states for car insurance if you’re looking for minimum coverage are Iowa, South Dakota and Wyoming costing an average of $263, $267, and $293, respectively. Meanwhile, the cheapest states for full coverage auto insurance are Ohio ($1,023), Maine ($1,116), and Idaho ($1,121).

The most expensive states for car insurance in terms of minimum coverage are New Jersey, Florida, and New York where drivers pay an average of $989, $908 and $875, respectively. For full coverage insurance, drivers in Florida ($2,560), Louisiana ($2,546), and Delaware ($2,137) pay the most in the country on average.

State

Minimum coverage

Full coverage

AK

$336

$1,359

AL

$420

$1,542

AR

$422

$1,597

AZ

$494

$1,617

CA

$582

$2,115

CO

$467

$1,940

CT

$773

$1,750

DE

$821

$2,137

FL

$908

$2,560

GA

$567

$1,647

HI

$389

$1,306

IA

$263

$1,321

ID

$326

$1,121

IL

$484

$1,578

IN

$384

$1,256

KS

$389

$1,594

KY

$717

$2,105

LA

$726

$2,546

MA

$523

$1,538

MD

$607

$1,640

ME

$330

$1,116

MI

$711

$2,133

MN

$479

$1,493

MO

$525

$2,104

MS

$434

$1,606

MT

$389

$1,692

NC

$396

$1,368

ND

$340

$1,419

NE

$350

$2,018

NH

$411

$1,307

NJ

$989

$1,901

NM

$376

$1,505

NV

$683

$2,023

NY

$875

$2,020

OH

$308

$1,023

OK

$352

$1,797

OR

$551

$1,244

PA

$398

$1,445

RI

$648

$1,845

SC

$628

$1,894

SD

$267

$1,581

TN

$368

$1,373

TX

$520

$1,875

UT

$526

$1,469

VA

$469

$1,321

VT

$306

$1,158

WA

$505

$1,371

WI

$375

$1,499

WV

$474

$1,610

WY

$293

$1,736

Average cost of insurance by company

Another factor that’s going to influence how much you can expect to pay for car insurance is the specific company you purchase your plan through.

According to U.S. News & World Report, USAA, Geico and State Farm offer the cheapest minimum coverage plans, while USAA, Geico, and Nationwide offer the least-expensive full-coverage insurance.

Farmers, Progressive, and Nationwide offer the most expensive minimum coverage rates while Allstate, Farmers, and Progressive offer the most expensive full coverage plans.

Insurance company

Minimum coverage

Full coverage

Allstate

$1,961

$2,138

American Family

$1,327

$1,388

Farmers

$1,782

$2,059

Geico

$1,064

$1,238

Nationwide

$1,347

$1,338

Progressive

$1,440

$1,650

State Farm

$1,191

$1,348

Travelers

$1,290

$1,448

USAA

$948

$1,056

Average cost of insurance by age

According to CarInsurance.com, the cost of both minimum and full coverage car insurance tends to decrease with age, as seen in the chart below. However, there is an uptick around age 70 where rates start to go back up.

Age

Minimum coverage

Full coverage

20

$1,109

$3,532

30

$539

$1,785

40

$520

$1,682

50

$496

$1,581

60

$482

$1,511

70

$554

$1,661

Average cost of insurance for young drivers

Young drivers are the most expensive age group to insure. Although there are a few exceptions, insurance rates decrease with age among young drivers.

Age

Minimum coverage

Full coverage

16

$2,402

$7,203

17

$1,971

$5,924

18

$1,706

$5,242

19

$1,234

$3,874

20

$1,109

$3,532

21

$884

$2,864

22

$794

$2,593

23

$736

$2,415

24

$690

$2,267

Average cost of insurance by credit score

According to the Insurance Information Institute, your credit score is a good indicator of how many insurance claims you’ll file. As a result, insurance companies use credit scores to determine risk, and those with a good credit score pay cheaper premiums. The Zebra found that individuals with poor credit pay approximately 114% more than those with great credit.

Credit score

Average annual rate

Very poor (300-579)

$2,887

Average (580-669)

$2,296

Good (670-739)

$1,912

Excellent (740-799)

$1,606

Exceptional (800-850)

$1,350

What factors affect your car insurance rate?

As you can see from the above charts, the cost of car insurance varies by the following factors:

Age: Typically, young drivers under the age of 25 and senior drivers over the age of 65 are charged more for car insurance.

State of residence: Since the minimum coverage required varies by state, your location is one of the factors that will influence the price.

ZIP code: In addition to your state of residence, your ZIP code will also play a role in the cost of insurance since your vehicle is more likely to be damaged in certain areas, such as ZIP codes with high crime rates. Typically, the cost of car insurance will be greater in cities than in rural areas.

Marital status: Statistically, married drivers are less risky than single drivers resulting in a lower insurance cost.

Gender: Based on risk, male teenage drivers tend to have the highest cost of car insurance of any demographic.

Credit history: Those with a low credit score tend to pay higher premiums than individuals with good credit.

Driving record: Since car insurance premiums are based on risk, individuals with a good driving record can expect to pay lower premiums, while those with a poor driving record may experience increased rates.

Car make and model: You may pay less if you drive a vehicle that insurance companies deem safe. On the other hand, you’re likely to pay more if you drive a small sports car since they pose a higher risk.

Mileage: Higher annual mileage increases the risk you’ll get into an accident and will likely raise your premiums.

High-risk violations: Driving under the influence andat-fault accidents are examples of violations that may result in you being considered a high-risk driver.

What’s the difference between full and minimum coverage?

Minimum coverage car insurance — liability coverage — is required in most states and is used if you’re at fault in an accident. This coverage will pay for damages and injuries of the other party when you’re responsible for the incident.

On the other hand, full coverage insurance, or collision coverage, includes liability coverage plus damage caused to your own vehicle. Keep in mind that lenders often require you to obtain full coverage insurance before you get an auto loan.

FAQ

Below, we’ve answered some common questions regarding the cost of auto insurance.

Can my driving record affect my car insurance rate?

Your driving record is one of the factors that affects your car insurance rate. As a result, those with traffic violations or accidents on their record can expect to pay higher premiums.

Does your car insurance cost go down after you pay off your car?

Your care insurance cost doesn’t typically go down after your pay off your car. However, you do have the option to decrease the amount of coverage on your vehicle once it’s paid off.

Which car insurance company is the cheapest?

As mentioned above, insurance companies that offer the cheapest plans include Geico, Auto-Owners, USAA and Erie.

Does car insurance decrease annually?

For young drivers in particular, car insurance rates decrease each year you renew your policy without filing a claim. You can expect to see the biggest drop in price at age 25.

The average cost of car insurance varies by factors including state, age, insurance company and credit score. Some factors, such as your age, are beyond your control, but other factors, such as your credit score, can be improved.

Check your credit score for free today to see if it’s a reason your car insurance is high.

Cyber-attacks are on the rise as hackers and criminals learn about and adapt to methods put in place by government agencies to prevent scams. The FBI’s Internet Crime Complaint Center (IC3) reported monetary losses totaling more than $1.4 billion in 2017. [1]

While anyone, regardless of age, can be a target of common money scams, many hackers specifically target seniors. Nearly 17% of reported cyber crimes in 2017 came from victims over the age of 60. And with losses of over $342 million, seniors are losing more money to scams than any other age group. [1] Considering the average age of retirement in the U.S. is 60, this trends is a serious threat to the financial security of many Americans as they enter retirement.

With an empty nest and retirement on the horizon, your senior years should be the time to pursue your passions—not get scammed out of your hard-earned savings.

This guide covers the basics of recognizing and preventing common online money scams, plus provides tips to help seniors navigate the online world safely.

Table of Contents:

Why Scammers Target Seniors

Pew Research shows that seniors are adopting technology, such as the Internet and smartphones, more than ever before. [2] If you’re among the technology adopters, you know how great technology is for connecting with your children and grandchildren who live far away and with friends you haven’t seen in years.

Con artists and scammers exploit seniors online believing that they aren’t Internet-savvy, despite many proving otherwise. Here are a few of the reasons seniors are a frequent target of scams online:

You generally have larger savings accounts and valuable assets.

You’re perceived as more trusting and polite.

You may not recognize and report the scam right away.

As you age, cognitive function and physical ability declines.

How to Recognize a Money Scam

As online scammers get increasingly sophisticated, certain types of fraud can be hard to spot even for the most adept Internet user. To keep from falling victim to scammers’ tactics, make yourself aware of common warning signs and stay vigilant. A gut feeling is always a good place to start. For example, if something feels too good to be true, it probably is. Also, if a request from someone you know feels out of character, trust your instincts and do your research before taking action.

An easy way to know if something is a likely con is to use the three U’s for identifying money scams.

Unexpected: If you receive an email from someone you trust making an unexpected or unusual request for money or personal information, contact them personally to confirm.

Urgent: If the tone of the message is threatening or asks you to act immediately, take time to think it over or tell a friend before acting. If you’re still unsure, check the IC3’s Alert Archive to see if there have been other incidents of the same scam.

Unsecure: Make sure the address bar reads “https://” and not “http://” when entering personal or financial information online. If a URL begins with “https://” that tells you the site is secure and protects information that’s transmitted. If you provide sensitive information to an unsecure site, it can easily be stolen.

Top 10 Online Scams That Affect Seniors

Scammers see senior citizens as easy victims, but you can prove them wrong by educating yourself on some of their common schemes. They often use things like healthcare, retirement savings and online dating to lure unsuspecting seniors into giving over their personal information. Here are 10 of the most common online schemes that target seniors.

1. Medicare Scams

If you’re 65 or older, you might rely on Medicare for your health coverage. Scammers know this and whenever Medicare sends out new cards or makes changes to its policies, they capitalize on opportunities to steal personal information. This can be done over the phone or by email. The scammer claims to be a Medicare representative and insists there’s a fee associated with getting you a new card or that your card has been compromised—neither of which is true.

According to Medicare.gov, “Medicare, or someone representing Medicare, will never contact you for your Medicare Number or other personal information unless you’ve given them permission in advance.”

How to protect yourself: Don’t respond to the email and mark it as junk or spam. If you need to speak with Medicare, call them directly at 1-800-MEDICARE (1-800-633-4227).

2. Health Insurance Scams

In order to make a profit, criminals may try to offer you health insurance plans that have little to no real value. In some cases, they may be selling discount cards or limited-benefit plans, but rarely explain how limited the coverage really is.

How to protect yourself: Never purchase insurance on the spot. Do your research on the company and thoroughly read the details of the coverage offered.

2. Counterfeit Medications

This scam is especially dangerous because it can cost you not only your money but your health. Prescription drugs aren’t cheap, and most seniors are dependent on a medication or two to maintain their health. Scammers exploit this by offering fake prescription medications for purchase online at a low cost. The number of counterfeit medication scams under investigation by the FDA is up four times since the 1990s. [3]

How to protect yourself: Always go through licensed medical professionals to get any prescriptions and pick up your medications at a local pharmacy. If you enjoy the convenience of ordering online, many reputable pharmacies allow you to refill your prescription online or have your medications delivered.

3. Phishing

Scammers often capitalize on your trust in people and institutions by posing as them in emails, on calls or in text messages. For example, the Social Security Scam is a form of phishing where scammers pose as government officials who need your social security information. Once they’ve gained your trust, they use that to gather personal, sensitive information like your Social Security number, bank/credit card information and/or passwords.

How to protect yourself: Always check the sender’s email address or phone number before clicking any links in emails or messages that request personal information.

4. Dating and Romance Scams

Online dating can be great for people of all ages—seniors included. But it’s important to practice the same kind of cautions online as you do in real-world dating. Online dating scams are one of the biggest and most costly scams, and scammers can break your heart and bank account if you’re not careful. It’s a red flag if someone builds a rapport with you only to turn around and ask for money. Even if the request seems heartfelt, like wanting to come see you, it could still be a play solely for money.

How to protect yourself: Take things slow, do your research and never send money to someone you don’t know personally. Even if you’ve met them, run the other way if they ask for money after you’ve known them only for a little while.

5. Investment Scams

In these cons, scammers take advantage of your need to build or maintain retirement savings. A lot of seniors are concerned about making their money last, which makes them vulnerable to ads or requests that promise high-profit, no-risk investments.

How to protect yourself: Stop and think, “Is this too good to be true?” Never accept an offer on the spot. If you’re not sure, talk it over with a trusted friend or check the IC3’s Alert Archive along with other online sources, such as the Scams and Frauds page on USA.gov.

6. Homeowner Scams

Seniors are at a point in life where they’re more likely to own their homes. While some may want to stay right where they are, others have grand dreams of moving to a new location—maybe somewhere warmer. In this scenario scammers work to identify the value of your property and then offer you a reassessment—for a fee, of course.

How to protect yourself: If you want to move, only work with a reputable realtor or go the for sale by owner route.

7. Sweepstakes and Lottery Scams

These scams use a surprise factor to trick you into thinking you need to click something to “claim a prize.” It can come as an email, a web pop up or even within a web page you’re reading.

How to protect yourself: If you receive an email that claims you’re a winner, it’s almost guaranteed to be a scam. On the off chance that you actually signed up for a sweepstakes, check your email inbox to see if you have a confirmation of your signup from the same email address. Better, yet, pick up the phone and call the company before you click on a link in an email or on a website.

8. Fake Charities

Seniors may feel more compelled to donate to those in need or contribute to disaster aid, but unfortunately fake charities often try and get donations after a natural disaster.

How to protect yourself: Do your research. Call a number to speak with someone from that charity or search the charity name and a phrase like “scam” or “fraud” in Google. You can also use the organizations listed by the FTC to research reputable charities.

9. Malware Scams

Using antivirus software is a great way to protect yourself from fraud. Unfortunately, scammers often pose as antivirus providers and instead install malware on your computer. These advertisements are often pop ups or web page ads.

How to protect yourself: Make sure anything you download to your computer is from a reputable source and never give anyone you don’t trust remote access to your computer.

10. Threats and Extortion

These types of scams utilize fear to get the desired outcome. Typically the scammer tells you that something terrible is going to happen if you don’t give them money or personal information.

How to protect yourself: Never act impulsively. Consider whether the scenario seems realistic. If you’re unsure or scared, talk to a friend. If the caller acts like a relative, hang up and call them back to ensure it is, in fact, your relative and not a stranger pretending to be your relative.

How to Protect Yourself Online

It’s good to know the basics about scams and the accompanying warning signs, but there are steps you can take to further protect your computer and online identity from fraud including. settings, tools and government resources.

Keep your firewall turned on. A firewall monitors incoming and outgoing network traffic to prevent unauthorized access to and from a private network. It protects your computer from hackers attempting to crash it or gain sensitive information.

Keep your computer’s operating system up-to-date. Make sure your computer software is up-to-date. You can usually subscribe to automatic updates online. If you keep your system updated, your computer will continue running smoothly and you’re sure to have the latest fixes for any security holes.

Turn on two-factor authentication. Two-factor authentication requires both a password and an additional piece of information to access your account. The second piece of information is typically a message sent to your phone or a code generated by an app or token.

Look out for unsecure networks and websites. If you get a warning message saying “Unsecure Wi-Fi Detected,” don’t visit any banking websites or store any passwords while on that network.Also, most browsers will warn you when you visit an unsecure site. The feature should already be enabled on most computers, but if not, make sure you enable this setting.

Install or update antivirus software. Antivirus software prevents malicious software programs from installing on your computer. Malware programs allow others to see your computer activity. Be wary of any ads on the Internet for these types of software as they are often not real solutions and instead are fraudulent.

Use a password manager. A password manager, like LastPass or Dashlane, lets you have a unique, strong password for every secure website—in other words, not your grandchild’s birth date. You won’t have to remember them all, because the password manager stores and encrypts your passwords for your protection.

Check your credit often. Major changes toyour credit can indicate potential fraud. Consider signing up for a free credit score and checking it every few weeks as a way to watch for changes.

Find Information About Active Scams

What To Do If You’re the Victim of a Scam

The best thing to do if you suspect you’ve been the victim of a scam is to report it. IC3 chief Donna Gregory says, “We want to encourage everyone who suspects they have been victimized by online fraudsters to report it to us.” IC3 receives over 800 complaints a day on average, so don’t let embarrassment keep you from reporting something.1 Reporting a scam helps law enforcement investigate similar scams and take action to bring the scammers to justice.

Steps to Take After Fraud

To report a scam, file a claim online at www.ic3.gov. You’ll be asked to provide complete information about the crime as well as any additional relevant information.

Once you’ve reported the scam to authorities, you also want to take action against any other loss. IC3 recommends that victims take actions, such as contacting banks, credit card companies and/or the credit bureaus to block accounts, freeze accounts, dispute charges or attempt to recover lost funds.

Keep a close watch on your credit reports and consider using credit monitoring tools.

In February 2018, the Justice Department made a coordinated sweep of elder fraud cases that resulted in several initiatives to reduce the number of annual cases. [4] This included building local, state and federal capacity to fight elder abuse, supporting research to improve elder abuse policy and practice, and helping older victims and their families.

Each year the number of Internet crimes increases and scammers become more sophisticated, but spreading knowledge and awareness is one of the best ways to combat the issue. Arming yourself with a basic understanding of the dangers online can help you protect yoursel f from fraud.

Additional Resources

Sources:

1 Federal Trade Commission Latest Internet Crime Report Released

2 Pew Research Center Tech Adoption Climbs Among Older Adults

3 National Council on Aging Top 10 Financial Scams Targeting Seniors

4 United States Department of Justice Justice Department Coordinates Nationwide Elder Fraud Sweep of More Than 250 Defendants

Zillow Home Loans is the direct lending arm of Zillow, the highly popular real estate listing website. The lender offers a standard lineup of purchase and refinance loans and can handle the loan process online. It may be a good fit if you have strong credit and plan to work with an affiliated real estate agent. Here’s what to know about working with Zillow Home Loans.

Zillow Home Loans overview

Zillow opened in 2006 and has since become one of most well-known marketplaces to browse real estate listings online. The company purchased Mortgage Lenders of America in 2018, then rebranded the company as Zillow Home Loans in 2019. The direct mortgage lender is headquartered in Irvine, California, and is licensed in the District of Columbia and all states except New York.

Zillow mortgage products

Zillow Home Loans offers the following types of mortgages:

Conventional purchase loans.

U.S. Department of Veterans Affairs (VA) loans.

Federal Housing Administration (FHA) loans.

Refinance loans.

Adjustable-rate mortgages.

Jumbo purchase loans up to $2.5 million.

You can choose between a fixed-rate mortgage, with terms ranging from 15 to 30 years, or an adjustable-rate mortgage (ARM), with a fixed rate for a certain amount of time. Zillow Home Loans offers ARM terms where the rate is fixed for either seven or 10 years. After the fixed period ends, the rate may reset every six months.

Borrowers also have several options if they’re looking to refinance a mortgage. Zillow Home Loans offers rate-and-term refinances, where you get a loan with new terms, and cash-out refinances, where you borrow more than your current loan balance and get the difference in cash. The lender also offers the FHA streamline refinance loan and the VA interest rate reduction refinance loan (IRRRL), both designed to speed up the refinance process.

Looking for the right home loan? Check out the best mortgage lenders

How to qualify for a Zillow Home Loans mortgage

Zillow Home Loans’ qualification requirements depend on the type of mortgage you want to get. With a conventional loan, you’ll need a minimum credit score of 620 and a maximum debt-to-income (DTI) ratio of 43%. And while your down payment can be as low as 3%, you’ll pay private mortgage insurance if it’s less than 20%.

The lender also offers jumbo mortgages, which are home loans that exceed the conforming loan limit in the county where you’re buying a home. Qualification requirements are higher for jumbo loans because they’re generally riskier for the lender. For jumbo loans, Zillow will lend up to $2.5 million and requires a minimum credit score of 700, a down payment of 20% and a maximum DTI ratio of 43%.

Borrowers can also get FHA loans through Zillow, but they’ll need a credit score of at least 620, along with a minimum down payment of 3.5%. Other lenders accept a credit score more in line with the Federal Housing Administration’s minimum of 580 or 500, depending on the borrower’s down payment. So if you’re looking for an FHA loan, you might consider working with another lender that accepts lower credit scores.

Another option with Zillow is the VA loan, available to eligible current and former service members of the armed forces and qualifying surviving spouses. These loans offer reduced closing costs and don’t require a down payment or mortgage insurance. With Zillow, you’ll need a credit score of at least 620 to qualify.

How to apply for a Zillow mortgage

The pre-approval process takes about five to 10 minutes and can be completed online or over the phone with a loan officer. Once you’re ready to submit the mortgage application, you can fill out the application online or over the phone. There are no branches to get in-person help.

To get a preapproval letter with Zillow Home Loans, you’ll need:

A recent pay stub.

A W-2 form from the most recent tax year.

Two most recent bank and investment statements.

Tax returns from the two most recent tax years.

You’ll also need these documents when applying for the mortgage. If you do the preapproval with Zillow, they’ll have everything on file when you’re ready to take the next step.

Pros of a Zillow Home Loans mortgage

Offers a post-closing rebate.

Provides a dedicated representative throughout the loan process.

Website offers solid consumer resources.

Cons of a Zillow Home Loans mortgage

No in-person branches.

Charges lender fees.

Doesn’t offer USDA loans, construction loans or home equity products.

Zillow Home Loans perks and special features

Rebate program

Zillow offers a rebate of up to $1,500 that you’ll receive after closing. To qualify, you’ll need to work with a real estate agent affiliated with the company and get the loan through Zillow Home Loans.

Helpful website

The Zillow Home Loans website offers several consumer resources, including articles that help explain mortgage topics and calculators that help you estimate your potential monthly payment. You can also get prequalified on the Zillow Home Loans website. The company will run a soft credit pull, so the prequalification won’t affect your credit. And while there are no mortgage rates on the Zillow Home Loans website, potential buyers can compare mortgage rates for different loan types on Zillow’s homepage.

How Zillow could improve

No in-person branches

Zillow Home Loans isn’t currently allowing homebuyers to visit their offices. You can apply for a mortgage and complete the underwriting process completely online, and contact your dedicated representative at any time. The online process can be helpful to some homebuyers, but if you want to visit a branch in person, you’ll need to look elsewhere.

Lender fees

For purchase and refinance mortgages, Zillow Home Loans charges a lender fee of $1,500 when borrowers apply for conventional loans, FHA loans and jumbo loans. The fee drops to $499 for VA loans. Some mortgage originators don’t charge a lender fee at all, which is why it’s important to shop around. You may even be able to negotiate with Zillow Home Loans if you find a better offer elsewhere.

Loan menu

Zillow Home Loans offers a pretty standard menu: You can apply for conventional loans, FHA loans, VA loans and jumbo loans. But you’ll need to shop with a different lender if you’re interested in a niche product, such as USDA loans, construction loans or home equity products.

Zillow Home Loans customer service and reviews

For routine questions or to get help with a loan application, you can visit Zillow Home Loans at its website or call 888-852-2212. If you have complaints or feedback, you can submit a message through an online contact form, call 877-661-3166 or send postal mail to:

Zillow Home Loans, LLC ATTN: COMPLIANCE/LEGAL DEPT. 1301 Second Avenue, 31st Floor Seattle, WA 98101

The lender also has a highly rated app, Zillow Mortgage, that’s available on iOS and Google Play. The app allows you to get a customized rate quote, calculate your estimated housing payment, get prequalified and check how much you can afford to borrow. But you won’t be able to submit a mortgage application, upload documents, and track your loan status using the app.

People who have worked with Zillow Home Loans tend to give the lender above-average ratings. As of June 2023, customers on the Better Business Bureau’s website gave the company 3.66 out of 5 stars, and Trustpilot reviewers gave the lender 4 out of 5 stars.

Positive reviews focus on strong customer service and competitive mortgage rates. However, there are some complaints regarding discrepancies in loan documents and confusion surrounding payment processing. Some customers also say they received poor customer service from loan officers.

Zillow Home Loans alternatives: Zillow vs. Rocket Mortgage vs. LoanDepot

Every mortgage lender has its own system of setting rates, qualification requirements and fees, so it’s important to shop around. According to a Consumer Financial Protection Bureau study, mortgage rates can vary by 0.5% or more for similarly qualified borrowers. That may not seem like much, but it can add up over time. For instance, say you want to get a home loan for $400,000 with a down payment of 20%, and two different lenders offer rates of 6% and 5.5%. Taking the lower rate would save you $102 a month or $36,720 over the life of the loan.

If you’re considering a mortgage with Zillow Home Loans, check out some alternatives.

Rocket Mortgage is a fully online mortgage lender that offers home loans in all 50 states and the District of Columbia. According to J.D. Power, it has earned the designation as best in customer satisfaction for the past 12 years.

LoanDepot launched in 2010 and is now the second-largest nonbank retail mortgage lender in the U.S. It earned an above-average score in the J.D. Power 2022 mortgage origination survey and offers home loans in all 50 states and the District of Columbia. Unlike Zillow Home Loans and Rocket Mortgage, applicants with loanDepot can get in-person help at branch locations or complete the mortgage process entirely online.

Frequently asked questions (FAQs)

Yes, Zillow Home Loans is a legitimate company. Zillow is also accredited with the Better Business Bureau and verified on Trustpilot.

Yes, you can get prequalified for a home loan with Zillow in about three minutes. You’ll need to answer a few questions about your purchase timeline, what you’re looking for, how much you want to spend, and details about your financial situation. The lender will run a soft credit pull that doesn’t impact your credit and then confirm whether you’re prequalified for a home loan.

Borrowers need a credit score of at least 620 to qualify for a conventional, FHA, or VA loan with Zillow Home Loans. The minimum credit score requirement increases to 700 for jumbo mortgages. The lender will also consider other factors, such as your employment status, income and debt-to-income ratio.

While full-on Crayola-like green conjures less than complimentary connotations—green with envy; green around the gills; the grass is always greener—take the hue down a notch by mixing in some gray or black and the color yields a whole different experience. Deep-green hues evoke nature in a more meditative manner. Such elements feel nearly spiritual; think of jade, pines, and seaweed. Green is the color of the outdoors and it nurtures the soul. So, pull deep green-decor into your home.

One might balk at the thought of a green dresser, but Acerbis’s Storet subtly teases color out of a rich walnut. Think of it as a functional fern in the corner of your bedroom. Astreus Clarke’s Roebling lamp is a minimalist and earthy green marble alternative to a banker’s lamp with a lollipop-green glass shade. And, it looks as home in a library as on a nightstand. Sara Hayat’s Bevel sofa is a statement piece around which one builds a room; luscious green velvet upholstery is much more inviting than gray. Dive into deep green; we consider a timeless neutral.

Acerbis back in 1994, and the 150-plus-year-old Italian furniture firm recently updated the cabinet’s wood surface. That said, its defining feature is the glossy, lacquered horizontal moldings, which come in a dozen colors both serious and playful, including dark green. $19,173

Sara Hayat scoured industry sources near and far to find a fill that would give the Bevel a bit of bounce while ensuring its cushions would retain their pebble-like shape. Indeed, each velvet-upholstered seat cradles a person perfectly. As it should: It takes the team about a month to hand-stitch this low-slung belted beauty. $28,495

Minotti who passed away in August, played with the idea of balance in the Solid Steel coffee table, despite the heavy-metal inference of its moniker. Party-ready glossy and mirrored finishes belie the architectural geometry of the streamlined, staggered slabs. Even with its fashion-forward feel (or backward: the materials reference 1970s glamour), it evokes an unflinchingly Bauhaus sensibility. Price upon request

Astraeus Clarke found inspiration in N.Y.C. The Roebling table lamp takes its form, albeit loosely, from the Brooklyn Bridge and its name from the bridge’s engineers, John A. Roebling and his wife, Emma. The lamp’s deep-green marble pillars support a gable-shaped top that hides the light source. But there’s a twist: That top segment pivots 360 degrees, allowing the user to direct illumination as needed. $12,500

New Ravenna. Duo, a waterjet mosaic, features boxy, mustard-toned cross-stitches that punctuate a large, dark grid over elegant marble with green veining. The coastal Virginia–based company replicates the texture of stone that has been well-worn by salt air, ensuring your kitchen, bath, or patio looks suitably lived-in. $229 per square foot

This correlation between the average cost of living and credit card limit continues when we look at the 10 states with the lowest average credit card limit. In the chart below, the states marked with an asterisk are also on the list of states with the lowest cost of living.

State

Average Credit Card Limit

Average Credit Score

Mississippi*

$21,676

667

Arkansas

$24,570

683

West Virginia*

$24,684

687

Alabama*

$25,621

680

Louisiana

$25,781

677

Kentucky

$25,962

692

Oklahoma*

$26,041

682

Indiana*

$26,676

699

Idaho

$26,871

711

Iowa*

$27,052

720

Source: Experian, Wisevoter

How Are Credit Card Limits Determined?

Credit card companies use several factors to determine your limit, which they review periodically over time. Some factors count more than others, varying by the credit card issuer.

Your Credit Score

A higher credit score indicates you are more likely to pay your debts, which tells credit card issuers you are lower-risk. As a result, people with higher credit scores often have higher credit card limits.

According to FICO®, a variety of factors determine credit scores, including:

Payment history: Your payment history determines 35% of your credit score, which shows how likely you are to pay your debts on time.

Credit utilization rate: Your credit utilization rate is the ratio of the debt you owe to the total amount of credit available to you. You can factor your credit utilization rate by dividing your current balance by your total credit limit and multiplying the result by 100. A healthy credit utilization rate is considered anything below 30% —any higher and potential lenders may consider you overextended.

Length of credit history: The longer your credit history, the better picture a lender has of your risk level. A short history isn’t necessarily bad unless it contains a poor payment history and high utilization rate.

Recent hard inquiries: A hard inquiry is a record of a lender checking your credit. Too many hard inquiries in a short period can lower your credit score temporarily, so experts recommend six months between hard inquiries.

Credit card companies also use your credit score to determine your interest rate, so keeping an eye on your score with free credit reports is important.

Monthly Income

Credit card issuers want to know if you have monthly income to ensure you can pay your debts. The higher your monthly income, the more likely you are to get approved for a higher credit limit.

Monthly Expenses

Credit card companies look at your total monthly expenses, especially compared to your monthly income. Generally, they’ll look at your monthly housing costs (mortgage or rent), although they may also ask for information about other regular expenses such as utilities. Your monthly expenses are then compared to your monthly income to determine your credit card limit.

High monthly expenses won’t hurt your credit card limit as long as your monthly income is high enough to cover them.

Debt-to-Income Ratio

Credit card issuers also examine your debt-to-income ratio when determining your credit card limit. Experts consider anything under 36% to be a good debt-to-income ratio for a credit card.

To calculate your DTI ratio, divide your total recurring monthly debt (mortgage, auto loan, student loans, existing credit card debt, etc.) by your gross monthly income (how much you make before taxes) and multiply the answer by 100.

Your History with the Issuer

If you already have a positive credit history with the company issuing the credit card, they may be more likely to give you a higher credit limit. However, if they feel you have too many cards or a rocky credit history with them, they may issue a lower credit limit.

The Issuer’s Credit Approval Policies

Every credit card company wants to avoid risk and crafts a specific set of policies to determine how much credit to extend to a cardholder. Its policies may consider elements not listed here or weigh factors differently than another company, which is why credit card limits are not standard across companies.

Current Economic Outlook

When the economy is healthy, credit card companies may be more open to taking risks and offer higher credit card limits. However, when the economy is uncertain, such as during the pandemic, issuers are less likely to take risks, offering lower credit card limits for new cardholders.

How to Get a Higher Credit Limit

A low credit card limit isn’t necessarily bad, but it can make getting approval for additional loans or credit challenging if your credit utilization rate is too high. It can also put large purchases, such as an appliance or unexpected car repair, out of reach.

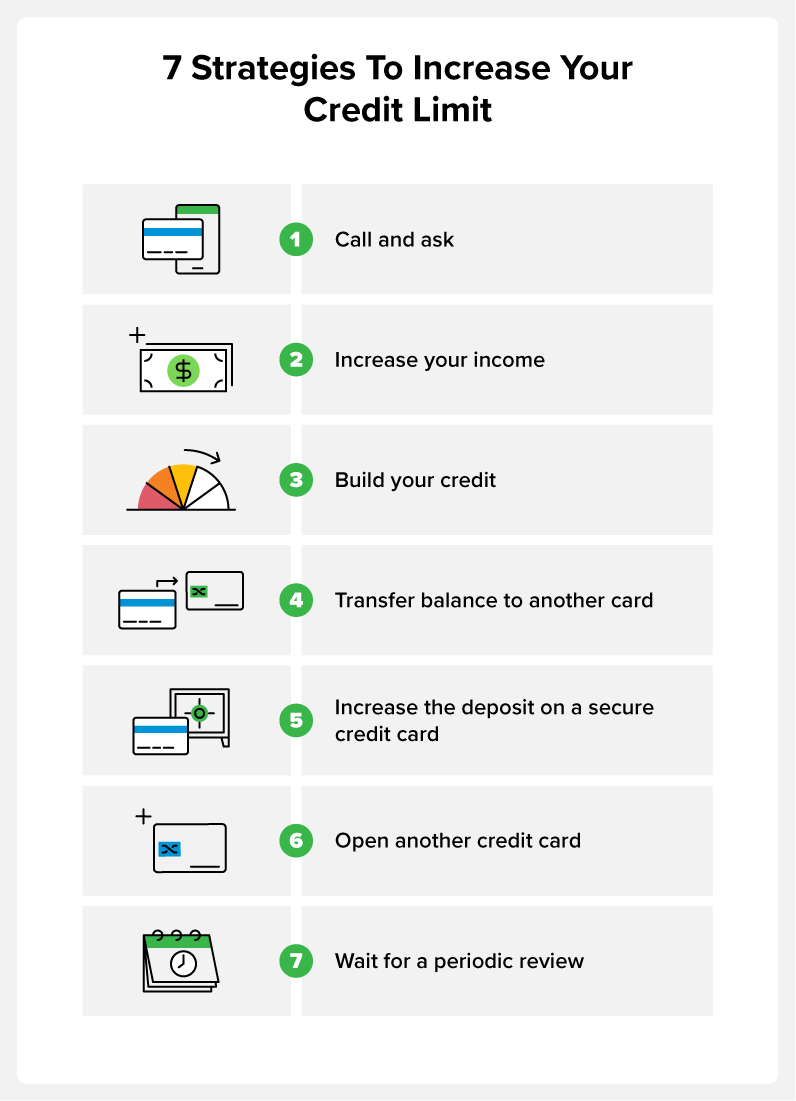

To get a higher credit card limit:

Call your credit card issuer and ask for an increase. Call the customer service number on the back of your card and ask the representative for a higher credit card limit. Only consider this if you are trying to lower your credit utilization rate to raise your credit score. They look for six months of on-time payments and will ask for updates on your annual income, employment status, and monthly expenses before deciding.

Increase your income. Since monthly income is a factor in your credit limit, increasing your monthly income can boost your credit card limit. Ask for a raise at work, get a second job, or start a side hustle. When your credit card issuer sees you have more income, they may offer you a higher credit limit. You can update this information with them anytime by contacting them directly, or you can wait until they discover it in a periodic review of your status.

Build your credit. Pay your bills on time and pay down debt to increase your credit score. Over time, your credit score should increase, which can lead your credit card issuer to raise your credit limit.

Transfer the balance from one card to another. Some credit cards allow you to transfer debt from one account to another in a credit transfer. If you have multiple credit cards and one allows credit transfers, transfer the debt from one card to another. This won’t increase your credit card limit overall, but it can increase the amount of credit available on a specific card.

Increase your deposit on a secure credit card. If your card is a secured credit card, your credit card limit directly correlates to your security deposit. Add more to your security deposit, and you’ll have a higher credit card limit.

Open another credit card. This won’t increase the credit card limit on your current card, but it will expand how much credit is available to you. Avoid temporarily dinging your credit score by waiting six months between credit card applications.

Wait. Most credit card companies annually review your account, and as long as you pay your bills on time, they can likely naturally increase your credit card limit.

You can also always pay off purchases immediately rather than waiting until the end of your payment period to gain access to more credit without increasing your credit limit.

Credit scores strongly indicate what your potential credit card limit will be, so learn more about yours today. Before applying for a new credit card, get a sense of where you stand with a credit report card. Then use the tools and features in ExtraCredit to see where you need to work toward your credit goals to qualify for a higher credit card limit.

FAQ

Here are some answers to common questions regarding credit card limits.

What Happens if I Go Over My Credit Limit?

If you try to make a purchase over your credit limit, most credit card companies will deny the transaction. Some may allow the purchase but charge a fee, although most companies have abandoned this practice.

If I Request an Increase to My Credit Limit, Will That Impact My Credit Score?

When you request an increase to your credit card limit, your credit score may drop if your credit card issuer places a hard inquiry on your credit score. This can temporarily lower your credit score, and not all credit card companies do so.

Digital mortgage automation solution provider Floify launched verification of income (VOI) and verification of employment (VOE) waterfall technology that aims to save lenders and mortgage brokers time and reduce costs during the loan origination process.

“The new VOI and VOE features in the Floify platform enable mortgage professionals to view the results of multiple verification reports from different providers, starting with the least expensive one, rather than having to run each one individually,” the company said in a release.

While running employment and income verification reports can be an expensive step in the mortgage process, it’s designed to reduce loan risk during underwriting.

“This unique technology will help our clients reduce costs, which is especially important today as verification-related fees increased significantly in the past three years,” said Sofia Rossato, Floify’s president and general manager.

As these waterfall technologies can be run within the Floify platform, clients may bypass loan origination system add-on fees that often come with enabling new features, Rossato noted.

Founded in 2013, Floify — a subsidiary of Porch Group Inc. — is a software development company that offers a digital loan origination and point-of-sale system for the mortgage industry.

The Colorado-headquartered firm was acquired by publicly traded proptech company Porch Group, Inc. in an $87 million deal in 2021.

Floify’s platform features a secure communications and document management portal and an e-signature option between lenders, borrowers, real estate agents and referral partners, according to the firm’s website.

Floify’s latest release includes a single sign-on (SSO) functionality that aims to improve security and streamline the digital loan origination process for loan officers.

By relying on a single set of trusted credentials from widely-used platforms, such as Google or Facebook, borrowers are able to streamline account creation and management when joining new applications, the company said in June at the time of the SSO launch.

The short answer is, yes, estate planning can be a smart move for everyone.

Though it’s not much fun to think about what will happen to your loved ones after you are gone, doing some estate planning early on, and readjusting it as needed throughout your lifetime, can help you prepare for the future and protect the people you care about.

One of the biggest reasons why is that without an estate plan, any assets you have may not go to the people you would have wanted to have them. And, if you have children, you won’t have a say in who becomes their guardian. Not having an estate plan can also create a lot of legal and administrative headaches for your family members and friends.

Contrary to what many people assume, you don’t have to be old, rich, or have children to benefit from making a financial plan for after you are gone.

Read on to learn what estate planning is all about and what you can do to get started.

What Is an Estate Plan?

Estate planning is deciding in advance and in writing who will get your assets and money after your death or in the event that you become incapacitated.

It can be as simple as designating certain people as your beneficiaries on your financial accounts. Estate planning also typically includes creating a will. It can also include setting up trusts and creating a living will that can be used should you ever become incapacitated.

Your “estate” is simply everything you own — money and assets, including your home and your car — at the time of your death.

Your debts are also part of your estate. Anything you owe on credit cards and loans may have to be paid off first by your estate before any further money or assets are distributed to your heirs.

Estate planning is not entirely about money, though. It may also leave instructions for how your incapacitation or death may be handled. For instance, you may not want to be kept on a life-support system if you were in a coma. You may want to be cremated instead of buried. These instructions can be included in your estate planning.

An estate plan may also include choosing a guardian for your children and any specific wishes regarding how you want them to be raised. 💡 Quick Tip: We all know it’s good to have a will in place, but who has the time? These days, you can create a complete and customized estate plan online in as little as 15 minutes.

The Importance of an Estate Plan

An estate plan can be beneficial no matter what your age, income, assets, or family status. Below are some key reasons why you may want to consider estate planning.

You Decide Where Your Assets Will Go

If you don’t have beneficiaries named in an estate plan, the courts will determine who gets your assets. That might be your closest kin (possibly someone you wouldn’t want to have your inheritance), and if you have none, the state may take those assets.

Likely you have someone who you would prefer to leave assets to, and if not, you can choose a charity.

You Have Children

If you have children, it’s important for you to consider how you want them cared for if you and your spouse were to pass away, and who you would want to be their guardians.

Your estate plan can even outline how you hope to pass on aspects of your life such as religion, education, and other values. You can also set up a trust so that your children receive an inheritance once they are 18.

It Can Help Avoid Legal Headaches

If you have beneficiaries you want to leave your assets to, having an estate plan and/or will can minimize the legal headache your loved ones have to deal with.

Without any kind of estate plan, a probate court may have to determine how assets are divided, and this can take months or years, delaying those assets making it to the people you want to have them.

It Can Help Prevent Family Conflict

Your family members may all get along well, but it’s a good idea to write a will so that things remain harmonious.

Regardless of the size of your estate, some careful estate planning can help prevent your family members from arguing over who gets what, whether it’s a small tiff or a full-on lawsuit.

It Can Ease the Financial Burden of Final Costs

Many people don’t consider planning their own funerals, and that may leave an emotional and financial burden on their loved ones.

A funeral can cost, on average, around $7,900, and a cremation about $6,900. Consider whether your loved ones would be in a financial situation to be able to afford to cover that expense, plus any others involved with your final arrangements.

Taking these final costs into consideration can be a part of your estate plan. You might decide to set aside funds to cover your funeral expenses.

You can do this with a “payable on death” account, which can be set up through your bank and allows the designated beneficiaries to receive the money in the account when you pass away.

Or, you might elect to purchase a prepaid funeral plan, which sends money directly to the funeral home to cover a casket, floral arrangements, service, and other aspects of your funeral. You may want to keep in mind, however, that prepaying for a funeral can lead to a loss of money if the funeral home goes out of business.

[embedded content]

What’s Included In an Estate Plan

While your estate plan will be unique to your own situation, there are a few things you might consider including.

A Will

Your will is the actual document that outlines who your beneficiaries are and what they will receive upon your passing. It may also identify a guardian if you have young children.

This is also where you can identify the executor, who will carry out the terms of your will.

Recommended: What Happens If You Die Without a Will?

Life Insurance Policy

Having this policy information with the rest of your estate plan makes it easy for your family to file a claim with your insurance company upon your death.

A Living Will

Death is not the only situation in which you may be unable to make a decision. You may be alive yet incapacitated, and in this scenario it can be difficult for your loved ones to know what you want them to do.

Writing a living will can be highly valuable because it lays out how you want to be treated during your end-of-life care, including specific treatments to take or refrain from taking.

A living will is often combined with a durable power of attorney, a legal document that can allow a surrogate to make decisions on behalf of the incapacitated individual.

Letter of Intent

This letter is directed to your executor, and provides instructions for carrying out your wishes in regards to your will, and possibly also funeral arrangements.

A Trust

If you have a sizable inheritance for your beneficiaries and don’t want them to have access to all the funds all at once, you can establish a trust with rules about how and when they receive the money.

For example, you could stipulate that your children receive a fixed allowance each month until they graduate college or get married, or that they use the money for college. 💡 Quick Tip: A trust is a customized estate planning tool that can be helpful for your heirs in addition to a will.

Key Account Information

You might also consider providing account numbers and passwords for bank accounts, investment accounts, and other important accounts that your family will need access to. This can make life much simpler for your loved ones.

Recommended: What Is the Difference Between Will and Estate Planning?

The Takeaway

Whether you have children and want to ensure they’re taken care of, or you’re single and would like your assets to go to certain people or a charity you care about, it’s wise to have a basic estate plan.

Having a financial plan in place in the event that you pass away or become incapacitated can protect surviving family members from unnecessary financial, legal, and emotional stress.

When you want to make things easier on your loved ones in the future, SoFi can help. We partnered with Trust & Will, the leading online estate planning platform, to give our members 15% off their trust, will, or guardianship. The forms are fast, secure, and easy to use.

Create a complete and customized estate plan in as little as 15 minutes.

Coverage and pricing is subject to eligibility and underwriting criteria.

Ladder Insurance Services, LLC (CA license # OK22568; AR license # 3000140372) distributes term life insurance products issued by multiple insurers- for further details see ladderlife.com. All insurance products are governed by the terms set forth in the applicable insurance policy. Each insurer has financial responsibility for its own products.

Ladder, SoFi and SoFi Agency are separate, independent entities and are not responsible for the financial condition, business, or legal obligations of the other, Social Finance. Inc. (SoFi) and Social Finance Life Insurance Agency, LLC (SoFi Agency) do not issue, underwrite insurance or pay claims under Ladder Life™ policies. SoFi is compensated by Ladder for each issued term life policy.

SoFi Agency and its affiliates do not guarantee the services of any insurance company.

All services from Ladder Insurance Services, LLC are their own. Once you reach Ladder, SoFi is not involved and has no control over the products or services involved. The Ladder service is limited to documents and does not provide legal advice. Individual circumstances are unique and using documents provided is not a substitute for obtaining legal advice.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

According to the Federal Reserve, consumer debt in the United States in the second quarter of 2021 totaled more than $4.2 billion. So if you’re struggling with debt, you’re definitely not alone. If you’re looking for a way to dig yourself out of debt, a debt consolidation loan could help.

But what is a debt consolidation loan? Find out if it’s the right option for you by learning more about it, including pros and cons. You’ll also find information about other alternatives.

In This Piece

What Is Debt Consolidation?

Debt consolidation occurs when you bring multiple existing debts under a single umbrella. This usually means you use some type of credit or other financial tool to convert multiple debts into a single debt. Debt consolidation loans are one of the most popular ways to consolidate debt.

What Is a Debt Consolidation Loan?

A debt consolidation loan consolidates, or combines, your various debts under a single account.

Pros of Debt Consolidation Loans

Cons of Debt Consolidation Loans

Potentially lower interest rates, especially if you now have the credit score to consolidate high-interest loans under better terms

May require good credit to obtain or get a good rate

A single payment, making it easier to manage your finances

Might leave paid-off credit card and other revolving accounts open, creating an opportunity to run up even more debt than you started with

Your debt possibly spreading out over a greater amount of time, making each monthly payment more affordable

Could potentially temporarily impact your credit score if it involves closing a lot of other accounts

What’s the Difference Between Debt Consolidation and a Personal Loan?

A personal loan is an unsecured loan that you can use for just about anything. In some cases, you could use the funds from a personal loan to consolidate some debts, making it a debt consolidation loan.

However, a loan specifically for the purpose of debt consolidation may be handled a bit differently. For example, in some cases, the lender may not pay the money directly to you. They might pay off your debts directly instead.

Alternatives to Debt Consolidation Loans

Your options depend on your credit, existing assets, and how much debt you want to consolidate. Some alternatives to debt consolidation loans are highlighted below.

1. Refinance Your Mortgage If You Have Equity

If you have equity in your home, you can refinance it or take out a home equity line of credit, or HELOC. These options give you cash you can use to pay down debt.

Pros of Refinancing a Mortgage to Consolidate Debt

Cons of Refinancing a Mortgage to Consolidate Debt

Home equity loans and HELOCs tend to have much lower interest rates than personal loans and credit cards

You use your home as collateral for the debt, which means if you don’t pay it, the lender has a claim on your house

You may be able to deduct interest on home loans to reduce tax burdens

Variable-rate loans could come with increased interest in the future

The total number of payments you need to manage each month is substantially reduced

Credit cards you pay off could be run up again, leaving you with more debt than you started with

You’re less likely to forget to pay a debt related to your home

Tip: Don’t pocket the money that refinancing frees up every month. Instead, use it to create an emergency fund. Once that’s set up, use the money as prepayment against your home loan or to boost retirement savings.

2. Use a Balance Transfer Card

Apply for a balance transfer card if your credit is in good shape, or call a card provider to ask if they’d be interested in offering you a balance transfer option on an existing card. This lets you transfer higher-interest credit card debt to a card with lower interest rates. Some balance transfer cards offer 0% APR for six to eighteen months on balance transfers for new account holders.

Pros of Balance Transfer Cards for Debt Consolidation

Cons of Balance Transfer Cards for Debt Consolidation

Can substantially reduce the cost of credit card debt

Balance transfers usually come with fees of 3% to 5%—still less than your typical interest costs might be on high-interest credit card debt, but something to keep in mind

Makes it easier to pay off credit card debt

It can be tempting to use your old credit cards again, running up more debt and ending up with double the debt you started with

Might let you consolidate multiple cards into a single account for easier management

If you don’t pay off the debt in the introductory period, you could end up with expensive interest fees

Tip: Keep your old credit card accounts open for extra benefits to your credit score. It helps your credit utilization rates and credit age. But avoid using those accounts unless you have the money to pay them immediately.

3. Borrow from Retirement Savings

If you have retirement savings, you might be able to borrow from it to pay off debt. Remember, though, that you’ll need that money later. Only consider this option if you can pay back the money quickly so you don’t lose time building your retirement funds.

Pros of Borrowing From Retirement Savings for Debt Consolidation

Cons of Borrowing From Retirement Savings for Debt Consolidation

Doesn’t require a credit check, so you don’t need a healthy credit file

You might owe taxes and penalties on the money if you withdraw early from your retirement

Interest rates are low, and you’re actually paying it back to your own account

You can borrow against some employer-sponsored retirement plans, but debt consolidation might not be an allowed reason

You could reduce how much money you have in retirement, especially if you can’t pay back the money

Tip: Consider this option as a last resort loan or if you have some money coming in soon, such as from a tax return. If you can pay the money back within a month or two, you don’t have as much to lose.

4. Ask a Friend or Relative for a Loan

If you know someone who has some extra money, it might be worth asking them for a loan at a low interest rate. You can use the money to pay off your debts and make one monthly payment to the person in question.

Pros of Asking Someone for a Loan for Debt Consolidation

Cons of Asking Someone for a Loan for Debt Consolidation

No credit check or requirements

If you blow it, you might ruin an important relationship

Your family member or friend can earn some interest

The IRS can be a real pain when it comes to family loans, so consult a tax professional

Loan payments won’t be reported to your credit reports or potentially help your score

Tip: Treat the transaction as you would with a bank or other lender. Put everything in writing, agree to fees or penalties if you miss payments, and strive to make timely payments.

5. Try Debt Counseling

Debt or credit counseling with a reputable organization can help you create a viable personal budget and potentially negotiate with creditors for better terms. Debt counselors may help you understand how to better manage your income and expenses and leverage debt payoff strategies to get out from under your debt.

Pros of Debt Counseling

Cons of Debt Counseling

Can provide you with some tools to better manage debt

May not reduce the overall cost of your debt

May help you see solutions that you didn’t see before

May rely on you making personal sacrifices in your budget

Helps you pay off debt with your own resources, which can be satisfying

If you don’t work with a reputable organization, you might be scammed out of large fees with promises that the company can’t keep

Tip: Don’t work with debt counseling companies that offer 100% guarantees to reduce or wipe out your debt or that charge excessive fees. These are red flags that could point to scams.

6. Enter a Creditor Assistance Program

Many creditors have assistance programs to help account holders who are experiencing financial distress due to sudden loss of income or an emergency. These programs range from mortgage modifications, which might reduce your interest rate or total monthly payment, to skipping a single payment and having it added onto the end of the loan penalty-free.

Pros of Creditor Assistance Program

Cons of Creditor Assistance Programs

May not require good credit, especially if you have a solid payment history with the creditor

Aren’t always available

Could offer a fast, convenient solution to short-term cashflow issues

You can typically only take advantage of these tools once or once every so often

Tip: Anytime you’re experiencing financial distress or might be late with a payment, don’t ignore the issue. Call your creditor to find out what they might be able to do to help.

7. Bankruptcy

Bankruptcy is a last-resort option that can help you discharge or restructure your debts and make a new start in a few years.

Pros of Bankruptcy

Cons of Bankruptcy

If successful, you can have all or many of your debts discharged

Bankruptcy can be a long and stressful process

You may be able to keep certain assets, such as your home or car

It can dramatically impact your credit in the short term

Filing for bankruptcy establishes an automatic stay, so creditors can’t continue to attempt to collect or foreclose unless the bankruptcy is dismissed

Depending on what type of bankruptcy you file, you may not be able to get credit for a while

Tip: Talk to a bankruptcy attorney about this option before you take action. Most provide free consultations to help you understand if bankruptcy is a good choice for you.

The Bottom Line on Debt Consolidation

If you’re struggling with debt, you’re not alone. And you do have options. Look into a debt consolidation loan or one of the options above to start working on financial stability for the future.

Nobody wants to think about dying, which is why many people actively avoid planning for their death. Creating a will, buying life insurance, making funeral arrangements—none of these are fun Friday night activities. Not only can it be unpleasant to think about, but life insurance can also be incredibly difficult to figure out. In fact, only 57% of Americans have life insurance.

Part of a new trend of online companies offering life insurance, Bestow breaks down a sometimes complicated topic so you can easily apply for term life insurance to better help your family plan for the future.

About Bestow

Bestow makes the life insurance

application process easy. You can get a quote in seconds—and coverage in

minutes—when you apply online.

It offers 10- and 20-year term life insurance policies with coverage from $50,000 up to $1 million. Premiums are as low as $8 per month—and they never change throughout the life of the policy, so you’ll always know what to budget for. One of the biggest benefits of Bestow is that it doesn’t require a medical exam as part of the application process.

Insurance companies can be notorious for being stuffy. Lucky for you,

Bestow is technically a life insurance agent: it acts as an intermediary

between you and the insurance provider. Bestow

works specifically with North American Company for Life and Health Insurance®, a well-established life insurance company. So even

though Bestow is new, you don’t have to worry about your policy. Bestow makes

the application process simple, while North American

Company for Life and Health Insurance® issues the policies, plus processes and pays claims.

Who Can Use Bestow

According to the website, you need to be

between 21 and 55 years old, have never had a felony charge, and be generally

in “good health” to qualify for a policy offered by Bestow.

It doesn’t clarify what “good health” means, but the application process asks

questions about your medical history, lifestyle and hobbies. Bestow also says they will

not be able to extend coverage if you have been diagnosed or treated for cancer

in the past ten years. As of publication, 20-year policies are only available

to individuals younger than 45.

Bestow is currently available in every state except New York.

Application Process

Bestow uses data points and artificial

intelligence to determine premiums and coverage. Unlike many other companies that offer life insurance, Bestow does not

require a medical exam for coverage.

The application process pulls available data about you—such as prescription and credit history, driving records, and prior insurance applications—to make a decision.

To start, you’ll need to provide your

name, gender, birth date, height, weight, and state, as well as whether you use

nicotine. That’s all you need to get your free quote! If you like what you see,

you can create an account and answer a few more in-depth questions about your

health and lifestyle, including citizenship, employment, HIV status, and

disability. After you provide your Social Security number and sign, you’ll get your approval and final premium. Your final

number may be higher than your quote based on your health and lifestyle.

You also get a 30-day free “look” period:

you can cancel for a full refund within the first 30 days of purchasing.

Coverage continues through a 60-day grace period from the date of your last

payment.

Making Claims

Your beneficiaries can start the claim

process simply online as well. After you initiate a claim with Bestow, the

claim is processed by its insurance provider, North American Company for Life and Health Insurance®.

The beneficiary will need to provide information about themselves as well as

information about the insured person—including the original policy number.

After that, you’ll receive a claimant’s packet and will be required to fill out

more paperwork. If there is no dispute, your claim should be processed within

ten days.

Term Life vs. Whole Life

Bestow offers only term life insurance

policies. If you’re interested in a whole life insurance policy, you’ll need to

look elsewhere.

Term life insurance lasts only as long as

the policy, making it a good choice for people who want to cover a specific

time in their life—the length of their mortgage, or while their children are

still dependents living at home, for example. Because these policies do not

last as long, they tend to be less expensive than whole life policies.

Benefits of Bestow

So you’ve spent your Friday night

deciding you want to get life insurance.

Congratulations! Why should you choose Bestow? Here are some reasons why you

might:

No medical exam required

Low premiums

Easy application

As with everything, though, there are

some downsides to getting a policy through Bestow:

No whole life policies available

Relatively low coverage capped at $1 million

Not available to people over 55

Why Get Life Insurance

If you have dependents—people who depend on your income, like your children, spouse, or older parents—life insurance is a way to help ensure that they will be covered should something happen to you. If you’re ready for a free quote from Bestow, check it out now!

With most of the year under our belt, the holiday season is just around the corner. No matter what you celebrate, this season is full of food, celebrating and spending time with loved ones.

While you’re hard at work prepping for the holiday season, scammers are too. A survey conducted by Experian found that a full 1 in 4. Americans have been a victim of identity theft or fraud in the holiday season. If you’re worried about scammers this year, don’t worry—we’ve got tips on how to look for holiday shopping scams this season.

When the pandemic hit in early 2020, COVID-19 scams became a popular method for criminals to get access to your information and steal your identity. However, the holidays are when these scammers go into overdrive, meaning it’s important to be extra cautious as you do your online shopping and holiday giving. Here are some of the most common holiday shopping scams to be aware of.

Illegitimate Charities

Many people use the holidays as a reason to be a bit more generous, but be careful before you make that donation. Many scammers create fake charities in an attempt to get you to donate. They get your money—and possibly access to your identity info—and no good ever comes from that generosity.

Check for social media presence, news stories, financial records and proof that any charity you’re considering donating to actually exists and has a good reputation.

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

Fake Online Stores

Online shopping is a convenient way to check off all the items on your list without having to actually brave the holiday crowds. However, it’s important to ensure that the sites you’re shopping from are actually legitimate. Scammers create fake online storefronts—sometimes even mimicking well-known retailers—and you don’t know it’s fake until the merchandise never comes or you start seeing evidence of identity fraud.

Empty Gift Cards

Gift cards are the perfect choice if you’re not sure what someone on your gift-giving list wants or if they like to pick out items themselves. But selling gift cards that have a $0 balance or have already expired is a common and remarkably easy scam. This happens most often on local sales sites, such as Craigslist and Facebook Marketplace.

Email Scams

Have you ever gotten an email about something you bought online—but you never actually purchased anything from that retailer? Maybe the email said you needed to reset your password or gave you a link to track your package. These are phishing email scams designed to get you to enter your personal info so scammers can use it for identity theft.

Shipping Problems

One of the biggest worries that comes with online shopping—especially with the supply chain issues that have come as a result of the COVID-19 pandemic—is whether the gifts will arrive on time. Criminals capitalize on this fear by sending out emails, texts and other communications letting you know there’s been an issue with your package. You’re asked to provide personal information such as your address, credit card info and birth date to confirm your order, but all you’re really doing is giving scammers the information they need to steal your identity.

While the holidays are a common time for shopping scams, it doesn’t mean there’s nothing you can do about it. Learn what to look for and how to protect yourself from identity theft with these tips.

1. Pay Attention to Website URLs

Online searches can lead you to scammer-run websites that unleash computer malware or collect credit card numbers for identity theft. Carefully read website domain names. Watch for unfamiliar vendors or missing letters, misspellings or other tweaks to the name of a legitimate company. Pay special attention to the last letters. For example, tiffanyco.mn indicates a Mongolia-based website, not the legitimate website for Tiffany & Co., tiffany.com.

2. Make Sure the Site Is Legitimate

Before ordering, check the “Contact Us” page for a phone number and physical address and the “Terms and Conditions” link detailing return policies and such. Unlike legitimate vendors, bogus websites are less likely to post these—or they’ll provide them in a suspicious manner, such as via a faxed request only.