As home affordability decreased, sellers reduced asking prices more frequentlythis September, with the pace coming in above typical seasonal patterns.

Approximately 6.5% of homes on the market saw asking prices reduced during the four-week period ending Sept. 27, according to new research from Redfin. The rate corresponds to approximately one in 15 properties on the market and represents an increase from 5.8% a month earlier. That is a sharp rise from what has been reported in past years over the same time frame, the real estate brokerage said.

The uptick in price cuts comes as low inventory and rising interest rates take a bite out of affordability, according to several recent reports. Conditions contributing to the current state of the market appear set to continue leaving their mark on affordability over the next several months, leading analysts said at this week’s Digital Mortgage conference in Las Vegas.

Redfin found the median sales price rose 3.1% year-over-year, coming in at $372,500, even with “relatively low” demand. A recent rise in the volume of new listings, also atypical for the time of year, is giving home shoppers more leverage.

“Buyers are using things like inspection negotiations and high insurance premiums to back out of deals,” said Heather Kruayai, a Redfin agent in Jacksonville, Florida, in a press release. “They’re holding a lot of the cards; today’s sellers need to concede on some details to close the deal.”

The latest affordability data from the Mortgage Bankers Association offers few signs of improvement for aspiring homeowners. In its monthly purchase-applications payment index released this week, the trade group reported the average monthly amount applied for by new home buyers increasing by a fraction to $2,170 in August, from $2,162 in both June and July. The current figure is higher by 18% compared to the mean level of a year ago — $1,839.

“Prospective homebuyers’ budgets continue to be impacted by the combination of high home prices and mortgage rates that remain higher than 7%,” said Edward Seiler, MBA’s associate vice president, housing economics, and executive director, Research Institute for Housing America.

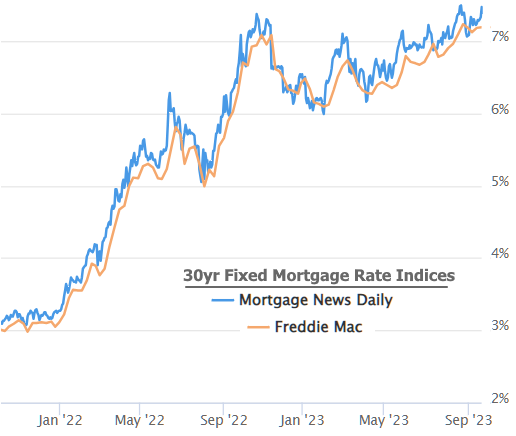

The latest PAPI report does not factor in September’s surge in mortgage rates, with the 30-year conforming average landing at 7.41% at the end of last week among MBA members — the highest point since late 2000. Similarly, Freddie Mac reported a consistent rise in the 30-year rate throughout September after a pullback in August.

Within individual segments, borrowers of Federal Housing Administration-backed mortgages saw their average payment hit a record of $1,901, jumping 2.5% from $1,854 in July and 29.4% from $1,469 in August 2022.

But even with the overall PAPI increase, conventional-loan borrowers saw a fall in the mean to $2,187 from $2,197 between July and August. But the number was still well above $1,901 a year ago.

The MBA’s national payments index for new purchase applications inched up 0.4% to a reading of 175.4 in August compared to 174.7 a month earlier. An increase in the number reflects declining affordability. Strong income earnings of over 4% over the past 12 months helped offset the steep climb upward in payment amounts.

The states showing the smallest degree of affordability were concentrated in the Western U.S., according to the MBA. Idaho led the country with a PAPI score of 269.6, followed by Nevada and Arizona at 265.7 and 238.6.

It depends quite a bit on the lender in question, but at some point between yesterday morning and this morning, the average lender dropped rates at the fastest single-day pace in months. Before you get excited, there’s a catch–two or three of them actually.

The first catch is that some lenders split that improvement between yesterday afternoon and this morning. The more general catch is that these sorts of “biggest drop in a long time” observations are almost always seen after rates have just surged to “the highest levels in a long time.” That’s absolutely the case this time around.

The third catch isn’t too important. It involves a bit of deterioration in the bond market resulting in some lenders bumping rates slightly higher this afternoon. The average lender is still in much better shape than yesterday morning (and much worse shape than most any other morning going back to June 2001).

Moving on from “catches” to plain old frustrating uncertainty, mortgage rates need new economic data in order to improve. Specifically, rates would need to see less resilience and growth in the economy. Frustratingly, the government shutdown (which looks likely if not certain as of this writing) would prevent several of the most important reports from coming out next week.

Granted, if those reports had come out strong, they would push rates higher, but as it stands, we don’t even have an opportunity for meaningful improvement.

It’s looking more likely that there will be a government shutdown beginning October 1st, which begs the question, what happens to mortgage rates?

Do they go up even more, do they fall, or do they do nothing at all?

At first glance, you might think that they’d rise because of the uncertainty involved with a shutdown.

After all, if no one is quite sure of the outcome, or duration, banks and lenders might price their rates defensively.

That way they don’t get burned if rates shoot higher. But history seems to tell a different story.

Bond Yields Tend to Fall During Government Shutdowns

As a quick refresher, mortgage rates track 10-year bond yields pretty consistently. So if the 10-year yield falls, long-term 30-year fixed rates often fall as well.

Conversely, if 10-year yields rise, which they have quite a bit lately, mortgage rates also increase.

The 10-year yield began 2022 at around 1.80 and is around 4.60 today. Since that time, the 30-year fixed has climbed from roughly 3% to 7.5%.

So there’s a pretty strong correlation between the two, though the spread between them has widened over the past couple years as well.

Since mortgage bonds are inherently riskier than government bonds, there’s a premium, or spread that must be paid to investors.

You used to be able to price the 30-year fixed mortgage at about 170 basis points above the 10-year yield. Today it might be closer to 275 bps or even more.

Anyway, the 10-year yield seems to fall during government shutdowns because of the old flight to safety.

And here’s what Morgan Stanley had to say on the matter: “On average, during shutdowns since 1976, the 10-year Treasury yield has fallen 0.59% while its price has ticked up, suggesting that investors favor the safe-haven asset during these periods of uncertainty.”

In other words, if the 10-year yield falls during the shutdown, 30-year mortgage rates should also drift lower.

How much lower is another question, but if they continue to track the 10-year yields, a .50 drop in Treasuries might result in a .25% drop in mortgage rates.

Did Mortgage Rates Fall During Prior Government Shutdowns?

Now let’s look at some data to see if mortgage rates actually fall when the government shuts down.

The most recent government shutdown took place from December 21st, 2018 until January 25th, 2019.

It was the longest shutdown in history, lasting 34 days. There was one in early 2018, but it only lasted two days.

I did a little research using Freddie Mac mortgage rate data and found that the 30-year fixed averaged 4.62% during the week ending December 20th, 2018.

And it averaged 4.46% during the week ending January 31st, 2019.

Of course, the shutdown drama started earlier in the month of December 2018 when the 30-year fixed was priced closer to 4.75%.

So if we factor all that in, you might be looking at a 30-basis point improvement in mortgage rates.

Prior to that shutdown was the one that occurred on September 30th, 2013 and lasted 16 days.

The 30-year fixed averaged 4.32% during the week ending September 26th, 2013, and fell to 4.28% during the week ending October 17th, 2013.

Not much movement there, but it did continue to drift lower in following weeks and ended October at 4.10%.

You then need to go all the way back to December 15th, 1995 to get another shutdown, which took place under President Clinton.

It lasted 21 days, ending during the first week of 1996. During that time, the 30-year fixed fell from around 7.15% to 7.02%, per Freddie Mac.

Prior to these shutdowns, most only lasted a few days and thus probably didn’t have much of an impact, at least directly.

All in all, mortgage rates did improve each time, though not necessarily by a huge margin. Still, any .125% or .25% improvement in pricing is welcomed right now.

A Lack of Data Makes It a Guessing Game

If the government does in fact shut down this coming week, it’ll mean that certain data reports won’t get released.

This means we won’t see the Employment Situation, scheduled for next Friday, nor will we see CPI report the following week.

There are many other reports that also won’t be released between this time and beyond, depending on how long the shutdown goes on.

As such, we’ll all be flying in the dark in terms of knowing the state of the economy. And the direction of inflation, which has been top of mind lately.

The good news is the Fed’s preferred inflation gauge, the personal consumption expenditures price index (PCE), already came out.

And it was weaker than expected. Prior to that report, we were getting some signs that the economy was still running too hot.

So the timing might work here in terms of higher bond prices and lower yields, which in turn would drive mortgage rates down too.

After all, our last piece of information was that inflation and consumer spending rose less than expected, which is good for rates.

Read more: How the Government Shutdown Affects Various Types of Mortgages

When you’re looking to purchase your first home, it’s a good idea to familiarize yourself with the different first-time homebuyer programs available in your area. They can help you afford this major purchase.

First-Time Homebuyer Programs

Programs vary in terms of their eligibility requirements and the types of assistance they offer, but all offer some form of financial aid. But what are these programs, and how do they work? Here’s what you need to know.

What Is a First-Time Homebuyer Program?

A first-time homebuyer program is a government-sponsored program designed to help people purchase their first home. Programs vary from state to state, but generally, they offer financial assistance in the form of low-interest rates, down payment assistance, and other incentives.

A few examples include:

The Federal Housing Administration (FHA)

The Veterans Affairs Homebuyer Assistance Program

The National Association of Realtors® (NAR)® Homebuyer Assistance Program

State-sponsored programs, such as the California New Home Grant Program, can also offer assistance.

Who Is Eligible for a First-Time Homebuyer Program?

Each program has its own eligibility requirements, which vary depending on the program and the state in which it is located.

However, generally speaking, you’re eligible if you purchase your first home and meet the criteria set by the program. These criteria can range from being newly divorced, a military veteran, or widowed to having a low income and getting ready to buy your first home. You may be eligible for other programs if you’ve already owned a home. Still, first-time homebuyer programs will automatically disqualify applicants attempting to purchase second homes or investment properties.

Get matched with a personal

loan that’s right for you today.

Learn

more

Related read: What Credit Score Do I Need to Buy a House?

How Do First-Time Homebuyer Programs Work?

Once you’ve determined that you’re eligible for a first-time homebuyer program, the next step is to find a program compatible with your needs. Programs typically offer a variety of incentives, such as low-interest rates or down payment assistance, to help you purchase your home. Once you have found a program you’re eligible for, you’ll need to submit an application and meet eligibility requirements.

Once you have been accepted into the program and met eligibility requirements, you’ll need to begin preparations for your home purchase. This may include searching for a qualifying home and making any necessary financial commitments. Finally, once all of the paperwork has been completed, and your financing has been approved, you can go ahead and purchase your home.

How Can I Use a First-Time Homebuyer Program?

There’s no one definitive answer to this question, as each program has different requirements and guidelines. However, if you’re approved for financial assistance, then the money will be given to help you purchase a home. Typically, these programs aren’t for rehabbing a home or house flipping. If you need help making repairs, consider instead getting a personal loan to finance home improvement. You’ll have a higher likelihood of getting approved for help covering repairs than a homebuyer’s program would offer.

The Bottom Line

A first-time homebuyer program can help you get into the market quickly and easily. They offer many benefits, including reduced interest rates and fees, waived closing costs, etc.

Medical debt can impact your credit score through either your length of credit history or your payment history, depending on the rest of your credit. Learn more about how exactly it can do that below.

In This Piece

Updates to Medical Debt Collections as of 2022

If you currently have unpaid medical debt, you’ll be happy to learn that there have been changes to the way this debt is recorded on credit reports. The three main credit reporting agencies, TransUnion, Equifax and Experian, are changing the way they handle medical debt.

Paid medical debt doesn’t stay on your reports. Perhaps the biggest change comes with how medical debt is reported once you pay it off. Starting July 1, 2022, all three credit reporting agencies no longer include paid medical debt on individual credit reports. Prior to this change, any medical debt would have remained on your credit report for up to 7 years. After July 1, 2022, any medical debt will be removed from your credit report as soon as it’s paid in full.

New medical debt won’t show up on your reports for a year. These credit reporting agencies are also giving consumers more time to pay off their medical debt. Previously, medical debt that was at least 6 months past due could be part of your credit report. However, the new changes push this waiting period up to 1 year. Thanks to this change, you now have 1 full year to pay off any medical debt or enter into a payment plan agreement before it impacts your credit report.

(2023) Bills under $500 will not appear on your credit reports. The third credit reporting agencies medical debt change takes effect in 2023 and involves health care bills under $500. The credit reporting agencies have agreed not to include unpaid medical debt under $500 on credit reports. The Consumer Financial Protection Bureau estimates that this change could impact two-thirds of all unpaid medical debt reported on credit reports.

It’s important to note that this change doesn’t relieve you from paying your medical debt. You still owe these medical bills, and medical debt collectors can still contact you. It only means this debt will no longer be part of your credit report. Medical organizations and collection agencies can still take other actions, such as court action, if you fail to pay this debt.

These changes could mean a significant improvement in your overall credit score. This is especially true if you currently have paid or unpaid medical debt on your credit report. The new changes may also hurt some consumers.

If medical debt is the only thing listed on your credit report, its removal could result in an unscorable credit score. This only happens when there isn’t enough information on your credit report to determine an accurate credit score.

What Impact Will Medical Debt Have on My Credit?

Medical debt listed on your credit report has a direct impact on your credit score. In fact, your payment history accounts for as much as 35% of your overall credit score. In the past, many credit score models treated medical debt just like all other forms of debt. In this scenario, medical debt could significantly lower your credit score.

However, there’s a new push to treat medical debt differently from other forms of debt. This different treatment is due to the fact that medical debt is often unplanned and unavoidable.

For example, with a credit card, you choose to establish a credit card and make purchases. It’s expected that you budget for this credit card debt prior to making purchases. Medical bills are different because you never know when a medical emergency may occur. You also don’t have an option about seeking treatment because your life may depend on it. For these reasons, many credit score models are changing their formulas.

For instance, VantageScore 3.0 and VantageScore 4.0 no longer consider medical debt when calculating credit scores. While FICO does still consider medical debt listed on a credit report, it holds less weight than other types of unpaid debts.

The reality is that unpaid medical bills can affect your credit score if they’re listed on your credit report. The extent of this effect depends on the credit score model. You can track your Experian credit score free for up to 14 days with Free Credit Score. This can give you some idea of how medical debt may be impacting your credit score.

How Long Does Medical Debt Stay on Your Credit Report?

If you have medical debt that’s over $500 and more than 1 year overdue, it can be reported to the credit reporting agency and be listed on your credit report. This unpaid medical debt can remain on your credit report for up to 7 years or until it’s paid in full. Thanks to the new changes on July 1, 2022, all paid medical debt is removed from your credit report. However, the removal process can take up to 30 days to complete.

How to Get Medical Debt Off of Your Credit Report

Everyone makes mistakes sometimes, and credit reporting agencies are no different. It’s important to regularly check your credit reports to make sure they don’t include any errors. All three major credit reporting agencies allow you to request one free credit report each year. You can also check out your Free Credit Report Card to see how information on your credit report is impacting your credit score.

If you believe any medical debt is listed on your credit report in error, you can take steps to have this debt removed. With the new reporting changes in mind, you should also take steps to have any medical debt that’s paid in full, unpaid medical bills less than $500 or debt that’s less than 1 year past due removed from your credit report.

You can file a dispute by submitting a credit challenge letter explaining the error, along with any documentation to prove your claim, directly to the credit reporting agency. These agencies are required to investigate all dispute claims. If these agencies find the debt is listed in error, they’ll remove it from your credit report.

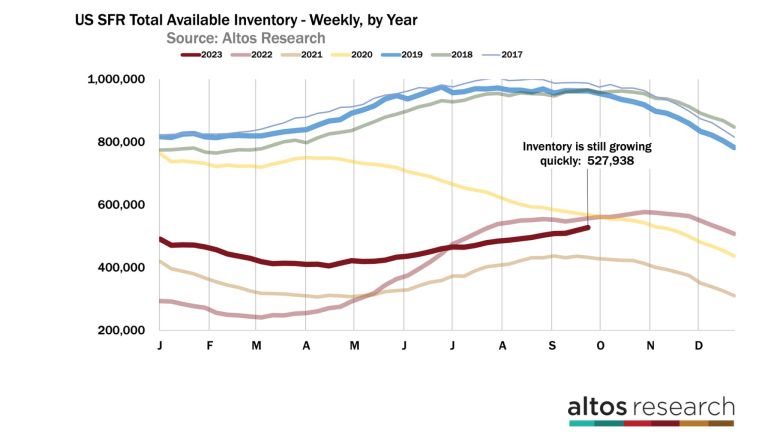

Available inventory of homes for sale is on the rise in late September, which is very unusual for this time of year. In fact, inventory is growing faster than this time a year ago.

This is a demand-driven slowdown, because new listings supply is still running 9% to 10% fewer homes for sale each week than this time last year. We’re seeing fewer new sellers each week, but inventory is building as homebuyers wait to see if mortgage rates will come down to make purchases more affordable.

What’s happening with inventory?

Fewer new sellers also means that inventory can’t grow too much; the real trouble develops when demand drops and supply surges. There’s no supply surge, but there is a notable demand drop. Consumers are very sensitive to changes in mortgage rates, and rates are still rising.

We can see these slowing changes build up each week. It’s a pretty sharp change from what was a surprisingly strong first half of the year. There are now 528,000 single-family homes on the market. That’s an increase of 1.8% from last week.

Normally by this point in September, available inventory is declining slightly each week. It’s late in the summer, so normally new listing volume drops as the last few sales of the peak summer months are concluding.

The fact that inventory grew by nearly 2% this week and last week is telling of how homebuyers are reacting to the highest mortgage rates in over two decades.

In this chart of each year’s inventory curves, you can see that the number of homes on the market is climbing faster now than this time last year. This year is the dark red curve, and last year the light red. Mortgage rates continue to climb, so there is no immediate relief for homebuyers on the horizon either.

At this point, it looks like we may see inventory grow to the end of October like we did last year. Look at the divergence in the curves from this year and the tan line from two years ago when we were still in the middle of the pandemic housing boom and record-low mortgage rates.

Pending-home sales continue to lag

New pending sales each week continue to run 10% to 15% below last year’s pace. If you follow the National Association of Realtors when they publish their existing-home sales report each month, you know that the latest report for August showed a sales pace of only 4 million seasonally adjusted annual home sales.

We can already see in the NAR data that there are no signs of improvement for the sales count through September and October. The home sales that are in contract now will close mostly in October. It’s not hard to imagine that next month’s seasonally adjusted home sales data from NAR will come in under 4 million.

In this chart, each bar is the total number of home sales pending on any given week. The shorter the bar, the fewer sales that are in progress. The light portion of the bar is the count of new pendings each week.

There are now 344,000 single-family homes in contract to close in the next couple months. That’s 14% fewer than last year and almost 30% fewer than in September of 2021.

Home sales are limited by the decreased demand, of course, and they’re also limited by the very low supply of new listings. You can’t buy what’s not for sale.

We’ve been talking all year about the market being supply constrained. Right now, sales are limited by declining demand from still-climbing mortgage rates.

Price reductions climb again

We can see the impact of weaker demand starting to creep into the pricing indicators. In the chart below, we look at the leading indicator of this trend: price reductions. This is the percent of homes on the market that have taken a price cut from their original list price.

For a while earlier this year, demand was exceeding supply in residential real estate, and you could measure that demand with the price-reductions curve improving each week. As mortgage rates lurched over 7% to their new highs, suddenly there are fewer offers.

And home-price reductions are climbing again, with 37% of the market taking a price cut. That’s more than any recent year except last year at this time. Price reductions are accelerating now, which bodes negatively for future sales prices.

A normal, balanced market will have 30% to 35% of the homes for sale that have reduced their asking price in recent months. As this dark red line approaches 40%, that’s a clear indicator that buyers are making fewer offers. Remember, the slope of this line captures how many properties are taking new price cuts each week. And this slope is increasing now.

These are transactions that will happen in the future, so it implies sales price weakness in the fourth quarter, which you’ll hear about in the headlines after the new year. But you can see it in the data now.

The median sales price of single-family homes in the U.S. right now is $440,000. That’s down 1% from last week and it’s just a tiny fraction higher than this time last year.

We can see the pressure on home prices in recent weeks. Home prices step downward in September for the seasonal change every year, and you can detect strength or weakness relative to changes in other years.

What we see now is that year-over-year price gains are just barely positive. And the comparison is getting weaker, not stronger, as our current mortgage markets deteriorate. There are fewer offers, and those that do happen are doing so at slight discounts each week.

Last year at this time, there were big price discounts being applied. So, our October comparisons may get slightly easier, but I sure haven’t seen any signals of price strength now.

Looking ahead to the end of 2023

So the question is will Q4 this year be a little better than Q4 2022? The median price of the new listings is fractionally higher than last year at $398,500. It will be fascinating to watch the light colored line here over the next couple weeks.

The new listings are where you see price weakness first. And last year, they were already headed lower.

The price of the new contracts this week came in at $370,000. These are the pending-home sales that went into contract in the last week. Prices of the homes going into contract are lower than last year by a fraction.

The next few weeks will be interesting to track this stat, too. Last year in mid-September is when mortgage rates jumped from 6% to 6.5% to 7.5%. By early October, any offers that were made for purchases came in at notably lower price points.

By September 2022, new pending-home sales prices fell by 3% per week. Will that happen again? Mortgage rates are even higher now than they were last year.

In this chart, you’ll notice the light-colored line started a big decline during this week in 2022. That’s when buyers reacted to newly increased mortgage rates. So, we’re watching to see where the new contracts come in over the next few weeks.

The macro trends impacting mortgage interest rates and the Fed have not given us any reprieve yet. The signals are that mortgage rates are still headed higher.

Consumer expectations for future mortgage rates have moved higher, too, so potential homebuyers are less optimistic than they were at the start of the year. And that’s what we’re seeing in the data each week now.

However, it’s important to point out that while buyer demand has backed off this fall, there is still no sign of any surge in new supply coming to the market. It can be very easy to focus on the negative momentum.

People on the fence should also know that while their competition is lessening, there’s no sign of an inventory flood. That may be an important factor in their home-buying decisions.

Mike Simonsen is president and founder of Altos Research.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

A personal loan is money borrowed from a lender that can be used for almost any purpose, from debt consolidation to home improvement projects.

Most people don’t have $5,000+ sitting in their bank accounts—that’s where personal loans come in. Just like a mortgage or auto loan, personal loans allow you to cover large purchases or expenses under the terms that you’ll pay off the loan over time, typically with interest.

If you’re considering taking out a personal loan, here’s all you need to know to ensure you’re making the right money moves to fund your future investment.

What Is a Personal Loan?

A personal loan is money borrowed from a bank, credit union, or other financial institution that can be used for virtually any personal expense. Like any other installment loan, personal loan borrowers are expected to pay the money back over a set period.

The typical amount you can take out for a personal loan can range anywhere from $1,000 to $50,000, depending on several factors. Interest rates are just as variable—they can be as low as 6% and as high as 36%, depending on your unique financial situation. The current average interest rate for personal loans is 11.04% as of May 2023.

Get matched with a personal

loan that’s right for you today.

Learn

more

Why Would I Need a Personal Loan?

If you’re planning on making a big purchase, getting a better handle on your debt, or have run into some unexpected expenses, applying for a personal loan can help cover the costs. People usually take out personal loans for:

Debt consolidation

Unexpected medical expenses

Home remodeling

Emergency expenses

Vehicle repairs or financing

Moving expenses

Vacations

Wedding expenses

While you could technically use this type of loan for, well, anything, there are a few things you should avoid using a personal loan for, like:

College tuition: It’d make more financial sense to use a federal student loan vs. a personal loan to pay for college tuition. Federal student loans typically come with lower interest rates, plus most don’t require a credit check. You may even qualify for a subsidized loan or an income-driven repayment plan.

Home down payment: Most mortgage lenders won’t accept a personal loan as a down payment, and even if they did, the increase a personal loan could cause to your debt-to-income ratio might disqualify you from the loan anyway.

Starting a business: Taking out a personal loan to open a business won’t help you build business credit since the loan is in your name. Instead, consider applying for a business credit card to start building credit so you can apply for a business loan down the road.

Everyday expenses: If you’re strapped for cash now, taking out a personal loan to cover bills and other living expenses may just create a bigger problem in the long run since you’ll have to repay the loan amount plus interest. Consider re-budgeting or finding ways to increase your income instead.

Personal Loans vs. Lines of Credit vs. Payday Loans

Personal loans, personal lines of credit, and payday loans are all money-borrowing options that can help you manage your finances or cover a significant expense. However, they’re typically used for different purposes.

Personal loans vs. lines of credit: Personal loans are typically used to cover large purchases or expenses since all the money is available upfront. On the other hand, personal lines of credit allow the borrower to use the credit available as needed and pay it off on their own timeline, so they’re more ideal for smaller everyday purchases.

Personal loans vs. payday loans: Whereas personal loans allow you to borrow a large sum of money with a loan term typically spanning several years, payday loans offer borrowers a small amount of cash—typically around $500 or less—at a higher interest rate that has to be repaid within 2-4 weeks. Payday loans are best if you have an urgent expense and know you can repay the loan within the term offered.

Definition

What it’s best for

Personal loan

Supplies the borrower with a large sum of money upfront that must be paid back in fixed monthly payments throughout the loan term

Large purchases or expenses

Personal line of credit

Lets the borrower use credit as needed and pay it back on their own timeline with a variable interest rate

Building credit on everyday purchases

Payday loan

Gives the borrower a small sum of money—around $500 or less—at a high-interest rate that usually has to be repaid within 2-4 weeks

Quick cash for urgent needs, especially if the borrower does not qualify for a traditional loan

Types of Personal Loans

Before you apply for a loan, research the type of personal loan that will best serve your unique financial needs. Your credit history, credit score, and reason for needing the loan will determine which is best for you.

Here’s a quick breakdown of the seven most common types of personal loans:

Type of personal loan

Definition

Who it’s best for

Unsecured personal loans

Do not require any sort of collateral to qualify

Borrowers with excellent credit and a steady source of income

Credit-builder loans

Allow you to take out a small sum of money to demonstrate that you’re a reliable borrower by making regular on-time payments

Borrowers with low or no credit history looking to improve their credit score

Debt consolidation loans

Typically can be borrowed at a lower interest rate than most credit cards or other bills you plan to consolidate, saving you money on interest

Borrowers with multiple debt balances or balances with high interest rates

Co-signed and joint loans

Allow a co-signer to assume responsibility for a loan if the borrower does not qualify

Borrowers who do not qualify for a traditional loan or are hoping to be approved for a lower interest rate

Fixed-rate loans

Come with an interest rate that does not change over the repayment term, so the borrower pays the same amount every month

Borrowers who plan on paying off their loan over an extended period

Variable-rate loans

Come with a fluctuating interest rate that could increase or decrease monthly payments over time, but rates are sometimes lower vs. fixed-rate loans

Borrowers who only need to borrow funds for a short period

How Do Personal Loans Work?

You have to receive a personal loan through an authorized lender, typically a bank or credit union. Here’s how the personal loan process works:

You must first apply for a personal loan. The lender will decide if you qualify based on your creditworthiness, income, and the type of personal loan you’re interested in.

If you qualify for a loan, your lender will usually set a loan term to determine how long you have to pay the money back. This can range anywhere from months to years, depending on the lender and your needs. A fixed or variable interest rate—the cost of taking out the loan—will also be applied to your monthly payments.

If you qualify for a loan, you’ll be issued a lump sum deposited into your bank account. You’re free to do with the money as you wish, but you’re expected to make regular monthly payments until the loan is paid off.

How to Apply for a Personal Loan

Personal loans are a great tool for financing some of life’s most important—and unexpected—milestones. If you’re ready to apply for a personal loan, follow these steps:

Check your credit: Your credit history will be one of the biggest determinants of whether or not you’re approved for a loan, so it’s important you know where you stand. Most lenders will want to see a “good” credit score (620) or above to ensure you can be trusted to meet your loan terms.

Decide how much to borrow: You may qualify for a $50,000 loan, but before you sign on the dotted line, you need to know how much you can realistically afford to borrow. Carefully consider your current and future financial situation before jumping into any personal loan.

Pro tip: Try our loan payment calculator to easily estimate monthly payments for different personal loan options.

Know your consumer rights: According to the Truth in Lending Act, lenders must disclose the APR finance charges, principal amount, and any fees and penalties associated with a loan offer. If you come across a lender that refuses to share this information, you’ll want to look for a different lender.

Gather essential documents: In addition to your credit report, potential lenders may also want to see the following documents to speed up the application process.

Proof of your annual income

Your debt-to-income ratio

Your Social Security number

Recurring monthly debt (like your house payment)

Employer information

Your cosigners financial information (if applicable)

Research loan options: Personal loan requirements and terms vary by the type of loan and lender, so you’ll want to research before applying. Details that may sway your decision include the loan amount, APR, monthly payments, loan term, secured or unsecured, and more. Ask lenders for this information in advance before applying for a personal loan.

Submit your application: Once you’ve settled on a loan that meets all your requirements, fill out your application, read it carefully for typos or errors, and submit it to your potential lender. You’ll likely know whether your application was approved within a day or two whether your application was approved.

How to Qualify for a Personal Loan

Each lender is different, so minimum requirements for personal loans vary. However, if you’re hoping to qualify for a large unsecured personal loan with a competitive interest rate, here are a few general requirements most lenders will want to see:

A minimum credit score of 620

A positive and established credit history

A debt-to-income ratio less than 36%

A steady income with proof of employment

Again, these requirements vary from lender to lender. In some cases, you may qualify for a loan with no credit at all. Some lenders even prioritize things like education and work history when evaluating applicants. Inquire with potential lenders before you apply for a personal loan to better understand what you need to qualify.

Personal Loan Alternatives

If credit history, high interest rates, or substantial fees are preventing you from applying for a personal loan, there are money-borrow alternatives that may be a better fit, like:

Home equity loans: Home equity loans or lines of credit (HELOC) are secured by the equity a borrower has built in their home. Because this is a type of secured loan, interest rates tend to be lower compared to an unsecured personal loan. The repayment terms are also longer than most personal loans, sometimes up to 20 years.

Credit Cards: Credit cards allow borrowers to use credit and pay it back as they go, offering more flexibility than personal loans. Many credit cards also offer rewards like cash back or airline miles for money spent.

Personal lines of credit: Like credit cards, personal lines of credit allow you to borrow money and pay it back as you go. However, personal lines of credit have a set draw period—once the period is over, you won’t be able to tap your line of credit and will need to pay back your balance. Interest rates for personal lines of credit are typically lower than credit cards, so they’re ideal for large ongoing projects.

Retirement loan: If you’re looking for more relaxed loan requirements, you may be able to borrow from your employer-sponsored retirement plan in the form of a 401(k) loan. This is a great alternative for borrowers with less-than-stellar credit, but keep in mind that you’ll be restricted to your current retirement accounts, and you may have to repay the loan early if you leave your current job before the loan term ends, often with penalties.

FAQs

Still weighing your personal financing options? We answered some of the most frequently asked questions about personal loans to help with your decision.

Will a Personal Loan Affect Your Credit Score?

Applying for a personal loan may cause a light dip in your credit score because lenders will run a hard inquiry on your credit. While a hard inquiry shouldn’t affect your credit score too much, it’s important to narrow down your options before applying to avoid multiple hard inquiries from multiple potential lenders.

It’s also wise to wait to apply for a personal loan if you’ve just opened another line of credit, which could cause an even bigger drop in your score.

Do You Need a Down Payment for a Personal Loan?

You do not need a down payment for a personal loan. However, In the case of a secured loan, you’ll need collateral, such as a car or money in a savings account.

Can You Use a Personal Loan for Whatever You Want?

A personal loan can be used for just about any purpose. Some lenders may want to know what the money will be used for, but others just want to be certain you’ll be able to pay it back. However, a better financing option may be available if you plan on using your loan for things like tuition or daily expenses. Research your options before applying for a personal loan.

How Big of a Loan Can I Get With a 700 Credit Score?

You’ll likely be able to borrow higher limits with a 700 credit score or higher, but other factors, including your income, employment status, and the type of loan you’re applying for will also impact how big of a loan you qualify for.

How Often Can You Apply for a Personal Loan?

There is no limit to how often you can apply for a personal loan. You can have multiple personal loans open at once, but remember that too much existing debt may lead lenders to disqualify you from taking out more loans or opening new lines of credit.

Researching personal loans can be daunting, especially if you’ve run into sudden unexpected expenses. The best loan for you will depend on your unique financial situation. Check out the personal loans at Credit.com to quickly compare options and see potential APR, terms, and maximum loan amounts.

For months, I’ve been banging on about the lack of a refinance program for private-label mortgages, those not backed by Fannie Mae and Freddie Mac.

Sure, HARP is great for underwater homeowners whose loans are owned by the pair, but what about those who aren’t so fortunate?

I’ve brought up proposals such as HARP 3 on several occasions, along with Oregon Senator Jeff Merkley’s refinance program that targets those who hold mortgages that aren’t government-backed.

The Obama administration has also been open to an expanded HARP for these types of borrowers, but without Congressional approval, any stirrings of such relief continue to fall on deaf ears.

But apparently these borrowers are actually receiving some assistance outside of HARP.

45% of Borrowers Have Received a Loan Modification

A new commentary released today by Fitch Ratings revealed that about 45% of all underwater borrowers with private-label mortgages have received a loan modification.

The company noted that loan modifications, distressed loan liquidations, and home price gains have reduced the number of underwater loans in private-label residential mortgage-backed securities (RMBS) by a sizable 25%.

There are still roughly 1.5 million underwater loans in these at-risk securities, though that number has fallen from 2.04 million.

Perhaps the biggest driver has been home price increases, with double-digit growth seen in some of the hardest-hit areas, including Arizona, California, and Nevada.

Assuming home prices continue to tick higher, which they’re expected to, the number of waterlogged loans will continue to drop at a steady clip.

While this is all good and well, the carnage is far from over. Fitch said about one-third of all outstanding borrowers in private-label RMBS pools (no pun intended) remain underwater.

It’s unclear how deeply underwater they are, but underwater nonetheless.

Additionally, the company projects some regions of the United States, notably the Northeast, to experience further home price declines before bottoming.

Why This Is Good and Bad

At first glance, it appears to be good news. Underwater borrowers with all types of loans are generally getting the help they need to continue making mortgage payments and hold on to their homes.

This benefits everyone involved because it makes for a stronger housing market. But the numbers can be deceiving.

Sure, 45% of these non-Fannie/Freddie underwater borrowers received loan mods, but what type of loan mod?

Did they get a $100 off their loan each month? Did they get a .125% interest rate reduction? Was principal forgiveness involved?

We don’t know what level of assistance they received, and if history tells us anything, a lot of these private loan mods weren’t all that attractive, at least not compared to HARP.

Through HARP, borrowers have been able to refinance their mortgages to interest rates a few percentage points lower than their previous rate.

That’s serious assistance, enough to stick around and see this crisis out. The private mods are another question.

This improvement also doesn’t bode well for an expanded HARP for non-Fannie/Freddie borrowers. The more improvement we see and hear about, the less likely Congress will be to act.

So the prospects of a new assistance program are dwindling each day.

The Multnomah Pilot Program

There is a small glimmer of hope though. Last month, the Treasury Department approved a new pilot program to assist underwater borrowers without Fannie and Freddie loans.

The so-called “Rebuilding American Homeownership Assistance” (RAHA) Pilot was launched in Multnomah County, which includes the city of Portland.

It’s limited to borrowers with “significant negative equity” who intend to stay in the prpoerty for 5+ years. They must not own any other residential property and be current on the mortgage.

Just weeks after New York-based digital lender Better Home & Finance Holding went public, Better issued pink slips to employees in early September in a new round of layoffs, Insider reported.

Better laid off about a quarter of its U.S. mortgage sales and origination team, according to the news outlet, citing two former employees who were affected by the latest downsizing.

The layoff news comes on the heels of Better going public via special purpose acquisition company (SPAC) Aurora Acquisition Corp. in August.

About 75 employees are left on the mortgage origination team in the U.S. as well as some employees in India, according to Insider.

While Better didn’t respond toHousingWire‘s inquiry about the number of affected employees, spokeswoman Jessica Schaefer told Insider the firm has more than 100 people left on the team.

Better plans to fill some vacant positions from the layoffs.

“As a publicly listed company, we’re focused on making prudent and disciplined decisions that account for market dynamics so that we can continue to serve both customers and shareholders for the long-term,” Better’s spokesperson said in an e-mailed statement to HousingWire.

“We are hiring more seasoned professionals who can sell in this tough mortgage environment and then making them 10X more productive through our continued investment [in] technologies such as Tinman and One Day Mortgage, which have created efficiencies that streamline and automate nearly every major function of homeownership,” the spokesperson said.

As of June, Better had 950 team members, a 91% decrease over an 18-month period from 10,400 in Q4 2021, according to its previous filing with the Securities and Exchange Commission (SEC).

While Better was an efficient refi shop during the pandemic years when rates hit record lows, the lender and other independent mortgage banks (IMBs) were hit hard by the Federal Reserve‘s monetary policy.

The digital lender reported a net loss of $45.5 million in Q2, an improvement from a net loss of $89.9 million the previous quarter.

In Q2, Better’s origination volume was $900 million across 2,421 loans, compared to production of $800 million across 2,347 loans funded in Q1.

When Better debuted on Nasdaq in late August, the SPAC deal unlocked $565 million of fresh capital for the unprofitable company.

The digital lender has pivoted its strategy from being a one-stop-shop to becoming a “mortgage-as-a-service” company or a white-label provider of mortgage tech.

“For things like homeowner’s insurance, title insurance, and Realtors, we’ve now just become a marketplace. We match the consumer with a partner capable of delivering the best product to them. So, we ended Better Real Estate for the sake of efficiency and savings for the consumer. We partner with best-in-class agents, insurance companies and title companies,” Better CEO Vishal Garg said in an interview with HousingWire in August.

Better will invest in tech-driven products like One Day Mortgage, a program that will allow customers to apply for a mortgage, get preapproved, lock their rate and receive a mortgage commitment letter within 24 hours.

“We are committed to further developing this technology during an interest rate environment where customers need it the most,” Better’s spokesperson noted.

Better was ranked as the 59th largest lender in Q1 2023, plummeting from the 19th in 2021, according to Inside Mortgage Finance.

Mortgage rates actually recovered a bit on Friday as the underlying bond market experienced a modest correction after spiking to the weakest levels in more than a decade over the past 2 days. Despite the improvement, mortgages are also still near multi-decade highs. Why is this the case when the Fed didn’t hike rates this week?

This counterintuitive movement is fairly common when it comes to the 8 Fed meetings each year. Rates have fallen on several occasions when the Fed hiked throughout this rate hike cycle. There are several reasons this can happen. Some are complicated, but two of the simplest reasons are all we need this time around.

First off, the Fed only has 8 scheduled opportunities to update rates every year while the bond market has thousands of opportunities every day. Because of that, a Fed rate hike is often just a lagging development that the market has already priced in. The Fed actually tries to avoid surprising the market when it comes to hikes/cuts. Via speeches and press conferences, it effectively preps the market for potential changes.

The market can trade these expectations in a variety of ways. The most direct is via Fed Funds Futures, which give traders a way to bet on the level of the Fed Funds Rate on any given month well into the future. Traders haven’t budged in their expectation of this week’s meeting resulting in a 5.375% Fed Funds Rate for months!

In other words, when the Fed held rates steady this week, it wasn’t a surprise to anyone and the market was already priced for it. We can thus rule out the rate decision as the catalyst for the mortgage rate volatility and look elsewhere. We won’t need to look far.

On 4 out of the 8 Fed announcements per year, and at the exact same moment as the Fed Funds Rate decision, the Fed also releases a “summary of economic projections.” Among these forecasts is a dot plot showing where each Fed member sees the Fed Funds Rate at the end of the next few years. These so-called “dots” have become a big deal for financial markets despite Fed Chair Powell’s requests to avoid reading too much into them.

The market doesn’t care about the dots due to some amazing track record of accuracy from the Fed. Rather, they simply offer a very detailed update as to how the Fed’s decision-making process is evolving when it comes to future rate hikes/cuts. If the average Fed member expected rates to be almost 1% lower by the end of 2024 and now only sees them being 0.25% lower, that would tell the market a lot about the Fed’s intention to keep rates higher for longer, all other things being equal.

That is exactly what happened.

Markets expected the dots to rise, but not by this much. Neither stocks nor bonds (aka rates) were happy about it.

Traders had already been pricing in a “higher for longer” path for the Fed Funds rate based on recent economic data. In the bigger picture, this week’s revelation didn’t materially alter the trend in those expectations, but it did give them a noticeable bump. Here’s how the market’s outlook for the Fed Funds Rate in September 2024 has been evolving.

The “bump” just happened to hit when rates were already near long-term highs. The average 30yr fixed rate didn’t technically break above the highest level seen last month, but it came within 0.01% based on the more timely data from Mortgage News Daily. We expect Freddie’s weekly numbers will challenge multi-decade highs next week.

Why is all this happening? In a nutshell, the Fed Funds Rate is a blunt instrument tasked with fighting inflation. Inflation has been coming down, but it’s still high and a bit of a rebound can’t be ruled out due to things like higher fuel prices, auto worker strikes, and an adjustment in the way certain health care costs are calculated. In addition, the Fed is not yet seeing the type of downturn in economic data that would suggest impending disinflation.

That last point is a matter of debate as some critics say the Fed has already done enough and simply needs to give their policy more time to have an impact. The Fed admits that this economic cycle is different than past cycles and that there’s no way to know with certainty when it’s time for a friendly shift.

Regardless of who’s right about the timing of a policy shift and whether enough has already been done, most can agree that it will be economic data that serves as the trigger for a change. Not just any economic data will do. The Fed and the market are both focused on several of the highest impact reports. Most of them will be released on the first week of October. If they take a turn for the worse, rates would likely recover. If they continue to surprise to the upside, so will rates, unfortunately.