Lenders are feeling the pinch too: “Also, what’s happening is your lenders are also trying to struggle through the fact that volumes are way down.” So what should we expect? All this we know, with the factors leading to higher rates by now well documented. But to glean some optimism from this mix is something … [Read more…]

Our experts answer readers’ home-buying questions and write unbiased product reviews (here’s how we assess mortgages). In some cases, we receive a commission from our partners; however, our opinions are our own.

The Federal Reserve stated after its September meeting that it would not raise the federal funds rate this time. Before inflation and high interest rates, mortgage rates were around 3% and now they can be as high as nearly 7%.

The higher interest rates have made many potential homeowners press pause, but are interest rates the only thing you should be watching when considering a home purchase?

It’s not just the buying of the home that should be the focus, but also the reality of owning it. If your budget isn’t ready for that, maybe buying a home isn’t the right choice.

Here are three signs that you cannot afford a home right now:

1. You don’t have any emergency savings

Saving for a down payment on a home can take a lot of time and resources, but when you do buy your home, it shouldn’t wipe you out financially. While you are saving to buy, you should still be building (or maintaining) your emergency fund.

Having cash on hand for unexpected emergencies and expenses is crucial and even more so when you own a home. Imagine my shock when I woke up one morning and the tree in my yard had fallen and landed on my neighbor’s car. I needed money immediately to take care of that situation.

SoFi Checking and Savings is one of the best checking account options if you want to keep your savings and checking with one bank SoFi offers Money Vaults, a tool that can help you save for individual goals.

2. You’re only expecting a mortgage payment

When thinking about purchasing a home, the amount of the mortgage payment seems to be the only thing anyone considers. You can even use online mortgage calculators to determine what your monthly payment will be based on interest rate and down payment variables.

But there is more to owning a home than the monthly payment. Once you are in the house, there are hidden expenses of homeownership. There are property taxes, homeowners insurance, maintenance, and more.

This is what is called the true cost of ownership. When you add up everything, it can be significantly more than just the mortgage payment. Make sure you run the numbers and determine if you can afford it all.

3. You have significant debt already

In reality, everyone seems to be carrying some form of debt. No, you do not have to be debt-free to purchase a home, but if you are carrying significant credit card debt or student loans, adding a monthly payment to your mortgage lender may not be right for you right now.

This is where the difference between renting and buying will come into play. If you are renting and student loan payments resume or you find yourself in a situation where affordability is an issue, you can move or you can try to negotiate down the rent on your apartment.

But when you own a home, there is much less wiggle room. To move, means you have to sell your home — and it is really hard to change your mortgage payment.

If you have significant debt, maybe wait to purchase a home until that debt is paid off.

Debt consolidation can be a useful tool to help pay down existing debt at a lower interest rate. Many of the best personal loans will allow you to check your personalized loan rates before you apply, allowing you to protect your credit score against unwanted hard inquiries. Get prequalified for loans without impacting your credit score.

Jennifer Streaks

Senior Personal Finance Reporter and Spokesperson

Jennifer is a Senior Personal Finance Reporter and Spokesperson for the Personal Finance vertical at Business Insider. She started her career covering personal finance at Black Enterprise Magazine, went on to CNBC where she covered personal finance, women and money and tech and then Forbes, where she reported on personal finance, business, tech and money matters related to the economy, investing, credit and entrepreneurship. Jennifer is also the author of Thrive!…Affordably: Your Month to Month Guide to living your Best Life without breaking the bank. The book offers advice, tips and financial management lessons geared towards helping the reader highlight strengths, identify missteps and take control of their finances. In addition, she has extensive experience as an on-air financial commentator and has been a featured expert discussing credit and savings, investing and retirement, mortgages and all things money and personal finance. She has an ability to discuss and simplify complex financial issues and make them easier to understand.

Are you thinking about selling your engagement ring? People sell their engagement rings for all sorts of reasons, such as no longer being in a relationship or inheriting a ring. Whatever your reason may be, you can most likely sell your engagement ring and make extra money. You can use this extra money towards paying…

Are you thinking about selling your engagement ring?

People sell their engagement rings for all sorts of reasons, such as no longer being in a relationship or inheriting a ring.

Whatever your reason may be, you can most likely sell your engagement ring and make extra money.

You can use this extra money towards paying off debt (like credit card debt or student loans), starting an emergency fund for unexpected expenses (like medical bills, vet visits, or house repairs), putting the money into your retirement savings, or even saving for financial goals (like a home deposit, buying a car, or going back to school).

Today, you’ll learn how to:

Get your engagement ring appraised

Negotiate for the highest price

Find the best place to sell your engagement ring

And, of course, the step-by-step process of how to sell an engagement ring!

How To Sell An Engagement Ring

How much is an engagement ring worth?

Before you sell your engagement ring, you should try and figure out how much it is worth.

One of the things to think about when valuing a diamond engagement ring is the “4 Cs of a Diamond.” If you want to know where to sell diamond rings, first you must figure this out.

The 4 Cs stand for:

Carat – This is the size of the diamond. Larger diamonds are usually worth more money.

Cut – This is not the diamond shape. Instead, this is the quality of the diamond’s cut which will impact how beautiful and brilliant the diamond is.

Color – A diamond’s value increases with less color, as a completely colorless diamond is worth more.

Clarity – Clarity is all about the imperfections and blemishes that a diamond may have. The fewer there are, the more valuable the diamond.

Other things that may increase or decrease the value of your used engagement ring include:

Condition – The overall condition of the ring is important. A ring that has been taken care of and shows minimal signs of use will typically hold onto more of its value in comparison to a ring that displays noticeable wear and tear.

Resale market – Rings with a popular style or from a well-known designer may see a higher price when resold.

Certification and documentation – Having a document such as a diamond grading certificate can help determine the quality of the ring.

Designer and brand name – Rings from certain designers or brands (such as Cartier or Tiffany & Co.) tend to have a higher resale value due to their reputation and craftsmanship.

Even though a pre-owned engagement ring may have a lower value compared to a new one, it can be a great value for buyers looking for a high-quality ring at a more budget-friendly price. And, that is why people buy them – they can save some money over a new ring.

Recommended reading: 8 Items To Sell Around Your Home For Extra Money

Gather documentation for your engagement ring

If you’ve decided to sell your engagement ring, it’s time to collect all of your paperwork related to the ring such as the diamond’s certification, receipts, and appraisals.

These documents will help figure out the ring’s value, establish its authenticity, and make the process of selling a little more smooth.

Here’s a list of the paperwork you might need:

Appraisal certificate – The appraisal certificate is a professional evaluation of the engagement ring. This document includes details about the diamond’s cut, color, clarity, carat weight, and quality.

Original receipt – Having the original receipt from the purchase of the engagement ring will help show that the ring is authentic.

Diamond certification – If the diamond was graded and certified by a recognized gemological laboratory, this can be helpful.

Gemstone certificates – If your engagement ring has other gemstones besides diamonds, include these certificates for the stones as well.

You don’t need any paperwork to sell an engagement ring, but, it can make things a little easier and may get you a little more money.

How to get an engagement ring appraised

Getting an engagement ring appraised by a certified gemologist or jewelry appraiser will give you an accurate estimate and valuation of how much your engagement or wedding ring is worth.

This can help you when negotiating (such as with a pawnshop) and simply knowing the amount that you should be looking for when selling your ring.

You can get your engagement ring appraised by:

Looking for appraisers – You can search online for certified gemologists or jewelry appraisers in your area. You can also ask local jewelry stores for their recommended appraisers. It’s important to find an appraiser with credentials from places such as the Gemological Institute of America (GIA), the American Gem Society (AGS), or the International Society of Appraisers (ISA).

Contacting the appraiser – Call the appraiser and ask for their fees and to schedule an appointment. You may need to bring documents such as receipts, certificates, or previous appraisals for the ring.

Getting the ring appraised – Take the engagement ring to the appraiser. They will examine the engagement ring’s characteristics including the diamond’s cut, color, clarity, and other important factors.

Receiving the appraisal report – Once the appraisal is done, the appraiser will provide you with the report. This report includes information about the ring’s characteristics as well as an estimated value based on the current market. Ask the appraiser any questions you might have or if you need a question answered.

Where to sell an engagement ring

Now is the time to look at your different options for selling the ring. You can sell engagement rings at jewelry stores, pawn shops, online marketplaces, auction houses, consignment shops, and more.

Some things that you will want to about when deciding where to sell your engagement ring include the amount that they are giving you (of course, you want the most money, right?), the fees that they may be charging to sell your ring, how much work it will take you to sell it (for example, do you have to create the listing or do they?), whether you feel safe meeting someone to exchange the ring for cash in-person, and more.

As you can see, there are going to be pros and cons for each of the places where you can sell your jewelry.

Below, I go further into each of the best places to sell an engagement ring:

1. Sell your engagement ring online in a marketplace

If you want to sell your engagement ring, one of the best ways to get the most money for it is to sell it online.

Selling your engagement ring online can be convenient and also help you reach a wider audience of possible buyers.

Some of the different places you can sell an engagement ring online include eBay, Facebook Marketplace, and Craigslist.

Here’s a step-by-step guide to help you sell your engagement ring online:

Make your ring presentable – You should clean your ring and take quality photos of it from different angles.

Choose the marketplace – There are many different sites to sell your engagement ring like eBay, Craigslist, Facebook Marketplace, specialized jewelry-selling websites, or online auction sites.

Create a detailed listing – In the listing, write a detailed description of the ring along with its condition and any unique features. Be honest about any imperfections. When listing your ring for sale, you should also describe the ring, such as the diamond’s cut, color, clarity, and carat weight.

Set a price – You should research similar engagement rings or get your ring appraised to find the most accurate price based on current market value.

Shipping – If you’re shipping the ring, make sure to package it securely to prevent any damage in transit and also pay for shipping insurance.

2. Sell your engagement ring on Worthy

Similar to the above, some websites are dedicated to selling jewelry and valuables, such as Worthy.

Worthy does not buy your engagement ring directly as that is not their business model, but they will clean it up and sell it for you.

Worthy makes it really easy to make money with your engagement ring and this is the best place to sell engagement rings online. You simply ship your jewelry to their office with a prepaid shipping label (a FedEx label) that they give you (it’s insured as well). Then, once they get the ring, they prep it for auction. They will clean the ring, take professional photos of it, and grade it.

After that, your ring will go up for auction, and professional jewelry buyers can bid on it. You can set a reserve price that you are comfortable with. Once the auction is done, you will receive the final sale amount after Worthy’s fee. Payment is then sent to you within 1-5 days.

The whole process typically takes around 2 weeks from shipping to getting paid.

So, what are Worthy’s fees? They do almost all of the work for you, so it makes sense that they would charge a fee. They take 18% for up to $5,000. After that, it is a 14% fee for $5,001 to $15,000, a 12% fee for $15,001 to $30,000, and a 10% fee for over $30,000.

So, for example, I found a 1-carat diamond ring on Worthy that eventually sold for $2,792. That means the seller received around $2,289 after the 18% fee that Worthy charges.

3. Work with a jeweler

Jewelers may offer to buy your engagement ring. You can simply call around local jewelry stores near you and ask if they buy used engagement rings.

Sometimes this can be the most straightforward and convenient option for selling your engagement ring as you can possibly sell your ring the same day.

To sell your engagement ring to a jeweler, you will want to look for jewelry stores near you and give them a phone call to see if they buy used engagement rings. I recommend looking for ones with positive reviews.

If you have any documentation for your ring then make sure to bring it with you so that you can show the jeweler.

If they are interested in your engagement ring, then they will give you an offer. If you’re happy with the offer, then you can ask any other questions and possibly sign paperwork to get your cash.

Jewelers may offer instant payment either via cash, check, or electronic transfer and you will want to confirm the payment method before completing the sale.

4. Sell your engagement ring to a consignment shop

You may decide you want to sell your used engagement ring to a consignment shop. Consignment shops have benefits such as offering exposure to multiple buyers. However, they likely charge a commission fee.

To sell your engagement ring through a consignment shop, you will want to Google search for consignment shops in your area and specifically look for shops that sell jewelry or high-end items (make sure the shop has good reviews and even testimonials of previous successful sales of engagement rings).

Once you have an idea of which consignment shops you’re interested in selling your ring at, you should ask them questions about their consignment process, what commission rate they charge, and the terms of the sale.

Then, you’ll give the shop the ring to display in their store.

The consignment shop handles the transaction if someone is ready to buy the ring. You’ll receive payment after the commission fees are taken out.

5. Sell your wedding ring to a pawnshop

When people think about where to sell an engagement ring, one of the first places they think about is probably a pawn shop.

And, it makes sense – pawn shops make it very easy and you can sell your engagement ring for cash here. You can most likely even get paid on the same day!

But, you should keep in mind that they usually give you the lowest amount of money.

If you want to sell your old wedding ring to a pawn shop you will first want to make sure the ring looks nice and clean because that can help you get a better price. Get any papers you have about the ring, like appraisals or certificates, to show how much it’s worth, and make sure you know this number before you go in because you will most likely have to negotiate.

Now, when selling at a pawn shop, you can typically negotiate. To do so, you will want to find out the ring’s value, current market trends, and comparable sales. You can even make a better case for your price by showing documents on the ring and appraisals from certified gemologists. If the pawn shop cannot meet that price, you may just want to move on and try to find another buyer.

When the pawn shop makes an offer, remember they need to make a profit too, so it might be lower than you expect. If you’re not happy with the offer, you can try selling it to someone else. If you agree to sell it, you’ll need to show some ID, sign some papers, and then you’ll get paid.

Frequently Asked Questions

Below are answers to common questions about how to sell an engagement ring.

Is it possible to sell an engagement ring?

Yes! Many places buy engagement rings and wedding rings so that you can make money.

How much can you get for selling your engagement ring?

The amount of money that you can get for selling your engagement ring will vary and usually, you can earn anywhere from around 20% to 60% of what was originally paid for it. Yes, this is a wide range (and can mean a difference of hundreds or even thousands of dollars) and this is because there are so many factors that come into the price, such as the condition of the ring, the market demand, and where you decide to sell it.

How much can I sell my 1 carat engagement ring for?

A 1-carat diamond engagement ring will vary due to the 4C’s (cut, clarity, color, and carat). Usually, you can earn around $1,000 to $5,000 for selling a used engagement ring that is 1 carat.

Is it better to sell or pawn an engagement ring?

This depends – do you want to get the ring back? If you decide to sell it, you can get cash right away. This is a good option if you need money quickly.

On the other hand, if you decide to pawn it, the ring can be used as collateral for a loan. This can be a temporary solution if you just need cash right now but you want to get the ring back later. However, it’s very, very important to carefully read and understand the terms and interest rates from the pawnshop so that you can eventually get your ring back.

Why is the resale value of diamonds so low?

So, you may be thinking “But, I paid $10,000 for this ring! Why am I only getting a few thousand dollars?”

You most likely won’t get the same price that the engagement ring was bought for. This is because places that buy your engagement ring still need to make a profit. Plus, they aren’t going to sell the engagement ring for the same price as a brand-new ring.

How can I be safe when selling a ring?

If you aren’t shipping the ring but are meeting in person instead, then you must be careful. You should avoid sharing personal information until you’re 100% sure they are the person they say they are.

I also highly recommend meeting in a public place, such as a police station parking lot. Bringing a family member or friend with you to the appointment or meeting is good so that you aren’t alone. Make sure to use secure payment methods like cash and do not share bank account information, your social security number, or any other sensitive information (buyers do not need this information!!). Also, ignore requests to send the ring before receiving payment and make sure the payment has cleared before proceeding.

Where to sell my wedding ring after a divorce? Is it OK to sell a wedding ring after divorce?

Many people sell their wedding rings after a divorce. If you decide to do so, you can sell your wedding ring on sites like Worthy, Facebook, eBay, and more. Before you sell your engagement ring, though, you should make sure that the ring is legally yours (check your divorce agreement).

How long does it take to sell an engagement ring?

The amount of time that it takes you to sell an engagement ring depends on where you are selling it. For example, selling a ring on Worthy will take around 2 weeks (it takes a little longer to sell on Worthy, but you may get the best price for your diamond jewelry this way because they have many diamond buyers). Whereas, selling it to a pawn shop may mean that you get paid the same day (however, it’s typically for a lot less money).

What is the best way to sell an engagement ring?

The best way to sell your engagement ring depends on what you’re looking for and there is no one best answer for everyone. Do you want to sell your ring for the most money? Or, do you want to sell your engagement ring as fast as you can? Some people may want to just sell the ring to a pawn shop and get it over with. Others may want to take their time and sell it online so that they can get the most money.

How To Sell An Engagement Ring For The Most Money

I hope you enjoyed this article on how to sell your engagement ring for the most money.

Deciding to sell an engagement ring is a big decision to make as you may have an emotional connection to it. Due to this, you should take your time deciding what to do and choose the option that feels best for your situation.

Some of the best places to sell diamond rings include online (such as through Worthy or eBay), or in-person at a consignment shop or to a local jeweler. Many of the places above can be used for selling other pieces of jewelry as well, such as fine jewelry, bracelets, necklaces, earrings, and more.

Each place has its pros and cons. Some will pay you a lot more than others, but some may be much easier and quicker.

I hope you can find the best place to sell your engagement ring and that you get the most money!

Have you tried selling an engagement ring? What do you think is the best place to sell an engagement ring?

HSBC and NatWest cut mortgage rates again as rivals tipped to follow

Decision will ease some pressure on UK homebuyers and people seeking remortgage deals

HSBC and NatWest have announced a fresh round of mortgage rate cuts and Britain’s remaining large lenders are expected to follow suit in a move that will ease some of the pressure on hard-pressed Britons.

HSBC said it was cutting rates across many of its new fixed products – including some of its first-time buyer, home mover and remortgage deals – with effect fromTuesday, when full details of the reductions will be published.

Third of UK mortgage holders ‘do not think they will pay it off by 65’Read more

Fellow high street lender NatWest said it would also be cutting rates from Tuesday.

The latest reductions will improve conditions for homebuyers and those looking to remortgage on to a new deal.

NatWest announced reductions of up to 0.35 percentage points on selected fixed deals. A five-year fixed rate deal aimed at homebuyers with a 5% deposit that is currently priced at 6.39% will result in its rate being cut to 6.04% at the bank.

Mortgage costs had been rising relentlessly for months but UK lenders have been reducing their rates since the second half of July after it emerged that UK inflation fell further than expected in June, prompting speculation that the Bank of England would not raise interest rates by as much as previously expected. The Bank’s base rate is 5.25% after an increase from 5% in August.

Nicholas Mendes, a mortgage technical manager at the broker John Charcol, said HSBC had “laid down the gauntlet and shown they mean business … This is their second rate reduction in a week, along with criteria changes which extend terms to 40 years.”

Accord Mortgages, part of Yorkshire Building Society, also said that all of its fixed rates were being cut by 0.20 percentage points from Tuesday.

Last week, Nationwide Building Society reduced some of its fixed and tracker rates by up to 0.15 percentage points.

skip past newsletter promotion

after newsletter promotion

Stephen Perkins, the managing director of the broker firm Yellow Brick Mortgages, said: “All these rate reductions are starting to feel like an avalanche … No doubt there will be more of these reductions over the week, as all lenders follow in a conga line.”

Lewis Shaw, the owner of the broker Shaw Financial Services, said that with NatWest following hot on the heels of HSBC, “There’s every chance we could see the remaining big four [Lloyds Banking Group, Barclays, Nationwide and Santander] come to the party this week, too.

“It would appear that lenders are struggling to get new business, and the rate tap is the only tool they can turn to.”

However, a silver lining in the subdued housing market is the strength in new-home sales. Builders are providing rate buy-downs for first-time homebuyers, which aligns with their interests, Duncan explained.

Read on to learn more about Duncan’s views on the housing market, loan performance and affordability challenges homebuyers face.

This interview was condensed and lightly edited for clarity.

Connie Kim: The Federal Reserve decided to keep the benchmark rate unchanged in the target range of 5.25%-5.5%. With the majority of Fed officials expecting another rate hike before the end of 2023, how do you think this decision will affect housing and your forecast for the economy?

Doug Duncan: It’s our forecast that they won’t make another change until they drop rates. I think the forwards suggest that in either November or December, there’s a 50/50 chance to make an increase. I would say the risks are tilted that way, but we don’t have it in our forecast model.

We don’t have (the Fed) dropping rates until the end of Q2 next year, and we have a mild recession that starts in that quarter.

The reason that forwards are suggesting a 50/50 chance of another increase is that growth has been stronger than anticipated. We actually think that’s going to slow; I think that this is kind of like a final burst of activity.

Wedon’t know what third-quarter growth was. Our expectation, at an annual rate, is it’s north of 3%. If there’s another quarter like that, and oil prices have pushed to $100, then I think you get another quarter-point move by the Fed, especially if you don’t see a substantive change in employment.

Kim: Spreads in the mortgage space are wide. What are the reasons for that?

Duncan: There are several reasons for that. If that business flow for a time period helps them cover the variable costs, then it can be effective.

For one thing, no fixed-income investor thinks that mortgage-backed securities with 7% mortgage rates will be there when the Fed finishes the inflation fight. They’re going to cut rates and that will prepay. So you’re having to encourage investors with wider spreads to accept that.

It’s also the case that the Fed is running its portfolio off because they don’t talk about it much. But somebody has to replace the Fed, and the Fed is not an economic buyer. That is they weren’t buying for risk-return metrics; they were buying to affect the structure of markets. So they are a policy buyer.

They were withdrawing volatility from the market, and they were lowering rates to benefit consumers. When [the Fed] is replaced, it’s likely to be by a private investor who’s going to have yield expectations. They may require wider spreads than the Fed because the Fed is not an economic buyer.

Kim: A bit of good news for lenders in Q2 was that their production volume went up and origination costs went down. Are you optimistic this trend will continue?

Duncan: If rates stay at the 7.25% level, it’s going to be worse, not better. On the production side, the mortgage business is in recession because the levels of existing-home sales are back where they were at the end of the great financial crisis at around 4 million units. That’s very low historically.

I don’t see how it can go much lower than that. Even if we have a recession, we don’t see it going just a hair under 4 million. The reason why some of the headlines look good about housing is because house prices were expected to fall when rates ran up. They did for a quarter as households sort of adjusted to the idea that they were going to be running at a new higher level.

But prices are rising again. For existing homeowners, that’s good news because it means equity accumulation. But if you’re a first-time buyer, that’s not good news because it means it’s harder to qualify — especially with interest rates where they are.

Production is in a recession. The servicing side of the business is doing very well because those loans are simply not going to prepay for a long time. So, the servicing valuation on those loans is strong, because pre-payments are low. It’s a bifurcated market in that sense. We expect production volumes to remain low through 2024 and start to pick up maybe toward the end of 2024.

Kim: The silver lining in the current housing market is an uptick in new construction sales due to a lack of existing-home inventory. To what extent builders will offer rate buy-downs to drive sales remains to be seen. How likely are builders to support rate buy-downs, especially when it’s becoming expensive to do so?

Duncan: The traditional way in which builders gave borrowers choices regarding affordability was to offer them granite countertops. So if sales volume slows, they will throw in granite countertops, finish the basement or finish out the garage.

In doing interest rate buy-downs, they’re focused more on the problem of the first-time buyer. That’s because [the cosmetic] attributes of a house are more for move-up buyers. Builders recognize they’ve got to do something for affordability for the first-time buyer.

The share of new-home sales that are going to first-time buyers is the highest it’s ever been. The share of total sales that are new-home sales is also the highest it’s ever been. This is a highly unusual structure for the market.

The builders know that those loans are likely to get refinanced, even if they buy down two points. So they go from 7.5% to 5.5%. When the Fed is done with the inflation fight and if economic growth is back to the 2% to 2.5% level, mortgage rates will probably run to 4.5% to 6% over the cycle. These loans are going to refinance, and the consumer will be in good shape, building equity to become a move-up buyer. So there is an alignment of interests for the builders in doing this.

Kim: The housing market was relatively active during the spring and summer homebuying seasons despite lower historical sales than previous years. Looking ahead, do you see another rough Q4 like last year when rates surged? What are some factors that Fannie Mae is monitoring?

Duncan: If growth surprises to the upside, that will get the Fed to increase interest rates, which will push [mortgage] rates again. That would be the biggest challenge and just seasonality; the fourth and first quarters are the low points for seasonality.

Kim:Bankruptcies and layoffs are still happening. How far are we into the industry’s consolidation?

Duncan: I was looking at the bankruptcy data. It’s just gotten back to the pace of bankruptcy we saw in 2019. It is true [consumer] bankruptcies have been rising but from extremely low levels. I actually expect that to continue. In part, that’s because some businesses (probably smaller and midsized businesses) were kept going by very low interest rates for a very long time.

In the mortgage space? Certainly, you’ll continue to see exits from the business. Typically, mortgage companies are not publicly owned. So it happens quietly. It’s people in the industry that know who the players are that are in trouble. The employment data comes out on a lag basis for brokers and loan officers. So that has picked up. I would expect more.

Kim:Executives at Dark Matter Technologies noted that lenders are most interested in bringing down their origination costs and retaining their clients in this rising-rate environment. What other demands do you see from lenders?

Duncan: They have been investing in technology — primarily consumer-facing technologies to get business in the door. Now, that’s not a possibility. Because of the changes in interest rates and a drop-off in demand, they are now focused on tech investments that go into cost savings.

They are turning their attention to what they can do to lower origination costs. Can they convert fixed costs to variable costs? That’s really the question that the industry has to focus on. If they can convert fixed costs to variable costs, then when the cycle changes, they don’t get hit as hard by the drop-off in this business. That’s because the operating structure also drops off.

Kim:I notice a lot of independent mortgage banks roll out down payment assistance (DPA) programs for conventional loans. DPA programs were predominantly for FHA loans. What are the pros and cons of IMBs rolling out DPA programs for conventional loans?

Duncan: For the independent mortgage companies, down payment assistance gets the business through the door, right? If they’re covering their variable costs, they can keep going for a while and, eventually, they have to cover the fixed costs.

The question is, what are the other credit characteristics of the borrower? If they are an IMB, they have to place it with an investor. So the investor will be monitoring. For example, if it’s Fannie Mae or Freddie Mac, we monitor that. We look at making sure there are not layered risks in any consumer’s profile. For example, if they have a spotty employment record, but they’ve always paid their bills on time, and they have savings, they’ve got money to pay 20% down, then it would probably be acceptable to have that spotty employment record. But if there’s a spotty employment record and a spotty repayment record on their credit, that’s not going to make it through the screen.

Kim: DPA programs offered with FHA loans come with higher rates. If the FHA loans layered with a DPA are more costly, how do first-time buyers benefit from these programs?

Duncan: The question you ask is a really interesting social question. The foreclosure rate for FHA loans is higher than the foreclosure rate for VA loans or Fannie Mae or Freddie Mac loans. Fannie and Freddie are the lowest; VA is a little bit higher. FHA is the highest. There’s not a clear answer on what’s the optimal rate of foreclosure.

If [that rate] is zero, we can get to zero. But we aren’t going to be making very many loans. So there is some optimal level of risk-taking to help people realize their hope of owning a home. But it’s not a hard and fast number. Different people have different points of view on that.

Article originally published December 13th, 2017. Updated February 16th, 2023.

Buying a home is an extensive process. It includes marshaling your assets, reviewing your credit—and potentially trying to improve it—and shopping for a house that meets your wants and needs. That’s all before you enter the process of applying for a mortgage and considering your offers.

The process can be daunting, but it’s important to take one step at a time to avoid becoming overwhelmed. One area where people become especially concerned is the overall cost of a home loan. Securing a mortgage can be challenging, but how can you get a good interest rate to reduce the long-term cost of your home?

Here are some tips to help you get the best rates for mortgages. Just remember that many of these tips take time, so plan months or even years ahead for your homebuying journey.

In This Piece

Tips for Getting the Best Interest Rate on Your Mortgage

When you’re looking to secure a mortgage or get the best possible interest, personal finances really matter. Our tips include those related to your credit history, savings and income, along with some advice about educating yourself on mortgage terms and interest types.

Understand Interest Rate Types: Fixed vs. Adjustable

A fixed-rate mortgage has the same interest rate throughout the loan’s entire life. This makes your rate and monthly payment predictable and consistent. An adjustable-rate mortgage comes with an interest rate that can change—and often one that could increase if interest rates in the market increase. This can make your rate and monthly payment unpredictable.

Get matched with a personal

loan that’s right for you today.

Learn

more

Knowing your plans for the future can help you understand which type of interest rate is best for you. If you only plan to hold on to the home for a few years before selling it to upgrade, an adjustable-rate mortgage—or ARM—might work for you. This is especially true if interest rates are currently low, as an ARM loan tends to start with lower rates than fixed-rate mortgages when all other factors are equal.

Keep Your Credit Healthy

You do typically need decent credit to secure a mortgage, but there are options for those with lackluster credit. While the credit score required to buy a home depends on many factors, the better your score, the better rates you may be able to command. Interest rates are a huge factor in how much your monthly payment is. Better credit typically equals more favorable rates, which equals lower monthly payments.

Make a Bigger Down Payment

The larger your down payment, the lower your overall loan amount is. That can lead to a lower interest rate when you secure a mortgage. That’s because your interest rate is partially based on your home’s loan-to-value, or LTV.

For example, if a home is worth $200,000 and the loan is for $199,000, that would be considered a high LTV and is riskier for a lender. That could lead to a higher interest rate. If the ratio is lower, however, you might be rewarded with a lower interest rate.

Have Stable Income

If you can prove that your line of work is in high demand with no sign of slowing down, or if you work for a large, profitable company, your lender may take this into account when processing your paperwork. Income stability demonstrates that you’re less likely to miss mortgage payments.

You can also demonstrate income stability by income history. Documents that show a stable income, such as check stubs, W2 forms and tax returns, might all be required by a mortgage lender when evaluating you for a loan.

Lower Credit Utilization Ratio

Credit utilization refers to how much of your available credit you’re actively using. A high credit utilization rate occurs when you use a large percentage of your available credit. For example, if you have $10,000 total in credit limits across your credit cards and you have a total balance of $5,000, that’s a credit utilization rate of 50%.

The Consumer Financial Protection Bureau notes that keeping your credit utilization at 30% or lower helps improve your credit score, which can lead to better interest rates for mortgages. It can also ensure mortgage lenders don’t see you as using credit in a desperate or risky way, making them more likely to approve you and offer better rates.

Make Mortgage Point Payments

It’s possible to pay extra directly to your lender to lower your interest rate. For every one percent of your loan amount you’re willing to pay upfront, you may be able to get as much as half a percent off your home loan interest rate. Essentially, you’re just paying a larger amount of interest upfront, and this is known as buying points.

Have Enough Savings

Most people know they should have enough savings to cover about 6 months’ worth of bills. Proving to your lender that you can still pay your mortgage in the event of a job loss because you have cash on hand can help you score a lower interest rate.

A Final Word on Getting the Best Interest Rates for Mortgages

Keeping your finances healthy is the best way to protect yourself when applying for loans. Do the work ahead of time to ensure you’re ready to apply for a mortgage. Then, you can start by comparing rates online to secure a mortgage that works for you.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

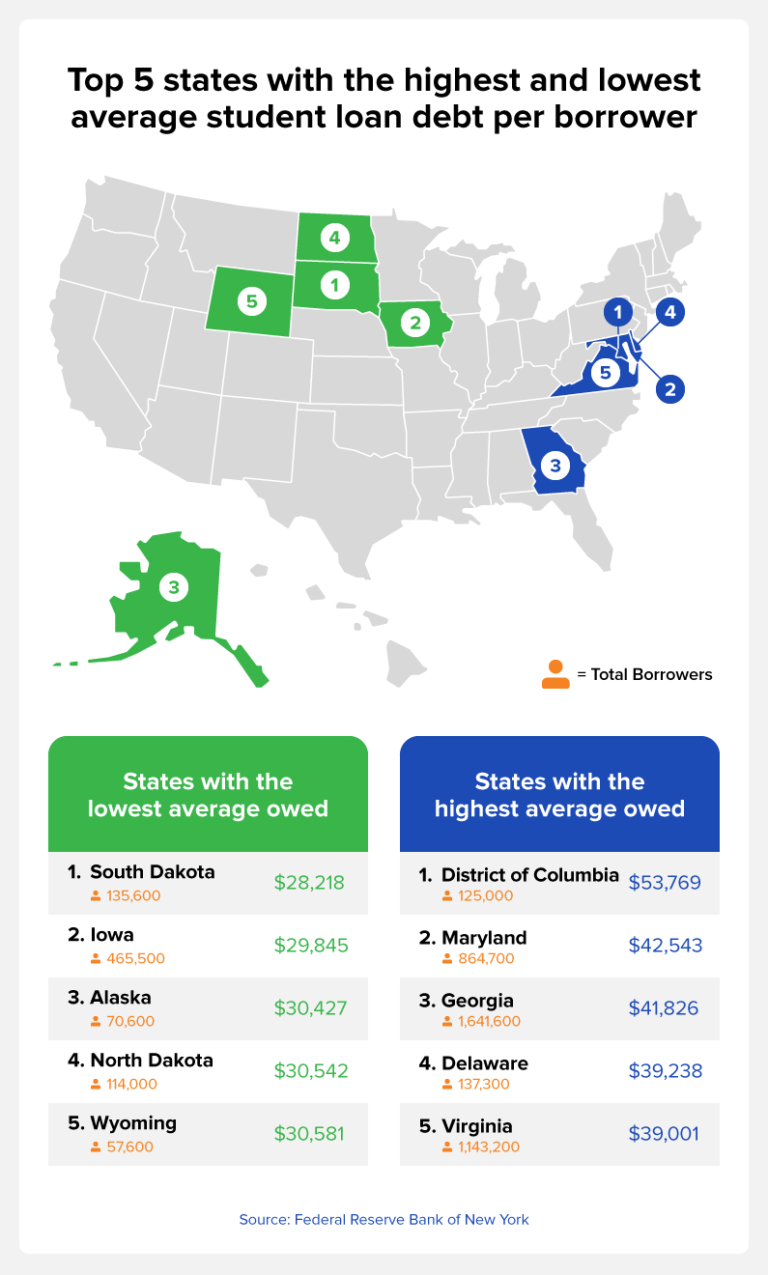

At the end of 2022, the Federal Reserve reported that roughly 43.5 million Americans have student loan debt, which totals over $1.7 trillion. Each borrower owes an average of $37,787.

If you owe tens of thousands of dollars in student loan debt, you’re not alone. According to the Federal Reserve’s Consumer Credit report, 43.5 million Americans have some form of federal or private student loan debt. That’s 13 percent of the population. Not only can you not declare bankruptcy on many forms of student loan debt, but it can also harm your credit.

Here, we’re going to help you better understand the student loan debt dilemma that millions of Americans are facing. We’ll cover both federal and private student loan statistics, which states have the most student loan debt as well as delinquency rates. This will help you see where you stand in comparison to others in a similar situation.

Table of contents:

Average student loan debt

How many Americans have student loan debt?

Student loan debt by state

Total federal student loan debt

Total private student loan debt

Average student loan debt by age group

Student loan repayment status

Student loan default and delinquency rates

Student loan debt forgiveness

Student loan debt FAQ

Average student loan debt

The Education Data initiative is a primary source for tracking data on student loan debt and other educational statistics. In a January 2023 report, their analysis showed that the average debt per borrower was over $37,000 for federal student loans and nearly $55,000 for private loans.

Get matched with a personal

loan that’s right for you today.

Learn

more

Student loan debt has reached new highs in recent years and has been rising since 2007. Less than 20 years ago, the average student loan debt per borrower was just $18,200. This means that by 2022, we saw a 106 percent increase.

Here’s some more interesting data from their report:

Those with a medical degree have an average student loan debt of over $300,000

The least amount of student loan debt is those with a Master of Education, which is $67,500

Stafford loan borrowers owe $25,249 on average

10 percent of borrowers owe more than $100,000 and 45 percent owe less than $20,000

How many Americans have student loan debt?

Over 43 million Americans have student loan debt. The following table from the U.S. Department of Education shows how many Americans have debt by federal loan type.

Year (Q4)

Direct loans (in millions)

Federal Family Education Loans (FFEL) (in millions)

Perkins loans (in millions)

Total (in millions)

2018

34.2

13.5

2.3

42.9

2019

35.1

12.1

2.0

42.9

2020

35.9

11

1.7

42.9

2021

37

10.2

1.5

43.4

2022

37.8

9.2

1.3

43.5

Source: U.S. Department of Education

As you can see, more people are accumulating different types of federal student loans, with a one-and-a-half percent increase in recipients between 2018 and 2022.

Student loan debt by state

The Federal Reserve Bank of New York tracks student loan debt by state. Below, we’ve provided a chart with each state listed in alphabetical order.

The state with the lowest average student loan debt per borrower as of the fourth quarter in 2021 is South Dakota, where borrowers owe an average of $28,218. The District of Columbia has the highest average owed per borrower at $53,769, which is nearly $16,000 higher than the national average.

State

Average balance

Alabama

$37,730

Alaska

$30,427

Arizona

$36,682

Arkansas

$31,851

California

$37,783

Colorado

$37,235

Connecticut

$36,391

Delaware

$39,238

District of Columbia

$53,769

Florida

$38,653

Georgia

$41,826

Hawaii

$34,608

Idaho

$34,196

Illinois

$37,869

Indiana

$32,045

Iowa

$29,845

Kansas

$33,954

Kentucky

$33,155

Louisiana

$34,839

Maine

$33,584

Maryland

$42,543

Massachusetts

$35,400

Michigan

$36,221

Minnesota

$33,161

Mississippi

$36,366

Missouri

$35,095

Montana

$32,459

Nebraska

$31,551

Nevada

$35,688

New Hampshire

$33,094

New Jersey

$37,003

New Mexico

$32,944

New York

$38,668

North Carolina

$37,511

North Dakota

$30,542

Ohio

$35,806

Oklahoma

$32,102

Oregon

$38,248

Pennsylvania

$35,349

Rhode Island

$33,838

South Carolina

$36,698

South Dakota

$28,218

Tennessee

$36,155

Texas

$32,998

Utah

$33,474

Vermont

$34,595

Virginia

$39,001

Washington

$34,846

West Virginia

$32,214

Wisconsin

$31,482

Wyoming

$30,581

States with the most student loan borrowers

The Federal Reserve Bank of New York also tracks how many borrowers there are per state. This gives us a good sense of how many individuals are seeking college degrees, but we should also keep in mind that the cost of living varies in different states as well as how much there is for state funding.

State

Total borrowers

California

4,021,200

Texas

3,759,300

Florida

2,646,400

New York

2,579,600

Pennsylvania

2,032,400

Ohio

1,810,900

Illinois

1,713,900

Georgia

1,641,600

Michigan

1,430,900

North Carolina

1,340,500

New Jersey

1,339,800

Virginia

1,143,200

Massachusetts

1,046,800

Indiana

924,000

Minnesota

902,500

Arizona

872,600

Tennessee

872,000

Maryland

864,700

Missouri

829,100

Washington

816,900

Colorado

804,300

Wisconsin

785,600

South Carolina

745,500

Louisiana

644,600

Alabama

615,800

Kentucky

588,800

Oregon

556,000

Connecticut

542,800

Oklahoma

480,800

Iowa

465,500

Mississippi

414,300

Kansas

395,200

Arkansas

374,900

Nevada

351,300

Utah

325,100

Nebraska

261,000

Idaho

219,400

New Hampshire

219,000

West Virginia

217,200

New Mexico

215,500

Maine

203,200

Rhode Island

153,200

Delaware

137,300

South Dakota

135,600

Montana

132,900

District of Columbia

125,000

Hawaii

123,600

North Dakota

114,000

Vermont

96,300

Alaska

70,600

Wyoming

57,600

States with the highest delinquency rates per borrower

As stated by the U.S. Department of Education, a student loan payment is considered delinquent the first day after missing a payment. If the payment goes unpaid for at least 270 days, the loan then goes into default.

The following are some consequences of going into default:

The entirety of the loan and the interest is due immediately

You lose the ability to obtain additional federal student aid

It will harm your credit score

The state with the highest borrower delinquency rate, `per the Federal Reserve of New York, is Maryland at a rate of 11 percent. This is followed by the state of Washington at 10.7 percent and Utah at 10 percent.

Total federal student loan debt

Included in the U.S. Department of Education’s report is the total amount of outstanding federal and private student loans. Outstanding FFEL loans have dropped over 50 percent since the fourth quarter of 2013, and outstanding Perkins loans have fallen the same amount.

Now, you may be wondering, “Then how is there more outstanding student loan debt than in previous years?” This is due to the rise in outstanding direct loans, which have risen over 133 percent since 2013.

Here’s a look at the past five years of outstanding federal student loan debt:

Year (Q4)

Direct loans (in millions)

Federal Family Education Loans (FFEL) (in millions)

Perkins loans (in millions)

Total (in millions)

2018

$1,150.3

$281.8

$7.1

$1,439.2

2019

$1,242.6

$261.6

$6.1

$1,510.3

2020

$1,315.2

$245.9

$5.2

$1,566.3

2021

$1,375.9

$230.4

$4.4

$1,610.7

2022

$1,422.8

$207.8

$3.9

$1,634.5

Source: U.S. Department of Education

Total private student loan debt

When taking out a student loan, you can receive federal student loans or private student loans. Private student loans aren’t provided by the federal government, and they often come with much higher interest rates. While federal student loans sometimes have forgiveness programs that can help eliminate some of your debt, private loans don’t have the same benefit.

Less than two percent of private student loan borrowers default on their student loans (MeasureOne)

The average interest rate on private loans is between four and 15 percent (Education Data Initiative)

Refinancing a private student loan can range between 2.25 to 12 percent (Education Data Initiative)

53 percent of private loan borrowers did not borrow the maximum amount of Stafford loans (TICAS)

11 percent of these borrowers didn’t apply for federal financial aid (TICAS)

Average student loan debt by age group

The debt among Americans is divided by age group in the U.S. Department of Education report, and it shows that people ages 35 to 49 owe the most in federal student loans. While this age group owes a total of $634 billion, those under 24 years of age only owe $104 billion, followed by people 62 and older at $107 billion.

Age group

Total outstanding loan balances (in billions)

Under 24

$104

25 to 34

$497

35 to 49

$634

50 to 61

$293

62 and older

$107

Source: U.S. Department of Education

Student loan repayment status

While many Americans are paying their student loans on a monthly basis, for a variety of reasons, some people may need to apply for a deferment or forbearance. If you’re facing financial hardships, you can apply for these services to pause your loan payments. It’s also helpful to know that you may still accrue interest while in forbearance or deferment.

The following table shows the total number of Americans by loan status as per the U.S. Department of Education during the fourth quarter in 2022:

Loan status

Recipients (in millions)

Currently in school

6.3

In grace period

1.3

Repayment

0.4

Deferment

3.0

Forbearance

25.6

Cumulative in default

4.8

Other

0.1

Source: U.S. Department of Education

Student loan default and delinquency rates

When graduating from college, it can take some time for people to begin making enough money to pay back their student loans. But remember, missed payments turn delinquent the day after missing the first payment and then go into default after 270 days.

Here are some notable statistics from the Education Data Initiative:

The majority of borrowers have at least one late payment in the first five years of repayment

Over 40 percent of borrows in default status owe between $20,000 and $40,000

Almost 11 percent of borrowers default within their first year of repayment

Less than 20 percent of borrowers are delinquent at least five times

Graduates with Arts and Humanities majors have the highest default rate at 26 percent

Student loan debt forgiveness

The most common form of federal student loan forgiveness is the Public Student Loan Forgiveness Program (PSLF). This is a student loan forgiveness program for a variety of different service jobs. According to the PSLF website, there are no specific jobs, and all a company needs to do is qualify for PSLF. Although there are no specific jobs listed, here are some of the typical careers that qualify, as reported by Kristen Kuchar at SavingforCollege.com:

Law enforcement

Public health

Education

Social work

Emergency management

Public safety

Government jobs

PSLF releases a monthly report with some interesting information. The following is data from their December 2022 report:

There were 1.8 million forms processed for people qualifying for PSLF

Of the more than 1.9 million forms processed, 88,202 did not qualify for PSLF

The largest portion of borrowers qualified for income-driven repayment, which allows for lower payments based on current income

34,000 people who applied have employers that do not qualify for PSLF

The primary sector qualifying for PSLF is government employees, who accounted for 61 percent of the processed forms

Student loan debt FAQ

We’ve covered a lot of data about student loan debt statistics in America, but you may have some lingering questions. Below is a list of some frequently asked questions, along with their answers.

What is the average student loan debt in 2023?

The average American graduate owes $37,787 in student loans.

Who suffers the most from student loan debt

According to the Education Data Initiative, Black and African American graduates owe $25,000 more than white graduates on average. About 48 percent of these former students also owe six percent more than they borrowed.

Is student loan debt increasing or decreasing?

The credit bureau Experian® shows the average student loan balance increased 91 percent between 2009 and 2022.

Who owns the most student loan debt?

As of September 2022, the U.S. Department of Education reported that people ages 35 to 49 owe the most student loan debt at a total of $634 billion.

Don’t let student loan debt affect your credit score

If you’re having trouble paying your student loan debt, you’re not alone. With 4.8 million Americans in default and 28.6 million in deferment or forbearance status, it’s clear to see that many people are in the same situation. Unfortunately, not paying your student loan debt can harm your credit score, which can make your financial life difficult and cause additional stress.

Fortunately, Credit.com is here to help. We offer different tools that can help you work to repair and improve your credit. We’re also here to help you learn how to manage your debt so you can make your payments on time and avoid any dings to your credit in the future. If you’re curious about your current credit status, sign up for your free credit report card today.

Visa and Mastercard are both card networks. Both organizations manage the payment networks through which their cards work. Visa and Mastercard are different companies, but they operate in a very similar way.

Four credit card networks tend to compete for space in consumer wallets. They are Mastercard, Visa, Discover and American Express.

According to Statista, Mastercard and Visa have had the largest market share for a while. As of 2021, they accounted for more than 87% of the market. Compare that to Amex’s 10.5% and Discover’s 2.2% and you can see that most credit cards are Mastercard or Visa.

But is one better than the other? Are there really any differences between these two major credit card networks? Find out in our guide to the difference between Mastercard and Visa below.

In This Piece

What’s the Difference Between Mastercard and Visa?

While they’re both credit card processing networks, these are unique and separate companies. They were founded at different times.

Originally known as the BankAmericard credit card program, Visa launched in 1958. Mastercard began as Master Charge: The Interbank Card when it emerged as a BankAmericard competitor in 1966.

Visa cards don’t work on the Mastercard network, and vice versa. You can’t, for example, use a Visa to pay for something in a store that only accepts Mastercard.

How Are Visa and Mastercard Similar?

There are more similarities between Visa and Mastercard than differences. As mentioned earlier, these are both card networks. They both play the middleman between payment processors and issuing banks.

Both companies operate globally, so if you alert your issuer in advance, you should be able to use your Visa or Mastercard in another country when you go on vacation. Whether you pay fees for this service depends on your card issuer and account details—not on Visa or Mastercard.

Both Visa and Mastercard have tens of millions of merchants in their networks, and both companies’ merchant fees are comparable. Both organizations are publicly traded.

What’s the Difference Between a Network and an Issuer?

The credit card network is the middleman between the payment processor and the issuer of the card. When you pay with a credit card, the information is processed through the network to the bank that issued your credit card. On the other side of the transaction, the data that supports the funds transaction is also processed through the network.

Visa and Mastercard are credit card networks. They’re responsible for the infrastructure for these transactions and for protecting the information as it passes between the payment processor and the issuer. For this service, the credit card networks charge a fee—usually paid in part via a small percentage of every transaction.

An issuer is the bank that issues the card. Examples include Chase, Citibank and Capital One. The issuer is the entity that decides whether you’re approved for a credit card and sets interest rates and fees. It’s also the lender that pays for the goods you purchase with your credit card and the entity you pay back with your payments.

How Does Payment Processing Work?

Visa and Mastercard credit card and debit card payments all go through the same payment process—albeit on different networks. The process looks like this:

Consumers swipe cards—or tap contactless cards—in physical stores or enter card details online.

Merchants send payment authorization requests to their payment processors.

Payment processors send payment requests to the appropriate card network.

Card networks “ask” issuing banks for payment authorization.

Issuing banks approve or deny the transaction.

At this point, transactions are—hopefully—authorized, but they’re not settled yet. The process must continue:

Merchants send approved payment requests to payment processors in batches.

Once again, payment processors send transaction details to Visa, Mastercard or other applicable card networks.

Card networks “ask” issuing banks for previously authorized funds.

Issuing banks release the funds, which travel to merchant banks.

Credit card processing network fees get taken out along the way.

Merchant banks transfer funds into individual merchant accounts.

At this point, the store or other merchant has been paid for the goods or services you bought with your credit card. Your next statement should also reflect the purchase.

Other Mastercard vs Visa Similarities

Visa and Mastercard issuers have a range of products to choose from. Debit cards let you spend money already in your bank account—plus your overdraft if you have one set up. Meanwhile, you must fund prepaid cards in advance.

Visa or Mastercard credit cards have the following things in common.

1. Credit Scores Matter

Card issuers make decisions based on consumers’ credit scores. If you want a card with an extra-low APR and a really high credit limit, you’ll need a top-notch credit score. Lower credit scores generally mean lower credit limits and higher interest rates.

If you’re new to credit or you need to repair your credit, look for a credit builder or credit repair card. You won’t have a very high limit to begin with, and your APR might not be very competitive, but if you make regular payments, you’ll soon qualify for a better product.

Surge Mastercard® Credit Card

All credit types welcome to apply!

Monthly reporting to the three major credit bureaus

Up to $1,000 credit limit doubles up to $2,000! (Simply make your first 6 monthly minimum payments on time)

Fast and easy application process; results in seconds

Use your card at locations everywhere that Mastercard® is accepted

Free online account access 24/7

Checking Account Required

See if you’re Pre-Qualified without impacting your credit score

2. Rewards Cards Provide Value

Mastercard and Visa both partner with issuers that offer rewards cards. Rewards include air miles, points, store-specific rewards, food and beverage rewards and cash back. If you use your rewards card in a savvy way, you can save a lot of money.

3. Fees Vary

Visa and Mastercard don’t set fees—issuing banks do. As a result, fees for Visa and Mastercard products vary widely. Make sure you’re familiar with the over-limit, balance transfer, late payment, and foreign transaction fees on each of your credit card accounts—and stay away from credit cards with unreasonable fee structures.

4. Smart Wallets Protect Information

Both Visa and Mastercard cards are compatible with smart wallets like Apple Pay and Google Pay. Smart wallets hide your card information, so they’re more secure than swiping a card or entering card details online. Every year, more and more brick-and-mortar and online retailers accept smart wallet payments.

5. Discount Programs Save You Money

Some credit cards—especially business credit cards—incorporate high-value discount programs. The Visa SavingsEdge program, for example, can save you more than 15% when you shop with qualifying merchants. Mastercard has a similar program, called Easy Savings. In both cases, you need to enroll your card to get money back.

Which Is Better: Visa or Mastercard?

What’s the difference between Mastercard and Visa? Not that much, actually. The major difference is the company that runs the network. Merchants that accept one usually tend to accept the other, and more merchants accept Visa and Mastercard than any other type of card.

Instead of considering whether you should get a Visa or a Mastercard, think about what type of card you want and which bank you want to work with. Apply for a card that offers the rewards you want and has fees that match your budget. Whichever one you choose, you’ll be able to use it around the globe and get a very similar experience from the card network.

Today was a rough day for mortgage rates as the market digested the Fed’s latest outlook, which confirmed its inflation fight is far from over.

While they didn’t raise their own fed funds rate yesterday, they did leave the door open for another hike in the future, assuming economic data warrants it.

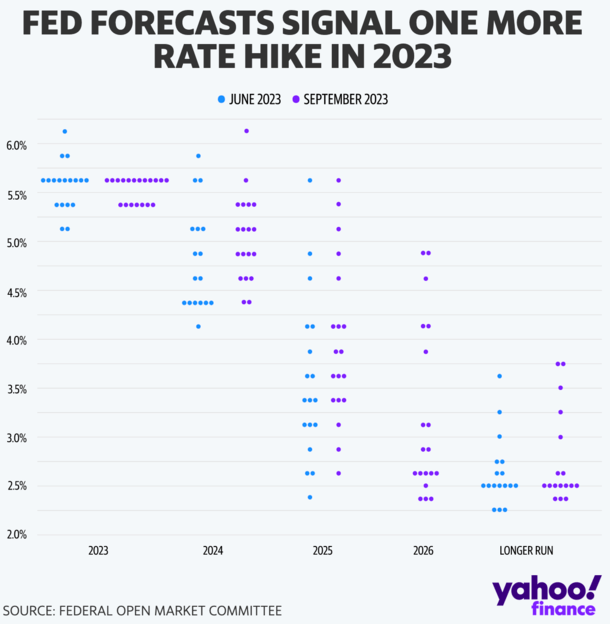

Their overall stance actually didn’t change, but their so-called “dot plot” revealed that more of the Federal Reserve’s policymakers expect another rate hike this year.

Granted, it appears only one more quarter percent (0.25%) hike is in the cards at this juncture.

So while we might be going higher, it might only be a tiny bit higher. And after that, there may be more certainty for mortgage rates.

Higher Mortgage Rates for Longer, However…

After the Fed’s announcement, everyone seemed to adopt a simple takeaway: “higher for longer.”

In other words, most don’t expect the Fed to pivot and begin loosening monetary policy anytime soon.

There had been some hope that we were at the terminal rate, where the Fed stops hiking. But maybe not just yet.

As it stands, the Fed has raised their own fed funds rate 11 times since early 2022, and mortgage rates have risen along with those hikes.

While the Fed doesn’t control mortgage rates, its policy decisions can affect the direction of long-term interest rates, such as those tied to 30-year fixed mortgages.

Simply put, they don’t set the rate on your 30-year fixed, but what they say or do can push rates higher or lower.

Of course, their decisions are rooted in economic data, so it’s really the economy that’s dictating the direction of mortgage rates.

Anyway, some market watchers were hopeful the Fed was done hiking rates prior to the announcement yesterday.

And again, while they did hold rates steady, the dot plot indicated one more hike could be in the cards before the end of the year.

The Dot Plot Got Worse

These individual estimates from the dot plot also moved higher for 2024 and 2025, meaning rates may have to stay where they’re at for a bit longer than expected.

However, what does higher actually mean? Does it mean one more 0.25% rate hike from the Fed, but nothing beyond that.

And how does that translate to mortgage rates? On the one hand, it’s another rate hike, but mortgage rates only take cues from the Fed’s monetary policy.

If the Fed follows through with one more hike, but also signals that it’s done hiking, mortgage rates could breathe a sigh of relief.

Continue to Watch the Economic Data, Not the Fed Announcements

While the initial reaction to the Fed’s latest forecast was not good news for mortgage rates, or the stock market for that matter, it’ll be interesting to see what transpires once the dust settles.

Economic data had been mostly improving recently, in the sense that inflation was trending lower, which is the Fed’s primary objective.

But there were some hiccups recently, including lower-than-expected jobless claims, pointing to more economic resiliency.

However, if weaker economic data continues to come down the pipe, the Fed will be less inclined to raise its own rate and perhaps provide more clarity on future policy.

In that sense, not much has really changed here. The Fed is still data-dependent as it has always been.

Instead of watching Jerome Powell’s pressers, you may want to continue looking at the data that comes in, whether it’s the CPI report or jobs report. This is more important than looking at the dot plot.

Assuming the data continues to show a cooler economy, interest rates may not rise much more, and could simply linger at these higher levels.

But until we see consecutive reports showing a real drop in inflation, it’s going to be more of the same.

More Certainty from the Fed Could Keep Mortgage Rates in Check

Lastly, we’ve got very wide mortgage spreads, which is the difference between the 10-year Treasury yield and the 30-year fixed.

It’s been close to 300 basis points for a while now, nearly double the long-run average of 170 bps.

If the Fed is able to provide more clarity on their policy by year-end, it might allow this spread to narrow. And that could offset any additional upward pressure on mortgage rates.

It’s somewhat bittersweet, but it could prevent the 30-year fixed from going even higher, say to 8%.

With the 10-year yield around 4.50 and the spread currently about 300 bps, 30-year fixed rates are hovering around 7.5%.

If that spread can come down to say 250 bps, you might get a mortgage rate back in the 6s, or at least offset any additional increases.

Tip: The prime rate, which is tied to HELOCs, moves in lockstep with the fed funds rate. So those with open-ended second mortgages have seen their rates go up each time the Fed raised its own rate.

Mortgage rates remained well above 7% on Thursday as markets digested Wednesday’s Fed meeting.

Freddie Mac‘s Primary Mortgage Market Survey, which focuses on conventional and conforming loans with a 20% down payment, shows the 30-year fixed rate averaged 7.19% as of Sept. 21, up one basis point from last week’s 7.18%. By contrast, the 30-year fixed-rate mortgage was at 6.29% a year ago at this time.

“Mortgage rates continue to linger above 7% as the Federal Reserve paused their interest rate hikes,” Sam Khater, Freddie Mac’s chief economist said.

Elevated mortgage rates weigh negatively on the housing demand, and by extension on homebuilders, Kharter added.

“Builder sentiment declined for the first time in several months and construction levels have dipped to a three-year low, which could have an impact on the already low housing supply,” he noted.

Other indices showed different mortgage rates this week.

HousingWire’s Mortgage Rates Center showed Optimal Blue’s 30-year fixed rate for conventional loans at 7.22% on Wednesday, compared to 7.16% the previous week. At Mortgage News Daily on Wednesday, the 30-year fixed rate for conventional loans was 7.33%, up from 7.22% the previous week.

Members of the Federal Open Market Committee expect interest rates to remain elevated for longer than had been expected

The Fed paused its rate hikes yesterday as several economic indicators — including the improved core CPI figures, lower job openings, and higher unemployment rate — point towards a cooling economy. However, members remained cautious and the committee’s updated outlook implies a forthcoming monetary policy that is “tighter for longer,” Jiayi Xu, economist at Realtor.com said.

“With the year-end projection for 2023 remaining at 5.6%, we are drawing closer to another potential rate hike as the year approaches its end,” she said.

Furthermore, the expected policy rate for the conclusion of 2024 and 2025 is now half a percentage point higher than what was anticipated back in June, reinforcing the trend toward a more restrictive monetary policy in the path forward.

While higher interest rates indicate additional hurdles to come for the housing market, the fall typically ushers in more favorable buying conditions compared to the rest of the year, according to Xu.

“For those looking to purchase a home in this tough year, the first week of October will emerge as the best time to make a move,” Xu said.

Historical data suggests that during this particular week, home prices tend to dip below their peak levels, competition subsides, and the housing inventory expands compared to the busy summer months, she explained.

Meanwhile, homebuyers who can’t afford to buy a house in today’s market can rely on renting as rental prices are going down.