Fixed rate mortgages have dipped below 5 per cent for the first time since early July, offering some hope to struggling homeowners.

Yorkshire Building Society has launched a 4.99 per cent fixed-rate deal which is available to both home buyers and those remortgaging.

It’s available at 75 per cent loan-to-value, meaning eligible customers can apply as long as they either have at least a 25 per cent deposit or 25 per cent equity within their home.

Best rate: Yorkshire Building Society has launched a 4.99 per cent fixed rate deal aimed at both homebuyers and those remortgaging

Someone with a £200,000 mortgage could expect to pay £1,168 a month if repaying over a 25-year term, compared to the market average of £1,249 a month.

The five-year deal comes with a £1,495 fee, however, and a mortgage with a higher rate but a lower fee may be a better deal for some customers.

You can compare rates and fees and work out the true cost of a mortgage using our calculator.

After Yorkshire BS, the next best deal is Virgin Money which has a five-year fix at 5.07 per cent and is available to home buyers purchasing with at least a 35 per cent deposit (65 per cent loan-to-value).

HSBC has a five-year fix at 5.09 per cent for home buyers with at least a 40 per cent deposit (loan-to-value of 60 per cent).

Nationwide also has a 10-year fix available at 5.04 per cent which is available to home buyers with a deposit of 15 per cent or more (85 per cent loan-to-value).

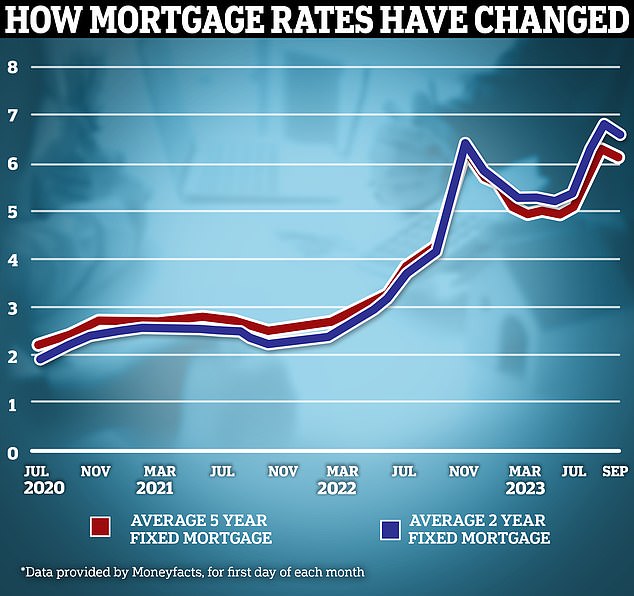

The average five-year fixed mortgage rate is now 5.67 per cent, according to Rightmove.

Rachel Springall, finance expert at Moneyfacts said: ‘It’s great to see such competitive deals launched by Yorkshire Building Society.

‘Borrowers looking for a new low-rate mortgage will find the sub-5 per cent five-year fixed deal is the lowest rate available in its sector.

‘The incentive packages available across all the new deals today may also be popular with borrowers looking to save on the upfront cost of their mortgage.’

Why are mortgage rates going down?

Yorkshire BS’ decision to cut rates, which includes shaving off up to 0.46 percentage points from its 95 per cent loan-to-value deals, is partly due to competition between lenders.

HSBC has also slashed mortgage rates by 0.15 percentage points on average today, alongside rate cuts across its buy-to-let range of up to 0.3 percentage points.

Last week there were also cuts from Coventry BS, Nationwide BS, Accord, Generation Home, Barclays, and Clydesdale Bank.

Past the peak? Fixed mortgage rates appear to be falling back somewhat after a barrage of rate hikes in recent months

Rate cuts have also been encouraged by future market expectations over where interest rates are heading.

Market expectations are reflected in swap rates. These are agreements in which two counter parties, for example banks, agree to exchange a stream of future fixed interest payments for a stream of future variable payments, based on a set amount.

Mortgage lenders enter into these agreements to shield themselves against the interest rate risk involved with lending fixed rate mortgages.

Put more simply, swap rates show what financial institutions think the future holds concerning interest rates.

Five-year swaps are currently at around 4.56 per cent, which is down from 4.74 per cent at the start of this month.

Only as recently as July, five year swaps were above 5 per cent. Similarly, the two-year swap rate is now 5.21 per cent. In July early this was around 6 per cent.

Ben Merritt, director of mortgages at Yorkshire Building Society, said: ‘This week, favourable market swap rates presented just such a window to reduce our mortgage costs, and offer the greatest incentive to those people who typically struggle the most, those with the lowest deposits to put down, including first-time buyers.’

Nicholas Mendes, mortgage technical manager at broker, John Charcol says he wouldn’t rule out a five-year fix at 4.5% by the end of the year

Will mortgages be hiked again if base rate rises?

The Bank of England is widely expected to increase the base rate from 5.25 per cent to 5.5 per cent on Thursday, though some economists are betting on it remaining the same.

The decision will come the day after we learn August’s inflation reading, which many are expecting may go up as a result of higher fuel prices. This may have some bearing on what the Bank of England decides to do with base rate.

If base rate does go up, this will likely increase costs for those on variable rate mortgage deals.

However, it is unlikely to have the same impact on fixed rate products, according to Nicholas Mendes, mortgage technical manager at broker John Charcol. In fact, he expects fixed rate deals to continue falling.

‘The MPC meeting is expected to either hold or rise by 0.25 per cent which will no doubt be the last [rate rise],’ says Mendes.

‘Even in the event there is a rate rise this has already been caked into fixed rate pricing.

‘As a result I expect to see fixed rate pricing on two and five year fixes continue to reduce.

‘While no one can accurately be confident, I wouldn’t rule out a five year fixed at 4.5 per cent by the end of the year based on current pricing trajectory.’

How are mortgage rates affecting the housing market?

While it is good news that mortgage rates are falling, we remain a long way from the low rates enjoyed in previous years.

This time last year, it was possible to secure a fixed rate at 3 per cent and the year before that borrowers were able to secure deals at less than 1 per cent.

The change in mortgage rates has unsurprisingly had an impact on the housing market. Transactions are down by almost 20 per cent, while house prices are also falling.

Last week it was reported that mortgage arrears had hit their highest level for nearly seven years.

The value of outstanding home loans with arrears climbed by 13 per cent to £16.9billion in the second quarter of this year, according to Bank of England figures.

It was the highest level since the third quarter of 2016, and 29 per cent higher than the same period a year ago.

Although there may be less activity across the housing market, Mendes says he isn’t expecting to see a sudden surge in forced sales.

‘Fixed rate mortgages around 5 per cent may dampen purchase demand as prospective home movers postpone their plans, but I still expect to see first-time buyers to continue purchasing,’ he says.

‘With rents continuing to increase, fixed rates at 5 per cent or less could encourage more first time buyers and those in rented accommodation to purchase as a cost-effective alternative.

‘A significant increase in arrears was down to landlords which is understandable in this climate over the past year.

Downwards: Over the past few weeks, mortgages rates have continued to trickle downwards due to competition between lenders and market expectations about interest rates in the future

‘For residential homeowners there are more options to avoid falling into arrears – unless they decide to bury their head in the sand.

‘There is more support from lenders and the Mortgage Charter which allows a grace period of six months which would allow mortgage holders to sell a property before things start to escalate downwards.’

Mark Harris, chief executive of mortgage broker SPF Private Clients, says that falling mortgage rates will result in buyers being able to afford bigger mortgages which should lead to an increase in transactions.

Harris adds: ‘Falling interest may encourage more borrowers to take the plunge and take on a mortgage. However, it is not just about falling mortgage rates but affordability and the underwriting of the loan.

‘Lenders are still required to stress test the borrowing at a minimum of 1 per cent above the reversion rate, with some lenders utilising different lower rates for long/longer term fixes.

‘When these stress rates also start to fall, borrowers will be able to take on bigger mortgages, which may lead to an uptick in transactions and mortgage lending.’

Finding out how much you’ve spent with a credit card probably isn’t anyone’s favorite task; nevertheless, it’s an important one for optimal financial health.

Checking your credit card balance is the only way to know how much you must pay the card issuer in order to avoid interest charges. As credit card APRs are notoriously high, paying off your credit card bill in full and on time saves you money — and preserves your credit scores.

Regular check-ins on your credit card account can also help you stay on budget and be more mindful of your spending habits.

Credit card issuers want to get paid, so they offer a variety of ways for cardholders to check their credit card balance, some of which are surprisingly low-tech.

Here’s how to do it.

What is a credit card balance?

At the most basic level, a balance on a credit card refers to the amount a cardholder owes to the card issuer, say, Barclays or Chase. There are a few different types:

Statement balance. The amount owed at the close of a billing cycle, which is usually 28-31 days long. The statement balance will appear on the credit card statement. Issuers may send electronic statements or hard copies via mail.

Current balance. Also known as an outstanding balance, the current balance is the amount you owe at the moment you check your account. It may or may not be the same as your statement balance, depending on your card usage and your payments in between billing cycles

Negative balance. If your account has a negative balance, you don’t owe the issuer anything. On the contrary, a negative balance indicates that the issuer owes you.

Ready for a new credit card?

Create a NerdWallet account for insight on your credit score and personalized recommendations for the right card for you.

How do you check your credit card balance?

There are many ways to check your credit card balance; pick the one that’s most convenient for you.

Log into your account online.

Log into your account via the issuer’s app.

🤓Nerdy Tip

If you want to know your current balance and statement balance, check your account online or in the app. Some credit card statements may not show both.

Review your credit card statement. An electronic statement may be accessed online or in the app, or you can request a paper statement. Note that some issuers charge a fee to send copies of credit card statements.

Call the issuer at the number on the back of your credit card.

Ask a representative in person. For example, if you have a Bank of America®-issued card, you could ask for your statement balance at a local branch. Want to know the balance on a store credit card such as a Macy’s card? Head to the closest store and ask one of the employees to look up your credit card balance.

Balance alerts. Some issuers allow cardholders to receive alerts that notify them when their credit card balance hits a certain amount. Alerts can usually be sent via text or email.

Michael Barr, vice chair for supervision at the Federal Reserve, said during an open meeting on the proposed Basel III endgame proposal that the central bank will “collect additional data to refine our estimates of the rule’s effects.” Banking trade groups have asked regulators to rescind the proposal and launched a public relations offensive against the proposal, including media buys.

Bloomberg News

The banking industry and its allies are ramping up their efforts to combat federal regulators’ plan to increase capital requirements on banks with at least $100 billion of assets.

Initially opting for a passive approach focused on research papers and a website dedicated to sussing out the “price tag” of higher capital requirements, bankers and bank lobbyists are taking the fight to regulators more directly through advertising campaigns and procedural challenges.

“The industry appears more willing to battle the regulators on this issue than any in recent memory, which suggests that we could see litigation on the other side of the rule being finalized,” said Isaac Boltansky, director of policy research at BTIG.

On Tuesday, several top banking and financial industry groups sent a joint letter to the Federal Reserve, Federal Deposit Insurance Corp. and Office of the Comptroller of the Currency asking them to issue a new proposal for their so-called Basel III endgame package to close data-disclosure gaps. The groups accuse the agencies of drawing from “nonpublic” data for their proposals, thus violating standards of the Administrative Procedure Act, or APA.

“To remedy this violation, the agencies must make available the various types of missing material — along with any and all other evidence and analyses the agencies relied on in proposing the rule — and re-propose the rule,” the groups wrote. “To remain consistent with what the agencies themselves have determined to be an ‘appropriate’ comment period, the agencies should provide for a new 120-day comment period in the re-proposal.”

Representatives from the Fed and OCC declined to comment on the letter. The FDIC did not respond to an interview request on Tuesday.

The letter was co-signed by the Bank Policy Institute, American Bankers Association, Financial Services Forum, Institute of International Bankers, Securities Industry and Financial Markets Association and the U.S. Chamber of Commerce. It cites several violations of “basic legal obligations” under the APA, potentially setting the stage for a legal challenge should the proposal be enacted.

Boltansky said it is unlikely that the letter will actually compel regulators to issue a new proposal, but he said it could make them think twice about finalizing the rule as is.

“It is difficult to envision the banking regulators pulling and reproposing, but the letter from industry groups will add even more pressure for the standard to be softened prior to finalization,” he said.

The letter comes less than a week after BPI, which represents banks with more than $100 billion of assets, launched its “Stop Basel Endgame” advertising campaign, a nationwide push to draw attention to the risks the rules present to the banking sector, the U.S. economy and individual households. The effort includes print and radio ads in Washington, D.C., and other select markets as well as targeted online ad buys.

“The current Basel proposal is unacceptable, and BPI is committed to ensuring that lawmakers, regulators and the public fully understand how this proposal will affect every person and every business in this country,” BPI President and CEO Greg Baer said. “The largest media campaign in the organization’s history is underway, and our goal is to force regulators to justify to the public why they are imposing these costs and pushing still more economic activity into the shadow banking system.”

Banks themselves have gotten in on the effort to undermine recent regulatory proposals, which call for additional risk-weighted capital requirements and new resolution standards for banks between $100 billion and $250 billion of assets. On Tuesday, Goldman Sachs released a survey of small-business owners in which 84% of respondents said they were “concerned that the proposal will negatively impact their ability to access capital in an already difficult market.”

On Monday, JPMorgan Chase CEO Jamie Dimon ripped the proposal during an on-stage appearance at Barclays Global Financial Services Conference, calling it “hugely disappointing.”

In fiery remarks, Dimon said the proposed risk capital rules would result in U.S. banks facing more stringent regulatory obligations than their international peers, undermining the initial goal of the international standards on bank regulation. “What was the goddamn point of Basel in the first place?” he said.

Dimon said the rules would likely drive certain activities — including mortgage lending and financing leveraged lending by nonbanks — out of the banking sector entirely. He argued that if that is the intended outcome the Fed, FDIC and OCC had in mind, they should have said so explicitly, adding that the proposal marks a low point in relations between banks and their regulators.

“I’m not sure it’s a great thing that we have this constant battle with regulators as opposed to open, thoughtful things. We used to have real conversation with regulators — there is none anymore in the United States. Like, virtually none,” he said. “This stuff is just all from up top and imposed down below. And then … we simply have to take it. They’re judge, jury and hangman, and that is what it is.”

Proponents of the potential changes say the all-out push by bankers and industry groups to combat the proposal was to be expected.

“Wall Street’s latest attack on these modest and sensible rules is as baseless as it is unsurprising,” said Dennis Kelleher, head of the consumer advocacy group Better Markets. “Wall Street is going to do and say anything to try to stop any increase in capital, no matter how baseless or false.”

Regulators released their risk-capital proposal at the end of July along with a potential change to their global systemically important bank, or GSIB, surcharge that could have a meaningful impact on some foreign banks.

Much of the 1,000-page Basel III endgame proposal is focused on justifications for the rule changes, including recent bank failures and disparate treatments of operational risks by large banks. Currently, banks are able to rely on internal models for managing these risks which, the documents notes, “include a degree of subjectivity, which can result in varying risk-based capital requirements for similar exposures.”

The Fed estimates the changes will lead to a 16% aggregate increase in capital requirements for the affected banks, with the largest burden falling on GSIBs, which are set to see their capital obligations increase by 19%.

Dimon, however, said the actual increase will be closer to 25% by JPMorgan’s calculations, though the exact impacts of the potential changes have been a subject of debate since they were proposed. Fed Vice Chair for Supervision Michael Barr, in remarks made during a public meeting about the proposals, said the central bank intends to “collect additional data to refine our estimates of the rule’s effects.”

The recent push by bank trade groups adds to the mounting opposition that has been building against the Fed’s capital proposal for the past year. Republicans and some moderate Democrats in Washington questioned whether new rules were necessary in the months before the proposal was rolled out, and thus far the proposal has few vocal champions on Capitol Hill.

But regulators do not need the backing of Congress to enact the rule changes, which fall within the regulatory framework codified by the Dodd-Frank Act of 2010 and modified by the Economic Growth, Regulatory Relief and Consumer Protection Act of 2018.

Kelleher said bank failures earlier this year underscore the importance of having a well capitalized banking system. He added that the rule changes would apply additional protection from the highest-risk activities at the 35 biggest banks in the country.

“It’s no different than when banks require their customers to put up a down payment when they buy a house,” he said. “The homeowner then has to absorb the first 20% of losses on the house, which protects the bank from losses. The American people should be protected as well.”

Strong household spending and a resilient labor market could help the U.S. economy avoid a recession in 2024, the American Bankers Association’s Economic Advisory Committee says.

Jamie Kelter Davis/Bloomberg

Resilient household spending and a strong labor market will likely help the U.S. economy avoid a severe recession, according to a new forecast from economists at some of the country’s biggest banks.

The economy is poised to grow at a rate of less than 1% through the second quarter of 2024, the American Bankers Association’s Economic Advisory Committee said Monday. That is low compared with the second quarter rate of 4.1% but well above the dire predictions some economists once harbored for 2024.

“The odds of a soft landing have improved quite dramatically in the near term,” said Simona Mocuta, chief economist at State Street Global Advisors and the chair of the ABA’s committee of economic advisors.

The specter of recession has weighed on banks for close to 18 months, since the Federal Reserve began its campaign of rate hikes in March 2022. The health of the U.S. economy plays a key role in the profitability of banks, so the prospect of a contraction in economic growth raised red flags for banks large and small. The likely avoidance of one of the harsher economic scenarios — a severe recession — is good news for banks, which are also contending with generally tighter profit margins and increasing competition for customers.

Robust consumer spending has helped boost the U.S. economy so far in 2023, the ABA economists noted. Low unemployment and strong wage gains mean households have been able to keep up with many of their spending habits, even as inflation has persisted.

Inflation is also expected to improve in the coming quarters. Big-bank economists anticipate inflation levels to continue to cool to an annualized rate of 2.2% by the second quarter of 2024, close to the central bank’s target rate of 2%.

Although the overall economic picture is brighter, economists warn that there are several lingering threats that could make it more difficult for the U.S. economy and banks alike to grow.

The economists expect businesses to invest less capital in the short term, which could weigh on loan growth at banks. Loan growth at U.S. commercial banks increased 4.5% in the second quarter from a year earlier, according to Federal Deposit Insurance Corp. data.

About 4.4% of the labor forcewill be unemployed by the end of 2024, according to the economists’ forecast. A higher unemployment rate could make it more difficult for laid-off workers to make loan payments, potentially boosting the level of charge-offs at banks.

Credit quality reached historic lows during the pandemic, when many creditors offered grace periods and other breaks to struggling borrowers until the economy got back on track. Analysts expect asset quality to continue to deteriorate, with loan-loss increases spreading beyond the credit card and commercial real estate arenas.

“Investors are eager to learn how much higher net charge-offs are expected to go, especially with the student loan moratorium coming to an end,” Jason Goldberg, managing director and senior equity analyst at Barclays, wrote in a recent research note.

Certain elements of the ABA’s advisory committee’s forecast provide a strong contrast to the details issued when the last forecast was issued earlier this year, when economists believed the U.S. was on the edge of a mild recession.

“The tone of the conversation certainly feels much more positive today,” Mocuta said.

The ABA committee includes economists from some of the country’s largest banks. The group meets twice a year to discuss the economic environment and issue forecasts on economic growth, inflation and the trajectory of interest rate moves.

This year’s committee features representatives from U.S. Bank, Wells Fargo, JPMorgan Chase, State Street, Comerica Bank, BMO, TD Bank, PNC Financial Services, Deutsche Bank, First Horizon, Regions Financial, Northern Trust, Wilmington Trust and Morgan Stanley.

Lesley Alli and Andrew Greenberg both joined NMI Holdings to serve as senior vice presidents, announced the parent company of National Mortgage Insurance Corporation Monday in a statement.

Adam Pollitzer, president and CEO of National MI, said that the addition of Alli and Greenberg would help drive value for borrowers, lenders and shareholders.

“We’re delighted to have two executives as talented and experienced as Lesley and Andrew join our strong executive management team,” said Pollitzer in a statement.

Alli was named senior vice president of industry relations and corporate communications. In this role, she will lead the company’s efforts in external public and industry relations, touching on corporate communications, public policy, government enterprise and agency affairs. Prior to this new position, she served as the chief investor and industry relations officer of Home Point Financial Corporation. She also held senior managerial positions at Federal National Mortgage Association (Fannie Mae) and Countrywide Home Loans, amounting to a 20+ years career in the mortgage industry.

Alli also received numerous accolades in her field: she was recognized as one of Housing Wire‘s 50 “Women of Influence” in 2021.

Meanwhile, Greenberg was promoted to senior vice president of finance where he will oversee investor relations, financial planning, analysis, data analytics and treasury. He previously served as senior vice president of business development and investor relations at Triton International Limited, a leading publicly-traded specialty finance company. From 2002 to 2014, Greenberg was a director of investment banking with Barclays where he led strategic advisory and capital raising efforts for financial institution clients.

XBOX is launching a new no annual fee credit card in partnership with Barclays. With the Xbox Mastercard credit card, players can earn card 5x points on Microsoft purchases and 1x on everyday purchases to redeem at xbox.com. The Xbox Mastercard will be available to Xbox Insiders in the US beginning on September 21, with availability to all Xbox players coming in 2024.

Press Release | Terms

Contents

Signup Bonus

Bonus of 5,000 card points (a $50 value) after your first purchase within the first 180 days.

You’ll also get three months of Xbox Game Pass Ultimate for new Game Pass members. If you are already a Game Pass member, you can gift it to a friend. (After first three months the subscription will automatically continue at the regular monthly rate, currently $16.99/month.)

Card Earning

Xbox & Microsoft – Earn 5x card points on eligible products at the Microsoft Store.

Streaming Services – Earn 3x card points on eligible streaming services like Netflix and Disney+.

Dining Delivery Services – Earn 3x card points on eligible dining delivery services like Grubhub and DoorDash.

Everyday purchases – Earn 1x card points on all other everyday purchases.

Card Points can be redeemed for Xbox Mastercard Gift Cards starting at 1,500 Card Points for $15. You can redeem Xbox Mastercard Gift Cards to your Microsoft account on an Xbox console or connected device; Xbox Mastercard Gift Cards have no expiration date and can be used for eligible purchases (exclusions apply) at select Microsoft digital stores.

Additional Details

$0 annual fee

3% foreign transaction fee

Choice of one of five iconic designs for their card, with the option of personalizing it with their gamertag.

Free online access to cardmembers’ FICO Credit Score

Flexibility of use with contactless payments and digital wallets.

Our Verdict

Nothing too exciting here, and a small signup bonus. I guess it could make sense for someone who spends a ton at XBOX/Microsoft for the 5x rewards there.

Barclays is offering 100,000 miles on the Lufthansa Miles & More when you spend $3,000 and pay the annual fee within the first 90 days

Card Details

Annual fee of $89 (waived for Senator and HON Circle Members, as long as they maintain their Senator or HON Circle Member status)

Free annual companion ticket after annual fee is paid and on card anniversary

Card earns at the following rates:

2 miles per $1 spent on all miles & more integrate partners

1 mile per $1 spent on all other purchases

Free FICO score

No foreign transaction fees

Two Lufthansa Business Lounge vouchers annually (note despite the name Business is their lowest class of lounge, senator is higher and 1st is their highest class of lounge)

0% Introductory APR for 15 months

Our Verdict

Previous best was 80,000 points. This is an extra 20,000, surprised to see such a big jump. If you have a use of Lufthansa miles then this is definitely worth considering if not applying for, although I’d want to make sure I could use them ASAP to avoid any devaluation. We will add this to our list of the best credit cad bonuses. If you’re going to apply for this card then I’d also recommend reading our post on things you should know about Barclays before applying.

Robo-advisors have barely been around for 10 years, but in the past couple of years several have been steadily expanding their investment menus, and even offering valuable add-on services. One of the leaders in this regard is Wealthfront. The robo-advisor has been growing its investment capability in every direction but is now even offering financial planning. The platform now bills itself as offering High-Interest Cash, Financial Planning & Robo-Investing for Millennials. If you’re looking for more than just investing, Wealthfront has it. And as has become their trademark, it’s all available at a low cost.

What is Wealthfront?

Based in Palo Alto, California, and founded in 2011, Wealthfront has about $25 billion in assets under management. It’s the second-largest independent robo-advisor, after Betterment. And while dozens of robo-advisors have arrived in recent years, Wealthfront stands out as one of the very best. There isn’t any one thing Wealthfront does especially well, but many. And they’re adding to their menu of services all the time.

Their primary business of course is automated online investing. You can open an account with as little as $500, and the platform will design a portfolio for you, then manage it continuously. Your money will be invested in a globally diversified portfolio of ETFs–just like most other robo-advisors. But Wealthfront takes it a step further, and also adds real estate and natural resources.

Like other robo-advisors, Wealthfront uses Modern Portfolio Theory (MPT) in the creation of portfolios. They first determine your investment goals, time horizon, and risk tolerance, then build a portfolio designed to work within those parameters. MPT emphasizes proper asset allocation to both maximize returns, and minimize losses.

But in a major departure from other robo-advisors, Wealthfront now offers the ability to customize your portfolio and get access to a variety of investment methodologies and portfolios, including Smart Beta, Risk Parity and Stock-Level Tax-Loss Harvesting. And more recently, they’ve also stepped into the financial planning arena. They now offer several financial planning packages, customized to very specific needs, including retirement planning and college planning.

If you haven’t checked out Wealthfront in the past year or so, you definitely need to give it a second look. This is a robo-advisor platform where things are happening–fast!

How Wealthfront Works

When you sign up with Wealthfront, they first have you complete a questionnaire. Your answers will determine your investment goals, time horizon, and risk tolerance. A portfolio invested in multiple asset classes will be constructed, with an exchange-traded fund (ETF) representing each.

The advantage of ETFs is that they are low-cost, and enable the platform to expose your portfolio to literally hundreds of different companies in each asset class. With your portfolio invested in multiple asset classes, it will literally contain the stocks and bonds of thousands of companies and institutions, both here in the U.S. and abroad.

Wealthfront offers tax-loss harvesting on all portfolio levels. But they’ve also added portfolio options for larger investors, that include stocks as well as ETFs. The inclusion of stocks gives Wealthfront the ability to be more precise and aggressive with tax-loss harvesting.

Each portfolio also comes with periodic rebalancing, to maintain target asset allocations, as well as automatic dividend reinvestment. As is typical with robo-advisors, all you need to do is fund your account–Wealthfront handles 100% of the investment management for you.

More recently, Wealthfront has also added external account support. The platform can now incorporate investment accounts that are not directly managed by the robo-advisor. This will provide a high-altitude view of your entire financial situation, helping you explore what’s possible and providing guidance to optimize your finances.

And much like many large investment brokers, Wealthfront now offers a portfolio line of credit. It’s available only to investors with $25,000 or more in a taxable account, but if you qualify you can borrow money against your investment account and set your own repayment terms in the process

Wealthfront Features and Benefits

Minimum initial investment: $500

Account types offered: Individual and joint taxable accounts; traditional, Roth, rollover and SEP IRAs; trusts and 529 college accounts

Account access: Available in web and mobile apps. Compatible with Android devices (5.0 and up), and available for download at Google Play. Also compatible with iOS (11.0 and later) devices at The App Store. Compatible with iPhone, iPad and iPod touch devices.

Account custodian: Account funds are held in a brokerage account in your name through Wealthfront Brokerage Corporation, which has partnered with RBC Correspondent Services for clearing functions, such as trade settlement. IRA accounts are held with Forge Trust.

Customer service: Available by phone and email, Monday through Friday, from 7:00 AM to 5:00 PM, Pacific time.

Wealthfront security: Your funds invested with Wealthfront are covered by SIPC, which insures your account against broker failure for up to $500,000 in cash and securities, including up to $250,000 in cash.

Wealthfront uses third-party providers to maintain secure, read-only links to your account. The providers specialize in tracking financial data, as well as employ robust, bank-grade security, and in general, they follow data protection best practices. In addition, Wealthfront does not store your account password.

Wealthfront Investment Methodology

For regular investment accounts, Wealthfront constructs portfolios from a combination of 10 different specific asset classes. This includes four stock funds, four bond funds, a real estate fund, and a natural resources fund.

Each portfolio will contain various allocations of each asset class, based on your investor profile as determined by your answers to the questionnaire. The one exception is municipal bonds. That allocation will appear only in taxable accounts. IRAs don’t include them since the accounts are already tax-sheltered.

Notice in the table below that most asset classes have two ETFs listed. This is part of Wealthfront’s tax-loss harvesting strategy. In each case, the two ETFs are very similar. To facilitate tax-loss harvesting, one fund position will be sold, then the second will be purchased at least 30 days later, to restore the asset class. (We’ll cover tax-loss harvesting in a bit more detail a little further down.)

The ETFs used for each asset class are as follows, as of December 29, 2018:

Specific Asset ClassGeneral Asset ClassPrimary ETFSecondary ETF

US Stocks

Stocks

Vanguard CRSP US Total Market Index (VTI)

Schwab DJ Broad US Market (SCHB)

Foreign Stocks

Stocks

Vanguard FTSE Developed All Cap ex-US Index (VEA)

Schwab FTSE Dev ex-US (SCHF)

Emerging Markets

Stocks

Vanguard FTSE Emerging Markets All Cap China A Inclusion Index (VWO)

iShares MSCI EM (IEMG)

Real Estate

Real Estate

Vanguard MSCI US REIT (VNQ)

Schwab DJ REIT (SCHH)

Natural Resources

Natural Resources

State Street S&P Energy Select Sector Index (XLE)

Vanguard MSCI Energy (VDE)

US Government Bonds

Bonds

Vanguard Barclays Aggregate Bonds (BND)

Vanguard Barclays 5-10 Gov/Credit (BIV)

TIPS

Bonds

Schwab Barclays Capital US TIPS (SCHP)

Vanguard Barclays Capital US TIPS 0-5 Years (VTIP)

Municipal Bonds (taxable accounts only)

Bonds

Vanguard S&P National Municipal (VTEB)

State Street Barclays Capital Municipal (TFI)

Dividend Stocks

Bonds

Vanguard Dividend Achievers Select (VIG)

Schwab Dow Jones US Dividend 100 (SCHD)

Wealthfront’s historical returns are as follows (through 1/31/2019). But keep in mind these numbers are general. Since the portfolios designed for each investor are unique, your returns will vary.

Specialized Wealthfront Portfolios

As mentioned in the introduction, Wealthfront has rolled out several different investment options, in addition to its regular robo-advisor portfolios. Each represents a specific, and generally more specialized investment strategy, and is typically available to those with larger investment accounts.

Smart Beta: You’ll need at least $500,000 to be eligible for this portfolio. Smart beta departs from traditional index-based investing, which relies on market capitalization. For example, since Apple is one of the most highly capitalized S&P 500 stocks, it has a disproportionate weight in strict S&P 500 index funds. In a smart beta portfolio, the position in Apple will be reduced based on other factors.

In general, under smart beta, the weighing of stocks in the fund uses a variety of factors that are less dependent on market capitalization. There’s some evidence this investment methodology produces higher returns. This portfolio is available at no additional fee.

Wealthfront Risk Parity Fund: This is actually a mutual fund–the first offered by Wealthfront. It involves the use of leverage with some positions within the portfolio. It attempts to achieve higher long-term returns by equalizing the risk contributions of each asset class. It’s based on the Bridgewater Hedge Fund, and requires a minimum of $100,000, with an additional annual fee of 0.25% (0.50% total). This is the only Wealthfront portfolio that charges a fee over and above the regular advisory fee.

Socially responsible investing (SRI): Wealthfront just recently began to offer a specific SRI portfolio option. Once you sign up, you’ll be able to customize your portfolio and add socially responsible ETFs.

Sector-specific ETFs: If you want to invest in a particular portion of the market, such as technology or healthcare, Wealthfront gives you the option to build a portfolio that focuses on certain industries to portions of the stock market.

Customized Wealthfront Portfolios:

Wealthfront also lets investors build their own portfolios, which is somewhat uncommon among robo-advisors.

Most robo-advisors will build your portfolio automatically based on your risk tolerance and goals. If you like that service, Wealthfront can do it. However, more hands-on investors are free to make tweaks to the automatically designed portfolio by adding or removing ETFs.

You can also build a portfolio entirely from scratch if you’d rather. You can choose which ETFs to invest in and how much you want to invest in them. You can then let Wealthfront handle things like rebalancing and tax-loss harvesting while maintaining the portfolio you desire.

Wealthfront Tax-loss Harvesting

If there’s one investment category where Wealthfront stands above other robo-advisors, it’s tax-loss harvesting. Not only do they offer it on all regular taxable accounts (but not IRAs, since they’re already tax-sheltered), but they also offer specialized portfolios that take it to an even higher degree.

Wealthfront starts with a tax location strategy. That involves holding interest and dividend-earning asset classes in IRA accounts, where the predictable returns will be sheltered from income tax. Capital appreciation assets, like stocks, are held in taxable accounts, where they can get the benefit of lower long-term capital gains tax rates.

But for larger portfolios, Wealthfront offers Stock-level Tax-Loss Harvesting. Three specialized portfolios are available, using a mix of both ETFs and individual stocks. The purpose of the stocks is to provide more specific tax-loss harvesting opportunities. For example, it may be more advantageous to sell a handful of stocks to generate tax losses, than to close out an entire ETF.

Given that Wealthfront puts such heavy emphasis on tax-loss harvesting, it’s not surprising they’ve published one of the most respected white papers on the subject on the internet. If you want to know more about this topic, it’s well worth a read. The paper concludes that tax-loss harvesting can significantly increase the return on investment of a typical portfolio.

US Direct Indexing

US Direct Indexing is an enhanced level of tax-loss harvesting that Wealthfront offers to people with account balances exceeding $100,000.

Instead of building a portfolio of ETFs, Wealthfront will use your money to directly purchase shares in 100, 500, or 1,000 US companies. By buying shares in so many companies, Wealthfront can emulate an index fund in your portfolio while owning individual shares in the businesses.

Owning individual shares in hundreds of companies makes tax-loss harvesting easier as it lets Wealthfront’s algorithm trade based on movements in individual stocks rather than in funds. This can increase the number of tax losses that Wealthfront harvests each year, reducing your income tax bill.

Other Wealthfront Features

Wealthfront Cash Account

Wealthfront offers acash account where you can safely and securely store your money for anything–emergencies, a down payment for a home, or to later invest. By working with what they call Program Banks, Wealthfront has quadrupled the normal FDIC insurance on this account, so you’re protected for up to $5 million.

There’s also no market risk since it’s not an investment account and the money isn’t being invested anywhere. You can make as many transfers in and out of the account as you’d like, and it only takes $1 to start.

So what’s the catch?

There really isn’t one. Wealthfront will skim a little off the top to make some money before giving you an industry-leading 4.30% APY, but other than that, you’re just giving them more financial data. Since we’re doing this all the time with technology anyway, it shouldn’t make that big of a difference.

I see no downside, especially if you’re already a client of Wealthfront.

They’re really making a play to be your all-in-one financial services provider, too.

A new feature, just launched, is the ability to use your cash account as a checking account. This includes the ability to access your paycheck up to two days early when you set up a direct deposit. Additionally, you can invest in the market within minutes using your Wealthfront Cash account. Put the two together and you give yourself the ability to invest more than 100 days more in the market. The account also allows you to auto-pay bills and use apps like Venmo and PayPal to send money to friends or family. Account-holders also get a debit card to make purchases and get cash from ATMs. And you can use the account to organize your cash into savings buckets – like an emergency fund, down payment on a house, or other large purchase – and use Wealthfront’s Self-Driving Money offering to automate your savings into those buckets.

If you have cash that’s getting rusty in a traditional bank account and you want to earn more, the Wealthfront Cash Accountis a great place to keep it.

Read more about the cash account in our Wealthfront Cash Account full review.

Wealthfront Portfolio Line of Credit

This feature is available if you have at least $25,000 in your Wealthfront account. It allows you to borrow up to 30% of your account value, and currently charges interest rates between 3.15% and 4.40% APR depending on account size. You can make repayments on your own timetable, since you’re essentially borrowing from yourself. And since the credit line is secured by your account, you don’t need to credit qualify to access it.

Wealthfront Free Financial Planning

This is Wealthfront’s entry into financial planning. But like everything else with Wealthfront, this is an automated service. There are no in-person meetings or phone calls with a certified financial planner. Instead, technology is used to help you explore your financial goals, and to provide guidance to help you reach them. And since the service is technology-based, there is no fee for using it.

The service can be used to help you plan for homeownership, college, early retirement, or even to help you plan to take some time off to travel, like an entire year!

Simply choose your financial objective, enter your financial information, and Wealthfront will direct you on how to plan and prepare.

Self-Driving Money

One of the biggest and largely unrecognized obstacles for most investors is something known as cash drag. That’s when you have too much of your portfolio sitting in cash, which may earn interest, but it doesn’t provide the investment returns you can get in a diversified investment portfolio.

Wealthfront has addressed the cash drag dilemma with their newly released Self-Driving Money features. It’s a free service offered by the robo-advisor that essentially automates your savings strategy. It does this by automatically moving excess cash to help meet your goals, including into investment accounts where it will earn higher returns. And in the process, it eliminates the need to make manual cash transfers, and the judgment needed to decide exactly when to make that happen.

Our vision of Self-Driving Money is going to be a complete game-changer for people’s finances, said Chris Hutchins, Head of Financial Automation at Wealthfront. We want to completely remove the burden of managing your money so you can focus on your career, your family or whatever is most important to you.

You can take advantage of Self-Driving Money from the Wealthfront Cash Account. You’ll set a maximum balance for the connected account, which should be an amount that’s more than you expect to spend or withdraw on a monthly basis.

How It Works

When Wealthfront determines you’re over your maximum balance by at least $100 it will schedule an automatic transfer of the excess cash based on your goals. For example, you can tell Wealthfront you want to save $10,000 in an emergency fund, then max out your Roth IRA, then put the rest toward saving for a down payment on a house. Once you set the strategy, Wealthfront will automate the rest.

And before it happens, you’ll receive an email alert, then always have 24 hours to cancel the transfer if you need to cover unexpected expenses. You’ll also be able to turn on and off your Self-Driving Money plan at any time.

It’s usually possible to set up automated transfers from external accounts into most investment accounts. But what sets Wealthfront apart is the fact that it will make those transfers automatically. They will make sure you always have enough cash to pay your bills, then automatically transfer any excess into your savings buckets or investment accounts to improve the return on your money.

The strategy is designed to optimize your money across spending, savings, and investments, and to make it all flow with no effort on your part. You can simply have your paycheck direct deposited into your external checking account or Wealthfront Cash Account, cover your expected monthly spending, then have excess funds automatically transferred into the Wealthfront account of your choice.

By delivering on its Self-Driving Money vision, Wealthfront is taking the robo-advisor concept to a whole new level. Not only do you not need to concern yourself with managing your investments, but now even funding those investments will happen automatically. The result will be near complete freedom from the financial stresses that plague so many individuals.

Wealthfront Fees

Wealthfront has a single fee structure of just 0.25% per year for their advisory fee. That means you can have a $100,000 portfolio managed for just $250, or only a little bit more than $20 per month.

The one exception is the Wealthfront Risk Parity Fund, which has a total fee of 0.50% per year.

How to Sign Up with Wealthfront

To open an account with Wealthfront, you’ll need to be at least 18 years old, and a U.S. citizen.

You’ll need to provide the following information:

Your name

Address

Email address

Social Security number

Date of birth

Citizenship/residency status

Employment status

As is the case with all investment accounts, you’ll also be required to supply documentation verifying your identity. This is usually accomplished by supplying a driver’s license or other state-issued identification.

As mentioned earlier, you complete a questionnaire that will be used to determine your investment goals, time horizon, and risk tolerance. Your portfolio will be based on your answers to that questionnaire, and will be presented to you upon completion of the questionnaire.

For funding, you can use ACH transfers from a linked bank account. You will also have the option to schedule recurring deposits, on a weekly, biweekly, or monthly basis. The platform can even enable you to set up dollar-cost averaging deposits.

If you already have a brokerage account with another company, Wealthfront makes it easy to transfer your funds to your new account. If you’re invested in ETFs that Wealthfront supports, Wealthfront will assist with an in-kind transfer.

That means that you won’t have to sell your shares before transferring funds, which lets you avoid capital gains taxes that would be triggered by a sale.

Wealthfront Alternatives

Wealthfront’s closest competitor, and the robo-advisor that offers the most comparable services, is Betterment. They also have an annual advisory fee of 0.25%, but require no minimum initial investment. That could make it the perfect robo-advisor for someone with no money, who plans to fund their account with monthly deposits. Read the full Betterment review here.

Related: Wealthfront vs. Betterment

Another alternative is M1. Also a robo-advisor, M1 enables you to invest your money in what they call “pies”. These are miniature investment portfolios comprised of both stocks and ETFs. You can invest in existing pies, or create and populate pies of your own design. Once you invest in one or more pies, the platform will automatically manage it going forward. What’s more, M1 is free to use. Read more about M1 here.

Related: Wealthfront vs. Vanguard

Read More: The Best Robo Advisors – Find out which one matches your investment needs.

Wealthfront Pros and Cons

Investment options: Wealthfront offers more investment options than just about any other robo-advisor, particularly for investors with at least $100,000.

Reasonably priced: The annual fee of 0.25% is extremely reasonable, especially when you consider the degree of sophistication offered by Wealthfront’s investment methodology.

Tax-loss harvesting: This is available on all accounts, and Wealthfront is probably better at this investment strategy than any other robo-advisor.

Portfolio credit line: Gives you the ability to borrow against your portfolio with ease, and represents a form of margin investing.

Financial planning feature: The financial planning service is free to use and is available to all investors.

Limited access for smaller investors: Some of the more advanced investment portfolios and services are available only to investors with $100,000 or more to invest.

$500 minimum initial investment: It’s a minor issue, though some competitors require no funds to open an account.

FAQs

[faqs-content id=”MXKBSNXLNBBI5PDCYD4XJTU4PM” /]

Should You Sign Up for Wealthfront?

In a word, absolutely! Wealthfront is one of the very top robo-advisors, and you can’t go wrong with this one. Not only do they offer far more services than most other robo-advisors, but they also allow you to grow along the way. For example, as your account increases in value, you can take advantage of more sophisticated investment strategies, including advanced tax-loss harvesting.

That Wealthfront offers its portfolio line of credit and free financial planning services only makes the platform a bit more attractive, But the real benefit is the actual investment service. Wealthfront’s investment service comes extremely close to that of traditional human investment advisors, but at only a fraction of the annual cost.

We’ll send you a myFT Daily Digest email rounding up the latest Mortgages news every morning.

UK lenders have cut the cost of mortgages, offering hope for the housing market in a week when the Bank of England hiked rates to their highest level in 15 years and house prices fell the most since 2009.

The BoE raised rates to 5.25 per cent on Thursday, its 14th consecutive increase, and Huw Pill, BoE chief economist, indicated on Friday that rates were likely to stay high for a prolonged period.

But over the past few weeks, markets have priced in a lower peak of interest rates next year and it is these “swaps” rates that banks use to price mortgages.

NatWest, Halifax and Virgin Money have all cut rates this week — by as much as 0.41 per cent in some cases. That action followed cuts by Nationwide, Barclays, TSB and HSBC last week. Santander and Coventry Building Society also announced reductions.

David Hollingworth, director at London & Country Mortgages, said that Thursday’s news had been priced in to lenders’ calculations.

Aneisha Beveridge, head of research at Hamptons, the estate agent, said: “If everything follows the BoE expectations from here on in, I think we’ve seen mortgage rates peak about a month ago. They might come down a tiny bit more but they won’t come done too much until we see inflation falling across the board.”

Aaron Strutt, director at broker Trinity Financial, said: “We are starting to see more of the lenders reducing rates.”

In spite of the individual rate cuts, the average two-year fixed mortgage rate is still at 6.85 per cent, close to the highest level in 15 years, according to data from website Moneyfacts.

The pain of higher interest rates is having a very uneven impact in the housing market, according to research by Savills.

Nearly three-quarters of cash buyers surveyed by the estate agency said that their purchasing budget had remained the same. But nearly 60 per cent of those seeking to take out a mortgage with a loan-to-value ratio above 50 per cent said they had cut their budget.

“Cash buyers who are not exposed to concerns around rising interest rates have been able to drive ahead strongest in the current market,” said Frances McDonald, director of research at Savills.

By contrast, Chris Storey, chief commercial officer at digital lender Atom Bank, warned that the 1.4mn households due to come off fixed rates this year faced a steep increase in costs.

“People will perhaps have to become more accustomed, in the long term, to higher interest rates than they’ve faced in the last 15 years . . . especially if they have a payment shock coming off of a fixed-rate mortgage,” he said.

“The Bank of England might have to start cutting rates late next summer,” said Beveridge. “You might see mortgage rates react a bit earlier because they’re priced off of swap rates.”

The BoE’s Pill said: “Monetary tightening . . . is working. There’s no pre-determined path for interest rates, but rather we are responding as the economy and the data evolve.”

Equifirst announced today that effective immediately, it will be ceasing lending operations.

Going forward, the Charlotte, North Carolina-based mortgage lender will no longer accept applications for “any type of Mortgage Loan product.”

“EquiFirst will continue to process any completed Mortgage Loan application and will notify the submitting Broker of the status of such Mortgage Loan application upon completion of underwriting and processing,” the company said on its website.

“All previously submitted Mortgage Loan applications must continue to comply with the terms of the Wholesale Mortgage Broker Agreement (“Agreement”) currently in effect between the Broker and EquiFirst. This action will not affect current Mortgage Loan applications that are already scheduled to close.”

Prior to the announcement, the company was offering run of the mill wholesale FHA loan products, meaning its departure wasn’t all that unexpected.

Over the second half of 2008, Equifirst transitioned its product line to be a “fully functional FHA lender,” closing more than 1,700 loans during the period.

As of February 17, underwriting turn times took a whopping 11 days, while conditions took an average of three days to be reviewed.

Equifirst was founded in 1990, and operated as both a retail and wholesale mortgage lender through the years; the company was subsequently acquired by Barclays Capital Real Estate Holdings Inc. in 2007 (yes, bad timing).

In mid-2007, the company was offering an assortment of subprime, Alt-A, and jumbo loan products, while sporting the slogan, “Non-Conforming Results.”

Shortly after, Equifirst cut more than 400 jobs as the mortgage crisis began to gather steam.

Note: The Equifirst website previously displayed a message regarding operations being shut down, but has since been replaced with the company’s standard layout. It’s unclear if this is a technical issue…or something else.