Two years ago fixed rates were reduced to levels not seen in decades, giving borrowers access to rates around 2 per cent and below.

Since then, there has been a considerable shift in the interest rate landscape with the Reserve Bank of Australia lifting the cash rate from a historic low of 0.1 per cent to 4.1 per cent within 13 months.

At its November meeting, the RBA hiked the cash rate for the 13th time within 19 months, taking the benchmark interest rate to 4.35 per cent.

While the strain from interest rate hikes has impacted many, home owners who fixed their loan in 2020-2021 are facing hundreds, and in many cases thousands, of dollars extra a month in repayments once they roll off their fixed-rate.

RBA data shows there were 590,000 mortgages that came off fixed rates in 2022, and there will be 880,000 in 2023 and 450,000 in 2024.

If your fixed-rate home loan is ending, experts say there are practical things you can do now to prepare.

What happens when your fixed-rate home loan expires?

Your home loan will typically revert to your lender’s standard variable rate at the end of your fixed term.

While this may sound like the easiest option to take, Two Red Shoes mortgage broker Brett Sutton said these rates can often be higher than other deals on the market.

“We often find that there aren’t many lenders out there that offer existing customers ‘new to bank’ rates,” Mr Sutton said.

“This type of scenario is also typical with insurance renewals and gym memberships, and is known as a loyalty tax.”

So instead of taking a back seat, it can be wise to review your options and start preparing earlier.

Mortgage Broker Brett Sutton says borrowers should plan a couple of months ahead of their fixed-rate expiry.(Supplied)

Take action for when your fixed-rate ends

Here are a number of steps you could consider taking if you’re approaching the fixed-rate cliff:

Create a buffer

Instead of sitting back and enjoying a low rate, Mr Sutton suggests working out what your repayments would look like when you roll off the fixed rate and how it fits into your current budget.

“Review what non-essential costs you are carrying that could be culled to assist in covering the increased mortgage repayment,” he said.

Even with a fixed-rate, most lenders let you make extra repayments, but there might be conditions attached such as a cap.

“If there are no penalties in doing so, start making increased repayments before you need to,” Mr Sutton said.

“This helps you trial the new repayment amount and gives you real time feedback if further budget adjustments are required.

“The excess will build in the home loan providing you with an increased buffer for life events and saving you interest.”

Negotiate a better rate with your current lender

Before you agree to automatically roll onto your lender’s standard variable rate, Mr Sutton says you should be ready to renegotiate a cheaper rate.

“Contact your lender and let them know your dissatisfaction with the rate and potentially give them an indication that you are looking to refinance elsewhere by requesting a discharge form,” he said.

“This will inform them that you’re serious about leaving, and is typically when they’ll come to the party with their best rate.”

He said a lender’s strategy is to retain borrowers so they will likely be willing to have that conversation with you.

Lenders typically reserve their best rates for new customers, so it can be worthwhile shopping around to find a competitive deal.(ABC News: Dannielle Maguire)

Refinance with a new lender

If your current lender doesn’t want to come to the party, you could try and refinance your loan elsewhere to potentially score a better deal.

According to Savings.com.au analysis on a $500,000, 30-year principal and interest loan, the monthly repayments with a rate of 5.75 per cent per annum (p.a.) would be around $2,918, compared to monthly repayments of $3,079 at a rate of 6.25 per cent p.a

That’s a $161 saving per month. Over the life of the loan, it would work out to be a total of $57,860.

However, Savings.com.au money analyst Dominic Beattie warns some people may have to pay lenders mortgage insurance (LMI) for a second time in order to refinance if the equity in their property is below 20 per cent.

“The cost of LMI alone — often several thousand dollars — may override any short-term savings you’re hoping to generate by refinancing, so you’ll need to calculate whether it’s worth it,” Mr Beattie said.

“In some very specific circumstances, you may qualify for a partial refund of the first LMI premium you paid, but don’t count on this.”

National Debt Helpline. They offer free and independent financial advice.

Financial disclaimer: This is general advice only. Please see a professional for advice on your individual circumstances.

During highly challenging times for mortgage holders as the Reserve Bank of Australia (RBA) hit borrowers with a succession of interest rate rises, the mortgage broking industry continued to deliver strong results.

The Mortgage and Finance Association of Australia’s latest Industry Intelligence Service report found in the 12 months to March 2023, mortgage brokers settled a record $358.68 billion in home loans.

The MFAA said brokers have maintained a strong market share, writing 69.6 per cent of all residential home loans in the March 2023 quarter. Conversely, market share of the major banks declined in the March 2023 quarter to 45.8 per cent following a 2.7 percentage point increase in the December 2022 quarter to 49.9 per cent.

MFAA CEO Anja Pannek said the 16th edition of the report focused on the six-month period from October 1 2022 to March 31 2023, drawing on data supplied by the industry’s leading aggregator brands to provide mortgage broker, industry performance and demographic data.

“The period covered in the report coincided with a period of intense refinancing as fixed rate mortgages reverted to variable, clients encountered serviceability constraints and a moderation of property prices in some markets,” Pannek said.

“This confluence of factors can be seen in this industry research, however, the outstanding service mortgage brokers deliver to their clients has remained a constant throughout this time.”

While another strong result for brokers, the report noted in comparison to the October 2021 – March 2022 period, the total value of loans settled by mortgage brokers declined 8.63 per cent.

However, Pannek said the broker channel still outperformed the overall home loan lending market.

“Whilst the value of home loans settled by brokers declined 8.63 per cent for the period, the lending market as a whole – broker and proprietary channels – declined 10.89 per cent over the same period. This highlights that the broker market is meeting more needs of more consumers in a challenging economic environment,” she said.

Bell Partners is ready to assist if you want a more competitive interest rate with your current lender or are looking to refinance to a different product elsewhere in the market.

NAB has delivered a cloud-based digital engine capable of reducing home loan approval to under 60 minutes, as part of a four-year journey to revamp customer experience and transform systems.

The new simple home loan platform has united multiple ways customers and brokers apply for a home loan into a single reusable process that is fully automated and underpinned by digital and data capabilities, leading to a reimagining of its operational banking processes.

The platform was developed in-house by a team of 250, split between NAB’s Australian and Vietnam-based engineering operations.

Acting chief information officer of personal banking and executive technology home ownership Paul Norman shared with the iTnews Podcast how the bank achieved its home loan application process revamp.

“Buying a home can be one of the biggest events in our customers’ financial lives. It can be a pretty stressful experience whether you’re buying your first home or you’re an experienced home buyer, and historically the banks can be quite complex to deal with,” he said.

“It can sometimes, historically, take many weeks to get an approval or an unconditional decision from the banks, and practically this means for customers that they can struggle to buy with confidence, especially when we have competitive property markets.”

Norman, who stepped into the acting CIO of personal banking role following the departure of Anastasia (Ana) Cammaroto, said this led NAB to work hard “on solutions to try and make this particular ‘moment of truth’ more frictionless”.

“What we realised at NAB about four years ago, was we needed to make a change. We had platforms that were aging. Our processes were typified by manual handling, paper forms, rework,” he said.

“We needed to not just to change the technology, but also our philosophy around the end-to-end customer experience.

“We’ve set ourselves an ambition – it was a bold ambition – that we wanted to deliver unconditional approval to our customers in less than 60 minutes.”

Norman said that upon undertaking the tech transformation, the bank “realised quite quickly that technology alone wasn’t going to get us there.”

“We had to solve this by bringing people, process and technology together. We needed to build a digital engine that converged the many ways our customers, bankers and brokers traditionally applied for a home loan into a single, reusable process.

“That process needed to have full automation, straight-through processing, right through the home buying value chain.

“We recognised that we needed to transform and simplify a lot of our processes such that we weren’t coding complexity.”

Norman said the project team also “needed to make sure we had the right engineering platforms in place such that we were able to use our cloud-enabled microservices architecture, as well as our internal capability, to take this on.”

It was also important to embed “colleague intervention where it mattered”.

Four years ago

Norman said the bank commenced its journey four years ago in 2019, starting by simplifying and automating some of the lodgement processes, creating “efficiencies”.

These tools are used when colleagues and brokers wish to help a customer apply for a home loan, Norman said.

At the time the bank “used our same legacy backend system” and has since built out “a new ‘factory’.”

“We started this in 2021. We leveraged our cloud-native microservices capability to build our backend capability,” he said.

“We loosely coupled that with our existing digital platform. What this allowed us to do is create a fully digitally enabled experience that’s been built in a fraction of the time it would’ve taken to do this on a traditional, monolithic platform.

“What this means is we’ve been able to offer more and more of our customers access to this simpler experience far more quickly.”

Global team reach

Part of the platform’s success has been the “ability to leverage our global workforce” across Australia and Vietnam, according to Norman.

“In terms of the [technology] migration, the flexibility we’ve built with this sort of microservices-based architecture is that we’re able to segment, implement and transform backend capabilities in smaller and smaller iterations.

“So that allows us to create more enhancements to automation with straight-through processing.

“Most exciting is we have enabled experimentation so we’re able to test and learn rather than design for perfection, and can fail fast where we need to.

“This means we can get features to market far faster than we were able to before, and it means that we can migrate in smaller and smaller chunks.”

The two teams are seen “equally” as part of the NAB ecosystem and collaborate, with the Vietnam team “really an extension of our team and able to deliver features and functionality end-to-end.”

The wider NAB cloud approach

In line with the home loan transformation journey, four years ago NAB undertook “the bold decision to launch a cloud-first multi-cloud strategy”.

“What’s exciting about this initiative is the ‘simple home loans’ product is cloud-native from the outset. So, for us, this is a critical proof point of our strategy,” Norman said.

“[Cloud] has been an enabler of our ability to do this. We’ve been able to build at pace and scale when we needed to.”

Norman said the “broader industry context around home lending has everyone on the same journey that we are.”

“Everybody wants to make it as seamless and frictionless as possible for our customers, such that people want to choose that particular financial institution for their home loan going forward.”

“It’s a critical part of all of our customers’ financial lifecycle, it’s probably the biggest thing a customer can do with us, so we want to make sure it’s right. We want to make sure our customers have access to the ability to get a home loan when they need it.

He added part of the broader focus is also making sure that throughout the life of customer’s home loan, “they have the ability to interact with it and the flexibility to make changes as they need.”

“A big focus for us, and as I know many of our competitors, is the ability to provide our customers to be able to access those capabilities through their digital channels, self-serve when they need to, and then importantly, be able to talk to one of our amazing colleagues in those moments of truth”.

Generative AI, talent pipelines and future growth

More broadly, Norman said a core tenet of NAB’s strategy is to build its talent pipelines.

Over the last five years, the NAB intern program, for example, has seen 1059 people join, with 250 joining in the last year alone.

“Of those 1059 people that have joined our intern program, more than 600 people have been hired permanently,” he said.

“For us, we see that as the workforce of the future, they create immense value. Today, we’re able to bring young, talented engineers into our workforce to enable us to do some of the things that I’ve been talking about, and it also make sure that we’ve got the talent that we need for the future.”

As its workforce continues to expand Norman and the NAB teams are already preparing for multiple opportunities that lay ahead as “we are in a world of immense change right now”.

“With the world of generative AI, we’re starting to look at what those opportunities mean for us [and] some of the use cases that might be relevant for our industry in experimenting with those,” he said.

“I think we’ve got a bold and ambitious and strategic agenda, and at the same time the technology landscape’s changing, and it will be really exciting to see how those two things come together.”

As for its generative AI approach, NAB is already using chatbots “for both our customers and our colleagues to deliver differentiated customer experiences”.

“So here at NAB we see lots of opportunities. Right now, we’ve picked a few key things that we’re going to experiment with.

“Within the personal bank we’re experimenting with how generative AI help our colleagues get faster information, so the knowledge they need when they’re serving one of our customers.

“But it’s important at the moment that we anchor that in an approach, that it meets customer expectations, fits within our regulatory obligations as a bank, as well as making sure it’s anchored in our own data ethics standards”.

Nichol’s vision goes beyond borders, aiming to help Canadians and Americans navigate the property market. Let’s help Canadians get into homes. Let’s prove our model and take our concept down South of the border, where obviously there’s a larger population and landmass to work with, ” he said. “You know, because in the beginning, we … [Read more…]

Urban Money, the fintech arm of India-based real estate marketplace Square Yards, says it expects to disburse INR300 billion ($3.6 billion U.S.) in home loans during the 12 months to March 2024 (FY23-24).

In a news release, Square Yards said that Urban Money facilitated INR153 billion in home loans during the 12 months to March 2023 (FY22-23).

Urban Money accounted for 35% to the total revenue of Square Yards in FY22-23, with the former’s revenue rising by 248% y-o-y.

“We identified this fundamental gap in 2019 and cracked this space in the last four years, emerging as the largest mortgage marketplace in the country,” Square Yards founder CEO Tanuj Shori said.

Shori’s optimism draws upon Urban Money’s continued expansion in India’s tier-two and tier-three cities and a network of over 200,000 channel partners, including banks and non-bank financial companies.

Founded in 2013, Square Yards operates in India, Australia, Canada and the Gulf states. It has a network of more than 500 real estate developers and 150,000 agents. Last month, the company filed for 18 patents in the areas of virtual reality, augmented reality and extended reality.

Related Articles

September 12, 2023

Square Yards, an India-based real estate marketplace, has filed for 18 international patents in the…

July 15, 2023

India-based real estate marketplace Square Yards’ 3D visualization arm PropVR has been named an authorized…

August 13, 2023

Russia-based Avito has seen its app restored to the Google Play Store after it was…

Silver is a valuable precious metal that has been a medium of exchange for thousands of years, offering both an investment opportunity and a hedge against inflation. The allure of silver extends beyond its industrial utility to its rarity, malleability, and its historical role as money.

As an investor, understanding how to buy silver can provide you with a solid tangible asset and a potential wealth generation strategy.

5 Ways to Buy and Sell Silver

Here’s a brief guide on five popular methods to buy and sell silver, each with their own advantages and considerations.

1. Silver Bullion: Bars and Coins

Silver bullion refers to physical silver, which can take the form of bars or coins. Bars offer versatility with various sizes, while coins, often minted by national institutions, hold potential collectible value along with their silver content.

Silver Bars

Bars can range from small 1-ounce bars suitable for individual investors, to large 1000-ounce bars typically used for institutional investment. They offer a straightforward, easily quantifiable way to invest in this precious metal.

Silver Coins

When it comes to silver bullion coins, there are several types to choose from, each offering its own unique advantages:

American Silver Eagles: These coins are produced by the United States Mint and are well known for their beautiful design and high purity. They contain one troy ounce of .999 fine silver. American Silver Eagles are legal tender in the United States, with a face value of $1. But they are generally bought and sold based on the market price of silver plus a small premium.

Canadian Silver Maple Leafs: The Royal Canadian Mint produces these coins, which are similarly admired for their design and purity (.9999 fine silver). They also contain one troy ounce of silver, and their face value is 5 Canadian dollars.

British Silver Britannias: Minted by the Royal Mint, these coins are .999 fine silver and have a face value of 2 pounds. They feature an iconic image of Britannia, the female personification of Britain.

Australian Silver Kangaroos: These are minted by the Perth Mint in Australia and also contain one troy ounce of .9999 fine silver. They carry a face value of 1 Australian dollar.

Silver Rounds: These are similar to coins but are not considered legal tender. Rounds can be produced by a wide variety of mints and usually contain one troy ounce of .999 fine silver. They often come with unique designs and can be a cost-effective way to invest in physical silver.

2. Silver ETFs

Exchange-traded funds (ETFs) offer a convenient method for investors looking to gain exposure to the silver market without the need to physically own the metal. Here are a few popular silver ETFs:

iShares Silver Trust (SLV): The largest silver ETF by far, iShares Silver Trust is designed to track the spot price of silver. Each share of this ETF represents a certain amount of physical silver held by the fund.

ETFS Physical Silver Shares (SIVR): This fund aims to replicate the performance of the price of silver, minus the Trust’s expenses. It offers a slightly lower expense ratio than SLV.

Invesco DB Silver Fund (DBS): Unlike SLV and SIVR, DBS invests in silver futures contracts, which can result in greater potential for returns but also higher volatility and risk.

ProShares Ultra Silver (AGQ): This fund seeks to provide 2x the daily performance of silver bullion as measured by the U.S. dollar fixing price for delivery in London. This makes it a more aggressive investment, as it leverages your potential gains (and losses).

Aberdeen Standard Physical Silver Shares ETF (SIVR): This fund is designed to track the price of silver, and each share is backed by physical silver bullion held by the fund.

Global X Silver Miners ETF (SIL): This ETF tracks the Solactive Global Silver Miners Total Return Index, giving investors exposure to a broad range of silver mining companies.

Investing in these silver ETFs is akin to buying shares on the stock market. Rather than owning physical silver, shareholders in a silver ETF own shares in a fund that owns silver. This introduces managerial risk and ongoing fees for the management and storage of the fund’s silver.

3. Silver Mining Stocks

Investing in silver mining stocks or a Silver Miners ETF offers an indirect approach to gaining exposure to the silver market. By purchasing shares of companies involved in the extraction and production of silver, you are essentially betting on their operational and financial success.

These stocks often move in correlation with silver prices, but they also hinge on factors like mining efficiency, management proficiency, geopolitical issues, and the overall health of the economy. For example, a company may suffer from operational issues that reduce its profitability, even if the price of silver rises.

Popular silver mining companies include Majestic Silver Corp, Wheaton Precious Metals Corp, and Pan-American Silver Corp. In addition, a Silver Miners ETF, like the Global X Silver Miners ETF, offers diversified exposure to a variety of silver mining companies in one package.

4. Silver Certificates

Silver certificates serve as a hassle-free alternative to physical silver ownership. Essentially, these are documents issued by a financial institution that grant the holder claim over a specified amount of silver.

The silver itself is stored and managed by the issuing institution, eliminating storage and security concerns for the investor. This can be a convenient option for those who wish to avoid the logistics involved with storing physical silver, while still having a stake in the precious metal’s value.

5. Silver Futures and Options

For more sophisticated investors, silver futures contracts provide a way to speculate on the future price of silver. A futures contract is an agreement to buy or sell a certain amount of silver at a future date for a set price.

Options work similarly, giving investors the right but not the obligation to buy or sell silver at a set price within a specific time frame. These types of investments are more complex and typically involve higher risk and potential reward than simply buying and holding silver.

Where and How to Buy Silver

Buying Silver Online

Purchasing coins, bars, or even silver stocks online is an increasingly popular method. Online retailers such as Money Metals Exchange, Gainesville Coins, and JM Bullion offer a wide range of silver bars, coins, and rounds with various designs, sizes, and prices. Buying silver online can often be cheaper than buying locally due to lower overheads, but it’s important to ensure the dealer is reputable.

Before buying, compare prices, check reviews, and ensure the site has secure payment methods. Be aware that when you buy silver this way, you’ll usually need to arrange for secure delivery or storage.

Buying Silver Locally

Local coin shops, some banks, and bullion dealers offer investors the chance to buy silver in person. This can be advantageous, as you can inspect the silver content and quality directly. It’s crucial to research dealers’ reputation and expertise, as well as comparing prices to the spot market price and other local dealers.

Buying Silver on the Stock Market

If you want to invest in silver ETFs, silver mining stocks, or silver futures contracts, you’ll need to use a stock trading platform. These can be accessed through online brokerages. The buying process is similar to buying shares in any public company. As with any investment, it’s important to do your research or consult a financial advisor before buying.

Pros and Cons of Buying Silver

Like all investments, buying silver comes with its own unique set of benefits and potential drawbacks. Let’s explore both sides of the coin to give you a more balanced perspective.

Pros of Buying Silver

Diversification: Silver can offer a good way to diversify an investment portfolio. It tends to move independently of stocks and bonds, meaning it can provide balance and reduce overall risk.

Hedge against inflation and economic uncertainty: Historically, precious metals like silver have held their value over time. As a hard asset, silver can act as a hedge against inflation and economic uncertainty, as its value often rises when the real value of fiat currencies declines.

Industrial demand: Unlike gold, which is primarily used for investment and jewelry, silver has numerous industrial applications. This demand can support the price of silver in a way that may not be applicable to other precious metals.

Affordability: Compared to other precious metals like gold and platinum, silver is more affordable. This lower price point allows more investors to buy physical silver bullion, such as bars and coins.

Tangible asset: When you invest in physical silver, you own a real, tangible asset that you can hold in your hand. This differs from digital or paper assets that only represent the ownership of an asset.

Cons of Buying Silver

Storage and insurance: Owning physical silver means dealing with storage and insurance costs. Whether it’s in a home safe or a safe deposit box, the costs and logistics of storage are factors to consider.

Price volatility: Silver prices can be quite volatile. While this can lead to significant gains, it can also lead to big losses.

Lower liquidity: Although silver is generally liquid, it can be harder to sell quickly compared to stocks and bonds. If you need to convert your silver into cash immediately, you might have to sell it for less than its market value.

No passive income: Unlike stocks and bonds, silver doesn’t produce dividends or interest. Your potential profit lies in the appreciation of the metal’s price.

Dealer premiums and selling costs: When you buy physical silver, you often pay a dealer premium over the spot price. Similarly, when you sell, you might receive less than the spot price.

Storing Your Silver

Deciding on the right place to store your silver is a crucial step. Here are some of your options:

Home storage: A personal safe at home can be sufficient for smaller quantities of silver. It’s convenient but comes with risks like theft or damage.

Bank safe deposit boxes: These offer high security and are good for medium quantities of silver. However, access is only during bank hours, and the contents are usually not insured by the bank.

Professional bullion storage: Ideal for larger investments, these facilities offer 24/7 security and typically include insurance coverage. Companies like the Royal Mint offer such services.

Silver IRA storage: If you have a Silver IRA, your silver will be stored by a qualified custodian in an approved facility, offering a hands-off and worry-free storage option.

Tax Implications of Buying Silver

The tax implications of owning silver depend on your country’s tax laws. In general, any profit from selling silver is subject to capital gains tax. Some silver investments, like silver mining stocks, silver ETFs, and silver futures contracts, might be held in a tax-advantaged account, like an IRA, but this is subject to specific rules and regulations.

Silver IRAs are a particular type of investment retirement account that allows you to hold physical bullion coins or bars in a tax-advantaged manner. They can be a valuable part of an investment portfolio, but they must be administered by a custodian and stored in an approved facility.

Conclusion

Investing in silver can provide diversification, a hedge against inflation, and potential for significant returns. There are many ways to buy silver, from physical bullion to silver ETFs, mining stocks, and more. Whatever path you choose, remember that like any investment, silver comes with risks. It’s important to do your research or consult a financial advisor before diving in.

Frequently Asked Questions

What’s the difference between spot price and market price in the context of silver?

The spot price of silver is the current price per ounce being traded on global commodity markets. The market price of silver, particularly when buying physical bullion, often refers to the spot price plus any dealer premiums, which can include costs for fabrication, distribution, and a minimal dealer fee.

Are silver coins or bars a better investment?

This often depends on the individual investor’s goals and circumstances. Coins can be more collectible and easier to sell in smaller quantities, but may carry higher premiums. Bars, particularly in larger sizes, often have smaller premiums and may be more cost-effective for larger investments.

Is investing in silver better than investing in gold?

Silver and gold are different assets with their own strengths and weaknesses. Silver is more affordable and has more industrial uses, which can drive demand. Gold, on the other hand, is more widely accepted as a store of wealth and is less volatile. Both can play a role in a diversified portfolio.

Are there any tax benefits to investing in silver?

Depending on your country’s laws, there may be tax advantages to investing in certain types of silver investments. For example, in the United States, silver held in a Silver IRA can grow tax-free. However, profits from selling silver are usually subject to capital gains tax. It’s important to consult a tax professional or financial advisor for personalized advice.

What is junk silver?

“Junk silver” is a term used to describe old coins that have no collector or numismatic value but are made of silver. These coins, like pre-1965 U.S. dimes, quarters, and half dollars, can be a cost-effective way to invest in silver, as they are often sold close to their actual melt value.

Online banking has made managing money easier than ever. However, it has also led most people to rely solely on digital assets.

Precious metals are a popular investment choice for people wishing to buy a tangible asset that retains its value over time. In particular, gold and silver generally maintain their value even when the stock market faces major financial fluctuations.

They also do well in times of inflation and political uncertainties. When traditional stocks fluctuate due to these external factors, precious metals only become more valuable.

Investors who prefer a hands-off approach have the option of purchasing gold and silver stocks. These stocks are traded daily just like any other stock. However, many people prefer to keep a physical store of their precious metal.

While relatively illiquid, buying physical gold and silver is typically viewed as a long-term investment. It’s certainly a practical option if you’re concerned about inflation or the future of fiat currency.

Best Places to Buy Gold and Silver Online

eBay and Craigslist are both great places to start. But unless you’re confident that you’re dealing with a reputable seller, you might want to look into other sites that specialize in precious metals.

To help you find the best place to buy gold and silver, we’ve compiled a list of the best online gold dealers.

Money Metals Exchange

Money Metals Exchange, or MoneyMetals.com, has received several accolades, including the “Best Overall Gold Dealer” by Investopedia.

They’ve also done over $2 billion in transactions.

Money Metals Exchange has an A+ rating from the BBB. They offer 24/7 online support, indicating a strong commitment to customer service.

Products include gold, silver, rhodium, palladium, and platinum. You can also invest in a self-directed precious metals IRA.

You can often find great deals and promotions on Money Metals Exchange, so it’s a site you may want to bookmark.

Silver Gold Bull

Silver Gold Bull offers a suite of services for their customers. In addition to buying and selling through the company’s website, you can also store your hard assets in their secure facilities.

Another helpful feature is an automated spot alert. You can get up-to-the-minute data on where prices are throughout the day and buy when they hit your target price.

Plus, the Silver Gold Bull sales team is full of seasoned veterans, so you can get answers to your questions from people who truly know their stuff.

The company sells a wide range of gold, silver, platinum, palladium, copper, and collectibles online and over the phone.

Gainesville Coins

With an A+ rating from the Better Business Bureau, Gainesville Coins has been keeping customers happy for more than ten years.

In fact, the company has also received a five-star rating from the National Inflation Association—the only bullion dealer to receive such a distinction.

You’ll find a wide selection of gold, silver, platinum, and other metals like copper, palladium, and rhodium on the Gainesville Coins website.

The company also sells pre-1933 gold and has an extensive clearance section with time-sensitive deals. In addition, you can calculate shipping based on your zip code and items placed in your cart. Only Florida residents pay sales tax on their purchases.

Gainesville is one of the best places to buy gold online.

Golden State Mint

Golden State Mint is a trusted source for premium precious metal products, providing buyers direct access to top-notch items straight from the manufacturer.

With 40+ years of experience, the company inspects each piece with precision before shipment, ensuring its authenticity and quality.

Customers can rest assured that all products are brand-new, never previously owned or circulated.

Investing in precious metals for retirement? Golden State Mint offers expert support in establishing an IRA account, stocked with an array of products that fully comply with IRS standards.

Whether you’re a seasoned pro or just starting out, Golden State Mint is committed to helping you achieve your investment objectives through purchasing physical gold and silver.

Provident Metals

What started as a precious metals trade show business has launched into one of today’s largest online bullion dealers.

Provident Metals holds several professional memberships. These include the American Numismatic Association, the Professional Coin Grading Service, and the Numismatic Guaranty Corporation.

Provident’s collections include gold, silver, copper, platinum, and palladium, with an extensive selection of each one. In addition to coins, rounds, and bullion bars, Provident Metals also sells U.S. and foreign coins, wholesale products, and IRA bullion products.

You’ll appreciate the company’s attentive service and timely delivery. And if you order $99 or more, shipping is free; otherwise, it costs just $5.95 to ship.

APMEX (American Precious Metals Exchange)

APMEX is one of the largest online dealers in the world, which allows it to pass along savings to its customers. This is due to the sheer volume of business it does each day. Not only can you buy silver, gold, and other metals, you can also sell or trade from your current holdings.

The selection is huge, covering the major precious metals, historic gold coins, “elite” coins, old banknotes, and foreign coins. It also has an extensive collectibles section with rare coins and currency from around the world.

Scottsdale Mint

Scottsdale Mint (formerly Scottsdale Silver) focuses on silver and gold while also offering each in different collectible series. They sell both types of metal in coins, bullion bars, and rounds, with a particular premium set on artistic minting.

For example, some recent popular collectible sets include a Vikings series and a Godfather set featuring images from the iconic movie franchise.

To qualify for free shipping with insurance, you must make a minimum purchase of $500. This may seem steep compared to some other companies providing free shipping at $99. However, much of the allure of Scottsdale Mint comes from the company’s creative minting process.

JM Bullion

Shipping is free on all JM Bullion orders over $199. They sell physical gold, silver, platinum, and other bullion that arrive directly at your door. They inspect every inventory item to ensure only quality products are sold. Payment options include Visa, MasterCard, PayPal, PayPal Credit, bank wires, paper checks, and Bitcoin.

JM Bullion is fully accredited at both state and federal levels. They also have reliable customer service that you can reach via phone or 24-hour Live Chat. Sign up for email, and they will mail you exclusive sales and promotions.

Kitco

Kitco has many precious metal types, including gold, silver, palladium, platinum, and rhodium.

The website also provides a slew of data and news to help you with your portfolio decisions. You can even download apps for gold news, market alerts, and scrap value calculations for your smartphone.

GoldSilver.com

As its name implies, GoldSilver solely sells gold bars, coins, and jewelry and silver bars and coins. They also sell products such as safes and storage containers. You can also create an account to sell back your gold bullion, gold coins, and silver bars through the website.

There’s a flat rate shipping fee of $25 for any order under $500. Otherwise, shipping, handling, and insurance are free. In addition to traditional payment options, GoldSilver also accepts PayPal.

Silver.com

Don’t be fooled by the name. While Silver.com could be the best place to buy silver online, they also sell various gold, platinum, and copper products. In addition to government mints, you can also find gold coins, gold bullion, silver coins, silver bars, and more from private domestic and foreign mints.

The order threshold for free shipping is high at $3,000, but their tiered flat rate shipping fees are reasonable. Smaller orders up to $299 cost just $4.95 for shipping and insurance. The highest tier of orders from $1,000 to $2,999 cost just $9.95.

SD Bullion

Silver, gold, platinum, and copper comprise SD Bullion’s core product line, with coins, bars, and rounds from around the world.

They also sell lead bullion in the form of ammo as well as vaults, survival food, and herbal medicine. In addition, SD Bullion offers weekly specials and currently has a promotion for all orders shipped at just $7.77.

Texas Precious Metals

Texas Precious Metals offers several unique features, including the ability to sign up for limit orders. For example, you can automatically place a standing order if gold or silver reaches your desired value.

All orders ship for free using UPS Next Day Air, and all orders ship within three business days of payment. The website offers a curated selection of gold coins, gold bars, silver coins, silver bars, and pre-1933 gold.

Golden Eagle Coins

Golden Eagle Coins is a place for gold and silver investors and collectors alike. Take one look at their website, and you’ll see why — their inventory is enormous.

Prices are updated in real time as their quotes come directly from the commodities exchange. This is a great site to use if you are researching when to buy.

Shipping is free on orders $99 and over. Also, be sure to check out their bi-monthly blog for new items and savings.

Gold Dealer

Quoted on CNN, CNBC, and PBS, Gold Dealer offers a complimentary newsletter written by industry masterminds Ken Edwards and Richard Schwary.

They have a physical office moments away from LAX. However, if you don’t want to travel to Los Angeles, you can visit website instead. It has everything you’d expect from a reputable gold dealer.

Gold Dealer offers free, insured shipping on every order. Their low prices are the result of reducing operating expenses over time.

Monarch Precious Metals

Monarch Precious Metals is a newer company established in 2008 to help with the immense public demand for gold bullion. They only use quality metals, so anything you buy from them will be .999+ fine.

They triple-check the weight of every bar they ship. If it is ever underweight, they re-melt it. If it’s ever overweight, it’s a win-win for you because they always let it pass and ship it as is.

Everything is custom hand-poured and marked in the old way, giving their metals a unique, old-fashioned look. They accept all methods of payment except PayPal, and every order is properly insured.

CMI: Gold & Silver

An A+ Accredited Business, CMI is located in Phoenix, Arizona. However, CMI will buy and sell precious metals online to investors all over the United States.

Its president, Bill Haynes, considers it his responsibility to educate the public about the dangers and benefits of buying gold and silver products.

He regularly updates his blog on global factors that influence the prices of metals. It’s a helpful resource for determining when to buy.

With solid prices, IRAs, and a plethora of educational material to read, CMI should be a website you routinely check if you are a serious investor.

BGASC: Buy Gold and Silver Coins

With thousands of positive customer reviews, it’s not hard to realize why BGASC is an A+ BBB accredited business. They offer free shipping on orders $99 and up. Every order is insured while in transit. Additionally, they always ship your order the next business day.

BGASC is one of the largest coin and bullion dealers in the US. They sell nearly every type of US coin ever made. They also have a large selection of mints from other countries, such as China, Mexico, and Canada.

The Basics of Precious Metals

Before buying gold or silver, it’s important to understand the different forms they come in. Each type has its pros and cons. Some people focus on one kind they prefer, while others create a diverse mix of different kinds. Before you buy precious metals, figure out which strategy is best for you.

Silver

Let’s start by talking about silver. Typically, you can buy silver either in the form of bullion or junk silver. Silver bullion refers to silver as a bar, coin, ingot, or round.

Silver Coins

The most popular silver coins you’ll come across are as follows:

American Silver Eagle

Canadian Silver Maple Leaf

British Silver Britannia

Mexican Silver Libertad

Austrian Silver Philharmonic

South African Silver Krugerrand

Australian Silver Kangaroo

Chinese Silver Panda

Junk Silver

Junk silver, on the other hand, is any type of old U.S. currency containing real silver. Any U.S. half-quarters, quarters, or dimes minted before 1965 are considered junk silver. However, in reality, they aren’t very junky at all.

You can sometimes find junk silver below the spot price. This can often allow you to start with a profit on your investment.

Silver Rounds

Silver rounds are privately minted silver pieces shaped like coins but produced by private mints. They are not government minted or legal tender, so they are not referred to as coins. The most popular silver round is the American Silver Buffalo. However, Scottsdale Mint also produces some beautiful rounds called “Omnia.”

Gold

Gold also comes in bars and coins, each one giving you a different type of entry point into precious metal investing. Buying gold coins is the easiest way for gold investors to start because you can begin by just purchasing a few at a low price point.

Gold Coins

The most popular gold coins to buy are as follows:

American Gold Eagle

Canadian Gold Maple Leaf

British Gold Britannia

British Gold Queen’s Beast

Mexican Gold Libertad

Austrian Gold Philharmonic

South African Gold Krugerrand

Australian Gold Kangaroo

Chinese Gold Panda

Gold Rounds

Similar to silver rounds, the most popular is the American Gold Buffalo.

Perhaps you’re stocking up as a hedge against inflation or to use as currency in a potential crisis. If so, you’ll find that coins of any type (gold or silver) will be easier to barter with than bars.

If you decide to buy bars, you can get them in different sizes to suit your space or budget. For example, you can purchase 1 to 10-ounce gold bars or up to 100-ounce silver bars. You can even find bars at just a fraction of an ounce if you want to start small.

One of the most significant advantages of this tactic is that you get the lowest premium when you buy larger bars. So while they might not be as easy to sell when you’re ready, you’ll get a better value if you can make that large of an investment upfront.

Copper

While silver and gold are the most popular, there are other precious metals to consider as well. For example, copper also comes in bars, rounds, and coins and is very affordable for novice investors.

Some experts believe it’s a wise investment opportunity because of its rising demand and shrinking supply.

Platinum and Palladium

Platinum is perhaps the most precious of all metals. It’s 15x rarer than gold, and its value exceeds that of gold. Platinum is usually sold as coins minted in the U.S., Canada, or Australia.

Palladium is similar to platinum in its properties and is actually 30x rarer than gold. Because these metals are so rare, not many people invest in them. However, a growing number of investors are adding them to their portfolios. It’s something you may want to consider as well.

Gold and Silver: Frequently Asked Questions

Where is the best place to buy gold?

The two best places to buy gold are online retailers and local coin shops.

Online retailers, such as the ones we’ve listed above, offer a wide selection of gold coins, bars, and rounds at competitive prices. These retailers often offer free shipping and insurance, making it easy and convenient to buy gold from the comfort of your own home.

Local coin shops are another great option if you want to prefer gold in person. These shops often have a knowledgeable staff who can help you find the right gold products for your needs and budget. You may also be able to negotiate on price of the gold.

Where is the best place to buy silver?

The best place to buy silver is typically also the best place to buy gold: online dealers and local shops. These options provide a wide range of products to choose from and allow you to compare prices and quality before making a purchase.

Online dealers offer the convenience of shopping from home, while local shops provide the advantage of in-person interaction with knowledgeable staff who can answer your questions and guide you towards the right products for your investment goals.

Whether you want to buy silver coins or silver bars, these options typically offer competitive prices, flexible shipping policies, and convenient payment options.

We recommend checking out at least a few of the best online gold dealers we mentioned above, regardless of what your needs are. Compare prices, selection, and shipping policies on numerous sites.

What is the cheapest way to buy gold and silver?

The most cost-effective method of acquiring gold and silver is by buying bars. They tend to have smaller markups compared to spot prices compared to coins, due to their lower production costs.

Buying in bulk is also a smart way to lower the cost per ounce as many online dealers offer discounts for larger purchases.

Is it safe to buy gold and silver online?

Buying precious metals online is as safe as any other transaction you make online. It’s also just as safe to buy online is as it is to buy from a physical retailer. The key is to buy gold and silver from a reputable gold dealer.

Is it better to buy gold coins or bars?

There is no right or wrong answer to this question. It depends on your situation, your needs, your budget, and what you prefer. As mentioned, it’s typically cheaper to buy gold bars. However, you will most likely get a better value from gold coins when it comes time to sell your gold.

Gold and silver coins and small bars offer more flexibility when it comes time to sell. Owning smaller units of gold and silver allows you to sell only a portion of your precious metals instead of your whole portfolio.

How much gold and silver should I own?

Experts recommend holding 5-25% of your net worth in precious metals. However, it depends on your goals, your situation, and risk tolerance. Precious metals can be a great addition to your portfolio as long as you know why you’re adding it.

Can I store gold at home?

Storing gold in your home offers a sense of security and privacy for your valuable assets. As a form of wealth preservation, it provides complete control without the need for outside storage. However, it’s crucial to be mindful of potential security threats and to ensure your assets are adequately insured.

To mitigate these risks, it’s advisable to implement a secure storage system. Ultimately, home storage is a viable solution for individuals who value personal ownership and control of their gold holdings.

Buying a home in the U.S. often involves weighing the trade-offs between a 15-year and 30-year mortgage. With the interest rate staying constant, the first option has higher monthly payments, but the loan is repaid sooner than it is with the second option that offers lower monthly payments.

But home loan borrowers in the U.K., Canada, Australia and most European countries have a wider array of choices: They can break up their loan tenure into smaller chunks of two, three, or five years, and get lower interest rates as their loan size reduces and credit rating improves over time.

A new research paper by Wharton finance professor Lu Liu, titled “The Demand for Long-Term Mortgage Contracts and the Role of Collateral,” focuses on the U.K. housing market to explain the choices in mortgage fixed-rate lengths by mortgage borrowers. She pointed out that the length over which mortgage rates stay fixed is an important dimension of how households choose their mortgage contracts, but that has “not been studied explicitly thus far.” Her paper aims to fill that gap.

Liu explained that the U.K. market is “an ideal laboratory” for the study for three reasons: It offers borrowers an array of mortgage length choices; it is a large mortgage market with relatively risky mortgage loans similar to the U.S.; and it offers the opportunity to study market pricing of credit risk in mortgages. In the U.S. market, the pricing of credit risk is distorted as the government-backed Fannie Mae and Freddie Mac provide protection against defaults. “The U.S. is a big outlier in mortgage structure. It has essentially removed credit risk in the markets for long-term contracts.”

How Beneficial Are Long-term Mortgages?

At first sight, long-term mortgage contracts may seem preferable because they have a fixed interest rate, and thus allow borrowers to protect themselves from future rate spikes, the paper noted. “Locking in rates for longer protects households from the risk of repricing, in particular having to refinance and reprice when aggregate interest rates have risen,” Liu said. “In order to insure against such risks, risk-averse households should prefer a longer-term mortgage contract to the alternative of rolling over two short-term mortgage contracts, provided that they have the same expected cost.”

But in studying the U.K. housing market, Liu found that there is an opposing force that may lead some households to choose less protection against interest rate risk. This has to do with how the decline of credit risk over time affects the credit spreads borrowers pay. She explained how that occurs: As a loan gets repaid over time, the loan-to-value (LTV) ratio decreases as households repay the loan balance and house prices appreciate, the paper noted. This reduces the credit spread that households pay on their mortgage over time. When high-LTV borrowers decide to lock in their current rate, the credit spread will account for a large portion of that rate.

“[30-year mortgages] have had knock-on effects on mobility and housing markets due to mortgage lock-in.” – Lu Liu

As the LTV ratio declines and collateral coverage improves over time, they raise the opportunity cost of longer-term contracts, in particular for high-LTV borrowers, Liu noted. “Locking in current mortgage rates [protects] households against future repricing, but it also locks in the current credit spread, leading households to miss out on credit spread declines over time.”

High-LTV borrowers, or those who opt for low down payments and bigger loans, have to initially pay large credit spreads that can be as high as 220 basis points higher than what a borrower with prime-grade credit would pay. But refinancing with shorter-term contracts allows them to reduce those credit spreads over time. “They’re not locking in to a rate over 30 years; they’re probably locking in at shorter terms of two, three, or five years, and they do it maybe six or seven times,” Liu said. Riskier borrowers with higher LTV ratios hence face a trade-off, as locking in rates while the LTV is high is relatively costly, so they end up choosing shorter-term contracts, meaning they choose less interest-rate protection than less risky borrowers.

“In markets where the credit risk is priced using market prices – without government intervention as in the U.S. — the credit risk is expensive as lenders charge relatively higher rates for that,” Liu said. “If I’m a risky borrower, I face this very difficult trade-off: I want to insure myself like everyone else. But it also means that I’m locking in relatively high rates, with a big credit spread.” That of course does not always make sense for borrowers, she pointed out. “This may help explain why very long-term mortgage contracts with high-LTV mortgage lending are rare across countries.”

Liu said her data, which covered the period from 2013 to 2017, showed that the propensity is lower among riskier borrowers to opt for a 5-year fixed-rate mortgage compared to a 2-year fixed-rate mortgage. The higher the loan-to-value ratio, the lesser was their incentive to choose longer mortgage tenures, her research found. “Borrowers at 95% LTV are less than half as likely to take out a 5-year fixed-rate contract, compared to borrowers at 70% LTV,” the paper stated. The findings help explain the “reduced and heterogeneous demand for long-term mortgage contracts.”

How to Make U.S. Mortgages More Efficient

Liu said the findings in her paper are relevant for mortgage market design. “High-LTV borrowers face a difficult trade-off between their demand to lock in overall interest rate levels, and an expected decline in credit spreads over time,” she said. “Households could benefit substantially from being able to lock in base interest rates, while repricing their credit spreads.”

The findings are important also from both a monetary policy and financial stability perspective, Liu continued. “High-LTV borrowers are more exposed to interest rate risk, which can also cause vulnerabilities in a rising rate environment, since these borrowers may be most affected by mortgage cost increases.”

“There is political resistance to institutional change and borrower resistance to novel mortgage products.” – Lu Liu

The findings of Liu’s research are also timely, given the recent spike in the inflation rate. She noted that the U.S. Federal Reserve has increased interest rates more aggressively than its counterparts in the U.K., Canada, and Australia. All those countries have varying degrees of short-term fixed or variable-rate mortgages. Unlike in those countries, U.S. mortgage borrowers are “relatively shielded from interest rate rises, as the vast majority of households have locked in previous low rates for 30 years,” she noted.

Unintended Consequences of Long-term Mortgage Contracts

But the design of mortgage contracts in the U.S. creates disruptions beyond the housing markets to the broader financial system. “The 30-year fixed-rate mortgages in the U.S. have led to duration mismatch and financial stability risks in the banking sector, as rate rises have reduced the market values of these loans and mortgage-backed securities,” Liu said. She cited the recent collapse of Silicon Valley Bank as a case in point, which was triggered by the fall in the valuation of its bond holdings in a rising interest rate environment. In the U.K., in contrast, banks typically hedge the 2-to 5-year fixed-rate legs of mortgages using swaps, with the remaining part of the contract having a variable rate and thus not causing duration mismatch for the banks.

Long-term contracts have other consequences, too. “The [30-year mortgages] have had knock-on effects on mobility and housing markets due to mortgage lock-in,” Liu continued. Mortgage lock-in occurs in a rising interest rate environment, where homeowners find it a losing proposition to refinance mortgages they had taken out when interest rates were at historical lows. As a result, “people aren’t moving, and the housing market is frozen,” she said.

Liu said policy makers ought to rethink the 30-year fixed-rate mortgage, noting that Harvard economics professor John Y. Campbell had proposed that in a presentation at the Georgia Tech-Atlanta Fed Household Finance Conference in March 2023.

That said, the nature of mortgage systems in different countries is “highly persistent over time,” so any recommendation to radically change them might be far-fetched, Liu noted. “There is political resistance to institutional change and borrower resistance to novel mortgage products,” she added. If the U.S. were to move in the direction of more of a Canadian system that has mortgage rates fixed for five years, she noted, “any implementation of shorter-term fixed-rate contracts would need to take into account the credit risk dimension, which could result in risky households insuring less against interest rate risk.” Such a move has the potential to make monetary policy more effective and the banking system more stable, but further research is needed, she added.

You probably know that you need a passport for international travel, but you may have also heard of another type of travel document called a visa. Depending on your travel plans, you might be able to travel with just a passport — or you might need to apply for a visa as well.

But what is the difference between a visa and a passport? Here’s what you need to know.

What is a passport?

A passport is a specific type of official identity document used for international travel. A country’s government issues the document to its citizens or in some cases, to noncitizen nationals. Passports contain identifying information like your name, birth date, gender, photo and passport number.

Many passports also contain electronic chips that store your identity information and signature digitally, which makes the passport difficult to fake or alter.

Most passports are regular, or tourist, passports. In the U.S., these are the blue passports that you’re most likely familiar with. But countries also issue diplomatic and official passports for officials traveling on government business.

When do you need a passport?

If you plan to travel internationally, you most likely need a passport. There are alternatives to passports for U.S. citizens going to Canada or Mexico by land, but most international travel will require a passport. International air travel always requires a passport.

What is a visa?

A visa is a document that permits you to enter another country for a specific length of time and purpose. Whether a visa is required to enter a country depends on your country of citizenship, your reason for travel, the duration of your stay and other factors.

Any country might issue dozens of different types of visas. It may have a complicated taxonomy of visa types or offer only a handful of visa types. Here are some of the most common types of visas:

Tourist visas are issued when you are traveling to a country for sightseeing, visiting friends or other noncommercial, nonofficial purposes. These visas are typically issued for a short stay of a few months.

Student visas are issued to those who will be studying in the country. They typically allow you to stay in a country during your studies, but there are often restrictions on how much you can work.

Work visas allow you to enter a country for the purposes of employment. Most countries require a specific work visa if you want to work during your stay.

Transit visas are issued when you need to pass through a country to catch a connecting flight. Transit visas are typically valid for a short period of time, and visa holders aren’t allowed to exit the airport while in the country.

How do you get a visa?

Countries that require a visa will often ask you to send your passport to an embassy or consulate before you travel. Requirements vary, but you will usually be asked to provide evidence of your travel bookings, a photograph, a completed visa form and proof of residence. Visa processing may take a few days to more than a month.

Even if a country requires a visa for travel, you don’t always have to apply for it in advance. Some countries will grant you a tourist visa on arrival. Egypt, for example, grants a 30-day tourist visa to U.S. citizens arriving by air for a $25 fee.

Finally, some countries allow you to apply for a visa electronically. Australia, for instance, allows U.S. citizens, as well as those from a handful of other countries, to obtain an Electronic Travel Authority. You can apply for the electronic visa online, allowing you to get a visa without submitting your passport to an embassy or consulate.

When do you need a visa?

Whether you require a visa for travel will depend on your citizenship, the country you are traveling to, your purpose for travel, and how long you intend to stay.

If you’re a U.S. citizen, one way to find out if you need a visa to travel is to use the State Department’s Learn About Your Destination tool, which contains visa information for most countries. Keep in mind that visa rules can change, so it’s best to verify entry requirements even if it’s a country you’ve been to in the past.

Visa and passport differences

Here’s a quick overview of the differences between a passport and a visa:

Document purpose

Identity verification.

Permission to visit a country.

Issuing authority

Your country of citizenship or nationality.

The embassy or consulate of the country to which you are traveling.

When it is needed

When traveling internationally, with limited exceptions.

When traveling to a country that requires a visa or when traveling for a reason that requires a visa.

Usually valid for 10 years, though validity times vary.

Often valid for the duration of your permitted stay, but may be valid for longer periods.

Visa vs. passport recapped

A passport is for identity verification, while a visa permits you to enter a country.

If you’re traveling internationally, you’ll need a passport. In addition to your passport, some countries require you to apply and be approved for a visa in advance of your travel.

You might also need a visa if you’re traveling for a specific nontourism purpose, such as work or study.

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are our picks for the best travel credit cards of 2023, including those best for:

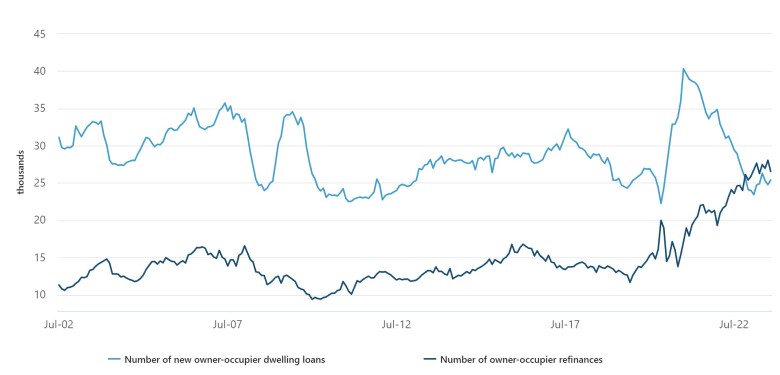

New owner-occupier loan commitments for dwellings rose 2.5%.

Dwelling approvals rose 7% in seasonally adjusted terms.

Master Builders forecasts a decline in home starts

Upticks in dwelling approvals and home lending have been recorded across August, according to the latest from the Australian Bureau of Statistics (ABS).

Dwelling approvals rose 7.0% in seasonally adjusted terms, and owner-occupier loan commitments for dwellings rose 2.5%.

New loans rise in August

New owner-occupier loan commitments for dwellings rose 2.5% in August, according to the ABS. However, the latest is still 12.3% below last year’s figures.

“Since February 2023, the number of new owner‑occupier loans appears to have returned to levels seen before the COVID-19 pandemic began, well below the peak in January 2021,” said ABS head of finance statistics, Mish Tan.

New owner-occupier dwelling loans vs external refinancing, number of commitments, Australia

Source: Australian Bureau of Statistics, new owner-occupier loans increased 2.5% in August 3/10/2023.

Refinancing numbers dropped, with the ABS figures on refinanced owner-occupied loan commitments between lenders falling 5.4% to 26,539; refinancing was at an all-time high last month.

“Since November 2022, the number of refinanced loans has been above the number of new owner‑occupier loan commitments. Refinancing has remained at unprecedented levels as households continued to seek better loans amid a high interest rate environment,” said Tan.

More homes to kick off construction

The latest 7% rise in dwelling approvals follows a 7.4% fall in July. The seasonally adjusted total homes approved for August came in at 13,647, with private sector houses comprising 8,635 homes, and private sector dwellings excluding houses coming in at 4,779.

“Approvals for private sector houses rose by 5.8%, following three months of stable movements,” said ABS head of construction statistics, Daniel Rossi.

“Approvals in the more volatile private sector dwellings excluding houses series rose by 9.4%, following a 14.6% fall in July”.

Dwelling units approved, by building type, seasonally adjusted

Source: Australian Bureau of Statistics, dwelling approvals rise in August 3/10/2023.

While there was a broad uplift, results were mixed state by state. New South Wales, Victoria, and Western Australia all recorded rises in dwelling approvals, up 12.5%, 22.2%, and 12.3% respectively. Queensland, Tasmania, and South Australia all recorded declines, down 26.9%, 10.1%, and 6.9% respectively.

“Both detached houses and higher density home building approvals shared in the expansion up 6.0% and 8.8% respectively,” observed Master Builders Australia (MBA) chief economist, Shane Garrett.

“However, the volume of new approvals is still considerably lower than this time last year.

“Over the year to August 2022, new home building approvals are still down by 13.0%.

“Detached house approvals have suffered a sharp reversal since their peak during the COVID.

“The pipeline of higher density home building activity, which is critical to ensuring adequate rental supply, has been weak since even before the pandemic.

“We still need to see a sustained improvement in the volume of higher density home building in order to relieve inflation which is at 15-year highs,” said Garrett.

Rate reprieve delivered

“The decision by the RBA to hold interest rates for a fourth consecutive month is a welcome reprieve for mortgage holders and renters who are bearing the brunt of the cost of living crisis,” added Wawn.

“The effect of the RBA’s tightening cycle is still flowing through to the sector and dampening investment.

“Master Builders has forecast 2023-24 will see home starts decline by another 2.1% to around 170,100, well below the 200,000 needed per year to meet population growth.”