DOJ’s concern over housing affordability and commission rates For the mortgage sector, the spotlight on commission rates comes at a time when the housing market is already grappling with low supply and escalating mortgage costs. The Biden administration’s focus on these rates is intertwined with the broader issue of housing affordability. On a median existing-home … [Read more…]

Many people are lured into the world of real estate investing by stories of millionaires who started their journey with no money down or no steady employment. But the reality is that making money in real estate isn’t easy; a good credit score, investment capital and steady income can help in the beginning.

You’ll also need to grasp the nuances of the local real estate market and learn how to manage financial aspects such as cash flow and property taxes. While real estate buying, selling, and renting may not be much like a game of Monopoly, it is possible to earn steady side income, supplement your retirement, or even build a full-time real estate investment business with the right tools, knowledge, and patience.

Unlike mutual funds, the stock market, cryptocurrency or many other investments, real estate is tangible. Real estate is a concrete asset—one can see, touch, and even reside in. That gives investors a sense of security. However, it also creates unique challenges.

Managed well, the stability and passive income from rental properties can be a safety net against more volatile investments.

This guide is here to clarify the process for beginners. It aims to empower you to make informed decisions, reduce risks, and lay a strong foundation for your real estate investing journey.

Benefits of Investing in Real Estate

The allure of real estate goes beyond the mere ownership of tangible assets. It presents a robust suite of financial benefits that have the potential to amplify wealth and provide stability in uncertain times. As we navigate the advantages, it becomes evident why many seasoned investors prioritize real estate in their portfolios.

Steady and Passive Income

Real estate investing, especially in rental properties, stands out for its potential to provide a consistent revenue stream. When you own a rental property, the monthly or quarterly distributions from tenants contribute to steady income, which can safeguard your finances against unexpected events or economic downturns.

This consistency contrasts with the often erratic nature of the stock market, which can fluctuate daily based on global events, company performances, and other factors. Additionally, for those aiming to attain financial freedom, the passive income generated from real estate can be a step closer to achieving that goal. Over time, as the mortgage payment decreases or remains static, rental rates may rise, increasing your monthly cash flow.

Appreciation Potential

Every investor dreams of their assets appreciating, and real estate often doesn’t disappoint. While there can be periodic downturns in the real estate market, historical trends suggest that properties generally gain value over the long run.

This means that not only can investors benefit from rental income, but they can also potentially see substantial gains when they choose to sell the property.

Tax Benefits

Navigating the world of taxes can be intricate, but real estate investors often find several advantages here. The ability to deduct mortgage interest and property taxes from taxable income can be a significant financial boon.

Furthermore, strategies like depreciation allow real estate investors to offset rental income, reducing their tax burden. Consulting with a financial advisor can help investors maximize these benefits and understand other potential tax advantages, such as 1031 exchanges or deductions related to property management.

Diversification

The saying “don’t put all your eggs in one basket” is sound investment advice. Diversification is a fundamental strategy to mitigate risks. By adding real estate to an investment portfolio, investors introduce a separate asset class that doesn’t directly correlate with the stock market or mutual funds. This can provide a buffer, ensuring that a downturn in one sector doesn’t wholly derail an investor’s financial trajectory.

Leverage

Leverage, in the context of real estate investing, refers to the ability to use borrowed capital to increase the potential return on an investment. When you purchase property with a mortgage loan, you’re often putting down only a fraction of the property’s total cost, while still reaping the benefits of its entire value in terms of appreciation and rental income.

This magnifies the return on investment, as the gains and income generated are based on the property’s total value, not just the down payment. It’s a powerful tool but should be used wisely. Over-leveraging or not accounting for potential rental vacancies can turn leverage into a double-edged sword.

Types of Real Estate Investments

As one dives deeper into the world of real estate, it becomes evident that this asset class is multifaceted, with various avenues to explore and invest in. The right choice often depends on an investor’s goals, risk tolerance, budget, and expertise. Here’s a closer look at some prominent types of real estate investments:

Residential Properties

Residential properties cater to individuals or families. They range from single-family homes to duplexes, triplexes, high-rise buildings with apartments, and other multi-unit properties. You may encounter the term “MDU” or “MUD,” which stand for multi-dwelling unit or multi-unit dwelling, to describe anything more than a single family home, or SFR (single family real estate).

Investing in residential real estate, especially the SFR market, is often a beginner’s first step due to its familiarity and the perpetual demand for housing. While these properties can be a reliable source of rental income, investors should be prepared for the challenges tied to property management, tenant turnover, and ongoing maintenance.

Commercial Real Estate

When one thinks of skyscrapers lining city horizons or sprawling office parks in suburban locales, that’s commercial real estate. These properties are tailored to businesses, and can include complete corporate headquarters or individual offices.

Commercial leases often run longer than residential ones, offering the potential for stable, long-term rental income. However, the entry point can be higher, with larger down payments and a more extensive due diligence process. Additionally, commercial real estate values can be closely tied to the business environment of the locality.

Industrial

Industrial real estate encompasses properties like warehouses, distribution centers, and manufacturing facilities. They’re integral to business operations, ensuring products move efficiently from manufacturers to consumers.

Investing in this sector can offer substantial rental yields, especially if the property is strategically located near transportation hubs. However, the nuances of industrial real estate, such as zoning laws and environmental concerns, necessitate a more in-depth understanding than residential or commercial sectors.

Retail

This sector includes shopping malls, strip malls, and standalone stores. What’s unique about retail real estate is that leases sometimes include a provision where the landlord gets a percentage of the store’s profits, termed as “percentage rent.”

In a thriving commercial area, retail properties can be quite profitable, with long-term leases and the potential for appreciating property values. However, investors should be mindful of shifts in consumer behavior and the evolving retail landscape, especially with the rise of e-commerce.

Multi-Purpose Commercial

A new breed of commercial real estate has emerged to compete with the growth of e-commerce. Multi-purpose commercial spaces blend housing units with office space and retail, often adding hospitality and entertainment venues.

Typically, these spaces are the domain of large real estate investment and property management firms. But if you invest in commercial office space or retail, you will be competing with these multi-purpose properties for tenants, so they are worth acknowledging.

Real Estate Investment Trusts (REITs)

For those not keen on direct property ownership, REITs present an attractive alternative. These are companies that own, operate, or finance income-producing real estate across various sectors. What makes REITs distinctive is that they’re traded on stock exchanges, similar to stocks.

By investing in a REIT, you’re buying shares of a company that manages a portfolio of properties, thus gaining exposure to real estate without the hassles of property management. Moreover, by law, REITs are required to distribute at least 90% of their taxable income to shareholders, leading to potentially attractive dividend yields. However, it’s essential to remember that like all publicly traded entities, REITs can be subject to market volatility.

9 Ways to Invest in Real Estate

Investing in real estate can seem tricky for beginners. But, with time and patience, anyone can master it. Focus on simple investment methods first to get to know your local property scene, meet experienced investors, and learn how to handle money wisely. As you learn and grow, you can dive into more complex investment options.

Here are some great ways for beginners to start in real estate:

1. Wholesaling

Acting as the bridge between property sellers and eager buyers, this method primarily focuses on securing properties at a rate below the prevailing market value. The secured contract is then transferred to an interested buyer, ensuring a margin for the wholesaler.

2. Prehabbing

Unlike intensive property renovations, prehabbing is about amplifying a property’s appeal through minimalistic enhancements. These properties, once given their facelift, usually attract investors with a keen eye for larger renovation projects.

3. Purchasing Rental Properties

An avenue promising consistent returns, this involves acquiring properties to lease them out. For those not inclined towards the intricacies of landlord duties, there’s always the option of hiring seasoned property management professionals.

4. House Flipping

A strategy that has garnered significant attention, house flipping involves a cycle of purchasing, upgrading, and promptly reselling properties, aiming for a profit. The emphasis is on swift transactions and keen market acumen.

5. Real Estate Syndication

Envision a collective where like-minded investors come together, pooling both resources and expertise. Such collectives venture into large-scale property acquisitions, and the ensuing profits or rental incomes are distributed among the participants.

6. Real Estate Investment Groups (REIG)

Primarily, these are conglomerates that steer their operations around real estate investments. By amassing capital from a plethora of investors, they dive into acquisitions of sizeable multi-unit residences or commercial holdings.

7. Investing in REITs

Real Estate Investment Trusts (REITs) revolve around the ownership and meticulous management of properties that yield income. However, investors don’t have to handle the management themselves. Instead, participants can relish the benefits of the real estate sector without the responsibilities of direct property ownership.

8. Online Real Estate Platforms

A fusion of technology with real estate, these platforms seamlessly connect potential investors with vetted property developers. This synergy enables backers to finance promising property ventures and, in exchange, enjoy periodic returns that encompass interest.

9. House Hacking

A blend of homeownership and investment, house hacking is about maximizing the potential of a multi-unit property or a single-family home. Investors live in one segment while leasing out the remaining portions. This dual approach can significantly reduce or even negate monthly housing expenses, serving as an excellent introduction to the world of property management for novice investors.

6 Steps to Get Started in Real Estate Investing

Starting on the path of real estate investing requires careful planning, due diligence, and a methodical approach to ensure that your investments are sound and have the potential for fruitful returns. Whether you’re dreaming of becoming a millionaire real estate investor or merely looking to diversify your investment portfolio, following a structured process can be the key to success. Here’s a step-by-step breakdown:

1. Assess Your Financial Health

Every investment journey should begin with introspection. As an aspiring real estate investor, it’s essential to have a clear understanding of your current financial standing. Ask yourself questions like:

How much capital am I willing to invest?

What are my short-term and long-term financial goals?

Do I have an emergency fund set aside?

Evaluating your risk tolerance is equally crucial. Some might be comfortable flipping houses, while others might prefer the steadiness of rental properties. Consulting a financial advisor at this stage can provide insights tailored to your financial health, enabling you to make informed decisions as you proceed.

2. Dive Deep into Market Research

Knowledge is power in the world of real estate. The local market can be significantly different from national or even statewide trends. Delve deep into understanding:

The demand for rental properties in your target area.

The average property values and rental rates.

The historical appreciation rates.

Any upcoming infrastructure projects or urban development initiatives.

Furthermore, familiarize yourself with real estate terminology. Phrases like “cap rate,” “loan-to-value,” and “operating expenses” will become a regular part of your vocabulary. The better informed you are, the more confidently you can navigate your investments.

3. Assemble Your Real Estate Team

No investor is an island. Success in the real estate business often hinges on the strength and expertise of your team. Look for professionals with a proven track record and positive reviews. Your team might include:

Real estate agents who understand the investor’s perspective.

Property managers to streamline tenant interactions and maintenance.

Lawyers specializing in real estate transactions.

Accountants familiar with the tax implications of real estate investments.

4. Explore Financing Options

The path to acquiring a property is paved with various financing methods. Traditional mortgages are common, but the real estate industry offers other mechanisms like:

Hard money loans.

Private money loans.

Real estate syndication where multiple investors pool resources.

Seller financing.

Each of these has different pros and cons, interest rates, and repayment terms. Understand each deeply to determine which aligns best with your financial strategy.

5. Analyze Potential Properties

The crux of real estate investing is ensuring that the numbers make sense. Before purchasing, assess the property’s potential for generating rental income. Break down:

Monthly mortgage payments

Property taxes

Maintenance costs

Potential vacancy rates

Your goal should be a positive cash flow, where the monthly income from the property (rent) exceeds all these expenses.

6. Negotiate and Close the Deal

Once you’ve zeroed in on a property, the negotiation phase begins. Here, understanding the property’s market value, any existing damages or repair needs, and the local real estate market dynamics can give you an edge.

When it comes to closing, be aware of all associated costs. These might include inspection fees, title insurance, and escrow fees. Being well-informed can help you negotiate these fees and ensure that you’re not overpaying.

Risks and How to Mitigate Them

Like any investment, real estate comes with its set of challenges and uncertainties. The difference between successful real estate investors and those who falter is often the ability to anticipate risks and prepare for them. Here’s an exploration of some prevalent risks in real estate and actionable steps to manage them:

1. Market Fluctuations

Real estate markets can be volatile, with property values rising and falling based on a myriad of factors.

Mitigation: To protect against market downturns, it’s essential to buy properties below their market value. Conducting comprehensive research and seeking expert investment advice can help investors make informed decisions. Remember, real estate is often a long-term game, so a short-term dip can be offset by long-term appreciation.

2. Unexpected Repairs and Maintenance

Properties can often come with surprises, from plumbing issues to roof repairs.

Mitigation: Regular property inspections can catch potential problems before they become major expenses. Setting aside a buffer fund specifically for maintenance can also cushion the financial blow of unforeseen repairs.

3. Vacancy Periods

There might be periods where your property remains unoccupied, leading to loss of rental income.

Mitigation: Properly vetting and building a good relationship with tenants can lead to longer lease periods. Diversifying your investment properties across different areas can also help, as vacancy rates might vary from one location to another.

4. Legal and Tax Implications

Real estate investors can sometimes find themselves entangled in legal disputes or facing unexpected tax bills.

Mitigation: Regular consultations with a tax professional or attorney familiar with the real estate industry can keep investors informed and protected.

Long-term Strategy and Growth

Real estate investing is not just about making a quick buck; it’s about building lasting wealth. Adopting a long-term perspective and continuously refining your strategy can pave the way for consistent growth in the real estate industry. Here’s how:

1. Define Your Real Estate Identity

Are you more comfortable with a buy-and-hold strategy, where properties are retained for long-term growth and steady rental income? Or do you thrive on the excitement of flipping houses, where properties are bought, renovated, and sold for profit? Understanding your preference can help tailor your investment strategy.

2. Reinvestment is Key

For those adopting a buy-and-hold strategy, reinvesting the rental income can substantially grow your real estate portfolio. By channeling profits into purchasing additional properties, investors can benefit from compounded growth.

3. Diversify Your Portfolio

As you gain experience, consider diversifying across various real estate sectors. Branching out into commercial real estate or exploring real estate investment trusts (REITs) can provide additional avenues for income and growth.

4. Continue Your Education

The real estate industry is continually evolving. By staying updated on market trends, attending seminars, and networking with other real estate professionals, you can adapt your strategy and seize new opportunities as they arise.

5. Scale Strategically

A real estate empire begins with just one property. With time, dedication, and a sound strategy, it’s possible to grow your holdings into a substantial full-time income. As you scale, ensure you’re not overextending; always prioritize the quality of investments over quantity.

Key Tips for Beginners

Embarking on a journey into real estate investing can be thrilling, yet the complexities of the industry can sometimes overwhelm beginners. Simplifying the learning curve is essential for novice investors to make informed decisions and find success. Here are some pivotal tips to guide those just starting out:

1. Start Small and Scale Gradually

Many millionaire real estate investors began their journey with a modest property. Purchasing a smaller, more manageable property as your first investment can help you navigate the nuances of the real estate business without being overwhelmed. As you gain confidence and experience, you can then venture into bigger and more diverse properties to scale your portfolio.

2. Prioritize Education

The world of real estate is vast and ever-evolving. Leverage online real estate platforms to learn about market trends, investment strategies, and financing options. Additionally, joining real estate investment groups can be invaluable. These groups not only provide mentorship but also offer opportunities to share resources, insights, and deals with other investors.

3. Location is Crucial

In the real estate realm, location often takes precedence over the type or condition of a property. A mediocre house in a prime location can fetch better returns than a grand mansion in a less desirable area. Research local market dynamics, neighborhood amenities, future development plans, and other location-specific factors before making an investment decision.

4. Networking is Key

Surrounding yourself with knowledgeable people can fast-track your learning process. By connecting with seasoned real estate investors, you can gain insights from their experiences, avoid common pitfalls, and even discover potential partnership opportunities. Attend local real estate seminars, join investor forums online, and participate actively in real estate conferences to grow your network.

5. Stay Updated and Adapt

The real estate industry is not static. Market conditions, property values, and investment strategies can change. Being adaptable and staying updated on industry trends will ensure you remain ahead of the curve and can capitalize on new opportunities.

6. Always Conduct Due Diligence

Before diving into any real estate transaction, thorough due diligence is imperative. From understanding property taxes and zoning laws to estimating potential repair costs and evaluating tenant profiles, leaving no stone unturned will protect you from potential setbacks.

8 Terms Beginner Real Estate Investors Should Know

Venturing into real estate can feel like you’ve entered a world with its own language. Don’t worry; everyone feels this way at the start. Knowing basic real estate terms can help you communicate confidently and make informed decisions.

Dive into these essential terms every beginner should grasp:

Appreciation: Appreciation is the increase in the value of a property over time. It’s one of the primary ways real estate investors make money, especially in growing markets. Appreciation can result from factors like inflation, increased demand, or improvements made to the property.

Capitalization rate (cap rate): Think of the cap rate as a tool to gauge the potential return on a property. It’s a percentage derived from comparing a property’s net operating income to its current market price.

Cash flow: This term captures the money dance – what’s coming in and what’s going out. In the context of rental properties, it means the rental earnings minus all the costs. Positive cash flow indicates you’re earning more than you’re spending.

Equity: Equity represents the value of ownership in a property. It’s calculated by taking the market value of the property and subtracting any outstanding mortgage or loans against it. As an investor pays down their mortgage or if the property appreciates in value, their equity in the property increases. This equity can be tapped into for various financial needs or reinvested.

Leverage: This term refers to the concept of using borrowed money, often in the form of a mortgage, to invest in real estate. It allows investors to purchase properties with a small down payment and finance the remainder. When used correctly, leverage can amplify returns, but it can also increase the risk if property values decline.

Net operating income (NOI): Simplified, NOI is the profit made from a property after deducting all operational costs. It’s your rental income minus all the expenses, showing the true earning potential of a property.

Real estate owned (REO): An REO property is one that didn’t sell at a foreclosure auction and is now owned by the bank. These properties are often sold at a lower price because banks aim to sell them quickly, making them attractive to investors.

Return on investment (ROI): In simple terms, ROI measures the bang you get for your buck. It’s calculated by comparing the profit you made to the amount you invested. The higher the ROI, the better your investment performed.

Conclusion

Real estate investing offers an avenue to diversify your portfolio, generate steady income, and potentially achieve long-term growth. With due diligence, a clear strategy, and the right team, beginners can successfully navigate the complexities of the real estate industry and lay the foundation for a prosperous investment journey. Remember, every millionaire real estate investor started with their first property. Your journey is just beginning.

AI and data-led fintech company Pagaya Technologies named Sanjiv Das as president. Das, a former CEO of Caliber Home Loans, will begin his new role on Oct. 16.

His responsibilities include overseeing the strategy and growth of Pagaya’s commercial business – including its single-family rental business and its subsidiary Darwin Homes – as it continues to enhance its tech-enabled product offering and expand its new and existing lending partnerships, the firm said in a news release.

“We’re excited to welcome Sanjiv as President of Pagaya. His global perspective and extensive entrepreneurial experience in the financial sector and capital markets, as well as his proven track record of building and growing global businesses at scale, uniquely positions him to guide Pagaya’s lending network and innovative product offerings in this next stage of growth,” Gal Krubiner, Pagaya’s co-founder and CEO, said.

Das spent six years as CEO of Caliber Home Loans — a NewRez-owned residential mortgage lending company — until January 2022.

Das’ career also includes positions as CEO, president and chairman of the board of directors for Citigroup‘s mortgage division. He has also held senior roles at Morgan Stanley, American Express and Bank of America.

The executive replaces Ashok Vaswani, who served as Pagaya’s president since June 2022. Vaswani will serve as an advisor to Pagaya for a smooth transition for Das.

“Under Vaswani’s leadership, Pagaya has successfully onboarded new, large partners and expanded its AI-driven lending network, enabling access to more financial opportunities for their customers,” the firm said.

Pagaya, founded in 2016, provides comprehensive consumer credit and residential real estate solutions for its partners, their customers and investors, according to the firm’s website. The fintech has more than 600 employees across two offices in New York and Tel Aviv, Israel.

The firm has been in the real estate business since 2020. Pagaya also offers personal loans, auto loans, credit cards and point-of-sale (POS) financing.

In January 2023, Pagaya acquired proptech Darwin Homes to capitalize on the rental market.

Targeting the single-family rental market, Pagaya shared plans to combine its AI tech and data network with Darwin’s software, operations and mobile app to create a “tech-forward” real estate platform that benefits residents, investors and service operators, the firm said at the time of acquisition.

PNC Bank issued pink slips to an undisclosed number of employees this week as part of its focus on controlling costs.

“As part of our strong focus on expense management, we have reviewed our organizational structure and have identified an opportunity to better position our company for long-term success. This includes a shift away from work not fully aligned to our strategic priorities and will result in a reduction in staffing levels in certain areas,” the company’s spokesperson said in an emailed statement.

While the spokesperson declined to comment further, an affected former employee’s LinkedIn post showed that her position would be eliminated on Dec. 1.

No Worker Adjustment and Retraining Notification (WARN) notices were submitted to the Pennsylvania Department of Labor & Industry. PNC is headquartered in Pittsburgh.

“We’re going to have to take a hard look at where we can generate savings in this company without cutting the potential for growth,” Bill Demchak, CEO of PNC, told analysts during its Q2 earnings call in July.

After setting a target to cut $400 million in expenses by 2023 at the beginning of the year, PNC increased that to $450 million in July.

PNC’s non-interest expense for the first half of 2023 was $6.7 billion, up from $6.4 billion during the same period in 2022.

HousingWire was unable to confirm which lines of business were affected, but it follows PNC’s layoffs in July when it made “limited organizational changes” within its mortgage and home equity groups, the spokesperson confirmed.

PNC has a retail banking business that covers residential mortgage, corporate and institutional banking and asset management.

The company reported total consumer loans of $101.8 billion, including residential mortgages, automobile, home equity and credit card loans in the first half of 2023, according to its 10-Q filed with the Securities and Exchange Commission (SEC).

Of the $101.8 billion in consumer loans, residential real estate loans took up 46% of the total volume at $46.8 billion in origination as of June 30.

PNC has 11,986 registered mortgage loan originators, according to the Nationwide Licensing System (NMLS).

WASHINGTON (September 14, 2023) – The current real estate market’s high home prices and mortgage rates, as well as limited inventory, are the top reasons that Realtors® and prospective home buyers across races and ethnicities cite as barriers to purchasing a home, according to two new reports from the National Association of Realtors®.

In partnership with Morning Consult, NAR’s 2023 Experiences & Barriers of Prospective Home Buyers Across Races/Ethnicities report surveyed White, Hispanic/Latino(a), Black and Asian prospective home buyers about their experiences. NAR’s 2023 Experiences & Barriers of Prospective Home Buyers: Member Study surveyed Realtors® who focus on residential real estate regarding the latest buyer with whom they worked who has not yet purchased a home, and it compares findings with the consumer study.

“Home buyers face the most difficult affordability conditions in nearly 40 years due to limited inventory and rising mortgage interest rates,” said Jessica Lautz, NAR’s deputy chief economist and vice president of research. “The impact is exacerbated among first-time buyers who are more likely to be from underrepresented segments of the population.”

Among prospective home buyers, Asian (27%), Hispanic (24%), Black (20%) and White (15%) respondents say the main reason they have not yet bought a home is because they are waiting for prices to drop. White respondents (15%) are just as likely to say it is because they are waiting for mortgage rates to drop. Additional market-related reasons that prospective home buyers cite as barriers include waiting for mortgage rates to decline (18% – 25% of all four groups) and not enough available homes within their budget (19% – 24% of all four groups).

The top three reasons why Realtors® say buyers have not yet purchased homes are the same as reported by consumers: not enough homes available for purchase in buyers’ budgets (34%), buyers are waiting for mortgage rates to drop as higher prices affect affordability (18%) and buyers are waiting for prices to drop (9%). These three factors greatly impact affordability since limited inventory drives up home prices and higher rates increase monthly mortgage payments.

Saving for a competitive home down payment is also a primary obstacle for prospective home buyers (6% – 9% of all four groups). In terms of what holds them back from saving for a sufficient down payment, prospective home buyers across races and ethnicities cite as barriers current rent/mortgage payments (43% – 56% of all four groups) and credit card payments (38% – 57% of all four groups). Despite this, awareness about existing down payment assistance programs is low among prospective buyers saving for down payments. Only 8% – 15% of all four groups applied for these programs, 20% – 33% considered but did not apply to these programs, 21% – 32% did not consider these programs, and one-third (30% – 33% of all four groups) say that they are not aware of these assistance programs. For prospective home buyers who are aware of down payment assistance programs, the primary reason they did not apply for them is because they did not know enough about the programs (44% – 58% of all four groups).

Likewise, more than half of Realtors® (53%) say that at least one issue is holding their latest buyer back from saving a competitive down payment: most likely current rent or mortgage payments (23%) or credit card balances or payments (17%). Further, only 23% of Realtors® say that their buyers experiencing these challenges have applied for down payment assistance programs. This is most likely because their income is too high (30%), they did not know enough about the programs (19%), or they are worried about the competitiveness of their offers in multiple-bid situations (17%).

“Down payment assistance programs often fly under the radar for potential home buyers. Using programs – like FHA, VA or USDA loans – can make homeownership more attainable. Experts, such as agents who are Realtors®, can educate potential buyers about these programs. Doing so will bring in more first-time buyers and narrow the racial homeownership gap,” added Lautz.

Discrimination also plays a role in the homebuying process. About one in six (13% – 16% of all four groups) prospective home buyers across races and ethnicities report facing discrimination. More than half of Black (63%), Asian (60%) and Hispanic (52%) prospective home buyers who report this say it was due to their race or ethnicity. Of these, the largest proportions of every group are most likely to report that this discrimination manifests in steering toward or away from specific neighborhoods (36% – 51% of all four groups) and more strict requirements (32% – 48% of all four groups). Despite all of this, most discrimination during the homebuying process goes unreported: 47% – 81% who describe it did not report it to a government agency or legal aid organization.

Interestingly, only 1% of Realtors® who took the survey report that their buyers experienced discrimination during the homebuying process, while 13% are not sure. Those reporting discrimination are most likely to say this is based on race or ethnicity and lay this at the feet of lenders, saying that buyers experienced this in the type of loan product offered (43%) or that buyers did not receive a call back from lender(s) (29%). Of those who report discrimination, 57% report it based on race, 29% report it based on age and 21% report it based on familial status (including marriage or parental status). Just 7% say that the buyer reported the discrimination, which was on the basis of either race or religion or both, to a government agency or legal aid organization.

To help address discriminatory practices in real estate, NAR offers several resources to its members, including Fairhaven, an interactive training simulation based on real fair housing cases; Bias Override, an implicit bias training course with practical tips to override bias; At Home With Diversity, a certification course aimed at serving diverse consumers; and a confidential voluntary self-testing program for brokerages to assess agents’ compliance with fair housing laws. In Washington, NAR advocates for strong fair housing and fair lending enforcement, and policies aimed at closing homeownership gaps among demographic groups.

About the National Association of Realtors®

The National Association of Realtors® is America’s largest trade association, representing more than 1.5 million members involved in all aspects of the residential and commercial real estate industries. The term Realtor® is a registered collective membership mark that identifies a real estate professional who is a member of the National Association of Realtors® and subscribes to its strict Code of Ethics.

Newrezhas launched Onward Home Mortgage, a joint venture mortgage companyin partnership with Keller Williams Georgia Legacy Group (GLCG).

Through the partnership with agents at Keller Williams GLG, mortgage professionals at Onward Home Mortgage and Newrez will target borrowers in the Southeast United States.

“This is a marriage of outstanding organizations that will now grow even stronger. I am humbled and honored to lead such a talented group of professionals and can’t wait to continue getting more borrowers into the homes of their dreams,” Kathy Vitali, President of Onward Home Mortgage, said in a prepared statement.

Headquartered in Roswell, Georgia, Onward Home Mortgage specializes in residential purchase mortgage lending and has a presence in the greater Georgia and Alabama areas. It is part of the Newrez Ventures platform.

GLG is a Keller Williams Realty franchise group of residential real estate brokerages located in Georgia, servicing Alpharetta as Keller Williams Realty North Atlanta, Roswell as Keller Williams Realty Consultants, Peachtree Corners as Keller Williams Realty Chattahoochee North and surrounding metropolitan Atlanta areas.

Established in 2017 as a group, the three franchises have been in operation independently for more than two decades and have more than 2,000 licensed real estate agents in Georgia.

Newrez has 15 joint venture partners including Carolina One Mortgage, Shelter Mortgage Company and Summit Home Mortgage, according to its website.

“Newrez and Newrez Ventures’ commitment to bringing affordable housing to borrowers nationwide continues as Onward’s vast product suite tailors uniquely to the needs of today’s borrowers, from FHA to First Time Homebuyer programs,” Newrez said.

A joint venture typically ramps up faster than a traditional mortgage company. At a mortgage brokerage joint venture, loan officers generally get paid a lower base salary than counterparts at traditional lenders and may get a smaller commission because the LO is doing less work finding customers as there are greater real estate agent referrals.

Though the mortgage-real estate brokerage JV model was popular during the pandemic years, the Consumer Financial Protection Bureau’s relative newfound interest in scrutinizing possible RESPA violations could chill interest.

Cecilian Partners, a proptech firm that offers comprehensive digital solutions for home builders and land developers, has successfully raised $11 million in its first institutional equity round led by Resolve Growth Partners. This funding will enable Cecilian to accelerate product innovation, expand its workforce in crucial areas, and further enhance its customer success team.

John Cecilian, Jr., the company’s co-founder and CEO, expressed his excitement and validation upon receiving the term sheet from Resolve Growth Partners:

“This investment transitions us from a ‘scrappy start-up’ to a focused organization positioned to win. We are grateful to the team at Resolve and ready to accomplish meaningful growth and customer expansion.”

Despite a recent decline in early-stage funding, Resolve selected Cecilian Partners after conducting extensive due diligence and evaluating numerous SaaS companies. They were impressed by Cecilian’s impressive revenue growth, proven business model, and a clear path to profitability.

“We’re thrilled to have the opportunity to partner with John and the rest of the team at Cecilian Partners to build the category-leading platform for land developers and home builders,” said Resolve co-founder and Managing Partner Chris Rhodes. “This market has traditionally been underserved by technology. Cecilian offers a first-of-its-kind solution to help its customers transform their businesses through digitization and a true partnership approach.”

Since its establishment in 2019, Cecilian Partners has focused on serving the rapidly growing new homes segment in residential real estate. Their innovative software suite streamlines the land and property development process, consolidating data, automating manual tasks, and providing an enhanced customer experience throughout the homebuying journey.

Cecilian’s revenue tripled in the past year, surpassing the typical growth rate for early-stage SaaS companies. Additionally, their client base expanded by 65%. The company now serves builders and developers across multiple states, boasting over 75 clients in Texas and Florida alone, where nearly one-third of all new homes in the US are constructed.

In addition to securing funding, Cecilian was recognized for its achievements throughout the year. They were included in the HousingWire TECH100 list, honored with a PHL Inno Fire Award, and acknowledged as one of the best places to work in the greater Philadelphia area.

With Resolve’s support, Cecilian will accelerate its pace of product innovation and talent acquisition. They will also benefit from Resolve’s financial expertise and experience in building successful SaaS companies. As part of this strategy, the company’s Board of Directors will undergo restructuring, with Chris Rhodes and Rocco Natalicchio from Resolve joining the board. Stephanie McCarty, Chief Marketing & Communications Officer at Taylor Morrison, and Ned Moore, co-founder and CEO of Clutch, will continue to serve on the board, bringing their expertise in real estate development and SaaS markets, respectively.

Stephanie McCarty expressed her belief that Cecilian Partners is well-positioned to drive innovation in the new home construction industry. She highlighted the company’s expansive suite of products, which can address outdated processes and longstanding challenges, ultimately enhancing the experience for customers, builders, and developers.

With Resolve’s investment, Cecilian will rapidly expand its team by hiring key roles in business development, in-house technology and research, customer success, and marketing. These new hires will help capture growth opportunities, drive innovation, improve client support, and increase brand visibility across the country. Over the next 12-15 months, Cecilian plans to increase its workforce by 50%, with additional staff based in Chicago, Dallas, Raleigh, and their headquarters in New Hope, Pennsylvania.

Find me on:

Mihaela Lica Butler is senior partner at Pamil Visions PR. She is a widely cited authority on public relations issues, with an experience of over 25 years in online PR, marketing, and SEO.She covers startups, online marketing, social media, SEO, and other topics of interest for Realty Biz News.

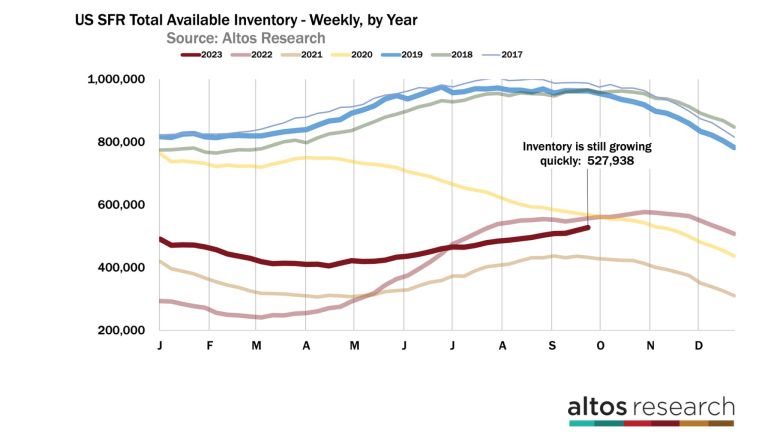

Available inventory of homes for sale is on the rise in late September, which is very unusual for this time of year. In fact, inventory is growing faster than this time a year ago.

This is a demand-driven slowdown, because new listings supply is still running 9% to 10% fewer homes for sale each week than this time last year. We’re seeing fewer new sellers each week, but inventory is building as homebuyers wait to see if mortgage rates will come down to make purchases more affordable.

What’s happening with inventory?

Fewer new sellers also means that inventory can’t grow too much; the real trouble develops when demand drops and supply surges. There’s no supply surge, but there is a notable demand drop. Consumers are very sensitive to changes in mortgage rates, and rates are still rising.

We can see these slowing changes build up each week. It’s a pretty sharp change from what was a surprisingly strong first half of the year. There are now 528,000 single-family homes on the market. That’s an increase of 1.8% from last week.

Normally by this point in September, available inventory is declining slightly each week. It’s late in the summer, so normally new listing volume drops as the last few sales of the peak summer months are concluding.

The fact that inventory grew by nearly 2% this week and last week is telling of how homebuyers are reacting to the highest mortgage rates in over two decades.

In this chart of each year’s inventory curves, you can see that the number of homes on the market is climbing faster now than this time last year. This year is the dark red curve, and last year the light red. Mortgage rates continue to climb, so there is no immediate relief for homebuyers on the horizon either.

At this point, it looks like we may see inventory grow to the end of October like we did last year. Look at the divergence in the curves from this year and the tan line from two years ago when we were still in the middle of the pandemic housing boom and record-low mortgage rates.

Pending-home sales continue to lag

New pending sales each week continue to run 10% to 15% below last year’s pace. If you follow the National Association of Realtors when they publish their existing-home sales report each month, you know that the latest report for August showed a sales pace of only 4 million seasonally adjusted annual home sales.

We can already see in the NAR data that there are no signs of improvement for the sales count through September and October. The home sales that are in contract now will close mostly in October. It’s not hard to imagine that next month’s seasonally adjusted home sales data from NAR will come in under 4 million.

In this chart, each bar is the total number of home sales pending on any given week. The shorter the bar, the fewer sales that are in progress. The light portion of the bar is the count of new pendings each week.

There are now 344,000 single-family homes in contract to close in the next couple months. That’s 14% fewer than last year and almost 30% fewer than in September of 2021.

Home sales are limited by the decreased demand, of course, and they’re also limited by the very low supply of new listings. You can’t buy what’s not for sale.

We’ve been talking all year about the market being supply constrained. Right now, sales are limited by declining demand from still-climbing mortgage rates.

Price reductions climb again

We can see the impact of weaker demand starting to creep into the pricing indicators. In the chart below, we look at the leading indicator of this trend: price reductions. This is the percent of homes on the market that have taken a price cut from their original list price.

For a while earlier this year, demand was exceeding supply in residential real estate, and you could measure that demand with the price-reductions curve improving each week. As mortgage rates lurched over 7% to their new highs, suddenly there are fewer offers.

And home-price reductions are climbing again, with 37% of the market taking a price cut. That’s more than any recent year except last year at this time. Price reductions are accelerating now, which bodes negatively for future sales prices.

A normal, balanced market will have 30% to 35% of the homes for sale that have reduced their asking price in recent months. As this dark red line approaches 40%, that’s a clear indicator that buyers are making fewer offers. Remember, the slope of this line captures how many properties are taking new price cuts each week. And this slope is increasing now.

These are transactions that will happen in the future, so it implies sales price weakness in the fourth quarter, which you’ll hear about in the headlines after the new year. But you can see it in the data now.

The median sales price of single-family homes in the U.S. right now is $440,000. That’s down 1% from last week and it’s just a tiny fraction higher than this time last year.

We can see the pressure on home prices in recent weeks. Home prices step downward in September for the seasonal change every year, and you can detect strength or weakness relative to changes in other years.

What we see now is that year-over-year price gains are just barely positive. And the comparison is getting weaker, not stronger, as our current mortgage markets deteriorate. There are fewer offers, and those that do happen are doing so at slight discounts each week.

Last year at this time, there were big price discounts being applied. So, our October comparisons may get slightly easier, but I sure haven’t seen any signals of price strength now.

Looking ahead to the end of 2023

So the question is will Q4 this year be a little better than Q4 2022? The median price of the new listings is fractionally higher than last year at $398,500. It will be fascinating to watch the light colored line here over the next couple weeks.

The new listings are where you see price weakness first. And last year, they were already headed lower.

The price of the new contracts this week came in at $370,000. These are the pending-home sales that went into contract in the last week. Prices of the homes going into contract are lower than last year by a fraction.

The next few weeks will be interesting to track this stat, too. Last year in mid-September is when mortgage rates jumped from 6% to 6.5% to 7.5%. By early October, any offers that were made for purchases came in at notably lower price points.

By September 2022, new pending-home sales prices fell by 3% per week. Will that happen again? Mortgage rates are even higher now than they were last year.

In this chart, you’ll notice the light-colored line started a big decline during this week in 2022. That’s when buyers reacted to newly increased mortgage rates. So, we’re watching to see where the new contracts come in over the next few weeks.

The macro trends impacting mortgage interest rates and the Fed have not given us any reprieve yet. The signals are that mortgage rates are still headed higher.

Consumer expectations for future mortgage rates have moved higher, too, so potential homebuyers are less optimistic than they were at the start of the year. And that’s what we’re seeing in the data each week now.

However, it’s important to point out that while buyer demand has backed off this fall, there is still no sign of any surge in new supply coming to the market. It can be very easy to focus on the negative momentum.

People on the fence should also know that while their competition is lessening, there’s no sign of an inventory flood. That may be an important factor in their home-buying decisions.

Mike Simonsen is president and founder of Altos Research.

Fed’s inflation fight tightens the U.S. housing supply and makes home buying even more difficult

Conventional wisdom dictates that U.S. inflation will continue to decline as the Federal Reserve keeps interest rates high. This action, which makes loans more expensive for businesses and consumers, should lead to less spending, less consumption and higher unemployment.

Or at least that’s Econ 101. Yet both consumers and investors have acclimated to the current market environment. Moreover the key driver of inflation — housing — cannot be adequately contained through the Federal Reserve’s usual tactics.

In fact, the Fed’s policies have created a Catch-22 in the housing market by creating “golden handcuffs.” Instead of easing consumer demand, the Fed’s actions unintentionally restricted U.S. housing supply, resulting in a stalemate between home buyers and sellers. Homeowners who locked into historically low mortgage rates before and during the pandemic are now reluctant to sell, which in turn is increasing the likelihood of persistent higher inflation.

The case for this condition to persist , which the market is mostly failing to consider, continues to grow stronger as the odds of a recession fade. This should be an alarm bell and a potential opportunity for investors to redeploy at least part of their capital into hard assets to serve as a hedge against inflation risk.

The recession that never was

Many economists have predicted that a recession would hit the U.S. Their reasoning was sound: aggressive monetary action by the Federal Reserve, investor dissatisfaction with inflation, loss of consumer confidence and reductions in home asking prices — all points that were hard to argue against.

Yet most of the key ingredients needed for a recession have not materialized. Investors have acclimated to inflation, consumer confidence is growing and the housing market has, by and large, entered a period of stalemate where prices remain high due to lack of supply.

In fact, the only relevant argument in the recession camp that remains is the Fed continuing its aggressive posture against inflation — now considered the fastest monetary policy tightening cycle in more than 40 years. Such action continues to lead many to speculate that recession is imminent, and the only questions left to answer are “when,” and “how deep it will be?”

Housing prices obey the laws of supply and demand

Housing is perhaps the most consequential category that makes up the Consumer Price Index (CPI), which markets track every month as a core measure of inflation.

The undersupply of housing in the U.S. is grounded in years of underbuilding and is not the result of a single federal policy, war, or external event. If anything, the power to create more housing supply rests with state and local governments, which often require working through a patchwork quilt of differing zoning and land-use regulations.

The high estimate of the country’s current housing shortage is pegged at about 7.3 million units, while the most conservative estimate shows it to be about 1.7 million. While the true shortage is most likely somewhere inbetween, the bottom line is that the United States faces a textbook housing shortage that cannot be solved overnight. Worse, the Fed’s current policies are making the prospect of home ownership even more difficult.

Nobody wants to move and reset their loans at much higher rates.

Central bank measures designed to clamp down on inflation by making borrowing more expensive (which theoretically should drive down the costs of homes), are having the opposite effect. This is because homeowners, who locked in historically low mortgage rates before and during the pandemic, are now reluctant to sell their home.

Simply put, nobody wants to move and reset their loans at much higher rates. Would-be sellers are therefore sitting on the sidelines, which has unintentionally created an even greater shortage in supply. Meanwhile, potential buyers, who cannot afford higher mortgage rates, are incentivized to rent instead.

To end this stalemate, the Fed would need to start cutting interest rates, which it has stated is unlikely this year. But if inflation is being driven by the cost of housing, as demonstrated in the Consumer Price Index, more attempts to tame inflation via rate hikes suggests homeowners will only become more entrenched as supply dwindles further As the labor market continues to prove surprisingly resilient, homeowners, and by extension everyday consumers, don’t seem to mind waiting it out.

Read: Nouriel Roubini says a return to 2% inflation is ‘mission impossible’

Also: Most long-term investors can ignore the Federal Reserve’s latest move

The case for hard assets

Seasoned investors know that during times of rising interest rates, restrictive credit and prolonged inflation, more investments flow into “hard” asset classes such as real estate. This hedging strategy is used almost like an insurance policy by investors to preserve capital from the depreciating effects of inflation. And according to research, it works. For example, a Stanford University study found that residential real estate is historically an investment haven during inflationary periods. Even during the inflation of the 1970s, home prices increased relative to the size of the economy. This is because housing is typically tied to consumer prices and rises with inflation.

With housing assets so closely tied to inflation, as well as to the laws of supply and demand, investments in this hard asset class deserve due consideration. Strong economic growth, coupled with the one-two punch of resilient consumer spending and near record-low unemployment, is good news. It also means the Fed won’t be lowering rates soon. Housing will remain a key driver of inflation, and future rate-hikes will further entrench homeowners and push more would-be buyers into renting.

To achieve a return to 2% inflation, U.S. policymakers would be wise to work with state and local governments to incentivize development, which would drive down the greatest expense for most Americans. But even with decisive action, fixing the fundamental housing shortage that is responsible for sustaining stubbornly persistent inflation will be a longer process than most investors realize.

David Piscatelli focuses on research, economic analysis and strategy at Avenue One, a property technology service platform and marketplace for institutional owners, buyers and sellers of residential homes. Views of the writer do not necessarily reflect the views of Avenue One.

More: Meet the brave Americans buying and selling their homes, despite stubbornly high interest rates

Plus: 9 ways home buyers can stretch their dollars even though mortgage rates are high

-David Piscatelli

This content was created by MarketWatch, which is operated by Dow Jones & Co. MarketWatch is published independently from Dow Jones Newswires and The Wall Street Journal.

Dark Matter Technologies, formerly Black Knight Origination Technologies, is focused on mainly two things: the smooth transition to new owners, and lowering the cost to originate loans for lenders.

Executives from Dark Matter Technologies, under the Constellation Software umbrella, said that a down market is the best time to make investments in technology and prepare for the next cycle.

With lenders focused on bringing origination costs down in a tough origination environment, the firm saw up to a 300% year-over-year growth in new user numbers for the past couple of years.

“We actually do well in any kind of market,” Rich Gagliano, CEO of Dark Matter Technologies and former president of Black Knight, said in an interview with HousingWire on Friday.

“Now we’re in a down cycle, they need to do it with fewer people and they need to be more efficient to get the cost down. So it’s really the same story, just different markets,” Gagliano said.

Dark Matter Technologies, which completed the acquisition of Black Knight’s Empower and Optimal Blue last week, will be working towards a smooth transition over to Constellation Software with its 1,300-plus employees for the remainder of the year.

The company doesn’t plan to raise pricing for Empower and is focused on services and products that will drive down the cost of origination and employee borrower retention, executives said.

Gagliano, Sean Dugan, CRO of Dark Matter Technologies and Tom George, co-president of Romulus, part of the Perseus Group of Constellation Software, participated in the interview.

Read on to learn more about Dark Matter Technologies’ plan for mortgage.

This interview has been condensed and lightly edited for clarity.

Connie Kim: Constellation’s Perseus Group has a pretty big real estate portfolio. What were the reasons for buying Black Knight’s Empower and Optimal Blue? What opportunities did the firm see?

Tom George: The way Constellation operates is that we focus on acquiring vertical market software companies and portfolios of vertical market software companies with the intent to stay in these industries forever.

We started almost 20 years ago and Perseus in the homebuilding industry, we built a significant player in homebuilding software, that led us to an adjacency residential real estate where we bought over 20 companies. More recently, we started acquiring businesses in the mortgage tech space.

We plan to be in the mortgage tech space forever. And we plan to continue to acquire there.

Kim: What other mortgage tech companies has Constellation Software acquired?

George: We’ve acquired three other businesses in the mortgage space. We bought Mortgage BuilderSoftware from Altisource Portfolio Solutions in 2019. There have been two additional acquisitions – ReverseVision, which is a leader in the reverse mortgage LOS space, and then a document storage product called Back Support.

Kim: Are you expecting any layoffs during the transition? Will the same management from Black Knight’s Empower and Optimal Blue be in place?

Rich Gagliano: We’re not expecting any changes. [About] 1300 [employees] are going to move over with us and it’s business as usual.

Kim: It’s a tough mortgage origination market right now. How does the company expect to manage profit amid industry consolidation, bankruptcies and attrition?

Gagliano: We’ve seen a strong pipeline. Even though the markets are down, what we encourage and talk to clients about is when you’re slow, that’s the best time to make technology changes. Now is the time for that change, and get yourself ready for the next cycle.

We actually do well in any kind of market. But honestly, when the market is crazy, lenders are looking for efficiencies because they can’t find and hire enough staff. Now we’re in a down cycle, they need to do it with fewer people and they need to be more efficient to get the cost down. So it’s really the same story, just different markets.

Kim: I definitely hear a lot of mortgage tech companies saying ‘this is the time to invest, especially when the market is down.’ You mentioned a strong pipeline, are we talking about new clients?

Sean Dugan: We’ve had 200% to 300% growth year-over-year for the last couple of years. And we don’t see that backing up. Those are not financial metrics, that was just on the number of clients acquired. When we took the Empower LOS platform to the down- to mid-market clients and really focused on that, we saw the number of acquisitions per year grow in a really significant fashion.

Kim: Empower has an estimated market share of around 10-15% after ICE’s Encompass which takes up about 40 to 45% of market share. How does Dark Matter plan to compete against Encompass?

Gagliano: We believe strongly in technology. We’re generally in most of the deals when we know about them. We believe that the automation, and the technology and the solution that we bring, and the ecosystem that we have, is best in the industry and really helps these lenders drive cost out of the system.

We compete with multiple product providers out there, including Encompass. But we like where we are positioned and I think our clients like the innovations that we’ve brought over the past over years.

Kim: When I talk to lenders, they say when using a company’s LOS, using the same company’s add-on products makes it more cost-efficient and seamless. What are some of the add-on products the company has already developed or is seeking to develop to win over lenders?

Gagliano: Just over the past couple of years, we’ve added Ava, which is our artificial intelligence capability. Ava has added a couple of additional products over the past two years. We’ve added an underwriting efficiency product, we’ve added a post-close product that’s going into production – so fairly new products.

We’re going to continue to use the products that we have in our bundle today and sell those so no changes there. But we are incrementally adding new technology, new innovations, that are going to help drive that cost down.

Dugan: We’ve also delivered digital portals for each one of our business channels within Empower, which would include retail, wholesale, correspondent, home equity and assumptions. We also have business intelligence as a component, and then a vendor aggregation platform, which was by the name of Exchange. Those are some of the components that make up the Dark Matter-owned bundle of services within Empower.

Kim:I know Ava has some kind of AI aspect to it. Right now, a lot of mortgage tech companies are focusing on AI. How they’re going to utilize AI to be that middleman between the customer and the loan originator. I’m curious how Dark Matter is going to integrate AI and machine learning (ML) to the LOS and other products.

Dugan: Regardless of what the technology solution is, clients are looking for flexibility, configurability – things that they can configure to meet their particular requirements. They’re looking for a really significant return on their investment, and they’re looking to drive the cost of origination as well as employee and borrower retention.

Kim: One of the concerns about the ICE-Black Knight merger was the fear that ICE would raise prices on the LOS products.Will there be any pricing changes for Dark Matter Technologies?

Gagliano: We don’t have anything planned at this point. Our Constellation partners haven’t asked us to come in and raise prices. That’s not part of their strategy, their strategy is to acquire quality companies and run the businesses.

Kim: Who does Dark Matter Technologies consider as competitors right now?

Dugan: It’s any origination technology provider. There are a number of providers that are delivering services specific to underwriting capabilities, so we would compete with them. So I think it’s a host of providers and vendors across the ecosystem of this particular vertical that we compete with on a day-by-day basis.

Kim: What are your prospects for the remainder of the year for mortgage origination? What are some of the larger goals for Dark Matter Technologies?

Gagliano: Through the end of the year, we’re going to be transitioning to Constellation moving off Black Knight Technologies. We’ve added some corporate-level capabilities already. So we feel good about where we are and stay focused on that through the end of the year.