423 cases per 100,000 resident for state with highest identity theft

This post originally appeared on Finder.com.

As the world continues to cope with COVID-19, America is seeing cases of identity theft soar to record highs. Of the 3.2 million reports to the FTC’s Consumer Sentinel Network Data Book in 2019, 20% — or 650,572 — related to identity theft. And already in the first quarter of 2020, reports of fraud and identity theft are up 20.1% from the previous quarter.

The numbers could rise as more people continue to work from home and new reports of coronavirus-related fraud and scams come in.

Among these all-time-high cases, credit card fraud leads the charge.

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

Identity Theft vs. Account Takeover

Identity theft involves the unauthorized access of personal information, such as your name and Social Security number. Account takeover is when a fraudster accesses account information, such as credit card numbers, with the intent of committing fraud on existing accounts.

In 2019, victims reported $160.3 million worth of losses resulting from identity theft, according to the FBI. Credit card fraud made up the overwhelming majority of that $160.3 million.

This number represents only what was reported through the FBI’s Internet Crime Complaint Center. However, and doesn’t account for reports made directly to field agents.

Most Common Types of Identity Theft

Swiping the competition in 2019 was credit card fraud, which accounted for 41.78% of all identity theft reports to the FBI, followed by other identity theft, which includes fraud conducted via email and social media. The least common was government documents or benefit fraud at 3.54%.

Identity Theft and Credit Card Fraud by State

The dubious honor of state with the most identity theft reports goes to Georgia, with the Peach State logging 423 cases per 100,000 people in 2019–176 of those falling under the credit card fraud umbrella.

Florida came in just south of Georgia with 154 cases of credit card fraud per 100,000 people, followed by California and Texas.

The state with the fewest number of reports was South Dakota, with 47 reports of fraud per 100,000 people, followed by Vermont and Wyoming.

Several states in the middle of the country also came in at the middle of the pack, like Missouri and Colorado, with 41 and 45 reports of credit card fraud per capita, respectively.

Credit Card Fraud by Metro Area

Georgia maintains its top spot in individual metropolitan areas, accounting for three of the five areas with the most reports of identity theft per capita–Warner Robins, Atlanta-Sandy Springs-Roswell and Macon-Bibb County. A person convicted of financial transaction card fraud of more than $100.00 within a six-month period in Georgia can be charged with a felony. The ramifications can be a fine of up to $5,000.00 or a prison term of one and five years. On the flip side, Muncie, Indiana, logged the least number of reports at 37 per 100,000 people, followed by Glens Falls, New York, and Tullahoma-Manchester, Tennessee.

Top 10 metropolitan areas with highest identity theft per 100,000 residents – data

Rank

Metropolitan area

Reports per 100,000 residents

Number of reports

1

Warner Robins, GA Metropolitan Statistical Area

661

1,281

2

Atlanta-Sandy Springs-Roswell, GA Metropolitan Statistical Area

570

33,940

3

Miami-Fort Lauderdale-West Palm Beach, FL Metropolitan Statistical Area

556

34,458

4

Macon-Bibb County, GA Metropolitan Statistical Area

455

1,045

5

Memphis, TN-MS-AR Metropolitan Statistical Area

446

6,027

6

Columbus, GA-AL Metropolitan Statistical Area

433

1,322

7

Columbia, SC Metropolitan Statistical Area

411

3,420

8

Los Angeles-Long Beach-Anaheim, CA Metropolitan Statistical Area

410

54,553

9

Houston-The Woodlands-Sugar Land, TX Metropolitan Statistical Area

367

25,656

10

Dallas-Fort Worth-Arlington, TX Metropolitan Statistical Area

367

27,637

Top 10 metropolitan areas with lowest identity theft per 100,000 residents – data

Rank

Metropolitan area

Reports per 100,000 residents

Number of reports

1

Muncie, IN Metropolitan Statistical Area

32

37

2

Tullahoma-Manchester, TN Micropolitan Statistical Area

34

35

3

Glens Falls, NY Metropolitan Statistical Area

34

43

4

Lewiston-Auburn, ME Metropolitan Statistical Area

38

41

5

Appleton, WI Metropolitan Statistical Area

41

97

6

Owensboro, KY Metropolitan Statistical Area

41

49

7

Wenatchee, WA Metropolitan Statistical Area

42

50

8

Bismarck, ND Metropolitan Statistical Area

41

54

9

Ogdensburg-Massena, NY Micropolitan Statistical Area

43

46

10

Eau Claire, WI Metropolitan Statistical Area

43

72

Methodology

Finder sourced all data from the Consumer Sentinel Network Data Book 2019, released by the Federal Trade Commission in January 2020. The Consumer Sentinel Network Data Book uses reports in its Sentinel secure online database available to law enforcement only. These consumer reports are about fraud, identity theft and other consumer protection topics, with more than 3.2 million consumer reports filed in 2019.

The reports in Sentinel are sourced directly from:

People who call the FTC’s call center or report online

Reports filed with other federal, state, local and international law enforcement

Organizations like the Better Business Bureau and Publishers Clearing House

Having your Social Security number or card stolen isn’t exactly like getting your bank account information taken. You can easily get a new bank account number and have your bank freeze your accounts. On the other hand, it’s a bit more difficult to get a new Social Security number from the Social Security Administration.

What Is a Social Security Number?

The Social Security Administration loosely defines a Social Security number as a nine-digit number for identity-tracking purposes. It’s also used to track wages earned during someone’s lifetime for Social Security benefits.

As of 2011, the selection of this number is randomized. Whenever you start a new job or apply for government benefits, you need your Social Security number. It’s used to verify your identity and keep track of Social Security earnings.

You can locate your Social Security number on your Social Security card. If you can’t find your card, make sure you reach out to the Social Security Administration directly.

What Can You Do with a Social Security Number?

Since the government uses your social security number as a unique identifier, you can use it to do the following.

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

Apply for jobs

Open a bank account

Sign up for a credit card

Apply for a passport

File taxes

Enroll in health insurance

Get a driver’s license

How Social Security Number Theft Occurs: What Happens If Someone Gets Your Social Security Number?

There are a lot of ways someone can steal your identity or Social Security number. Thieves could swipe your Social Security number by exploiting data breaches, going through the trash for personal documents or using any number of other approaches. Thieves can then sell your identity or pretend to be you to open various accounts in your name, access medical care, file fraudulent tax returns or, at worst, commit crimes.

ExtraCredit’s Guard It feature offers dark web monitoring and proactive alerts if it discovers that your Social Security number or other personal information has been compromised or shared online. In addition to alerts, Guard It offers $1 million identity theft insurance to help you with costs associated with identity restoration, legal expenses, and lost wages. Sign up now!

What Can Someone Do with Your Social Security Number?

Once an identity thief has your Social Security number, they can commit all sorts of financial fraud, potentially leaving you on the hook for their misconduct. Social Security numbers are wrapped up in most aspects of Americans’ lives—employment, medical history, taxes, education and bank accounts, to name a few. Below is a list of just a few things someone can do with your SSN if they get their hands on it.

1. Open Financial Accounts

Your Social Security number is the most important piece of personal information a bank needs when extending you credit or opening an account. With that number, a thief can get credit cards or loans. And when it’s time to repay them, they won’t, which will damage your credit score. Those missed payments are tied to your Social Security number, so they’ll end up on your credit report and could impact your ability to apply for any type of loan or new account in the future.

Once you spot suspicious transactions, you can use your credit scores and credit reports to detect fraud and put an end to it. Unfortunately, it could take years for the fraudulent information to be removed from your credit report and, as a result, for your credit scores to recover.

Can Someone Access My Bank Account with My Social Security Number?

Thieves might have a difficult time accessing your bank account if they only knew your Social Security number. Most of the time, to either access an existing account or open up a new bank account, the bank would require additional forms of identification, such as your physical Social Security card, Real ID or passport.

Also, many banks have implemented additional security measures to prevent this, such as requiring security questions to access your bank account.

2. Get Medical Care

Someone using your Social Security number could also undergo medical treatment, effectively tainting your medical records. Inaccurate medical records can have deadly consequences. For example, imagine what could happen if you received treatment based on a false history listing the wrong blood type. Additionally, thieves can poach your health insurance coverage, which could leave you in a bind when you need it.

3. File a Fraudulent Tax Refund

Taxpayer identity theft continues to be a problem in the United States, although theIRS reported in 2018 that incidents were on the general decline, noting a 40% decrease in taxpayer reports of identity theft since 2016. However, in 2017, the IRS still received 242,000 reports of identity theft from taxpayers.

Identity thieves use stolen Social Security numbers to get a fraudulent refund, which then delays any refund the victim is rightfully owed.

So, the sooner you file your taxes, the more likely you’ll get your refund before an identity thief has an opportunity to take advantage of your stolen identity. You’ll know someone stole your identity if your return is rejected as a duplicate. Then, you get to start the process of resolving the fraud and, if necessary, getting the refund you deserve.

4. Commit Crimes

Getting your Social Security number might just be a fraction of the thief’s crimes. If the identity thief gets arrested for another crime and gives your Social Security number to law enforcement, you can become tangled in their criminal history. Their criminal record could prevent you from getting jobs or interfere with anything else that requires a criminal background check.

5. Steal Your Benefits

A thief could also use your Social Security number to file for unemployment or Social Security benefits, depleting those resources and preventing you from accessing that assistance when you need it later on.

How to Find Out If Your Social Security Number Has Been Stolen

Thieves can operate under your identity for years without discovery, and some of these crimes are very difficult to detect. One of the best things you can do is regularly check your credit report from Credit.com’s credit report card. Review your credit report thoroughly for unauthorized accounts or public records not related to you. These red flags could indicate clerical errors or identity theft. Either way, you want to watch out for it and act as soon as you see something suspicious.

If you sign up for an ExtraCredit account, our dark web monitoring feature will alert you of suspicious activity right away. When you get an alert, you’ll know it’s time to check your report and take preventative actions.

Sign Up Now

Privacy Policy

You can also go to IdentityTheft.gov, a website run by the Federal Trade Commission, or call its hotline at 877-ID-THEFT.

Crossing over the Ohio River from Kentucky right into the Queen City is breathtaking, as it’s known for its architecture and expansive skyline. After a decline in population since the 1950s, Cincinnati has been slowly but steadily growing since the aughts.

Today, the greater Cincinnati population clocks in just below 1.8 million, with a median age of 32 years old. The average income of Cincinnati residents is a little over $40,000. Cincinnati isn’t the cheapest for its cost of living, but it’s definitely not the most expensive, so many are able to live comfortably.

Cincinnati’s culture is booming, as the city works with local businesses to bring bold colors, flavors and brews into town. The fine arts scene is expansive and residents love festivals, so there’s always something to do. Cincinnati is home to the University of Cincinnati and Xavier University, along with pro sports teams like the Cincinnati Bengals, Cincinnati Reds, FC Cincinnati and the minor-league hockey team, Cincinnati Cyclones. Made up of 52 neighborhoods with individual cultures, events and perks, there truly is something always going on in the Queen City! Here are the best neighborhoods in Cincinnati.

Median 1-BR rent: $685

Median 2-BR rent: $915

Walk score: 67/100

Clifton is historic and eclectic. Located in the heart of Cincinnati, it’s pretty convenient. Just nine minutes away from Downtown, it’s near the University of Cincinnati and its medical centers. Thanks to its location, the residents are a good mix of doctors, young professionals, students and artists alike.

The homes are what you might expect from a downtown area. Lots of trees line the old streets and cottages and mansions are speckled throughout the residential areas. But there’s one thing that’s different about Clifton: The neighborhood isn’t too partial toward chain restaurants and shops. So, in the heart of the borough on Ludlow Avenue, all the dining and shopping is local.

Median 1-BR rent: $710

Median 2-BR rent: $950

Walk score: 42/100

College Hill used to have two colleges. Although both colleges have closed down, the area maintains the well-manicured streets typical of college campuses. That combined with the local revitalization efforts going on thanks to the College Hill Community Urban Redevelopment Corporation (CHCURC) and $43.1 million building plans split between rentals and retail spaces, College Hill has been building up to the cusp of a big boom for years.

Plus, the area has big breweries coming in to join existing pubs, bringing in more outside traffic and attention to the area.

Median 1-BR rent: $675

Median 2-BR rent: $860

Walk score: 44/100

Columbia Tusculum, sometimes referred to as the oldest neighborhood in Cincinnati (dating back to a month before Cincinnati debuted in 1788), is home to the Victorian “Painted Ladies,” a row of brightly painted architectural homes overlooking the Ohio River.

The area has plenty of pubs and breweries — arguably more than restaurants — along with plenty of gyms and fitness centers. Here, residents can enjoy the hilly, river-view 94-acre Alms Park. Easy to see why this is one of the best neighborhoods in Cincinnati.

Median 1-BR rent: $1,532

Median 2-BR rent: $2,381

Walk score: 52/100

Downtown Cincinnati is the place for residents constantly looking for something to do. It’s got a little bit of everything for everyone. The kids enjoy the splash pad in Washington Park during hot summer days, and everyone in the family loves a trip to the Play Library to rent out games and toys for family game nights. There are ample boutiques and shops downtown to score local finds, clothes, vintage goods, plants and greens, kitchen utensils and even an old-school hat shop.

The Cincinnati Museum Center at Union Terminal is home to several museums inside the 1933 Art Deco train station. Look for the Cincinnati History Museum, the Duke Energy Children’s Museum, the Museum of Natural History & Science and the Cincinnati Historical Society Library. Bonus: It’s home to the OMNIMAX Theatre, too. Throw in some amazing dining and bar options, plus a few outdoor shows and concerts, and Downtown really is fun for everyone.

Median 1-BR rent: N/A

Median 2-BR rent: N/A

Walk score: 52/100

East End is one of the oldest neighborhoods in Cincinnati. Back in the day, it was known for the sublime wooden ships built in the shipyard. Located right off the bend of the Ohio River, this area saw a mass exodus, like much of the rest of the city, as residents fled for the suburbs. But now, seeing its potential, developers have started returning to the riverside area, bringing with it new amenities and residencies, retailers and restaurants.

Median 1-BR rent: $1,150

Median 2-BR rent: $1,100

Walk score: 70/100

Since 1896, Hyde Park has sought to provide residents with a quiet place to call home. It’s done just that, while providing a well-balanced mix of nature-driven and architectural respite, too.

At the heart of this best neighborhood in Cincinnati is the Square, a well-manicured lawn perfect for sitting under the shady trees to enjoy the weather, rest after browsing local shops or eateries or meet up with friends.

Median 1-BR rent: $1,100

Median 2-BR rent: $1,725

Walk score: 66/100

If you dream of a chill neighborhood with a view overlooking the city and the Ohio River, Mount Adams is what you’ve been looking for! Located on a hilltop for peak visibility, Mount Adams is the perfect mix between San Francisco and a European village.

As one of the more upscale areas, doctors, lawyers and young professionals tend to call this place home. But don’t let that fool you. While it’s a quiet area throughout the week, these professionals and neighboring college students line the streets to enjoy the nightlife. With loads of different food options, residents’ palettes are rarely bored.

Close to Downtown, there’s also an outdoor amphitheater and Playhouse in the Park, where visitors can catch a play or performance throughout the year.

Median 1-BR rent: $1,254

Median 2-BR rent: N/A

Walk score: 54/100

Mount Lookout is a hilly, slightly ritzy neighborhood with incredible views. It’s home to the country’s oldest working telescope at the Cincinnati Observatory (National Historic Landmark) and has an incredible vineyard-turned-park that’s a fan-favorite among locals.

The area is also packed with great dining and café options, along with a beautiful town square lined with shops and businesses.

Median 1-BR rent: $1,081

Median 2-BR rent: $1,430

Walk score: 66/100

Northside is a quick 15-minute commute north of Downtown and has become quite the hipster hangout. With coffee houses, breweries and pubs to call home, it’s no wonder there’s such a Northside following, making this one of the best neighborhoods in Cincinnati.

The neighborhood is notably a safe space for LGBTQ+ members thanks to the presence of allies and supporters. With an annual 4th of July parade and other events, everyone can feel at home in Northside.

Median 1-BR rent: $955

Median 2-BR rent: $1,350

Walk score: 95/100

Located just north of Downtown, German immigrants tended to settle into this area back in the day. Having to cross the Miami and Erie Canal to get to work, residents started calling it “the Rhine,” like the river that runs through Germany. Thus, the neighborhood’s name, Over the Rhine, was born.

It’s hard to imagine now, but Over the Rhine was once seen as one of the most crime-infested and dangerous areas in the city. However, over the past decade, Cincinnati has been pouring money and investments into the area to revitalize it. These efforts have worked and many Cincinnatians say OTR is now one of the most interesting and eclectic neighborhoods the city has to offer.

Once the city funding came through, trendy bars, restaurants and shops started coming into the area. The new businesses and the community mainstays, like the 1878 Music Hall that hosts symphonies, operas and ballets, have made OTR a beloved Cincinnati staple.

Median 1-BR rent: $1,299

Median 2-BR rent: $1,510

Walk score: 52/100

Pendleton, located to the east of Over the Rhine, is often referred to as the arts district. Not only is the Pendleton Art Center located there, but many residents have livened up the area by bringing bright colors to their homes’ exteriors and businesses have followed suit, as there are ample murals all over local shops and restaurants.

Aside from art, there’s a great food scene, lots of things to keep kids busy and cafés and bars for the adults. The supportive neighborly vibes run deep in this bright, cheery area.

Median 1-BR rent: $849

Median 2-BR rent: $1,054

Walk score: 46/100

Pleasant Ridge is one of Cincinnati’s oldest neighborhoods, dating back to 1795. Now, it holds up its end of a storied past, as most of the businesses have been locally and independently owned for years and years, earning Cincinnati’s first Community Entertainment District title.

After a push to reinvigorate the area in the early 2000s, Pleasant Ridge has been basking in the rays of success and is still a trending neighborhood today. The charming town is colorful, too, as its business district has murals throughout.

Median 1-BR rent: $1,299

Median 2-BR rent: $1,510

Walk score: 52/100

Traditionally, South Fairmount has been an overlooked area. Most people wrote it off as hopeless. But with $100 million being funneled into the neighborhood, it’s quickly turning around.

Thanks to the Lick Run Greenway, a creek with wide sidewalks running alongside the water, South Fairmount is on the upswing. What was once dreary and gloomy, this area is getting a lot of attention from businesses and restaurants looking to capitalize on the new Greenway’s attention and it’s the perfect time to join in on the commotion.

Median 1-BR rent: $944

Median 2-BR rent: $1,124

Walk score: 67/100

Founded back in 1804, Walnut Hills is rich with history and culture. One house in the neighborhood was a stop for the Underground Railroad, thanks to its resident, author of “Uncle Tom’s Cabin,” Harriet Beecher Stowe. Her house is now a historic landmark and offers tours.

Just two miles from Downtown Cincinnati, Walnut Hills serves as an overflow area for top professionals and creatives alike. Home to Eden Park, Walnut Hills residents can enjoy a lovely scenic stroll scattered with fountains, sculptures and playgrounds, along with the Art Museum and Kohn Conservatory.

Median 1-BR rent: $736

Median 2-BR rent: $760

Walk score: 29/100

Westwood is the city’s biggest neighborhood and has been through quite a revolution over the past couple of years. It’s still in the process of its makeover and newer residents have been smart to jump aboard and join the team.

Residents tend to stick around and for good reason. They see real potential in the neighborhood and they’re willing to find out they were right. Westwood’s foodie scene has popped off. From pizza to delis to more adventurous options like Ethiopian food, just about anything you try in Westwood is something worth writing home about

Find the best Cincinnati neighborhood for you

If one of these neighborhoods sounds like your ideal future home, be sure to check out these apartments for rent in the best neighborhoods in Cincinnati.

The rent information included in this article is based on a median calculation of multifamily rental property inventory on Apartment Guide and Rent. as of November 2021 and is for illustrative purposes only. This information does not constitute a pricing guarantee or financial advice related to the rental market.

Identity theft is a major problem. According to the Federal Trade Commission (FTC), there were more than 650,000 victims of identity theft in 2019, making ID theft the most-reported type of FTC complaint. Chances are good that you will encounter identity theft in your lifetime. That was the case for at least 1 in 10 Americans ages 16 and older in 2016, according to the most recent data from the Bureau of Justice Statistics.

Protecting your identity and privacy should be a priority for you, and knowing what identity theft is can help you prepare. There are many different types of ID theft, which can make safeguarding your personal information even more important—and more difficult. Let’s look at some of the most common examples of identity theft and what you can do to manage the risks.

Defining Identity Theft

The term “identity theft” is used a lot, often interchangeably with “fraud.” Though many instances of identity theft are committed for fraudulent reasons, the two are slightly different. If you are a victim of identity theft, you want to catch it before it becomes fraud.

According to the National Center for Victims of Crime (NCVC), identity theft is “the knowing transfer or use, without lawful authority, of another person’s identity with the intent to commit, aid, or abet unlawful activity.” In simpler terms, ID theft is the act of stealing another person’s information, like through mail theft, phishing, card skimming, unsecure Wi-Fi or a data breach. Fraud is when a criminal illegally uses that information for their own gain.

The NCVC calls the latter “identity fraud,” which encompasses crimes like credit card fraud, medical fraud, and Social Security number theft. Identity fraud can be financially driven, but is also committed out of other motivations. Someone might try to steal your passport or driver’s license information to travel unnoticed by law enforcement, for example.

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

Whether an ID thief uses your credit card or medical insurance, the cost to you can be big. Javelin Research found that the 2018 out-of-pocket costs for victims of identity theft were $1.7 billion.

Different Types of Identity Fraud

As a popular saying goes, “Know your enemy.” Let’s take a closer look at identity fraud types and preventative measures you can take to prepare yourself and protect your finances.

1. Credit Cards

Credit card fraud is by far the most prevalent type of identity theft, according to FTC numbers.

You probably store your credit card information with different vendors or subscription services. If you used your card once at a retail store, they’ll still have your information on file. If a data breach occurs at one of those businesses, someone may gain access to your credit card number and begin to make fraudulent purchases.

While it may be easier to catch a fraudulent charge on a card you have, it could be harder to spot a new account in your name. In the meantime, hard inquiries and high credit utilization due to fraud could wreck your credit score.

What you can do: Requesting a chargeback might help you avoid paying for specific fraudulent transactions, but checking your credit report will show you if the problem is deeper. Sign up for ExtraCredit to keep an eye on your credit report and scores at the same time to make sure that fraudulent accounts aren’t being opened or used. You can also request your free credit report from each of the three credit reporting agencies once a year to keep close control over your identity and credit profile. If you notice anything fishy, request a freeze immediately and file a report with the FTC.

Note: Due to the COVID-19 coronavirus pandemic, you can currently review your credit reports from each of the three credit bureaus for free each week, through April 2022.

2. Loans and Leases

Somebody with your personal information might try to apply for a loan online. Fraudsters may then be able to get financing to buy a car or real estate. The FTC has also reported fraud instances related to student loans and payday loans.

Loan application fraud is a challenge to track, but the impact is someone racking up debt in your name. When creditors come calling, it won’t be the thief who has to answer the phone.

What you can do: As with credit card fraud, regularly check your credit reports to watch for red flags. If you spot something, immediately contact the responsible financial institution. You may also want to file a police report or contact the office of the attorney general for your state. If you are the victim of loan/lease fraud, consider using credit repair services to help you recover.

3. Phones and Utilities

Mobile takeover fraud is a complicated scheme, but it’s a growing problem. Basically, it involves a fraudster using your information to access your smartphone and then lock you out. In the meantime, they can use your apps, read saved documents, or scam others by impersonating you. They might also harvest your personal and financial information that you have saved. The same might happen for an electricity or water account: A criminal finds a way in and consumes services that are ultimately billed to you.

The common theme with identity theft here is that if someone has your info, they can do just about anything with it. This includes opening up utility accounts in your name, getting free electricity, gas, water, internet or cable.

What you can do: Maintain strong passwords for all the accounts you have. If you need to, use a password manager to help you keep track of all the complex log-in credentials. Never, ever make your passwords using personally identifiable information, like a pet, birthdate, or home street. Should something happen, immediately contact your service provider.

4. Tax Fraud

Come tax time, a refund is a happy surprise for some Americans. Others may get a nasty shock when they’ve learned someone has claimed their return before they even file their taxes. Tax fraud typically occurs when someone has stolen your Social Security number, which they can then manipulate to falsely file a return and claim your refund.

What you can do: Under no circumstances should you give your SSN to anybody but trusted entities like the government, your bank, or your credit card company. Be wary of scammers posing as the IRS who will call or email you demanding your SSN information. This is a surefire sign of fraud. You can also opt to file your taxes early, thereby eliminating the opportunity for thieves to file for you and claim your return.

The IRS recommends watching out for various scams. If you believe you’ve been a victim, file a report on IdentityTheft.gov, call the IRS at 1-800-908-4490, and complete and submit the identity theft Affidavit.

Taking the Next Steps to Protect Your Identity

Identity theft is a constant threat, so you’ll always need to be on your toes.

Guard It from ExtraCredit provides you with proactive alerts, dark web monitoring, account monitoring, and $1 million in ID theft insurance. Sign up today or read more articles about identity theft and fraud.

According to IBM’s annual Cost of a Data Breach report, the average cost of a data breach to an organization in 2021 was 4.24 million dollars. That’s the highest average figure in its 17-year history. Most of these breaches were the result of compromised user credentials (where an attacker is able to gain unauthorized access to an account) and are often more costly where remote working is involved.

cyber attack

These breaches aren’t just costly for large enterprises, though. Many small organizations fail to recover from a serious data breach (where the average cost is just under $700,000), with 60% of them going out of business within 6 months of an attack.

But of course, we can also fall victim to cyber attacks as individuals, and the cost to us can be significant, too. If you’ve been unlucky enough to have been a victim of a data breach, or (worse), identity theft, you’ll know that you can lose eye-watering and potentially crippling sums: this hacking victim lost over $13k in 2020.

But when we talk about the cost of a cyber attack to an individual, we’re not talking simply about financial losses.

How to Avoid a Cyber Attack

Psychologically, the after-effects of a cyber attack can be damaging. The feeling that you’ve been manipulated by a stranger (and your personal data has been ‘invaded’) can be deeply unsettling. It can lead to a serious loss of confidence, and make you increasingly wary of trusting others. It can cause embarrassment, too, as a victim of a hack can be made to feel as if it’s their fault.

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

In the most extreme cases (where a cyber attack has led to a significant loss of funds or even the loss of a job) the effect can be even more harmful, leading to stress, anxiety and even depression. Whatever the financial cost of an attack, the emotional cost is often far more significant in the long run.

Fortunately, there are a number of steps you can take to secure your data and ensure you’re aware of the threats you might face while online.

Check If Your data Is at Risk

Without knowing it, your data might have already been involved in a breach. A breach usually occurs when a hacker gains access to the database of a service or company which contains users’ private information, including (but not limited to) usernames, passwords, email addresses and, in the worst cases, bank account details. If you’ve been involved in a data breach, some of your personal information might have been made public without you realizing, which could put you at risk of identity theft.

But don’t panic. You can check if your email address or phone number has been exposed in a data breach by going to Have I Been Pwned. If any of your accounts may have been compromised, change those passwords immediately, and make sure you’re not reusing the same passwords across multiple accounts.

Use Strong Passwords

Speaking of passwords, nearly a quarter of Americans have admitted to using a password like “password” or “123456”. These should clearly be avoided, as they’re easily guessable and won’t take long for a hacker to crack. The longer and more complex a password is, the stronger it is. You can check the strength of your passwords at Security.org.

Using a “passphrase” (a series of unrelated words with spaces in between) is often more effective than using a simple combination of letters and numbers, as these can be harder to crack. This can help to protect your accounts from threats like brute-force attacks, in which attackers will submit vast numbers of possible passwords in an effort to guess correctly.

Protect Your Website(s)

This action may not apply to you, of course — but if you happen to run a website (for a small business, perhaps, or even just a hobby such as blogging) then your personal information is inextricably linked to it, and it can be a huge point of vulnerability. If someone gains access to it through a CMS exploit or a comparable weakness, they can learn your passwords, uncover private information, or even hold the site hostage in an effort to extort you.

Keeping extortion efforts at bay is largely a matter of investing in technical safeguards. Top managed hosting platforms are particularly good at keeping ahead of potential attackers, and some (e.g. Cloudways with its 2022-launched Cloudflare CDN integration) are investing in native features that make it all but impossible for run-of-the-mill hackers to gain access. Overall, though, the biggest thing you can do is refrain from storing any sensitive information on your website. Anything intended for public viewing inevitably makes a bad storage vault.

Beware of Suspicious Emails

One of the most common ways individuals fall victim to cyber crime is through phishing attacks, a type of ‘social engineering’ where an attacker sends a fraudulent email to an intended victim enticing them to click a suspicious link or hand over personal information. Phishing emails often appear as though they’re from a legitimate organization (like your bank, for example) but there are some classic signs to look out for.

Check the email domain (the bit after the @ symbol) to see if it looks legitimate. If it’s misspelled (or a public domain like gmail.com) it could be a scam. Next, check for poor spelling and grammar in the body of the email, as phishing attempts are often shoddily written. If you have the slightest suspicion that the email may not be legitimate, do not respond or click any links in the email. To ensure you’re aware of the telltale signs, IT Governance has produced a handy guide on the ways to detect a phishing email.

Update Your Software

Cyber threats are constantly evolving, with hackers developing newer, more sophisticated ways to gain access to our devices and our personal data. That’s why it’s so important that our operating systems and software programs are always updated to the latest available versions. These newer versions will fix previously discovered vulnerabilities and offer greater protection against emerging threats.

If you’re still using an outdated operating system, for example, it may contain weaknesses that can quite easily be exposed by an attacker, especially if those weaknesses are public knowledge. Use a tool like Soft4Boost to check for out-of-date and potentially vulnerable software, and update to the latest supported versions where necessary.

Secure Your Devices

It’s also important to protect our physical devices, as a lost or stolen device could present an easy opportunity for an attacker to gain access to your personal data. Ensure a password or PIN is always required to access the device (and don’t use anything easily guessable like 0000 or 1234). Many devices now enable facial recognition or fingerprint access, so enable these functions where possible. When you’re not using your device, make sure it’s locked.

Backing up your data is essential, too, so that it can be recovered in the event of a data breach. Most computers will include a backup facility, while mobile phone data can usually be backed up using cloud storage. Finally, beware of unsecured public Wi-Fi networks (where no password is required for access) as these are often prime targets for an attacker, and disable your Bluetooth function when you’re not using it.

Between 2000 and 2007, 5,306 people with criminal backgrounds became loan originators in Florida, according to an investigation conducted by the Miami Herald.

Of that group, 2,201 had committed a financial crime such as mortgage fraud, money laundering, or worse, but still managed to enter the business with little or no opposition.

This could be attributed to the fact that loan originators aren’t subject to the same licensing requirements as mortgage brokers, and as such, are significantly less regulated.

The Herald found that more than half of the 120,563 “mortgage professionals” registered in Florida joined the troubled industry this decade without being state-licensed.

But even mortgage brokers managed to find work in the industry as loan originators after having their licenses stripped or denied, with some knowingly circumventing the law.

One former broker who had previously committed $4 million in mortgage fraud in the state of Maryland wittingly applied as a loan originator, knowing this would be his only way back in.

Interestingly, that broker is now in charge of compliance at the firm he works for, though he rationalizes that he’s the best man for the job because of his checkered past.

The investigation, which utilized court documents, state industry reports, police reports, and internal e-mails, found that one in five loan originators at 30 mortgage lenders that employed 50 or more workers had a criminal background.

Sure, your child needs to be 15 before becoming an authorized user on a credit card account, 18 before signing a binding loan agreement, and 21 before applying for a credit card without a cosigner or some income to pay the bills. But long before that, they are “eligible” to have their identity stolen. In fact, according to a Child Identity Fraud Survey conducted by Javelin Strategy & Research, 1 in 40 households with children under age 18 had at least one child with personal information compromised by identity fraud in 2012.

Fortunately, there are ways to protect your kid from becoming a victim of child identity theft. For starters, parents can request credit reports for children under 14; children 14 and over can request a copy of their own credit reports. There are also credit monitoring services they can employ if they’re worried their kin’s personal information fell into the wrong hands. Here’s how to use credit monitoring to protect your child’s identity.

Why Is Your Child at Risk of Identity Theft?

Identity thieves are targeting children 18 and younger, swiping their Social Security numbers and applying for credit accounts in their names and piling up charges. Why? Because children aren’t in the habit of checking their credit. In fact, they often won’t even have a legitimate credit report unless something’s amiss. Remember, credit reports are a detailed account of your credit history, so until your child becomes an authorized user on your credit card account or gets a student loan, for example, they won’t leave a paper trail. In the meantime, thieves can wreak havoc by opening up bank accounts, credit lines, service contracts like a cellphone plan or more if they get their hands on a kid’s Social Security number.

A stranger who accesses a child’s Social Security Number, a dishonest family member or a friend of the family with access to a child’s personal records may commit this crime. Foster care children are particularly vulnerable to child identity theft because of the number of people who have access to their Social Security numbers.

How Can I Monitor My Kid’s Credit?

To protect your child, get in the habit of monitoring his or her credit reports. Reach out to each of the three major credit reporting agencies — Equifax, Experian and TransUnion — and request copies of your child’s credit records.

You will need to provide each credit reporting agency with your child’s name, address, date of birth, plus copies of your child’s birth certificate and Social Security card. You will also need to provide a copy of your driver’s license or other government-issued identification card and a utility bill showing you live at your current address.

Remember, children generally won’t have credit file unless you’ve added them to a credit card account in your name, so the mere fact that a bureau can generate a credit report for your child could be a sign that something’s amiss. Other signs that your child’s identity may have been stolen include:

Pre-approved credit card mail solicitations in your child’s name

Calls from a debt collector asking to speak to your child

An unexpected denial when you go to open up a bank account for your child

The arrival of cell phone or utility bills in your child’s name

If you discover your child is a victim of identity theft, be sure to report the fraud to the local authorities and the Federal Trade Commission.

What Is Credit Monitoring?

A credit monitoring service keeps tabs on your (or your child’s) credit report and notifies you of any changes that may occur. The major credit bureaus offer their own credit monitoring services, along with many of the major financial institutions and credit card issuers. Some services are even specifically designed to monitor a child’s identity.

Of course, prices for credit monitoring can vary, so it’s a good idea to shop around and compare and contrast them carefully. It’s also a good idea to thoroughly vet any company you’re considering. You can check out their record with online review sites, the Better Business Bureau, the Consumer Financial Protection Bureau or even your state Attorney General’s office.

How Can I Monitor My Own Credit for Identity Theft?

If you’re worried about your own identity being compromised, you should monitor your financial accounts regularly — daily if possible. The earlier you can spot unauthorized charges, the faster you can alert your financial institution and fix the problem.

Monitoring your credit regularly is also important. You should pull the free copies of your credit reports you can get once a year from each of the major credit reporting agencies at AnnualCreditReport.com. Signs of identity theft include mysterious addresses, unfamiliar credit inquiries and a major drop in your credit scores. To keep a closer eye on your credit, you can monitor two of your credit scores for free on Credit.com.

Jeanine Skowronski contributed to the reporting of this article.

This article has been updated. It was originally published August 21, 2014.

In the United States, it’s illegal to drive a car without car insurance. Depending on the state you’re driving in, the consequences of doing so can range from a fine to a misdemeanor on your record. So, if you’re planning on hitting the road anytime soon, be sure to purchase car insurance to avoid penalties.

In this article, we’ve researched the average cost of car insurance by state to give you a better idea of how much to budget.

Key findings:

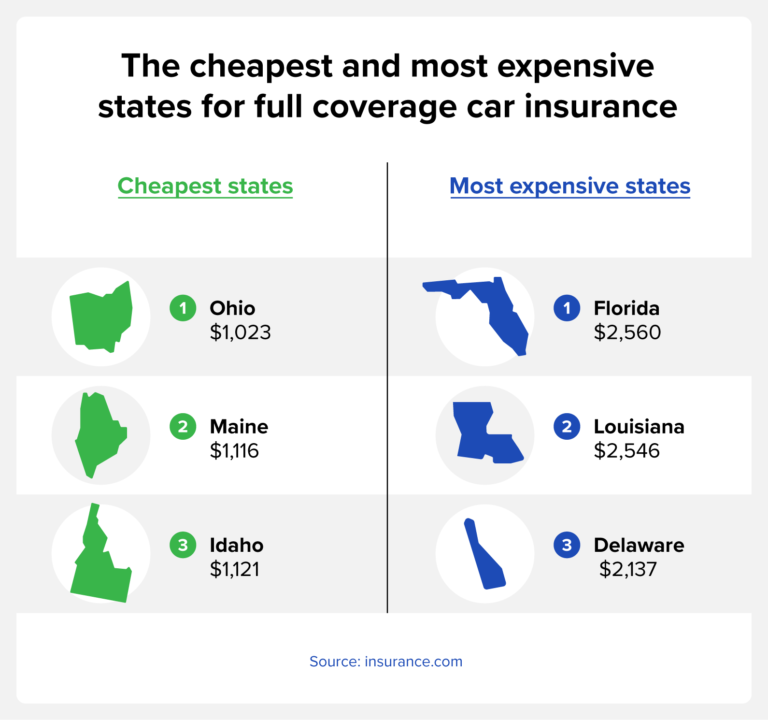

According to AAA, the national average cost of car insurance for a full-coverage policy was $1,588 in 2022.

On average, the cheapest states for full coverage car insurance are Ohio, Maine and Idaho, while the most expensive states are Florida, Louisiana and Michigan.

USAA, Geico and State Farm offer the cheapest minimum coverage plans, while USAA, Geico and Nationwide offer the cheapest full-coverage insurance.

The average cost of car insurance tends to decrease with age, but starts to rise again around age 70.

Individuals with high credit scores pay lower car insurance premiums on average compared to those with poor credit.

How much is car insurance?

According to AAA, the national average cost of car insurance for a full-coverage policy was $1,588 in 2022. This figure is based on an under 65 years old driver who lives in the city or suburbs, has over six years of driving experience, and has not been involved in any accidents.

Average cost of car insurance by state

When calculating the cost of car insurance, the state you live in plays a role in how much you can expect to pay. This is because factors like population density, climate, road conditions and crime rate in your area can play a part in the likelihood that you’ll file a claim.

According to insurance.com, the cheapest states for car insurance if you’re looking for minimum coverage are Iowa, South Dakota and Wyoming costing an average of $263, $267, and $293, respectively. Meanwhile, the cheapest states for full coverage auto insurance are Ohio ($1,023), Maine ($1,116), and Idaho ($1,121).

The most expensive states for car insurance in terms of minimum coverage are New Jersey, Florida, and New York where drivers pay an average of $989, $908 and $875, respectively. For full coverage insurance, drivers in Florida ($2,560), Louisiana ($2,546), and Delaware ($2,137) pay the most in the country on average.

State

Minimum coverage

Full coverage

AK

$336

$1,359

AL

$420

$1,542

AR

$422

$1,597

AZ

$494

$1,617

CA

$582

$2,115

CO

$467

$1,940

CT

$773

$1,750

DE

$821

$2,137

FL

$908

$2,560

GA

$567

$1,647

HI

$389

$1,306

IA

$263

$1,321

ID

$326

$1,121

IL

$484

$1,578

IN

$384

$1,256

KS

$389

$1,594

KY

$717

$2,105

LA

$726

$2,546

MA

$523

$1,538

MD

$607

$1,640

ME

$330

$1,116

MI

$711

$2,133

MN

$479

$1,493

MO

$525

$2,104

MS

$434

$1,606

MT

$389

$1,692

NC

$396

$1,368

ND

$340

$1,419

NE

$350

$2,018

NH

$411

$1,307

NJ

$989

$1,901

NM

$376

$1,505

NV

$683

$2,023

NY

$875

$2,020

OH

$308

$1,023

OK

$352

$1,797

OR

$551

$1,244

PA

$398

$1,445

RI

$648

$1,845

SC

$628

$1,894

SD

$267

$1,581

TN

$368

$1,373

TX

$520

$1,875

UT

$526

$1,469

VA

$469

$1,321

VT

$306

$1,158

WA

$505

$1,371

WI

$375

$1,499

WV

$474

$1,610

WY

$293

$1,736

Average cost of insurance by company

Another factor that’s going to influence how much you can expect to pay for car insurance is the specific company you purchase your plan through.

According to U.S. News & World Report, USAA, Geico and State Farm offer the cheapest minimum coverage plans, while USAA, Geico, and Nationwide offer the least-expensive full-coverage insurance.

Farmers, Progressive, and Nationwide offer the most expensive minimum coverage rates while Allstate, Farmers, and Progressive offer the most expensive full coverage plans.

Insurance company

Minimum coverage

Full coverage

Allstate

$1,961

$2,138

American Family

$1,327

$1,388

Farmers

$1,782

$2,059

Geico

$1,064

$1,238

Nationwide

$1,347

$1,338

Progressive

$1,440

$1,650

State Farm

$1,191

$1,348

Travelers

$1,290

$1,448

USAA

$948

$1,056

Average cost of insurance by age

According to CarInsurance.com, the cost of both minimum and full coverage car insurance tends to decrease with age, as seen in the chart below. However, there is an uptick around age 70 where rates start to go back up.

Age

Minimum coverage

Full coverage

20

$1,109

$3,532

30

$539

$1,785

40

$520

$1,682

50

$496

$1,581

60

$482

$1,511

70

$554

$1,661

Average cost of insurance for young drivers

Young drivers are the most expensive age group to insure. Although there are a few exceptions, insurance rates decrease with age among young drivers.

Age

Minimum coverage

Full coverage

16

$2,402

$7,203

17

$1,971

$5,924

18

$1,706

$5,242

19

$1,234

$3,874

20

$1,109

$3,532

21

$884

$2,864

22

$794

$2,593

23

$736

$2,415

24

$690

$2,267

Average cost of insurance by credit score

According to the Insurance Information Institute, your credit score is a good indicator of how many insurance claims you’ll file. As a result, insurance companies use credit scores to determine risk, and those with a good credit score pay cheaper premiums. The Zebra found that individuals with poor credit pay approximately 114% more than those with great credit.

Credit score

Average annual rate

Very poor (300-579)

$2,887

Average (580-669)

$2,296

Good (670-739)

$1,912

Excellent (740-799)

$1,606

Exceptional (800-850)

$1,350

What factors affect your car insurance rate?

As you can see from the above charts, the cost of car insurance varies by the following factors:

Age: Typically, young drivers under the age of 25 and senior drivers over the age of 65 are charged more for car insurance.

State of residence: Since the minimum coverage required varies by state, your location is one of the factors that will influence the price.

ZIP code: In addition to your state of residence, your ZIP code will also play a role in the cost of insurance since your vehicle is more likely to be damaged in certain areas, such as ZIP codes with high crime rates. Typically, the cost of car insurance will be greater in cities than in rural areas.

Marital status: Statistically, married drivers are less risky than single drivers resulting in a lower insurance cost.

Gender: Based on risk, male teenage drivers tend to have the highest cost of car insurance of any demographic.

Credit history: Those with a low credit score tend to pay higher premiums than individuals with good credit.

Driving record: Since car insurance premiums are based on risk, individuals with a good driving record can expect to pay lower premiums, while those with a poor driving record may experience increased rates.

Car make and model: You may pay less if you drive a vehicle that insurance companies deem safe. On the other hand, you’re likely to pay more if you drive a small sports car since they pose a higher risk.

Mileage: Higher annual mileage increases the risk you’ll get into an accident and will likely raise your premiums.

High-risk violations: Driving under the influence andat-fault accidents are examples of violations that may result in you being considered a high-risk driver.

What’s the difference between full and minimum coverage?

Minimum coverage car insurance — liability coverage — is required in most states and is used if you’re at fault in an accident. This coverage will pay for damages and injuries of the other party when you’re responsible for the incident.

On the other hand, full coverage insurance, or collision coverage, includes liability coverage plus damage caused to your own vehicle. Keep in mind that lenders often require you to obtain full coverage insurance before you get an auto loan.

FAQ

Below, we’ve answered some common questions regarding the cost of auto insurance.

Can my driving record affect my car insurance rate?

Your driving record is one of the factors that affects your car insurance rate. As a result, those with traffic violations or accidents on their record can expect to pay higher premiums.

Does your car insurance cost go down after you pay off your car?

Your care insurance cost doesn’t typically go down after your pay off your car. However, you do have the option to decrease the amount of coverage on your vehicle once it’s paid off.

Which car insurance company is the cheapest?

As mentioned above, insurance companies that offer the cheapest plans include Geico, Auto-Owners, USAA and Erie.

Does car insurance decrease annually?

For young drivers in particular, car insurance rates decrease each year you renew your policy without filing a claim. You can expect to see the biggest drop in price at age 25.

The average cost of car insurance varies by factors including state, age, insurance company and credit score. Some factors, such as your age, are beyond your control, but other factors, such as your credit score, can be improved.

Check your credit score for free today to see if it’s a reason your car insurance is high.

Cyber-attacks are on the rise as hackers and criminals learn about and adapt to methods put in place by government agencies to prevent scams. The FBI’s Internet Crime Complaint Center (IC3) reported monetary losses totaling more than $1.4 billion in 2017. [1]

While anyone, regardless of age, can be a target of common money scams, many hackers specifically target seniors. Nearly 17% of reported cyber crimes in 2017 came from victims over the age of 60. And with losses of over $342 million, seniors are losing more money to scams than any other age group. [1] Considering the average age of retirement in the U.S. is 60, this trends is a serious threat to the financial security of many Americans as they enter retirement.

With an empty nest and retirement on the horizon, your senior years should be the time to pursue your passions—not get scammed out of your hard-earned savings.

This guide covers the basics of recognizing and preventing common online money scams, plus provides tips to help seniors navigate the online world safely.

Table of Contents:

Why Scammers Target Seniors

Pew Research shows that seniors are adopting technology, such as the Internet and smartphones, more than ever before. [2] If you’re among the technology adopters, you know how great technology is for connecting with your children and grandchildren who live far away and with friends you haven’t seen in years.

Con artists and scammers exploit seniors online believing that they aren’t Internet-savvy, despite many proving otherwise. Here are a few of the reasons seniors are a frequent target of scams online:

You generally have larger savings accounts and valuable assets.

You’re perceived as more trusting and polite.

You may not recognize and report the scam right away.

As you age, cognitive function and physical ability declines.

How to Recognize a Money Scam

As online scammers get increasingly sophisticated, certain types of fraud can be hard to spot even for the most adept Internet user. To keep from falling victim to scammers’ tactics, make yourself aware of common warning signs and stay vigilant. A gut feeling is always a good place to start. For example, if something feels too good to be true, it probably is. Also, if a request from someone you know feels out of character, trust your instincts and do your research before taking action.

An easy way to know if something is a likely con is to use the three U’s for identifying money scams.

Unexpected: If you receive an email from someone you trust making an unexpected or unusual request for money or personal information, contact them personally to confirm.

Urgent: If the tone of the message is threatening or asks you to act immediately, take time to think it over or tell a friend before acting. If you’re still unsure, check the IC3’s Alert Archive to see if there have been other incidents of the same scam.

Unsecure: Make sure the address bar reads “https://” and not “http://” when entering personal or financial information online. If a URL begins with “https://” that tells you the site is secure and protects information that’s transmitted. If you provide sensitive information to an unsecure site, it can easily be stolen.

Top 10 Online Scams That Affect Seniors

Scammers see senior citizens as easy victims, but you can prove them wrong by educating yourself on some of their common schemes. They often use things like healthcare, retirement savings and online dating to lure unsuspecting seniors into giving over their personal information. Here are 10 of the most common online schemes that target seniors.

1. Medicare Scams

If you’re 65 or older, you might rely on Medicare for your health coverage. Scammers know this and whenever Medicare sends out new cards or makes changes to its policies, they capitalize on opportunities to steal personal information. This can be done over the phone or by email. The scammer claims to be a Medicare representative and insists there’s a fee associated with getting you a new card or that your card has been compromised—neither of which is true.

According to Medicare.gov, “Medicare, or someone representing Medicare, will never contact you for your Medicare Number or other personal information unless you’ve given them permission in advance.”

How to protect yourself: Don’t respond to the email and mark it as junk or spam. If you need to speak with Medicare, call them directly at 1-800-MEDICARE (1-800-633-4227).

2. Health Insurance Scams

In order to make a profit, criminals may try to offer you health insurance plans that have little to no real value. In some cases, they may be selling discount cards or limited-benefit plans, but rarely explain how limited the coverage really is.

How to protect yourself: Never purchase insurance on the spot. Do your research on the company and thoroughly read the details of the coverage offered.

2. Counterfeit Medications

This scam is especially dangerous because it can cost you not only your money but your health. Prescription drugs aren’t cheap, and most seniors are dependent on a medication or two to maintain their health. Scammers exploit this by offering fake prescription medications for purchase online at a low cost. The number of counterfeit medication scams under investigation by the FDA is up four times since the 1990s. [3]

How to protect yourself: Always go through licensed medical professionals to get any prescriptions and pick up your medications at a local pharmacy. If you enjoy the convenience of ordering online, many reputable pharmacies allow you to refill your prescription online or have your medications delivered.

3. Phishing

Scammers often capitalize on your trust in people and institutions by posing as them in emails, on calls or in text messages. For example, the Social Security Scam is a form of phishing where scammers pose as government officials who need your social security information. Once they’ve gained your trust, they use that to gather personal, sensitive information like your Social Security number, bank/credit card information and/or passwords.

How to protect yourself: Always check the sender’s email address or phone number before clicking any links in emails or messages that request personal information.

4. Dating and Romance Scams

Online dating can be great for people of all ages—seniors included. But it’s important to practice the same kind of cautions online as you do in real-world dating. Online dating scams are one of the biggest and most costly scams, and scammers can break your heart and bank account if you’re not careful. It’s a red flag if someone builds a rapport with you only to turn around and ask for money. Even if the request seems heartfelt, like wanting to come see you, it could still be a play solely for money.

How to protect yourself: Take things slow, do your research and never send money to someone you don’t know personally. Even if you’ve met them, run the other way if they ask for money after you’ve known them only for a little while.

5. Investment Scams

In these cons, scammers take advantage of your need to build or maintain retirement savings. A lot of seniors are concerned about making their money last, which makes them vulnerable to ads or requests that promise high-profit, no-risk investments.

How to protect yourself: Stop and think, “Is this too good to be true?” Never accept an offer on the spot. If you’re not sure, talk it over with a trusted friend or check the IC3’s Alert Archive along with other online sources, such as the Scams and Frauds page on USA.gov.

6. Homeowner Scams

Seniors are at a point in life where they’re more likely to own their homes. While some may want to stay right where they are, others have grand dreams of moving to a new location—maybe somewhere warmer. In this scenario scammers work to identify the value of your property and then offer you a reassessment—for a fee, of course.

How to protect yourself: If you want to move, only work with a reputable realtor or go the for sale by owner route.

7. Sweepstakes and Lottery Scams

These scams use a surprise factor to trick you into thinking you need to click something to “claim a prize.” It can come as an email, a web pop up or even within a web page you’re reading.

How to protect yourself: If you receive an email that claims you’re a winner, it’s almost guaranteed to be a scam. On the off chance that you actually signed up for a sweepstakes, check your email inbox to see if you have a confirmation of your signup from the same email address. Better, yet, pick up the phone and call the company before you click on a link in an email or on a website.

8. Fake Charities

Seniors may feel more compelled to donate to those in need or contribute to disaster aid, but unfortunately fake charities often try and get donations after a natural disaster.

How to protect yourself: Do your research. Call a number to speak with someone from that charity or search the charity name and a phrase like “scam” or “fraud” in Google. You can also use the organizations listed by the FTC to research reputable charities.

9. Malware Scams

Using antivirus software is a great way to protect yourself from fraud. Unfortunately, scammers often pose as antivirus providers and instead install malware on your computer. These advertisements are often pop ups or web page ads.

How to protect yourself: Make sure anything you download to your computer is from a reputable source and never give anyone you don’t trust remote access to your computer.

10. Threats and Extortion

These types of scams utilize fear to get the desired outcome. Typically the scammer tells you that something terrible is going to happen if you don’t give them money or personal information.

How to protect yourself: Never act impulsively. Consider whether the scenario seems realistic. If you’re unsure or scared, talk to a friend. If the caller acts like a relative, hang up and call them back to ensure it is, in fact, your relative and not a stranger pretending to be your relative.

How to Protect Yourself Online

It’s good to know the basics about scams and the accompanying warning signs, but there are steps you can take to further protect your computer and online identity from fraud including. settings, tools and government resources.

Keep your firewall turned on. A firewall monitors incoming and outgoing network traffic to prevent unauthorized access to and from a private network. It protects your computer from hackers attempting to crash it or gain sensitive information.

Keep your computer’s operating system up-to-date. Make sure your computer software is up-to-date. You can usually subscribe to automatic updates online. If you keep your system updated, your computer will continue running smoothly and you’re sure to have the latest fixes for any security holes.

Turn on two-factor authentication. Two-factor authentication requires both a password and an additional piece of information to access your account. The second piece of information is typically a message sent to your phone or a code generated by an app or token.

Look out for unsecure networks and websites. If you get a warning message saying “Unsecure Wi-Fi Detected,” don’t visit any banking websites or store any passwords while on that network.Also, most browsers will warn you when you visit an unsecure site. The feature should already be enabled on most computers, but if not, make sure you enable this setting.

Install or update antivirus software. Antivirus software prevents malicious software programs from installing on your computer. Malware programs allow others to see your computer activity. Be wary of any ads on the Internet for these types of software as they are often not real solutions and instead are fraudulent.

Use a password manager. A password manager, like LastPass or Dashlane, lets you have a unique, strong password for every secure website—in other words, not your grandchild’s birth date. You won’t have to remember them all, because the password manager stores and encrypts your passwords for your protection.

Check your credit often. Major changes toyour credit can indicate potential fraud. Consider signing up for a free credit score and checking it every few weeks as a way to watch for changes.

Find Information About Active Scams

What To Do If You’re the Victim of a Scam

The best thing to do if you suspect you’ve been the victim of a scam is to report it. IC3 chief Donna Gregory says, “We want to encourage everyone who suspects they have been victimized by online fraudsters to report it to us.” IC3 receives over 800 complaints a day on average, so don’t let embarrassment keep you from reporting something.1 Reporting a scam helps law enforcement investigate similar scams and take action to bring the scammers to justice.

Steps to Take After Fraud

To report a scam, file a claim online at www.ic3.gov. You’ll be asked to provide complete information about the crime as well as any additional relevant information.

Once you’ve reported the scam to authorities, you also want to take action against any other loss. IC3 recommends that victims take actions, such as contacting banks, credit card companies and/or the credit bureaus to block accounts, freeze accounts, dispute charges or attempt to recover lost funds.

Keep a close watch on your credit reports and consider using credit monitoring tools.

In February 2018, the Justice Department made a coordinated sweep of elder fraud cases that resulted in several initiatives to reduce the number of annual cases. [4] This included building local, state and federal capacity to fight elder abuse, supporting research to improve elder abuse policy and practice, and helping older victims and their families.

Each year the number of Internet crimes increases and scammers become more sophisticated, but spreading knowledge and awareness is one of the best ways to combat the issue. Arming yourself with a basic understanding of the dangers online can help you protect yoursel f from fraud.

Additional Resources

Sources:

1 Federal Trade Commission Latest Internet Crime Report Released

2 Pew Research Center Tech Adoption Climbs Among Older Adults

3 National Council on Aging Top 10 Financial Scams Targeting Seniors

4 United States Department of Justice Justice Department Coordinates Nationwide Elder Fraud Sweep of More Than 250 Defendants

Is Kansas City in Kansas, or is it in Missouri? It’s kind of both. Both are individually incorporated cities, but together they make up the greater Kansas City metropolitan area.

Long ago, in the 1830s, KCMO got started as a trade outpost to fit hunters with furs and traps. Now, that’s morphed into manufacturing and it dabbles in tech, transportation and healthcare. For visitors, it’s better known for LEGOLAND, the National World War I Museum, tons of art galleries and museums, the Airline History Museum, too many fountains to count and, of course, Kansas City barbecue.

The concentration of barbecue alone is enough to focus on, as Kansas City has the most barbecue restaurants per capita than anywhere else in the U.S. Characterized by burnt ends with extra flavor, and a thicker-than-most tomato-based sweet barbecue sauce smothered on the smoked meat (not on the side!), Kansas City barbecue has made a name for itself for obvious reasons.

Residents cheer on several pro sports teams, like the Kansas City Chiefs, the Kansas City Royals and the Kansas City Current.

The Kansas City metro area has 2.34 million residents. The median age is 35 years old and the median household earns about $55,000. With a whopping 240 neighborhoods making up the city, there’s plenty of variety and subcultures to add to the spice of life for Kansas City residents. Here are 15 of the up-and-coming best neighborhoods in Kansas City for 2022.

Median 1-BR rent: $1,135

Median 2-BR rent: $1,410

Walk score: 48/100

Constructed in the 1920s, Brookside has that beloved historical feeling. But throw in a couple of community staples, like festivals, parades and fairs, and you’ve got a local color you can’t beat.

Kansas City residents claim Brookside is “quintessential Kansas City.” From ghost tours, toy shops, local makers and retailers, art galleries and museums — not to mention all the great food, pubs and cafes — Brookside has a little bit of everything for everyone and offers a whole lot of fun.

Walk score: 83/100

The Country Club Plaza can often feel otherworldly to the rest of Kansas City, thanks to its Spanish-inspired architecture. It’s a pretty popular area since it’s known as the shopping capital of the city, spanning 15 blocks of retail. From designer to local, there’s a shop for everyone.

If visitors don’t come for the shopping, they probably came for the food because it’s just that good. And if they didn’t come for either, they definitely came for one of the two art museums in the neighborhood. If nothing else, maybe they’re there to count all the fountains, of which there are many. It’s no wonder this is one of the best neighborhoods in Kansas City.

Median 1-BR rent: $1,420

Median 2-BR rent: $1,695

Walk score: 85/100

Like many neighborhoods in metropolitan cities across the U.S., Crossroads was once a warehouse district. When the manufacturers left, the area was vacant until someone had a vision. The area became what it’s known for today, the Crossroads Arts District.

Each month on the first Friday, this neighborhood puts on an art crawl spanning 20 blocks with 70 retailers involved. The neighborhood is also home to the Kauffman Center for the Performing Arts, which stages theatrical performances, music and dance recitals.

The area has plenty of breweries and bars to make a whole evening out of the arts, along with great restaurants, too. Hipsters and young professionals flock to the area for its creative vibes and good times.

Median 1-BR rent: $1,735

Median 2-BR rent: $2,420

Walk score: 69/100

Home to LEGOLAND, the city’s aquarium, the Money Museum and a covered ice rink in the winter, there are tons of things to do in Crown Center for families and singles.

Just south of Downtown, this neighborhood also has the Crown Center Mall where there’s plenty of shopping opportunities and local retailers, too. Obviously, the area has plenty of great dining options to boot.

Median 1-BR rent: $1,135

Median 2-BR rent: $1,410

Walk score: 48/100

As one of America’s leading best downtowns, Downtown Kansas City has a lot to offer to keep itself in the ranks. Home to a year-round, Saturday-and-Sunday City Market, come rain or shine, residents have every excuse to go downtown on the regular.

Downtown also hosts about 130 free events each year and boasts dining options from across the world.

Median 1-BR rent: N/A

Median 2-BR rent: N/A

Walk score: 48/100

East Bottoms was a booming neighborhood closer to its founding back around 1800. It was well known for its J. Rieger & Co. Distillery, producer of over 100 different products, founded in 1887.

The distillery was eventually forced to shut down during the prohibition, but in 2014, the original owner’s great-great-great-grandson got the distillery up and running again. In addition to its specialty spirits you can taste all over the country in craft cocktails, this distillery opened up its own tasting and dining rooms which revitalized the area and urged other pubs and breweries to join the mix, making it one of the best neighborhoods in Kansas City.

This is a great area in Kansas City to meet up with friends to have a great time.

Median 1-BR rent: N/A

Median 2-BR rent: N/A

Walk score: 54/100

Two of KCMO’s most notable, must-see museums are in the 18th & Vine District: The Negro Leagues Baseball Museum and the American Jazz Museum. Throw in some barbecue (there are plenty of options in the area), and you have three of Kansas City’s biggest passions: Baseball, jazz and barbecue.

Since it’s such a storied area, residents and visitors can enjoy live entertainment and music regularly.