The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

If you have a car loan, making your payments on time and in full each month should help build your credit over time.

Having good credit can save you a significant amount of money in interest fees on a car loan. Ideally, you’ll want a credit score of 660 or higher to get a favorable interest rate, but did you know that having a car loan may also help improve your credit?

We’re going to explain how car loans can affect your credit report and how they may be able to help raise your credit. You’ll also learn how to find the best car loans to help you save money on your new vehicle.

Is a car loan good for your credit?

Applying for a car loan can hurt your credit temporarily, but your credit can recover and even improve in time. When you apply for a car loan, the lender needs to run a hard inquiry to check your credit history, which is what can lower your score. The decrease can also happen if you refinance your car, but in both cases, the impact is usually minimal.

The good news is that a car loan can help you boost your credit in the long term. One of the primary factors that determines your credit score is your payment history. If you take out a car loan and make your monthly payments on time, these payments are reported to the major credit bureaus. If you’re wondering how fast a car loan will raise your credit, the answer is that it can take a few months to start seeing results.

One way to ensure you make your monthly payments on time is to set up automatic payments. After months of making these on-time payments, the consistent positive payments should far outweigh the temporary decrease from the hard inquiry.

How auto loans affect your credit report

Your credit report has a lot of data, and it can seem a bit overwhelming. Before going over how auto loans affect your credit report, it’s helpful to know the five factors affecting your credit score.

Each factor is weighted differently, so they’ll have a different level of impact on your credit. The following percentages are based on the FICO® scoring model, which is the most commonly used model.

Payment history (35 percent)

Your payment history is the most heavily weighted factor of your credit score at 35 percent. Late and missed payments can result in derogatory marks, which have a negative impact on your credit. On the other hand, when you make your car payments on time, the credit bureaus report them, which can help your credit.

Credit utilization (30 percent)

Credit utilization is how much you owe compared to your overall credit limit. Your utilization is often in the form of a percentage or a ratio. Ideally, you want to keep your credit utilization under 30 percent. For example, if you have a $1,000 credit limit and only owe $200, that’s a 20 percent utilization rate. Your car loan won’t affect your credit utilization.

Credit age (15 percent)

Your credit report also shows the length of your credit history, and this helps lenders see how much experience you have with credit. When you acquire an auto loan, you’re typically paying off the vehicle for years, and this is factored into the average age of all of your credit accounts. By having a long history of making your payments on time, it can help your credit.

New credit (10 percent)

Earlier, we mentioned that the application process can temporarily lower your credit due to hard inquiries. If someone is regularly applying for new lines of credit, it may be a red flag to lenders. But remember, financing a car can also help you build your credit over time, eventually outweighing the negative impact of the hard credit check.

Credit mix (10 percent)

The two primary types of credit are installment credit and revolving credit. Credit cards are considered revolving credit because when you make your payments, you can access that money again. With a line of installment credit, you owe a set amount each pay cycle, and car loans fall into this category. When you have a variety of types of credit, it helps improve your credit mix.

On your credit report, you will find two categories that will provide information about your car loan:

Types of accounts: In this category, you will find your credit mix, and under the installment accounts category, you will find your car loan as well as other installment loans. Other examples of installment loans include mortgage loans and student loans.

Current status: You will also see the status of your auto loan. If you make your payments on time, it may say that the account is “current,” or it will say “paid as agreed.” Basically, this showcases your payment history on a specific account. If you’re 30 days late on your payments, this can hurt your credit, and the lender may even repossess your vehicle.

It’s also possible that a reporting error inaccurately shows a missed or late payment, and this can unfairly lower your score. Should this happen, you can file a dispute to address it.

How to find the best car loan

It’s common for people to shop around for the best deal on a car, but it can also be helpful to shop around for the best car loan. When taking out a loan, one of the primary considerations should be the interest rate. The overall interest rate of the car can vastly change the price.

For example, let’s say you put $1,000 down on a $20,000 vehicle with a loan term of five years and a 5 percent interest rate. The total interest on the vehicle would be $2,513, making the vehicle cost $21,513.

Using that same example, you would pay far more at an 8 percent interest rate. At an 8 percent interest rate, the total interest would be $4,115, which is around $1,500 more than the 5 percent interest rate.

You may be able to find better interest rates by going through your current bank or other lenders. Good credit is another key factor in finding a good interest rate.

Repair your credit before shopping for a car

Your credit can have a major impact on how much interest you pay for your vehicle. According to recent data, the average car loan interest rate for a new car for people with a credit score of 781 or higher is 5.07 percent. If your credit score is under 661, the average interest rate for a new car is 8.99 percent.

If you need help with your credit prior to getting a car, reach out to Lexington Law Firm. There may be errors on your credit report hurting your credit, and we have a team who will work to address these errors on your behalf. Sign up today to get a free credit assessment.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.

Reviewed By

Brittany Sifontes

Attorney

Prior to joining Lexington, Brittany practiced a mix of criminal law and family law.

Brittany began her legal career at the Maricopa County Public Defender’s Office, and then moved into private practice. Brittany represented clients with charges ranging from drug sales, to sexual related offenses, to homicides. Brittany appeared in several hundred criminal court hearings, including felony and misdemeanor trials, evidentiary hearings, and pretrial hearings. In addition to criminal cases, Brittany also represented persons and families in a variety of family court matters including dissolution of marriage, legal separation, child support, paternity, parenting time, legal decision-making (formerly “custody”), spousal maintenance, modifications and enforcement of existing orders, relocation, and orders of protection. As a result, Brittany has extensive courtroom experience. Brittany attended the University of Colorado at Boulder for her undergraduate degree and attended Arizona Summit Law School for her law degree. At Arizona Summit Law school, Brittany graduated Summa Cum Laude and ranked 11th in her graduating class.

The holidays are fast approaching, and the time to book holiday flights is even closer. But as travelers securing end-of-year trip reservations begin to reach for their wallets, another payment option is on the table.

A growing list of airlines offers travelers the chance to buy expensive flights now and get an interest-free loan to pay off the purchase in smaller monthly installments. These “buy now, pay later” financing options are available through third-party providers, like Affirm, Uplift, Klarna or PayPal Credit, directly on the airline’s checkout page.

Almost 1 in 5 holiday travelers (about 18%) plan to use a buy now, pay later service to pay for their holiday travel expenses, according to a NerdWallet survey conducted by The Harris Poll in September among over 2,000 U.S. adults. For the purposes of the survey, holiday travelers were defined as people who plan to spend money on flights/hotels for 2023 holiday travel.

Buy now, pay later is a way for holiday travelers to finance the $1,947 they plan to spend on holiday flights and hotels this season, according to NerdWallet’s findings. This is an increase of more than 23% from last year’s holiday travel spending ($1,582 on average). That’s despite a decline in airfare prices since last year, according to the consumer price index data released in October.

The question is whether using these programs is a good idea.

The rise of buy now, pay later services

The agency also noted the dollar value of loans doled out by those companies rose from $2 billion before the pandemic to a whopping $24.2 billion in 2021. Buy now, pay later usage included everything from beauty products to groceries, gas, pet care and travel.

Experts say the jury is still out on whether buy now, pay later programs benefit consumers. A big reason for the uncertainty is the rapid rise of these financing options.

“There’s a lot we still don’t know about consumer uses of these,” says Michael Collins, an expert in consumer and personal finance at the University of Wisconsin.

According to the CFPB, these loans, paid down monthly by consumers, range in size from $50 to $1,000.

Benefits of using buy now, pay later for travel

There are some benefits to using buy now, pay later for travel.

For one, buy now, pay later can keep travelers from immediately paying for a sizable airfare expense when holiday gifts and other year-end costs can quickly add up.

Plus, there’s a convenience factor to making a buy now, pay later purchase, Collins says.

“You can instantly finance it even if you don’t have cash in the bank and you don’t want to use your credit card,” he says, noting its appeal to those who might not have stellar credit or who don’t have a credit card.

Unlike a credit card, though, many of these programs don’t charge interest if you make the minimum monthly payment.

Drawbacks of using buy now, pay later for travel

Buy now, pay later programs do carry risks, especially if you miss your monthly payment.

In the CFPB’s report on Buy Now, Pay Later trends, the explosion in popularity of these financing options last year is discussed, and users are cautioned about the risks of data harvesting, inconsistent consumer protections, minimal dispute resolution options and the potential to accumulate debt and late fees.

“We will be working to ensure that borrowers have similar protections, regardless of whether they use a credit card or a Buy Now, Pay Later loan,” the bureau’s director, Rohit Chopra, said in the report.

The agency also found that 10.5% of buy now, pay later borrowers were charged at least one late fee in 2021.

Use credit responsibly

Ultimately, Collins says, consumers considering taking advantage of one of these programs — or incurring any other debt, for that matter, should consider the basic principles of responsible credit.

“You should be your own best judge of what you can handle,” he says. “You have to take out these loans with the intent to pay them back in a timely way, or else they will get very expensive very fast.”

Survey Method:

The 2023 survey was conducted online within the United States by The Harris Poll on behalf of NerdWallet from September 5-7, 2023, among 2,057 U.S. adults ages 18 and older, among whom 967 plan to spend money on flights/hotel stays this upcoming holiday season. The sampling precision of Harris online polls is measured by using a Bayesian credible interval. For this study, the sample data is accurate to within +/- 2.7 percentage points using a 95% confidence level. For complete survey methodology, including weighting variables and subgroup sample sizes, please contact [email protected].

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are our picks for the best travel credit cards of 2023, including those best for:

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

A 680 credit score is in the “good” range based on the most common scoring model, FICO®. With a 680 credit score, you can get approved for credit cards as well as personal, auto, and home loans.

Having a low credit score not only makes it difficult to secure lines of credit and loans, but it can also cost you quite a bit of money. Low credit scores mean you need to put down larger deposits on rental homes and services, and you also get charged higher interest rates.

According to the recent credit score statistics, the national credit score average is 716. While a score in the 700s is good, having a 680 credit score may be all you need to improve your financial well-being.

Today, you’ll learn what a 680 credit score means and how to achieve one. Most importantly, you will learn how to maintain a good score and continue improving your credit with helpful tips.

What Does a 680 Credit Score Mean?

The meaning of a 680 credit score depends on what credit scoring model is being used. FICO® has the most commonly used scoring model, and it ranges from 300 to 850. If you have a 680 FICO score, you have a “good” credit score. According to the FICO scoring model, the following are the typical ranges:

Exceptional: 800–850

Very Good: 740–799

Good: 670–739

Fair: 580–669

Poor: 300–579

Your credit score is a simple way for financial institutions to gauge risk. Lower credit scores are often a red flag and signal to lenders that a person may not pay back a loan. Typically, low credit scores are due to late payments, a short credit history, and overspending. In some cases, low credit scores are due to errors on your credit report that you may need to dispute.

Can You Get a Credit Card With a 680 Credit Score?

Whether or not you get approval for a credit card depends on the type of card and the company, but in many cases, a 680 credit score should get you approved for a credit card. You can get a credit card with bad credit, but these cards often come with high fees and interest rates. Having a 680 credit score can get you a good credit card with typical fees, and it may even have additional perks like cashback rewards.

Note that your credit score is only one aspect of the credit approval process. When you apply for a credit card, lenders look at your credit report. The report shows additional details like other debts you have as well as your payment history. When you apply, there will also be questions about your current income and expenses.

Can You Get a Car With a 680 Credit Score?

Much like with credit cards, a car loan approval may vary by lender, but a 680 is often good enough to qualify for a car loan. When it comes to car loans, in addition to the price, one of the most important factors is the car loan interest rate. Paying off a car loan takes years, which means an interest rate can potentially add thousands of dollars to the loan.

According to recent data, the average car loan interest rate with a 680 credit score for new cars is 5.82% and 7.83% for a used car. By improving your credit score, you can get average interest rates as low as 4.75% for a new car or 5.99% for a used car. It may also be beneficial to use a loan calculator to see how much a loan will cost you over time.

Can You Get a Mortgage With a 680 Credit Score?

It shouldn’t be a problem to qualify for a mortgage loan with a 680 credit score. Like other loans, there’s much more that goes into the mortgage than just your credit score. When applying for a home loan, the mortgage lender takes a much more detailed look into your finances. They’ll want to see your debt-to-income ratio, employment status, assets, bank statements, and more.

It’s also helpful to remember that a major aspect of purchasing a home is the down payment. Knowing how much you should put down on a house can help you plan for the future and discover how much you need to buy a home in addition to having a good credit score.

Can You Get a Personal Loan With a 680 Credit Score?

Yes, you should be able to get a personal loan from many lenders with a 680 credit score. Some lenders may require a higher score in the 700s, and these lenders may also give you a better interest rate. Having a 680 credit score may get you a loan with a higher interest rate, so it’s always helpful to improve your credit score before taking out a personal loan.

5 Tips to Improve Your 680 Credit Score

As you now know, a 680 credit score is good, but improving your credit score to 740 or higher can help you get even lower interest rates and more lines of credit. Here, we go over five ways you can improve your credit.

Make your payments on time: Your payment history makes up 35% of your FICO score, so making all of your payments on time can help boost your credit score.

Keep your spending low: After payment history, credit utilization is the most significant factor in determining your credit score. This is how much you owe compared to your total credit limit. It’s recommended to keep this ratio below 30%.

Don’t close old credit cards: It’s common for people to close credit cards they don’t use, but it’s better to keep them open. In addition to helping with your credit age, keeping a credit card open can help you keep your credit utilization ratio low, which is good for your score.

Check your score regularly: Checking your credit score regularly can motivate you to stay on the right track as well as let you know if you need to make changes. There are services to get your credit score for free as well.

Dispute any errors: Sometimes, there are errors on your credit report, and you can dispute them on your own with the credit bureaus or work with a credit professional.

Not only are these good habits to help improve your credit, but they’ll help you maintain a high score as well.

Get Help With Your Credit Score

If you have a 680 credit score, you’re off to a good start, but improving your credit score can help save you money and get approved for better loans. For those who have bad credit, striving for a 680 credit score is a good goal to have. To see where you stand with your credit, sign up for Credit.com’s free credit report card for a full picture of your credit situation.

Editorial Note: Blueprint may earn a commission from affiliate partner links featured here on our site. This commission does not influence our editors’ opinions or evaluations. Please view our full advertiser disclosure policy.

Getty Images

Mortgage rates are trending high across the board. Here are today’s average mortgage rates:

30-year fixed: 8.30%

15-year fixed: 7.35%

30-year jumbo: 8.09%

*Data accurate as of October 23, 2023, the latest data available.

30-year fixed mortgage rates

Today’s 30-year fixed mortgage rate is 8.30% which is higher than last week’s 8.06%, according to data from Curinos. This is a steep increase from last month’s 7.85%. Last year around the same time, 30-year fixed rates were 6.30%, which makes today’s rate much higher than it was a year ago.

At the current 30-year fixed rate, you’ll pay about $756 each month for every $100,000 you borrow — up from about $742 last week.

Ready to buy? Compare the best mortgage lenders

15-year fixed mortgage rates

Today’s 15-year fixed mortgage rate is 7.35%, slightly higher than last week’s 7.21%. This is an increase from last month’s 6.95%. Last year around the same time, 15-year fixed rates were 5.51%, which makes today’s rate much higher than it was a year ago.

At the current 15-year fixed rate, you’ll pay about $920 each month for every $100,000 you borrow, up from about $914 last week.

30-year jumbo mortgage rates

Today’s 30-year jumbo mortgage rate is 8.09% which is higher than last week’s 7.93%. This is an increase from last month’s 7.58%. Last year around the same time, 30-year jumbo rates were 5.81%, which makes today’s rate more than 2 percentage points higher than it was a year ago.

At the current 30-year jumbo rate, you’ll pay around $744 each month for every $100,000 you borrow, up from about $733 last week.

Methodology

To determine average mortgage rates, Curinos uses a standardized set of parameters. For conventional mortgages, the calculations are based on an owner-occupied, one-unit property with a loan amount of $350,000. For jumbo mortgages, the loan amount is $750,000. These calculations assume an 80% loan-to-value ratio, a credit score of 740 or higher and a 60-day lock period.

Frequently asked questions (FAQs)

Mortgage rates are determined by a variety of factors, including the overall economy, inflation and the actions of the Federal Reserve. Mortgage lenders then set their loan rates based on these economic elements.

The rate you’re offered on a mortgage will also depend not only on the lender but also on your credit score, income, debt-to-income (DTI) ratio and other parts of your financial profile.

If you opt for a rate lock, you can typically do so for 30 to 60 days, depending on the lender. In some cases, you might be able to lock in your rate for up to 120 days.

Keep in mind that while some lenders allow you to lock in a mortgage rate for free, you’ll likely have to pay a fee for a longer lock period. This fee generally ranges from 0.25% to 0.5% of your loan amount. You could also be charged a fee if you want to extend the lock period — usually 0.375% of the loan amount.

There are several strategies that could help you qualify for the best mortgage rate, such as:

Checking your credit: When you apply for a mortgage, the lender will review your credit to determine your creditworthiness as well as your interest rate. In general, the higher your credit score, the lower your rate will be. So before you apply, it’s a good idea to check your credit to see where you stand. If you find any errors in your credit report, dispute them with the appropriate credit bureau to potentially boost your score.

Comparing lenders: Taking the time to shop around and compare your options from as many lenders as possible can help you find the best deal. In addition to rates, make sure to also consider each lender’s terms, fees and eligibility requirements.

Improving your credit score: If you have less-than-perfect credit and can wait to apply for a mortgage, it could be worth working to improve your credit beforehand to qualify for better rates in the future. Some possible ways to boost your credit include paying all of your bills on time and aiming to keep your credit utilization (the amount of credit you’ve used compared to your credit limits) on credit cards and lines of credit at 30% or less.

Reducing debt: Paying down debt could help lower your DTI ratio, which is how much you owe in monthly debt payments compared to your income. Having a lower DTI ratio can make you look like less of a risk in the eyes of a lender, which can result in a lower rate.

Choosing a shorter repayment term: Lenders typically offer lower rates to borrowers who opt for shorter terms. For example, you’ll likely get a lower rate on a 15-year mortgage compared to a 30-year loan.

Blueprint is an independent publisher and comparison service, not an investment advisor. The information provided is for educational purposes only and we encourage you to seek personalized advice from qualified professionals regarding specific financial decisions. Past performance is not indicative of future results.

Blueprint has an advertiser disclosure policy. The opinions, analyses, reviews or recommendations expressed in this article are those of the Blueprint editorial staff alone. Blueprint adheres to strict editorial integrity standards. The information is accurate as of the publish date, but always check the provider’s website for the most current information.

Jamie Young is Lead Editor of loans and mortgages at USA TODAY Blueprint. She has been writing and editing professionally for 12 years. Previously, she worked for Forbes Advisor, Credible, LendingTree, Student Loan Hero, and GOBankingRates. Her work has also appeared on some of the best-known media outlets including Yahoo, Fox Business, Time, CBS News, AOL, MSN, and more. Jamie is passionate about finance, technology, and the Oxford comma. In her free time, she likes to game, play with her two crazy cats (Detective Snoop and his girl Friday), and try to keep up with her ever-growing plant collection.

Megan Horner is editorial director at USA TODAY Blueprint. She has over 10 years of experience in online publishing, mostly focused on credit cards and banking. Previously, she was the head of publishing at Finder.com where she led the team to publish personal finance content on credit cards, banking, loans, mortgages and more. Prior to that, she was an editor at Credit Karma. Megan has been featured in CreditCards.com, American Banker, Lifehacker and news broadcasts across the country. She has a bachelor’s degree in English and editing.

Ashley is a USA TODAY Blueprint loans and mortgages deputy editor who has worked in the online finance space since 2017. She’s passionate about creating helpful content that makes complicated financial topics easy to understand. She has previously worked at Forbes Advisor, Credible, LendingTree and and Student Loan Hero. Her work has appeared on Fox Business and Yahoo. Ashley is also an artist and massive horror fan who had her short story “The Box” produced by the award-winning NoSleep Podcast. In her free time, you can find her drawing, scaring herself with spooky stories, playing video games and chasing her black cat Salem.

The average credit score for those aged 18 to 25 is 679. This average credit score is the lowest on our list because this age group is just beginning to build their credit scores Lower earnings, student loans, and higher credit card usage can impact credit scores.

Average Credit Score by 30

The average credit score for those aged 26 to 41 is 687. This age group is building their credit along with higher salaries. This age group may be paying off education loans or large investments like cars and homes.

Average Credit Score by 40 – 50

The average credit score for those aged 42 to 57 is 706. This age group is investing more in retirement finances and working to reduce debt and large investments like mortgages.

Average Credit Score by 60 and Higher

The average credit score for those aged 58 to 76 is 742. For those older than 77, the average credit score is 760. These groups are either stepping into retirement or enjoying the rewards of retirement life. These groups may be working off a debt to have minimal debt going into retirement or avoiding accumulating debt altogether. These groups have the highest credit scores due to their ability to pay off debts and build credit scores over the years.

Average Credit Score by State

As of September 2022, Minnesota had the highest average credit score at 742, whereas Mississippi had the lowest average credit score at 680. Overall, the southern states produced lower credit scores than the northwestern and midwestern states.

How to Build Credit at 18

Building credit sooner than later will provide you with more loan options and lower interest rates. There are many ways to start building credit and improving your credit.

1. Improve Your Financial Literacy

Before building credit, it’s important to learn about credit management and personal finance. Spend some time researching how credit works and how to make the best financial decisions for your circumstances. Take a look at Credit.com’s extensive tips and guides for further help and information.

2. Get a Starter Credit Card

Your first option to start building your credit is with a secured credit card. A secured credit card is much easier to apply for. However, it requires a security deposit. This security deposit acts as collateral in case you can’t make your credit card payments. Be sure the credit card company you choose reports to the three major credit reporting agencies.

From here, begin using your starter credit to build your credit and submit your monthly payments on time.

3. Become an Authorized User

If you have a family member or friend with a credit card and a good credit score, you can ask them to add you as an authorized user. Just double-check that their credit card company reports authorized user information to the credit bureaus, or this won’t work.

As an authorized user, you don’t need to access the account owner’s credit card or even use the account to reap its credit benefits. When you’re an authorized user, the on-time credit payments made by the account owner are automatically reflected on your credit report. Becoming an authorized user is a great way to quickly start building your credit. However, if the account owner doesn’t submit payments on time, this can negatively impact you.

4. Submit Payments on Time

This may be the most important way to build credit, as payment history makes up 35% of your FICO® credit score. It’s crucial to make credit card payments on time, so it’s best to only take on debt if you can pay it off by the time it’s due. If your payment is 30 days past due, your credit card company can report it, which would likely hurt your credit score.

5. Check Your Credit Report

Monitor your credit report regularly. Although uncommon, payment inaccuracies and misinformation found on your credit report can drop your credit score. You are legally entitled to one free credit report each year from the three major credit reporting agencies. If you see an error on your credit report, you can dispute it with the agency.

FAQ

Below are frequently asked questions about your credit score and how to improve it.

What Is the Average U.S. Credit Score?

In September 2022, the average U.S. credit score was 714, which is unchanged from 2021.

When Does Your Credit Score Build the Most?

Your credit score builds the most when you’re actively contributing to improving your credit score. Establishing initial credit in a good range (around 670 – 700 or higher) can take at least six months, but building your credit up to a good credit score can take several years. Practicing good credit management, like submitting payments on time, will make the biggest difference in how fast your credit builds up.

How Do You Find Your Credit Score?

It’s important to check your credit score regularly. There are a few ways to get your credit score, such as:

Look at your credit card or loan statement: Most credit card, loan, and bank institutions provide credit scores for customers. You may be able to find an up-to-date credit score on your most recent bank statement.

Use a credit score service: Use a free or subscription-based credit score service to see your credit score. Some credit scoring sites provide a free trial for new users to test out their site, during which you can check your credit score.

Apply for a free credit report: The three major credit reporting agencies must legally provide you with a free credit report every year upon request. You may request your credit report from Experian®, Equifax®, or TransUnion®.

You should also check your credit report regularly to verify your credit report is free of any inaccuracies or misinformation.

Review Your Next Credit Report With Credit.com

Now that you know the average credit score by 18 (679), it’s time to start building your credit. Setting up financial goals and practicing good credit management will help you build credit.

Curious about your financial health? Get graded with our free credit report card to see what is affecting your credit score.

This program can reduce the time needed to save for a down payment and provide another option for those who are otherwise ready to take on a mortgage payment

SEATTLE, Aug. 24, 2023 /PRNewswire/ — Zillow Home Loans announced its 1% Down Payment program to allow eligible home buyers to pay as little as 1% down on their next home purchase. This program is initially being offered on properties located in Arizona, with plans to expand to additional markets. With the 1% Down Payment program, borrowers who qualify can now save just 1% to cover their portion of the down payment and Zillow Home Loans will contribute an additional 2% at closing. The 1% Down Payment program can reduce the time eligible home buyers need to save and open homeownership to those who are otherwise ready to take on a mortgage.

Most markets are in the midst of an affordability crisis, and saving for a down payment remains one of the biggest barriers for many potential home buyers. This is especially true for first-time buyers, who are often paying high rents. Typical asking rent nationwide is $2,062, or 3.6% higher than one year ago and up 31% since the start of the pandemic. (The typical rent in the U.S. in February 2020 was $1,597.) The combination of record-breaking home price appreciation and rising interest rates means a majority of first-time buyers (64%) are putting down less than 20%, and one-quarter of first-time buyers are putting down 5% or less.

Zillow Home Loans’ 1% Down Payment program lowers the down payment barrier and increases access to the housing market for eligible borrowers. An analysis by Zillow Home Loans’ shows that by reducing the down payment burden to 1% of the purchase price, a home buyer looking to purchase a $275,000 home in Phoenix, Arizona, who makes 80% of their area’s median income and saves 5% of their income would need only 11 months to save for the down payment. By comparison, the same buyer who needed to save 3% of the purchase price would require two and half years (31 months) to save that amount.

“For those who can afford higher rent payments but have been held back by the upfront costs associated with homeownership, down payment assistance can help to lower the barrier to entry and make the dream of owning a home a reality,” said Zillow Home Loans’ senior macroeconomist Orphe Divounguy. “The rapid rise in rents and home values means many renters who are already paying high monthly housing costs may not have enough saved up for a large down payment, and these types of programs are welcome innovations in lowering the potential barriers to homeownership for those who qualify.”

Home buyers looking to purchase in the next year should take steps to research and prepare for getting a mortgage as they start on their home-financing journey. Among those steps:

Understand your credit profile: Credit scores are key to getting approved for a mortgage, but for many home buyers, understanding credit is complex.

Improve your credit score: Once buyers familiarize themselves with what’s in their credit report, they can take steps to pay down existing debts, pay bills on time, and review their credit report and dispute possible errors.

Avoid closing accounts: Don’t close an account to remove it from your report. Those accounts aren’t automatically removed and will continue to show up on your report.

Hold off on financing large new purchases: Wait to make purchases that need to be financed, such as a car, until after you close on a home. This type of purchase will impact your debt-to-income ratio, which will negatively affect the amount of home loan you qualify for.

Determine what affordability looks like: Once buyers have a good understanding of their credit report and their credit score is at least 620 (generally the lowest score accepted by mortgage lenders) it’s time to understand how much home they can afford. Use Zillow’s mortgage affordability calculator to customize payment details.

Zillow Home Loans’ 1% Down Payment program is currently available to eligible borrowers in Arizona, with plans to expand. Through the 1% Down Payment program, Zillow Home Loans will pay 2% of the down payment for eligible borrowers. The 2% is paid through closing and not as a payment to the borrower. Interested applicants should call 1-833-372-1449 to speak with a Zillow Home Loans representative to learn more about the program and determine if it’s the right fit for their circumstances.

About Zillow Group Zillow Group, Inc. (NASDAQ: Z and ZG) is reimagining real estate to make it easier to unlock life’s next chapter. As the most visited real estate website in the United States, Zillow® and its affiliates offer customers an on-demand experience for selling, buying, renting, or financing with transparency and ease.

Zillow Group’s affiliates and subsidiaries include Zillow®; Zillow Premier Agent®; Zillow Home Loans™; Trulia®; Out East®; StreetEasy®; HotPads®; and ShowingTime+™, which houses ShowingTime®, Bridge Interactive®, and dotloop®. Zillow Home Loans, LLC is an Equal Housing Lender, NMLS #10287 (www.nmlsconsumeraccess.org).

SOURCE Zillow Home Loans

For further information: Media contact: Jessica Drum, Zillow Home Loans, [email protected]

Shopping for a mortgage has never been easier, thanks to the array of online options. Brick and mortar lenders may still be a viable option, but you may find that an online lender has even more to offer.

Furthermore, exploring online mortgage lenders allows you to compare mortgage rates. You can also receive customized mortgage loan offers in your inbox in minutes. Even better, you’ll have direct access to a loan officer in case you have questions.

Who are the top online mortgage lenders for 2023?

If you’re in the market for a new home and ready to start your search for online lenders, here are some reputable options to choose from.

Best Online Mortgage Lenders of 2023

loanDepot

loanDepot is an online lender, but don’t think that means they are lacking in customer service. They provide over 150 loan stores across the country for customers that prefer in-person service.

The lender is a suitable option for anyone who wants to take out a mortgage with the assistance of a loan officer.

loanDepot offers various mortgage products, including fixed and adjustable-rate mortgages. You can also apply for jumbo loans, VA loans, and FHA loans. You’ll need a minimum credit score of 620 to qualify for a mortgage.

loanDepot ranks high in customer satisfaction and most buyers seem to have a good experience working with them. However, they do charge higher fees than other mortgage lenders.

Quicken Loans

This online lender takes the hassle out of securing a mortgage by letting you complete the entire process online.

You’ll need to provide a few key details about your finances using this form to get started. A Home Loan Expert will review your application and contact you to discuss loan options.

And no need to worry about getting overwhelmed. Quicken Loans offers online tools to help you understand loan options and the home buying process. Plus, the customer service is excellent; a live representative is always standing by.

You can also upload all your documents and monitor the status of your application directly from the portal. This means you never have to pick up the phone if you don’t want to.

And when you’re ready to close, you have the option to schedule the closing when it’s convenient for you.

Better.com

If you’re looking for an online mortgage lender, you should check out Better.com. The company uses technology to simplify the lending process for its customers. Better.com promises a fast and transparent mortgage experience.

The lender is willing to work with all different kinds of buyers, including individuals who are self-employed or have unique job situations.

At least a third of its mortgages are taken out by first-time homebuyers, and over 70% of all buyers pay a down payment that is less than 20%.

Better.com mortgages don’t come with any hidden fees; there are no application or origination fees. To get started, you can visit the company’s website and get pre-approved in just a few minutes.

Rocket Mortgage by Quicken Loans

Rocket Mortgage is a division of Quicken Loans. Their key competitive advantage is the asset importer tool, which takes the guesswork out of determining whether you’re approved.

Instead of uploading documents, importing them from the information provider guarantees the accuracy of the numbers and allows you to receive loan offers using real-time interest rates in a matter of minutes.

And once you’ve selected a loan that works for you or created a custom option, you’ll be able to close in record time. Plus, Rocket Mortgage customer service experts are standing by to assist with questions you may have every step of the way.

NBKC Bank

NBKC Bank is not as widely known as many of the other lenders on this list. But that doesn’t mean you should rule them out as a potential mortgage lender.

There are several features that make the Kansas City-based lender a great option. The bank promises fast home closings and provides exceptional customer service.

NBKC Bank focuses mostly on online mortgages and offers its customers competitive interest rates. It does have several brick-and-mortar locations but focuses mostly on processing online mortgages.

You’ll need a minimum credit score of 620 to qualify for a mortgage, so this is a suitable option for borrowers with fair credit. NBKC Bank offers various mortgage products, as well as personal accounts. This makes them a great option for anyone looking for a full-service lender.

Guaranteed Rate

You can apply for a mortgage in a matter of minutes from the homepage of this digital mortgage provider’s site.

All you have to do is answer a few questions about your desired home, credit, and finances to receive a comprehensive listing of loan types and interest rates you may qualify for.

Guaranteed Rate has plenty of no-down-payment loan options like VA loans and USDA loans. They also offer a knowledge center to help you understand mortgages and how the process works.

Once you decide on a mortgage product that best suits your needs, you’ll work directly with a loan expert to upload and sign documents and finalize the loan. If you prefer to meet with a loan expert, there are 170 Guaranteed Rate branches across the United States.

Truist

Truist is known for its brick-and-mortar presence, but they also have an impressive online mortgage platform. Available in English and Spanish, Truist mortgage offers an array of mortgage solutions to choose from.

You can initiate the application process online or directly from your mobile device through the SMARTGUIDE tool.

You can also call 877-907-1020 to speak with a loan officer or chat online from the website. Or if you wish to meet with a loan officer, use the locator tool to find a Truist branch near you.

You can also take advantage of their Doctor Loan program if you’re a medical professional and meet select income criteria.

SoFi Mortgage

SoFi mortgage is another online lender that stands out from the masses. Although they don’t offer government-backed home loans, SoFi mortgage has programs that require a down payment as low as 10 percent, and they do not assess mortgage insurance.

Customers also enjoy a seamless prequalification and application process, along with no origination fees. Even better, it may be possible to close on your loan in under 30 days.

Penny Mac

If you’re searching for flexibility, Penny Mac may be the ideal lender for you. They offer several options to consumers of varying financial backgrounds. To date, they’ve served over 1 million customers and funded over $5 billion in loans in 2017, alone.

You can request a no-obligation free quote online, chat with an expert, or call (888)870-6229 to get started.

Reali

Crediful’s rating

Reali caters to consumers looking to purchase or refinance their homes. Through their Interactive Loan Dashboard, you can apply, upload any documents needed, and track your loan’s progress at the tap of a fingertip.

You’ll also have access to a Home Loan Advisor 24/7 to address any concerns you may have. And because of their streamlined process and low fees, you can expect to close in record time without spending a fortune.

Unfortunately, Reali does not offer government-backed products, like FHA loans, USDA loans, and VA loans.

This can be a turnoff to first-time, credit-challenged, or cash-strapped buyers.

Another major drawback is that they only operate in Arizona, California, Colorado, Florida, Georgia, Illinois, Michigan, Oregon, Pennsylvania, Texas, Virginia, and Washington.

The good news is they plan to expand their offerings to more states soon.

Pros and Cons of Online Mortgage Lenders

The rise of the internet has revolutionized many industries, and the mortgage industry is no exception. Online mortgage lenders have steadily been gaining a more substantial market share due to their distinct advantages. However, as with anything, they come with their own set of disadvantages. Here, we break down the pros and cons of opting for an online mortgage lender.

Pros of Online Mortgage Lenders

1. Lower Costs: Operating primarily online, these lenders often have fewer overhead costs compared to traditional brick and mortar lenders. This can translate into competitive mortgage rates and lower lender fees, making online mortgage lenders potentially cheaper.

2. Convenience: The ability to initiate and complete the entire application process online is a significant advantage. You don’t have to schedule meetings with a loan officer or travel to a bank branch. Instead, you can apply anytime, anywhere, which fits well with busy schedules and modern, on-the-go lifestyles.

3. Range of Loan Products: Online mortgage lenders often offer a broad range of loan products, including FHA and VA loans, USDA loans for rural properties, conventional loans, and jumbo mortgages. These lenders often cater to a diverse demographic, meaning whether you’re a first-time homebuyer seeking down payment assistance, a veteran, or someone with less-than-perfect credit, you can often find an online mortgage product that suits your needs.

Cons of Online Mortgage Lenders

1. Technological Hurdles: Not everyone is tech-savvy. If you’re not comfortable navigating online platforms or don’t have reliable internet access, you may find the online mortgage process daunting. The learning curve associated with digital platforms can be a deterrent for some people.

2. Lack of Personal Interaction: Some people prefer a high-touch, personalized service when dealing with significant transactions like buying a home. With online lenders, face-to-face interaction is usually minimal or non-existent, which can be a downside for those who prefer a more traditional approach to their financial transactions.

3. Negotiability of Fees: While online mortgage lenders are often cheaper, certain costs like origination fees and closing costs may not be as negotiable as they could be with a traditional lender. Also, mortgage insurance may still be required for government-backed loans, like FHA or VA loans, and the requirements for jumbo loans may be stricter.

4. Trustworthiness: The online space can be a breeding ground for scams and unscrupulous practices. Not all online mortgage lenders are trustworthy, making it crucial to do your homework. It’s important to research each online lender thoroughly, checking their reputation, reading customer reviews, and ensuring they are registered with appropriate financial oversight institutions.

Despite these potential downsides, many homebuyers find that the convenience, competitive rates, and the ability to shop around from multiple lenders offered by online mortgage lenders outweigh the cons. But the best online mortgage lender for you ultimately depends on your personal finance needs, comfort level with technology, and unique home loan situation.

Factors to Consider when Choosing an Online Mortgage Lender

Finding the right online mortgage lender for your home-buying journey involves more than just hunting for the lowest interest rate. You need to consider a variety of factors, from loan types to the speed of loan processing. Here’s a breakdown of what to look for:

Interest Rates

As a prospective borrower, interest rates are often one of your first considerations. The interest rate can significantly influence your monthly mortgage payment and the total cost of your loan. Due to their lower overhead costs, online mortgage lenders often advertise competitive rates. However, it’s essential to compare rates across different lenders to ensure you’re getting the best deal.

Fees and Hidden Charges

While interest rates play a crucial role in determining your loan cost, it’s equally important to consider fees and potential hidden charges. This could include origination fees, appraisal fees, closing costs, and other service charges. Some lenders may also charge additional fees for rate locks or early repayments. Always ask for a comprehensive cost breakdown and be wary of lenders who are not transparent about their charges.

Loan Types

Each online mortgage lender may offer a variety of loan types, such as FHA loans, VA loans, conventional loans, and more. Depending on your personal circumstances and needs, you might need specific loan products like USDA loans for rural properties, FHA or VA loans for a low down payment, or jumbo loans for larger properties. Ensure that the lender you choose caters to the type of loan that suits your situation best.

Customer Service and Support

Excellent customer service is crucial when dealing with online lenders as your primary communication methods will be via phone, email, or online chats. Lenders who offer high-quality customer service can significantly streamline the mortgage process, making it less stressful for you. Consider checking customer reviews and ratings for insights into a lender’s customer support.

Speed of Loan Processing

The time it takes for online mortgage lenders to process your loan application and close your loan can vary. If you’re working within a specific timeframe, you may prefer a lender known for quick processing. This is particularly crucial in competitive real estate markets, where being able to close swiftly could make all the difference.

Pre-approval Process

A seamless pre-approval process can signify an efficient online mortgage lender. Pre-approval offers you a rough estimate of how much you can borrow and helps you stand out in competitive property markets. Seek lenders that provide easy pre-approvals, preferably with only a soft credit check to avoid impacting your credit score.

User-friendly Technology

With most of your interaction with online lenders taking place digitally, user-friendly technology becomes paramount. Consider factors such as the simplicity of the application process, online document upload functionality, digital signature capabilities, and the ease of online loan tracking. A lender with a robust, intuitive platform can significantly simplify your online mortgage process.

Tips for Applying for a Mortgage Online

Embarking on the journey of applying for a mortgage online can feel overwhelming, especially if it’s your first time. But don’t worry – we’ve got some helpful tips to guide you through the process.

How to Prepare

Before you start your online mortgage application, it’s important to get your financial house in order. Here’s how:

Check your credit score: Your credit score is one of the main factors that lenders consider when evaluating your loan application. Make sure to check your credit reports for any errors and dispute them if needed. If your score is low, you might want to consider improving it before applying for a mortgage.

Verify your income: You will need to provide proof of income, so gather your recent pay stubs, W-2s, or tax returns. If you’re self-employed, you may need to provide additional documentation, like bank statements or profit and loss statements.

Get your documents in order: Apart from income verification, you’ll need other documentation, like identification, proof of assets, and information about your debts. Having these documents ready can speed up the application process.

Navigating the Application Process

Once you’re ready to apply, keep the following in mind:

Understand the terms: Make sure you understand the terms of the mortgage, like the interest rate, whether it’s fixed or adjustable, the length of the loan, and any fees involved.

Use online tools: Many online lenders offer useful tools like mortgage calculators. These can help you understand what your monthly payments might be based on different interest rates and down payment amounts.

Stay organized: Keep track of where you are in the application process. Most online platforms will save your progress, but it’s good to have your own record too.

Questions to Ask Your Lender

Securing a mortgage can often feel like a daunting process, particularly when applying online. To navigate this path with more confidence, it’s crucial to arm yourself with the right questions when engaging with potential lenders. The responses to these questions will not only give you a clearer idea about the mortgage terms but also about the lender’s transparency and commitment to customer service.

What types of loans do you offer?

The world of mortgages encompasses a variety of loan types designed to cater to different borrower needs. This includes conventional loans, government-backed loans such as FHA, VA, and USDA loans, and jumbo loans for larger mortgages.

Understanding the unique benefits and requirements of each type is important. For example, FHA loans may be suitable for those with lower credit scores, while VA loans are primarily designed for veterans. Your potential lender should be able to provide a comprehensive explanation of each option and help guide you towards the loan type that best fits your unique situation.

What are the interest rates and APR?

While the interest rate of a loan often takes center stage, the Annual Percentage Rate (APR) should not be overlooked. The APR provides a more comprehensive measure of cost as it includes the interest rate, lender fees, and other loan charges, offering a more complete picture of the long-term cost of the loan.

What fees are involved?

Beyond the interest rate, mortgages often involve several other fees that can impact the overall cost of the loan. These include origination fees, appraisal fees, home inspection fees, and potentially prepayment penalties. Some lenders may even charge for rate locks, which secure your interest rate for a specified period. It’s critical to ask for a detailed breakdown of all fees involved to ensure that there are no hidden costs that might surprise you down the line.

What Is the estimated timeline for approval and closing?

Mortgage approval and closing timelines can vary greatly among different lenders. Knowing the expected timeline can be crucial, especially if you’re working with a specific move-in date. In a competitive real estate market, a quick approval and closing process could make all the difference when multiple offers are being considered.

What are your minimum credit score and down payment requirements?

Understanding a lender’s minimum credit score and down payment requirements can help you gauge your chances of approval. These requirements can vary greatly depending on the loan type and the individual lender’s policies.

Do you consider alternative credit data?

For those with a limited credit history, some lenders may consider alternative credit data such as utility bill payments or rent payment history. Asking about these possibilities could potentially help you qualify for a loan even with less conventional credit information.

What is your process for loan servicing?

Understanding whether the lender will service your loan or if they intend to sell it to another company is important. If they plan to sell it, knowing who your point of contact would be for any issues or inquiries is crucial.

Bottom Line

Choosing an online mortgage lender is a significant decision that can impact your financial situation for years to come. Therefore, it’s critical to take the time to carefully evaluate each lender. From comparing interest rates to analyzing the type of customer service they offer, there are many factors to consider in this selection process.

We’ve touched upon some of the best online mortgage lenders available today. These lenders were chosen based on their competitive rates, comprehensive loan options, excellent customer service, and user-friendly platforms. However, remember that the “best” lender will vary depending on individual circumstances, and the top choices for others might not be the best for you.

While online mortgage lenders offer convenience and often competitive rates, they also come with their unique set of challenges. It’s vital to remember that transparency, trustworthiness, and a clear understanding of the terms and conditions are paramount in any financial decision, including choosing a mortgage lender.

We encourage you to conduct your own research and take advantage of online tools and resources that many of these lenders offer. Shopping around and comparing multiple lenders will help you find the best mortgage fit for your specific needs.

Remember, a mortgage is a long-term commitment. The time and effort spent in making a careful, well-researched decision now will pay dividends over the life of your loan. Happy home hunting!

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

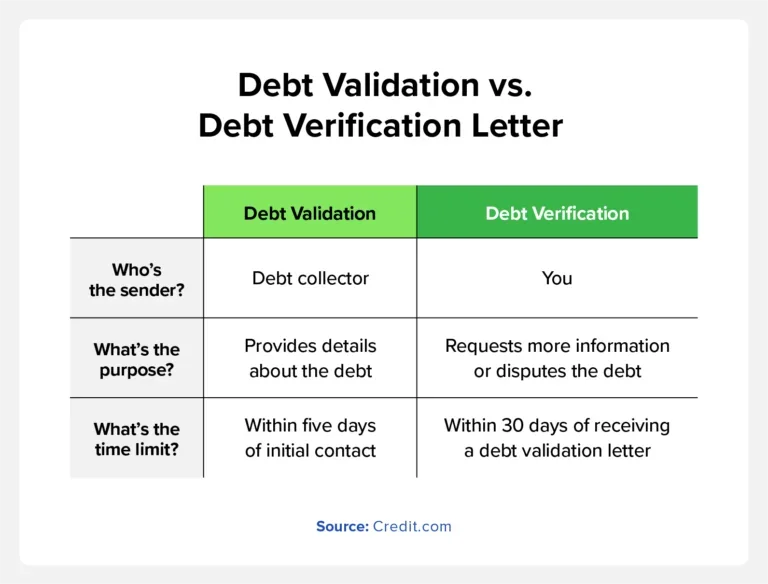

Debt collectors send debt validation letters show what debts you owe, the amount, and to whome you owe it to.

While a debt collector contacting you can be stressful, it’s important to pause and remember your rights as a debtor. Before paying the debt collector, verify that the debt is actually yours. The debt collection industry is subject to mishaps and mistakes, with some individuals being asked to pay debts they don’t owe.

That’s why you should receive a debt validation letter from the debt collector proving the debt is yours. If you still don’t recognize the debt, you can send a debt verification letter requesting more information or disputing the debt.

In this article, we’ll discuss the importance of debt validation letters and what information they should include. We’ll also provide a debt verification letter sample and a free template to help you get started.

Key takeaways:

Debt collectors are legally required to send you a debt validation letter within five days of initially contacting you.

A debt validation letter should include information about the debt, such as the amount you owe and the original creditor’s name.

If you’re unsure if the debt is accurate, send a debt verification letter to dispute the debt or ask for additional details.

Table of Contents:

What Is a Debt Validation Letter?

What Should a Debt Validation Letter Include?

When to Send a Debt Verification Request

Debt Verification Letter vs. Debt Validation Letter: What’s the Difference?

Debt Verification Letter Template + Sample

How Long Does a Creditor Have to Respond to a Debt Verification Request?

What to Do If a Debt Collector Doesn’t Respond to a Debt Verification Request

What Is a Debt Validation Letter?

A debt validation letter is written correspondence that debt collectors are legally obligated to send you that provides information about the debt they’re collecting. The letter should include details about the debt, the original lender, and the debt collector’s authority to collect the money.

The creditor should send a debt validation within five days of their initial contact with you. If you don’t receive a debt validation letter, the debt collector could be an illegitimate person attempting to scam you. Therefore, you should avoid providing sensitive information to the debt collector until you’ve verified they’re legitimate.

What Should a Debt Validation Letter Include?

According to the Consumer Financial Protection Bureau (CFPB), the debt validation letter should include:

The amount of debt you owe

The name of the original lender requesting payment

The account details associated with the debt

An option to dispute the debt within a 30-day time period

An opportunity to request more details about the original lender

A statement acknowledging that the collector will provide verification if you dispute the debt

When to Send a Debt Verification Letter

If after receiving the debt validation letter and you’re still unsure of whether the debt is accurate, you can send a debt verification request to the debt collector. A debt verification request is a letter that you, as the consumer, can send to the debt collector to ask for information about the debt they’re collecting.

Typically, you have 30 days to send your debt verification request after receiving the debt validation letter. If you don’t send the letter within this time frame, the debt collector will assume the debt is valid and legally continue their efforts to collect.

Debt Verification Letter vs. Debt Validation Letter: What’s the Difference?

It’s important to understand the difference between a debt verification letter and a debt validation letter:

A debt verification letter is a correspondence that you, the consumer, send to the debt collector requesting more information about the debt.

A debt validation letter is a document the debt collector sends to you, providing details about the debt.

Debt Verification Letter Template + Sample

When writing a debt verification letter, it’s important to be clear and concise. State that you’re disputing the debt and list what information you’re requesting from the debt collector.

Below is a debt verification letter sample and a template to help you get started. Remember to use your own information where there is bolded text.

[Name]

[Address]

[Today’s date]

[Name of the debt collector]

[Address of the debt collector]

Re: [Debt account number, if it was provided to you]

Dear [Name of the debt collector]:

I’m replying to your communication regarding a debt you’re attempting to collect. You reached out to me via [phone/mail] on [date] and provided the following account details:

[Account number, if provided]

[Name of the original creditor, if provided]

I am informing you that I dispute the debt you’re claiming I owe.

If you have reason to believe that I’m still responsible for this debt, kindly provide the following details to ensure I have all the necessary information:

The creditor’s name and address who is currently requesting payment

The original creditor’s name and address (if different from above)

The amount owed

The account number

Documentation that proves there is a legitimate reason you think I owe the debt, i.e., a copy of the original contract

The most recent billing statement the original creditor sent to me

An itemized list of any additional interest or fees

An itemized list of any payments since the most recent billing statement

If you’re providing this data to a credit bureau, please report that I’m disputing this debt.

Sincerely,

[Your name]

How Long Does a Creditor Have to Respond to a Debt Verification Request?

There isn’t a specific time frame in which creditors must reply to a debt verification request. However, if you send the debt verification letter within 30 days of receiving the validation letter, they must cease all collection efforts until they respond to your letter and provide verification.

What to Do If a Debt Collector Doesn’t Respond to a Debt Verification Request

If the debt collector doesn’t respond to your debt verification request, it could be due to one of the following reasons:

The debt collector requires additional time to gather the information you’ve asked for.

The debt collector cannot verify the debt.

The debt is beyond the statute of limitations, so the debt collection agency cannot file a lawsuit.

You were dealing with a debt collection scammer.

If you sent the debt verification letter within the 30-day time frame, the debt collector cannot attempt to collect until they provide the information you requested. If the debt collector continues with attempts to contact you, you can submit a complaint with the CFPB, your state’s attorney general’s office, or the Federal Trade Commission.

Debt validation and verification letters can help you exercise your rights and avoid potential debt collection scams. If the debt collector fails to verify your debt, be aware that it may be wrongfully hurting your credit. Check your credit report for inaccurate information and report errors to the credit bureaus to potentially remove the accounts from your credit report.

It’s important to monitor your credit so you can get alerted if inaccurate information is hurting your credit. Try ExtraCredit® for free today for help managing your credit.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Disclosure regarding our editorial content standards.

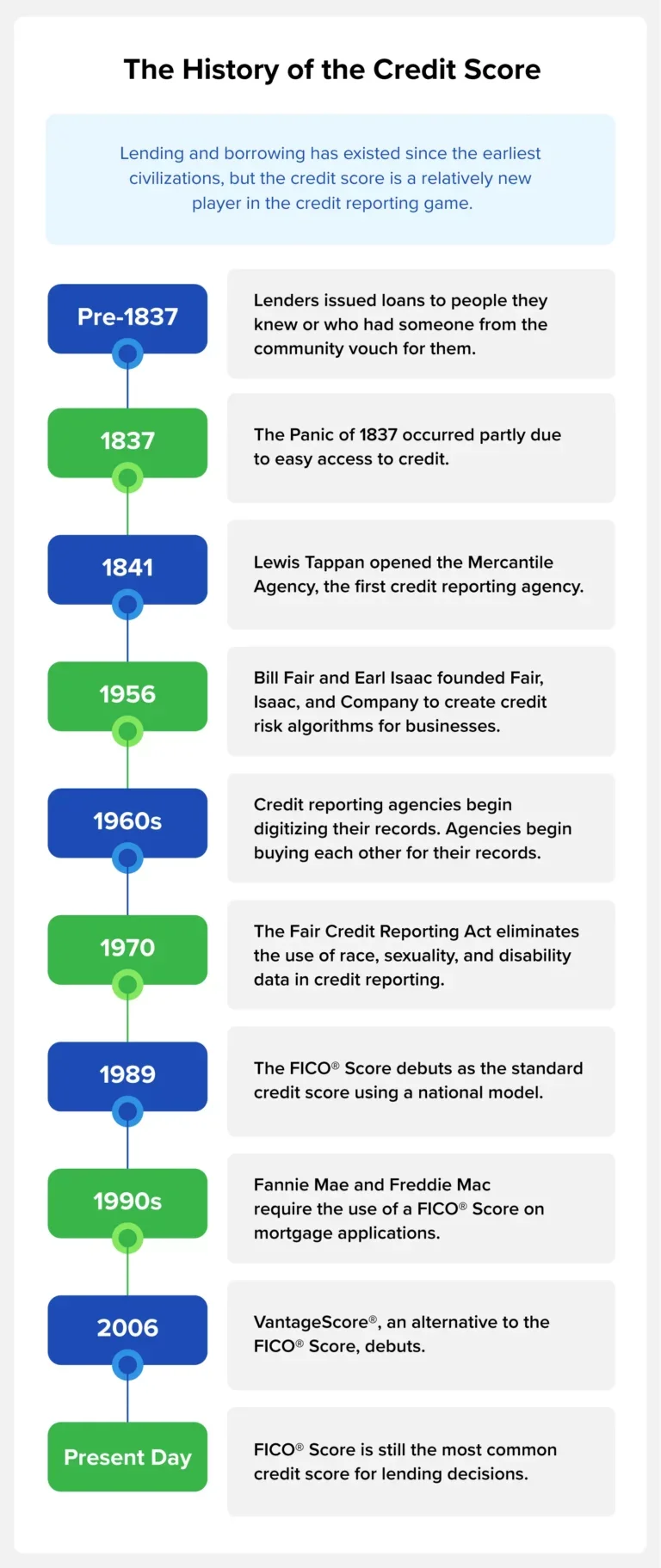

The credit score was invented in 1989 to make credit reports more actionable for lenders.

Credit scores affect many parts our lives: whether we qualify for a loan, what interest rate we pay, even where we can rent or whether we get our dream job. But that three-digit number is a relatively new invention—the credit score was invented in 1989, less than 50 years ago.

Understanding the origins of the credit score can help you better comprehend why lenders use it and how to improve your financial situation.

When Credit Scores Were Invented

People have borrowed and lent money for centuries. In the early days, storekeepers and lenders only extended credit to people they knew, or they would ask people they respected in town for their views on a person’s credit risk. This informal credit reporting system was highly localized and incredibly subjective.

But as credit became more critical to daily life and people began to move around more, the need for a more widespread credit reporting method arose.

The 1800s: The Rise of Credit Reporting Agencies

After the Panic of 1837 (partly caused by easy access to credit), Lewis Tappan recognized that businesses might benefit from a better understanding of who to issue credit to. In 1841, he formed Tappan’s Mercantile Agency, the first credit reporting agency in America, to meet this need.

His company hired “correspondents,” reliable men (often attorneys and ministers) who would investigate people’s standing in their communities and report it to the central office. They would then add the information to a central ledger in New York City. Many businesses subscribed to the Mercantile Agency to view these reports before issuing credit.

Tappan was a strict abolitionist, so he only worked with businesses in free states, so other credit reporting agencies began to spring up to work with businesses in the South. Hundreds of these credit reporting agencies existed all over the country by the end of the Civil War, but the system had a few problems:

Each agency had different information based on who they hired as correspondents.

Information was highly subjective and included information about a person’s race, gender, and overall moral character, which allowed bias to play a role in lending decisions.

Lenders didn’t know how to interpret the information in the credit reports because they were so subjective, and lenders often didn’t know the person applying for credit.

As more people began to access credit to purchase items like cars and homes in the late 1880s and early 1900s, these credit reporting agencies continued to thrive.

1950s and 1960s: Digitizing Credit Reports

This system was still in place in the 1950s when the ability to digitize records meant that some standardization could occur. Larger agencies started buying their smaller counterparts for additional data they could add to their reports, and national credit bureaus began to form.

In 1956, Bill Fair and Earl Isaac created Fair, Isaac, and Company to make credit reports more actionable for lenders. They used the data in a credit report to perform a statistical analysis that would inform a lender of a person’s credit risk. What resulted was a more analytical approach to interpreting credit reports, but each business or lender had its own algorithm based on the factors they prioritized.

As records continued to be digitized, many people became concerned about the surveillance being done to gather credit information and discriminatory practices in credit reporting. People also realized that credit mistakes would be available forever and could potentially hurt people’s ability to borrow for their entire lifetimes. The Fair Credit Reporting Act of 1970 put several protections into place, including:

Removing data related to race, sexuality, and disability from credit reports

Requiring credit reporting agencies to delete information after seven to 10 years, depending on the type of data

1989: The FICO Credit Score

While more effective for lenders than the previous system, scores varied widely based on a company’s priorities.

The credit reporting bureaus wanted something more standardized, so they partnered with Fair, Isaac, and Company (now known as FICO®) to create the FICO Score, a national scoring model for everyone. The FICO Score debuted in 1989 and quickly became popular with lenders, who no longer needed to hire companies to create their own algorithms. Consumers, who could now know their credit score before applying for a loan, also appreciated the FICO Score.

In the 1990s, the FICO Score cemented itself as part of the lending landscape when Fannie Mae and Freddie Mac began requiring the score as part of mortgage applications.

VantageScore and Other Credit Scores

In 2006, the three major credit reporting bureaus—Equifax®, Experian®, and TransUnion®—launched the VantageScore®, an alternative to the FICO score. There have been four iterations of the VantageScore since 2006, and the latest version incorporates trended credit data, which includes monthly data points over 24 months. It also utilizes machine learning and does not factor medical debt into its algorithms.

Each major credit reporting bureau also has its own proprietary scoring models that lenders may also consider:

Equifax Credit Score

Experian PLUS Score

TransUnion CreditVision New Account score

Despite these options, most top lenders use the FICO Score.

Why Credit Scores Were Invented

Before the credit score, lenders determined a person’s credit risk based on credit reports, which include:

Personal information

Account information

Hard inquiries into your credit

Public financial records such as liens or bankruptcies

Often, lenders weren’t sure how to interpret your credit report, which led to bias in lending decisions and general confusion for consumers regarding whether they would be approved for a loan when they applied.

The credit score was invented to standardize the lending process to make it faster and more equitable. It prevented lenders from using racial, gender, and class bias when determining someone’s credit risk.

Problems With Modern Credit Scoring

While credit scores eliminated the problems of previous credit reporting systems, they aren’t perfect. Here are a few issues with modern credit scoring:

Inappropriate use of credit scores. When the credit score was originally invented, its sole purpose was to determine credit risk for loans. Now, lenders, landlords, and employers often use it to determine a person’s level of responsibility, which can influence car insurance rates and hiring decisions.

Upholding social hierarchies: People with low credit scores, or the roughly 10% of Americans with no credit history, are often denied access to loans or credit cards. When they receive a loan, they often have to make a larger down payment and pay more in interest.

Racial disparities: While the Fair Credit Reporting Act of 1970 removed the use of race as an explicit factor in one’s credit, institutional racism may still impact the remaining factors. For example, redlining continues to prohibit many Black Americans from purchasing a home, preventing them from building wealth through homeownership. As a result, their credit length and payment history, two factors that impact your credit score, may be shorter. This may explain why multiple studies have shown that racial minorities have lower credit scores than white people.

Inaccurate information: A recent study found that 34% of people have at least one error on their credit report. These errors can lower your credit score, resulting in you paying more in interest. While you can dispute errors on your credit report, it may take time to see an increase in your credit score.

These problems could result in you paying more in interest for a loan or being denied the loan altogether.

The Future of Credit Scores

Credit scores have changed since they were invented and will continue to do so as consumer spending and technology change. Here are a few trends that may impact how credit bureaus determine your credit score in the near future:

Buy Now, Pay Later (BNPL): Also called point-of-sale (POS) installment loans, BNPL plans allow you to divide purchases into lower monthly payments, often without interest. Currently, these short-term loans aren’t reported to a credit bureau unless you don’t make your payments, but that may change as technology advances to allow real-time data and these become more popular with consumers.

AI and Machine Learning: Experts are currently debating the use of AI and machine learning to automate and improve credit scoring. Some parties claim it will result in more accurate credit risk assessments and allow credit reporting to occur in real time, making it more accurate. Others are concerned about the potential invasion of privacy and the ethical use of data since AI is only as good as the data it is fed.

Inclusion of alternative data: Nearly 37 million Americans are credit underserved, meaning they have little to no credit history. As a result, they are unable to get access to credit. To help the credit invisible gain credit, credit reporting companies have begun considering alternative data, called consumer-permissioned data, including bank account information and monthly payments like rent, utilities, and streaming subscriptions. Currently, consumers can choose to share this information with lenders and then retract access once they’ve built credit, but this information could begin factoring into everyone’s credit score since AI can make this data easier to use.

Track Your Credit Score With Credit.com

Your credit score is one of the most important numbers in your life. Understanding the history of the credit score and its challenges can help you in your journey to improve your credit. As technology continues to advance, stay informed on the latest updates to credit scoring and take proactive steps to manage your credit with Credit.com.

Real estate investment trust Rithm Capital Corp. has increased its offer to acquire Sculptor Capital Management Inc. by 7.62% to $676 million amid competition from a group of investors and a dispute among the shareholders at the asset management firm.

On July 24, Rithm said it struck a deal to acquire the New York-based company for $639 million, or $11.15 per Class A share. The transaction brings to Rithm Sculptor’s $34 billion of assets under management, including real estate, credit and multi-strategy investing spectrum.

The July deal led to a dispute among the shareholders at the asset management firm as Sculptor also received a $12.76 per-share bid from a consortium of investors, including Boaz Weinstein, Bill Ackman, Marc Lasry and Jeff Yass.

Sculptor said it still prefers the deal with Rithmdue to the closing certainty. However, it put pressure on Rithm to increase its bid.

The new offer announced Thursday brings the price per share to $12. The boards of directors of both companies have unanimously approved it, the parties said.

In a statement, Marcy Engel, chairperson of Sculptor’s board of directors, said they are focused on “consummating a transaction that maximizes value and certainty of closing for Sculptor stockholders.”