Dave Ramsey warns Americans about the damage ‘Bloody Sunday’ has left in its wake, offering advice for anyone who want to buy a home amid spiking interest rates

If sky-high house prices and mortgage rates have made you hit pause on your home buying plans, you may want to think again, or so says personal finance personality Dave Ramsey.

The average 30-year fixed mortgage rate increased to 7.79% last week — up from the prior week’s average of 7.63% — and hitting (another) highest level since 2000. At the same time, house prices continue to rise, primarily due to low inventory.

Don’t miss

“[House] prices aren’t going to go anywhere but up, even with interest rates going up,” Ramsey said on a recent episode of “FOX & Friends.”

“The housing market is just stalled and, man, we’ve got Bloody Sunday with the student loans kicking back in [as of Oct. 1] and Christmas is bearing down on us so it is time to get on a budget and get on a plan.”

With that in mind, Ramsey says you shouldn’t sit back and wait for conditions to improve — reminding potential buyers that you can always refinance your home loan to get a better rate down the road. In fact, if you meet two criteria — “you’re out of debt and you’ve got your emergency fund” — Ramsey suggests going for it now.

Here’s how you can hit Ramsey’s critical financial conditions to buy your dream home — plus some other ways to invest in real estate while dodging housing market headwinds.

Become debt free

Ramsey was joined on “FOX & Friends” by his “The Ramsey Show” co-host George Kamel, who backed Ramsey’s bold housing call and mirrored his advice around becoming debt free.

“If you’re a millennial or you’re Gen Z, you’re feeling hopeless right now, you’re feeling cynical,” says Kamel. “Your parents are saying: ‘You’re throwing away money on rent, get a house, get a house, get a house’ — and you’re broke.

“You’ve got to have some patience because rent and mortgages are not apples to apples,” Kamel said, adding buying a home also comes with taxes and insurance — and in some cases, homeowners’ association fees and private mortgage insurance. All those expenses can add up, which is why the Ramsey camp argues it’s important to ensure you’re debt free with an emergency fund established before making an offer.

There are many different ways to handle debt, but in his well-known seven “baby steps” to financial success, Ramsey advocates for the snowball method. With this strategy, you pay off the smallest debt (or account with the lowest balance) first and make only minimum payments on all of your other outstanding debts. Once you’ve paid off your smallest debt, you move on to the next smallest debt, and so on.

But how much interest you end up paying on your debt is an important factor. If you’ve got a pile of high-interest debt on your credit card or your car loan, you could fall behind on your payments, be subject to financial penalties and your balance can quickly spiral out of control, making it even harder to get debt free. For you, it might make more sense to use the “avalanche method” of debt repayment, where you tackle the loan with the highest interest rate first and go from there.

Regardless, to succeed in this journey, you’ll need to stick to a budget that breaks down your monthly income into necessities, wants, savings and debt repayments.

Read more: Thanks to Jeff Bezos, you can now use $100 to cash in on prime real estate — without the headache of being a landlord. Here’s how

Build an emergency fund

Ramsey believes every adult American should have at least $1,000 set aside to cover life’s inevitable surprises, like you’re suddenly slapped with a big medical bill or your car breaks down. That back-up fund will stop you from falling into financial distress.

But that’s just meant to get you started. Once you’ve paid down your debts, Ramsey suggests revisiting your emergency fund to set aside three to six months worth of living expenses — including your rent or mortgage, other loan repayments, grocery and energy bills and other regular expenditures — to cover larger surprises like a job layoff or a long hospital stay.

Wherever you are on your savings journey, you might consider stashing some cash in a high-yield savings account (HYSA). With an HYSA, you could earn more interest on your money and benefit from greater compound growth than you would with a traditional savings or checking account.

You may also want to consider using other high-yield savings products like money market deposit accounts (MMDA) or a certificate of deposit (CD) to make the most of the current high interest rates. But remember that banks and credit unions will often charge an early withdrawal penalty for taking money out of a CD before its maturity date.

Other real estate options

Once you’ve hit those two financial milestones — paying down your debt and building an emergency fund — then Ramsey says you should go ahead and buy a house (if that’s what you want to do). But if you’re unconvinced, there are other ways to get a foothold in the real estate market without dealing with the extensive costs of homeownership.

For instance, you may want to consider putting your money in a real estate investment trust (REIT), which are publicly-traded companies that collect rent from tenants and pass that rent to shareholders in the form of regular dividend payments.

There are also online crowdfunding platforms that allow everyday investors to pool their money to purchase property (or a share of property) as a group.

If you don’t want to make investment decisions on your own, some new online platforms can even help you invest in diversified real estate portfolios that will maximize your returns while keeping your fees low.

What to read next

This article provides information only and should not be construed as advice. It is provided without warranty of any kind.

Not all debt is created equal, and when you’re looking to pay it down, the order in which you do so is important. Two common types of debt are student loans and credit cards. Are you wondering if you should pay off student loans or credit cards first?

Different Ways to Pay Down Debt

One of the first things that you should do when looking to pay down debt is to list out all of your amounts due. Gather the totals owed, the interest rates, the monthly payments, and all other information for each of your different debts. Then, you can make a plan for how to eliminate them.

Learn more about two popular methods – the debt snowball and debt avalanche.

In Most Cases, it Makes Sense to Pay Off Your Credit Cards First

There isn’t a single answer for whether it’s better to pay off student loans or credit cards first, but credit cards often have higher interest rates than student loans. The exact method you choose for paying down debt is less important than making a plan that you’ll stick to.

When it comes to money matters, it’s natural to have questions — lots of them. At SoFi Learn, you’ll find answers, plus tools, guides, calculators and more.

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law Firm’s editorial disclosure for more information.

The debt avalanche method is an accelerated debt repayment strategy that involves paying off the debt with the highest interest first, then rolling those payments to your next highest-interest debt until all your debt is paid off.

Getting out of debt can seem overwhelming when you’re sitting at your kitchen table trying to pay bills each month or if debt collectors are harassing you. It’s even worse when all you can think about is everything else you could spend money on: a family vacation, a new car. But with a bit of dedication and a plan, it’s possible to regain your financial freedom with an accelerated debt repayment strategy like the debt avalanche method.

Read on to learn how to use the debt avalanche method to pay off your debt faster than you may have thought possible.

What is the debt avalanche method?

The debt avalanche method is an accelerated debt repayment method. When using this strategy, you make minimum monthly payments on all your debts and put any additional funds toward paying down the debt with the highest interest rate.

Once you’ve repaid that debt, roll that minimum payment and additional funds over into the debt with the next highest interest rate. Repeat the process until you’ve paid off all your debts.

The debt avalanche method is a good strategy for most types of debt:

Student debt

Credit card debt

Auto loans

Medical debt

Debt avalanche vs. debt snowball: What’s the difference?

The debt avalanche is often compared to the debt snowball—another accelerated debt repayment method. In a debt snowball, instead of paying off the debt with the highest interest rate, you direct all your extra money toward paying off the debt with the lowest balance.

While both methods will pay off debt faster than if you had no strategy, you’ll see more quick wins if you opt for the snowball method, making it a good option for people who are easily discouraged.

You can also combine the two methods by prioritizing paying off the smallest debt with the highest interest rate to save on interest and see quick wins.

How to use the debt avalanche method to pay down debt

To use the debt avalanche method, follow these steps:

Build up an emergency fund. This will ensure an unexpected bill doesn’t throw off your payment plan. Experts recommend having enough in your emergency fund to cover six months of living expenses.

Make a list of all your debts. Include their balances, interest rates and minimum payment amounts. Organize your list from the highest interest rate to the lowest.

Total your monthly expenses and income. Add up all the money you spend on monthly living expenses and monthly minimum payments on debt. Also note your monthly income.

Determine how much money you have to put toward additional debt payments. Tally what you have left over each month after paying monthly expenses and minimum payments. You’ll put this “extra money” toward debt each month.

Each month, put the extra money toward the debt with the highest interest rate. This should be in addition to the regular monthly minimum payments.

Put any unexpected income toward the debt with the highest interest rate. If you get any unexpected income, such as a tax refund or bonus at work, put that toward your accelerated payment as well.

When you’ve paid that debt off, roll over that debt’s minimum payment and your extra monthly income toward the debt with the next highest interest rate. Continue paying the minimum payment on all other debts.

Repeat until you’ve cleared all your debts. As you pay off debts, your payments to the other debts will increase.

Debt avalanche example

Let’s look at an example use of the debt avalanche method.

You have three outstanding debts:

A student loan for $10,000 with 5 percent interest and a minimum monthly payment of $400

A credit card debt of $5,000 with 25 percent interest and a minimum monthly payment of $100

A home repair loan for $3,000 with 15 percent interest and a minimum monthly payment of $275

And after monthly living expenses and the three minimum payments, you have $250 leftover in your budget to put toward accelerated payments.

Since your credit card debt has the highest interest rate, start by paying the extra $250 in addition to the $100 monthly payment. That means you’ll pay $350 each month.

Once you’ve paid off your credit card debt, your debt with the next highest interest rate is the home repair loan, so that’s where you’ll start sending your extra payments each month. Roll over the $350 you paid monthly for the credit debt to the home repair loan. Added to the minimum payment of $275, you’ll pay $625 toward the loan each month.

When the home repair loan debt is clear, focus on your student loan, which has the lowest interest rate of your three debts. Roll over the $625 you were paying to the home repair loan to the minimum payment for the student loan, for a total monthly payment of $1,025.

If you use the debt snowball method discussed earlier, you’d start by paying off your smallest debt, which in this case is the home repair loan.

Pros and cons of the debt avalanche method

The debt avalanche method is one of the most logical and cost-effective debt repayment plans, but it isn’t perfect.

The advantages of the debt avalanche method are:

You’ll save on interest. This method helps you pay off your debt early, saving you what you would have paid in interest.

You’ll pay back your debt faster. By steadily making payments larger than the minimum, you can shave months off your repayment plan.

The disadvantages of the debt avalanche method are:

Larger debts can take longer to pay back. If you know you need small wins to stay motivated, this can negatively impact your ability to stick with your accelerated payment plan.

Unexpected bills or unstable income can hinder your progress. This method only works if you can make regular payments larger than your minimum payment.

Other ways to pay off credit card debt

While many people find the debt avalanche method to be a helpful strategy for getting out of debt, there are other ways to pay off debt that may better fit your situation.

You can also use any of the following methods:

Balance transfer credit card: Some credit cards have promotional offers for 0 percent APR on balance transfers to new customers. If you qualify, you can transfer your debt on a high-interest credit card to one of these cards. Pay attention to when the promotional 0 percent APR ends, or you’ll have to pay interest again. In this situation, it makes the most sense to devote any extra income after monthly expenses to this debt to clear it faster.

Debt consolidation loan: Take out a loan for the amount of all your debt and use the money to pay off those individual debts. Then pay off your consolidation loan each month. This makes repayment easier because you’re only making one monthly payment, but be careful that the interest rate on your consolidation loan is less than the interest rates on your other debt. Otherwise, you’ll end up paying more in interest over time.

Home equity line of credit: Borrow against your home’s equity. Often these lines of credit have lower interest rates than credit cards.

Debt management plans: If you cannot pay off your debt within five years even with a strict budget, or if your total monthly minimum payments are more than your monthly income, consider getting professional help. A debt counselor can help you create a debt management plan to pay off your debt. However, secured debt (a debt with collateral, such as your car or your home) won’t qualify for a debt management plan.

Is the debt avalanche method right for you?

The debt avalanche method is an excellent option for repaying debt faster, but it doesn’t fit every situation. If you are intent on saving money while you repay debt and are motivated enough to keep going without small wins along the way, the debt avalanche method may be your path to financial freedom. While using the debt avalanche—or any accelerated debt repayment plan—it’s essential to continue with behaviors that maintain or improve your credit. Stay current on all your bills, create and stick to a budget and track your spending. Lexington Law Firm may be able to help you on your journey to repair your credit. Take our free credit assessment today to learn more.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.

Reviewed By

Alexis Peacock

Supervising Attorney

Alexis Peacock was born in Santa Cruz, California and raised in Scottsdale, Arizona.

In 2013, she earned her Bachelor of Science in Criminal Justice and Criminology, graduating cum laude from Arizona State University. Ms. Peacock received her Juris Doctor from Arizona Summit Law School and graduated in 2016. Prior to joining Lexington Law Firm, Ms. Peacock worked in Criminal Defense as both a paralegal and practicing attorney. Ms. Peacock represented clients in criminal matters varying from minor traffic infractions to serious felony cases. Alexis is licensed to practice law in Arizona. She is located in the Phoenix office.

Imagine a life where your monthly paycheck isn’t eaten up by debt payments, where your financial choices aren’t driven by outstanding balances on credit accounts, and unexpected expenses don’t plunge you deeper into debt.

This is the essence of a debt-free life. Living debt free means you owe no money to any person or institution. It’s a state of financial freedom that many dream of, yet few achieve.

But like any significant life choice, it’s not without its pros and cons. The aim of this article is to dive deeper into the advantages and drawbacks of leading a debt-free life. Whether you’re buried under credit card debt or still paying off student loans, understanding the impacts of a debt-free lifestyle can help you set goals and envision a future of financial freedom.

Even if you’re simply looking to improve your personal finance habits, this knowledge can empower you to make informed decisions about your financial future. Let’s unravel the truth behind the debt-free life, its challenges, and rewards.

What does it mean to live a debt-free life?

Living a debt-free life can mean different things to different people, but in the broadest sense, it means having no outstanding debts to your name. This means zero credit card debt, no car loans, and no mortgage.

It’s a financial state where your income is entirely yours, unburdened by any obligations to lenders. But it’s crucial to note that not all debt is bad. Some forms of debt, like low interest debt such as a mortgage, can actually work to improve your financial situation over time.

The Path to Debt-Free Living

So, how do you achieve this seemingly elusive state of debt free living? The first step involves knowing exactly how much debt you have. It’s not enough to know your minimum payments or even your monthly payment, you need a full understanding of your entire debt landscape.

This process involves pulling together data from all your credit accounts, from credit cards to personal loans, and noting the interest rates and balances. If your debt consists of high-interest debt like credit cards, consider strategies like debt consolidation to lower the interest charges and make repayment manageable. You can also consider using the debt snowball or debt avalanche method to pay down your debt over time.

Once you know how much debt you have, the next step is creating a monthly budget. Your budget should include your income, living expenses, debt payments, and any discretionary spending. Budgeting is a vital tool in the journey to financial freedom, allowing you to see where your money is going and where you can start saving money.

As you pay down debt, you’ll also want to focus on building an emergency fund. This is money set aside to cover unexpected expenses when they arise, like car repairs or medical bills. Having an emergency fund helps ensure that these unexpected expenses don’t push you further into debt.

Pros of Living a Debt-Free Life

Living a debt-free life has several notable benefits.

Financial Stability

Being debt-free can contribute to a greater sense of financial stability. Without debt payments to worry about, you can put more money towards savings or investments. You won’t be worried about covering minimum payments or juggling high interest debt.

Financial Flexibility

A debt-free lifestyle also provides financial flexibility. When you don’t owe money to creditors, you have more freedom to make financial decisions based on your needs and wants, not on your obligations.

Improved Credit Score

Less debt usually leads to a better credit score, especially if you have a history of timely payments. Credit bureaus take note of how much of your available credit you’re using, and lower utilization generally leads to a higher score.

Sense of Accomplishment and Personal Growth

The journey to become debt-free isn’t easy, but it can be incredibly rewarding. The discipline and determination required to pay off your debts can lead to personal growth and a significant sense of accomplishment.

Cons of Living a Debt-Free Life

While the benefits of living debt-free are substantial, there are also some downsides to consider.

Lost Opportunities for Leveraging Debt

While it’s true that being in debt can be stressful, not all debt is bad. Certain types of low interest debt can work in your favor. For example, taking out a mortgage to buy a home or borrowing money to start a business can be considered good debt, as these investments often increase in value over time.

Potential for Reduced Credit Score

While it may seem counterintuitive, having no debt can actually hurt your credit score in some cases. Credit scoring models like to see some level of debt management, so a history of well-managed debt can be beneficial. If you have no debt – and have never had debt – you’ll have no credit history. This can make it harder to rent an apartment or even get good car insurance rates.

Risk of Overly Conservative Financial Practices

Living a debt free life can sometimes result in overly conservative financial practices. Avoiding all debt means you might miss out on investment or business opportunities that require upfront capital.

Debt-Free Living vs. Debt Leveraging

Both debt-free living and leveraging debt as a financial tool have their merits. It’s all about understanding your financial goals and your tolerance for risk. If the thought of any debt causes stress, then the path to a debt-free lifestyle is likely right for you. B

ut if you’re comfortable with some level of risk, and understand the potential for greater returns, then responsibly leveraging debt could be a viable strategy.

5 Tips to Achieve and Maintain a Debt-Free Life

If you decide a debt-free lifestyle aligns with your financial goals, your next step is to develop a detailed strategy to get there. Here’s a closer look at some of the key elements of a plan to achieve and maintain a life free from debt:

1. Create a Realistic Budget

One of the cornerstones of any successful financial plan is a realistic budget. This outlines not only your living expenses, but also your debt payments, savings, and discretionary spending. A budget gives you a clear snapshot of exactly where your money goes each month, enabling you to make informed decisions about your spending.

The first step in creating a budget is understanding your monthly expenses. This includes everything from rent or mortgage payments, utility bills, groceries, and transportation costs to smaller expenses like subscriptions, leisure activities, and dining out.

The second part of your budget will be dedicated to any debt payments you have. This could be credit card debt, personal loans, or car payment. Your goal should be to manage these payments while striving to save money and pay down your debt more quickly.

2. Build an Emergency Fund

Life is full of surprises, and not all of them are pleasant. That’s why an emergency fund is a critical component of any personal finance strategy. An emergency fund is money you’ve set aside to cover any unexpected expenses that might arise, such as car repairs, medical bills, or job loss.

By having this safety net in place, you avoid the need to borrow money in an emergency. How much you need to save will depend on your individual circumstances, but a good rule of thumb is to aim for three to six months’ worth of living expenses.

3. Increase Your Income

Sometimes, cutting expenses isn’t enough to move the needle towards your goal of living a debt-free life. You may need to increase your income to make significant progress.

There are numerous ways to bring in extra money. You could seek a higher-paying job, take on freelance work or start a side hustle, or invest in opportunities that yield a return. The key is to use this additional income wisely, funneling it towards your debt payments or savings.

4. Keep Your Credit Utilization Low

Your credit utilization rate, the ratio of your outstanding credit card balances to your credit limits, can significantly impact your credit score. A lower credit utilization rate (generally below 30%) can lead to a higher credit score.

This is beneficial because a higher credit score can make it easier to secure low-interest loans in the future, should you need to borrow. Maintaining low balances on your credit cards, or paying them off in full each month, can help keep your credit utilization rate low.

5. Be Mindful About Taking On New Debt

Finally, as you work towards your debt-free goals, it’s important to be mindful about taking on new debt. While not all debt is bad, taking on debt should not be done lightly. Before borrowing, take the time to thoroughly consider the potential implications.

Ask yourself if the debt is necessary, and whether it aligns with your financial goals. For example, a mortgage to purchase a home or a loan to start a business could be considered “good” debt, as these are likely to increase your net worth over time. However, high interest debt from credit cards or personal loans for unnecessary purchases can hinder your financial progress.

Remember, achieving and maintaining a debt-free life is a journey, not a destination. It requires discipline, planning, and a commitment to your financial goals. But with these strategies in hand, you’ll be well-equipped to navigate your way to financial freedom.

Conclusion

Living a debt-free life can bring numerous benefits, including financial stability, increased flexibility, and a significant sense of accomplishment. But it’s important to remember that not all debt is detrimental, and in some cases, you can leverage debt to reach your financial goals more quickly.

Ultimately, the decision to live debt free or to leverage debt should align with your individual financial situation and long-term goals. By keeping these considerations in mind, you can embrace debt free living in a way that suits your lifestyle and helps you achieve your financial goals.

Remember, personal finance isn’t about following a one-size-fits-all approach. It’s about understanding your financial needs, your tolerance for risk, and your aspirations. Only then can you chart a path that leads to your version of financial freedom, whether that means zero debt, well-managed debt, or somewhere in between.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

The average household credit card debt in America is $9,654, and the states with the largest amount of credit card debt are Alaska, Hawaii, and New Jersey.

Between the first quarters of 2022 and 2023, The Federal Reserve Bank of New York reported that the credit card debt in America rose by $145 billion. As of June 2023, we saw a 12-month inflation increase of 3%, the smallest year-over-year increase since March 2021.

By understanding American credit card debt statistics, you’ll better understand where you stand and what you can do to potentially lower your debt. Credit card debt increases your credit utilization ratio, which can hurt your credit and ultimately cost you more money in interest.

We surveyed over 1,100 Americans to learn more about credit card debt statistics in the United States. This data covers the average debt by state, average interest rates, and more. While many of the statistics from our other sources look at the situation as a whole, our data helps us see what’s happening on an individual level.

Despite the national average of Americans having over $9,000 in credit card debt per household, only 14% say they’re “very worried” about their debt.

67% of respondents said they have less than $2,000 in debt, which may indicate that only a concentrated number of people have high amounts of credit card debt.

20% of respondents don’t know how long they’ve been in debt.

The majority of respondents (56%) say their credit card debt is due to unexpected expenses.

74% of respondents said at least one collection agency has contacted them about a past due debt.

In this article, we’ll also provide tips on how to get out of debt and work toward better credit.

Table of contents:

Key Credit Card Debt Statistics

Many factors play into credit card debt, such as the average interest rates, which cards have the best offers, and the balance people carry on their card. These statistics will help you compare your own credit card balance to the national average and see if you’re getting a good deal with your current cards.

Here are the standout findings of various debt statistics:

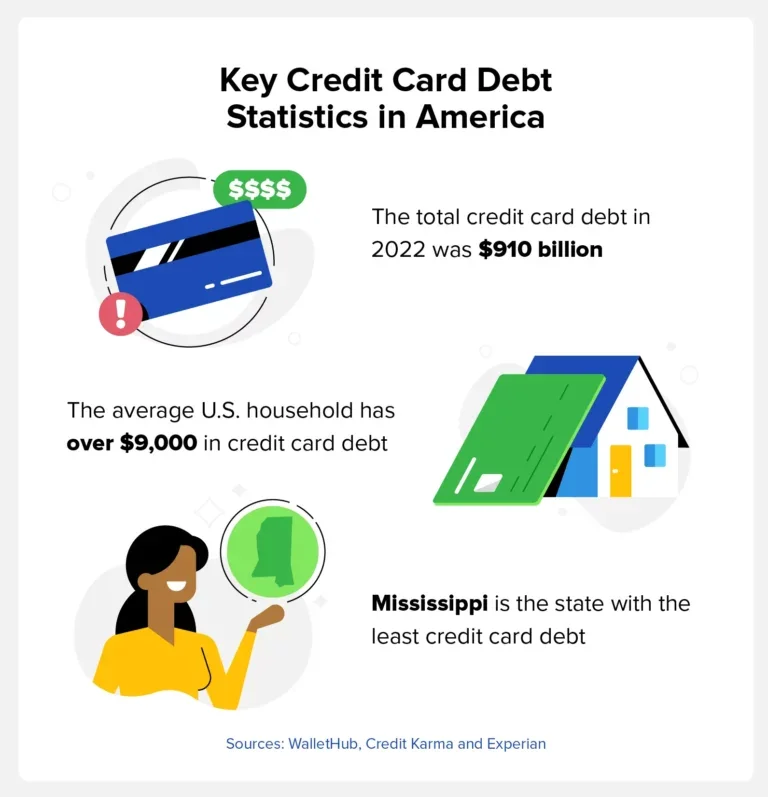

The average American household has over $9,000 in credit card debt. (WalletHub)

Mississippi has the least credit card debt at $5,259 per person. (Credit Karma)

Alaska has the most credit card debt on average at $8,139. (Credit Karma)

Credit cards 90 days or more past due rose to 4.57% in 2023. (FRBNY)

Individuals making $184,000 or more per year have the most credit card debt at an average of $12,600. (Federal Reserve)

The total credit card debt in America as of Q3 2022 was $910 billion. (Experian®)

How Many Credit Cards Carry a Balance

The American Bankers Association releases a quarterly report for consumer credit conditions, and the most recent data comes from the third quarter of 2022.

In America, approximately 43% of credit cards carried a balance, 23% were dormant, and 34% were used but paid off each month. Those who pay off their credit card balance are able to keep a low credit utilization ratio and prevent the accumulation of debt.

Tip: Use our credit card payoff calculator to estimate when you’ll be debt free.

Average Interest Rates for New Credit Card Offers

LendingTree analyzed the terms and conditions of 200 credit cards from upwards of 50 different credit card companies, banks, and credit unions. With this data, they were able to gather an assortment of information involving annual percentage rates (APR).

The APR is the amount of interest consumers pay for their purchases, and the following table is broken down by credit card type.

The following table is based on data from July 2023.

Average Credit Card Debt by State

In February 2023, Credit Karma gathered data from 74 million of their members to see which states had the most and least amount of credit card debt. Below, we’ve compiled a complete list based on Credit Karma’s data that contains the average credit card debt for each of the 50 states alphabetically.

Top 10 States With the Most Credit Card Debt

The following states had the most credit card debt, with Alaska having the highest average credit card debt in America at $8,139 per person.

State

Average credit card debt

1.

Alaska

$8,139

2.

Hawaii

$7,444

3.

New Jersey

$7,306

4.

Maryland

$7,248

5.

Virginia

$7,174

6.

Connecticut

$7,032

7.

New York

$7,029

8.

California

$6,952

9.

Washington

$6,869

10.

Florida

$6,783

Top 10 States With the Least Credit Card Debt

The major credit bureau, Experian, tracks credit card debt data as well and found that between 2021 and 2022, overall credit card debt in the U.S. increased from $785 billion to $910 billion—a 16% increase. The average debt also increased in many states, according to Credit Karma’s report.

State

Average credit card debt

1.

Mississippi

$5,259

2.

Kentucky

$5,455

3.

Wisconsin

$5,593

4.

Arkansas

$5,600

5.

Indiana

$5,601

6.

Alabama

$5,647

7.

West Virginia

$5,674

8.

Iowa

$5,732

9.

Idaho

$5,737

10.

Maine

$5,788

Average Credit Card Debt by Age

Credit Karma’s report with the state-by-state data also broke down credit card debt by age group. Currently, Generation X carries the most credit card debt, while Generation Z carries the least.

Age group

Average credit card debt

11-26 (Generation Z)

$2,781

27-42 (Millennials)

$5,898

41-58 (Generation X)

$8,266

59-77 (Baby Boomers)

$7,464

78-95 (Silent Generation)

$5,649

Average Credit Card Debt by Income

The following data comes from the Federal Reserve’s Survey of Consumer Finances (SCF) and was most recently updated in 2019. The Federal Reserve completed a new survey at the end of 2022 and will have updated data later in 2023.

As you’ll see, higher-income individuals have much more credit card debt than those who make less. This makes sense because high-income individuals are able to get much larger credit lines. But when you look at the debt-to-income ratio, lower-income households have much more consumer debt compared to the amount of money they make.

Percentile of Income

Average credit card debt

Less than 20%

$3,800

20%-39%

$4,700

40%-59%

$4,900

60%-79%

$7,000

80%-89%

$9,800

90%-100%

$12,600

Average Household Credit Card Debt

A recent study from WalletHub found that while total credit card debt in the United States rose 14.1% between 2022 and 2023, household credit card debt only rose by 8.39%.

Their data shows that the average household credit card debt at the end of the first quarter in 2023 was $9,654 adjusted for inflation, which is $738 higher than the same time the previous year. WalletHub’s chart goes back to 1986, and the highest household credit card debt was in 2007 when it was $12,221 on average per household.

Average Credit Card Debt by Race or Ethnicity

Research from Annuity.org shows that Black and Hispanic Americans are less likely to feel financially stable and less likely to have a bank account. This information can help us better understand what’s happening in the financial lives of different communities.

This data comes from the Federal Reserve’s 2019 SCF.

Race

Average credit card debt

White (non-Hispanic)

$6,940

Black or African American (non-Hispanic)

$3,940

Hispanic or Latino

$5,510

Other or multiple races

$6,320

Credit Card Delinquency Rates in America

When someone is at least 30 days past due on their credit card payment, their status becomes delinquent. The number of delinquencies in the United States can be a measure of people’s ability to pay down their credit card debt.

To track this data, Experian conducted a study between 2021 and 2022:

Accounts 30 to 59 days past due increased from 1.04% of total accounts to 1.67%.

The delinquency rate of accounts 60 to 89 days past due increased to 1.01%.

Accounts 90 to 180 days past due rose to 0.63%.

How to Get Out of Credit Card Debt and Improve Your Credit

Credit card debt in America is something many individuals struggle with, and when your debt isn’t under control, it can affect your credit. A lower credit score leads to higher interest rates, which means you’re paying more for your purchases. It can also lead to being denied new credit lines.

Here are some simple steps you can take to start getting out of debt sooner rather than later:

Reduce additional credit card spending: You don’t want to add to your current debt if you don’t have to.

Create a budget: Cutting your spending can help you save additional funds to pay down your debt.

Use the snowball method: Each month, pay off your smallest debt in full. This can help you build momentum as you chip away at your overall debt.

Try debt consolidation: Consolidating your debt may help reduce the interest rate and keep your debt in one place rather than with different creditors.

Get a balance transfer card: Balance transfer cards allow you to transfer credit card debt to a different account, which may have a lower interest rate and will also help you consolidate your debt.

If you need help getting your debt under control and improving your credit, Credit.com has resources to help you learn to better manage your finances. To begin managing your credit, sign up for a free credit report card and check out ExtraCredit®. Our services can help you learn how to work on your credit and educate you about managing your finances so you know how to work toward the life you want.

Methodology for Credit.com data: This survey was conducted for Credit.com using Suzy. The sample consisted of a total of 1,154 responses per question and is statistically representative of the general population. This survey was conducted in December 2022.

Is your poor credit history preventing you from obtaining your financial goals, such as getting a credit card, buying a car, or purchasing a home? If so, there are steps you can take right now to improve your credit score in as little as three months.

This article provides actionable steps you can take today to start on the path to rebuilding your credit.

In This Piece

How Quickly Can You Improve Your Credit?

The exact amount of time it can take to repair your credit score depends on several factors, such as your current credit score, the amount of debt you owe, your ability to repay your debt, and your overall credit history.

Despite this, you can start making improvements in as little as three months. Below is a look at five things you can do to improve your credit score, along with tips to keep in mind.

1. Pay Off the Debt You Can

Start by paying off as much debt as possible. There are several strategies you can use to pay down your debt, including the debt avalanche method, the snowball method, and a debt consolidation loan. No matter which method you use, the faster you can pay down some of your debt, the sooner your credit can start to improve.

Keep in mind that it could take your creditors up to 30 days to report payments to the credit bureaus and another 30 days for the credit bureaus to post these payments to your account.

2. Minimize Your Credit Utilization

Your credit utilization ratio accounts for up to 30% of your overall credit score. This ratio compares the amount of credit you have available with the amount of credit you’ve used. It’s recommended to keep this ratio below 30%. If you’re having trouble hitting this number, here are some things you can do.

Ask for a Higher Credit Limit

If your credit utilization ratio is above 30%, you can ask your credit card company to increase your credit card limit. This strategy will increase the amount of credit you have available, which can help lower your credit utilization ratio.

Use as Little Credit as Possible

Instead of using your credit card to make multiple or large purchases, consider using another method to pay. The less you have charged to your credit card, the better your credit utilization ratio will be.

Taking these steps to decrease your credit utilization rate could start to improve your credit in as little as 60 days.

3. Keep an Eye on Your Credit Report

According to a recent study, 34% of Americans found at least one mistake on their credit report. Just one credit card error could damage your credit score. This is why it’s so important to keep an eye on your credit report.

You can request a free credit report from all three major credit reporting agencies, Experian, Equifax, and TransUnion, at annualcreditreport.com. Obtaining your credit report is just the first step; you also want to perform the following tasks.

Check Your Report for Errors

Carefully review your credit report to make sure all the information listed is correct, including your personal information and account details. Make a list of any incorrect information and any accounts or personal information that’s missing.

Dispute Inaccurate Information

The best way to remove incorrect information on your credit report is to file a dispute with the credit reporting agency. Write a dispute letter that clearly explains what inaccurate information is listed on your credit report and why it’s incorrect. Submit this letter, along with any supporting documents, to the credit bureaus listing the error.

Typically, the credit reporting agencies have up to 30 days to investigate your dispute and another 5 days to let you know their decision.

Ask if Lenders Will Remove Paid-Off Items From Your Report

Many lenders report past-due accounts to credit reporting agencies to entice customers to pay their debts. Once you pay your debt off, the lender may be willing to remove this debt from your credit report. Contact your lender directly to make this request.

It could take days, weeks, or months to receive a clear answer from your lender. If they do agree to remove this debt, it could take up to 60 days to reflect on your credit report.

How to Add Your Utility Bills to Your Credit Report

Typically, utility companies don’t report on-time payments to the credit bureaus. You can, however, work with a reporting service company, such as Credit.com’s ExtraCredit service, to make sure these payments along with your rent payments are listed on your credit report. This step can help prove you have a strong payment history.

Once you sign up for a credit reporting service, you can expect to see these payments on your credit report within 60 days.

4. Consider Applying for a New Line of Credit

Having a mix of different types of credit accounts, such as revolving credit accounts and fixed-payment accounts, makes up to 10% of your credit score. If you want to boost your credit score, it’s important to have a nice mix of different accounts. Below is a look at some types of credit accounts you may qualify for even if you don’t have good credit.

Are Credit Builder Loans Right for You?

As the name suggests, credit builder loans are designed to help you build credit. This type of loan is different from traditional loans, as you don’t have access to the money until you make all your payments. Obtaining a credit builder loan can be a great way to save money while building your credit because these lenders often report loan payments to the credit bureaus.

Types of Credit to Consider

If you can’t obtain a traditional credit card, there are other options, such as:

Secured credit card. With a secured credit card, you’ll be required to put down a cash security deposit prior to obtaining your card. Otherwise, these credit cards work just like traditional cards and can help you build your credit.

Authorized user. If you can’t obtain your own credit card, you can ask a friend or family member to add you as an authorized user to their account. If the credit card company reports your authorized user status, it can help build your credit.

Tips for Applying for New Credit

While maintaining a mix of credit accounts can help you build your credit, you want to make sure you don’t open too many new accounts too quickly. This action could damage your credit score due to excessive credit inquiries. Instead, take it slow and gradually open a mix of accounts.

Opening just two different types of credit accounts, such as a car loan and a credit card, can impact your credit as soon as they’re reported on your credit report.

5. Keep on Top of Your Finances

Keeping on top of your finances is a very important building block in your credit foundation. Start by building a budget and sticking to it. This step can make sure you don’t overspend, help you start to save money, and learn to be more conscious of how you’re spending your money on credit.

What to Do if You Don’t Have Credit

If you currently have little to no credit, you may be wondering how you can build credit in just a few months. Taking some of the steps above, such as working with a reporting service company, obtaining a secured credit card, or becoming an authorized user, can help you build credit as soon as they are reported.

Knowing how to raise a credit score in three months is just the first step. Now, it’s time to take action.

One of the key factors that determine your credit score is your credit utilization ratio. In fact, this ratio accounts for as much as 30% of your credit score. With this much influence on your credit score, it’s important to understand what credit utilization is, how to calculate it, and how it impacts your finances.

This article delves deeper into the answers to these questions. It also provides valuable tips for improving your credit utilization ratio.

In This Piece

What Is Credit Utilization?

In the most basic terms, your credit utilization is the amount of debt you owe in comparison to your overall credit limit. Only revolving credit is used when determining credit utilization. Things like mortgage loans, car loans, and student loans aren’t included.

What Is Revolving Credit?

Revolving credit is any type of credit account that continuously renews as you pay off the debt connected to that account. Some prime examples of revolving credit include credit card accounts and home equity lines of credit.

How to Calculate Credit Utilization

You can easily calculate your credit utilization ratio using a credit utilization calculator or the following formula.

Start by adding up all your revolving credit account balances.

Next, you need to add together the credit limit amounts for each of these accounts.

With this information, you can calculate your credit utilization ratio by dividing your total account balances by the total credit limits and multiplying this total by 100.

Credit utilization ratio formula:(Total amount of revolving credit account balances / Total credit account limits) x 100

How Balance Reporting Affects Credit Utilization

While credit card companies are under no obligation to report your credit information to the credit report agencies, almost all of them do. In fact, most credit cards submit your credit information every billing cycle. This means your credit card company will likely update your credit card balance every 25–30 days or so.

This frequent reporting affects your credit score because the amount of credit you have available versus your credit balances impacts your credit utilization ratio. Depending on your spending and repayment habits, credit card balance reporting could cause your credit score to change from month to month.

Understanding Per-Card vs. Overall Utilization

It’s important to understand the difference between overall credit and per-card utilization. Your overall credit card utilization combines all your revolving credit accounts into one ratio. Your per-card utilization only takes into account one card at a time. For per-card utilization, you can use a credit card utilization calculator or the formula listed above, but instead of adding all your account balances together, you calculate each card separately.

Most experts recommend keeping your overall credit utilization score under 30%. However, some creditors look at revolving accounts separately. It’s a good idea to spread your revolving credit across multiple accounts rather than just one or two credit accounts. This keeps the credit utilization from getting too high on any one card.

There are also two other utilization numbers that could be helpful to know:

Line-item utilization measures your individual credit card balances against your individual limits. For example, suppose you have three credit cards, each with a $10,000 limit. Based on your current balances, your line-item utilizations break down like this:

Card A: Balance of $4,500 / Credit limit of $10,000 = 0.45 × 100 = 45% utilization

Card B: Balance of $2,000 / Credit limit of $10,000 = 0.20 × 100 = 20% utilization

Card C: Balance of $3,300 / Credit limit of $10,000 = 0.33 × 100 = 33% utilization

Aggregate utilization is the average of your credit card utilizations. Calculate yours by combining your current balances and dividing them by your total credit limit. In the example above, your total balance is $9,800 and your total limit is $30,000; therefore, your aggregate credit utilization is $9,800 / $30,000 = 0.32 × 100 = 32.6%

Why Is Credit Utilization So Important?

Every factor of credit scoring is crucial, but credit utilization is responsible for 30% of your overall score, second only to your payment history’s weight of 35%. Credit utilization measures your revolving balances against your total credit limit.

Lenders and credit card issuers rely on credit utilization to predict risk and future behavior. In general, the higher your utilization ratio, the greater your risk of defaulting on your balances. Risky behavior isn’t rewarded in the world of credit scoring, and you may see a decrease in your scores as your utilization ratio goes up.

How Does Credit Utilization Affect Your Credit?

Your credit utilization ratio directly impacts your credit score. In fact, five primary factors influence your score for FICO and VantageScore, the two most common credit scoring companies used.

The Five Credit Factors

Payment history: Your payment history, including both on-time and late payments. FICO: 35% of your credit score VantageScore: 41% of your credit score

Credit utilization: The amount of debt you have compared the amount of your current available credit balance accounts. FICO: 30% of your credit score VantageScore: 34% of your credit score. This includes credit utilization, outstanding balances, and available credit.

Age of credit history: The length of time you’ve held each credit account. FICO: 15% of your credit score VantageScore: N/A

Account mix: The different types of accounts you have. You should have a variety of accounts, including installment loans and revolving credit accounts. FICO: 10% of your credit score VantageScore: 20% of your credit score

New credit inquiries that impact your credit score. Work at building your credit slowly to reduce the risk of too many hard inquiries to your account over a short period of time. FICO: 10% of your credit score VantageScore: 11% of your credit score

What Is a Good Credit Utilization Ratio?

Experts agree that you should try to keep your credit utilization ratio under 30% if possible. When it comes to revolving credit, you may also want to keep your credit utilization ratio under 30% for each account you have.

How to Improve Your Credit Utilization

If your credit utilization is higher than the recommended ratio of 30%, you can take several steps to improve your rate.

1. Check Your Credit Reports for Accuracy

It can’t be stressed enough how important it is to check your credit reports for accuracy. You’re entitled to one free credit report from each of the major credit reporting agencies every year. If you haven’t requested your credit reports within the last 12 months, do so today.

Once you receive your credit reports, make sure your personal and financial information is correct and up to date. If you notice any errors, take the necessary steps to file a dispute with each credit bureau reporting the error.

2. Pay Down Your Balances

Another step you can take to lower your credit utilization ratio is to pay off some of your debt. There are several methods you can use to pay off your debt, including a debt consolidation loan, the avalanche method, and the snowball method. The more debt you can pay off, the bigger impact it will have on your credit utilization ratio.

3. Request a Credit Increase

Requesting a credit limit increase on one or more of your revolving credit accounts can also help to improve your credit utilization. Keep in mind that this strategy only works if you also limit spending on these accounts. If you use these increased credit limits to make more purchases, it could actually increase your credit utilization ratio.

4. Consider Balance Transfer Cards

Another option for lowering your credit utilization ratio is to open a balance transfer card. Many of these cards offer a 0% introductory interest rate. Transferring your balances to this new card won’t decrease your credit utilization. But it can help reduce your interest costs and keep your utilization rates from increasing each month. This can also help you pay down your debt more quickly.

5. Change Your Bills’ Due Dates

If you’re having trouble making your credit card payments on time, you can request to have your due date changed. For example, if you get paid on the 1st and 15th of each month, you may want to move your due date closer to the 20th.

This step ensures you’ll have enough money to make these payments. Making your due date closer to your payday can also encourage you to pay off more of your balance before you have time to spend your money on other things.

Does Opening Credit Cards Improve Your Credit Utilization?

Opening a new credit account can help to improve your credit utilization ratio by increasing the amount of credit you have available. However, if you use this card to make more purchases and can’t pay the balance off each month, it can actually hurt your credit utilization ratio. The exception is if you open a new balance transfer credit card account to get better interest rates. This transfer strategy won’t increase your credit balance, but it may help you pay down your debt faster.

Keep in mind, however, that opening new lines of credit can also negatively impact your credit score by creating more hard inquiries on your credit report.

Does Closing Credit Cards Improve Your Credit Utilization?

Unless you absolutely need to, it’s not recommended to close your credit card. First, closing your credit card can lower the amount of credit you have available. Secondly, you could lose the history attached to the card.

The age of your credit history represents up to 15% of your overall credit score for FICO. So, keeping an account open, even if you have a very low balance on it, can help to improve both your credit utilization and your credit score.

Sign up for Credit.com’s ExtraCredit today to access FICO scores, reports from all three major credit report agencies, and more.

According to reports from the second quarter of 2022, the total of all household debt in the United States is a whopping $16.15 trillion. Mortgages make up the bulk of that debt, with student loan, auto loan and credit card debt trailing behind.

On average, adults in the United States carry debt loads ranging between $20,800 and $146,200. If you’re in debt and looking for a way to pay it off, making a plan is a critical step. Find out more about how to get out of debt below.

1. Collect All Your Paperwork in One Place

Before you can get out of debt, you need to know how much debt you actually have. You should also know who you owe and what the terms are, as this can help you prioritize debt payments to pay them off faster.

Start by collecting all your debt paperwork in one place and creating a master list of everything you owe. You can do this in a spreadsheet or with a pen and paper. Information to gather includes:

Statements for all your debts. One way to do this is to spend a month saving all your financial mail and email so you have a comprehensive picture of your debt.

Regular bills that aren’t debts. Your cell phone and utility bills, as well as your rent, should all be included when you gather this financial information. Information about income. Look at paycheck stubs or your bank accounts so you know what, on average, you can expect in income each month.

Your credit reports. Get your free credit reports at AnnualCreditReport.com to ensure you know about all the debt you owe.

Tip: Sign up for ExtraCredit to see your credit reports and 28 FICO® scores in one place.

2. Create a Budget and Determine What You Can Pay Every Month

Using the information you gathered in the above step, create a monthly budget. Make sure you cover all your bills and minimum debt payments. When possible, include an amount that can go toward building your savings. Allocate funds for essentials, such as groceries and gas.

Once you cover all the needs for the month, figure out how much money you have left. How much of that can you put toward extra debt payments so you can start getting ahead on debt?

3. Manage Your Debts in Collections

If you see that you have any debts in collections when you pull your credit reports, make sure you have a plan for taking care of them. Collection accounts have a serious negative impact on your credit score. Creditors may also sue you and try to collect on these accounts via wage garnishments or bank levies if you don’t take action to manage collections. That can throw a huge wrench into your plan for getting out of debt.

Tip: If you don’t enjoy manual calculations, check out Tally. You can use Tally to total up your expenses, pay down credit card bills, and generally figure out where you stand.

4. Consider Your Options

There are two main approaches to paying off debt as quickly as possible: the snowball method and the avalanche method.

The snowball method involves paying off accounts with the lowest balances first. You take any extra money you have—even if it’s just $50—and add it to your regular minimum monthly payment on that small balance. When that balance is paid off, you take the extra $50 plus the minimum payment and add it to the next biggest balance. You keep doing this as you work your way up to larger balances, paying your debt off faster and faster.

With the avalanche method, you tackle accounts according to interest rates. You start by paying off accounts with the highest interest rates first. The thought behind this method is that you save money in the long run by tackling high-interest debt first.

5. Try to Reduce Your Interest Rates

Interest refers to how much your debt costs. If you have a lower interest rate, your debt costs less and you can pay it off faster. Here are some ways you can try to reduce interest rates on your debts:

Ask for a lower interest rate. If you’re a credit card account holder in good standing and your credit history and score has improved since you got the card, you may be able to get a better rate. Call customer service for your card and let them know you are looking for a better deal. They may agree to lower the rate to keep you as a cardholder.

Look into debt consolidation or refinancing. A debt consolidation loan provides funds you can use to pay off higher-interest debts. Refinancing occurs when you get a new loan for a home or car. If you had lackluster credit when you got your auto loan, for example, you may be able to refinance it for a lower rate if your credit has improved.

Get a balance transfer credit card. You may be able to transfer balances from a credit card with a high interest rate to one that has an introductory low APR offer. This may allow you to pay off the debt over the course of 12 to 22 months without incurring any more interest expense.

Upgrade Triple Cash Rewards Visa®

$200 bonus after opening a Rewards Checking Plus account and making 3 debit card transactions*

Unlimited cash back on payments: 3% on Home, Auto, and Health categories and 1% on everything else after you make payments on your purchases

No annual fee

Combine the flexibility of a credit card with the predictability of a personal loan

No touch payments with contactless technology built in

See if you qualify in minutes without hurting your credit score

Great for large purchases with predictable payments you can budget for

Mobile app to access your account anytime, anywhere

Enjoy peace of mind with $0 Fraud liability

*To qualify for the welcome bonus, you must open and fund a new Rewards Checking Plus account through Upgrade and make 3 qualifying debit card transactions from your Rewards Checking Plus account within 60 days of the date the Rewards Checking Plus account is opened. If you have previously opened a checking account through Upgrade or do not open a Rewards Checking Plus account as part of this application process, you are not eligible for this welcome bonus offer. Your Upgrade Card and Rewards Checking Plus account must be open and in good standing to receive a bonus. To qualify, debit card transactions must have settled and exclude ATM transactions. Please refer to the applicable Upgrade VISA® Debit Card Agreement and Disclosures for more information. Welcome bonus offers cannot be combined, substituted, or applied retroactively. The bonus will be applied to your Rewards Checking Plus account as a one-time payout credit within 60 days after meeting the conditions.

Do Your Best to Pay More Than the Minimum

Only paying the minimum on high-interest debt, such as credit card debt, doesn’t get you out of debt fast. It can take years—dozens of them—to pay off credit card balances if you’re only making minimum payments.

Instead, put more than the minimum on your debt whenever possible. You may also want to put any additional funds you receive—such as a tax refund—on your debt to help with this process.

Consider More Options for Getting Out of Debt

Creating a budget, managing your money wisely, and making extra payments toward your debt all help you get out of debt. Here are some other ways you can deal with debt:

Increase your income while cutting unnecessary spending. Join the gig economy with a side job to earn extra money, or sell things you don’t need via online marketplaces.

Undergo credit education and counseling. These services can help you make the most of your monthly budget.

Engage in debt settlement. You may be able to negotiate with creditors, especially for accounts in collections, to settle debts for less than you owe. Just make sure you understand any effects on your credit.

Enter a debt management plan. During such a plan, you make a single payment to a trustee. They use those funds to pay your debts, hopefully in a way that gets you out of debt faster. Declare bankruptcy. If you find you’re unable to pay your debts, much less make extra payments, you may need another option. Chapter 7 and Chapter 13 bankruptcy are potential considerations.

How to Avoid Getting into Debt

Paying off debt doesn’t have to be impossible, but it can be challenging. For many people, it requires altering years’ worth of financial habits. If you’re not already in debt, it may be easier to stay out of it. Create a budget and stick to it, spend wisely and avoid using credit cards for things you don’t need or can’t afford to buy with cash.

Flight delays can be unpredictable, but it’s also possible for a delayed flight to suddenly become available. The flight could get back on schedule — and if you’re not there, it may leave without you.

That’s why you shouldn’t usually stray too far from your gate.

Now this doesn’t mean you can’t retreat to an airport lounge or grab a drink at the airport bar, particularly if you’re faced with a multihour wait. But if you do leave the boarding area, pay close attention so you’re not left behind should your flight get back on schedule.

Here’s what to do when your flight is delayed, and how you can still escape a potentially crowded boarding area without missing your flight when it finally happens.

Why flight delays happen — and how they can get un-delayed

In the first four months of 2023, only 76.58% of U.S. flights arrived on time, according to Bureau of Transportation Statistics data. The most common cause of delays in that period was the inbound aircraft arriving late, affecting 7.6% of all flights. In short, an issue with an earlier flight can lead to a snowball of flight delays.

The second-most common reason was air carrier issues (which impacted 7.1% of flights in that period). That includes maintenance or crew problems, aircraft cleaning, baggage loading and fueling.

That said, airlines want to depart as close to the originally scheduled departure time as possible. Even though U.S. airlines aren’t required to compensate passengers for delays like they do in the European Union, airlines still lose money. According to the Federal Aviation Administration’s Office of Aviation Policy and Plans, delays cost airlines a combined $8.3 billion in increased expenses in 2019 to cover costs like overtime crew wages.

Given that, airlines are incentivized to get back on schedule. An aircraft experiencing technical issues might initially trigger an alert that the flight has been delayed. But if the airline has another aircraft on standby, then the flight could get back on schedule as originally intended.

When airlines seize such an opportunity, it’s generally a win-win, as the airline gets back on schedule and passengers arrive on time. However, it can end up disrupting passengers who didn’t realize their flight got back on schedule, particularly if they aren’t even at the airport because they intended to wait it out at home or at their hotel.

But there are ways to find out the status of your flight and stay alerted should that delay get un-delayed.

How to find out why a flight is delayed

Your first task is to find out why the flight is delayed. Something like a shortage of available gates might be solved fairly quickly if the airport can reshuffle idle aircraft and make space for boarding.

Meanwhile, a delay due to a massive storm likely means no flights can take off.

The FAA’s National Airspace System Status page displays delays at certain airports.

Use the FAA’s flight delay website, which displays airport-wide delays impacting major U.S. airports in real time, to better estimate how long you’ll have to wait. Sometimes the FAA’s website provides its own estimates of delay durations, though note that those are exactly that — just estimates.

If you’re at the airport already, you might also just ask the gate agent.

Keep tabs on your delayed flight with the right tools

U.S. airlines are legally required to provide passengers with flight status changes within 30 minutes of being made aware of the status change. While the DOT requires that information be posted on the airline’s website and through the airline’s telephone reservation system, most airlines make it even easier by sending you flight alerts by email, smartphone app or text message.

The United Airlines website provides updated schedules and also displays the reason for the delay.

When booking your flight, provide contact information and opt in to alerts if you want the airline to message you with updates (you can also typically add your contact information after booking). Download the airline’s app, connect it to your reservation and subscribe to push notifications if you want real-time updates about your flight status.

Third–party tools can also help you keep tabs on your flight — sometimes even better than the airline itself. For example, FlightAware amalgamates real-time flight tracking, airport information and weather data into a user-friendly interface that lets you track your flight status. It offers notifications and visualizations of the flight’s progress on a live map. A FlightAware tool called “Where is my plane now?” shows the location of the aircraft, which can give you an idea of the delay’s length, assuming the issue has to do with the inbound aircraft arriving late.

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are our picks for the best travel credit cards of 2023, including those best for:

After more than 2 weeks of relentless selling that took yields to their highest levels since 2007, bonds have increasingly been sitting on dry powder–at least from a technical standpoint. Today’s PMI data provided the spark. The explosion of bond buying began in Europe where PMIs were much weaker across the board in the services sector. US numbers weren’t as bad by comparison, but far enough below consensus to greenlight the rally. Interestingly, and perhaps importantly, the rally didn’t let up ahead of the 20yr Treasury auction, but the auction was decent nonetheless. This increases the temptation to conclude “the top is in” for rates, but that top is only as good as the forthcoming data is bad. We also need to see if Powell has anything interesting to say on Friday (or at least if enough of the market was waiting on Jackson Hole before making even bigger moves).

S&P Global PMI

Services: 51.0 vs 52.2 f’cast, 52.3 prev

Manufacturing: 47.0 vs 49.3 f’cast, 49.0 prev

09:33 AM

Big gains on EU PMI data. 10yr down 9bps at 4.24 and MBS up nearly half a point.

12:58 PM

Sideways at stronger levels, despite some volatility in MBS due to illiquidity. UMBS up half a point and 10yr yields down 12.4bps at 4.208

03:59 PM

10yr down 15bps at lows of the day, 4.184. MBS up 18 ticks (.56).

Download our mobile app to get alerts for MBS Commentary and streaming MBS and Treasury prices.