It’s a common misconception that all debt is bad. Some forms of debt—such as student loans, mortgages, and auto loans—can help you improve your professional and personal life. But while debt can be useful, overspending while already in debt can lead to an unmanageable situation.

To find tips to ensure you aren’t adding unnecessarily to your debt or falling behind on payments, we asked Bob G. Wood—a professor of finance at the University of South Alabama’s Mitchell College of Business—to share his top debt-crushing strategies. These tips and ideas can help you gain lasting financial freedom.

Keep reading to learn how to get out of debt and stay there.

1. Avoid increasing what you owe on your credit cards

One of the first steps to getting out of debt is to stop adding to it. While credit cards are a helpful payment option (especially for unplanned expenses), continually building up a card balance that you can’t pay off every month can negatively impact your debt load and your credit score.

“A debt-averse individual pays the total balance on each credit card before the payment due date to avoid interest charges and late fees,” Wood explains. “This approach helps people avoid using the cards to buy things they cannot afford.”

2. Put some investments on hold

If you’re struggling to figure out how to pay off debt, you may want to put discretionary investments on hold until you’re debt-free. (Think: that $100 in crypto your buddy suggests you buy, or the IPO you’ve been reading about.) In some cases, paying off your debt faster will save you more money than your investments can earn. According to Wood, the exception to this rule is investing as a part of your retirement savings strategy, such as in a 401(k).

“I recommend continuing to fund retirement account investments, especially for those individuals with employer-provided accounts,” Wood says. “Many of these accounts provide a match for individual investments into the account, and that provides a 100% return on the individual’s contribution. Also, delaying retirement investment contributions can drastically reduce the future value of the account.”

3. Commit to a plan

While putting extra cash toward debt payments can help you make progress, having a steady plan is necessary to tackle debt efficiently. Wood shared the following steps consumers need to take when they’re budgeting to pay off debt:

Step 1. Differentiate between your needs and wants, and review your current expenses. “Be honest—upgrading to the latest cell phone model or adding items to an already full closet are more than likely wants rather than needs,” Wood says.

Step 2. Develop a realistic budget. Not sure how to budget to pay off debt? Be thoughtful when you create a budget to help keep your spending in check. This new budget should include a fixed monthly amount for debt repayment, beyond any monthly payments for student, auto, or home loans.

4. Choose the ‘snowball’ or the ‘avalanche’ style of debt reduction

When creating a plan to tackle your debt, you may consider the popular “debt snowball method,” which targets the smallest debt first. As soon as this first debt is satisfied, you focus on the next-lowest balance.

While seeing a debt of any size reduced to zero can be incredibly motivating, this approach may come with a cost. “Unfortunately, the strategy often results in more interest paid by the borrower,” Wood explains.

“As an alternative, the ‘debt avalanche method’ targets the highest interest debt first,” Wood explains. “By paying off the debt with the highest interest first, the borrower reduces the total amount of interest paid. Although this approach is more financially sound, it requires the borrower to focus on the long-term result and remain diligent in their payment plan.”

Note that with either of these approaches, staying current on all debt payments is important, meaning that you should pay at least the minimum amount due, while dedicating any extra contributions to the targeted debt.

5. Try to renegotiate your debt

One of the ways to pay off debt is to renegotiate it. While there are no guarantees that a lender will agree to negotiate the terms of your debt, you may have more luck if you’re a long-term customer with a history of on-time payments. In this case, a lender may be willing to waive fees, shift due dates, or even lower the interest rate. And these actions should not affect the individual’s credit rating, Wood notes.

Before committing to an arrangement, you should seek guidance from a professional about your specific situation, needs, and goals.

6. (Carefully) consider a balance transfer vs. debt consolidation loan

Transferring credit card debt to a new account has advantages, as many transfer offers may have an introductory period with an interest rate of 0%. A balance transfer can also reduce multiple payments to one, with a single payment date.

But keep an eye on your calendar so you’re aware of when the introductory period ends and the new interest rate begins.

He explains that debt consolidation is similar in concept, but these balances are typically rolled over into a personal loan for debt consolidation, a home equity loan, or a credit card with a lower interest rate (and concurrent lower payment).

7. Consider a rewards checking account

Looking to make the most of the cash you aren’t spending but still need access to? This is where a rewards checking account such as the Discover® Cashback Debit account can be handy when considering how to budget to pay off debt.

Earn cash back with your debit card

Discover Bank, Member FDIC

A rewards checking account can assist consumers in managing their debt by offering perks such as cash back or interest rewards on certain transactions. Consumers can then take those earnings and put them toward debt payments as needed.

8. Make it a family affair

Borrowing money from a trusted family member can help you save a lot on interest, making it easier to get out of debt faster. Let’s say that loved ones lend you the money you need to pay off your high-interest debts in full. You can then focus on paying them back at a lower interest rate or with no interest at all—whatever you agree on.

Just ensure you and your loved ones are on the same page about what this repayment agreement will look like so you don’t strain any relationships.

9. Know when to seek professional help

There may come a point when you need to hire a professional to help with get out of debt planning. “An individual should seek debt counseling when the anxiety associated with the debt interferes with the person’s personal and professional life or when the minimum debt payments are not possible without sacrificing necessities,” Wood says.

“There are both for-profit firms and nonprofit counseling agencies available to help an individual through the process.” The Consumer Financial Protection Bureau offers advice and resources on how to select a reputable counselor.

Consider what strategies might work best for you

There are many different approaches you can implement to help you get debt-free faster. Take some time to devise a realistic plan to tackle your debt so you can pay it off for good and start making your money work for you.

When you’re paying off debt, every boost of extra cash can help. A Discover Cashback Debit Account can help you earn cash rewards on debit card purchases1 with no account fees.

Articles may contain information from third parties. The inclusion of such information does not imply an affiliation with the bank or bank sponsorship, endorsement, or verification regarding the third party or information.

1 On up to $3,000 in debit card purchases each month. See Deposit Account Agreement for details on transaction eligibility, limitations and terms.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

The average household credit card debt in America is $9,654, and the states with the largest amount of credit card debt are Alaska, Hawaii, and New Jersey.

Between the first quarters of 2022 and 2023, The Federal Reserve Bank of New York reported that the credit card debt in America rose by $145 billion. As of June 2023, we saw a 12-month inflation increase of 3%, the smallest year-over-year increase since March 2021.

By understanding American credit card debt statistics, you’ll better understand where you stand and what you can do to potentially lower your debt. Credit card debt increases your credit utilization ratio, which can hurt your credit and ultimately cost you more money in interest.

We surveyed over 1,100 Americans to learn more about credit card debt statistics in the United States. This data covers the average debt by state, average interest rates, and more. While many of the statistics from our other sources look at the situation as a whole, our data helps us see what’s happening on an individual level.

Despite the national average of Americans having over $9,000 in credit card debt per household, only 14% say they’re “very worried” about their debt.

67% of respondents said they have less than $2,000 in debt, which may indicate that only a concentrated number of people have high amounts of credit card debt.

20% of respondents don’t know how long they’ve been in debt.

The majority of respondents (56%) say their credit card debt is due to unexpected expenses.

74% of respondents said at least one collection agency has contacted them about a past due debt.

In this article, we’ll also provide tips on how to get out of debt and work toward better credit.

Table of contents:

Key Credit Card Debt Statistics

Many factors play into credit card debt, such as the average interest rates, which cards have the best offers, and the balance people carry on their card. These statistics will help you compare your own credit card balance to the national average and see if you’re getting a good deal with your current cards.

Here are the standout findings of various debt statistics:

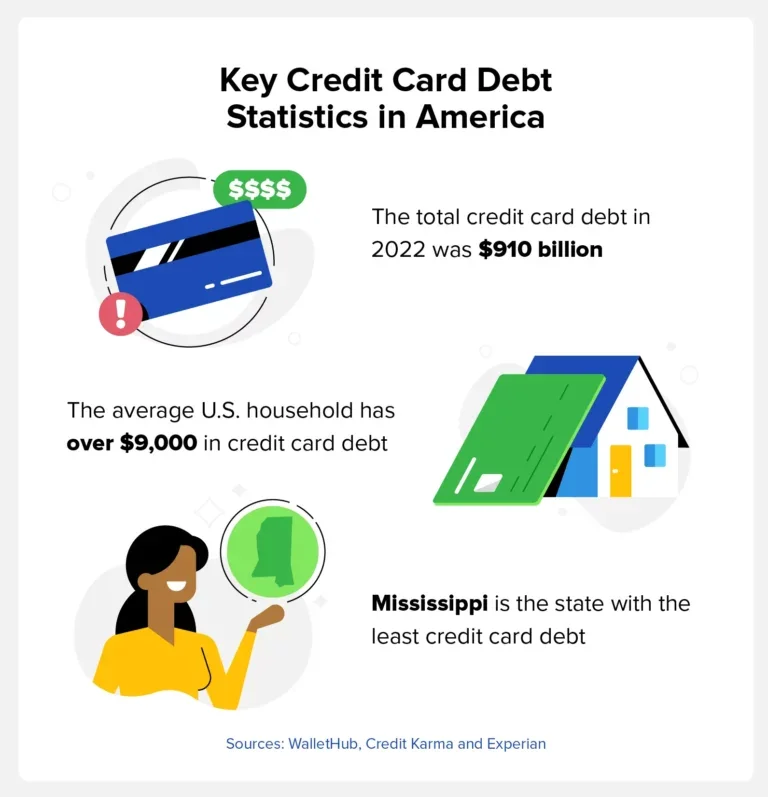

The average American household has over $9,000 in credit card debt. (WalletHub)

Mississippi has the least credit card debt at $5,259 per person. (Credit Karma)

Alaska has the most credit card debt on average at $8,139. (Credit Karma)

Credit cards 90 days or more past due rose to 4.57% in 2023. (FRBNY)

Individuals making $184,000 or more per year have the most credit card debt at an average of $12,600. (Federal Reserve)

The total credit card debt in America as of Q3 2022 was $910 billion. (Experian®)

How Many Credit Cards Carry a Balance

The American Bankers Association releases a quarterly report for consumer credit conditions, and the most recent data comes from the third quarter of 2022.

In America, approximately 43% of credit cards carried a balance, 23% were dormant, and 34% were used but paid off each month. Those who pay off their credit card balance are able to keep a low credit utilization ratio and prevent the accumulation of debt.

Tip: Use our credit card payoff calculator to estimate when you’ll be debt free.

Average Interest Rates for New Credit Card Offers

LendingTree analyzed the terms and conditions of 200 credit cards from upwards of 50 different credit card companies, banks, and credit unions. With this data, they were able to gather an assortment of information involving annual percentage rates (APR).

The APR is the amount of interest consumers pay for their purchases, and the following table is broken down by credit card type.

The following table is based on data from July 2023.

Average Credit Card Debt by State

In February 2023, Credit Karma gathered data from 74 million of their members to see which states had the most and least amount of credit card debt. Below, we’ve compiled a complete list based on Credit Karma’s data that contains the average credit card debt for each of the 50 states alphabetically.

Top 10 States With the Most Credit Card Debt

The following states had the most credit card debt, with Alaska having the highest average credit card debt in America at $8,139 per person.

State

Average credit card debt

1.

Alaska

$8,139

2.

Hawaii

$7,444

3.

New Jersey

$7,306

4.

Maryland

$7,248

5.

Virginia

$7,174

6.

Connecticut

$7,032

7.

New York

$7,029

8.

California

$6,952

9.

Washington

$6,869

10.

Florida

$6,783

Top 10 States With the Least Credit Card Debt

The major credit bureau, Experian, tracks credit card debt data as well and found that between 2021 and 2022, overall credit card debt in the U.S. increased from $785 billion to $910 billion—a 16% increase. The average debt also increased in many states, according to Credit Karma’s report.

State

Average credit card debt

1.

Mississippi

$5,259

2.

Kentucky

$5,455

3.

Wisconsin

$5,593

4.

Arkansas

$5,600

5.

Indiana

$5,601

6.

Alabama

$5,647

7.

West Virginia

$5,674

8.

Iowa

$5,732

9.

Idaho

$5,737

10.

Maine

$5,788

Average Credit Card Debt by Age

Credit Karma’s report with the state-by-state data also broke down credit card debt by age group. Currently, Generation X carries the most credit card debt, while Generation Z carries the least.

Age group

Average credit card debt

11-26 (Generation Z)

$2,781

27-42 (Millennials)

$5,898

41-58 (Generation X)

$8,266

59-77 (Baby Boomers)

$7,464

78-95 (Silent Generation)

$5,649

Average Credit Card Debt by Income

The following data comes from the Federal Reserve’s Survey of Consumer Finances (SCF) and was most recently updated in 2019. The Federal Reserve completed a new survey at the end of 2022 and will have updated data later in 2023.

As you’ll see, higher-income individuals have much more credit card debt than those who make less. This makes sense because high-income individuals are able to get much larger credit lines. But when you look at the debt-to-income ratio, lower-income households have much more consumer debt compared to the amount of money they make.

Percentile of Income

Average credit card debt

Less than 20%

$3,800

20%-39%

$4,700

40%-59%

$4,900

60%-79%

$7,000

80%-89%

$9,800

90%-100%

$12,600

Average Household Credit Card Debt

A recent study from WalletHub found that while total credit card debt in the United States rose 14.1% between 2022 and 2023, household credit card debt only rose by 8.39%.

Their data shows that the average household credit card debt at the end of the first quarter in 2023 was $9,654 adjusted for inflation, which is $738 higher than the same time the previous year. WalletHub’s chart goes back to 1986, and the highest household credit card debt was in 2007 when it was $12,221 on average per household.

Average Credit Card Debt by Race or Ethnicity

Research from Annuity.org shows that Black and Hispanic Americans are less likely to feel financially stable and less likely to have a bank account. This information can help us better understand what’s happening in the financial lives of different communities.

This data comes from the Federal Reserve’s 2019 SCF.

Race

Average credit card debt

White (non-Hispanic)

$6,940

Black or African American (non-Hispanic)

$3,940

Hispanic or Latino

$5,510

Other or multiple races

$6,320

Credit Card Delinquency Rates in America

When someone is at least 30 days past due on their credit card payment, their status becomes delinquent. The number of delinquencies in the United States can be a measure of people’s ability to pay down their credit card debt.

To track this data, Experian conducted a study between 2021 and 2022:

Accounts 30 to 59 days past due increased from 1.04% of total accounts to 1.67%.

The delinquency rate of accounts 60 to 89 days past due increased to 1.01%.

Accounts 90 to 180 days past due rose to 0.63%.

How to Get Out of Credit Card Debt and Improve Your Credit

Credit card debt in America is something many individuals struggle with, and when your debt isn’t under control, it can affect your credit. A lower credit score leads to higher interest rates, which means you’re paying more for your purchases. It can also lead to being denied new credit lines.

Here are some simple steps you can take to start getting out of debt sooner rather than later:

Reduce additional credit card spending: You don’t want to add to your current debt if you don’t have to.

Create a budget: Cutting your spending can help you save additional funds to pay down your debt.

Use the snowball method: Each month, pay off your smallest debt in full. This can help you build momentum as you chip away at your overall debt.

Try debt consolidation: Consolidating your debt may help reduce the interest rate and keep your debt in one place rather than with different creditors.

Get a balance transfer card: Balance transfer cards allow you to transfer credit card debt to a different account, which may have a lower interest rate and will also help you consolidate your debt.

If you need help getting your debt under control and improving your credit, Credit.com has resources to help you learn to better manage your finances. To begin managing your credit, sign up for a free credit report card and check out ExtraCredit®. Our services can help you learn how to work on your credit and educate you about managing your finances so you know how to work toward the life you want.

Methodology for Credit.com data: This survey was conducted for Credit.com using Suzy. The sample consisted of a total of 1,154 responses per question and is statistically representative of the general population. This survey was conducted in December 2022.

According to reports from the second quarter of 2022, the total of all household debt in the United States is a whopping $16.15 trillion. Mortgages make up the bulk of that debt, with student loan, auto loan and credit card debt trailing behind.

On average, adults in the United States carry debt loads ranging between $20,800 and $146,200. If you’re in debt and looking for a way to pay it off, making a plan is a critical step. Find out more about how to get out of debt below.

1. Collect All Your Paperwork in One Place

Before you can get out of debt, you need to know how much debt you actually have. You should also know who you owe and what the terms are, as this can help you prioritize debt payments to pay them off faster.

Start by collecting all your debt paperwork in one place and creating a master list of everything you owe. You can do this in a spreadsheet or with a pen and paper. Information to gather includes:

Statements for all your debts. One way to do this is to spend a month saving all your financial mail and email so you have a comprehensive picture of your debt.

Regular bills that aren’t debts. Your cell phone and utility bills, as well as your rent, should all be included when you gather this financial information. Information about income. Look at paycheck stubs or your bank accounts so you know what, on average, you can expect in income each month.

Your credit reports. Get your free credit reports at AnnualCreditReport.com to ensure you know about all the debt you owe.

Tip: Sign up for ExtraCredit to see your credit reports and 28 FICO® scores in one place.

2. Create a Budget and Determine What You Can Pay Every Month

Using the information you gathered in the above step, create a monthly budget. Make sure you cover all your bills and minimum debt payments. When possible, include an amount that can go toward building your savings. Allocate funds for essentials, such as groceries and gas.

Once you cover all the needs for the month, figure out how much money you have left. How much of that can you put toward extra debt payments so you can start getting ahead on debt?

3. Manage Your Debts in Collections

If you see that you have any debts in collections when you pull your credit reports, make sure you have a plan for taking care of them. Collection accounts have a serious negative impact on your credit score. Creditors may also sue you and try to collect on these accounts via wage garnishments or bank levies if you don’t take action to manage collections. That can throw a huge wrench into your plan for getting out of debt.

Tip: If you don’t enjoy manual calculations, check out Tally. You can use Tally to total up your expenses, pay down credit card bills, and generally figure out where you stand.

4. Consider Your Options

There are two main approaches to paying off debt as quickly as possible: the snowball method and the avalanche method.

The snowball method involves paying off accounts with the lowest balances first. You take any extra money you have—even if it’s just $50—and add it to your regular minimum monthly payment on that small balance. When that balance is paid off, you take the extra $50 plus the minimum payment and add it to the next biggest balance. You keep doing this as you work your way up to larger balances, paying your debt off faster and faster.

With the avalanche method, you tackle accounts according to interest rates. You start by paying off accounts with the highest interest rates first. The thought behind this method is that you save money in the long run by tackling high-interest debt first.

5. Try to Reduce Your Interest Rates

Interest refers to how much your debt costs. If you have a lower interest rate, your debt costs less and you can pay it off faster. Here are some ways you can try to reduce interest rates on your debts:

Ask for a lower interest rate. If you’re a credit card account holder in good standing and your credit history and score has improved since you got the card, you may be able to get a better rate. Call customer service for your card and let them know you are looking for a better deal. They may agree to lower the rate to keep you as a cardholder.

Look into debt consolidation or refinancing. A debt consolidation loan provides funds you can use to pay off higher-interest debts. Refinancing occurs when you get a new loan for a home or car. If you had lackluster credit when you got your auto loan, for example, you may be able to refinance it for a lower rate if your credit has improved.

Get a balance transfer credit card. You may be able to transfer balances from a credit card with a high interest rate to one that has an introductory low APR offer. This may allow you to pay off the debt over the course of 12 to 22 months without incurring any more interest expense.

Upgrade Triple Cash Rewards Visa®

$200 bonus after opening a Rewards Checking Plus account and making 3 debit card transactions*

Unlimited cash back on payments: 3% on Home, Auto, and Health categories and 1% on everything else after you make payments on your purchases

No annual fee

Combine the flexibility of a credit card with the predictability of a personal loan

No touch payments with contactless technology built in

See if you qualify in minutes without hurting your credit score

Great for large purchases with predictable payments you can budget for

Mobile app to access your account anytime, anywhere

Enjoy peace of mind with $0 Fraud liability

*To qualify for the welcome bonus, you must open and fund a new Rewards Checking Plus account through Upgrade and make 3 qualifying debit card transactions from your Rewards Checking Plus account within 60 days of the date the Rewards Checking Plus account is opened. If you have previously opened a checking account through Upgrade or do not open a Rewards Checking Plus account as part of this application process, you are not eligible for this welcome bonus offer. Your Upgrade Card and Rewards Checking Plus account must be open and in good standing to receive a bonus. To qualify, debit card transactions must have settled and exclude ATM transactions. Please refer to the applicable Upgrade VISA® Debit Card Agreement and Disclosures for more information. Welcome bonus offers cannot be combined, substituted, or applied retroactively. The bonus will be applied to your Rewards Checking Plus account as a one-time payout credit within 60 days after meeting the conditions.

Do Your Best to Pay More Than the Minimum

Only paying the minimum on high-interest debt, such as credit card debt, doesn’t get you out of debt fast. It can take years—dozens of them—to pay off credit card balances if you’re only making minimum payments.

Instead, put more than the minimum on your debt whenever possible. You may also want to put any additional funds you receive—such as a tax refund—on your debt to help with this process.

Consider More Options for Getting Out of Debt

Creating a budget, managing your money wisely, and making extra payments toward your debt all help you get out of debt. Here are some other ways you can deal with debt:

Increase your income while cutting unnecessary spending. Join the gig economy with a side job to earn extra money, or sell things you don’t need via online marketplaces.

Undergo credit education and counseling. These services can help you make the most of your monthly budget.

Engage in debt settlement. You may be able to negotiate with creditors, especially for accounts in collections, to settle debts for less than you owe. Just make sure you understand any effects on your credit.

Enter a debt management plan. During such a plan, you make a single payment to a trustee. They use those funds to pay your debts, hopefully in a way that gets you out of debt faster. Declare bankruptcy. If you find you’re unable to pay your debts, much less make extra payments, you may need another option. Chapter 7 and Chapter 13 bankruptcy are potential considerations.

How to Avoid Getting into Debt

Paying off debt doesn’t have to be impossible, but it can be challenging. For many people, it requires altering years’ worth of financial habits. If you’re not already in debt, it may be easier to stay out of it. Create a budget and stick to it, spend wisely and avoid using credit cards for things you don’t need or can’t afford to buy with cash.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

Are you struggling with debt and feeling overwhelmed? You might also be tired of hearing the same old tips that don’t help at all, like “Don’t buy coffee out” or “Just stop spending money.” Don’t worry — you’re not alone.

Many hardworking individuals like you face similar challenges. The good news is that there are effective strategies for paying off debt faster, even on a tight budget.

This guide will walk you through 10 practical and actionable steps that can significantly impact your journey to financial autonomy. Are you ready to better control your finances? Here is how to pay off debt fast with low income.

In This Piece:

Take Inventory of Your Debts

Create a Realistic Budget

Avoid Any New Debts

Try the Debt Avalanche Method

Consider the Debt Snowball Method

Increase Your Income

Negotiate a Better Rate

Increase Your Credit Score

Consider Debt Relief or Consolidation

Stay Consistent

Step 1: Take Inventory of Your Debts

Before tackling your debts, taking inventory of them is a crucial first step to clearly understanding what you owe, allowing you to understand the full extent of your financial obligations, and developing a comprehensive and more effective action plan.

Start by gathering all your financial statements and creating a comprehensive list of your debts. This includes credit card balances, student loans, medical bills, and other outstanding obligations.

You gain a complete picture of your economic landscape by documenting each debt, including the creditor, outstanding balance, interest rate, and minimum monthly payment. This knowledge empowers you to make informed decisions and prioritize debt repayment strategies.

Step 2: Create a Realistic Budget

A budget can help track your income and expenses, clearly showing where your money goes, but if you want a successful budget, it needs to be realistic.

Creating a realistic budget is essential to pay off debt fast with a low income. You can start by identifying areas to cut back on unnecessary expenses, like reducing discretionary spending, such as eating out. Look for creative ways to save money, such as using coupons, shopping sales, or negotiating lower bills. Though this is good advice, it might not be enough or as simple as it sounds.

Here are more steps and tips to help you create a budget that could work for you:

Track income and expenses: Start by calculating your total monthly income, including your salary, freelance earnings, or any other sources of income. Next, track your expenses for a month to understand where your money is going. Categorize your expenses into fixed costs (rent, utilities, etc.) and variable costs (groceries, entertainment, etc.).

Set attainable goals: Determine how much you can allocate toward monthly debt payments while covering your essential expenses. It’s crucial to set realistic goals that consider your income. Remember, even small monthly contributions can make a significant difference over time.

Prioritize debt repayment: Allocate a specific portion of your budget to debt repayment. Consider prioritizing your debts using the debt avalanche or snowball methods mentioned earlier. By focusing on one debt at a time while making minimum payments on the others, you can make steady progress and gain a sense of accomplishment.

Monitor and adjust: Regularly review your budget and track your progress. Adjust as needed to stay on track and meet your financial goals. Be flexible and willing to adapt your budget as your circumstances change.

Creating a realistic budget requires discipline and commitment, and it’s crucial to paying off debt. By understanding your income, tracking your expenses, and making intentional choices, you can take control of your financial situation.

Step 3: Avoid Any New Debts

It might sound obvious but avoiding new debts can help greatly. Avoid the temptation to rely on credit cards or take out additional loans. Instead, focus on living within your means and prioritizing your financial goals. Of course, implementing this step is easier said than done.

Here are some recommendations to help you avoid accumulating additional debt:

Change your mindset: Understand that taking on new debts will only prolong your journey to becoming debt-free. Embrace living within your means and making conscious choices to avoid unnecessary borrowing will help you pay off your debt faster.

Cultivate healthy financial habits: Practice mindful spending, distinguishing between needs and wants, and make conscious choices aligned with your financial goals.

Building an emergency fund: This is a crucial step to prevent relying on credit or loans during unexpected expenses or financial setbacks. Start by setting aside a small amount from your monthly income until you have a comfortable cushion to cover unforeseen emergencies.

Practice delayed gratification: Avoid impulsive purchases and practice delayed gratification. Before making a nonessential purchase, give yourself a 24-48 hour cooling-off period. This allows you to assess whether the item is a genuine necessity or a momentary desire.

Seek alternative solutions: When faced with financial needs, explore alternatives before committing to new debts, like borrowing from friends or family, negotiating payment plans with service providers, or seeking assistance from local community resources or nonprofit organizations that offer financial aid or low-interest loans.

Remember, avoiding new debts requires discipline and commitment. By adopting a proactive approach to managing your finances and being mindful of your spending, you can stay on track toward paying off your existing debts and achieving financial freedom. Stay focused, make intentional choices, and celebrate your progress.

Step 4: Try the Debt Avalanche Method

The debt avalanche method is a powerful strategy for paying off debt efficiently. With this approach, you prioritize the debts based on interest rates. Additionally, this method provides a clear road map for debt repayment, allowing you to stay focused and motivated as you see progress with each debt you eliminate.

Start by arranging your debts in descending order based on their interest rates, with the highest interest debt at the top of the list. This order will determine the repayment priority. Doing this minimizes the interest that accrues over time, saving you money in the long run. Once you pay off the highest interest, move on to the next one and continue the process.

Remember to continue making at least the minimum payments on all your debts to maintain a good credit standing and avoid penalties. By staying committed to this method and directing your extra funds strategically, you’ll make significant strides toward paying off your debts.

Step 5: Consider the Debt Snowball Method

Another effective debt repayment strategy is the Debt Snowball method. It involves listing your debts from smallest to largest balance and focusing on paying off the smallest debt first while making minimum payments on the others. Once you pay off the smallest debt, you apply the money you were putting toward it to the next smallest debt.

Begin by creating a comprehensive list of all your debts, including credit cards, personal loans, student loans, and other outstanding balances. Arrange your debts in ascending order based on their balances, with the debt carrying the lowest balance at the top of the list. This order will determine the repayment priority.

Continue focusing on one debt at a time until you can pay off all your debts. The debt snowball method is advantageous because it focuses on building momentum and providing a sense of accomplishment by creating small wins, motivating you to continue your debt payment journey.

While this method may not prioritize debts based on interest rates, it provides a structured and motivating approach that can be particularly beneficial for individuals seeking emotional and psychological encouragement along their debt repayment journey.

Step 6: Increase Your Income

How to get out of debt when you are broke? Finding ways to increase your income can significantly impact you but can also be challenging. Consider taking up a side hustle or part-time job to generate extra money.

There are numerous opportunities available, such as freelance work, online tutoring, or selling handmade crafts. Dedicating your additional income solely to debt repayment accelerates your progress. It helps you achieve financial goals sooner, and if everything goes well, you’ll only need to do this for a short time.

Here are a few ideas on how to make extra money to pay off debt fast:

Explore freelance opportunities in your field of expertise

Take on part-time jobs or gig work

Monetize your hobbies or skills

Consider renting out a spare room or property

Participate in online surveys or market research studies

See if you qualify for blood and plasma donations, some places pay for this help

Step 7: Negotiate a Better Rate

Lowering the interest rates on your debts can help you save money and pay them off faster. Reach out to your creditors and explore the possibility of negotiating a lower interest rate. Even a slight reduction in interest rates can make a significant difference.

Here’s a detailed explanation of how to negotiate a better rate and why it can be beneficial:

Review your current rates: This includes credit cards, personal loans, and other forms of debt. Take note of the interest rates, promotional offers, and the terms and conditions associated with each debt.

Research and compare: Understand market rates basics and terms for similar financial products. This will provide you with a baseline for negotiation and help you determine if your rates are higher than what is commonly available. Look for competing offers, promotions, or lower interest rates from other lenders or credit card companies.

Prepare your case: Highlight your payment history, creditworthiness, and loyalty as a long-term customer. Compile improved financial stability or credit score evidence since you obtained the debt. The goal is to present a compelling case for why you deserve a better rate.

If negotiating directly with your creditors doesn’t yield the desired results, consider other options like balance transfers or refinancing.

Balance transfers involve moving high-interest debt to a credit card with a lower interest rate, often with an introductory 0% interest period. Refinancing involves replacing an existing loan with a new one with better terms and a lower interest rate. Both options can help reduce the overall interest you’ll pay and accelerate your debt payoff.

Step 8: Increase Your Credit Score

Improving your credit score can have a positive impact on your financial well-being. A higher credit score can lead to lower interest rates on future loans and credit cards, potentially saving you thousands of dollars in the long run. To boost your credit score, make timely payments, reduce your credit card balances, and keep your credit utilization ratio low. Regularly review your credit reports to identify and address any errors or discrepancies.

Step 9: Consider Debt Relief or Consolidation

If your debts feel overwhelming and unmanageable, exploring debt relief or consolidation options might be a viable solution. Debt relief programs, such as credit counseling or debt settlement, can help you negotiate with creditors to reduce the amount you owe or establish more manageable payment plans.

Debt consolidation allows you to combine multiple debts into a single loan with a lower interest rate. However, it’s essential to research and choose reputable organizations to ensure you make an informed decision that aligns with your financial goals.

Step 10: Stay Consistent

So, what is the best way to pay off debt fast? Consistency is always key. Make your debt repayment a priority and stick to your plan. Celebrate small victories along the way to stay motivated and maintain your momentum.

Remember, achieving financial freedom takes time and dedication. You can overcome your debts and build a brighter financial future with persistence.

Congratulations on taking the first step toward improving your financial well-being. Remember, Credit.com is here to support you on your journey.

Explore our ExtraCredit® program, which provides valuable resources to help you monitor and manage your credit for a small monthly price Or sign-up for our free service that provides an Experian Vantage 3.0 score along with a free credit report card.

As a mom, finding clever ways to save money can help secure your family’s financial future.

Yes, I know, there are many other, more impactful ways to build wealth, and in the grand scheme of things, saving a buck here and there might not seem like the recipe for propelling yourself (with your entire brood in tow) to millionaire status, but hear me out.

Unless you stop the bleeding (in this case, frivolous spending), it will take you a lot longer to get there.

In my mind, building generational wealth is a combination of developing marketable skills, earning from those skills, investing wisely, and frugal spending.

…And putting your foot down when any member of your brood wants to splash $1,000 on a pair of, in my view, hideous sneakers.

That’s why I rave about How to Create a Budget and Everything You Need to Know to Start Using Coupons.

A Mom’s Guide to Saving Money the Smart Way

Of course, as with everything worth doing, it’s much easier said than done. Believe me; I’ve had moments of taking on unnecessary expenses at the grocery store despite having blown past our monthly budget.

It happens; you are going to slip up sometimes. The key is to have a solid hold on your spending habits and a savings system. That way, even if you go off the rails occasionally, you can recover and stay focused on your ultimate savings goals.

With that in mind, here are my top-secret (shhhhhh) creative ways to save money monthly.

1. Start Budgeting

It sounds obvious, doesn’t it?

Would it surprise you to learn that only 30% of American households actually have a detailed monthly budget prepared? Yes, according to a Gallup poll, two in every three Americans don’t have a monthly budget, nor do they have a long-term financial plan or investment goals.

I kid you not; budgeting is one of those things that everyone knows they should do, yet up to two-thirds of us don’t!

Having a detailed monthly budget will open your eyes to the reckless spending on everyday purchases you are currently engaging in.

From unnecessary online shopping sprees to pizza deliveries, even your grocery bill might have something you don’t need, or you can find cheaper alternatives if you just look.

You won’t know where all the money is going until you have an actual, written-down budget. THEN you will see just how badly you’ve been throwing cash around.

Here’s a quick guide on budgeting categories for the family if you want to get started right away.

2. Use Money Saving Apps

If you are anything like me, you put most of your grocery shopping, utility bills, and monthly bills on your credit or debit cards. While most of these offer rewards when you use them, you can go further and use savings apps.

Here’s why. Many of these apps highlight saving opportunities and fetch rewards such as cash back on many purchases you would make anyway.

Neat, huh?!!

Here are a few that I like using. You can check them out and see what you think:

Ibotta: I get cash back for most purchases.

Acorns: This one helps me save and invest.

Rakuten: These guys give you cash back on online purchases you make in over 3,500 stores.

3. Try Out Capital One Shopping

Now this is a tool I simply love! Capital One Shopping is not only free, but it also works in the background. So you don’t need to remember to use it every time.

If you want to find the best deals online and gift cards and coupons, you must install Capital One Shopping on your browser.

You will save a ton of money. Trust me on this one! It is by far one of my favorite and most clever ways to save money.

4. Create a Meal Plan

Have you ever found yourself at the grocery store buying things that weren’t on your list because they looked “interesting to try out?” I know I have!

I’m not saying you shouldn’t try new things and new recipes (what would life be without these little adventures?). I’m saying that meal planning will help you cut back on a lot of unnecessary expenditures when it comes to groceries.

Here’s why I meal plan:

It helps us avoid food wastage (leftovers are planned for)

Encourages a better diet

Saves money on impulse purchases at the grocery store

But most importantly, meal planning helps me save money and curb my spending habits on those nights I don’t know what my family will eat. I will already have a plan in place to help cut down on ordering in and eating out.

Check out my free printable meal plan!

5. Conduct a Personal Finance Audit

I know! I know! That sounds like what the IRS is for, but hear me out.

There are things you are paying for now that you either don’t need or don’t even remember that you are paying for unless you run a complete audit of your finances.

When was the last time you actually saw your husband reading that “Monster Trucks Forever” magazine that keeps coming in the mail?

How about you? Are you really going to visit all those vineyards someday? Then why are you paying for that subscription?

We often put so many little $1-a-month subscriptions on our cards because they seem important at the time, or a dollar a month doesn’t seem like that much. But they add up.

Run a quick audit on your bank statements to find out what you are paying for that you no longer use or don’t actually need, and cut it out.

These are just some creative ways I use to reduce our spending and save money. Saving money doesn’t have to be painful. You just need to find ways to reduce your living expenses (not necessarily lifestyle) and channel all that extra cash into your savings account.

Also see: How to get out of debt fast when you don’t have much money

How about you? What are some of your clever ways to save money?

Financial literacy can be boiled down to one basic concept: Just save more money than you spend. Easy-peasy, right?

Yet, only 57% of Americans are financially literate, per the S&P Global FinLit Survey. And you can’t afford to be among the 43% that don’t make the grade. According to a study by the National Financial Educators Council (NFEC), lack of personal finance knowledge cost each American an average of $1,389.06 in 2021.

This isn’t due to incompetence, of course. Unfortunately, the term “financial literacy” comes with all kinds of condescension — as if those who don’t qualify are utterly clueless when it comes to cash. And there are plenty of stereotypes attached, like that financial literacy equals wealth. And vice versa.

But so-called “financial literacy” is dictated by numerous factors: from access to financial education and banking services in your community to generational wealth or financial trauma. And let’s get real: there’s a lot of jargon in the finance world that can make the savviest of us feel like we have no idea what we’re talking about when it comes to our own money.

All this to say, that even if you are among those dubbed “financially literate,” you probably know how to manage your money, but you probably also realize there’s a lot still for you to learn. So, how much do you really need to know? Let’s break down the basics with a bit of financial literacy 101.

What’s Ahead:

What Is Financial Literacy?

Financial Literacy Definition

Financial literacy is the combination of knowledge, skill, and confidence needed to use money in sound and healthy ways.

Note that I didn’t include “access to money” in that list. That’s because having wealth doesn’t necessarily make you more financially literate, and not having money doesn’t make you less so. Traditionally, any talk of financial literacy has assumed you have a certain base level of money in the bank, but that’s simply not true.

Let’s keep it simple: If a stranger puts a dollar in your hand, do you know exactly what to do with it? If you do, then you can count yourself as financially literate. Which means, no, you don’t need to know what an ETF is or how to buy bitcoin. And even if you’re living paycheck to paycheck just to cover your food and rent, but you know how to make it work — that’s financial literacy.

After all, there’s a big difference between knowing what to do and being able to do it. And so, if some of these are out of reach for you right now, that doesn’t mean you’re financially illiterate.

Financial literacy means you can check off the following:

You know to pay your bills on time because late fees are expensive, they hurt your credit score, and they just generally make you angry.

You know to spend less than you earn.

You understand how compounding interest on your savings/investments can set you up for retirement.

You understand how compounding interest can be used against you through subprime loans.

You’re allergic to overpaying for products or services.

You’re just generally awesome at adulting, no matter your income.

Why Is Financial Literacy Important?

You might say I’m passionate about this topic. Full disclosure: I literally wrote a book about my own financial metamorphosis, called The Frugalista Files: How One Woman Got Out of Debt Without Giving Up the Fabulous Life.

Once upon a time, I too was among the financially unlettered. Sure, I had a decent job, and I knew how to pay my bills on time. But I had too many bills and too little savings.

I didn’t consider myself financially literate until I realized that the little decisions I made daily determined my financial future and, quite honestly, the course of my life.

The same applies to all of us. Either we figure out a plan for how to thrive or we won’t survive. Financial literacy is a non-negotiable.

Financial literacy doesn’t mean your finances are perfect. However, it allows you to at least manage the imperfect parts.

Basics of Financial Literacy

While the fundamental ‘save more than you spend’ essence of financial literacy seems simple enough, there are some foundational skills and concepts that you need to master in order to truly pull it off.

Budgeting

“A budget is a plan you write down to decide how you will spend your money each month,” according to Consumer.gov, a site by the Federal Trade Commission.

Understanding your personal cash flow is an essential component of financial literacy. Every dollar that you earn should be accounted for so that you don’t end up wasting money on things that you don’t need. Budgets help you to control and organize your spending and provide a framework for your income.

A good budget covers housing expenses, food, debt repayments, savings, and yes, discretionary spending. We are social creatures, and we need fun.

Some people think of budgets as restrictive, but they don’t have to be. Instead, treat your budget as the financial roadmap that you need to travel through life. You wouldn’t take a road trip without directions, would you? Don’t move through life without knowing exactly where your money is going.

Read more: How to Make a Budget — Our Step-By-Step Guide to Managing Your Money

Saving and Emergency Funds

Sometimes “life happens.” An emergency fund is a stash of savings reserved for when something goes awry.

Think of that time you got hit with a surprise tax bill. Or when you were freelancing and your main client unexpectedly shut down their business. Your emergency fund should be enough of a cushion to keep you financially stable when you face these unexpected expenses or periods of low income.

How much is enough? Play around with an emergency fund calculator for a ballpark figure of what you need to save given: A. Your approximate monthly expenses; B. Your existing savings; and C. The estimated time it would take for you to replace your usual income if it’s cut off.

If you’re at the beginning of your savings journey and the amount you have left to save for a fully-stocked emergency fund is overwhelming, take a deep breath. Start small by putting $1,000 into an account you only touch for true, must-handle crises, and then gradually grow the fund month by month.

FYI, new video games or the latest Yeezy drop don’t count as emergencies, cool? Acknowledging that simple fact already makes you more financially literate than many of your peers!

Read more: Everything You Need to Know About Emergency Funds

Debt

Debt is money you owe to someone else. It’s typically subject to compounding interest, i.e., a sum of money you must pay to the lender in addition to the amount of money you’ve borrowed. The lower the interest rate on the debt, the less the borrower will pay overall. The higher the interest rate, the more money the lender stands to make.

In some cases, taking on a sustainable amount of low-interest debt can be a financially literate move. You might need to borrow money to pay for an essential expense that facilitates your career goals, like a car or a college education. Or you might borrow money to pay for a large asset that will appreciate in value, like a home.

However, using debt to pay for daily expenses on a credit card, and then carrying an unpaid card balance from one month to the next, can lead to a ruinous, unending cycle of debt.

Financially literate people know when to acquire debt and when to shun it. They work diligently to pay off their debts because they understand that high balances can hurt their credit scores and their ability to save.

Read more: How to Get Out of Debt — a DIY Guide

Investing

Investing is buying an asset in anticipation that it will increase in value and provide financial returns. It’s how you put your money to work for you and achieve wealth.

Conversely, an asset you purchase can also decrease in value, so there’s always a degree of risk involved. But some investments are less risky than others. Bonds can be a relatively low-risk investment, whereas buying crypto is highly speculative.

Financially literate people recognize the importance of investing and aim to have part of their discretionary income tied up in investments.

They also diversify their investment profiles and only invest money that they can afford to potentially lose. They do their research before spending one dollar on an investment. They know their risk tolerance and allocate assets appropriately.

Read more: Essential Advice to Help You Start Investing

How to Improve Financial Literacy

Improving your financial literacy is like anything else that you want to master — you need to work at it every day. When I wanted to become smarter with my money, I started reading reputable personal finance blogs, news articles, Twitter feeds, and books. Financial podcasts can be a great source of knowledge as well. No two people have the same finances, so you need to consume lots of different material to figure out what works best for your situation.

Focus on money management — budgeting, saving/building an emergency fund, and repaying debt — at the beginning of your financial literacy journey. When you’re comfortable with those elements, start to devote more time to building your investment plan. There are a lot of scammers in the financial world, so avoid any get-rich-quick schemes like the plague. If it sounds too good to be true, it is.

As you become more sophisticated and confident in your financial knowledge, you might pair up with a fee-only certified personal financial advisor to help you navigate the investing world. And even when using a financial advisor, you still have to keep abreast of how your portfolio is performing. The more you work at financial literacy, the luckier you become.

Read more: Should I Get a Financial Advisor?

Financial Literacy Quiz

One of the best steps you can take toward improving your financial literacy is to test your knowledge. You don’t know what you don’t know, but a test will certainly show where you need to tighten up on the money front!

Should Financial Literacy Be Taught in Schools?

Educators might understandably resist the notion of adding a separate financial literacy class to already-packed school days. But financial literacy is clearly a must-have skill for everyone, and we’d be hamstringing our youth by excluding it from their education.

Here’s an idea: Instead of a dedicated financial literacy class, why not incorporate short financial literacy lessons into existing classes, at all ages, starting from first grade?

Kids can play around with the fundamentals of budgeting as soon as they learn to add and subtract.

When older students learn about supply and demand in their economics course, it’s typically taught to them as a matter of commodities and products. Why not relate the concept to human resources and an individual’s professional market value?

I remember talking to a group of bright high school students who balked at the idea that a prepaid debit card sponsored by a popular celebrity wasn’t a good financial move. To these kids, prepaid debit cards were financial saviors. After all, their celebrity hero told them so.

What if their English class had emphasized that the wizard in the Wizard of Oz was just marketing and no substance? And that self-professed miracle workers — and the products they shill — might not bear close inspection?

Had they been properly armed with critical thinking skills, the students I met might have dug a little deeper into the realities of prepaid debit cards before they signed up for them. They likely would have discovered that prepaid cards typically cost too much money to maintain over time and do absolutely zilch for credit scores.

Final Thoughts

I wish I could sincerely tell you that personal finance is as easy as spending less than you make, but it’s of course a tad more complex than that. Our lives and our finances are too fluid to be governed by hard-and-fast rules.

Yes, you always want to increase your savings. Yes, you always want to repay debt. But there are exceptions to every ‘always.’

For instance, you shouldn’t save money at the expense of getting necessary health care procedures to save your life. Nor should you spend all your savings on paying off your student loan debt and then be forced to run up a high-rate credit card to pay for life’s emergencies.

These kinds of financial dilemmas pop up for everyone, and they’re too numerous to cover in this article. But that’s where the literacy part of financial literacy comes into play. Literacy of your own financial status and aspirations will guide you through the day-to-day choices that take up the bulk of your financial brainpower. Turning to the wealth of personal finance resources you have at your fingertips will help you with the less intuitive decisions that pop up along the way.

I shared a list of my favorite books about money once before, but that was over two years ago. I’ve read dozens of books since then (and thumbed through dozens more). Here is a revised list of 25 great books about money.

These are all books that I found entertaining or influential. There are still many “big name” books that I haven’t read, such as “A Random Walk Down Wall Street” and “The Intelligent Investor,” and I’ve left off some perennial favorites such as “The Richest Man in Babylon” and “The Wealthy Barber.”

These books are grouped into sections, roughly following the financial progression of the average person (from debt to financial independence). I’ve linked to the Amazon page for each book, but, as always, I encourage you to borrow the titles that interest you from your public library. If you prefer to read on a device, get to know Overdrive, which allows you to borrow e-books for free.

Debt Reduction

For those in the first stage of personal finance, debt reduction is the most important task. I know from experience that this can seem like a long, lonely battle. But others have fought it before, and have lived to document the process. Here are three books that describe different approaches to winning the fight:

The Total Money Makeover by Dave Ramsey — Ramsey is an anti-credit zealot. He made a $4 million fortune by his mid-twenties, and then lost it to bankruptcy. Now he runs a personal-finance empire. He takes a lot of criticism for his support of the debt snowball, which he describes in detail here, but the thing is, his methods work. If you’re struggling with debt, there’s no better starting place than this book. Ramsey’s advice is permeated with his Christianity, but you can get a lot out of this book even if you’re not religious. [My review.]

Debt is Slavery by Michael Mihalik — Debt is Slavery is a deceptively simple book. It’s short. Its advice seems basic. And it’s self-published, so how good can it be? Well, I think it’s great. In fact, I found myself wishing that I had written it. Mihalik’s advice is spot-on, and he covers a lot of topics that other authors shy away from, such as the effects of advertising, the weight of possessions, and the soul-sucking misery that comes from a bad job. This book may be short, but it’s sweet. Especially great for recent graduates, I think.

How to Get Out of Debt, Stay Out of Debt, and Live Prosperously by Jerrold Mundis — How to Get Out of Debt is built on the principles of Debtors Anonymous, a twelve-step program founded in 1971 to help those who struggle with compulsive debt. Mundis was himself a debtor, and he based this book on his own experience. This isn’t purely theoretical information from the mind of some Wall Street finance whiz who has never struggled; this book contains real tips and real stories from real people. If you’ve tried Dave Ramsey without success, read this. It’s 20 years old, but the information is timeless. [My review.]

Everyday Personal Finance

After you’ve defeated debt, you enter the second stage of personal finance, mastering the everyday habits that allow you to build wealth. The books listed here offer a wide view, discussing many aspects of money. They offer advice about saving, investing, and frugality. They don’t go into much detail about any one subject, but they provide motivation to get started. And that’s what’s most important.

Your Money or Your Life by Dominguez, Robin, and Tilford — A classic, and one of the foundation books for the simplicity movement. The authors play off the concept “time is money” in a very literal sense. They encourage readers to sort out priorities, to cut expenses, and then to seek passive income in pursuit of financial independence. A little New Age-y in spots. An excellent book, and a huge influence on many prominent personal-finance bloggers. I hope to review the new, revised edition of YMoYL soon.

All Your Worth: The Ultimate Lifetime Money Plan by Elizabeth Warren and Amelia Warren Tyagi — I didn’t like All Your Worth when I first read it. The book takes a dim view of frugality and thrift, and it contains some wild assumptions (like 12% stock market returns). But with time, I’ve come to appreciate the strength of All Your Worth, not just for those struggling to shake off debt, but also for those of us who are beginning to build wealth. This book’s balanced money formula is probably the single most important part of my current financial plan. There’s good stuff here, though you may need to filter some of the authors’ rhetoric. [My review.]

I Will Teach You to Be Rich by Ramit Sethi — This book is great, but it’s not for everyone. It’s targeted almost exclusively at young adults. If you’re under 30 and single, and if you make a decent living, this book is perfect. But if you’re 45 and married with two children, and if you struggle to make ends meet, this book is less useful. Plus, Ramit has a strong authorial voice. He’s bold, sarcastic, and even a little sassy. Not everyone likes this. If you’re turned off by his blog (or by his guest posts at Get Rich Slowly), you’ll be turned off by his tone in this book. These caveats aside, I Will Teach You to Be Rich is packed with solid advice, cites its sources, and provides scores of tactical tips for managing money. [My review.]

The Complete Tightwad Gazette by Amy Dacyczyn — “The Tightwad Gazette” was a newsletter published during the early 1990s by Amy Dacyczyn (pronounced “decision”). Eventually the back issues were collected into a series of books, which were in turn collected as The Complete Tightwad Gazette. Dacyczyn wrote articles like: “Used Shoes: Are they Good or Bad?”, “Budget Bug-Busting”, “Tightwad Toys”, and “Saving Money on Your Mortgage”. Sounds just like a personal finance blog, doesn’t it? This book has thousands of tips, many of which were contributed by readers of the newsletter. (You won’t find any info on investing here. This book is about frugality!)

Investing

Learning to invest your money wisely is one important aspect of the middle stages of financial development. Wall Street is not friendly to the small investor. It’s designed to part you from your hard-earned dollars. These books can help you develop an investment philosophy that will let you improve your odds of retiring wealthy.

The Four Pillars of Investing by William Bernstein — I’ve read dozens of books about investing. Of these, The Four Pillars of Investing is probably my favorite. Most investing manuals espouse one sure-fire method or another. Four Pillars does that to an extent, but the author provides a great deal of depth and color to support his argument. I love that Bernstein takes a comprehensive, holistic approach to the subject, not just looking at the theory and business of investing, but also looking at the history and psychology of investing. This is a great book. [My review.]

The Random Walk Guide to Investing by Burton Malkiel — Malkiel is best known for his classic A Random Walk Down Wall Street. This book is shorter, written in plain English (there’s no investing jargon), and easy to understand. But that doesn’t mean it’s simplistic. This is an excellent book, filled with advice based on sound financial principles. It covers risk tolerance, asset allocation, diversification, and even a little behavioral finance. An excellent guide for beginners. [My review.]

The Only Investment Guide You’ll Ever Need by Andrew Tobias — Andrew Tobias is an entertaining writer. His jocular, conversational tone will keep you interested as he describes mutual funds, bonds, and treasury bills. There’s a good section on how to handle a windfall (lottery, inheritance). My favorite bit from Tobias is his three-step budget: destroy your credit cards, invest 20% of everything you earn (and never touch it), and live on the remaining 80% no matter what. Awesome. This is a classic introduction to the subject of investing, though at times it seems a little dated. (You can read Andrew Tobias every day at his blog.

The Bogleheads’ Guide to Investing by Larimore, Lindauer, and LeBoeuf — You want expert investment advice? You can’t beat the info found here. These devotees of Vanugard founder John Bogle are big on slow, sure investments like indexed mutual funds. They tap their decades of experience to teach about diversification, inflation, and asset allocation. It’s not nearly as boring as it sounds. This book covers a broad range of topics, though its primary focus is investing. Highly recommended.

The Automatic Millionaire by David Bach — There’s more to David Bach than just “the latté factor”. The system he recommends here is excellent — an automated approach to managing your personal finances. If you’ve been meaning to open a Roth IRA, but have never actually done so, then read this book! He’ll explain how to set it up so that it’s painless. The only caveat I’d note is that this book is several years old now, and because it contains specific recommendations for financial companies, it may be be in need of an update.

Financial Independence

This next group of books may be my favorite. These volumes cover topics related to Financial Independence — that magical point where you no longer have to work. This is the final stage of money management. For many people, this means retirement. But it doesn’t have to be that way. These books offer solid advice for how to create a future that matches your dreams.

The Millionaire Next Door by Stanley and Danko — The authors interviewed and surveyed a pool of millionaires, attempting to find common connections among them. They discovered that millionaires live below their means. They budget. They let their adult children make it on their own. This book introduces several key concepts, including degrees of wealth accumulation. It’s a bit tedious in spots, at least in the audio version. This is one of just a few books to cover both sides of the wealth equation: saving money and earning money. [My review.]

Yes, You Can…Achieve Financial Independence by James Stowers — Yes, You Can…Achieve Financial Independence is informative without being dense. It’s accessible without being condescending. Its advice is solid. The book is filled with investment advice, but it gives equal time to thrift and savings. Best of all, it asks as many questions as it provides answers. It prompts the reader to think, to evaluate her priorities. Its message is that yes, you can achieve Financial Independence, but you can’t get there overnight, and you can’t get there without setting goals and making sacrifices. [My review.]

The Incredible Secret Money Machine by Don Lancaster — This hard-to-find volume from 1978 looks like a get-rich-quick book. It’s not. It’s all about starting and running small businesses, especially craft businesses. To Lancaster, a “money machine” is any venture that generates “nickels”. Nickels are small streams of revenue from individual customers. If your goal is simply to earn a comfortable income for yourself by doing something you love, then this book can help you explore the idea of business ownership. One of my Dad’s favorites, and one of my favorites, too. [My review.]

The 4-Hour Workweek by Tim Ferriss — The 4-Hour Workweek is a frustrating book. A lot of the advice seems impractical and out-of-reach for the average person. But on the other hand, it’s filled with inspirational anecdotes and provocative ideas about how you can make the leap from desk jockey to the pursuit of your dreams. In my review, I wrote that this book “is like a kick in the head”, and it’s true. The flow of ideas is relentless. Despite its flaws, I think this is a great book. [My review.]

Work Less, Live More: The Way to Semi-Retirement by Bob Clyatt — While Financial Independence is my long-term dream, semi-retirement is my more immediate goal. Clyatt describes techniques for leaving the workaday world years (or decades) before the traditional retirement age of 65. Work Less, Live More includes sections on defining your goals, learning to live on less, putting your investments on autopilot, and more. This book is like a toned-down, practical version of The 4-Hour Workweek. I like it. A lot.

The Psychology of Money

I firmly believe that success with money is more about mind than it is about math. We all understand the arithmetic behind personal finance — to build wealth, you must spend less than you earn — it’s mastering the emotions and habits that causes us trouble. These books explore your money and your brain.

Why Smart People Make Big Money Mistakes (and How to Correct Them) by Gary Belsky and Thomas Gilovich — In this short book, Belsky and Gilovich catalog a menagerie of mental mistakes that cause people to spend more than they should. What might have been a boring topic becomes fascinating thanks to an engaging style and plenty of anecdotes and examples. This book covers more than a dozen psychological barriers to wealth and explains how to prevent them from sabotaging you. [My review.]

The Paradox of Choice by Barry Schwartz — I just finished this book the other night, and hope to provide a full review in the next week. It’s fascinating. Schwartz argues that the vast array of choices available to us in the marketplace actually make us less happy. We’d be better off with two options for a wide-screen plasma television instead of twenty. Too much choice doesn’t just make us unhappy — it prevents us from making smart decisions. Fascinating stuff.

Kids and Money

Many parents are unprepared to teach their children about money. You needn’t be one of them. These books suggest methods for getting kids to understand how money works.

Living Simply with Children by Marie Sherlock — Sherlock offers tips for how to raise children that aren’t part of the consumerist culture. She encourages strong family ties as a counter to the relentless purchase to acquire “stuff”. Sherlock is also a proponent of using family rituals to replace consumer-oriented cultural activities. There’s some great advice here (the book is strongly influenced by Your Money or Your Life), but some readers may be put off by the author’s philosophy.

Growing Money: A Complete Investing Guide for Kids by Gail Karlitz — Growing Money has good chapters on banks and bonds, but most of the book is devoted to stocks. The book also contains chapters on the history of the stock market, how investors make money, and how to buy and sell stocks. This is probably my favorite book for children, but it does have some weak spots. Only one page out of 120 is devoted to mutual funds. Because the book is aimed at children, taxes are barely considered. Still, its strengths outweigh its weaknesses. It’s the sort of book to buy for your nephew, but read yourself before you pass it on. [My review.]

What Color is Your Piggy Bank? by Adelia Cellini Linecker — This slim volume is a great choice for kids from 10-14 who are beginning to show an interest in entrepreneurship. Linecker covers the world of jobs, setting up shop, and how to manage money.

Financial Journalism

This final trio of books won’t help you get rich — at least not directly. These don’t contain overt stock tips or advice for frugal living. Instead, they tell real-life stories about certain aspects of finance.

Den of Thieves by James B. Stewart — It’s not just Bernie Madoff. Wall Street has fallen prey to all sorts of unscrupulous men over the course of its history. In Den of Thieves, Stewart takes us inside the high-finance worlds of Michael Milken, Ivan Boesky, Martin Siegel, and Dennis Levine. These men were embroiled in the insider trading scandals that shook the market during the 1980s, and through their stories were able to see just how corrupting the influence of money can be. A little dense at times, but a great way to learn about the market.

Buffett: The Making of an American Capitalist by Roger Lowenstein — It’s no secret that Warren Buffett is one of my financial heroes. In this biography of Buffett, Roger Lowenstein describes the events that shaped his life, starting as a boy in the early 1930s. As we follow Buffett’s growth, we learn about the development of investment theory. There’s plenty of information here about Buffett’s investment philosophy. Entertaining and educational.

Hard Times: An Oral History of the Great Depression by Studs Terkel — Writer Studs Terkel published Hard Times in 1970. It features excerpts from over 100 interviews he conducted with those who lived through the 1930s. Terkel spoke with all sorts of people: old and young, rich and poor, famous and not-so-famous, liberal and conservative. By including the perspectives of so many different people, Terkel is able to paint a richer picture of what things were like. [My review.]

Bonus! The Worst Book About Money

Over the past few years, I’ve read many bad books about money. But none can compare to to the idiocy contained in The Secret by Rhonda Byrne. This book promotes all of the wrong messages, and encourages readers to believe that if they simply wish for something, it will come true.

The Secret contains tips like:

“It is helpful to use your imagination and make-believe you already have the money you want. Play games of having wealth and you will feel better about money; as you feel better about it, more will flow into your life.”

“The only reason any person does not have enough money is because they are blocking money from coming to them with their thoughts.”

“Visualize checks in the mail.”

“This kind of crap is dangerous,” I wrote in my original review. “It’s get-rich-quick drivel of the worst sort. It doesn’t help people address their money issues. It puts them into a pattern of wishful thinking.”

This book is awful.

Final Thoughts

Few personal finance books are perfect. For most, you need to employ personal filters. Dave Ramsey’s The Total Money Makeover is a fantastic book on debt reduction, but if you’re not Christian, you’ll have to tune out the Bible verses. All Your Worth contains a great plan for achieving financial balance, but you may need to ignore its constant disparaging of frugality and thrift.

Because I’ve limited myself to 25 books, I’ve had to leave a lot of great titles off the list. Please feel to share your favorite books about money and explain why others should read them.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

Have you ever wondered what it would be like to have a million dollars?

The first thing that comes to mind might be the ability to purchase whatever you want, whenever you want. But do not let your imagination run wild just yet! There are many things beyond material goods that come with this kind of money.

We will dive into the life experiences that come with being independently wealthy. Plus, everyone will have a different number to be classified as independently wealthy.

You have probably heard that it is impossible to be rich and independent. While others truly believe they are capable of being wealthy.

Becoming financially independent might sound like an impossible goal, but with a little bit of hard work and determination, you are capable of reaching your dreams.

Independent wealth is a life state that you can have and maintain without having to rely on your job or family.

This post will help newbies become financially independent, so you will be able to live their best lives without any external pressures.

In the last few years, many people have taken up the idea of becoming wealthy on their own, without relying on a company or organization to make money. There are numerous ways in which one can become wealthy, but oftentimes it requires a great deal of time, effort, and dedication.

Let’s make sure you enjoy a life of independent wealth with these tips for success.

What Is Independently Wealthy?

Independent wealth is a term often used to describe people who are wealthy enough that their personal finances are not impacted by the economy.