Cash back benefits are no longer just for credit card users. Learn how to use Discover® Cashback Debit to get the most out of it.

September 29, 2023

Making money for spending money? It might sound too good to be true, but it’s a reality for some debit card holders. Debit cards like the Discover Cashback Debit card now offer a wide range of rewards and benefits to checking account holders, who are enjoying extra money in their pockets, added convenience, and more peace of mind thanks to all the advantages.

Lately, debit card benefits have started to include overdraft protection, receiving your paycheck early,1 online privacy protection, and more. But often the biggest benefit for debit card holders is the cash back they earn on purchases made with their cards.

What does ‘cash back’ mean?

As a debit card benefit, “cash back” refers to money that a bank adds to your checking account in exchange for using the debit card associated with that account. The amount of money you receive thanks to a debit card’s cash back benefit can depend on several factors, such as the financial institution, the type of card, and the type of transaction. For example, some financial institutions will reward customers with a percentage of the amount they spend with their card, while others may give customers a predetermined dollar amount for using the card at particular stores or restaurants. Some financial institutions restrict rewards to certain categories of purchases, such as gas or travel. Each financial institution and card has its own rules for what it considers a qualifying purchase, so make sure you understand the terms.

How does cash back work on debit cards?

Cash back rewards for qualifying purchases made with your debit card will typically appear in your account after the close of each statement period. Depending on your bank, the money could be added into a dedicated section of your online banking portal for you to redeem, or it could be directly deposited into your checking account. Make sure you understand how cash back works for your particular debit card so that you know when you’ll see the funds, how much you’ll receive, if there are any limits, and what types of transactions qualify.

How does Discover cash back work?

The Discover Cashback Bonus for the Discover Cashback Debit card works by providing 1% in cash rewards to customers on qualifying purchases. Discover Cashback Debit card users can earn 1% cash back on up to $3,000 in debit card purchases each month.2 That’s potentially $30 per month—or $360 per year—back in your pocket!

Earn cash back with your debit card

Discover Bank, Member FDIC

When does cash back show up on Discover Cashback Debit Accounts?

Discover Cashback Bonus rewards will post to the Rewards Detail section of your account summary at the end of each month. You can view your Cashback Bonus amount in either the Discover Mobile App or the Online Account Center.

Curious about the best way to redeem Discover Cashback bonus rewards? Well, you’ve got options. Through your account, you can manually transfer your Cashback Bonus into your Discover checking account, Online Savings Account, or Money Market Account. Discover customers are also able to enroll in Auto Redemption, which means Discover will automatically deposit your Cashback Bonus into your Discover Online Savings Account each month. Customers can also manually transfer their bonus to any Discover Credit Card Cashback Bonus® Account.

Ready to open a Discover Cashback Debit Account?

If you’re ready to get the most out of your debit purchases, including 1% in cash rewards2, then it’s time to get Discover Cashback Debit. Not only will you enjoy earning money on your everyday purchases, but you’ll also access amazing benefits like fraud protection, early pay1, and a network of over 60,000 fee-free ATMs.

Ready to get started? Open your Discover Cashback Debit account today.

Articles may contain information from third parties. The inclusion of such information does not imply an affiliation with the bank or bank sponsorship, endorsement, or verification regarding the third party or information.

1 Early Pay is automatically available to checking, savings (excluding IRA savings), and money market customers who receive qualifying ACH direct deposits. At our discretion, and dependent on the timing of our receipt of the direct deposit instructions, we may make funds from these qualifying direct deposits available to you up to 2 days early. See our Deposit Account Agreement for more information.

2 ATM transactions, the purchase of money orders or other cash equivalents, cash over portions of point-of-sale transactions, Peer-to-Peer (P2P) payments (such as Apple Pay Cash), online sports betting and internet gambling transactions, and loan payments or account funding made with your debit card are not eligible for cash back rewards. In addition, purchases made using third-party payment accounts (services such as Venmo® and PayPal®, who also provide P2P payments) may not be eligible for cash back rewards. Apple Pay® is a trademark of Apple Inc. Venmo and PayPal are registered trademarks of PayPal, Inc. Samsung Pay is a registered trademark of Samsung Electronics Co., Ltd. Google, Google Pay, and Android are trademarks of Google LLC.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

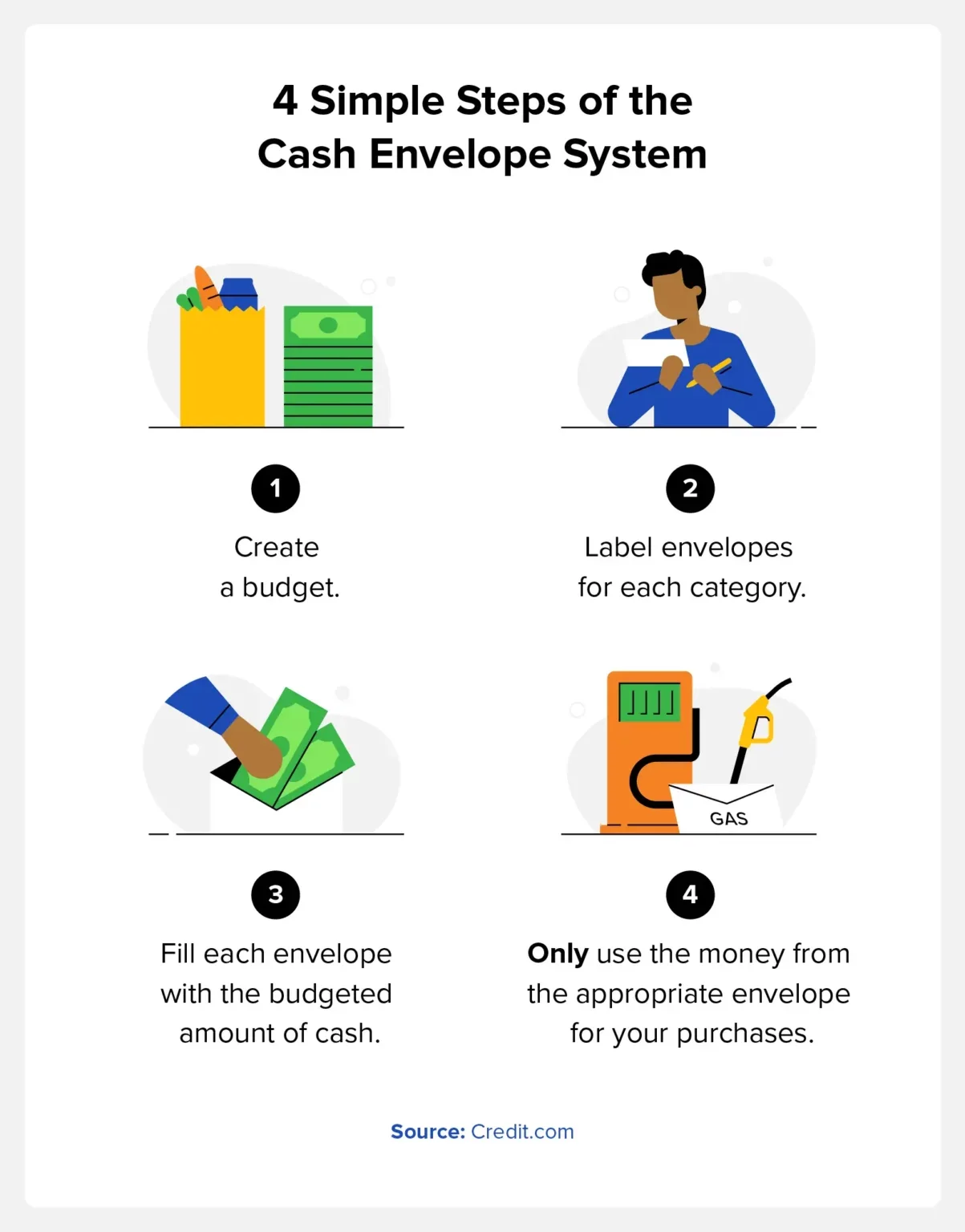

The cash envelope system is a budgeting tool that helps you develop self-discipline by only spending the allotted amount of cash from labeled envelopes each month. It can help reduce overspending and impulsive purchases.

Budgeting is one of the best ways to keep track of your spending, pay down debt, and build wealth. Unfortunately, many Americans don’t take advantage of preparing a monthly budget. Our team at Credit.com surveyed over 1,000 Americans, and 27 percent said they don’t think a budget is necessary.

We also found that 15 percent of people don’t want to feel restricted by a budget, and 24 percent simply don’t think they will stick to it. Fortunately, with the cash envelope system, it’s easy to do both.

Today, you will learn about this simple budgeting method that can help you save money, lower your debt, and potentially help raise your credit score.

Key takeaways:

You can use cash envelopes as a monthly budget by putting cash in different envelopes for spending categories.

The system is ideal for people who have a habit of impulsive spending or overspending.

It allows you to monitor your money rather than guessing how much you’re spending.

The cash envelope system is often called “cash stuffing” on social media apps like TikTok.

What Is the Cash Envelope System?

The cash envelope system, also known as “cash stuffing,” is an easy-to-use budgeting tool that helps track how much money you have to spend. You’ll put the cash in labeled envelopes and check each envelope throughout the budgeting period to see how much money you have left to spend.

Different budgeting systems work for different people. For some, having a monthly budget template on their computer is the best option. Others may benefit more from being able to physically see how much money they have left for purchases like groceries, gas, and entertainment.

How the Cash Envelope System Works

Before cash stuffing, you will need to organize your money envelopes into different categories. If it helps, you can start with a spreadsheet budget template, or you can write down the categories in a notebook. Some of the top budget categories to consider include:

Utilities

Fuel or transportation costs

Groceries

Healthcare and medications

Savings

Debt

It’s also beneficial to ensure you have cash envelopes for areas where you typically overspend. This may be eating out, buying clothes, or online shopping. You can allocate money toward these areas, but the goal is to ensure you don’t overspend.

During the month, whenever you spend money in one of these categories, you only use the money from the appropriate envelope. For example, if you enjoy buying a $5 cup of coffee on your way to work and allocate $100 to that envelope, take $5 out of it each morning.

The cash envelope system is a way to hold yourself accountable for your spending. This means that once the money is gone from an envelope, it’s gone. If you miscalculated how much you need in a certain category, revisit your budget the following month and tweak the amounts.

You can refill your envelopes at the start of each budgeting period or after each paycheck.

The Benefits of the Cash Envelope System

There are pros and cons that come along with every budgeting strategy, so it’s helpful to know the benefits and drawbacks and find the one that’s right for you. The cash-stuffing envelope system is great for people who don’t check their bank account daily or are better with their money when using cash.

Additional benefits include:

Avoiding overdraft fees

Minimizing overspending

Increasing accountability

Helping with disciplined spending

By sticking to cash, the system also helps reduce the frequency with which you use your credit card, minimizing interest fees.

The Downsides of the Cash Envelope System

The cash envelope system isn’t for everyone, and it may create some additional challenges. The primary downside of this budgeting system is that you need to go to your bank or an ATM whenever you need to refill your envelopes. It’s also beneficial to consider that carrying large amounts of cash has the risk of losing it for the money being stolen.

Some of the other downsides include:

It’s time-consuming.

You get no credit card rewards.

You can only spend the amount contained within each envelope.

The other challenge with the cash envelope system is making online payments or automatic payments. Automatic payments are a great way to avoid forgetting about a payment and accruing late fees. You can still use the cash envelope system, but you will need to keep track by writing on the back of the envelope, similar to balancing a checkbook.

Should You Use the Cash Envelope System?

This budgeting system is ideal for people who are quick to pull out their debit or credit card and have trouble with overspending. It can be difficult to track your money electronically, but using physical cash can help many people stick with a budget.

The system is also a great way to budget for beginners. It’s a simple system, and you can start with just a few categories. If you know you have a problem with overspending on ordering food or going out, use this system to allocate a specific amount of cash for these activities.

FAQ

Although the cash stuffing system is a simple method, there are some common questions people have when getting started.

Can the Cash Envelope System Work If You Make Online Payments?

The most common method is to create a physical envelope while keeping the money in your bank account for online payments. You can keep track by writing on the back of the envelope each month.

What If an Envelope Runs Out of Cash?

If you run out of cash from the envelope, stay disciplined and avoid borrowing money from other envelopes. Revisit your budget and find ways to save in different categories, earn extra money, or reduce your spending.

How Do You Use the System When Emergency Expenses Happen?

Emergencies happen, and in these cases, you can shift money around from your envelopes and budget accordingly the following month. It’s also helpful to build an emergency fund for these situations, and you can also keep a credit card for emergency funds.

What Do You Do If There’s Money Left Over in Your Cash Envelope?

Money left over in cash envelopes means you’re doing a great job with your budget. You can use this to treat yourself or add to your personal spending money envelope the next month. You may also want to use this extra money to make extra debt payments or put it in your savings account.

How the Cash Envelope Budget System Can Help Improve Your Credit

Creating a budget is a great way to get your finances under control and create quality spending habits. The cash envelope system is also helpful for reducing your debt and improving your credit. One of the key factors of your credit score is credit utilization, so allocating an envelope toward paying down your debt and using leftover money for additional payments can help increase your score.

For additional credit resources, you can sign up for Credit.com’s free credit report card or our ExtraCredit service.

Inside: Are you looking for an affordable budgeting app that offers a range of features? YNAB may be the perfect choice for you! This guide will compare YNAB vs Mint, highlight their key features, and help you decide which is best for your needs.

Are you trying to make a choice between Mint and YNAB for managing your financials?

Here’s a comprehensive overview that would definitely point you in the right direction.

Both Mint and YNAB have proven to be efficient and reliable online budgeting tools, but their offering varies in some aspects.

While Mint shines with its free budgeting tools and comprehensive credit score and report management capabilities, YNAB stands distinguished with its robust features and specialist credit management options, making it worth its fee for some users.

Herein, we dive into the similarities, differences, and unique functionalities of both platforms to help you decide which one best aligns with your financial management needs and lifestyle.

As a finance expert, I’ve seen both YNAB and Mint apps work wonders for different people.

In my opinion, both have unique value. Novices may find Mint’s overview helpful, while more determined budgeters might prefer YNAB.

Remember, it’s perfectly fine to use both if it aids your long-term money management.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What is YNAB?

YNAB is a budgeting software I’ve utilized that provides detailed financial tracking and education for effective money management. Also, known as you need a budget app.

Adhering to its unique Four Simple Rules for Successful Budgeting, every dollar is assigned a specific task. YNAB operates via an online account or a mobile app, involving color codes and features like ‘The Inspector’ for efficient budget overview. However, it’s important to note that YNAB caters only to the zero budgeting style and charges a monthly subscription fee.

This is a great budgeting method as it gives you a cash flow budget plan for your money.

Overall, YNAB helped me gain control over my finances by setting realistic goals, getting one month ahead on bills, and focusing on each dollar’s purpose.

What is Mint?

Mint is a free, all-in-one finance platform owned by Intuit that can be used to easily manage my money.

It links all accounts in one place for easy tracking and includes features such as budgeting, credit score monitoring, and bill tracking.

For instance, Mint categorizes transactions, monitors changes in my credit score, and sets up budgetary limits.

With over 30 million users, Mint is a leading free tool in personal finance management.

A step up from Mint would be Intuit’s Quicken platform or Simplifi budget app.

Comparison of YNAB and Mint Apps

Mint is a comprehensive, free budgeting app, that provides an overall view of your finances. It links to your accounts, tracking and categorizing spending, while also offering savings tips. Conversely, YNAB, a paid app, focuses on giving users control over budgeting. It will link to your accounts and encourage a proactive role in handling finances.

These are two of the budget apps available on the market.

In my opinion, if you’re seeking an easy-to-use app offering a holistic view of your spending and savings, Mint is a perfect choice. However, if you’re looking for a stringent budget management system with more control, YNAB is worth the investment.

Kristy @ Money BLiss

1. YNAB vs Mint: Features

YNAB and Mint are both renowned budgeting apps, but they possess some notable differences.

While both support account linking, goal setting, and spending tracking, Mint pulls ahead with its investment and credit score tracking features.

YNAB distinguishes itself with a forward-thinking, zero-based budgeting strategy and benefits like manually adding transactions. Think budget by paycheck style.

From the ease of use standpoint, both are equally user-friendly.

2. YNAB vs Mint: Budgeting Snapshot

YNAB offers a rigorous, manually updated budgeting snapshot that employs a zero-based budgeting philosophy. This feature provides a detailed outlook, encouraging users to assign every dollar a job.

On the other hand, Mint has an automated tracking system that offers an all-in-one snapshot of all financial accounts and spending categories.

Mint integrates your accounts, offering useful tips and an overview of your finances. Conversely, YNAB requires a manual categorization of income and expenses but affords more budgeting control. Similar to using the ideal household budget percentages.

The budgeting snapshot in Mint is best suitable for individuals seeking a hands-off approach, while YNAB is ideal for those who prefer an in-depth, hands-on budget strategy.

A great way to move digital from your budget binder with envelopes.

3. YNAB vs Mint: Goal Setting

The Goal Tracking feature in YNAB allows users to set various budgeting goals such as saving targeted amounts of money or conversely working towards getting out of credit card debt. This in-built functionality provides a structured pathway for users to stick to and pursue their financial objectives effectively.

Your interaction with your YNAB account through the goal-tracking tool ties back to YNAB’s four Simple Rules for Successful Budgeting, aiding in fiscal responsibility.

This innovative feature assists individuals in staying focused on their planned budgets, ensuring they are empowered to make strides toward their unique financial goals.

Mint however doesn’t offer this feature.

4. YNAB vs Mint: Interface

While YNAB is ideal for meticulous budgeters prioritizing forward planning, Mint is perfect for those seeking an easy-to-use, comprehensive glimpse of their financial standing.

YNAB’s interface is focused on budgeting, featuring tools for expense tracking, goal setting, and manual transaction input.

In contrast, Mint offers a comprehensive overview of your financial health, automatically categorizing expenses, tracking investments, and offering set-up alerts.

5. YNAB vs Mint: Categorization

Mint offers automated categorization of transactions, which eases the process of budgeting for the user. However, it doesn’t allow the removal of default categories, and the addition of new ones might take time due to server communication.

On the other hand, YNAB allows a deeper level of categorization, with an option to visually nest categories, and more effortless editing of these categories.

In my opinion, Mint’s categorization feature suits a casual budgeter looking for automation, while YNAB would be ideal for those desiring granular control over their personal budget categories.

6. YNAB vs Mint: Mobile App & Cross Platforms

Both YNAB and Mint offer comprehensive personal finance management via mobile apps, compatible with iOS, Android, and desktops.

YNAB stands out with its Apple Watch integrations and a slightly better syncing experience based on user reviews on Trustpilot1.

YNAB also syncs across a desktop app as well.

7. YNAB vs Mint: Alerts

Mint provides a wide selection of alerts, including low balances, upcoming bill payments, over-budget warnings, ATM fees, and unusual expenditure notifications.

These comprehensive alerts from Mint give a more thorough financial pulse check but can be overwhelming for some.

On the other hand, YNAB recently added live push notifications based on your preferences.

8. YNAB vs Mint: Syncing

YNAB leads the game when it comes to synchronization, outshining Mint. While Mint supports numerous banks, issues with synchronization often lead to grievances among its users. YNAB, on the other hand, offers smoother syncing and fewer complaints, proving its superiority.

Many users find YNAB’s syncing consistent and reliable.

Personally, I believe that if you prioritize seamless syncing and don’t mind spending $14.99 a month, YNAB becomes a clear choice.

However, if you’re okay with potential sync issues and prefer free usage, Mint could be more suitable.

It’s crucial to pick according to your priorities and needs.

9. YNAB vs Mint: Savings Accounts

Mint offers automatic expenditure tracking and classifies my spending into categories, providing a comprehensive view of where my money is going.

YNAB, on the other hand, empowers me to manually budget my net income each month, ensuring I don’t overspend and promoting a proactive approach to saving.

10. YNAB vs Mint: Investment Tracker

Mint offers investment tracking features, allowing users to view their investment portfolio and monitor performance.

In contrast, YNAB lacks this feature, not providing any investment tracking at all.

As a user, if you highly prioritize tracking investments in one place, you may lean towards using Mint. Conversely, if investment tracking is less important to you than budgeting, YNAB’s strong budgeting emphasis, despite its lack of investment tracking, makes it a considerable option.

11. YNAB vs Mint: Learning Curve with your Finances

YNAB has a steeper learning curve, necessitating a proactive approach to money management by assigning every dollar a purpose. Thus, YNAB gives you a free 34-day free trial to understand how to use the app.

Mint, however, requires minimal user input post-account linkage and auto-categorizes your spending. For sheer ease of use, Mint might appeal to novices looking for automated budget tracking.

On the other hand, users wishing to take charge of their finances might appreciate YNAB’s proactive, behavior-altering approach. Despite having a steeper learning curve, YNAB offers an abundance of online tutorials and customer support, making the learning process manageable and rewarding.

The same is true when you are learning to use the biweekly budget template.

12. YNAB vs. Mint: Data Security

Data security is a paramount concern when utilizing online budgeting apps as they deal with sensitive financial information.

Apps like YNAB and Mint incorporate stringent security measures to protect user data.

For instance, YNAB uses a one-way salted and hashed password system and data encryption.

Mint, on the other hand, employs two-factor authentication and a Touch ID sensor for iOS for enhanced security.

Nonetheless, it’s important to note that while these apps provide bank-level security, Mint does anonymize and sell user data to advertisers.

13. YNAB vs Mint: Advertising

YNAB derives income primarily from subscription fees offering an ad-free experience, holding a straightforward revenue model. In contrast, Mint generates income through affiliate commissions by advertising financial products to users and selling anonymized user data!

Mint, contrastingly, is a free app reliant on ads and sells anonymized user data for third-party advertisements.

From my perspective, if avoiding ads and preserving data privacy matters to you, YNAB’s approach might be more appealing. However, if you prefer a free service and don’t mind the ads, Mint would be suitable.

14. YNAB vs Mint: Customer Support

When evaluating the customer support of Mint and YNAB, it’s evident that YNAB takes a more well-rounded approach.

With a commitment to respond to email queries within 24 hours, YNAB also provides educational resources such as the “get started” class, their blog, and user forums. This is in contrast to Mint, which, despite offering live chat support, has had reports of slow response times.

Both platforms offer online training materials, but YNAB seems more comprehensive and responsive in its support-providing role. Overall, YNAB appears to be the preferred choice when customer support is a primary consideration.

15. YNAB vs Mint: Cost

Mint is a free, ad-supported budgeting app while YNAB is a subscription-based model of $14.99 monthly or $99 annually.

However, for individuals seeking in-depth surgical budgeting capabilities without concerns for associated costs, YNAB’s price might represent a great investment.

Given the claimed average user saves $600 in two months and $6,000 in the first year.2

For those budgeting with minimal funds, the free price tag of Mint might be more attractive, but you are giving away your privacy.

Pros and Cons of YNAB vs Mint

Our Favorite

Key Features:

YNAB offers a comprehensive approach to budgeting, helping you plan monthly budgets based on your income. It also offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

YNAB’s superior synchronization skills make it the winner in this area. YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners

YNAB provides an option to manually add and upload transactions from accounts each month, a feature that Mint does not offer.

YNAB prioritizes user privacy, requires an opt-in to access budgeting data, and doesn’t sell user data.

Key Features:

Mint offers a centralized platform for monitoring all your financial accounts, including credit cards and bank accounts.

It provides a complete financial overview at a glance through the auto-population of data from linked accounts.

Mint’s features include detailed reporting in multiple categories, free credit score access, and exceptional compatibility with financial institutions.

The service is free, funded by ads and offers, and it best serves those who wish to categorize spending, budget their monthly expenses, and access all financial details from one place.

Lack of investment tracking feature

Customer service is only accessible via email, which might not be ideal for urgent queries

Steep learning curve which requires time and effort to navigate through.

Mint, which belongs to Intuit, automatically accesses all data and sells the data. Thus, an intrusion of privacy.

Budgeting feature doesn’t enable effective planning of future expenses.

Mint suffers from more technical glitches and synchronization issues.

Ads included in the free version of Mint can be obtrusive and may deter users.

$14.99 monthly or $99 annually

Free to Use, But Served Ads and They Sell your Data.

Offers a 100% money-back guarantee at any point of use.

Does not require credit card information to signup, a departure from the usual free trial model)

Our Favorite

Key Features:

YNAB offers a comprehensive approach to budgeting, helping you plan monthly budgets based on your income. It also offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

YNAB’s superior synchronization skills make it the winner in this area. YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners

YNAB provides an option to manually add and upload transactions from accounts each month, a feature that Mint does not offer.

YNAB prioritizes user privacy, requires an opt-in to access budgeting data, and doesn’t sell user data.

Lack of investment tracking feature

Customer service is only accessible via email, which might not be ideal for urgent queries

Steep learning curve which requires time and effort to navigate through.

$14.99 monthly or $99 annually

Offers a 100% money-back guarantee at any point of use.

Does not require credit card information to signup, a departure from the usual free trial model)

Key Features:

Mint offers a centralized platform for monitoring all your financial accounts, including credit cards and bank accounts.

It provides a complete financial overview at a glance through the auto-population of data from linked accounts.

Mint’s features include detailed reporting in multiple categories, free credit score access, and exceptional compatibility with financial institutions.

The service is free, funded by ads and offers, and it best serves those who wish to categorize spending, budget their monthly expenses, and access all financial details from one place.

Mint, which belongs to Intuit, automatically accesses all data and sells the data. Thus, an intrusion of privacy.

Budgeting feature doesn’t enable effective planning of future expenses.

Mint suffers from more technical glitches and synchronization issues.

Ads included in the free version of Mint can be obtrusive and may deter users.

Free to Use, But Served Ads and They Sell your Data.

Who should use YNAB?

From my experience, YNAB works best for those who are ready to seriously manage their money and spend some time learning a new budgeting approach. Its use of the zero-based budgeting system not only makes you more intentional with your money but also demands active participation in decision-making.

YNAB’s ability to link to your accounts and its multitude of educational resources available are admirable features I’ve used.

YNAB offers detailed financial tracking and built-in education, but its monthly subscription fee and suitability for a specific budgeting style may be limiting for some.

However, it comes with a monthly or annual cost – a worthy investment for those searching for a robust, hands-on, and future-focused budgeting tool. Most YNAB budgets agree they save multiples of the subscription cost.

However, it can be less suitable for those not ready for a hands-on approach or those sensitive to subscription pricing.

Who should use Mint?

On the other hand, Mint is an all-in-one app that automatically tracks and categorizes your spending.

Based on my experience, Mint is an excellent tool for novice-level budgeters seeking to track their expenses, set budgets, and manage their finances with ease. This budgeting app allows a comprehensive view of all your financial accounts, which differentiates it from YNAB.

If you’re comfortable seeing ads and not needing investing features, Mint could be a perfect fit. However, if you require the ability to assign multiple savings goals to one account or a bill pay feature, YNAB may be more suitable for you.

Therefore, Mint is most applicable for beginners seeking a free and user-friendly budgeting platform.

YNAB vs. Mint: Which is better for you?

As a content writer and budgeting app user, I find Mint and YNAB are unique in their offerings.

Mint automatically tracks and categorizes your spending, providing an intuitive picture of where your money goes, ideal for beginners in budgeting.

In contrast, YNAB promotes a proactive approach, helping to set and monitor budgets, hence perfect for those with specific financial goals. To sum up, Mint offers a simplified, passive overview, while YNAB is excellent for a detailed, forward-thinking approach to managing finances.

Personal preferences and needs really influence the choice here. Do you need intricate control and don’t mind paying a fee? YNAB might be your fit. Prefer automation and want a free option? Mint could work for you.

YNAB vs Mint: Verdict

As an expert in personal finance tools, I’ve explored both YNAB and Mint.

In my experience, there are distinct differences between YNAB and Mint. For my readers, I recommend YNAB.

YNAB, with its laser-focused approach towards budgeting, is a boon for individuals needing extensive assistance in the budgeting arena. You learn to assign every dollar with intention, thereby gaining a higher degree of control over your finances.

This proactive approach will help you to be financially independent faster.

To sum up, if detailed budgeting is your priority, choose YNAB.

YNAB

Enjoy guilt-free spending and effortless saving with a friendly, flexible method for managing your finances.

Pros:

Comprehensive approach to budgeting, helping you plan monthly budgets based on your income.

Offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

Superior synchronization skills make it the winner in this area.

YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners.

Option to manually add and upload transactions from accounts each month.

YNAB prioritizes user privacy.

Start 34 Day Free Trial

However, for a more holistic financial insight with less emphasis on budgeting, Mint might be the better choice.

Now, make sure to check out our Quicken Review.

Source

TrustPilot. “YNAB Review.” https://www.trustpilot.com/review/ynab.com. Accessed on September 27, 2023.

YNAB. “YNAB Pricing.” https://www.ynab.com/pricing/. Accessed on September 27, 2023.

Know someone else that needs this, too? Then, please share!!

This article originally appeared on Finder.com and has been republished here with permission.

Credit card fraud is becoming more sophisticated, with scammers using devices called “skimmers” that steal and store your information after you swipe or insert your card.

Thankfully, you can visually identify skimmers if you know what to look for. Here are a few low-tech ways you can keep your card safe.

What Does a Credit Card Skimmer Look Like?

A skimmer is a small device that scammers attach to card readers on ATMs, gas pumps or any other device where you insert your card for payment or withdrawal. They look similar to the card reader itself and might increase the length of the reader by a small amount.

These stealthy devices are a highly effective way for scammers to easily steal your info if you don’t know how to spot them.

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

How Does a Skimmer Work?

When you insert or swipe your credit or debit card, the skimming device captures the information found in your card’s magnetic strip. You’re able to complete your transaction like normal, but the crook who installed the skimmer can collect the skimmer later, download your information and make purchases or withdrawals without your knowledge.

What’s in My Card’s Magnetic Strip?

A wealth of information is stored in that little black strip on the back of your card. It contains the name of your bank or issuer, your name and country, your account number and PIN and other details specific to your account, like your account limits and the types of charges your card accepts. In short, enough to make purchases with your data.

How Common Are Gas Pump and ATM Skimmers?

While there isn’t a great amount of data on the prevalence of skimmers, it’s thought that their use is on the rise. A single credit card skimmer can capture information on up to 100 credit cards in a day.

Credit card chip technology has done a lot to prevent skimmers at retailers and most major ATMs, so gas stations and non-major ATMs remain the primary targets of skimmers. This may change since gas stations now must comply with the merchant fraud liability shift from October 2020.

How to Spot and Avoid Credit Card Skimmers

Although skimming can happen almost anywhere you use your card, you can prevent losing your data to a skimmer.

Here are a few simple ways to stay safe:

Study the card reader. Jiggle or shake the card reader before using it. Skimmers are often not securely attached, and moving it around could release and expose it. Look for ATMs, gas pumps and any other credit card readers in well-lit and monitored locations.

Give your card a glance. Scratches, markings or stickiness left on your card after swiping are all signs that your card may have been tampered with.

Manage your card settings. Most offer a way for you to control where your card can be used. For instance, you can set parameters that limit high-total purchases or request notification by text or email if your card is used online rather than in person at a store.

Track your balances. Monitor your account balances to avoid being blindsided by an overdraft or unauthorized purchase. By adjusting notification services, you can be informed if an attempt is made to charge over an allotted amount.

Dip your chip. Using the chip reader, instead of swiping the magnetic strip, significantly lessens the chance of fraud. If your card doesn’t have a chip, request one from your financial institution.

Consider cash. At the pump, pay for your gas inside or with an attendant. For other purchases, sign and save your receipts until you’re able to verify purchases on your next statement.

What to Do If Your Credit Card Has Been Skimmed

If you suspect your credit card information was skimmed during a recent transaction, you should respond with a few common measures. This includes notifying your bank, alerting the FTC and placing an initial fraud alert.

From here, keep an eye on your credit card accounts. Regular monitoring of your account can keep you informed of any unusual activity and let you quickly respond. You can also contact a credit monitoring service to help you maintain oversight of your account. These services automatically notify you if any changes or activity occur on your account.

Most credit cards at this point possess an EMV chip for an additional layer of security. If your credit card doesn’t have this feature, call your bank and see if you can receive a card that has one. While they won’t protect you from skimming, they do help protect against other forms of credit card fraud.

Moving forward, take a closer look at the card reader at any ATM or gas station you use. If it looks unusual, such as misaligned, loose or a different color than the rest of the device, you should skip on using your card there.

How Do I Report a Skimmer?

If you find a skimmer or confirm that you’ve been a victim of one, first call your financial institution to let them know when and where you think it happened. Cancel your card and request a replacement, and follow up by email to further document your claim.

From there, place an initial fraud alert on your card. A fraud alert requires businesses to contact you before issuing credit in your name for up to 90 days.

Filing a police report and alerting the Federal Trade Commission (FTC) are also good practices. The FTC works to prevent skimming rings and catching crooks that skim.

Bottom Line

There’s no sure-fire way to prevent skimming. Every time you swipe your card, there’s a chance someone could be attempting to carry off your info. Be aware of how and where your card is used to significantly decrease the likelihood of your personal and financial details being skimmed. Read more about credit card security to keep your personal finances safe.

When it comes to your overall loss after your ATM or debit card has been stolen or skimmed, the amount of your liability will depend on factors that include how quickly you report it and how much is stolen from your account. Call first and follow it up in writing to start an investigation.

Federal law limits a cardholder’s liability for fraudulent charges, under certain circumstances. For credit cards, generally your liability caps at $50 if you report it within two days. For a debit card, your liability is usually the same within two business days, but $500 if it has been more than two business days after you report it, but less than 60 calendar days after your statement. Anything more than 60 days, and you’re likely liable for all the money in your account. If you report fraud immediately, your liability could be $0.

Frequently asked questions

What does a skimmer look like?

Skimmers vary in appearance based on where they are located. YouTube offers many videos showing how you can spot one.

Do police investigate credit card skimming?

Generally, no. Cases of skimming are best resolved by your bank and FTC. However, you can still call your local police to inform them of recent skimming practices.

Will I have to pay for fraudulent charges made to my credit card?

Federal law limits a cardholder’s liability for fraudulent charges to $50, under certain circumstances. By calling your credit card’s customer service line, you’ll likely find they’ll waive even that amount.

When it comes to your overall loss after your ATM or debit card has been stolen or skimmed, the amount of your liability will depend on factors that include how quickly you report it and how much is stolen from your account. Call first and follow it up in writing to start an investigation.

According to reports from the second quarter of 2022, the total of all household debt in the United States is a whopping $16.15 trillion. Mortgages make up the bulk of that debt, with student loan, auto loan and credit card debt trailing behind.

On average, adults in the United States carry debt loads ranging between $20,800 and $146,200. If you’re in debt and looking for a way to pay it off, making a plan is a critical step. Find out more about how to get out of debt below.

1. Collect All Your Paperwork in One Place

Before you can get out of debt, you need to know how much debt you actually have. You should also know who you owe and what the terms are, as this can help you prioritize debt payments to pay them off faster.

Start by collecting all your debt paperwork in one place and creating a master list of everything you owe. You can do this in a spreadsheet or with a pen and paper. Information to gather includes:

Statements for all your debts. One way to do this is to spend a month saving all your financial mail and email so you have a comprehensive picture of your debt.

Regular bills that aren’t debts. Your cell phone and utility bills, as well as your rent, should all be included when you gather this financial information. Information about income. Look at paycheck stubs or your bank accounts so you know what, on average, you can expect in income each month.

Your credit reports. Get your free credit reports at AnnualCreditReport.com to ensure you know about all the debt you owe.

Tip: Sign up for ExtraCredit to see your credit reports and 28 FICO® scores in one place.

2. Create a Budget and Determine What You Can Pay Every Month

Using the information you gathered in the above step, create a monthly budget. Make sure you cover all your bills and minimum debt payments. When possible, include an amount that can go toward building your savings. Allocate funds for essentials, such as groceries and gas.

Once you cover all the needs for the month, figure out how much money you have left. How much of that can you put toward extra debt payments so you can start getting ahead on debt?

3. Manage Your Debts in Collections

If you see that you have any debts in collections when you pull your credit reports, make sure you have a plan for taking care of them. Collection accounts have a serious negative impact on your credit score. Creditors may also sue you and try to collect on these accounts via wage garnishments or bank levies if you don’t take action to manage collections. That can throw a huge wrench into your plan for getting out of debt.

Tip: If you don’t enjoy manual calculations, check out Tally. You can use Tally to total up your expenses, pay down credit card bills, and generally figure out where you stand.

4. Consider Your Options

There are two main approaches to paying off debt as quickly as possible: the snowball method and the avalanche method.

The snowball method involves paying off accounts with the lowest balances first. You take any extra money you have—even if it’s just $50—and add it to your regular minimum monthly payment on that small balance. When that balance is paid off, you take the extra $50 plus the minimum payment and add it to the next biggest balance. You keep doing this as you work your way up to larger balances, paying your debt off faster and faster.

With the avalanche method, you tackle accounts according to interest rates. You start by paying off accounts with the highest interest rates first. The thought behind this method is that you save money in the long run by tackling high-interest debt first.

5. Try to Reduce Your Interest Rates

Interest refers to how much your debt costs. If you have a lower interest rate, your debt costs less and you can pay it off faster. Here are some ways you can try to reduce interest rates on your debts:

Ask for a lower interest rate. If you’re a credit card account holder in good standing and your credit history and score has improved since you got the card, you may be able to get a better rate. Call customer service for your card and let them know you are looking for a better deal. They may agree to lower the rate to keep you as a cardholder.

Look into debt consolidation or refinancing. A debt consolidation loan provides funds you can use to pay off higher-interest debts. Refinancing occurs when you get a new loan for a home or car. If you had lackluster credit when you got your auto loan, for example, you may be able to refinance it for a lower rate if your credit has improved.

Get a balance transfer credit card. You may be able to transfer balances from a credit card with a high interest rate to one that has an introductory low APR offer. This may allow you to pay off the debt over the course of 12 to 22 months without incurring any more interest expense.

Upgrade Triple Cash Rewards Visa®

$200 bonus after opening a Rewards Checking Plus account and making 3 debit card transactions*

Unlimited cash back on payments: 3% on Home, Auto, and Health categories and 1% on everything else after you make payments on your purchases

No annual fee

Combine the flexibility of a credit card with the predictability of a personal loan

No touch payments with contactless technology built in

See if you qualify in minutes without hurting your credit score

Great for large purchases with predictable payments you can budget for

Mobile app to access your account anytime, anywhere

Enjoy peace of mind with $0 Fraud liability

*To qualify for the welcome bonus, you must open and fund a new Rewards Checking Plus account through Upgrade and make 3 qualifying debit card transactions from your Rewards Checking Plus account within 60 days of the date the Rewards Checking Plus account is opened. If you have previously opened a checking account through Upgrade or do not open a Rewards Checking Plus account as part of this application process, you are not eligible for this welcome bonus offer. Your Upgrade Card and Rewards Checking Plus account must be open and in good standing to receive a bonus. To qualify, debit card transactions must have settled and exclude ATM transactions. Please refer to the applicable Upgrade VISA® Debit Card Agreement and Disclosures for more information. Welcome bonus offers cannot be combined, substituted, or applied retroactively. The bonus will be applied to your Rewards Checking Plus account as a one-time payout credit within 60 days after meeting the conditions.

Do Your Best to Pay More Than the Minimum

Only paying the minimum on high-interest debt, such as credit card debt, doesn’t get you out of debt fast. It can take years—dozens of them—to pay off credit card balances if you’re only making minimum payments.

Instead, put more than the minimum on your debt whenever possible. You may also want to put any additional funds you receive—such as a tax refund—on your debt to help with this process.

Consider More Options for Getting Out of Debt

Creating a budget, managing your money wisely, and making extra payments toward your debt all help you get out of debt. Here are some other ways you can deal with debt:

Increase your income while cutting unnecessary spending. Join the gig economy with a side job to earn extra money, or sell things you don’t need via online marketplaces.

Undergo credit education and counseling. These services can help you make the most of your monthly budget.

Engage in debt settlement. You may be able to negotiate with creditors, especially for accounts in collections, to settle debts for less than you owe. Just make sure you understand any effects on your credit.

Enter a debt management plan. During such a plan, you make a single payment to a trustee. They use those funds to pay your debts, hopefully in a way that gets you out of debt faster. Declare bankruptcy. If you find you’re unable to pay your debts, much less make extra payments, you may need another option. Chapter 7 and Chapter 13 bankruptcy are potential considerations.

How to Avoid Getting into Debt

Paying off debt doesn’t have to be impossible, but it can be challenging. For many people, it requires altering years’ worth of financial habits. If you’re not already in debt, it may be easier to stay out of it. Create a budget and stick to it, spend wisely and avoid using credit cards for things you don’t need or can’t afford to buy with cash.

You’ve probably used Venmo a lot this past year, but is Venmo safe? And if so, what are the advantages of Venmo over other online payment providers? Read answers to these questions and more in our helpful guide below.

In This Piece

What Is Venmo?

Venmo is a type of peer-to-peer—or person-to-person—payment app. Its parent company is money-moving giant PayPal, which had over 377 million registered users in the last quarter of 2020. Think of Venmo like “PayPal lite”—you can receive cash and send money to people, but you can’t send invoices or do anything complex.

PayPal launched Venmo for one reason—to compete in the P2P payment marketplace. Not everyone needs PayPal’s full suite of services, but they appreciate a convenient way to split the bill. You can pay for part of a dinner or your share of the shopping with Venmo, and some online retailers also accept Venmo as a form of payment.

Venmo began offering a cash back rewards debit card—the Venmo Debit Card—in 2018. In late 2020, it launched the Venmo Credit Card. Like the Venmo Debit Card, the Venmo Credit card offers cash back—up to 3% on your “top spend” category.

How Does Venmo Work?

Venmo works a little like PayPal. To use the services you simply:

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

Download and install the app on your phone

Link the app to your bank account, debit card, or credit card

Begin sending payments to friends, family members, and select online retailers

Venmo has an initial $299.99 weekly sending and receiving limit. To lift that limit, you need to provide identification documents. Once your ID is confirmed, you’ll have a $4,999.99 weekly limit.

If you want a Venmo Debit Card, you’ll need to apply online. To get a Venmo Credit Card, you need to be over 18 and a U.S. resident—and you also need to have had your Venmo account for at least 30 days.

Is Venmo Safe? What Are the Risks of Using Venmo?

Venmo is generally very safe—the company uses bank-level encryption to keep your data safe. You can add a PIN number and enable multi-factor authentication (MFA) to make your account even more secure. A strong password combined with a PIN and MFA greatly reduces the chance of hacking.

Venmo’s default profile and payment settings are public. Thankfully, you can change your privacy settings to keep your payment settings under wraps. Venmo’s three privacy levels are:

Anyone can find you and see your transactions.

Only you and the person you send payment to will see a transaction.

Friends only. Your Venmo friends can see you and can also see your transactions.

You can set your privacy settings to default to any of these three levels, or you can set levels on a transaction-by-transaction basis. You can also hide your past transactions.

Is Venmo Free?

Depending on how you use Venmo, it can be 100% free. Believe it or not, if you’re strictly using Venmo to transfer payments from one party to another and you’re not using a credit card, you may be able to use it for free.

However, there are some instances where Venmo does charge a fee. For example, if you’re using Venmo as part of your business, you’ll likely need to pay merchant fees. Here’s a look at the various fees Venmo charges account holders.

Instant Transfer Fees

You can transfer money from your Venmo account to your bank account at any time. This process can take 1-2 days to complete. If you need the money faster, you can opt for the instant transfer option, but it will cost you. Venmo charges an instant transfer fee of 1.75%, with a minimum fee of $0.25 and a maximum fee of $25.

Processing Fees

If you choose to make a Venmo payment using your bank account or debit card, you’ll incur no additional fee. If, on the other hand, you use a credit card to make this payment, you must pay processing fees. Venmo’s processing fees are 3%.

Check Deposit Fees

Venmo allows account holders to deposit checks directly into their Venmo account. However, it charges a fee for this service. The check deposit fee is 1% or a $5 minimum when depositing government-issued or payroll checks and 5% or a $5 minimum when depositing all other checks.

Merchant Fees

If you’re using Venmo to accept payments for a business you operate, you must pay merchant fees. Venmo charges business owners a 1.9% merchant fee plus an additional $0.10 per transaction.

What Is Venmo Debit Card and How Does It Work?

If you use your Venmo account quite often or have your payroll or government check deposited into your Venmo account, you might want to consider applying for a debit card with Venmo. This card is similar to any other debit card from a financial institution. It lets you spend the money in your Venmo account anywhere that accepts debit cards.

You can track your deposits and payments directly on the Venmo app, and you can also check the balance in your account. Since this is a debit card, it doesn’t have the same strict credit requirements you might run into when attempting to obtain a credit card. Obtaining this type of debit card can avoid the need to transfer funds from your Venmo account to your bank account.

There can be some fees associated with having a Venmo debit card. For instance, you incur a $2.50 fee when you withdraw funds from your Venmo account via an out-of-network ATM. There’s no fee for using an in-network MoneyPass ATM. A $3 fee applies for an over-the-counter cash withdrawal at a bank. Additionally, you can only withdraw up to $400 per day from your Venmo account.

Venmo and Taxes

If you’re only using Venmo to transfer funds to friends and family members, taxes won’t be an issue. If, on the other hand, you’re using Venmo to collect payments for your business, you may be responsible for paying taxes. If you earn over a certain amount during the year, you need to include any Venmo payments you received for your business on your taxes. Before starting any business, it’s important to understand what your tax responsibilities are.

Venmo Scams to Watch Out for

If you’re wondering “Is Venmo safe to use?” the answer is yes, it’s relatively safe to use. Venmo uses encryption security to protect your personal information from hackers. Its robust security features are in place to keep your money safe.

Even these robust security features can’t stop all scammers. But there are steps you can take to avoid this type of bank account fraud. It’s important to recognize these scams before scammers take advantage of you. Below is a look at the most common Venmo scams.

Fake Products for Sale

One of the most common Venmo scams involves online sales. The scammer pretends to be selling something online. However, once you make a payment, you never receive the product.

Once a Venmo payment is processed, you can’t reverse it and there’s no way to get your money back. This is why it’s so important to only submit payments to people and businesses you know and trust.

Pretending to Be from Venmo

Another common scam involves scammers pretending to be Venmo. If you receive an email or text message claiming to be from Venmo, don’t automatically assume it is. Some scammers send these messages to try to steal your personal information, such as your account number and password. Once they have this information, they can hack into your account and make payments without your permission.

Using Your Phone

There have been reports of strangers asking a person to borrow their phone. Instead, they actually open the Venmo account on your phone to send money to an account associated with them. Unfortunately, trying to do a good deed by letting someone borrow your phone could cost you hundreds or thousands of dollars.

Why Does Venmo Require Identify Verification?

If you open an account with Venmo, you’ll have to prove your identity. This isn’t just a Venmo requirement. According to the Consumer Identification Program under the U.S. Patriot Act, all financial institutions must verify the identities of all their customers.

This program helps prevent terrorists from sending and receiving money and helps to stop money laundering. It can also help reduce the risk of fraud on Venmo. However, even identity verification can’t prevent all forms of fraud. It’s important to always remain vigilant and report any suspicious activity to Venmo.

Staying Safe with Venmo

There are several things you can do to protect yourself when using Venmo.

Monitoring Your Account

Be sure to periodically check your Venmo account for unauthorized transactions. If you notice any, report it to Venmo immediately.

Set Up Venmo Notifications

Receiving notifications as soon as there’s suspicious activity on your Venmo account may help prevent a scammer from accessing your account. Always be sure to have your notifications on for Venmo.

Secure Your Account

There are multiple ways to secure your Venmo account if you lose your phone or allow someone to use it. First, turn on the PIN feature. This step requires you to enter a specific PIN number before you can even open your Venmo account. You should also set up the two-function authentication feature to make it even more difficult for someone to hack into your account.

Choose Private Setting

You may not realize it, but Venmo automatically makes all accounts public. While other users can’t see the specific details of your account, they can see how often you use Venmo. To keep your account safe, it’s recommended to switch your account to private so only your friends and family members can see your information.

Don’t Keep a High Balance

It’s recommended to avoid keeping a high balance in your Venmo account. This way, if your account is hacked, you’re not at risk of losing too much money. Instead, take steps to transfer your Venmo balance to your bank account as soon as possible.

Don’t Share Phone

Even if you’re using the passcode and two-factor authentication features, it’s recommended not to let a stranger use your phone. Only those you know and trust should have access to your phone.

Only Enter Venmo Through the App or Website

Don’t activate your Venmo account through a link you receive in an email or text message. This could be a phishing email designed to steal your Venmo account information, such as your account number and password. Instead, only access your Venmo account through the Venmo app or website.

Venmo Alternatives

Venmo isn’t alone in the payment marketplace. Like most other payment options, it has a long list of rivals. Let’s line up three formidable adversaries for comparison.

Tip: PayPal is another popular payment app. Check out our safety review for more information.

App Name

Venmo

Zelle

Cash App

Parent company

PayPal

Early Warning Services

Square

Need a bank account?

No

Yes—but you can still use and download the app if your bank doesn’t offer Zelle

No

Who can you pay?

Friends, family members and other people you trust

Friends, family members and other people you trust

Anyone, including contractors, utility companies and charities

Debit card available?

Yes

No

Yes

Can you hold a balance?

Yes

No—but Zelle is connected to your bank account by default

Yes

How much does it cost?

Free if you use a bank account, a debit card or your Venmo balance. If you use a credit card, Venmo charges a 3% fee. Instant outgoing bank transfers cost 1%, while standard bank transfers are free.

No fees to send or receive money. Your connected bank may charge fees, however.

Free if you use a bank account, a debit card or your Cash App balance. If you use a credit card, Cash App charges a 3% fee. Instant outgoing bank transfers cost 1.5%, while standard bank transfers are free.

Any limits?

You’ll have a $299.99 weekly peer-to-peer limit immediately after signup. If you confirm your identity, your weekly limit will go up to $4,999.99.

Limits depend on the financial institution. If your bank doesn’t offer Zelle, your weekly transaction limit will be $500.

You can send or receive up to $1,000 during a period of 30 days.

Venmo Versus Credit Cards

What if you don’t want to pay via an app, and you don’t like carrying cash around either? In that case, your best bet might be a credit card. You’ll need to ask your waiter or your cashier to split the bill, but most merchants are happy to oblige.

Look for credit cards with the following perks:

A low APR. Choose a low-interest credit card to save money on interest payments.

Cash back rewards. Why go for a standard credit card when you can get a little money back each time you shop?

Balance transfer offers. Transferring your balance from another credit card? In that case, look for a 0% balance transfer offer.

Credit builder cards. If you don’t qualify for an unsecured credit card, go for a secured card or a credit builder card to boost your credit score.

So is Venmo Safe?

Let’s recap. Venmo is a P2P payment app, and its parent company is PayPal. You can send money to friends, family members and other trusted individuals via Venmo. Some online stores accept the payment method, too. Venmo offers a debit card and—if you qualify—a credit card. You can fund your account with your bank account, a credit card or a debit card.

If you prefer not to pay by app and you don’t feel safe carrying cash, you might want to go with a credit card. Looking for the right credit card for you? Check out ExtraCredit® today. You’ll see select personalized credit offers when you visit your Reward It portal.

Many people use the terms ATM card and debit card interchangeably, but these aren’t actually the same thing. To understand whether an ATM card is also a debit card, you have to know a bit about the history of these cards and what they’re used for.

We’ve got the details on ATM cards vs. debit cards below. Find out the difference and get answers to some common debit and ATM questions.

What Is the Difference Between ATM and Debit Cards?

ATM and debit cards look quite similar. They resemble credit cards and typically have bars you can swipe. They may also have secure chips. However, they aren’t the same and don’t serve the same purpose.

If the question is which came first, the ATM or debit card, the answer is ATM card. According to a report from the World Economic Forum, the patent for an early cash dispenser was filed back in 1960. ATMs became operational later that decade, along with automated teller machine cards—ATM cards. The first official debit card didn’t debut until 1972. It was called the ATM account debit card from City National Bank of Cleveland.

ATM cards were originally designed to do one thing. Instead of going to the bank to get money, you could take cash out of your checking account via a machine. These machines were connected by regional networks. While the cards were issued by banks, they could be used to withdraw money anywhere there was a machine for a potential fee.

As such, ATM cards are cards that are only used to interact at ATMs. Debit cards, on the other hand, have a wider function.

In the past, ATM networks began looking for new revenue streams. They started creating relationships with retailers and eventually joined forces with the credit card networks to create what we now know as debit cards. Debit cards can be used like credit cards at checkouts in person and online.

Most banks also issue debit cards that can act as ATM cards. However, an ATM-only card can’t act as a debit card. Debit cards have Mastercard or Visa logos on them, indicating which network they run on. ATM cards don’t have these logos.

Find Your Card Now

Privacy Policy

Pros and Cons of an ATM Card

Some banks will still issue an ATM-only card if an account holder asks for one. These cards can only be used at automatic teller machines.

Pros of ATM cards include:

You can get cash at any machine, creating flexibility for money management.

You can’t swipe the card to pay for goods and services, which can help reduce impulse purchases.

They may be a good tool to go along with a cash envelope budget system.

The main disadvantage of an ATM card is its limitation. You can’t use it to pay for goods and services. If you don’t have another payment method in your wallet, this can lead to you having to find an ATM and get cash anytime you want to purchase something.

Pros and Cons of a Debit Card

Most checking accounts come with the option for a debit card, and some banks issue one automatically. You can also get prepaid debit cards.

Pros of debit cards include:

Flexibility, as you can use your card at ATMs and pay for goods and services with it anywhere Visa or Mastercard is accepted

You may be able to swipe your debit card as a credit card for added protection

Options for managing your budget, as you can set limits on your debit card or get a prepaid debit card that limits how much you can spend

They’re a common and recognized financial tool that won’t raise eyebrows when you use them

The biggest con of a debit card is that it’s tied to your bank account. This can lead to impulse spending that brings your account balance low, even if you didn’t budget for the spending. You may also find your debit card is limited by daily or individual purchase amounts.

FAQS

Can you use ATM cards at all ATMs?

Yes, you can generally use an ATM card at any automatic teller machine. This means you don’t have to look for an ATM that’s associated with your financial institution.

Are there fees for using different ATM cards at different brand ATMs?

Yes, there are fees for using ATM cards that aren’t associated with your financial institution or bank. Your bank might charge a fee for this activity, and you may also pay a fee to the ATM company.

What happens when an ATM transaction fails?

ATM transactions can fail for a few reasons. When they do, the machine notifies you of the failure and the reason. Some common reasons include:

You don’t have enough money in your account to cover the withdrawal.

The machine experienced a malfunction and couldn’t complete the process.

You entered an incorrect PIN.

Your card couldn’t be read by the ATM reader.

In cases where a technical malfunction or incorrect PIN entry caused the transaction to fail, you may be able to try again.

Are there any limits to how much can be withdrawn with debit and ATM cards?

Yes, banks set limitations on how much can be withdrawn with debit and ATM cards. There may be a limitation on how much you can withdraw in a single transaction. Daily limitations also usually exist. For example, your bank may only allow you to withdraw $300 at a time or $1,000 in a single day. No standards exist for these limitations—each financial institution decides for itself.

Which Is Right for You?

Ultimately, you have to decide whether an ATM or debit card is right for you. Take into account your own budget and the way you spend money. You should also consider what financial habits you need support for and which type of card would help.

Update 9/21/23: Bonus is at 30,000 if you apply via the Credit Karma link (ht RJ)

As rumored Wells Fargo has launched the new Autograph card. Card details are as follows:

Welcome bonus 30,000 points on $1,500 in first 3 months (worth $300)

Card earns at the following rates:

3x on dining, transit, travel, and streaming services, gas, phone plans

1x everywhere else.

Redemption details:

Rewards can be redeemed in $25 increments for 2,500 points. Or get in $20 increments for 2,000 points at the Wells Fargo ATM.

Minimum of 100 Rewards Points or $1 in Cash Rewards in your Rewards Account is required.

Redeem for Purchases is another option.

Automatica redemptions can be set up in $25 increments.

Points do not expire while this Credit Card account is open.

No annual fee.

No foreign transaction fees.

Visa Signature benefits.

Update History:

Update 5/13/23: Bonus now 20,000 instead of 30,000.

Update 3/25/23: Bonus is 30,000 points when you do a google search for Wells Fargo Autograph. Hat tip to TheBigDonDom. You can also use this link.

Update 1/12/23: Bonus reduced to 20,000 points.

Update 7/20/22: It’s now possible to product change to this card. Most Visa® credit card types are available to switch with the exception of College, Secured, The Private Bank, Wells Fargo Advisors, Hotels.com® and any Propel American Express® cards.

If you’re in the market for purchasing a new home or taking on a business loan or personal loan, you’re likely finding it difficult to score the almost-2% APR we saw in 2020. That’s becausethe Federal Reserve has been hiking interest rates since March 2022 in an effort to cool inflation.

“The Fed has two objectives: To keep inflation low, their current obsession, and to keep unemployment low, which is of current lesser concern,” says Amy Hubble, a certified financial planner who has a Ph.D. in consumer economics. “In practice, this means they lower rates to incentivize growth and hiring, and raise rates to combat inflation when the economy gets overextended. This leads to a policy teeter-totter meant to balance out economic activity in the US.”

So the question remains: When will we finally see interest rates start to come down? CNBC Select asked three experts to give their take on what lies ahead for interest rates. Here’s what they had to say.

What we’ll cover

When will interest rates come back down?

Nobody outside of the Federal Open Market Committee (FOMC), the 12 men and women tasked with setting target interest rates, can predict with any certainty what will happen with rates and when. But that hasn’t stoppedeconomists like Preston Caldwell, a senior U.S. economist for Morningstar Research Services LLC, from making their own educated guesses.

“I think rates will start cutting in early 2024,” Caldwell says. “I think inflation will be nearing the Federal Reserve’s 2% target at that phase and the economy will show signs of slowing, but it’s hard to predict.”

Other professionals in the space echo a similar vision. Hubble points to a recent FOMC report that includes committee members’ projections on gross domestic product (GDP) growth, inflation and the unemployment rate — all factors the Fed will weigh when deciding how aggressively to cut rates.

“All FOMC members believe that rates will be stable or higher through 2023 before slowly coming down in 2024–2025 to settle at a comfortable 2.5% for the longer-term,” she says.

Elliot Eisenberg, the Chief Economist at Graphs and Laughs agrees. “There was a belief that once the second half of 2023 came around, rates would’ve been lower than they were at the end of 2022,” he says. “But it hasn’t come down. These things take a long time to work their way through the economy, so sometime in 2024 sounds about right.”

However, he also warns that it’s hard to believe that we’ll see any interest rate cooling in 2023.

Subscribe to the CNBC Select Newsletter!

Money matters — so make the most of it. Get expert tips, strategies, news and everything else you need to maximize your money, right to your inbox. Sign up here.

What should you do when interest rates go down?

Lower interest rates make borrowing money cheaper. That means all other factors (like your credit score) being equal, you’ll generally pay less in interest on anynewstudent loans, personal loans, business loans and mortgages than you would during today’s high-rate environment. Existing loans with a variable rate may also start charging less interest as the Fed lowers interest rates.

That’s why waiting until interest rates come down beforeborrowing money for alarge purchase — like a home — can be easier on your bank account. The current average mortgage interest rate on a 30-year loan is 7.98% even for borrowers witha credit score between 700 and 719. That’s a tough pill for a first-time homebuyer to swallow month after month as they pay their mortgage.

However, if holding off on getting a mortgage isn’t doable for you, make sure you improve your credit score before applying so you can qualify for an interest rate that’s as low as possible. Also consider choosing a mortgage lender that helps you save money throughout the process. Ally Bank, for instance, doesn’t charge any lender fees. And if you qualify for a Navy Federal Credit Union mortgage, you can get a home loan with no private mortgage insurance (PMI) requirements even if you make a down payment of less than 20%.

Ally Home

Annual Percentage Rate (APR)

Apply online for personalized rates; fixed-rate and adjustable-rate mortgages included

Types of loans

Conventional loans, HomeReady loan and Jumbo loans

Terms

15 – 30 years

Credit needed

Minimum down payment

3% if moving forward with a HomeReady loan

Terms apply.

Navy Federal Credit Union

Annual Percentage Rate (APR)

Apply online for personalized rates

Types of loans

Conventional loans, VA loans, Military Choice loans, Homebuyers Choice loans, adjustable-rate mortgage

Terms

10 – 30 years

Credit needed

Not disclosed but lender is flexible

Minimum down payment

0%; 5% for conventional loan option

You can also refinance your mortgage down the line during a lower interest rate environment so you can score a better rate on your loan. PNC Bank is one of the most accessible lenders because it has locations in all 50 states and customers can apply both online and in-person.

PNC Bank Mortgage Refinance

Annual Percentage Rate (APR)

Apply online for personalized rates; fixed-rate and adjustable-rate mortgages included

Types of loans

Fixed-rate, adjustable-rate, FHA loans, VA loans and jumbo loans

Fixed-rate Terms

10 – 30 years

Adjustable-rate Terms

Available in periods of 7 and 10 years for a fixed rate, followed by an adjustment period when the interest rate may increase or decrease on an annual or semi-annual basis

Credit needed

Not disclosed

Pros

Refinance available for primary and secondary homes, and investment properties

Offers a wide variety of loans to suit an array of customer needs

Offers refinancing for VA and FHA loans

Available in all 50 states

Online and in-person service available

Cons

Doesn’t offer home renovation loans

Lower interest rates can also have an impact on the APY you earn on your high-yield savings account. While buying a house or taking out a personal loan becomes more affordable during lower interest rate environments, you typically can’t earn as high an interest rate from the money in your deposit accounts.

That’s becausebanks use the Fed rate as a benchmark for yields on savings accounts. So when the Fed rate falls, the interest rate on your high-yield savings account will likely also decrease. Right now, some high-yield savings accounts, like the UFB High Yield Savings Account, are offering more than 5% APY on account balances.

UFB High Yield Savings

UFB High Yield Savings is offered by Axos Bank, a Member FDIC.