Inside: Are you looking for a way to help your kids learn about money? If so, Cash App for kids is the ideal answer. This guide will teach you how to manage money simply by using apps.

Ever wondered why it’s crucial for your kids and teens to have a cashless payment option?

In this digital age, teaching money management skills early to our younger generation is vital.

Having features likeCash App for kids is a great way to introduce them to responsible spending. Not only does it provide a secure method for purchases without the need for carrying physical money, but it also serves as an excellent tool for setting spending limits and tracking budgeting habits.

Plus, it’s a win-win for parents and teens as you can visually monitor transactions while they enjoy a sense of financial independence.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What is Cash App?

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

It offers a range of services including a free custom Visa debit card and the option to receive paychecks up to two days earlier.

Additionally, with the Cash App, users can instantly buy and sell stocks commission-free and even trade in bitcoin.

Can a child have Cash App?

Yes, a child can have a Cash App account if they are 13 years old or older. However, it requires parental approval.

Remember, this gives your child the opportunity to learn money management, but it also comes with the responsibility of overseeing their spending.

Why would kids need Cash App?

Well, we are moving to a cashless world. There are thousands of stores and restaurants that only offer cash. We learned this when our son went to an MLB baseball game with his middle school. No cash. Only debit or credit cards were accepted as well as Visa gift cards.

So, we needed to give our kids an introduction to modern, simple, and secure ways of money management.

Cash App might be the perfect solution. Another great option is Greenlight for kids.

Cash App – Do More with Your Money

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

What are the benefits of using Cash App for kids?

Education: Cash App can be an effective way to teach your children about responsible money handling and the dynamics of a digital economy.

Control: You have the flexibility to set spending limits and disable certain features, ensuring responsible use of the application.

Security: Cash App’s encrypted connection adds an extra layer of security, keeping your kid’s transactions and personal data secure.

Emergencies and convenience: It’s an incredibly handy tool for sending cash to your kid during emergencies. No need to rush, just a tap on your phone, and you can send money.

What cash apps can 13 year olds use?

In today’s cashless society, it’s more important than ever for kids to learn how to manage money digitally.

Below are some alternatives to Cash App that serve well for 13-year-olds:

Description:

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track your child’s spending and saving habits.

Learn to earn, save, and invest together. The banking and investing app for kids and teens.

Comes with a debit card

Allows kids to make savings goals.

Limited deposit methods

Monthly fee

Starts at $4.99/month

Description:

Prepaid cards and a family finance app for kids, teens, and parents.

More than money.

A financial education.

If you want your child to learn money habits that match your values, you’re in the right place.

Description:

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

Description:

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track your child’s spending and saving habits.

Learn to earn, save, and invest together. The banking and investing app for kids and teens.

Comes with a debit card

Allows kids to make savings goals.

Limited deposit methods

Monthly fee

Starts at $4.99/month

Description:

Prepaid cards and a family finance app for kids, teens, and parents.

More than money.

A financial education.

If you want your child to learn money habits that match your values, you’re in the right place.

No bank account needed.

No fancy phone needed.

Affordable for all! Plus free trial!

Mobile setup is not user friendly.

No investing option.

$5.99 month or $3.33/month for 12 months

Description:

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

Only able to spend what is loaded on Card.

Free CashApp debit card.

No maintenance or annual fees.

Not FDIC insured.

No parental controls.

Remember, each app has its own unique strengths and weaknesses. Do some research and try out a few to see which one best suits your teen’s financial needs.

How do I create a Cash App account for my child?

Teaching kids about money management is vital for their financial future.

One excellent way to do this effectively is by setting up a Cash App account for children, giving them practical experience in handling finances while under a parent’s supervision. Also, known as a sponsored account.

This guide will walk you through the process of creating a Cash App account for your child and highlight the numerous benefits it offers.

Step 1: Download Cash App

To download Cash App, click this Cash App link to make sure you are in the right spot. Both you and your teen will need to do this step.

It’s easily recognizable – look for the white dollar sign on a green background. Once you’ve found it, simply hit ‘Install’ and sit back while your phone does the work.

Remember, this green goodness is only accessible to users in the United States.

When learning which payment type is best when trying to stick to a budget, you will be pleasantly surprised at how well Cash App works.

Step 2: Create an Account

This is a simple process. Both the teen and the adult will need to do this step separately. If as the parent you don’t have a Cash App account, then you will need to do this step.

To create a Cash App account, follow these steps:

Once installed, open the application and follow the on-screen instructions to set up your account.

You will have to enter your phone number or email address.

For security certification, the Cash App will send you a secret code to verify you. Enter it.

Select a $cashtag, which is a unique username to send and receive money (similar to Venmo)

Step 3: Connect a Bank Account

For the parent account, you need to complete this step and the teen will need to wait.

Remember, in “My Cash” you’ll spot the “Add Money” option for funding.

Open Cash App; it’s the icon with a white dollar sign on a green background.

Tap the top-right profile icon.

Navigate to “My Cash” – it’s a tab on the home screen.

Click “Link a Bank,” nestled within the options.

Follow the prompts to add your bank account or debit card info.

Once your card is linked, you’re all set.

Learn where can I load my Cash App card.

Step 4: Authorization Request of a Family or Sponsor Account

Now, you must link the two accounts together. Cash App calls this a sponsored account. There are one of two ways to accomplish this.

Option #1 – Parents Initiate the Request

To invite someone 13-17, then open the app:

Tap the Profile Icon on your Cash App home screen

Select Family

Tap Invite a teen

Follow prompts to share links using text or email

Option #2 – By the Teen

On the Home Screen, tap the Cash App profile icon.

Proceed to Family Accounts and choose the option “I’m a Teen”.

Complete the Cash App for Kids application form with your details including your name and birthday.

Hit the Request Approval button.

Enter the name, email, phone number, or $CashTag of your parent/guardian.

Lastly, tap Send. This will send an authorization request to your parent or guardian’s Cash App account. They need to approve this request before you can start using the app.

Note: You can’t add funds, send payment, or request a Cash Card until this authorization is approved.

Step 5: Have Your Child Design and Order a Free Cash Card

Now, the fun part! Ordering your own Cash App Card.

Designing and ordering your Cash Card is packed with creativity and ease.

Customize your card to represent your unique personality, with choices ranging from the material, font size, and base design, to text lines.

You can seek inspiration from an array of cool Cash App Card design ideas. Notably, the glow-in-the-dark cards are quite popular among minors.

The whole process is about making your debit card unmistakably yours.

Step 6: Limitations on Certain Features

Certain financial apps cater to teens by setting limits on transactions.

For example, a teen on Cash App can send and receive up to $1,000 every 30 days. This safeguard is designed to prevent overspending and encourage smart budgeting practices.

Furthermore, parents and guardians have the option to impose their own customized spending limits through the app according to their teen’s financial maturity. However, it’s essential to keep in mind, that these apps are not recommended to be used by teens just like regular accounts due to the risks of misspending and overspending.

Be aware that certain transactions are blocked, including bars, dating services, and rental car services

Encourage your kids to use robust, unique passwords and activate features like PIN lock and facial ID to enhance security.

You can ensure safety by setting a PIN, turning on notifications, and limiting money requests to ‘contacts only’.

This is similar to understanding the advantages of mobile phones for kids.

Step 7: Pick a unique $Cashtag

Tell your child to select a unique and fun $Cashtag for their Cash App account. It’s like a username and can be used in transactions.

Emphasize the originality of the $Cashtag as it needs to be unique.

Expert Tip: To secure their $Cashtag, avoid using personal information like birthdate or social security number. Instead, opt for quirky, fun, and uncommon word combinations.

Step 8: Send & receive money

Cash App provides an easy-to-use platform for instantly transferring money between friends and family at no cost.

A few quick taps allow users to request, receive, or send money, presenting a convenient method for paying a dinner, settling rent with roommates, or any other financial interactions.

In addition, users get a free custom Visa debit card, which they can order directly from the Cash App for both virtual and physical use. The card enables users to make purchases from any merchant accepting Visa cards.

Plus, with the Cash Boost feature, users gain from immediate discounts at select restaurants, stores, applications, and websites when they use their Cash App card.

An Alternative – Use Greenlight Debit Card for Kids

Looking for an all-in-one alternative to the Cash App for your kids?

Explore the Greenlight Debit Card for kids – a superb choice for money management and financial education.

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track their child’s spending and saving habits.

Plus it offers 1% cash back on all purchases and up to 2% interest on savings, this card is accepted anywhere MasterCard is used and comes with built-in features that include educational programming and real-time notifications for every transaction.

Greenlight

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track your child’s spending and saving habits.

Pros:

Offers a comprehensive financial education pathway

Broad acceptance due to affiliation with Mastercard

Parents retain control over spending limits

Real-time notifications improve security

Cashback rewards are an added bonus

Cons:

Greenlight charges a monthly fee starting from $4.99

Limitations on direct deposits

No possibility for payments from Paypal, Venmo or Apple Cash

Kids under 13 require parental access

Some transaction types are blocked

It’s an innovative and secure financial platform for kids, with plans starting at $4.99 a month.

Safety Measures for Using Cash App for Kids

Educating children about safety measures while using cash apps and debit cards is crucial in today’s digital age.

With increased online scams, it’s important that kids understand the equivalence of digital cash to real money and how to protect their accounts.

This brief overview will highlight key practices to ensure your child’s safety when handling digital transactions.

1. Know the App’s Safety Features

Knowing the app’s safety features is crucial for maintaining security while using cash apps.

These features can include password protection, two-step verification, and biometric scans such as fingerprint or facial ID. Many apps also offer robust encryption to secure data and transactions.

Keeping abreast of the app’s safety protocols not only helps safeguard against potential scams but also instills a better understanding of digital literacy. Understanding these safety measures and functionalities can greatly lessen the likelihood of falling victim to fraudulent activities.

Make sure they don’t learn how to unlock borrow on CashApp!

2. Talk to Your Kids About Money

It is essential to talk to your children about financial literacy from an early age especially if your parents never spoke about money.

Start by making them aware of the concept of saving by using tools like a piggy bank and elucidate the value of delayed gratification.

As they mature, introduce them to the functionalities of debit cards and apps like Cash App that provide hands-on experience in managing finances. Teach them about budgeting, saving, and investing in an age-appropriate manner.

Above all, impart the message that money doesn’t just grow on trees and that every purchase needs to be evaluated against future needs and plans.

3. Use Account Alerts to Stay Up to Date

Account alerts on Cash App are not only handy but critical to your kid’s financial safety. Setting them up is a breeze.

Firstly, head to the “Notification” tab in your app settings.

Thereafter, opt for “Account alerts” and switch it on. This will ensure you’re notified of all transactions.

For an added layer of security, enable “Suspicious activity” alerts; this helps to flag any odd movements swiftly.

4. Set Up a Strong Account Passwords

It is crucial to ensure that your online accounts are secured with robust and unique passwords.

Complex passwords that incorporate a mix of uppercase and lowercase letters, numbers, and special characters can provide a strong line of defense against unauthorized access. Also, you should look at changing these passwords regularly, which further enhances security.

Using a password manager, either online or paper-based, can assist in maintaining and keeping track of different account credentials, maximizing security while minimizing the risk of forgetting passwords.

However, if opting for a paper-based version, it is crucial to store it in a secure and confidential location to prevent unauthorized access.

5. Have a Conversation About Scams and Fraud

The proliferation of digital transactions and cash transfer apps has given rise to numerous scams, making it critical for users to look out for fraud.

Online scams can result in financial loss, with cash apps often not assisting in the recovery of misdirected funds due to errors or fraudulent activities.

Additionally, cybercriminals use these scams to steal personal data, leading to issues like identity theft and fraudulent transactions. Furthermore, the anonymity of digital platforms enables scammers to disappear without a trace after executing a scam, sometimes befriending and exploiting minors.

Therefore, everyone must stay vigilant about potential scams to protect their money, personal information, and overall digital safety.

Key Tips to Watch for:

Discuss current scams happening. Use reliable resources to educate them about how fraud works and precautions to take.

Teach them to *slow down* during transactions to avoid sending money to the wrong contacts.

Advise against sending money to strangers to avoid being scammed.

6. Check Bank Accounts for Any Unauthorized Payments

As a parent, it is essential to regularly check your teen’s checking accounts linked to their mobile wallet for unauthorized payments.

By staying vigilant, you can detect suspicious activity early and prevent possible instances of fraud.

Tracking their spending patterns also helps you understand if they are managing their digital money wisely or if there are sudden changes in their spending habits.

Remember, it is better to be proactive in monitoring these accounts, as most money transfer app funds are not FDIC insured, making the recovery of accidental transfers or payments a challenging task.

7. Ability to Give Your Kids an Allowance

If you choose to do so, giving your kids an allowance on Cash App is a safe and effective way to teach them about responsible money management. It provides hands-on experience while putting the power of monitoring in your hands.

To set this up, simply create an account for your minor and periodically send money to it as an allowance. They can spend or save it, while you observe their spending habits.

This is a simple way for kids and teens to start managing a small amount of money.

Cash App – Do More with Your Money

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

Which cash app will you choose for your kids

To sum it up, equipping your kids with financial responsibility via Cash App or Greenlight is an intelligent move.

These apps provide a platform for learning about savings, investments, and the value of money.

Although risk exists its potential scams, with proper guidance, your teen can safely navigate this. The added perks of trading, direct cash exchanges, and options like BusyKid and Bankaroo can further enrich their financial literacy journey.

So, which digital wallet will you pick for your kid’s first leap into financial independence?

Know someone else that needs this, too? Then, please share!!

UK ‘mortgage meltdown’ looms amid ‘terrifying’ growth in arrears

Jump in borrowers unable to make payments with landlords particularly hit and ‘worse to come’

Analysis: will the Bank listen to business and halt rate rises?

Mortgage balances with arrears jumped by 13% in the second quarter of the year to the highest level since 2016, according to Bank of England figures that underscore the stress in the UK mortgage market.

Rising interest rates and unemployment over recent months have put pressure on household disposable incomes, forcing some families to cut or suspend their monthly mortgage payments.

Buy-to-let mortgage payers have also come under pressure in parts of the country where tenants are struggling with the cost of living crisis.

The Bank of England said the total value of mortgage balances which had some arrears rose to £16.9bn, up by 29% on the previous year and the highest since the third quarter of 2016.

Mortgage arrears are based on figures showing the number of borrowers failing to make payments equivalent to at least 1.5% of the outstanding mortgage balance or where the property is in possession.

Mortgage lending was also hit in the second quarter with gross advances falling by £6.3bn to £52.4bn. Year on year, mortgage lending slumped by almost a third, to the lowest level since the worst of the Covid-19 collapse in lending in the second quarter of 2020.

Lewis Shaw, founder of Mansfield-based Shaw Financial Services, told the news agency Newspage a “mortgage meltdown” is approaching, unless the Bank of England changes its approach.

Shaw said: “The speed at which mortgage arrears are increasing is terrifying and should give cause to pause at the next Bank of England interest rate meeting. This is dire data, and we know that it’s about to get an awful lot worse with 1.6m mortgage holders due to renew over the next 12 months at significantly higher rates than anyone has been used to for well over a decade.”

Simon Gammon, managing partner at the finance arm of estate agents Knight Frank, said the proportion of mortgage payers falling behind with payments remained low at just 1%, despite the “sizeable jump in arrears”.

He said: “That’s because the vast majority of outstanding mortgages were issued under the post-global financial crisis regime, which was much more stringent when it comes to affordability.”

However, while homeowners were more likely to make cuts to other spending before falling behind with mortgage payments, buy-to-let landlords may take a different view, he said.

“We are more likely to see arrears in the buy-to-let sector, where landlords face a unique set of challenges. If a landlord finds their mortgage is no longer affordable, or the rent no longer covers their outgoings, they only have two choices – sell or default. If they opt to sell, they may have to wait up to a year for the tenancy to end, unless they are willing to sell with a tenancy in place, which is more difficult.

“Landlords are also more likely to opt to default than those struggling with a mortgage secured against their main residence, so this is an area to watch,” he added.

Incoming Bank of England deputy governor Sarah Breeden said she agreed with her future colleagues on the monetary policy committee (MPC), which sets UK interest rates, that inflation may fall at a slower pace next year than expected, forcing the central bank to keep the cost of borrowing higher for longer than expected.

Breeden, who will replace Jon Cunliffe as the Bank’s deputy governor for financial stability after the MPC’s meeting next week, said there was also a risk that growth and unemployment will worsen.

skip past newsletter promotion

after newsletter promotion

“I will, after November, be very careful in balancing those two factors: the risk of inflation becoming embedded through more persistent, second-round effects, as well as the impact of tightening coming through,” she told parliament’s Treasury Committee in a hearing convened to approve to her appointment.

“The challenge right now is that wages are high and rising and there is a real risk that second-round effects means that this inflation becomes embedded,” she said, adding that in keeping a lid on inflation, “it is not our intention to cause a recession”.

The MPC is expected to raise interest rates by a quarter point to 5.5% on 21 September, raising the average mortgage payments by £3,000 a year for a household that refinances a 2-year fixed product.

Breeden said she expected inflation to be “around the [Bank of England’s] 2% target in two years’ time”.

Starting a family comes with an entirely new set of responsibilities. One of the most important, yet frequently overlooked, necessities is setting up a will. This crucial document outlines tons of important details should you pass away, including what happens to your child.

Estate planning for parents can be broken down into just a few digestible steps. Here’s everything you need to think about, plus tips on how to organize all of your documents.

Estate Planning for New Parents

1. Draft a Will

About 67% of Americans don’t have a will. Setting up a will can be simpler than it seems. A will is a document that outlines how you want things handled after you pass away, including distribution of assets and how any minor children to be cared for.

While some people with complex investments and multiple properties may want to hire a lawyer for help, younger, healthy individuals can seek out online services that can walk them through the steps to make a will and sometimes have no initial cost.

Then, you can follow the execution instructions, which typically include signing your will in front of eligible witnesses. Check your state’s individual requirements. Sometimes, you must have your will notarized in order to become valid. Many banks and public libraries offer this service for free.

If you’re married, consider drafting a joint will with your spouse. This gives you the ability to plan for different scenarios, like what happens when one spouse passes away versus both passing away at the same time. Remember to regularly update your will whenever a major life change occurs, like having another child or adding new major assets. 💡 Quick Tip: We all know it’s good to have a will in place, but who has the time? These days, you can create a complete and customized estate plan online in as little as 15 minutes.

2. Choose an Executor

When you’re setting up a will, you’ll need to choose an executor. This is the person responsible for handling the legal and logistical aspects of disbursing your assets. They are also responsible for filing any remaining taxes and settling your debts.

Consequently, your executor should be someone you trust and who has the ability to handle the tasks involved. This is especially important when you have young children because the executor’s ability to tie up your finances will impact your kids’ inheritance.

Once you choose an executor, let them know that you’ve chosen them. Give them a quick rundown of what to expect, and also let them know where to find your will and other relevant documents.

3. Name a Guardian

When you start having kids, you also need to name a guardian to care for them if you pass away before they reach legal adulthood. There are a lot of things to consider when making this important decision.

First, think about the potential guardian’s ability to care for children. Are their grandparents too old to take care of them? Does the guardian live far away from other friends and family who could serve as a support system?

Also consider their financial capabilities and their ability to manage any assets you leave to help pay for your kids’ expenses.

Finally, think about your values and who would raise your children in a way that’s similar to your own parenting style. Also realize that your kids will be going through a tough time, so their guardian would ideally be someone whom they trust and would provide emotional comfort.

If you have more than one child, make sure you name a guardian for each one, even if it’s the same person. That means you need to update your will every time you have a new baby. Be as explicit as possible when naming a guardian; for instance, if you pick a sibling and their spouse, name both individuals as coguardians.

4. Set Up the Right Accounts

Some types of accounts may help you pass on your assets without having to pay as much in taxes. It’s an important part of the estate planning process and can help you maximize the amount of money you’re able to pass onto your kids. A trust fund can protect the money from being spent too quickly, either by the guardian or your children themselves.

You can implement safeguards as to how much money can be taken out and when. Even if your kids are of legal age, you can put annual withdrawal limits on the trust to prevent a young adult from overspending. Alternatively, even if you pick a guardian to oversee the emotional wellbeing of your children, that same person may not be the best at handling money. Choosing a trust can limit their spending on behalf of your children as well.

There are many different types of trusts, so you may consider consulting an estate planning attorney to choose the best one for your family’s needs. 💡 Quick Tip: A trust is a customized estate planning tool that can be helpful for your heirs in addition to a will.

5. Designate Beneficiaries

The final step of estate planning for parents is to designate a beneficiary for every account and insurance policy you have. Include bank accounts, retirement and other investment accounts, and life insurance policies.

When choosing beneficiaries, find out how each type of account is taxed for the recipient. Also create a list of all of your account numbers and other pertinent details and include them with your will. This makes it easy for your executor to locate all of your assets. Include debt information as well, like your mortgage and/or auto loan servicer.

You can also update beneficiaries as life changes. For instance, you might initially name your spouse as your life insurance beneficiary. But if they pass away before you, it’s time to update that designation to someone else.

[embedded content]

6. Safely Store Your Documents

Once you’ve drafted your will and signed it in accordance with your state’s laws, it’s time to store all of the appropriate estate planning documents to make it easy for your executor and beneficiaries to access.

Lots of documents are now stored online, but you’ll still need to keep your original, signed will in physical form. You can keep it in a fire-proof box at home, or in a safety deposit box at your local bank. Be sure your executor knows where and how to access your documents.

7. Outline Access to Financial Accounts

Remember to keep an up-to-date list of all your financial accounts that need to be taken care of. Bank statements should include the account numbers to make it easy for your executor to find. Also include the location of any valuable items, like art or jewelry.

Finally, it’s helpful to include the contact information for any professionals you work with, like an accountant, financial advisor, and estate attorney. Include insurance policy numbers, loan details, credit card numbers, and any other financial accounts that would need to be closed.

The Takeaway

Estate planning for parents isn’t a one-time event. Get started when you have your first child, but also review your intentions and make changes at least once a year. That way, you always have an up-to-date and comprehensive will that reflects your current financials and family structure.

When you want to make things easier on your loved ones in the future, SoFi can help. We partnered with Trust & Will, the leading online estate planning platform, to give our members 15% off their trust, will, or guardianship. The forms are fast, secure, and easy to use.

Create a complete and customized estate plan in as little as 15 minutes.

Coverage and pricing is subject to eligibility and underwriting criteria.

Ladder Insurance Services, LLC (CA license # OK22568; AR license # 3000140372) distributes term life insurance products issued by multiple insurers- for further details see ladderlife.com. All insurance products are governed by the terms set forth in the applicable insurance policy. Each insurer has financial responsibility for its own products.

Ladder, SoFi and SoFi Agency are separate, independent entities and are not responsible for the financial condition, business, or legal obligations of the other, Social Finance. Inc. (SoFi) and Social Finance Life Insurance Agency, LLC (SoFi Agency) do not issue, underwrite insurance or pay claims under Ladder Life™ policies. SoFi is compensated by Ladder for each issued term life policy.

SoFi Agency and its affiliates do not guarantee the services of any insurance company.

All services from Ladder Insurance Services, LLC are their own. Once you reach Ladder, SoFi is not involved and has no control over the products or services involved. The Ladder service is limited to documents and does not provide legal advice. Individual circumstances are unique and using documents provided is not a substitute for obtaining legal advice.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

The short answer is, yes, estate planning can be a smart move for everyone.

Though it’s not much fun to think about what will happen to your loved ones after you are gone, doing some estate planning early on, and readjusting it as needed throughout your lifetime, can help you prepare for the future and protect the people you care about.

One of the biggest reasons why is that without an estate plan, any assets you have may not go to the people you would have wanted to have them. And, if you have children, you won’t have a say in who becomes their guardian. Not having an estate plan can also create a lot of legal and administrative headaches for your family members and friends.

Contrary to what many people assume, you don’t have to be old, rich, or have children to benefit from making a financial plan for after you are gone.

Read on to learn what estate planning is all about and what you can do to get started.

What Is an Estate Plan?

Estate planning is deciding in advance and in writing who will get your assets and money after your death or in the event that you become incapacitated.

It can be as simple as designating certain people as your beneficiaries on your financial accounts. Estate planning also typically includes creating a will. It can also include setting up trusts and creating a living will that can be used should you ever become incapacitated.

Your “estate” is simply everything you own — money and assets, including your home and your car — at the time of your death.

Your debts are also part of your estate. Anything you owe on credit cards and loans may have to be paid off first by your estate before any further money or assets are distributed to your heirs.

Estate planning is not entirely about money, though. It may also leave instructions for how your incapacitation or death may be handled. For instance, you may not want to be kept on a life-support system if you were in a coma. You may want to be cremated instead of buried. These instructions can be included in your estate planning.

An estate plan may also include choosing a guardian for your children and any specific wishes regarding how you want them to be raised. 💡 Quick Tip: We all know it’s good to have a will in place, but who has the time? These days, you can create a complete and customized estate plan online in as little as 15 minutes.

The Importance of an Estate Plan

An estate plan can be beneficial no matter what your age, income, assets, or family status. Below are some key reasons why you may want to consider estate planning.

You Decide Where Your Assets Will Go

If you don’t have beneficiaries named in an estate plan, the courts will determine who gets your assets. That might be your closest kin (possibly someone you wouldn’t want to have your inheritance), and if you have none, the state may take those assets.

Likely you have someone who you would prefer to leave assets to, and if not, you can choose a charity.

You Have Children

If you have children, it’s important for you to consider how you want them cared for if you and your spouse were to pass away, and who you would want to be their guardians.

Your estate plan can even outline how you hope to pass on aspects of your life such as religion, education, and other values. You can also set up a trust so that your children receive an inheritance once they are 18.

It Can Help Avoid Legal Headaches

If you have beneficiaries you want to leave your assets to, having an estate plan and/or will can minimize the legal headache your loved ones have to deal with.

Without any kind of estate plan, a probate court may have to determine how assets are divided, and this can take months or years, delaying those assets making it to the people you want to have them.

It Can Help Prevent Family Conflict

Your family members may all get along well, but it’s a good idea to write a will so that things remain harmonious.

Regardless of the size of your estate, some careful estate planning can help prevent your family members from arguing over who gets what, whether it’s a small tiff or a full-on lawsuit.

It Can Ease the Financial Burden of Final Costs

Many people don’t consider planning their own funerals, and that may leave an emotional and financial burden on their loved ones.

A funeral can cost, on average, around $7,900, and a cremation about $6,900. Consider whether your loved ones would be in a financial situation to be able to afford to cover that expense, plus any others involved with your final arrangements.

Taking these final costs into consideration can be a part of your estate plan. You might decide to set aside funds to cover your funeral expenses.

You can do this with a “payable on death” account, which can be set up through your bank and allows the designated beneficiaries to receive the money in the account when you pass away.

Or, you might elect to purchase a prepaid funeral plan, which sends money directly to the funeral home to cover a casket, floral arrangements, service, and other aspects of your funeral. You may want to keep in mind, however, that prepaying for a funeral can lead to a loss of money if the funeral home goes out of business.

[embedded content]

What’s Included In an Estate Plan

While your estate plan will be unique to your own situation, there are a few things you might consider including.

A Will

Your will is the actual document that outlines who your beneficiaries are and what they will receive upon your passing. It may also identify a guardian if you have young children.

This is also where you can identify the executor, who will carry out the terms of your will.

Recommended: What Happens If You Die Without a Will?

Life Insurance Policy

Having this policy information with the rest of your estate plan makes it easy for your family to file a claim with your insurance company upon your death.

A Living Will

Death is not the only situation in which you may be unable to make a decision. You may be alive yet incapacitated, and in this scenario it can be difficult for your loved ones to know what you want them to do.

Writing a living will can be highly valuable because it lays out how you want to be treated during your end-of-life care, including specific treatments to take or refrain from taking.

A living will is often combined with a durable power of attorney, a legal document that can allow a surrogate to make decisions on behalf of the incapacitated individual.

Letter of Intent

This letter is directed to your executor, and provides instructions for carrying out your wishes in regards to your will, and possibly also funeral arrangements.

A Trust

If you have a sizable inheritance for your beneficiaries and don’t want them to have access to all the funds all at once, you can establish a trust with rules about how and when they receive the money.

For example, you could stipulate that your children receive a fixed allowance each month until they graduate college or get married, or that they use the money for college. 💡 Quick Tip: A trust is a customized estate planning tool that can be helpful for your heirs in addition to a will.

Key Account Information

You might also consider providing account numbers and passwords for bank accounts, investment accounts, and other important accounts that your family will need access to. This can make life much simpler for your loved ones.

Recommended: What Is the Difference Between Will and Estate Planning?

The Takeaway

Whether you have children and want to ensure they’re taken care of, or you’re single and would like your assets to go to certain people or a charity you care about, it’s wise to have a basic estate plan.

Having a financial plan in place in the event that you pass away or become incapacitated can protect surviving family members from unnecessary financial, legal, and emotional stress.

When you want to make things easier on your loved ones in the future, SoFi can help. We partnered with Trust & Will, the leading online estate planning platform, to give our members 15% off their trust, will, or guardianship. The forms are fast, secure, and easy to use.

Create a complete and customized estate plan in as little as 15 minutes.

Coverage and pricing is subject to eligibility and underwriting criteria.

Ladder Insurance Services, LLC (CA license # OK22568; AR license # 3000140372) distributes term life insurance products issued by multiple insurers- for further details see ladderlife.com. All insurance products are governed by the terms set forth in the applicable insurance policy. Each insurer has financial responsibility for its own products.

Ladder, SoFi and SoFi Agency are separate, independent entities and are not responsible for the financial condition, business, or legal obligations of the other, Social Finance. Inc. (SoFi) and Social Finance Life Insurance Agency, LLC (SoFi Agency) do not issue, underwrite insurance or pay claims under Ladder Life™ policies. SoFi is compensated by Ladder for each issued term life policy.

SoFi Agency and its affiliates do not guarantee the services of any insurance company.

All services from Ladder Insurance Services, LLC are their own. Once you reach Ladder, SoFi is not involved and has no control over the products or services involved. The Ladder service is limited to documents and does not provide legal advice. Individual circumstances are unique and using documents provided is not a substitute for obtaining legal advice.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

HSBC and NatWest cut mortgage rates again as rivals tipped to follow

Decision will ease some pressure on UK homebuyers and people seeking remortgage deals

HSBC and NatWest have announced a fresh round of mortgage rate cuts and Britain’s remaining large lenders are expected to follow suit in a move that will ease some of the pressure on hard-pressed Britons.

HSBC said it was cutting rates across many of its new fixed products – including some of its first-time buyer, home mover and remortgage deals – with effect fromTuesday, when full details of the reductions will be published.

Third of UK mortgage holders ‘do not think they will pay it off by 65’Read more

Fellow high street lender NatWest said it would also be cutting rates from Tuesday.

The latest reductions will improve conditions for homebuyers and those looking to remortgage on to a new deal.

NatWest announced reductions of up to 0.35 percentage points on selected fixed deals. A five-year fixed rate deal aimed at homebuyers with a 5% deposit that is currently priced at 6.39% will result in its rate being cut to 6.04% at the bank.

Mortgage costs had been rising relentlessly for months but UK lenders have been reducing their rates since the second half of July after it emerged that UK inflation fell further than expected in June, prompting speculation that the Bank of England would not raise interest rates by as much as previously expected. The Bank’s base rate is 5.25% after an increase from 5% in August.

Nicholas Mendes, a mortgage technical manager at the broker John Charcol, said HSBC had “laid down the gauntlet and shown they mean business … This is their second rate reduction in a week, along with criteria changes which extend terms to 40 years.”

Accord Mortgages, part of Yorkshire Building Society, also said that all of its fixed rates were being cut by 0.20 percentage points from Tuesday.

Last week, Nationwide Building Society reduced some of its fixed and tracker rates by up to 0.15 percentage points.

skip past newsletter promotion

after newsletter promotion

Stephen Perkins, the managing director of the broker firm Yellow Brick Mortgages, said: “All these rate reductions are starting to feel like an avalanche … No doubt there will be more of these reductions over the week, as all lenders follow in a conga line.”

Lewis Shaw, the owner of the broker Shaw Financial Services, said that with NatWest following hot on the heels of HSBC, “There’s every chance we could see the remaining big four [Lloyds Banking Group, Barclays, Nationwide and Santander] come to the party this week, too.

“It would appear that lenders are struggling to get new business, and the rate tap is the only tool they can turn to.”

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

Your credit score may improve if your collection debt is reported to a new credit scoring model—FICO 9®, FICO 10®, VantageScore 3.0® or VantageScore 4.0®. Most creditors still report to old scoring models, so it’s unlikely paying off the debt will improve your credit score.

If you’ve gotten behind on payments to a creditor or lender, your debt could be sent to collections after around 120 days of missed payments. If this has happened to you, your credit score has likely taken a hit and you may be asking, “Does paying off collections improve your credit score?”

Find out what it means to have collections debt, how it affects your credit and what you can do to raise your score after a hit from collections.

In This Piece:

What Is Collections Debt?

When you default on a payment, the company you owe may sell your debt to a third-party collection agency. When this happens, it means your debt has gone to collections and debt collectors from the collection agency will now try to contact you for payment.

There are many kinds of debts that can be sent to collections, including:

Credit card payments

Student loans

Medical bills

Rent payments

Utility payments

Auto loans

Personal loans

Tax debt

The time it takes the original creditor to transfer your debt to collections varies. Some contracts may have a grace period where you can still pay your debt after it’s due. In other cases, creditors may send you to collections the day after your payment is due.

How Does Collections Debt Affect Your Credit Score?

Collections debt shows up as a negative mark on your credit and, as a result, will significantly harm your credit. This is because collections fall under the category of payment history, which accounts for 35% of your FICO credit score, making it the biggest impact on your score.

The effect on your credit may depend on what your score was to begin with. For example, a score in the 700s may take a more dramatic hit than a score in the 500s.

It also depends on the type of debt you have in collections. Recent changes to medical collection debt mean unpaid bills under $500 won’t be reported to credit bureaus, and paid medical collection debt won’t be reported, thus won’t hurt your credit score either.

The impact of negative collection marks also decreases with time and eventually falls off your report, generally after seven years, as part of the Fair Credit Reporting Act (FCRA).

Does Paying Collections Help Your Credit Score?

Paying off collections can help your credit score if the lender reports to new credit scoring models, including FICO 9®, FICO 10®, VantageScore 3.0® and VantageScore 4.0®. These models ignore collections with a balance of zero, so you’ll see a boost in your score if you pay off collection debt.

However, if your lender reports to older scoring models, which most do, it’s unlikely you’ll see a difference in your score even if you pay the debt, as these models don’t lessen a negative mark from collections regardless of if it’s marked as paid or unpaid.

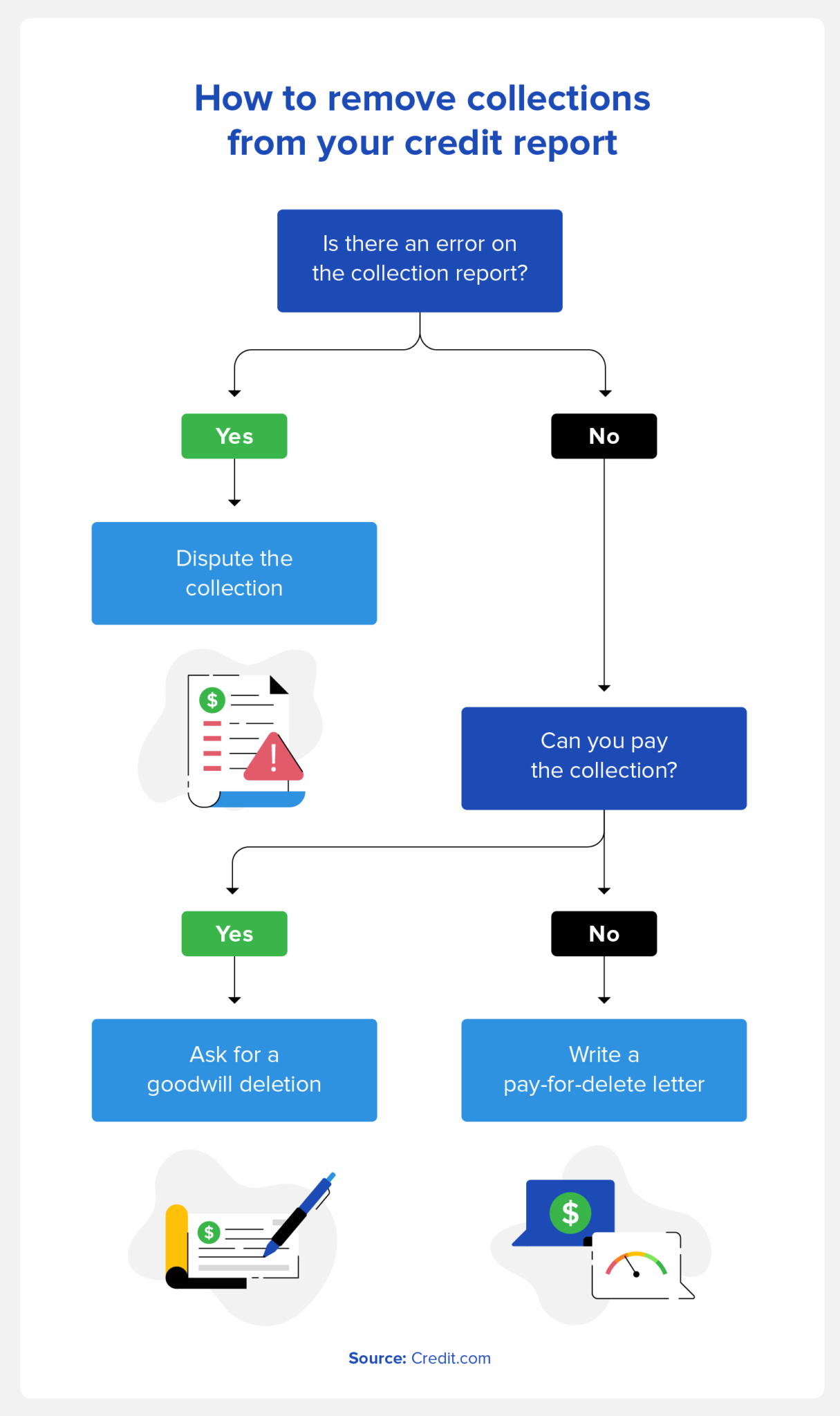

How to Remove Collections from Your Credit Report

There are a few methods for removing collections debt from your credit report. Keep in mind that results may vary as each individual’s financial situation is different. Here are a few ways you can attempt to get collections removed from your report.

Dispute Errors

You have the right to dispute any items on your credit report that are inaccurate or outdated. Here are the steps to take to find and challenge errors on your credit report:

Get copies of your credit report from all three bureaus—Equifax®, Experian® and TransUnion®. You can get one free copy per bureau a year at AnnualCreditReport.com.

Look for mistakes like collections past the statute of limitations or debt that isn’t yours.

If you find a mistake or need more information, send a 609 letter. This letter requires the bureaus to verify or correct items you’ve called out within 30 and 45 days.

Once you have proof of an error, you can write a dispute letter asking for the incorrect item to be removed. This can be filed online with the major credit bureaus or mailed.

Make sure to keep a record of all correspondence with bureaus.

Removing mistakes on your credit report can help raise your credit score, depending on various factors. However, the process of disputing errors can be difficult and long. Consider using a professional credit repair service that has experience working with credit bureaus, especially if you have a lot of inaccurate collection accounts or a more complicated situation.

Ask for a Goodwill Deletion

If you have an otherwise positive credit history and a long-standing relationship with the creditor of your collection, you may be able to receive a goodwill deletion.

This process begins with writing a goodwill letter to the original creditor of the collections, which should include:

Time with creditor

Positive items on your credit report

Intention to stay in good standing

Request for a line item adjustment

If successful, the creditor will delete the item you’ve highlighted as a gesture of goodwill.

Write a Pay for delete Letter

You may be able to arrange a deal with your collection agency to delete the collection account in exchange for payment. This is done with a pay for delete letter.

Keep in mind that not all agencies accept pay for delete letters, especially banks or larger creditors. Collection agencies tend to sell debts, which means your debt may end up with a new agency where you can try this method again.

To write a pay for delete letter, include the following information in your letter:

Dates

Proposed payment amount (can be less than the amount owed)

Terms of negotiation

Before resorting to this method, make sure the debt is verified as yours with a 609 letter. Also, make sure to get any communication from the collection agency documented in writing and keep a copy of your letter.

Is It Worth It to Pay Off Collections?

While paying off collections may not always improve your credit score, it can have other financial benefits. Additionally, there are potential consequences for not paying collections. Ultimately, the decision depends on your financial situation and goals. Here are some reasons to pay your collection debt:

Dodge lawsuits: If you don’t pay off your collection debt, the debt collectors may sue you.

Avoid interest and fees: You may rack up additional interest and fees on this debt.

Secure future loans: Some lenders won’t work with anyone with collections on their credit report. They can be flexible if you can prove you have paid the debt or a repayment plan is in place.

Increase credit score: Depending on your circumstances and credit reporting model, you may be able to increase your credit score by paying the debt.

If your debt has already passed the statute of limitations, debt collectors most likely won’t be able to continue asking for repayment or pursue legal action against you.

However, making a payment or a written acknowledgment of the debt could restart that time period. Once the time period restarts, you could be sued for the debt again. So, if you decide to pay the debt, it’s best to pay it all at once instead of partial payments to avoid restarting the statute of limitations.

How to Improve Your Credit after Collections

If none of the above methods for removing collections from your credit report worked for you, there are other ways to improve your credit. Here are some ways to repair your credit after collections:

Pay on time: Pay your other bills on time to avoid more collection debt and to positively affect your credit.

Try to keep your credit accounts open: Credit age is an important factor for your credit score, and closing an old account can decrease the average age of your accounts and lower your score.

Pay down credit card balances: If you have a large credit card balance, paying down that balance can help lower your credit utilization rate and raise your score.

Think before opening new lines of credit: When you apply for credit, a hard inquiry is made on your report, which lowers your score.

Use a credit repair service: Professional credit repair companies can help you address errors on your report and find other ways to increase your score.

It’s a good idea to follow these tips even if your collection debt is reported to a newer credit scoring model, as it still may take time to see improvements to your credit score.

Debt Collections FAQ

Have more questions about debt collections? Check out the answers to these common collections questions.

What Are Your Debt Collection Rights?

If you haven’t found out already, debt collectors can be very persistent. It’s important you know your debt collection rights and how a debt collection agency is legally allowed to handle your accounts and communicate with you.

As outlined by the Fair Debt Collection Practices Act (FDCPA), debt collectors have to follow these guidelines:

Written Notice: Debt collectors must provide written notice with information about your debt within five days of contacting you.

Time and place: They can’t contact you before 8 a.m. or after 9 p.m. They also can’t contact you at work if you’ve communicated you’re not allowed to take personal calls at work.

Harass or abuse: Collection agencies can’t yell at you, threaten violence, or use obscene language.

Deception: They can’t lie about their identity, how much you owe, your legal rights, or any other form of deception.

Privacy: Debt collectors can receive your contact information (address, phone number, work address) from certain people, but they can’t contact people more than once. They can only contact your spouse, guardian, or attorney.

Attorney correspondence: If you’re being represented by an attorney, debt collectors may only communicate with your attorney once they’re aware of your representation.

If a debt collector has infringed on any of these rights, you can file a report with your state’s Attorney General’s office or the Federal Trade Commission (FTC).

How Long Will Collections Debt Stay on My Credit Report?

Collections debt stays on your credit report for at least seven years as part of the FCRA, regardless of whether you’ve paid the debt or not.

The debt doesn’t go away necessarily, but the negative item will drop off your credit report eventually, and you can no longer be sued for the debt after the statute of limitation time period passes.

How Many Points Does a Collection Drop Your Credit Score?

A collection debt’s impact on your credit score varies, but generally speaking, it could drop your score significantly. The impact depends on your initial score, with higher scores taking a bigger hit than lower scores. Multiple collections on your credit report could drop your score even more.

How Many Points Will My Credit Score Increase When I Pay off Collections?

Your credit score may not increase at all when you pay off collections. However, if your debt is reported using a newer credit scoring model, your score may increase by however many points were impacted by the collections debt.

It would also depend on the time passed since getting the negative mark. You’re more likely to see a positive increase from paying off the collection if it was recently incurred than a collection you’ve had for six years since the effects on your credit lessen over time.

If late payments are hurting your credit score, you may need a little extra help understanding how your credit is impacted and what you can do about it. Try ExtraCredit to help track your credit score, with other features available to help you work to meet your credit’s full potential.

Fill out and submit the Social Security Form SS-5 if you are updating or replacing your existing Social Security card, or if you’re requesting one for the first time. Form SS-5 is one page, but it has 18 boxes that request 22 different types of information.

Even though Social Security Form SS-5 includes instructions, filling it out can be confusing. Here’s what you need to know to understand and accurately complete it.

What is Form SS-5?

Form SS-5 is for requesting a Social Security card for the first time, replacing an existing Social Security card or changing information associated with your Social Security record

. It is a part of the application process with the Social Security Administration (SSA), and typically you must provide supporting documentation to prove your identity.

Social Security Form SS-5

How to fill out Form SS-5

Form SS-5 has 18 boxes — some are optional, but you must fill out every field that applies to you. The Social Security Administration might deny your application if you don’t provide all of the relevant information.

Step 1: Provide your current name and previous names

For box 1, all applicants must fill out the first line. Spell out your current name as you want it spelled on your Social Security card. If you had a different name at birth — the one on your birth certificate — write it on the second line. If you’ve used any other legal names, such as if you’ve changed your name before, include those names in the third line.

Step 2: Provide your Social Security number

Box 2 requires you to fill in your Social Security number if you already have one. If you are requesting your first Social Security card, leave this line blank.

Step 3: Write in information about your birth

Boxes 3 and 4 are side by side, so be sure you fill in both boxes. In box 3, provide your place of birth. This should match your birth certificate. Spell out the places rather than abbreviating them.

In box 4, enter your date of birth. Use numbers only, and put the full four digits for the year. This should also match your other documentation.

Step 4: Indicate your citizenship status

Select the option in box 5 that matches your citizenship status. You may only select one category. If you check a box for “Legal Alien Not Allowed to Work” or “Other,” you’ll need to provide documentation for why you need a Social Security card. The documentation can be from a federal, state or local agency. If you’re not sure if you need a Social Security number, you can call the SSA to ask.

Step 5: Decide if you want to indicate your ethnicity and race (optional)

Boxes 6 and 7 are also side by side. These boxes are optional, and your application will not be affected if you skip both boxes. If you want to include this information, check the appropriate answer in box 6 to categorize your ethnic identity. For box 7, check as many boxes as necessary to capture your racial identity.

Step 6: Mark your preferred gender identity

Box 8 lets you mark your preferred gender identity. Although the form uses the term “sex,” you are allowed to choose which gender you want associated with your Social Security record. You can select a gender identity that doesn’t match the one currently on record, and you aren’t required to provide legal or medical records to support the gender you select on your application.

🤓Nerdy Tip

The SSA currently designates binary genders only for Social Security purposes. The agency is investigating how to record nonbinary identities for programs in the future.

Step 7: Provide your parents’ names and Social Security numbers

Box 9A requires you to provide your mother’s birth name. This might be different from her current name if she legally changed her name for any reason, such as getting married. For box 9B, fill in your mother’s Social Security number.

For box 10A, fill in your father’s birth name as well. This might be different from his current name if he legally changed his name for any reason, such as getting married. For box 10B, fill in your father’s Social Security number.

If you don’t know the Social Security number for one or both of your parents and have no way of finding out, check the box for “Unknown” on the right. Don’t leave the box blank — you should either fill in the Social Security number or check the box for “Unknown.”

Step 8: Indicate whether you already have a Social Security number

For box 11, check the box that applies to you:

“Yes” if you have a Social Security number and are requesting a new card or updating the information.

“No” if you’ve never had a Social Security number and are requesting one for the first time.

“Don’t Know” if you are unsure if you have a Social Security number.

Step 9: If you checked “Yes” for box 11, fill in boxes 12 and 13

If you answered “Yes” for box 11, you must fill out box 12 to complete the application. This information relates to your old Social Security card. For box 12, put your name as it appears on your most recent Social Security card. Spell it the same as it appears on the card, even if it’s misspelled on the card.

If you or your parent used a different date of birth when applying for your previous Social Security card — as in, you made a typo — enter that date in box 13. For an application where the date of birth in box 4 differs from the date of birth you entered in box 13, you’ll need to provide documentation to prove that the date of birth in box 4 is your actual date of birth, such as an amended birth certificate.

If you’ve always used the same date of birth for Social Security card documentation, leave box 13 blank.

Step 10: Fill in boxes 14, 15 and 16

Enter the current date in box 14. In box 15, enter a phone number where you can be reached during the daytime, such as a cell phone number.

In box 16, put your complete mailing address. Only use an address where you have regular access to receive mail and will be able to get your card in the mail within seven to 14 days of submitting your application. Don’t abbreviate any words in the address. For example, spell out “Street” instead of using “St.”

Step 11: Sign the form and indicate your relationship to the person requesting a card

Sign the form in box 17. Be sure to read the statement right above box 17 before signing. If you are unsure who should sign the application, read the instructions on page 3 of the application. For box 17, there is a section titled “WHO CAN SIGN THE APPLICATION?” that outlines who should sign in certain situations.

In box 18, check the box that describes your relationship to the person requesting a card:

“Self” means you are requesting a card for yourself.

“Natural Or Adoptive Parent” means you are either a biological parent or a parent who adopted the child requesting the card.

“Legal Guardian” means you have court-ordered custody of the child requesting the card and the authority to fill out the form on the child’s behalf

.

“Other Specify” means the other three options don’t fit your relationship to the child or person requesting the card. If you choose this option, you need to fill in the blank with your relationship to the person.

Did you know…

Because Form SS-5 is a legal document, if you intentionally lie on the form and sign it, you could be committing fraud. If you are unsure about any of the information you put on the form, take a break to double-check that everything is accurate.

How to submit Form SS-5

Submitting Form SS-5 online

In most cases, you can fill out the SS-5 form online on the SSA’s website

. You can usually submit the form online if you are changing your name or requesting a Social Security number for the first time. You will still need to provide your supporting documentation in person at a Social Security office to complete your application.

However, if you live in New Hampshire, Oklahoma, Alaska or a U.S. territory, you might need to submit the form through the mail if you want to replace your Social Security card. That means you’ll need to print out the form, fill it out and mail it (along with your supporting documents) to your nearest Social Security office.

Submitting Form SS-5 in person

You’ll need to submit the SS-5 form in person if you’re changing any of the following information on your Social Security card or record:

Gender identity.

Date or place of birth.

A parent’s name.

Citizenship status.

🤓Nerdy Tip

The SSA occasionally uses the terms “sex identification” and “gender identity” interchangeably when referring to Social Security records. However, “sex identification” is more common in the agency’s documents.

To submit your form in person:

Download and fill out the S-55 form. You can fill it out digitally, then print it, or print it first, then fill it out by hand.

Gather the required documentation. All records must be original versions or a form of certification, such as a signature or raised seal. You can’t submit photocopies.

Locate the SSA office you want to visit.

Call ahead to ensure you don’t need an appointment to speak with someone.

4 tips for submitting Form SS-5

Gather the information you need before starting. This can make the process go more smoothly. This is especially true for information you might need from someone else, such as your mother’s Social Security number.

Read the instructions before filling out a box. If it’s not immediately clear to you what you need to put in a box, take a minute to read the instructions. If you still have questions, call your local SSA office to ask what information you should include. The time spent clarifying the information will be much shorter than time spent redoing the application if you fill it out incorrectly.

Double-check the information before submitting it. Read through the completed application carefully and double-check that everything is correct, especially your contact information. If the SSA has a question, this is how they will contact you.

Check the mail often. It can take seven to 14 days to get your Social Security card in the mail, and it could come anytime in that range. Check your mail frequently to ensure you get it when it’s delivered; don’t leave it in a mailbox where it could be stolen.

Frequently asked questions

Can I submit Form SS-5 online?

Yes, you can submit the form online through the SSA website if you are updating your name or requesting a card for the first time. For other updates, you might have to submit the form in person.

What do I need to send in with my Form SS-5?

What you need to submit as documentation depends on what you are requesting. You can see the SSA’s list of basic documentation requirements. For any additional requirements, contact a local SSA office.

Can someone else fill out Form SS-5 for me?

Yes, someone else can fill out your form for you, but they need to sign in box 17 and indicate their relationship to you in box 18.

An internshipship is an opportunity to work in a field that interests you, gain valuable work experience, enhance your college resume, and possibly even earn some extra money.

While internships are more commonly available to college students, it may be possible to get an internship when you’re still in high school.

Read on to learn more about high school internships, including how they work, their pros and cons, and how to find one.

What Is the Purpose of an Internship?

An internship is a temporary position that’s often related to a student’s academic field of study or career interests. It offers students a chance to apply lessons learned in the classroom in a professional setting, while also developing additional skills. Internships also give students an opportunity to make connections in their field of interest and determine if they want to pursue further study and a career in that area. Internships also give employers the opportunity to discover and develop future talent.

💡 Quick Tip: Some lenders help you pay down your student loans sooner with reward points you earn along the way.

The Duties of an Intern

The duties of an intern vary from job to job. For example, those interning at a doctor’s office might shadow medical professionals and take notes on patient visits. Those interning at a marketing firm might sit in on marketing meetings and assist in any communication needs.

An internship experience can be somewhat similar to an entry-level employee position. However, there is typically an educational component. The point is to learn more about the career path, not just get coffee or file the office mail (though you may be asked to do this, too).

Recommended: Is Getting A Degree In Marketing Worth It?

Pros and Cons of High School Internships

There are plenty of pros when it comes to getting internship experiences in high school. For one, an internship allows you to learn about a particular career path without having to commit to a lifelong job.

Learning about a path early on could help you determine whether you want to go to college (rather than directly enter the working world) and help you decide what you’d like to study in school.

Another pro of completing an internship in high school is gaining new experiences and skills. An internship allows you to learn from professionals and add relevant skills to your resume. This can give you a leg up in applying for jobs in the future.

And, of course, all this experience and new learning make for excellent items to add to any potential college applications. A potential downside to seeking an internship in high school is that they can be hard to find. In addition, the position may not be paid, and might be time-consuming, taking time away from other obligations like homework, studying for SATs, and applying to college.)

Recommended: What is the Hardest Year of High School?

Finding the Right Internship

Finding the perfect internship is a wholly personal experience. A good first step is to consider your interests in both the near and far term. By thinking about career paths you might be interested in, you might identify internship opportunities around you.

However, not every young person knows, or believes they know, exactly what they want to do in the future. But you may have a general interest. For example, if your favorite class is English, an internship at a local newspaper may make sense. If you’re interested in nature, an internship with a local parks and recreation group may make a good fit.

If you’re a high schooler, make a shortlist of interests and sit down with a parent or guardian to identify careers that may fit within these bounds.

Next, it’s time to identify a few companies you might be interested in interning with. Search around for companies near you that may be taking interns. From there, check out career pages on the individual companies to see if they have internship listings. If they don’t, try emailing the company to get in touch with the human resource (HR) department to see what may be available.

One quick tip: While researching and reaching out about internships, make sure to stay realistic about the time commitment. If an internship takes place during the school year, you may only be available in afternoons. Ensure the hiring manager knows the hours you’re available before committing to any long-term work.

Recommended: 10 Ways to Prepare for College

Resources to Find Internships in High School

While there isn’t any centralized listing location for internships for high school students, there are still plenty of places to find information on opportunities.

Schools: You can reach out to school resources like guidance counselors, principals, and individual teachers who may know of companies worth looking into.

Individual companies: Again, seek out information from company websites and reach out to human resource departments to see what may be available.

Job search websites: Check out job search websites, such as Linkedin and Indeed, and search for “Internships in [specific field here].” Make sure to search by location to ensure the internship is nearby.

Friends and family: This is the simplest tip — just ask around. Friends and family members are the ultimate social and work network. Make it known you’re looking for an internship and ask people for their advice on just where to look.

Recommended: College Planning Guide for High School Students

Questions to Ask Before Accepting an Internship

After figuring out your interests, asking your network, and finding an internship opportunity, you may think the work is done. However, there are still a few more questions to ask.

Before accepting an internship offer, make sure to ask about the full details. What are the hours? What can you expect to learn while on the job? What are the specific job duties and how will you be evaluated along the way? Will there be opportunities for mentorship? And finally, one of the most important questions: Is the internship paid?

💡 Quick Tip: It’s a good idea to understand the pros and cons of private student loans and federal student loans before committing to them.

Paid vs. Unpaid Internships

Scoring a paid internship isn’t a guarantee, but it’s not a completely far-fetched idea either. If a paid internship isn’t available, you can always ask about an exchange for class credit. Unpaid internships are a hotly contested issue so just make sure to do whatever feels right and comfortable for your situation.

Also keep in mind that even a paid internship likely won’t pay enough to make a major dent in your college expenses (though it can help).

If you’re concerned about how you and your family will pay for the cost of tuition, a good first step is to fill out the Free Application for Federal Student Aid (FAFSA) with your family. This will let you know if you are eligible for financial aid, including grants, scholarships, work-study, and federal student loans. If those do not cover your costs, you may also consider private student loans.

Private student loans are available through private lenders, including banks, credit unions, and online lenders. Rates and terms vary, depending on the lender. Generally, borrowers (or cosigners) who have strong credit qualify for the lowest rates.

Keep in mind, though, that private loans may not offer the borrower protections — like income-based repayment plans and deferment or forbearance — that automatically come with federal student loans.

If you’ve exhausted all federal student aid options, no-fee private student loans from SoFi can help you pay for school. The online application process is easy, and you can see rates and terms in just minutes. Repayment plans are flexible, so you can find an option that works for your financial plan and budget.

Cover up to 100% of school-certified costs including tuition, books, supplies, room and board, and transportation with a private student loan from SoFi.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

SoFi Private Student Loans Please borrow responsibly. SoFi Private Student Loans are not a substitute for federal loans, grants, and work-study programs. You should exhaust all your federal student aid options before you consider any private loans, including ours. Read our FAQs.