What a difference a few months make in the real estate market. Last summer, home prices were selling on the cheap in many cities across the nation.

Fast forward to spring, and the housing market kind of “sucks.” There’s really no other way to put it.

First off, there’s no inventory. This has been an issue for a while now.

Put simply, there’s just very little out there for an individual or family looking to buy a home, at least in the areas they might want to live.

Sure, there are those properties that have been on the market for months, but there’s a reason they’ve been on the market for months.

And yes, you can probably go to a new community built by a mega home builder and find a house, but it’ll likely be on the fringe of a major city next to empty dirt lots and tractors.

Bad Inventory Rising

Because there is a shortage of homes to buy

Prospective sellers are able to list their duds

Knowing that buyers are becoming increasingly desperate

And may overlook flaws or simply settle as a result of the slim pickings available

Now that the housing market is heating up and the media is (rather obnoxiously) getting on board, inventory is finally rising. Let’s call it an inevitable timing thing.

You see, there is real hope in the housing market. And while hope is good for some, it’s not good for buyers, just sellers who finally see the light after so many years in the dark.

Their real estate agents are giving them the green light to dump their properties while avoiding the lengthy short sale process and nasty credit score ding.

Today, these would-be sellers are able to push the values just that little bit more to sell them as standard sales, instead of going the formerly popular short sale route.

After all, a short sale made sense when there was no hope of getting out unscathed, but now that things are looking up, why not hang on a touch longer and avoid the negative ramifications of selling short?

Unfortunately, this means the individual on the other end is picking up the slack at an inflated price, instead of snagging a deal.

Competition Is Extremely Fierce

Not only are the available homes often less desirable

But the competition for these properties is much higher than normal

Making the housing market a really bad place to be as a buyer

Since no one wants to overpay for a home they don’t even love

Factor in the intense competition and you’ve got a double whammy on your hands.

We’re talking inflating the listing price to make it a standard sale, then receiving multiple bids that often push the final sales price above the original ask.

In other words, today’s buyers are acquiring properties with the future home price appreciation already built in.

And that assumes prices actually do increase – it’s not a foregone conclusion, just a rosy expectation at the moment.

I’m also seeing a lot of the notoriously bad properties rear their ugly heads again. Many of these homes sat on the market for months without a single offer, but now they’re going into escrow in a matter of days.

Something is definitely wrong with this picture. I don’t care how low mortgage rates are…

I’ll Wait for Another Dip

The housing recovery won’t feature home prices that go up in a straight line

Just like the downturn ebbed and flowed despite ultimately declining

There might be windows if you’re patient and keep an eye on things

But do expect home prices to keep on rising, and know that it’s okay to just hold off if you don’t find something you truly love

If I wanted to buy a home, I’d hang on and wait for the temporary madness to come to an end. There’s clearly a bubble mentality in the air again, with everyone and their mother bullish on housing.

Whenever that’s the case, it makes for a rather ominous situation. The increase in inventory involves a ton of previously underwater homes that no one wanted, even at lower prices. Or homes that were taken off market and abruptly thrown back on the MLS.

So why would you buy these same homes today at a significant premium? Because a magazine cover said, “Housing Is Back?”

The economy is still in tatters and things don’t exactly appear bright. If anything, a looming stock market crash seems to be on the horizon.

No, the sky isn’t falling, and housing is indeed on the mend after so many off years. But I do see the current cycle as an unsustainable period of growth that will likely unravel as the year goes on.

It’s going to be a bumpy road to recovery, not just a bottom followed by a surge back to new highs. We’ve seen this optimism in past years, only to watch the wheels fall off time and time again.

If you see something you love, go for it. If you’re worried about the missing the boom, you might want to sit down and reassess the situation.

Read more: Buying a home during a seller’s market.

You’ve done your research, checked your credit reports to make sure they’re accurate, and you’re ready to get serious about buying a car. You feel more than ready to sign on the dotted line and drive home in your new ride.

It could happen. Or, you could drive home in your old vehicle, kicking yourself for having forgotten one of the documents you need to finalize the purchase. Here’s how to lay the groundwork for getting the deal done on the day you’re ready to buy.

Four Steps to Prepare to Buy a Car

Step 1:

You’ll want to talk to your insurance agent about what it will cost to insure the make and model you are considering buying. You don’t want that figure to be a surprise, and you also want to find out how soon you will need to notify your insurer you have the new vehicle.

Step 2:

Talk to your bank or credit union and get pre-approved for the loan you’ll need—and do this close to your planned purchase date. You may get something resembling a blank check (up to a certain maximum) that must be signed by you and the dealer. By getting pre-approved, you will know the total loan amount and interest rate you qualify for. Even if you plan to finance at the dealer, it can’t hurt to come in with a pre-approval; you are far less likely to agree to a longer term or higher interest rate because you really want to drive that new car home today. It can also help you stay within your budget by serving as a solid reminder of how much you planned to spend and how long you were willing to make payments — before the showroom floor made it so hard to remember.

Get matched with a personal

loan that’s right for you today.

Make sure you have your driver’s license and proof of auto insurance with you. You shouldn’t be driving without these documents anyway.

Step 4:

Obvious as this seems, be sure you have a way of funding your down payment. If it’s not cash, make sure the dealer accepts the form of payment you’re planning to use. (If you forget to do this, you would not be the first, but that would be little consolation.)

Expert Tip: Be cautious about having your credit pulled unnecessarily. Each inquiry made for the purpose of extending credit can cause a small, temporary decrease in your credit score. And while inquiries for the purpose of getting a car loan made in a two-week period should count as only one entry, we’ve heard from consumers who have told us their credit scores dropped as the result of multiple auto loan inquiries. Some dealerships now ask customers to fill out a credit application even before a test drive, and there are reports that some have checked credit without customer consent. It can help to keep an eye on your credit through this process for this reason. Hard inquiries into your credit require permission, and it can be illegal for your credit to be pulled without your approval in this manner. You can get a credit report summary and two credit scores, updated monthly for free on Credit.com, to track your standing.

Can You Purchase a Car with a Credit Card?

Speaking of your down payment, you may have wondered if this can be charged to a credit card — or if the entire car can be paid that way. The answer is yes and no. It is possible that the dealership will not accept a credit card payment for the car, as this can come with large merchant fees that lower their profits. However, if your credit is in good standing, then it is still possible.

A better option would be to use your credit card for just the down payment. Not only is this better for your credit, since using all of your available $10,000–$15,000 credit limit can damage your credit score, but it’s more likely to be accepted by the dealer.

Finally, you’ll want to use a credit card that has excellent benefits. An appropriate credit card can earn you big rewards on your car purchase or other auto-related purchases. We have given you a couple examples of worthy rewards cards below.

Planning to Trade In Your Car? Don’t Forget These Items for the Dealership

If you plan to trade in a car, you have a bit more to do.

You will need to bring the following items to the dealership:

Your car’s certificate of title (If it has gone missing, your state department of motor vehicles can tell you how to get it replaced.)

The car’s current registration

Your car keys and the owner’s manual

Your account number or a payment stub if you still have a car loan (We’re going to hope that if this is the case, your car is worth more than you owe.)

A clean car, paying special attention to areas out of sight but convenient for stashing things: under seats, over the visors, in the glovebox and in every corner of the trunk

Besides a new car, expect to come home with a good bit of paperwork. Pay special attention to the purchase and sale agreement. You will need the information there to get or update your insurance — and you might even need it at tax time next year if you bought a car that qualifies for a tax credit.

What Do I Need to Apply for an Auto Loan?

While you won’t need to drive all the way to a dealership to get an auto loan (you can simply apply online), you will still need some important documents in front of you to easily fill out the application.

What do you need?

Proof of identity through an ID or passport

Your credit report, which the lender can pull using your name, address, date of birth and social security number

A valid state-issued driver’s license

Proof of monthly income through pay stubs or social security income receipts

Proof of residence through mortgage statements or utility bills

Contact information for personal references (note: this may not be required)

Vehicle make and model

Proof of car insurance

Payment type (cash, credit, debit, etc.)

Your car’s registration if you are trading in the vehicle

The list is rather long, but having each document will speed up the process and prevent you from going back and forth between your files.

Get Your Auto Loan and Car with the Help of Credit.com

Make sure that you can qualify for an auto loan by checking your free credit score, provided through Experian. From there, you can apply for your auto loan with confidence and compare credit cards that can help you finance your new car.

Frequently Asked Questions

Will my credit rating affect my auto insurance rates?

You should choose auto insurance coverage based on your credit rating and overall coverage needs. Check out Credit.com for car insurance quotes and to compare rates.

How can I find a credit card with a low interest rate to charge my car purchase?

We don’t recommend that you put your entire purchase onto your credit card, but there are cards with low APR or no APR for up to 15 months available to compare. If you can pay off the remaining balance during this period, then these credit cards may be for you.

How good should my credit be to get a credit card that is appropriate for a car purchase?

You mentioned that hard inquiries can affect my credit score. What is a hard inquiry?

A hard inquiry is a credit check that indicates you have applied for credit, usually through a loan. Each time a hard inquiry is pulled from a different lender, your credit score can drop by up to 10 points, because it indicates that a lender has reviewed your credit and that you are trying to open up a new line of credit.

Note: At publishing time, the Chase Sapphire Preferred® Card and American Express Green card are offered through Credit.com product pages, and Credit.com is compensated if our users apply and ultimately sign up for this card. This content is not provided by the card issuer(s). Any opinions expressed are those of Credit.com alone, and have not been reviewed, approved or otherwise endorsed by the issuer(s).

Note: It’s important to remember that interest rates, fees and terms for credit cards, loans and other financial products frequently change. As a result, rates, fees and terms for credit cards, loans and other products cited in these articles may have changed since the date of publication. Please be sure to verify current rates, fees and terms with credit card issuers, banks or other financial institutions directly.

According to the Federal Reserve, consumer debt in the United States in the second quarter of 2021 totaled more than $4.2 billion. So if you’re struggling with debt, you’re definitely not alone. If you’re looking for a way to dig yourself out of debt, a debt consolidation loan could help.

But what is a debt consolidation loan? Find out if it’s the right option for you by learning more about it, including pros and cons. You’ll also find information about other alternatives.

In This Piece

What Is Debt Consolidation?

Debt consolidation occurs when you bring multiple existing debts under a single umbrella. This usually means you use some type of credit or other financial tool to convert multiple debts into a single debt. Debt consolidation loans are one of the most popular ways to consolidate debt.

What Is a Debt Consolidation Loan?

A debt consolidation loan consolidates, or combines, your various debts under a single account.

Pros of Debt Consolidation Loans

Cons of Debt Consolidation Loans

Potentially lower interest rates, especially if you now have the credit score to consolidate high-interest loans under better terms

May require good credit to obtain or get a good rate

A single payment, making it easier to manage your finances

Might leave paid-off credit card and other revolving accounts open, creating an opportunity to run up even more debt than you started with

Your debt possibly spreading out over a greater amount of time, making each monthly payment more affordable

Could potentially temporarily impact your credit score if it involves closing a lot of other accounts

What’s the Difference Between Debt Consolidation and a Personal Loan?

A personal loan is an unsecured loan that you can use for just about anything. In some cases, you could use the funds from a personal loan to consolidate some debts, making it a debt consolidation loan.

However, a loan specifically for the purpose of debt consolidation may be handled a bit differently. For example, in some cases, the lender may not pay the money directly to you. They might pay off your debts directly instead.

Alternatives to Debt Consolidation Loans

Your options depend on your credit, existing assets, and how much debt you want to consolidate. Some alternatives to debt consolidation loans are highlighted below.

1. Refinance Your Mortgage If You Have Equity

If you have equity in your home, you can refinance it or take out a home equity line of credit, or HELOC. These options give you cash you can use to pay down debt.

Pros of Refinancing a Mortgage to Consolidate Debt

Cons of Refinancing a Mortgage to Consolidate Debt

Home equity loans and HELOCs tend to have much lower interest rates than personal loans and credit cards

You use your home as collateral for the debt, which means if you don’t pay it, the lender has a claim on your house

You may be able to deduct interest on home loans to reduce tax burdens

Variable-rate loans could come with increased interest in the future

The total number of payments you need to manage each month is substantially reduced

Credit cards you pay off could be run up again, leaving you with more debt than you started with

You’re less likely to forget to pay a debt related to your home

Tip: Don’t pocket the money that refinancing frees up every month. Instead, use it to create an emergency fund. Once that’s set up, use the money as prepayment against your home loan or to boost retirement savings.

2. Use a Balance Transfer Card

Apply for a balance transfer card if your credit is in good shape, or call a card provider to ask if they’d be interested in offering you a balance transfer option on an existing card. This lets you transfer higher-interest credit card debt to a card with lower interest rates. Some balance transfer cards offer 0% APR for six to eighteen months on balance transfers for new account holders.

Pros of Balance Transfer Cards for Debt Consolidation

Cons of Balance Transfer Cards for Debt Consolidation

Can substantially reduce the cost of credit card debt

Balance transfers usually come with fees of 3% to 5%—still less than your typical interest costs might be on high-interest credit card debt, but something to keep in mind

Makes it easier to pay off credit card debt

It can be tempting to use your old credit cards again, running up more debt and ending up with double the debt you started with

Might let you consolidate multiple cards into a single account for easier management

If you don’t pay off the debt in the introductory period, you could end up with expensive interest fees

Tip: Keep your old credit card accounts open for extra benefits to your credit score. It helps your credit utilization rates and credit age. But avoid using those accounts unless you have the money to pay them immediately.

3. Borrow from Retirement Savings

If you have retirement savings, you might be able to borrow from it to pay off debt. Remember, though, that you’ll need that money later. Only consider this option if you can pay back the money quickly so you don’t lose time building your retirement funds.

Pros of Borrowing From Retirement Savings for Debt Consolidation

Cons of Borrowing From Retirement Savings for Debt Consolidation

Doesn’t require a credit check, so you don’t need a healthy credit file

You might owe taxes and penalties on the money if you withdraw early from your retirement

Interest rates are low, and you’re actually paying it back to your own account

You can borrow against some employer-sponsored retirement plans, but debt consolidation might not be an allowed reason

You could reduce how much money you have in retirement, especially if you can’t pay back the money

Tip: Consider this option as a last resort loan or if you have some money coming in soon, such as from a tax return. If you can pay the money back within a month or two, you don’t have as much to lose.

4. Ask a Friend or Relative for a Loan

If you know someone who has some extra money, it might be worth asking them for a loan at a low interest rate. You can use the money to pay off your debts and make one monthly payment to the person in question.

Pros of Asking Someone for a Loan for Debt Consolidation

Cons of Asking Someone for a Loan for Debt Consolidation

No credit check or requirements

If you blow it, you might ruin an important relationship

Your family member or friend can earn some interest

The IRS can be a real pain when it comes to family loans, so consult a tax professional

Loan payments won’t be reported to your credit reports or potentially help your score

Tip: Treat the transaction as you would with a bank or other lender. Put everything in writing, agree to fees or penalties if you miss payments, and strive to make timely payments.

5. Try Debt Counseling

Debt or credit counseling with a reputable organization can help you create a viable personal budget and potentially negotiate with creditors for better terms. Debt counselors may help you understand how to better manage your income and expenses and leverage debt payoff strategies to get out from under your debt.

Pros of Debt Counseling

Cons of Debt Counseling

Can provide you with some tools to better manage debt

May not reduce the overall cost of your debt

May help you see solutions that you didn’t see before

May rely on you making personal sacrifices in your budget

Helps you pay off debt with your own resources, which can be satisfying

If you don’t work with a reputable organization, you might be scammed out of large fees with promises that the company can’t keep

Tip: Don’t work with debt counseling companies that offer 100% guarantees to reduce or wipe out your debt or that charge excessive fees. These are red flags that could point to scams.

6. Enter a Creditor Assistance Program

Many creditors have assistance programs to help account holders who are experiencing financial distress due to sudden loss of income or an emergency. These programs range from mortgage modifications, which might reduce your interest rate or total monthly payment, to skipping a single payment and having it added onto the end of the loan penalty-free.

Pros of Creditor Assistance Program

Cons of Creditor Assistance Programs

May not require good credit, especially if you have a solid payment history with the creditor

Aren’t always available

Could offer a fast, convenient solution to short-term cashflow issues

You can typically only take advantage of these tools once or once every so often

Tip: Anytime you’re experiencing financial distress or might be late with a payment, don’t ignore the issue. Call your creditor to find out what they might be able to do to help.

7. Bankruptcy

Bankruptcy is a last-resort option that can help you discharge or restructure your debts and make a new start in a few years.

Pros of Bankruptcy

Cons of Bankruptcy

If successful, you can have all or many of your debts discharged

Bankruptcy can be a long and stressful process

You may be able to keep certain assets, such as your home or car

It can dramatically impact your credit in the short term

Filing for bankruptcy establishes an automatic stay, so creditors can’t continue to attempt to collect or foreclose unless the bankruptcy is dismissed

Depending on what type of bankruptcy you file, you may not be able to get credit for a while

Tip: Talk to a bankruptcy attorney about this option before you take action. Most provide free consultations to help you understand if bankruptcy is a good choice for you.

The Bottom Line on Debt Consolidation

If you’re struggling with debt, you’re not alone. And you do have options. Look into a debt consolidation loan or one of the options above to start working on financial stability for the future.

You can get an apartment with bad credit, but it may take some strategizing. Apartment applicants with low credit scores can boost their odds by applying with a cosigner, paying more upfront, offering references, or changing the type of units they apply to.

In today’s housing market, you want every possible advantage on a rental application. While letters of recommendation and a solid rental history will get you far, more and more landlords want a high credit score. As a result, it isn’t uncommon to ask if you can get an apartment with bad credit.

While it takes some strategizing, you can get an apartment with low credit. To help you along, we’ll explain how credit impacts your application, explain steps you can take to compensate for low credit, and share tips on boosting your score.

How Credit Impacts Getting Approved for an Apartment

Many landlords and renters run a credit check as part of their rental application process. Like lenders, landlords check your credit to see if you can pay your bills on time. Because renting is an investment, property owners want to minimize risk. So, they assume tenants with high credit are more likely to pay their bills on time.

Remember that your credit score isn’t the only factor on a rental application. While a high score helps, the details on your credit report matter, too. How you got a high or low score can sway property managers one way or the other.

What Credit Score Do You Need to Rent an Apartment?

The score you need depends on the unit. Some rental companies provide an ideal range for their listings. A score of 620 or higher will generally keep landlords from denying your rental application. However, some landlords will expect more, while others don’t look at your score at all.

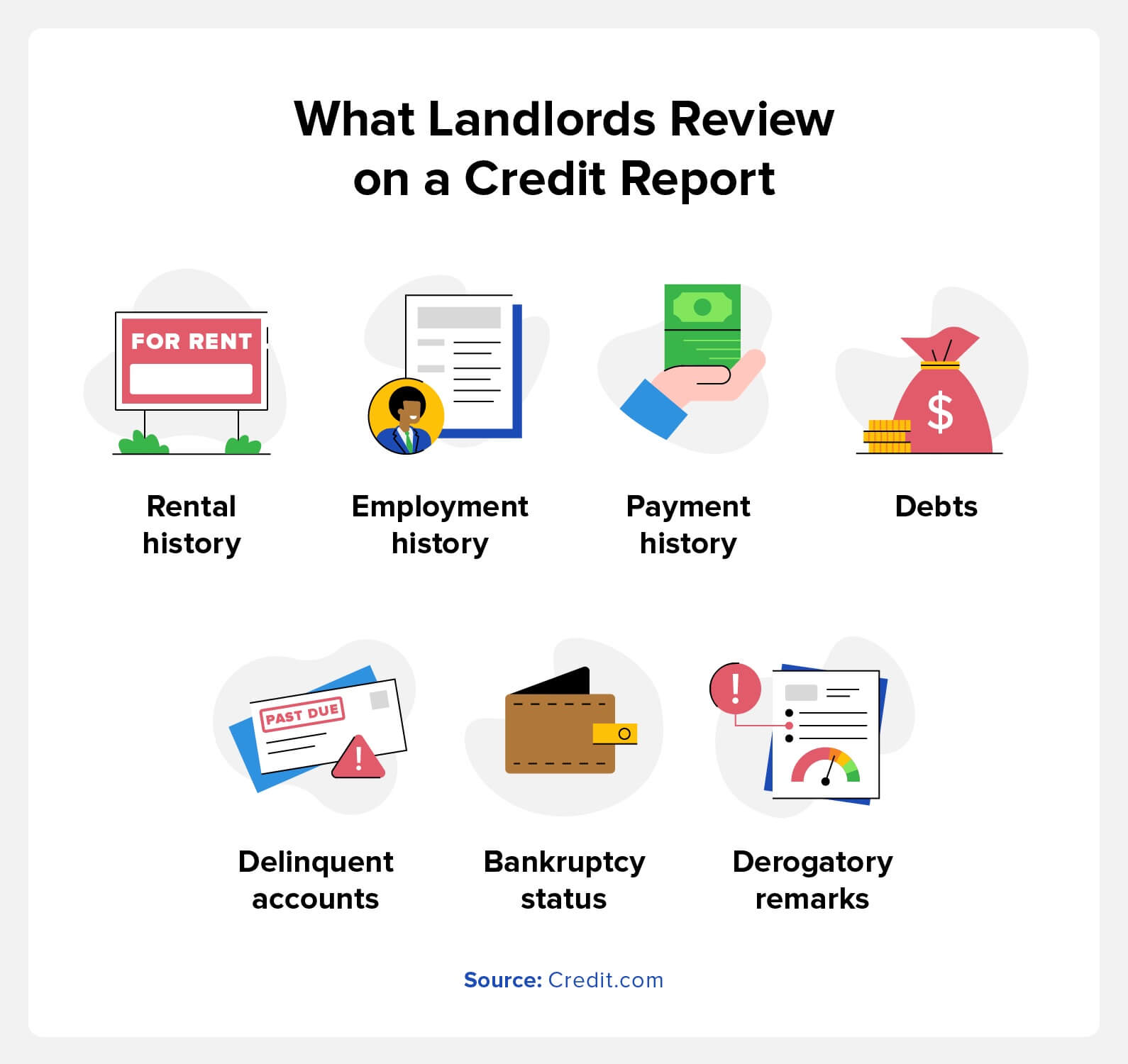

What Do Landlords Look for on a Credit Report?

Renters may treat your credit score like a headline, but there’s more to a credit report than a number. Credit reports tell a story about your spending habits and income. To help landlords pick reliable tenants, a rental credit check includes:

Rental history: Some landlords report rent payments to credit bureaus. As a result, evictions, broken leases, and late or missing payments may appear.

Employment history: Current or past employers may show up on a credit report. Typically, they only appear if you listed them on a credit card application or loan.

Payment history: Credit reports show your history of payments to lenders. Late or missing payments will lower your score and work against your rental application.

Debts: Current and past debts show up on your credit report. By providing payslips, landlords can calculate your debt-to-income ratio. If you make enough to repay your debts responsibly, that improves your application.

Delinquent or collections accounts: An account is delinquent if you miss a payment due date. If you miss enough payments for lenders to transfer your account to a collection agency or sell it to a debt buyer, it becomes a collections account. Both of these hurt your credit score.

Bankruptcy status: Bankruptcy filings will affect your credit score. Landlords may take recent bankruptcies as a sign that you’re a high-risk tenant.

Derogatory remarks: These remarks refer to negative items on your credit report. They include auto repossessions or foreclosures. They hurt your score and hamper a rental application.

Landlords gauge the risk they pose by looking at how applicants spend their money. Someone with a high income but a history of late payments may not make the cut. On the other hand, someone who filed for bankruptcy years ago may be more responsible now.

How to Get an Apartment with Bad Credit

While a low score sets you back, you can learn how to get approved for an apartment with low credit. By following these methods, you can get a leg up in rental applications:

Make an Upfront Payment

Putting down more money upfront can give you an edge on rental applications. Landlords will usually request a security deposit or the first and last month’s rent upfront. To sway a landlord’s opinion, offer the first three months’ rent or put down a higher security deposit.

At the end of the day, renting is an investment. If you can show your landlord that you’ll give them a reliable ROI, it’s all the more likely they’ll accept you. As a bonus, paying more in advance saves you a financial burden for the next few months.

Find a Guarantor or Cosigner for Your Apartment

If a landlord can’t trust you to make payments, you can get someone to sign your lease with you. Someone with a great credit score who signs on with you can assuage a property manager’s worries. However, remember that the person who helps you takes on financial risk. You have two options for this approach:

Cosignerssign a rental agreement with you and share the financial responsibility for it. They must do so on your behalf if you can’t or won’t pay rent.

Guarantors share cosigners’ responsibilities, but they have fewer rights. More specifically, they vouch for you and can make payments on your behalf. However, they aren’t entitled to reside in your unit.

Offer References and Supporting Documents

While credit reports outline your financial history, you aren’t the sum of your spending decisions. You can offer other documents to show your responsibility in an apartment application. Additionally, these documents can prove you can pay rent each month. Some examples of supporting documents include:

Payslips: Offer pay stubs that show you make enough money to pay rent each month.

Letters of recommendation: Reference letters from a friend or employer can attest to your character and responsibility.

Proof of reliable rental history: Account statements and landlord testimonials can prove you always pay rent on time.

A snapshot of your savings account: If all else fails, you can show landlords you have the money to make rent. Be sure to censor sensitive information on your snapshot.

Utility payments: A history of on-time utility payments shows your trustworthiness.

Find Apartments to Rent with No Credit Check

While credit checks are common, not all landlords require one. While these properties aren’t the most competitive, that isn’t always a problem. Apartments with no credit check tend to cost less than ones with one.

If you’re looking for another option, some landlords advertise units with low credit requirements. Again, these properties set a low credit requirement for a reason. That said, if you inspect the unit and it looks good, this route can save you a headache. As you live in low-credit apartments, you can build your score for future applications.

Adjust Your Expectations

If you can’t get around a credit check, reassess the kinds of apartments you can apply for. This isn’t to say you should only apply to units in poor condition. Instead, consider what you’re willing to compromise on. You may have an easier time qualifying for an apartment:

Farther away from your work or downtown area

Without amenities like a gym or pool

That doesn’t include parking

With less square footage than you’d prefer

If you apply with a roommate

Bear in mind that compromising on these points means the apartment may cost less. While living in a less-than-ideal unit, you can save and rebuild your credit while renting. When it comes time to look for a new apartment, you’ll have better odds of getting the one you want.

Tips to Raise Your Credit Before Renting an Apartment

If you plan to send rental applications down the line, you should work to improve your credit. Bear in mind that increasing your credit score takes time. To see a major change, expect months or even a year of work. In that time, follow these tips to improve your credit:

Pay Your Bills on Time

A person’s payment history can make or break their credit score. Central to that payment history: whether you paid your bills on time. Making timely and consistent payments plays a big role in improving your credit score. On top of that, timely payments prove your reliability to a landlord, boosting your chance of getting approved.

Pay Down Any Debt

Paying down debts is one of the best ways to improve your credit score. For this reason, someone who takes on and pays off debt won’t get punished for the debt they take on. Paying off debts shows your fiscal responsibility and proves your finances are on an upward trajectory.

Paying off any kind of debt can improve your score. The main ones to look out for include:

Credit card debt

Student loans

Medical debt

Auto loans

Become an Authorized User for Credit Piggybacking

If you don’t have the resources to boost your credit alone, you can try credit piggybacking. Credit piggybacking lets you benefit from a friend or family member who pays down their debts. By becoming an authorized user on their account, your credit report reflects their payoffs.

You can break the process into a few steps:

Find a friend or family member you trust to spend responsibly.

Become an authorized user on one of their credit cards or lines of credit.

As they pay down their debts, this will show up on your credit report.

By piggybacking on their credit payoffs, your score will improve.

Dispute Credit Report Errors

Sometimes, a low credit score isn’t your fault. Credit reporting errors can come from major credit reporting agencies or the companies giving them information. Credit reporting errors aren’t uncommon, so you should review your report for issues.

Credit reports may contain errors related to:

Accounts held by another person with a similar name to you

Accounts opened by fraudsters who committed identity theft

Closed accounts that still read as open

Accounts incorrectly labeled as delinquent or in collections

Payments that don’t get reflected in your report

Multiple listings of the same debt

Accounts with inaccurate balances or credit limits

To dispute credit report errors, contact the credit bureaus and the company that reported inaccurate information to them. You want to provide supporting documentation that proves the report contains errors. While you can send a dispute by phone, this doesn’t leave a paper trail. Instead, mail a dispute letter or use an online form.

FAQs on Renting an Apartment with Bad Credit

You may still have questions about getting approved for an apartment. To help you out, we’ve answered FAQs on renting apartments with bad credit.

Is 500 a High Enough Credit Score for an Apartment?

You can rent an apartment with a credit score of 500. While it might take you out of the running for expensive units, you should still have a good chance of renting:

Apartments with low credit requirements

Apartments with no credit requirements

Apartments you apply to with a cosigner or roommate.

Can I Reapply for an Apartment After I Get Denied for Bad Credit?

You can apply for the same apartment after getting denied on your first attempt. That said, some renters may throw out your application or ignore it. If you reapply, try to improve your credit and finances between applications.

Do Landlords Need Permission to Run a Credit Check?

Landlords need your permission to run a credit check. The Fair Credit Reporting Act calls rental applications a “permissible purpose.” This gives them the right to view your credit. However, that doesn’t mean landlords can check your score without your consent.

Improve Your Credit for an Apartment with Credit.com

Managing apartment applications is hard enough, even without a low credit score. However, you can get an apartment with bad credit by following the right steps. You’ll see more housing opportunities by learning how credit works, reviewing strategies for getting an apartment with low credit, and following tips to boost your score.

If you’d like a way to streamline raising your credit for rental applications, Credit.com can help. Our rent and utility reporting services ensure that your on-time payment gets reflected on your report. Even if your landlord doesn’t report payments, our tool helps build your credit with every rent payment reported.

Falling behind on your debt can be frightening. You may wonder if the creditor will come for your property or sue you. Sometimes, you don’t even realize you owe a debt before a credit collection service comes calling. But you do have rights and options. Get some tips for negotiating with creditors below.

In This Piece

1. Determine Whether Negotiation Is the Right Move

Settling your debt isn’t always the right move. If you can pay your debt off quickly without settling, it may be better for your credit. On the flip side, the debt will cost you more money.

Consider the big picture of your personal finances to figure out whether you should just pay off your debt fast or negotiate for more time or a lower payment requirement.

2. Make Sure the Debt Is Yours

While you’re thinking about whether debt negotiation is right for you, take some time to validate the debt. Mistakes happen—and so does fraud. It’s possible you didn’t originate the debt yourself, and if that’s the case, you can dispute it.

While validating the debt, you should also check that it falls in the statute of limitations. If debt falls outside the statute, collectors can’t continue to collect it and the creditor can’t sue you for the debt.

3. Don’t Negotiate Without Knowing What You Can Afford

If you decide to settle a debt, figure out what you can afford. Sit down and go through your finances with a fine-tooth comb. What do you really need to spend money on every month, and what can you kick to the curb? Go to the negotiating table with a firm figure in mind. Keep in mind that lump-sum settlements generally cost less in total than monthly repayment plans.

4. Understand Your Rights

Under the terms of the federal Fair Debt Collection Practices Act (FDCPA), creditors and debt collectors aren’t legally allowed to:

You also have a right to information about your debt, such as the name of the original creditor and how much you owe. Knowing your rights helps you protect yourself throughout the negotiation process.

5. Keep Your Story Straight

Falling behind on debt often happens because of serious life factors, but reps at credit collection services or lenders aren’t counselors. They’re just employees trying to do a job.

Give a condensed version of why you can’t pay your debt as agreed, and avoid drama. If you’re in a difficult situation, make that clear, and tell your lender what you’re trying to do to get back on track.

Before you talk with your creditor, it might help to write down and rehearse a few go-to sentences. This can make the discussion less emotional, making sure you’re better able to discuss the details and stand up for your rights.

Whatever you do, tell the truth. It’s much easier to keep the truth straight, and you’ll feel better if you don’t tell tales.

6. Ask Questions

Don’t be afraid to ask questions. You have a right to know where the debt came from, how the total amount owed was calculated and what fees might be included.

7. Take Notes

Talking about debt can be stressful and overwhelming. Keep a pen and paper handy so you can take written notes whenever you communicate with a debt collector. Make sure you write down the full name of the person you spoke to, the time of the call, how long the call went on and what you spoke about. You should also jot down any of the bad behaviors we mentioned above if they occur to create a written record of potentially illegal collection practices.

8. Read and Save Your Mail

It can be tempting to throw bills in the trash, but don’t do it. Instead, open them, read them and face your debt head-on. If a debt looks familiar, put the bill in a file and think about how you’d like to settle or discharge the amount. If you don’t remember accruing the debt, ask the lender for proof that you owe it.

9. Talk to Creditors, Not Collection Agencies

Try to negotiate with your original creditors before they sell your debts. Taking the bull by the horns at this stage could help you keep a few points on your credit score. Your original creditor may also have programs that can help you get back on track with payments.

10. Get Any Agreement in Writing

Get any settlement or repayment plan in writing as soon as possible once you conclude negotiations. Don’t pay any money before you see the agreement in black and white. If you pay before receiving confirmation, you might have trouble later on. Some unfortunate consumers end up getting chased twice for the same debt.

11. Stay Friendly

Debt is a nerve-wracking topic. It’s easy to get emotional when talking to creditors and debt collectors, but try to be friendly and stay on topic. Remember—debt collectors can’t come into your home and confront you, and they can’t take the resources you need to live away from you. If they start making such threats, end the conversation and report them instead of getting heated and angry.

12. Put the Past Behind You

Once you settle a debt, prepare to move into the future as positively as possible. Continue making your other payments on time to avoid this issue in the future. And keep an eye on your credit reports to ensure these old debts don’t crop up again via new collections accounts. Save all the records of your debt settlement so you can prove you don’t owe the money if that does happen.

Car insurance can be confusing. First, there are all the policy considerations: Do you want a policy with comp and collision? How much liability should you carry? Do you need uninsured motorist coverage? Even once you make decisions on all these things, the bill that arrives can be difficult to understand—exactly what goes into the pricing for your car insurance premium? Here’s what car insurance companies don’t want you to know about premium pricing.

Your car insurance may not be tied to the driver.

The type of car you drive matters.

Prior claims and questions raise rates.

You can check your report for errors.

Your credit score impacts your car insurance costs.

Where you live impacts your premium account.

Your age affects your car insurance premium.

Gender, marital status, job and education level can affect premiums.

If you bought your car with a loan, your premium may be higher.

You can lower your insurance rates.

You have options if insurance denies your claim.

Is Car Insurance Tied to Car or Driver?

Technically, car insurance is tied to the car. That means if you let someone else drive your car, your insurance may kick in if there is an accident. Not all insurance policies cover all uses of your vehicle, though, so read the fine print on yours before you allow someone else to drive it. You may also be able to exclude drivers who live with you from your policy if you don’t ever want them driving your car and don’t want them impacting the cost of your policy.

>> Find Car Insurance Quotes.

Does It Matter What Kind of Car You Drive?

The total value of your car, what type of vehicle it is and what type of safety rating it has all factor into the cost of your policy. Other factors can include how many miles you drive each year, where you park your car, and how many expensive extra features your car has.

Does Your Driving Record Affect Your Insurance?

Every claim you make—and even if you ask an insurance agent about making a claim—gets entered into a database that your current and future insurance carriers can access. If you have had any recent accidents or traffic violations, you may be more expensive to insure than someone with a clean driving record. If you’ve made any recent claims, your insurance premiums will likely go up. And if you shop around for a new company, they’ll have access to your records and will take your driving record into consideration.

Can You Check Your Insurance Reports?

Your insurance companies share information with two databases: the Comprehensive Loss Underwriting Exchange (CLUE) and the Automated Property Loss Underwriting System (A-PLUS). These databases are run by outside agencies—LexisNexis runs CLUE and Verisk Analytics runs A-PLUS—and any claims you make stay in your report for five to seven years, depending on the database.

The Fair Credit Reporting Act entitles you to one free copy of your report every 12 months. You can dispute inaccurate or incomplete information on your report. You are also entitled to notice about any negative decisions based on information in your report. Requesting your reports does not affect your credit score.

Request your CLUE report from LexisNexis online or call 866-312-8076.

Request your A-PLUS report from Verisk by calling 800-627-3487.

Does Credit Score Impact Your Car Insurance Cost?

In most states, your credit score can impact the cost of your car insurance. The only states that don’t allow car insurance companies to use credit score as a factor in pricing are California, Massachusetts and Hawaii. Statistical studies from the Federal Trade Commission and other research organizations show a correlation between credit score and how much a person is likely to cost a car insurance company. In short, someone with a poor credit score is seen as a greater risk, so the insurance company may charge more for the insurance to help cover expenses related to future claims.

Does Where You Live Impact Your Premium Amount?

Where you live can impact your car insurance cost. In 2018, for example, the average car insurance premium in Michigan was 64% higher than the national average. Other states with car insurance premium averages on the high end included Louisiana, Florida, Rhode Island and Connecticut. States with the least expensive average car insurance premiums included Vermont, Ohio, Virginia, Idaho and Iowa.

Does Age Impact Your Premium?

When it comes to what car insurance companies don’t want you to know, this one isn’t super secret. Age does impact your premiums, with the youngest and oldest drivers typically paying the most on average.

The youngest drivers pay the most for insurance. Premiums are highest at the age of 18 and decline steadily until the driver turns 25. In the eyes of carriers, drivers then enter adulthood, during which time premiums stay pretty flat for the next 30 years or so, until the age 55. Premiums inch up slowly between ages 55 and 65 before jumping way up around the age of 75.

In addition to your age, your gender, marital status, education level and even your job can affect your insurance rates.

If You Bought Your Car Via a Loan, Is Your Insurance Cost Higher?

If you don’t own your vehicle outright, then you may pay more to insure it. If you own a vehicle outright, you’re only required to carry liability on it. Liability is the part of your insurance policy that kicks in to cover damage caused to other people’s cars or property in an accident you’re at fault in.

When you have a loan, the bank is concerned about protecting its investment. That means it may require you to carry comp and collision as well. This is the part of an auto policy that covers damage to your car in an accident you’re at fault in. A policy with this added coverage is more expensive than one without it.

How Can You Lower Your Car Insurance Costs?

No matter your age, gender, or location, you can potentially lower your car insurance via a variety of methods. Here are some tips your car insurance company doesn’t want you to know to put into action to save on premiums.

Drive carefully. Not only does driving carefully help you avoid rate-raising accidents, but many companies also provide good driver bonuses when you haven’t had an accident or filed any claims for a certain amount of time.

Pay your bills on time. Paying your bills on time goes a long way toward improving your credit score, which can improve your rate depending on where you live. Paying your bills on time also demonstrates trustworthiness to your insurance company, which means you may be able to negotiate for a lower rate.

Ask for discounts. When it comes to your insurance rates, it doesn’t pay to be shy. Ask your insurance company about discounts, including multi-driver or multi-car discounts, good student discounts or safe driver discounts. You may be able to score a large portion off your premium because you’re a good student or you follow all the traffic laws.

Review your credit report. Know what’s on your credit report and what you can do to drive up your score. Once you’ve improved your score, ask for a new quote for car insurance.

>> Need to review your credit report? Sign up for the free Credit Report Card.

Consider a higher deductible. Look carefully at your coverage and consider whether you can tweak anything in your policy. If you can afford to cover $2,000 in damages if you get in an accident, consider changing your deductible from $500 to $2,000 to save on your monthly premium.

Shop around for a better rate with other insurance companies. The insurance market is highly competitive, and you may find a better rate with an online company or through a broker that works with multiple companies. If you find a better rate, go back to your current company to see if they’ll match or beat the offer.

Choose your next vehicle carefully. Because the type of car you drive affects your insurance rates, do your research before your next purchase. Look for a car with plenty of safety features (but without too many other bells and whistles) that will get you a lower rate.

What Happens When Car Insurance Denies a Claim?

Of course, you don’t just pay for car insurance for the fun of it. If you get into an accident, you expect the insurance to step in and help cover the expenses. If your insurance company denies your claim, you have some options for appealing the claim.

Contact the insurer. After you’ve reviewed your claim denial, reach out to the insurance company directly. You may be able to explain your claim better or gather additional information to help you understand the reason for the denial.

File an official appeal. Most insurance companies will have an appeals process clearly set out online. You’ll want to write a clear, direct letter that explains why the evidence you originally gathered and submitted with your claim contradicts the insurance company’s decision to deny the claim.

Talk to a legal professional. If you feel that your insurance company is denying your claim in bad faith, talk to a legal professional about your options.

Bringing Down the Total Cost of Car Ownership

Car ownership is expensive. Make sure you pay attention to all the potential expenses to get the best possible deal overall—and don’t forget to shop around for the best rates before locking yourself in.

Identity thieves are almost always opportunistic—but the crimes they commit feel very personal. Unauthorized credit card charges, bogus loan applications, missing money, and other financial violations make fraud a major nightmare. To keep fraud in check, you need to know how to check your credit report for identity theft, and how to deal with problems when they arise.

In this post, we’ll talk about the warning signs of identity theft—and then we’ll show you how to stamp out fraud before it starts.

Warning Signs of Identity Theft

How Do I Check My Credit for Identity Theft?

To avoid falling victim to identity theft, examine your credit report regularly. You can access a free copy of your credit report from all three bureaus—Equifax, Experian, and TransUnion—once a year. (Through April 2022, you can get free weekly copies of your reports.) You can also use a tool like Credit.com’s Credit Report Card or ExtraCredit to monitor your credit.

When you download your credit report with ExtraCredit, you’ll see a list of positive accounts, late accounts, collections, public records, inquiries and account balances. Your credit report contains a lot of information about you and about your financial habits, and if that information changes unexpectedly, it can indicate identity theft. Here are five of the biggest fraud warning signs to watch out for.

Warning Sign 1: Incorrect Personal Information

Sometimes, incorrect personal information is the result of an innocent mistake. Other times, it means something sinister is going on. If you see your name misspelled, a wrong phone number or address, or an incorrect Social Security number on your credit report, investigate immediately.

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

Warning Sign 2: Lender Inquiries You Don’t Recognize

Credit bureaus keep the details of companies who ask for information about you on record for at least two years. Promotional inquiries and account review inquiries are nothing to worry about, because they’re preapproved credit offer inquiries or inquiries by companies you already do business with.

Hard enquiries from companies you don’t recognize are a different matter. Sometimes, fraudsters make a lot of credit card and personal loan applications in a short period of time, so if you see a recent list of unknown inquiries, someone might be trying to steal your identity.

Tip:Sometimes, the name of a financial institution doesn’t precisely match the name of the company checking your credit. Car dealerships, for example, sometimes run a series of credit checks via different finance companies—so it’s worth double checking before filing a fraud complaint.

Warning Sign 3: Accounts You Never Opened

Only your own accounts—including accounts that you’ve cosigned and for which you’re an authorized user—should appear on your credit report. If you find an unknown account on your credit report, one of two things has happened:

Your credit information has been commingled with someone else’s information by mistake

Your credit has been compromised by a fraudster

If you find an unknown account on your credit report, contact the relevant lender right away and tell them what’s going on.

Warning Sign 4: You Credit Utilization Goes Up

If you suddenly owe more than before and you haven’t changed your spending habits, someone else might be splurging on your behalf. Check your credit card statement very carefully and flag any suspicious transactions straight away. Most credit card companies have a maximum 120-day limit for chargebacks, so it’s important to review purchases regularly.

Warning Sign 5: Your Score Goes Up or Down Unexpectedly

Credit scores change over time. When negative information falls off your credit report after a certain period of time, your score increases. On the other hand, if you apply for too many loans or credit cards in a short space of time, your credit score could take a hit. If your credit score changes dramatically—especially if it’s for the worse—dig deeper.

Warning Sign 6: Public Records You Don’t Recognize

Negative public records can substantially impact your creditworthiness. Bankruptcies, for instance, often remain on record for up to a decade. If you see public records you don’t recognize, alert the issuing agency without delay.

Tip:Liens and civil court judgments used to appear on credit reports, but credit bureaus no longer collect information about those types of public records. Bankruptcies are now the only public records included on credit reports.

Can Someone Steal Your Identity with Your Credit Report?

Your credit report contains a lot of personal information, so it’s a goldmine for identity thieves. With a copy of your report in hand, a potential fraudster might be able to see:

Full name

Birth date

Social Security number

Current and past home addresses

Phone number

Accounts held in your name

Payment records

Public records, including bankruptcies

Many other valuable personal and financial details

Credit report content sometimes varies according to the credit bureau.

If thieves need more information after accessing your credit report, they often choose to misrepresent themselves to get it. Phishing and smishing scams are when criminals pretend to be legitimate financial institutions—or government agencies like the IRS—to get personal information from victims via email or text.

What Is the Safest Way to Check My Credit Report?

You can check your credit report quickly and easily with Credit.com’s ExtraCredit monitoring service. ExtraCredit includes five helpful tools, which help you monitor, build, earn, protect, and restore your credit profile. Two tools in particular can help you avoid or combat identity fraud: Track It and Guard It.

Track It

With ExtraCredit’s Track It tool, you get access to all three credit bureau reports. You can also monitor 28 FICO® scores—the real scores lenders see when they consider auto loan, credit card, and mortgage applications. Track It also includes a helpful credit monitoring tool, which gets updated every month. If something suspicious happens, you’ll notice right away.

Guard It

Many hackers sell consumer information on the dark web. Nefarious individuals use software, specific net configurations, or special authorizations to access the dark web. Thankfully, ExtraCredit’s Guard It tool actively monitors the dark web for consumer information and sends out security alerts when data breaches happen. You also get a $1 million ID insurance policy when you sign up with ExtraCredit.

Get Identity Theft Protection

Identity theft is a big problem in the United States. There were 650,572 cases of identity theft in America in 2019—and over 270,000 of those cases involved credit card fraud. If you see an unknown address or notice an unknown credit card on your credit report, flag it up right away. Tools like ExtraCredit from Credit.com make it easier to monitor your report on a monthly basis, so you can rest more easily.

Every item on this page was chosen by a Woman’s Day editor. We may earn commission on some of the items you choose to buy.

1

Best for Floating Flowers

Webelkart Diya Shape Urli Bowl

1

Best for Floating Flowers

Webelkart Diya Shape Urli Bowl

Credit: Webelkart

This special bowl can hold floating flowers and candles. You’ll appreciate the intricate detail on its metallic finish. Just fill it with water and artificial or real flowers with no stems. You can also use it for scented potpourri.

2

Most Festive Rangoli

Itiha Indian Rangoli Floor & Table Decoration

2

Most Festive Rangoli

Itiha Indian Rangoli Floor & Table Decoration

Credit: Itiha

This gorgeous rangoli is a great addition to tabletops. You can also lay it on the floor. Handcrafted by Indian artisans, you can use this to hold one candle at a time.

3

Best Diwali Door Decorations

Diwali Peacock Porch Banner

3

Best Diwali Door Decorations

Diwali Peacock Porch Banner

During Diwali, people might also decorate with peacocks due to their bright colors. This intricate door decor — which is made of polyester so it won’t wrinkle — will impress your neighbors.

Advertisement – Continue Reading Below

4

Best Budget Diwali Decoration

Diwali Backdrop

4

Best Budget Diwali Decoration

Diwali Backdrop

Credit: TENCOW

Hang this on any wall in your house for your Diwali party. The bold banner can also serve as a beautiful backdrop for a party photo booth. It features festive images of diyas, rangolis, and candles to boot.

5

Best Diwali Photo Booth Props

Duormal Diwali Photo Booth Props

5

Best Diwali Photo Booth Props

Duormal Diwali Photo Booth Props

Credit: Duormal

Who doesn’t love a good photo opp? This 16-piece kit comes with some fun adornments for your photo booth. With signs that say Happy Diwali, Festival of Light, and Warm Diwali Wishes, you can spread joy and awareness of the event. In true photo booth style, you’ll also get fun glasses, lips, mustaches, and more to complete your shot.

RELATED: 40 Fun Diwali Captions to Celebrate the Holiday

6

Best Diwali Centerpieces

Diwali Honeycomb Table Centerpieces

6

Best Diwali Centerpieces

Diwali Honeycomb Table Centerpieces

Credit: Know Me

These fabulous Diwali decorations can adorn your tables and other surfaces with bright colors and fun images. This 9-piece set comes flat, but easily opens up into 3D centerpieces. And the best part is, you can reuse them year after year.

Advertisement – Continue Reading Below

7

Best Diwali Decorative Table Runner

Linen Diwali Table Runner

7

Best Diwali Decorative Table Runner

Linen Diwali Table Runner

Credit: Jiudungs

Tablecloths are often either too formal or a little corny, depending on the design. To elevate your table for Diwali and keep things chic yet festive, a table runner is the perfect solution. This one in a lovely purple and gold color scheme will truly dazzle in any party space.

8

Best Fill-in Rangoli Template

Aditri Creation Designer Rangoli Mat

8

Best Fill-in Rangoli Template

Aditri Creation Designer Rangoli Mat

Don’t let the simplicity of this rangoli template fool you. When you pair it with colorful rangoli powder, it’ll be a lovely addition to tabletops. If you don’t want to make a mess of the powder, you can also paint it beautifully!

Hosting a dinner party or having people over for some delicious treats? A personalized plate can be a great addition to your tablescape. This round plate features a diya. Simply customize with your family name to make it your own.

Advertisement – Continue Reading Below

10

Best Large Diwali Banner

Diwali Banner for Fence

10

Best Large Diwali Banner

Diwali Banner for Fence

Credit: FARMNALL

If you have the space, let your neighbors know you celebrate Diwali with this 8-foot long sign. Display it on your fence or garage. Made of durable fabric, it can withstand wind and snow and won’t fade or wrinkle, so you can use it for years to come.

11

Best Happy Diwali Outdoor Decor

Diwali Yard Signs

11

Best Happy Diwali Outdoor Decor

Diwali Yard Signs

Credit: ADXCO

By now, you’ve likely seen graduation, baby shower, and birthday yard signs on your neighbor’s lawns. For Diwali, you can do the same! Share your Diwali pride with your community by staking these fun Diwali decorations outside. The set comes with 11 different pieces that scream Happy Diwali.

With this kit, you’ll get five feet of sweet artificial marigold garland to display over mantles, bookcases, or doorways. Choose from three different color combinations of orange, pink, and yellow.

Advertisement – Continue Reading Below

13

Best Rangoli Stencil Set

Rangoli Stencils

13

Best Rangoli Stencil Set

Rangoli Stencils

Use these rangoli stencils to easily create your own beautiful rangoli designs at home. Get the whole family involved for a fun and inexpensive Diwali activity!

14

DIY Sand Art Decor

A Kailo Chic Life

During Diwali, you will undoubtedly have candles all over your home. While you can use your standard candle holders, you may want to add some fun for the holiday by making these lovely (and easy!) sand art holders.

Get the Sand Art Decor tutorial at A Kailo Chic Life.

SHOP CRAFT SAND

15

DIY Dancing Ribbon Rings

Buggy and Buddy

One of the simplest crafts we’ve seen to date, these dancing ribbon rings can be made with your favorite hues. Since Diwali is marked by bold colors, select several colors to tie around wood rings. You can then hang these rings around the house or let kids craft and play with them during your Diwali party.

Get the Dancing Ribbon Ring tutorial at Buggy and Buddy.

SHOP RAINBOW RIBBON

Advertisement – Continue Reading Below

16

DIY Tissue Tassel Garland Cake Topper

See Vanessa Craft

We love the idea of using this DIY garland cake topper for your dessert table. If you’re serving a cake or pie, consider hanging it on top to give your table that extra added color that Diwali calls for. And the best part is, it’s easy to make and requires only a few materials.

Get the Tissue Tassel Garland Cake Topper tutorial at See Vanessa Craft.

SHOP COLORFUL TISSUE PAPER

Ysolt Usigan is a lifestyle writer and editor with 15+ years of experience working in digital media. She has created share-worthy content for publishers Shape, What To Expect, Cafe Mom, TODAY, CBS News, HuffPo, The Bump, Health, Ask Men, and Best Gifts. A working mom of two, her editorial expertise in parenting, shopping, and home are rooted in her everyday life.

A new survey from Campbell Communications and Inside Mortgage Finance Publications revealed that real estate agents hold sway when it comes to choosing a lender.

In fact, the survey claims 45% of buyer decisions regarding which lender to go with are controlled or influenced by real estate agents.

So instead of shopping around for the best deal or using a family/friend’s referral, many home buyers instead follow the lead of their real estate agent, for better or worse.

This is especially important news for lenders, now that the refinance boom is finally coming to an end, and purchase-money mortgages are expected to take center stage.

The Mortgage Bankers Association expects home purchase lending to increase from $503 billion in 2012 to $585 billion this year.

And you better believe that banks and lenders will want to align with real estate agents to ensure they get as much of that business as possible.

After all, refinance activity is expected to slow tremendously, so they’ll need to make up for that lack of business elsewhere.

Agents Prefer Quick and Reliable Lenders

Real estate agents need to know their buyers can obtain financing

So they prefer to have some sort of control over the lender you choose

Or perhaps they choose one for you or at least direct you toward one

Which explains why they always have a preferred lender

The survey also noted that real estate agents prefer speed and reliability above all else, meaning they might not have a borrower’s best interests in mind.

Sure, it’s better to close than not, but at what price to the borrower? A preferred lender may be quick, but also offer mortgage rates a .25% to .50% above the competition.

And even then, there may still be hiccups, regardless of the relationship.

Real estate agents also indicated that they were big on meaningful status updates, seemingly to ensure loans close on time without delay.

This is especially important in today’s market, seeing that loan origination staff appears to be constrained, and demand is on the up and up.

In fact, two-thirds of the nearly 2,000 agents that responded to the survey said they wanted mortgages to close in 30 days or less.

That can be a tall order at the moment, given the fact that the average purchase transaction has been taking around to a month and half to close.

But there are certainly lenders who move quicker than others, and if a real estate agent can develop a relationship with one that offers competitive pricing, it could be beneficial for everyone involved.

Should You Use the Real Estate Agent’s Lender?

You can choose to be diplomatic and speak to their lender

Often they’ll ask that you at least get pre-approved though there’s no obligation

You don’t have to do either really

But it may not hurt to get another rate quote just to see if they can save you some money on your home loan

Often times when you make an offer on a home, the agent will ask you to get pre-approved with their “preferred lender.”

While it may be in your best interest to get the pre-approval, just to show you’re very serious about buying the property (especially when there are multiple bids), you don’t need to use their lender to obtain your financing.

If anything, you can chalk it up to another mortgage quote, along with the others you hopefully obtain while shopping around.

Just blindly going with the referred bank or lender clearly isn’t wise, because when it comes down to it, you really won’t know how competitive they are unless you shop your loan elsewhere.

Yes, it requires more work, and yes, the real estate agent will probably tell you their mortgage broker or lender is the best in the business, with the lowest possible rates.

They may even go as far as to use scare tactics to get you to use their guy or gal.

But you may regret using them after the fact, especially if they weren’t even able to fulfill expectations on the customer service front.

In other words, get pricing from their preferred lender and see how it stacks up with your other offers, then go from there.

That way you can appease the agents involved and make sure you’re doing your due diligence.

Read more: How to get a better deal on your mortgage rate.

After you’ve debated the pros and cons of living with someone and decided to have a roommate, the next challenge is figuring out how to find one. If you don’t already have a potential roommate in mind, you’ll need to start looking for one, which is its own challenge. Here are tips on how to find a roommate who will be compatible with your lifestyle.

Ask around

You can ask your family, friends and other acquaintances if they know anyone looking for a place to live. At the very least, you can let others know you’re seeking a roommate, so they can pass along the word to their friends and family. There’s a good chance that your contacts know someone who needs a place to live.

Furthermore, you’ll have the benefit of a reference you know already. You can ask your friends and family about the potential roommates and what they think of them. If a friend says their old roommate is looking to move, you can get great insights on if the potential roommate is clean, easy to live with, etc., from your friend, rath

er than relying on unknown references provided to you by that potential roommate.

Leverage social media

This can be a farther-reaching method of asking friends and family if they know anyone looking for a place to live. You can make a post with details, such as the area you’ll be living in, how much rent will be and how many other people will be living in the apartment. Make sure that your post is shareable, then ask everyone to share your post to get the word out!

You can also do some searching on socials to see if others from your city are posting about looking for an apartment. Reach out to those individuals and let them know what your apartment and the living situation would offer!

Some social media platforms like Facebook have groups specifically for housing in certain cities or areas. You can post in these groups that you’re looking for a roommate and it will be seen by plenty of others.

Place ads and listings

There’s no shame in using platforms like Craigslist and Facebook Marketplace to find a roommate. It’s easy and usually free to create a listing and it’s searchable by location, so those who are actively seeking to live in your area will quickly find your listing. Many local or state news networks will have a place for classified listings and rentals, so check to see if your city has one where you can post your apartment.

Try an app

Using apps is one of the best ways to find a roommate. There are plenty to choose from, but some of the most popular are Cirtu, Roomster, Roomi and SpareRoom. Such apps often allow for a more personalized search where you can specify what qualities you want in a roommate (quiet and keeps to themselves, extroverted and likes to socialize, clean, etc.). They also often require background checks or multi-step verification for users, so it can be safer for you to use.

You’ve found a roommate, now what?

As much as you want to find a roommate, your personal safety, credit history and even your reputation matter. So, make sure you research every potential roommate thoroughly.

1. Review references

Ask applicants for references from employers and previous landlords. Even notes from friends, clergy, professors and former roommates can help you get a sense of their character and habits.

Search each potential roommate’s social media pages to see if they’re respectful in their interactions with others and if they show good judgment in what they post publicly. If you see evidence of illegal activity, angry messages from friends or hostile, hateful, racist or sexist posts from your potential roommate, cross them off the list.

2. Check their criminal background

Search each applicant’s name and look for arrest records. Some states also have circuit court access websites available for your reference. People with common names are sometimes mixed up, so make sure you’re researching the right individual by cross-referencing details like photos and location.

If you find something questionable, you can reach out to the police department that made an arrest. They can offer clarification while still preserving privacy.

3. Do a financial check

Of all the questions to ask potential roommates, financial questions are among the most important. You’ll be paying bills with this person, so their bad credit and financial habits could affect you.

You can request a credit check from a potential roommate to make sure they have a solid payment history and ask about their job. Someone with a steady full-time job is likely more stable than someone who works sporadically or changes jobs frequently. You can ask for pay stubs as proof if you’re concerned.

Keep in mind that a potential roommate might have alternative sources of income, like alimony, savings, stipends and investments. Or, if they’re a student, they can typically get extra help via student loans or grants.

Other questions to ask potential roommates

Once you’ve narrowed down your list of candidates, it’s time to go a little deeper by discussing your personalities and habits to find the best fit.

Consider creating a rough outline of a roommate agreement and using it as a conversational guide. If you hit it off, you and your future roommate can edit it together before they move in.

1. Additional financial questions

You don’t have to be best friends to be successful roommates. But you do have to cooperate and be good financial partners.

Ask your roommate what they can spend on rent and utilities and how much they can contribute to the security deposit. Discuss how and when you’ll pay bills and what will happen if someone comes up short.

2. Chores and responsibilities

The bills aren’t the only thing you’ll be dividing — roommates need to split the chores, as well. Be honest about how often you plan to clean, which chores you’d like to handle and if you’re tidy or messy. If you’re on opposite sides of the spectrum, you could face an uphill battle.

Shopping, deep cleaning and other household management tasks like corresponding with your landlord also fall under this category. Hash out how you’ll allocate these tasks and figure out a system that will work for both of you.

3. Personalities and habits

An introvert and an extrovert can live together quite happily, as long as they establish ground rules. Figure out a communication style that works for both of you.

Little disagreements can cause big drama, so chat about seemingly insignificant things like how warm you like the apartment and what you consider a “normal” volume level before you move in. If your views on habits like drugs, alcohol and smoking don’t line up, that’s probably a deal-breaker.

4. Schedules

Get an idea of how often your potential roommate will be at home. A traveling sales rep has a very different schedule than someone who works and socializes on a laptop in their bedroom.

It’s also smart to talk about how they plan to use your joint living spaces. If they cook three-course dinners every evening, like to throw parties or plan movie marathons every weekend, find ways to make sure their activities don’t interfere with your at-home workout sessions or meditation time.

5. Personal relationships

How do you feel about friends and family members coming over or spending the night? What happens if you both want company at the same time? If they’re dating someone, discuss how often their partner will be in the apartment and expectations around what privacy will look like.

Pets are like family, so make sure you know the details about your potential roommate’s pets. Discuss how they’ll share the space with yours and brainstorm how you might split pet-related chores. If one of you is allergic to animals — or if pets aren’t allowed in the building — move on.

The best way to find a roommate

Once you’ve done your homework, it’s time to make your future roommate an offer. Eliminate anyone who gave you a bad feeling or people with whom you just didn’t click. Basic respect and good communication are the building blocks of a solid roommate partnership.

Figuring out how to find a roommate can be challenging. But it doesn’t have to be complicated. Ask smart questions, leverage your personal networks and use tools available to help you find someone with similar goals who will be a good fit.