Rent prices are on the rise, with the average cost increasing 18% between 2017 and 2022. But buying a home requires a hefty down payment and good credit. Renting to own your home can give you the best of both worlds, but there are some downsides.

If you’re thinking about signing a rent-to-own agreement, it’s important to weigh the pros/cons of rent-to-own home deals. Here’s what you need to know before you sign on the dotted line.

What are rent-to-own homes?

When you own a home, part of your monthly payments goes toward paying off the principal. If you stay in the home long enough, you’ll own it.

The same doesn’t apply to rentals. Your monthly rent solely covers your costs of living in that home, whether it’s a condo, apartment, townhouse, or single-family house.

A rent-to-own home lets you pay rent to live on the property, with the option to buy it when the lease runs out. In some cases, a portion of your rent goes toward the purchase price, but that isn’t always the case.

How does rent-to-own work?

A rent-to-own agreement is essentially a lease agreement with an option to buy. Rent-to-own contracts should be read thoroughly. Those options can vary from one contract to another.

When you sign a rent-to-own contract, you pay an upfront fee called an option fee. This is typically 1 to 5% of the home’s purchase price, and it’s non-refundable.

It’s important to note that a lease does not relieve you of the requirements to buy a house. You’ll still have to qualify for a mortgage and make a down payment. It’s merely a way to buy yourself some time and possibly put some of your rent toward the purchase price of a home.

Lease Option vs. Lease Purchase

Before you sign, pay close attention to the lease agreement you’re signing. There are two types, and one contractually obligates you to buy the property.

Lease Option Agreement

A lease option agreement is the best deal of the two for you, the buyer. You’re signing a lease option contract that merely gives you first rights to the house when the lease is up. If you change your mind, find a better deal, or can’t qualify for a mortgage, you can find somewhere else to live and move your belongings out.

Since the option fee is nonrefundable, it’s important to note that you will lose money if you choose not to buy. Calculate this loss when you’re deciding whether to buy.

Lease Purchase Agreement

Unlike a lease option agreement, lease purchase agreements obligate you to buy at the end of the lease. Since it’s a contract, that means you’re legally obligated to purchase the house.

This can be risky for a couple of reasons. Once you’re in the house, you may see issues you didn’t notice when you were first touring the house. Things could change with the neighborhood or your circumstances that you couldn’t know at the outset.

But the biggest issue with a lease purchase contract could simply be that you aren’t eligible for a mortgage to buy the house. Make sure you know, up front, what penalties or liabilities you’ll face if you can’t buy the house when your lease is up.

Even though both agreements operate differently on your end, they do obligate the seller to give you the option to buy when your lease expires. This puts you in a position to own a home at a predetermined future date, giving you the opportunity to start planning.

Length of a Rent-to-Own Agreement

Rent-to-own contracts start with a lease period that can be up to five years but is usually less than three. The thought is that the rental period will give a renter time to qualify for a mortgage. During this time, you’ll work on building your credit, if necessary, and saving for a down payment.

In some cases, a rent-to-own arrangement could have renewal terms. That means if you reach the end of the lease and want more time, you can extend the lease. With this option, though, the property owner could increase your monthly rent or the purchase price.

Preparing for Homebuying

During your lease term, you’ll make each monthly rent payment in exchange for remaining in the house. But it’s important during that time that you work toward purchasing the house when your time is up. Here are some things to do to boost your chances of landing a mortgage once your lease expires.

Boost Your Credit Score

Your rent-to-own deal requires that you qualify for a mortgage once the term is up. To do this, you will need to meet the minimum credit score requirements. You can get a free copy of your credit report each year at AnnualCreditReport.com, but there are also credit monitoring services that can help you stay on top of things.

Although requirements can vary from one lender to the next, Experian cites the following credit scores as necessary to land a mortgage:

FHA: If you qualify, a Federal Housing Association loan will accept credit scores as low as 500.

USDA loans: Those who meet the requirements can qualify with a score as low as 580.

Conventional loan: Generally 620 or higher, but some lenders require 660 at minimum.

VA loans: Eligible military community members and their families can obtain loans with scores as low as 620.

Jumbo loan: These loans cover houses at a higher price, so you’ll need a score of at least 700.

Save for a Down Payment

In addition to a good credit score, you’ll need to put some money down on your new home. Down payment requirements vary by loan type, but it’s recommended that you put at least 20% down. That means if you’re buying a $200,000 home, you’ll need at least $40,000 by closing.

There are lower down payment options, but if you choose those, your mortgage payments will include something called private mortgage insurance. This will increase your monthly payment by $30 to $70 per $100,000 borrowed.

If you can’t save up 20%, you may qualify for an FHA loan, which requires as little as 3.5% down. Both VA and USDA loans have zero down payment options, and there are programs offering down payment assistance to those who qualify.

The best part about rent-to-own properties, though, is that some come with rent credits. With a rent credit, a percentage of your rent will go toward your required down payment. Calculate in advance how much you’ll have in that escrow account at the end of your lease to make sure you save enough to supplement it.

What are the pros of rent-to-own?

Rent-to-own homes can be a great option, especially during a tight housing market. If there’s a house you want to buy, but you can’t make a down payment or your credit isn’t where it should be, it could be a great workaround. Here are some of the biggest benefits of rent-to-own agreements.

Rent May Go Toward Purchase Price

Depending on the terms of the rental agreement, renting to own could help you work toward paying for the home. Instead of the full amount of your rent being pocketed by a landlord, a percentage of your rent could go toward the eventual purchase price. Before signing, pay attention to rent credits and try to negotiate the best deal possible.

The Purchase Price Is Locked In

When a landlord agrees to a lease option, the home’s purchase price is written into the contract. That price will typically be higher than what the market says it’s currently worth. This means if the U.S. housing market sees an unexpected increase, you’ll be buying the home for less than its value. Even if the market dips, once you purchase the house and remain there for a few years, you may be able to sell it at a profit.

You’ll Buy Extra Time

For many renters, the rent-to-own period provides time to qualify for a mortgage. If you’ve researched all the options and found you’re close but not quite there yet, a rental period could be just what you need.

Before you choose this option, though, take a look at your circumstances. If substantial existing debt and poor credit mean you won’t qualify, you may need more than the few years you’ll get with a rent-to-own agreement.

No Moving Necessary

Let’s face it. Moving can be a pain. You have to pack everything up, line up a moving truck and get help moving, and unpack your items once you’re in the new location.

With a rent-to-own agreement in place, you skip the hassle of moving. You’ve already been in that home, making monthly rent payments, for at least a couple of years. You’ll simply go through the closing process and switch from rent payments to mortgage payments.

What are the cons of rent-to-own?

If you can get a mortgage, that’s always going to be a better option than renting or leasing to own. But there are some instances where renting without the buy option could be better for you. Here are some things to consider.

Rent-to-Own Home Maintenance

Before you sign any lease agreement, it’s important to read the fine print. One thing to note, specific to own agreements, is who will be responsible for maintenance during the rent-to-own period. If you rent without the promise of eventual ownership, your landlord will take care of those costs. In some cases, rent-to-own agreements require the renter to handle all repairs.

But there’s an upside to handling repairs on your own. To your landlord, the property is technically yours. That means you likely will give it more TLC. Still, it’s well worth it to pay for a home inspection before you agree to a rent-to-own agreement. This will identify any serious issues that will need to be addressed before you buy.

Option Fee

One distinguishing feature of a rent-to-own property is the option fee. This is usually between 1 and 5% of the purchase price and is non-refundable. That means if you don’t ultimately qualify for a mortgage, you’ll lose that money.

Home Values Could Drop

Property values aren’t guaranteed. Your landlord estimates the value of the property, but if you’re in a rising market, you might get that home at a steal. While that’s good news for you, the reverse can happen. If housing prices drop substantially during that time frame, you could find yourself buying a property for more than it’s worth.

Contract Breaches Can Be Costly

Rental agreements are a legal obligation. If you don’t pay your rent, your landlord can evict you and keep your security deposit. But rent-to-own contracts bring an additional level of risk. Missed payments mean you could be evicted and lose all the money you’ve put in. That includes the upfront fee and any rent credit you’ve earned.

All that money will also be lost if you can’t qualify for a mortgage when your rental time is up. These agreements can give you some breathing room. However, if your low credit scores, income, lack of a down payment, or employment situation make you ineligible for a mortgage, you could be searching for another rental while losing everything you’ve paid on the lease-to-own home.

Steps to Buy a Rent-to-Own Home

Once you’ve decided renting to own is the route you want to take, you may wonder what to do next. The following steps can help you ensure you get the best deal in a rent-to-own agreement.

1. Find a Home

This is more challenging than it might sound, especially if you’re looking in a competitive real estate market. Rent-to-own homes are extremely rare, so you may have to find a home for sale and try to negotiate this type of setup.

Typically, homeowners become renters when they can’t sell their homes. This means your rent-to-own contract might be on a home that’s in a less desirable or convenient area of town. For someone whose home has been on the market for a while, being able to collect rent money with the promise of a sale in a few years can be a huge relief.

For best results, find a real estate agent who can help you track down a home and negotiate with the seller. The National Association of REALTORS® maintains a directory of real estate agents, but you can also ask for a referral or find real estate agents nearby who have brokered these types of deals recently.

2. Research the Home

Even if it’s tough to find a lease-to-own home in your area, don’t snatch up the first one you find. Crunch the numbers to make sure the rent and purchase price make financial sense for you. Look at the sale history of the home to verify that the owner’s estimated purchase price is somewhat within what the median home price will likely be when your lease expires.

3. Research the Seller

The seller needs to be looked into as well. This is even more important with rent-to-own agreements since this person will be your landlord for the entire lease period. If you see any red flags during your interactions with the seller, move on.

4. Choose the Right Terms

Before you make a real estate purchase, you would have a closing attorney review the documents. The same goes for a rent-to-own agreement. Run all the paperwork past a real estate attorney to make sure there’s nothing in the contract that will hurt you in the long run.

Your real estate agent should be able to negotiate the best terms for you, including how each rent credit will help you build equity and what happens at the end of the lease.

5. Get a Property Inspection

Any time you make a home purchase, it’s essential to know what you’re buying. The same is true for rent-to-own properties. A home inspector can check things out and make sure you aren’t purchasing a home with serious issues.

6. Start Preparing to Buy

Once you start making rent payments, it’s time to start preparing for your eventual home purchase. Chances are, you’ll have to make a sizable down payment on a home loan, so plan to have that ready. Also, keep an eye on your score with all three credit bureaus and make sure you’ll qualify.

A rent-to-own contract can be a good deal for both the buyer and the seller. It can give you time to save money and improve your credit score. A real estate lawyer should take a look at your contracts and make sure your best interests are protected.

Bottom Line

Rent-to-own homes present a unique option for potential homeowners. This approach offers the opportunity to enter the homeownership arena at a slower pace, allowing individuals to build credit, save for a down payment, and experience living in the home before making a final purchase decision.

However, the rent-to-own path isn’t free from drawbacks. Potential buyers should be wary of unfavorable terms, higher monthly payments, and the risk of losing money if they decide not to buy. Ultimately, like all significant decisions in life, choosing a rent-to-own option requires careful consideration and thorough research.

Frequently Asked Questions

Where can I find rent-to-own houses?

Rent-to-own houses can be found through specialized websites dedicated to these types of listings, local real estate agents familiar with the concept, or sometimes through classified advertisements in local newspapers or online platforms.

Can I find rent-to-own homes on Zillow?

Yes, Zillow does list rent-to-own homes. When searching for properties, you can filter the search results to show only rent-to-own options. However, availability may vary based on the region and market conditions.

How long is the typical rent-to-own contract?

The typical lease term ranges from one to five years, but terms can vary based on the agreement between the homeowner and tenant.

Do I have to buy the house at the end of the lease?

No, the decision to buy is optional. However, if you decide not to purchase, you may lose any upfront fees or additional monthly amounts set aside for the potential purchase.

Can the seller change the purchase price once set?

Generally, the purchase price is fixed in the initial agreement. However, some contracts may have clauses allowing price adjustments based on market conditions.

What happens if the property value decreases during the lease period?

If the home’s value decreases and you’ve agreed on a set purchase price, you could end up paying more than the current market value. It’s crucial to negotiate terms that protect your interests.

Who is responsible for repairs and maintenance?

The agreement should clearly outline these responsibilities. In most cases, the tenant bears the responsibility for maintenance and repairs during the lease term.

What’s the benefit of a rent-to-own agreement for sellers?

Sellers can generate rental income while waiting to sell, often at a premium. It also widens the pool of potential buyers, especially those who need time to improve their credit or save for a down payment.

How do property taxes work in a rent-to-own agreement?

In a rent-to-own scenario, the property taxes are typically the responsibility of the homeowner, as they still retain ownership of the property during the rental period. However, the specific arrangement can vary based on the terms of the agreement.

Some contracts may stipulate that the tenant pays the property taxes directly or reimburses the homeowner. It’s crucial for both parties to clearly understand and agree upon who will cover the property tax obligation before entering into a rent-to-own contract.

If I don’t buy, do I get a refund for the extra money paid?

Typically, the extra money paid above regular rent, often referred to as “rent premium,” is forfeited if you decide not to buy.

Is the rent in a rent-to-own agreement higher than usual?

Often, yes. A portion of the monthly rent may be used for the potential down payment or purchase price, making it higher than the average rent for similar properties.

What’s the difference between rent-to-own and mortgage?

Rent-to-own is an agreement where a tenant rents a property with the option to buy it at the end of the lease. No bank is involved initially, and the tenant isn’t obligated to buy. A mortgage, on the other hand, is a loan specifically for purchasing a property. The buyer borrows money from a bank or lender and agrees to pay it back with interest over a predetermined period.

Does rent-to-own hurt your credit?

A rent-to-own agreement, in itself, doesn’t usually affect your credit. However, if the homeowner reports late payments to credit bureaus, it could hurt your credit score. On the positive side, consistently paying on time and eventually securing a mortgage can benefit your credit.

What is another name for rent-to-own?

Rent-to-own agreements can go by various names, including:

Lease to purchase

Lease option

Rent-to-buy

Rent-to-purchase option

Lease purchase

Each of these terms represents the concept of renting a property with the potential option to buy it after a set period.

Sometimes it seems like there’s no middle ground. In California, it tends to go from summer to winter overnight.

We’re talking A/C pumping all day to whipping out extra blankets that same evening. Fortunately, we don’t really have a winter, just some semi-brisk nights.

And it looks as if the housing market hasn’t been much different as of late. You blink and you miss your opportunity.

At least, that’s what the latest round of news tells us, whether true or not.

Two telling reports were released this week that sound great for housing, assuming you already own one, or more specifically, bought one recently at or around the “bottom.”

It wasn’t long ago that housing was looked at as a losing endeavor, but seemingly overnight it has become the hottest investment on planet earth. Well, not in Spain.

In fact, I’m getting a lot of “this is the best time EVER to buy a home” from friends of mine that never uttered a word about housing in the past, let alone anything to do with money or investing.

Perhaps they might be on to something. And every other person I know is either looking for a home or in contract to buy a home, assuming they’re not stuck with an underwater one.

Unfortunately, once the “secret” is out, it’s usually too late.

Buy When No One Else Is

While researchers try to pinpoint the best time to buy a home

It’s not necessarily a certain season or month

Instead it’s when no one else is buying (assuming home prices aren’t absurd)

Because it means less competition and potentially a contrarian victory

The best time to buy a house is when nobody else is. Unfortunately, that time has come and gone.

Just look at a new report from Zillow, which noted that “massive inventory shrinkage” (bad choice of words) has hit the nation.

Nationally, nearly one-fifth of the housing stock has gone bye-bye (-19.4%) in just 365 days.

The change in inventory is measured by looking at the difference in the number of homes listed for sale on Zillow across the country from Sept. 30, 2011 to Sept. 30, 2012.

The drop is even more pronounced in the large metros that were hard-hit by the mortgage crisis.

In Los Angeles, housing inventory is down 37.1%, meaning it’s that much harder to find a property to buy if you haven’t already purchased one.

The largest inventory drop in California was seen in Fresno, where listings have just about been cut in half (-49.4%).

Similar numbers are seen in other hard-hit markets, such as Phoenix (-38.4%), Las Vegas (-35.4%), and Miami (-34%).

Investors Are Taking All the Good Stuff

As per usual it is the pros who are cashing in on the bargains

While first-time home buyers often don’t even get a chance to make an offer

This is one of the main advantages of paying all-cash and knowing what you’re doing

My expectation is for these homes to eventually be flipped and sold to these newbies

Unfortunately, it’s not first-time homebuyers that are getting in on the action, according to Zillow.

Instead, it is savvy investors who are scooping up the homes before first-timers even get a chance to make an offer, mainly because they can pay in cash and close in days, not months.

Yes, it’s take a long, long time to get a mortgage these days, so dealing in cash is much more practical.

These investors then either list the properties as rentals to former homeowners who were foreclosed on, or simply flip them and turn a quick profit.

The newbies might wind up with the homes eventually, but at a premium because they’ve changed hands twice.

Of course, some of these properties are probably in need of some TLC, as most foreclosed properties are typically left in poor condition.

It’s almost like it was during the lead up to the housing crisis, with the developers and flippers making money again.

The difference this time around is the lack of loose financing, and perhaps even underwriting guidelines that are too tight, ironically making it more difficult for everyday Joes to compete.

The result is not a healthier housing market, but one ruled by even more investors than before.

By the way, Zillow has a new report coming out titled, “California’s Housing Market: Navigating the Post-Bottom Landscape.”

So clearly they believe the worst is behind us. I tend to agree, though there will always be ups and downs along the way. And some regions of the country will recover faster than others for reasons unique to those areas.

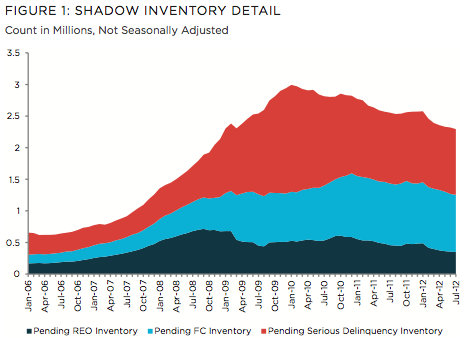

Shadow Inventory Dropping Too

One thing housing economists feared deeply was the shadow inventory

Which was the overhang of foreclosed or soon-to-be foreclosed homes

That came about from the massive housing crisis we experienced

But banks have been extremely patient in unloading them to keep demand strong and supply low

Meanwhile, over at CoreLogic, the so-called shadow inventory has continued to drift lower.

The shadow inventory refers to properties not listed openly on the market, but most likely on their way to being for sale because the owners are either seriously delinquent, in the process of foreclosure, or held by banks but not yet listed on the MLS.

As of July 2012, there were only 2.3 million such units, down 10.2% from a year earlier, thanks to an increase in short sales and other loss mitigation efforts.

The company noted that the decline in shadow inventory foreshadows (no pun intended, just a lack of another word) a rise in home prices, which again, is good news for those who already purchased a home.

But somewhat bad news for those still looking to buy a property, as it probably feels like every week brings with it an unwelcome uptick in home prices.

There’s also the sense that sidelined sellers are probably on the rise. After all, why list your home now if you can list it in a few months and sell at a much higher price?

The sliver of good news is that mortgage interest rates are very low historically, which makes it a great time to take out a fixed-rate home loan for a long, long time.

An inspector general’s report spotlighting talent challenges at the government-sponsored enterprises administering federal home loans Thursday, found that while competition for people remains tight, factors like mission and workplace flexibilities have helped address them.

The white paper, published Thursday by the Federal Housing Finance Agency’s OIG, evaluated the human capital risk trends facing the regulatory agency and the components it oversees — including GSEs Fannie Mae and Freddie Mac, Federal Home Loan Banks and Common Securitization Solutions, LLC — finding common challenges in recruiting and retainment in areas like tech talent demand and compensation constraints.

Agency officials told the OIG that those challenges, combined with external factors like a robust labor market and low unemployment, helped drive a period of higher turnover at some of the regulated entities between 2021 and 2022, though it began to decline at Fannie Mae and reached “historic lows as of mid-2023.”

“Specifically, Fannie Mae reported vacancies in its 2021 and 2022 annual reports—an average of 8 percent to 9 percent of total positions and 10 percent to 12 percent of its technology-related positions,” the report said. “A Freddie Mac document shows its September 2022 overall voluntary turnover was three times its turnover level in 2020.”

Likewise, at the 11 FHLBanks overseen by FHFA, the people risk of turnover was higher for specialized skillsets such as information technology and risk management staff.

The report notes that this is not surprising, given the competition for tech talent nationally and its importance to the regulated entities’ IT operations and data modeling, but noted that market pressures had led Fannie Mae — who reported that 41% of its workforce are in technology-related jobs — to expand its campus hiring of critical skills in IT, modeling and analytics.

Other recent departures in the regulated entities have come from senior leadership positions. Among the factors driving that attrition within the C-suite of Fannie Mae and Freddie Mac were compensation limitations imposed by FHFA’s conservatorship of the two entities, which began in 2008 at the onset of The Great Recession, though the conservatorship itself was not a contributing factor to turnover.

The senior leadership attrition at the regulated entities led them to make adjustments to their succession plans to help mitigate losses.

“One enterprise told us that bolstering its senior level ranks elsewhere in the company exhausted its succession talent pool. In response, this enterprise said it changed its succession planning approach,” the report said. “It now focuses on mitigating people risk for the most critical roles and piloted an effort to strengthen the talent pool for positions below the officer level. The other enterprise says it enhanced its succession planning efforts, too. Its divisions can identify talent below the most senior levels and craft specific development for ‘high potential’ employees.”

Positives from the report also noted that diversity and inclusion efforts have helped talent recruitment and retention, while workplace flexibilities like hybrid work were a mixed bag,

One enterprise told the OIG that hybrid work contributed to its recruitment and retention challenges, but Fannie Mae, CSS and the FHLBanks all cited it as a factor in mitigating turnover and recruiting talent.

Factors like agency mission continue to be a draw for recruiting talent, the report said, but it noted that economic and labor factors will continue to challenge the regulated entities. That makes it important for them to focus on areas like succession planning, while being cognizant of other determinants like workplace flexibilities, organizational size and geographic location.

Millions of Social Security recipients will get a 3.2% increase in their benefits in 2024, far less than this year’s historic boost and reflecting moderating consumer prices.

The cost-of-living adjustment, or COLA, means the average recipient will receive more than $50 more every month beginning in January, the Social Security Administration said Thursday. The AARP estimated that increase at $59 per month.

“This will help millions of people keep up with expenses,” said Kilolo Kijakazi, Social Security’s acting commissioner.

Thursday’s announcement follows this year’s 8.7% benefit increase, brought on by record 40-year-high inflation, which pushed up the price of consumer goods. With inflation easing, the next annual increase is markedly smaller.

Mortgage rates up again

Home loan borrowing costs rose for the fifth straight week, keeping the average long-term U.S. mortgage rate at its highest level in more than two decades and taking another bite out of prospective homebuyers’ purchasing power.

The average rate on the benchmark 30-year home loan rose to 7.57% from 7.49% last week, mortgage buyer Freddie Mac said Thursday. A year ago, the rate averaged 6.92%.

Borrowing costs on 15-year fixed-rate mortgages, popular with homeowners refinancing their home loan, also increased. The average rate rose to 6.89% from 6.78% last week. A year ago, it averaged 6.09%, Freddie Mac said.

The elevated rates combined with a near-historic low level of homes for sale nationally has worsened homebuyers’ affordability crunch by keeping home prices near all-time highs even as sales of previously occupied U.S. homes have fallen 21% through the first eight months of this year versus the same stretch in 2022.

As the Federal Reserve raises interest rates, the cost savings for Veterans’ Affairs home loans could make a substantial difference in affordability

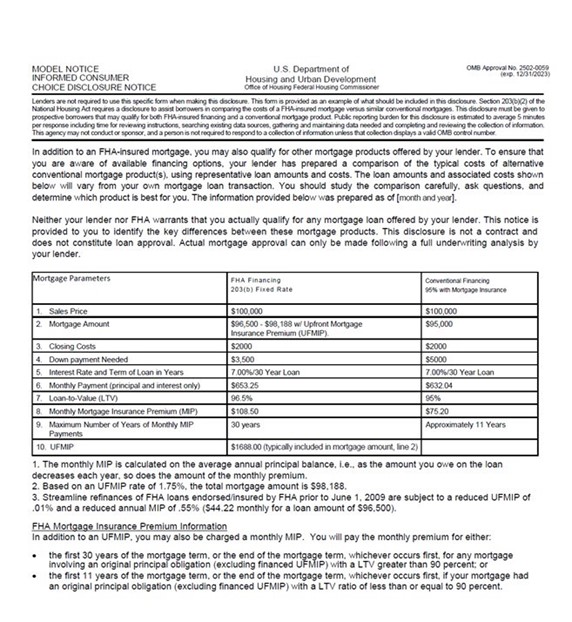

WASHINGTON – U.S. Senators Ben Cardin (D-Md.) and John Boozman (R-Ark.) have introduced legislation, the VA Loan Informed Disclosure Act of 2023 (VALID Act/S. S.2496), that will require a side-by-side comparison between conventional, Federal Housing Administration (FHA), and Veterans’ Affairs (VA) home loans to be included in the U.S. Department of Housing’s “Informed Consumer Choice Disclosure Notice.” VA home loans can offer veterans, active duty, reservists, and national guard members lower down payments, interest rates, and closing costs, saving them tens of thousands of dollars over the life of the loan. Despite these benefits, overall usage of VA home loans is surprisingly low, with only 10 to 15 percent of veterans reported as using the benefit.

“Buying a home often is the most expensive purchase an individual makes in their lifetime. For our veterans and servicemembers who have earned these benefits through service to our nation, we need to make it easier for them to learn about and access the savings they deserve. Far too many are missing out on tens of thousands of dollars of savings; we aim to change that by making the disclosures and comparisons clear and upfront,” said Senator Cardin.

“We can help fulfill the dream of homeownership by informing veterans about the benefits they have earned. VA’s home loans are underutilized, but this bipartisan legislation will provide the men and women who served in uniform another opportunity to learn about resources available to them to save money and meet the needs of their families,” Senator Boozman said.

The VALID Act (S.2496), will provide potential homebuyers a comprehensive picture of veterans’ financing options through a side-by-side comparison of conventional, FHA, and VA home loans. This legislation will help veterans make more informed choices about their financing options and potentially increase the utilization of VA home loans.

“As part of its ongoing commitment to veterans, VAREP applauds Senators Ben Cardin and John Boozman for support of expansion of legislation to include VA loans in the Informed Consumer Choice Disclosure, addressing a key informational gap. This change will empower veterans and servicemembers to make fully informed home loan decisions as they set their sights on the American dream of homeownership,” said G2 Varrato, National Legislative Committee Director of the Veterans Association of Real Estate Professionals (VAREP).

The bill text may bedownloaded here.

Below is a sample of a current Informed Consumer Choice Disclosure Notice. The VALID Act would add an additional column for VA home loans.

Mortgage rates remain at jarringly lofty levels. In late September, the average rate on a 30-year home loan surged past 7.5 percent for the first time since November 2000, according to Bankrate data.

For October, experts don’t expect rates to depart much from that high point.

The biggest risk to mortgage rates is a broad souring of sentiment for Treasurys — a low-probability but extremely high-impact event. Barring that, October will likely bring renewed concerns about a weakening economy and strained consumer, helping reel mortgage rates back in a bit, but not enough to get below the 7 percent threshold.

— Greg McBride, Bankrate chief financial analyst

Fed’s ‘higher for longer’ keeps pressure on mortgages

Mortgage rates broke through 7 percent faster than anticipated. The average rate on a 30-year home loan was 7.42 percent as of early September, according to Bankrate’s weekly national survey of lenders. That figure surged all the way to 7.55 percent in Bankrate’s final survey of the month.

For a 30-year loan at that rate, you’d pay $702 per month for every $100,000 borrowed. At the current median national price of $407,100, that equates to about $2,775 per month, assuming you’re making a 3 percent down payment.

Not long ago, experts thought rates might fall to 5 percent this year.

At its September meeting, the Federal Reserve declined to boost its policy rate again, but did signal it doesn’t expect to cut rates any time soon.

That new outlook led to a spike in 10-year Treasury yields, which are correlated with 30-year mortgage rates.

“Higher for longer seems to be the mentality of the Fed right now,” says Scott Haymore, head of Capital Markets and Mortgage Pricing at TD Bank. “They pushed out any decrease in rates until Q2 2024.”

For months, the major mortgage rate driver was inflation and the Fed’s response. While the policymaker doesn’t directly control mortgage rates, its moves set the overall tone for borrowing costs.

Outlook hazy for the rest of the year

Economists agree that the pandemic-era 3 percent rates aren’t coming back. The question now is how much higher they’ll go.

“The biggest risk to mortgage rates is a broad souring of sentiment for Treasurys — a low-probability but extremely high-impact event,” says Greg McBride, chief financial analyst for Bankrate. “Barring that, October will likely bring renewed concerns about a weakening economy and strained consumer, helping reel mortgage rates back in a bit, but not enough to get below the 7 percent threshold.”

Some are optimistic. The Mortgage Bankers Association (MBA) predicts rates will drop to 6.3 percent by the end of 2023.

Haymore, of TD Bank, sees little change in rates in the near future.

“I think over the remainder of the year, we’ll be within a quarter point of where we are now,” says Haymore. “I don’t think we’ll see 8 percent.”

Lawrence Yun, chief economist at the National Association of Realtors, says that threshold is very much in the realm of possibility.

“In the short run, it’s possible mortgage rates may go to 8 percent,” says Yun.

More forecasts

A roadblock in more ways than one

Despite rising mortgage rates, home price appreciation hasn’t slowed and listings are still moving quickly. As the height of homebuying season fades, buyers are now weighing whether to take a higher rate — in hopes of refinancing later — or, perhaps more frustrating, wait things out.

If your aim is to close by the end of 2023, don’t delay, and carefully consider a rate lock.

“The trend has not been our friend and rates continue to get worse than I had expected based on recent data,” says James Sahnger of C2 Financial Corporation in Jupiter, Florida, adding “until we receive additional data to indicate a decidedly weaker economy, take a defensive posture when locking your rate.”

Rates above 7 percent are as much a psychological barrier as a financial one, says Lisa Sturtevant, chief economist at Bright MLS, a listing service in the Mid-Atlantic region.

“For many would-be homebuyers, a mortgage rate above 7 percent simply means that the numbers do not work for them,” says Sturtevant. “Consumer confidence has started to stumble as individuals and households are becoming more anxious about the economy.”

Indeed, 42 percent of respondents to a recent Bankrate survey cited paying for housing, either a mortgage or rent, as a negative influence on their mental health.

Still, American homeowners have proven their ability to adapt. In the 1980s, mortgage rates averaged 12 percent, but we kept buying homes.

Of course, home values weren’t nearly as high then. Add those two things together, Sturtevant says, and “the seemingly unstoppable housing market may be about to finally and truly stall out.”

Refinancing your mortgage can be a smart financial move if you do it the right way. You can tap into your home equity, get a lower interest rate, or even shorten or lengthen the terms of your loan. All of these are great outcomes for you and your wallet.

But here’s something that’s not so great: Picking the wrong mortgage refinance lender.

This one major mistake can potentially cost you tons of money in closing costs, hidden fees, and high interest rates.

You can avoid that by learning just a bit about what to expect throughout the refinance process and how to find the right lender. We’ll walk you through everything you need to know and give you some suggestions for the big decision.

9 Best Mortgage Refinance Lenders of 2023

We’ve compiled a list of the best mortgage refinance companies with the most competitive mortgage rates. Read through our short reviews to understand what kind of mortgage products they offer and how their process works. It’s an excellent resource for narrowing down your list of refinance lenders to consider.

1. loanDepot

loanDepot is a lender that values and earns customer loyalty. This is evident by their refinancing lifetime guarantee. Once you refinance with them the first time, they will waive their lender fees and reimburse your appraisal fee.

It’s also an excellent choice for people who like a person-to-person connection. You can call them at any time to talk directly to a loan officer.

This can be especially helpful for a refinance because there are many reasons for refinancing and many ways to refinance.

After defining your goals, they let you choose from both fixed-rate and adjustable-rate loans. There are other loan types available, such as jumbo and government, or even home equity loans. The minimum credit score is 620.

They are committed to customer satisfaction and back it up with extensive refinance products.

Terms and conditions apply.

Read our full review of loanDepot

2. LendingTree

LendingTree offers a ton of benefits when it comes to refinancing. First, the online process is very easy and can even get you a mortgage rate quote in under three minutes.

LendingTree isn’t a direct lender and instead matches you up with multiple loan offers with mortgage lenders, so you can compare your options.

Here’s why that’s so helpful.

It makes LendingTree’s refinance options much more robust than many other online lenders. For example, you can convert an adjustable-rate mortgage into a fixed rate or refinance your FHA loan or even VA loan.

You can also cash out home equity as part of your refinance or choose from multiple loan terms.

If you’re still in the information-gathering stage of your refinance journey, LendingTree’s website has many valuable resources.

Play around with numbers to check out different scenarios using tools like their refinance calculator and cost estimator.

Read our full review of LendingTree

3. Rocket Mortgage

Another driving force in the online refinance marketplace is Rocket Mortgage, which is part of Quicken Loans.

The application process is straightforward and can be completed entirely online. You can pick your goal for your refinance to help Rocket tailor your loan offers.

You can even link your financials and property information so that you don’t have to gather and upload all the documentation manually. In fact, 98% of financial institutions in the U.S. can be imported for both your bank statements and investment assets.

Rocket Mortgage also allows you not only to browse different options but also customize them. You can choose from a traditional mortgage product, FHA loans, VA loans, USDA loans as well as fixed or adjustable rates. The minimum credit score is 620.

For an exceptional customer service focused experience that’s entirely based online, Rocket Mortgage is certainly worth exploring.

Read our full review of Rocket Mortgage

4. New American Funding

Another direct lender, New American Funding, is a mortgage company that simplifies the online mortgage process. Get started by selecting the type of real estate you want to refinance.

You can choose from:

Single family home

Condo

Townhouse

Multi-unit

Other

You’ll then answer a series of questions about your personal information, including the existing loan amount and your credit scores.

Afterward, you’ll get a quote estimate on the type of refinance loan you could potentially receive. You can also call the 800-number at any time to speak to one of New American Funding’s loan officers.

The average refinance saves their customers about $360 per month. So, they’re definitely worth checking out, especially if your goal is to lower your payment amount.

Read our full review of New American Funding

5. SoFi

SoFi started as a student loan refinance company and has recently branched out to mortgage refinancing as well. One of the key advantages here is that they go beyond the traditional credit score and base your qualification on high-tech algorithms using various criteria.

In addition to the typical refinance and cash-out refinance options, SoFi also offers a refinance product specific to paying off your student loan debt.

As a result, you could end up lowering your monthly mortgage payment on top of getting rid of your student loan payments.

SoFi lets you check your prequalification for a refinance in just two minutes without affecting your credit score. You can usually close on your new loan within 30 days, and you don’t have to pay any lender origination fees.

A final bonus? If you have an existing SoFi loan, you can qualify for an additional 0.125% rate discount on your refinance.

Read our full review of SoFi

6. Guaranteed Rate

This major lender has offices in each state (plus the District of Columbia) but also lets you get started using its Digital Mortgage platform.

Guaranteed Rate requires a minimum credit score of 620 for mortgage approval. However, alternative credit data, such as utility and rent payments, are considered in some cases.

Guaranteed Rate is highly rated for customer service. They consistently receive stellar customer reviews with a satisfaction rate above 95%.

Whether you want a completely online refinance experience or a more personal one, they deliver.

Read our full review of Guaranteed Rate

7. Carrington Mortgage Services

Carrington begins the process by asking you to select one of four goals:

Lowering your interest rate

Lowering your payments or consolidating debt

Remodeling your home

Getting cash out

Fill out a contact form to have them get in touch with you. Alternatively, you can call Carrington anytime between 7:00 a.m. and 6:00 p.m. PST, Monday through Friday.

If you like a lot of personal care and attention throughout the process, you’ll appreciate Carrington. Their mortgage professionals walk with you every step of the way to ensure you have a speedy and successful closing.

Read our full review of Carrington Mortgage Services

8. Bank of America

One of the biggest banks out there, Bank of America puts its resources to good use by creating a comprehensive and easy online user experience.

You can zip through the application from start to finish by uploading all of your supporting documentation and e-signing with a touch of your finger.

Plus, Bank of America practically has a complete offering of refinancing products, including fixed-rate loans, ARMs, jumbo loans, FHA loans, and VA loans. B of A’s interactive website also makes it easy to get a rough estimate of current mortgage interest rates.

All you have to do is type in your zip code and desired loan amount, and you can see where refinance rates start for various mortgage types.

If you already bank with B of A and are a Preferred Rewards member, you may also be eligible for a reduction of your mortgage origination fee anywhere between $200 and $600.

Read our full review of Bank of America

9. Chase

You don’t need to be a bank member to refinance with Chase. And if you prefer to work with a traditional bank over a strictly online lender or matching website, then Chase is a strong choice.

Start the process online by choosing one of two goals: lowering your monthly payment or cashing out your home equity.

From there, you can get started on the prequalification form. Be prepared to enter information on your current mortgage and your finances.

If you ever have a question before or during the application process, you can either call or connect with a home lending advisor in person in one of 28 states.

There are plenty of refinancing options available through Chase, including jumbo, FHA, VA, and HARP loans. As with most other lenders, the minimum credit score is also 620.

Read our full review of Chase

How does refinancing a mortgage work?

Applying for a refinance is very similar to applying for a home loan. It’s also important to note that you don’t have to use your current lender or servicer. You can pick any mortgage lender that you’d like for your refinance.

After shopping around for lenders and comparing your loan options, you’ll have to complete a formal application. This involves submitting your income and financial statements. The loan officer and underwriter will review your materials to make sure you can afford the new terms.

Mortgage Refinance Requirements

Mortgage refinance lenders are primarily concerned with three things: credit score, debt-to-income ratio, and average loan-to-value ratio (LTV).

Credit score: The minimum credit score for most mortgage refinance companies is around 620.

Debt-to-income ratio: Your monthly debt should not exceed 43% of your monthly take-home pay, just like a regular mortgage. In addition to personal loans and credit card debt, they also include your new mortgage payment in that number.

Loan-to-value ratio (LTV): Lenders would like to see a low loan-to-value ratio (LTV). Typically, you should have at least a 20% equity in your home. In addition to personal loans and credit card debt, they also include your new mortgage payment in that number.

You’ll be required to get an appraisal of your home as part of the process. This makes sure the property lives up to its estimated value and helps determine your total equity in the home. You don’t need to do anything special before the appraiser arrives. However, it is wise to clean and tidy up to make a favorable impression.

Thereafter, you just have to wait for closing. Usually, your lender lets you pick the date, time, and location. Next, they’ll send a notary who will walk you through signing the closing documents. Then, you’ll start fresh with your new payment schedule. If you’ve cashed out some of your home equity, you can typically receive a check or have it deposited directly into your bank account.

How to Choose a Lender to Refinance Your Mortgage

When you decide to refinance, picking the right lender is vital to your financial success.

Mortgage refinance lenders structure loans differently, depending on whether you want to minimize closing costs or lower monthly payments—or a combination of the two.

The first thing to look at is what kind of refinance loans the lender offers. For example, you can find FHA refinance loans with lower minimum credit score requirements than conventional loans if you’re looking for a government-backed refinance.

Loan Terms

Alternatively, you may want to refinance into a shorter term than the standard 30-year fixed mortgage. Look for mortgage refinance companies that offer multiple options, such as 10, 15, or 20-year mortgages. Then, you can compare refinance rates and payments and pick the best one.

As with any kind of loan, you also want to shop around for mortgage rates. Not every lender automatically offers the same interest rate or APR. You’ll also want to compare closing costs as part of the evaluation process. You need to know both your upfront costs and long-term costs in terms of interest.

Closing Costs

If you want to minimize the amount of cash you bring to the table, ask whether your closing costs can be rolled into the loan.

There are numerous ways you can tackle mortgage refinancing. That’s why picking the right refinance lender can make a huge difference. They can help you understand the pros and cons of different options, so you can make the right choice.

Don’t be afraid to ask questions. Ask for specific numbers, and talk to a few different lenders to get an idea of their recommendations and refinance process.

When to Refinance a Mortgage

Now that you’ve learned of the best refinance lenders out there, make sure you’re refinancing for the right reasons. Here are some of the most common reasons for refinancing a mortgage.

Lower Your Monthly Payments

It’s entirely possible to refinance to lower your payment amount. To save money over the life of your loan, you could refinance into a lower interest rate if mortgage rates have dropped since you got your loan. Or, if your credit score has improved, you might be able to qualify for a lower refinance rate as well.

If you’re having trouble making your payments, you could also consider refinancing into a longer loan term. This spreads out your existing mortgage amount over more years.

For example, if you’ve been paying your mortgage for 10 years on a 30-year loan, you could extend the existing 20 years over another 30 years. However, you should proceed with caution, depending on your financial situation and retirement plans.

Cash Out Your Home Equity

If you have equity in your home—at least 20%—you could potentially qualify for a cash-out refinance. This allows you to get a lump sum of money and then add that amount to your existing loan. Usually, you can borrow up to 80% of your equity.

Let’s take a look at an example.

Say your home is valued at $200,000, and your mortgage is down to $150,000. That leaves you with $50,000 in equity. The bank will let you borrow up to 80% of that, which is $40,000.

If you qualify for the mortgage, you could then refinance a total of $190,000. You can then use the cash for home renovations, college tuition, medical bills, high-interest debt, or anything else.

Change the Terms

Shorter loan terms typically come with lower mortgage rates since there’s less of a chance for you to default on the loan. Once you’ve paid off a portion of your current 30-year mortgage, you may be able to save on interest by switching to a 15-year mortgage.

If, for example, you’re 15 years into a 30-year fixed mortgage, you only have 15 years left to pay. So, you could potentially save thousands by getting a lower interest rate via an actual 15-year fixed mortgage.

Switch to a Fixed Rate Mortgage

If you initially took out an adjustable-rate mortgage (or ARM) and your fixed period is ending, you should consider refinancing your loan. There’s a cap on how high your adjustable mortgage can go. It could potentially be much higher than current fixed interest rates.

Talk to a lender to see the best option to avoid a significant jump in your monthly payment. And be sure to plan ahead since it can take time for the approval process to finish.

See also: How to Refinance Your Mortgage

When Not to Refinance

When shouldn’t you refinance? If your credit score has dropped significantly since you took out your original mortgage, you may be surprised by higher interest rates. Similarly, refinancing today may not save you money if you qualified for a rock-bottom rate during the recession.

Furthermore, consider that every mortgage refinance comes with closing costs, just like your initial home loan. Therefore, you need to make sure any financial benefits you expect to receive from your refinance outweigh the added closing costs.

All of these considerations can be discussed with a suitable lender, whether in person, on the phone, or online. Do the research it takes to make sure you’re making an intelligent decision on your next home refinance.

Frequently Asked Questions

What are the steps to refinancing a mortgage?

The process of refinancing a mortgage typically includes the following steps:

Determine if refinancing makes sense for your financial situation and goals.

Research and compare different mortgage lenders.

Choose the right lender and loan product for your needs.

Complete a formal application, providing all necessary income and financial documents.

Wait for the lender’s underwriting process, which includes verifying your information and appraising the home.

Once approved, arrange for a closing where you will sign all required documents.

Begin your new payment schedule, or receive your funds if you’ve done a cash-out refinance.

How does refinancing a mortgage affect my credit score?

Refinancing a mortgage can temporarily lower your credit score, as the lender will perform a hard credit check during the application process. This is typically a small drop and should recover over time as long as you continue to make regular, on-time payments. Additionally, the old mortgage will be marked as paid off on your credit report, which can be beneficial to your credit history in the long run.

What are some reasons I might not qualify for a mortgage refinance?

If your credit score has significantly dropped since you took out your original mortgage, you may not qualify for a favorable interest rate, making refinancing less beneficial. Additionally, if your debt-to-income ratio is too high, you may not qualify. Lastly, if you do not have sufficient equity in your home (usually at least 20%), you may not qualify for certain types of refinancing.

Can I refinance my mortgage with bad credit?

While it may be more difficult to refinance your mortgage with bad credit, it’s not impossible. Some lenders specialize in loans for individuals with poor credit, and government programs like the FHA refinance loans may have lower credit score requirements. However, be aware that you will likely be offered higher interest rates.

How much does it cost to refinance a mortgage?

The cost of refinancing a mortgage typically includes an origination fee, an application fee, an appraisal fee, and closing costs, among other potential costs. This can usually amount to between 2% and 6% of the loan amount. However, in some cases, you may be able to roll these costs into your loan to reduce your out-of-pocket expenses at closing.

Can I refinance my mortgage more than once?

Yes, you can refinance your mortgage more than once. However, it’s important to consider the costs of refinancing, such as closing costs and possible prepayment penalties, and weigh them against the benefits you expect to receive. You’ll want to make sure that refinancing makes financial sense each time.

What’s the difference between a cash-out refinance and a rate-and-term refinance?

In a cash-out refinance, you take out a new mortgage for more than what you currently owe, and then receive the difference in cash. This can be useful if you need to cover large expenses or consolidate higher-interest debt.

A rate-and-term refinance, on the other hand, changes the interest rate, the term length, or both of your existing mortgage, but you don’t receive any cash. This is typically done to lower monthly payments or to pay off the loan faster.

When should I consider a fixed-rate mortgage over an adjustable-rate mortgage?

A fixed-rate mortgage may be a better option if you plan to stay in your home for a long period of time and want predictable, stable monthly payments. On the other hand, an adjustable-rate mortgage (ARM) may initially offer a lower interest rate, but it can fluctuate over time. An ARM could be a suitable option if you plan to sell or refinance your home before the interest rate starts adjusting.

Buying a home in the U.S. often involves weighing the trade-offs between a 15-year and 30-year mortgage. With the interest rate staying constant, the first option has higher monthly payments, but the loan is repaid sooner than it is with the second option that offers lower monthly payments.

But home loan borrowers in the U.K., Canada, Australia and most European countries have a wider array of choices: They can break up their loan tenure into smaller chunks of two, three, or five years, and get lower interest rates as their loan size reduces and credit rating improves over time.

A new research paper by Wharton finance professor Lu Liu, titled “The Demand for Long-Term Mortgage Contracts and the Role of Collateral,” focuses on the U.K. housing market to explain the choices in mortgage fixed-rate lengths by mortgage borrowers. She pointed out that the length over which mortgage rates stay fixed is an important dimension of how households choose their mortgage contracts, but that has “not been studied explicitly thus far.” Her paper aims to fill that gap.

Liu explained that the U.K. market is “an ideal laboratory” for the study for three reasons: It offers borrowers an array of mortgage length choices; it is a large mortgage market with relatively risky mortgage loans similar to the U.S.; and it offers the opportunity to study market pricing of credit risk in mortgages. In the U.S. market, the pricing of credit risk is distorted as the government-backed Fannie Mae and Freddie Mac provide protection against defaults. “The U.S. is a big outlier in mortgage structure. It has essentially removed credit risk in the markets for long-term contracts.”

How Beneficial Are Long-term Mortgages?

At first sight, long-term mortgage contracts may seem preferable because they have a fixed interest rate, and thus allow borrowers to protect themselves from future rate spikes, the paper noted. “Locking in rates for longer protects households from the risk of repricing, in particular having to refinance and reprice when aggregate interest rates have risen,” Liu said. “In order to insure against such risks, risk-averse households should prefer a longer-term mortgage contract to the alternative of rolling over two short-term mortgage contracts, provided that they have the same expected cost.”

But in studying the U.K. housing market, Liu found that there is an opposing force that may lead some households to choose less protection against interest rate risk. This has to do with how the decline of credit risk over time affects the credit spreads borrowers pay. She explained how that occurs: As a loan gets repaid over time, the loan-to-value (LTV) ratio decreases as households repay the loan balance and house prices appreciate, the paper noted. This reduces the credit spread that households pay on their mortgage over time. When high-LTV borrowers decide to lock in their current rate, the credit spread will account for a large portion of that rate.

“[30-year mortgages] have had knock-on effects on mobility and housing markets due to mortgage lock-in.” – Lu Liu

As the LTV ratio declines and collateral coverage improves over time, they raise the opportunity cost of longer-term contracts, in particular for high-LTV borrowers, Liu noted. “Locking in current mortgage rates [protects] households against future repricing, but it also locks in the current credit spread, leading households to miss out on credit spread declines over time.”

High-LTV borrowers, or those who opt for low down payments and bigger loans, have to initially pay large credit spreads that can be as high as 220 basis points higher than what a borrower with prime-grade credit would pay. But refinancing with shorter-term contracts allows them to reduce those credit spreads over time. “They’re not locking in to a rate over 30 years; they’re probably locking in at shorter terms of two, three, or five years, and they do it maybe six or seven times,” Liu said. Riskier borrowers with higher LTV ratios hence face a trade-off, as locking in rates while the LTV is high is relatively costly, so they end up choosing shorter-term contracts, meaning they choose less interest-rate protection than less risky borrowers.

“In markets where the credit risk is priced using market prices – without government intervention as in the U.S. — the credit risk is expensive as lenders charge relatively higher rates for that,” Liu said. “If I’m a risky borrower, I face this very difficult trade-off: I want to insure myself like everyone else. But it also means that I’m locking in relatively high rates, with a big credit spread.” That of course does not always make sense for borrowers, she pointed out. “This may help explain why very long-term mortgage contracts with high-LTV mortgage lending are rare across countries.”

Liu said her data, which covered the period from 2013 to 2017, showed that the propensity is lower among riskier borrowers to opt for a 5-year fixed-rate mortgage compared to a 2-year fixed-rate mortgage. The higher the loan-to-value ratio, the lesser was their incentive to choose longer mortgage tenures, her research found. “Borrowers at 95% LTV are less than half as likely to take out a 5-year fixed-rate contract, compared to borrowers at 70% LTV,” the paper stated. The findings help explain the “reduced and heterogeneous demand for long-term mortgage contracts.”

How to Make U.S. Mortgages More Efficient

Liu said the findings in her paper are relevant for mortgage market design. “High-LTV borrowers face a difficult trade-off between their demand to lock in overall interest rate levels, and an expected decline in credit spreads over time,” she said. “Households could benefit substantially from being able to lock in base interest rates, while repricing their credit spreads.”

The findings are important also from both a monetary policy and financial stability perspective, Liu continued. “High-LTV borrowers are more exposed to interest rate risk, which can also cause vulnerabilities in a rising rate environment, since these borrowers may be most affected by mortgage cost increases.”

“There is political resistance to institutional change and borrower resistance to novel mortgage products.” – Lu Liu

The findings of Liu’s research are also timely, given the recent spike in the inflation rate. She noted that the U.S. Federal Reserve has increased interest rates more aggressively than its counterparts in the U.K., Canada, and Australia. All those countries have varying degrees of short-term fixed or variable-rate mortgages. Unlike in those countries, U.S. mortgage borrowers are “relatively shielded from interest rate rises, as the vast majority of households have locked in previous low rates for 30 years,” she noted.

Unintended Consequences of Long-term Mortgage Contracts

But the design of mortgage contracts in the U.S. creates disruptions beyond the housing markets to the broader financial system. “The 30-year fixed-rate mortgages in the U.S. have led to duration mismatch and financial stability risks in the banking sector, as rate rises have reduced the market values of these loans and mortgage-backed securities,” Liu said. She cited the recent collapse of Silicon Valley Bank as a case in point, which was triggered by the fall in the valuation of its bond holdings in a rising interest rate environment. In the U.K., in contrast, banks typically hedge the 2-to 5-year fixed-rate legs of mortgages using swaps, with the remaining part of the contract having a variable rate and thus not causing duration mismatch for the banks.

Long-term contracts have other consequences, too. “The [30-year mortgages] have had knock-on effects on mobility and housing markets due to mortgage lock-in,” Liu continued. Mortgage lock-in occurs in a rising interest rate environment, where homeowners find it a losing proposition to refinance mortgages they had taken out when interest rates were at historical lows. As a result, “people aren’t moving, and the housing market is frozen,” she said.

Liu said policy makers ought to rethink the 30-year fixed-rate mortgage, noting that Harvard economics professor John Y. Campbell had proposed that in a presentation at the Georgia Tech-Atlanta Fed Household Finance Conference in March 2023.

That said, the nature of mortgage systems in different countries is “highly persistent over time,” so any recommendation to radically change them might be far-fetched, Liu noted. “There is political resistance to institutional change and borrower resistance to novel mortgage products,” she added. If the U.S. were to move in the direction of more of a Canadian system that has mortgage rates fixed for five years, she noted, “any implementation of shorter-term fixed-rate contracts would need to take into account the credit risk dimension, which could result in risky households insuring less against interest rate risk.” Such a move has the potential to make monetary policy more effective and the banking system more stable, but further research is needed, she added.

Customer engagement platform Total Expert‘s customer intelligence and mortgage tech firm Polly‘s product and pricing engine (PPE) will help California-based lender Mountain West Financial identify lending opportunities from its existing database.

By deploying customer intelligence from Total Expert — a customer engagement platform for financial institutions — Mountain West Financial will provide automated alerts that notify its loan officers in real-time when a customer’s behavior or financial situation signals they’re a good candidate for a home loan, Total Expert said.

Total Expert’s customer intelligence identifies a potential customer through home listings, interest rates, home equity and credit pulls, according to the company.

“The only way for today’s financial institutions to not just survive, but actually thrive, is by growing their customer lifetime value,” Joe Welu, founder and CEO of Total Expert, said.

Polly’s PPE is designed to maximize margins and facilitate speed and accuracy across all loan pricing and lock processes.

Polly’s API integration with Total Expert enables lenders to speed up the deal flow by engaging with the borrower’s lifecycle earlier via action-oriented product offers, according to both companies.

The tailored rate fliers feature personalized interest rates, payments and APRs based on unique borrower details, such as loan type, loan amount, property location and down payment.

The combination of Polly and Total Expert will “modernize and transform outdated mortgage processes that impair the lending sales process, and as a result, creates a far more relevant and optimal experience for borrowers,” Parvesh Sahi, chief revenue officer at Polly, added.

Since its launch in 2022, Total Expert’s customer intelligence created automated alerts that led to more than $10.7 billion in generated loan application volume, and $6.7 billion in funded loans, according to the firm.

California-headquartered Polly is a provider of mortgage capital markets technology for banks, credit unions and mortgage lenders nationwide.

UK mortgage war ‘under way’ as lender offers 4.99% fixed rate

Brokers say borrower confidence likely to lift after the first below 5% deal surfaces since June with more offers likely soon

A fixed-rate mortgage priced at below 5% has gone on sale for the first time since June as leading lenders announced a fresh wave of home loan reductions.

Brokers said a mortgage rate war was “well and truly under way” and that the lower pricing should provide a boost to borrowers worried about the imminent end of their current deal, as well as would-be homebuyers who have been sitting on the sidelines.

UK lenders have been reducing their rates for several weeks, and the last few days have seen a flurry of reductions, with further cuts due to take effect on Friday courtesy of banks including the Halifax.

On Thursday, a five-year fixed-rate deal priced at 4.99% was launched by The Mortgage Works, a division of Nationwide building society, which brokers said was the first sub-5% fixed deal they had seen for several months. It is thought it is the first fixed-rate product priced at below that level since late June.

The 4.99% product is a buy-to-let deal rather than a standard residential mortgage and is available to people borrowing up to 55% of the property’s value. Ranald Mitchell, a director at the broker firm Charwin Private Clients, said: “Seeing rates starting with a 4 is a sight for sore eyes and could provide a stimulus to the market and borrower confidence.”

Moneyfacts, the financial data provider, said the average rate on a new fixed-rate deal lasting for five years was now 6.14%, though there are best-buy deals available that are considerably cheaper than that: for residential mortgages, the cheapest five-year fix on Thursday was priced at 5.12%.

Halifax has announced reductions of up to 0.5 percentage points on selected fixed deals, taking effect from Friday. It means it will have five-year fixed deals priced at 5.15%.

The Mortgage Works has also cut rates by up to 0.5 percentage points, with effect from Thursday, while brokers say Coventry building society is also reducing some rates on Friday.

These moves come hard on the heels of cuts by other high street players. On Wednesday, Nationwide reduced some of its fixed rates by up to 0.29 percentage points, while on the same day Santander trimmed selected new fixes by up to 0.14 percentage points.

Mortgage costs had been rising for months, but UK lenders have been reducing their rates since the second half of July after it emerged that UK inflation fell further than expected in June.

skip past newsletter promotion

after newsletter promotion

However, another Bank of England rate rise next week – a decision will be announced on 21 September – could put the brakes on further reductions. The Bank’s base rate is now at 5.25%, and many commentators anticipate a rise to 5.5%.

Amit Patel, an adviser at the broker Trinity Finance, said: “After a summer of doom and gloom, it feels that as we head into the autumn months, we may have turned the corner.”

Diarmuid Phoenix, an adviser at Mint Mortgages & Protection, said: “Seeing the return of rates under the 5% bracket in line with falling swap rates should hopefully give a boost of confidence to borrowers who have been living in fear of the end of their current fixed-rate deals, as well as those who have been sitting on the fence waiting for rates to come down before purchasing.”