According to Kelley Blue Book, the average price for a light vehicle in the United States was almost $38,000 in March 2020. Of course, the sticker price will depend on whether you want a small economy car, a luxury midsize sedan, an SUV or something in between. But the total you pay for a vehicle also depends on a number of other factors if you’re taking out a car loan.

Get the 4-1-1 on financing a car so you can make the best decision for your next vehicle purchase.

Decide Whether to Finance a Car

Whether or not you should finance your next vehicle purchase is a personal decision. Most people finance because they don’t have an extra $20,000 to $50,000 they want to part with. But if you have the cash, paying for the car outright is the most economical way to purchase it.

For most people, deciding whether to finance a car comes down to a few considerations:

Do you need the vehicle enough to warrant making a monthly payment on it for several years?

Is the deal, including the interest rate, appropriate?

Factors to Consider When Financing a Car

Obviously, the first thing to consider is whether you can afford the vehicle. But to understand that, you need to consider a few factors.

Total purchase price. Total purchase price is the biggest impact on how much you’ll pay for the car. It includes the price of the car plus any add-ons that you’re financing. Depending on the state and your own preferences, that might include extra options on the vehicle, taxes and other fees and warranty coverage.

Interest rate, or APR. The interest rate is typically the second biggest factor in how much you’ll pay overall for a car you finance. APR sounds complex, but the most important thing is that the higher it is, the more you pay over time. Consider a $30,000 car loan for five years with an interest rate of 6%—you pay a total of $34,799 for the vehicle. That same loan with a rate of 9% means you pay $37,365 for the car.

The terms. A loan term refers to the length of time you have to pay off the loan. The longer you extend terms, the less your monthly payment is. But the faster you pay off the loan, the less interest you pay overall. Edmunds notes that the current average for car loans is 72 months, or six years, but it recommends no more than five years for those who can make the payments work.

It’s important to consider the practical side of your vehicle purchase. If you take out a car loan for eight years, is your car going to still be in good working order by the time you get to the last few years? If you’re not careful, you could be making a large monthly payment while you’re also paying for car repairs on an older car.

Get matched with a personal

loan that’s right for you today.

You can buy a car anytime if you have the cash for the purchase. If you have no credit or bad credit, your options for financing a car might be limited. But that doesn’t mean it’s impossible to get a car loan without credit.

Many banks and lenders are willing to work with people with limited credit histories. Your interest rate will likely be higher than someone with excellent credit can command, though. And you might be limited on how much you can borrow, so you probably shouldn’t start looking at luxury SUVs. One tip for increasing your chances is to put as much cash down as you can when you buy the car.

If you can’t get a car loan on your own, you might consider a cosigner. There are pros and cons to asking someone else to sign on your loan, but it can get you into the credit game when the door is otherwise barred.

Personal Loans v. Car Loans: Which One Is Better?

Many people wonder if they should use a personal loan to buy a car or if there is really any difference between these types of financing. While technically a car loan is a loan you take out personally, it’s not the same thing as a personal loan.

Personal loans are usually unsecured loans offered over relatively short-term periods. The funds you get from a personal loan can typically be used for a variety of purposes and, in some cases, that might include buying a car. There are some great reasons to use a personal loan to buy a car:

If you’re buying a car from a private seller, a personal loan can hasten the process.

Traditional auto loans typically require full coverage insurance for the vehicle. A personal loan and liability insurance may be less expensive.

Lenders typically aren’t interested in financing cars that aren’t in driving shape, so if you’re buying a project car to work on in your garage during your downtime, a personal loan may be the better option.

But personal loans aren’t necessarily tied to the car like an auto loan is. That means the lender doesn’t necessarily have the ability to repossess the car if you stop paying the loan. Since that increases the risk for the lender, they may charge a higher interest rate on the loan than you’d find with a traditional auto loan. Personal loans typically have shorter terms and lower limits than auto loans as well, potentially making it more difficult for you to afford a car using a personal loan.

Steps You Should Follow When Financing a Car

Before you jump in and apply for that car loan, review these six steps you should take first.

1. Check your credit to understand whether you are likely to be approved for a loan. Your credit also plays a huge role in your interest rate. If your credit is too low and your interest rate would be prohibitively high, it might be better to wait until you can build or repair your credit before you get an auto loan. Sign up for ExtraCredit to see 28 of your FICO scores from all three credit bureaus.

2. Research auto loan options to find the ones that are right for you. Avoid applying too many times, as these hard inquiries can drag your credit score down with hard inquiries. The average auto loan interest rate is 27% on 60-month loans (as of April 13, 2020).

3. Get your trade-in appraised. The dealership might give you money toward your trade-in. That reduces the price of the car you purchase, which reduces how much you need to borrow. A few thousand dollars can mean a more affordable loan or even the difference between being approved or not.

4. Get prequalified for a loan online. While most dealers will help you apply for a loan, you’re in a better buying position if you walk into the dealership with funding ready to go. Plus, if you’re prequalified, you have a good idea what you can get approved for, so there are fewer surprises.

5. Buy from a trusted dealer. Unfortunately, there are dealerships and other sellers that prey on people who need a car badly. They may charge high interest or sell you a car that’s not worth the money you pay. No matter your financial situation, always try to work with a dealership that you can trust.

6. Talk to your car insurance company. Different cars will carry different car insurance premiums. Make a call to your insurance company prior to the sale to discuss potential rate changes so you’re not surprised by a higher premium after the fact.

Next to buying a home, buying a car is one of the biggest financial decisions you’ll make in your life, and you’ll likely do it more than once. Make sure you understand the ins and outs of financing a car before you start the process.

The Fannie Mae Flex Modification Program (FMP) is a mortgage assistance solution designed to relieve borrowers facing financial hardship.

Are you looking to improve your mortgage management but don’t know where to start? Handling mortgage payments is challenging, especially if you’re facing economic difficulties and don’t know where or how to get financial assistance. The Fannie Mae and Freddie Mac Flex Modification Program may be the solution you’re looking for.

Learn what you need to know about the Flex Modification Program: how it works, who qualifies for it, and how you can apply. This comprehensive guide will help you understand the many benefits of FMP for a more stable financial future.

In This Piece:

What Is the Flex Modification Program?

The Fannie Mae Flex Modification program is a mortgage assistance solution designed to relieve borrowers facing financial hardship. This program offers a flexible framework for loans that helps eligible borrowers to modify their monthly mortgage payments and avoid foreclosure.

Modifying the loan terms can make mortgage payments more affordable and sustainable for struggling homeowners.

Get matched with a personal

loan that’s right for you today.

Learn

more

How Do Fannie Mae and Freddie Mac Work?

The mortgage market has a few essential entities, including the government-sponsored enterprises called Fannie Mae and Freddie Mac. Their approach allows lenders to free up funds to provide more mortgage loans to borrowers.

But how does it work? Fannie Mae and Freddie Mac helped make mortgages more accessible by buying them from lenders. This allows lenders to have more money available to provide new mortgages to borrowers or invest in other financial opportunities. For example, if a lender originates a mortgage, they can sell it to Fannie Mae or Freddie Mac, who then include it in their portfolio or package it into mortgage-backed securities.

How Flex Modification Works

The Flex Modification Program offers loan modifications to eligible borrowers experiencing financial hardship. Here’s a breakdown of how the program operates:

Eligibility Requirements:

You must have a mortgage loan owned or guaranteed by Fannie Mae or Freddie Mac.

The mortgage loan must be at least 60 days delinquent or at risk of imminent default.

You must demonstrate a hardship that affects your ability to make timely mortgage payments.

Modification Terms:

The program aims to reduce your monthly mortgage payment to 20% or more below your pre-modification.

The modification may involve adjusting the interest rate, extending the loan term, or forbearing a principal portion.

The goal is to make the mortgage payment more affordable while ensuring it’s sustainable for you.

Application Process:

Apply to the Flex Modification Program through a loan servicer.

The loan servicer will assess your eligibility and collect the necessary documentation.

Once approved, the loan servicer will work with you to finalize the modification terms.

Why Should You Consider the Flex Modification Program?

Before considering the Flex Modification Program, it’s essential to understand its potential pros and cons.

Pros:

Lower monthly payments: The program aims to reduce your mortgage payment to a more affordable level, making it easier to manage your finances on time.

Protection from foreclosure: By modifying your loan, the program can help you avoid the devastating consequences of foreclosure.

Improved financial stability: By participating in the Flex Modification Program, you can regain control of your financial situation. Providing you with a sense of stability and peace of mind, allowing you to focus on rebuilding your financial health.

Simplified application process: Applying for the program is relatively straightforward, and you can work directly with your loan servicer to navigate the process.

Potential principal reduction: The FMP may offer this, which means that a portion of the outstanding loan balance could be forgiven or deferred, reducing the overall amount owed. This can be particularly beneficial if you owe more on the mortgage than your current property value.

Preservation of homeownership: One of the primary goals of the FMP is to help borrowers preserve their homeownership. The program offers a viable alternative to foreclosure by providing a framework for loan modifications.

Cons:

Extended loan term: Modifying your loan may result in a more extended repayment period, meaning you’ll make mortgage payments for longer.

Impact on credit score: While participating in the program doesn’t directly affect your credit score, the delinquency prior to modification might be reported on your credit report.

Limited availability: The program is specifically for Fannie Mae or Freddie Mac borrowers with owned or guaranteed loans. You won’t qualify for this program if either entity doesn’t back your loan. However, other programs may exist. Contact your lender if you’re struggling to make your mortgage payments.

Remember, these pros and cons will vary based on your circumstances. It’s essential to consult with your loan servicer and thoroughly review the modification terms to understand the potential benefits you may receive from participating in the program.

Who Qualifies for the Flex Modification Program?

The Flex Modification Program is designed for borrowers struggling with mortgage payments due to financial hardship.

To qualify for the program, you must meet the following criteria:

Loan ownership: The mortgage loan must be owned or guaranteed by Fannie Mae or Freddie Mac.

Delinquency or imminent default: Borrowers must be at least 60 days delinquent on their mortgage payments or at risk of imminent default.

Demonstrated hardship: Borrowers need to demonstrate a hardship that affects their ability to make timely mortgage payments. Hardships may include job loss, income reduction, medical expenses, divorce, or other significant life events.

Additionally, you must comprehend what a “hardship” entails to be considered for a loan modification. Each situation is evaluated individually, but common examples of hardships include loss of income, disability, serious illness, divorce, or the death of a co-borrower.

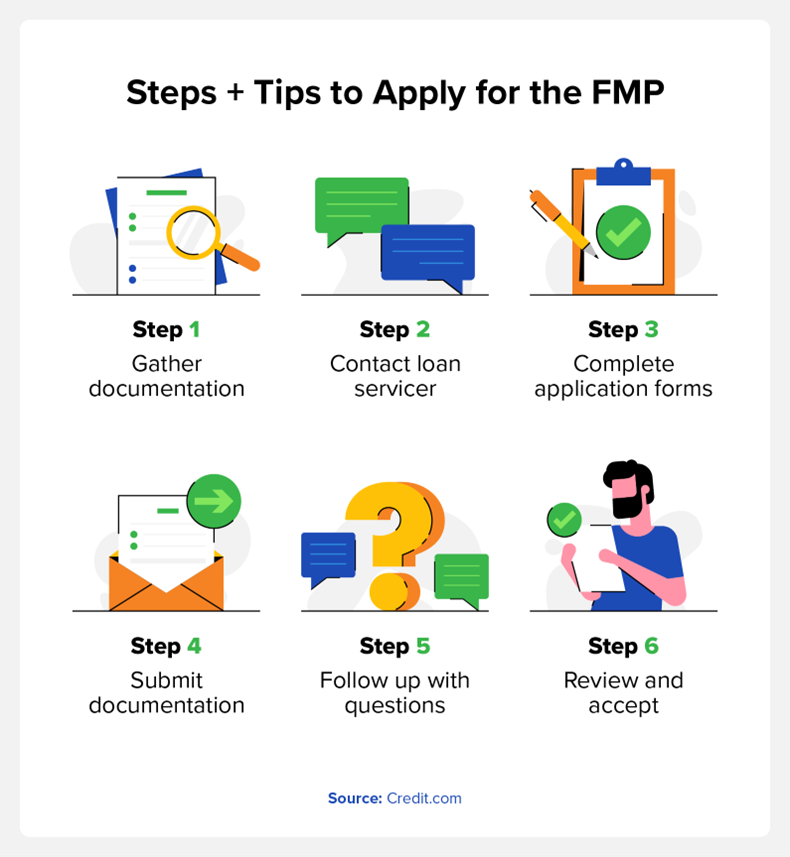

How to Apply for the FMP

If you believe you meet the eligibility requirements for the Flex Modification Program, you can follow these steps and tips to apply:

Gather documentation: Prepare the necessary documents, such as proof of income, bank statements, tax returns, and any other documentation required by your loan servicer.

Contact your loan servicer: Inform your loan servicer about your interest in the Flex Modification Program.

Complete application forms: Your loan servicer will provide the necessary forms and guidance to complete the application process.

Submit documentation: Submit all the required documentation and the completed application forms to your loan servicer.

Follow up and provide additional information: Be proactive in promptly following up with your loan servicer and providing any additional information they request.

Review and accept the modification terms: Once your loan servicer evaluates your application, they will provide you with the proposed modification terms. Review them carefully and, if acceptable, sign and return the necessary paperwork to proceed with the modification.

Remember, each loan servicer may have a specific application process, so it’s crucial to communicate directly with them to ensure you have all the necessary information and are following the correct steps. Having to redo the application process due to easily-avoided mistakes is the last thing you need.

Other Mortgage Payment Help Options

What if I don’t qualify? What can I do? Other mortgage payment assistance options are available if the FMP is not the right fit.

Fannie Mae and Freddie Mac offer additional programs catering to different circumstances. Some of these options include:

Home Affordable Modification Program (HAMP): This aims to help homebuyers struggling with financial hardship and mortgage payments.

Repayment plan: Allows you to catch up on missed mortgage payments by adding a portion of the past-due amount to your regular expenditures over an agreed-upon period.

Forbearance: Temporarily suspends or reduces your mortgage payments with this program. It can be for a specific period, providing short-term relief during financial difficulties, so you can reassess the situation.

But before you move forward with one of these, it’s essential to analyze your alternatives and consult with your loan servicer to determine the best course of action based on your specific circumstances.

FAQs

Let’s address some frequently asked questions about the Flex Modification Program:

Does the Flex Modification Program Affect Your Credit Score?

Participating in the Flex Modification Program doesn’t directly impact your credit score. However, the delinquency prior to modification might be reported on your credit report

What if Fannie Mae or Freddie Mac Doesn’t Own My Loan?

If your loan isn’t owned or guaranteed by Fannie Mae or Freddie Mac, you won’t be eligible for the Flex Modification Program. However, you should contact your loan servicer to inquire about other available mortgage assistance options or loan modification programs specific to your loan type.

How Long Does the Flex Modification Program Last?

The duration of the Flex Modification Program varies depending on the specific terms of the modification. Typically, the program aims to provide long-term mortgage relief by modifying the loan terms to make payments more affordable and sustainable for the borrower.

The revised terms may involve extending the loan term or adjusting the interest rate. It’s important to discuss the duration of the modification with your loan servicer, as it will depend on your circumstances and the terms agreed upon.

Can I Qualify for the Flex Modification Program if I’ve Previously Received a Loan Modification?

If you have previously received a loan modification, you may still be eligible for the Flex Modification Program. However, the specific requirements and eligibility criteria may change depending on your previous modification and the current guidelines set by Fannie Mae and Freddie Mac.

It’s crucial to communicate with your loan servicer and provide them with all the necessary information regarding your previous modification. They will assess your eligibility based on your unique circumstances and guide you through the application process.

Remember, these answers are general guidelines, and you must consult with your loan servicer to get accurate and personalized information based on your situation.

What Are the Next Steps?

The Fannie Mae Flex Modification Program provides borrowers with a potential lifeline during financial hardship. It aims to make mortgage payments more manageable and sustainable by offering loan modifications. If you’re facing challenges with your mortgage payments, exploring the Flex Modification Program and other mortgage payment help options can help you find the assistance you need.

To take control of your mortgage management and improve your financial well-being. Consult with your loan servicer for accurate and personalized information based on your situation, and research different mortgage rates to make informed financial decisions.

Car insurance can be confusing. First, there are all the policy considerations: Do you want a policy with comp and collision? How much liability should you carry? Do you need uninsured motorist coverage? Even once you make decisions on all these things, the bill that arrives can be difficult to understand—exactly what goes into the pricing for your car insurance premium? Here’s what car insurance companies don’t want you to know about premium pricing.

Your car insurance may not be tied to the driver.

The type of car you drive matters.

Prior claims and questions raise rates.

You can check your report for errors.

Your credit score impacts your car insurance costs.

Where you live impacts your premium account.

Your age affects your car insurance premium.

Gender, marital status, job and education level can affect premiums.

If you bought your car with a loan, your premium may be higher.

You can lower your insurance rates.

You have options if insurance denies your claim.

Is Car Insurance Tied to Car or Driver?

Technically, car insurance is tied to the car. That means if you let someone else drive your car, your insurance may kick in if there is an accident. Not all insurance policies cover all uses of your vehicle, though, so read the fine print on yours before you allow someone else to drive it. You may also be able to exclude drivers who live with you from your policy if you don’t ever want them driving your car and don’t want them impacting the cost of your policy.

>> Find Car Insurance Quotes.

Does It Matter What Kind of Car You Drive?

The total value of your car, what type of vehicle it is and what type of safety rating it has all factor into the cost of your policy. Other factors can include how many miles you drive each year, where you park your car, and how many expensive extra features your car has.

Does Your Driving Record Affect Your Insurance?

Every claim you make—and even if you ask an insurance agent about making a claim—gets entered into a database that your current and future insurance carriers can access. If you have had any recent accidents or traffic violations, you may be more expensive to insure than someone with a clean driving record. If you’ve made any recent claims, your insurance premiums will likely go up. And if you shop around for a new company, they’ll have access to your records and will take your driving record into consideration.

Can You Check Your Insurance Reports?

Your insurance companies share information with two databases: the Comprehensive Loss Underwriting Exchange (CLUE) and the Automated Property Loss Underwriting System (A-PLUS). These databases are run by outside agencies—LexisNexis runs CLUE and Verisk Analytics runs A-PLUS—and any claims you make stay in your report for five to seven years, depending on the database.

The Fair Credit Reporting Act entitles you to one free copy of your report every 12 months. You can dispute inaccurate or incomplete information on your report. You are also entitled to notice about any negative decisions based on information in your report. Requesting your reports does not affect your credit score.

Request your CLUE report from LexisNexis online or call 866-312-8076.

Request your A-PLUS report from Verisk by calling 800-627-3487.

Does Credit Score Impact Your Car Insurance Cost?

In most states, your credit score can impact the cost of your car insurance. The only states that don’t allow car insurance companies to use credit score as a factor in pricing are California, Massachusetts and Hawaii. Statistical studies from the Federal Trade Commission and other research organizations show a correlation between credit score and how much a person is likely to cost a car insurance company. In short, someone with a poor credit score is seen as a greater risk, so the insurance company may charge more for the insurance to help cover expenses related to future claims.

Does Where You Live Impact Your Premium Amount?

Where you live can impact your car insurance cost. In 2018, for example, the average car insurance premium in Michigan was 64% higher than the national average. Other states with car insurance premium averages on the high end included Louisiana, Florida, Rhode Island and Connecticut. States with the least expensive average car insurance premiums included Vermont, Ohio, Virginia, Idaho and Iowa.

Does Age Impact Your Premium?

When it comes to what car insurance companies don’t want you to know, this one isn’t super secret. Age does impact your premiums, with the youngest and oldest drivers typically paying the most on average.

The youngest drivers pay the most for insurance. Premiums are highest at the age of 18 and decline steadily until the driver turns 25. In the eyes of carriers, drivers then enter adulthood, during which time premiums stay pretty flat for the next 30 years or so, until the age 55. Premiums inch up slowly between ages 55 and 65 before jumping way up around the age of 75.

In addition to your age, your gender, marital status, education level and even your job can affect your insurance rates.

If You Bought Your Car Via a Loan, Is Your Insurance Cost Higher?

If you don’t own your vehicle outright, then you may pay more to insure it. If you own a vehicle outright, you’re only required to carry liability on it. Liability is the part of your insurance policy that kicks in to cover damage caused to other people’s cars or property in an accident you’re at fault in.

When you have a loan, the bank is concerned about protecting its investment. That means it may require you to carry comp and collision as well. This is the part of an auto policy that covers damage to your car in an accident you’re at fault in. A policy with this added coverage is more expensive than one without it.

How Can You Lower Your Car Insurance Costs?

No matter your age, gender, or location, you can potentially lower your car insurance via a variety of methods. Here are some tips your car insurance company doesn’t want you to know to put into action to save on premiums.

Drive carefully. Not only does driving carefully help you avoid rate-raising accidents, but many companies also provide good driver bonuses when you haven’t had an accident or filed any claims for a certain amount of time.

Pay your bills on time. Paying your bills on time goes a long way toward improving your credit score, which can improve your rate depending on where you live. Paying your bills on time also demonstrates trustworthiness to your insurance company, which means you may be able to negotiate for a lower rate.

Ask for discounts. When it comes to your insurance rates, it doesn’t pay to be shy. Ask your insurance company about discounts, including multi-driver or multi-car discounts, good student discounts or safe driver discounts. You may be able to score a large portion off your premium because you’re a good student or you follow all the traffic laws.

Review your credit report. Know what’s on your credit report and what you can do to drive up your score. Once you’ve improved your score, ask for a new quote for car insurance.

>> Need to review your credit report? Sign up for the free Credit Report Card.

Consider a higher deductible. Look carefully at your coverage and consider whether you can tweak anything in your policy. If you can afford to cover $2,000 in damages if you get in an accident, consider changing your deductible from $500 to $2,000 to save on your monthly premium.

Shop around for a better rate with other insurance companies. The insurance market is highly competitive, and you may find a better rate with an online company or through a broker that works with multiple companies. If you find a better rate, go back to your current company to see if they’ll match or beat the offer.

Choose your next vehicle carefully. Because the type of car you drive affects your insurance rates, do your research before your next purchase. Look for a car with plenty of safety features (but without too many other bells and whistles) that will get you a lower rate.

What Happens When Car Insurance Denies a Claim?

Of course, you don’t just pay for car insurance for the fun of it. If you get into an accident, you expect the insurance to step in and help cover the expenses. If your insurance company denies your claim, you have some options for appealing the claim.

Contact the insurer. After you’ve reviewed your claim denial, reach out to the insurance company directly. You may be able to explain your claim better or gather additional information to help you understand the reason for the denial.

File an official appeal. Most insurance companies will have an appeals process clearly set out online. You’ll want to write a clear, direct letter that explains why the evidence you originally gathered and submitted with your claim contradicts the insurance company’s decision to deny the claim.

Talk to a legal professional. If you feel that your insurance company is denying your claim in bad faith, talk to a legal professional about your options.

Bringing Down the Total Cost of Car Ownership

Car ownership is expensive. Make sure you pay attention to all the potential expenses to get the best possible deal overall—and don’t forget to shop around for the best rates before locking yourself in.

Identity thieves are almost always opportunistic—but the crimes they commit feel very personal. Unauthorized credit card charges, bogus loan applications, missing money, and other financial violations make fraud a major nightmare. To keep fraud in check, you need to know how to check your credit report for identity theft, and how to deal with problems when they arise.

In this post, we’ll talk about the warning signs of identity theft—and then we’ll show you how to stamp out fraud before it starts.

Warning Signs of Identity Theft

How Do I Check My Credit for Identity Theft?

To avoid falling victim to identity theft, examine your credit report regularly. You can access a free copy of your credit report from all three bureaus—Equifax, Experian, and TransUnion—once a year. (Through April 2022, you can get free weekly copies of your reports.) You can also use a tool like Credit.com’s Credit Report Card or ExtraCredit to monitor your credit.

When you download your credit report with ExtraCredit, you’ll see a list of positive accounts, late accounts, collections, public records, inquiries and account balances. Your credit report contains a lot of information about you and about your financial habits, and if that information changes unexpectedly, it can indicate identity theft. Here are five of the biggest fraud warning signs to watch out for.

Warning Sign 1: Incorrect Personal Information

Sometimes, incorrect personal information is the result of an innocent mistake. Other times, it means something sinister is going on. If you see your name misspelled, a wrong phone number or address, or an incorrect Social Security number on your credit report, investigate immediately.

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

Warning Sign 2: Lender Inquiries You Don’t Recognize

Credit bureaus keep the details of companies who ask for information about you on record for at least two years. Promotional inquiries and account review inquiries are nothing to worry about, because they’re preapproved credit offer inquiries or inquiries by companies you already do business with.

Hard enquiries from companies you don’t recognize are a different matter. Sometimes, fraudsters make a lot of credit card and personal loan applications in a short period of time, so if you see a recent list of unknown inquiries, someone might be trying to steal your identity.

Tip:Sometimes, the name of a financial institution doesn’t precisely match the name of the company checking your credit. Car dealerships, for example, sometimes run a series of credit checks via different finance companies—so it’s worth double checking before filing a fraud complaint.

Warning Sign 3: Accounts You Never Opened

Only your own accounts—including accounts that you’ve cosigned and for which you’re an authorized user—should appear on your credit report. If you find an unknown account on your credit report, one of two things has happened:

Your credit information has been commingled with someone else’s information by mistake

Your credit has been compromised by a fraudster

If you find an unknown account on your credit report, contact the relevant lender right away and tell them what’s going on.

Warning Sign 4: You Credit Utilization Goes Up

If you suddenly owe more than before and you haven’t changed your spending habits, someone else might be splurging on your behalf. Check your credit card statement very carefully and flag any suspicious transactions straight away. Most credit card companies have a maximum 120-day limit for chargebacks, so it’s important to review purchases regularly.

Warning Sign 5: Your Score Goes Up or Down Unexpectedly

Credit scores change over time. When negative information falls off your credit report after a certain period of time, your score increases. On the other hand, if you apply for too many loans or credit cards in a short space of time, your credit score could take a hit. If your credit score changes dramatically—especially if it’s for the worse—dig deeper.

Warning Sign 6: Public Records You Don’t Recognize

Negative public records can substantially impact your creditworthiness. Bankruptcies, for instance, often remain on record for up to a decade. If you see public records you don’t recognize, alert the issuing agency without delay.

Tip:Liens and civil court judgments used to appear on credit reports, but credit bureaus no longer collect information about those types of public records. Bankruptcies are now the only public records included on credit reports.

Can Someone Steal Your Identity with Your Credit Report?

Your credit report contains a lot of personal information, so it’s a goldmine for identity thieves. With a copy of your report in hand, a potential fraudster might be able to see:

Full name

Birth date

Social Security number

Current and past home addresses

Phone number

Accounts held in your name

Payment records

Public records, including bankruptcies

Many other valuable personal and financial details

Credit report content sometimes varies according to the credit bureau.

If thieves need more information after accessing your credit report, they often choose to misrepresent themselves to get it. Phishing and smishing scams are when criminals pretend to be legitimate financial institutions—or government agencies like the IRS—to get personal information from victims via email or text.

What Is the Safest Way to Check My Credit Report?

You can check your credit report quickly and easily with Credit.com’s ExtraCredit monitoring service. ExtraCredit includes five helpful tools, which help you monitor, build, earn, protect, and restore your credit profile. Two tools in particular can help you avoid or combat identity fraud: Track It and Guard It.

Track It

With ExtraCredit’s Track It tool, you get access to all three credit bureau reports. You can also monitor 28 FICO® scores—the real scores lenders see when they consider auto loan, credit card, and mortgage applications. Track It also includes a helpful credit monitoring tool, which gets updated every month. If something suspicious happens, you’ll notice right away.

Guard It

Many hackers sell consumer information on the dark web. Nefarious individuals use software, specific net configurations, or special authorizations to access the dark web. Thankfully, ExtraCredit’s Guard It tool actively monitors the dark web for consumer information and sends out security alerts when data breaches happen. You also get a $1 million ID insurance policy when you sign up with ExtraCredit.

Get Identity Theft Protection

Identity theft is a big problem in the United States. There were 650,572 cases of identity theft in America in 2019—and over 270,000 of those cases involved credit card fraud. If you see an unknown address or notice an unknown credit card on your credit report, flag it up right away. Tools like ExtraCredit from Credit.com make it easier to monitor your report on a monthly basis, so you can rest more easily.

In July 2016, the Consumer Federation of America (CFA) and VantageScore Solutions reported that most consumers—more than 80%—knew basic facts about their credit scores, including that credit scores are used by lenders to approve or deny mortgages and by credit card issuers to approve or deny credit cards.

While it’s good that most people know the importance of credit scores, the same survey found that many consumers don’t understand credit score details. In other words, about how personal credit works and how credit scores work still confuses people.

How Are Credit Scores Created?

When you borrow money, whether through a revolving account, like credit cards, or an installment account, like an auto loan or student loan, the information is gathered by the credit bureaus. The data the bureaus keep in your credit files is the date used to calculate your credit scores.

When you apply for a loan or card, the bank or issuer may look at just your credit score or at your entire credit file. There are five major areas of information in your credit file that are used to calculate your score:

Payment history

Debt usage, also known as your credit utilization ratio

Age of credit accounts

Types of accounts or account mix

The number of hard inquiries on your credit, not soft inquiries

A good credit score includes a healthy mix of all these factors. Each factor though weighs differently toward a score. Payment history makes up 35% of your score. Debt usage 30%, credit age 15%, and account mix and credit inquiries each make up about 10% of your score.

How Are Credit Scores Used?

You have multiple scores and types of scores and there are different scoring models. The resulting scores and your credit file are used to determine your risk factor for future loans. The three-digit score is a numerical representation that indicates how risky a borrower you are from a lender’s perspective.

Score ranges break down as follows:

Excellent credit: 750+

Good credit: 700-749

Fair credit: 650-699

Poor credit: 600-649

Bad credit: below 600

A higher credit score—roughly 700 or above—can result in your getting approved for better terms and conditions. For example, your credit reports and/or scores impact the deals and interest rate you get when you buy a home, finance a car, rent an apartment, apply for a job, buy insurance, purchase a cell phone or open a new credit card.

The best way to improve your credit score or maintain it is to be responsible with the credit cards and loans you have. Remember those five factors mentioned a minute ago? This is where they come into play—things like making loan and credit card payments on time each month and maintaining a good debt usage or a credit utilization rate—the amount of debt, including credit card debt, you have in relation to your overall credit limit—can help you reach the credit score you’re after.

Using credit irresponsibly by making late payments and maxing out credit limits can have an affect your credit negatively and lower your credit score.

How Does Credit Reporting Work?

The credit reporting system includes three main players:

Consumers

Credit bureaus

Financial companies, such as banks, lenders and credit card issuers

Information about your credit cards, loan accounts and credit inquiries is reported electronically to the three main national credit bureaus—TransUnion, Equifax and Experian—by lenders and creditors roughly every 30 days. The bureaus collect and store your credit information in your credit file for future reference. Meaning, your behaviors can be reviewed in the future by others to determine your risk level.

Businesses, such as auto loan lenders, banks, credit unions, credit card companies and insurance agencies—even employers—use your credit data from the credit bureaus to determine your risk level. Once they have an idea of how risky it is to lend you money, they determine the rates you have to pay or other terms and conditions. Or, they may determine not to loan you money or give you a credit card at all. They may also use this information to send you pre-approved offers in the mail.

The three national credit reporting agencies don’t share information with each other and not all lenders or creditors report to each. As such, your credit reports from TransUnion, Equifax and Experian can contain different information about you. So, it’s important to monitor all three reports because you can never be sure which one will be used when you apply for a new account. You also want to make sure you review them for any errors that are damaging your scores. Learn more about how to dispute an error on your credit reports.

Are Creditors Required to Report to Credit Bureaus?

Not all creditors report your account information to the credit bureaus. And they’re not required to. While businesses are legally required to report accurate information, there’s no law that says they have to report at all. While nearly every major creditor reports to all three bureaus, smaller lenders and banks may not send your monthly account information to all three or any of the credit bureaus.

What’s On Credit Reports?

Along with your credit card and loan account records, basic information about you, like your name, address and recent applications, is recorded in your credit files. Public records such as bankruptcies, tax liens and judgments can also appear on your reports.

Information about your income, race, gender, age, religion or health details isn’t included on credit reports.

Most information expires from your credit reports after 7 to 10 years, but when information expires can vary depending on the circumstance. It’s important to keep the information on your credit reports positive and accurate. And if there’s something inaccurate on your credit reports, you can file a dispute with one or more of the credit reporting bureaus to try and have it removed from your file.

Find Out Where You Stand

Finding out how credit works is important. And now that you’ve done that, you likely want to know where you stand. You can get your free Experian credit score and a free credit report card on Credit.com.

Your report card includes including a grade for each area that makes up your scores. You see how your payment history, debt and other factors affect your scores, and get recommendations for ways to improve each area if needed.

Your report card is updated every two weeks, so you can check your credit regularly and ensure nothing unexpected pops up. An unexpected change in your score can indicate an issue, such as potential identity theft.

The FOMC also said it would continue to reduce its holdings of Treasury securities and agency debt and agency mortgage-backed securities.

During a press conference with reporters on Wednesday, Fed Chair Jerome Powell said that the committee decided to leave their policy interest rate unchanged. However, looking ahead, he did not exclude the possibility of another hike.

In spite of a higher-than-expected CPI reading in August, core inflation readings have been falling every month in 2023. Meanwhile, the pace at which new jobs were added to the economy slowed. Other labor market indicators, such as job openings and the unemployment rate, also point to a cooling economy, Danielle Hale, chief economist at Realtor.com noted.

Today’s decision not to raise rates will likely influence credit markets.

“In the mortgage market, for instance, consumers who have been holding off may begin to be motivated by the announcement to consider making the home purchase they have been waiting on,” Michele Raneri, vice president and head of U.S. research and consulting at TransUnion,said.

In fact, mortgage applications picked up in the week leading up to the Fed meeting, signaling a wave of optimism.

The CME FedWatch Tool showed a 99% chance the Fed would halt its hikes to the 5.25 to 5.5% range on Wednesday morning, according to interest rate traders. However, only 70.9% of these investors bet officials will freeze the rate hike at the November 1st meeting.

On Monday, mortgage rates for 30-year fixed-rate mortgages were at 7.21%, according to HousingWire‘s Mortgage Rates Center. However, at Mortgage News Daily, mortgage rates were higher on Tuesday, at 7.30%.

The effects of tighter policy have already reverberated across the economy. While mortgage rates have steadied just below recent highs, they remain more than 3 percentage points above their pandemic-era lows. In the housing sector, the combined impact of higher rates and higher home prices drove the cost of financing a home up more than $400, or 22.5%, from a year ago.

Overall, the market has been rather optimistic about the rate picture this year. However, a number of experts are concerned that lifting rates too high could send the economy into recession.

Inflation picked up to 3.7% in August, down significantly from where it was a year ago but still higher than the 2% threshold. Core inflation—which excludes food and energy costs—rose 4.3% in August. Raising interest rates is designed to tackle those still-high prices outside of the volatile food and energy sectors.

If shelter was excluded from the CPI calculation, inflation would be about 1% in August, said Bright MLS Chief Economist Lisa Sturtevant last week. In August, the rent index was up 7.2%, rising for the 40th consecutive month. Meanwhile, rent growth slowed considerably and median rents nationally fell year-over-year in August, according to Sturtevant. Additionally, apartment construction is strong, which puts an additional pressure on landlords to avoid vacancy. In the second quarter of 2023, the national vacancy rate was 6.3%, up from 5.6% a year earlier. However, it takes months for those aggregate rent trends to show up in the CPI measures.

What’s next?

Although the Fed decided to hold steady this time, it remains fixated on taming inflation and bringing it back to the 2% target. In light of this goal, Realtor.com’s Hale expects the Fed to keep the option for an additional future rate hike on the table.

During the press conference, Powell remained extremely cautious, insisting on the Fed’s data dependent approach. He reiterated that the decisions that will be made at the two remaining meetings in 2023 will depend on the totality of all the data gathered, including the inflation data, the labor market data, the growth data, the balance of risks, etc. As is custom now, he sidestepped questions from reporters about what would prompt the FOMC to raise rates again before the end of 2023 or hold them steady.

Powell also shared the committee’s economic projections, showing a longer period of elevated rates.

“FOMC participants expect the rebalancing in the labor market to continue, easing upward pressure on inflation,” Powell said. “The median unemployment rate projection in the summary economic projections rises from 3.8% at the end of this year to 4.1% over the next two years.”

Meanwhile, the median projection for total PCE inflation is 3.3% this year, 2.5% next year and to reach 2% in 2026, he added.

Even though inflation remains well above the Fed’s longrunning goal of 2%, he acknowledged that inflation has moderated since the middle of last year.

On the housing market, he noted that activity “picked up somewhat” although it remains well below the levels of a year ago, largely reflecting higher mortgage rates.

Indeed, Sturtevant highlighted the resilience of the housing market in the face of rising interest rates. “Over the past year, buyer interest has remained high, home prices continued to rise in most markets, and homebuilding activity has surged,” she said.

However, she underlined that, even with today’s pause, the aggressive rate hikes have had major and somewhat deferred impacts on the housing market.

As demand might decline in the fall, Sturtevant expects home prices to fall in some markets. However, price declines will remain modest as supply will remain low, she added.

“The biggest downfall of the market cooling is that many individuals and families–particularly first-time homebuyers–have been priced out of the market as a result of the Fed’s aggressive rate increase,” she said.

This afternoon’s projections give valuable insight into the amount of improvement in inflation that the Fed would want to see before pausing or ending the current tightening.

“The Federal Reserve is rightly on pause and is looking for more data before determining its next course on interest rates,” NAR Chief Economist Lawrence Yun said. “With fewer job openings, slowing job gains, and softening core consumer price inflation, the Fed must consider the potential economic damage arising from any future rate hikes.”

Both personal loans and credit cards provide access to extra funds and can be used to consolidate debt. However, these two lending products work in very different ways.

A credit card credit is a type of revolving credit. You have access to a line of credit and your balance fluctuates with your spending. A personal loan, by contrast, provides a lump sum of money you pay back in regular installments over time. Generally, personal loans work better for large purchases, while credit cards are better for day-to-day spending, especially if you are able to pay off the balance in full each month.

Here’s a closer look at how credit cards and personal loans compare, their advantages and disadvantages, and when to choose one over the other.

Personal Loans, Defined

Personal loans are loans available through banks, credit unions, and online lenders that can be used for virtually any purpose. Some of the most common uses include debt consolidation, home improvements, and large purchases.

Lenders generally offer loans from $1,000 to $50,000, with repayment terms of two to seven years. You receive the loan proceeds in one lump sum and then repay the loan, plus interest, in regular monthly payments over the loan’s term.

Personal loans are typically unsecured, meaning you don’t have to provide collateral (an asset of value) to guarantee the loan. Instead, lenders look at factors like credit score, debt-to-income ratio, and cash flow when assessing a borrower’s application.

Unsecured personal loans typically come with fixed interest rates, which means your payments will be the same over the life of the loan. Some lenders offer variable rate personal loans, which means the rate, and your payments, can fluctuate depending on market conditions.

Personal loans generally work best when they are used to reach a specific, longer term financial goal. For example, you might use a personal loan to finance a home improvement project that increases the value of your home. Or, you might consider a debt consolidation loan to help you pay down high-interest credit card debt at a lower interest rate.

Key Differences: Credit Card vs Personal Loan

Both credit cards and personal loans offer a borrower access to funds that they promise to pay back later, and are both typically unsecured. However, there are some key differences that may have major financial ramifications for borrowers down the line.

Unlike a personal loan, a credit card is a form of revolving debt. Instead of getting a lump sum of money that you pay back over time, you get access to a credit line that you tap as needed. You can borrow what you need (up to your credit limit), and only pay interest on what you actually borrow.

Interest rates for personal loans are typically fixed for the life of the loan, whereas credit cards generally have variable interest rates. Credit cards also generally charge higher interest rates than personal loans, making it an expensive form of debt. However, you won’t owe any interest if you pay the balance in full each month.

Credit cards are also unique in that they can offer rewards and, in some cases, may come with a 0% introductory offer on purchases and/or balance transfers (though there is often a fee for a balance transfer).

Line of Credit vs Loan

A line of credit, such as a personal line of credit or home equity line of credit (HELOC), is a type of revolving credit. Similar to a credit card, you can draw from a line of credit and repay the funds during what’s referred to as the draw period. When the draw period ends, you’re no longer allowed to make withdrawals and would need to reapply to keep the line of credit open.

Loans, such as personal loans and home equity loans, have what’s called a non-revolving credit limit. This means the borrower has access to the funds only once, and then they make principal and interest payments until the debt is paid off.

Consolidating Debt? Personal Loan vs Credit Card

Using a new loan or credit credit card to pay off existing debt is known as debt consolidation, and it can potentially save you money in interest.

Two popular ways to consolidate debt are taking out an unsecured personal loan (often referred to as a debt or credit card consolidation loan) or opening a 0% interest balance transfer credit card. These two approaches have some similarities as well as key differences that can impact your financial wellness over time.

Using a Credit Card to Consolidate Debt

Credit card refinancing generally works by opening a new credit card with a high enough limit to cover whatever balance you already have. Some credit cards offer a 0% interest rate on a temporary, promotional basis — sometimes for 18 months or longer.

If you are able to transfer your credit card balance to a 0% balance transfer card and pay it off before the promotional period ends, it can be a great opportunity to save money on interest. However, if you don’t pay off the balance in that time frame, you’ll be charged the card’s regular interest rate, which could be as high (or possibly higher) than what you were paying before.

Another potential hitch is that credit cards with promotional 0% rate typically charge balance transfer fees, which can range from 3% to 5% of the amount being transferred. Before pulling the trigger on a transfer, consider whether the amount you’ll save on interest will be enough to make up for any transfer fee.

Using a Personal Loan to Consolidate Debt

Debt consolidation is a common reason why people take out personal loans. Credit card consolidation loans offer a fixed interest rate and provide a lump sum of money, which you would use to pay off your existing debt.

If you have solid credit, a personal loan for debt consolidation may come with a lower annual percentage rate (APR) than what you have on your current credit cards. For example, the average personal loan interest rate is 11.31% percent, while the average credit card interest rate is now 24.37%. That difference should allow you to pay the balance down faster and pay less interest in total.

Rolling multiple debts into one loan can also simplify your finances. Instead of keeping track of several payment due dates and minimum amounts due, you end up with one loan and one payment each month. This can make it less likely that you’ll miss a payment and have to pay a late fee or penalty.

Both 0% balance transfer cards and debt consolidation loans have benefits and drawbacks, though credit cards can be riskier than personal loans over the long term — even when they have a 0% promotional interest rate.

Is a Credit Card Ever a Good Option?

Credit cards can work well for smaller, day-to-day expenses that you can pay off, ideally, in full when you get your bill. Credit card companies only charge you interest if you carry a balance from month to month. Thus, if you pay your balance in full each month, you’re essentially getting an interest-free, short-term loan. If you have a rewards credit card, you can also rack up cash back or rewards points at the same time, for a win-win.

If you can qualify for a 0% balance transfer card, credit cards can also be a good way to consolidate high interest credit card debt, provided you don’t have to pay a high balance transfer fee and you can pay the card off before the higher interest rate kicks in.

With credit cards, however, discipline is key. It’s all too easy to charge more than you can pay off. If you do, credit cards can be an expensive way to borrow money. Generally, any rewards you can earn won’t make up for the interest you’ll owe. If all you pay is the minimum balance each month, you could be paying off that same balance for years — and that’s assuming you don’t put any more charges on the card.

Cash in on up to $300–and 3% cash back for 365 days.¹

Apply and get approved for the SoFi Credit Card. Then open a bank account with qualifying direct deposits. Some things are just better together.

When is a Personal Loan a Good Option?

Personal loans can be a good option for covering a large, one-off expense, such as a car repair, home improvement project, large purchase, or wedding. They can also be useful for consolidating high-interest debt into a single loan with a lower interest rate.

Personal loans usually offer a lower interest rate than credit cards. In addition, they offer steady, predictable payments until you pay the debt off. This predictability makes it easier to budget for your payments. Plus, you know exactly when you’ll be out of debt.

Because personal loans are usually not secured by collateral, however, the lender is taking a greater risk and will most likely charge a higher interest rate compared to a secured loan. Just how high your rate will be can depend on a number of factors, including your credit score and debt-to-income ratio.

The Takeaway

When comparing personal loans vs. credit cards, keep in mind that personal loans usually have lower interest rates (unless you have poor credit) than credit cards, making it a better choice if you need a few years to pay off the debt. Credit cards, on the other hand, can be a better option for day-to-day purchases that you can pay off relatively quickly.

Think twice before turning to high-interest credit cards. Consider a SoFi personal loan instead. SoFi offers competitive fixed rates and same-day funding. Checking your rate takes just a minute.

SoFi’s Personal Loan was named NerdWallet’s 2023 winner for Best Online Personal Loan overall.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

This article originally appeared on The Avocado Toast Budget.

This post is sponsored by Credit.com.

Here at the ATB, we are all about budgeting in a way that works for you and finding realistic ways to feel more confident with your money.

Now that 2020 is (finally) over, here are ways that you can start to take hold of your finances and build confidence with your money in 2021.

Write down your short, medium and long term financial goals

I’m a big believer that you don’t need to stress over how to maximize the value of every dollar you come across.

Much of personal finance is behavioral and relies on us finding value in how we navigate our money!

Because of this, I found it incredibly helpful to sit down and brainstorm short, medium and long-term financial goals to decide what I wanted my money to do for me.

Write down your short, medium and long term financial goals

Here’s how I break it up:

Short-term goals – less than two years

Medium-term goals – 2 – 10 years

Long-term goals – 10+ years

Feel free to dream big!

We want to make realistic and attainable goals, but we also want to allow ourselves to dream about what we really want our lives to look like, and how our money plays a role in that.

Get to know your credit score

Wanna know a secret? I avoided my credit score for the longest time.

Turns out, once I finally faced my credit score, I became more empowered to understand how my credit score affects my finances and what I could do to change it.

While free resources can give you a ballpark estimate of your credit score, that score isn’t very useful and certainly isn’t what creditors see!

Knowing your true score, and seeing your credit reports from all three major credit bureaus, gives you security and control over how to navigate your credit score going forward.

While it can be daunting, credit plays an important role in our lives from renting, to car insurance, to mortgages, to career opportunities and more.

That’s why it’s important that you stay informed of what your credit actually looks like that’s why I signed up for ExtraCredit’s free trial!

Set up automatic savings

Automating your savings is LIFE CHANGING.

Setting up automatic savings is often referred to as “paying yourself first” because you are prioritizing saving money for Future You.

There are tons of different savings goals that you can put this money toward, but the important part right now is to set up automatic savings so you can set it and forget it.

Trust me—you miss that money a lot less if you never see it in your account in the first place.

If you have automatic deposits at work, it’s super easy to add a savings account and have a certain % or dollar amount go into that account every month without it EVER hitting your checking.

In my opinion, this is the best way to go. Out of sight, out of mind.

You’re way less likely to touch this money, and you’ll be shocked at how much it grows over time!

If this isn’t an option for you, you’re not out of luck. You can set up automatic savings transfers into your savings account from your checking account through your bank.

Find a budget that works for you

Here at the ATB, we are all about budgeting in a way that makes sense for you and your life.

Budgeting doesn’t have to be stressful and restrictive. It should actually be freeing and allow you to feel more confident and in control of your money!

There’s no one right way to budget, and there are TONS of different types of budgets depending on your income and financial goals.

Personally, I use a zero-based budget which allows me to track and decide where every single dollar I have is going.

If you have big savings goals, low income or high debt, I definitely recommend checking out a zero-based budget.

Learn how to increase your credit score

Your credit score has a bigger impact on your life than just determining your eligibility for loans.

Credit can impact your ability to rent, job opportunities, car insurance rates and more.

Once you know what your credit score is, it’s important to understand what makes up your credit score, and what steps you can take to increase it.

There are five factors that influence your credit score:

Payment History

Amounts Owed

Length of Credit History

New Credit

Credit Mix

Payment History makes up 35% of your credit score, so it is the most important factor.

ExtraCredit gives you the ability to report rent and utility payments, adding new tradelines to your credit profile. Adding payment history to your credit file.

And if you need help working to repair your credit, you can also use the Restore It feature to get an exclusive discount from a leading credit repair company. Remember: your best credit score is an accurate one.

Understanding how to increase your credit can take a lot of stress out of your finances and help you feel more in control of your credit future.

Make a debt payoff plan

I paid off $20k in CC debt in less than a year, and in order to do that, I needed a concrete plan of how I was going to tackle my debt.

Prior to that point, I had just been throwing a little bit here and there, hoping that my balance would eventually decrease.

Shockingly, that never happened.

Once I decided to use the debt avalanche to tackle my credit card debt, I was able to calculate how much extra money I could throw at my debt every month in order to make progress toward my debt free goal.

With this method, I paid the minimum payments on all of my debt except for the one with the highest interest.

With the highest interest debt, I put any extra money I had toward paying that down.

This gave my money more of a purpose than just throwing extra money here and there at my different debts.

It was also reassuring and motivating to see the loan amount decrease drastically as I threw the extra money I had towards it.

Are you thinking about selling your engagement ring? People sell their engagement rings for all sorts of reasons, such as no longer being in a relationship or inheriting a ring. Whatever your reason may be, you can most likely sell your engagement ring and make extra money. You can use this extra money towards paying…

Are you thinking about selling your engagement ring?

People sell their engagement rings for all sorts of reasons, such as no longer being in a relationship or inheriting a ring.

Whatever your reason may be, you can most likely sell your engagement ring and make extra money.

You can use this extra money towards paying off debt (like credit card debt or student loans), starting an emergency fund for unexpected expenses (like medical bills, vet visits, or house repairs), putting the money into your retirement savings, or even saving for financial goals (like a home deposit, buying a car, or going back to school).

Today, you’ll learn how to:

Get your engagement ring appraised

Negotiate for the highest price

Find the best place to sell your engagement ring

And, of course, the step-by-step process of how to sell an engagement ring!

How To Sell An Engagement Ring

How much is an engagement ring worth?

Before you sell your engagement ring, you should try and figure out how much it is worth.

One of the things to think about when valuing a diamond engagement ring is the “4 Cs of a Diamond.” If you want to know where to sell diamond rings, first you must figure this out.

The 4 Cs stand for:

Carat – This is the size of the diamond. Larger diamonds are usually worth more money.

Cut – This is not the diamond shape. Instead, this is the quality of the diamond’s cut which will impact how beautiful and brilliant the diamond is.

Color – A diamond’s value increases with less color, as a completely colorless diamond is worth more.

Clarity – Clarity is all about the imperfections and blemishes that a diamond may have. The fewer there are, the more valuable the diamond.

Other things that may increase or decrease the value of your used engagement ring include:

Condition – The overall condition of the ring is important. A ring that has been taken care of and shows minimal signs of use will typically hold onto more of its value in comparison to a ring that displays noticeable wear and tear.

Resale market – Rings with a popular style or from a well-known designer may see a higher price when resold.

Certification and documentation – Having a document such as a diamond grading certificate can help determine the quality of the ring.

Designer and brand name – Rings from certain designers or brands (such as Cartier or Tiffany & Co.) tend to have a higher resale value due to their reputation and craftsmanship.

Even though a pre-owned engagement ring may have a lower value compared to a new one, it can be a great value for buyers looking for a high-quality ring at a more budget-friendly price. And, that is why people buy them – they can save some money over a new ring.

Recommended reading: 8 Items To Sell Around Your Home For Extra Money

Gather documentation for your engagement ring

If you’ve decided to sell your engagement ring, it’s time to collect all of your paperwork related to the ring such as the diamond’s certification, receipts, and appraisals.

These documents will help figure out the ring’s value, establish its authenticity, and make the process of selling a little more smooth.

Here’s a list of the paperwork you might need:

Appraisal certificate – The appraisal certificate is a professional evaluation of the engagement ring. This document includes details about the diamond’s cut, color, clarity, carat weight, and quality.

Original receipt – Having the original receipt from the purchase of the engagement ring will help show that the ring is authentic.

Diamond certification – If the diamond was graded and certified by a recognized gemological laboratory, this can be helpful.

Gemstone certificates – If your engagement ring has other gemstones besides diamonds, include these certificates for the stones as well.

You don’t need any paperwork to sell an engagement ring, but, it can make things a little easier and may get you a little more money.

How to get an engagement ring appraised

Getting an engagement ring appraised by a certified gemologist or jewelry appraiser will give you an accurate estimate and valuation of how much your engagement or wedding ring is worth.

This can help you when negotiating (such as with a pawnshop) and simply knowing the amount that you should be looking for when selling your ring.

You can get your engagement ring appraised by:

Looking for appraisers – You can search online for certified gemologists or jewelry appraisers in your area. You can also ask local jewelry stores for their recommended appraisers. It’s important to find an appraiser with credentials from places such as the Gemological Institute of America (GIA), the American Gem Society (AGS), or the International Society of Appraisers (ISA).

Contacting the appraiser – Call the appraiser and ask for their fees and to schedule an appointment. You may need to bring documents such as receipts, certificates, or previous appraisals for the ring.

Getting the ring appraised – Take the engagement ring to the appraiser. They will examine the engagement ring’s characteristics including the diamond’s cut, color, clarity, and other important factors.

Receiving the appraisal report – Once the appraisal is done, the appraiser will provide you with the report. This report includes information about the ring’s characteristics as well as an estimated value based on the current market. Ask the appraiser any questions you might have or if you need a question answered.

Where to sell an engagement ring

Now is the time to look at your different options for selling the ring. You can sell engagement rings at jewelry stores, pawn shops, online marketplaces, auction houses, consignment shops, and more.

Some things that you will want to about when deciding where to sell your engagement ring include the amount that they are giving you (of course, you want the most money, right?), the fees that they may be charging to sell your ring, how much work it will take you to sell it (for example, do you have to create the listing or do they?), whether you feel safe meeting someone to exchange the ring for cash in-person, and more.

As you can see, there are going to be pros and cons for each of the places where you can sell your jewelry.

Below, I go further into each of the best places to sell an engagement ring:

1. Sell your engagement ring online in a marketplace

If you want to sell your engagement ring, one of the best ways to get the most money for it is to sell it online.

Selling your engagement ring online can be convenient and also help you reach a wider audience of possible buyers.

Some of the different places you can sell an engagement ring online include eBay, Facebook Marketplace, and Craigslist.

Here’s a step-by-step guide to help you sell your engagement ring online:

Make your ring presentable – You should clean your ring and take quality photos of it from different angles.

Choose the marketplace – There are many different sites to sell your engagement ring like eBay, Craigslist, Facebook Marketplace, specialized jewelry-selling websites, or online auction sites.

Create a detailed listing – In the listing, write a detailed description of the ring along with its condition and any unique features. Be honest about any imperfections. When listing your ring for sale, you should also describe the ring, such as the diamond’s cut, color, clarity, and carat weight.

Set a price – You should research similar engagement rings or get your ring appraised to find the most accurate price based on current market value.

Shipping – If you’re shipping the ring, make sure to package it securely to prevent any damage in transit and also pay for shipping insurance.

2. Sell your engagement ring on Worthy

Similar to the above, some websites are dedicated to selling jewelry and valuables, such as Worthy.

Worthy does not buy your engagement ring directly as that is not their business model, but they will clean it up and sell it for you.

Worthy makes it really easy to make money with your engagement ring and this is the best place to sell engagement rings online. You simply ship your jewelry to their office with a prepaid shipping label (a FedEx label) that they give you (it’s insured as well). Then, once they get the ring, they prep it for auction. They will clean the ring, take professional photos of it, and grade it.

After that, your ring will go up for auction, and professional jewelry buyers can bid on it. You can set a reserve price that you are comfortable with. Once the auction is done, you will receive the final sale amount after Worthy’s fee. Payment is then sent to you within 1-5 days.

The whole process typically takes around 2 weeks from shipping to getting paid.

So, what are Worthy’s fees? They do almost all of the work for you, so it makes sense that they would charge a fee. They take 18% for up to $5,000. After that, it is a 14% fee for $5,001 to $15,000, a 12% fee for $15,001 to $30,000, and a 10% fee for over $30,000.

So, for example, I found a 1-carat diamond ring on Worthy that eventually sold for $2,792. That means the seller received around $2,289 after the 18% fee that Worthy charges.

3. Work with a jeweler

Jewelers may offer to buy your engagement ring. You can simply call around local jewelry stores near you and ask if they buy used engagement rings.

Sometimes this can be the most straightforward and convenient option for selling your engagement ring as you can possibly sell your ring the same day.

To sell your engagement ring to a jeweler, you will want to look for jewelry stores near you and give them a phone call to see if they buy used engagement rings. I recommend looking for ones with positive reviews.

If you have any documentation for your ring then make sure to bring it with you so that you can show the jeweler.

If they are interested in your engagement ring, then they will give you an offer. If you’re happy with the offer, then you can ask any other questions and possibly sign paperwork to get your cash.

Jewelers may offer instant payment either via cash, check, or electronic transfer and you will want to confirm the payment method before completing the sale.

4. Sell your engagement ring to a consignment shop

You may decide you want to sell your used engagement ring to a consignment shop. Consignment shops have benefits such as offering exposure to multiple buyers. However, they likely charge a commission fee.

To sell your engagement ring through a consignment shop, you will want to Google search for consignment shops in your area and specifically look for shops that sell jewelry or high-end items (make sure the shop has good reviews and even testimonials of previous successful sales of engagement rings).

Once you have an idea of which consignment shops you’re interested in selling your ring at, you should ask them questions about their consignment process, what commission rate they charge, and the terms of the sale.

Then, you’ll give the shop the ring to display in their store.

The consignment shop handles the transaction if someone is ready to buy the ring. You’ll receive payment after the commission fees are taken out.

5. Sell your wedding ring to a pawnshop

When people think about where to sell an engagement ring, one of the first places they think about is probably a pawn shop.

And, it makes sense – pawn shops make it very easy and you can sell your engagement ring for cash here. You can most likely even get paid on the same day!

But, you should keep in mind that they usually give you the lowest amount of money.

If you want to sell your old wedding ring to a pawn shop you will first want to make sure the ring looks nice and clean because that can help you get a better price. Get any papers you have about the ring, like appraisals or certificates, to show how much it’s worth, and make sure you know this number before you go in because you will most likely have to negotiate.

Now, when selling at a pawn shop, you can typically negotiate. To do so, you will want to find out the ring’s value, current market trends, and comparable sales. You can even make a better case for your price by showing documents on the ring and appraisals from certified gemologists. If the pawn shop cannot meet that price, you may just want to move on and try to find another buyer.

When the pawn shop makes an offer, remember they need to make a profit too, so it might be lower than you expect. If you’re not happy with the offer, you can try selling it to someone else. If you agree to sell it, you’ll need to show some ID, sign some papers, and then you’ll get paid.

Frequently Asked Questions

Below are answers to common questions about how to sell an engagement ring.

Is it possible to sell an engagement ring?

Yes! Many places buy engagement rings and wedding rings so that you can make money.

How much can you get for selling your engagement ring?

The amount of money that you can get for selling your engagement ring will vary and usually, you can earn anywhere from around 20% to 60% of what was originally paid for it. Yes, this is a wide range (and can mean a difference of hundreds or even thousands of dollars) and this is because there are so many factors that come into the price, such as the condition of the ring, the market demand, and where you decide to sell it.

How much can I sell my 1 carat engagement ring for?