Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

The cash envelope system is a budgeting tool that helps you develop self-discipline by only spending the allotted amount of cash from labeled envelopes each month. It can help reduce overspending and impulsive purchases.

Budgeting is one of the best ways to keep track of your spending, pay down debt, and build wealth. Unfortunately, many Americans don’t take advantage of preparing a monthly budget. Our team at Credit.com surveyed over 1,000 Americans, and 27 percent said they don’t think a budget is necessary.

We also found that 15 percent of people don’t want to feel restricted by a budget, and 24 percent simply don’t think they will stick to it. Fortunately, with the cash envelope system, it’s easy to do both.

Today, you will learn about this simple budgeting method that can help you save money, lower your debt, and potentially help raise your credit score.

Key takeaways:

You can use cash envelopes as a monthly budget by putting cash in different envelopes for spending categories.

The system is ideal for people who have a habit of impulsive spending or overspending.

It allows you to monitor your money rather than guessing how much you’re spending.

The cash envelope system is often called “cash stuffing” on social media apps like TikTok.

What Is the Cash Envelope System?

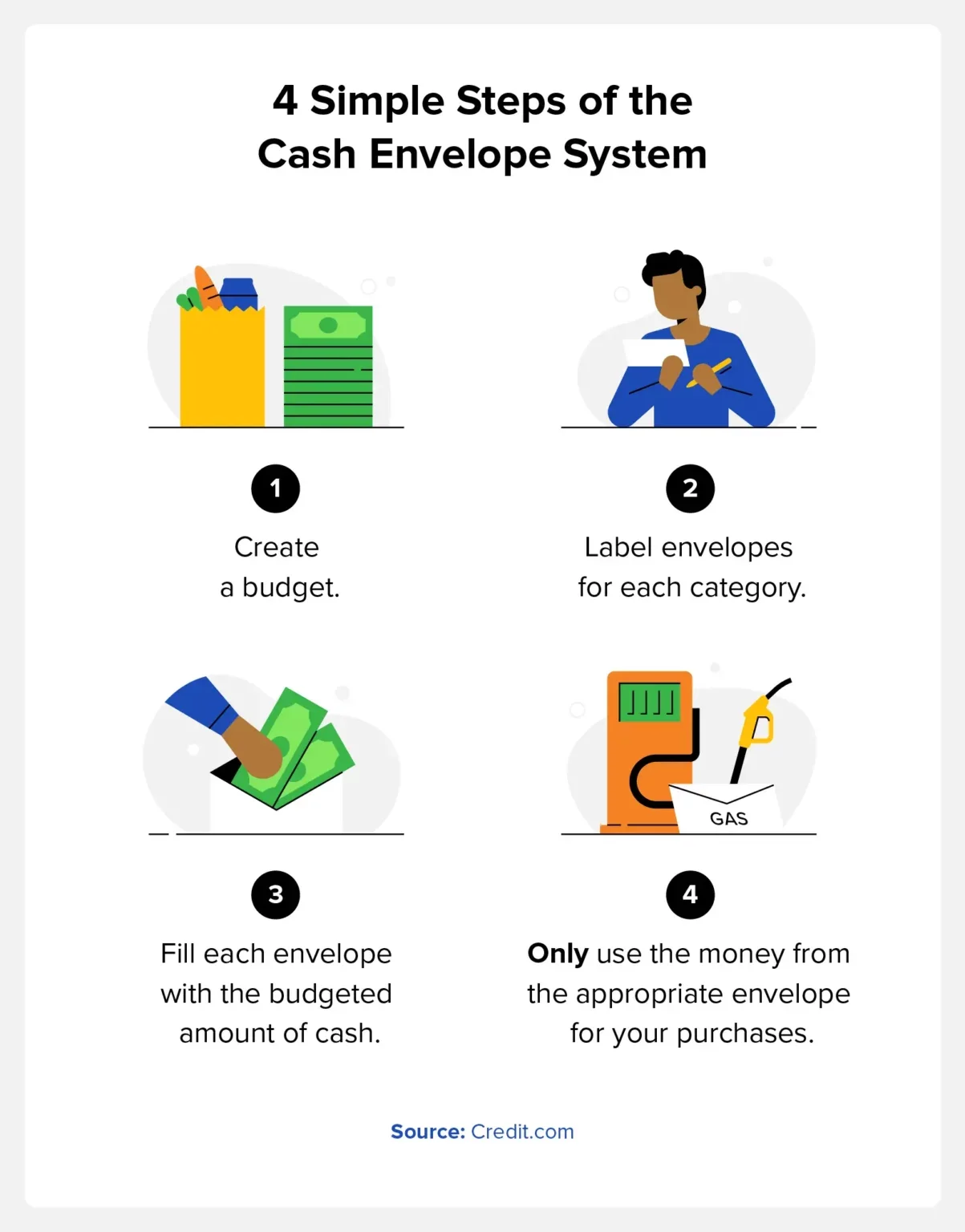

The cash envelope system, also known as “cash stuffing,” is an easy-to-use budgeting tool that helps track how much money you have to spend. You’ll put the cash in labeled envelopes and check each envelope throughout the budgeting period to see how much money you have left to spend.

Different budgeting systems work for different people. For some, having a monthly budget template on their computer is the best option. Others may benefit more from being able to physically see how much money they have left for purchases like groceries, gas, and entertainment.

How the Cash Envelope System Works

Before cash stuffing, you will need to organize your money envelopes into different categories. If it helps, you can start with a spreadsheet budget template, or you can write down the categories in a notebook. Some of the top budget categories to consider include:

Utilities

Fuel or transportation costs

Groceries

Healthcare and medications

Savings

Debt

It’s also beneficial to ensure you have cash envelopes for areas where you typically overspend. This may be eating out, buying clothes, or online shopping. You can allocate money toward these areas, but the goal is to ensure you don’t overspend.

During the month, whenever you spend money in one of these categories, you only use the money from the appropriate envelope. For example, if you enjoy buying a $5 cup of coffee on your way to work and allocate $100 to that envelope, take $5 out of it each morning.

The cash envelope system is a way to hold yourself accountable for your spending. This means that once the money is gone from an envelope, it’s gone. If you miscalculated how much you need in a certain category, revisit your budget the following month and tweak the amounts.

You can refill your envelopes at the start of each budgeting period or after each paycheck.

The Benefits of the Cash Envelope System

There are pros and cons that come along with every budgeting strategy, so it’s helpful to know the benefits and drawbacks and find the one that’s right for you. The cash-stuffing envelope system is great for people who don’t check their bank account daily or are better with their money when using cash.

Additional benefits include:

Avoiding overdraft fees

Minimizing overspending

Increasing accountability

Helping with disciplined spending

By sticking to cash, the system also helps reduce the frequency with which you use your credit card, minimizing interest fees.

The Downsides of the Cash Envelope System

The cash envelope system isn’t for everyone, and it may create some additional challenges. The primary downside of this budgeting system is that you need to go to your bank or an ATM whenever you need to refill your envelopes. It’s also beneficial to consider that carrying large amounts of cash has the risk of losing it for the money being stolen.

Some of the other downsides include:

It’s time-consuming.

You get no credit card rewards.

You can only spend the amount contained within each envelope.

The other challenge with the cash envelope system is making online payments or automatic payments. Automatic payments are a great way to avoid forgetting about a payment and accruing late fees. You can still use the cash envelope system, but you will need to keep track by writing on the back of the envelope, similar to balancing a checkbook.

Should You Use the Cash Envelope System?

This budgeting system is ideal for people who are quick to pull out their debit or credit card and have trouble with overspending. It can be difficult to track your money electronically, but using physical cash can help many people stick with a budget.

The system is also a great way to budget for beginners. It’s a simple system, and you can start with just a few categories. If you know you have a problem with overspending on ordering food or going out, use this system to allocate a specific amount of cash for these activities.

FAQ

Although the cash stuffing system is a simple method, there are some common questions people have when getting started.

Can the Cash Envelope System Work If You Make Online Payments?

The most common method is to create a physical envelope while keeping the money in your bank account for online payments. You can keep track by writing on the back of the envelope each month.

What If an Envelope Runs Out of Cash?

If you run out of cash from the envelope, stay disciplined and avoid borrowing money from other envelopes. Revisit your budget and find ways to save in different categories, earn extra money, or reduce your spending.

How Do You Use the System When Emergency Expenses Happen?

Emergencies happen, and in these cases, you can shift money around from your envelopes and budget accordingly the following month. It’s also helpful to build an emergency fund for these situations, and you can also keep a credit card for emergency funds.

What Do You Do If There’s Money Left Over in Your Cash Envelope?

Money left over in cash envelopes means you’re doing a great job with your budget. You can use this to treat yourself or add to your personal spending money envelope the next month. You may also want to use this extra money to make extra debt payments or put it in your savings account.

How the Cash Envelope Budget System Can Help Improve Your Credit

Creating a budget is a great way to get your finances under control and create quality spending habits. The cash envelope system is also helpful for reducing your debt and improving your credit. One of the key factors of your credit score is credit utilization, so allocating an envelope toward paying down your debt and using leftover money for additional payments can help increase your score.

For additional credit resources, you can sign up for Credit.com’s free credit report card or our ExtraCredit service.

As part of its broader affordable housing initiatives, Wells Fargo will sponsor a homeownership program alongside the Asian Real Estate Association of America.

The Wells Fargo-AREAA alliance will focus specifically on sustainable homeownership for first-time homebuyers and low to moderate-income Asian American, Native Hawaiian and Pacific Islander (AANHPI) communities.

AREAA found in its annual report that 72% of White Americans own homes. Yet, there are several Asian subcategories where homeownership is 55% or less, including Native Hawaiian, Indonesian, Korean, Pakistani, Hmong, Sri Lankan, Burmese, Bangladeshi, and Nepalese.

Additionally, the initiative will also feature a housing affordability symposium as well as regional events across the U.S. for homebuyers.

“We are committed to being a part of the solution and breaking down the systemic barriers that make homeownership more difficult to attain,” said Valeria Esparza-Chavez, head of Home Lending, Asian Segment at Wells Fargo.

The partnership comes after the bank was hit by several scandals related to its lending practices.

The bank repeatedly misapplied loan payments, wrongfully foreclosed on homes, illegally repossessed vehicles and charged surprise overdraft fees, affecting 16 million customers’ accounts, according to the CFPB. Wells Fargo eventually agreed to pay $1.7 billion to settle multiple consent orders last December.

Additionally, Bloomberg reported in March 2022 that only 47% of Black homeowners who completed a refinance application with Wells Fargo in 2020 were approved, compared with 72% of white homeowners. (The bank denied any wrongdoing.)

Since then, Wells Fargo announced plans to invest an additional $100 million to advance racial equity through its $210 million special purpose credit program.

Earlier in April, the bank announced a 10-year partnership with Dallas megachurch affiliate T.D. Jakes Group to build “inclusive communities.”

Looking for an app that does it all – automate savings, track spending, investing, and get a free $250 cash advance?

Welcome to my Albert App Review.

Looking for an all-in-one personal finance app that will help you manage your money, save for your future, or even get a free cash advance when you need it?

In that case, you’ve come to the right spot!

In this Albert App Review, I’ll go over everything you need to know about the popular Albert app, and I will discuss its features, benefits, how the app can help you, and more.

You can sign up for the Albert app here.

The Albert app is becoming more and more popular as a money tool that can simplify your life. Instead of needing a bunch of different financial apps, Albert can help you consolidate your phone and need less. The app is a one-stop shop for your monthly financial needs – it automates savings, helps you manage your budget, and has spending, borrowing, and investing tools. With this easy app and the wide range of tools that you can use, Albert has many benefits.

This app reduces the need for multiple apps since it offers a wide range of tools and features.

If you’re looking for a money saving app, Albert can be a great option to start with. There’s a reason why it’s one of the top money apps in the App Store!

9

Albert is one of the most popular personal finance apps, and it is designed to make it easier to save and invest all in one place. This app has features for saving, investing, and budgeting.

Quick Summary – Albert App Review

Albert app is a financial management tool that helps you to save, spend, and invest right in the app

The Genius feature allows you to ask any money question and get a real response from a real person

Albert app’s cash advance feature can get you up to $250

The app is free, but some features do require a monthly subscription

Albert App Review

What Is The Albert App?

The Albert app is a personal finance app that will help you manage your money better by making it easier to save and invest all in one place. This app has features for saving, investing, budgeting, and more.

It has many different features, such as budgeting tools, real-time alerts, and a helpful service where you can ask an expert money questions and get real answers catered to your situation. The app strives to make financial management easier and more organized for everyone.

Albert makes it easy to manage your finances, eliminating the need for visits to physical bank branches or formal phone calls with a financial expert. With the ease of using an app, you can easily track your financial well-being, helping you stay organized, reach goals, and find smart ways to save, spend, and invest. Albert stands out by simplifying your personal finances, all while keeping things very easy to use.

Albert also has a feature where you can get a small cash advance of up to $250 with no late fees, interest, or credit check. This advance is repaid from your next paycheck, giving you the option to avoid high-interest personal loan lenders for those in need of quick cash.

There are no hidden fees, and it is free to sign up. They do have a paid subscription plan that you can sign up for which will give you access to different features such as financial advice from experts. I talk about the paid part further below.

Does The Albert App Give You Money?

Albert provides instant cash advances to users who need small amounts of money before their payday. They do not charge late fees, interest, or run a credit check for this feature.

This can be a great way to not pay high rates on payday loans for when you just need a little bit of cash.

How it works is that the Albert app will send you up to $250 from your next paycheck straight to your bank account. Then, you simply repay them when you get paid. You can pay a small fee to get your money instantly, or you can wait 2-3 days and get the cash advance for free.

Albert Instant is available to all members of the Albert app who qualify, whether they are a paid subscriber or not. Now, not everyone will qualify. To determine your eligibility for a cash advance, they look at things such as if your income is direct deposited into your connected bank account, if your bank account has been open for at least 2 months and has a balance greater than $0, and if you’ve received consistent income in the past 2 months from the same employer.

Albert App Features

The Albert App has many other features, such as:

Banking with Albert

Albert has a user-friendly banking service through its partnership with FDIC-insured Sutton Bank. This includes features like no minimum balance requirement and access to your paycheck up to two days early.

With an Albert account, you can also earn cash back rewards, such as getting a cash back bonus on gas, groceries, and more when you purchase items with your Albert debit card. You can earn an average of $2.00 per gas tank fill-up. You do need to be a Genius subscriber to take advantage of this benefit.

The app also has fee-free ATMs for their paid subscribers at over 55,000 ATMs (when using the Albert Mastercard debit card).

Albert Savings

Albert Savings is the app’s automatic savings tool that is available to Genius subscribers. It saves money from your linked bank account to your Albert Savings account.

This automated savings tool helps you build up your funds without the stress of manual transfers. It analyzes your income and expenses to calculate the amount you can save comfortably. Or, you can manually set your own savings schedule.

The Albert saving feature can help you to save more money and reach your goals.

The money in your Albert Savings account is yours, and you can withdraw it at any time.

Albert Budgeting

The Albert Budgeting feature is super handy and packed with a bunch of useful tools to help you manage your money with ease.

The Albert app has budgeting tools to help you track your income and expenses, find fees that you shouldn’t be paying, and watch your financial progress. The app will send real-time alerts and notifications to help you stay on track with your budget. But, that’s not all.

Other features of Albert Budgeting include:

The Albert app can negotiate your bills so that you can save money. The app will help you lower your bills such as for cable TV, internet, cell phone, and more.

The Albert app also makes it easy to see all of your budgeting info in one quick place, such as tracking your recent bills, seeing how much you’re spending in different categories, and more.

The app will categorize your spending so that you can see where your money is going (this can help you to realize where you may need to cut back)

Also, the app will help you find hidden charges and subscriptions that you may not be using.

These are all very helpful features that can help you save a lot of money in the long run.

Albert Investing

If you’re new to investing or you’re looking for an easier way to invest, the Albert Investing side of the app can make getting started much, much easier.

With Albert Investing, you can start an investment portfolio that matches the amount of investment risk you want to take on and your financial goals. The app even provides investment guidance and lets you start investing without any minimum investment amount needed.

So, that means that you can start investing with Albert Investing with just $1.

You can get started investing in the app by answering some questions (the app wants to learn more about you so that it can make selections based on your personal situation). The app will then choose individual stocks or funds for you to invest in (or, you can choose these yourself if you know what you want to invest in). You can even ask the app to only invest in themes as well, such as companies that are interested in sustainability and the environment. You can then continue to invest automatically or on a recurring schedule. The auto-investing feature can be a great tool if you are looking to save time and invest regularly without really thinking about it.

Albert Genius

This is one of my favorite parts in the app.

The Albert Genius service gives you financial advice from a team of expert financial advisors (this is a team of real human experts that you are able to talk to – not a robot), available through a paid monthly subscription in the app.

You can ask their experts any money question that you have, whether it’s a big or small question, a general question, or something more specific to your personal situation. Your questions can be about anything from credit cards, budgeting, student loans, investing, credit card rewards, life insurance, your personal financial life, and more. These experts will help you answer your questions 7 days a week too. And, there’s no limit to the amount of questions you can ask.

This is a very nice feature to have access to.

Some of the questions you can ask include:

How do I start a budget?

How do I lower my car insurance? Am I paying too much?

How much can I personally afford to spend on a house?

How can I improve my credit score?

How much money should I have in my emergency fund?

Should I use extra cash to pay off debt or invest?

Can you help me to better under travel miles and credit cards?

There are so many different questions that you can ask the team at Albert!

Albert Protect

Albert Protect is a feature for paid subscribers on the app.

The Albert Protect feature monitors your money around the clock. The app will alert you if something suspicious comes up for any of your connected financial accounts or your identity. The app continuously watches for suspicious activity on your credit report, the dark web, data breaches, and unusual charges.

How Does The Albert App Work?

Signing up for Albert is easy!

Simply click here to get started.

Or, you can head to the Google Play or App Store, depending on your device (Android or iOS), and download the app. Once installed, the app will walk you through the setup process. There’s no need to worry about a credit check as Albert doesn’t require one for signing up.

Next, you’ll be asked some questions about yourself such as your name and age. The app is trying to learn more about you. Here’s what Albert says specifically about the questions that they ask: “We do this in order to best serve your needs: a 19-year-old single student has different financial objectives and priorities than a 37-year-old professional with two kids who will be starting college soon.”

Then, you’ll be asked to connect your financial accounts to the app. So, you may connect your bank account that your bills come out of, your credit card accounts, student loans, mortgage, investments accounts, and more. You can connect as many or as little as you want. This information helps the app better serve you so that it can give you recommendations, track your spending, give you alerts, and more.

After you sign up, you’ll have access to the many features mentioned above to help you manage your finances. As you learned above, there are a lot of tools in this app, so I recommend just playing around in the app at first to better familiarize yourself with it and see how it can help you. Maybe sit down for a few minutes at a time until you understand how to use the app in the best way for your financial situation. That’s exactly what I did when I first downloaded the app because it was a little intimidating at first trying to see all of the different things that the app can do. But, it’s so nice that everything can be done right from one app!

To sign up for the app, they do require that you be a U.S. citizen or resident, be at least 18 years old, and have a bank account with a U.S. financial institution. Unfortunately, at this time, the app is not available to those outside the U.S.

How Much Does Albert App Cost?

The Albert app has a lot of different features, so you may be wondering what the cost is or if there are any monthly fees.

The great thing is that many of the tools and features on the Albert app are free.

For example, the Albert App has a fee-free cash advance feature to help you cover unexpected expenses. If you need some extra cash until your next paycheck, you can get up to $250 as a cash advance, with no cost. There are no late fees, overdraft fees, or maintenance fees associated with this service.

You can also start investing with as little as $1 and use the free cash advances feature (as long as you meet eligibility requirements) without the need for a subscription.

Now, the Genius subscription does have a cost.

If you’re looking to unlock all of Albert’s helpful budgeting, saving, and investing tools, you might want to consider their Genius subscription. This subscription starts at just $14.99 per month and gives you access to some helpful benefits like cash bonuses and personalized financial advice. Keep in mind that the true value of the Genius subscription depends on how often you use the app and all its features. So, if you’re a frequent user of the app, it could be a great investment in your financial well-being.

Is Albert App Safe to Use?

Yes, Albert is safe to use.

Let’s start with the basics – the Albert app isn’t a bank, but it teams up with FDIC-insured Sutton Bank to offer you banking services. That means that the money in your Albert Cash account is safe because it’s protected by the Federal Deposit Insurance Corporation (also known as FDIC). That’s a fancy way of saying your funds are insured for up to $250,000.

Your Albert Savings accounts are held at FDIC-insured banks, including Coastal Community Bank, Axos Bank, and Wells Fargo.

When it comes to data security and privacy, Albert takes that seriously too. The app has security measures to protect your sensitive personal and financial information.

As for customer service, if you ever face any issues with the Albert app, you can easily reach out to their support team for assistance. Many Albert app reviews have mentioned their responsive customer service.

Pros and Cons of Albert

Like with any personal finance app, there are pros and cons. I can’t write an Albert app Review and not talk about the pros and cons, so that you can make the best decision for yourself.

Some of the benefits of using Albert include:

The app aggregates all of your accounts – Albert gives you an overview of your financial life by combining all your accounts in one place.

Savings and investments – The app offers customizable savings goals and can create a custom portfolio for your investment needs. It will also keep track of your transactions and help you identify potential savings opportunities as well as avoid late fees.

The Albert app is safe – Your information is kept safe with the same level of security used by major banks, as well as FDIC insurance.

Albert Genius – This feature provides personalized money advice from financial experts (real people, not a robot!) to help you make smarter financial decisions. You can ask any money question and will get personalized advice.

Free cash advance – Get a cash advance on your next paycheck without any late fees using Albert Instant, or access your paycheck up to two days early with direct deposit.

Free ATM withdrawals – This is a feature paid monthly members get to have.

While Albert has many helpful tools and features, there are some potential downsides to using the app such as:

App-only functionality – All features of Albert are limited to the app, which may be inconvenient for some people who prefer to be on their computer instead of their cell phone.

Fees – While many features in Albert are free to use, some, such as the Albert Genius service, require a subscription fee. The fee is quite affordable for the services you receive, though.

No phone calls – If you need to talk to customer support, there is no phone number to call. Instead, it’s all done through the app, text message, or email.

Frequently Asked Questions

Here are answers to commonly asked questions about the Albert app.

Is Albert a trustworthy app?

Yes, Albert is a trustworthy app. Your banking money is FDIC-insured, with coverage up to $250,000, and your investments are SIPC-insured. The app has many financial tools and you can even get personalized advice from experts.

How much can you borrow with Albert?

The maximum for a cash advance is $250.

How do you get $250 from Albert app?

Albert offers a cash advance feature called Albert Instant. After you enable this feature and meet the requirements, you can access funds quickly, sometimes up to $250.

Does Albert give you money right away?

In some cases, Albert can provide instant cash advances or help you get your paycheck up to two days early via direct deposit, depending on your employer and banking situation.

How long does it take to get money from Albert?

Getting your hands on the cash you need from Albert is all about the service you’re using. If you’re in a hurry, instant cash advances could have those funds in your pocket right away. But for paycheck advances and other features, it might take a couple of days before you see the money.

What are the requirements to get a cash advance on Albert?

Requirements for a cash advance with Albert include a history of consistent income, using the Albert app for a certain period, and having a bank account linked.

Does Albert hurt your credit?

Albert does not directly impact your credit score as it is not a lender. However, using the app’s guidance to improve financial management can help you work towards building or maintaining a higher credit score.

Does Albert need your social security number?

Yes, when signing up for the Albert app, it will ask you for your SSN. This is because it is an investment app and they need to verify that it is actually you signing up.

Is Albert or Chime better?

Albert and Chime are different financial apps with different features. Albert focuses on money management, investing, and advice, while Chime is a mobile banking app offering checking and savings account services. Your choice should depend on your financial goals and preferences.

Why is Albert taking money from my account?

If you’re already an Albert user, this may be a troubleshooting question that you have (and perhaps you searched Google and found this blog post). Albert takes money from your account (such as your bank checking account) to fund the services you’ve opted into, such as investments or automatic savings. You can check the app’s settings or contact Albert to learn more,

Is Albert app affiliated with a specific local bank?

Albert is backed by Sutton Bank.

Is the Albert app reliable and secure for banking?

Yes, Albert is a reliable and secure app for managing your finances. It is FDIC and SIPC-insured and has a variety of financial tools and resources to help you improve your financial situation.

How is Albert app customer service?

I did some research and I found great Albert app reviews on their customer service. The Albert app has customer service options within the app and online. They do not have an option to call their customer service and speak on the phone. But, if you’re like me, you probably prefer to get your questions answered via text message or email anyways.

Is Albert app legit?

Yes, the Albert app is a legitimate personal finance app that can help you manage and improve your finances. Millions of people (last I checked, over 10,000,000 people use this app) use the app’s many helpful tools. The app is available for people on Apple or Android devices and it has great reviews.

Who is Albert app best for? Who should not use it?

The Albert app is a helpful all-around financial app that can help many different people. If you’re looking for an all-in-one app to help you save, spend, borrow, and invest, Albert might be a good fit for you. The app is helpful for people who:

Want fee-free cash advances up to $250 (this is a feature that many people like because they don’t have to sign up for high-interest rate loans when they just need something for a short amount of time)

Need an app that gives you an overview of all your accounts in one place

Are interested in automatic savings and easy investing tools

Albert takes the work out of managing your finances and may be helpful for people who are trying to stay on top of their personal budget without having to juggle multiple apps.

However, Albert may not be the best fit for everyone and not everyone needs to have it. So, if you fall into any of the below, then this may not be the app for you

If you’re an experienced investor looking for more advanced trading tools, then this may not be the best investing app for you (the Albert app is basic in this area because I think it caters more to those who are new investors or are looking for something easier to manage)

If you’re someone who doesn’t feel comfortable linking their bank accounts to a third-party app (you will need to link accounts in order to get full use of the app – I understand that some people may not want to do this)

Albert App Review – Summary

I hope you enjoyed my Albert App Review.

I think this is a very helpful app, and I can see why it’s one of the most popular money apps today.

Albert is an app designed to help manage your saving, budgeting, investing, and more, all in one easy app. The app has all of the different money tools that you would want, plus some extras that you may have not realized you needed yet.

Albert is an app that helps you to manage many different parts of your financial life right from your cell phone (it’s not available on computers).

They even have the Genius feature (one of my favorite parts of the app), which is an in-app chat where you can ask one of their experts anything related to money, from credit cards, buying a car, student loans, and more. This is very helpful if you ever have questions about money.

And, if you need cash now, Albert may be able to give you a small advance of up to $250. There are no late fees, interest, or a credit check. If you want to avoid personal loan lenders who have high-interest rates, and only need a small cash advance, then Albert may be a place to start with. How this works is that they send you $250 from your next paycheck. You simply repay them when you receive your next paycheck.

You should keep in mind that investment options don’t include retirement plans and customer service can only be reached via email and text. Though the app’s budgeting tools are more basic compared to budgeting-focused apps, the Albert app still has many, many benefits to help you manage your finances effectively and it’s all from one easy-to-use app.

You can learn more about Albert here.

What’s your favorite personal finance app? Do you use the Albert app?

If you’re like most people, credit card interest and taxes are two things you don’t want to pay. Luckily, paying one may help you pay less for the other. Credit card interest and fees are tax-deductible in some cases. That means every dollar you pay in credit card interest might reduce a dollar of your taxable income.

If that sounds too good to be true, there is a catch — credit card interest and fees are typically only considered tax-deductible if they are legitimate business expenses. If you don’t run a business, or the interest and fees were not incurred in the operation of a business, you generally won’t be able to deduct them on your tax return.

How Credit Card Interest Works

When you make a purchase with a credit card, you don’t have to pay for it right away. Instead, you are borrowing the money for the duration of your statement (usually one month). At the end of your statement balance, you must make at least a minimum payment. But if you don’t pay the full statement amount, you will be charged credit card interest on any outstanding balance. Charging this interest is one way that issuers fund credit card perks and benefits like credit card rewards.

💡 Quick Tip: When choosing a credit card, look for one that aligns with your existing spending habits. For example, some cards offer rewards on airline purchases for frequent travelers, while others, like the SoFi Credit Card, offer cash-back rewards on all purchases.

Unlimited 2% cash back rewards*

Earn 3% cash back on up to $12,000 in purchases your first year when you set up direct deposit through SoFi.** After that, earn 2% unlimited cash back on everything.*

Is Credit Card Interest Tax Deductible?

Whether or not credit card purchase interest charges are tax-deductible depends mostly on whether it is personal or business credit card interest.

Business Credit Card Interest

Business credit card interest may be tax-deductible in certain situations. Generally speaking, in order to deduct any expenses, they must be incurred in the regular operation of the business. The IRS does not have requirements about what type of credit card is used, as long as the interest is incurred on business expenses.

You may be able to deduct credit card interest on a personal credit card used for business purchases. However, most credit card agreements prohibit the use of personal credit cards for business purposes on a regular basis.

Not surprisingly, you cannot typically deduct credit card interest on personal expenses charged to a business credit card. And if you pay for personal and business expenses with the same credit card, you may not be able to deduct the full amount of interest. Consult with your accountant or tax advisor if you have questions about what can and cannot be deducted.

Personal Credit Card Interest

Personal credit card interest is not tax-deductible under any circumstances. You cannot deduct interest that you pay for personal expenses on a credit card. That’s one more reason to always pay your credit card statement in full, each and every month. That way you aren’t charged any credit card interest.

Recommended: How to Do Taxes as a Freelancer

Are Credit Card Fees Tax Deductible?

Just like credit card interest, the deductibility of credit card fees largely depends on whether they are for business expenses.

Business Credit Card Fees

Credit card fees that are incurred as business expenses are generally considered deductible. This includes credit card annual fees, overdraft fees, foreign transaction fees, late fees, and balance transfer fees. As long as the credit card is used for business purposes, any fees charged by the credit card issuer will be tax-deductible.

💡 Quick Tip: When using your credit card, make sure you’re spending within your means. Ideally, you won’t charge more to your card in any given month than you can afford to pay off that month.

Personal Credit Card Fees

In contrast, personal credit card fees are not generally considered deductible. Any fees that you are charged by your credit card issuer that are not business expenses cannot be deducted from your taxable income.

Recommended: Can You Use a Personal Checking Account for Business?

Avoiding Interest and Fees vs Tax Deductions

While it’s important to understand that you may be able to deduct credit card interest and fees if they are business expenses, avoiding credit card interest may be the more prudent thing to do. If you are in a 30% tax bracket, that means deducting one dollar of interest will save you 30 cents. But if you pay your balance in full, you won’t be charged any interest and save the full dollar.

The Takeaway

Some credit card fees and interest is deductible on your annual tax return. Generally speaking, you cannot deduct personal credit card interest or fees. You may be able to deduct them if they are legitimate business expenses. Keeping your business and personal expenses separate can help you determine which fees and interest you may be able to deduct.

Looking for a new credit card? Consider a rewards card that can make your money work for you. With the SoFi Credit Card, you earn cash-back rewards on all eligible purchases. You can then use those rewards for travel or to invest, save, or pay down eligible SoFi debt.

The SoFi Credit Card offers unlimited 2% cash back on all eligible purchases. There are no spending categories or reward caps to worry about.1 Take advantage of this offer by applying for a SoFi credit card today.

FAQ

Can you deduct credit card interest as business expense?

As credit card interest rates rise, the amount of interest that you’re charged each month on any unpaid balances also rises. So you may be wondering if you can deduct credit card interest from your taxable income. The good news is that as long as the interest is a legitimate business expense, you can generally deduct the interest.

Are credit card fees tax deductible?

It’s important to understand how different credit card-related items affect your taxes. Credit card rewards are generally not considered taxable, while some credit card fees may be tax-deductible. You may be able to deduct most credit card fees as long as they are considered legitimate business expenses. Personal credit card fees are not generally considered deductible.

Can you write off personal credit card annual fees?

No, in nearly all cases, you cannot take a tax deduction for personal credit card fees. Only credit card fees that are legitimate business expenses are tax-deductible. However, it’s important to understand that the IRS does not make any distinction between what might be marketed as a “personal” card or a “business” credit card.

Photo credit: iStock/Cameron Prins

The SoFi Credit Card is issued by The Bank of Missouri (TBOM) (“Issuer”) pursuant to license by Mastercard® International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi cardholders earn 2% unlimited cash back rewards when redeemed to save, invest, or pay down eligible SoFi debt. Cardholders earn 1% cash back rewards when redeemed for a statement credit.1 1Members earn 2 rewards points for every dollar spent on eligible purchases. If you elect to redeem points for cash deposited into your SoFi Checking or Savings account, SoFi Money® account, or fractional shares in your SoFi Active Invest account, or as a payment to your SoFi Personal, Private Student, or Student Loan Refinance, your points will redeem at a rate of 1 cent per every point. If you elect to redeem points as a statement credit to your SoFi Credit Card account, your points will redeem at a rate of 0.5 cents per every point. For more details please visit SoFi.com/card/rewards. Brokerage and Active investing products offered through SoFi Securities LLC, member FINRA/SIPC. SoFi Securities LLC is an affiliate of SoFi Bank, N.A.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Online bill pay can be a major convenience: It can allow you to schedule payments to transfer money from your bank account to your creditors. Using this technology can also be a money-saving move. It can lower the odds of your forgetting to pay a bill or winding up with late payment charges.

To be honest, paying bills likely isn’t anyone’s favorite way to spend free time. Automating the process may let you focus your energies elsewhere without needing to worry about how much money is due when and where.

If you’re curious to know the answer to, “How does bill pay work?” and understand how it could simplify your life, read on.

What Is Online Bill Pay?

Bill pay is a way of paying your bills online and automating your finances. It allows you to use your mobile device, laptop, or tablet to send money from your account to that of another person or business. No check writing required.

You specify the funds and provide details on the recipient, and the amount is automatically taken from your account and sent to the payee.

Yes, you can do this in real time, but you can also determine the “when.” That means you can schedule bills for payment in advance whenever you have time free, which can be a huge life hack.

Using Bill Pay to Organize Your Bills

When you set up bill pay, it can be a good opportunity to review your finances and the money you have coming in and going out.

You might also decide to stagger the payment dates on your bills to enhance your cash flow. To help with this, you may be able to change due dates on your bills by contacting your creditor.

Here are some of the ways you might use bill pay:

• Mortgage or rent

• Utilities

• Car loan payments

• Credit card bill

• Gym memberships

• Streaming channel and other subscriptions

• Student loans

• Charity donations

💡 Quick Tip: Make money easy. Open a bank account online so you can manage bills, deposits, transfers — all from one convenient app.

Setting Up Online Bill Pay

While bill pay can help make managing finances simpler, it does require some initial manual set-up. But, once you’ve learned how bill pay works, this automatic feature can make keeping track of and paying bills less cumbersome. Here are some ways to get started:

1. Finding a Financial Partner that Offers Bill Pay

While many financial institutions offer digital payment tools, like bill pay, it’s worth investigating the features that are included at each, before opening up an account. Online billing is free with some accounts, while some providers may charge for each transaction — either per bill or on a repeating monthly basis.

Recommended: When All Your Money Goes to Bills

2. Determining which Bills to Autopay

Utility bills, loan payments, credit card bills — you can pay just about any bill using bill pay. One benefit of centralizing bill payments is that, whether it’s a one-off charge payment or recurring bill, the user can rest assured that the bill will get paid on time — assuming bill pay has been set up correctly and there are sufficient funds in the linked account.

To streamline bill payments even further, it may be helpful to think about which ongoing bills you want to automate on a revolving basis through bill pay. Every month, bill payment could go out automatically, on a schedule determined by you, to the businesses or service providers where the money is due.

Predictable expenses that don’t fluctuate from month to month, such as loan and mortgage payments or the internet bill, are solid candidates for recurring automated payments. After all, it can be easier to budget for an expense that won’t go up and down from month to month. For bills that always cost the same, you may want to schedule payment for a time each month when you know there’ll be sufficient funds in your account to cover what’s come due. Some service providers may even allow you to change the due date on certain bills.

3. Gathering Together All Bills

Once a person has figured out which bills to pay automatically, they still might want to gather together all their regular bills in one place. (Organizing your bills can really help you see exactly where your money goes.) While individual bills are generally due at the same time each month, bills from different businesses or providers will have different due dates.

With all the bills in one place, you can then enter the various billing accounts into your money management provider’s bill pay system. It could be useful to research each bill ahead of time, determining whether they’re delivered by snail mail, paperless emails, or both.

4. Logging on to Personal Finances

As with other personal finances, bill pay is generally managed through a financial institution’s website or mobile app. A person interested in accessing bill pay could simply sign on to their secure account and search for the “Pay a Bill” or “Online Bill Pay” function.

5. Inputting Billing Information

Once logged on, you might follow the prompts to add individual billing accounts, indicating for each the funds you wish to pay with. You’ll likely be asked to input the name of the business or service whose payments you’re seeking to automate. You may also be asked for more specific details, such as your individual account number.

If you can’t find the business or service provider listed, you want to try spelling out the full name, removing abbreviations. If you still can’t find the payee, it’s possible that you can still utilize bill pay, but you may need to manually add in the payment details.

Having printed or saved digital copies of previous bills handy can be helpful here. (One other potential option is to set up automated payments, linked to your money accounts, directly through the provider — for instance, the water department of the city where you live).

When paying electronically, you’ll need to add your account number so that your payment is properly credited to you. You can also add the amount and frequency of payments, selecting a specific payment date (for one-time payments) or a regular schedule (for repeat bills that get paid on the same date every month).

Some financial institutions place a cap on the amount of money that can be transferred electronically through bill pay. If an automatic payment exceeds that designated transaction limit, users may then need to pay via a physical method, such as a personal or cashier’s check.

6. Taking Note of the Billing Schedule

high-yield checking account online and earn 0.50% APY.

Keeping Track of Outstanding Bills and Extra Fees

One research report (spanning 2,000 individuals) indicates that 28% of Americans report difficulty in paying their bills on time. In this group, 52% of those earning less than $25,000 or less noted difficulty with paying bills, while only 11% of those earning $125,000 or higher reported the same bill-paying challenges.

benefits to automatic bill pay, including avoiding overdue accounts.

Here are some consequences of not paying bills on time.

Imposing Late Fees

One of the ways companies or service providers enforce on-time payments is by penalizing people for, well, paying late. Whether it’s a credit card, utility bill or simply missing a payment date by a single day, submitting a late payment can result in late fees, higher interest rates, or other charges.

Put another way, not paying right now can cost individuals more in the long run. It’s worth noting that these fees or penalties can be higher if a person has a previous history of late or unpaid bills.

Accruing Interest Charges

On top of late penalties, some providers may also charge interest on the balance owed, essentially creating a double-wallop of fees if you’re late paying a bill. In some cases, the interest may be charged starting the day an account becomes overdue. In others, it may accrue going back to the purchase date or transaction day.

Depending on the interest rate charged and how frequently that interest compounds, this fee could quickly balloon to more than the initial fee assessed.

Experiencing Service Disruptions

In some cases, a provider may have the right to shut off your service if you pay a bill late. Not only are such disruptions a major interruption to daily life (ahem, no water, ahem) individuals may also have to pay a reinstatement fee once account has been paid—just to reactivate the service, such as electricity, natural gas, or the internet.

Declining Credit Rating

Think no one other than the service provider will notice a missed bill payment? Not so, in many cases. Payment history on outstanding debts makes up 35% of a FICO credit score. So, things like, overdue credit card bills, unpaid mortgage or car payments, and other late payments can erode an individual’s credit score.

It’s worth recalling that lenders and landlords can rely in part on credit scores when evaluating the risk of doing business with someone. So, dings to a credit score—things like late payments—can impact the likelihood of being approved for a loan or a lease. (Generally speaking, lenders consider a score below 580 a sign that the borrower is at a higher risk of not paying back the money loaned).

Even if approved, having a lower credit score could increase the rate of interest charged on a loan or credit card, potentially costing the borrower thousands of dollars over time.

Ready for a Better Banking Experience?

Open a SoFi Checking and Savings Account and start earning 4.50% APY on your cash!

Weighing the Benefits of Bill Pay

Not having enough money is just one reason people pay bills late. In many cases, the complexity of managing competing bills is a factor. It can be difficult to stay on top of each individual due date, especially for one-off bill payments or those bills that get paid less frequently, such as quarterly and annual bills. If you pay different bills from separate accounts, paying bills can become even more tangled.

Adopting regular strategies for paying bills can help solve remembering when to pay each bill (and with which account).

One payment strategy is to use online bill pay tools to automate your finances. Instead of remembering to pay each individual bill, while keeping track of competing due dates and amounts, bill pay allows users to set a payment schedule in advance and then, essentially, to forget about it.

Automatic bill payments can be a key way to prevent late payments and to simplify this important aspect of managing one’s finances. Now that you know what bill pay is and how it works, you can decide if it’s a wise move for you.

The Takeaway

Bill paying is a necessity that can be simplified. Signing up for automated bill-pay can put you in control. It can ensure that outstanding bills get paid on time or when you have more money in your accounts, reducing the likelihood of late-payment or overdraft fees.

Interested in opening an online bank account? When you sign up for a SoFi Checking and Savings account with direct deposit, you’ll get a competitive annual percentage yield (APY), pay zero account fees, and enjoy an array of rewards, such as access to the Allpoint Network of 55,000+ fee-free ATMs globally. Qualifying accounts can even access their paycheck up to two days early.

Better banking is here with up to 4.50% APY on SoFi Checking and Savings.

FAQ

Does bill pay take the money out right away?

In many cases you can determine when you want the transfer of funds to occur. You can pay in real time or schedule the payment for a later date.

Does bill pay send a physical check?

Bill pay is an electronic process that moves funds from one account to another. You do not have to write a check, nor does the payee receive one.

What is the difference between bill pay and ACH

Bill pay is a way of automating your finances. ACH (Automated Clearing House) is a network that moves funds electronically between banks. Bill pay may use the ACH network.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with direct deposit can earn up to 4.50% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. There is no minimum direct deposit amount required to qualify for the 4.50% APY for savings. Members without direct deposit will earn up to 1.20% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Interest rates are variable and subject to change at any time. These rates are current as of 8/2/2023. There is no minimum balance requirement. Additional information can be found at http://www.sofi.com/legal/banking-rate-sheet.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Rohit Chopra, director of the Consumer Financial Protection Bureau, has said the bureau is “no stranger” to litigation challenging the agency’s constitutionality. The Supreme Court is poised to hear oral argument on another such case this fall that could hold much of the agency’s rulemaking agenda in the balance.

Bloomberg News

The Consumer Financial Protection Bureau has a jam-packed agenda ahead with final rules coming soon that would cut credit card late fees to $8, create a registry of corporate “bad actors,” and require nonbanks to disclose terms waiving consumers’ rights to arbitration.

But the CFPB is operating under a cloud of uncertainty with the Supreme Court scheduled to hear oral arguments in October in a case challenging whether the bureau’s funding is constitutional. The legal and regulatory uncertainty will continue until the high court rules on the case by June 2024 at the latest. CFPB Director Rohit Chopra has been clear that the bureau is “not holding back” on rulemaking or enforcement.

“The CFPB is certainly no stranger to these types of challenges,” Chopra told American Banker in a recent interview.

But the CFPB got hit with further legal turbulence this week when a federal judge in Texas temporarily blocked implementation of the bureau’s small business data collection rule until the Supreme Court case is decided. Bankers have since urged the bureau to halt all bank data collection under the rule until after the outcome of the Supreme Court’s decision.

The ruling could change the calculus for the CFPB’s regulatory agenda going forward, potentially holding off several rules from going into effect. The judge granted a preliminary injunction to members of two bank trade groups and a private bank that had sued the CFPB, setting the stage for other trade groups to follow suit.

“This creates the precedent that fundamentally alters the CFPB’s agenda for the next year,” said Ed Mills, managing director at Raymond James. “The biggest development in favor of the industry is the most recent ruling and that there is a judge that says the CFPB can’t do anything until the Supreme Court has decided.”

The big question for banks, consumers and investors is not whether industry trade groups will sue the CFPB to block any final rules from going into effect but when and where they will sue. Trade groups have already threatened to sue the CFPB over the credit card late fee proposal, with the choice of venue likely in Texas, where Republican jurists dominate the U.S. Court of Appeals for the Fifth Circuit.

The CFPB “is going to get sued for everything and part of the reason why they get sued is because a number of the lawsuits have been successful,” added Mills.

The industry’s playbook for how to successfully gut a CFPB rule — and challenge the constitutionality of the bureau — is the years-long litigation over the payday lending rule. The bureau issued the payday rule in 2017 and was sued in 2018 by two Texas payday groups. Last year, a three-judge panel on the Fifth Circuit ruled that the CFPB was unconstitutionally funded through the Federal Reserve System and invalidated the payday rule. The CFPB appealed that ruling last year, teeing up the current constitutionality case before the Supreme Court.

In the case this week that temporarily halted the small business data collection rule for banks, the two bank trade groups also had appealed to the Fifth Circuit.

CFPB Director Rohit Chopra is poised to issue four final rules by year-end that could be challenged. A rule on credit card late fees is expected to be finalized in September or October and go into effect early next year. The rule is a priority for Chopra and many experts think the CFPB will not change its proposal to drop late fees to $8 from between $30 to $41 currently.

“Chopra has the authority to issue the rule on credit card late fees, and trade groups likely will look to file a lawsuit in Texas to get before the Fifth Circuit,” said Dan Smith, president and CEO at the Consumer Data Industry Association and a former CFPB assistant director.

Todd Zywicki, a law professor at the Antonin Scalia Law School at George Mason University, said the credit card late fee rule “does seem more likely to get the chopping block if the final rule resembles the proposal.”

Two more final rules expected by year end on nonbank registries — one for so-called “bad actors,” and the other that is a workaround of the CFPB’s invalidated arbitration rule — are also expected to be challenged. The CFPB proposed a rule in December that would create a public database of corporate lawbreakers, requiring nonbanks to report any state and local court orders or judgments involving consumer financial products. A second registry proposed in January would require nonbanks to register contract terms waiving consumers’ rights to arbitration.

“The bad actors’ registry just puts a bull’s eye on the industry,” said Eric Johnson, a partner at Hudson Cook. “I can see somebody challenging both of those rules while we’re waiting for the Supremes to act, especially now that two banking associations have had success before a judge.”

Finally, a much-anticipated proposal on open banking that would give consumers control over their personal financial data is expected to be finalized in 2024.

Chopra is mindful of the timeframe and deadlines for getting rules from the proposal stage through the public notice-and-comment process, and to the final rule stage before enactment. If the CFPB waits too long, there is always a threat — albeit a minor one, experts say — that a rule could be repealed by Republicans, assuming they take control of the Senate and Presidency and retain the House in 2024. Republicans used an obscure legislative process called the Congressional Review Act to overturn the CFPB’s arbitration rule in 2017 by a vote of 51-50.

The Congressional Review Act is one of the reasons the CFPB is moving quickly to propose other rules and get them finalized next year before the election. Proposed rules are coming in 2024 on overdraft fees, nonsufficient funds fees and credit reporting.

By halting compliance with a rule, industry hopes to stall or at least put off enactment until another day.

“The delay is really important for the industry because it opens up other avenues,” said Mills. “If there is an effective delay, could industry be saved by a Supreme Court decision and by the 2024 presidential election?”

The CFPB is moving quickly on rules to appear as though it is “business as usual,” despite the threat of the Supreme Court case, experts said.

“I can see where Chopra has sped up the bureau’s activities because they are trying to show all the good they think they’re doing for consumers to justify their existence and prove their worth to Congress,” said Johnson.

Do you ever have trouble keeping up with when bills are due and paying them on time? Welcome to the club. It can be a challenge for many busy people, but paying bills on time is important. Doing so helps you dodge those pricey late fees and maintain your credit score.

For many people, a solution to this challenge is to set up automatic bill payments. This can be done through an automatic payment system, usually referred to as “autopay.” This means that, without needing to remember any dates, write any checks, or click on any payment links, your recurring bills are seamlessly taken care of.

This can be a game-changer that helps you enjoy stronger financial management status and less money stress. But it might not be right for everyone. As with most financial tools, there are pros and cons to using autopay.

So what is autopay? And how do you set it up? Learn the answers to these questions, along with the pros and cons of autopay, so you can determine whether to consider using this option.

What Is Autopay?

What many people call “autopay” is a scheduled, regular transfer of money, usually monthly. These payments are generally transferred from the payer’s bank account (or credit card) to a vendor, or what is known as a payee.

When you link an account to a particular bill or vendor, autopay usually works over an electronic payment system called ACH.

Autopay is typically set up in one of two ways.

• The first is through the company receiving the payment.

• The second is through a bank’s online bill-pay portal.

When you link an account to a particular bill or vendor, autopay usually works over an electronic payment system called Automated Clearing House (ACH). Sometimes automatic payments are referred to as “ACH payments” instead of autopay. If you were to use your credit card, the recurring payment would simply show up as a charge on your card. 💡 Quick Tip: Don’t think too hard about your money. Automate your budgeting, saving, and spending with SoFi’s seamless and secure online banking app.

How Does Autopay Work?

Here’s a closer look at how autopay works. When autopay is set up, you are authorizing debits to occur on a regular basis. You will not be responsible for sending the funds. Some people may see this, however, as not being in control of their money.

When autopay is set up, either the payee is authorized to deduct funds from your bank account or your bank will send the funds for you.

You do need to pay attention to when your funds are whisked out of your account. If you aren’t on top of your finances, you could wind up in overdraft and getting assessed overdraft or NSF fees, plus late charges.

Autopay vs. Scheduled Payments

You may hear the terms autopay and scheduled payments used interchangeably but they are actually quite different.

• Autopay means that payments have been set up in advance to happen regularly on a certain date. You establish the date and the frequency and then don’t need to do anything else to transfer the funds on a recurring basis.

• With a scheduled payment, however, you are manually setting when you want a payment to be made and for how much. You can do this regularly, of course, but it requires more effort on your part to transfer funds.

Autopay vs. Bill Pay

Here’s another situation in which you may hear two terms (autopay and bill pay) used interchangeably. There is a slight difference, however.

Bill pay refers to the process in which your bank initiates payments from your account to the payee. In other words, the payee is not authorized to go in and deduct the money; your bank is instead providing this service.

Setting Up Autopay

Here is some more detail on setting up autopay so you can have your bills taken care of more easily.

1. Looking at Vendor Requirements

You can think of autopay as either pushing money from your account to the vendor, or the vendor pulling money from your account.

Many vendors require you to set up autopay through their website, so your first step may be to look into their requirements. If you are currently receiving a paper bill, they often include instructions on where you can go online to set up autopay — looking there is a good place to start.

For example, if you have a $1,800 monthly mortgage payment, you may be able to provide your mortgage company with your checking account information (such as your bank account number and routing number). They can pull the money for payment automatically. This is the “pull” version of automated payments as the vendor is pulling the money out.

2. Choosing the Day Your Payment Is Made

You generally get to choose the day that the payment is made — you could consider doing this a few days before the bill is due. This should give the automated payment time to move through the ACH system, including when the due date lands on a weekend.

Also, you’ll likely want to be cognizant that you aren’t setting up any automatic payments until you’re sure that any necessary deposits are made. For example, if you need your paycheck to cash before making a rent payment, making sure to give your paycheck at least a few days to settle in your account may be the pragmatic choice. Or you could see if the payee is willing to move your bill’s due date slightly to better accommodate your needs.

Setting Up ACH Payments

Another potential option is to set up an ACH transfer through your bank; this is the bill pay option mentioned above. Doing this typically requires logging onto your bank account’s website and navigating to the bill pay section.

If you go through your bank, you may need to provide them with the information for the vendor, such as the account number and mailing address. You can usually find this information on your bill or monthly statements.

Using the same example as above, you would enter the information for your mortgage lender into your bank’s bill pay portal. Similarly, the money would be sent via ACH on the date you’ve picked to send the money to the vendor.

You may want to consider selecting a date a few days prior to the due date to avoid a late payment. This is the “push” method of automated payments as you are pushing the money out of your account to the vendor.

Ready for a Better Banking Experience?

Open a SoFi Checking and Savings Account and start earning 1% APY on your cash!

Pros and Cons of Autopay

Autopay can be a wonderful tool for many people looking to simplify their finances. But it won’t be for everyone. Here’s a look at some of the pros and cons of using autopay.

Pros of Autopay

Consider these upsides of autopay:

Convenience: Gone are the days of sitting down to write a check for every last outstanding bill. In fact, these days you don’t even need to log into a computer every time a bill comes due. With autopay, you can pay all or most of your bills without lifting a finger.

This means no more having to log online to pay bills while you’re on vacation or busy with work or family. There is something beautiful about the convenience of the “set it and forget it” method to financial management, if you can make it work.

Improving Your Finances: We don’t need to tell you that it is a smart idea to pay your bills on time.

Not only can autopay help you to avoid frustrating late fees, but taking care of your bills right away may help you to avoid agonizing or allowing it to take up precious room on your to-do list.

Paying your bills on time may help your credit score.

Also, paying your bills on time may positively impact your credit score. Currently, debt payment history is the single biggest factor in terms of determining your score. It makes up 35% of a FICO®️ Score.

That means that paying debt-related bills, such as a mortgage, car loan, or credit card bill, on time, could potentially positively impact your FICO®️ Score.

Learning Good Behavior: If you can take the philosophy behind automatically paying your bills and apply it to your savings strategy, this may help your overall financial success. Just as you can automate the payment of your bills, you can automate your savings to retirement and other savings accounts.

If you don’t automatically set money aside, it can be far too easy to spend the money that lands in your checking account. Warren Buffett famously recommended that people “spend what is left after saving, do not save what is left after spending.”

Other ways to use automatic payments? Pay down debt aggressively or save for your future (even beyond a 401(k) if you have one). In either of these scenarios, you could simply set up an automatic transfer of funds as you would with autopay, but direct the funds toward your financial goal.

That way, the money is whisked from your checking account before you’ve even had the chance to consider spending it.

Potentially Saving Money: Vendors and service providers want to get paid on time. Therefore, some vendors or service providers offer a discount for customers that set up autopay, which could save you money.

For example, you may receive an interest rate discount if you set up autopay for a loan. Other vendors may provide a discount on their product or service if you use autopay.

Recommended: Understanding ACH Transfer Limits

Cons of AutoPay

Now, for the potential downsides:

Possible Overdraft Fees: If there isn’t enough money in your account to cover a bill, an ill-timed automatic payment could cause your account to overdraft. According to the FDIC (Federal Deposit Insurance Corporation), overdraft fees can average $35 a pop, depending on your bank.

You’d need to be especially careful if you leverage multiple checking or savings accounts with fluctuating balances or tend to keep your account balance close to zero. In the latter situation, you might benefit from keeping a cash cushion in your account.

Late Fees: Consider the transaction time when setting up your autopay in order to avoid annoying late fees. Late payment fees will vary by vendor but could be costly.

While giving yourself, for example, a four-day buffer could be a good start, it’s important to check with each vendor to determine their recommended timeline. Finally, after you’ve set up autopay, monitoring payments during the first few months to be sure they happen on time can help ease the transition.

Potentially Reinforcing Bad Habits: For some people and in some specific cases, it may not be a good idea to have your finances on autopilot. For example, those who are actively paying off credit card debt may want more control over how much they pay towards their debt each month.

There is almost always an option to autopay the “minimum payment” on a credit card, which may be tempting. There is no penalty when you pay the minimum payment, so it is certainly better than doing nothing.

But, it is much better to pay off the balance in full, if possible. When you do not pay the balance in full, the card will accrue interest, costing you money over time.

If you aren’t at a place where you can pay off the entire balance quite yet, you may want to try and set your autopay for an amount that’s more than the minimum payment so you can make progress on the balance. (And you may want to try to stop using your card in the meantime if this is the case.) If this won’t work for you, you may want to remain in manual control of payments.

Paying for Things You Don’t Need: Subscription services are sneaky. Amounts may seem small and you hardly notice them on a monthly basis, but they can wreak havoc on your annual budget. It is too easy to forget that you are paying for something, especially when you don’t use the service.

If you take advantage of the perks of autopay, don’t forget to reassess your subscriptions every few months to determine whether you actually need the thing you’re paying for. One example: You might not realize how much entertainment you are signed up for, and could save money on streaming services by dropping a platform or two.

Potentially Less Monitoring of Your Accounts: One issue with using autopay could be that you develop a sense of false security that your personal finances are running just fine. You might not check in with your money and review your spending as often as you might. This could have a negative impact. How often should you monitor your checking account? For many people, a couple or a few times a week is a good pace. 💡 Quick Tip: Most savings accounts only earn a fraction of a percentage in interest. Not at SoFi. Our high-yield savings account can help you make meaningful progress towards your financial goals.

Should You Use Autopay?

The digital age can be confusing and overwhelming, but this is one case where it may help to simplify our lives. Managing money can be a tedious task, and paying bills is just one part of it.

By streamlining the bills portion, you may find that using autopay gives you more freedom to focus your attention on other financial goals.

That said, autopay won’t be right for everyone and in every circumstance. For example, autopay might not be a great idea for those who haven’t organized their bills and tend to overdraft their accounts. It may not make sense for someone who is between jobs or out of work.

Autopay could potentially be difficult to manage for freelancers or other workers with variable income throughout the month. Ideally, a person would have some cash buffer for bills in any of these scenarios, but that is not the way it always works out in the real world. 💡 Quick Tip: When you overdraft your checking account, you’ll likely pay a non-sufficient fund fee of, say, $35. Look into linking a savings account to your checking account as a backup to avoid that, or shop around for a bank that doesn’t charge you for overdrafting.

The Takeaway

Autopay can be a convenient way to get your bills taken care of with less time, energy, and stress. However, in some cases, it can have its downsides, so it’s wise to know the pros and cons and continue to monitor your money carefully if you do sign up for autopay.

Interested in opening an online bank account? When you sign up for a SoFi Checking and Savings account with direct deposit, you’ll get a competitive annual percentage yield (APY), pay zero account fees, and enjoy an array of rewards, such as access to the Allpoint Network of 55,000+ fee-free ATMs globally. Qualifying accounts can even access their paycheck up to two days early.

Better banking is here with up to 4.40% APY on SoFi Checking and Savings.

FAQ

What should you not put on autopay?

It can be wise not to put bills that fluctuate on autopay. You are less likely to wind up with an overdraft situation that way. For instance, if your energy bill is usually $100 a month but goes up to double that during the winter or summer, that might throw off your personal finances if you autopay your bills.

When should I set up autopay?

It can be wise to set up autopay when you are familiar with your finances and cash flow and feel confident that automating your payments won’t lead to an overdraft situation. You might also consider signing up if there is a bonus or perk for you, such as a discount or a lower interest rate.

Why do people not use autopay?

Some people do not feel comfortable with autopay; they would rather be in control of making payments individually and maintaining that control over their finances. Also, some people may have bills that fluctuate considerably and they may therefore prefer to pay manually to avoid overdrafting.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with direct deposit can earn up to 4.40% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. There is no minimum direct deposit amount required to qualify for the 4.40% APY for savings. Members without direct deposit will earn up to 1.20% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Interest rates are variable and subject to change at any time. These rates are current as of 7/11/2023. There is no minimum balance requirement. Additional information can be found at http://www.sofi.com/legal/banking-rate-sheet.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.