Equity Prime Mortgage (EPM), which shifted to the TPO business after exiting its retail channel in the fall, has embarked on a new chapter. EPM wants to help grow the industry’s wholesale channel through its newly launched broker recruiting website.

BLVR – a marketing and promotional campaign launched by EPM on Monday – aims to reach as many retail loan officers to provide information about the wholesale channel.

When retail loan originators visit the website, LOs are asked to fill out their names, contact information and comments or questions about wholesale lending.

A third-party call center agent of BLVR will reach out to the loan officer for a follow-up and potentially connect the LO with another broker to explore business options in the wholesale channel.

“They can continue the conversation [with another broker] to the point where they make the decision to stay in retail or move over to the light side of the force,” Phil Mancuso, president and chief investment officer of EPM, said in an interview with HousingWire.

“As folks come into the funnel, we just push it through a call center and out to the brokers (…) There are no strings attached. If EPM happens to get one of those loans down the line, great, even better. We believe that we will earn business if the pie is bigger.” Mancuso explained.

The goal is to bring more than 4,000 loan officers to the wholesale channel over the next 12 months, EPM said.

The BLVR website gives retail loan officers a glimpse of the opportunities in wholesale origination, Mancuso added.

With mortgage rates having sharply risen since 2022, loan officers who have already made the jump to wholesale say they have an advantage in being able to shop around for lower rates.

Not having to bake in overhead costs found in the retail channel is a key advantage, wholesale lenders say.

About 16.8% of first-lien mortgage originations last quarter came from the broker channel, correspondent lending took up 26.8% and retail consisted of 56.5% of total volume, according to data from Inside Mortgage Finance (IMF).

That’s a jump in the broker (13.9%) and correspondent (24.1%) channels while a drop in retail origination(62%) in Q2 2022.

“The broker portion of the industry is less than it was pre-financial crisis. Yet, brokers have never been more competitive. The offering had never been more compelling. We’re pretty adamant, as others are about the future of this segment of our business (wholesale lending),” Mancuso said.

Timing the market, as it relates to trading and investing, requires a whole lot of luck. In effect, it means waiting for ideal market conditions, and then making a move to try and capitalize on the best market outcome. But nobody can predict the future, and it’s a high-risk strategy.

When seeing stock market charts and business news headlines, it can be tempting to imagine striking it rich by timing investments perfectly. In reality, figuring out when to buy or sell stocks is extremely difficult. Both professional and at-home investors make serious mistakes when trying to time their market entrance or exit.

Why Timing the Stock Market Doesn’t Work

Waiting to start investing could cost an individual thousands of dollars over their lifetime. It’s also important to know that by leaving money in a checking or savings account, a person is not protecting their money from inflation risk. That’s because the value of that cash in a checking or savings account erodes if the prices of goods and services increase.

Meanwhile, stock market timing is incredibly complex. Stock prices can be influenced by global macroeconomic events, political events in a country, developments in specific industries or companies, as well as the sentiment of investors as a collective.

Even professional investors struggle to “beat the market,” which often means simplifying trying to outperform a benchmark stock index. In fact, most investors can’t beat the market, and are likely better off sticking to index investing.

Fear and Greed in Investing

When investing, it’s also important not to let two key emotions – fear and greed – drive decisions. That means if the stock market is plummeting, investors may be fearful, but they can’t let those feelings push them toward a decision to sell. That could cause them to “lock in” losses. There’s even a Fear and Greed Index that investors sometimes use to make contrarian decisions.

Take for instance what happened during the 2008 financial crisis. After Lehman Brothers Holdings Inc. filed for bankruptcy in September 2008, the stock market entered a tumultuous stretch. The S&P 500 finally bottomed on March 9, 2009. However, the index eventually regained all its losses in the course of roughly the next four years. Investors who had hung on likely may have recovered their losses.

Meanwhile, greed can cause investors to make poor decisions as well. For instance, during the dotcom bubble, investors bought into many newly public Internet companies without always doing the research. Some of these stocks weren’t even turning a profit, making their businesses vulnerable to going belly up. Ultimately, many at-home investors suffered losses when the dot-com bubble burst.

Of course there are no guarantees when it comes to investing. There’s always risk and volatility involved. However, one of the most tried and true methods for building wealth has been a buy-and-hold strategy when it comes to stock investing.

💡 Quick Tip: When people talk about investment risk, they mean the risk of losing money. Some investments are higher risk, some are lower. Be sure to bear this in mind when investing online.

Why It May Be a Good Idea to Invest Immediately

One of the most important predictors of your returns is the length of time you’ve invested in the stock market. While it’s difficult to predict what the market will do in the near future, an investor can get a better sense over the long term.

When an investor lets their money grow, it has the chance to weather short-term ups and downs and grow over time. On average, the S&P 500, often used as a market benchmark, has grown 7% a year after adjusting for inflation. That doesn’t mean a person can predict what will happen this year, or even in the next 10 years, but looking at long term trends can give them a better sense of market dynamics.

An individual might put off investing because they want to pay off all debts first or achieve other goals, like buying a house. In some cases, that might be true, like paying off high-interest credit cards or saving for a short-term goal, such as a three to six-month emergency fund.

But once a person has an emergency fund and is out of credit card debt, they should consider investing, even if they have a mortgage or student loan debt. Even if they’re only investing for retirement, it’s a good idea to start as soon as possible.

💡 Quick Tip: How to manage potential risk factors in a self-directed investment account? Doing your research and employing strategies like dollar-cost averaging and diversification may help mitigate financial risk when trading stocks.

Consider Investing as Early as Possible

The younger you are when you invest, the better the chances are that you’ll reach your financial goals. For example, imagine Person A invests $200 a month in a retirement account starting at age 25.

Person B invests the same amount starting at age 35. They both continue to add $200 a month to their account. When they both retire at age 65, Person A will have almost twice as much as Person B: $306,689, compared to $167,550, assuming a 6% rate of return, 2% inflation rate, and 15% tax rate.

That’s true even though Person A only contributed 33% more to her account. This is how compound interest grows investments, or the power of how earnings from one’s investments can continue to build wealth.

Percentage of Retail Investors in Stock Market

As mentioned, after the 2008 financial crisis, many people were reluctant to invest in the stock market. But in recent years, that’s changed. Retail investor participation in the U.S. stock market increased considerably in 2020 and 2021, for a variety of reasons.

As of 2023, retail inventors comprise about a quarter of all total trading volume in the stock market. That may change in the future, too, as younger investors – with quicker, easier access to investing tools, in many cases – look at getting into the markets.

The Takeaway

Timing the market is difficult, if not impossible, and involves trying to “time” trading or investing moves to coincide with an increase or decrease in the stock market. Nobody can tell what the future holds, so it’s generally hard to accurately pick the right investments at the right time. That’s not to say that some investors don’t get it right from time to time, but as an overall strategy, it’s likely not advisable.

If an individual is skittish about investing, their anxiety makes sense in light of the dramatic market ups and downs many have witnessed in the past two decades. But trying to time the market doesn’t work. Instead, investing in a diversified portfolio can be a good step toward building individual wealth.

Ready to invest in your goals? It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here).

For a limited time, opening and funding an Active Invest account gives you the opportunity to get up to $1,000 in the stock of your choice.

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Claw Promotion: Customer must fund their Active Invest account with at least $10 within 30 days of opening the account. Probability of customer receiving $1,000 is 0.028%. See full terms and conditions.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

Feeling guilty shouldn’t stop you from taking care of yourself and your career. In today’s economy, switching jobs is often the surest way to get a significant pay raise, and it’s common to do so every few years.

“We all kind of grow out of things, and that’s a really normal process,” says Emily Frank, a Denver-based career counselor and coach who helps clients through her private practice called the Career Catalyst.

If you’re feeling guilty about leaving a job, experts recommend keeping the following points in mind.

Quitting may be better than staying

Think of it this way: Once you know you’re ready to move on, you probably notice a change in your attitude that makes work feel more like a drag. Is that a good thing for your coworkers and your employer?

When you’re feeling bored or unchallenged, it’s time to start looking for your next job move, Frank says. “Boredom isn’t good, and we don’t do our best work when we’re feeling unengaged.”

It’s normal to feel a sense of loss

The guilt you’re feeling about leaving your job may indicate that you care. You’ve invested time and energy into your work, as well as into your work relationships, says Jackie Cuevas, an Orange County, California-based human resources professional known on TikTok for giving career advice from “your friend in HR.”

“Obviously there’s a sense of guilt, because you’re like, ‘man, I’m leaving a lot behind,’ or ‘I have a lot of projects that I haven’t finished and they have to hire my replacement,’” Cuevas says.

“You have developed a bond with people that you work closely with. So it’s only natural and human to feel this feeling of guilt whenever you leave anyone behind.”

You can help with the transition

Channel your feelings of guilt into helping your coworkers and boss prepare for your departure. While it’s common to give two weeks’ notice that you’ll be leaving, standards vary depending on your industry and role. Give enough notice so that you have time to hand off projects, record any important notes or procedures and delegate responsibilities.

Bear in mind that you probably won’t answer every conceivable question before you leave. While it’s kind to offer to stay in touch if the team you’re leaving behind has questions after you’re gone, it’s not required. And you shouldn’t leave that door open just because you feel bad.

Focus on doing your best to help with the transition and then let the rest go, Cuevas says. “It’s up to management and the team to be able to really be solutions-focused and essentially figure it out.”

Your next chapter needs your attention, too

Wrapping up at an old job can be stressful. But your next phase needs your energy, too. Perhaps you’re moving to a new city or taking on a new level of responsibility.

If you can, take some time between ending one job and beginning another so you can decompress from the stress of your exit and shift your attention to what’s ahead of you.

It doesn’t have to be a lot of time — it could be a few days or a week. If, in order to get a bit of that transition time, you must give little notice at your old job, that’s a valid choice to make.

“You want to be able to close the door and get your mindset ready for this new, exciting position,” Cuevas says.

Should you feel guilty for quitting your job without notice?

Sometimes, circumstances require you to quit a job without notice, and you shouldn’t feel guilty about that.

It’s true that giving some notice before quitting your job would be the preferred route. It could help you maintain a professional relationship with your boss or coworkers. You never know when you might need help from people in your network.

But giving notice is not required and, in some instances, it may not be advisable, says Frank of the Career Catalyst.

You may decide to leave your job immediately because your new job starts right away or you are facing some kind of personal emergency. In those events, you may not be capable of doing your best work at your old job, and it’s probably better for everyone that you resign without notice.

If the fault is not on your end but lies with a harmful work culture, leaving immediately could be a way to protect yourself.

“If a workplace has gotten really bad, if there are bullying behaviors or sort of abusive treatment going on, then those are the times when you should throw professionalism out the window,” Frank says. “You just need to get out of there.”

Home is where we spend most of our time, the safe space that welcomes us at the end of a long day, the special place where we raise our families, bond with our loved ones, or retreat to for some well-deserved solitude.

And much like everything else in life, our home needs to be properly taken care of. I’m not talking about property improvements, upgrades or anything fancy.

Today, we just want to go over some general home maintenance aspects that you’re likely well aware of, but we’re hoping that a little reminder will help bring them to the forefront.

There are many things you can do, from doing regular maintenance with proper cleaning products like the ones from HG to taking extra safety measures. When you take care of your home properly, it will be the most comfortable place in the world. Keep reading to learn more about how you can achieve that.

Perform regular maintenance

The first tip to make your home is always in top condition is to perform regular maintenance.

This usually includes inspecting some points in your house, such as pipelines, roofs, ceilings, and HVAC systems. When you find something wrong at one or some of those points, you have to quickly address the issue.

Of course, you can always rely on professionals who are specialized in fixing such problems if you don’t feel like you have the expertise to do it yourself.

Make a regular cleaning schedule

The next tip is to keep your house clean at all times by making a regular cleaning schedule.

You can set the cleaning schedule once a month, twice a month, or even once a week depending on how often your home gets cluttered. Usually, the more people living in the house, the more easily it gets cluttered and accumulates dust.

Photo by Josue Michel on Unsplash

You can adjust your regular cleaning schedule based on how many people live in your house. Besides, you have to stock up on several kinds of cleaning products to make your regular cleaning activities much easier.

Take security measures

Another thing you must not miss when taking care of your home is to take security measures.

This is very important because the safety of your house as well as its inhabitants must be a key priority. And this doesn’t only mean safety from burglars who can break into your house. It also means keeping your home safe from hazards such as fire and potential short circuits.

A few easy ways to achieve this is to ensure your home has all the basic security features like security locks, smoke detectors, and fire extinguishers. It’s also a good idea to install an alarm system and several CCTVs around your home (if your budget can accommodate that) to make it more secure.

Photo by Sebastian Scholz (Nuki) on Unsplash

Perform landscaping and outdoor maintenance regularly

To make your home more comfortable and aesthetically pleasing, you have to perform landscaping and outdoor maintenance regularly.

This is very important because the exterior of your house can change drastically if you don’t tend to it regularly. One of the most important outdoor maintenance activities that you have to do is to mow your lawn due to how fast weeds grow.

You also have to trim bushes and trees if you have any in your yard. You also have to check the drainage to make sure it’s not blocked by dirt.

More stories

7 Top Decorating Ideas for Your Bedroom this Fall: Making Your Room More Cozy & Stylish

Here’s Everything You Need to Set Up a Meditation Corner in Your House

10 Unique Picture Frames and Holders to Create the Perfect Photo Wall

Do you want to learn how to find online typing jobs? There are many online typing jobs that may suit you well, and today’s article will help show you where to look. How to find online typing jobs What are online typing jobs? An online typing job is a job where you simply need an…

Do you want to learn how to find online typing jobs?

There are many online typing jobs that may suit you well, and today’s article will help show you where to look.

How to find online typing jobs

What are online typing jobs?

An online typing job is a job where you simply need an internet connection in order to work. You may be working for yourself as a small business owner or freelancer, or working for a company as an employee.

You can find online typing jobs in many different places, such as job boards, through recruiters, by networking, and more. Some job websites that you may be interested in include Upwork, FlexJobs, Indeed, Monster, and more.

Related content:

How much money can you make with an online typing job?

The amount of money that you can make with an online typing job varies.

This is because there are so many different types of jobs where you are typing online!

From starting your own blog to becoming a proofreader, live chat agent, transcriptionist and more, there are many, many different types of online typing jobs. And, they all pay a different amount of money. You can see below what some of them have for starting pay.

What are the pros and cons of an online typing job?

Pros of online typing jobs include:

If you are a fast typer, then this may be an easy gig for you

You can work from home

You may be able to have a flexible work schedule

You probably already have a laptop or computer, so you probably don’t need much in terms of equipment to get started

Cons of online typing jobs include:

Some online typing jobs may be a little repetitive. While this isn’t always a con, it could be for some

There are some scams out there, so you will need to do your research and make sure it’s a legitimate online typing job that you are looking at

What skills does an online typing job need?

The skills that you need will vary depending on the online typing job that you are interested in. But, some important ones for most will include accuracy in typing and a fast typing speed.

14 Best Online Typing Jobs

Below are the 14 best online typing jobs for beginners.

Blogger

My favorite online typing job is to start your own blog.

I spend most of my working time typing, and I really enjoy it!

Blogging allows me to travel whenever I would like, work from home, have a flexible schedule, earn an income, and more.

I created Making Sense of Cents in 2011, and since then I have earned over $5,000,000 with my blog.

My blog was created on a random day as a way to track my own personal finance progress. And when I first started my own blog, I honestly didn’t even know that people could make money blogging or how to start a successful blog!

I did not create Making Sense of Cents to earn money from home, but after only six months, I began to make money.

Blogging is quite affordable to start too, and you really just need a computer and an internet connection. I spend most of my time typing new blog posts, talking to readers and companies through email, and more.

You can sign up to learn how to start a blog with my free How To Start a Blog Course.

Proofreader

Proofreading is a flexible and detail-oriented job that only requires a laptop or tablet, an internet connection, and a good eye for finding mistakes.

Oh yeah, and accurate typing skills!

Proofreaders look for punctuation mistakes, misspelled words, lack of consistency, and formatting errors.

You might be proofreading books, articles, blog posts, student essays, lessons, scripts, emails, advertising content, medical documents, and more – anything that can be delivered electronically and be proofread on a computer or tablet.

You can learn more at How To Start A Proofreading Business And Make $4,000+ Monthly.

Sell printables on Etsy

Selling printables is an online job where you may be typing, creating graphics, and more.

Making printables on Etsy can be a great way to earn an income because you just need to create one digital file per product, which you can then sell an unlimited number of times.

So, what exactly is a printable?

Printables are digital products that customers can download and print at home. Some ideas for printables include grocery shopping checklists, gift tags, printable quotes for wall art, and more.

You can sign up for this free ebook that helps you figure out where to start when it comes to selling printables on Etsy.

You can also learn more at How I Make Money Selling Printables On Etsy.

Online bookkeeper

A bookkeeper is someone who tracks the finances of a business. As an online bookkeeper, you would be typing from home.

And, yes, you can start this even if you are brand new.

Online bookkeepers are in high demand. If you’ve been wanting to work from home and want to earn $40,000+ each year, bookkeeping could be perfect for you.

As a bookkeeper, you are responsible for helping businesses take care of their finances, such as by tracking receipts and spending.

A bookkeeper is someone who helps manage and track the financial side of a business. They will typically keep track of sales and expenses, and produce financial reports.

Those with virtual bookkeeping jobs work remotely from home, and they do not physically need to go into the office. Bookkeeping is an excellent option for remote work because all of a bookkeeper’s work can be done online or with computer software.

I recommend checking out the free How To Become An Online Bookkeeper Workshop to see if becoming a bookkeeper interests you.

Freelance writer

Freelance writing is a very popular career path, and I think it will only continue to grow!

And, you would be typing all the time. If you like to type, then this may be a great fit for you.

A freelance writer is someone who writes for a number of different clients, such as websites, blogs, magazines, news publications, and more. They don’t work for one specific company, rather they work for themselves and contract out their writing.

If you have a fast typing speed, then you can also write more blog posts and earn a higher income.

Learn more at How I Earn $200,000+ Writing Online Content.

Virtual assistant

As a virtual assistant, you would be typing from home and doing a variety of tasks.

The internet allows us to complete more daily tasks online, and more and more people also have stay-at-home jobs and businesses, such as running a website, social media, real estate, advertising, etc. That’s why virtual assistant jobs are in high demand.

Virtual assistant tasks may include:

Managing social media

Formatting and proofreading content

Scheduling travel and appointments

Managing email

Maintaining spreadsheets

Handling phone calls

And so much more. As a virtual assistant, you can get paid to do any task that needs to be done in someone’s business but doesn’t need to be done by them.

You can learn more at How This Virtual Assistant Earns $10,000 Month From Home as a Virtual Assistant.

Survey taker

Paid online surveys aren’t a full-time job, but if you’re looking for something that just takes up a little bit of your time each month, then this may be one to look into.

As a survey taker, you would mainly be completing surveys online from your laptop. You would be answering questions and simply just giving your feedback. Usually, you are paid via money sent to your PayPal account, gift cards, and free items.

Companies need people to take surveys so that they can see what the public thinks about their product and company, so that they know what to improve.

People typically sign up for as many survey companies as they can, as you usually won’t receive more than just a few surveys from a company each month.

Below are the companies I recommend signing up for:

American Consumer Opinion

Survey Junkie

Swagbucks

InboxDollars

Branded Surveys

Pinecone Research

PrizeRebel

User Interviews

Book reviewer

As a book reviewer, you can get paid to type from home, as you would be typing reviews for books that you have read!

There are websites that will pay you to review books, or you could even start your own book review blog. Each site varies, but you are typically paid cash via PayPal or bank transfer, or you may receive a free book in exchange for your review.

Here are some of the best websites for online typing jobs that will pay for you to review books:

Online Book Club – With this website, you are only paid with a free book for the first review. After the first review, you will be eligible to be paid for the book review opportunities, plus the books will always be free. With this website, you can get paid around $5 to $60 for each book that you review.

Kirkus – This platform is looking for book reviewers of English and Spanish language books. They need reviews that are about 350 words long, and they are due two weeks after you are assigned to read a book.

Upwork – With Upwork, you would need to create your own profile and make a listing as a book reviewer. This way, clients and authors can find you and hire you directly to read their book and review it. Plus, on Upwork, you can set your own pricing and decide which clients you want to work with.

The US Review of Books – This website uses freelance writers to review books and write reviews that are around 250 to 300 words long.

Reedsy – Here, you can review hundreds of different books before they are published and earn money at the same time. Authors submit their books to Reedsy, specifically to be reviewed by book reviewers. You then get paid by readers (those who buy a book) as a tip for the review. These tips can be $1, $3, or $5.

Booklist – This website pays for reviews that are around 150 to 175 words long that describe the plot, suggest an ideal audience, etc. Booklist pays $15 for each published book review.

Related content: 7 Best Ways To Get Paid To Read Books

Translator

Are you fluent in another language? If so, then you may be able to find an online typing work-from-home job where you translate content, books, articles, and more.

There are lots of places you can find translation jobs, including:

Upwork – On Upwork, you simply create a free profile and apply for translation jobs.

Babelcube – This is a website that sends freelance translation projects to you. You select which books you translate, translate them to one of more than 15 different languages, and partner with published authors.

Guru – Guru is a website that lists freelance writing and translation jobs.

Indeed – Indeed lists translation jobs that they find from job boards, staffing firms, company websites, and more.

FlexJobs – It will cost you to join FlexJobs, but they do list translation jobs, which can be worthwhile.

Today Translations – This is a website that is looking for translators to freelance for them.

Fiverr – Fiverr is an online marketplace where you can find freelance jobs all over the world. You can list your translation services and pricing here.

Ulatus – Ulatus is a website that provides translation services and they hire translators.

As you can see, there are lots of options if you want to put your translation skills to work.

Transcriptionist

Transcription work is when you turn audio or video content into a text document.

There are many businesses looking to fill positions for online transcription jobs since general transcriptionists convert audio files and video to text for virtually any industry. Some examples include marketers, authors, filmmakers, speakers, conferences, legal transcription, and more.

Online transcriptionist jobs can start around $15 an hour to begin with.

You can learn more about becoming a transcriptionist in the interview Make Money At Home By Becoming A Transcriptionist. The interview explains:

What a transcriptionist does

How much you can earn transcribing content

The type of training you need

How to find transcription jobs

And more!

Another online typing job similar to this is captioning, and I know we have all seen captions before. Captioning is when you transcribe a video and synchronize it with the video.

Live chat agent

Many large companies outsource their customer service departments to people who are working at home and they usually pay via an hourly wage.

This means you may be able to find a job as an online chat agent.

Customer service representatives may be responsible for a number of things, like:

Working as an online chat agent

Offering technical support

Providing customer support

A typing job as a customer service representative may be that you respond to help/support requests online, such as through an online live chat, or email support.

Affiliate marketer

I am an affiliate marketer through this blog, Making Sense of Cents, and I spend most of my working hours typing.

I think this can be a great way to earn income if you are interested in finding an online typing career path.

Affiliate marketing is when you earn an income by placing a referral link on your website, blog, Instagram, and so on and have people purchase a product or service through your referral link.

An example would be selling a book and you link to a specific book on your blog and try to get people to purchase the book through your affiliate link.

If you get someone to sign up through your affiliate link, the company (such as Amazon) pays you for sharing the product that they sell through the affiliate link.

If you want to learn more about affiliate marketing, I recommend signing up for Affiliate Marketing Tips For Bloggers – Free eBook.

Scopist

As a scopist, you would be typing from home.

Scoping is when you are editing legal documents for court reporters. This is different from proofreading for court reporters.

Scopists who are working with a court reporter tend to earn around $30,000 to $45,000 each year working around full-time hours.

I interviewed an expert on the topic – Linda from Internet Scoping School. She has been scoping for over 35 years and has taught scoping online for around 20 years.

She has a free course that will introduce you to scoping so that you can decide if it’s one of the online business ideas you want to pursue. You can find the free course by clicking here.

You can learn more at How To Become A Scopist.

Google rater

A search engine evaluator (also known as a Google rater) is a person who rates websites based on their quality and usefulness.

You are rating websites to help Google improve its search engine results.

This can be a great online typing job for beginners because you don’t need experience in this area to start, nor do you have to know what you are doing. This is because Google wants average people rating their sites.

Another great thing – since Google operates in nearly every country around the world, you can work on sites that are in your native language.

Learn more at How To Become a Search Engine Evaluator.

Are online typing jobs legitimate?

Yes, online typing jobs are real and legitimate.

I work online and I know many, many other people who also work online and spend most of their day typing.

Many companies hire online workers, and there are many different kinds of online typing businesses that you can start as well.

There are so many online typing jobs, especially in today’s day and age. I recommend seeing which ones you are most interested in and learning more about them.

Online Typing Jobs – Summary

As you can see, there are many different online typing jobs that may interest you.

Depending on your typing speed, accuracy, skills, whether you are looking for full-time or part-time jobs, if you need entry-level work, and more, there are many different online typing jobs that may interest you.

These may include typist jobs such as:

Blogger

Proofreader

Sell printables on Etsy

Bookkeeper

Freelance writer

Virtual assistant

Survey taker

Book reviewer

Translator

Transcriptionist

Live chat agent

Affiliate marketer

Scopist

Google rater

What do you think are the best online typing jobs?

The recently completed $300 million-plus acquisition of Home Point Capital by Mr. Cooper provided an attractive opportunity to bolster the company’s existing mortgage servicing rights (MSR) portfolio, and it’s expected to boost the company’s bottom line within the next couple of quarters.

This is according to Jay Bray, CEO of Mr. Cooper, in an interview on HousingWire’s Housing News podcast hosted by HW Media CEO Clayton Collins.

“We’ve known the management team [at HomePoint] well, [and] we’ve talked to them over the years about different strategic options,” Bray said. “As we entered the year, we felt like there was going to be an opportunity to buy some MSRs, and HomePoint presented a wonderful opportunity.”

Part of that stems from its large portfolio predominantly composed of Fannie Mae and Freddie Mac-backed loans, and aligned with Mr. Cooper’s own strengths, Bray explained.

“We just felt like that made a ton of sense,” he said. “We can add [them] to our platform without a lot of incremental costs, and continue to grow the platform that we’ve discussed over the years. And so, it just made a lot of sense for us.”

Bray said incorporating the company and its $84 billion in MSR assets has proven to be a smooth process so far, adding that it made a lot of sense for Mr. Cooper to explore strategically.

When asked about the differences in complexity between acquiring a company and an MSR portfolio, Bray explained that this particular acquisition was not very complex since Home Point Capital had spent much of the last year “simplifying their operation,” he said. That actually created more commonality with an asset purchase, he explained.

[embedded content]

“Once we got to the stage where we were able to execute on a transaction, really, all that was left was predominantly the servicing asset,” Bray said. “And the servicing asset was being subserviced, so they just didn’t have a ton of operations [or] people that were supporting that asset. So, it was almost like buying an MSR asset.”

Prior transactions Mr. Cooper has been involved in were comparatively more complicated since they involved bringing over people and associated platforms in addition to the companies themselves, Bray said.

“We’ve done more, I would say, asset transactions than really true company or platform transactions in the past,” he said. “We can certainly do either, but the complexity of HomePoint was pretty simple because they had really simplified their operation. So, that’s really the way to think about it.”

When asked about any added complexity existing subservicing relationships may add to an acquisition, Bray explained that Mr. Cooper typically pulls any related subservicing into its own platform.

“We view our platform as, if not the most efficient, one of the most efficient platforms out there,” Bray said. “And so with our scale, size [and] profitability, it always makes sense to move it onto our platform. Now, there may be a period of time that we keep it at the subservicer just from a logistics [or] approval standpoint, but we generally always move it to our platform.”

There were no real surprises to be found in the transaction process that were not previously identified by prior due diligence conducted by Mr. Cooper, Bray added.

Listen to the full discussion with Jay Bray on the recent episode of Housing News.

This statement from the Fed is classic Fed at work.

The Fed has not helped its own cause here, as Austan Goolsbee, president and CEO of the Federal Reserve Bank of Chicago, said in a speech last week: “I’m still trying to process why long-end interest rates are increasing.”

My answer: “Stop talking about raising rate at this stage with a hawkish outlook!”

The Fed has expressed that real yields, meaning where inflation is currently and where rates are, are restrictive to the economy, so sounding hawkish on monetary policy at this stage can lead the bond market to go higher more than the Fed would like. Land the plane, folks, land the plane!

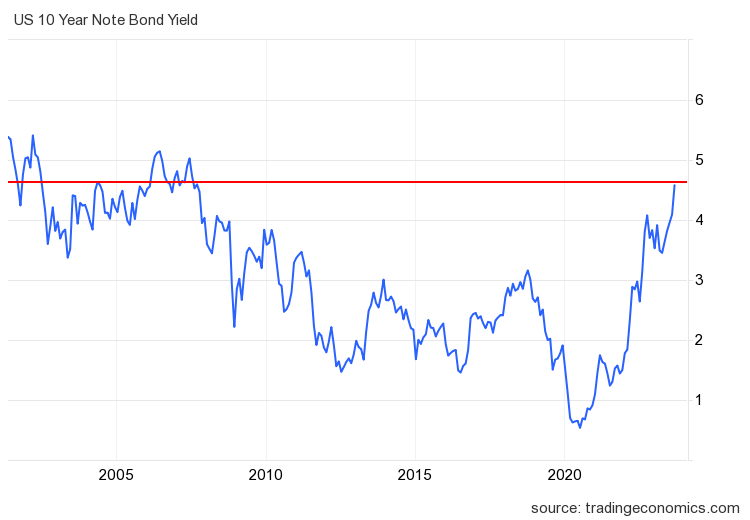

As you can see in the chart below, it was another wild week in the bond market. Mortgage rates went from 7.39% to a high of 7.65% and ended the week at 7.44%. Before last week the high for mortgage rates this year was 7.49%.

The bond market has been volatile, but after the 10-year yield broke the 4.34% level, I am watching for the 4.63% level. A close above that and follow-through bond market selling could lead to higher mortgage rates. Hopefully, the last two weeks caught the Fed’s attention. If they cared about a soft landing, which I have been skeptical about from the start, as I talked about here on CNBC, the Fed would be more mindful of what they say and do.

Weekly housing inventory data

One of the things I got wrong this year is that I believed if mortgage rates stayed higher for longer, active inventory would grow between 11,000 and 17,000 for at least some of the weeks; that hasn’t happened recently with higher rates — close but no cigar. T

Last week, the growth of active listings slowed to 6,808. Seasonality is kicking in now, but we should be able to continue growing housing inventory like we did last year, as higher rates slow sales down, keeping homes on the market longer.

Last year, the seasonal peak was Oct. 28. Last week, according to Altos Research:

Weekly inventory change (Sept.22-29): Inventory rose from 527,938 to 534,746

Same week last year (Sept. 23-30): Inventory rose from 556,865 to 561,229

The inventory bottom for 2022 was 240,194

The inventory peak for 2023 so far is 534,746

For context, active listings for this week in 2015 were 1,187,2000

After some volatile weeks with the new listings data, things look similar to earlier in the year when we had an orderly seasonal decline in new listings data, which has been trending at the lowest levels ever for over 13 months. Even with rates spiking, the new listing data hasn’t created another new leg lower. This is important, as I expect flat to slightly positive data soon due to a shallow bar.

Historically, one-third of all homes have price cuts every year. Last week’s price cuts were lower than last year at the same time by 4%. This is happening even with rates over 7% and part of the reason is that housing inventory has been negative year over year since mid-June. As mortgage rates move higher, the percentage of price cuts can grow but it’s trailing last year’s percentage as home sales aren’t crashing like they did last year.

Price cuts for last week over the years:

2021: 29%

2022: 42%

2023: 38%

Purchase application data

Purchase application data was 2% lower last week versus the previous week, making the year-to-date count 17 positive prints, 19 negative prints, and one flat week. If we start from Nov. 9, 2022, it’s been 24 positive prints versus 19 negative prints and one flat week. The week-to-week data has gotten softer since mortgage rates have been trending above 7%. However, it’s not crashing like last year because we are working from a lower bar.

The week ahead: It’s jobs week! (If the government is open)

If we don’t have a government shutdown, the week ahead will be jobs week again! The Fed was happy about labor data last month as job openings have been falling, and the job growth data is cooling down. However, jobless claims are still going strong, so they have more work to do in attacking the labor supply. In addition to jobless claims, this week we will also have job openings, the ADP jobs report, and the BLS Jobs Friday report, which could move the bond market this week.

Also, I will watch this week to see if more Fed members comment about rising long-term rates. The Fed would like to keep rates higher for longer, but if the bond market gets a whiff of any terrible recession data, it will take yields down. So far, jobless claims data hasn’t given them any reason to do so.

Very few of us can freshen our home design on an endless budget. But you don’t have to feel constrained by your wallet. That’s because not every piece needs to be the highest quality.

We asked Dallas interior designers where they splurge and where they save to help you stretch your home-decorating fund.

Advertisement

Invest in key parts of your bedroom.

No surprises here. We spend a third of our lives sleeping, so your bedroom matters — even though it’s an area guests may not see.

Advertisement

“Your main bedroom is where you should splurge on yourself,” advises Denise McGaha, owner and principal of Denise McGaha Interiors. “A lot of my clients leave that to the last, and I think it’s so important for you to have a really luxurious, amazing night’s sleep. If you don’t sleep well, you’re not fun to be around the next day.”

Get updates from Abode

Sign up for the Abode newsletter for a weekly roundup of the latest home, design and real estate stories.

Your sleeping environment is key, so invest in a great mattress and high-quality linens. You can save on your accent pieces. This bedroom was created by Nikki Watson of The Design Quad.(Courtesy The Design Quad)

McGaha says the mattress is key, but linens are too. So that’s where to concentrate your funds. What about the rest of your bedroom design? Consider buying lower-tier antiques or quality used pieces instead of brand-new furniture.

Advertisement

You can also look for deals on lamps, rugs and throw pillows, creating a designer-approved look that is budget friendly. “Every time you walk in that space,” McGaha says, “I want it to make you smile.”

Chairs trump table in your dining room.

McGaha used an antique table in this dining room. She advises concentrating your budget on striking dining chairs. A statement light fixture is another good investment.(Stephen Karlisch)

What about the star of the show in the dining area: the table? McGaha says don’t spend a lot, even though it’s one of the biggest pieces, size-wise, in your home.

“I want to encourage people to buy vintage or used tables, because the chairs are where it’s at. People are paying attention to the chair and they’re going to see the back of the chair. Do they even see the base of the table? Especially if you love to entertain, you’re going to put a tablecloth over it a lot. So let’s get you a beautiful antique or vintage table, or use your grandmother’s table, and get new chairs.”

Advertisement

When it comes to what’s over the table, that’s another place to go all out. “Lighting is where you want to spend money,” says Nikki Watson, founder of The Design Quad. “Especially with a new build, people will put in basic fixtures. But if they want to update the space and make it look awesome, then lighting makes a big difference.”

Advertisement

How to redecorate your house for free — using items you already own

In the living room, spend money where people sit.

The living room is all about the return on investment — or in designers’ terms, “seat time.” The more time someone is likely to sit there, the more you should invest in the piece, says McGaha.

Advertisement

So spend time and money picking out a great sofa that will last a long time, but go for less expensive pieces when it comes to to accent furniture. “Like a lounge chair that goes in the room with your really great sofa, you don’t have to spend nearly as much money on that. That way if you get tired of it, you can change it out,” McGaha notes.

“I wouldn’t spend tons of money there because people don’t sit in a lounge chair as long as they relax on a sofa.”

Watson agrees that a sofa is really worth investing in — a neutral sofa, in particular. Bargain accent pillows and throws can be incorporated to stay on trend.

A living space can also be a good choice for spending on lighting, wallpaper and custom upholstery. After all, this room is where we spend many of our waking hours.

Advertisement

“I love to splurge on upholstery,” McGaha shares. “By upholstery I mean getting a piece that’s custom for you, meaning it’s deeper or it’s got a different fill on the cushion, so that every time you sit down you say, ‘I just love this sofa.’”

Where can you save in a living room? Look under your feet. “Rugs are something trendy, so they can be replaced pretty often,” points out Watson.

“I wouldn’t say spend a lot of money, because that trend will change. I know we have faded antique rugs that have been the style for about three to four years now, but now geometrics are coming back in.”

Use lower-cost art prints in secondary spaces, such as a bathroom or guest bedroom. This bathroom is part of a home designed by Watson.(Courtesy The Design Quad)

Advertisement

Limit what you spend in your guest room.

It can be tempting to go big in the guest room to really make an impression on people who stay with you, but resist the urge, says McGaha. Your investment in a space should relate to how much time you, the homeowner, spend there.

“I love to use artist prints instead of originals in hallways or guest bedrooms or bathrooms. I’m always going to tell you not to spend all your dollars in those secondary spaces,” says McGaha. “And while I love my guest rooms to be luxurious and really elegant for guests, let’s not put something in there that only that one person gets to enjoy. They’re only there for a few nights.”

To save in a guest room, you could paint instead of doing high-end wallpaper. Your window coverings can be sale items; so can guest linens and bedding. When you look for deals, you can more easily change out those elements for a style update.

Advertisement

Go for cost-effective pieces in kids’ rooms.

You don’t have to spend a lot on a child’s room. Less-expensive, trendy pieces will create a space they’re happy with — and when their tastes change, you can more easily swap out the furnishings and accessories.(Getty Images)

Keep in mind that kids tend to be harder on furnishings, and their tastes will change as they grow up — so feel free to choose lower-cost, trendier pieces for their spaces. McGaha says the bed is a particular place you can save in a child’s room. Use a metal bed frame and score a fun and comfy upholstered headboard.

Don’t neglect your entryway.

You might not think about splurging on the entry to your home, but hear us out. It’s often the first thing you see when you return home and the last thing you see before you leave. And it’s the first and last impression of your home that guests have, too.

Advertisement

This is where you want to go for original art, amazing lighting and the wallpaper of your dreams. And best of all, it’s a small space compared to other areas in your home, so you can choose just a few things and still have a big impact.

Figuring out how to double your money with investments often hinges on striking the right balance between risk and reward. Your personal risk tolerance and goals can influence how you invest and the returns your portfolio generates.

However, doubling your money is a reasonable goal, especially if you’re willing to wait for your money to grow. And that’s a big variable to keep in mind: Time. If you’re interested in doubling your money and growing wealth for the long-term, there are several investing strategies to consider.

Investing Strategies to Double Your Money

1. Get to Know the Rule of 72

The rule of 72 can be a helpful guideline for answering this question: How long to double your money?

If you’re not familiar with this investing rule, it’s not complicated. It uses a simple formula to estimate how long doubling your money might take, based on your annual rate of return. You divide 72 by your annual return to get the number of years you’ll need to wait for your investment to double.

So, for example, if you have an investment that generates a 5% annual return, it would take around 14.5 years to double it. On the other hand, an investment that’s generating a 12% annual return would double in about six years.

The rule of 72 doesn’t predict how an investment will perform. But it can give you an idea of how quickly (or slowly) you can double your money, based on the returns you’re getting each year. Just keep in mind that the rule’s accuracy tends to decrease as the rate of return increases, so it’s more of a guideline than a hard-and-fast rule.

💡 Quick Tip: How do you decide if a certain trading platform or app is right for you? Ideally, the investment platform you choose offers the features that you need for your investment goals or strategy, e.g., an easy-to-use interface, data analysis, educational tools.

2. Leverage Your Employer’s Retirement Plan

One way to attempt to double your money through investing may be through your workplace retirement plan. If your employer offers a matching contribution to the money you’re deferring from your paychecks, that’s essentially free money for you.

Employer matching contributions are low-hanging fruit, in that you don’t need to change your investment strategy to take advantage of them. All that’s required is contributing enough of your salary to your employer’s retirement plan to qualify for the match.

The matching formula that companies use varies, but some companies offer a dollar-for-dollar match, meaning that the money you put into a 401(k) would automatically double when you receive your match. Keep in mind that some companies use a vesting schedule, meaning that you have to work at the company for a certain period of time before you get to keep all the employer contributions.

Aside from potentially helping to double your money, investing your 401(k) or a similar qualified retirement plan can also yield tax benefits. Contributions made with pre-tax dollars are deducted from your taxable income, which could lower your annual tax bill.

3. Diversify Strategically

Diversification means spreading your money across different investments to create a portfolio that will meet your needs for both risk and return.

As a general rule of thumb, riskier investments like stocks have the potential to generate higher returns. More conservative investments, such as bonds, tend to generate lower returns but there’s less risk that you’ll lose money on the investment.

If you want to double your money, then it’s important to pay attention to diversification and what that means for your return on investment. For instance, if you’re investing heavily in stocks then you could see greater returns but you might experience deeper losses if the market takes a hit. Playing it too safe, on the other hand, could cause your portfolio to underperform.

Also, keep in mind that there are many types of investments besides stocks, mutual funds and bonds. Real estate, stock options, futures, precious metals and hedge funds are just some stock and bond alternatives you could use to build a portfolio. Understanding their risk/reward profiles can help you decide what to invest in if you’re focused on doubling your money.

💡 Quick Tip: Distributing your money across a range of assets — also known as diversification — can be beneficial for long-term investors. When you put your eggs in many baskets, it may be beneficial if a single asset class goes down.

4. Consider Buying When Others Are Selling

The stock market is cyclical and you’re guaranteed to experience ups and downs during your investing career. How you approach the down periods can impact your ability to double your money when the market goes up again.

When the market drops, some investors start selling off stocks or other investments to avoid losses. But if you’re comfortable taking risks, the sell-off could present an opportunity to buy the dip.

If you can purchase stocks at a discount during periods of volatility when other investors are selling, you could double your money when those same stocks increase in value again. But again, making this strategy work for you comes down to knowing how much risk is acceptable to you.

5. Commit for the Long Term

There are different investment philosophies you can adopt. For example, traders regularly buy and sell investments to try and get quick wins from the market. A buy-and-hold strategy takes a different approach, but it could pay off if you’re trying to double your money.

Buy-and-hold investing involves buying an investment and holding onto it for the long-term. The idea is that during that holding period, the investment will grow in value so you can sell it at a sizable profit later.

This is a passive investment strategy that relies on patience and time to increase your portfolio’s value. The longer you have to invest, the more you can capitalize on the power of compounding gains, or gains you earn on your gains.

If you’re using a buy-and-hold strategy with a value investing strategy, you could potentially double your money or more if your investments meet your expectations. Value investing means investing in companies that you believe the market has undervalued.

This strategy takes a little work since you have to learn how to understand the difference between a stock’s market value and its intrinsic value. But if you can find one of these bargain hidden gems and hold onto it, you could reap major return rewards later when you’re ready to sell.

6. Step Up Your Investment Contributions

Another simple strategy to double your money is to invest more. Assuming your portfolio is performing the way you want and need it to to reach your goals, doubling your investment contributions could be a relatively easy way to boost your returns.

If you can’t afford to put big chunks of money into the market all at once, there are ways to increase your investments gradually. For instance, you could start building a portfolio with fractional shares and increase your contributions by a few dollars each month.

If you’re investing your 401(k) at work, you could ask your plan administrator about raising your contribution rate annually. For example, you might be able to automatically bump up salary deferrals by one or two percent each year. And if that coincides with a pay raise you may not even miss the extra money you’re contributing.

7. Focus on Tax Efficiency

Minimizing tax liability is another opportunity to stretch your investment dollars. There are different ways to do that inside your portfolio.

Investing in your retirement plan at work is an obvious one, so if you aren’t doing that yet you may want to consider getting started. Remember, the longer you have to invest, the more time your money has to grow.

If you don’t have a 401(k) or a similar plan at work, you could open a traditional or Roth Individual Retirement Account (IRA) instead. A traditional IRA allows for tax-deductible contributions, meaning you get an upfront tax break. Then, you pay ordinary income tax on that money when you withdraw it in retirement.

Roth IRAs aren’t tax-deductible, since you fund them with after-tax dollars. The upside of that, however, is that qualified withdrawals in retirement are 100% tax-free.

A taxable brokerage account is another way to invest, without being subject to annual contribution limits the way you would with a 401(k) or IRA. The difference is that you’ll pay capital gains tax on your investment growth.

Paying attention to asset location can help with maximizing tax efficiency across different investment accounts. For example, exchange-traded funds can sometimes be more tax-efficient than other types of mutual funds because they have lower turnover. That means the assets in the fund aren’t bought or sold as frequently, so there are fewer taxable events.

Keeping ETFs in a taxable account while putting less tax-efficient investments into a tax-advantaged account, such as a 401(k) or IRA, could help with doubling your money if it means reducing the taxes you pay on investment gains.

The Takeaway

Learning how to double your money can mean taking a slow route or a quicker one, but it all comes down to how much risk you’re comfortable with and how much time you have to invest. One of the keys to growing your investments is being consistent and that’s where automated investing can help.

There are numerous strategies and tactics that you can try to leverage to your advantage. But ultimately, whether you’re able to double your money will likely come down to how much you’re willing to risk, how much time you have on your side, and probably a little bit of luck.

Ready to invest in your goals? It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here).

For a limited time, opening and funding an Active Invest account gives you the opportunity to get up to $1,000 in the stock of your choice.

Photo credit: iStock/South_agency

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Claw Promotion: Customer must fund their Active Invest account with at least $10 within 30 days of opening the account. Probability of customer receiving $1,000 is 0.028%. See full terms and conditions.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

Hate cold calling? Hear how to ditch it entirely on this podcast with organic-lead-gen expert Charlie Cameron. Charlie generated an incredible amount of real estate business incredibly fast, and it was very inexpensive. Today, he shares the low-cost tech tools and proven strategies that helped make it happen. Discover how he built a booming Facebook group, how he consistently ranks above competitors on Google, and more on this Real Estate Rockstars!

Listen to today’s show and learn:

About Charlie Cameron [0:54]

“Easy money” [2:20]

Getting clients from a Facebook group [3:25]

You don’t have to cold call [4:54]

How NOT to fail at Facebook groups [6:37]

Ways to help your Facebook group grow [8:46]

Charlie’s follow-up process for Facebook leads [12:44]

How much business Charlie gets from his Facebook group [19:22]

Attracting clients and agents with blogging and SEO [20:43]

How to ensure potential clients find you online [27:42]

Ways to get ahead with organic lead gen now [30:14]

Charlie’s content-machine goal [36:44]

Advice on picking a platform for your content [38:11]

Charlie Cameron’s advice for real estate agents [44:56]

Charlie Cameron

Real estate super nerd, family man and veteran! I’m passionate about real estate and obsessed with helping others win and with continuous growth.

Charlie Cameron is a Dad, military spouse, and Air Force veteran (turned reservist) who found a passion for real estate while serving. Thanks to real estate—largely eXp Realty and investing—he was able to transition out of Active Duty military service to focus on real estate! People and real estate are his passions, and helping other succeed is what he finds most rewarding.

Charlie enjoys mentoring growth-minded agents the most. At this time, he is growing an international real estate team, building a local military-focused real estate team along the Florida Panhandle, and scaling an as-passive-as-possible real estate portfolio of short term rentals, residential assisted living, and more! He is also an Air Force Reservist in a part time capacity (2 weeks a year) as a weapon program manager.

By leveraging teams, systems, automation, and intentional task prioritization, Charlie is able to prioritize his most important thing: living in the moment with family & friends!

Current lines of effort:

Grow international real estate team: help other real estate agents become successful, grow their leads and business, create multiple income streams, and achieve financial freedom. Team growth achieved through blog and content creation.

Lead a local military-first real estate team: though long term low effort client attraction efforts, Charlie provides clients to his local military focused team to work and close!

Scale a real estate investment portfolio: real estate investing is best investing!

Charlie has a bachelors in Mechanical Engineering from the University of Virginia and a Masters in Industrial Engineering from New Mexico State. He starting investing in real estate while serving in 2017 by STARTING with 8 apartments which he self managed. After scaling a small multifamily portfolio he transitioned and 1031 exchanged into a self managed short term rental portfolio, all of which he managed from afar. Recently he has pivoted again into the residential assisted living niche. Charlie partners on just about every investment deal he does.

Charlie spent 11 years on Active Duty, as an engineer and officer developing, testing, and managing cutting edge weapons systems programs to ensure the Air Force stays undefeatable! He led hundreds of tests and ran hundreds of million dollar a year programs and contracts developing, acquiring, and testing new weapons for the warfighter. During that time, he also served as a USAA Advisory Panel Member, providing direct feedback on bank and insurance products as a military member to the board of directors. In a past life, he has also been a Firefighter, EMT, and lifeguard.

Charlie is a nerd who loves to tinker and find new ways to grow and implement things in his businesses. While he wishes he was able to focus on only one business, he knows now that resistance is futile and he must find ways to grow multiple lines of effort without consuming more time!

Related Links and Resources:

It might go without saying, but I’m going to say it anyway: We really value listeners like you. We’re constantly working to improve the show, so why not leave us a review? If you love the content and can’t stand the thought of missing the nuggets our Rockstar guests share every week, please subscribe; it’ll get you instant access to our latest episodes and is the best way to support your favorite real estate podcast. Have questions? Suggestions? Want to say hi? Shoot me a message via Twitter, Instagram, Facebook, or Email.