After exceeding 8 percent in October, rising mortgage rates overtook “lack of housing inventory” as the top concern for real estate agents, according to the results of the latest monthly Inman Intel Index.

The verdict is in — the old way of doing business is over. Join us at Inman Connect New York Jan. 23-25, when together we’ll conquer today’s market challenges and prepare for tomorrow’s opportunities. Defy the market and bet big on your future.

Approximately one-third of agents and the brokerage executives who lead them believe high mortgage rates are the biggest for concern in the housing market today, surpassing low inventory and fallout from commission lawsuits such as Sitzer | Burnett, according to the results of October’s Inman Intel Index survey, released last week.

After exceeding 8 percent in October, rising mortgage rates overtook “lack of housing inventory” as agents’ top fear after ranking second in the same survey a month earlier. The findings are among hundreds gleaned from the Inman Intel Index, or Triple I, which was conducted Oct. 23-31 and drew 1,269 responses. The 168-page report is available exclusively to Inman Intel subscribers and includes a comprehensive breakdown of all survey responses.

This month’s Inman Intel Index survey is open now.

“I think that homebuyers and real estate agents understand well that the 3 percent mortgage rate is a historic abnormality and is not the norm,” Gay Cororaton, chief economist for the Miami Association of Realtors, told Inman by email. “But the current rate of 8 percent is also not normal, and I expect rates to go further down in 2024.”

Mortgage rates have fallen significantly in November, with the average 30-year fixed mortgage closer to 7 percent than it has been in two months. For homebuyers and sellers, the benefit is clear, but after more than a year of rates in excess of 6 percent, the decline in rates is also a huge morale booster for real estate professionals, according to the survey results.

Only one group surveyed in the Triple-I didn’t rank interest rates as their top business concern in October. Mortgage originators, who did rank them first in September, put them second behind lack of home inventory. With refinance activity down severely, it stands to reason that brokers and bankers are focused on homes coming on the market.

To track industry sentiment, the Triple-I polls real estate agents, loan originators, brokers, industry executives and proptech leaders monthly. November’s survey opened today and can be accessed here.

No one gets a bite at the apple, though, until someone decides to buy a home, and elevated interest rates continue to factor heavily into the homebuying equation for many Americans. A new consumer survey undertaken by Inman, in partnership with Dig Insights, surveyed 3,000 potential homebuyers and found that many need to see a far more dramatic rate drop to move forward.

More than 2 out of 3 Americans surveyed by Dig Insights indicated they were unlikely to buy in the next 12 months, and 35 percent of those said that high interest rates were a factor in their decision. Asked how much mortgage rates would need to decrease for them to become likely to buy, one-third chose “More than 2 percent.”

According to an Inman Intel analysis last month, a mortgage payment that would have been close to $1,175 four years ago now comes to over $2,600 a month. That’s a problem for a lot of homebuyers, first-timers or not.

“With mortgage rates still expected to be elevated at over 5 percent, there’s naturally a higher financial hurdle for existing homeowners to move,” wrote Cororaton, a former senior economist and the director of housing and commercial research at the Research Group of the National Association of Realtors.

With a potential ceiling on rates, real estate agents and loan originators are looking toward 2024 with cautious optimism. While nearly 70 percent of agents indicated their buyer pipeline was either lighter or substantially lighter than it was 12 months ago, less than 30 percent felt that would be the case one year from now. Over one-quarter of them responded “Heavier,” while just under 44 percent said they expected it to be about the same.

Mortgage originators were even more optimistic, with over 37 percent expecting a heavier borrower pipeline in 12 months.

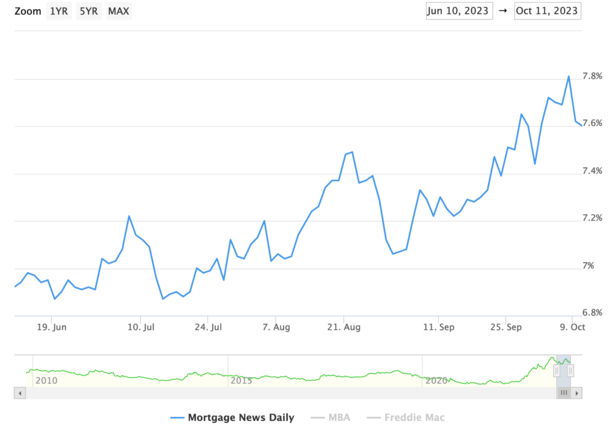

If you’ve been keeping track lately, you might be wondering why mortgage rates plunged this week.

Last week was a totally different story, with a hotter-than-expected jobs report almost enough to push the 30-year fixed across the daunting 8% threshold.

But then the unexpected happened over the weekend, as is often the case with geopolitical events.

In times of uncertainty, bonds are typically a safe haven, and when demand for them rises, their associated yields (or interest rates) fall.

This, coupled with some more dovish talk from Fed speakers, might explain the recent pullback in rates.

How Much Have Mortgage Rates Plunged?

First off, the word “plunge” might be a strong one given how much mortgage rates have climbed over the past 18 months.

While mortgage rates have indeed fallen all week, they remain well above recent lows. And even much higher than levels seen this summer.

If we want to use MND’s widely cited daily rate survey as the measure, the 30-year fixed now stands at 7.60%.

That’s down from 7.81% on Friday October 6th. So basically mortgage rates have improved by about 20 basis points, or perhaps .25% depending on the lender.

It also reduced the year-over-year change in rates from 0.77% to 0.46%, providing a glimmer of hope that the worst could be behind us.

And better yet, perhaps mortgage rates have peaked. While that remains to be seen, it’s been hard to get any meaningful relief lately.

Typically, any pullback or improvement in rates has been met with further increases. And the wins are generally short-lived.

Will that be the case again this time or is there finally light at the end of the tunnel?

Mortgage Rates Helped by New Geopolitical Risks

As for why mortgage rates improved this week, one would be quick to point to the events that took place in Israel (and continue to unfold).

Generally, mortgage rates tend to go down if there is the threat of war or similar tension in the air.

The reason is uncertainty, which is a friend to bonds because of their relative certainty.

In short, investors will flee riskier markets like equities and pile into bonds, which is known as the flight to safety.

If more investors are buying bonds, the price goes up and the yield drops. Since Friday, the 10-year bond yield has fallen from 4.84 to about 4.61 today.

Of course, this could prove to be a short-term reaction to what has been a clear move higher for bond yields lately.

So it’s entirely possible that the 10-year yield marches on back to those recent levels (and beyond) depending on what transpires.

And the conflict in the Middle East could actually exacerbate inflation if oil prices (and gas prices) rise.

No More Fed Rate Hikes Could Take Pressure Off Mortgage Rates

Another factor related to the recent mortgage rate plunge has been some dovish talk from Fed officials.

Atlanta Fed President Raphael Bostic came out this week and basically said no more interest rate hikes were needed.

The Fed has already raised its key policy rate 11 times since early 2022, pushing mortgage rates up along with it.

But Bostic “told the American Bankers Association that Fed policy is sufficiently restrictive.”

Additionally, he said rate cuts could even be in the cards “if things get ugly in the Middle East.”

“You can pretty much count on the Fed taking that into its world view and that’s only going to be lower rates.”

Earlier in the week, Dallas Fed President Lorie Logan said higher bond yields could do the heavy lifting for the Fed, requiring no additional tightening on their part.

And Fed Vice Chair Jefferson made comments that suggested he was in favor of pausing the fed rate hikes.

Interest rate traders have taken that to mean that the Fed rate hikes could be over, and the next move might be lower.

Per the CME FedWatch Tool, that cut could come by the June meeting, based on the current odds.

Though if the situation worsens in the Middle East, cuts could materialize even earlier in 2024.

As it stands now, another rate hike looks exceedingly unlikely, while a rate cut appears to be coming sooner-than-expected.

Now it’s important to note that the Fed doesn’t control mortgage rates, but their long-term outlook can have an effect on mortgage rates.

Fed Clarity Can Lower Bond Yields and Narrow the Spread

Additionally, more clarity from the Fed could go a long way in fixing the spread between 10-year bond yields and mortgage rates.

It’s currently about double its usual amount, at around 300 bps vs. 170. Knowing the Fed’s position on monetary policy could normalize spreads.

If we assume the 10-year bond yield settles in at current levels of say 4.50%, adding a more typical spread of 200 bps puts the 30-year fixed back to 6.50%.

That would spell relief for many prospective home buyers, who might be facing mortgage rates as high as 8% depending on their individual loan attributes.

Factor in paying mortgage points at closing, and it’s possible home buyers could obtain mortgage rates back in the high-5% range.

That would likely be good enough for now to get transactions flowing again, and potentially unlock some existing homeowners trapped by so-called mortgage rate lock-in.

Just beware that the trend has not been friendly to mortgage rates for a long time, and things can easily reverse course again depending on what transpires.

While it might signal a turning point, mortgage rates can also remain stubborn at these levels without significant economic data pointing to lower inflation.

And tomorrow’s CPI report alone could completely reverse the big move lower over the past couple days.

So while we’ve gotten some relief over the past few days, this so-called mortgage rate plunge may easily unwind if more hot economic data comes in. Or if global tensions ease.

The other day I wrote about how adjustable-rate mortgages might soon make a comeback, given how high fixed mortgage rates have become.

Now that the popular 30-year fixed is priced in the 7-8% range, some home buyers might be looking at alternative products.

This may include the 5-year or 7-year ARM, both of which provide a fixed interest rate for a lengthy period of time before becoming adjustable.

Given how much mortgage rates have increased in such a short time span, these could be viewed as short-term solutions until a refinance makes sense again in the future.

But if for whatever reason you keep your ARM once it becomes adjustable, it’s important to understand how it works.

Adjustable-Rate Mortgage Caps Limit Rate Movement

Today we’re going to talk about caps on adjustable-rate mortgages, which limit how much the rate can move once it becomes a variable rate loan.

As noted, many ARMs are hybrids, which means they offer a fixed-rate period initially before becoming adjustable.

Two of the most popular ARM option are the 5/1 (or 5/6 ARM) and the 7/1 (or 7/6 ARM).

They are fixed for 60 months and 84 months, respectively, before becoming adjustable for the remainder of the loan term.

That loan term is the usual 30 years, so there are still 23-25 years left once it becomes adjustable.

If there’s a 1 after the 5 or 7, it means the loan is annually adjustable. So it can adjust just once per year.

If there’s a 6 after the 5 or 7, it means it can adjust semi-annually. So two adjustments per year.

Once an adjustable-rate mortgage becomes variable, the initial rate is replaced by the fully-indexed rate, which is a combination of a fixed margin and variable mortgage index.

For example, an ARM might feature a margin of 2.25% and be tied to the SOFR, currently priced at say 5.25%. Combined, that would result in a rate of 7.50%.

While a rate adjustment is probably the most frightening aspect of an ARM, note that there are “caps” in place that restrict rate movement.

The purpose of these rate caps is to limit interest rate increases as a means of avoiding payment shock.

So even if the associated mortgage index tied to the ARM skyrockets, the homeowner won’t see their monthly payment become unsustainable.

Of course, these caps can still allow for a big payment increase, so they’re more a buffer than a full-on solution.

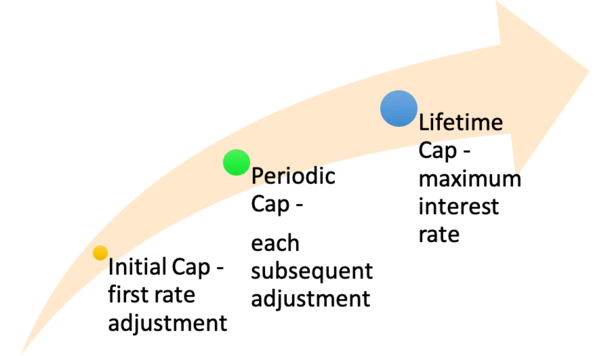

There Are Three Types of Caps on Adjustable-Rate Mortgages

Now let’s discuss the different types of caps featured on ARMs, as there are three to take note of.

There is the initial cap, which limits how much the rate can go up (or down) at first adjustment.

There is the periodic cap, which limits how much the rate can go up (or down) at subsequent adjustments.

And there is the lifetime cap, which limits the total amount the rate can go up (or down) during the entire loan term.

For the record, the lifetime cap may also be referred to as the “maximum interest rate,” which is how high an adjustable-rate mortgage can go.

And the “minimum interest rate” is how low an adjustable-rate mortgage can go, which will often either be the margin or the start rate.

So an ARM loan with an initial rate of 4.5% might have a minimum rate of 4.5% as well, or it might have a minimum rate set to the margin, which could be as low as 2.25%.

As for the maximum, it might be 5% higher than the initial rate. So if the initial rate was 4.5%, it could go as high as 9.5%. Ouch!

But both the initial and periodic caps would apply as well, which could limit the speed at which the rate climbs to those levels.

For example, if the caps were 2/2/5, which is common, the rate could only go to 6.5% after the first 60 or 84 months.

And then it could adjust to 8.5% six months or a year later, depending on if its annually or semi-annually adjustable.

That could effectively slow down the rate increases if the associated mortgage index was surging, as they have been lately.

Of course, it can work against you too if the indexes are falling, limiting rate improvement by the same measure.

Check Your Disclosures to See What the Caps Are On Your ARM

If you elect to take out an ARM instead of a fixed-rate mortgage, it’s imperative to know what your interest rate caps are (and also what index the loan is tied to).

Fortunately, this information is readily available on both the Loan Estimate (LE) and the Closing Disclosure (CD).

It will tell you whether your interest rate can increase after closing, and if so, by how much.

You’ll see the maximum mortgage rate possible, along with the maximum principal and interest (P&I) payment listed.

The year in which the rate can adjust to those levels will also be displayed for your convenience.

A more in-depth “Adjustable Interest Rate Table,” known as the AIR Table, can be found on page 2 of the LE and page 4 of the CD.

As seen in the image above, you’ll find the index, the margin, and the caps, including first change, subsequent change, and the change frequency.

All the details you need to determine how your ARM may adjust will be in that table. This way there are no surprises if and when your ARM becomes adjustable.

Remember, it’s also possible to refinance your mortgage before it becomes adjustable, given these ARMs are often fixed for five to seven years.

So you’ve got time to watch mortgage rates and jump on an opportunity if one comes along while the initial interest rate remains fixed.

This gives you options if you’re hoping for mortgage rates to come down. Just be aware that there’s no guarantee rates will improve and you’ll still need to qualify for a refinance in the future.

This is why the date the rate, marry the house strategy can backfire if the stars don’t quite align.

Still, with ARMs beginning to price a lot lower than the 30-year fixed, they could be worth looking into finally.

Just take the time to educate yourself first before you dive in as they are a bit more complicated than your plain old 30-year fixed mortgage.

In July 2021 alone, more than 700,000 new home sales were processed. While that sounds like a lot, the number is lower compared to 2020, due in part to a housing shortage. Pair that shortage with plenty of people looking to make a home purchase and you have a competitive market in 2021 and beyond.

You might think that these are just numbers—but understanding the housing market is pivotal to the mortgage approval process. If you’re considering buying a home, we’re here to guide you through the mortgage process. Get ready to be set up for success.

In This Piece

Understand Your Credit History and Score

The home loan approval process includes a pretty thorough credit check. While you might be able to get approved for an FHA mortgage loan with a credit score as low as 500, most traditional mortgage loans require at least a 620 or higher.

While your credit score might make or break you at the beginning of a mortgage application process, once you continue the process, your entire credit history becomes important. Mortgage lenders look at issues such as delinquencies or open collections accounts on your credit history. They may also require that you make good on any open collections accounts before your mortgage approval can go through.

It’s a good idea to understand your credit history and score months before you plan to apply for a home loan. That way, you have time to resolve any issues or dispute inaccurate negative information that could be dragging your score down.

You can get a free credit report from each of the major credit bureaus at AnnualCreditReport.com. You can also sign up for services such as ExtraCredit to get ongoing access to your credit reports and scores. ExtraCredit also includes features such as Build It that help you work on building your credit so you have a better chance at getting the mortgage loan—and rates—you want in the future.

Get matched with a personal

loan that’s right for you today.

Learn

more

Prepare Your Personal Finances for the Home-Buying Process

Your credit isn’t the only financial factor that impacts your mortgage application process. Yes, your history of on-time payments to other creditors is important. But so is your ability to make payments on the mortgage loan in the future. Lenders are likely to be concerned with:

Your debt-to-income ratio, or DTI. This is how much of your income you need each month to pay your existing debts. The lower this figure is, the better. According to the Consumer Financial Protection Bureau, most mortgage lenders won’t approve home loans that bring a consumer above 43% DTI.

Your income. In most cases, you’ll need to demonstrate that you have the income or other financial means to make your monthly mortgage payments. Your income can impact how much you can get approved for or whether you’re approved at all.

Your cash savings or other assets. If you need to make a down payment on your mortgage loan, you may need to demonstrate where that cash came from. You can get creative with sourcing your down payment within some rules, but you can’t always borrow it. And you can’t have cash show up in your account suddenly in the middle of your mortgage approval process without an explanation.

Understanding what mortgage lenders look at when considering you for a home loan could proactively help your case. Start early and work on reducing debt, increasing income and saving money for your down payment.

Decide What Mortgage You Can Afford

When you’re close to ready to start looking for a house and applying for a mortgage, take time to get an idea of how much mortgage you can actually afford. Start by taking a look at your budget—or create one if you don’t already have one.

Try to factor in expenses related to a new home, including savings for emergency repairs or maintenance. Once you know how much of a monthly payment you can afford, use an online mortgage calculator to test various loan and interest amounts. This helps you figure out your limits for home price, so you look for properties you can afford.

Research Potential Mortgage Options

Armed with knowledge about your budget, your credit and your overall financial status, hopefully you’re ready to do some research. Don’t apply yet—you want to apply for mortgages when you’re ready to make an offer on a home.

In the meantime, do some research. Talk to your bank, and maybe even reach out to a mortgage broker. That way, you’ll know your options and what you might qualify for.

Gather Documents to Apply for a Mortgage

During your research, make notes about what documents and items a mortgage lender requires for the application. Gather those documents and information before you apply for preapproval or a mortgage. You’ll save major time and hassle during the home loan approval process.

Some items you might need include:

Identification, such as a driver’s license or other government-issued ID.

Documentation of your income, such as paycheck stubs, W2 forms or tax returns.

Documentation of assets, especially assets like savings or investment accounts that might be involved in sourcing your down payment.

Your Social Security number for the credit check.

Documents showing you paid or settled any collections accounts or other negative issues on your credit report.

You may be asked for other items or documents throughout the mortgage underwriting process. When you apply for a mortgage make sure you’re available via email or phone, in case lenders have extra questions for you.

Consider Getting Pre-approved for a Mortgage

Getting pre-approved for a mortgage can be a good step. Preapproval doesn’t mean you’ve successfully completed the entire mortgage approval process. However, it does mean the lender did a cursory review of your credit history and score—as well as any income information you reported—and is fairly comfortable saying you’ll be approved with a certainrate.

Preapproval letters let you shop more confidently for a home. They also help demonstrate to sellers that you’re serious about your offer and will probably follow through without financial hiccups. In a competitive market with numerous offers on each home, this can make your offer more attractive to some sellers.

Apply for Mortgages Within a Short Period of Time

Finally, once you’re ready to purchase a home, ensure you apply for mortgages within a short period of time. Each time you apply for a loan, your credit is hit with a hard inquiry—which will bring your score down a bit. But the credit scoring models treat multiple mortgage applications within a short period of time as a single hard inquiry, because it’s assumed you may want to shop around for a good deal.

You should also be ready for the prospect of being approved with conditions. This means the mortgage lender will approve your loan as long as you meet certain conditions, which could include:

Providing supplemental documentation of credit history or income.

Satisfying the lender’s requirements for copies of banking statements or other documents.

Explaining an inconsistency or issue on your credit report.

Settling an old collections account or other debt.

Verifying where funds for a down payment came from.

Start Your Mortgage Application Process Today

Ultimately, being successful with the home loan application process comes down to being prepared and in good financial standing—or as in as good financial standing as you can. If you’ve gone through the above steps and are ready to apply for a mortgage, consider shopping for rates today.

When you’re considering starting home shopping, it’s important to put yourself in the best possible position. To do this, you’ll want to shore up your finances and increase your credit score. Follow these simple steps to get you closer to your homebuying dream.

Improving Credit for Future Homebuyers

1. Check Your Credit Score

Your credit score will be one of the main considerations in your mortgage application, so check yours to see what needs the most work. A credit score is based on a number of factors: payment history, credit usage, types of credit, age of credit, and recent inquiries. Though you can’t impact all of these in a short period of time, you can take steps to improve in some areas.

Make sure you’re paying all of your bills on time, as on-time payments have a huge impact on your score. Don’t apply for new lines of credit, but you can request a credit limit increase to current credit lines to improve your usage percentage. If you see any errors on your credit report, dispute them so that errors can be removed or corrected, and target credit usage when you make your budget.

2. Assess Your Finances

To know what you have to do to buy the home of your dreams, you need to know where you stand. Write down everything you have coming in and going out each month first. Some of these expenses, such as your car and student loan payments, stay the same over time and will come with you to your new home. Others are variable and change from month to month, including how often you eat out and your entertainment expenses, and these expenditures can most likely be shaved down or eliminated entirely with a budget.

Because homebuying comes with many expenses–a down payment, inspection fees, closing costs–your budget should be tighter in the period before you buy than normal. You’ll also want to budget for a home warranty; see if a home warranty is worth the money. When developing your budget, focus on eliminating your high-interest debt and saving for those homebuying expenses.

Lenders will also look at your debt-to-income ratio or DTI which is the amount of money you have coming in each month versus the expenses you have. Though it varies between lenders, many lenders will not give a mortgage to someone whose DTI is higher than 43%.

Get matched with a personal

loan that’s right for you today.

Learn

more

3. Understand Homebuying Costs

For nearly every type of mortgage, a down payment is required. A down payment of no less than 20% is suggested to have better home options and lower monthly costs. Conventional loans allow 20%, however, you can also have a down payment of as little as 3%; for down payments below 20%, PMI (private mortgage insurance) is required. Other types of loans, like an FHA loan, require between a 3.5-10% down payment, depending on your credit score. Make sure you understand how much you’ll be spending on your new home by using a mortgage calculator.

Other homebuying fees can add up quickly and be more variable. You will likely have a loan origination fee, inspection fee, appraisal fees, and other fees. You may be able to control some of these by choosing your own professionals. However, others will be selected by the seller, real estate office, or mortgage company.

A brokerage commission may be paid to real estate agents on closing. Your home warranty, property insurance and taxes, and any points you wished to pay to lower your mortgage rate as well as current interest rates will all go into your final costs. Account for all of these expenses when deciding how much mortgage you can afford.

Take steps to improve your creditworthiness and your DTI, and know what you’re looking for when you begin shopping for a lender to work with so you get the best rate possible. With the right moves, you’ll be closing on your dream home in no time.

Proposed legislation that would allow bankruptcy judges to modify the terms of mortgages on primary residences could reduce foreclosures by 20 percent, according to a report from Credit Suisse.

The investment bank’s analysts believe that if such legislation were to become law, it would prompt banks and lenders to step up loan modification efforts.

“We expect the new bankruptcy reform will increase loan mods, particularly principal reduction mods, as it is likely to both pressure and also give justification to servicers to more actively pursue principal reduction mods,” said a report from Credit Suisse Fixed Income Research.

Of course, true foreclosure prevention depends on how much mortgage lenders are willing to budge, considering many borrowers are well underwater, even with a sizable principal reduction factored in.

It’s hard to believe many borrowers will stick around unless they have at least some amount of home equity, and with prices continuing to slide, that task is becoming increasingly difficult.

By the way, the average foreclosure in California now has $180,000 in negative equity.

Opponents of a so-called mortgage cram down, such as the Mortgage Bankers Association, believe it will lead to interest rates one-and-a-half to two points higher, making homeownership that much less affordable.

They also believe it would make it more difficult to accurately appraise property values, and lead to higher down payment requirements and closing costs.

Second mortgage holders would also likely see their positions disappear in the event of a bankruptcy proceeding, spelling trouble for these types of lenders and investors.

But sentiment has shifted in recent months, with the National Association of Home Builders even pulling a 180 in support of such a bill in their latest bid to stem foreclosures and buoy home prices.

Currently, bankruptcy judges are allowed to modify the terms of second homes and even yachts.

US mortgage rates jumped this week, climbing closer to 7%. The move follows last week’s rate hike from the Federal Reserve, and the downgrade this week by Fitch Ratings agency of US sovereign debt, and of Freddie Mac and Fannie Mae.

The 30-year fixed-rate mortgage averaged 6.90% in the week ending on August 3, up from 6.81% the week before, according to data from Freddie Mac released Thursday. A year ago, the 30-year fixed-rate was 4.99%, the lowest rates have been in the last 12 months.

“The combination of upbeat economic data and the U.S. government credit rating downgrade caused mortgage rates to rise this week,” said Sam Khater, Freddie Mac’s chief economist. “Despite higher rates and lower purchase demand, home prices have increased due to very low unsold inventory.”

The average mortgage rate is based on mortgage applications that Freddie Mac receives from thousands of lenders across the country. The survey includes only borrowers who put 20% down and have excellent credit.

Next up: Employment and inflation data

The fixed rate for a 30-year mortgage continued to close in on 7% this week as 10-year Treasury yields climbed past the 4% threshold, said Hannah Jones, economic data analyst at Realtor.com.

“On Wednesday, the US Treasury announced it would sell off more than $100 billion of long-term securities, driving 10-year Treasury yields to the highest level since November,” said Jones. “This development, along with upcoming employment and inflation data, will determine how much mortgage rates may rise in the short term.”

Should employment and inflation pick up steam, she said, mortgage rates are likely to continue climbing as markets anticipate further monetary tightening.

Last week, the Fed raised its benchmark lending rate by a quarter point, as expected.

“The committee’s statement emphasized that incoming economic data will guide future rate hike choices,” Jones said. “Home buyers continue to feel the effects of tighter policy, which keeps a floor under mortgage rates.”

While the Fed does not set the interest rates that borrowers pay on mortgages directly, its actions influence them. Mortgage rates tend to track the yield on 10-year US Treasuries, which move based on a combination of anticipation about the Fed’s actions, what the Fed actually does and investors’ reactions. When Treasury yields go up, so do mortgage rates; when they go down, mortgage rates tend to follow.

Inventory remains a challenge

Home inventory remains tight, further hampering affordability. Existing home sales and sales of newly constructed homes were down in June as higher rates have been keeping inventory low and prices higher.

“Still-high home prices and elevated mortgage rates have eaten into purchasing power for many buyers, leading to both fewer home sales and fewer listings,” said Jones. “Today’s housing market is grappling with low for-sale inventory amid sustained, though historically low, buyer demand.”

Active inventory fell compared to the previous year each week in July, according to Realtor.com. Many homeowners held off on listing their home for sale, largely in response to today’s high mortgage rates, Jones said.

“The drop in for-sale inventory was met with the typical seasonal pickup in buyer demand, despite affordability constraints, which propped up home prices,” she said.

Homeowner vacancy fell to a historical low of 0.7% in the second quarter of 2023, Jones said, as many homeowners stayed put and home shoppers snapped up available inventory, leaving fewer homes vacant.

“The housing market continues to face more than a decade of underbuilding, and the resulting gap in home supply is being exacerbated by the lower level of existing homes for sale,” she said.

Freddie Mac’s Primary Mortgage Market Survey, which focuses on conventional and conforming loans with a 20% down payment, shows the 30-year fixed rate averaged 6.90% as of August 3, up from last week’s 6.81%. By contrast, the 30-year fixed-rate mortgage was at 4.99% a year ago at this time. The 15-year fixed-rate mortgage also rose this week to 6.25%, up 14 basis points from the prior week.

“The combination of upbeat economic data and the U.S. government credit rating downgrade caused mortgage rates to rise this week,” said Sam Khater, Freddie Mac’s chief economist. “Despite higher rates and lower purchase demand, home prices have increased due to very low unsold inventory.”

The sudden hike of the 10-year Treasury, along with upcoming employment and inflation data, will influence how much mortgage rates may rise in the short term, economists say. If employment and inflation pick up steam, mortgage rates are likely to continue climbing as markets prepare for further monetary tightening, said Realtor.com Economic Data Analyst Hannah Jones. On the bright side, the prospect of a recession is dimming for the next six to 12 months.

Other mortgage rate indices showed mixed results on Thursday morning:

HousingWire’s Mortgage Rates Center showed Optimal Blue’s 30-year fixed rate for conventional loans at 7.02% on Wednesday, compared to 6.85% the previous week. At Mortgage News Daily on Thursday morning, the 30-year fixed rate for conventional loans was at 7.20%, up 25 basis points from the previous week.

The economy remains on firm footing

Regarding the housing market, new economic data further solidify the view that the economy remains on firm footing, highlighted George Ratiu, chief economist at Keeping Current Matters.

“Construction spending advanced in June, a sign that companies and the government continue investing in real estate and infrastructure projects. Meanwhile, the number of open jobs retreated slightly, but remained above 9 million, while the number of workers leaving their positions for better ones remained elevated. Many companies still deal with a shortage of labor, as evidenced by the private payroll data which outpaced market expectations,” said Ratiu in a statement.

Look for payroll employment data tomorrow

“Tomorrow’s government report on payroll employment will add another data point to the bigger picture, with economists looking for changes in the unemployment rate and wage figures,” he added.

Meanwhile, active inventory fell compared to the previous year each week in July as many homeowners held off on listing their home for sale, noted Realtor.com Economist Jones.

“The drop in for-sale inventory was met with the typical seasonal pick-up in buyer demand, despite affordability constraints, which propped up home prices. In the second quarter of 2023, homeowner vacancy fell to a historical low of 0.7% as many homeowners stayed put and home shoppers snapped up available inventory, leaving fewer homes vacant,” she said.

This gap between supply and demand, exacerbated by a decade of under building, pushes prices up. Consequently, it also brings back market competition, especially in more affordable metro areas. Scarce inventory leads to a modest pace of sales for existing homes. On the new home front, growing options and more approachable prices have led to a pickup in sales transactions.

Lastly, Ratiu added that mortgage rates are expected to remain elevated for the next couple of months, keeping pressure on affordability.

“For buyers who are not in a hurry, the fall and winter months could bring better values and a less competitive environment to find the right home,” Ratiu concluded.

Our experts answer readers’ home-buying questions and write unbiased product reviews (here’s how we assess mortgages). In some cases, we receive a commission from our partners; however, our opinions are our own.

Mortgage rates increased last week and remain high today. High rates have strained affordability for those who are trying to purchase a home during the peak homebuying season. But some relief may be on the way for those who wait to buy later in the season.

In its latest mortgage forecast, the Mortgage Bankers Association predicted that 30-year mortgage rates will finally drop below 6% by the end of 2023. Looking further ahead, the MBA thinks rates could reach 4.8% by the end of 2024 and 4.5% by the end of 2025.

Today’s Mortgage Rates

Mortgage type

Average rate today

This information has been provided by

Zillow. See more

mortgage rates on Zillow

Real Estate on Zillow

Today’s Refinance Rates

Mortgage type

Average rate today

This information has been provided by

Zillow. See more

mortgage rates on Zillow

Real Estate on Zillow

Mortgage Calculator

Use our free mortgage calculator to see how today’s mortgage rates will affect your monthly and long-term payments.

Mortgage Calculator

$1,161 Your estimated monthly payment

Total paid$418,177

Principal paid$275,520

Interest paid$42,657

Paying a 25% higher down payment would save you $8,916.08 on interest charges

Lowering the interest rate by 1% would save you $51,562.03

Paying an additional $500 each month would reduce the loan length by 146 months

By plugging in different term lengths and interest rates, you’ll see how your monthly payment could change.

Mortgage Rate Projection for 2023

Mortgage rates started ticking up from historic lows in the second half of 2021 and increased over three percentage points in 2022.

But many forecasts expect rates to fall later this year. In their latest forecast, Fannie Mae researchers predicted that 30-year fixed rates will trend down throughout 2023 and 2024.

But whether mortgage rates will drop in 2023 hinges on if the Federal Reserve can get inflation under control.

In the last 12 months, the Consumer Price Index rose by 4.9%. Inflation has continued to slow for several months now, which is a sign that the Fed’s efforts are working.

For homeowners looking to leverage their home’s value to cover a big purchase — such as a home renovation — a home equity line of credit (HELOC) may be a good option while we wait for mortgage rates to ease. Check out some of our best HELOC lenders to start your search for the right loan for you.

A HELOC is a line of credit that lets you borrow against the equity in your home. It works similarly to a credit card in that you borrow what you need rather than getting the full amount you’re borrowing in a lump sum. It also lets you tap into the money you have in your home without replacing your entire mortgage, like you’d do with a cash-out refinance.

Current HELOC rates are relatively low compared to other loan options, including credit cards and personal loans.

When Will House Prices Come Down?

Home prices declined a bit on a monthly basis late last year, but we aren’t likely to see huge drops this year, even if there’s a recession.

Fannie Mae researchers expect prices to decline 1.2% in 2023, while the Mortgage Bankers Association expects a 0.6% decrease in 2023 and a 1.4% decrease in 2024.

Sky high mortgage rates have pushed many hopeful buyers out of the market, slowing homebuying demand and putting downward pressure on home prices. But rates may start to drop this year, which would remove some of that pressure. The current supply of homes is also historically low, which will likely keep prices from dropping too far.

What Happens to House Prices in a Recession?

House prices usually drop during a recession, but not always. When it does happen, it’s generally because fewer people can afford to purchase homes, and the low demand forces sellers to lower their prices.

How Much Mortgage Can I Afford?

A mortgage calculator can help you determine how much you can afford to borrow. Play around with different home prices and down payment amounts to see how much your monthly payment could be, and think about how that fits in with your overall budget.

Typically, experts recommend spending no more than 28% of your gross monthly income on housing expenses. This means your entire monthly mortgage payment, including taxes and insurance, shouldn’t exceed 28% of your pre-tax monthly income.

The lower your rate, the more you’ll be able to borrow, so shop around and get preapproved with multiple mortgage lenders to see who can offer you the best rate. But remember not to borrow more than what your budget can comfortably handle.

Inside: This guide will teach you about the different factors you need to consider when purchasing a home with a 70k salary.

There are a lot of factors to consider when you’re trying to figure out how much house you can afford. Your income, your debts, your down payment, and the interest rate on your mortgage all play a role in determining how much house you can afford.

Your situation will be different than the person next-door or your co-coworker.

Making 70000 a year is a great salary. You are making the median salary in the United States.

It’s enough to comfortably afford most homes and gives you plenty of room to save money each month.

But how much house can you actually afford?

It depends on several factors, including your down payment, interest rate, income, and credit score.

In this ultimate guide, we’ll walk you through everything you need to know about how much house you can afford making 70000 a year.

how much house can i afford on 70k

In general, you can expect to spend 28-36% of your income on housing.

Generally speaking, if you make $70,000 a year, you can afford a house between $226,000 and $380,000.

How much mortgage on 70k salary?

In general, you should expect to spend no more than 28% of your monthly income on a mortgage payment.

Thus, you can spend approximately$1633-2100 a month on a mortgage.

Just remember this is relative to the interest rate, term length of the loan, down payment, and other factors.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

28/36 Rule

But there’s one factor that trumps all the others: The 28/36 rule.

Also known as the debt-to-income (DTI) ratio.

The 28/36 rule is a guideline that says that your housing costs (mortgage payments, property taxes, homeowners insurance, and HOA fees) should not exceed 28% of your gross monthly income.

And your total debt (housing costs plus any other debts you have, like car payments or credit card bills) should not exceed 36% of your gross monthly income.

You must follow the 28/36 rule.

How to calculate how much mortgage you can afford?

If you’re like most people, you probably don’t know how to calculate how much mortgage you can afford.

This is actually a really important question that you need to ask yourself before beginning the home-buying process.

The answer will help determine the price range of homes you should be looking at. Plus know how much money you’ll need to save for a down payment.

Step #1: Check Interest Rates

Research current mortgage rates to get an accurate estimate. You can also check your credit score and search for average mortgage rates based on your credit score.

Right now, with sky-high inflation, you are unable to afford a bigger house when interest rates are hovering around 6% compared to ultra-low interest rates of 2.5%.

With a 70k salary, this can be the difference between $50-100k on the total mortgage amount you can afford.

Step #2: Use a Mortgage Calculator

Use a mortgage calculator to get an estimate of the home price you can afford based on your income, debt profile, and down payment.

Generally, lenders cap the maximum amount of monthly gross income you can use toward the loan’s principal and interest payment to not more than 28% of your gross monthly income (called the “Front-End” or “Housing Expense” ratio). Then, limit your total allowable debt-to-income ratio (called the “Back-End” ratio) to not more than 36%.

You can use a mortgage calculator to a ballpark range of what house you can afford.

Step #3: Taxes, Insurance, and PMI

When planning for a home purchase, it’s important to factor in all of your monthly expenses, including taxes, insurance, and PMI.

This will ensure that you get an accurate estimate of your home-buying budget based on your household annual income.

Don’t forget to include these payments to get a realistic understanding of your monthly budget.

Step #4: Remember your Living Expenses

When considering how much house you can afford based on your $70,000 salary, you must consider your lifestyle and current expenses.

It is important to factor in other monthly expenses such as cell phone and internet bills, utilities, insurance costs, and other bills.

More than likely, you will be approved for a higher mortgage amount than you would feel comfortable with. This is 100% what lenders will do.

They want to provide you with the most you can afford – not what you should afford.

Step #5: Get prequalified

Prequalifying for a mortgage is an important first step to take when estimating how much house you can afford.

It gives you a more precise figure to work with and helps you make a more informed decision based on your personal situation.

Remember that your final amount will vary depending on a number of factors, especially your interest rate, which will be based on your credit score.

Taking the time to research current mortgage rates helps you secure a better mortgage rate, giving you more buying power.

Home Buying by Down Payment

How much house can you afford?

It’s a common question among home buyers — especially first-time home buyers. Use this table to figure out how much house you can reasonably afford given your salary and other monthly obligations.

The assumption is 30 year fixed mortgage, good credit (690-719), no monthly debt, and a 4% interest rate.

Annual Income

Downpayment

Monthly Payment

How Much House Can I Afford?

$70,000

$9,552 (3%)

$1,750

$318,412

$70,000

$16,215 (5%)

$1,750

$324,316

$70,000

$34,058 (10%)

$1,750

$340,581

$70,000

$53,573 (15%)

$1,750

$357,152

$70,000

$75,094 (20%)

$1,750

$375,468

$70,000

$98,933 (25%)

$1,750

$395,731

**Your own interest rate, monthly payment, and how much house you can afford will vary on your personal circumstances.

Mortgage on 70k Salary Based on Monthly Payment and Interest Rate

How much house can you afford on a $70,000 salary?

This largely depends on the current interest rate of the mortgage loan you’re considering. When interest rates are high, people aren’t actively buying as when interest rates are low.

By understanding these factors, you can better gauge how much house you can afford on a $70,000 salary.

The assumption is 30 year fixed mortgage, good credit (690-719), no monthly debt, and a 20% downpayment.

Annual Income

Monthly Payment

Interest Rate

How Much House Can I Afford?

$70,000

$1,750

3.25%

$406,796

$70,000

$1,750

3.5%

$396,231

$70,000

$1,750

3.75%

$386,101

$70,000

$1,750

4%

$375,994

$70,000

$1,750

4.5%

$357,554

$70,000

$1,750

5%

$339,954

**Your own interest rate, monthly payment, and how much house you can afford will vary on your personal circumstances.

Home Affordability Calculator by Debt-to-Income Ratio

Around here at Money Bliss, we always stress that debt will hold you back.

In the case of buying a house, debt increases your DTI ratio.

Here is a glimpse at what monthly debt can cause your debt-to-income (DTI) ratio to increase. Thus, making the house you want to buy to be more difficult.

Annual Income

Monthly Payment

Monthly Debt

How Much House Can I Afford?

$70,000

$2,100

$0

$440,085

$70,000

$1,900

$200

$404,584

$70,000

$1,800

$300

$382,334

$70,000

$1,600

$500

$337,883

$70,000

$1,350

$750

$282,208

$70,000

$1,100

$1000

$226,582

**Your own interest rate, monthly payment, and how much house you can afford will vary on your personal circumstances.

Increase your Home Buying Budget

Here are a few ways you can increase your home buying budget when buying a house on a $70k annual income.

By following these steps, you can increase your home buying budget and find a more suitable house for your income.

1. Pick a Cheaper Home

Home prices vary significantly in different parts of the country.

Moving out of a major metropolitan area with notoriously high housing costs can help you find more affordable homes.

There are plenty of ways to find a home that is cheaper than you would normally expect.

Look for homes that are for sale in less desirable neighborhoods.

Find homes that are for sale by owner or have not been listed yet.

Check for homes that are for sale outside of your usual price range and haven’t sold as they may drop their price.

Move to a lower cost of living area.

2. Increase Your Down Payment Savings

A larger down payment can reduce the amount you have to finance, which lowers your monthly payment.

Plus help you get a lower interest rate and avoid paying PMI.

Putting down at least 10-20 percent of the home sale price can help boost your home buying power. You can also take advantage of down payment assistance programs in your area.

3. Pay Down Your Existing Debt

Paying down your debts such as credit card debts or auto loans can help raise your maximum home loan.

Paying down your debts can help you qualify for a higher loan amount.

This is because when you have lower amounts of debt, your credit score is higher and your debt-to-income ratio is less. This means you are less likely to be rejected for a home loan.

4. Improve Your Credit Score

A higher credit score can lead to lower rates and more affordable payments.

You can improve your credit score by:

Paying your bills on time

Paying down your credit card balances

Avoiding opening new credit before applying for a mortgage

Disputing any errors on your credit report

This is very true! We had an unfortunate debt that wasn’t ours added to our credit report right before closing. While the debt was an error, it still cost us a higher interest rate and forced us to refinance once the credit report was fixed.

5. Increase Your Income

Asking for a raise, seeking a higher-paid position, or starting a side gig can help you increase the amount of home you can afford.

While you need two years of income from a side gig or your own online business to count as income, the extra cash earned helps you to increase the size of your downpayment. Plus it lowers your debt-to-income ratio with the savings you are setting aside.

What factors should you consider when deciding how much you can afford for a mortgage?

How much house can you afford on your current salary and with your current monthly debts?

This is a question that we are often asked, and it’s one that we love to answer.

We’ll walk you through all the different factors that go into this decision so that you can make an informed choice.

1. Loan amount

The loan amount is a key factor that affects the total cost of a mortgage.

If you have no outstanding debt, a 20% down payment, a high credit score, and a 3.5% interest rate from an FHA loan, you could be able to afford up to $508,000.

However, if you have debt, a smaller down payment, or a lower credit score, the loan amount you can qualify for will be lower.

Similarly, if you choose a 15-year fixed-rate loan, your monthly payments will be higher, but you will end up paying less in interest over the life of the loan than with a 30-year fixed-rate loan.

Ultimately, your loan amount will affect the total cost of your mortgage, so it’s important to consider all the factors when making your decision.

2. Mortgage Interest rate

Mortgage interest rates can have a significant impact on the cost of a mortgage. The higher the interest rate, the more expensive the loan will be.

For example, a difference between a 3% and 4% interest rate on a $300,000 mortgage is more than $150 on the monthly payment.

Remember, in the first few years of a mortgage, the majority of the payment goes toward interest rather than trying to reduce the principal amount.

3. Type of Mortgage

The primary difference between a fixed and variable mortgage is the interest rate and the amount of your payment

Fixed-rate mortgages offer the stability of having the same interest rate for the life of the loan.

Adjustable-rate mortgages (ARMs) come with lower interest rates to start, but those rates can change over the life of the loan. ARMs are often a riskier choice, as if the economy falters, the interest rate can go up.

Fixed-rate loans are typically the most popular choice, as the monthly payment amount is more predictable and easier to budget for. The terms of a fixed-rate loan can range from 10 to 30 years, depending on the lender.

Adjustable-rate mortgages (ARMs) have interest rates that can increase or decrease annually based on an index plus a margin. ARMs are typically more attractive to borrowers who plan on staying in the home for a shorter period of time, as the lower initial interest rate can make the payments more manageable.

The Money Bliss recommendation is to choose a 15-year fixed-rate mortgage.

4. Property value

Property value can have a direct effect on how much you can afford for a mortgage.

As the value of the property increases, so does the amount of money you will need to borrow to purchase it. This, in turn, affects the monthly payments and the amount of interest you will pay over the life of the loan.

This is especially important as many people have been priced out of the market with the rising home prices.

Additionally, higher property values can mean higher taxes, which will add to the amount you need to budget for your mortgage payments.

5. Homeowner insurance

Homeowner’s insurance is a requirement when securing a loan and it can vary depending on the value and location of the home.

Additionally, certain areas that are prone to natural disasters or are located in densely populated areas may have higher premiums than other locations and may require additional insurance like flood insurance.

As a result, lenders typically require that you purchase homeowners insurance in order to secure a loan, and may have specific requirements for the type or amount of coverage that you need to purchase.

Before committing to a mortgage, it is important to consider the cost of homeowner’s insurance and make sure it fits into your budget.

This is something you do not want to skimp on as the cost to replace a home is very expensive.

6. Property taxes

Property taxes are calculated based on the value of a home and the tax rate of the city or county where the property resides.

The higher the property taxes, the more you will have to pay in your monthly mortgage payment.

In states with high property taxes, the property tax bill can be a large sum of the mortgage payment.

It is important to consider these costs when comparing different homes and locations to ensure you can afford the home without stretching your budget too thin.

7. Home repairs and maintenance

It’s important to also consider other factors such as the age of the house, since some properties may require renovation and repairs that can cost more than the house price itself.

Beyond the cost of purchasing a home, homeowners will likely have other expenses related to owning and maintaining the property.

Also, many homeowners prefer to do significant upgrades to the home before moving in, which comes at an additional expense.

These can include ordinary expenses such as painting, taking care of a lawn, fixing appliances, and cleaning living spaces, which can add up.

Additionally, it’s advisable to buy a home that falls in the middle of your price range to ensure you have some extra money for unexpected costs, such as repairs and maintenance.

8. HOA or Homeowners Association Maintenance

This is often an overlooked factor by many new homebuyers, but extremely important as some HOAs add $500-800 per month to the total housing budget.

The purpose of a homeowners association (HOA) is to establish a set of rules and regulations for residents to follow as well as maintain the community or building.

These fees are typically used to pay for maintenance, amenities, landscaping, and concierge services.

HOA fees are used to finance community upkeep, including landscaping and joint space development, and can range from $100 to over $1,000 per month, depending on the amenities in the association.

9. Utility bills

When switching from renting to buying a home, you will have to factor in the costs of your monthly utility bills such as electricity, natural gas, water, garbage and recycling, cable TV, internet, and cell phone when calculating how much mortgage you can afford.

In addition, the larger the home, the higher the costs to heat and cool your new home.

Make sure to ask your realtor for previous utility bills on the property you are interested in.

10. Private Mortgage Insurance

The purpose of private mortgage insurance (PMI) is to protect the lender in the event of foreclosure. It is typically required when a borrower is unable to make a 20% down payment on a home purchase.

PMI allows borrowers to purchase a home with less upfront capital, but also comes with additional monthly costs that are added to the mortgage payment. These fees range from 0.5% to 2.5% of the loan’s value annually and are based on the amount of money put down.

PMI can also be canceled or refinanced once the borrower has achieved 20% equity in the home or when the outstanding loan amount reaches 80% of the home’s purchase price.

11. Moving costs

Moving is expensive, but also a pain to do. So, consider the moving costs associated with relocating from one location to another.

Typically fees for packing, transportation, and possibly storage, and can vary depending on the size of the move and the distance the move needs to cover.

Also, consider if by buying a home, you will stop having moving costs associated with moving from rental to rental.

FAQ

When determining how much house you can afford, it’s important to consider several factors.

These include your income, existing debts, interest rates, credit history, credit score, monthly debt, monthly expenses, utilities, groceries, down payment, loan options (such as FHA or VA loans), and location (which affects the interest rate and property tax). Also, think about the costs of maintaining or renovating a home.

Additionally, you should also evaluate your own budget and assess whether now is the right time to purchase a home. Taking all of these factors into account can help you set the maximum limit on what you can realistically afford.

A mortgage calculator can help you determine your home affordability by providing an estimate of the home price you can afford based on your income, debt profile, and down payment.

It works by inputting your annual income and estimated mortgage rate, which then calculates the maximum amount of money you’re able to spend on a house and the expected monthly payment.

Additionally, different methods are available to factor in your debt-to-income ratio or your proposed housing budget, allowing you to get a more accurate estimate of your home buying budget.

The debt-to-income ratio or DTI is used by lenders to assess a borrower’s ability to make mortgage payments.

This ratio is calculated by taking the total of all of a borrower’s monthly recurring debts (including mortgage payments) and dividing it by the borrower’s monthly pre-tax household income.

A high DTI ratio indicates that the borrower’s debt is high relative to income, and could reduce the amount of loan they are qualified to receive.

Generally, lenders prefer a DTI of 36% or less, which allows borrowers to qualify for better interest rates on their mortgages.

To calculate their DTI, borrowers should include debt such as credit card payments, car loans, student and other loans, along with housing expenses. It is important to note that the DTI does not include other monthly expenses such as groceries, gas, or current rent payments.

Closing costs can have an enormous impact on how much home you’re able to afford.

From application fees and down payments to attorney costs and credit report fees, these costs can add up quickly and affect your overall budget. Unfortunately, most of these closing costs are non-negotiable, but you can ask the seller to pay them.

When buying a house, it is important to research the different mortgage options available to you.

You can typically choose between a conventional loan that is guaranteed by a private lender or banking institution, or a government-backed loan. Depending on your monthly payment and down payment availability, you may be able to select between a 15-year or a 30-year loan.

A conventional loan typically offers better interest rates and payment flexibility.

While a government-backed loan may be more lenient with its credit and down payment requirements.

For veterans or first-time home buyers, there may be special mortgage options available to them.

Ultimately, it is important to talk to a lender to see which loan type is best for your personal circumstances.

When it comes to saving for a down payment, it’s important to understand how much you’ll need and how much it will affect your budget.

Generally, you’ll need 20% of the cost of the home for a conventional mortgage and 25% for an investment property. When you put down more money, it gives you more buying power and may help you negotiate a lower interest rate.

For example, if you’re buying a $300,000 house, you’ll need a down payment of $60,000 for a conventional mortgage. On the other hand, if you put down 10%, you can still afford a $395,557 house. But, you will have to pay for private mortgage insurance.

In addition, there are other ways to help you cover these upfront costs. You can look into down payment assistance programs.

Ultimately, the size of your down payment will depend on your budget and financial goals. You should never deplete your savings account just to make a larger down payment. It’s important to factor in emergency funds and other expenses when deciding on the best option.

Eligibility requirements for loan lenders can vary, but in general, lenders are looking for borrowers with a good credit score, a reliable income, and a history of employment or income stability.

For most loan types, borrowers will need to show a history of two consecutive years of employment in order to qualify. However, lenders may be more flexible if the borrower is just beginning their career or if they are self-employed and do not have W2 forms and official pay stubs.

Income verification also needs to be done “on paper”, meaning that cash tips that do not appear on pay stubs or W2s can not be used as income. The lender will look at the household’s average pre-tax income over a two-year period before determining the amount that can be borrowed.

In order to make sure that the borrower is financially secure, lenders will also pull the borrower’s credit report and base their pre-approval on the credit score and debt-to-income ratio. Employment verification may also be done.

For certain government-backed loan types, such as FHA, VA, and USDA loans, there may be additional or different requirements for eligibility. For instance, for FHA loans, the borrower must intend to use the home as a primary residence and live in it within two months after closing. VA loans are more lenient, and may not require a down payment.

The qualifications for VA loans vary based on the period and amount of time the borrower has served. There are many ways to qualify, whether the borrower is a veteran, active duty service member, reservist, or member of the National Guard. For more information on eligibility requirements for VA loans, borrowers can visit the U.S. Department of Veteran Affairs.

A good credit score will mean you have access to more lending options, better interest rates, and more purchasing power.

On the other hand, a poor credit score could mean you are approved for a loan, but at a higher interest rate and with a smaller house.

This means your budget will be more limited and you may not be able to buy as much home as you had hoped for. Additionally, lenders will also look at other factors, such as your debt-to-income ratio, employment history, and loan term, in order to determine your overall affordability.

What House Can I Afford on 70k a year?

As a borrower, you need to consider the interest rate, down payment, credit score, debt-to-income ratio, employment history, and loan term when determining how much house you can afford.

A higher credit score can often mean a lower interest rate, and a larger down payment can bring down the monthly payments.

All of these factors can have an effect on the amount of money you can borrow and the home you can afford.

Ultimately, understanding the impact of different factors can help borrowers make the best decisions when it comes to getting a mortgage.

Now that you know how much house you can afford, it’s time to start saving for a down payment.

The sooner you start saving, the sooner you’ll be able to move into your dream home. But you may have to wait if you are considering a mansion.

By taking into consideration this guide into account, you can make a more informed decision about the cost of a mortgage for your new home.

Know someone else that needs this, too? Then, please share!!