I’ve already written about it not being the best time to buy a home right now, at least from a pure investment standpoint.

In short, home prices are expensive relative to incomes, mortgage rates have more than doubled, and there’s little quality inventory.

And now we can quantify just how long it takes to break even on a house, per a new analysis from Zillow.

Hint: it’s a long, long time, even if you’re able to muster a big 20% down payment.

So if you’re thinking about buying a home today, prepare to stick around for the long-haul.

How Long to Break Even on a House These Days?

– 3% down payment: 13 years and six months to make a profit. – 5% down payment: 13 years and three months to make a profit. – 10% down payment: 12 years and seven months to make a profit. – 20% down payment: 11 years and three months to make a profit.

A new Zillow analysis tried to determine how long you’d need to own your home before you could sell it for a profit.

This factors in the closing costs associated with the home purchase, the mortgage interest paid, home maintenance costs, and the sales costs once it came time to list the property.

Specifically, they assume 3% closing costs at purchase, 1% home maintenance fees, and 6% in closing costs at the time of sale, along with all that mortgage interest.

In reality, it could be even higher. It’s not unusual for real estate agents to charge 5-6% of the sales price.

So if you’re putting down just 3%, you’re already in the hole, especially once you consider those closing costs as well.

To offset all those expenses, you need to make regular payments to principal each month and hope the property appreciates in value over the years as well.

The rule of thumb says it normally takes about 3-7 years to break even on a home purchase, with perhaps five years the average.

But that number has risen sharply lately thanks to a combination of sky-high asking prices and equally expensive mortgage rates.

How long you ask? Per Zillow, home buyers today can expect to spend approximately 13.5 years in their house before being able to sell at a profit!

In other words, you better really like your house unless you want to sell for a loss, or worse, be forced to do a short sale.

It Takes More Time to Turn a Profit in Affordable Housing Markets

And here’s the irony. It actually takes longer to turn a profit in more affordable housing markets.

Those purchasing a home in places like Cleveland, Baton Rouge, El Paso, Akron, or Indianapolis might need to wait at least 20 years to reach this crucial profit point.

As for why, it’s because of the slower historical growth rate in these more affordable areas.

Without home price appreciation doing most of the heavy lifting, it takes a lot more time to build home equity.

Simply put, principal payments are a lot less impactful than increases in property values, especially on a high-rate mortgage where most of the payment goes toward interest.

It’s the worst in Cleveland, where Zillow says it can take a whopping 22 years and 10 months to turn a profit.

Similar timelines can be seen in the other metros mentioned, meaning it’s not always advisable to buy a home just because it’s cheap.

There’s a Faster Road to Profit in Expensive Housing Markets

Again, while seemingly counterintuitive, it’s actually easier to turn a profit if you buy a home in an expensive metro.

Of course, the barrier to entry will likely be higher, but it’s one of those rich get richer stories.

For example, in notoriously expensive Bay Area metros such as San Jose or San Francisco, California, the break-even timeline to profit is a much shorter 7 to 7.5 years.

This is still a long time historically speaking, but it is considerably less than in those “cheap” housing markets.

Similar short purchase-to-sale profit timelines can be found in San Diego, Los Angeles, and Miami.

As you can see, these are highly-sought after cities where demand always tends to be strong, and supply always low. And because of that, home prices are often rising.

But there’s a big barrier to entry, whether it’s the high asking price or the large down payment required.

Either way, this data tells us it might not be the best time to purchase a home at the moment, even if you can muster a 20% down payment.

It could be advantageous to wait for a better combination of lower asking prices, cheaper mortgage rates, and better inventory.

Of course, there are reasons to buy a home other than for the investment. But you still need to be prepared to stick around for a while.

Read more: Pros and cons of renting vs. buying a home

Real estate across the country has certainly been crazy over the past three years, but the housing market in Ohio still looks pretty sane. This isn’t California or Massachusetts, and that’s a good thing for house-hunters: Homes in the Buckeye State are significantly more affordable than in many other states around the country, and prices here tend to be far below national levels. Read on for everything you need to know about the cost to buy a house in Ohio.

How much does it cost to buy a house in Ohio?

The average price of a home in Ohio was $275,461 as of September 2023, according to statistics from Ohio Realtors. That’s quite a bit lower than the nationwide median price for the same month, which was $394,300.

Depending on where you’re hoping to call home in the state, though, your budget may look a bit different. Consider the average sale prices in some of the most popular cities: In Cincinnati, the average was $319,310; in Columbus, $348,569; and in Dayton, $261,583.

Outside the bigger cities, you’ll find a smaller price point. For example, the average sale price was around $203,000 in Ashland and Athens, and less than $200,000 in both Mansfield and Lancaster.

It’s helpful to focus on how a home’s price tag will translate into your monthly payments as its owner, especially with today’s high mortgage rates. Consider the monthly obligation on a $275,000 home, assuming a 20 percent down payment on a 30-year mortgage with a 7.5 percent interest rate: According to Bankrate’s mortgage calculator, that scenario would result in principal and interest payments of $1,538 a month (not including the additional costs of property taxes and homeowners insurance).

Down payment

How much money have you saved for a down payment? This upfront cost is crucial, because the more you are able to pay upfront, the less you have to borrow.

You don’t have to put down 20 percent, necessarily, although that is the magic number to avoid paying an extra monthly premium for private mortgage insurance. Here are the minimum down payment requirements for some of the most popular types of home financing (if you qualify):

Conventional loans: 3 percent

FHA loans:5 percent with a credit score of at least 580, or 10 percent with a credit score between 500 and 579

VA loans: No down payment required for qualifying military service members or veterans

USDA loans: No down payment required if you buy a rural property that meets specific criteria

One piece of good news for first-time buyers: Ohio has some generous first-time homebuyer programs that can help you cover your down payment and closing costs. You’ll need to meet certain qualifications for credit score, income and purchase price to be eligible.

Closing costs

According to data from Core Logic’s ClosingCorp, closing costs in Ohio add on another 2 percent of the purchase price — approximately $5,500 on an average-priced $275,461 Ohio home. That amount isn’t all coming out of your pocket, though. Closing costs are split between buyers and sellers.

Costs that are the buyer’s responsibility will include a variety of fees charged by your lender for things like a credit check and loan origination, as well as a required appraisal of the home’s value. You’ll also want to get a home inspection to verify the home’s condition. Lenders typically like to see a cushion that will keep you protected in the event of an emergency, too, so make sure you set aside some extra cash in reserve.

Cost to move

Don’t forget about the additional expense of moving all your stuff to your new Ohio home. According to HomeAdvisor, the average cost of a local move is just over $1,700. If you’re moving long-distance to get to Ohio, though, you’ll need to set aside a lot more money. A cross-country move has an average price tag of $4,617.

Homeownership costs

Once you buy a house in Ohio, you’ll need to be prepared to pay for its upkeep. While there’s no crystal ball for home maintenance costs, State Farm advises homeowners to budget between 1 and 4 percent of their home’s value for annual upkeep. On an average-priced Ohio home, that means you should plan to set aside up to $11,018 each year for upkeep.

You’ll also need to plan for property tax costs. In Ohio, the typical homeowner paid $3,235 to the government in property taxes in 2022. And don’t forget to budget for your homeowners insurance coverage, too, as well as HOA fees if your new home is part of a homeowners association.

Reducing the costs to buy a house in Ohio

Buying a house can seem overwhelmingly challenging, especially with today’s high mortgage rates. Consider these options to reduce your costs:

Ask for seller concessions: Across the country, more sellers are agreeing to cover a portion of the buyer’s closing costs, according to a report by Redfin. Don’t hesitate to ask a seller if they’re willing to help out with some of your costs. They don’t have to say yes, but they also don’t want to see you walk away from the deal.

Cast a wide net: If you have a flexible work arrangement that doesn’t require you to be in one specific location, look at cheaper locations beyond where your job is based. And if you don’t need a huge amount of space, a condo or townhouse is a great way to achieve homeownership for a lower price than a single-family home.

Hold out for longer: It’s OK to press pause if you think now just isn’t the right time. Mortgage rates are the highest they have been in more than two decades. There’s no guarantee they’ll come down, but taking some time to build your savings and your credit score while you wait might not be a bad idea.

Next steps

While Ohio’s home prices are certainly more appealing than many other parts of the country, buying a house here is not necessarily easy. For example, Redfin data shows that the typical home in Columbus gets four offers, which shows that the Buckeye housing market can feel just as competitive as Big Ten football. With that in mind, make sure you have an experienced local real estate agent on your team.

FAQs

As of September 2023, the average sale price for a home in Ohio was $275,461, according to data from Ohio Realtors.

No, they are increasing. Between September 2022 and September 2023, the average sales price in the Buckeye State rose 5.9 percent, according to Ohio Realtors data.

Yes — buyers pay some portion of closing costs in every state, including Ohio. These typically include an array of fees charged by the mortgage lender, among others.

The cost to replace a chimney ranges from $1,000 to $15,000, depending on the type and size of the chimney. You can install a smaller or prefabricated chimney for $1,000 to $5,000, but a full masonry chimney replacement cost can reach $15,000.

Below, we’ll explain new chimney cost factors, break down labor and materials expenses, discuss financing options, and help you determine if you might be able to replace the chimney yourself.

Chimney Replacement Costs: An Overview

How much does a chimney replacement cost? Anywhere from $1,000 to $15,000. A full chimney replacement is on the higher end of that range while a partial replacement — or a basic prefab chimney installation — is on the lower end.

In some cases, it might be possible to repair the chimney instead of replacing it. Chimney repair costs typically range between $1,000 and $3,000, though it varies depending on the extent of the damage.

Recommended: The Ultimate Home Maintenance Checklist

Full Chimney Replacement

A full chimney replacement costs between $5,000 and $10,000 — or up to $15,000 in some cases. Prefabricated chimneys are the lowest-cost option. You’ll pay moderate prices for a metal chimney and the highest prices for a brick chimney.

Partial Chimney Replacement (Rebuild)

You may only need to replace part of a chimney, like the stack, which extends above the roof. In other cases, you may need to pay for the repair of specific elements, like collapsing mortar, a damaged chimney crown, or a cracked flue.

Partial chimney replacement costs may top out at $5,000 while repair typically ranges between $1,000 and $3,000 per job.

Recommended: Home Improvement Calculator

Chimney Installation Labor Cost

Labor makes up a large portion of the cost to replace a chimney. Depending on your geographic location, if you can reach the chimney by ladder or you need scaffolding, and the type of chimney being installed, labor rates may range from $50 to $150 an hour for an experienced mason.

You will usually need to hire a structural engineer before the mason can begin their work, which adds to your overall labor costs. Depending on where you live, that can cost around $500.

Chimney Installation Material Costs

Material costs vary depending on the type of chimney being replaced, rebuilt, or repaired. Prefab chimneys have lower material costs while masonry chimneys require more expensive materials like bricks and mortar.

Chimney Installation Cost Financing

Paying for a new chimney — or even a more basic chimney repair — can be difficult on a tight budget. If you don’t have the money in emergency savings, you can explore other options like:

• A payment plan with the contractor: Ask the contractor if they can set you up with a payment plan over a set number of months, rather than requiring the full payment all at once. Costs may be higher if you go this route.

• A credit card: Some contractors will let you pay with a credit card but be careful. Your credit card may have a high APR, and if you can’t afford to pay the full bill at the end of the month, you could end up paying a lot of interest, which will make the new chimney even more expensive.

• A home improvement loan: Home improvement loans are a low-cost option for homeowners. These personal loans typically have a lower interest rate than your credit card, and you can choose repayment terms — often three to five years — that make sense for your budget. A personal loan can be a cost-effective way to pay for common home repair costs.

• Home equity loans: Homeowners can also tap into their home equity with a home equity loan or home equity line of credit (HELOC).

Before you decide on the best financing option, you will want to compare the difference between home equity loans vs. home improvement loans.

Can I Replace the Chimney Myself?

A chimney replacement requires special skills and training. A lot can go wrong if you install or repair a chimney incorrectly. It could become a fire hazard or potentially collapse. No matter your DIY skills, we highly recommend hiring a qualified mason to tackle all repairs and replacements.

Recommended: How to Keep Inflation From Blowing Your Home Reno Budget

What Factors Impact a Chimney Replacement Price?

Several factors can impact your overall chimney replacement cost, including:

• Permits needed: You’ll almost always need to get a permit for larger chimney replacement projects. Permit costs vary depending on your state and municipality.

• Level of work required: Wholesale chimney replacements cost significantly more than minor work. For example, chimneys may just require some repointing or tuckpointing to keep them in good shape, or you may need to replace the crown or cap or only rebuild the stack. If you have to replace the whole chimney, it may require demolition, which can be expensive. Talk with your contractor about the extent of the work to get a better idea of the total chimney installation cost.

• Type of chimney: Prefab chimneys are the most affordable to install. You’ll spend more to replace a metal chimney, but the most expensive type of chimney to replace is a brick one.

• Size and location: Larger chimneys will cost more to replace than small ones. Chimneys that are easy to access (by ladder, for example) are also more affordable to repair or replace. If the positioning of the chimney makes it harder for the contractor to access, labor costs will be higher.

Signs Your Chimney Needs to Be Replaced

How do you know when it’s time to replace your chimney? Here are a few signs to watch for:

1. Crumbling brick: If the brick is visibly crumbling or deteriorating, call a mason quickly to determine the extent of the damage and begin the repair or replacement work.

2. Leaks: If your chimney is the source of leaks (look for water damage to the surrounding walls and ceiling), it’s time to call a contractor to look at it.

3. Cracks: It’s good practice to have your chimney inspected each year. During the inspection, the contractor will look for large cracks. These could be a sign that it’s time to repair or replace the chimney.

The Takeaway

Chimney replacement costs can range from $1,000 to $15,000 — it’s not a cheap project, but luckily, it’s also not a common one. Get your chimney inspected every year, and keep up with regular maintenance and cleaning. Unless there’s unexpected storm damage or the chimney is old, you may not have to replace the chimney the entire time you live in your home.

Think twice before turning to high-interest credit cards. Consider a SoFi personal loan instead. SoFi offers competitive fixed rates and same-day funding. Checking your rate takes just a minute.

Replace your chimney asap with a home improvement loan from SoFi.

FAQ

How long does it take to replace a chimney?

Basic chimney repairs can be quick: A professional should be able to repair a partially damaged chimney in one to four days. Significant damage may lead to longer timelines — in some cases, it might take weeks or even months to repair and rebuild a chimney.

Can I replace my chimney myself, or do I need to hire a professional?

Replacing and repairing a chimney requires specialized knowledge, skills, and equipment, not to mention physical strength. If you make even a small mistake when replacing your chimney, you might accidentally cause a leak, inadvertently create a fire hazard, or build a structurally unsound chimney that could collapse. Always hire a professional for this work.

What qualifications should I look for in a chimney replacement contractor?

When looking for a contractor to work on your chimney, always confirm that they are licensed and insured. You should also verify that they’re certified by the Chimney Safety Institute of America.

Ask the contractors if they offer warranties or guarantees for their work and read reviews online to make sure they provide quality services. You can also ask them for references.

How do I compare quotes from different chimney replacement contractors?

Before getting quotes from any chimney replacement contractors, read online reviews and ask the contractors about their licenses, insurance, and certifications. Only get quotes from qualified contractors.

When comparing quotes, look not just at the overall cost but also the timeline to ensure they can replace your chimney quickly, if needed. Also verify what is and isn’t covered in the quote. For example, has the contractor included the necessary permits, or is that a separate cost not part of the estimate?

You’ll also want to ask about their payment schedule and how they prefer to be paid (cash, check, or credit card, for example).

Are there permits or inspections required for chimney replacement, and how much do they cost?

When replacing a chimney, you almost always will need to get a permit and an inspection. The costs will vary depending on where you live, but you might pay up to $500 for an inspection by a structural engineer, and permits can reach $150.

How often should I replace my chimney, and what factors affect its lifespan?

A well-built chimney should last several generations of homeowners. In theory, you may never need to replace your chimney (but regular inspections are a good idea). If you do replace your chimney, you likely won’t need to replace it again as long as you’re in that house.

That said, certain elements may need to be repaired or replaced more frequently. Chimney liners, for instance, last 15 to 20 years, and mortar lasts 25 to 30 years.

Extreme weather, like high and low temperatures, hail, and earthquakes, may shorten a chimney’s lifespan, as can exposure to water. As your home settles over time, it may also lead to premature cracks in your chimney.

What are the risks of not replacing a chimney that is in disrepair?

If you ignore the signs that it’s time to replace or repair your chimney, you’re exposing your home to a lot of risk. Water could more easily get into your home, leading to mold and mildew. Walls, ceilings, and floors could deteriorate over time, and the inner workings of your chimney would be exposed to rust. Eventually, your chimney might collapse, leading to much more expensive and extensive structural damage to your home.

Photo credit: iStock/AntonioSolano SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

As if you needed more evidence that it’s not a good time to buy a home.

The latest piece comes from the WSJ, which revealed that renting is 50% more expensive than buying.

This comes on top of a recent Fannie Mae survey that said home buyer sentiment matched an all-time survey low, with only 16% indicating it was a good time.

The culprit continues to be mortgage rates, which surpassed 8% last week and continue to erode affordability.

So is it better to hold off and keep renting or continue to house hunt?

It’s Not Always a Good Time to Purchase a Home

First off, it’s not always a good time to purchase a home, or condo for that matter.

Ultimately, there are better times and worse times, at least if we’re framing the question in terms of investment returns.

There’s also the sheer matter of affordability, which could jeopardize the transaction long-term if the buyer isn’t able to keep up with payments.

That’s essentially what transpired in the early 2000s, when home buyers with no business buying homes went through with the transaction regardless.

Often, this involved some creative financing and perhaps some stated income underwriting to get to the finish line.

In the end, while they qualified for the loan and closed on the purchase, they often didn’t make it past the first few mortgage payments before they fell behind.

Today, the situation is different because many of those questionable loan types, like stated income loans and option ARMs, no longer exist.

You can thank the Ability to Repay/Qualified Mortgage rule (ATR/QM Rule), which was born out of the prior mortgage crisis.

It requires lenders to “make a reasonable, good faith determination of a consumer’s ability to repay a residential mortgage loan according to its terms.”

That’s good news because it means fewer unqualified home buyers are getting approved for mortgages.

And more homeowners have safer loan products, such as the 30-year fixed, as opposed to an interest-only loan or something else that’s potentially high-risk.

Affordability Is a Problem No Matter How You Slice It

While the existing stock of homeowners has never been better, thanks to those aforementioned rules and the low, fixed interest rates they hold, it’s a different story for prospective buyers.

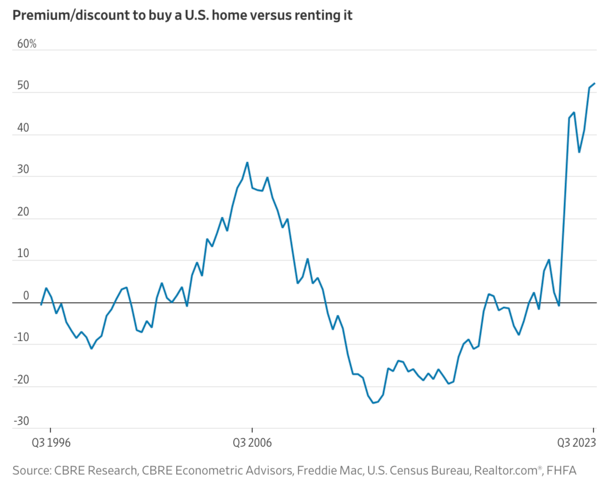

Today’s home buyer is looking at an average mortgage payment that is 52% higher than the average apartment rent, per a CBRE analysis.

This is the worst premium since at least 1996, and even well above the prior housing market peak in 2006 when it stood at 33%.

If you look at the chart above, it’s basically all because of the sharp rise in mortgage rates, which increased from sub-3% levels to around 8% today in less than two years.

That’s unprecedented movement, even if rates remain below 1980s mortgage rates. The bigger takeaway is the speed at which rates climbed higher.

We’re talking a near-200% increase in rates in less than 24 months. Meanwhile, home prices haven’t come down, thanks to a dearth of supply.

And a phenomenon known as the mortgage rate lock-in effect, where existing homeowners with 2-3% mortgage rates feel trapped.

Or are simply unwilling to move and take on a much higher interest rate.

Taken together, we have the worst home buying affordability in 30+ years history.

That buy versus rent premium is also up from 51.1% during the second quarter and 45.3% a year ago.

Again, this is largely due to higher mortgage rates, which have continued to climb higher throughout the year thanks to a stronger-than-anticipated economy.

It Now Takes Over a Decade to Break Even on a Home Purchase

Thanks to the big price tag on a home purchase these days, combined with high mortgage rates, it now takes over a decade to break even, per new data from Zillow/Axios.

The typical home buyer who puts down 3% on a $376,000 home purchase with a 7.045% mortgage rate won’t reach this point for 13.5 years.

This assumes a typical increase in home values, 3% closing costs, 1% in home maintenance fees, along with 6% closing costs and 6% agent commissions paid at time of sale.

In other words, you won’t be able to turn a profit until you’ve been in it long enough to whittle down the balance to offset all the associated costs.

Using that same purchase price, the loan balance would be about $285,000 after 13.5 years of regular monthly mortgage payments.

If the mortgage rate was 3%, the balance would be roughly $240,000 at that time because a lot more of each payment goes toward principal.

Someone who puts 20% down on a house can break even a bit sooner, at around 11.3 years, which is still about double the five-year timeline.

What does this say. That maybe it’s not a great time to buy a home, at least from an investment standpoint.

See: Rent vs. buy calculator

Should You Wait to Buy a House?

At this juncture, I don’t think anyone would call you crazy for pumping the brakes on a home purchase, though everyone has different reasons for buying.

And over time when you bought can matter less, assuming you stay the course (ask the 2006 home buyers who still own).

Aside from housing affordability being at multi-decade lows, the available inventory of homes is also quite poor.

Simply put, there isn’t a lot to choose from at the moment, and affordability stinks to boot.

At the moment, there are only about 2.5 months of supply at the existing sales rate, about half the normal 4-5-month level of for-sale inventory, per Redfin.

So despite the horrible lack of affordability, home prices are holding up just fine. In fact, the median sales price is up 1.9% from a year ago.

In other words, if you’re a prospective home buyer today, you might be looking at slim pickings, intense competition from other buyers, and an 8% mortgage rate.

That sure doesn’t sound like favorable home buying conditions.

Those who bought last year and more recently may have been told to marry the house and date the rate.

The argument is the house can be yours forever but the interest rate doesn’t have to be. The problem is mortgage rates have continued to go up.

So that advice hasn’t panned out so well for those who bought banking on refinancing to a lower rate by now.

This means if you do buy a home today, you need to be prepared to pay the mortgage rate you’re given.

Not a temporary buydown rate or a potentially lower rate in the future that may not materialize.

One compromise might be a hybrid adjustable-rate mortgage, which is fixed for the first five or seven years.

By then, hopefully mortgage rates drift over. If you believe the forecasts, they’re actually expected to drop by 2024. But that’s subject to change. And there’s still the question of just how much.

One worry along these lines is lower mortgage rates could be accompanied by lower home prices. And that could make it difficult to refinance if the mortgage is underwater.

In other words, if you buy today, you better be able to afford it. And you better really like the house.

Read more: 10 reasons to buy a house other than for the investment

Rent prices are on the rise, with the average cost increasing 18% between 2017 and 2022. But buying a home requires a hefty down payment and good credit. Renting to own your home can give you the best of both worlds, but there are some downsides.

If you’re thinking about signing a rent-to-own agreement, it’s important to weigh the pros/cons of rent-to-own home deals. Here’s what you need to know before you sign on the dotted line.

What are rent-to-own homes?

When you own a home, part of your monthly payments goes toward paying off the principal. If you stay in the home long enough, you’ll own it.

The same doesn’t apply to rentals. Your monthly rent solely covers your costs of living in that home, whether it’s a condo, apartment, townhouse, or single-family house.

A rent-to-own home lets you pay rent to live on the property, with the option to buy it when the lease runs out. In some cases, a portion of your rent goes toward the purchase price, but that isn’t always the case.

How does rent-to-own work?

A rent-to-own agreement is essentially a lease agreement with an option to buy. Rent-to-own contracts should be read thoroughly. Those options can vary from one contract to another.

When you sign a rent-to-own contract, you pay an upfront fee called an option fee. This is typically 1 to 5% of the home’s purchase price, and it’s non-refundable.

It’s important to note that a lease does not relieve you of the requirements to buy a house. You’ll still have to qualify for a mortgage and make a down payment. It’s merely a way to buy yourself some time and possibly put some of your rent toward the purchase price of a home.

Lease Option vs. Lease Purchase

Before you sign, pay close attention to the lease agreement you’re signing. There are two types, and one contractually obligates you to buy the property.

Lease Option Agreement

A lease option agreement is the best deal of the two for you, the buyer. You’re signing a lease option contract that merely gives you first rights to the house when the lease is up. If you change your mind, find a better deal, or can’t qualify for a mortgage, you can find somewhere else to live and move your belongings out.

Since the option fee is nonrefundable, it’s important to note that you will lose money if you choose not to buy. Calculate this loss when you’re deciding whether to buy.

Lease Purchase Agreement

Unlike a lease option agreement, lease purchase agreements obligate you to buy at the end of the lease. Since it’s a contract, that means you’re legally obligated to purchase the house.

This can be risky for a couple of reasons. Once you’re in the house, you may see issues you didn’t notice when you were first touring the house. Things could change with the neighborhood or your circumstances that you couldn’t know at the outset.

But the biggest issue with a lease purchase contract could simply be that you aren’t eligible for a mortgage to buy the house. Make sure you know, up front, what penalties or liabilities you’ll face if you can’t buy the house when your lease is up.

Even though both agreements operate differently on your end, they do obligate the seller to give you the option to buy when your lease expires. This puts you in a position to own a home at a predetermined future date, giving you the opportunity to start planning.

Length of a Rent-to-Own Agreement

Rent-to-own contracts start with a lease period that can be up to five years but is usually less than three. The thought is that the rental period will give a renter time to qualify for a mortgage. During this time, you’ll work on building your credit, if necessary, and saving for a down payment.

In some cases, a rent-to-own arrangement could have renewal terms. That means if you reach the end of the lease and want more time, you can extend the lease. With this option, though, the property owner could increase your monthly rent or the purchase price.

Preparing for Homebuying

During your lease term, you’ll make each monthly rent payment in exchange for remaining in the house. But it’s important during that time that you work toward purchasing the house when your time is up. Here are some things to do to boost your chances of landing a mortgage once your lease expires.

Boost Your Credit Score

Your rent-to-own deal requires that you qualify for a mortgage once the term is up. To do this, you will need to meet the minimum credit score requirements. You can get a free copy of your credit report each year at AnnualCreditReport.com, but there are also credit monitoring services that can help you stay on top of things.

Although requirements can vary from one lender to the next, Experian cites the following credit scores as necessary to land a mortgage:

FHA: If you qualify, a Federal Housing Association loan will accept credit scores as low as 500.

USDA loans: Those who meet the requirements can qualify with a score as low as 580.

Conventional loan: Generally 620 or higher, but some lenders require 660 at minimum.

VA loans: Eligible military community members and their families can obtain loans with scores as low as 620.

Jumbo loan: These loans cover houses at a higher price, so you’ll need a score of at least 700.

Save for a Down Payment

In addition to a good credit score, you’ll need to put some money down on your new home. Down payment requirements vary by loan type, but it’s recommended that you put at least 20% down. That means if you’re buying a $200,000 home, you’ll need at least $40,000 by closing.

There are lower down payment options, but if you choose those, your mortgage payments will include something called private mortgage insurance. This will increase your monthly payment by $30 to $70 per $100,000 borrowed.

If you can’t save up 20%, you may qualify for an FHA loan, which requires as little as 3.5% down. Both VA and USDA loans have zero down payment options, and there are programs offering down payment assistance to those who qualify.

The best part about rent-to-own properties, though, is that some come with rent credits. With a rent credit, a percentage of your rent will go toward your required down payment. Calculate in advance how much you’ll have in that escrow account at the end of your lease to make sure you save enough to supplement it.

What are the pros of rent-to-own?

Rent-to-own homes can be a great option, especially during a tight housing market. If there’s a house you want to buy, but you can’t make a down payment or your credit isn’t where it should be, it could be a great workaround. Here are some of the biggest benefits of rent-to-own agreements.

Rent May Go Toward Purchase Price

Depending on the terms of the rental agreement, renting to own could help you work toward paying for the home. Instead of the full amount of your rent being pocketed by a landlord, a percentage of your rent could go toward the eventual purchase price. Before signing, pay attention to rent credits and try to negotiate the best deal possible.

The Purchase Price Is Locked In

When a landlord agrees to a lease option, the home’s purchase price is written into the contract. That price will typically be higher than what the market says it’s currently worth. This means if the U.S. housing market sees an unexpected increase, you’ll be buying the home for less than its value. Even if the market dips, once you purchase the house and remain there for a few years, you may be able to sell it at a profit.

You’ll Buy Extra Time

For many renters, the rent-to-own period provides time to qualify for a mortgage. If you’ve researched all the options and found you’re close but not quite there yet, a rental period could be just what you need.

Before you choose this option, though, take a look at your circumstances. If substantial existing debt and poor credit mean you won’t qualify, you may need more than the few years you’ll get with a rent-to-own agreement.

No Moving Necessary

Let’s face it. Moving can be a pain. You have to pack everything up, line up a moving truck and get help moving, and unpack your items once you’re in the new location.

With a rent-to-own agreement in place, you skip the hassle of moving. You’ve already been in that home, making monthly rent payments, for at least a couple of years. You’ll simply go through the closing process and switch from rent payments to mortgage payments.

What are the cons of rent-to-own?

If you can get a mortgage, that’s always going to be a better option than renting or leasing to own. But there are some instances where renting without the buy option could be better for you. Here are some things to consider.

Rent-to-Own Home Maintenance

Before you sign any lease agreement, it’s important to read the fine print. One thing to note, specific to own agreements, is who will be responsible for maintenance during the rent-to-own period. If you rent without the promise of eventual ownership, your landlord will take care of those costs. In some cases, rent-to-own agreements require the renter to handle all repairs.

But there’s an upside to handling repairs on your own. To your landlord, the property is technically yours. That means you likely will give it more TLC. Still, it’s well worth it to pay for a home inspection before you agree to a rent-to-own agreement. This will identify any serious issues that will need to be addressed before you buy.

Option Fee

One distinguishing feature of a rent-to-own property is the option fee. This is usually between 1 and 5% of the purchase price and is non-refundable. That means if you don’t ultimately qualify for a mortgage, you’ll lose that money.

Home Values Could Drop

Property values aren’t guaranteed. Your landlord estimates the value of the property, but if you’re in a rising market, you might get that home at a steal. While that’s good news for you, the reverse can happen. If housing prices drop substantially during that time frame, you could find yourself buying a property for more than it’s worth.

Contract Breaches Can Be Costly

Rental agreements are a legal obligation. If you don’t pay your rent, your landlord can evict you and keep your security deposit. But rent-to-own contracts bring an additional level of risk. Missed payments mean you could be evicted and lose all the money you’ve put in. That includes the upfront fee and any rent credit you’ve earned.

All that money will also be lost if you can’t qualify for a mortgage when your rental time is up. These agreements can give you some breathing room. However, if your low credit scores, income, lack of a down payment, or employment situation make you ineligible for a mortgage, you could be searching for another rental while losing everything you’ve paid on the lease-to-own home.

Steps to Buy a Rent-to-Own Home

Once you’ve decided renting to own is the route you want to take, you may wonder what to do next. The following steps can help you ensure you get the best deal in a rent-to-own agreement.

1. Find a Home

This is more challenging than it might sound, especially if you’re looking in a competitive real estate market. Rent-to-own homes are extremely rare, so you may have to find a home for sale and try to negotiate this type of setup.

Typically, homeowners become renters when they can’t sell their homes. This means your rent-to-own contract might be on a home that’s in a less desirable or convenient area of town. For someone whose home has been on the market for a while, being able to collect rent money with the promise of a sale in a few years can be a huge relief.

For best results, find a real estate agent who can help you track down a home and negotiate with the seller. The National Association of REALTORS® maintains a directory of real estate agents, but you can also ask for a referral or find real estate agents nearby who have brokered these types of deals recently.

2. Research the Home

Even if it’s tough to find a lease-to-own home in your area, don’t snatch up the first one you find. Crunch the numbers to make sure the rent and purchase price make financial sense for you. Look at the sale history of the home to verify that the owner’s estimated purchase price is somewhat within what the median home price will likely be when your lease expires.

3. Research the Seller

The seller needs to be looked into as well. This is even more important with rent-to-own agreements since this person will be your landlord for the entire lease period. If you see any red flags during your interactions with the seller, move on.

4. Choose the Right Terms

Before you make a real estate purchase, you would have a closing attorney review the documents. The same goes for a rent-to-own agreement. Run all the paperwork past a real estate attorney to make sure there’s nothing in the contract that will hurt you in the long run.

Your real estate agent should be able to negotiate the best terms for you, including how each rent credit will help you build equity and what happens at the end of the lease.

5. Get a Property Inspection

Any time you make a home purchase, it’s essential to know what you’re buying. The same is true for rent-to-own properties. A home inspector can check things out and make sure you aren’t purchasing a home with serious issues.

6. Start Preparing to Buy

Once you start making rent payments, it’s time to start preparing for your eventual home purchase. Chances are, you’ll have to make a sizable down payment on a home loan, so plan to have that ready. Also, keep an eye on your score with all three credit bureaus and make sure you’ll qualify.

A rent-to-own contract can be a good deal for both the buyer and the seller. It can give you time to save money and improve your credit score. A real estate lawyer should take a look at your contracts and make sure your best interests are protected.

Bottom Line

Rent-to-own homes present a unique option for potential homeowners. This approach offers the opportunity to enter the homeownership arena at a slower pace, allowing individuals to build credit, save for a down payment, and experience living in the home before making a final purchase decision.

However, the rent-to-own path isn’t free from drawbacks. Potential buyers should be wary of unfavorable terms, higher monthly payments, and the risk of losing money if they decide not to buy. Ultimately, like all significant decisions in life, choosing a rent-to-own option requires careful consideration and thorough research.

Frequently Asked Questions

Where can I find rent-to-own houses?

Rent-to-own houses can be found through specialized websites dedicated to these types of listings, local real estate agents familiar with the concept, or sometimes through classified advertisements in local newspapers or online platforms.

Can I find rent-to-own homes on Zillow?

Yes, Zillow does list rent-to-own homes. When searching for properties, you can filter the search results to show only rent-to-own options. However, availability may vary based on the region and market conditions.

How long is the typical rent-to-own contract?

The typical lease term ranges from one to five years, but terms can vary based on the agreement between the homeowner and tenant.

Do I have to buy the house at the end of the lease?

No, the decision to buy is optional. However, if you decide not to purchase, you may lose any upfront fees or additional monthly amounts set aside for the potential purchase.

Can the seller change the purchase price once set?

Generally, the purchase price is fixed in the initial agreement. However, some contracts may have clauses allowing price adjustments based on market conditions.

What happens if the property value decreases during the lease period?

If the home’s value decreases and you’ve agreed on a set purchase price, you could end up paying more than the current market value. It’s crucial to negotiate terms that protect your interests.

Who is responsible for repairs and maintenance?

The agreement should clearly outline these responsibilities. In most cases, the tenant bears the responsibility for maintenance and repairs during the lease term.

What’s the benefit of a rent-to-own agreement for sellers?

Sellers can generate rental income while waiting to sell, often at a premium. It also widens the pool of potential buyers, especially those who need time to improve their credit or save for a down payment.

How do property taxes work in a rent-to-own agreement?

In a rent-to-own scenario, the property taxes are typically the responsibility of the homeowner, as they still retain ownership of the property during the rental period. However, the specific arrangement can vary based on the terms of the agreement.

Some contracts may stipulate that the tenant pays the property taxes directly or reimburses the homeowner. It’s crucial for both parties to clearly understand and agree upon who will cover the property tax obligation before entering into a rent-to-own contract.

If I don’t buy, do I get a refund for the extra money paid?

Typically, the extra money paid above regular rent, often referred to as “rent premium,” is forfeited if you decide not to buy.

Is the rent in a rent-to-own agreement higher than usual?

Often, yes. A portion of the monthly rent may be used for the potential down payment or purchase price, making it higher than the average rent for similar properties.

What’s the difference between rent-to-own and mortgage?

Rent-to-own is an agreement where a tenant rents a property with the option to buy it at the end of the lease. No bank is involved initially, and the tenant isn’t obligated to buy. A mortgage, on the other hand, is a loan specifically for purchasing a property. The buyer borrows money from a bank or lender and agrees to pay it back with interest over a predetermined period.

Does rent-to-own hurt your credit?

A rent-to-own agreement, in itself, doesn’t usually affect your credit. However, if the homeowner reports late payments to credit bureaus, it could hurt your credit score. On the positive side, consistently paying on time and eventually securing a mortgage can benefit your credit.

What is another name for rent-to-own?

Rent-to-own agreements can go by various names, including:

Lease to purchase

Lease option

Rent-to-buy

Rent-to-purchase option

Lease purchase

Each of these terms represents the concept of renting a property with the potential option to buy it after a set period.

Home is where we spend most of our time, the safe space that welcomes us at the end of a long day, the special place where we raise our families, bond with our loved ones, or retreat to for some well-deserved solitude.

And much like everything else in life, our home needs to be properly taken care of. I’m not talking about property improvements, upgrades or anything fancy.

Today, we just want to go over some general home maintenance aspects that you’re likely well aware of, but we’re hoping that a little reminder will help bring them to the forefront.

There are many things you can do, from doing regular maintenance with proper cleaning products like the ones from HG to taking extra safety measures. When you take care of your home properly, it will be the most comfortable place in the world. Keep reading to learn more about how you can achieve that.

Perform regular maintenance

The first tip to make your home is always in top condition is to perform regular maintenance.

This usually includes inspecting some points in your house, such as pipelines, roofs, ceilings, and HVAC systems. When you find something wrong at one or some of those points, you have to quickly address the issue.

Of course, you can always rely on professionals who are specialized in fixing such problems if you don’t feel like you have the expertise to do it yourself.

Make a regular cleaning schedule

The next tip is to keep your house clean at all times by making a regular cleaning schedule.

You can set the cleaning schedule once a month, twice a month, or even once a week depending on how often your home gets cluttered. Usually, the more people living in the house, the more easily it gets cluttered and accumulates dust.

Photo by Josue Michel on Unsplash

You can adjust your regular cleaning schedule based on how many people live in your house. Besides, you have to stock up on several kinds of cleaning products to make your regular cleaning activities much easier.

Take security measures

Another thing you must not miss when taking care of your home is to take security measures.

This is very important because the safety of your house as well as its inhabitants must be a key priority. And this doesn’t only mean safety from burglars who can break into your house. It also means keeping your home safe from hazards such as fire and potential short circuits.

A few easy ways to achieve this is to ensure your home has all the basic security features like security locks, smoke detectors, and fire extinguishers. It’s also a good idea to install an alarm system and several CCTVs around your home (if your budget can accommodate that) to make it more secure.

Photo by Sebastian Scholz (Nuki) on Unsplash

Perform landscaping and outdoor maintenance regularly

To make your home more comfortable and aesthetically pleasing, you have to perform landscaping and outdoor maintenance regularly.

This is very important because the exterior of your house can change drastically if you don’t tend to it regularly. One of the most important outdoor maintenance activities that you have to do is to mow your lawn due to how fast weeds grow.

You also have to trim bushes and trees if you have any in your yard. You also have to check the drainage to make sure it’s not blocked by dirt.

More stories

7 Top Decorating Ideas for Your Bedroom this Fall: Making Your Room More Cozy & Stylish

Here’s Everything You Need to Set Up a Meditation Corner in Your House

10 Unique Picture Frames and Holders to Create the Perfect Photo Wall

The Keystone State boasts an array of architectural styles, reflecting its rich historical tapestry, from colonial heritage to contemporary design. In such a diverse setting, the home inspection offers a unique perspective into the essence of a potential new home, uncovering both its inherent charm and potential challenges. Conversely, sellers can leverage this process to transparently highlight their property’s worth and proactively address any concerns.

So, whether you’re starting your journey buying a home in Philadelphia or preparing to sell a house in Pittsburgh, this Redfin article provides comprehensive guidance on navigating the home inspection process in Pennsylvania with valuable insights from local home inspectors. Equipped with this knowledge, you’ll confidently navigate the Pennsylvania real estate market.

Why should you get a home inspection in Pennsylvania?

“The houses in Pennsylvania, half of which were built before 1959, can certainly give a neighborhood character, but can also cause a multitude of problems for the occupants,” mentions Wolfe Home Inspections LLC. “Some of the old homes are filled with health hazards such as asbestos, lead paint, radon, and outdated wiring. Our picturesque rolling hills can also lead to moisture issues and foundation problems. It’s imperative that home buyers hire themselves a highly qualified home inspector to thoroughly evaluate the property for these potential issues.”

Are there any specialized inspections that Pennsylvania buyers should consider?

“Buyers should consider getting specialized inspections when necessary,” says Win Home Office. “Many buyers opt for a standard home inspection but specialized inspections, such as Mold Testing, Infrared Scanning, Radon Testing, Sewer Scope Inspections, and Fireplace and Chimney Inspections can help ensure that buyers are not only making a sound investment, but also prioritizing their future health and safety in that home.”

How much does a home inspection cost in Pennsylvania?

“The cost of a home inspection in Pennsylvania can vary based on factors such as location and the size of the property, but it generally ranges from $300 to $500,” notes Briton Inspection Services Pittsburgh.

Expert advice for Pennsylvania buyers before they get a home inspection

“Home buyers are smart to have a home inspection prior to purchasing the home as a second set of trained eyes can provide extra value in the form of a documented report on the property,” advises Kirschner Home Inspections, LLC. “A home inspection report documents the current condition at the time of the inspection and highlights any potential deficiencies. If major deficiencies are identified, the buyer may utilize the information in making a final decision on the purchase of the home or possibly negotiating a better offer.”

Ask your agent to point out possible problems

“Ask your agent during your initial or subsequent house showings if they see any possible home inspection issues,” shares The Home Pros. “Agents will regularly solicit important information from their trusted home inspectors before the offer. This can eliminate surprises during the actual inspection.”

Attend the home inspection

“I highly encourage attending your home inspection,” insists Heritage Home Inspectors. “This gives you the ability to become very comfortable and familiar with your new purchase and allows you to ask the inspector any questions while onsite together. Gaining a strong understanding of your future home is an excellent way to start your home ownership.”

Hire a certified home inspector

“Pennsylvania does not have a state level license for Home Inspectors, though many of us carry state credentials for additional services, like radon testing, mold sampling, and wood destroying insect inspections,” says The Watson Team. “Because of this, it is important to make sure that the home inspector you are hiring is fully certified by a national association like ASHI and/or interNACHI.”

Pennsylvania home inspection: the bottom line

In the realm of Pennsylvania real estate, where history merges with contemporary living and unique environmental factors come into play, home inspections hold immense importance. Whether scrutinizing over buying historic homes or brand-new constructions, the pivotal factor is better understanding what’s going on inside the home beyond its exterior. For both buyers and sellers in the Keystone State, a thorough home inspection is not merely recommended—it’s imperative. It guarantees well-informed choices, transparency, and the smooth execution of property transactions.

In the dynamic landscape of the New Jersey real estate market, where rich historical heritage from colonial roots to contemporary designs, makes each property a compelling narrative. A home inspection in the great state of New Jersey is a journey through the layers of time and innovation that define a property’s character, revealing its captivating charm and possible underlying problems. On the flip side, sellers can leverage this process to transparently present their property’s value and proactively address any homebuyer concerns.

So, whether you’re buying a home in Hoboken or gearing up to sell a property in Jersey City, this Redfin article offers comprehensive insights and guidance to help you navigate the unique home inspection landscape in New Jersey.

Why should you get a home inspection in New Jersey?

“New Jersey homebuyers should never skip the stucco inspection,” says Stucco Safe. “Problems with stucco systems that leak to the structure are incredibly common in New Jersey due to the extremes in temperature. Repairs for these problems can easily exceed $100,000. When making your offer, always include ‘invasive stucco inspection’ in your inspection requests. You won’t regret it.”

“Homebuyers in New Jersey should get a home inspection so that they know the true condition of the home and that there are no hidden issues when they take ownership,” recommends Cooper Inspection Services. “Along with the home inspection, New Jersey buyers should also get a WDI (wood destroying insect) inspection, Radon Test, and depending on the age of the house, they should also do a tank sweep to make sure there are no underground oil storage tanks.”

Are there any specialized inspections that New Jersey buyers should consider?

“One common issue we hear from clients is the difficulty of finding a licensed structural engineer, often resulting in delays with property transactions,” says Kiro Engineering. These types of inspection help to better understand the overall “structural integrity of residential and commercial properties” by conducting “thorough evaluations and considers various factors when assessing the need for repairs.”

“When selecting a home inspector, I would recommend an inspector that has a Home Inspectors License and has been inspecting homes for at least 10 years,” suggests Eagle Eye Home Inspectors. “The home inspection includes a Structural and Mechanical inspection. Some additional tests you might want to consider are:

Termite Inspections

Radon Testing

Swimming Pool Inspections

Sewer Line Inspections: using a camera to inspect the underground sewer line

Level 2 Chimney Inspections: this is an in-depth inspection of the chimney, including using a camera to inspect the internal liner

Mold/Air Quality Tests

For older homes, an Oil Tank Sweep (used to find underground oil tanks) may be needed.”

Are home inspections required in New Jersey?

“First, Home Inspections are not required in New Jersey,” notes Four Dogs Inspections. “My buyers tip would be to always get a tank sweep if buying an older home and always have a sewer scope done when purchasing a home with city sewers.”

How much does a home inspection cost in New Jersey?

“Home inspection costs can vary,” says Inspector Seltzer. “I recommend budgeting roughly two-thousand for an inspection. Including radon, termite, mold, oil tank sweep, sewer line scope, and a level two chimney inspection.”

“In fairness to all home inspection prices vary depending on the age, size, and complexity of the home,” shares Accurate Inspections, Inc. “A single price to inspect any home is either going to be unfair to the home buyer or the home inspector. Two bathroom three bedroom 1,500 sq homes should pay less than home buyers of a home three times that size.”

Expert advice for New Jersey buyers before they get a home inspection

“My advice to a home buyer is to use the process of the home inspection to get to know their new home. We take the time to help our clients not only be aware of any deficiencies in the home, but also to provide an overall education about the home itself,” suggests Michael Czar, from Safeway Home Inspections.

Ask questions

“Do not be afraid to ask questions,” urges Spectora. “You should work with a home inspector that makes you feel comfortable asking questions. Whether you’re buying or you’re doing a checkup on your own home, it can be a little intimidating and people feel embarrassed asking questions they think are silly or unimportant. There’s no better time to ask those questions. Not asking them is a missed opportunity.”

Don’t skip the inspection

“Due to the low inventory in the last few years, New Jersey saw housing demand skyrocket, with many homes selling above their asking price. Consequently, buyers often waived their inspection contingencies,” says Liliana Militaru, Redfin’s Principal Lead Agent. “ However, it is a misconception that waiving the inspection contingency prohibits the buyer from performing an inspection. On the contrary, by waiving the inspection contingency, the buyer only forfeits the right to request repairs or credits for various defects the inspector may find. Therefore, my buyers will always schedule an inspection, even when buying land-only; we still conduct at least an oil tank search.”

Don’t forget the chimney

“For properties with chimneys, considering a specialized Thermocrete inspection can help ensure the safety and functionality of this critical feature,” suggests Approved Chimney. “Thermocrete assessments can identify and address any chimney-related issues, such as cracks or deterioration, making them a valuable addition to the inspection process, especially in regions prone to harsh weather conditions.”

Hire a well-reviewed inspector that offers multiple services

A tip is to read the reviews of your home inspection company before hiring them. Home inspectors who truly take the time to invest in a full understanding of the home will have clients who are happy to share their experiences. It’s also helpful to utilize a company that does several services, including radon testing, oil tank sweeps, main waste line sewer scopes, and wood destroying insect inspections, in addition to the home inspection itself, to maximize your time and money as a client,” shares Safeway Home Inspections.

New Jersey home inspection: the bottom line

In New Jersey real estate, home inspections, though not required, are highly recommended. Whether it’s an old or new property you’re looking to buy or sell, it’s essential to have an inspector look beyond the surface of the home. For both buyers and sellers, a home inspection ensures smart decisions and a smooth transaction.

Our homes are filled with electrical appliances, from the ubiquitous refrigerator and television to the occasional coffee maker left on standby. While some diligently unplug their devices, swearing by the energy savings and safety benefits, others consider it a mere myth or an inconvenient chore. But as we grapple with pressing environmental concerns and soaring energy bills, the question looms larger: does unplugging appliances genuinely lead to energy conservation?

In this Redfin article, we’ll dive into the science behind phantom energy consumption, debunking myths, and demystifying the real impact on our planet and pockets. So whether you own a home in Los Angeles or rent an apartment in Phoenix, keep reading to learn if unplugging appliances really saves electricity.

What is phantom energy consumption?

Phantom energy consumption, often referred to as “vampire power” or “standby power,” describes the energy that devices and appliances use when they are turned off but still plugged into an electrical outlet. Even though these devices may appear inactive, they often remain in a state that allows them to respond to remote controls or maintain digital clocks and timers.

Over time, this seemingly negligible energy use can accumulate, leading to unnecessary electricity costs and contributing to environmental impacts associated with power production.

How phantom energy impacts energy bills

To comprehend the impact of phantom energy consumption on our energy bills, it’s important to consider the cumulative effect of multiple devices over time. While individual devices may use minimal power in standby mode, the cumulative effect across numerous appliances and electronics in a home can lead to significant costs. For example, chargers left plugged in, televisions on standby, and digital clocks on microwaves, among others, can collectively add up.

According to the U.S. Department of Energy, standby power can account for up to 10% of an average household’s annual electricity use. This equates to a substantial portion of your energy bill being attributed to devices that are essentially sitting idle.

Does unplugging appliances actually save energy?

The act of unplugging appliances is a practical approach that can lead to tangible energy savings. By physically disconnecting devices from power sources, you eliminate any potential standby power draw. However, the effectiveness of this approach varies depending on several factors.

1. Frequency of use

Devices that are used frequently, such as a refrigerator or a television, might not yield substantial savings from unplugging, given the hassle of constant plugging and unplugging. On the other hand, devices that are used infrequently, like chargers or printers, can benefit more from this practice.

2. Accessibility

Some appliances might be challenging to unplug regularly due to their location. For instance, entertainment systems with numerous components can be cumbersome to manage in terms of constant plugging and unplugging.

3. Long-term savings vs. convenience

While unplugging appliances can save electricity, the amount saved might not always justify the inconvenience and effort required. For busy households, finding a balance between energy savings and convenience is crucial.

Energy-efficient alternatives

Unplugging appliances isn’t the only way to reduce phantom energy consumption. Several alternatives can help strike a balance between energy savings and convenience.

Smart power strips: Unlike traditional power strips, these are designed to detect when a device is in standby mode and automatically cut off power, preventing any unnecessary energy drain. Some models even allow users to designate specific outlets for “always-on” devices, ensuring that essential gadgets remain uninterrupted.

Energy-efficient appliances: Energy-efficient appliances are specifically designed to use less electricity while delivering the same performance as their standard counterparts. They often incorporate advanced technologies and designs that reduce waste and optimize energy use. Investing in these appliances lowers electricity bills and contributes to a reduced carbon footprint, making them a sustainable choice for environmentally-conscious consumers.

Timers and settings: Many devices allow users to pre-set periods when appliances, such as lights or heaters, should operate, thereby avoiding unnecessary energy consumption during inactive hours. Many modern appliances come equipped with built-in timers or eco-modes, enabling optimal energy use by automatically powering down after a certain time or during periods of inactivity.

The verdict: Does unplugging appliances save electricity?

In conclusion, the answer to this question is a resounding yes. Unplugging devices, especially those with infrequent use, can indeed contribute to energy savings and a reduction in your electricity bills. However, the extent of these savings depends on factors like device usage patterns, accessibility, and personal preferences.

By being mindful of phantom energy consumption and adopting energy-saving habits, you can contribute to both a greener planet and a healthier household budget.

Residential sale-leaseback platform EasyKnock continues to gobble up proptech startups. Home maintenance company Onder is EasyKnock’s latest acquisition, according to GeekWire, which first reported the story.

The terms of the acquisition were not disclosed.

Founded in 2021, Onder sells a subscription-based home maintenance service that deploys technicians to help with both interior and exterior property maintenance. Customers can request help for HVAC cleaning, plumbing, painting, power washing, gutter cleaning, and roof repair, and it covers more than 100 homes.

Onder raised an undisclosed amount of venture capital including a pre-seed round led by Rackhouse Ventures in 2021, but in late 2022, as the housing market slowed and economic uncertainty rose, the flow of venture capital funds slowed.

“The venture capital environment continued to be a headwind and we had been operating with very little margin for error,” David Krieger, the CEO and co-founder of Onder, told GeekWire in an email. “[S]o when we evaluated the landscape with our advisors, it just made sense to include mergers and acquisitions as an attractive path forward.”

Krieger said customers will not experience an interruption in their service due to the acquisition.

Through the acquisition, Onder’s services will be offered to EasyKnock’s customers. In a statement, EasyKnock said the acquisition is part of its larger goal of creating the “first nationwide property maintenance platform for homeowners.”

Kreiger and Onder’s employees (numbering fewer than 10) will join EasyKnock, and Kreiger will serve as EasyKnock’s chief product strategy officer.

EasyKnock received $57 million in venture capital last year. Investors included Blumberg Capital, Gaingels, Moderne Ventures, QED Investors, Viola FinTech, and Zillow founder, Spencer Rascoff’s venture firm 75 & Sunny.

In May, EasyKnock acquired struggling power buyer firm Ribbon for an undisclosed amount.