American Dream

Apache is functioning normally

The Center for Human Resource Research at Ohio State released the results of a study today that claims Americans own a larger share of their homes than the Fed’s quarterly report indicated last week.

According to the Fed’s U.S. Flow of Funds Accounts report issued a week ago, the percentage of equity owned in American homes crept to just 47.9 percent in the fourth quarter of 2007, the lowest on record.

But a survey conducted by Ohio State found that in reality, Americans have roughly 70 percent equity in their homes on average.

The study pointed out that the Fed data doesn’t account for homeowners who have fully paid off their homes, so those without a mortgage are excluded from the data.

This can obviously skew the data wildly, despite the fact that the situation is clearly getting worse.

“Things are rough on the housing front, but they aren’t as bad as some of these stories would lead us to believe,” said Randall Olsen, the director of the Center. “While many homeowners are hurting and the economy is definitely vulnerable, the sky is not falling.”

The Center conducted the survey by calling 3,500 randomly selected households across the country, finding that 40 percent do not have a mortgage on their home, and for those who do, the average mortgage is $138,000.

It also found that the average home in the survey was worth nearly $283,000, putting homeowners’ equity as a fraction of home value at 70 percent.

Interestingly, it’s higher than a 2004 survey conducted for the Federal Reserve that revealed home equity to be just 65 percent.

Olsen also noted that mortgage lenders traditionally measure a well-secured loan as one that sports a loan-to-value below 80 percent, of which 82 percent of homeowners in the survey said they had.

“Owning your own home has always been part of the American dream, and people do not readily part with their dreams,” Olsen said.

Unfortunately, he may be leaving out the scores of prospectors and other unfit homeowners who have begun walking away.

(photo: bslavin)

Source: thetruthaboutmortgage.com

Apache is functioning normally

Owning your own home is typically a foundation of the American Dream, and many people are saving for a down payment right this minute. But when you are already paying rent, it can be a challenge to save for a down payment on a house, especially if you live in an area with a high cost of living or are dealing with the impact of inflation.

But that doesn’t mean it can’t be done. You can save up for your home purchase by following some wise financial advice and simplifying the process of socking away your cash.

If buying a home is a priority for you, read on. You’ll learn how to grow your down payment savings while still paying rent.

5 Tips to Save for a Home While You’re Still Renting

Rent can take a big bite out of your take-home pay, but it doesn’t rule out saving for a down payment on a house. Here’s some smart budgeting advice to help you set aside money for your future homeownership.

💡 Quick Tip: You deserve a more zen mortgage. Look for a mortgage lender who’s dedicated to closing your loan on time.

1. Pay Down Your Debt First

In order to save for a house, it’s wise to figure out a plan to pay down your existing debt. This will free up more money for you to save for that down payment. Also, when you do apply for a mortgage, you will likely have a lower debt-to-income ratio, or DTI ratio. Reducing you DTI ratio can help your application get approved.

Student loan debt is a common kind of debt to have; the average American right now has $37,338 in loans. If you’re a full-time employee, reach out to your company’s HR department to learn more about student debt repayment assistance. A recent survey by the Employee Benefit Research Institute found that 17% of companies in the U.S. currently have this type of assistance, so it’s worth a try.

Gain home-buying insights

with the latest housing

market trends.

As a more drastic measure, you could always think about going into a profession that offers partial or total student loan forgiveness (such as teaching in certain public schools) or moving to a state that will help pay off your student loan debt just for moving there (currently Kansas, Maine, Maryland, and Michigan).

For an easier fix, you could consider student loan refinancing options, which might lower your rate. By dropping your interest rates, you could significantly reduce both your payments and the length of time you’ll be making them.

However, a couple of points to note. If you extend your term to lower the payment, you will pay more interest over the life of the loan. Also, do be aware that, when refinancing federal loans to private ones, you may then no longer be eligible for federal benefits and protections. However, by getting a lower interest rate, you may accelerate your path to saving for your down payment and getting keys to your very own home.

Credit card debt can also play a role in preventing you from saving for a down payment. This is typically high-interest debt, with rates currently hovering just below 25%.

There are a variety of ways to pay down this debt, such as the debt avalanche method, which has you focus on your highest-interest debt first; the debt snowball; and the debt fireball methods.

If none of these techniques seems right for you, you might look into getting a balance transfer credit card, which will give you a period of zero interest in which you may pay down debt. Or you might take out a personal loan to pay off the credit card debt and then potentially have a lower interest loan to manage.

2. Create a Budget That Will Help You Spend Less and Save More

Another way to free up funds for that down payment is to budget well. Creating and sticking to a realistic budget can help you spend less while saving for a house. While budgeting can sound like a no-fun, punitive exercise, that really doesn’t have to be the case. A budget is actually a helpful tool that allows you to manage your income, spending, and saving optimally.

To get there, you can pick from the different budgeting methods. Most involve these simple steps.

Gather your data: Figure out how much you’re earning each month (after taxes), along with how much you’re currently spending. Add it all up including cell phone bills, insurance, grocery bills, rent, utilities, your coffee habit, the dog walker, gym membership, etc. Don’t miss a dime.

List your current savings: Are you currently putting money into an IRA, 401(k), or other savings plan? List it, so you can see what you’ve already got in the bank.

Really dig into and optimize your spending: Can you cut back anywhere? You might trim some spending by bundling your renters and car insurance with one provider. Perhaps you can save on streaming services by dropping a platform or two. And how’s your takeout habit? If you really want to save for a house, you may need to learn to cook. You might even consider taking in a roommate or moving to a less expensive place to turbocharge your savings for your down payment while renting.

Making cuts, admittedly, can be the toughest step in the budgeting process, but it’s crucial to be honest with yourself about your spending. Remember: However much you cut back can help you get a new home that much sooner.

Finally, check in on your budget every so often and adjust as needed. For example, if you land a new job, get a promotion, or are given an annual raise, perhaps you can add that money to your savings account or put it toward paying off your loans. Whichever one feels more important to you is OK, so long as that extra cash isn’t vanishing on impulse buys.

3. Investigate How Big a Down Payment You Actually Need

Many prospective homebuyers think they must have 20% down to buy a house, but that is not always the case. That is how much you need to avoid paying for private mortgage insurance (PMI) with a conventional conforming loan. Private mortgage insurance typically ranges from 0.5% to 2% of the loan amount, and it’s automatically canceled when your equity reaches 78% of the home’s original value.

Here are some valuable facts: You may be able to take out a conforming loan with as little as 3% down, plus PMI. Certainly, that’s a sum that can be easier to wrangle than 20%, though your mortgage principal will be higher. According to National Association of Realtors data, the average first-time homebuyer puts down about 6%.

In addition, you might qualify for government loans that don’t require any down payment at all, such as VA and USDA loans.

You might also look into regional first-time homebuyer programs that can provide favorable terms and help you own a property sooner.

💡 Quick Tip: Don’t have a lot of cash on hand for a down payment? The minimum down payment for an FHA mortgage loan is as little as 3.5%.

4. Grow Your Savings

If you’ve paid off your debt, set realistic budgeting goals, and are raking in some dough to add to a savings account, you’re already on the right track. A good next move is to put your money to work for you. Among your options:

• Open a high-interest savings account. These can pay multiples of the average interest rate earned by a standard savings account. You will frequently find these accounts at online vs. traditional banks. Since they don’t have brick-and-mortar branches, online financial institutions can save on operating costs and can pass that along to consumers. Just be sure to look into such points as any account fees, as well as opening balance and monthly balance requirements. (Features such as round-up savings can also help you save more quickly.)

You can also look into certificates of deposit (CDs) and see what interest rates you might get there. These products typically require you to keep your funds on deposit for a set period of time with the interest rate known in advance.

• If you have a fairly long timeline, you might consider opening an investment account to grow your savings. The market has a historical 10% rate of return, though past performance isn’t a guarantee of future returns. You could try using a robo advisor, or you could work with a financial advisor who will walk you through investment strategies for beginners and beyond and help you invest. Just be aware that investments are insured against insolvency of the broker-dealer but not against loss.

Recommended: First-time Homebuyer Guide

5. Automate as Much of Your Finances as Possible

This is a lot of information to process, but once you get through all the work upfront, you can start automating as much as possible. For example, have a portion of your paycheck automatically go into your savings account each month to plump up that down payment fund.

You might set up the direct deposit of your paycheck to send most of your pay to your checking account and a portion to a savings account earmarked for your down payment. You can check with your HR or Benefits department to see if this is possible.

Another way to automate your savings is to have your bank set up a recurring transfer from your checking account, as close to payday as possible. That can route some funds to your down payment savings without any effort on your part. Nor will you see the cash sitting in your checking account, tempting you to spend it.

The Takeaway

While saving for a down payment isn’t exactly a piece of cake, it doesn’t have to feel overwhelming. By trying five effective strategies, which can include budgeting, paying down debt, and automating your savings, you can accumulate enough money to start on your path to homeownership.

Once you have the down payment taken care of, you’ll be ready to shop for a home mortgage that suits you.

Looking for an affordable option for a home mortgage loan? SoFi can help: We offer low down payments (as little as 3% – 5%*) with our competitive and flexible home mortgage loans. Plus, applying is extra convenient: It’s online, with access to one-on-one help.

SoFi Mortgages: simple, smart, and so affordable.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility for more information.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

¹FHA loans are subject to unique terms and conditions established by FHA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. FHA loans require an Upfront Mortgage Insurance Premium (UFMIP), which may be financed or paid at closing, in addition to monthly Mortgage Insurance Premiums (MIP). Maximum loan amounts vary by county. The minimum FHA mortgage down payment is 3.5% for those who qualify financially for a primary purchase. SoFi is not affiliated with any government agency.

SoFi Student Loan Refinance

If you are a federal student loan borrower, you should consider all of your repayment opportunities including the opportunity to refinance your student loan debt at a lower APR or to extend your term to achieve a lower monthly payment. Please note that once you refinance federal student loans you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans or extended repayment plans.

SOHL1023251

Source: sofi.com

Apache is functioning normally

Many people consider homeownership a rite of passage, a part of the American Dream, and a key way to build wealth. But recently, as home prices and mortgage interest rates have risen, some may wonder, “Is buying a home a good investment, no matter what?”

It can be challenging to gather enough funds for a down payment, qualify for a mortgage, and then afford all of the costs that go along with homeownership, such as property taxes, maintenance expenditures, and utilities. But to live in a place you love while building equity can be a win-win.

So if you’re wondering “Is buying a house a good investment?” vs. say, investing your money, you’ll have to take a closer look at how homeownership relates to your personal financial situation. Read on to learn how to evaluate what will be the right decision for you, starting with important questions to contemplate.

Is It a Good Investment to Buy a House?

In order to determine if buying a home is a good investment for you, you’ll need to estimate the amount of time you plan to own the house and the real estate marketplace dynamics.

• If you don’t plan to own the house for at least five years, you may not break even when you sell the home. When you buy a home, you pay for more than just the house and those costs can add up. You’re often paying for appraisals, mortgage application fees, inspections, movers, real estate agent fees, and that can add up to thousands of dollars.

In order to recoup all those fees, conventional wisdom says you need to wait at least five years for your home to appreciate before selling it. If you plan to live somewhere for less than five years, it could make the most financial sense just to rent property.

• You may also want to consider other aspects of whether it’s a good time to buy a house. For example, is it a hot or cool market? Are you likely to wind up in a bidding war (and possibly overpay) because there isn’t enough supply to meet demand? Are interest rates likely to fall over the next year? These dynamics can impact whether now is the right time to jump into the housing market.

💡 Quick Tip: With SoFi, it takes just minutes to view your rate for a home loan online.

Do You Have Sufficient Savings to Buy a House?

In order to buy a home, you’ll generally have to take out a mortgage to finance your home purchase. Before that’s not the only expense. These costs must also be covered:

• Before you even get to the mortgage stage, you’ll have to save for a down payment (which is often anywhere between 3% and 20% of the property’s purchase price) and closing costs, which are typically 3% to 6% of the loan amount. This can mean a significant chunk of change.

• There are continuing costs you’ll have to account for, such as home insurance, property taxes, general maintenance, and emergency home repairs.

When you are renting, if the kitchen sink springs a leak, your landlord will take care of it. But when you own a home, those repairs will be entirely your responsibility. Having an emergency fund saved up will help you deal with unexpected costs associated with homeownership.

Also, if you are purchasing a house as an investment vs. using it as a primary residence, can you afford to buy a house while still renting? That is a situation in which you will want to map out your cash flow and make sure you are prepared if you can’t flip or rent the property as quickly as anticipated. An emergency fund could also be invaluable in that scenario.

Are You Confident in the Housing Market?

The housing market rises and falls; take a close look to evaluate current trends. Home prices skyrocketed during the Covid pandemic and have continued to rise recently. This can make it difficult for first-time homebuyers to find a suitable home that is in their price range. It’s important to be prepared as you start to look at homes. Understand your budget and make sure you have saved enough money to make a down payment on the property.

Also be sure that you understand how mortgage rates can impact the affordability of housing and what your home shopping budget looks like.

💡 Quick Tip: If you refinance your mortgage and shorten your loan term, you could save a substantial amount in interest over the lifetime of the loan.

Are You Ready for the Responsibility?

When you own your own home, you have a lot of freedom to make the space completely your own. With all of this flexibility comes a lot of responsibility. If the house has a yard, you’ll be responsible for regular maintenance and upkeep.

Will you need to pay for a new roof soon? Buy a lawn mower? If you live in an area with harsh winters, will you need to get a snow blower or hire someone to clear the driveway after each snow storm? These costs can add up.

So make sure you are ready for the financial responsibility that comes with owning a home before you make the purchase. You’ll have to account for repairs, improvements, general upkeep, insurance, and taxes. Not only does all of this cost money, it will take your time and attention as well, which isn’t necessarily the case when you rent. If you’re not ready to always be “on call” for your property’s needs, it could be a homebuying mistake to purchase.

Recommended: Should I Sell My House?

Are You Willing to Live with a Long-Term Loan?

Buying a home can mean you’re taking on a loan for perhaps 15 or 30 years. That’s a major undertaking. Part of the process of learning how to buy a house is educating yourself on how mortgages work and the different types available. Generally, there are two types: fixed rate and adjustable-rate mortgages.

• A fixed-rate mortgage keeps your payment level over time, typically 15 or 30 years, because the interest rate remains stable.

• The interest rate on an adjustable-rate mortgage loan fluctuates over time. They usually start out lower than a fixed-rate loan but often rise in later years.

To see what a mortgage could mean for your finances, take a look at an online mortgage calculator to compare different types of loans and see what your costs might look like. If a loan could be part of your life for three decades, you want to make sure you’re comfortable with it.

Remember that while it may seem daunting to take on a 30-year obligation, a mortgage helps you build equity in an asset that generally increases in value as time passes. Is a house a good investment? Historically, yes, if you take the long view.

Over the years, homeowners build up equity in the house as they methodically pay off more and more principal with less monthly payments on each loan payment. Many smart borrowers pay extra each month toward the principal to pay off the mortgage sooner.

Recommended: Quiz: Should You Buy or Rent a Home?

Pros and Cons of Buying a Home as an Investment

Before a major financial move, it’s important to consider the benefits and downsides. You’ll want to know what are the pros and cons of buying a starter home or a subsequent property. Consider these points.

Pros of Buying a House

Here are some of the upsides of buying and owning a home:

• You will build equity in your home over time, which can help you grow your wealth. Your home value may appreciate as well.

• There may be tax advantages to homeownership, such as deducting mortgage interest.

• Paying your mortgage payments on time can help build your credit.

• You can renovate the property as you see fit, unlike the case with rental units.

• You likely have a good idea of your monthly housing costs for the long term. If you are renting, you could face significant fluctuations.

• There’s a feeling of security for many people when they know they own their home.

Cons of Buying a House

Next, it’s wise to consider the disadvantages of buying a home:

• You typically need to pay for the down payment and closing costs, which can be a significant financial hurdle.

• You are likely locking into long-term debt, and it can take a while to build equity.

• There is no guarantee that your home’s value will grow over time.

• The costs related to owning a home can be significant. This includes expenses like property taxes and insurance, as well as home repairs.

• You will have less flexibility if you need to move for a job, say, or want to relocate to be closer to friends and family. Selling a house can involve time, energy, and money.

Ready to Buy? Consider a SoFi Mortgage

Looking for an affordable option for a home mortgage loan? SoFi can help: We offer low down payments (as little as 3% – 5%*) with our competitive and flexible home mortgage loans. Plus, applying is extra convenient: It’s online, with access to one-on-one help.

SoFi Mortgages: simple, smart, and so affordable.

FAQ

Is it wise to buy a house as an investment?

Whether it’s wise to buy a house as an investment will depend on many factors, such as your personal finances and current economic and real estate trends, as well as whether the property is a place that’s a good home for you to live in for at least several years.

Is buying a house worth it in 2023?

Buying a house in 2023 can be challenging because home prices and mortgage rates have been rising. However, if you can afford the monthly mortgage payments, plus the down payment and ongoing costs of homeownership, it may still be the right move for you.

Is owning a home an asset?

In general, a home is considered an asset. Yes, you typically have a mortgage, which is a liability, but on the plus side, you are building equity while having a place you enjoy living.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility for more information.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SOHL1023243

Source: sofi.com

Apache is functioning normally

Declining housing affordability pressuring Millennials Data from the BofA shows Millennials have experienced a near 20% increase in mortgage debt since the fourth quarter of 2021 compared to Gen X and Baby Boomers. With the rise of inflation, the Federal Reserve has hiked interest rates 11 times since March 2022 in an effort to balance … [Read more…]

Apache is functioning normally

Chances are, your mortgage interest probably makes up a large proportion of your monthly expenses.

So, how can you secure the best mortgage rate possible? The potential savings you unlock can have a substantial and lasting impact on your lifestyle and disposable income for many years to come.

Read on as we delve into the world of mortgage interest rates, where we’ll explore their implications, and reveal the keys to securing the most favorable terms.

Verify your home buying eligibility. Start here

In this article (Skip to…)

What is interest?

Merriam-Webster defines interest as “a charge for borrowed money, generally a percentage of the amount borrowed.” You can think of it as the rent you pay to lenders for giving you access to their money.

That makes it different from the money you access. The money you borrow is called the “principal,” and the interest you pay is almost always a percentage of that.

Verify your home buying eligibility. Start here

You pay the interest monthly, but it’s calculated annually. So, if you borrow $100,000 at a 5% interest rate, you’ll pay $5,000 a year in interest, which is $600 a month.

With an installment loan, such as a mortgage, you have to pay the principal back over the life of the loan plus the interest that accumulates.

Nearly all mortgages are “fully amortized.” That means, for a fixed-rate loan, all the monthly payments are the same. But your mortgage lender works them out so you zero your balance (including interest and the principal sum borrowed) when you make the final monthly payment at the end of your home loan’s term, often 30 years.

Amortization and mortgage interest

When you make your first monthly payment on a new mortgage, you owe a huge amount of money. So, almost all that payment goes on interest and your principal debt reduces only a little.

Gradually, over the years, your principal decreases and the interest you owe each month does, too. As each payment is made, the percentage allocated to interest shrinks while the portion allocated to reducing the debt grows larger and larger.

By the time you make your last payment, only a tiny bit is interest and nearly all of it reduces your principal — to zero.

This stuff isn’t easy. So, to discover more, read How mortgage amortization works, and why it matters.

How costly is mortgage interest?

When this was written, in October 2023, mortgage rates had just reached a 20-year high. So, it may feel as if mortgage interest is expensive.

But, of course, mortgages are actually one of the least costly ways of borrowing. The problem isn’t the mortgage interest itself but the large sums home buyers borrow over long periods.

Even a low interest rate can result in high monthly mortgage payments when you’re borrowing big. And your mortgage is likely to be by far your largest loan, at least at the start.

Verify your home buying eligibility. Start here

What’s that in dollars?

So, how much might your mortgage interest cost on a conventional 30-year, fixed-rate mortgage? Let’s try an example. We’re basing it on the average rate for such a loan on the day this was written (7.522%) and on a property at the current median home price ($416,100 in the second quarter of 2023). We’ll assume a 20% down payment.

We fed those numbers into our mortgage calculator. And you can do the same with your own figures. Here’s what we got:

So, that’s $2,333 each month for the mortgage, plus property taxes and homeowners insurance. Did you spot the View Full Report button at the bottom? That provides the real low down:

So, as the Totals section reveals, “By the end of the 30-year mortgage loan term, you would pay $839,722 in total amount ($332,880 would be for the original loan amount and $506,845 in interest).”

Yes, that sounds a lot. But you’re borrowing a considerable loan amount over a long period of time.

It’s actually good value, especially when you think that, at the end, you’re likely to own outright a hugely valuable asset. And you won’t have had to pay rent for the next 30 years to live somewhere else.

By the way, the graph top-right on that page shows amortization in action.

What factors determine the mortgage interest you pay?

There are two main groups of factors that affect the mortgage rates you’ll be quoted: Things you can change and things you can’t.

Verify your home buying eligibility. Start here

The economy and markets

Let’s start with what’s outside your control. That’s mostly the economy and its effect on the bond market for mortgage-backed securities. It’s that market that largely determines current mortgage rates.

Generally, mortgage rates fall when the economy’s in trouble and rise when it’s thriving. Inflation also plays a role, with above-average price rises tending to drive higher interest rates.

Your financial circumstances

Now, for some things you can control. Lending is all about risk. Lenders know that some of their home loans will turn bad. But which?

So, they analyze your personal finances to discover how much of a risk you pose. And the bigger that perceived risk, the higher the interest rate they’ll quote you. Of course, if they think there’s a serious danger of your mortgage loan turning bad, they’ll simply decline your application.

So, what specifically do they look for? It’s mainly:

- A consistent and adequate source of income — That’s often easy to prove if you’re an employee. But it can be harder for the self-employed and those in the gig economy

- A history of managing debt well — That’s your credit score and credit report

- A manageable level of existing debts — How easily will you afford the new monthly mortgage payments once you’ve met all your other inescapable financial commitments each month? This is called your debt-to-income ratio or DTI

- The down payment amount — The bigger your down payment, the more skin you have in the game. And that means you’re less of a risk. So a high down payment helps get you a lower interest rate. However, most borrowers can easily get a mortgage with just 3% or 3.5% (zero for some) down. This is your loan-to-value ratio (LTV)

Each of those normally affects a lender’s calculations when deciding what mortgage interest rate to quote you. And, of course, you have a great deal of control over them.

For example, spending time before you apply, building your credit score and reducing your debt (especially card balances) can earn you an appreciably lower interest rate.

Verify your home buying eligibility. Start here

Rate shopping

How would you like to save more than $1,000 a year for many years to come for just a few hours’ work?

It’s easy. And yet, a surprising number of mortgage borrowers pass on the opportunity.

In May 2023, federal regulator the Consumer Financial Protection Bureau (CFPB) released a report under the headline:

Mortgage data shows that borrowers could save $100 a month (or more) by choosing cheaper lenders

The CFPB found the spread among different lenders’ mortgage interest rates is “often around 50 basis points of the annual percentage rate.” Fifty basis points is 0.5%. So, it could be the difference between paying a rate of 7% or 6.5%. Try running those figures through our mortgage calculator!

The report also says that such differences apply in “virtually every segment of the mortgage housing market, including loans backed by Fannie Mae and Freddie Mac, Federal Housing Administration loans, U.S. Department of Veterans Affairs (Veterans Affairs) loans, as well as jumbo loans.”

And all you have to do to unlock such potential savings is request quotes from multiple lenders. Of course, your preferred lender may come up with the best deal. But suppose it doesn’t.

Fixed vs. adjustable-rate mortgage

Most Americans, especially first-time home buyers, opt for a fixed-rate mortgage (FRM). They’re prepared to pay a little more for the security of knowing that every monthly payment they make on their loan will be the same as the last one.

A fully amortized FRM is as predictable as anything gets. You pay the same $x each month until you finish paying down the loan — or sell the home or refinance the mortgage.

Verify your home buying eligibility. Start here

Adjustable-rate mortgages (ARMs) are very different. Or they can be after a few years.

An ARM almost always starts with a lower interest rate than an FRM. And that rate is fixed for an initial period, after which it can float in line with general interest rates, usually once each year.

So, a 5/1 ARM has a fixed rate for the first five years, a 7/1 ARM’s rate is fixed for seven years, and so on. The second numeral tells you how often the rate can be adjusted after the initial fixed-rate period expires. That numeral is most often a 1, meaning the rate can then float up or down annually (once a year).

That’s fine as long as mortgage rates remain low. But it can cause real pain when those interest rates shoot up, as they have done in recent years.

Luckily, that pain is usually moderated because most ARMs come with caps that limit how much their interest rates can rise. But even moderated pain is still pain.

Some home buyers can still be better off with ARMs. If you know you’ll be moving home within seven years and choose a loan type such as the 7/1 ARM, your mortgage interest rate will be fixed for as long as needed.

The bottom line on mortgage interest

At worst, mortgage interest is often seen as a practical necessity. The other option is to spend a lifetime paying rent, ultimately without the prospect of building valuable assets.

When mortgage rates are high, the weight of interest payments can become a substantial concern. But, if mortgage rates fall one day, refinancing is always an option, provided you remain creditworthy.

And there are things you can do to pay as low a mortgage interest rate as possible. Comparison shopping among several lenders could save you $100+ a month. Meanwhile, improving your credit score and reducing your existing debts can make another big difference.

Homeownership remains as much a part of the American dream as it always has. If you’re ready to fulfill your dream, don’t delay.

Time to make a move? Let us find the right mortgage for you

Source: themortgagereports.com

Apache is functioning normally

The New York State Assembly today passed a rather robust legislative package aimed at addressing the “national sub-prime lending crisis.”

The four-bill bundle contains legislation that, if enacted, would offer assistance to homeowners in default or facing foreclosure, establish requirements on all home loans, provide consumer info to all residential mortgage applicants, and most notably, create a one-year foreclosure moratorium for New York residents.

Assembly Speaker Sheldon Silver slammed the Feds for bailing out mortgage lender and investment bank Bear Stearns while leaving everyday homeowners at risk of losing their homes.

He insisted that the slew of bills was not a bailout, but rather an assistance program to help homeowners keep the American dream alive.

The first bit of the legislation would provide assistance payments up to an amount equal to three months of mortgage payments and provide legal services and counseling to help select homeowners in default or facing foreclosure.

The second part of the package would establish the duties of mortgage brokers and remedies for violations, ensure that lenders verify borrower income and the ability to repay loans, and prohibit practices such as balloon mortgage payments, negative amortization and prepayment penalties.

The third bill would permit the courts to delay foreclosure up to one year for subprime borrowers who meet specific conditions, allowing at-risk homeowners to work with their respective lenders to avoid losing their homes.

The final piece of the legislative package would create a “Mortgage Applicant’s Bill of Rights,” which requires mortgage lenders and brokers to provide consumers with a pamphlet that must be read and signed by the borrower prior to applying for a mortgage.

(photo: bogjagendorf)

Source: thetruthaboutmortgage.com

Apache is functioning normally

Just when everything looked oh so good in housing, a new report has revealed that investors have already lost interest.

The latest Campbell/Inside Mortgage Finance HousingPulse Tracking Survey found that so-called “investor participation” in the housing market slipped to 21.9% of all transactions in July, down from 23.5% in June.

It hit a two-year high as recently as May, when investors scooped up more than a quarter (25.3%) of all transactions.

So why the sudden reversal? Well, survey respondents have pointed to higher home prices, which cut into investors’ profits.

After all, they work on tight margins, so if the pricing isn’t just right, it doesn’t make for a good investment.

Some respondents even noted that the “smart money” has left the housing market, and it’s now “dumb” investors stepping in.

That last comment came from a real estate agent in Arizona, where home prices have been on a tear in the past year.

In fact, recent home price appreciation has pushed negative equity levels there from 55.5% to 51.6% in just one quarter, according to a recent report from Zillow.

It’s great news for existing owners and those who recently purchased, but bad news for investors looking for a bargain.

Another agent in Florida said “rookie investors” were moving in and paying too much for properties, which sounds like another bubble all over again.

Existing Homeowners Still Pumped About Housing

While investor sentiment has shifted, existing homeowners still seem to be pretty amped about housing.

They accounted for 43.5% of home purchases in July, up from 42% in June and 40.3% in May.

Participation by first-time home buyers was flat month-to-month.

It’s likely that demand is being driven in part by the record low mortgage rates, which have made it very attractive to own versus rent in many parts of the country.

But Campbell Surveys research director Thomas Popik warned that a reversal in rates could lead to another flood of distressed properties, and a subsequent drop in home prices.

Of course, the distressed supply has been dropping as of late, with only a 42.2% share in July, down from 45.1% in June and 46.1% in May.

And in many hot markets across the country, inventory is so low that prospective homebuyers have no choice but to wait for properties to come to market.

Even if there are suitable properties, many are clouded by intense bidding wars, so it’s clear that swelling inventory isn’t a huge concern, at least for the moment.

Homeownership Rate Lowest in Nearly 50 Years

Meanwhile, the “real homeownership rate,” which is the percentage of households who own a home and are not 90 days or more behind on their mortgage, fell to the lowest point in nearly half a century, per a report from John Burns Real Estate Consulting.

The company said the Census Bureau’s 65.5% homeownership rate is grossly overstated, and the actual rate is closer to 62.1%.

Historically, this spread is just below 1%, as there are still distressed homeowners, even when things are golden.

Obviously it has widened considerably thanks to the ongoing mortgage crisis, but they believe housing will make a serious comeback.

Their survey of 20,000 “confirms that the American dream of homeownership is as strong as ever.”

Additionally, they have started to see foreclosed homeowners return as home buyers after the three-year waiting period required by most banks and mortgage lenders.

This is especially prevalent in parts of the country where the foreclosure process runs more smoothly, such as in Arizona and Texas.

So if you believe the homeownership rate will climb back over time, there will certainly be plenty of demand in coming years, and with that, ideally some decent home price appreciation for those who get in early.

Sure, it won’t happen overnight, but a good time to believe in housing is at a time when no one else does.

Source: thetruthaboutmortgage.com

Apache is functioning normally

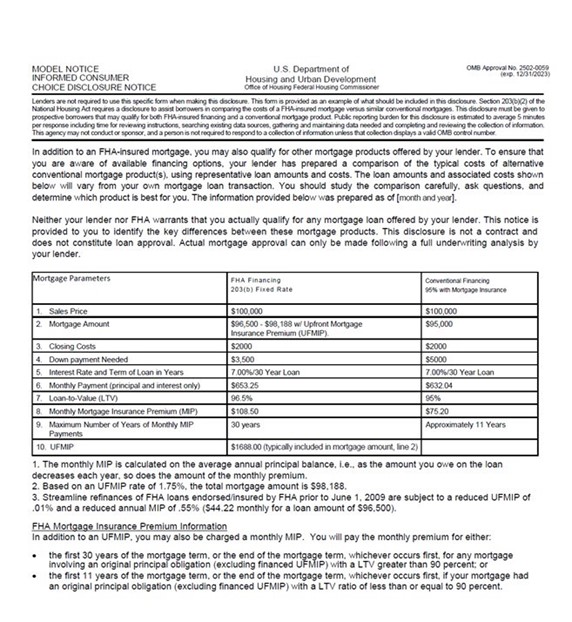

As the Federal Reserve raises interest rates, the cost savings for Veterans’ Affairs home loans could make a substantial difference in affordability

WASHINGTON – U.S. Senators Ben Cardin (D-Md.) and John Boozman (R-Ark.) have introduced legislation, the VA Loan Informed Disclosure Act of 2023 (VALID Act/S. S.2496), that will require a side-by-side comparison between conventional, Federal Housing Administration (FHA), and Veterans’ Affairs (VA) home loans to be included in the U.S. Department of Housing’s “Informed Consumer Choice Disclosure Notice.” VA home loans can offer veterans, active duty, reservists, and national guard members lower down payments, interest rates, and closing costs, saving them tens of thousands of dollars over the life of the loan. Despite these benefits, overall usage of VA home loans is surprisingly low, with only 10 to 15 percent of veterans reported as using the benefit.

“Buying a home often is the most expensive purchase an individual makes in their lifetime. For our veterans and servicemembers who have earned these benefits through service to our nation, we need to make it easier for them to learn about and access the savings they deserve. Far too many are missing out on tens of thousands of dollars of savings; we aim to change that by making the disclosures and comparisons clear and upfront,” said Senator Cardin.

“We can help fulfill the dream of homeownership by informing veterans about the benefits they have earned. VA’s home loans are underutilized, but this bipartisan legislation will provide the men and women who served in uniform another opportunity to learn about resources available to them to save money and meet the needs of their families,” Senator Boozman said.

The VALID Act (S.2496), will provide potential homebuyers a comprehensive picture of veterans’ financing options through a side-by-side comparison of conventional, FHA, and VA home loans. This legislation will help veterans make more informed choices about their financing options and potentially increase the utilization of VA home loans.

“As part of its ongoing commitment to veterans, VAREP applauds Senators Ben Cardin and John Boozman for support of expansion of legislation to include VA loans in the Informed Consumer Choice Disclosure, addressing a key informational gap. This change will empower veterans and servicemembers to make fully informed home loan decisions as they set their sights on the American dream of homeownership,” said G2 Varrato, National Legislative Committee Director of the Veterans Association of Real Estate Professionals (VAREP).

The bill text may be downloaded here.

Below is a sample of a current Informed Consumer Choice Disclosure Notice. The VALID Act would add an additional column for VA home loans.

Source: cardin.senate.gov